Embed Size (px)

Citation preview

Equipment Leasing 913

■ The options available to the lessee at the end of the lease term are criti-cal in determining the nature of the lease for tax purposes and the clas-sification of the lease for financial accounting purposes.

■ Non-tax-oriented leases or conditional sale leases transfer all incidentsof ownership of the leased property to the lessee and usually give thelessee a fixed price bargain purchase option or renewal option notbased on fair market value at the time of exercise. For tax purposes, thetransaction is treated as a loan.

■ In a tax-oriented true leases, the lessor claims and retains the tax ben-efits of ownership and passes through to the lessee most of such taxbenefits in the form of reduced lease payments. The principal advan-tage to a lessee of using a true lease to finance an equipment acquisi-tion is the economic benefit that comes from the indirect realizationof tax benefits that might otherwise be lost because the lessee cannotuse the tax benefits.

■ True leases are categorized as single-investor leases (or direct leases)and leveraged leases. Single-investor leases are essentially two-partytransactions, with the lessor purchasing the leased equipment with itsown funds and being at risk for 100% of the funds used to purchasethe equipment. Conceptually, a leveraged lease of equipment is similarto a single-investor lease. However, it is more complex in size, docu-mentation, legal involvement, and, most importantly, the number ofparties (particularly lenders who provide the major portion of funds topurchase the equipment) involved and the unique advantages that eachparty gains.

■ Full payout leases are basically financing transactions. In contrast, anoperating lease is one for which the lease term is much shorter than theexpected life of the equipment.

■ The reasons cited for leasing rather than borrowing to purchase equip-ment are cost savings, conservation of working capital, preservation ofcredit capacity by avoiding capitalization, elimination of risk of obso-lescence and disposal of equipment, less restrictions on management,and flexibility and convenience. Not all of these claims are valid, par-ticularly cost savings since cost reduction depends on whether the leaseis tax-oriented.

■ For financial reporting purposes, a lease is classified as either an operat-ing lease or a capital lease. FAS 13 sets forth the conditions for classify-ing a lease. For a capital lease, the transaction is shown on the lessee’sbalance sheet as a liability and the leased property reported as an asset.For an operating lease, the lessee need only disclose certain informationregarding lease commitments in a footnote.

■ The value of the lease is found by discounting the direct cash flow fromleasing by the adjusted discount rate. A negative value for a lease indi-

27-Equipment Leasing Page 913 Wednesday, June 4, 2003 12:07 PM

914 SELECTED TOPICS IN FINANCIAL MANAGEMENT

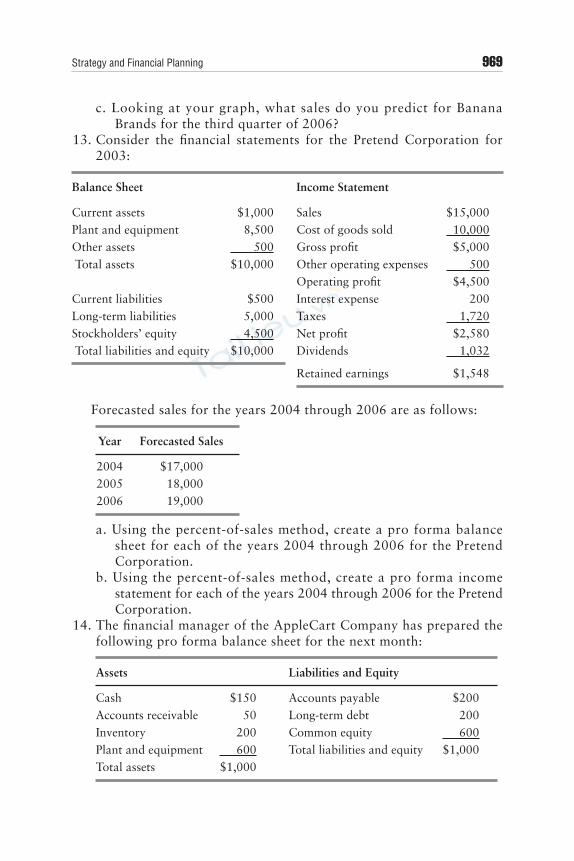

cates that leasing will not be more economically beneficial than bor-rowing to purchase. A positive value means that leasing will be moreeconomically beneficial. However, leasing will be attractive only if theNPV of the asset assuming normal financing is positive and the value ofthe lease is positive, or if the sum of the NPV of the asset assuming nor-mal financing and the value of the lease is positive.

QUESTIONS

1. Why in a tax-oriented true lease can the lessee benefit from a lowerleasing cost?

2. How does a single-investor lease differ from a leveraged lease?3. Explain how a lessor expects to recover its investment in a full payout

lease.4. How does an operating lease differ from a full payout lease?5. How is an operating lease treated for tax purposes?6. How can a corporation that cannot currently use tax benefits associ-

ated with equipment ownership because it lacks currently taxableincome or net operating loss carryforward benefits from leasing?

7. Why, if it were not for the different tax treatment for owning and leasingequipment, would the costs be identical in an efficient capital market?

8. Explain why the cost of a true lease depends on the size of the transac-tion and whether the lease is tax-oriented or non-tax-oriented.

9. A frequently cited advantage for leasing is that it conserves workingcapital. The validity of this advantage for financially sound firms dur-ing normal economic conditions is questionable. Explain why.

10. Why do chief financial officers generally prefer that lease agreements bestructured as an operating lease for financial accounting purposes?

11. Critically evaluate the claim that by leasing, a corporation can avoidthe risk of obsolescence of equipment and the risk of disposal of theequipment.

12. Who are corporate lessors?13. Explain the role of lease brokers and financial advisers in a lease trans-

action.14. a. What is a master lease?

b. What is a sale-and-leaseback transaction?15. a. For financial reporting purposes, what determines if a lease is treated

as an operating lease or capital lease?b. If a lease for equipment that has a 15-year expected economic life

has a lease term of two years, how will the lease be treated forfinancial reporting purposes?

27-Equipment Leasing Page 914 Wednesday, June 4, 2003 12:07 PM

Equipment Leasing 915

c. If a lease for equipment allows the lessee to buy the equipment atthe end of the lease term for $1, how will the lease be treated forfinancial reporting purposes?

16. For tax reporting purposes, explain why a purchase option based onfair market value rather than a nominal purchase option is a strongindication of intent to create a lease rather than a conditional sale lease.

17. Explain why when structuring a tax-oriented lease transaction, corpo-rations requiring the use of equipment will seek to have the leasetreated as an operating lease for financial reporting purposes but as atrue lease for tax purposes.

18. What is a synthetic lease?19. The Mishthosi Company is considering the acquisition of a machine

that costs $50,000 if bought today. The company can buy or leasethe machine. If it buys the machine, the machine would be depreci-ated as a 3-year MACRS asset and is expected to have a salvagevalue of $1,000 at the end of the 5-year useful life. If leased, thelease payments are $12,000 each year for four years, payable at thebeginning of each year. The marginal tax rate of Mishthosi is 30%and its cost of capital is 10%. Assume that the lease is a net lease,that any tax benefits are realized in the year of the expense, and thatthere is no investment tax credit.

MACRS rates of depreciation on a 3-year asset are:

a. Calculate the depreciation for each year in the case of the pur-chase of this machine.

b. Calculate the direct cash flows from leasing initially and for eachof the five years.

c. Calculate the adjusted discount rate.d. Calculate the value of the lease.

20. The Mietet Company is considering the acquisition of a machine thatcosts $1 million if bought today. The company can buy or lease themachine. If it buys the machine, the machine would be depreciatedas a 3-year MACRS asset and is expected to have a salvage value of$10,000 at the end of the 5-year useful life. If leased, the lease pay-ments are $250,000 each year for four years, payable at the begin-ning of each year. Mietet’s marginal tax rate is 35% and the cost ofcapital is 12%. Use the MACRS rates as provided in Problem 1.

Year Rate

1 33.33%2 44.45%3 14.81%4 7.41%

27-Equipment Leasing Page 915 Wednesday, June 4, 2003 12:07 PM

916 SELECTED TOPICS IN FINANCIAL MANAGEMENT

Assume that the lease is a net lease, that any tax benefits are realizedin the year of the expense, and that there is no investment tax credit.a. Calculate the depreciation for each year in the case of the purchase

of this machine.b. Calculate the direct cash flows from leasing initially and for each of

the five years.c. Calculate the adjusted discount rate.d. Calculate the value of the lease.

21. The Rendilegping Company is considering the acquisition of amachine that costs $100,000 if bought today. The company can buyor lease the machine. If it buys the machine, the machine would bedepreciated as a 3-year MACRS asset and is expected to have a sal-vage value of $5,000 at the end of the 5-year useful life. If leased,the lease payments are $24,000 each year for four years, payable atthe beginning of each year. The marginal tax rate of the Rendileg-ping Company is 30% and the cost of capital is 15%. Use theMACRS rates as provided in Question 19 and assume that the leaseis a net lease, that any tax benefits are realized in the year of theexpense, and that there is no investment tax credit.a. Calculate the depreciation for each year in the case of the pur-

chase of this machine.b. Calculate the direct cash flows from leasing initially and for each

of the five years.c. Calculate the adjusted discount rate.d. Calculate the value of the lease.e. Calculate the amortization of the equivalent loan.

22. The Arrende Corporation is considering the acquisition of a machinethat costs $73,000 if bought today. The company can buy or lease themachine. If it buys the machine, the machine would be depreciatedusing the straight-line method, depreciating the full asset cost over fiveyears, and is expected to have a salvage value of $2,000 at the end ofthe 5-year useful life. If leased, the lease payments are $17,500 eachyear for four years, payable at the beginning of each year. Arrende’smarginal tax rate is 38% and the appropriate cost of capital is 10%.Assume that the lease is a net lease, that any tax benefits are realized inthe year of the expense, and that there is no investment tax credit.a. Calculate the depreciation for each year in the case of the pur-

chase of this machine.b. Calculate the direct cash flows from leasing initially and for each

of the five years.c. Calculate the adjusted discount rate.d. Calculate the value of the lease.e. Calculate the amortization of the equivalent loan.

27-Equipment Leasing Page 916 Wednesday, June 4, 2003 12:07 PM

CHAPTER 28

917

Project Financing

tructured financing is a debt obligation that is backed by the value ofan asset or credit support provided by a third party. In Chapter 26

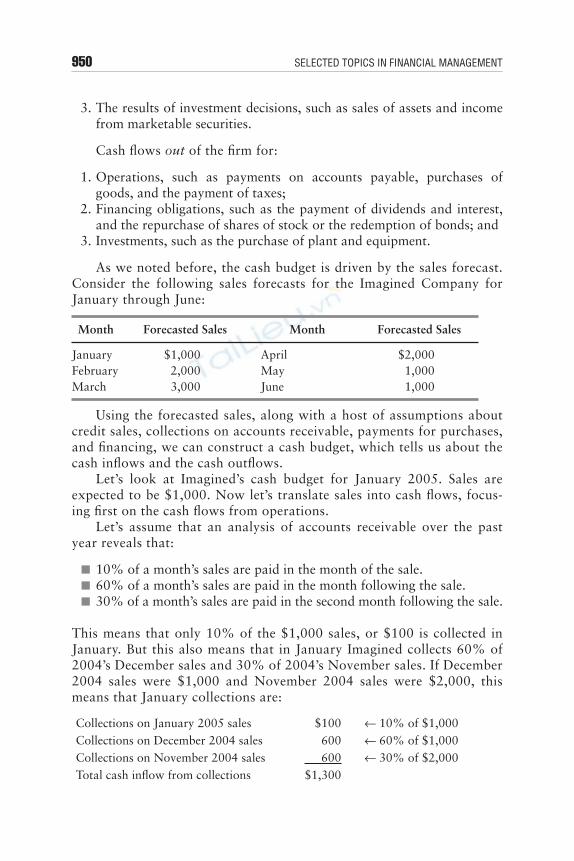

we described one form of structured finance transaction—asset securiti-zation. The key in an asset securitization is to remove the assets (i.e.,loans and receivables) from the balance sheet of an entity. Recall thatthe special purpose vehicle (SPV) is the entity that acquires the asset andsells the securities to purchase the assets.1 Structured finance is also usedby corporations to fund major projects so that the lenders look to thecash flow from the project being financed rather than corporation orcorporations seeking funding. This financing technique is called projectfinancing (or project finance) and uses the SPV to accomplish its financ-ing objectives. Both project financing and asset securitization use SPVs,yet project financing involves cash flows from operating assets, whereasasset securitization involves cash flows from financial assets, such loansor as receivables.

Industries engaged in the production, processing, transportation oruse of energy have been particularly attracted to project financing tech-niques because of the needs of such companies for new capital sources.Enterprises located in countries privatizing state-owned companies havemade extensive use of project financing.

In this chapter we look at the basic features of project financing.Discussions associated with project financing tend to focus on largecomplex projects. This might lead one to the conclusion that the projectfinancing principles discussed in this chapter have little application tosmaller, more ordinary financings. This is not the case. The same princi-ples used to finance a major pipeline, copper mine, or a power plant canbe used to finance a cannery, a hotel, a ship, or a processing plant.

1 Another name for the SPV is the special purpose entity, or SPE.

S

28-Project financing Page 917 Wednesday, April 30, 2003 12:20 PM

918 SELECTED TOPICS IN FINANCIAL MANAGEMENT

The use of project financing, and the use of an SPV to accomplish it,have been under attack by the press and some legislative leaders. Thisattack is the result of the bankruptcy of Enron in 2002. Enron usedproject financing in a manner that made little economic sense and purelyas a means for avoiding disclosing information to shareholders andcreditors. At the end of this chapter, we discuss the impact of Enron’sbankruptcy on the use of project financing by corporations.

WHAT IS PROJECT FINANCING?

Although the term “project financing” has been used to describe alltypes of financing of projects, both with and without recourse, the termhas evolved in recent years to have a more precise definition:

A financing of a particular economic unit in which alender is satisfied to look initially to the cash flows andearnings of that economic unit as the source of funds fromwhich a loan will be repaid and to the assets of the eco-nomic unit as collateral for the loan.2

A key word in the definition is “initially.” While a lender may bewilling to look initially to the cash flows of a project as the source offunds for repayment of the loan, the lender must also feel comfortablethat the loan will in fact be paid on a worst case basis. This may involveundertakings or direct or indirect guarantees by third parties who aremotivated in some way to provide such guarantees.

Project financing has great appeal when it does not have a substan-tial impact on the balance sheet or the creditworthiness of the sponsor-ing entity. Boards of directors are receptive to proceeding with projectswhich can be very highly leveraged or financed entirely or substantiallyon their own merits.

The moving party in a project is its promoter or sponsor. A projectmay have one or several sponsors. The motivation of construction com-panies acting as sponsors is to profit in some way from the constructionor operation of the project. The motivation of operating companies forsponsoring a project may be simply to make a profit from selling theproduct produced by the project. In many instances the motivation forthe project is to provide processing or distribution of a basic product ofthe sponsor or to ensure a source of supply vital to the sponsor’s business.

2 Peter K. Nevitt and Frank J. Fabozzi, Project Financing: Seventh Edition (London:Euromoney, 2001), p. 1.

28-Project financing Page 918 Wednesday, April 30, 2003 12:20 PM

Project Financing 919

The ultimate goal in project financing is to arrange a borrowing fora project which will benefit the sponsor and at the same time be com-pletely non-recourse to the sponsor, in no way affecting its credit stand-ing or balance sheet. One way this can be accomplished is by using thecredit of a third party to support the transaction. Such a third party thenbecomes a sponsor. However, projects are rarely financed independentlyon their own merits without credit support from sponsors who are inter-ested as third parties and who will benefit in some way from the project.

There is considerable room for disagreement between lenders andborrowers as to what constitutes a feasible project financing. Borrowersprefer their projects to be financed independently off-balance sheet withappropriate disclosures in financial reports indicating the exposure ofthe borrower to a project financing. Lenders, on the other hand, are notin the venture capital business. They are not equity risk takers. Lenderswant to feel secure that they are going to be repaid either by the project,the sponsor, or an interested third party. Therein lies the challenge ofmost project financings.

The key to a successful project financing is structuring the financingof a project with as little recourse as possible to the sponsor while at thesame time providing sufficient credit support through guarantees orundertakings of a sponsor or third party, so that lenders will be satisfiedwith the credit risk.

There is a popular misconception that project financing means off-balance sheet financing to the point that the project is completely self-supporting without guarantees or undertakings by financially responsibleparties. This leads to misunderstandings by prospective borrowers whoare under the impression that certain kinds of projects may be financedas stand-alone, self-supporting project financings and, therefore, proceedon the assumption that similar projects in which they are interested canbe financed without recourse to the sponsor, be off-balance sheet to thesponsor, and be without any additional credit support from a financiallyresponsible third party.

It would be a happy circumstance if it were possible simply to arrangea 100% loan for a project (non-recourse to sponsors) which looked asthough it would surely be successful on the basis of optimistic financialprojections. Unfortunately, this is not the case. There is no magic aboutproject financing. Such a financing can be accomplished by financial engi-neering which combines the undertakings and various kinds of guaranteesby parties interested in a project being built in such a way that none of theparties alone has to assume the full credit responsibility for the project, yetwhen all the undertakings are combined and reviewed together, the equiv-alent of a satisfactory credit risk for lenders has resulted.

28-Project financing Page 919 Wednesday, April 30, 2003 12:20 PM

920 SELECTED TOPICS IN FINANCIAL MANAGEMENT

REASONS FOR JOINTLY OWNED OR SPONSORED PROJECTS

There has been an increasing trend towards jointly owned or controlledprojects. Although most corporations prefer sole ownership and controlof a major project, particularly projects involving vital supplies and dis-tribution channels, there are factors that encourage the formation ofjointly owned or controlled projects that consist of partners withmutual goals, talents, and resources. These factors include:3

■ The undertaking is beyond a single corporation’s financial and/or man-agerial resources.

■ The partners have complementary skills.

■ Economics of a large project lower the cost of the product or servicesubstantially over the possible cost of a smaller project if the partnersproceeded individually.

■ The risks of the projects are shared.

■ One or more of the partners can use the tax benefits (i.e., depreciationand any tax credit).

■ Greater debt leverage can be obtained.

The joint sponsors will select the legal form of the SPV (corpora-tion, partner, limited partnership, limited liability company, contractualjoint venture, or trust) that will be satisfy their tax and legal objectives.

CREDIT EXPOSURES IN A PROJECT FINANCING

To place a project financing into perspective, it is helpful to review thedifferent credit exposures that occur at different times in the course of atypical project financing.

Risk PhasesProject financing risks can be divided into three time frames in whichthe elements of credit exposure assume different characteristics:

■ engineering and construction phase

■ start-up phase

■ operations according to planned specifications

3 Nevitt and Fabozzi, Project Financing, Seventh Edition, p. 265.

28-Project financing Page 920 Wednesday, April 30, 2003 12:20 PM

Project Financing 921

Different guarantees and undertakings of different partners may be usedin each time frame to provide the credit support necessary for structur-ing a project financing.

Engineering and Construction PhaseProjects generally begin with a long period of planning and engineering.Equipment is ordered, construction contracts are negotiated, and actualconstruction begins. After commencement of construction, the amountat risk begins to increase sharply as funds are advanced to purchasematerial, labor, and equipment. Interest charges on loans to finance con-struction also begin to accumulate.

Start-Up PhaseProject lenders do not regard a project as completed on conclusion ofthe construction of the facility. They are concerned that the plant orfacility will work at the costs and to the specifications which wereplanned when arranging the financing. Failure to produce the productor service in the amounts and at the costs originally planned means thatthe projections and the feasibility study are incorrect and that there maybe insufficient cash to service debt and pay expenses.

Project lenders regard a project as acceptable only after the plant orfacility has been in operation for a sufficient period of time to ensurethat the plant will in fact produce the product or service at the price, inthe amounts, and to the standards assumed in the financial plan whichformed the basis for the financing. This start-up risk period may runfrom a few months to several years.

Operations According to SpecificationOnce the parties are satisfied that the plant is running to specification,the final operating phase begins. During this phase, the project begins tofunction as a regular operating company. If correct financial planningwas done, revenues from the sale of the product produced or serviceperformed should be sufficient to service debt—interest and principal—pay operating costs, and provide a return to sponsors and investors.

Different Lenders for Different Risk PeriodsSome projects are financed from beginning to end with a single lender orsingle group of lenders. However, most large projects employ differentlenders or groups of lenders during different risk phases. This is becauseof the different risks involved as the project facility progresses through

28-Project financing Page 921 Wednesday, April 30, 2003 12:20 PM

922 SELECTED TOPICS IN FINANCIAL MANAGEMENT

construction to operation, and the different ability of lenders to copewith and accept such risks.

Some lenders like to lend for longer terms and some prefer short-termlending. Some lenders specialize in construction lending and are equippedto monitor engineering and construction of a project, some are not. Somelenders will accept and rely on guarantees of different sponsors during theconstruction, start-up or operation phases, and some will not. Some lend-ers will accept the credit risk of a turn-key operating project, but are notinterested in the high-risk lending during construction and start-up.

Interest rates will also vary during the different risk phases ofproject financing and with different credit support from sponsors duringthose time periods.

Short-term construction lenders are very concerned about the avail-ability of long-term “take out” financing by other lenders upon comple-tion of the construction or start-up phase. Construction lenders live infear of providing their own unplanned take out financing. Consequently,from the standpoint of the construction lender, take out financingshould be in place at the outset of construction financing.

KEY ELEMENTS OF A SUCCESSFUL PROJECT FINANCING

There are several elements that both sponsors and lenders to a projectfinancing should review in order to increase the likelihood that a projectfinancing will be successful. The key ones are listed below:4

■ A satisfactory feasibility study and financial plan should be preparedwith realistic assumptions regarding future inflation rates and interestrates.

■ The cost of product or raw materials to be used by the project is assured.

■ A supply of energy at reasonable cost has been assured.

■ A market exists for the product, commodity, or service to be produced.

■ Transportation is available at a reasonable cost to move the product tothe market.

■ Adequate communications are available.

■ Building materials are available at the costs contemplated.

■ The contractor is experienced and reliable.

■ The operator is experienced and reliable.

■ Management personnel are experienced and reliable.

■ Untested technology is not involved.

4 Nevitt and Fabozzi, Project Financing, Seventh Edition, p. 7.

28-Project financing Page 922 Wednesday, April 30, 2003 12:20 PM

Project Financing 923

■ The contractual agreement among joint venture partners, if any, is sat-isfactory.

■ The key sponsors have made an adequate equity contribution.

■ Satisfactory appraisals of resources and assets have been obtained.

■ Adequate insurance coverage is contemplated.

■ The risk of cost overruns have been addressed.

■ The risk of delay has been considered.

■ The project will have an adequate return for the equity investor.

■ Environmental risks are manageable.

When the project involves a sovereign entity, the following criticalelements are important to consider to ensure the success of a project:

■ A stable and friendly political environment exists; licences and permitsare available; contracts can be enforced; legal remedies exist.

■ There is no risk of expropriation.

■ Country risk is satisfactory.

■ Sovereign risk is satisfactory.

■ Currency and foreign exchange risks have been addressed.

■ Protection from criminal activities such as kidnaping and extortion.

■ Existence of a commercial legal system protecting property and con-tractual rights.

CAUSES FOR PROJECT FAILURES

The best way to appreciate the concerns of lenders to a project is to reviewand consider some of the common causes for project failures, whichinclude the following:5

■ Delay in completion, with consequential increase in the interestexpense on construction financing and delay in the contemplated reve-nue flow

■ Capital cost overrun

■ Technical failure

■ Financial failure of the contractor

■ Uninsured casualty losses

■ Increased price or shortages of raw material

■ Technical obsolescence of the plant or equipment

■ Loss of competitive position in the marketplace

5 Nevitt and Fabozzi, Project Financing, Seventh Edition, p. 2.

28-Project financing Page 923 Wednesday, April 30, 2003 12:20 PM

924 SELECTED TOPICS IN FINANCIAL MANAGEMENT

■ Poor management

■ Overly optimistic appraisals of the value of pledged security, such as oiland gas reserves

In addition, for projects in a foreign country, the following arecauses for project failures:

■ Government interference

■ Expropriation

■ Financial insolvency of the host government

For a project financing to be successfully achieved, these risks mustbe properly considered, monitored, and avoided throughout the life ofthe project.

CREDIT IMPACT OBJECTIVE

While the sponsor or sponsors of a project financing ideally would pre-fer that the project financing be a non-recourse borrowing which doesnot in any way affect its credit standing or balance sheet, many projectfinancings are aimed at achieving some other particular credit impactobjective, such as any one or several of the following:6

■ To avoid being shown on the face of the balance sheet

■ To avoid being shown as debt on the face of the balance sheet so as notto impact financial ratios

■ To avoid being shown in a particular footnote to the balance sheet

■ To avoid being within the scope of restrictive covenants in an indentureor loan agreement which precludes direct debt financing or leases forthe project

■ To avoid being considered as a cash obligation which would diluteinterest coverage ratios, and affect the sponsor’s credit standing withthe rating services

■ To limit direct liability to a certain period of time such as during con-struction and/or the start-up period, so as to avoid a liability for theremaining life of the project

■ To keep the project off-balance sheet during construction and/or untilthe project generates revenues

6 Nevitt and Fabozzi, Project Financing, Seventh Edition, p. 4.

28-Project financing Page 924 Wednesday, April 30, 2003 12:20 PM

Project Financing 925

Any one or a combination of these objectives maybe sufficient reasonfor a borrower to seek the structure of a project financing.

Liability for project debt for a limited time period may be accept-able in situations in which liability for such debt is unacceptable for thelife of the project. Where a sponsor cannot initially arrange long-termnon-recourse debt for its project that will not impact its balance sheet,the project may still be feasible if the sponsor is willing to assume thecredit risk during the construction and start-up phase, and providedlenders are willing to shift the credit risk to the project after the projectfacility is completed and operating. Under such an arrangement, most ofthe objectives of an off-balance sheet project financing and limitedcredit impact can be achieved after the initial risk period of constructionand start-up. In some instances, the lenders may be satisfied to rely onrevenue produced by unconditional take-or-pay contracts from users ofthe product or services to be provided by the project to repay debt.7 Inother instances, the condition of the market for the product or servicemay be such that sufficient revenues are assured after completion ofconstruction and start-up so as to convince lenders to rely on such reve-nues for repayment of their debts.

ACCOUNTING CONSIDERATIONS

Project financing is sometimes called off-balance sheet financing. How-ever, while the project debt may not be on the sponsor’s balance sheet,the project debt will appear on the face of the project balance sheet. Inany event, the purpose of a project financing is to segregate the creditrisk of the project in order that the credit risk of lending to either thesponsor or the project can be clearly and fairly appraised on theirrespective merits. The purpose is not to hide or conceal a liability of thesponsor from creditors, rating agencies, or stockholders.

Significant undertakings of sponsors and investors in projects subjectto the Financial Accounting Standards Board must usually be shown infootnotes to their financial statements if not in the statements themselves.

7 A take-or-pay contract is a long-term contract to make periodic payments over thelife of the contract in certain minimum amounts as payments for a service or a prod-uct. The payments are in an amount sufficient to service the debt needed to financethe project which provides the services or the product and to pay operating expensesof the project. The obligation to make minimum payments is unconditional and mustbe paid whether or not the service or product is actually furnished or delivered. Incontrast, a take-and-pay contract is a contact in which payment is contingent upondelivery and the obligation to pay is not unconditional.

28-Project financing Page 925 Wednesday, April 30, 2003 12:20 PM

926 SELECTED TOPICS IN FINANCIAL MANAGEMENT

Because project financings are concerned with balance sheet accountingtreatment, familiarity with accounting terms used to describe or rational-ize balance sheet reporting is important. Terms such as contingent liabil-ity, indirect liability, deferred liability, deferred expense, fixed charges,equity accounting, and materiality are used to rationalize the appropriatepositioning of entries in a sponsor’s financial statements and footnotes.Accounting rules for reporting these types of liabilities are under contin-ual review, as the accounting profession grapples with the problem ofproper and fair disclosure and presentation of objective information tostockholders, lenders, rating agencies, guarantors, government agencies,and other concerned parties.8

MEETING INTERNAL RETURN OBJECTIVES

As explained in Chapter 13, corporations set target rates of return fornew capital investments. If a proposed capital expenditure will not gen-erate a return greater than a company’s target rate, it is not regarded asa satisfactory use of capital resources. This is particularly true when acompany can make alternative capital expenditures which will producea return on capital in excess of the target rate.

Project financing can sometimes be used to improve the return onthe capital invested in a project by leveraging the investment to a greaterextent than would be possible in a straight commercial financing of theproject. This can be accomplished by locating other parties interested ingetting the project built, and shifting some of the debt coverage to suchparties through direct or indirect guarantees. An example would be anoil company with a promising coal property which it did not wish todevelop because of better alternative uses of its capital. By bringing in acompany which required the coal, such as a public utility, an indirectguarantee might be available in the form of a long-term take-or-paycontract which would support long-term debt to finance the construc-tion of the coal mine. This, in turn, would permit the oil company’sinvestment to be highly leveraged and consequently to produce a muchhigher rate of return.

8 On June 28, 2002, the Financial Accounting Standards Board (FASB) issued an ex-posure draft of a proposed interpretation of Accounting Research Bulletin No. 51,“Consolidation of Certain Special-Purpose Entities.” This exposure draft, which issubject to public comment, is an attempt to clarify the issue of whether to consolidatespecial purpose entities within the sponsor company’s financial statements.

28-Project financing Page 926 Wednesday, April 30, 2003 12:20 PM

Project Financing 927

OTHER BENEFITS OF A PROJECT FINANCING

There are often other side benefits resulting from segregating a financingas a project financing which may have a bearing on the motives of thecompany seeking such a structure. These benefits include:9

■ Credit sources may be available to the project that would not be avail-able to the sponsor.

■ Guarantees may be available to the project that would not be availableto the sponsor.

■ A project financing may enjoy better credit terms and interest costs insituations in which a sponsor’s credit is weak.

■ Higher leverage of debt to equity may be achieved. ■ Legal requirements applicable to certain investing institutions may be

met by the project but not by the sponsor. ■ Regulatory problems affecting the sponsor may be avoided. ■ For regulatory purposes, costs may be clearly segregated as a result of a

project financing. ■ Construction financing costs may not be reflected in the sponsor’s

financial statements until such time as the project begins producingrevenue.

In some instances, any one of the reasons stated above may be the pri-mary motivation for structuring a new operation as a project financing.

TAX CONSIDERATIONS

Tax benefits from any applicable tax credits, depreciation deductions,interest deductions, depletion deductions, research and development taxdeductions, dividends-received credits, foreign tax credits, capital gains,and non-capital start-up expenses are very significant considerations inthe investment, debt service, and cash flow of most project financings.Care must be used in structuring a project financing to make sure thatthese tax benefits are used. Where a project financing is housed in a newentity that does not have taxes to shelter, it is important to structure theproject financing so that any tax benefits can be transferred to parties ina position currently able to use such tax benefits.

For U.S. federal income tax purposes, 80% control is required fortax consolidation, except in the case of certain foreign subsidiaries, inwhich 50% control may require consolidation.

9 Nevitt and Fabozzi, Project Financing, Seventh Edition, p. 6.

28-Project financing Page 927 Wednesday, April 30, 2003 12:20 PM

928 SELECTED TOPICS IN FINANCIAL MANAGEMENT

DISINCENTIVES TO PROJECT FINANCING

Project financings are complex. The documentation tends to be compli-cated, and the cost of borrowing funds may be higher than conventionalfinancing. If the undertakings of a number of parties are necessary tostructure the project financing, or if a joint venture is involved, the nego-tiation of the original financing agreements and operating agreements willrequire patience, forbearing, and understanding. Decision making in part-nerships and joint ventures is never easy, since the friendliest of partnersmay have diverse interests, problems, and objectives. However, therewards and advantages of a project financing will often justify the specialproblems that may arise in structuring and operating the project.

ENRON’S EFFECT ON PROJECT FINANCING

Because of Enron’s use of project financing, concerns have been expressedover the use of this method of financing. Unfortunately, attacks on projectfinancing that were reported in the press and concerns expressed by mem-bers of Congress simply failed to recognize that what Enron did had verylittle to do with traditional project financing. Enron used partnerships asits legal entity in project financing and these partnerships had little of thecharacteristics of a project financing described in this chapter. Instead,according to Barry Gold, a managing director at Salomon Smith Barney,the project financings used by Enron were an “attempt to unduly benefitfrom accounting, tax, and disclosure requirements and definitions.”10

In a project financing, there is transparency about the economics ofthe project. The project lenders are well informed of the risks and arefurnished the financial projections and economic analysis along with theassumptions. In general, there is more information provided in a projectfinancing than there is in a typical corporate bond prospectus. All par-ties to a project financing can perform due diligence and raise questionswith the sponsor. In contrast, in the project financings of Enron, thefirm’s shareholders and creditor did not have enough information toundertake due diligence.

While project financing as discussed in this chapter had nothing to dowith the use of off-balance sheet SPVs utilized by Enron, there have beensome changes in the market. As a result of the Enron bankruptcy, majorcorporate users of project financing are providing even more disclosure

10 Henry A. Davis, “How Enron Has Affected Project Finance,” The Journal ofStructured and Project Finance (Spring 2002), p. 19.

28-Project financing Page 928 Wednesday, April 30, 2003 12:20 PM

Project Financing 929

about projects.11 What management will want to be sure of is that anyproject financings that are treated as off-balance sheet are truly non-recourse to the sponsor. If there is potential recourse to the sponsor thatmay be significant in nature, management should report the project financ-ing on the balance sheet. That is, the debt of the project should be treatedas a liability and the value of the project should be treated as an asset.

In concluding his analysis of the use of project finance after Enron,Henry Davis, managing editor of The Journal of Structured and ProjectFinance, writes:

... project finance is alive and well. We just need to reminda few people of its basic fundamentals. Neither projectfinance nor sensible innovations in structured finance withsound, well-explained business reasons have been shakenby Enron. The principal lessons learned from the Enrondebacle have to do with transparency and disclosure.When some of your businesses or your financing structuresbecome hard to explain, you may begin to questionwhether they make sense in the first place.12

SUMMARY

■ In a project financing or project finance, lenders initially look to thecash flow from the project being financed rather than the corporationor corporations seeking funding. The moving party in a project is itspromoter or sponsor.

■ The ultimate goal in project financing is to arrange a borrowing for aproject which will benefit the sponsor and, at the same time, be com-pletely non-recourse to the sponsor, in no way affecting its creditstanding or balance sheet. This can be accomplished by using thecredit of a third party to support the transaction. However, projectsare typically not financed independently on their own merits withoutcredit support from sponsors who are interested third parties whowill benefit in some way from the project.

■ Although most corporations prefer sole ownership and control of amajor project, there are several factors that encourage the formation ofjointly owned or controlled projects. Joint sponsors will select the legalform of the SPV that will satisfy their tax and legal objectives.

11 Davis, “How Enron Has Affected Project Finance.”12 Davis, “How Enron Has Affected Project Finance,” p. 25.

28-Project financing Page 929 Wednesday, April 30, 2003 12:20 PM

930 SELECTED TOPICS IN FINANCIAL MANAGEMENT

■ There are three time frames that are associated with the risk of aproject financing: (1) engineering and construction phase, (2) start-upphase, and (3) operations according to planned specifications. Differ-ent guarantees and undertakings of different partners may be used ineach time frame to provide the credit support necessary for structur-ing a project financing. Most large projects employ different lendersor groups of lenders because of the different risks involved as theproject facility progresses through construction to operation, and thedifferent ability of lenders to cope with and accept such risks.

■ For a project financing to be successfully achieved, the risks associatedwith a project must be understood and monitored throughout the lifeof the project.

QUESTIONS

1. What types of industries have been engaged in project financing?2. Why do lenders in a project financing look very closely at the

project’s expected cash flows?3. Comment on the following statement: “The sole purpose of a project

financing is to provide the sponsors with off-balance sheet financing.”4. What are the advantages of a jointly sponsored project financing?5. The key to a project financing is to finance a project with as little

recourse to the sponsor as possible. Explain why.6. Comment on the following statement: “Project financing means off-

balance sheet financing to the point that the project is completelyself-supporting without guarantees or undertakings by financiallyresponsible parties.”

7. What types of risk are associated with the following phases of aproject financing:a. engineering and construction phase?b. start-up phase?c. operations according to planned specifications?

8. For most large projects there are different lenders or groups of lend-ers during different risk phases. Explain why.

9. What is the concern of short-term construction lenders to a projectfinancing?

10. Identify some important factors that a company considering aproject financing in another country should consider.

11. Identify some of the common causes for project failures.12. What are some of the ways that a project financing can be used to

improve the return on the capital invested in a project?

28-Project financing Page 930 Wednesday, April 30, 2003 12:20 PM

Project Financing 931

13. Identify some of the motives for a project financing.14. Comment on the following statement: “Enron Corporation used

project financing and got itself into a lot of trouble. Enron is a per-fect example of why project financing and special purpose vehiclesshould not be used by reputable firms.”

28-Project financing Page 931 Wednesday, April 30, 2003 12:20 PM

28-Project financing Page 932 Wednesday, April 30, 2003 12:20 PM

CHAPTER 29

933

Strategy and Financial Planning

business that maximizes its owners’ wealth allocates its resourcesefficiently, resulting in an efficient allocation of resources for society

as a whole. Owners, employees, customers, and anyone else who has astake in the business enterprise are all better off when its managersmake decisions that maximize the value of the firm.

Just as there may be alternative routes to a destination, there may bealternative ways to maximize owners’ wealth. A strategy is a sense ofhow to reach an objective such as maximizing wealth. And just as someroutes may get you where you are going faster, some strategies may bebetter than others.

Suppose a firm has decided it has an advantage over its competitorsin marketing and distributing its products in the global market. Thefirm’s strategy may be to expand into European market, followed by anexpansion into the Asian market. Once the firm has its strategy, it needsa plan, in particular the strategic plan, which is the set of actions thefirm intends to use to follow its strategy.

The investment opportunities that enable the firm to follow its strat-egy comprise the firm’s investment strategy. The firm may pursue itsstrategy of expanding into European and Asian markets by either estab-lishing itself or acquiring businesses already in these markets. This iswhere capital budgeting analysis comes in: We evaluate the possibleinvestment opportunities to see which ones, if any, provide a returngreater than necessary for the investment’s risk. And let’s not forget theinvestment in working capital, the resources the firm needs to supportits day-to-day operations.

Suppose as a result of evaluating whether to establish or acquirebusinesses, our firm decides it is better—in terms of maximizing thevalue of the firm—to acquire selected European businesses. The next

A

29-Strategy_FinancialPlan Page 933 Wednesday, April 30, 2003 12:19 PM

934 SELECTED TOPICS IN FINANCIAL MANAGEMENT

step is to figure out how it is going to pay for these acquisitions. Thefinancial managers must make sure that the firm has sufficient funds tomeet its operating needs, as well as its investment needs. This is wherethe firm’s financing strategy enters the picture. Where should the fundsneeded come from? What is the precise timing of the needs for funds?To answer these questions, working capital management (in particular,short-term financing) and the capital structure decision (the mix of long-term sources of financing) enters the picture.

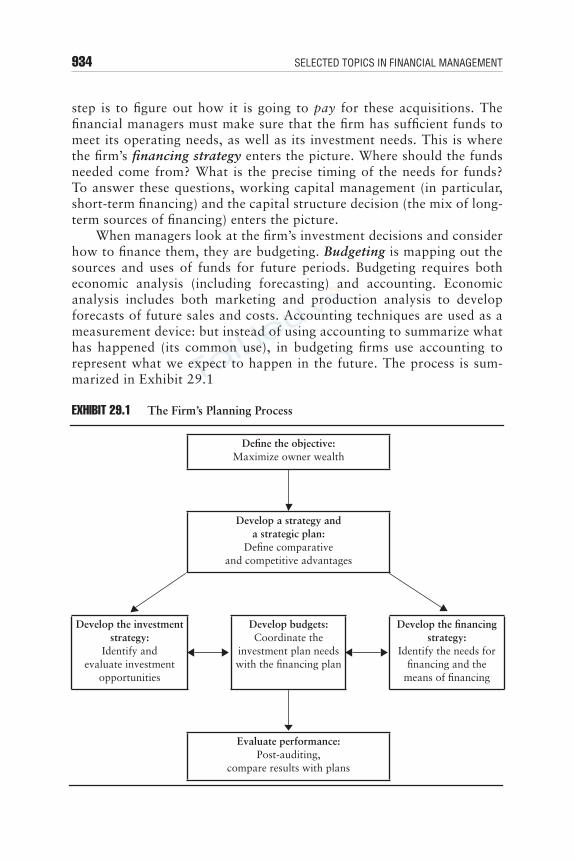

When managers look at the firm’s investment decisions and considerhow to finance them, they are budgeting. Budgeting is mapping out thesources and uses of funds for future periods. Budgeting requires botheconomic analysis (including forecasting) and accounting. Economicanalysis includes both marketing and production analysis to developforecasts of future sales and costs. Accounting techniques are used as ameasurement device: but instead of using accounting to summarize whathas happened (its common use), in budgeting firms use accounting torepresent what we expect to happen in the future. The process is sum-marized in Exhibit 29.1

EXHIBIT 29.1 The Firm’s Planning Process

Define the objective:Maximize owner wealth

Develop a strategy anda strategic plan:

Define comparativeand competitive advantages

Develop the investmentstrategy:

Identify andevaluate investment

opportunities

Develop budgets:Coordinate the

investment plan needswith the financing plan

Develop the financingstrategy:

Identify the needs forfinancing and the

means of financing

Evaluate performance:Post-auditing,

compare results with plans

29-Strategy_FinancialPlan Page 934 Wednesday, April 30, 2003 12:19 PM

Strategy and Financial Planning 935

Once these plans are put into effect, they must compare what hap-pens with what was planned. This is referred to as post-auditing, whichfirms use to:

■ evaluate the performance of management,

■ analyze any deviations of actual results from planned results, and

■ evaluate the planning process to determine just how good it is.

STRATEGY

“Whilst every man is free to employ his capital where he pleases, he willnaturally seek for it that employment which is most advantageous; hewill naturally be dissatisfied with a profit of 10 per cent, if by removinghis capital he can obtain a profit of 15 per cent.”David Ricardo, The Principles of Political Economy and Taxation (Lon-don, 1817).

The way to create wealth from investments is to invest in projects thathave positive net present values. But where do these positive net presentvalues come from? From the firm’s comparative advantage or its com-petitive advantages.

Comparative and Competitive AdvantagesA comparative advantage is the advantage one firm has over others interms of the cost of producing or distributing goods or services. For exam-ple, Wal-Mart Stores, Inc. had for years a comparative advantage over itscompetitors (such as K Mart) through its vast network of warehouses andits distribution system. Wal-Mart invested in a system of regional ware-houses and its own trucking system. Combined with bulk purchases and aunique customer approach (such as its “greeters”), Wal-Mart’s compara-tive advantages in its warehousing and distribution systems helped it growto be a major (and very profitable) retailer in a very short span of time.However, as with most comparative advantages, it took competitors a fewyears to catch up and for Wal-Mart’s advantage to disappear.

A competitive advantage is the advantage one firm has over anotherbecause of the structure of the markets, input and output markets, theyboth operate in. For example, one firm may have a competitive advan-tage due to barriers to other firms entering the same market. This hap-pens in the case of governmental regulations that limit the number offirms in a market, as with banks, or in the case of governmental grantedmonopolies. A firm itself may create barriers to entry (although with the

29-Strategy_FinancialPlan Page 935 Wednesday, April 30, 2003 12:19 PM

936 SELECTED TOPICS IN FINANCIAL MANAGEMENT

help of the government) that include patents and trademarks.NutraSweet Company, a unit of Monsanto Company, had the exclusivepatent on the artificial sweetener, aspartame, which it marketed underthe brand name, NutraSweet. However, this patent expired December14, 1992. The loss of the monopoly on the artificial sweetener reducedthe price of aspartame from $70 per pound to $20–35 per pound, sinceother firms could produce and sell aspartame products starting Decem-ber 15, 1992.1,2

NutraSweet had a competitive advantage as long as it had thepatent. But as soon this patent expired, this competitive advantage waslost and competitors were lining up to enter the market.

Only by having some type of advantage can a firm invest in some-thing and get more back in return. So first you have to figure out whereyour firm has a comparative or competitive advantage before you candetermine your firm’s strategy.

Strategy and Owners’ Wealth MaximizationOften firms conceptualize a strategy in terms of the consumers of thefirm’s goods and services. For example, you may have a strategy tobecome the world’s leading producer of microcomputer chips by pro-ducing the best quality chip or by producing chips at the lowest cost,developing a cost (and price) advantage over your competitors. So yourfocus is on product quality and cost. Is this strategy in conflict withmaximizing owners’ wealth? No.

To maximize owners’ wealth, we focus on the returns and risks offuture cash flows to the firm’s owners. And we look at a project’s netpresent value when we make decisions regarding whether or not toinvest in it. A strategy of gaining a competitive or comparative advan-tage is consistent with maximizing shareholder wealth. This is becauseprojects with positive net present value arise when the firm has a com-petitive or comparative advantage over other firms.

Suppose a new piece of equipment is expected to generate a returngreater than what is expected for the project’s risk (its cost of capital).But how can a firm create value simply by investing in a piece of equip-ment? How can it maintain a competitive advantage? If investing in thisequipment can create value, wouldn’t the firm’s competitors also wantthis equipment? Of course—if they could use it to create value, theywould surely be interested in it.

1 Lois Therrien, Patrick Oster, and Chuck Hawkins, “How Sweet It Isn’t At Nutra-Sweet,” Business Week (December 14, 1992), p. 42.2 Monsanto sold its sweetener division in 2000.

29-Strategy_FinancialPlan Page 936 Wednesday, April 30, 2003 12:19 PM

Strategy and Financial Planning 937

Now suppose that the firm’s competitors face no barriers to buying theequipment and exploiting its benefits. What will happen? The firm and itscompetitors will compete for the equipment, bidding up its price. Whendoes it all end? When the net present value of the equipment is zero.

Now suppose instead that the firm has a patent on the new piece ofequipment and can thus keep its competitors from exploiting the equip-ment’s benefits. Then there would be no competition for the equipmentand the firm would be able to exploit it to increase its owners’ wealth.

Consider an example where trying to gain a comparative advantagewent wrong. Schlitz Brewing Company attempted to reduce its costs togain an advantage over its competitors: It reduced its labor costs andshortened the brewing cycle. Reducing costs allow it to reduce its pricesbelow competitors’ prices. But product quality suffered—so much thatSchlitz lost market share, instead of gaining it.

Schlitz attempted to gain a comparative advantage, but was not trueto a larger strategy to satisfy its customers—who apparently wantedquality beer more than they wanted cheap beer. And the loss of marketshare was reflected in Schlitz’s declining stock price.3

Value can only be created when the firm has a competitive or compara-tive advantage. If a firm analyzes a project and determines that it has a posi-tive net present value, the first question should be: Where did it come from?

FINANCIAL PLANNING AND BUDGETING

“As certainly as financial planning centers about commitments and utili-zation of capital, the protective function of management is also germaneto the process. This function comprehends the integrity of capital, theprofitable survival of the business entity, and the safe-guarding of therights of the capital contributors,” Paul M. Van Arsdell, CorporationFinance (New York: The Ronald Press Company, 1968), p. 550.

A strategy is the direction a firm takes to meet its objective. A strategicplan is how a firm intends to go in that direction. In financial manage-ment, a strategic investment plan includes policies to seek out possibleinvestment opportunities: Do we spend more on research and develop-ment? Do we look globally? Do we attempt to increase market share?

A strategic plan also includes resource allocation. If a firm intendsto expand, where does it get the capital to do so? If a firm requires more

3 The case of Schlitz Brewing is detailed in George S. Day and Liam Fahey in “PuttingStrategy into Shareholder Value Analysis,” Harvard Business Review (March–April1990), pp. 156–162.

29-Strategy_FinancialPlan Page 937 Wednesday, April 30, 2003 12:19 PM

938 SELECTED TOPICS IN FINANCIAL MANAGEMENT

capital, the timing, amount, and type of capital (whether equity or debt)comprise elements of a firm’s financial strategic plan. These things mustbe planned to implement the strategy.

Financial planning allocates a firm’s resources to achieve its invest-ment objectives. Financial planning is important for several reasons.

First, financial planning helps managers assess the impact of a par-ticular strategy on their firm’s financial position, its cash flows, itsreported earnings, and its need for external financing.

Second, by formulating financial plans, the firm’s management is ina better position to react to any changes in market conditions, such asslower than expected sales, or unexpected problems, such as a reductionin the supply of raw materials. By constructing a financial plan, manag-ers become more familiar with the sensitivity of the firm’s cash flowsand its financing needs to changes in sales or some other factor.

Third, creating a financial plan helps managers understand the trade-offs inherent in its investment and financing plans. For example, by devel-oping a financial plan, the financial manager is better able to understandthe tradeoff that exists between having sufficient inventory to satisfy cus-tomer demands and the need to finance the investment in inventory.

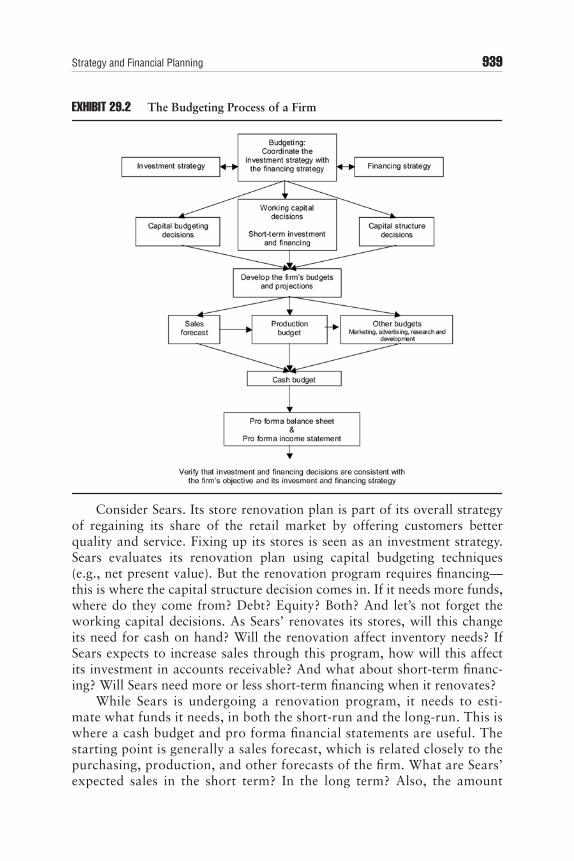

Financial planning consists of the firm’s investment and financingplans. Once we know the firm’s investment plan, we need to figure outwhen funds are needed and where they will come from. We do this bydeveloping a budget,4 which is basically the firm’s investment and financ-ing plans expressed in dollar terms. A budget can represent details suchas what to do with cash in excess of needs on a daily basis, or it canreflect broad statements of a firm’s business strategy over the nextdecade. Exhibit 29.2 illustrates the budgeting process.

Budgeting for a short-term (less than a year) is usually referred to asoperational budgeting; budgeting for the long-term (typically three to fiveyears ahead) is referred to as long-run planning or long-term planning.But since long-term planning depends on what is done in the short-term,the operational budgeting and long-term planning are closely related.

The budgeting process involves putting together the financing andinvestment strategy into terms that allow the financial manager to deter-mine what investments can be made and how these investments should befinanced. In other words, budgeting pulls together decisions regarding capi-tal budgeting, capital structure, and working capital. Managers preparebudgets by preparing financial statements that represent these decisions.

4 The term “budget” originates from the French bouge, meaning a bag and its con-tents. We use the term budget to refer to the allocation of a firm’s resources (in dol-lars) over future periods. The bag is therefore the firm; its contents are the firm’sresources, its funds.

29-Strategy_FinancialPlan Page 938 Wednesday, April 30, 2003 12:19 PM

Strategy and Financial Planning 939

EXHIBIT 29.2 The Budgeting Process of a Firm

Consider Sears. Its store renovation plan is part of its overall strategyof regaining its share of the retail market by offering customers betterquality and service. Fixing up its stores is seen as an investment strategy.Sears evaluates its renovation plan using capital budgeting techniques(e.g., net present value). But the renovation program requires financing—this is where the capital structure decision comes in. If it needs more funds,where do they come from? Debt? Equity? Both? And let’s not forget theworking capital decisions. As Sears’ renovates its stores, will this changeits need for cash on hand? Will the renovation affect inventory needs? IfSears expects to increase sales through this program, how will this affectits investment in accounts receivable? And what about short-term financ-ing? Will Sears need more or less short-term financing when it renovates?

While Sears is undergoing a renovation program, it needs to esti-mate what funds it needs, in both the short-run and the long-run. This iswhere a cash budget and pro forma financial statements are useful. Thestarting point is generally a sales forecast, which is related closely to thepurchasing, production, and other forecasts of the firm. What are Sears’expected sales in the short term? In the long term? Also, the amount

29-Strategy_FinancialPlan Page 939 Wednesday, April 30, 2003 12:19 PM

940 SELECTED TOPICS IN FINANCIAL MANAGEMENT

that Sears expects to sell affects its purchases, sales personnel, andadvertising forecasts. Putting together forecasts requires cooperationamong Sears’ marketing, purchasing, and financial management.

Once Sears has its sales and related forecasts, the next step is a cashbudget, detailing the cash inflows and outflows each period. Once thecash budget is established, pro forma balance sheet and income state-ments can be constructed. Following this, Sears must verify that its bud-get is consistent with its objective and its strategies.

Budgeting generally begins four to six months prior to the end of thecurrent fiscal period. Most firms have a set of procedures that must be fol-lowed in compiling the budget. The budget process is usually managed byeither a Vice-President to Planning, the Director of the Budget, the Vice-President of Finance, the Chief Financial Officer, or the Corporate Con-troller. Each division or department provides its own budgets that are thenmerged into a firm’s centralized budget by the manager of the budget.

A budget looks forward and backward. It identifies resources the firmwill generate or need in the near- and long-term, and it serves as a measureof the current and past performance of departments, divisions, or individ-ual managers. But we have to be careful when we measure deviationsbetween budgeted and actual results. We must separately identify devia-tions that were controllable from deviations that were uncontrollable. Forexample, suppose we develop a budget expecting $10 million sales from anew product. If actual sales turn out to be $6 million, do we interpret thisresult as poor performance on the part of management? Maybe, maybenot. If the lower-than-expected sales are due to an unexpected downturnin the economy, probably not. But yes, if they are due to what turns out tobe obviously poor management forecasts of consumer demand.

Sales ForecastingSales forecasts are an important part of financial planning. Inaccurateforecasts can result in shortages of inventory, inadequate short-termfinancing arrangements, and so on.

If a firm’s sales forecast misses its mark, either understating or overstat-ing sales, there are many potential problems. Consider Coleco Industries,which missed its mark. This company introduced a toy product in 1983, itsCabbage Patch doll, which enjoyed runaway popularity. In fact, this dollwas so popular, that Coleco could not keep up with demand. It was in suchdemand and inventory so depleted that fights broke out in toy stores, someparents bribed store personnel to get scarce dolls just before Christmas, andfake dolls were being smuggled into the country.

Coleco missed its mark, significantly underestimating the demandfor these dolls. While having a popular toy may seem like a dream for a

29-Strategy_FinancialPlan Page 940 Wednesday, April 30, 2003 12:19 PM

Strategy and Financial Planning 941

toy manufacturer, this doll turned into a nightmare. With no CabbagePatch dolls on the toy shelves, other toy manufacturers introduced dollswith similar (but not identical) features, capturing some of Coleco’smarket. Also, many consumers—the parents—became irate at Coleco’screating the demand for the toy through advertising, but not having suf-ficient dolls to satisfy the demand.

Coleco Industries tried but failed to introduce a toy as successful asthe Cabbage Patch doll. It filed for bankruptcy in 1988, with most of itsassets (including its Cabbage Patch doll line) sold to Hasbro Inc., a rivaltoy company. Hasbro was then acquired by Mattel, Inc. Cabbage PatchDolls are experiencing a resurgence of interest, thanks to the increasedmarketing power of Mattel and a tie-in with the 1996 summer Olympics.

To predict cash flows we forecast sales which are uncertain becausethey are affected by future economic, industry, and market conditions.Nevertheless, we can usually assign meaningful degrees of uncertaintyto our forecasts. We forecast sales in one of the following ways:

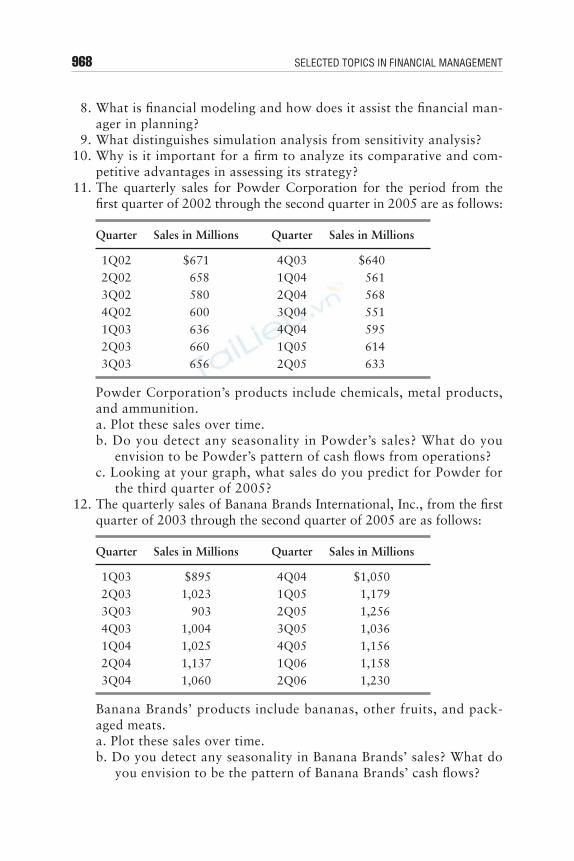

■ regression analysis;

■ market surveys; and

■ opinions of management.

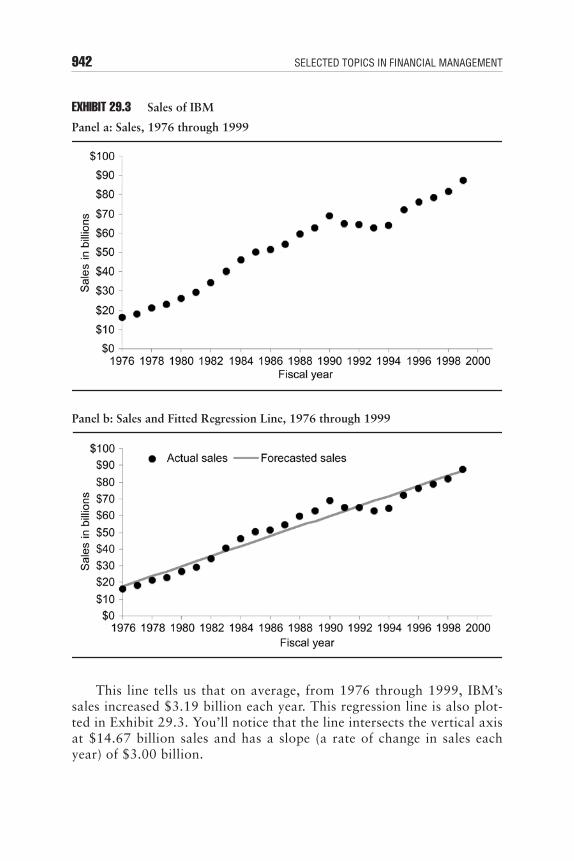

Forecasting with Regression Regression is a statistical method that enables us to “fit” a straight linethat on average represents the best possible graphical relationshipbetween sales and time. This best “fit” is called the regression line. Oneway regression can be used is to simply extrapolate future sales basedon the trend in past sales. In Exhibit 29.3, let’s look at the sales of Inter-national Business Machines’ sales over the period 1976 through 1999.During much of this period, sales increased each year, hence the salestrend is positive. If we were to connect each point representing sales andtime, the result would look almost like a straight line that slopesupward. But we can’t do much with an “almost” straight line. We needa straight line.

Let’s simplify the regression against time by noting the years 1976,1977, ..., 1999 as 1, 2, ..., 24. Regressing IBM’s sales against time weestimate a regression line described as:

IBM annual sales, in billions = $14.67 + $3.00

× time

↑ ↑Intercept of

line withvertical axis,

in billions

Slope ofthe line, inbillions of

dollars per year

29-Strategy_FinancialPlan Page 941 Wednesday, April 30, 2003 12:19 PM

942 SELECTED TOPICS IN FINANCIAL MANAGEMENT

EXHIBIT 29.3 Sales of IBM

Panel a: Sales, 1976 through 1999

Panel b: Sales and Fitted Regression Line, 1976 through 1999

This line tells us that on average, from 1976 through 1999, IBM’ssales increased $3.19 billion each year. This regression line is also plot-ted in Exhibit 29.3. You’ll notice that the line intersects the vertical axisat $14.67 billion sales and has a slope (a rate of change in sales eachyear) of $3.00 billion.

29-Strategy_FinancialPlan Page 942 Wednesday, April 30, 2003 12:19 PM

Strategy and Financial Planning 943

EXHIBIT 29.3 (Continued)

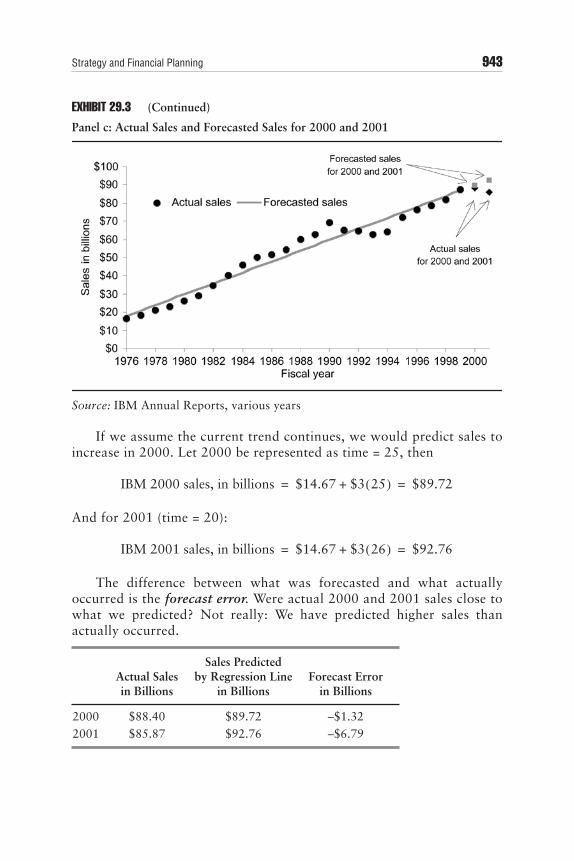

Panel c: Actual Sales and Forecasted Sales for 2000 and 2001

Source: IBM Annual Reports, various years

If we assume the current trend continues, we would predict sales toincrease in 2000. Let 2000 be represented as time = 25, then

And for 2001 (time = 20):

The difference between what was forecasted and what actuallyoccurred is the forecast error. Were actual 2000 and 2001 sales close towhat we predicted? Not really: We have predicted higher sales thanactually occurred.

Actual Salesin Billions

Sales Predictedby Regression Line

in BillionsForecast Error

in Billions

2000 $88.40 $89.72 –$1.322001 $85.87 $92.76 –$6.79

IBM 2000 sales, in billions $14.67 $3 25( )+ $89.72= =

IBM 2001 sales, in billions $14.67 $3 26( )+ $92.76= =

29-Strategy_FinancialPlan Page 943 Wednesday, April 30, 2003 12:19 PM

944 SELECTED TOPICS IN FINANCIAL MANAGEMENT

EXHIBIT 29.4 Sales and Capital Expenditures for IBMPredicted Sales for 2000 and 2001, Based on Regression of Sales and Capital Expenditures for 1976–1999

Source: IBM Annual Reports, various years

Predicted and actual 2000 and 2001 sales are shown in Exhibit29.3, panel c. You’ll notice that we overestimated sales. This illustratesa problem with regression analysis: Past trends do not always continue.Sales growth slowed in 2000 and 2001.

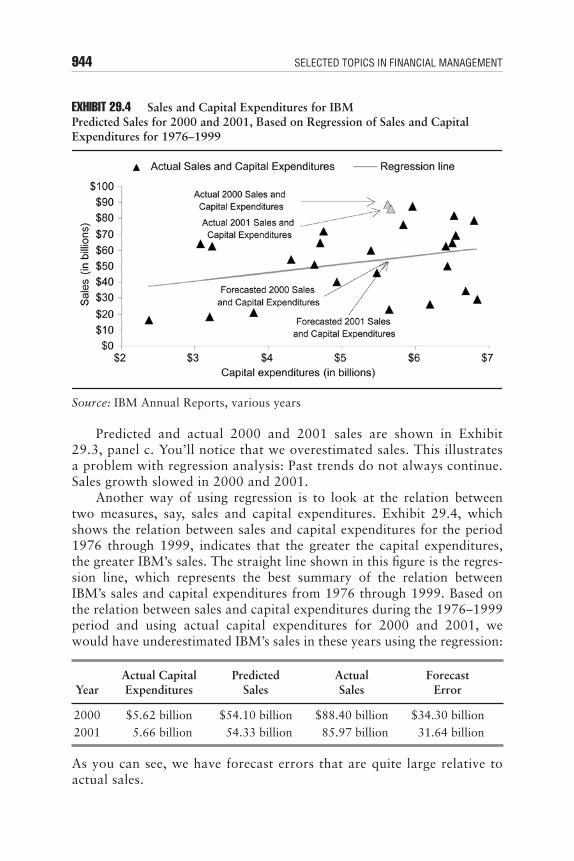

Another way of using regression is to look at the relation betweentwo measures, say, sales and capital expenditures. Exhibit 29.4, whichshows the relation between sales and capital expenditures for the period1976 through 1999, indicates that the greater the capital expenditures,the greater IBM’s sales. The straight line shown in this figure is the regres-sion line, which represents the best summary of the relation betweenIBM’s sales and capital expenditures from 1976 through 1999. Based onthe relation between sales and capital expenditures during the 1976–1999period and using actual capital expenditures for 2000 and 2001, wewould have underestimated IBM’s sales in these years using the regression:

As you can see, we have forecast errors that are quite large relative toactual sales.

YearActual CapitalExpenditures

PredictedSales

ActualSales

ForecastError

2000 $5.62 billion $54.10 billion $88.40 billion $34.30 billion2001 5.66 billion 54.33 billion 85.97 billion 31.64 billion

29-Strategy_FinancialPlan Page 944 Wednesday, April 30, 2003 12:19 PM

Strategy and Financial Planning 945

We also could look at the relation between IBM’s sales and a num-ber of factors, such as IBM’s capital expenditures, a measure of eco-nomic activity such as Gross Domestic Product (GDP), and IBM’scompetitor’s capital expenditures. Estimating the relation among thesefactors over a number of years, combined with forecasts of GDP andcompetitors’ expenditures, we could predict IBM’s sales for 1994. Themore factors we include, the more accurate should be our predictions.

While regression analysis gives us what may seem to be a precisemeasure of the relationship among variables, there are a number ofwarnings that the financial manager must heed in using it:

■ Using historical data to predict the future assumes that the past rela-tionships will continue into the future, which is not always true.

■ The period over which the regression is estimated may not be represen-tative of the future. For example, data from a recessionary period oftime will not tell much about a period that is predicted to be an eco-nomic boom.

■ The reliability of the estimate is important: If there is a high degree oferror in the estimate, the regression estimates may not be useful.

■ The time period over which the regression is estimated may be tooshort to provide a basis for projecting long-term trends.

■ The forecast of one variable may require forecasts of other variables.For example, you may be convinced that sales are affected by GDP anduse regression to analyze this relationship. But to use regression to fore-cast sales, you must first forecast GDP. In this case, your forecast ofsales is only as good as your forecast of GDP.

Market SurveysMarket surveys of customers can provide estimates of future revenues.In the case of IBM, we would need to focus on the computer industryand, specifically, on the personal computer, mini-computer, and main-frame computer markets. For each of these markets, we would have toassess IBM’s market share and also the expected sales for each market.We should expect to learn from these market surveys:

■ product development and introductions by IBM and its competitors;and

■ the general economic climate and the projected expenditures on com-puters.

A firm can use its own market survey department to survey its custom-ers. Or it can employ outside market survey specialists.

29-Strategy_FinancialPlan Page 945 Wednesday, April 30, 2003 12:19 PM

946 SELECTED TOPICS IN FINANCIAL MANAGEMENT

Management ForecastsIn addition to market surveys, the firm’s managers may be able to pro-vide forecasts of future sales. The experience of a firm’s managementand their familiarity with the firm’s products, customers, and competi-tors make them reliable forecasters of future sales.

The firm’s own managers should have the expertise to predict themarket for the goods and services and to evaluate the costs of producingand marketing them. But there are potential problems in using manage-ment forecasts. Consider the case of a manager who forecasts rosy out-comes for a new product. These forecasts may persuade the firm toallocate more resources—such as a larger capital budget and additionalpersonnel—to that manager. If these forecasts come true, the firm willbe glad these additional resources were allocated. But if these forecaststurned out to be too rosy, the firm has unnecessarily allocated theseresources.

Forecasting is an important element in planning for both the short-term and the long-term. But forecasts are made by people. Forecasterstend to be optimistic, which usually results in rosier than deserved fore-casts of future sales. In addition, people tend to focus on what workedin the past, so past successes carry more weight in the developing fore-casts than an analysis of the future.

One way to avoid this is to make managers responsible for theirforecasts, rewarding accurate forecasts and penalizing the ones forbeing way off the mark.

Seasonal ConsiderationsThe operating activities of a firm typically vary throughout the year,depending on seasonal demand and supply factors. Seasonality influ-ences a firm’s short-term investment and financing activities.

Let’s look at a few U.S. corporations’ quarterly revenues to get anidea of different seasonal patterns of activity:

■ Coca Cola, a beverage producer

■ Amazon.com, an online retailer

■ Walt Disney, a film and amusement firm

■ Nike, a shoe manufacturer

■ Delta Airlines, a national airline

The quarterly revenues for each of these firms is plotted in Exhibit 29.5from the first quarter 1999 through the fourth quarter 2002. The sea-sonal patterns are quite different:

29-Strategy_FinancialPlan Page 946 Wednesday, April 30, 2003 12:19 PM

Strategy and Financial Planning 947

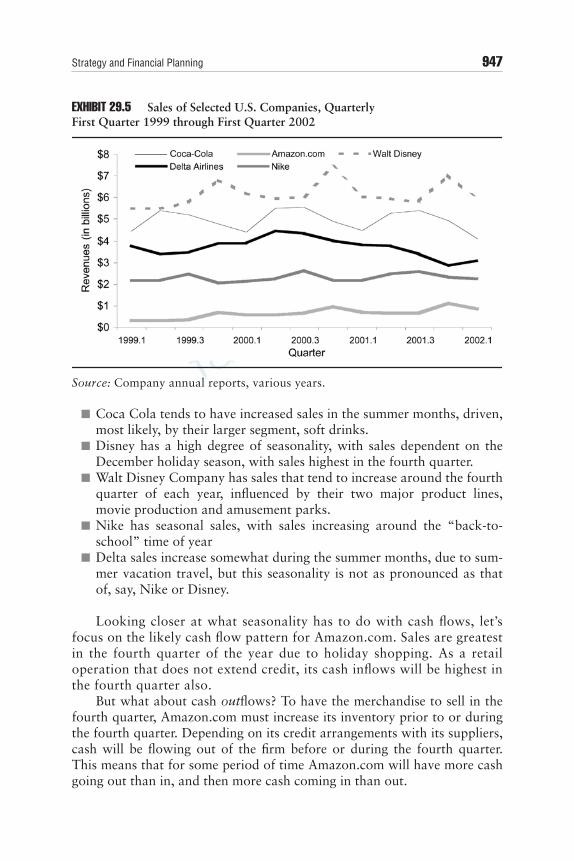

EXHIBIT 29.5 Sales of Selected U.S. Companies, QuarterlyFirst Quarter 1999 through First Quarter 2002

Source: Company annual reports, various years.

■ Coca Cola tends to have increased sales in the summer months, driven,most likely, by their larger segment, soft drinks.

■ Disney has a high degree of seasonality, with sales dependent on theDecember holiday season, with sales highest in the fourth quarter.

■ Walt Disney Company has sales that tend to increase around the fourthquarter of each year, influenced by their two major product lines,movie production and amusement parks.

■ Nike has seasonal sales, with sales increasing around the “back-to-school” time of year

■ Delta sales increase somewhat during the summer months, due to sum-mer vacation travel, but this seasonality is not as pronounced as thatof, say, Nike or Disney.

Looking closer at what seasonality has to do with cash flows, let’sfocus on the likely cash flow pattern for Amazon.com. Sales are greatestin the fourth quarter of the year due to holiday shopping. As a retailoperation that does not extend credit, its cash inflows will be highest inthe fourth quarter also.

But what about cash outflows? To have the merchandise to sell in thefourth quarter, Amazon.com must increase its inventory prior to or duringthe fourth quarter. Depending on its credit arrangements with its suppliers,cash will be flowing out of the firm before or during the fourth quarter.This means that for some period of time Amazon.com will have more cashgoing out than in, and then more cash coming in than out.

29-Strategy_FinancialPlan Page 947 Wednesday, April 30, 2003 12:19 PM

948 SELECTED TOPICS IN FINANCIAL MANAGEMENT

BudgetingIn budgeting, we bring together analyses of cash flows, projected incomestatements, projected balance sheets. The cash flow analyses are mostimportant, though you also need to generate the income statement andbalance sheet as well.

Most firms extend or receive credit, so cash flows and net income donot coincide. Typically, you must determine cash flows from accountinginformation on revenues and expenses. Combining sales projectionswith our estimates of collections of accounts receivable results in anestimate of cash receipts.

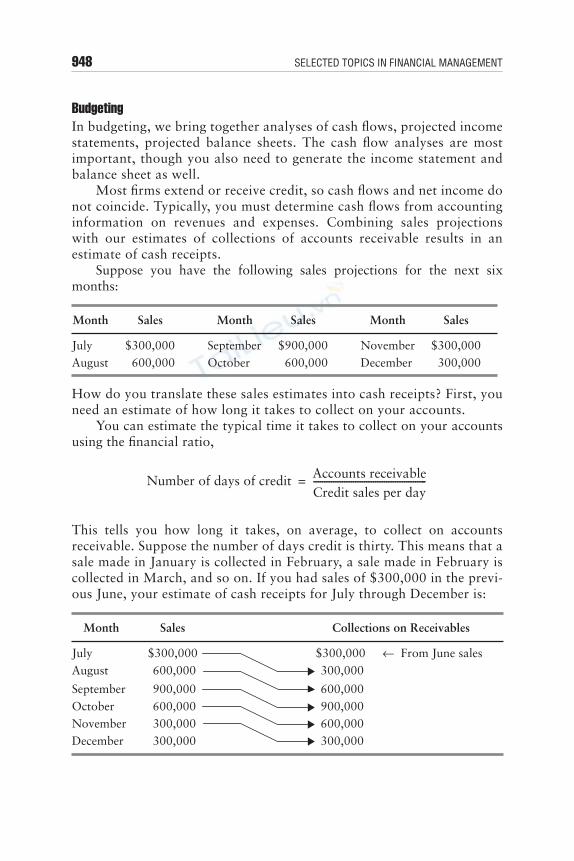

Suppose you have the following sales projections for the next sixmonths:

How do you translate these sales estimates into cash receipts? First, youneed an estimate of how long it takes to collect on your accounts.

You can estimate the typical time it takes to collect on your accountsusing the financial ratio,

This tells you how long it takes, on average, to collect on accountsreceivable. Suppose the number of days credit is thirty. This means that asale made in January is collected in February, a sale made in February iscollected in March, and so on. If you had sales of $300,000 in the previ-ous June, your estimate of cash receipts for July through December is:

Month Sales Month Sales Month Sales

July $300,000 September $900,000 November $300,000August 600,000 October 600,000 December 300,000

Month Sales Collections on Receivables

July $300,000 $300,000 ← From June salesAugust 600,000 300,000

September 900,000 600,000October 600,000 900,000November 300,000 600,000December 300,000 300,000

Number of days of credit Accounts receivableCredit sales per day---------------------------------------------------=

29-Strategy_FinancialPlan Page 948 Wednesday, April 30, 2003 12:19 PM

Strategy and Financial Planning 949

An alternative, and more precise method, is to look at the aging ofreceivables—how long each account has been outstanding—and use thisinformation to track collections. However, this requires a detailed esti-mate of the age of all accounts and their typical collection period.

Whether you use an overall average or an aging approach, you needto consider several factors in our cash collections estimate:

■ An estimate of bad debts—accounts that will not be collected at all; ■ An analysis of the trend in the number of days it takes customers to

pay on account; and ■ An estimate of the seasonal nature of collections of accounts; often cus-

tomers’ ability to pay is influenced by the operating cycle of their ownfirm.

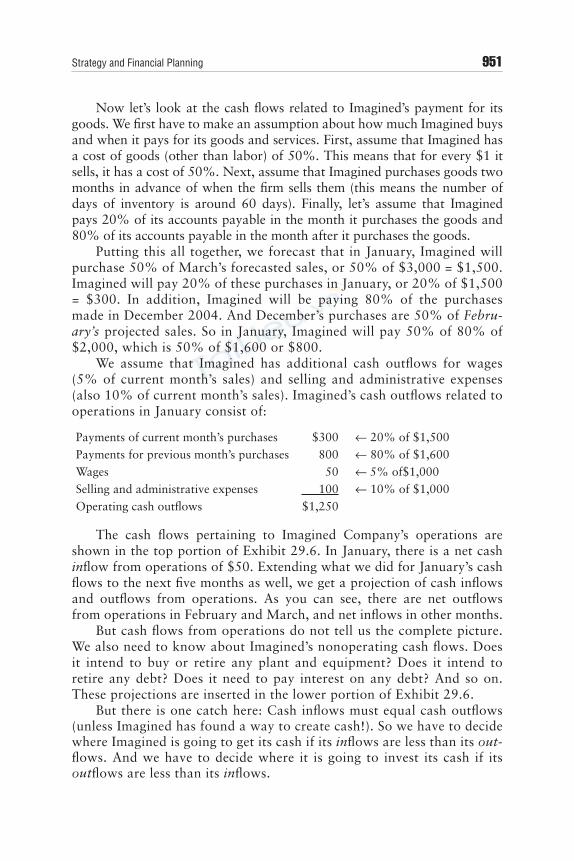

As with revenues and cash receipts, there is a relation betweenexpenses and cash disbursements. Firms typically do not pay cash for allgoods and services; purchases are generally bought on account (creatingaccounts payable) and wages and salaries are paid periodically (weekly,bi-monthly, or monthly). Therefore, there’s a lagged relationship betweenexpenses and cash payments.

You can get an idea of the time it takes to pay for your purchases onaccount with the number of days of purchases:

And you can determine the time it takes to pay for wages and salaries bylooking at the firm’s personnel policies. Putting these two piecestogether, you can estimate how long it takes to pay for the goods andservices you acquire.

The Cash BudgetA cash budget is a detailed statement of the cash inflows and outflowsexpected in future periods. This budget helps you identify our financingand investment needs. You can also use a cash budget to compare youractual cash flows against planned cash flows so that you can evaluateboth your performance and your forecasting ability.

Cash flows in to the firm from:

1. Operations, such as receipts from sales and collections on accountsreceivable;

2. The results of financing decisions, such as borrowings, sales of sharesof common stock, and sales of preferred stock; and

Number of days of purchases Accounts payableAverage day’s purchases---------------------------------------------------------------=

29-Strategy_FinancialPlan Page 949 Wednesday, April 30, 2003 12:19 PM

950 SELECTED TOPICS IN FINANCIAL MANAGEMENT