Embed Size (px)

Citation preview

Equity Research Special Report January 2013

The Bank of Nova Scotia is the parent company and a related issuer of Scotia Capital Inc. and ultimate parent company and related issuer of Scotia Capital (USA) Inc. CI Financial Corp. is a Related Issuer of Scotia Capital Inc. Scotia Capital Inc was retained by Telus Corporation to provide a fairness opinion with respect to a proposed share conversion. For Reg AC Certifi cation and important disclosures see Appendix A of this report. Analysts employed by non-U.S. affi liates are not registered/qualifi ed as research analysts with FINRA in the U.S.

Focus 2013

Bottom Line Trumping Headline

Focus 2013 January 2013

1

Contents

Director’s Comment

Bottom Line Trumping Headline 3

Portfolio Strategy: Bottom Line Trumping Headline

Revisiting 2012: S&P 500 Beats TSX for Second Consecutive Year 5

Small Cap Strategy

Small Caps Delivering Gains in 2013 21

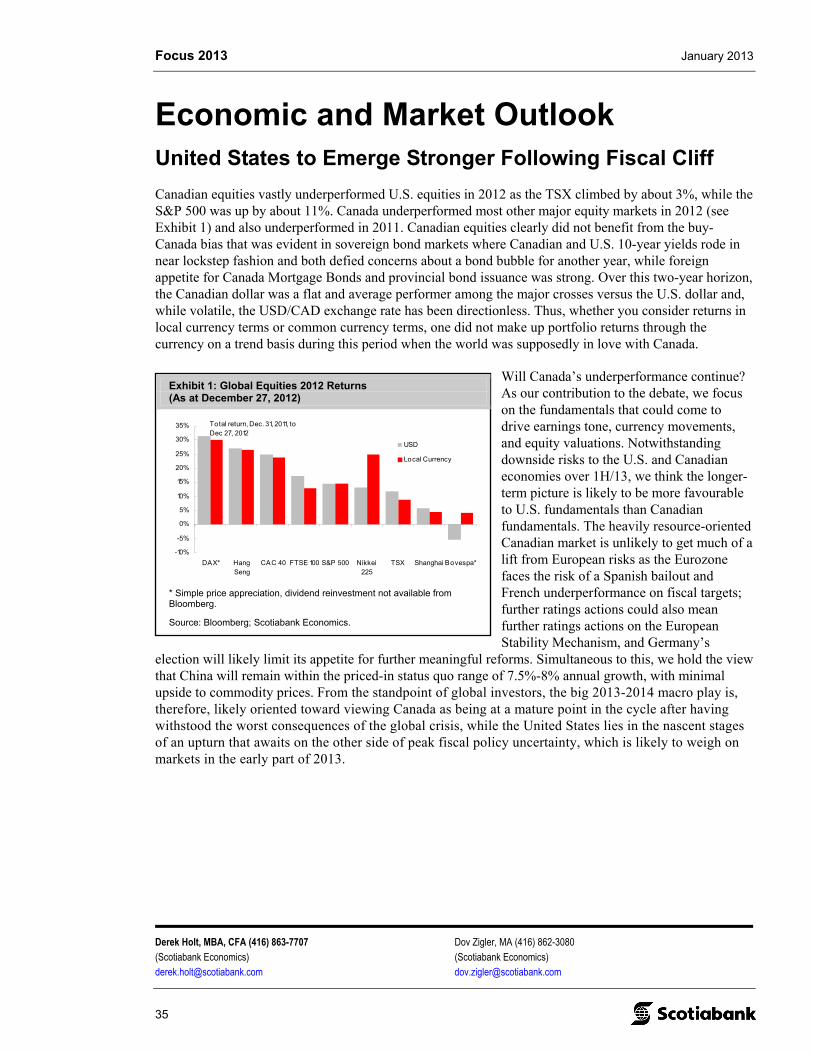

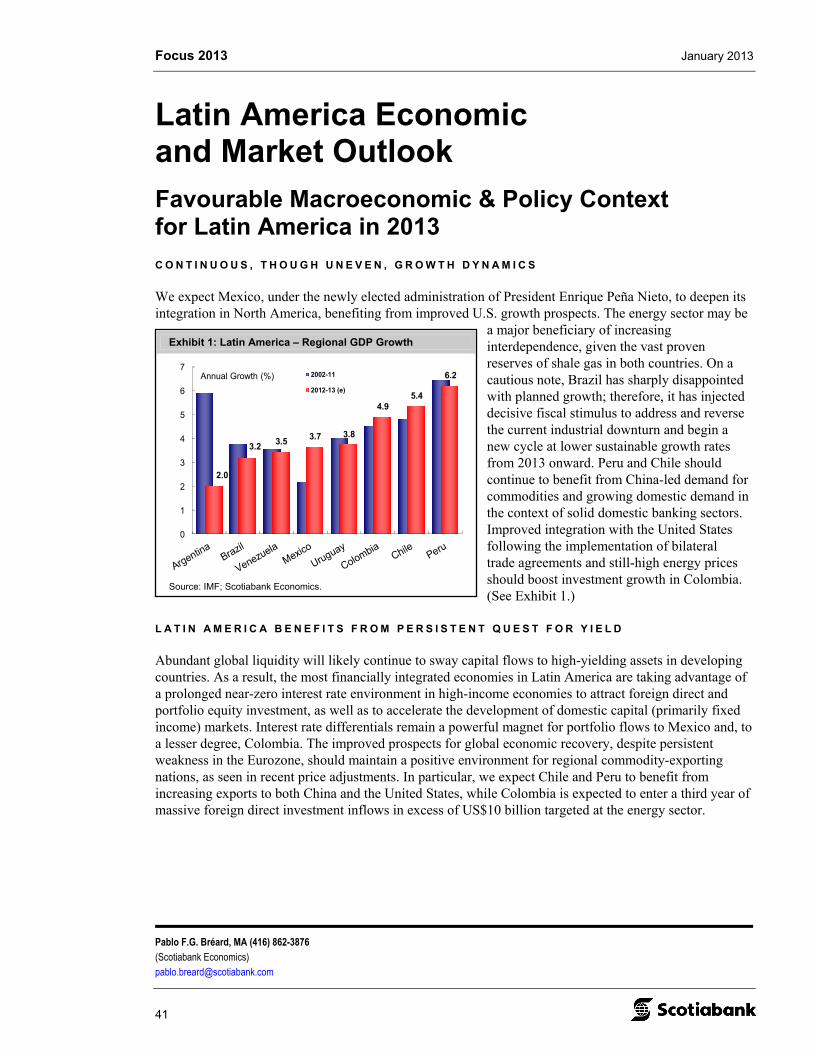

Economic and Market Outlook

United States to Emerge Stronger Following Fiscal Cliff 35

Latin America Economic and Market Outlook

Favourable Macroeconomic & Policy Context for Latin America in 2013 41

Sector Comments

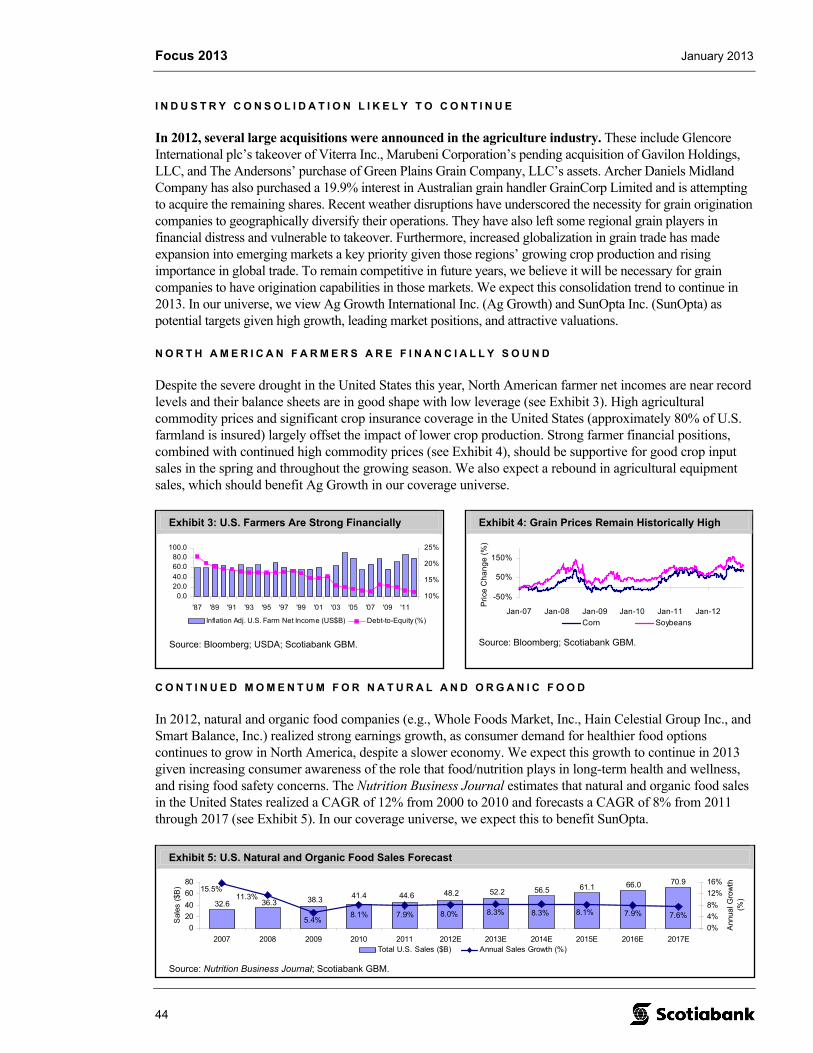

Agriculture

Weather Market Here to Stay 43

Banks, Americas

Refocused Banking System – Return of Capital – Valuation Recovery 47

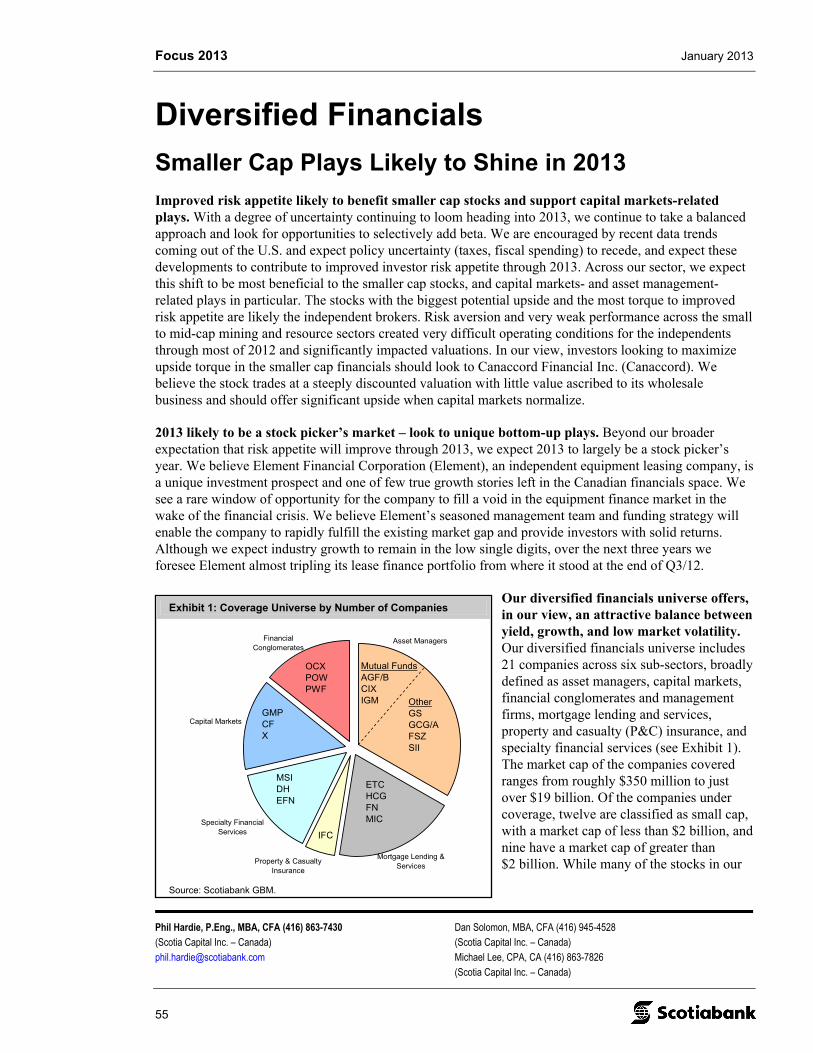

Diversified Financials

Smaller Cap Plays Likely to Shine in 2013 55

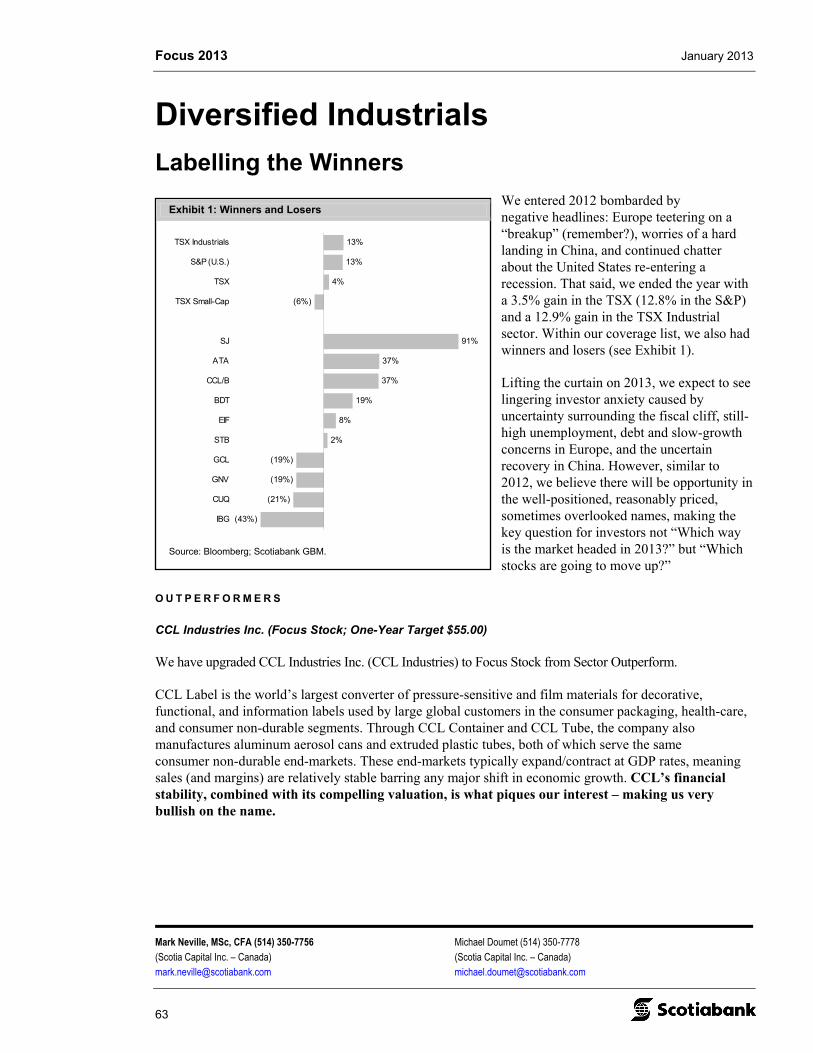

Diversified Industrials

Labelling the Winners 63

Energy Infrastructure

Pipelines and Power Lines 71

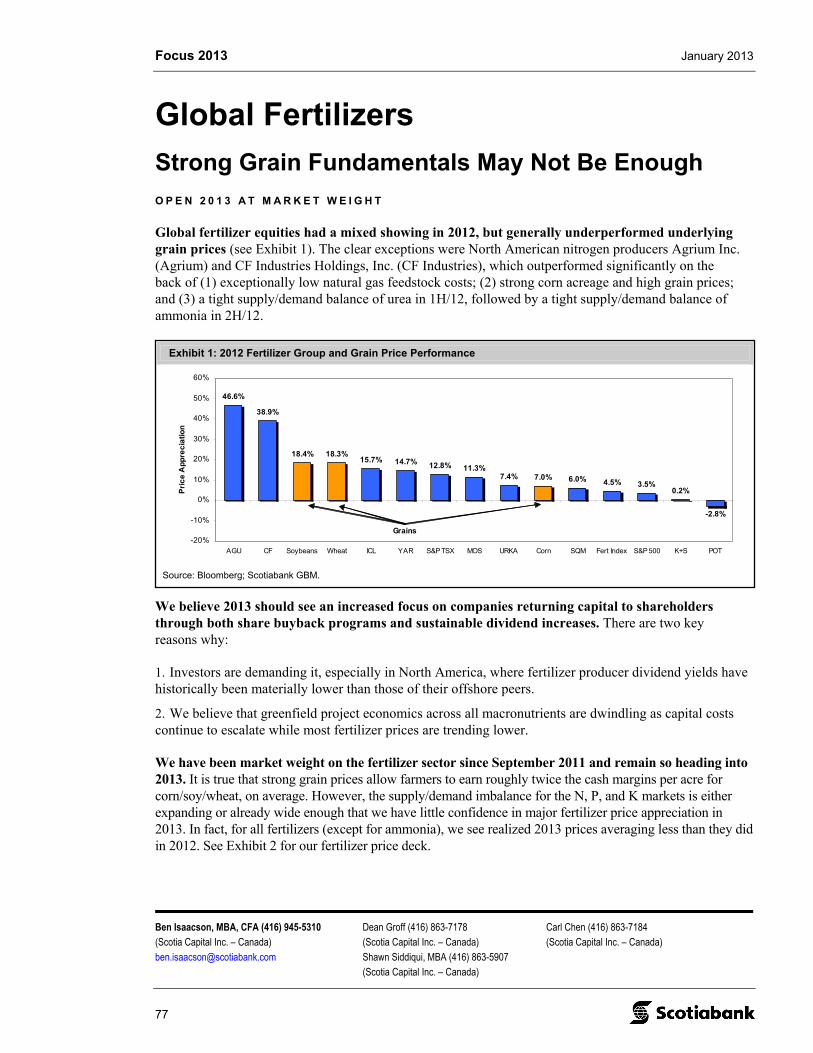

Global Fertilizers

Strong Grain Fundamentals May Not Be Enough 77

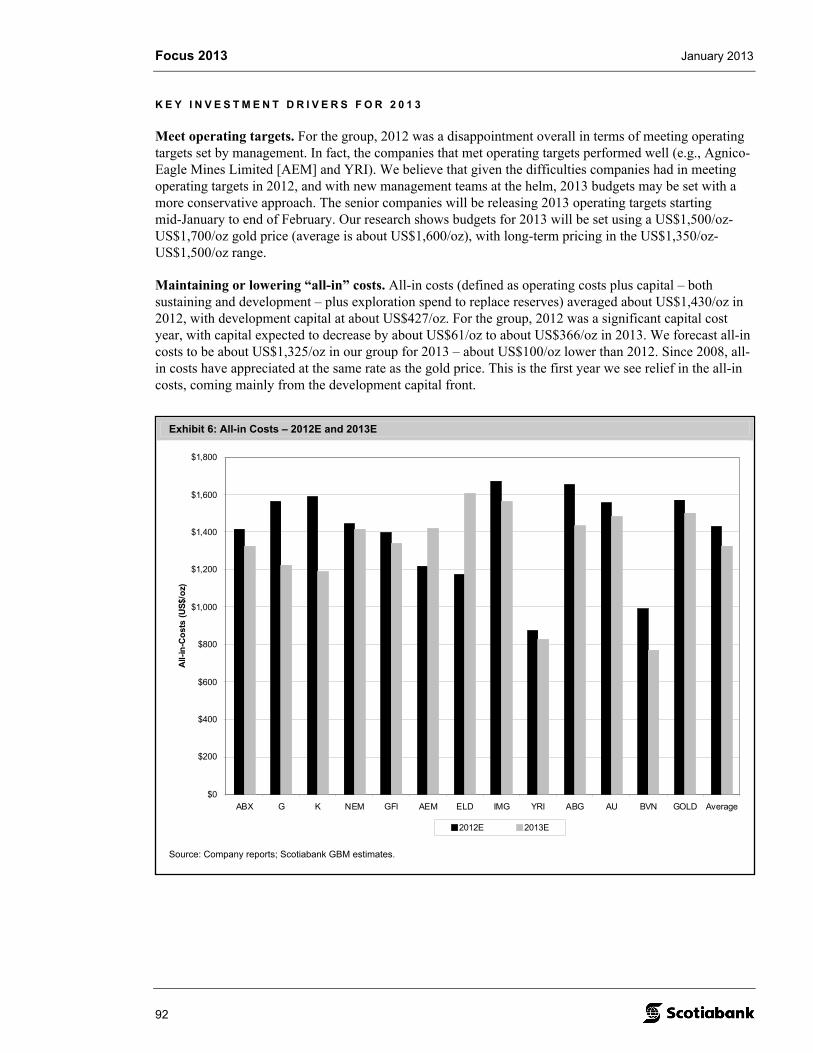

Gold & Precious Minerals

A New Year… Starting Afresh 85

Industrial Products

Prefer Steel & Wheels over Big Iron in 2013 99

LatAm Airports

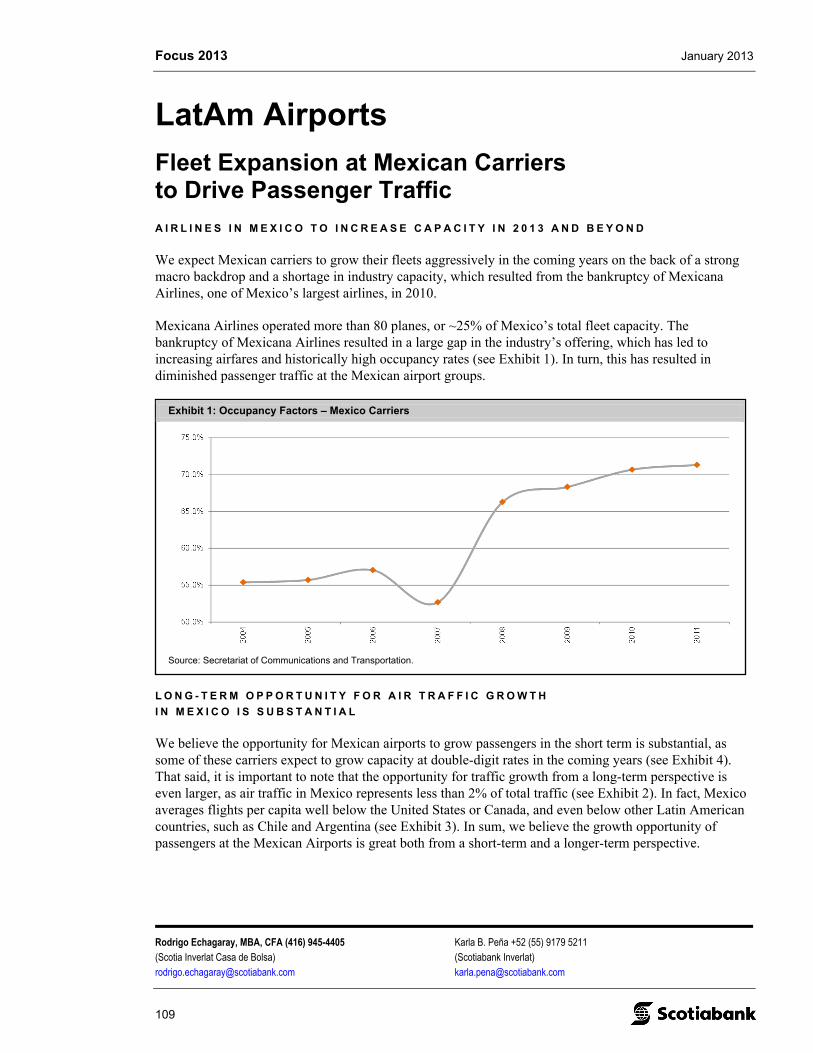

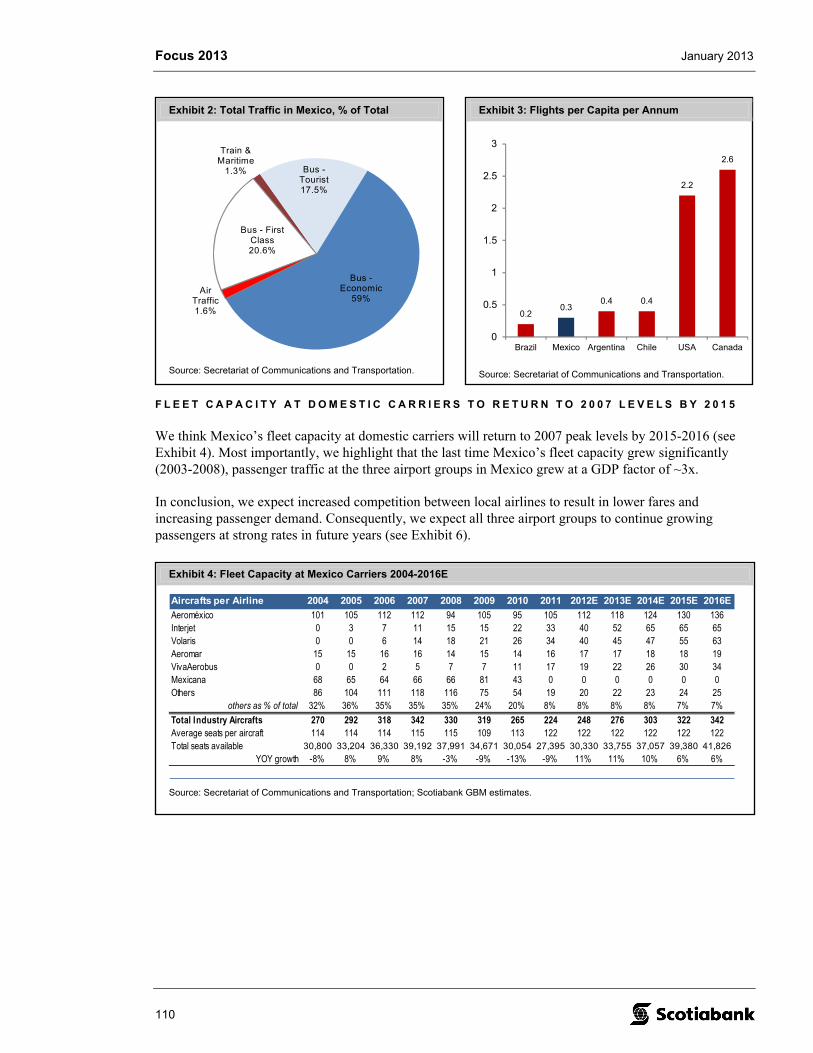

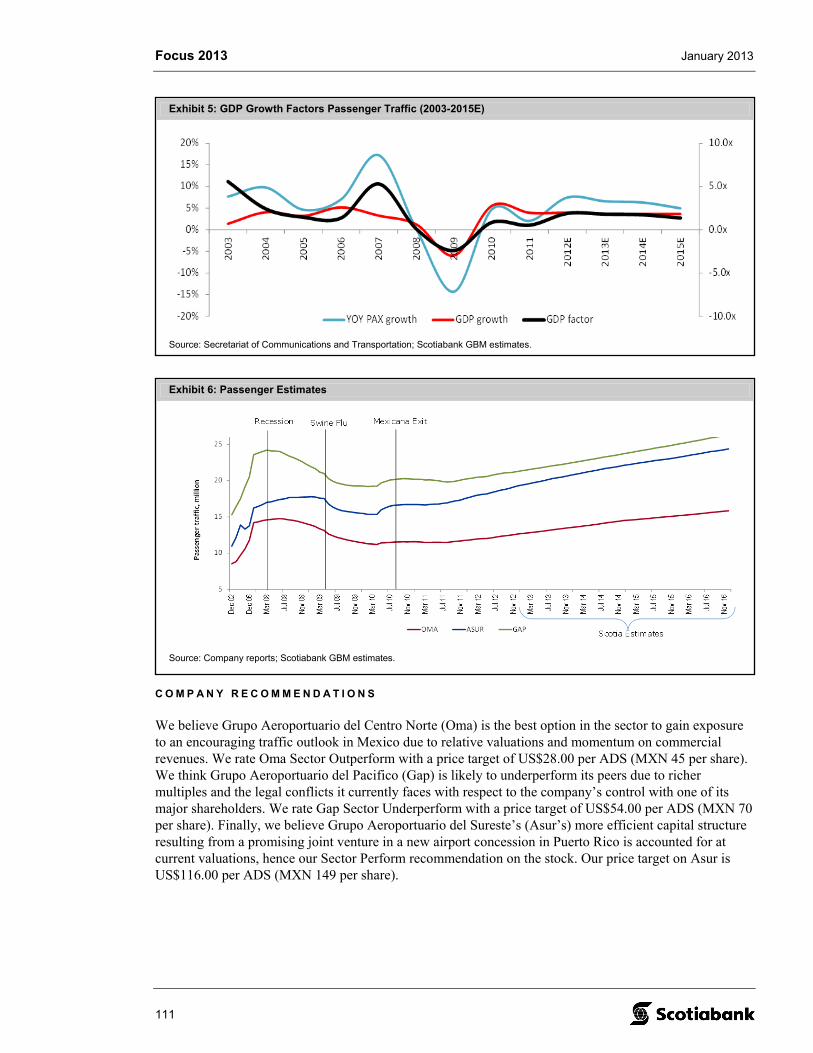

Fleet Expansion at Mexican Carriers to Drive Passenger Traffic 109

LatAm Construction & Infrastructure

Key Drivers: New Administration in Mexico and Private and Public Investment in Peru 115

Focus 2013 January 2013

2

Media

Advancing the Transition Toward Online Media 121

Metals & Mining

Same Challenges, New Opportunities 127

North American Life Insurance

Selective Opportunities Despite Stiff Headwinds 131

Oil & Gas

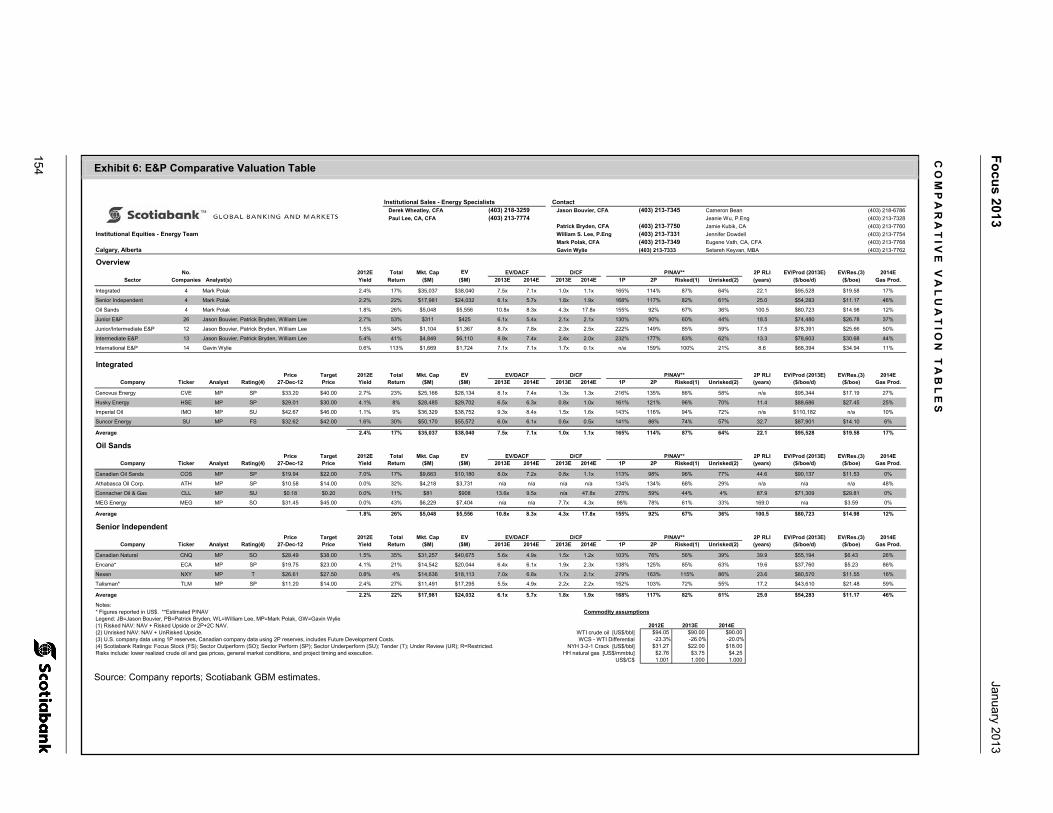

Canadian E&P – Themes for 2013 137

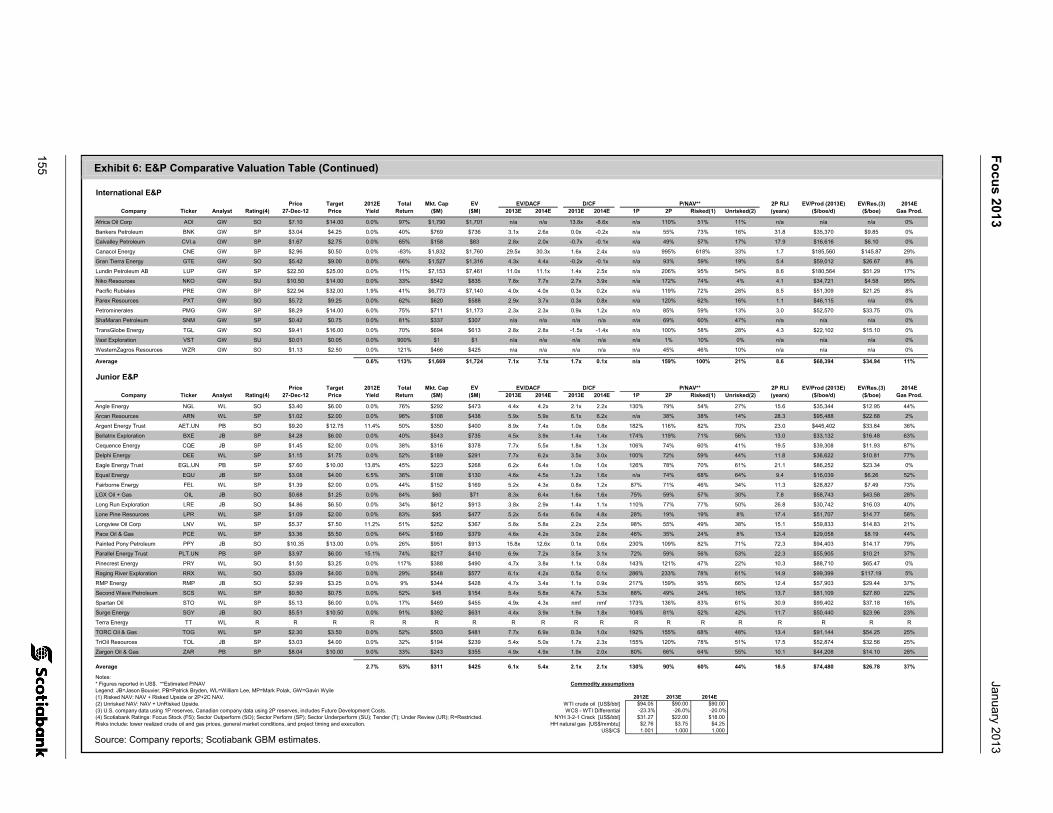

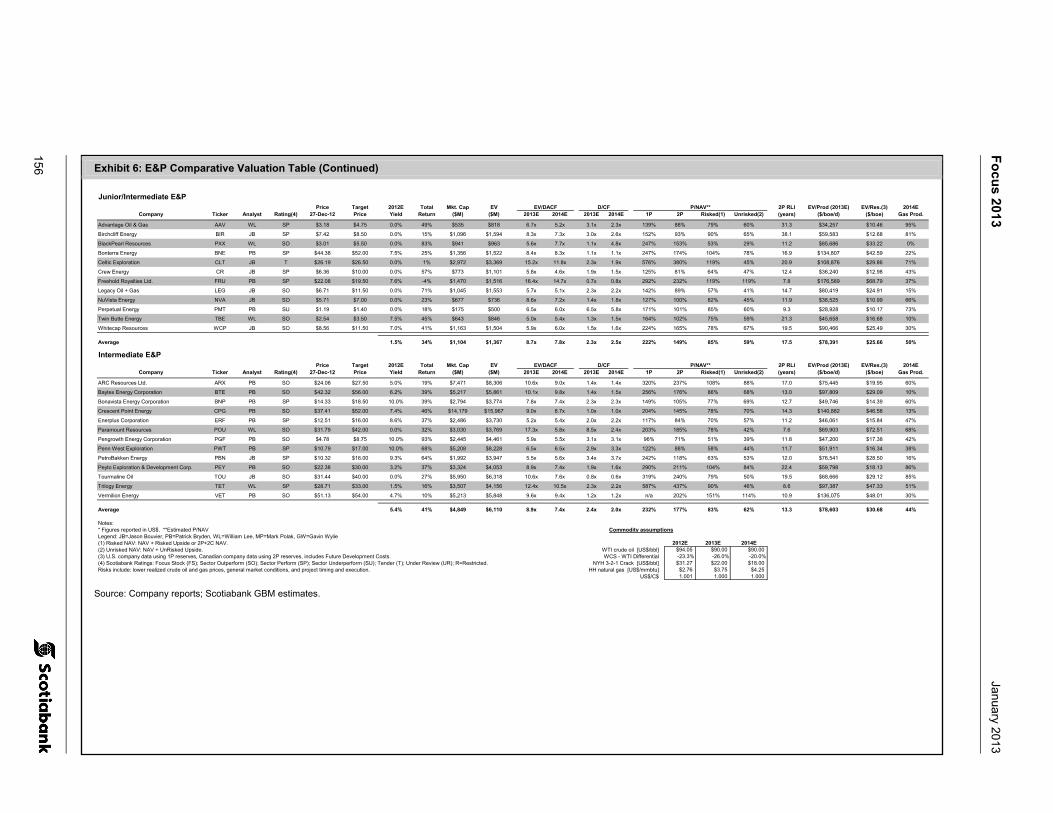

International E&P – Themes for 2013 144

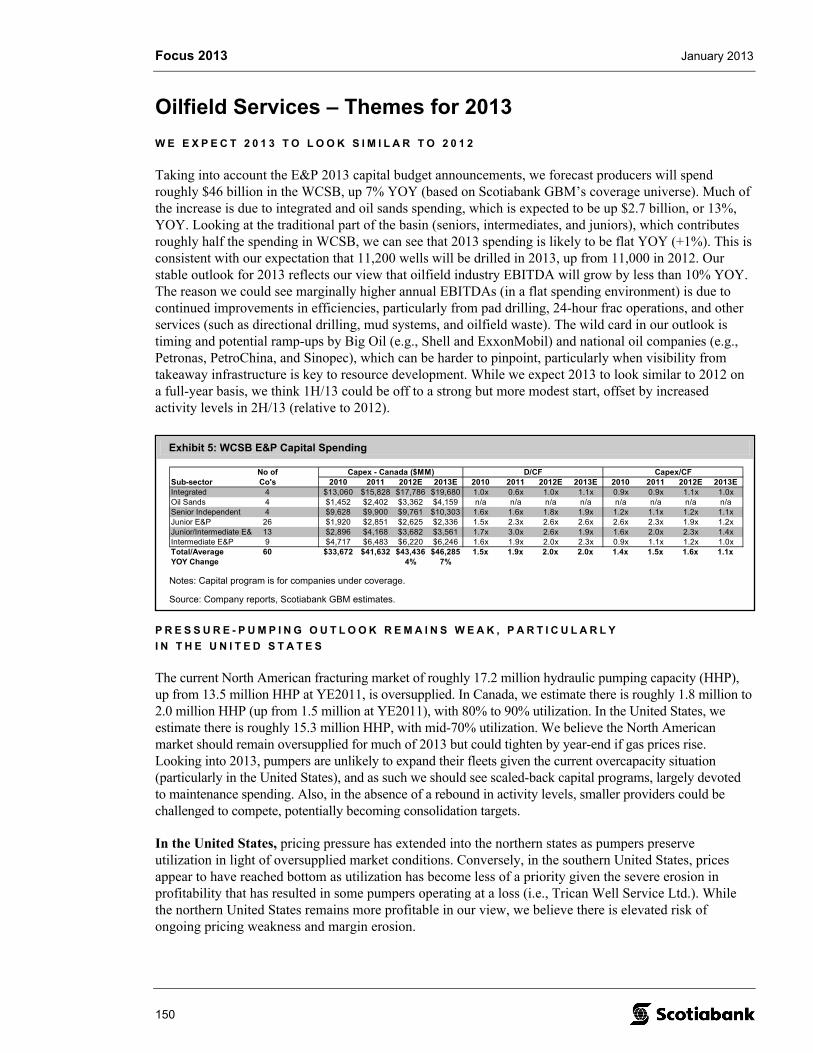

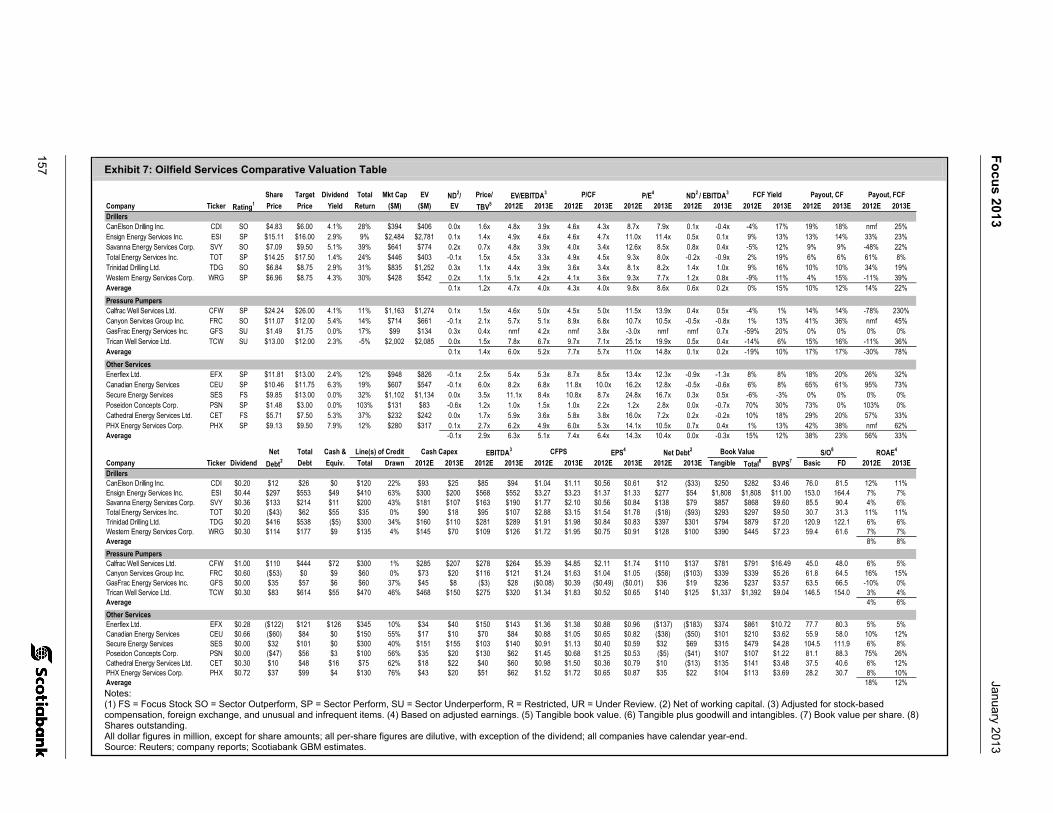

Oilfield Services – Themes for 2013 150

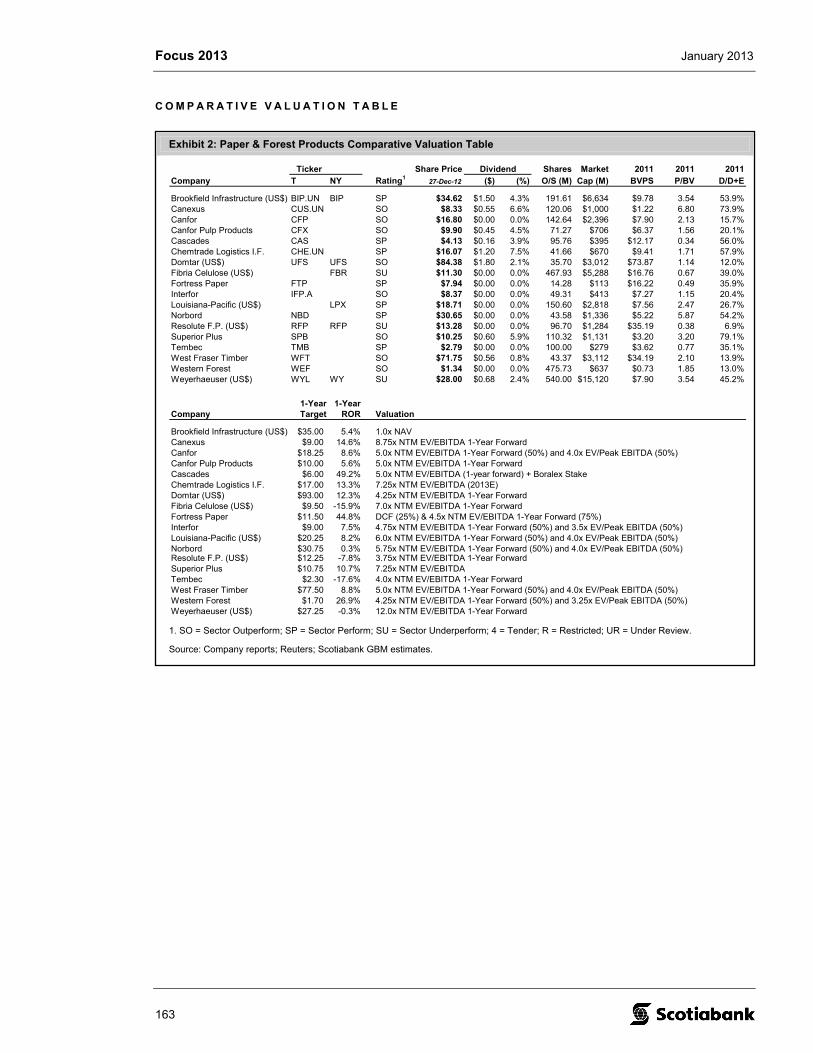

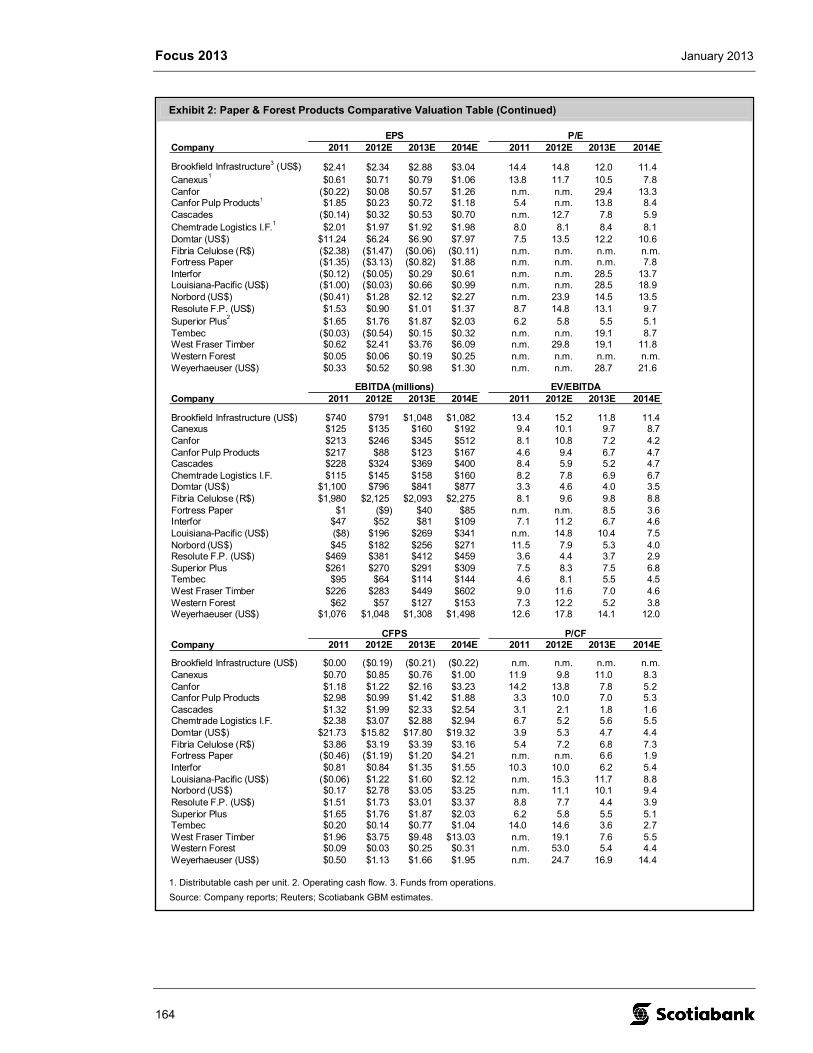

Paper & Forest Products

Run, Forrest, Run! 159

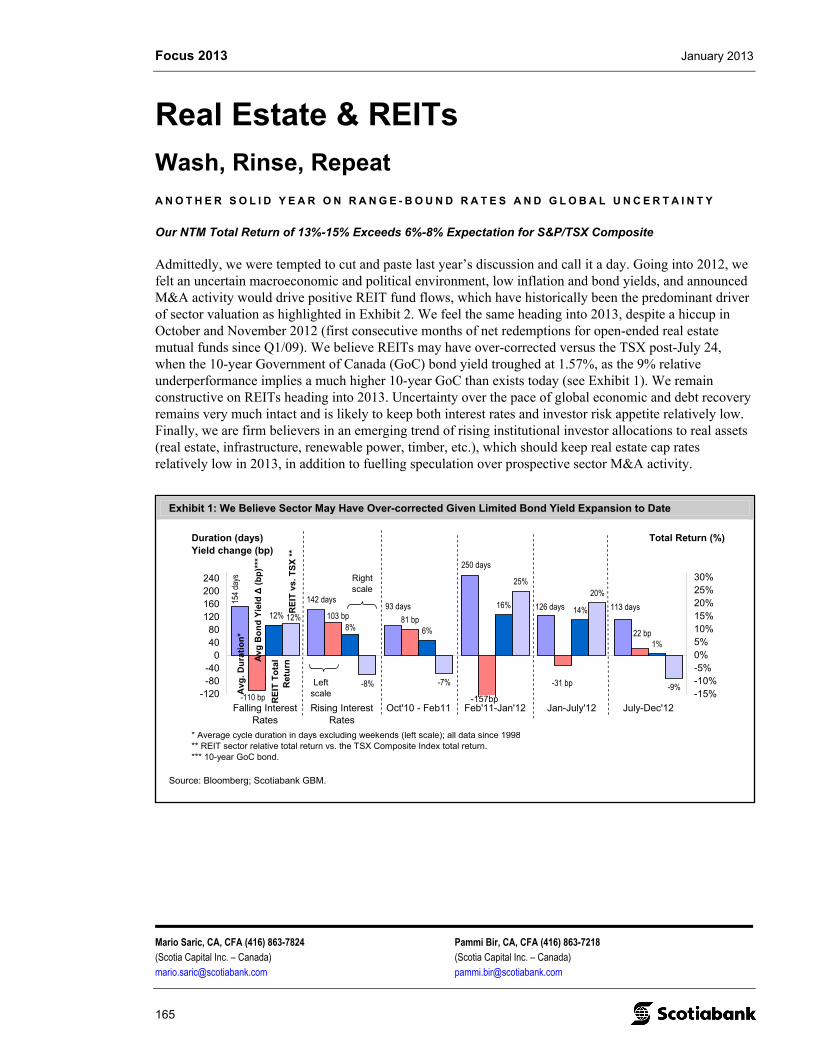

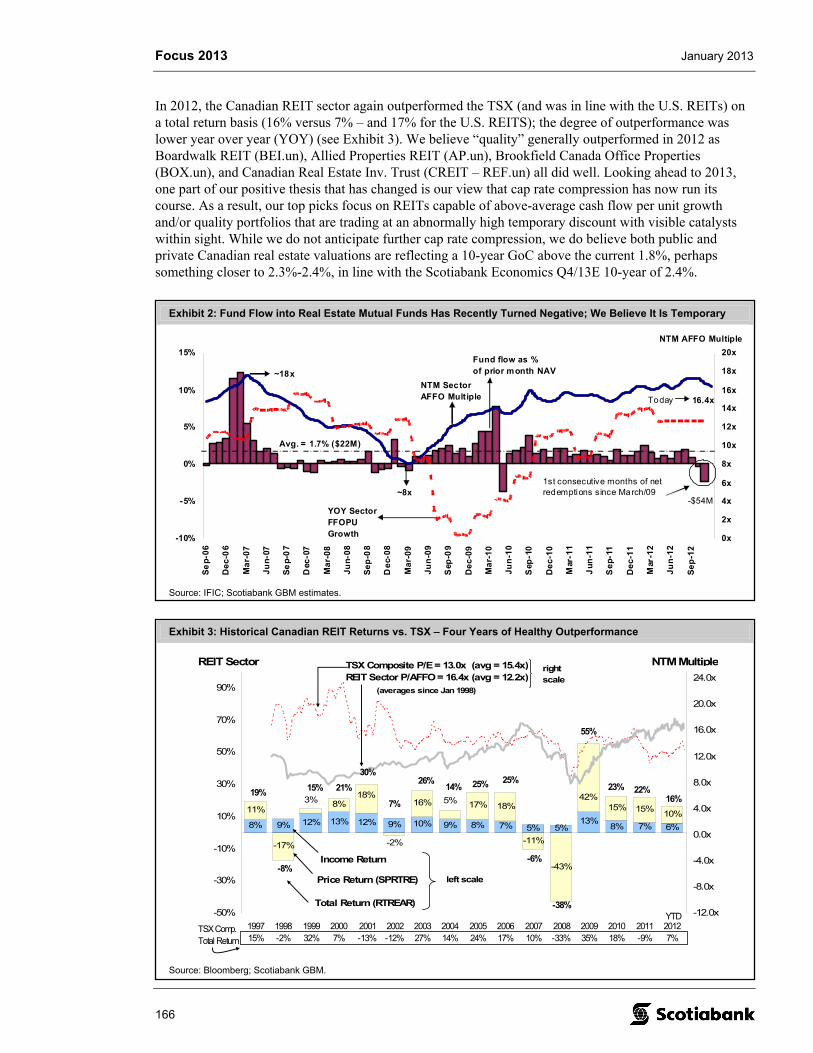

Real Estate & REITs

Wash, Rinse, Repeat 165

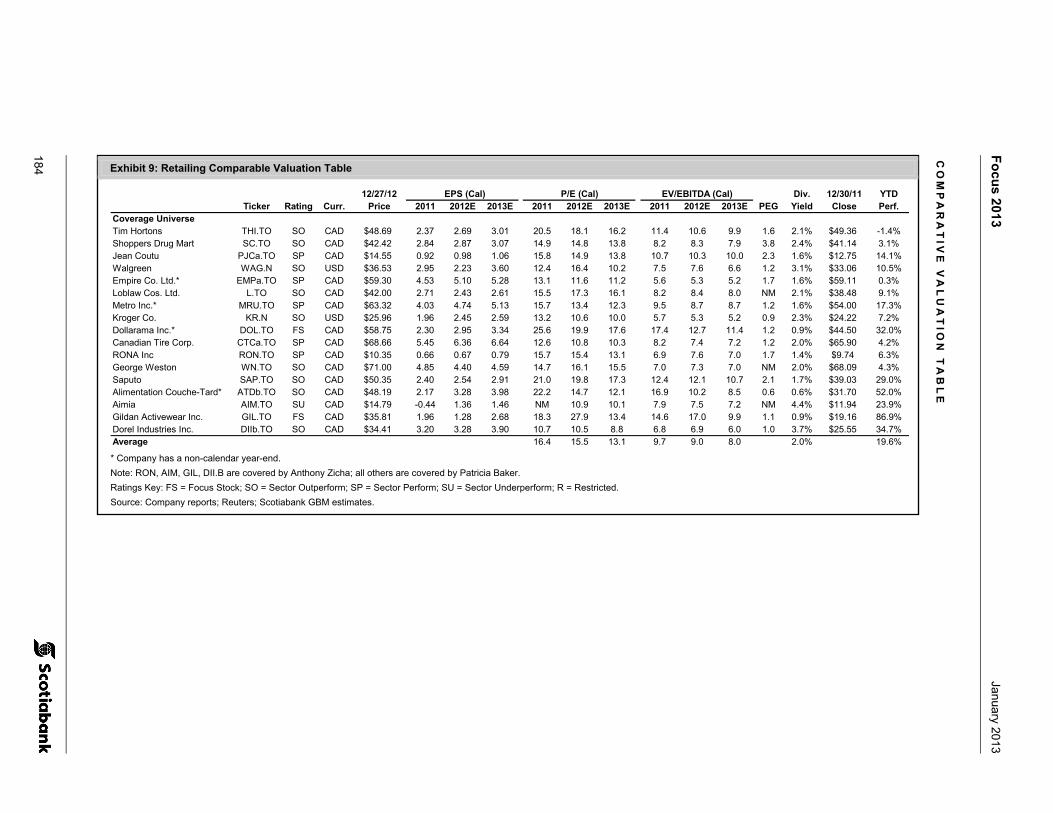

Retailing

Consumer 2013: More of the Same – Constraint 177

Software & IT Services

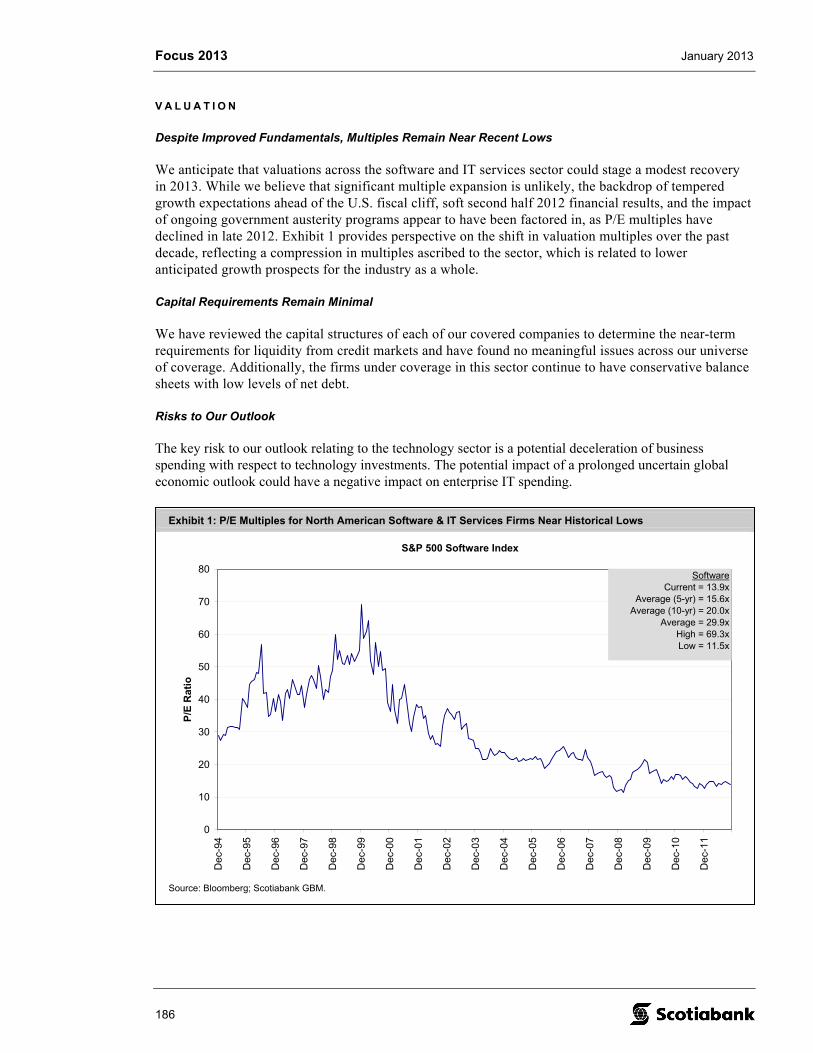

Stabilization of Demand 185

Special Situations: Industrials

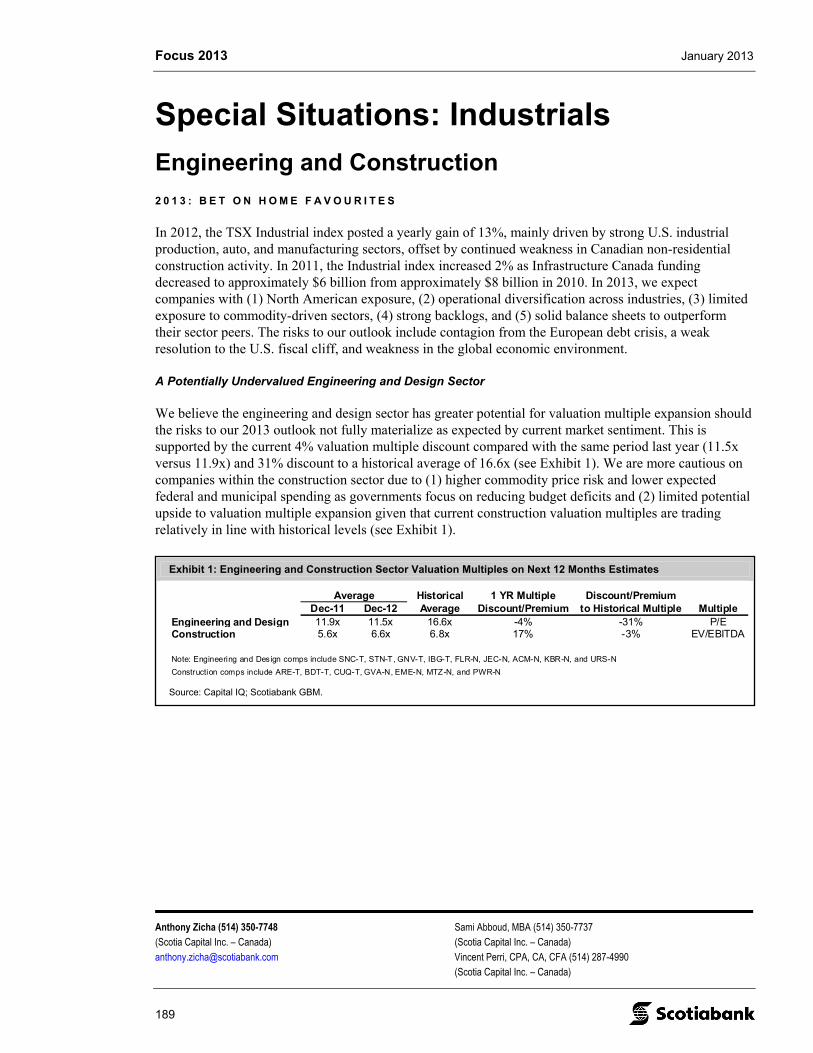

Engineering and Construction 189

Technology Hardware

Act III: The Internet’s Next Phase 193

Telecommunications & Cable

Dividend and Disciplined Allocation of Capital Remain a Key Focus 199

Transportation & Aerospace

Macro Tailwind Desperately Needed 211

Appendix 1 – China Outlook Published by CNC Asset Management Ltd., exclusively distributed by Scotia Capital Inc.

A Year of Recovery i

Publication date January 7, 2013.

Pricing as at December 27, 2012, unless otherwise stated.

Currencies in Canadian dollars unless otherwise stated.

Cover photo credit: www.istockphoto.com/ugurhan

Focus 2013 January 2013

John Henderson, MBA, P.Eng. (416) 945-7393 (Scotia Capital Inc. – Canada) [email protected]

3

Director’s Comment

Bottom Line Trumping Headline

It is my pleasure to introduce Focus 2013, Scotiabank GBM’s annual investment outlook for the coming year. In this report, we highlight industry outlooks, themes, and stock recommendations. We also introduce a new Focus Stock (FS) tier in our rating system to better identify changes in our analysts’ best ideas throughout the year.

This report begins with our portfolio strategy outlook prepared by Vincent Delisle, while Hugo Ste-Marie offers his perspective on implications for small cap strategy. Our general economic outlook is summarized by Derek Holt and Dov Zigler, while Pablo Bréard shares his views specific to Latin America’s economic prospects. Collectively, they outline reasons for near-term bullishness for stock markets and the economy, although perhaps more so in the United States and Latin America than in Canada. Na Liu summarizes expected impacts of developments in China, primarily on commodity markets (shown in Appendix 1). Our analysts present a brief overview of key themes expected to drive performance in their respective sectors, as well as their top stock recommendations for the year.

We caution readers that this report contains highlight commentaries only. Investors are encouraged to contact their Scotiabank salesperson or our analysts for a more complete review of our research views and recommendations. Our published research is available on our website, ScotiaView.

Thank you for your interest in this publication. We wish you a successful year of investing in 2013.

Focus 2013 January 2013

4

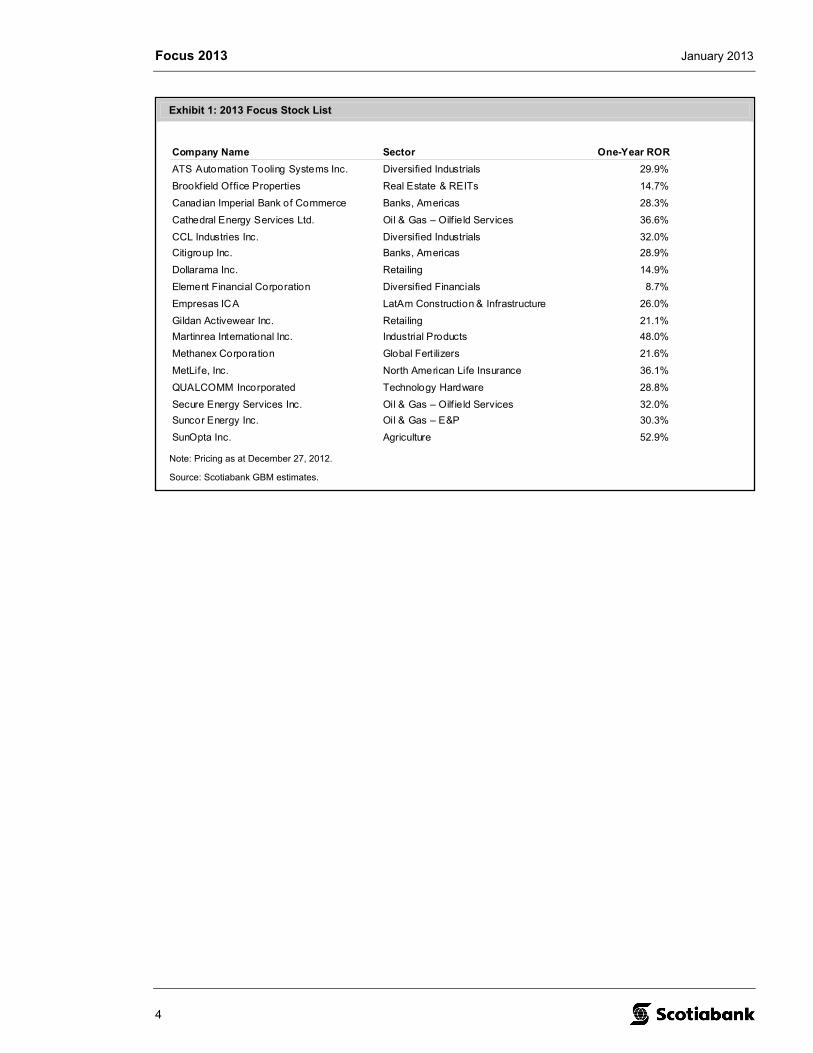

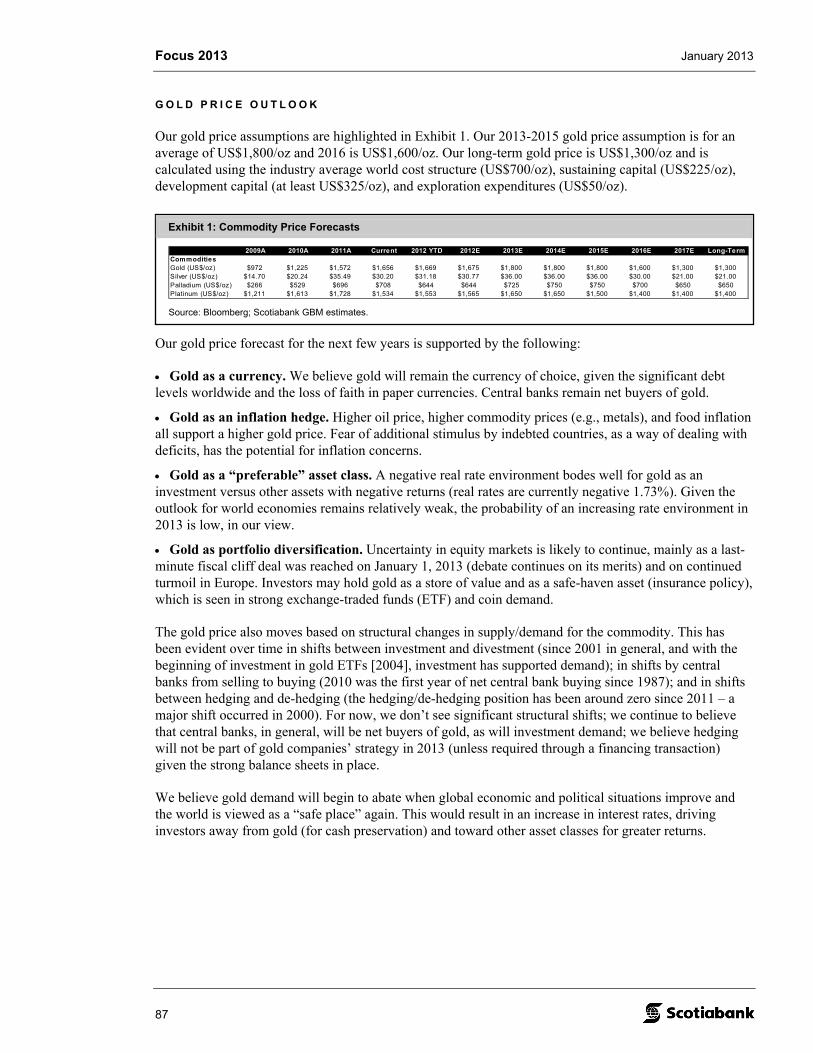

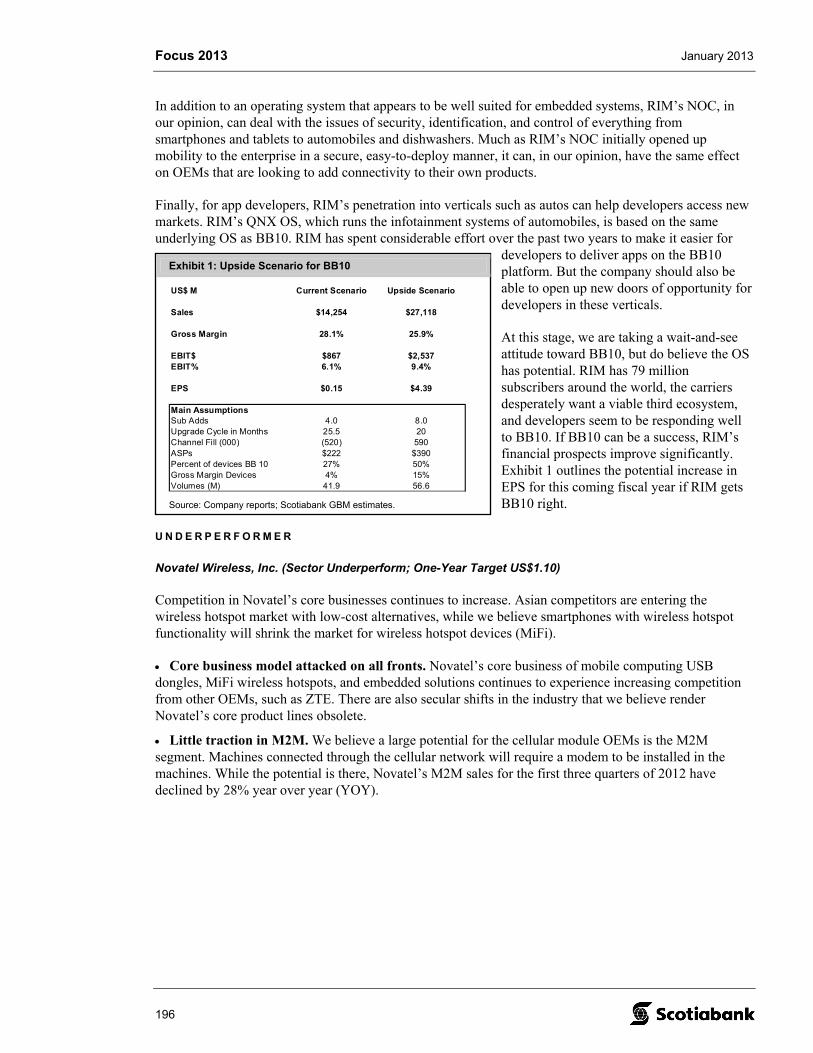

Exhibit 1: 2013 Focus Stock List

Company Name Sector One-Year ROR

ATS Automation Tooling Systems Inc. Diversified Industrials 29.9%

Brookfield Office Properties Real Estate & REITs 14.7%

Canadian Imperial Bank of Commerce Banks, Americas 28.3%

Cathedral Energy Services Ltd. Oil & Gas – Oilf ield Services 36.6%

CCL Industries Inc. Diversified Industrials 32.0%

Citigroup Inc. Banks, Americas 28.9%

Dollarama Inc. Retailing 14.9%

Element Financial Corporation Diversified Financials 8.7%

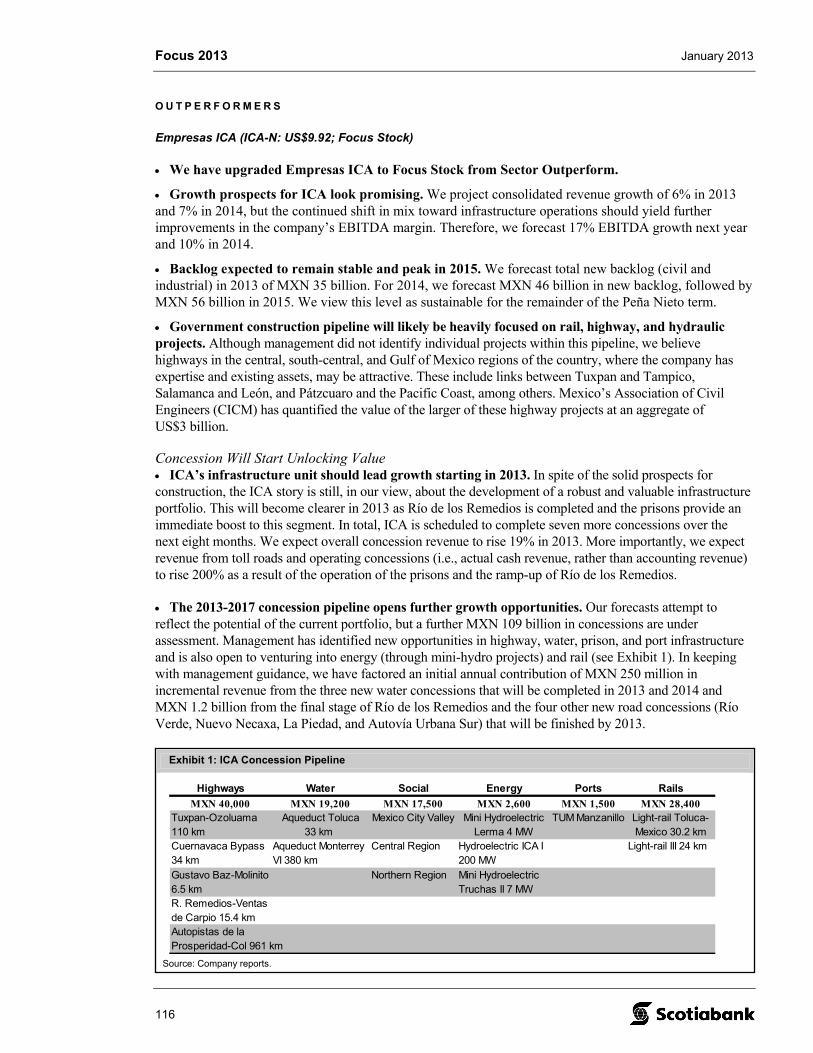

Empresas ICA LatAm Construction & Infrastructure 26.0%

Gildan Activewear Inc. Retailing 21.1%

Martinrea International Inc. Industrial Products 48.0%

Methanex Corporation Global Fert ilizers 21.6%

MetLife, Inc. North American Life Insurance 36.1%

QUALCOMM Incorporated Technology Hardware 28.8%

Secure Energy Services Inc. Oil & Gas – Oilf ield Services 32.0%

Suncor Energy Inc. Oil & Gas – E&P 30.3%

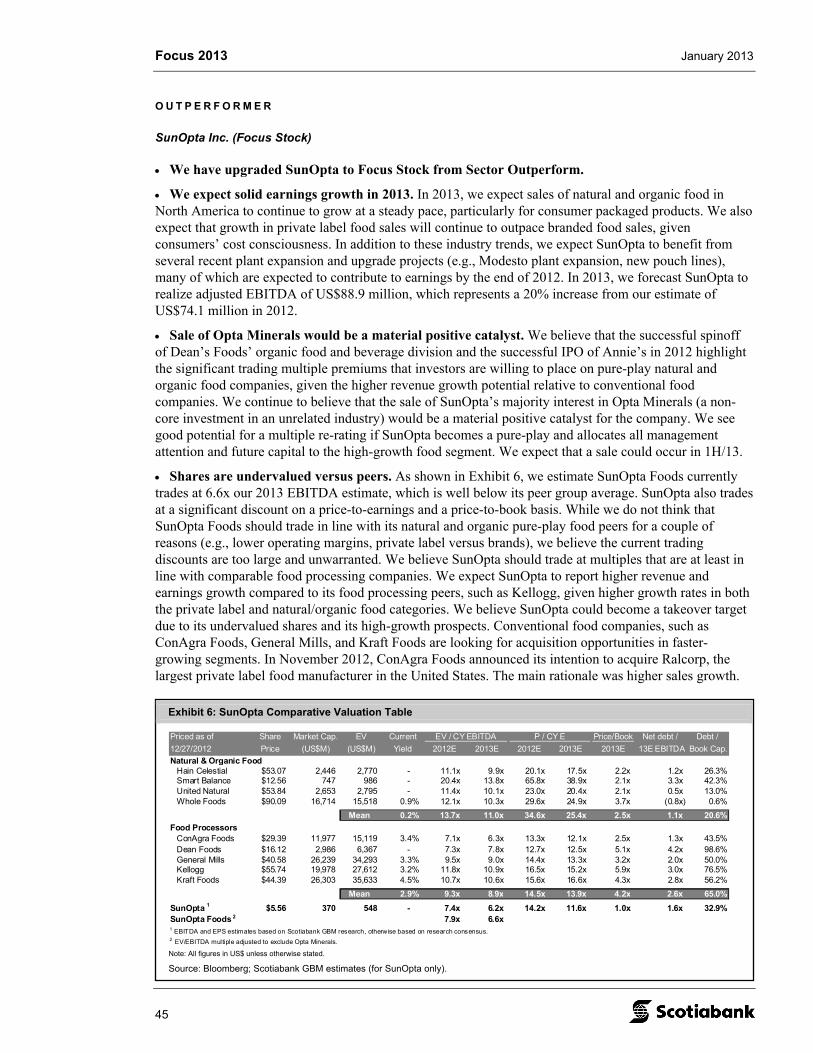

SunOpta Inc. Agriculture 52.9%

Note: Pricing as at December 27, 2012.

Source: Scotiabank GBM estimates.

Focus 2013 January 2013

Vincent Delisle, CFA (514) 287-3628 Jean-Michel Gauthier, MMF (514) 287-3661 (Scotia Capital Inc. – Canada) (Scotia Capital Inc. – Canada) [email protected] [email protected]

5

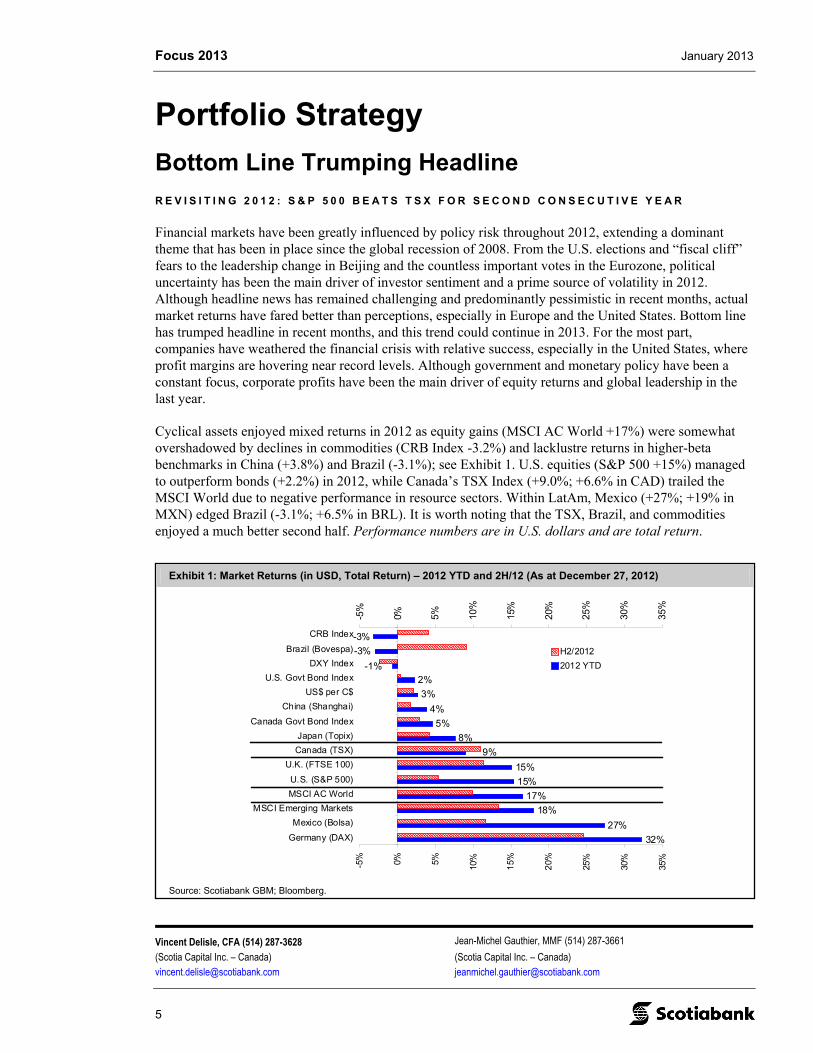

Exhibit 1: Market Returns (in USD, Total Return) – 2012 YTD and 2H/12 (As at December 27, 2012)

32%

27%

18%

17%

15%

15%

8%

5%

4%

3%

2%

-3%

-3%

-1%

9%

-5% 0% 5%

10%

15%

20%

25%

30%

35%

Germany (DAX)

Mexico (Bolsa)

MSCI Emerging Markets

MSCI AC World

U.S. (S&P 500)

U.K. (FTSE 100)

Canada (TSX)

Japan (Topix)

Canada Govt Bond Index

China (Shanghai)

US$ per C$

U.S. Govt Bond Index

DXY Index

Brazil (Bovespa)

CRB Index

-5%

0% 5% 10%

15%

20%

25%

30%

35%

H2/2012

2012 YTD

Source: Scotiabank GBM; Bloomberg.

Portfolio Strategy

Bottom Line Trumping Headline

R E V I S I T I N G 2 0 1 2 : S & P 5 0 0 B E A T S T S X F O R S E C O N D C O N S E C U T I V E Y E A R

Financial markets have been greatly influenced by policy risk throughout 2012, extending a dominant theme that has been in place since the global recession of 2008. From the U.S. elections and “fiscal cliff” fears to the leadership change in Beijing and the countless important votes in the Eurozone, political uncertainty has been the main driver of investor sentiment and a prime source of volatility in 2012. Although headline news has remained challenging and predominantly pessimistic in recent months, actual market returns have fared better than perceptions, especially in Europe and the United States. Bottom line has trumped headline in recent months, and this trend could continue in 2013. For the most part, companies have weathered the financial crisis with relative success, especially in the United States, where profit margins are hovering near record levels. Although government and monetary policy have been a constant focus, corporate profits have been the main driver of equity returns and global leadership in the last year.

Cyclical assets enjoyed mixed returns in 2012 as equity gains (MSCI AC World +17%) were somewhat overshadowed by declines in commodities (CRB Index -3.2%) and lacklustre returns in higher-beta benchmarks in China (+3.8%) and Brazil (-3.1%); see Exhibit 1. U.S. equities (S&P 500 +15%) managed to outperform bonds (+2.2%) in 2012, while Canada’s TSX Index (+9.0%; +6.6% in CAD) trailed the MSCI World due to negative performance in resource sectors. Within LatAm, Mexico (+27%; +19% in MXN) edged Brazil (-3.1%; +6.5% in BRL). It is worth noting that the TSX, Brazil, and commodities enjoyed a much better second half. Performance numbers are in U.S. dollars and are total return.

Focus 2013 January 2013

6

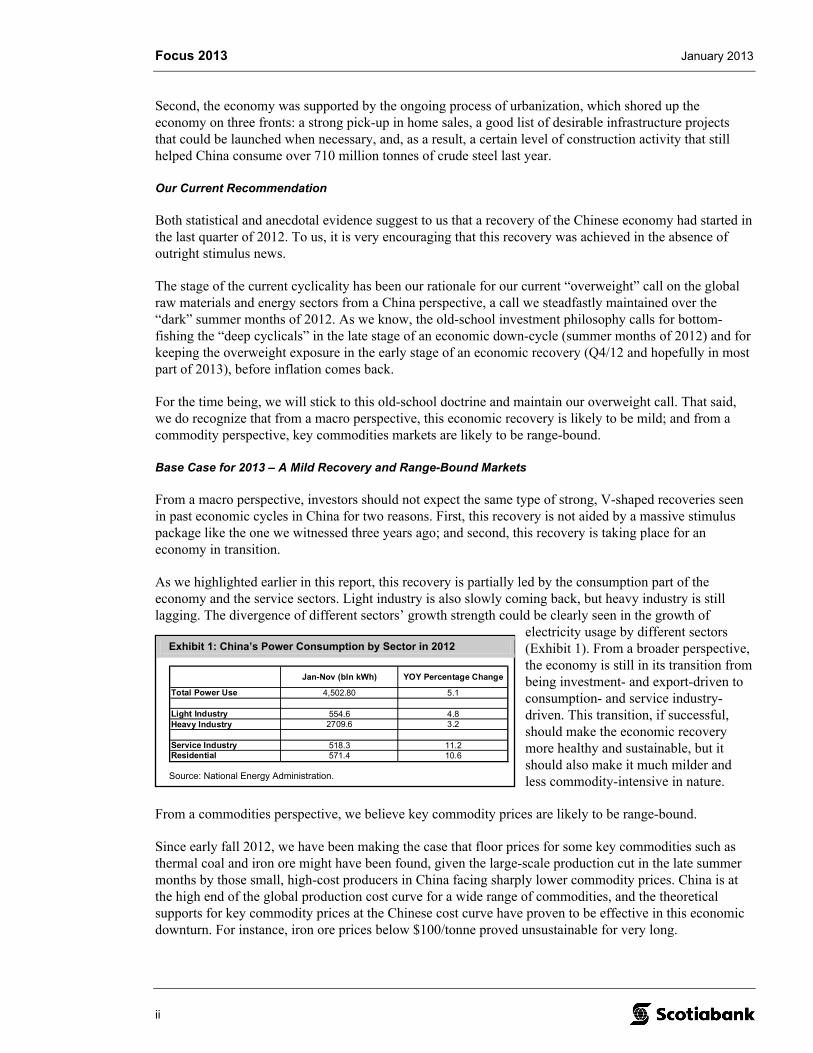

Exhibit 2: Real GDP Growth YOY (%) – Developed vs. Emerging Countries

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

World U.S. Canada Eurozone Japan Brazil China India Mexico

2013 IMF Forecast

2012 IMF Forecast

2011

2004-2010 Average

Source: Scotiabank GBM; IMF.

Exhibit 3: Change in Forward EPS Estimates – Normalized at 100 on January 2012

90

92

94

96

98

100

102

104

106

Jan

-12

Fe

b-1

2

Ma

r-1

2

Ap

r-1

2

Ma

y-1

2

Jun

-12

Ju

l-12

Au

g-1

2

Se

p-12

Oct

-12

No

v-12

De

c-1

2

Jan

-13

90

92

94

96

98

100

102

104

106

TSX

MSCI Germany

MSCI China

MSCI Brazil

MSCI Mexico

S&P 500

Source: Scotiabank GBM; Thomson Financial.

As shown in Exhibit 1, global equity leadership was concentrated in developed markets throughout 2012, but some key emerging market benchmarks suffered. Slower-than-expected GDP growth in developing countries, along with diverging earnings trends, are at the root of 2012 global equity leadership.

According to the IMF, world GDP growth slowed to 3.3% in 2012 (versus 3.8% in 2011), with the loss of speed coming mainly from China (7.7% versus 9.3% in 2011), Europe (-0.4% versus 1.4%), India (4.9% versus 6.8%), and Brazil (1.5% versus 2.7%). North America fared better, with U.S. GDP momentum improving to 2.2% in 2012 (1.8% in 2011), Mexico pacing at 3.8% (3.9% in 2011), and Canada slipping below 2% (2.4% in 2011). Tepid momentum in emerging markets dealt a blow to earnings estimates of commodity-sensitive benchmarks, and forward (next-12-months) earnings estimates have been cut by 1%-9% in Canada, Brazil, and China. In contrast, forward earnings estimates have increased in Mexico (+0.1%), Germany (+4.0%), and the United States (+5.1%) in the last 12 months, the performance leaders for 2012 (see Exhibit 3).

Focus 2013 January 2013

7

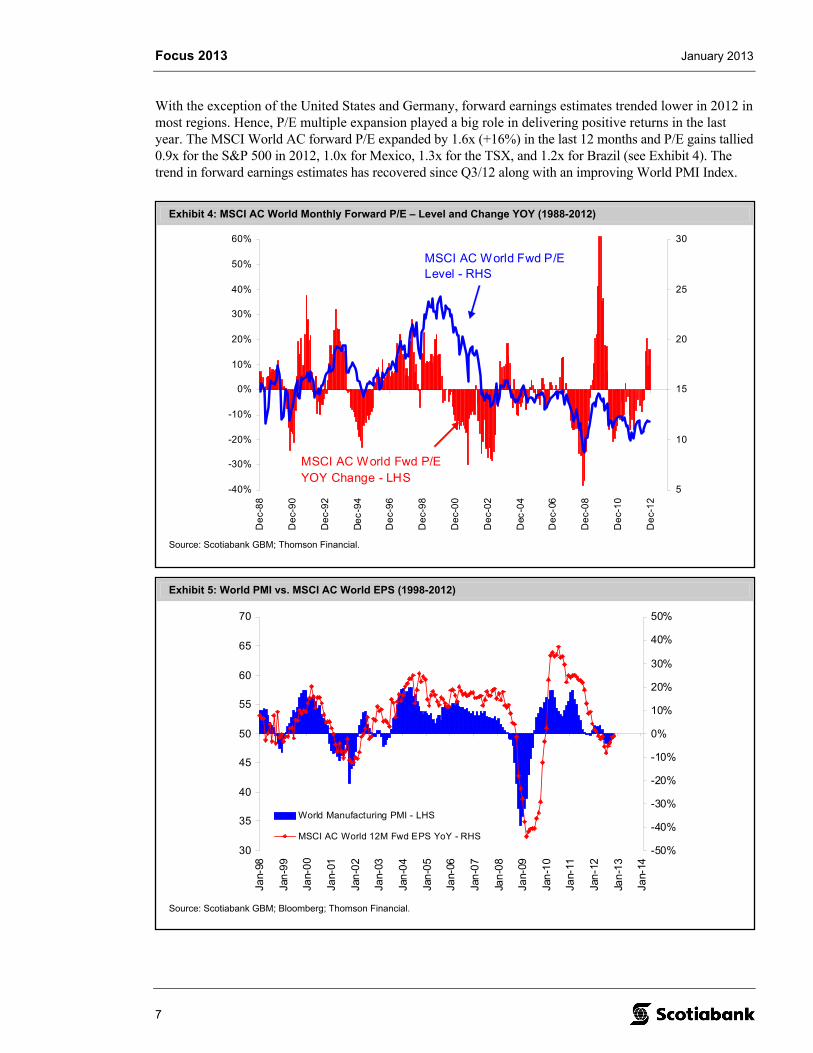

Exhibit 4: MSCI AC World Monthly Forward P/E – Level and Change YOY (1988-2012)

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

De

c-8

8

De

c-9

0

De

c-9

2

De

c-9

4

De

c-9

6

De

c-9

8

De

c-0

0

De

c-0

2

Dec

-04

De

c-06

De

c-0

8

De

c-1

0

De

c-1

2

5

10

15

20

25

30

MSCI AC World Fwd P/E Level - RHS

MSCI AC World Fwd P/E YOY Change - LHS

Source: Scotiabank GBM; Thomson Financial.

Exhibit 5: World PMI vs. MSCI AC World EPS (1998-2012)

30

35

40

45

50

55

60

65

70

Jan-

98

Jan

-99

Jan-

00

Jan-

01

Jan

-02

Jan-

03

Jan

-04

Jan

-05

Jan-

06

Jan

-07

Jan

-08

Jan-

09

Jan

-10

Jan-

11

Jan

-12

Jan

-13

Jan-

14

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

World Manufacturing PMI - LHS

MSCI AC World 12M Fwd EPS YoY - RHS

Source: Scotiabank GBM; Bloomberg; Thomson Financial.

With the exception of the United States and Germany, forward earnings estimates trended lower in 2012 in most regions. Hence, P/E multiple expansion played a big role in delivering positive returns in the last year. The MSCI World AC forward P/E expanded by 1.6x (+16%) in the last 12 months and P/E gains tallied 0.9x for the S&P 500 in 2012, 1.0x for Mexico, 1.3x for the TSX, and 1.2x for Brazil (see Exhibit 4). The trend in forward earnings estimates has recovered since Q3/12 along with an improving World PMI Index.

Focus 2013 January 2013

8

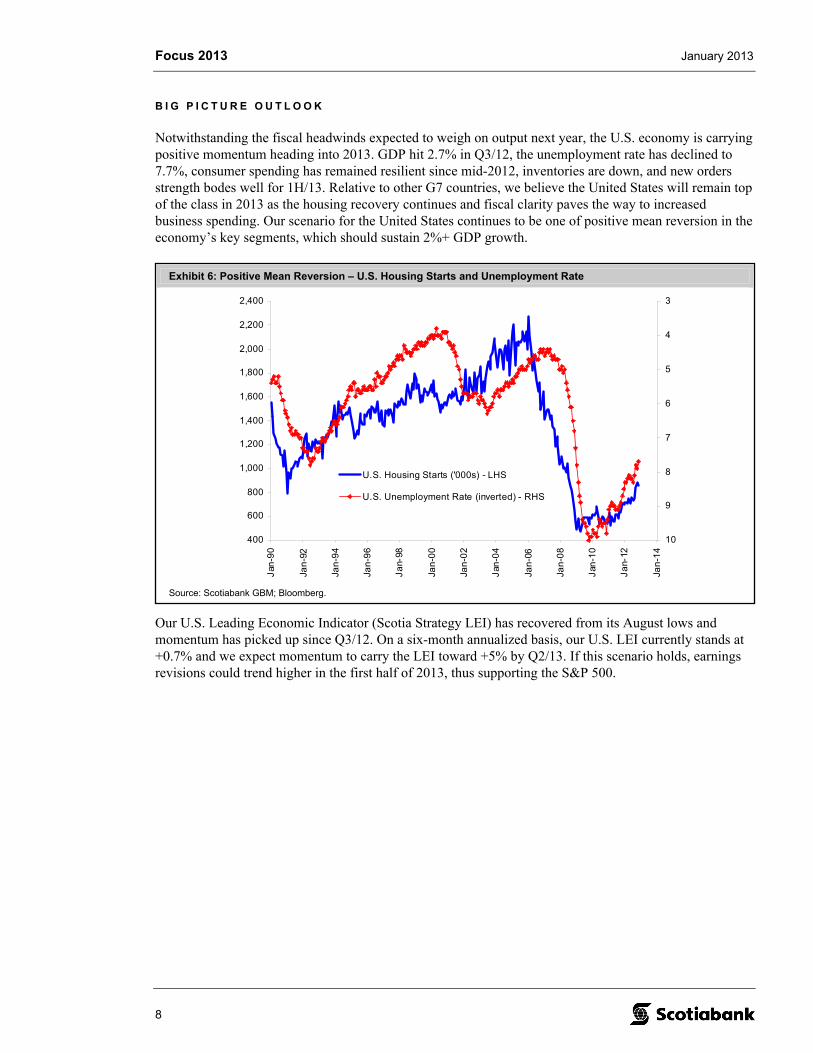

Exhibit 6: Positive Mean Reversion – U.S. Housing Starts and Unemployment Rate

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2,400

Jan

-90

Jan

-92

Jan

-94

Jan

-96

Ja

n-98

Jan

-00

Jan

-02

Jan

-04

Jan

-06

Jan

-08

Jan

-10

Ja

n-12

Jan

-14

3

4

5

6

7

8

9

10

U.S. Housing Starts ('000s) - LHS

U.S. Unemployment Rate (inverted) - RHS

Source: Scotiabank GBM; Bloomberg.

B I G P I C T U R E O U T L O O K

Notwithstanding the fiscal headwinds expected to weigh on output next year, the U.S. economy is carrying positive momentum heading into 2013. GDP hit 2.7% in Q3/12, the unemployment rate has declined to 7.7%, consumer spending has remained resilient since mid-2012, inventories are down, and new orders strength bodes well for 1H/13. Relative to other G7 countries, we believe the United States will remain top of the class in 2013 as the housing recovery continues and fiscal clarity paves the way to increased business spending. Our scenario for the United States continues to be one of positive mean reversion in the economy’s key segments, which should sustain 2%+ GDP growth.

Our U.S. Leading Economic Indicator (Scotia Strategy LEI) has recovered from its August lows and momentum has picked up since Q3/12. On a six-month annualized basis, our U.S. LEI currently stands at +0.7% and we expect momentum to carry the LEI toward +5% by Q2/13. If this scenario holds, earnings revisions could trend higher in the first half of 2013, thus supporting the S&P 500.

Focus 2013 January 2013

9

Exhibit 8: China PMI* and Real GDP Growth (%) – 2004-2012

40

42

44

46

48

50

52

54

56

58

60

Ap

r-0

4

Oct

-04

Apr

-05

Oct

-05

Apr

-06

Oct

-06

Apr

-07

Oct

-07

Apr

-08

Oct

-08

Apr

-09

Oct

-09

Apr

-10

Oct

-10

Apr

-11

Oct

-11

Ap

r-1

2

Oct

-12

Ap

r-1

3

6

7

8

9

10

11

12

13

14

China Manufacturing PMI* - LHS

China Real GDP YoY - RHS

* 50% Official Manufacturing PMI, 50% HSBC Manufacturing PMI.

Source: Scotiabank GBM; Bloomberg.

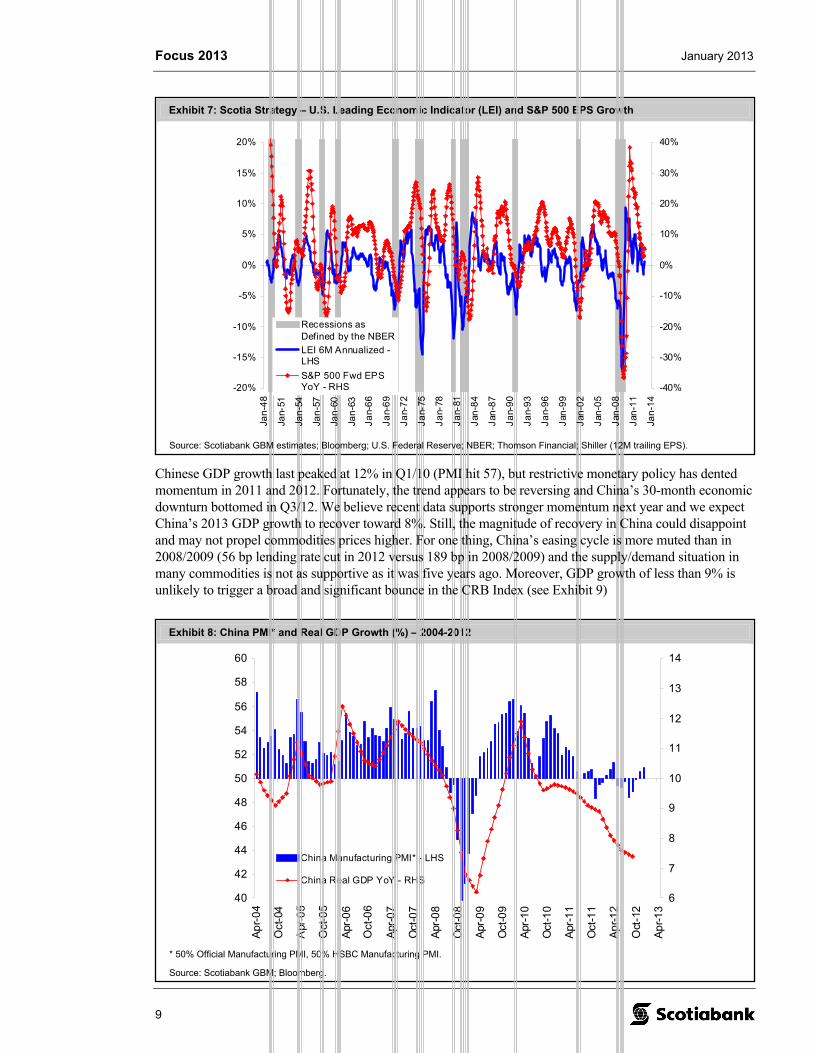

Exhibit 7: Scotia Strategy – U.S. Leading Economic Indicator (LEI) and S&P 500 EPS Growth

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

Jan

-48

Jan-

51

Jan

-54

Jan

-57

Jan

-60

Jan

-63

Ja

n-6

6

Ja

n-6

9

Ja

n-7

2

Ja

n-75

Ja

n-78

Ja

n-81

Jan

-84

Jan

-87

Ja

n-9

0

Ja

n-9

3

Ja

n-9

6

Jan

-99

Jan

-02

Jan

-05

Jan

-08

Jan

-11

Jan

-14

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

Recessions asDefined by the NBER

LEI 6M Annualized -LHS

S&P 500 Fwd EPSYoY - RHS

Source: Scotiabank GBM estimates; Bloomberg; U.S. Federal Reserve; NBER; Thomson Financial; Shiller (12M trailing EPS).

Chinese GDP growth last peaked at 12% in Q1/10 (PMI hit 57), but restrictive monetary policy has dented momentum in 2011 and 2012. Fortunately, the trend appears to be reversing and China’s 30-month economic downturn bottomed in Q3/12. We believe recent data supports stronger momentum next year and we expect China’s 2013 GDP growth to recover toward 8%. Still, the magnitude of recovery in China could disappoint and may not propel commodities prices higher. For one thing, China’s easing cycle is more muted than in 2008/2009 (56 bp lending rate cut in 2012 versus 189 bp in 2008/2009) and the supply/demand situation in many commodities is not as supportive as it was five years ago. Moreover, GDP growth of less than 9% is unlikely to trigger a broad and significant bounce in the CRB Index (see Exhibit 9)

Focus 2013 January 2013

10

Exhibit 9: China GDP and Commodities (2001-2012)

6%

7%

8%

9%

10%

11%

12%

13%

Jan-

01

Jan-

02

Jan

-03

Jan-

04

Jan-

05

Jan

-06

Jan-

07

Jan-

08

Jan

-09

Jan-

10

Jan-

11

Jan

-12

Jan-

13

-60%

-40%

-20%

0%

20%

40%

60%

80%China Real GDP YoY - LHS

CRB Index YoY - RHS

Source: Scotiabank GBM; Bloomberg.

Exhibit 10: China Lending Rate, TSX, and MSCI LatAm (1997-2012)

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

May

-97

May

-98

May

-99

May

-00

May

-01

May

-02

May

-03

May

-04

May

-05

May

-06

May

-07

May

-08

May

-09

May

-10

May

-11

May

-12

May

-13

-100%

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

China Lending Rate YoY - LHS

TSX YoY - RHS

MSCI LatAm YoY - RHS

Source: Scotiabank GBM; Bloomberg.

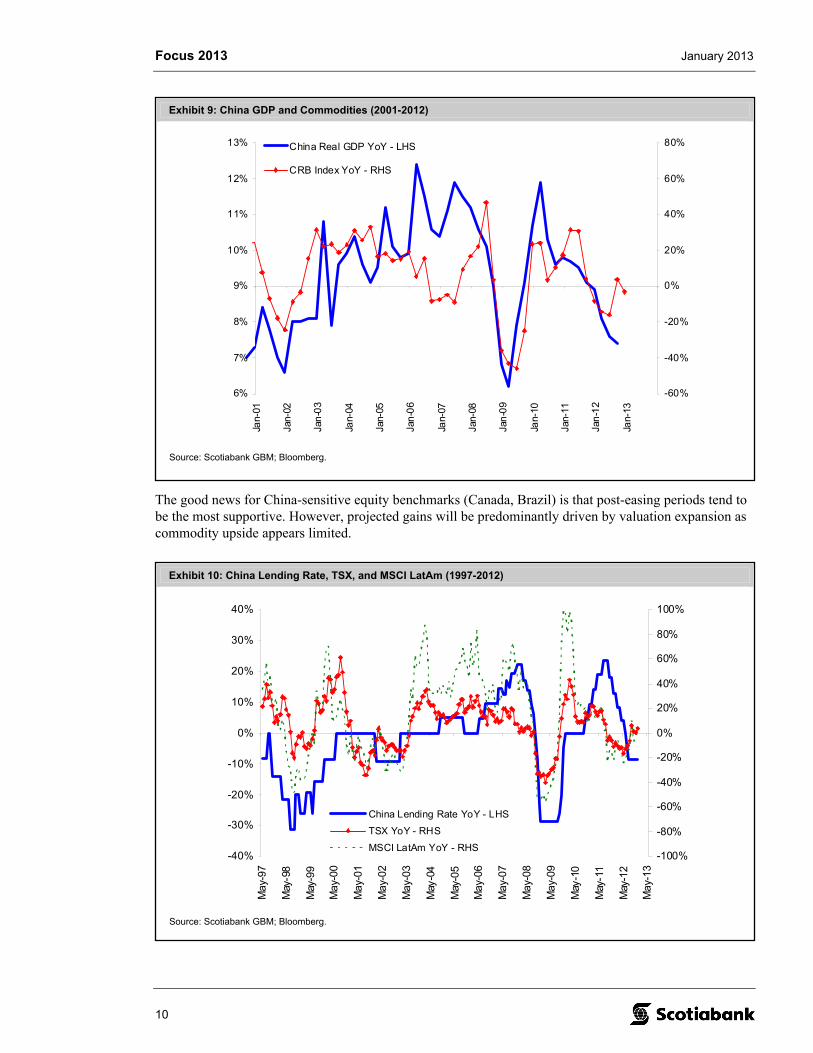

The good news for China-sensitive equity benchmarks (Canada, Brazil) is that post-easing periods tend to be the most supportive. However, projected gains will be predominantly driven by valuation expansion as commodity upside appears limited.

Focus 2013 January 2013

11

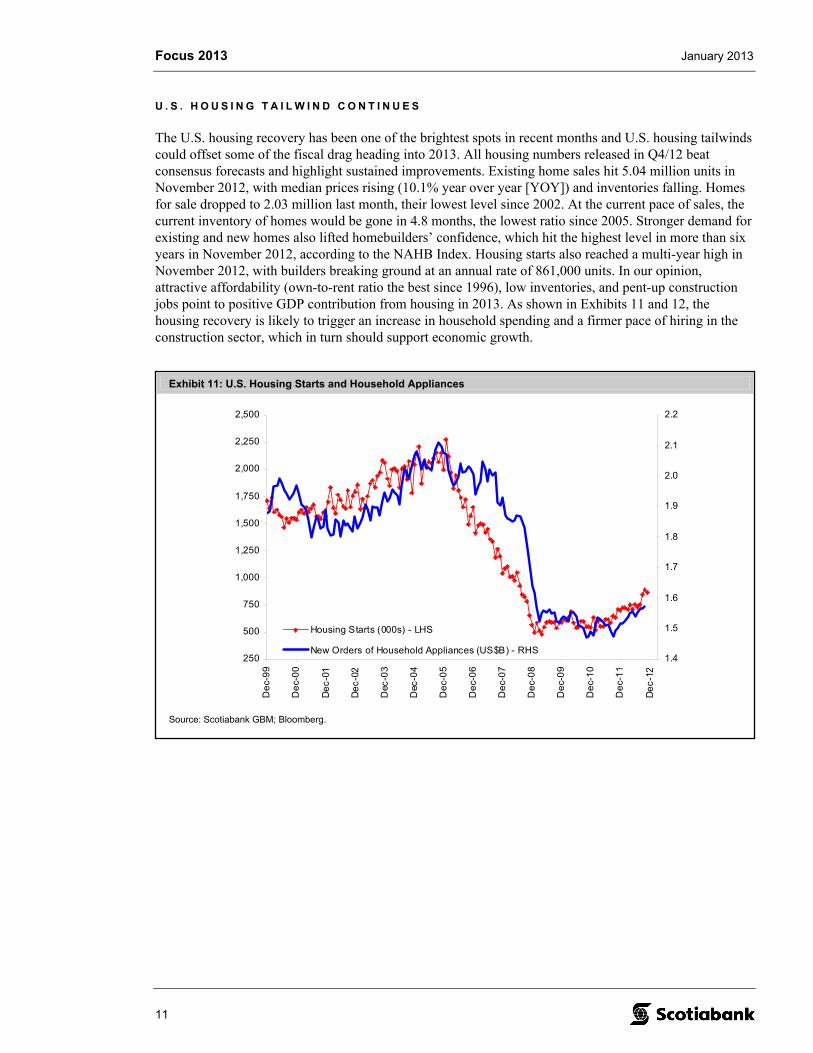

Exhibit 11: U.S. Housing Starts and Household Appliances

250

500

750

1,000

1,250

1,500

1,750

2,000

2,250

2,500

De

c-9

9

De

c-0

0

De

c-0

1

De

c-0

2

Dec

-03

Dec

-04

De

c-0

5

De

c-0

6

De

c-0

7

De

c-0

8

De

c-0

9

De

c-1

0

De

c-1

1

De

c-1

21.4

1.5

1.6

1.7

1.8

1.9

2.0

2.1

2.2

Housing Starts (000s) - LHS

New Orders of Household Appliances (US$B) - RHS

Source: Scotiabank GBM; Bloomberg.

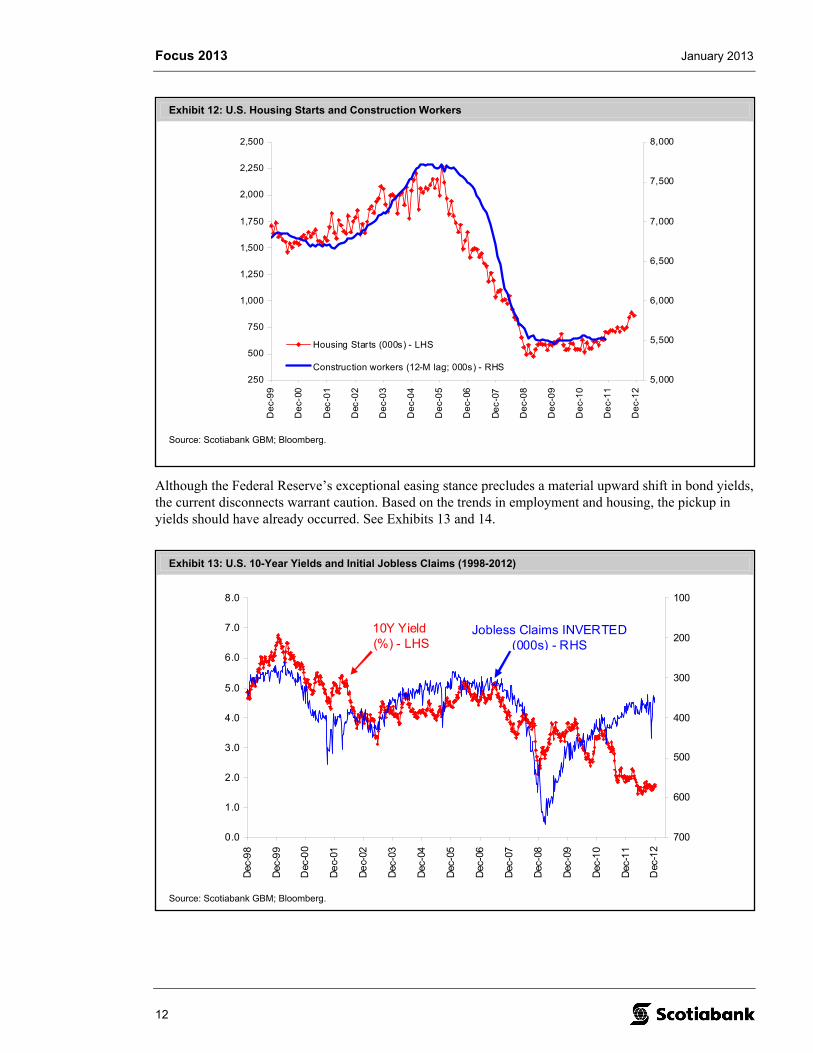

U . S . H O U S I N G T A I L W I N D C O N T I N U E S

The U.S. housing recovery has been one of the brightest spots in recent months and U.S. housing tailwinds could offset some of the fiscal drag heading into 2013. All housing numbers released in Q4/12 beat consensus forecasts and highlight sustained improvements. Existing home sales hit 5.04 million units in November 2012, with median prices rising (10.1% year over year [YOY]) and inventories falling. Homes for sale dropped to 2.03 million last month, their lowest level since 2002. At the current pace of sales, the current inventory of homes would be gone in 4.8 months, the lowest ratio since 2005. Stronger demand for existing and new homes also lifted homebuilders’ confidence, which hit the highest level in more than six years in November 2012, according to the NAHB Index. Housing starts also reached a multi-year high in November 2012, with builders breaking ground at an annual rate of 861,000 units. In our opinion, attractive affordability (own-to-rent ratio the best since 1996), low inventories, and pent-up construction jobs point to positive GDP contribution from housing in 2013. As shown in Exhibits 11 and 12, the housing recovery is likely to trigger an increase in household spending and a firmer pace of hiring in the construction sector, which in turn should support economic growth.

Focus 2013 January 2013

12

Exhibit 12: U.S. Housing Starts and Construction Workers

250

500

750

1,000

1,250

1,500

1,750

2,000

2,250

2,500

De

c-9

9

De

c-00

Dec

-01

Dec

-02

De

c-0

3

De

c-0

4

De

c-0

5

De

c-06

De

c-0

7

De

c-0

8

De

c-0

9

De

c-1

0

De

c-1

1

De

c-1

2

5,000

5,500

6,000

6,500

7,000

7,500

8,000

Housing Starts (000s) - LHS

Construction workers (12-M lag; 000s) - RHS

Source: Scotiabank GBM; Bloomberg.

Exhibit 13: U.S. 10-Year Yields and Initial Jobless Claims (1998-2012)

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

Dec

-98

Dec

-99

Dec

-00

De

c-01

De

c-02

Dec

-03

Dec

-04

Dec

-05

Dec

-06

Dec

-07

Dec

-08

Dec

-09

Dec

-10

Dec

-11

Dec

-12

100

200

300

400

500

600

700

Jobless Claims INVERTED (000s) - RHS

10Y Yield (%) - LHS

Source: Scotiabank GBM; Bloomberg.

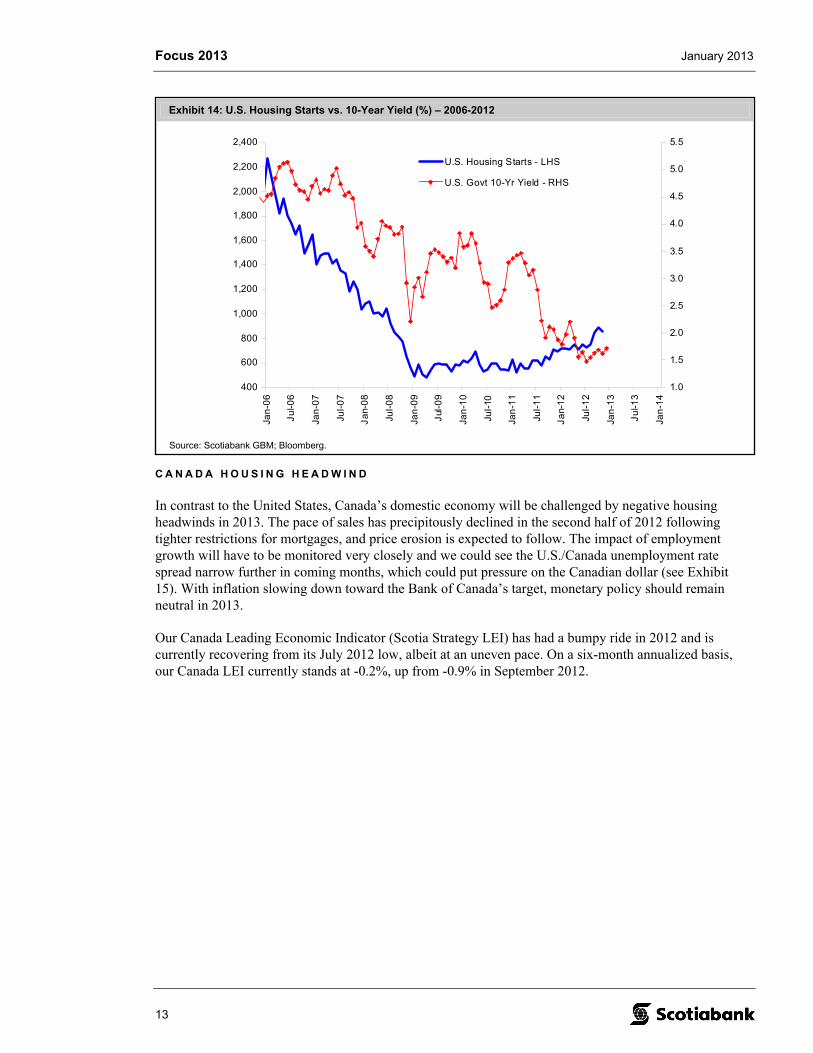

Although the Federal Reserve’s exceptional easing stance precludes a material upward shift in bond yields, the current disconnects warrant caution. Based on the trends in employment and housing, the pickup in yields should have already occurred. See Exhibits 13 and 14.

Focus 2013 January 2013

13

Exhibit 14: U.S. Housing Starts vs. 10-Year Yield (%) – 2006-2012

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2,400

Jan

-06

Ju

l-06

Jan

-07

Jul-

07

Ja

n-0

8

Jul-

08

Jan

-09

Jul

-09

Jan

-10

Jul-

10

Jan

-11

Jul-

11

Ja

n-1

2

Jul-

12

Jan

-13

Ju

l-13

Jan

-14

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

U.S. Housing Starts - LHS

U.S. Govt 10-Yr Yield - RHS

Source: Scotiabank GBM; Bloomberg.

C A N A D A H O U S I N G H E A D W I N D

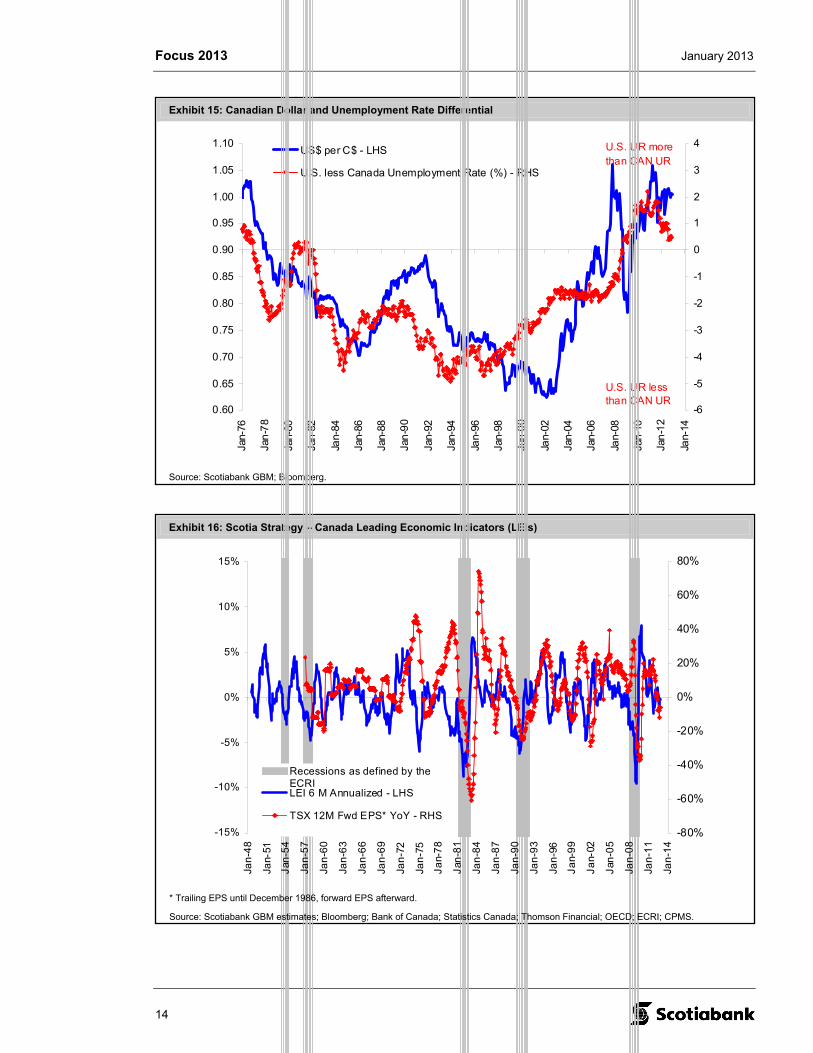

In contrast to the United States, Canada’s domestic economy will be challenged by negative housing headwinds in 2013. The pace of sales has precipitously declined in the second half of 2012 following tighter restrictions for mortgages, and price erosion is expected to follow. The impact of employment growth will have to be monitored very closely and we could see the U.S./Canada unemployment rate spread narrow further in coming months, which could put pressure on the Canadian dollar (see Exhibit 15). With inflation slowing down toward the Bank of Canada’s target, monetary policy should remain neutral in 2013.

Our Canada Leading Economic Indicator (Scotia Strategy LEI) has had a bumpy ride in 2012 and is currently recovering from its July 2012 low, albeit at an uneven pace. On a six-month annualized basis, our Canada LEI currently stands at -0.2%, up from -0.9% in September 2012.

Focus 2013 January 2013

14

Exhibit 15: Canadian Dollar and Unemployment Rate Differential

0.60

0.65

0.70

0.75

0.80

0.85

0.90

0.95

1.00

1.05

1.10

Jan-

76

Jan

-78

Jan-

80

Jan-

82

Jan-

84

Jan-

86

Jan-

88

Jan

-90

Jan-

92

Jan-

94

Jan-

96

Jan-

98

Jan

-00

Jan-

02

Jan-

04

Jan-

06

Jan-

08

Jan-

10

Jan

-12

Jan-

14

-6

-5

-4

-3

-2

-1

0

1

2

3

4US$ per C$ - LHS

U.S. less Canada Unemployment Rate (%) - RHS

U.S. UR less than CAN UR

U.S. UR more than CAN UR

Source: Scotiabank GBM; Bloomberg.

Exhibit 16: Scotia Strategy – Canada Leading Economic Indicators (LEIs)

-15%

-10%

-5%

0%

5%

10%

15%

Jan

-48

Jan-

51

Jan

-54

Jan

-57

Jan

-60

Jan

-63

Jan

-66

Jan

-69

Jan

-72

Jan

-75

Ja

n-7

8

Jan

-81

Jan

-84

Jan

-87

Jan

-90

Jan

-93

Jan

-96

Ja

n-9

9

Ja

n-02

Jan

-05

Jan

-08

Jan

-11

Jan

-14

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

Recessions as defined by theECRILEI 6 M Annualized - LHS

TSX 12M Fwd EPS* YoY - RHS

* Trailing EPS until December 1986, forward EPS afterward.

Source: Scotiabank GBM estimates; Bloomberg; Bank of Canada; Statistics Canada; Thomson Financial; OECD; ECRI; CPMS.

Focus 2013 January 2013

15

Exhibit 17: Corporate America – Cash Hoard Is High and Capex Low

4%

6%

8%

10%

12%

14%

16%

De

c-5

1

Dec

-54

Dec

-57

Dec

-60

De

c-63

De

c-66

De

c-6

9

De

c-7

2

De

c-7

5

De

c-7

8

De

c-8

1

Dec

-84

Dec

-87

De

c-9

0

De

c-9

3

De

c-96

De

c-9

9

De

c-0

2

De

c-0

5

De

c-0

8

De

c-1

1

Liquid Assets as % of GDP

Capex as % of GDP

* Based on U.S. non-financial corporate business data.

Source: Scotiabank GBM; Bloomberg.

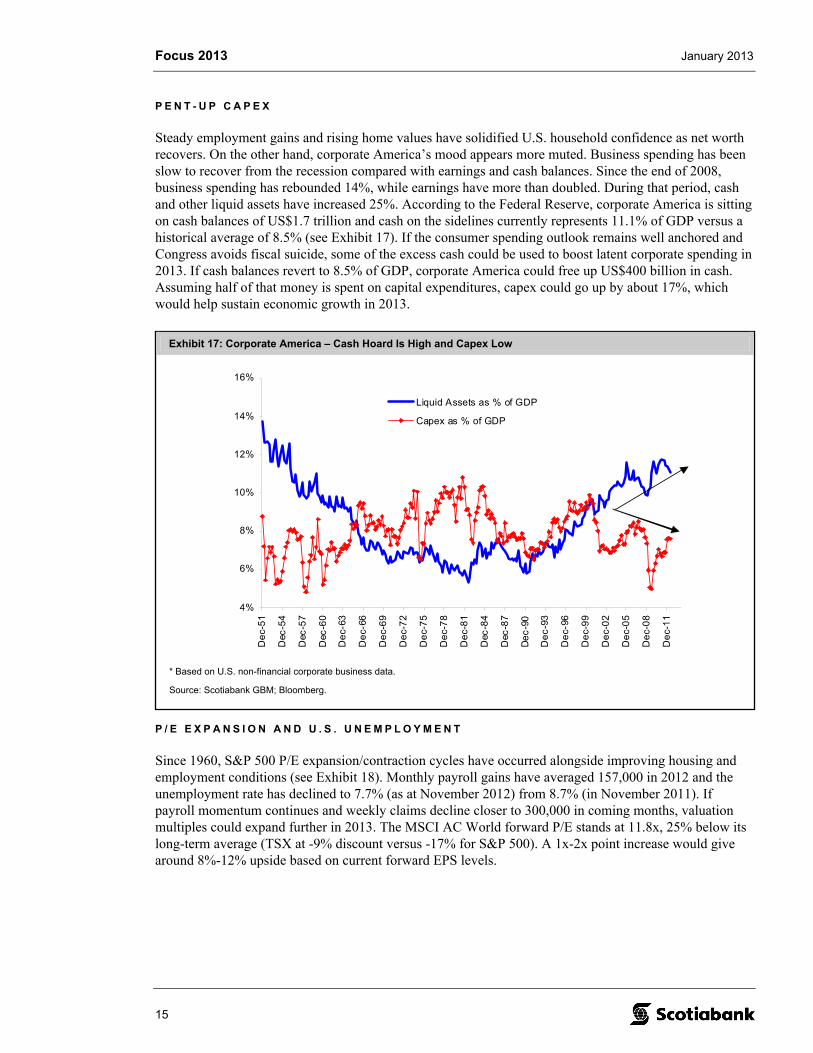

P E N T - U P C A P E X

Steady employment gains and rising home values have solidified U.S. household confidence as net worth recovers. On the other hand, corporate America’s mood appears more muted. Business spending has been slow to recover from the recession compared with earnings and cash balances. Since the end of 2008, business spending has rebounded 14%, while earnings have more than doubled. During that period, cash and other liquid assets have increased 25%. According to the Federal Reserve, corporate America is sitting on cash balances of US$1.7 trillion and cash on the sidelines currently represents 11.1% of GDP versus a historical average of 8.5% (see Exhibit 17). If the consumer spending outlook remains well anchored and Congress avoids fiscal suicide, some of the excess cash could be used to boost latent corporate spending in 2013. If cash balances revert to 8.5% of GDP, corporate America could free up US$400 billion in cash. Assuming half of that money is spent on capital expenditures, capex could go up by about 17%, which would help sustain economic growth in 2013.

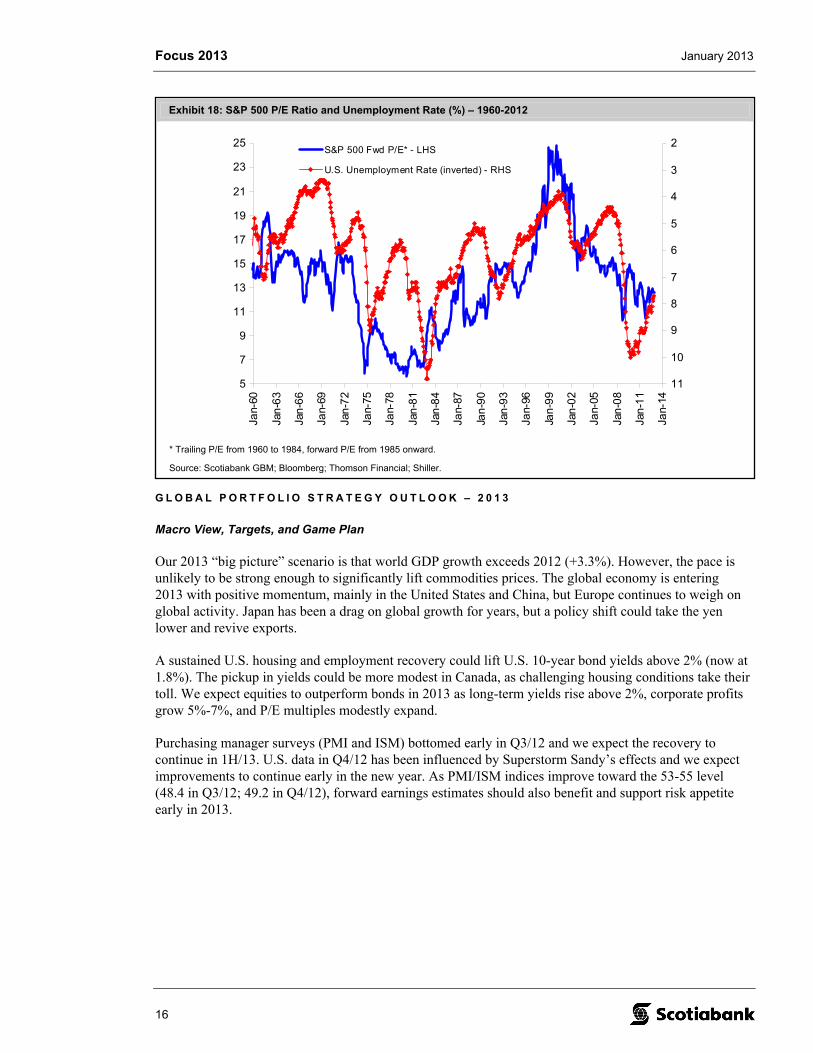

P / E E X P A N S I O N A N D U . S . U N E M P L O Y M E N T

Since 1960, S&P 500 P/E expansion/contraction cycles have occurred alongside improving housing and employment conditions (see Exhibit 18). Monthly payroll gains have averaged 157,000 in 2012 and the unemployment rate has declined to 7.7% (as at November 2012) from 8.7% (in November 2011). If payroll momentum continues and weekly claims decline closer to 300,000 in coming months, valuation multiples could expand further in 2013. The MSCI AC World forward P/E stands at 11.8x, 25% below its long-term average (TSX at -9% discount versus -17% for S&P 500). A 1x-2x point increase would give around 8%-12% upside based on current forward EPS levels.

Focus 2013 January 2013

16

Exhibit 18: S&P 500 P/E Ratio and Unemployment Rate (%) – 1960-2012

5

7

9

11

13

15

17

19

21

23

25

Jan-

60

Jan

-63

Jan

-66

Jan-

69

Jan

-72

Jan-

75

Jan-

78

Jan

-81

Jan

-84

Jan-

87

Jan

-90

Jan

-93

Jan-

96

Jan

-99

Jan

-02

Jan-

05

Jan

-08

Jan

-11

Jan-

14

2

3

4

5

6

7

8

9

10

11

S&P 500 Fwd P/E* - LHS

U.S. Unemployment Rate (inverted) - RHS

* Trailing P/E from 1960 to 1984, forward P/E from 1985 onward.

Source: Scotiabank GBM; Bloomberg; Thomson Financial; Shiller.

G L O B A L P O R T F O L I O S T R A T E G Y O U T L O O K – 2 0 1 3

Macro View, Targets, and Game Plan

Our 2013 “big picture” scenario is that world GDP growth exceeds 2012 (+3.3%). However, the pace is unlikely to be strong enough to significantly lift commodities prices. The global economy is entering 2013 with positive momentum, mainly in the United States and China, but Europe continues to weigh on global activity. Japan has been a drag on global growth for years, but a policy shift could take the yen lower and revive exports.

A sustained U.S. housing and employment recovery could lift U.S. 10-year bond yields above 2% (now at 1.8%). The pickup in yields could be more modest in Canada, as challenging housing conditions take their toll. We expect equities to outperform bonds in 2013 as long-term yields rise above 2%, corporate profits grow 5%-7%, and P/E multiples modestly expand.

Purchasing manager surveys (PMI and ISM) bottomed early in Q3/12 and we expect the recovery to continue in 1H/13. U.S. data in Q4/12 has been influenced by Superstorm Sandy’s effects and we expect improvements to continue early in the new year. As PMI/ISM indices improve toward the 53-55 level (48.4 in Q3/12; 49.2 in Q4/12), forward earnings estimates should also benefit and support risk appetite early in 2013.

Focus 2013 January 2013

17

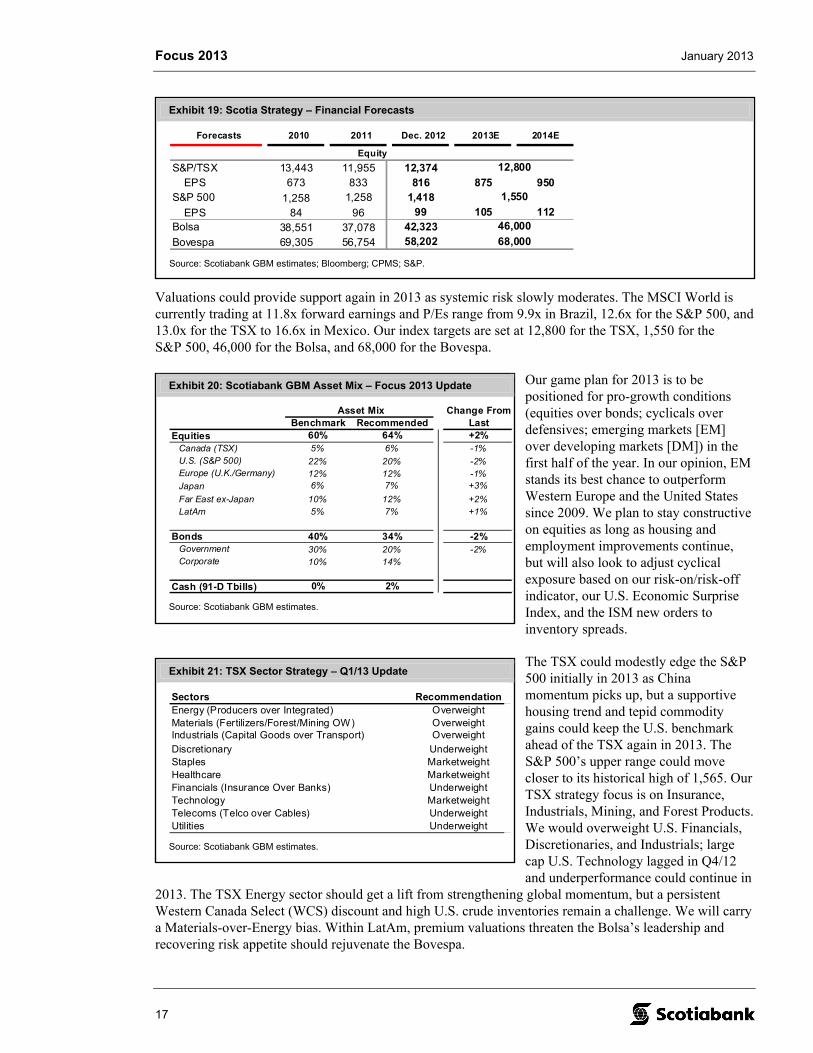

Exhibit 19: Scotia Strategy – Financial Forecasts

Forecasts 2010 2011 Dec. 2012 2013E 2014E

S&P/TSX 13,443 11,955 12,374 EPS 673 833 816 875 950S&P 500 1,258 1,258 1,418

EPS 84 96 99 105 112Bolsa 38,551 37,078 42,323

Bovespa 69,305 56,754 58,202

Equity

12,800

1,550

46,000

68,000

Source: Scotiabank GBM estimates; Bloomberg; CPMS; S&P.

Exhibit 20: Scotiabank GBM Asset Mix – Focus 2013 Update

Change FromBenchmark Recommended Last

Equities 60% 64% +2% Canada (TSX) 5% 6% -1% U.S. (S&P 500) 22% 20% -2% Europe (U.K./Germany) 12% 12% -1% Japan 6% 7% +3%

Far East ex-Japan 10% 12% +2% LatAm 5% 7% +1%

Bonds 40% 34% -2% Government 30% 20% -2% Corporate 10% 14%

Cash (91-D Tbills) 0% 2%

Asset Mix

Source: Scotiabank GBM estimates.

Exhibit 21: TSX Sector Strategy – Q1/13 Update

SectorsEnergy (Producers over Integrated)Materials (Fertilizers/Forest/Mining OW)Industrials (Capital Goods over Transport)

DiscretionaryStaplesHealthcareFinancials (Insurance Over Banks)TechnologyTelecoms (Telco over Cables)Utilities

MarketweightUnderweightUnderweight

UnderweightMarketweightMarketweightUnderweight

RecommendationOverweightOverweightOverweight

Source: Scotiabank GBM estimates.

Valuations could provide support again in 2013 as systemic risk slowly moderates. The MSCI World is currently trading at 11.8x forward earnings and P/Es range from 9.9x in Brazil, 12.6x for the S&P 500, and 13.0x for the TSX to 16.6x in Mexico. Our index targets are set at 12,800 for the TSX, 1,550 for the S&P 500, 46,000 for the Bolsa, and 68,000 for the Bovespa.

Our game plan for 2013 is to be positioned for pro-growth conditions (equities over bonds; cyclicals over defensives; emerging markets [EM] over developing markets [DM]) in the first half of the year. In our opinion, EM stands its best chance to outperform Western Europe and the United States since 2009. We plan to stay constructive on equities as long as housing and employment improvements continue, but will also look to adjust cyclical exposure based on our risk-on/risk-off indicator, our U.S. Economic Surprise Index, and the ISM new orders to inventory spreads.

The TSX could modestly edge the S&P 500 initially in 2013 as China momentum picks up, but a supportive housing trend and tepid commodity gains could keep the U.S. benchmark ahead of the TSX again in 2013. The S&P 500’s upper range could move closer to its historical high of 1,565. Our TSX strategy focus is on Insurance, Industrials, Mining, and Forest Products. We would overweight U.S. Financials, Discretionaries, and Industrials; large cap U.S. Technology lagged in Q4/12 and underperformance could continue in

2013. The TSX Energy sector should get a lift from strengthening global momentum, but a persistent Western Canada Select (WCS) discount and high U.S. crude inventories remain a challenge. We will carry a Materials-over-Energy bias. Within LatAm, premium valuations threaten the Bolsa’s leadership and recovering risk appetite should rejuvenate the Bovespa.

Focus 2013 January 2013

18

1 0 T H E M E S F O R 2 0 1 3

1. Jobless claims as guide. This has been a constant theme of ours since 2009, and we are sticking to it. In our opinion, monitoring the trend in weekly jobless claims helps filter the background noise. As long as U.S. employment conditions improve, we will maintain a constructive S&P 500 bias and stand ready to buy the dips.

2. U.S. housing will dictate sentiment. Attractive affordability and low inventories point to a sustained recovery in U.S. housing activity in 2013, a development that could solidify Main Street confidence. A pickup in housing data (starts, sales, prices) could represent the biggest threat to the bond bull market. Homebuilders and lumber companies should perform well.

3. Canada’s housing sector is going the wrong way. In contrast to the situation in the United States, Canada’s domestic economy will be challenged by weaker housing activity in 2013. Although a U.S.-style downturn remains a low-probability scenario, in our opinion, the threat to wealth effect and consumer spending will weigh on growth. Canada’s 2013 GDP growth should lag that of the United States for the second consecutive year.

4. China growth picking up… modestly. Following a disappointing 2012, China GDP should rebound toward 8.0% in 2013. Commodity-sensitive markets should be supported by stronger momentum in China, but modest easing and muted European demand are likely to keep Chinese GDP below the 9% threshold and restrain commodity price gains. EM also stands its best chance to outperform Western Europe and the United States since 2009.

5. Europe bottoms, but stays in the slow lane. Fiscal consolidation, a heavy debt load, and political disagreements will restrict European growth at least through the middle of the decade. Southern Europe will remain in recession in 2013, with France struggling to grow. Germany and U.K. GDP growth could hover near 1% next year.

6. Correlations decline, slowly back to basics. Sector correlations have steadily declined in recent months and 2012 proved to be much more of a “stock picker’s market.” Company fundamentals and top-down signals should combine again to dictate market trends in 2013. Sporadic risk-on/risk-off leadership should prevail with shorter duration and lower intensity than in 2008-2011.

7. Valuations to increase from below-average levels. P/E multiples increased in 2012 and we expect the trend to continue in 2013 as systemic risk moderates. Since 1960, S&P 500 P/E expansion/contraction cycles have occurred alongside improving housing and employment conditions. The MSCI AC World forward P/E stands at 11.8x, 25% below its long-term average (TSX at -9% discount versus -17% for S&P 500). A 1x point P/E increase would provide roughly 8%-12% upside based on current forward EPS levels.

8. Challenges to TSX Energy and Financials leadership. U.S. Energy (+2.0% in 2012) and U.S. Financials (+26%) outperformed their TSX counterparts by 426 bp and 1015 bp, respectively, in 2012, and 2013 is shaping up to be challenging. Increasing U.S. energy production combined with low export capacity in Canada is weighing on TSX Energy. Commodity sentiment could improve in 1H/13, as Chinese data recovers, and the TSX Energy sector should benefit. Still, the WCS discount to West Texas Intermediate will need to recover in order to support a period of sustained outperformance. A slowdown in Canadian housing is also likely to increase background noise for Canadian Financials and could limit valuation expansion in the sector.

Focus 2013 January 2013

19

9. Play the yield theme, but mind the premium. Faith in the dividend theme is directly linked to the direction of long-term bond yields, and since U.S. monetary policy is expected to remain accommodative until 2015, a low rate environment should support dividend stocks. Still, investors should mind the valuation gap as it also influences leadership. High-dividend TSX stocks are currently trading at a 12% premium (price to book) over the non-dividend payers group (was 5% in December 2011). The yield theme has underperformed in 2H/12 after the premium hit 23%.

10. Diet and Bundestag. Political focus will shift to Japan and Germany in 2013. Japanese leadership change could trigger a more stimulative focus from the Bank of Japan through a lower yen (higher U.S. dollar) and a higher inflation target. In Germany, voters will get a chance to voice their concerns on how the country has navigated the Eurozone crisis since 2010.

Focus 2013 January 2013

20

T H I S P A G E L E F T I N T E N T I O N A L L Y B L A N K .

Focus 2013 January 2013

Hugo Ste-Marie, CFA (514) 287-4992 (Scotia Capital Inc. – Canada) [email protected]

21

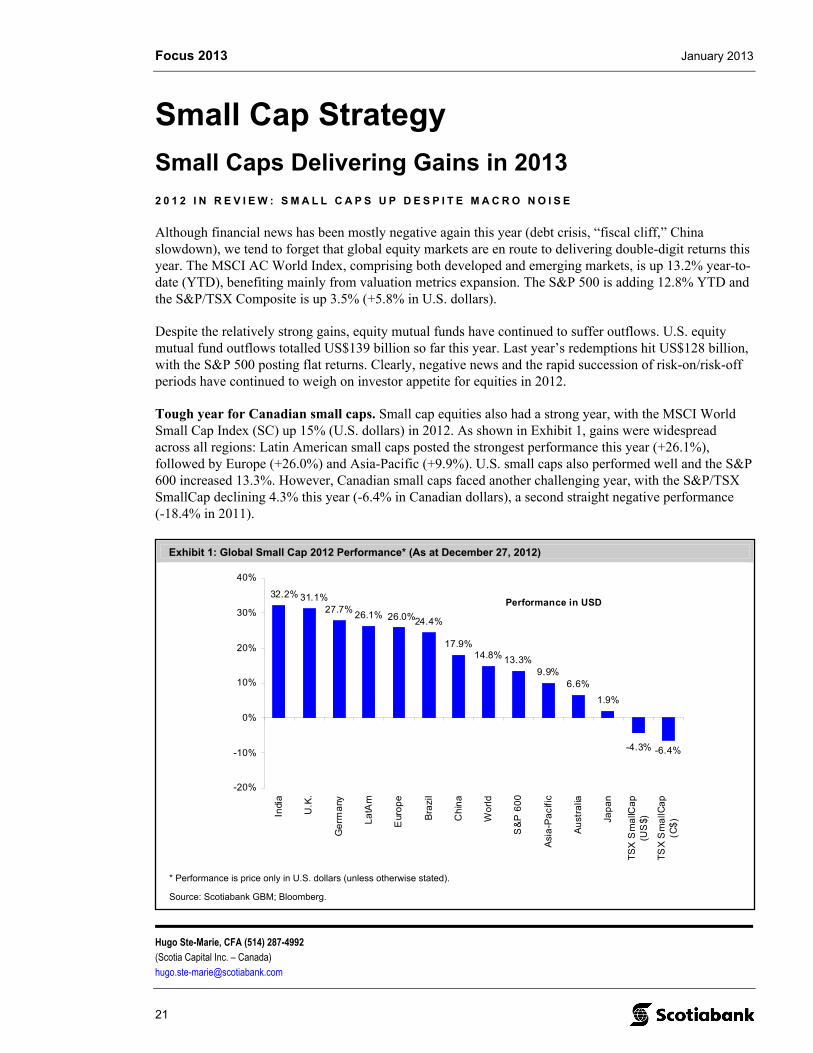

Exhibit 1: Global Small Cap 2012 Performance* (As at December 27, 2012)

27.7%26.1%

24.4%

17.9%14.8% 13.3%

9.9%6.6%

1.9%

-6.4%

31.1%

26.0%

-4.3%

32.2%

-20%

-10%

0%

10%

20%

30%

40%

Indi

a

U.K

.

Ge

rma

ny

La

tAm

Eur

op

e

Bra

zil

Ch

ina

Wo

rld

S&

P 6

00

Asi

a-P

ac

ific

Au

stra

lia

Jap

an

TS

X S

ma

llCa

p(U

S$)

TS

X S

ma

llCa

p(C

$)

Performance in USD

* Performance is price only in U.S. dollars (unless otherwise stated).

Source: Scotiabank GBM; Bloomberg.

Small Cap Strategy

Small Caps Delivering Gains in 2013

2 0 1 2 I N R E V I E W : S M A L L C A P S U P D E S P I T E M A C R O N O I S E

Although financial news has been mostly negative again this year (debt crisis, “fiscal cliff,” China slowdown), we tend to forget that global equity markets are en route to delivering double-digit returns this year. The MSCI AC World Index, comprising both developed and emerging markets, is up 13.2% year-to-date (YTD), benefiting mainly from valuation metrics expansion. The S&P 500 is adding 12.8% YTD and the S&P/TSX Composite is up 3.5% (+5.8% in U.S. dollars).

Despite the relatively strong gains, equity mutual funds have continued to suffer outflows. U.S. equity mutual fund outflows totalled US$139 billion so far this year. Last year’s redemptions hit US$128 billion, with the S&P 500 posting flat returns. Clearly, negative news and the rapid succession of risk-on/risk-off periods have continued to weigh on investor appetite for equities in 2012.

Tough year for Canadian small caps. Small cap equities also had a strong year, with the MSCI World Small Cap Index (SC) up 15% (U.S. dollars) in 2012. As shown in Exhibit 1, gains were widespread across all regions: Latin American small caps posted the strongest performance this year (+26.1%), followed by Europe (+26.0%) and Asia-Pacific (+9.9%). U.S. small caps also performed well and the S&P 600 increased 13.3%. However, Canadian small caps faced another challenging year, with the S&P/TSX SmallCap declining 4.3% this year (-6.4% in Canadian dollars), a second straight negative performance (-18.4% in 2011).

Focus 2013 January 2013

22

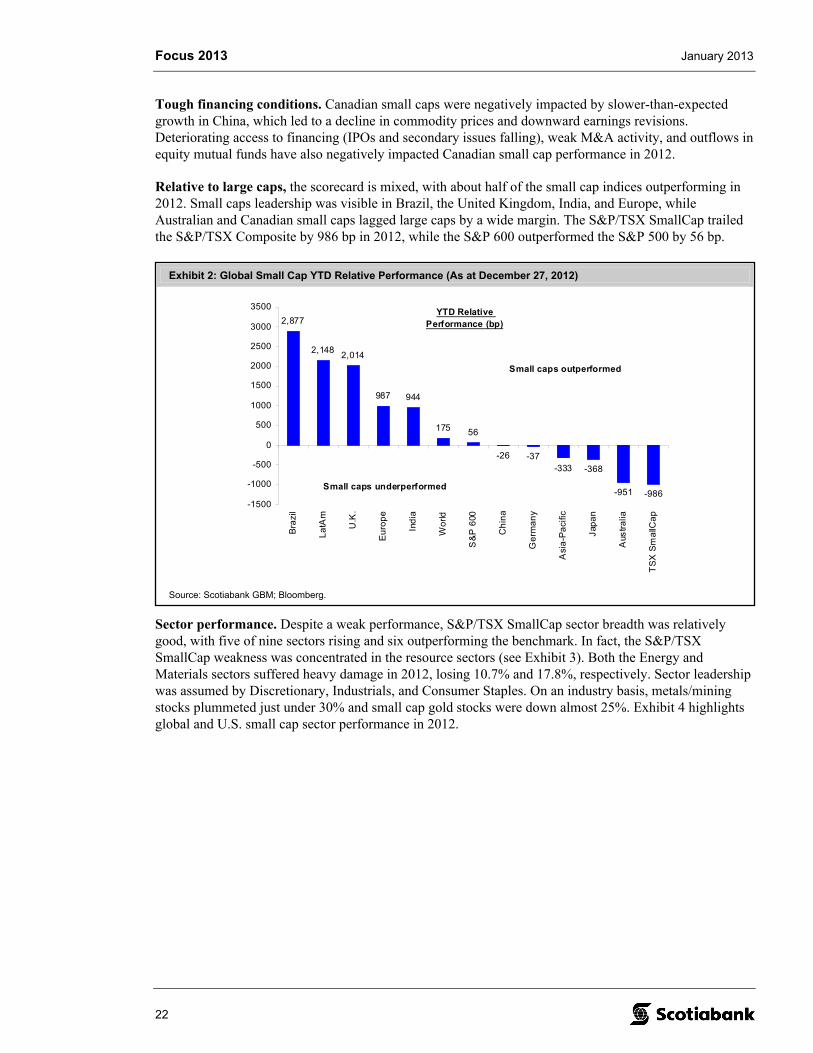

Exhibit 2: Global Small Cap YTD Relative Performance (As at December 27, 2012)

2,877

2,1482,014

987 944

175 56

-26 -37-333 -368

-951 -986-1500

-1000

-500

0

500

1000

1500

2000

2500

3000

3500

Bra

zil

La

tAm

U.K

.

Eu

rop

e

Ind

ia

Wo

rld

S&

P 6

00

Ch

ina

Ge

rma

ny

Asi

a-P

aci

fic

Jap

an

Aus

tra

lia

TS

X S

ma

llCa

p

YTD Relative Performance (bp)

Small caps outperformed

Small caps underperformed

Source: Scotiabank GBM; Bloomberg.

Tough financing conditions. Canadian small caps were negatively impacted by slower-than-expected growth in China, which led to a decline in commodity prices and downward earnings revisions. Deteriorating access to financing (IPOs and secondary issues falling), weak M&A activity, and outflows in equity mutual funds have also negatively impacted Canadian small cap performance in 2012.

Relative to large caps, the scorecard is mixed, with about half of the small cap indices outperforming in 2012. Small caps leadership was visible in Brazil, the United Kingdom, India, and Europe, while Australian and Canadian small caps lagged large caps by a wide margin. The S&P/TSX SmallCap trailed the S&P/TSX Composite by 986 bp in 2012, while the S&P 600 outperformed the S&P 500 by 56 bp.

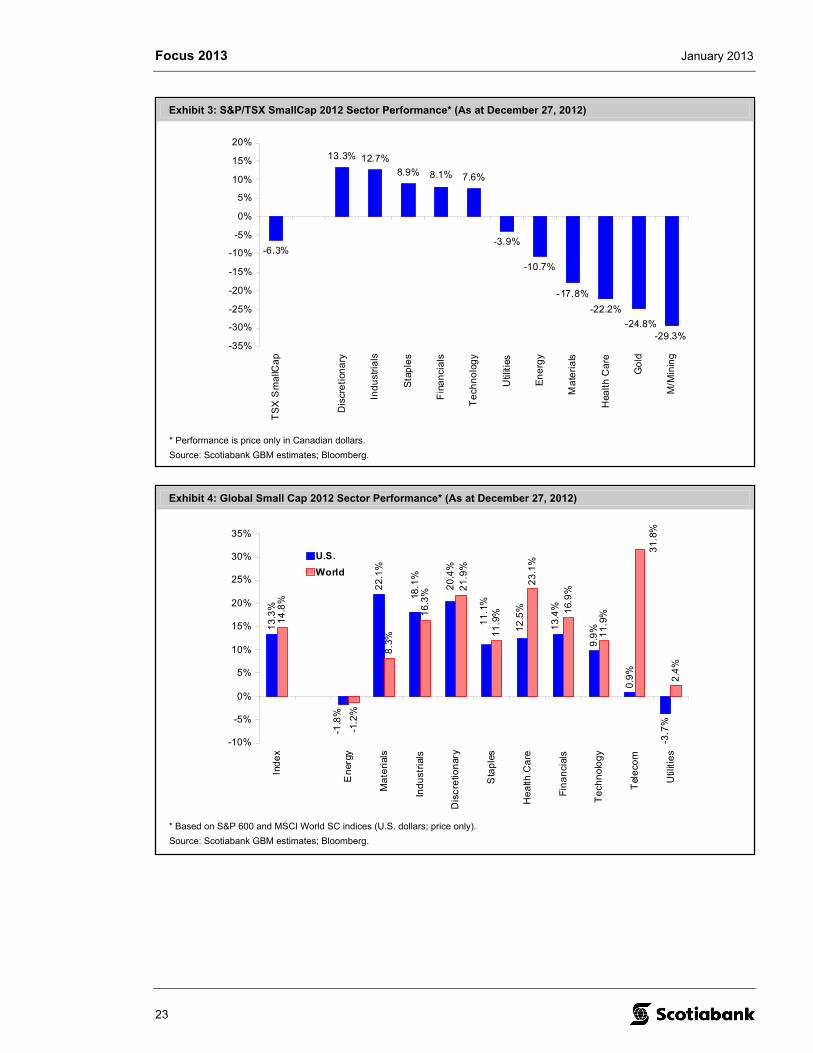

Sector performance. Despite a weak performance, S&P/TSX SmallCap sector breadth was relatively good, with five of nine sectors rising and six outperforming the benchmark. In fact, the S&P/TSX SmallCap weakness was concentrated in the resource sectors (see Exhibit 3). Both the Energy and Materials sectors suffered heavy damage in 2012, losing 10.7% and 17.8%, respectively. Sector leadership was assumed by Discretionary, Industrials, and Consumer Staples. On an industry basis, metals/mining stocks plummeted just under 30% and small cap gold stocks were down almost 25%. Exhibit 4 highlights global and U.S. small cap sector performance in 2012.

Focus 2013 January 2013

23

Exhibit 3: S&P/TSX SmallCap 2012 Sector Performance* (As at December 27, 2012)

12.7%

8.1% 7.6%

-10.7%

-17.8%

-22.2%

-29.3%-24.8%

-6.3%-3.9%

13.3%

8.9%

-35%

-30%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

TS

X S

ma

llCa

p

Dis

cre

tion

ary

Ind

ust

ria

ls

Sta

ple

s

Fin

an

cia

ls

Te

chn

olo

gy

Util

ities

En

erg

y

Ma

teri

als

Hea

lth

Ca

re

G

old

M

/Min

ing

* Performance is price only in Canadian dollars.

Source: Scotiabank GBM estimates; Bloomberg.

Exhibit 4: Global Small Cap 2012 Sector Performance* (As at December 27, 2012)

13

.3%

22

.1%

9.9

%

0.9

%

-3.7

%

14

.8%

-1.2

%

8.3

%

16

.3%

11

.9%

23

.1%

16.

9%

11

.9%

2.4

%

18.1

%

-1.8

%

13

.4%

12

.5%

11

.1%

20

.4%

31

.8%

21

.9%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

Ind

ex

En

ergy

Ma

teri

als

Ind

ust

rial

s

Dis

cre

tion

ary

Sta

ple

s

He

alth

Ca

re

Fin

an

cial

s

Te

chn

olo

gy

Tel

eco

m

Util

itie

s

U.S.

World

* Based on S&P 600 and MSCI World SC indices (U.S. dollars; price only).

Source: Scotiabank GBM estimates; Bloomberg.

Focus 2013 January 2013

24

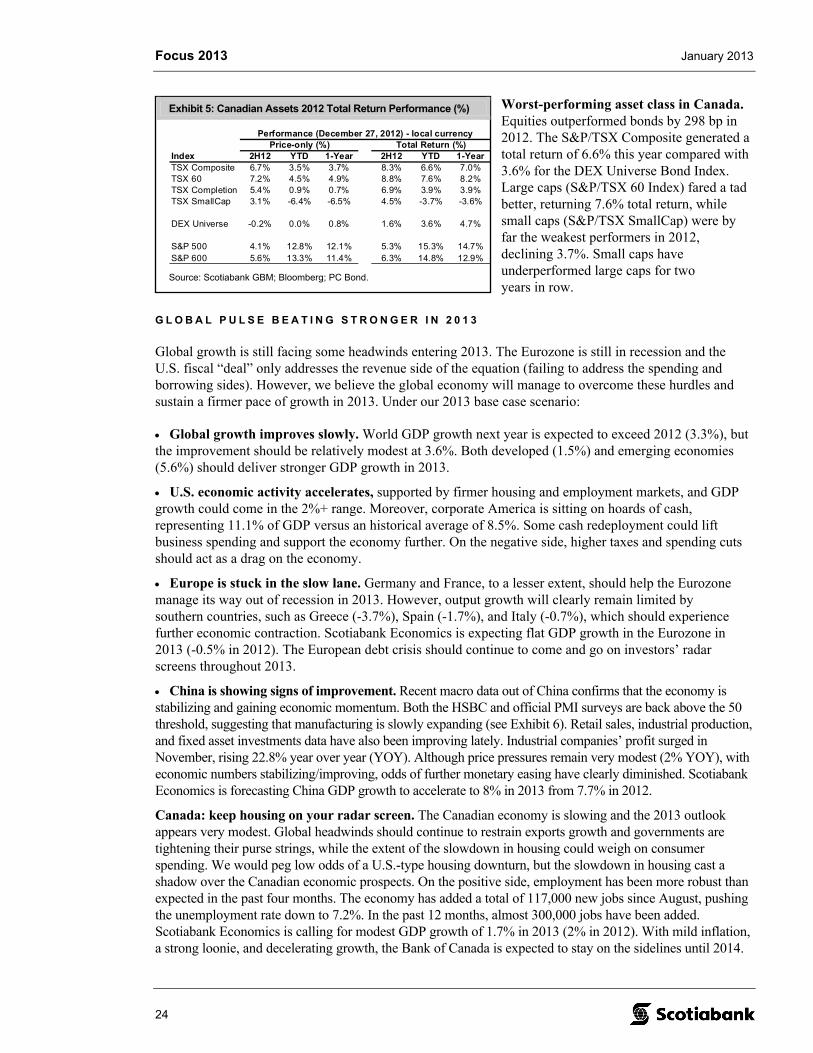

Exhibit 5: Canadian Assets 2012 Total Return Performance (%)

Index 2H12 YTD 1-Year 2H12 YTD 1-YearTSX Composite 6.7% 3.5% 3.7% 8.3% 6.6% 7.0%TSX 60 7.2% 4.5% 4.9% 8.8% 7.6% 8.2%TSX Completion 5.4% 0.9% 0.7% 6.9% 3.9% 3.9%TSX SmallCap 3.1% -6.4% -6.5% 4.5% -3.7% -3.6%

DEX Universe -0.2% 0.0% 0.8% 1.6% 3.6% 4.7%

S&P 500 4.1% 12.8% 12.1% 5.3% 15.3% 14.7%S&P 600 5.6% 13.3% 11.4% 6.3% 14.8% 12.9%

Price-only (%) Total Return (%)Performance (December 27, 2012) - local currency

Source: Scotiabank GBM; Bloomberg; PC Bond.

Worst-performing asset class in Canada. Equities outperformed bonds by 298 bp in 2012. The S&P/TSX Composite generated a total return of 6.6% this year compared with 3.6% for the DEX Universe Bond Index. Large caps (S&P/TSX 60 Index) fared a tad better, returning 7.6% total return, while small caps (S&P/TSX SmallCap) were by far the weakest performers in 2012, declining 3.7%. Small caps have underperformed large caps for two years in row.

G L O B A L P U L S E B E A T I N G S T R O N G E R I N 2 0 1 3

Global growth is still facing some headwinds entering 2013. The Eurozone is still in recession and the U.S. fiscal “deal” only addresses the revenue side of the equation (failing to address the spending and borrowing sides). However, we believe the global economy will manage to overcome these hurdles and sustain a firmer pace of growth in 2013. Under our 2013 base case scenario:

Global growth improves slowly. World GDP growth next year is expected to exceed 2012 (3.3%), but the improvement should be relatively modest at 3.6%. Both developed (1.5%) and emerging economies (5.6%) should deliver stronger GDP growth in 2013.

U.S. economic activity accelerates, supported by firmer housing and employment markets, and GDP growth could come in the 2%+ range. Moreover, corporate America is sitting on hoards of cash, representing 11.1% of GDP versus an historical average of 8.5%. Some cash redeployment could lift business spending and support the economy further. On the negative side, higher taxes and spending cuts should act as a drag on the economy.

Europe is stuck in the slow lane. Germany and France, to a lesser extent, should help the Eurozone manage its way out of recession in 2013. However, output growth will clearly remain limited by southern countries, such as Greece (-3.7%), Spain (-1.7%), and Italy (-0.7%), which should experience further economic contraction. Scotiabank Economics is expecting flat GDP growth in the Eurozone in 2013 (-0.5% in 2012). The European debt crisis should continue to come and go on investors’ radar screens throughout 2013.

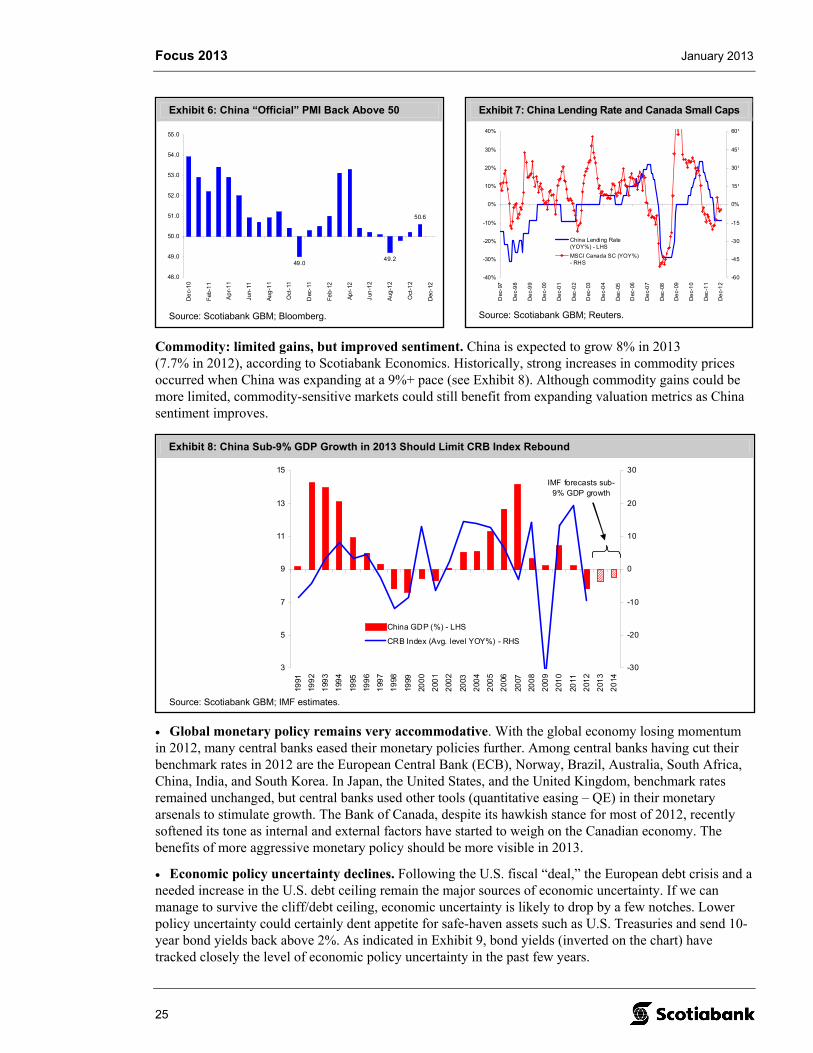

China is showing signs of improvement. Recent macro data out of China confirms that the economy is stabilizing and gaining economic momentum. Both the HSBC and official PMI surveys are back above the 50 threshold, suggesting that manufacturing is slowly expanding (see Exhibit 6). Retail sales, industrial production, and fixed asset investments data have also been improving lately. Industrial companies’ profit surged in November, rising 22.8% year over year (YOY). Although price pressures remain very modest (2% YOY), with economic numbers stabilizing/improving, odds of further monetary easing have clearly diminished. Scotiabank Economics is forecasting China GDP growth to accelerate to 8% in 2013 from 7.7% in 2012.

Canada: keep housing on your radar screen. The Canadian economy is slowing and the 2013 outlook appears very modest. Global headwinds should continue to restrain exports growth and governments are tightening their purse strings, while the extent of the slowdown in housing could weigh on consumer spending. We would peg low odds of a U.S.-type housing downturn, but the slowdown in housing cast a shadow over the Canadian economic prospects. On the positive side, employment has been more robust than expected in the past four months. The economy has added a total of 117,000 new jobs since August, pushing the unemployment rate down to 7.2%. In the past 12 months, almost 300,000 jobs have been added. Scotiabank Economics is calling for modest GDP growth of 1.7% in 2013 (2% in 2012). With mild inflation, a strong loonie, and decelerating growth, the Bank of Canada is expected to stay on the sidelines until 2014.

Focus 2013 January 2013

25

Exhibit 8: China Sub-9% GDP Growth in 2013 Should Limit CRB Index Rebound

3

5

7

9

11

13

15

1991

199

2

199

3

199

4

1995

199

6

199

7

19

98

1999

200

0

200

1

200

2

2003

200

4

200

5

20

06

2007

200

8

200

9

201

0

2011

201

2

201

3

20

14

-30

-20

-10

0

10

20

30

China GDP (%) - LHS

CRB Index (Avg. level YOY%) - RHS

IMF forecasts sub-9% GDP growth

Source: Scotiabank GBM; IMF estimates.

Exhibit 7: China Lending Rate and Canada Small Caps

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

Dec

-97

De

c-9

8

De

c-9

9

De

c-00

De

c-0

1

Dec

-02

Dec

-03

De

c-0

4

Dec

-05

Dec

-06

De

c-0

7

Dec

-08

De

c-09

De

c-1

0

Dec

-11

De

c-1

2

-60%

-45%

-30%

-15%

0%

15%

30%

45%

60%

China Lending Rate(YOY%) - LHS

MSCI Canada SC (YOY%)- RHS

Source: Scotiabank GBM; Reuters.

Exhibit 6: China “Official” PMI Back Above 50

50.6

49.249.0

48.0

49.0

50.0

51.0

52.0

53.0

54.0

55.0

De

c-1

0

Feb

-11

Ap

r-1

1

Jun-

11

Au

g-1

1

Oct

-11

Dec

-11

Fe

b-12

Ap

r-12

Jun

-12

Aug

-12

Oct

-12

Dec

-12

Source: Scotiabank GBM; Bloomberg.

Commodity: limited gains, but improved sentiment. China is expected to grow 8% in 2013 (7.7% in 2012), according to Scotiabank Economics. Historically, strong increases in commodity prices occurred when China was expanding at a 9%+ pace (see Exhibit 8). Although commodity gains could be more limited, commodity-sensitive markets could still benefit from expanding valuation metrics as China sentiment improves.

• Global monetary policy remains very accommodative. With the global economy losing momentum in 2012, many central banks eased their monetary policies further. Among central banks having cut their benchmark rates in 2012 are the European Central Bank (ECB), Norway, Brazil, Australia, South Africa, China, India, and South Korea. In Japan, the United States, and the United Kingdom, benchmark rates remained unchanged, but central banks used other tools (quantitative easing – QE) in their monetary arsenals to stimulate growth. The Bank of Canada, despite its hawkish stance for most of 2012, recently softened its tone as internal and external factors have started to weigh on the Canadian economy. The benefits of more aggressive monetary policy should be more visible in 2013.

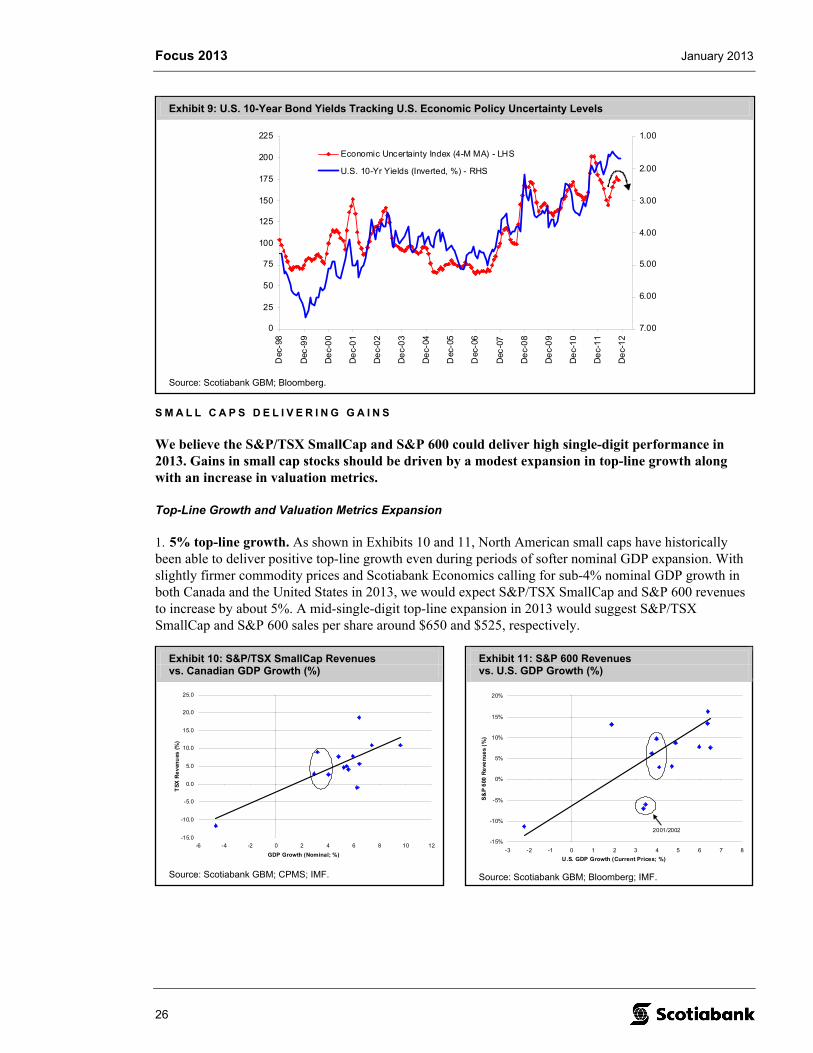

• Economic policy uncertainty declines. Following the U.S. fiscal “deal,” the European debt crisis and a needed increase in the U.S. debt ceiling remain the major sources of economic uncertainty. If we can manage to survive the cliff/debt ceiling, economic uncertainty is likely to drop by a few notches. Lower policy uncertainty could certainly dent appetite for safe-haven assets such as U.S. Treasuries and send 10-year bond yields back above 2%. As indicated in Exhibit 9, bond yields (inverted on the chart) have tracked closely the level of economic policy uncertainty in the past few years.

Focus 2013 January 2013

26

Exhibit 9: U.S. 10-Year Bond Yields Tracking U.S. Economic Policy Uncertainty Levels

0

25

50

75

100

125

150

175

200

225

Dec

-98

Dec

-99

De

c-0

0

De

c-0

1

De

c-0

2

De

c-0

3

De

c-04

Dec

-05

Dec

-06

Dec

-07

De

c-0

8

De

c-0

9

De

c-1

0

De

c-1

1

De

c-1

2

1.00

2.00

3.00

4.00

5.00

6.00

7.00

Economic Uncertainty Index (4-M MA) - LHS

U.S. 10-Yr Yields (Inverted, %) - RHS

Source: Scotiabank GBM; Bloomberg.

Exhibit 11: S&P 600 Revenues vs. U.S. GDP Growth (%)

-15%

-10%

-5%

0%

5%

10%

15%

20%

-3 -2 -1 0 1 2 3 4 5 6 7 8

U.S. GDP Growth (Current Prices; %)

S&

P 6

00 R

eve

nu

es

(%)

2001/2002

Source: Scotiabank GBM; Bloomberg; IMF.

Exhibit 10: S&P/TSX SmallCap Revenues vs. Canadian GDP Growth (%)

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

25.0

-6 -4 -2 0 2 4 6 8 10 12

GDP Growth (Nominal; %)

TS

X R

ev

enu

es (

%)

Source: Scotiabank GBM; CPMS; IMF.

S M A L L C A P S D E L I V E R I N G G A I N S

We believe the S&P/TSX SmallCap and S&P 600 could deliver high single-digit performance in 2013. Gains in small cap stocks should be driven by a modest expansion in top-line growth along with an increase in valuation metrics.

Top-Line Growth and Valuation Metrics Expansion

1. 5% top-line growth. As shown in Exhibits 10 and 11, North American small caps have historically been able to deliver positive top-line growth even during periods of softer nominal GDP expansion. With slightly firmer commodity prices and Scotiabank Economics calling for sub-4% nominal GDP growth in both Canada and the United States in 2013, we would expect S&P/TSX SmallCap and S&P 600 revenues to increase by about 5%. A mid-single-digit top-line expansion in 2013 would suggest S&P/TSX SmallCap and S&P 600 sales per share around $650 and $525, respectively.

Focus 2013 January 2013

27

Exhibit 14: S&P/TSX SmallCap Upside/Downside Matrix

TSX SmallCap Level: 568

Trailing sales: 617

Trailing P/S Ratio: 0.92

P/S Ratio0.85 498 -12% 538 -5% 551 -3% 564 -1% 577 2%0.90 528 -7% 569 0% 583 3% 597 5% 611 8%

0.93 545 -4% 588 4% 603 6% 617 9% 631 11%

0.95 557 -2% 601 6% 615 8% 630 11% 645 14%0.98 574 1% 620 9% 635 12% 650 14% 665 17%

1.00 586 3% 632 11% 648 14% 663 17% 679 19%

$586+7.5%$663

+10%$679

2013 Top-line Growth ($ / %)+5%$648

+2.5%$632

-5%

Source: Scotiabank GBM estimates; Bloomberg.

Exhibit 15: S&P 600 SmallCap Upside/Downside Matrix

S&P 600 SmallCap Level: 468

Trailing sales: 500

Trailing P/S Ratio: 0.94

P/S Ratio0.85 404 -14% 436 -7% 446 -5% 457 -2% 468 0%0.90 428 -9% 461 -1% 473 1% 484 3% 495 6%

0.93 442 -6% 477 2% 488 4% 500 7% 512 9%

0.95 451 -4% 487 4% 499 7% 511 9% 523 12%0.98 463 -1% 500 7% 512 9% 524 12% 536 15%

1.00 475 1% 513 10% 525 12% 538 15% 550 18%

+5% +7.5% +10%$550$525 $538

+2.5%$475 $513

2013 Top-line Growth ($ / %)-5%

Source: Scotiabank GBM estimates; Bloomberg.

Exhibit 13: S&P 600 P/S Ratio

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

1.1

1.2

Jun-

98

Jun

-99

Jun

-00

Jun

-01

Jun-

02

Jun-

03

Jun

-04

Jun

-05

Jun

-06

Jun-

07

Jun-

08

Jun

-09

Jun

-10

Jun

-11

Jun-

12

+1 Stdev.

-1 Stdev.

Source: Scotiabank GBM; Bloomberg.

Exhibit 12: S&P/TSX SmallCap P/S Ratio

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

Jun-

99

Jun-

00

Jun

-01

Jun

-02

Jun

-03

Jun-

04

Jun-

05

Jun

-06

Jun

-07

Jun-

08

Jun-

09

Jun-

10

Jun

-11

Jun

-12

Jun-

13

+1 Stdev.

-1 Stdev.

Source: Scotiabank GBM; CPMS; Bloomberg.

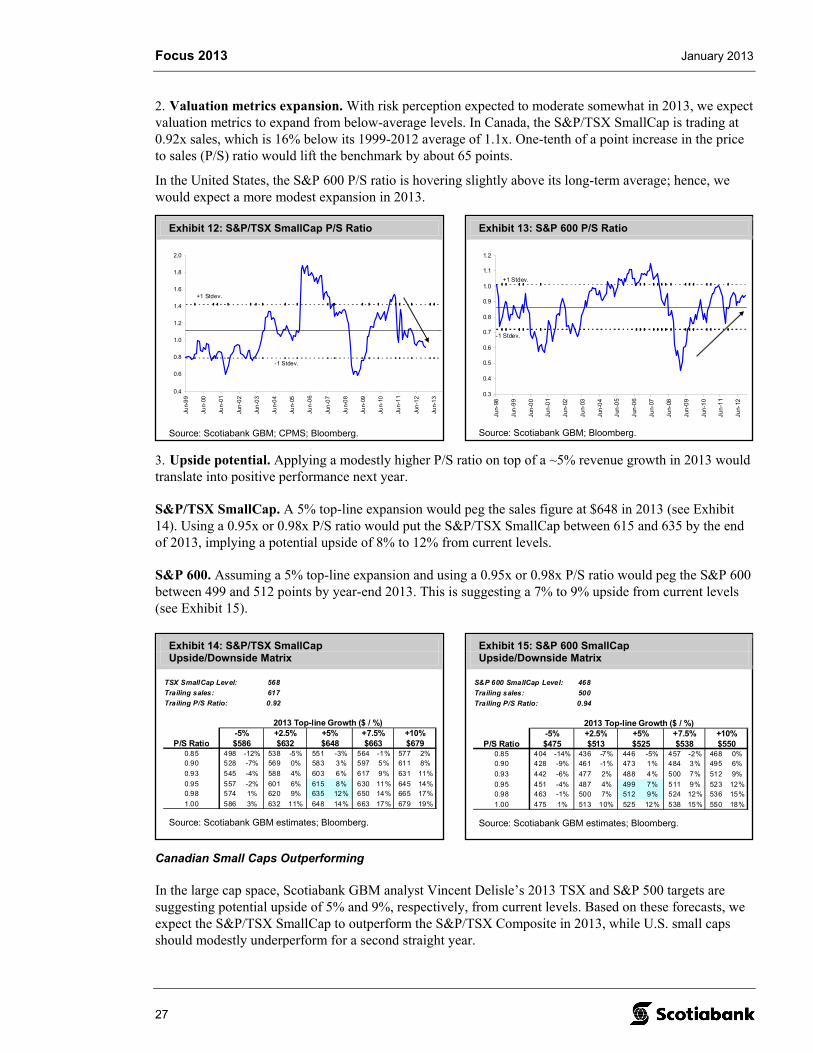

2. Valuation metrics expansion. With risk perception expected to moderate somewhat in 2013, we expect valuation metrics to expand from below-average levels. In Canada, the S&P/TSX SmallCap is trading at 0.92x sales, which is 16% below its 1999-2012 average of 1.1x. One-tenth of a point increase in the price to sales (P/S) ratio would lift the benchmark by about 65 points.

In the United States, the S&P 600 P/S ratio is hovering slightly above its long-term average; hence, we would expect a more modest expansion in 2013.

3. Upside potential. Applying a modestly higher P/S ratio on top of a ~5% revenue growth in 2013 would translate into positive performance next year.

S&P/TSX SmallCap. A 5% top-line expansion would peg the sales figure at $648 in 2013 (see Exhibit 14). Using a 0.95x or 0.98x P/S ratio would put the S&P/TSX SmallCap between 615 and 635 by the end of 2013, implying a potential upside of 8% to 12% from current levels.

S&P 600. Assuming a 5% top-line expansion and using a 0.95x or 0.98x P/S ratio would peg the S&P 600 between 499 and 512 points by year-end 2013. This is suggesting a 7% to 9% upside from current levels (see Exhibit 15).

Canadian Small Caps Outperforming

In the large cap space, Scotiabank GBM analyst Vincent Delisle’s 2013 TSX and S&P 500 targets are suggesting potential upside of 5% and 9%, respectively, from current levels. Based on these forecasts, we expect the S&P/TSX SmallCap to outperform the S&P/TSX Composite in 2013, while U.S. small caps should modestly underperform for a second straight year.

Focus 2013 January 2013

28

Exhibit 18: China CPI vs. S&P/TSX SmallCap/ S&P 600 Ratio

-6

-4

-2

0

2

4

6

8

10

Jun-

99

Jun-

00

Jun-

01

Jun-

02

Jun-

03

Jun-

04

Jun-

05

Jun

-06

Jun

-07

Jun-

08

Jun

-09

Jun

-10

Jun

-11

Jun

-12

1.00

1.10

1.20

1.30

1.40

1.50

1.60

1.70

1.80

1.90

2.00

TSX SmallCap (USD) / S&P 600 - RHS

China CPI (%) - LHS

Source: Scotiabank GBM; Bloomberg.

Exhibit 19: China CPI vs. Small Cap Materials/Staples*

0.30

0.50

0.70

0.90

1.10

1.30

1.50

1.70

Dec

-98

De

c-9

9

De

c-0

0

De

c-0

1

Dec

-02

Dec

-03

Dec

-04

De

c-0

5

De

c-0

6

De

c-0

7

De

c-0

8

Dec

-09

Dec

-10

De

c-1

1

De

c-1

2

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

Small cap Materials / Staples* - LHS

China CPI (%) - RHS

* Based on MSCI Canada Small Cap indices.

Source: Scotiabank GBM; Reuters.

Exhibit 16: U.S. Small Caps Relative Performance and Tax Rate on Capital Gains

10

15

20

25

30

35

40

45

197

5

19

77

197

9

198

1

198

3

198

5

198

7

198

9

1991

199

3

1995

199

7

1999

200

1

2003

200

5

2007

200

9

2011

201

30.60

0.80

1.00

1.20

1.40

1.60Maximum tax rate oncapital gains (%) - LHS

Russell 1000 / Russell2000 - RHS

Top tax rate on capital gains is set to increase to 24% in 2013

Source: Scotiabank GBM; U.S. Tax Policy Center; Bloomberg.

Exhibit 17: U.S. Small Cap Relative P/S Ratio

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

Jun-

98

Jun

-99

Jun

-00

Jun-

01

Jun-

02

Jun

-03

Jun

-04

Jun-

05

Jun

-06

Jun

-07

Jun-

08

Jun-

09

Jun

-10

Jun

-11

Jun-

12

-1 Stdev.

+1 Stdev.

Source: Scotiabank GBM; Bloomberg.

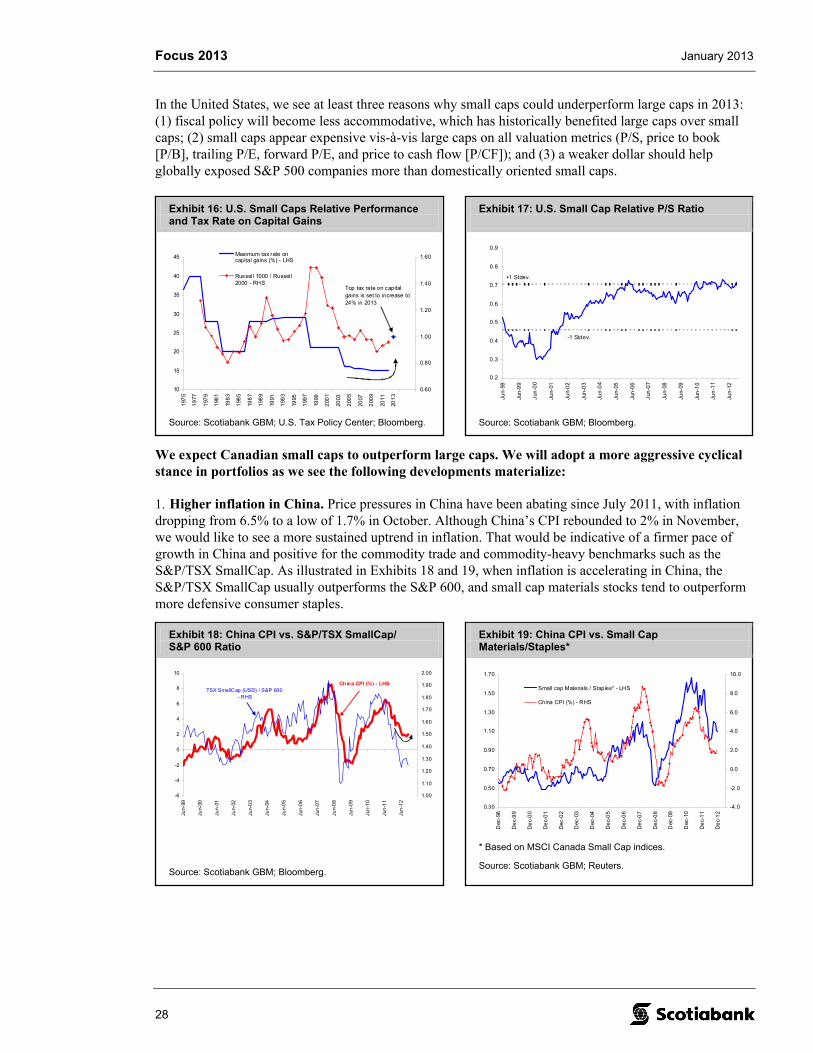

In the United States, we see at least three reasons why small caps could underperform large caps in 2013: (1) fiscal policy will become less accommodative, which has historically benefited large caps over small caps; (2) small caps appear expensive vis-à-vis large caps on all valuation metrics (P/S, price to book [P/B], trailing P/E, forward P/E, and price to cash flow [P/CF]); and (3) a weaker dollar should help globally exposed S&P 500 companies more than domestically oriented small caps.

We expect Canadian small caps to outperform large caps. We will adopt a more aggressive cyclical stance in portfolios as we see the following developments materialize:

1. Higher inflation in China. Price pressures in China have been abating since July 2011, with inflation dropping from 6.5% to a low of 1.7% in October. Although China’s CPI rebounded to 2% in November, we would like to see a more sustained uptrend in inflation. That would be indicative of a firmer pace of growth in China and positive for the commodity trade and commodity-heavy benchmarks such as the S&P/TSX SmallCap. As illustrated in Exhibits 18 and 19, when inflation is accelerating in China, the S&P/TSX SmallCap usually outperforms the S&P 600, and small cap materials stocks tend to outperform more defensive consumer staples.

Focus 2013 January 2013

29

Exhibit 20: MSCI World SC Relative Performance vs. U.S. Dollar Index

80

100

120

140

160

180

200

220

240

260

280

Dec

-06

Jun-

07

Dec

-07

Jun-

08

De

c-0

8

Jun

-09

De

c-0

9

Jun

-10

De

c-1

0

Jun

-11

De

c-1

1

Jun

-12

Dec

-12

Jun-

13

70

73

76

79

82

85

88

91

MSCI World SC - LHS

DXY (Inverted) - RHS

Source: Scotiabank GBM; Bloomberg.

Exhibit 21: S&P/TSX SmallCap Relative Performance vs. U.S. Dollar Index

0.030

0.035

0.040

0.045

0.050

0.055

0.060

0.065

De

c-0

6

Jun-

07

Dec

-07

Jun

-08

Dec

-08

Jun

-09

De

c-0

9

Jun-

10

De

c-1

0

Jun

-11

Dec

-11

Jun

-12

Dec

-12

Jun-

13

70

73

76

79

82

85

88

91

TSX SmallCap / TSX Composite - LHS

DXY (Inverted) - RHS

Source: Scotiabank GBM; Reuters.

Exhibit 23: MSCI Canada Small Cap Materials

100

300

500

700

900

1100

1300

1500

Jun-

07

De

c-0

7

Jun

-08

Dec

-08

Jun-

09

De

c-0

9

Jun

-10

De

c-1

0

Jun

-11

Dec

-11

Jun

-12

De

c-1

2

Source: Scotiabank GBM; Reuters.

Exhibit 22: MSCI Canada Small Cap Energy

300

400

500

600

700

800

900

1000

1100

1200

1300

Jun-

07

De

c-0

7

Jun

-08

Dec

-08

Jun-

09

De

c-0

9

Jun

-10

De

c-1

0

Jun

-11

Dec

-11

Jun

-12

De

c-1

2

Source: Scotiabank GBM; Reuters.

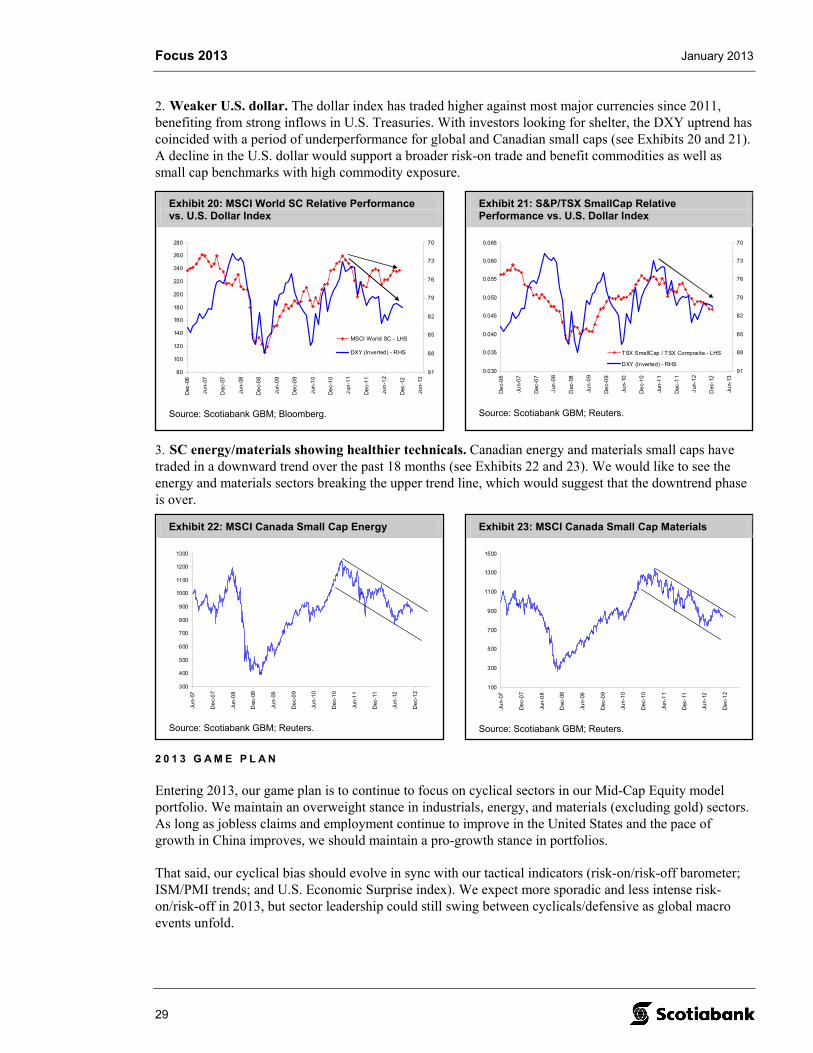

2. Weaker U.S. dollar. The dollar index has traded higher against most major currencies since 2011, benefiting from strong inflows in U.S. Treasuries. With investors looking for shelter, the DXY uptrend has coincided with a period of underperformance for global and Canadian small caps (see Exhibits 20 and 21). A decline in the U.S. dollar would support a broader risk-on trade and benefit commodities as well as small cap benchmarks with high commodity exposure.

3. SC energy/materials showing healthier technicals. Canadian energy and materials small caps have traded in a downward trend over the past 18 months (see Exhibits 22 and 23). We would like to see the energy and materials sectors breaking the upper trend line, which would suggest that the downtrend phase is over.

2 0 1 3 G A M E P L A N

Entering 2013, our game plan is to continue to focus on cyclical sectors in our Mid-Cap Equity model portfolio. We maintain an overweight stance in industrials, energy, and materials (excluding gold) sectors. As long as jobless claims and employment continue to improve in the United States and the pace of growth in China improves, we should maintain a pro-growth stance in portfolios.

That said, our cyclical bias should evolve in sync with our tactical indicators (risk-on/risk-off barometer; ISM/PMI trends; and U.S. Economic Surprise index). We expect more sporadic and less intense risk-on/risk-off in 2013, but sector leadership could still swing between cyclicals/defensive as global macro events unfold.

Focus 2013 January 2013

30

Exhibit 24: NAHB Housing Index vs. Homebuilders and Lumber Stocks (2005-2012)

0

10

20

30

40

50

60

70

80

Jan-

05

Jul-

05

Jan

-06

Jul-

06

Jan

-07

Jul-

07

Jan-

08

Jul-0

8

Jan-

09

Jul-0

9

Jan

-10

Jul-

10

Jan

-11

Jul

-11

Jan

-12

Jul-

12

Jan

-13

Jul-1

3

Jan-

14

0

20

40

60

80

100

120

140

160NAHB Housing Index - LHS

Interfor - RHS

Louisiana-Pacific - RHSWest Fraser Timber - RHS

Norbord - RHS

Stocks Normalized at 100 on Jan. 2005

Source: Scotiabank GBM; Bloomberg.

Exhibit 25: U.S. 10-Year Yields and Consumer Confidence

40.0

50.0

60.0

70.0

80.0

90.0

100.0

110.0

De

c-0

0

De

c-0

1

De

c-0

2

De

c-0

3

Dec

-04

Dec

-05

Dec

-06

De

c-0

7

De

c-0

8

De

c-0

9

De

c-1

0

De

c-1

1

Dec

-12

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

5.00

5.50

6.00

Consumer confidence - LHS

10-yr yields (3-M MA; %) - RHS

Source: Scotiabank GBM; Bloomberg.

Exhibit 26: U.S. 10-Year Yields and S&P/TSX SmallCap P/S

0.00

1.00

2.00

3.00

4.00

5.00

6.00

Dec

-06

Jun

-07

De

c-0

7

Jun-

08

Dec

-08

Jun

-09

De

c-0

9

Jun-

10

De

c-1

0

Jun

-11

De

c-1

1

Jun-

12

De

c-1

2

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

U.S. 10-Yr Yields (%) - LHS

TSX SmallCap P/S - RHS

Source: Scotiabank GBM; CPMS; Bloomberg.

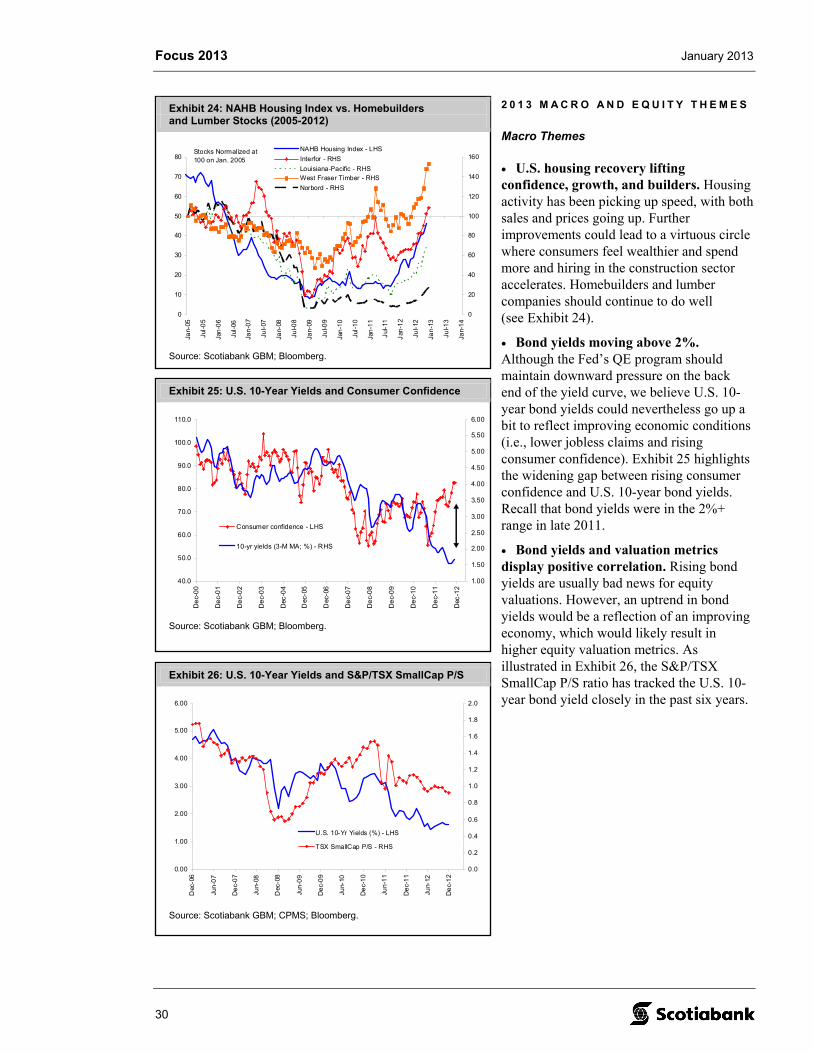

2 0 1 3 M A C R O A N D E Q U I T Y T H E M E S

Macro Themes

• U.S. housing recovery lifting confidence, growth, and builders. Housing activity has been picking up speed, with both sales and prices going up. Further improvements could lead to a virtuous circle where consumers feel wealthier and spend more and hiring in the construction sector accelerates. Homebuilders and lumber companies should continue to do well (see Exhibit 24).

• Bond yields moving above 2%. Although the Fed’s QE program should maintain downward pressure on the back end of the yield curve, we believe U.S. 10-year bond yields could nevertheless go up a bit to reflect improving economic conditions (i.e., lower jobless claims and rising consumer confidence). Exhibit 25 highlights the widening gap between rising consumer confidence and U.S. 10-year bond yields. Recall that bond yields were in the 2%+ range in late 2011.

• Bond yields and valuation metrics display positive correlation. Rising bond yields are usually bad news for equity valuations. However, an uptrend in bond yields would be a reflection of an improving economy, which would likely result in higher equity valuation metrics. As illustrated in Exhibit 26, the S&P/TSX SmallCap P/S ratio has tracked the U.S. 10-year bond yield closely in the past six years.

Focus 2013 January 2013

31

Exhibit 28: S&P/TSX SmallCap vs. Number of New Equity Issues in Canada*

100

300

500

700

900

1100

1300

1500

1700

De

c-0

0

Dec

-01

Dec

-02

De

c-0

3

De

c-0

4

De

c-05

Dec

-06

Dec

-07

De

c-0

8

De

c-0

9

De

c-10

Dec

-11

Dec

-12

100

200

300

400

500

600

700

800

900

# of New Equity Issues (last 12-M) - LHS

TSX SmallCap Index - RHS

Correlation: 86%

* Including IPOs and follow-on.

Source: Scotiabank GBM; FP Infomart.

Exhibit 27: Correlation Expected to Fall Following Huge Run-Up

0%

20%

40%

60%

80%

100% Correlation based on IFM GDP

estimates

10%15%20%25%30%35%40%45%50%55%60%

1994

199

6

199

8

200

0

2002

200

4

200

6

200

8

20

10

2012

2014

201

6

Canada: Small Cap

Sector Correlation

Country Correlation

(17 countries)

Source: Scotiabank GBM; IMF estimates.

Exhibit 29: S&P/TSX SmallCap and M&A Activity in Canada (Deal Size Below $500 Million)

1100

1200

1300

1400

1500

1600

1700

De

c-0

4

Dec

-05

Dec

-06

De

c-0

7

De

c-0

8

Dec

-09

De

c-1

0

De

c-1

1

De

c-1

2

300

400

500

600

700

800

900

# of M&A in Canada (12-M Rolling) - LHS

TSX SmallCap - RHS

Source: Scotiabank GBM; Bloomberg.

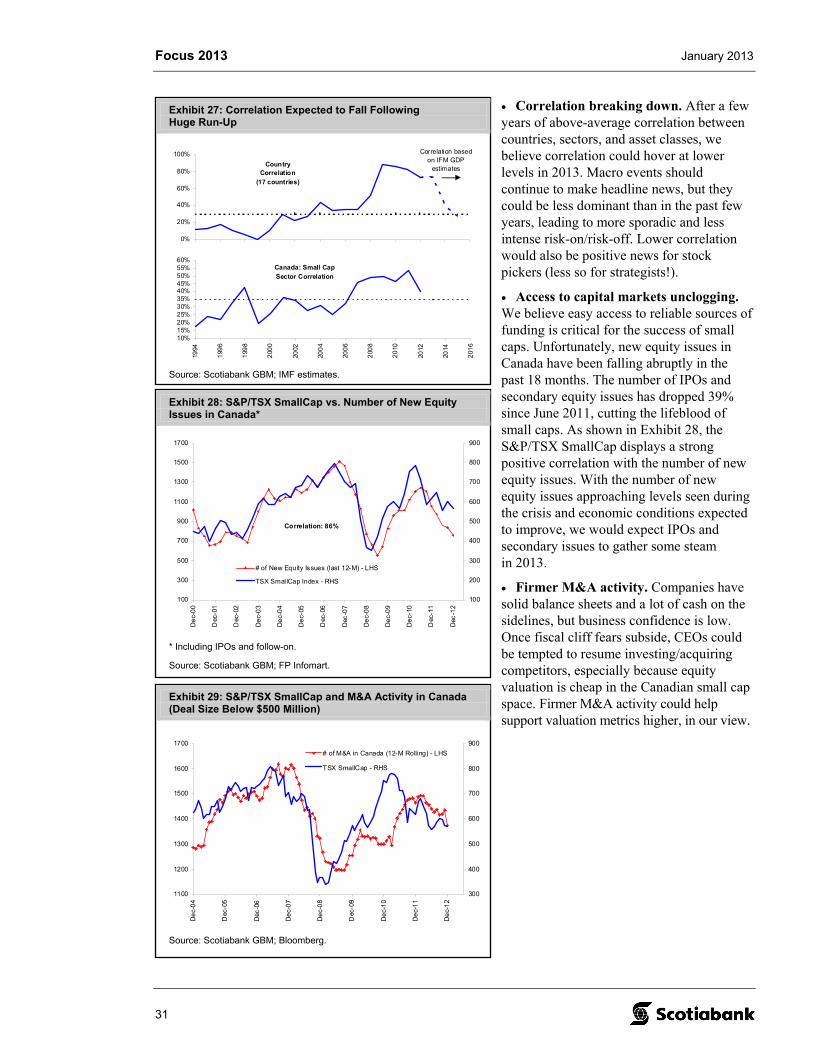

• Correlation breaking down. After a few years of above-average correlation between countries, sectors, and asset classes, we believe correlation could hover at lower levels in 2013. Macro events should continue to make headline news, but they could be less dominant than in the past few years, leading to more sporadic and less intense risk-on/risk-off. Lower correlation would also be positive news for stock pickers (less so for strategists!).

• Access to capital markets unclogging. We believe easy access to reliable sources of funding is critical for the success of small caps. Unfortunately, new equity issues in Canada have been falling abruptly in the past 18 months. The number of IPOs and secondary equity issues has dropped 39% since June 2011, cutting the lifeblood of small caps. As shown in Exhibit 28, the S&P/TSX SmallCap displays a strong positive correlation with the number of new equity issues. With the number of new equity issues approaching levels seen during the crisis and economic conditions expected to improve, we would expect IPOs and secondary issues to gather some steam in 2013.

• Firmer M&A activity. Companies have solid balance sheets and a lot of cash on the sidelines, but business confidence is low. Once fiscal cliff fears subside, CEOs could be tempted to resume investing/acquiring competitors, especially because equity valuation is cheap in the Canadian small cap space. Firmer M&A activity could help support valuation metrics higher, in our view.

Focus 2013 January 2013

32

Exhibit 30: S&P/TSX SmallCap P/B Ratio Relative to S&P/TSX Composite

0.4

0.5

0.6

0.7

0.8

0.9

1.0

1.1

1.2

Jun-

99

Jun-

00

Jun-

01

Jun

-02

Jun

-03

Jun

-04

Jun

-05

Jun

-06

Jun

-07

Jun

-08

Jun

-09

Jun

-10

Jun

-11

Jun

-12

Jun

-13

+1 Stdev.

-1 Stdev.

Source: Scotiabank GBM; Bloomberg.

Exhibit 31: Canadian Small Caps Relative to U.S. Small Caps (YOY%)

-11%

-23% -25% -21%-28%-29%

-60%

-40%

-20%

0%

20%

40%

60%

80%

Dec

-95

De

c-96

De

c-9

7

De

c-9

8

De

c-9

9

De

c-0

0

Dec

-01

Dec

-02

Dec

-03

De

c-0

4

De

c-0

5

De

c-0

6

De

c-0

7

Dec

-08

Dec

-09

Dec

-10

De

c-11

De

c-12

Canadian small caps outperforming

U.S. small caps outperforming

+1 Stdev.

-1 Stdev.

Global Manufacturing PMI (YOY%)

* Based on MSCI Canada Small Cap index (USD) and S&P 600.

Source: Scotiabank GBM; Bloomberg.

Exhibit 32: S&P/TSX SmallCap Dividend Payers Relative Valuations at the Top End of the Range

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

De

c-0

3

De

c-0

4

Dec

-05

De

c-0

6

De

c-0

7

De

c-08

Dec

-09

De

c-1

0

De

c-1

1

Dec

-12

Source: Scotiabank GBM; Bloomberg.

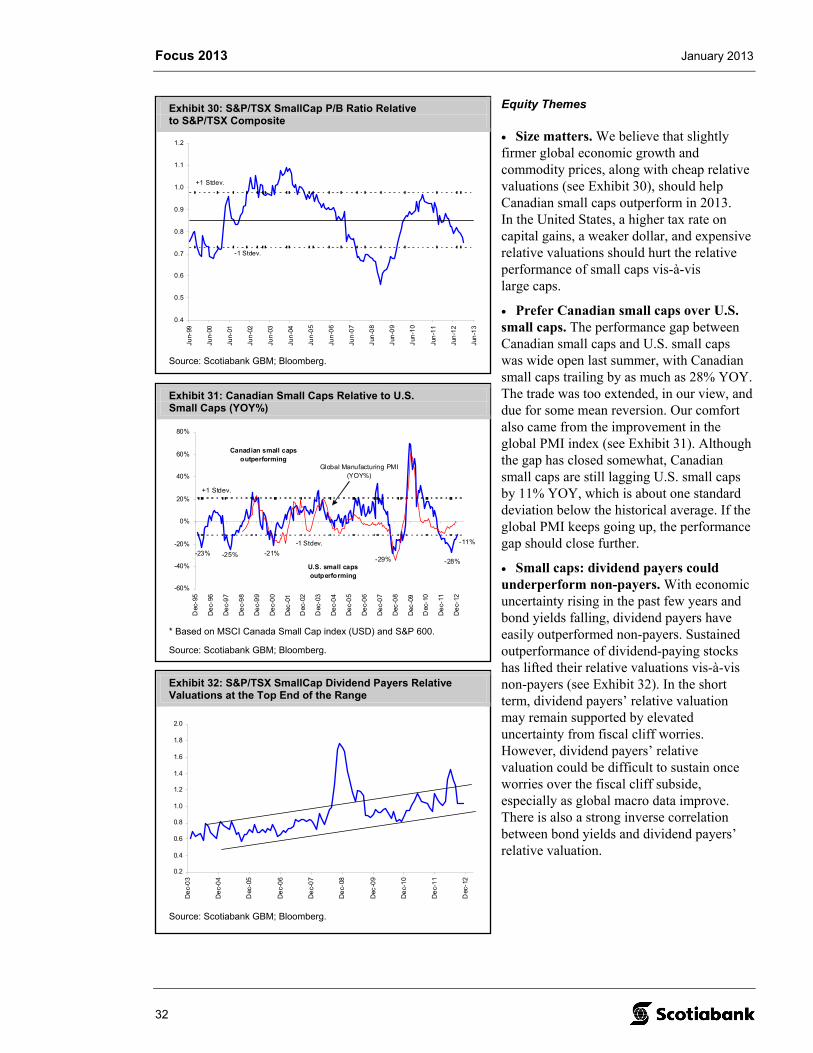

Equity Themes

• Size matters. We believe that slightly firmer global economic growth and commodity prices, along with cheap relative valuations (see Exhibit 30), should help Canadian small caps outperform in 2013. In the United States, a higher tax rate on capital gains, a weaker dollar, and expensive relative valuations should hurt the relative performance of small caps vis-à-vis large caps.