Embed Size (px)

Citation preview

Corporate Governance and Shariah Governance at

Islamic Financial Institutions:Assessing from Current Practice in Malaysia

Tadashi Mizushima 1

Abstract The purpose of this study is to examine the relation between corporate governance and Shariah governance, and how those gover-nance concepts are handled at Islamic financial institutions.

Although using the same word “governance,” Western corporate governance and Islamic Shariah governance may be different. The main research question is how different or similar are governance at conven-tional banks and Shariah governance at Islamic banks? We would like to find an answer to this question by undertaking a comparative analy-sis of widely accepted guidelines. There is limited analytical work in the existing literature on this simple question. This study is unique in that it presents a critical comparative analytical perspectives of a veteran practitioner in the Western banking industry2, 3.

In order to clarify the relationship of several governance concepts, we first review the concept of corporate governance that originated in Organization of Economic Cooperation and Development (OECD). Then, we explain how the corporate governance concept was forwarded to the conventional banking industry and then how it is introduced to the Islamic banking industry. Following that, we examine the Shariah governance concept at Islamic banks. The analytical findings show that Shariah governance is a concept that comes first at Islamic banks. Our analysis shows that actual Shariah governance practice, however, looks to be limited to exercising Shariah compliance. Furthermore, for the

1. Representative Director, PNB Asset Management (Japan) Co. Ltd. and Visiting Fellow, Reitaku Institute of Political Economics and Social Studies. The views express here are solely those of the author in his private capacity and do not in any way represent the views of PNB Asset Management (Japan) Co. Ltd.

2. For example, Islamic Finance Principles and Practice by Hans Vissar (2009), a popular book on Islamic Finance does not mention Shari’ah governance. Another example, Critical Issues on Islamic Banking and Financial Markets by Saiful Azhar Rosly (2005), a popular textbook on Islamic banking in Malaysia, discusses Islamic Corporate Governance in three pages of his 618-page book.

3. The word “conventional” is used to mean Western style banking, which uses the concept of interest.

Reitaku Journal of Interdisciplinary Studies

60 RJIS [Vol. 22, No. 1

purpose of understanding the degree of non-compliant risk, three cases of Shariah compliant risk are analyzed.

Lastly, we explain the current development of governance in West-ern countries. Governance has evolved from passive to active. An expanded interpretation of corporate governance has become popular particularly in the context of corporate social responsibility (CSR). New concepts such as creating shared value (CSV) and Impact Investing have been increasingly recognized. In this context, while it has become evident that Western capitalism is trying to find ways to realize social justice and welfare, but neither of which has been its main purpose. On the contrary, Shariah governance is narrowly focused on Shariah compli-ance, and its function at financial institutions looks passive.

Key Words: Islamic finance, corporate governance, Shariah governance, Shariah compliance, CSR

Interdisciplinary Fields: International economics, International finance

Introduction: The Development of Islamic Finance

Islamic finance has been expanding throughout the world mainly due to an increase in the Islamic population and the economic development of Islamic nations. Islamic finance is gaining attention from Western financial circles because of its development as a source of additional revenue and because its unique concepts backed by actual transactions provides as an alternative to the Western financial system.

The increasing Muslim population is a key factor. Currently estimated to be 1.6 billion, within 10 years, one in three of the total world population will be Muslim. The size of Islamic finance is said to be around US$1.631 trillion with an annualized growth rate of 20.4% for the past five years as of the end of March 20124. The total size is smaller than the size of the world’s largest financial institutions, with 18 banks in the world having assets of more than US$1.631 trillion, according to The Banker’s magazine’s world ranking of banks 2013.

Here, we summarize Islamic finance concepts. Islamic finance is a way to accommodate the values of Islam in finance. It is based on Islamic law, or Shariah, which is designed to promote social and economic jus-tice. Shariah is known for prohibiting interest or usury (Riba), speculation or gambling (Maisir), excessive risk or uncertainty (Gharar) and oppressive practices. Muslims must evaluate business activities to determine whether the business is Halal (“just” or “lawful”), which can be handled, or Haram

4. Data from Edbiz Consulting (2013) Global Islamic Finance Report 2013.

2014] 61Corporate Governance and Shariah Governance at Islamic Financial Institutions:

Assessing from Current Practice in Malaysia

(“unjust” or “sinful”), which cannot be handled in financing. Haram busi-ness activities include the manufacturing or marketing of products such as alcohol, gambling or gambling activities, pork and pork products, certain forms of adult entertainment.

It is important to mention that Shariah specifies no finance is given without actual contracts unless and until all contracts meet the following requirements: (i) there must be a minimum of two parties to an arrange-ment; (ii) the product must be real and must be owned by one party; (iii) there must be an offer and an acceptance of the offer; (iv) all parties must fully agree to the deal’s purpose and terms; (v) the price must be agreed on mutually, with no party subject to duress; (vi) there must be no undue bur-den on one party to the advantage of another; (vii) the term must be in ac-cordance with other Shariah principles5. For example, a contract involving a prohibited product such as alcohol or pork would not be acceptable.

In addition to qualitative restrictions, three types of quantitative re-strictions are widely applied in investment activities. The first one is debt availed by the company. This restriction is to exclude companies where interest-bearing debt liabilities exceed or equal one third (1/3) of the compa-ny’s total assets or market capitalization (depending on methodology used). This test is not applicable to Shariah compliant financing. Secondly, cash plus interest-bearing securities of the company. This criteria is to exclude companies where cash plus interest-bearing securities exceed or equal one third (1/3) of the company’s total assets or market capitalization (depend-ing on methodology used). This test is not applicable to Shariah compliant financing. Thirdly, extent of cash and receivables with the company. In Is-lamic finance, debt and cash can only be traded at par. Therefore cash plus receivables must be less than 33% of market capitalization.

Contemporary Islamic finance has been a quest for an alternative to conventional financing, which is composed of interest-bearing loans and transactions. This is achieved through the use of various Islamic contracts such as sales, leases and partnerships since the beginning of Shariah history. Islamic financing typically takes the form of (i) sales-purchase, and (ii) risk-sharing investments. The use of these contracts in Islamic finance means a whole new way of doing business be it in banking, capital market transac-tions or insurance. The desire for financing modes and investment vehicles that are in accordance with Shariah principles has impacted the growth of Islamic finance today. “Shariah governance” is typically described as “a set of institutional and organisational arrangements through which Islamic

5. Concept of Islamic finance is from Virginia B. Morris, 2009, A Muslim’s Guide to Invest-ment & Personal Finance, Lightbulb Press.

62 RJIS [Vol. 22, No. 1

Financial Institutions (IFIs) ensure that there is an effective independent oversight of Shariah compliance over the issuance of relevant Shariah pro-nouncements, dissemination of information and an internal Shariah compli-ance review.”6 “Shariah compliance” is “to describe financial activities and investments that comply with Islamic law which prohibits the charging of interest and involvement in any enterprise associated with activities and products forbidden by Islamic law.”7

Since Shariah is the backbone and foundation for the existence of the Islamic banking and finance industry, Islamic finance experts assert Shariah governance should be considered as the single most important distinction between a conventional and an Islamic financial institution. But, the termi-nology of Shariah governance is not easy to understand for persons who live in conventional finance.

Against this background, this paper intends to examine the relation between corporate governance and Shariah governance, and how those gov-ernance concepts are handled at Islamic Financial Institutions. Definition of corporate governance is presented in Section 1 followed by a compara-tive analysis of conventional and Islamic Financial Institutions in Section 2. Section 3 reviews Shariah governance at Islamic Financial Institutions by comparing the guidelines issued by Bank Negara Malaysia and Islamic Fi-nancial Services Board. In order to clarify Shariah compliant risks vis-a-vis Shariah governance, we highlight three case studies in Section 4. Section 5 concludes the paper.

Section 1: Definition of Corporate Governance

The word “governance” usually means “corporate governance” to persons in conventional finance. In this section, we first begin with an examina-tion of the concept of corporate governance from Organization of Economic Co-operation and Development (OECD). We then review the concept of corporate governance at conventional banks, which is shown in guidelines announced by Bank for International Settlements (BIS). This comparison is intended to clarify how the concept of corporate governance advocated by OECD and BIS, respectively, is related. The best known concept of corpo-rate governance in the Western world is the one announced by the OECD in June 2004. The OECD concept comprises six frameworks.

First, Ensuring the basis for an effective corporate governance frame-

6. Islamic Financial Services Board (IFSB), 2009, IFSB-10, Kuala Lumpur.7. QFinance’s Dictionary, “Definition of Shari’ah Compliant” www.qfinance.com retrieved

on November 1, 2013.

2014] 63Corporate Governance and Shariah Governance at Islamic Financial Institutions:

Assessing from Current Practice in Malaysia

work: the corporate governance framework should promote transparent and efficient markets, be consistent with the rule of law and clearly articu-late the division of responsibilities among different supervisory, regulatory and enforcement authorities.

Second, the rights of shareholders and key ownership functions: the corporate governance framework should protect and facilitate the exercise of shareholders’ rights.

Third, the equitable treatment of shareholders: the corporate gover-nance framework should ensure the equitable treatment of all shareholders, including minority and foreign shareholders. All shareholders should have the opportunity to obtain effective redress for violation of their rights.

Fourth, the role of stakeholders in corporate governance: the corpo-rate governance framework should recognize the rights of stakeholders established by law or through mutual agreements and encourage active co-operation between corporations and stakeholders in creating wealth, jobs, and the sustainability of financially sound enterprises.

Fifth, disclosure and transparency: the corporate governance frame-work should ensure that timely and accurate disclosure is made on all ma-terial matters regarding the corporation, including the financial situation, performance, ownership, and governance of the company.

Six, the responsibilities of the board: the corporate governance frame-work should ensure the strategic guidance of the company, the effective monitoring of management by the board, and the board’s accountability to the company and the shareholders.

In the conventional financial world, the most widely accepted concept of corporate governance is that issued by the Basel Committee on Bank-ing Supervision (the BIS-Committee) at BIS. Actually, the BIS-Committee issued two guidelines on corporate governance. The first, “Enhancing corporate governance for banking organizations,” was announced in February 2006 and the second, “Principles for enhancing corporate governance,” was an-nounced in October 2010.

The BIS-Committee’s 2010 guideline refers to the OECD principles as follows.

“The Committee’s 2006 guideline drew from principles of corporate governance that were published in 2004 by OECD. The OECD’s widely ac-cepted and long-established principles aim to assist governments in their efforts to evaluate and improve their frameworks for corporate governance and to provide guidance for participants and regulators of financial mar-kets.”

The BIS-Committee’s 2010 guideline summarizes the OECD principles as follows.

64 RJIS [Vol. 22, No. 1

“The OECD principles define corporate governance as involving a set of relationships between a company’s management, its board, its sharehold-ers, and other stakeholders. Corporate governance also provides the struc-ture through which the objectives of the company are set, and the means of attaining those objectives and monitoring performance are determined. Good corporate governance should provide proper incentives for the board and management to pursue objectives that are in the interests of the com-pany and its shareholders and should facilitate effective monitoring. The presence of an effective corporate governance system, within an individual company or group and across an economy as a whole, helps to provide a de-gree of confidence that is necessary for the proper functioning of a market economy.” (emphasis added by author).

This summary comes from the Preamble of the OECD report in 2004, not from the six major frameworks of corporate governance issued by OECD. The wording in the Preamble sounds more like “Wall Street” than “Main Street.” It talks about “incentives and monitoring,” which invokes a “carrot and whip” relation between management and board members. It also mentions, “the proper functioning of a market economy,” which does not appear in the six frameworks of the OECD’s concept of corporate gover-nance. The BIS’s stance on corporate governance here seems somewhat re-laxed, and we cannot totally dismiss the suspicion that such a loose stance on corporate governance may have triggered the Bear Sterns crisis in March 2008 and the Lehman crisis in September 2008 in the Western financial in-dustry. If BIS had adhered to the six principles of OECD, BIS would have had tighter control over the world’s financial institutions.

Section 2: Corporate Governance in Conventional and Islamic Financial Institutions

We continue our review of the BIS-Committee’s guidance. In the 2010 up-date, we can find that the BIS-Committee placed focus on six issues.

First, board practices: the board should actively carry out its overall re-sponsibility for the bank, including its business and risk strategy, organiza-tion, financial soundness and governance. The board should also provide effective oversight of senior management.

Second, senior management: under the direction of the board, senior management should ensure that the bank’s activities are consistent with the business strategy, risk tolerance/appetite and policies approved by the board.

Third, risk management and internal controls: a bank should have a risk management function (including a chief risk officer (CRO) or equivalent

2014] 65Corporate Governance and Shariah Governance at Islamic Financial Institutions:

Assessing from Current Practice in Malaysia

for large banks and internationally active banks), a compliance function and an internal audit function, each with sufficient authority, stature, inde-pendence, resources and access to the board.

Fourth, compensation: the bank should fully implement the Financial Stability Board’s (FSB- formerly the Financial Stability Forum) Principles for Sound Compensation Practices (FSB Principles).

Fifth, complex or opaque corporate structure: the board and senior management should know, understand and guide the bank’s overall corpo-rate structure and its evolution, ensuring that the structure (and the entities that form the structure) is justified and does not involve undue or inappro-priate complexity.

Sixth, disclosure and transparency: transparency is one tool to help emphasize and implement the main principles for good corporate gover-nance.

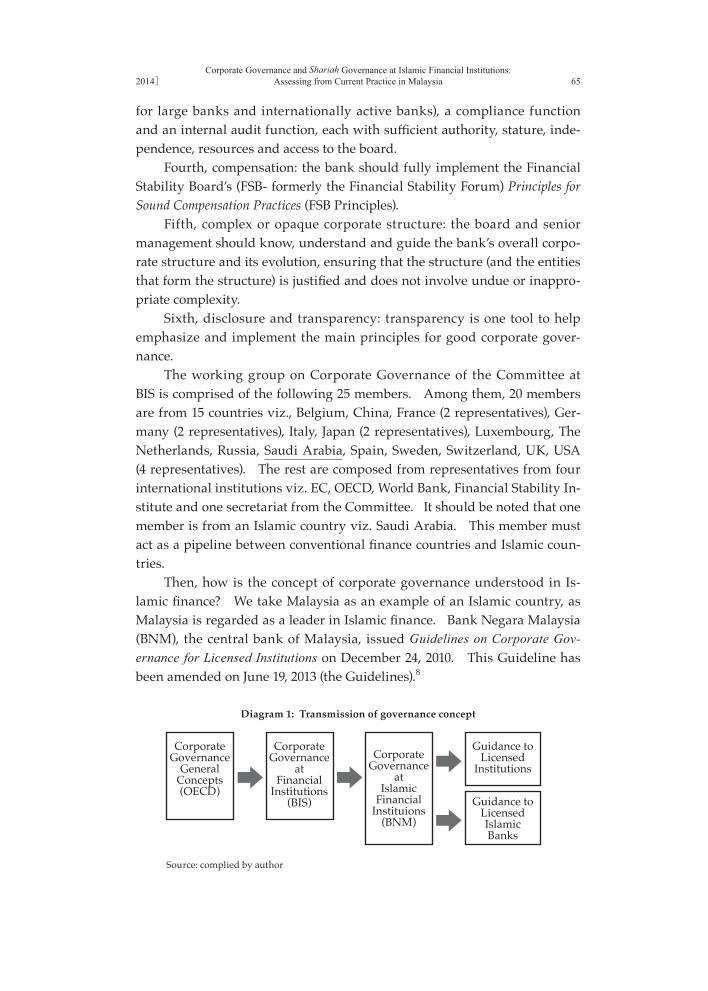

The working group on Corporate Governance of the Committee at BIS is comprised of the following 25 members. Among them, 20 members are from 15 countries viz., Belgium, China, France (2 representatives), Ger-many (2 representatives), Italy, Japan (2 representatives), Luxembourg, The Netherlands, Russia, Saudi Arabia, Spain, Sweden, Switzerland, UK, USA (4 representatives). The rest are composed from representatives from four international institutions viz. EC, OECD, World Bank, Financial Stability In-stitute and one secretariat from the Committee. It should be noted that one member is from an Islamic country viz. Saudi Arabia. This member must act as a pipeline between conventional finance countries and Islamic coun-tries.

Then, how is the concept of corporate governance understood in Is-lamic finance? We take Malaysia as an example of an Islamic country, as Malaysia is regarded as a leader in Islamic finance. Bank Negara Malaysia (BNM), the central bank of Malaysia, issued Guidelines on Corporate Gov-ernance for Licensed Institutions on December 24, 2010. This Guideline has been amended on June 19, 2013 (the Guidelines).8

CorporateGovernance

GeneralConcepts(OECD)

CorporateGovernance

atFinancial

Institutions(BIS)

CorporateGovernance

atIslamic

FinancialInstituions

(BNM)

Guidance toLicensed

Institutions

Guidance toLicensedIslamicBanks

Diagram 1: Transmission of governance concept

Source: complied by author

66 RJIS [Vol. 22, No. 1

Diagram 1 shows the transmission of the governance concept from OECE to Islamic financial institutions.

The BNM’s Guidelines, in the section of “Alignment with other corpo-rate governance codes,” state as follows.1.05 The broad principles, standards and requirements under the Guide-

lines are aligned with the principles enshrined in:The Malaysian Code on Corporate Governance;The BIS Guidelines on “Enhancing Corporate Governance for Bank-ing Organizations;” andOther international best practices on corporate governance.(emphasis is added by author)

Consequently, it is clear that BNM has adopted BIS’s guidelines, so let’s see the details of the Guidance. 1.06 The Guidelines are formulated based on the fundamental concepts of

responsibility, accountability and transparency, with greater empha-sis on the role of the board and management. The Guidelines high-light the principles of corporate governance that are translated into minimum standards and specific requirements.

1.07 The Guideline contains broad principles dealing with(i) Board matters;(ii) Management oversight;(iii) Accountability and audit; and(iv) Transparency.

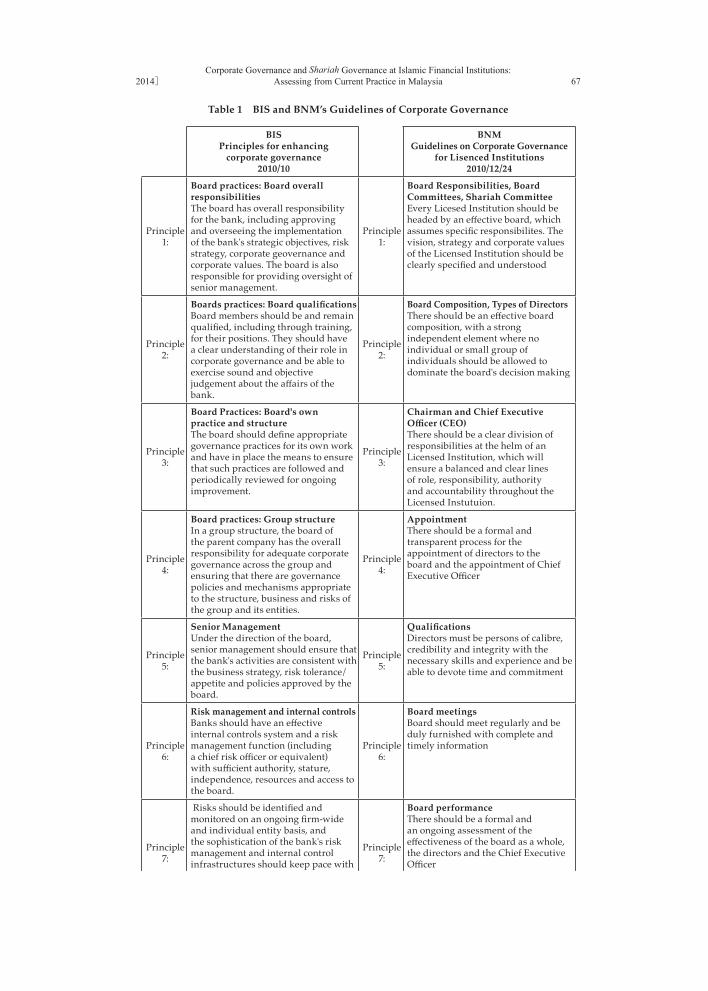

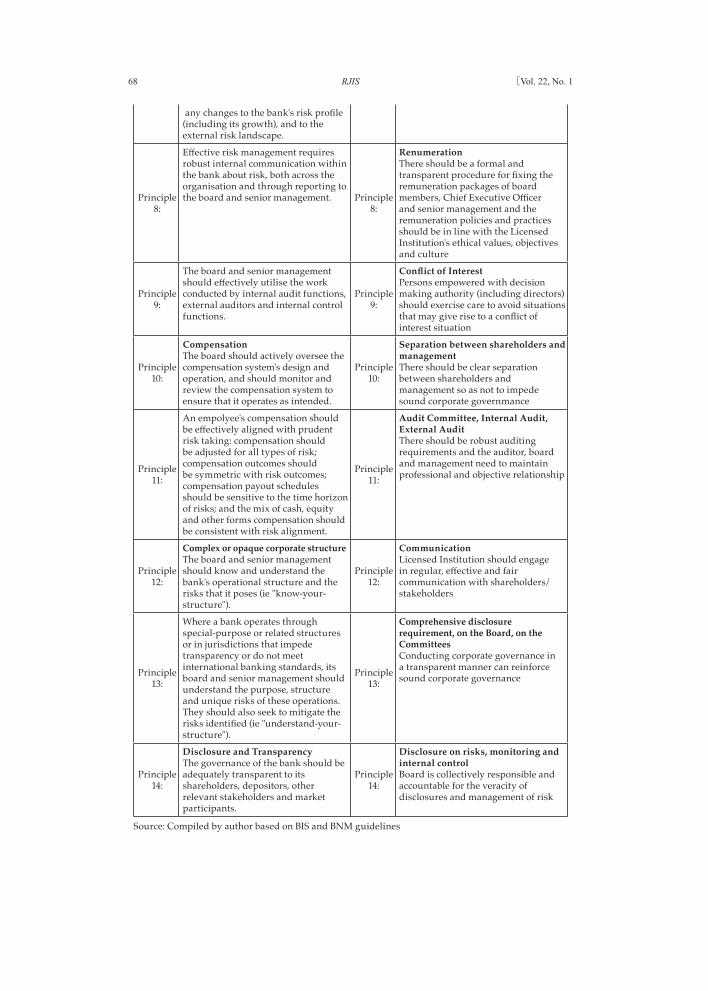

Now let us compare the principles of corporate governance at BIS and BNM. The comparison of BIS and BNM’s Guidelines of Corporate Gover-nance is shown in Table 1.

The principles on the Guidelines of BNM are quite similar to those of BIS. Both place strong emphasis on (i) board, (ii) management and (iv) transparency. While BNM highlights (iii) accountability and audit more than BIS, BIS puts more emphasis on risk management and compensation.

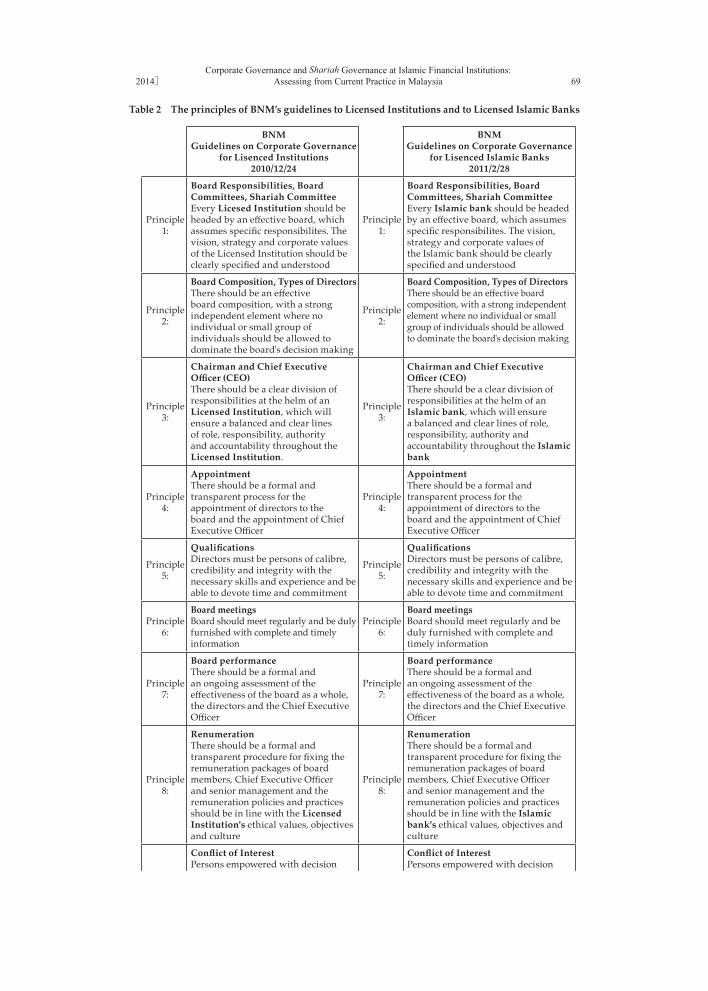

BNM issued guidelines to Islamic Banks, called “Guidelines on Cor-porate Governance for Licensed Islamic Banks9,” at the same time it issued guidelines to conventional banks. A comparison of the principles of BNM’s guidelines to Licensed Institutions and to Licensed Islamic Banks is shown in Table 2.

8. Guideline on Corporate Governance for Licensed Institutions (BNM/RH/GL 001-1). Is-sued on December 24, 2010, amended on June 19, 2013.

9. Bank Negara Malaysia (BNM), Guidance on Corporate Governance for Licensed Islamic Banks (BNM/RH/GL 002-1). Issued on February 28, 2011, amended on June 19, 2013, Kuala Lumpur.

2014] 67Corporate Governance and Shariah Governance at Islamic Financial Institutions:

Assessing from Current Practice in Malaysia

Table 1 BIS and BNM’s Guidelines of Corporate Governance

BISPrinciples for enhancing

corporate governance2010/10

BNMGuidelines on Corporate Governance

for Lisenced Institutions2010/12/24

Principle 1:

Board practices: Board overall responsibilities The board has overall responsibility for the bank, including approving and overseeing the implementation of the bank's strategic objectives, risk strategy, corporate geovernance and corporate values. The board is also responsible for providing oversight of senior management.

Principle 1:

Board Responsibilities, Board Committees, Shariah Committee Every Licesed Institution should be headed by an effective board, which assumes specific responsibilites. The vision, strategy and corporate values of the Licensed Institution should be clearly specified and understood

Principle 2:

Boards practices: Board qualifications Board members should be and remain qualified, including through training, for their positions. They should have a clear understanding of their role in corporate governance and be able to exercise sound and objective judgement about the affairs of the bank.

Principle 2:

Board Composition, Types of Directors There should be an effective board composition, with a strong independent element where no individual or small group of individuals should be allowed to dominate the board's decision making

Principle 3:

Board Practices: Board's own practice and structure The board should define appropriate governance practices for its own work and have in place the means to ensure that such practices are followed and periodically reviewed for ongoing improvement.

Principle 3:

Chairman and Chief ExecutiveOfficer (CEO) There should be a clear division of responsibilities at the helm of an Licensed Institution, which will ensure a balanced and clear lines of role, responsibility, authority and accountability throughout the Licensed Instutuion.

Principle 4:

Board practices: Group structureIn a group structure, the board of the parent company has the overall responsibility for adequate corporate governance across the group and ensuring that there are governance policies and mechanisms appropriate to the structure, business and risks of the group and its entities.

Principle 4:

AppointmentThere should be a formal and transparent process for the appointment of directors to the board and the appointment of Chief Executive Officer

Principle 5:

Senior Management Under the direction of the board, senior management should ensure that the bank's activities are consistent with the business strategy, risk tolerance/appetite and policies approved by the board.

Principle 5:

Qualifications Directors must be persons of calibre, credibility and integrity with the necessary skills and experience and be able to devote time and commitment

Principle 6:

Risk management and internal controlsBanks should have an effective internal controls system and a risk management function (including a chief risk officer or equivalent) with sufficient authority, stature, independence, resources and access to the board.

Principle 6:

Board meetings Board should meet regularly and be duly furnished with complete and timely information

Principle 7:

Risks should be identified and monitored on an ongoing firm-wide and individual entity basis, and the sophistication of the bank's risk management and internal control infrastructures should keep pace with any changes to the bank's risk profile (including its growth), and to the external risk landscape.

Principle 7:

Board performance There should be a formal and an ongoing assessment of the effectiveness of the board as a whole, the directors and the Chief Executive Officer

68 RJIS [Vol. 22, No. 1

any changes to the bank's risk profile (including its growth), and to the external risk landscape.

Principle 8:

Effective risk management requires robust internal communication within the bank about risk, both across the organisation and through reporting to the board and senior management. Principle

8:

Renumeration There should be a formal and transparent procedure for fixing the remuneration packages of board members, Chief Executive Officer and senior management and the remuneration policies and practices should be in line with the Licensed Institution's ethical values, objectives and culture

Principle 9:

The board and senior management should effectively utilise the work conducted by internal audit functions, external auditors and internal control functions.

Principle 9:

Conflict of Interest Persons empowered with decision making authority (including directors) should exercise care to avoid situations that may give rise to a conflict of interest situation

Principle 10:

Compensation The board should actively oversee the compensation system's design and operation, and should monitor and review the compensation system to ensure that it operates as intended.

Principle 10:

Separation between shareholders and managementThere should be clear separation between shareholders and management so as not to impede sound corporate governmance

Principle 11:

An empolyee's compensation should be effectively aligned with prudent risk taking: compensation should be adjusted for all types of risk; compensation outcomes should be symmetric with risk outcomes; compensation payout schedules should be sensitive to the time horizon of risks; and the mix of cash, equity and other forms compensation should be consistent with risk alignment.

Principle 11:

Audit Committee, Internal Audit, External AuditThere should be robust auditing requirements and the auditor, board and management need to maintain professional and objective relationship

Principle 12:

Complex or opaque corporate structureThe board and senior management should know and understand the bank's operational structure and the risks that it poses (ie "know-your-structure").

Principle 12:

Communication Licensed Institution should engage in regular, effective and fair communication with shareholders/stakeholders

Principle 13:

Where a bank operates through special-purpose or related structures or in jurisdictions that impede transparency or do not meet international banking standards, its board and senior management should understand the purpose, structure and unique risks of these operations. They should also seek to mitigate the risks identified (ie "understand-your-structure").

Principle 13:

Comprehensive disclosure requirement, on the Board, on the CommitteesConducting corporate governance in a transparent manner can reinforce sound corporate governance

Principle 14:

Disclosure and Transparency The governance of the bank should be adequately transparent to its shareholders, depositors, other relevant stakeholders and market participants.

Principle 14:

Disclosure on risks, monitoring and internal controlBoard is collectively responsible and accountable for the veracity of disclosures and management of risk

Source: Compiled by author based on BIS and BNM guidelines

2014] 69Corporate Governance and Shariah Governance at Islamic Financial Institutions:

Assessing from Current Practice in Malaysia

Table 2 The principles of BNM’s guidelines to Licensed Institutions and to Licensed Islamic Banks

BNM Guidelines on Corporate Governance

for Lisenced Institutions2010/12/24

BNM Guidelines on Corporate Governance

for Lisenced Islamic Banks2011/2/28

Principle 1:

Board Responsibilities, Board Committees, Shariah Committee Every Licesed Institution should be headed by an effective board, which assumes specific responsibilites. The vision, strategy and corporate values of the Licensed Institution should be clearly specified and understood

Principle 1:

Board Responsibilities, Board Committees, Shariah Committee Every Islamic bank should be headed by an effective board, which assumes specific responsibilites. The vision, strategy and corporate values of the Islamic bank should be clearly specified and understood

Principle 2:

Board Composition, Types of Directors There should be an effective board composition, with a strong independent element where no individual or small group of individuals should be allowed to dominate the board's decision making

Principle 2:

Board Composition, Types of Directors There should be an effective board composition, with a strong independent element where no individual or small group of individuals should be allowed to dominate the board's decision making

Principle 3:

Chairman and Chief Executive Officer (CEO) There should be a clear division of responsibilities at the helm of an Licensed Institution, which will ensure a balanced and clear lines of role, responsibility, authority and accountability throughout the Licensed Institution.

Principle 3:

Chairman and Chief Executive Officer (CEO)There should be a clear division of responsibilities at the helm of an Islamic bank, which will ensure a balanced and clear lines of role, responsibility, authority and accountability throughout the Islamic bank

Principle 4:

Appointment There should be a formal and transparent process for the appointment of directors to the board and the appointment of Chief Executive Officer

Principle 4:

Appointment There should be a formal and transparent process for the appointment of directors to the board and the appointment of Chief Executive Officer

Principle 5:

Qualifications Directors must be persons of calibre, credibility and integrity with the necessary skills and experience and be able to devote time and commitment

Principle 5:

Qualifications Directors must be persons of calibre, credibility and integrity with the necessary skills and experience and be able to devote time and commitment

Principle 6:

Board meetings Board should meet regularly and be duly furnished with complete and timely information

Principle 6:

Board meetings Board should meet regularly and be duly furnished with complete and timely information

Principle 7:

Board performance There should be a formal and an ongoing assessment of the effectiveness of the board as a whole, the directors and the Chief Executive Officer

Principle 7:

Board performance There should be a formal and an ongoing assessment of the effectiveness of the board as a whole, the directors and the Chief Executive Officer

Principle 8:

Renumeration There should be a formal and transparent procedure for fixing the remuneration packages of board members, Chief Executive Officer and senior management and the remuneration policies and practices should be in line with the Licensed Institution's ethical values, objectives and culture

Principle 8:

Renumeration There should be a formal and transparent procedure for fixing the remuneration packages of board members, Chief Executive Officer and senior management and the remuneration policies and practices should be in line with the Islamic bank's ethical values, objectives and culture

Principle 9:

Conflict of Interest Persons empowered with decision making authority (including directors) should exercise care to avoid situations that may give rise to a conflict of interest situation

Principle 9:

Conflict of Interest Persons empowered with decision making authority (including directors) should exercise care to avoid situations that may give rise to a conflict of interest situation

70 RJIS [Vol. 22, No. 1

Principle 9:

making authority (including directors) should exercise care to avoid situations that may give rise to a conflict of interest situation

Principle 9:

making authority (including directors) should exercise care to avoid situations that may give rise to a conflict of interest situation

Principle 10:

Separation between shareholders and managementThere should be clear separation between shareholders and management so as not to impede sound corporate governmance

Principle 10:

Separation between shareholders and managementThere should be clear separation between shareholders and management so as not to impede sound corporate governmance

Principle 11:

Audit Committee, Internal Audit, External AuditThere should be robust auditing requirements and the auditor, board and management need to maintain professional and objective relationship

Principle 11:

Audit Committee, Internal Audit, External AuditThere should be robust auditing requirements and the auditor, board and management need to maintain professional and objective relationship

Principle 12:

Communication Licensed Institution should engage in regular, effective and fair communication with shareholders/stakeholders

Principle 12:

Communication Islamic bank should engage in regular, effective and fair communication with shareholders/stakeholders

Principle 13:

Comprehensive disclosure requirement, on the Board, on the CommitteesConducting corporate governance in a transparent manner can reinforce sound corporate governance

Principle 13:

Comprehensive disclosure requirement, on the Board, on the CommitteesConducting corporate governance in a transparent manner can reinforce sound corporate governance

Principle 14:

Disclosure on risks, monitoring and internal controlBoard is collectively responsible and accountable for the veracity of disclosures and management of risk

Principle 14:

Disclosure on risks, monitoring and internal controlBoard is collectively responsible and accountable for the veracity of disclosures and management of risk

Source: Compiled by author based on BNM guidelines

Surprisingly, the principles are exactly the same except for the wording of “Licensed Institutions” and “Licensed Islamic Banks.” Apart from the 14 principles that everyone pays attention to, a careful examination of the body of the guidelines reveals differences in handling Shariah issues. In the guidelines to conventional banks, there is no mention of Shariah issues. The guidance on Licensed Islamic Banks, however, has extensive descrip-tion of Shariah issues.

Importance of Corporate Governance1.04 (iv) Align corporate activities and behaviors with the expectation that

institutions will operate in a safe and sound manner, and in compli-ance with the Shariah and the applicable laws and regulations;

Part 2: Principles of Corporate Governance2.02 The board carries ultimate responsibility for the proper stewardship

of its Islamic bank. It has the responsibility in ensuring the maxi-mization of shareholders’ value and safeguarding the stakeholders’

2014] 71Corporate Governance and Shariah Governance at Islamic Financial Institutions:

Assessing from Current Practice in Malaysia

interests. This could be done through rigorous and diligent oversight over the Islamic bank’s affairs, establishing, amongst others, Shariah compliance, the corporate value, vision and strategy that will direct the activities of the Islamic bank, and to be aware of the types of ma-terial financial activities the Islamic bank intends to pursue.

Major Responsibilities of the Board2.10 (vi) Institute comprehensive policies, processes and infrastructure to

ensure Shariah compliance in all aspects of the Islamic bank’s opera-tions, products and activities.The board should establish a Shariah Committee and institute com-prehensive policies, processes and infrastructure for the purpose of ensuring that the business operations of the Islamic bank is con-ducted in accordance with Shariah principles. The compliance with Shariah principles is an integral feature in the Islamic bank. A com-prehensive and effective Shariah framework is imperative in assuring such compliance. The appointment and reappointment of the Shariah Committee member requires prior written approval of Bank Negara Malaysia. In approving the appointment and reappointment, Bank Negara Malaysia may impose necessary conditions it deems fit in ad-dition to the requirements in the Shariah Governance Framework for Islamic Financial Institutions

(vii) Set up an effective internal audit department, staffed with quali-fied internal audit personnel to perform internal audit functions, cov-ering the financial, management and Shariah audit.

Shariah Committee2.19 In addition to the board committee, the board is required to establish

a Shariah Committee.

Internal Audit2.99 The internal audit function is an important part of any effective inter-

nal control and risk management system because it provides an inde-pendent assessment of the adequacy of, and compliance with, estab-lished policies and procedures. In addition, internal auditors should review and evaluate the reliability, adequacy and effectiveness of the Islamic bank’s internal control. The scope of internal audit should cover financial, management and Shariah audit.

2.100 The internal audit function should complement the Shariah Commit-tee in ensuring Shariah compliance in all aspects of the Islamic bank’s products, operations and activities. The internal auditors, in consul-

72 RJIS [Vol. 22, No. 1

tation with the Shariah Committee, shall determine the scope of Sha-riah audit and are encouraged to produce internal Shariah compliant reports. The internal auditors shall acquire the relevant and appro-priate training to enhance their Shariah compliance review skills.

Comprehensive Disclosure Requirement2.110 Shariah Committee

(i) Key information and background of Shariah Committee members (including name, qualification and experience);

(ii) Terms of reference of the Shariah Committee;(iii) Roles and responsibilities of the Shariah Committee;(iv) Number of Shariah Committee meetings held in that year. Is-

lamic banks are encouraged to disclose information on the num-ber of meetings attended by each member of the committee; and

(v) Endorsement by the Shariah Committee on the conformity of the Islamic bank’s operations in accordance with Shariah principles.

(all underlines are added by the author for emphasis)

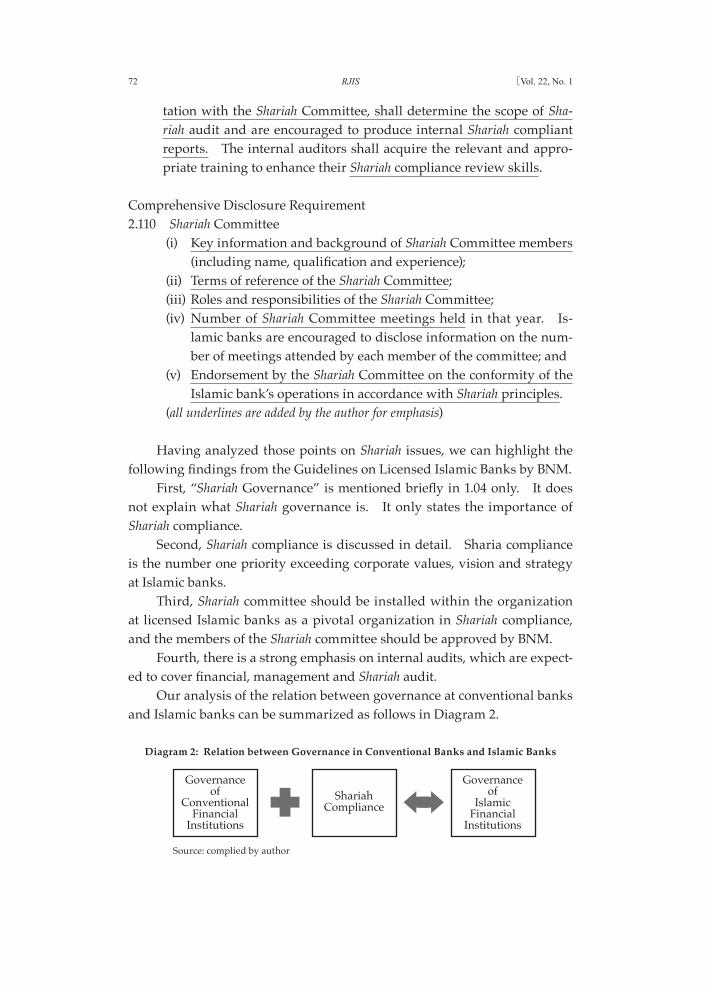

Having analyzed those points on Shariah issues, we can highlight the following findings from the Guidelines on Licensed Islamic Banks by BNM.

First, “Shariah Governance” is mentioned briefly in 1.04 only. It does not explain what Shariah governance is. It only states the importance of Shariah compliance.

Second, Shariah compliance is discussed in detail. Sharia compliance is the number one priority exceeding corporate values, vision and strategy at Islamic banks.

Third, Shariah committee should be installed within the organization at licensed Islamic banks as a pivotal organization in Shariah compliance, and the members of the Shariah committee should be approved by BNM.

Fourth, there is a strong emphasis on internal audits, which are expect-ed to cover financial, management and Shariah audit.

Our analysis of the relation between governance at conventional banks and Islamic banks can be summarized as follows in Diagram 2.

Diagram 2: Relation between Governance in Conventional Banks and Islamic Banks

Source: complied by author

Governanceof

ConventionalFinancial

Institutions

ShariahCompliance

Governanceof

IslamicFinancial

Institutions

2014] 73Corporate Governance and Shariah Governance at Islamic Financial Institutions:

Assessing from Current Practice in Malaysia

Section 3: Shariah Governance at Islamic Financial Institutions

In order to clarify the difference between Shariah governance and Shariah compliance, we would like to review the definition of Shariah governance.

BNM issued guidelines on Shariah governance called “Shariah Gover-nance Framework for Islamic Financial Institutions (SGF).” How is Shariah governance described in SGF?10

1 Introduction1.1 Shariah principles are the foundation for the practice of Islamic finance

through the observance of the tenets, conditions and principles es-poused by Shariah. Comprehensive compliance with Shariah principles would bring confidence to the general public and the financial markets on the credibility of Islamic finance operations.

1.2 Bank Negara Malaysia (the Bank) places great importance in ensuring that the overall Islamic financial system operates in accordance with Shariah principles. This is to be achieved through the two-tier Shariah governance infrastructure comprising two (2) vital components, which are a centralized Shariah advisory body at the Bank and an internal Shariah Committee formed in each respective Islamic financial institu-tion (IFI).

1.5 The Bank has developed the Shariah governance framework for IFIs with the primary objective of enhancing the role of the board, the Sha-riah Committee and the management in relation to Shariah matters, including enhancing the relevant key organs having the responsibility to execute the Shariah compliance and research functions aimed at the attainment of a Shariah-based operating environment.(emphasis is added by author)

Although 1.2 refers to a two-tier Shariah governance framework, there is no explanation of the meaning of Shariah governance in BNM’s guide-lines. All we can determine from BNM’s guidelines is that Shariah gover-nance is the structure to implement Shariah compliance.

An international standard setting organization called the Islamic Fi-nancial Services Board (IFSB) was established on March 10, 2003, by central banks of mostly Islamic countries. IFSB’s council members are composed of the central banks of the following 20 countries: Bahrain, Bangladesh, Brunei, Djibouti, Egypt, Indonesia, Iran, Jordan, Kuwait, Malaysia, Mal-dives, Mauritius, Nigeria, Pakistan, Qatar, Saudi Arabia, Singapore, Sudan,

10. Shari’ah Governance Framework for Islamic Financial Institutions (BNM/RH/GL_012_3). Issued on October 26, 2013.

74 RJIS [Vol. 22, No. 1

Syria and UAE. Also, the president of the Islamic Development Bank is a council member.

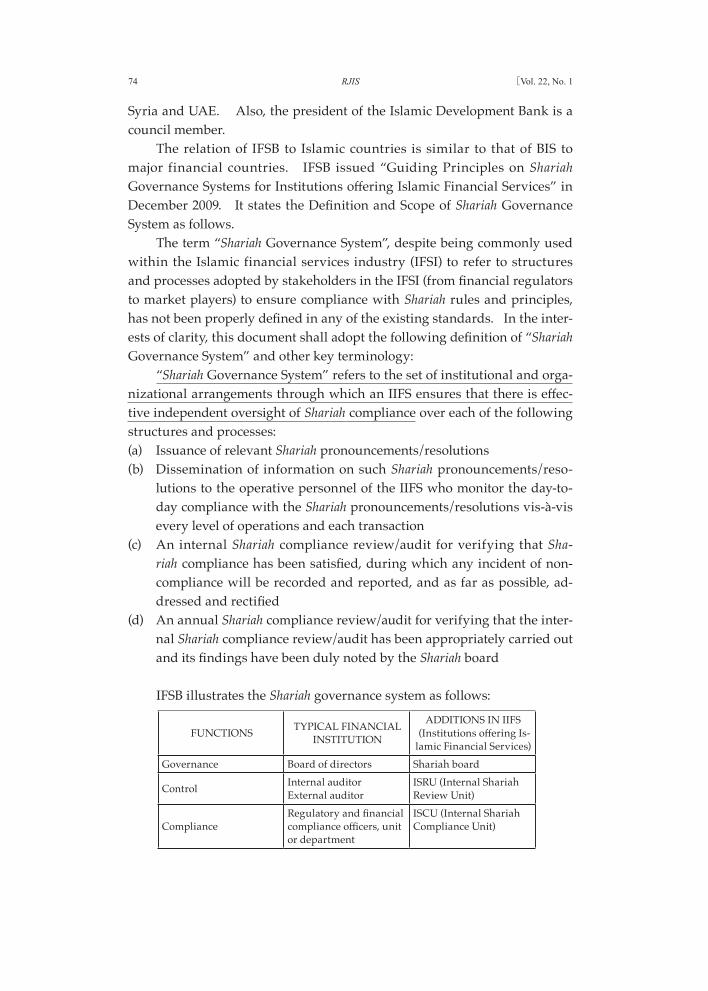

The relation of IFSB to Islamic countries is similar to that of BIS to major financial countries. IFSB issued “Guiding Principles on Shariah Governance Systems for Institutions offering Islamic Financial Services” in December 2009. It states the Definition and Scope of Shariah Governance System as follows.

The term “Shariah Governance System”, despite being commonly used within the Islamic financial services industry (IFSI) to refer to structures and processes adopted by stakeholders in the IFSI (from financial regulators to market players) to ensure compliance with Shariah rules and principles, has not been properly defined in any of the existing standards. In the inter-ests of clarity, this document shall adopt the following definition of “Shariah Governance System” and other key terminology:

“Shariah Governance System” refers to the set of institutional and orga-nizational arrangements through which an IIFS ensures that there is effec-tive independent oversight of Shariah compliance over each of the following structures and processes:(a) Issuance of relevant Shariah pronouncements/resolutions(b) Dissemination of information on such Shariah pronouncements/reso-

lutions to the operative personnel of the IIFS who monitor the day-to-day compliance with the Shariah pronouncements/resolutions vis-à-vis every level of operations and each transaction

(c) An internal Shariah compliance review/audit for verifying that Sha-riah compliance has been satisfied, during which any incident of non-compliance will be recorded and reported, and as far as possible, ad-dressed and rectified

(d) An annual Shariah compliance review/audit for verifying that the inter-nal Shariah compliance review/audit has been appropriately carried out and its findings have been duly noted by the Shariah board

IFSB illustrates the Shariah governance system as follows:

FUNCTIONS TYPICAL FINANCIAL INSTITUTION

ADDITIONS IN IIFS (Institutions offering Is-lamic Financial Services)

Governance Board of directors Shariah board

Control Internal auditorExternal auditor

ISRU (Internal Shariah Review Unit)

ComplianceRegulatory and financial compliance officers, unit or department

ISCU (Internal Shariah Compliance Unit)

2014] 75Corporate Governance and Shariah Governance at Islamic Financial Institutions:

Assessing from Current Practice in Malaysia

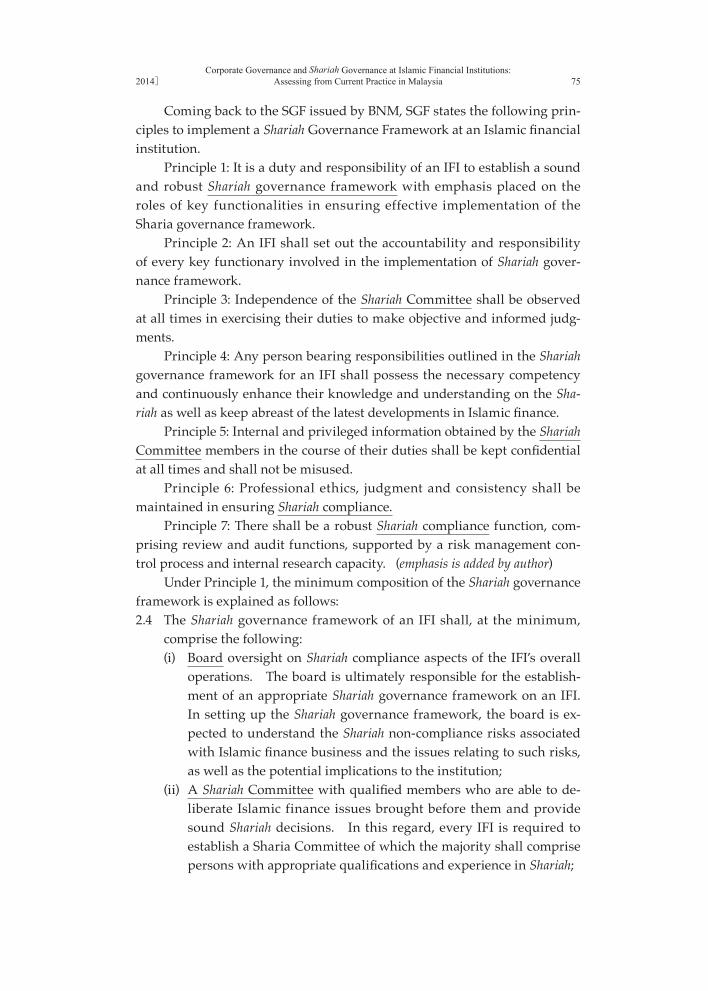

Coming back to the SGF issued by BNM, SGF states the following prin-ciples to implement a Shariah Governance Framework at an Islamic financial institution.

Principle 1: It is a duty and responsibility of an IFI to establish a sound and robust Shariah governance framework with emphasis placed on the roles of key functionalities in ensuring effective implementation of the Sharia governance framework.

Principle 2: An IFI shall set out the accountability and responsibility of every key functionary involved in the implementation of Shariah gover-nance framework.

Principle 3: Independence of the Shariah Committee shall be observed at all times in exercising their duties to make objective and informed judg-ments.

Principle 4: Any person bearing responsibilities outlined in the Shariah governance framework for an IFI shall possess the necessary competency and continuously enhance their knowledge and understanding on the Sha-riah as well as keep abreast of the latest developments in Islamic finance.

Principle 5: Internal and privileged information obtained by the Shariah Committee members in the course of their duties shall be kept confidential at all times and shall not be misused.

Principle 6: Professional ethics, judgment and consistency shall be maintained in ensuring Shariah compliance.

Principle 7: There shall be a robust Shariah compliance function, com-prising review and audit functions, supported by a risk management con-trol process and internal research capacity. (emphasis is added by author)

Under Principle 1, the minimum composition of the Shariah governance framework is explained as follows:2.4 The Shariah governance framework of an IFI shall, at the minimum,

comprise the following: (i) Board oversight on Shariah compliance aspects of the IFI’s overall

operations. The board is ultimately responsible for the establish-ment of an appropriate Shariah governance framework on an IFI. In setting up the Shariah governance framework, the board is ex-pected to understand the Shariah non-compliance risks associated with Islamic finance business and the issues relating to such risks, as well as the potential implications to the institution;

(ii) A Shariah Committee with qualified members who are able to de-liberate Islamic finance issues brought before them and provide sound Shariah decisions. In this regard, every IFI is required to establish a Sharia Committee of which the majority shall comprise persons with appropriate qualifications and experience in Shariah;

76 RJIS [Vol. 22, No. 1

(iii) Effective management responsibilities in providing adequate re-sources and capable manpower support to every function involved in the implementation of Shariah governance, in order to ensure that the execution of business operations are in accordance with the Shariah;

(iv) An internal Shariah review that is conducted on a continuous basis, which is a review of processes and deliverables, as well as deter-mining that such processes and outcomes satisfy the needs of the Shariah;

(v) A regular Shariah audit, at least on an annual basis, verifying that the IFI’s key functions and business operations comply with Sha-riah;

(vi) A Shariah risk management process to identify all possible Shariah non-compliance risks and, where appropriate, remedial measures that need to be taken to reduce the risk;

(vii) An internal Shariah research team to conduct research on Shariah; and

(viii) Issuance and dissemination of Shariah decisions to the relevant stakeholders.

(emphasis is added by author)Also, under Principle 2, BNM’s intention to integrate Shariah with IFI’s

business direction is shown as follows. It may take time to know whether this will indeed be effective.2.4 The Board may consider appointing at least one (1) member of the Sha-

riah Committee as a member of the board that could serve as ‘bridge’ between the board and the Shariah Committee. The presence of a di-rector with sound Shariah knowledge would foster greater understand-ing and appreciation amongst the board members on the decisions made by the Shariah Committee.

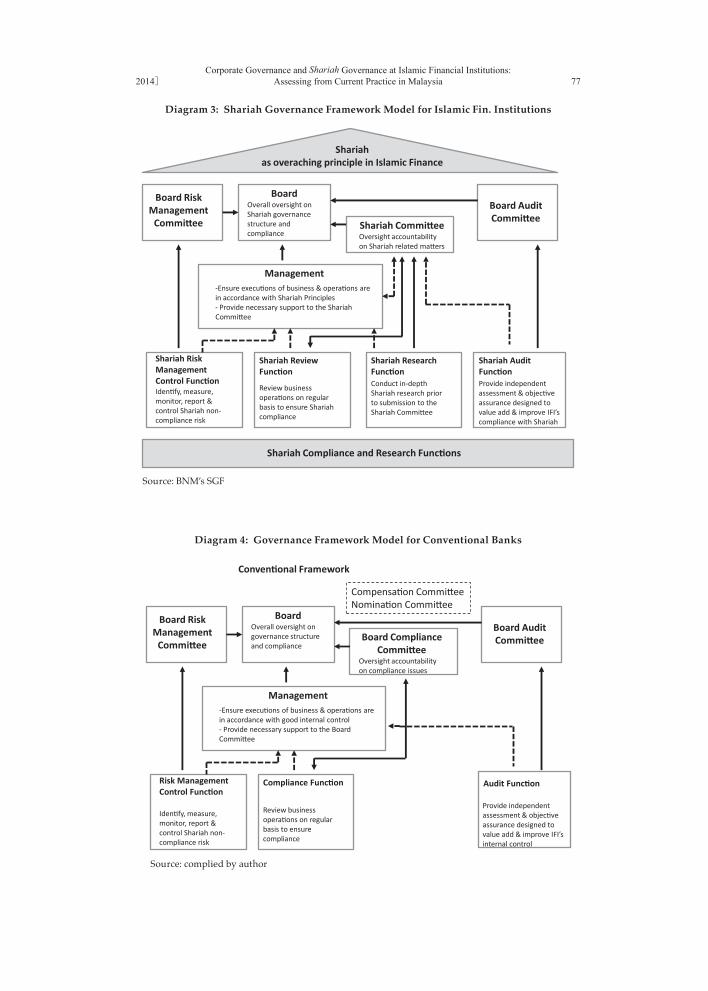

As a summary of the above-mentioned minimum requirements, BNM’s SGF provides the following diagram (Diagram 3) to show the rela-tion of each element. In addition, The governance framework at conven-tional banks, which summarizes the guidelines issued by BIS, is shown in Diagram 4.

Diagram 3 clearly tells us that Shariah governance is not only a com-prehensive concept but also a superior concept in managing Shariah banks. Shariah governance is the governance framework to make the bank account-

11. The Committee of Sponsoring Organization of Treadway Commission (COSO) “Internal Control-Integrated Framework” announced in 1992, amended in 2013.

2014] 77Corporate Governance and Shariah Governance at Islamic Financial Institutions:

Assessing from Current Practice in Malaysia

Diagram 3: Shariah Governance Framework Model for Islamic Fin. Institutions

Diagram 4: Governance Framework Model for Conventional Banks

Source: BNM’s SGF

Shariahas overaching principle in Islamic Finance

Board RiskManagement

Committee

BoardOverall oversight on Shariah governance structure and compliance

Board Audit Committee

Shariah CommitteeOversight accountability on Shariah related matters

Management-Ensure executions of business & operations are in accordance with Shariah Principles- Provide necessary support to the ShariahCommittee

Shariah Risk Management Control FunctionIdentify, measure, monitor, report & control Shariah non-compliance risk

Shariah Review Function

Review business operations on regular basis to ensure Shariahcompliance

Shariah Research FunctionConduct in-depth Shariah research prior to submission to the Shariah Committee

Shariah Audit FunctionProvide independent assessment & objective assurance designed to value add & improve IFI’s compliance with Shariah

Shariah Compliance and Research Functions

Conventional Framework

Board RiskManagement

Committee

BoardOverall oversight on governance structure and compliance

Board Audit CommitteeBoard Compliance

CommitteeOversight accountability on compliance issues

Management-Ensure executions of business & operations are in accordance with good internal control- Provide necessary support to the Board Committee

Risk Management Control Function

Identify, measure, monitor, report & control Shariah non-compliance risk

Compliance Function

Review business operations on regular basis to ensure compliance

Audit Function

Provide independent assessment & objective assurance designed to value add & improve IFI’s internal control

Compensation CommitteeNomination Committee

Source: complied by author

78 RJIS [Vol. 22, No. 1

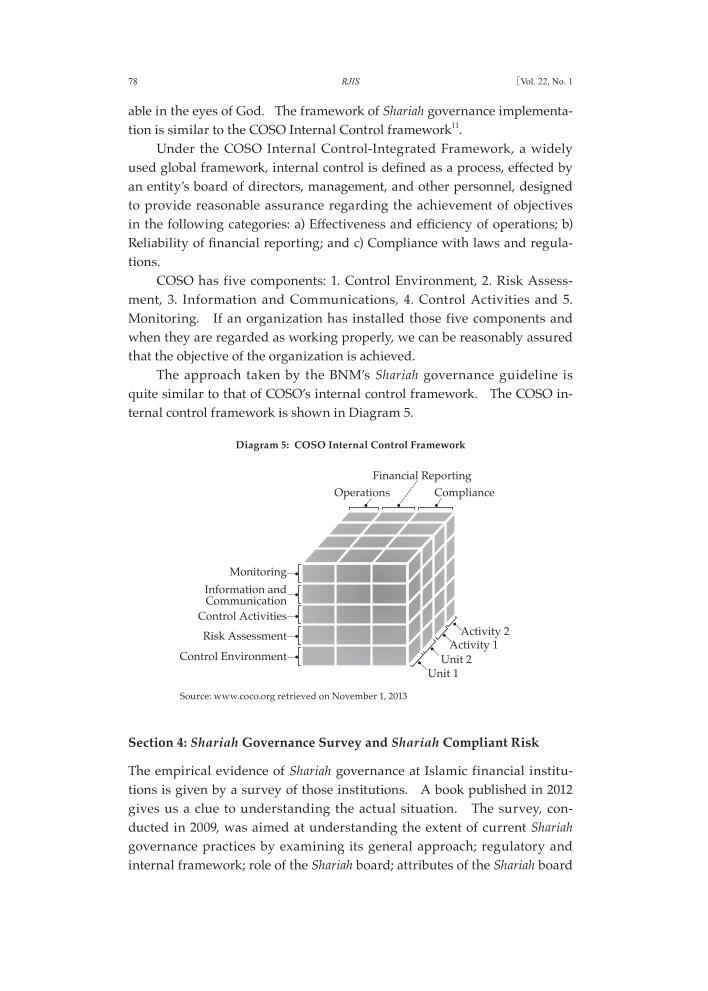

able in the eyes of God. The framework of Shariah governance implementa-tion is similar to the COSO Internal Control framework11.

Under the COSO Internal Control-Integrated Framework, a widely used global framework, internal control is defined as a process, effected by an entity’s board of directors, management, and other personnel, designed to provide reasonable assurance regarding the achievement of objectives in the following categories: a) Effectiveness and efficiency of operations; b) Reliability of financial reporting; and c) Compliance with laws and regula-tions.

COSO has five components: 1. Control Environment, 2. Risk Assess-ment, 3. Information and Communications, 4. Control Activities and 5. Monitoring. If an organization has installed those five components and when they are regarded as working properly, we can be reasonably assured that the objective of the organization is achieved.

The approach taken by the BNM’s Shariah governance guideline is quite similar to that of COSO’s internal control framework. The COSO in-ternal control framework is shown in Diagram 5.

Section 4: Shariah Governance Survey and Shariah Compliant Risk

The empirical evidence of Shariah governance at Islamic financial institu-tions is given by a survey of those institutions. A book published in 2012 gives us a clue to understanding the actual situation. The survey, con-ducted in 2009, was aimed at understanding the extent of current Shariah governance practices by examining its general approach; regulatory and internal framework; role of the Shariah board; attributes of the Shariah board

Diagram 5: COSO Internal Control Framework

Source: www.coco.org retrieved on November 1, 2013

Monitoring

OperationsFinancial Reporting

Compliance

Information andCommunication

Control Activities

Risk Assessment

Unit 1Unit 2

Activity 1Activity 2

Control Environment

2014] 79Corporate Governance and Shariah Governance at Islamic Financial Institutions:

Assessing from Current Practice in Malaysia

in terms of independence, competence, transparency and confidentiality; operational procedures; and assessment of the Shariah board. The result shows the formality of the Shariah governance framework, but it does not give us information how effective Shariah governance is in managing ac-countability to God12.

When we talk about Shariah governance, we always mention Shariah compliant risk, but what are practical examples of such risks? In this chap-ter, we analyze three cases.

Case 1. Sukuk issuance from Malaysia based on the Islamic contract of Murabahah and Bai Bithaman Ajil (BBA)Sukuk are Shariah compliant fixed income instruments with features that resemble bonds in the conventional market. They are widely used as a Sha-riah compliant method for raising capital and may be structured around a variety of Islamic contracts.The earliest form of Sukuk originated from Malaysia were based on the Is-lamic contract of Murabahah and BBA whereby the sale contract between the Issuer and the Investors / Sukuk-holders consequently results in a debt obligation from the Issuer. In Malaysia, Murabahah Sukuk were utilized primarily for short term issuance whilst BBA Sukuk were employed pri-marily for longer term issuances. Although approved by the Shariah Advi-sory Council of both regulatory bodies i.e. the Bank Negara Malaysia (the Malaysian Central Bank, BNM) and the Securities Commission of Malaysia (SC), the usage of the Malaysian version of Murabahah and BBA was not accepted elsewhere. This raised questions on standardization of Sukuk structures particularly in view of the fact that Shariah scholars from Malay-sia also sits on Shariah Boards of Islamic financial institutions outside of Ma-laysia where the Malaysian version of Murabahah and BBA was prohibited. Despite the divergence, BNM and the SC continued to allow the use of Mu-rabahah and BBA, the Malaysian Sukuk market began to gravitate towards a more universally acceptable Islamic structures and the use of Murabahah and BBA began to decline considerably as more counterparties shied away from its usage. Recent survey by Rating Agency Malaysia on Sukuk shows the issuance of BBA Sukuk is almost non-existent today. However Murabahah Sukuk con-tinues to be in practice, this may have been structured to be more univer-sally accepted by Shariah scholars.

12. Zulkifili Hassan, 2012, Shari’ah Governance in Islamic Banks, Edinburgh University Press.

80 RJIS [Vol. 22, No. 1

Case 2. The Goldman Sachs proposed SukukIn 2011, Goldman Sachs announced its intention to issue a $2 billion Sukuk program. Goldman Sachs registered its Sukuk program with the Irish Stock Exchange and set up a special-purpose vehichle in the Cayman Is-lands. HSBC had earlier successfully issued a $500 million Sukuk in a mar-ket environment where demand for premium rated Sukuk exceeds supply. The general perception at that stage was that the Goldman Sachs Sukuk would be equally successful.But Goldman’s plan ran into controversy among Islamic scholars and analysts, who questioned whether the U.S. investment bank was obeying religious principles. Two issues that received widespread attention were in connection with Shariah compliance, firstly whether the proceeds from the Sukuk would be utilized to fund non- Shariah compliant activities and secondly whether the Murabahah structure that Goldman Sachs opted meets the standard Shariah requirements. There were also confusion as to whether or not the proposed Goldman Sachs Sukuk received approval from Shariah scholars. Some scholars reported that the fatwa was already issued, while other scholars involved said that they did not sign off on the fatwa, which contradicted what Goldman Sachs and its advisors were saying. By this time however the damage in the eyes of Shariah compliant investors was already done. The Sukuk was never issued and the prospectus on the Irish Stock Exchange was past its 12-months validity period13.

Case 3. Islamic Total Return Swap (Wa’ad) Arrangement The Islamic Total Return Swap, also known as the Shariah Conversion Technology and the dual Wa’ad contract first surfaced in 2007 and were of-fered by several Islamic banks. However, it is perhaps better known in the Islamic finance industry as an Islamic investment product that originated from Deutsche Bank. The product provides investments into Shariah com-pliant assets which then swap the returns from the Shariah compliant assets with a hedge fund index which can contain conventional or non- Shariah compliant underlying assets, in order to enhance the returns from the origi-nal Shariah compliant investments. The assets the clients invested in directly are Shariah compliant, which en-abled this product to obtain approval from its Shariah Board. The swap however is referenced to a hedge fund index that may or may not be Sharia compliant. This second leg of the transaction is less obvious and was a sub-

13. Several articles on Goldman’s sukuk issuance, such as “Islamic Finance: Islamic Sukuk by Goldman Sacks Causes Debate” Reuters, Feb 23, 2012; and “Shari’ah adviser of Ill-fated Gold-man Sachs sukuk closed down” Euroweek, Jan 30, 2013.

2014] 81Corporate Governance and Shariah Governance at Islamic Financial Institutions:

Assessing from Current Practice in Malaysia

ject of debate among Shariah scholars. A research paper by Sheikh Yusuf Talal DeLorenzo, a Shariah Board member of AAOIFI raised concerns that the underlying asset for the swap i.e. the hedge fund index would open the floodgate for all manner of non- Shariah compliant investments that could potentially give better returns than Shariah compliant investments and is therefore attractive, by simply adopting this swap mechanism. Deutsche Bank, however, argued that the product allows Islamic investors to widen its investment exposure to a far wider universe of investment assets that were not available to Islamic investors previously. Nonetheless overtime, the product slowly fell out of favor after doubts were cast on its Shariah au-thenticity. The above three cases show that Shariah compliance risk is primarily a re-sult of contradictions in opinions among Shariah scholars. Academic study has not yet advanced to the point to analyze these situations further.

Conclusion

We compared several governance concepts. The concept of governance first started from the OECD, was transferred to BIS, and then transferred to BNM.

Shariah governance is accountability to God, which is the first priority at Islamic banks. The guidelines of Shariah governance mainly deal with Shariah compliance. Creating an internal control framework for Shariah compliance is the way to in install a Shariah governance system.

We would like to mention recent examples of deficiency in governance. We would like to point out the effectiveness of governance largely depends on society. Recently, there have been two interesting examples: JP Morgan and Mizuho.

JP Morgan announced on October 11, 2013, that it had set aside $9.2 billion to cover its mounting legal expenses, leading it to report its first quarterly loss under Jamie Dimon, JP Morgan’s chief executive. Mr. Dimon described the legal expenses as “painful.” JP Morgan has many problems with governance, and the following are just a few: (i) a $2 billion loss from a huge CDS position in London, nicknamed the “Whale in London;” (ii) manipulating energy prices, for which JPMorgan was charged a fine; (iii) a mortgage payment manipulation during 2008-2011 that JPMorgan was charged for. Frequent misconduct is evidence of weak governance, but the CEO was not asked to resign because he contributed a large profit to JP Morgan. Mass media has not been critical of Mr. Dimon.

The situation is quite different at Mizuho. In October 2013, Mizuho Bank was found to have supplied car loans through its affiliate consumer

82 RJIS [Vol. 22, No. 1

credit company, Orient Credit. The total loan amount was 200 million yen (about $2 million) for 230 instances. The Financial Services Agency, the governing authority on banks, cited the bank for allowing the loans to re-main in place even after they were discovered at the end of 2010. Japanese media was very critical of Mizuho, and Mizuho announced its plan to pun-ish over 30 senior executives. President Sato is subject to a half-year sus-pension in pay. Chairman Tsukamoto will step down from the bank.

The big difference between the U.S. and Japan is caused by the culture at the society. Japanese society has a strong culture to follow rules, conse-quently even minor violations lead to harsh criticism by the media. In such an environment, governance is very effective. In Japan, the oversight of a $2 million loan in a $500 billion portfolio led to the resignation of the chair-man, which sounds ridiculous to Westerners.

In the U.S., Mr. Dimon says in his 2012 letter to the shareholders that “the problems were our fault, and it is our job to fix them. In fact, I feel ter-rible that we let our regulators down.” He doesn’t apologize for his error. In such a culture, it may be difficult to expect self-governance.

Muslim culture may differ from one country to another. Even though Shariah governance and accountability to God is first priority, the effective-ness of governance will differ country by country, depending on the people. In short, even if a perfect Shariah governance framework is installed, it is human conduct that is ultimately accountable to God.

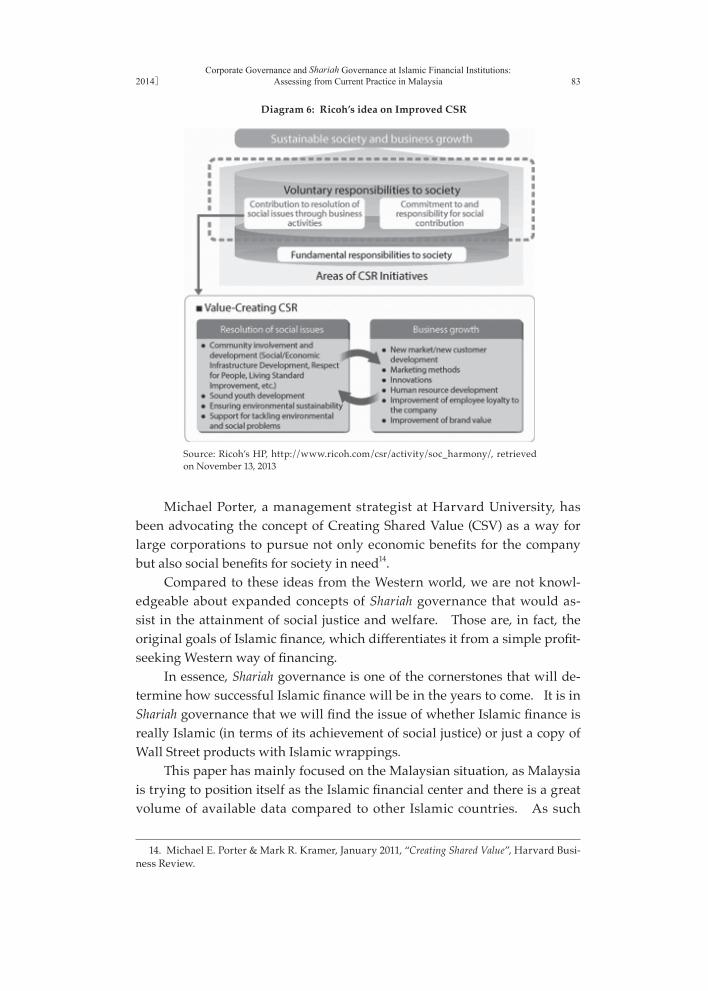

In ending our study, we would like to mention recent developments in the concept of governance in the Western world. The concept of gov-ernance has developed into several advanced steps. Corporate Social Re-sponsibility (CSR) is now a well-known concept all over the world. Let’s take the example of Ricoh, a Japanese business equipment manufacturing company. The disclosure magazine of Ricoh mentions its CSR activity as follows.

The Ricoh Group is engaged in “two-tier” CSR activities based on the three ideas constituting the foundation of CSR specified in the chart be-low: the first tier involves basic social responsibilities and the second tier involves voluntary social responsibilities. We aim to build public trust through our first tier activities and enhance our attractiveness through second tier activities and by achieving these goals simultaneously to in-crease the value of the company. We develop and implement action plans focusing on the four key areas specified in our CSR Charter: integrity in corporate activities, harmony with the environment, respect for people, and harmony with society.

Ricoh’s explanation about the evolution of its CSR concept shows its clear dedication to solve social issues through improved CSR (Diagram 6) .

2014] 83Corporate Governance and Shariah Governance at Islamic Financial Institutions:

Assessing from Current Practice in Malaysia

Michael Porter, a management strategist at Harvard University, has been advocating the concept of Creating Shared Value (CSV) as a way for large corporations to pursue not only economic benefits for the company but also social benefi ts for society in need14.

Compared to these ideas from the Western world, we are not knowl-edgeable about expanded concepts of Shariah governance that would as-sist in the attainment of social justice and welfare. Those are, in fact, the original goals of Islamic fi nance, which diff erentiates it from a simple profi t-seeking Western way of fi nancing.

In essence, Shariah governance is one of the cornerstones that will de-termine how successful Islamic fi nance will be in the years to come. It is in Shariah governance that we will fi nd the issue of whether Islamic fi nance is really Islamic (in terms of its achievement of social justice) or just a copy of Wall Street products with Islamic wrappings.

This paper has mainly focused on the Malaysian situation, as Malaysia is trying to position itself as the Islamic fi nancial center and there is a great volume of available data compared to other Islamic countries. As such

Diagram 6: Ricoh’s idea on Improved CSR

Source: Ricoh’s HP, http://www.ricoh.com/csr/activity/soc_harmony/, retrieved on November 13, 2013

14. Michael E. Porter & Mark R. Kramer, January 2011, “Creating Shared Value”, Harvard Busi-ness Review.

84 RJIS [Vol. 22, No. 1

our analysis has not yet dealt with actual Shariah governance practices at Islamic banks. Therefore, our next step of study is to conduct fact-finding interviews and survey of several Islamic banks and investment companies to find out how they actually exercise Shariah governance. Also, we would like to examine how they tackle issues of social justice and welfare through their financial services offerings15.

ReferencesEdbiz Consulting, 2013, Global Islamic Finance Report 2013, LondonHassan, Zulkifli, 2012, Shariah Governance in Islamic Banks, Edinburgh University PressMorris, Virginia B., 2009, A Muslim’s Guide to Investment & Personal Finance, Lightbulb

PressPorter, Michael M & Kramer, Mark R, January 2011, Creating Shared Value, Harvard Busi-

ness ReviewSaiful Azhar Rosly, 2005, Critical Issues on Islamic Banking and Financial Markets, Dinama

PublishingVissar, Hans, 2009, Islamic Finance Principles and Practice, Edward Elgar Publishing Lim-

ited

15. The author is grateful to Mr. Nik Norishky Tani at PNB for his continuous support in sharing his knowledge of Shari’ah finance.