Embed Size (px)

Citation preview

Factors Affecting Deposit Mobilization of Commercial Banks;the case

of Commercial Bank of Ethiopia at Hawassa City Branches.

The thesis Submitted to Hawassa University School of Graduate Studies In

Partial Fulfillment Of The Requirements For The Degree Of Master In

Business Administration Specialization In Marketing Management.

By:

Tadele Shamebo

Principal Advisor: Dr.YlimaGelatu

Co –Advisor Abdulaziz Abdella (hpD canditate)

Hawassa University

College of Business and Economics

School of Management and Accounting

June 2019

Hawassa, Ethiopia

Factors Affecting Deposit Mobilization of Commercial Banks;the

case of Commercial Bank of Ethiopia at Hawassa City Branches.

By:

Tadele Shamebo

Principal Advisor: Dr.Ylima Gelatu

Co –Advisor Abdulaziz Abdella (phD canditate)

The thesis Submitted to Hawassa University School of Graduate

Studies In Partial Fulfillment Of The Requirements For The Degree

Of Master In Business Administration Specialization In Marketing

Management.

Hawassa University

College of Business and Economics

School of Management and Accounting

June 2019

Hawassa, Ethiopia

Declaration

I declare that this work has not be previously submitted and approved for the award of a degree

by this or any other university. To the best of my knowledge and belief, the project contains no

material previously published or written by another person except where due reference is made

in the project itself.

Nane: Tadele Shamebo

Signature: ------------------------

Date: -------------------------------

SCHOOL OF GRADUATE STUDIES

HAWASSA UNIVERSITY

ADVISORS’ APPROVAL SHEET

This is to certify that the thesis entitled "Factors Affecting Deposit Mobilization of

Commercial Banks ,the case of Commercial Bank Ethiopia at Hawassa city branches

submitted in partial fulfillment of the requirements for the degree of Master's with

specialization in marketing management , the graduate program of the school of management

and accounting, and has been carried out by Tadele Shamebo Id. No 037/09 under my

supervision. Therefore I recommend that the student has fulfilled the requirements and hence

hereby can submit the thesis to the School.

Name of Principal Advisor Signature Date

Dr.Ylima Gelatu

---------------- -----------------

Name of co-Advisor Signature Date

Abdulaziz Abdella (phD Canditate)

---------------------- ------------------

SCHOOL OF GRADUATE STUDIES

HAWASSA UNIVERSITY

EXAMINERS‟ APPROVAL SHEET

===============================================================

We, the undersigned, members of the Board of Examiners of the proposal open defense by

Tadele Shamebo have read and evaluated his/her thesis entitled “_Factors Affecting Deposit

Mobilization of Commercial Banks ,the case of Commercial Bank Ethiopia, at Hawassa

city branches”, and examined the candidate. This is, therefore, to certify that the thesis has been

accepted in partial fulfillment of the requirements for the degree in Business Administration.

________________________ _______________________ ____________

Name of the Chairperson Signature Date

________________________ _______________________ ____________

Name of Principal Advisor Signature Date

________________________ _______________________ ____________

Name of Co- Advisor Signature Date

________________________ _______________________ ____________

Name of Internal Examiner Signature Date

________________________ _______________________ ____________

Name of External examiner Signature Date

________________________ _______________________ ____________

SGS Approval Signature Date

Final approval and acceptance of the thesis is contingent upon the submission of the final copy of

the thesis to the School of Graduate Studies (SGS) through the School Graduate Committee

(DGC/SGC) of the candidate‟s department.

Stamp of SGS Date: ______________

i

ACKNOLEDGEMENTS

First, I am thankful to the Almighty GOD who saw me through the toughest moments of this

program.

Next, I would like to sincerely thank my principal advisor: Dr.Ylima Gelatu for his constructive

comments, valuable suggestions and good guidance since the beginning to the end of the project

.I equally thank my co-advisor Abdulaziz Abdella (phD candidate) for his strong comments,

suggestions and necessary encouragement. I also thank all my lectures who thought me

throughout the program. I also wish to thank my classmates particularly those whom I closely

shared many special learning experiences. I wish to thank respondents to this study without

whom this study would not have been complete.

Finally, my appreciation also goes to my family, friends& work classmates for their moral &

financial support throughout this study.

ii

Table of contents

Contents page ACKNOLEDGEMENTS ................................................................................................................. i

Table of contents ............................................................................................................................. ii

List of Table .................................................................................................................................... v

List of Figure.................................................................................................................................. vi

LIST OF ACRONYMS ................................................................................................................ vii

ABSTRACT ................................................................................................................................. viii

CHAPTER ONE ............................................................................................................................. 1

1. Introduction ................................................................................................................................. 1

1.1. Background of the Study ...................................................................................................... 1

1.2. Statement of the Problem ..................................................................................................... 4

1.3. Objectives of the study ......................................................................................................... 6

1.3.1General Objectives ........................................................................................................................ 6

1.3.2. The specific objectives ................................................................................................................ 6

1.3.3 Research hypothesis ................................................................................................................... 6

1.4 Research questions ................................................................................................................ 7

1.5 Significance of the study ....................................................................................................... 7

1.6. Scope of the study ......................................................................................................................... 7

1.7. Limitation of the study ......................................................................................................... 8

1.8 Organization of the thesis ...................................................................................................... 8

1.9. Operational definition of the study ...................................................................................... 9

CHAPTER TWO ........................................................................................................................ 10

2. LITERATURE REVIEW ...................................................................................................... 10

2.1 Chapter overview ................................................................................................................ 10

2.2. Theoretical conceptualization of deposit ........................................................................... 10

2.3 The role of commercial Banks in Financial Systems .......................................................... 12

2.4 Major Types of Deposit products ........................................................................................ 12

2.5 .Importance of Deposit mobilization ................................................................................... 13

2.6 Factors that affects the deposit mobilization of commercial banks in Ethiopia ................. 14

iii

2.6.1 Institutional factors and saving mobilization ............................................................................. 14

2.6.1.1 Internal saving policy .................................................................................................... 14

2.7 External environmental factors and saving mobilization .................................................... 23

2.7.1. Competition .............................................................................................................................. 25

2.7.2. Inflation rate ............................................................................................................................. 25

2.7.3. Saving interest rate (Deposit rate) ............................................................................................ 26

2.7.4 per Capita Income of the Society ............................................................................................... 28

2.8 The research gap ................................................................................................................. 30

2.9. Empirical Evidence of Deposit Mobilization from Developing Countries ........................ 30

2.10 Empirical Evidence of Deposit Mobilization from Ethiopian‟s Commercial Banks ........ 32

2.11 Conceptual framework ...................................................................................................... 36

CHAPTER THREE .................................................................................................................... 38

3. Research Methodology ........................................................................................................... 38

3.1 Description of the Study Area ............................................................................................. 38

3.2 research design .................................................................................................................... 39

3.3 Data type and sources .......................................................................................................... 40

3.4 Target population ................................................................................................................ 40

3.5 Sample design ..................................................................................................................... 42

3.5 .1 Sample size determination ....................................................................................................... 42

3.6 Data collection method ....................................................................................................... 43

3.7 Data analysis ....................................................................................................................... 43

3.7.1. Descriptive Analysis .................................................................................................................. 43

3.7.2. The inferential statistics ............................................................................................................ 44

3.8 Model specifications ........................................................................................................... 44

3.7.3. Qualitative analysis ................................................................................................................... 46

3.9. Reliability test .................................................................................................................... 46

3.10 Validity test ....................................................................................................................... 47

3.11 Ethical considerations ....................................................................................................... 48

CHAPER FOUR ......................................................................................................................... 49

FINDING AND DISCUSSIONS ................................................................................................ 49

4.1 Chapter over view ............................................................................................................... 49

4.3 Demographic characteristics of respondents ....................................................................... 49

iv

4.3.1 Gender distribution of respondents .......................................................................................... 50

Table 4.3.1 Gender of respondents ............................................................................................ 50

4.3.2 Respondents age distribution .................................................................................................... 50

4.3.3 Respondents Educational level .................................................................................................. 51

4.3.4 Respondents experience in deposit mobilization ...................................................................... 51

4.3.5 Respondent by role played in the deposit mobilization ............................................................ 52

4. 4 .The trend and current status of saving mobilization by commercial banks ...................... 53

4.5 Factors influencing of saving mobilization by commercial banks ...................................... 55

4.5.1 Influence of institutional factors on deposit mobilization ......................................................... 55

4.5.2The influence of external environment on the saving mobilization. .......................................... 60

4.6 Multiple Regression analysis of the study .......................................................................... 63

CHAPTER FIVE ........................................................................................................................ 71

SUMMERY, CONCLUSION AND RECOMENDITIONS .................................................... 71

5.1 Chapter overview ................................................................................................................ 71

5.2.1 The trends and current status of saving mobilization by commercial banks ............................ 71

5.3 Conclusion........................................................................................................................... 72

5.4 Recommendations ............................................................................................................... 73

5.5 Limitations of the study ...................................................................................................... 74

5.6 Areas for further research .................................................................................................... 75

REFERENCES .......................................................................................................................... 76

Appendixes................................................................................................................................... 80

v

List of Table

Table 3.1 Target population of the study------------------------------------------------------------------44

Table 3.2: Reliability Statistics------------------------------------------------------------------------------------49

Table 3.3: Item Statistics----------------------------------------------------------------------------------50

Table 4.1 Rate of response by respondents-------------------------------------------------------------52

Table 4.3.1 Gender of respondents ----------------------------------------------------------------------53

Table 4.3.2 Age of the respondents----------------------------------------------------------------------53

Table 4.3.3 Respondents Educational level-----------------------------------------------------------54

Table 4.3.4 work experience in the bank---------------------------------------------------------------54

Table 4.3.5 Position of respondents in the bank ------------------------------------------------------55

Table 4.5.1 Descriptive statistics of institutional factors--------------------------------------------58

Table 4.5.2 Pearson chi square correlation analysis result for institutional factors

and deposit mobilization.--------------------------------------------------------------------------------59

Table 4.5.2.1 Descriptive statistics of the influence of external factors on

Deposit mobilization-------------------------------------------------------------------------------------60

Table 4.5.2.2Pearson chi square correlation analysis result for external

Environmental factors and deposit mobilization---------------------------------------- -------------63

Table4.6.1Model Summary------------------------------------------------------------------------------64

Table 4.6.2 Analysis of variance (ANOVA) ---------------------------------------------------------65

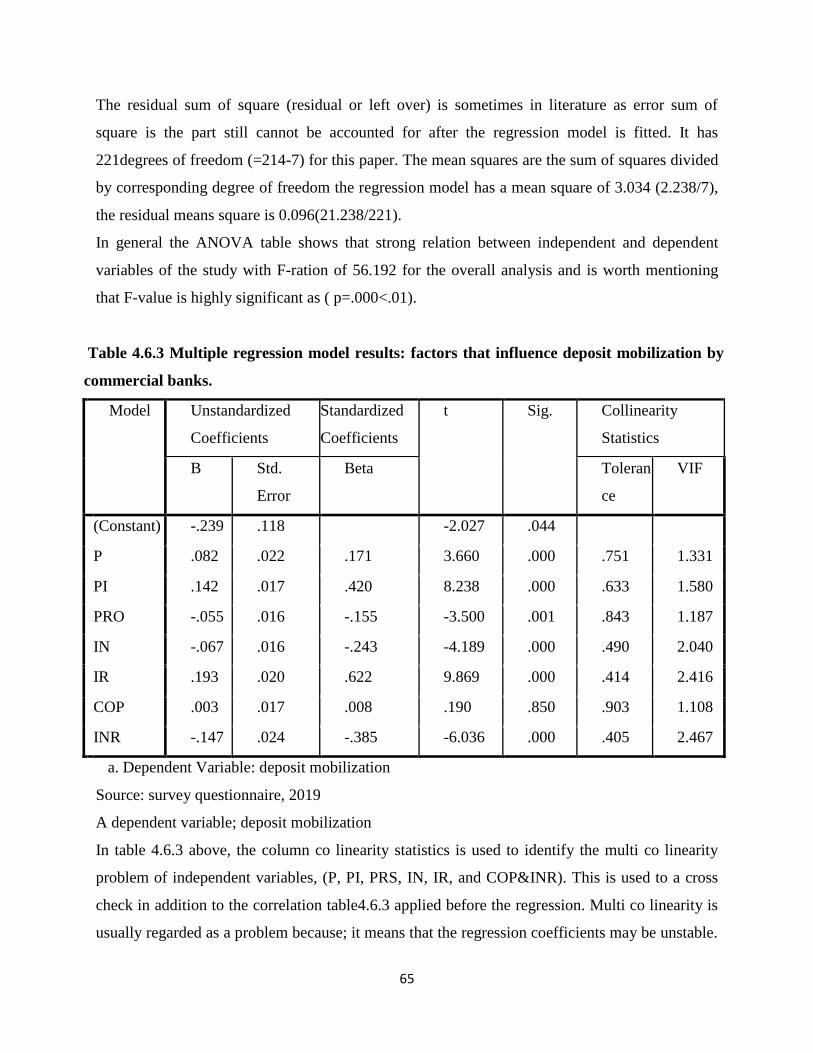

Table 4.6.3 .Multiple regression model results: factors that influence

Deposit mobilization by commercial banks--------------------------------------------------------------67

Table 4.6.4 Independent variable with coefficient and p-value---------------------------------------70

vi

List of Figure

Figure 2.1 Conceptual frameworks-----------------------------------------------------------------------39

Figure 4.4.1 saving as a percentage of planned mobilized and total variation deposit-------------56

Figure 4.4.2 the percentage distribution of scores on performance in deposit mobilization-------57

vii

LIST OF ACRONYMS

AEBP---------------------------------------------Ability and Experience of Bank Personnel

CD----------------------------------------------------Certificate of Deposit

CBE ---------------------------------------------Commercial Bank of Ethiopia

CSA------------------------------------Central Statistical Authority

DMB ----------------------------------------------Deposit Money Banks

EVA------------------------------------------------Economic Value Added

GDP-----------------------------------------------Gross Domestic Product

ICB -------------- ---------------------------------International Commercial Bank

IMF------------------------------------------------International Monetary Fund

ISSER---------------------------------------- Institute of Statistical, Social and Economic Research

MIFs ----------------------------------------------Microfinance Institutions

LDC------------------------------------------------Least Developed Countries

NI -------------------------------------------------- Net Income

NBE----------------------------------------------National Bank of Ethiopia

ROI ------------------------------------------------Return on Investment

RBI---------------------------------------------------Reserve Bank of India

ROA ------------------------------------------------Return on Asset

RQ -------------------------------------------------Research Questions

SACS-----------------------------------------------Saving and Credit Associations

SPSS ----------------------------------------------Statistical Package for Social Science

viii

ABSTRACT

The objective of this study is to assess the factors that affects deposit mobilization in

commercial bank of Ethiopia at Hawassa District, and to establish the extent to which the

institutional and the external Environmental factors influence the saving mobilization by

commercial banks. The study also adopted descriptive and quantitative method to obtain data

useful in evaluating present practices and providing a basis for decision making. The

populations of the study were managers & employees of CBE under Hawassa city branches.

The sample design used for this study was purposive sampling technique with an objective of

insuring that only those which had operated more than five years were included in the study

to allow analysis of trend in saving mobilization for the last six years. The study used the

qualitative &quantitative approaches the data collection method was survey method by

employing both questionnaire and interview and the collected data was analyzed by using

both qualitative and quantitative data by using descriptive data analysis method. The

descriptive analysis revealed the trend of deposit mobilization by commercial banks with the

current status considered unsatisfactory. The multiple regression analysis model revealed

that a significant influence of institutional &external environmental factors on deposit

mobilization. The institutional factors are inappropriate management &employee’s attitude

on deposit mobilization, inappropriate product/service promotional strategy, poor job

commitments &performance in deposit mobilization, inappropriate rewarding system which

do not significantly impact on employees motivation .The external factors are competition

with other deposit taking institutions. Such as microfinance institution, other private banks&

the persistent increase of inflation rate would affect bank deposit. In the light of the findings,

the researcher recommended the leadership and the management of commercial bank of

Ethiopia need to re-focus on their performance management police and strategy towards

improving incentive systems, change employees attitude to enhance employee’s motivation

and job commitments. The bank should also advise innovative measures to position more

strategically and competitively to attract more saving and mitigate the negative impact of

competition with other deposit -taking institutions on their performance on deposit

mobilization.

Key words/phrases: Deposit mobilization, inflation rate, competition, interest rate, rewards.

1

CHAPTER ONE

1. Introduction

This section of the study is introductory part which consists of background of the study,

statement of the problem, objective of the study, research question, significant of the study,

scope of the study, limitation of the study, operational definitions and organization of the study.

1.1. Background of the Study

Mobilization of deposits is one of the important functions of banking business. It is an important

source of working fund for the bank. Deposit mobilization is an indispensable factor to increase

the sources of the banks to serve effectively. Mobilization of deposit plays an important role in

providing satisfactory service to different sectors of the economy. The Commercial Banks must

tap deposits from urban and rural areas. This helps the banks to provide large amount of funds to

priority sectors for development. The success of the banking greatly lies on the deposit

mobilization. Performances of the bank depend on deposits, as the deposits are normally

considered as a cost effective source of working fund.

The reserve bank of India (RBI) encourages the banks to mobilize deposits, by providing subsidy

for branch expansion. The successful functioning of commercial banks depends on the extent of

funds mobilized. Deposits are the life blood of banking companies. Deposits constitute a vital

source of funds required for banking business. There are different types of deposits, with

different maturity pattern carrying different rates of interests. Deposit mobilization is depending

on the cost of deposits.

Mobilization of deposits for a bank is as essential as oxygen for human being. In the post

liberalization scenario, the number of players in banking industry has increased considerably

which developed competition in bank marketing. „The survival of the fittest‟ has made

applicable for the banks. To enhance profitability, banks take steps to minimize the expenditure

and are forced to mobilize low cost deposits. In the present context bank‟s efficiency is measured

based on the deposit mix and on the quantum of low cost deposits in the mix. In the present era

2

of competition and with the emergence of private and multinational banks, an ideal mix of

deposits is a must to survive. Since the interest paid on deposit forms a big burden on bank, the

mobilization of low cost deposits, like current account and savings bank deposit is the urgent

need for the bank. Banks borrow and lend, they borrow money by accepting deposits from the

public including members of the bank. Deposit mobilization is the chief source of funds to

undertake lending operations, for profitable operation, the amount of deposits is very important.

The banks should introduce various deposits schemes to attract the public to deposit. It is the size

of the deposits that largely decides the lending potential of banks.

Economic growth is the common goal of all nations. Everybody lives with more comfortable,

better standard of living than before and holding a better welfare because of the surge in

economic growth. Government in each country aims to reduce poverty and increase the level of

national income. Therefore, to achieve the main target of economic growth, governments may

implement various kinds of policies such as encouraging saving, stimulating investment and

production in their countries (Pinchawawee, 2011).

Mobilizing deposits is one of the essential issues in developing countries as domestic funds

provide cheap and reliable source of funds for development, which is of great value to these

countries, especially when the economy has difficulty raising capital from international donors,

investors and markets. Yet, in many developing countries, there is a considerable amount of

savings that are not intermediated through the formal sector particularly there exist significant

savings potential in the rural (and/or semi-urban) sector of many developing countries.

Selvaraj& Kumar (2015) State that, the success of the banking greatly lies on the deposit

mobilization. Performances of the bank depend on deposits, as the deposits are normally

considered as a cost effective source of working fund. Mobilization of rural savings is one of the

important objectives of the Commercial Banks. It helps to expand banking operations. The

successful functioning of commercial banks depends on the extent of funds mobilized. Deposits

constitute a vital source of funds required for banking business. There are different types of

deposits, with different maturity pattern carrying different rates of interests. Mobilization of

deposits for a bank is as essential as oxygen for human being. Compared to most countries,

Ethiopia has taken a cautious approach toward the liberalization of its banking industry. For all

intents and purposes, its industry is closed and generally less developed than its regional peers.

The industry comprises one state-owned development bank and the financial giant dominant

3

Commercial Bank of Ethiopia (CBE) which embarks on aggressive branch network expansion

aimed at mobilization of deposit resources; continued amassing of foreign currency proceeds of

export items channeled from China, channeling of savings made for the housing project in the

capital city (though it also lends householders at a lower interest rate); imposition of private

banks to purchase NBE-Bills and the sum effect of the above and other factors enable the CBE

secure competitive edge over private banks with assets accounting for more than 65 percent of

the industry‟s total holdings. The banking industry‟s nonperforming loan ratio is commendably

low, and profitability is good, but the dominance of public sector banking certainly restricts

financial intermediation and economic growth. It contrasts with regional and international peer

countries where banking industries have a much higher share of private sector and foreign

participation (Dereje, 2017).

According to (Abay, 2010), by sub-Saharan Africa standards, Ethiopia„s rate of domestic saving

has been very low. From 1997 to 2010, the average saving rate in low-income countries of the

region was about 9 per cent, while it was about 19 per cent for middle-income countries. In the

same period, the average saving rate of ―fragile sub-Saharan African states was 11.5 per cent,

still significantly higher than Ethiopia„s rate of 4 per cent.

The aim of this study is to assess the factors that affect the deposit mobilization of commercial

bank of Ethiopia targeted at Hawassa District city branches .And the main focusing area that the

study will concern is about identifying the institutional and external environmental factors

affecting deposit of commercial bank of Ethiopia an empirical study on Hawassa district. The

most institutional factors will be relating to the governance, and organizational structure,

appropriateness of saving products and technology ,management capabilities (with especial

attention to risk and liquidity management) deposit regulatory environments –strategy, police,

guidelines, employees attitude, performance management system, incentives, monitoring &

marketing strategy. The external factors concerns emergence of potential competitors, the

financial regulatory environment such as change of interest rate, employees saving schemes,

income level, unemployment level &inflation which will result in a great impact on the deposit

of the commercial bank of Ethiopia, and in relation to this, the change in customers‟ attitude and

preference in banking service such as loan services, money transfer, deposit services and

customer service of bank. These factors will affect the market share of the bank largely and

decrease in the market share, which in turn leads to decrease in amount of deposit. So this study

4

enables banks and regulators to keep control to the issue of deposit which is very important to

the security of their operation as well as the economy as a whole in the country. Therefore, this

paper aimed to assess, identify and evaluate those factors that affecting deposit of Commercial

Bank of Ethiopia, an empirical study at Hawassa District.

1.2. Statement of the Problem

Deposits are the primary source of funds for a bank, which facilitates the uses of funds (loans

and investments). The higher the deposits amount, the bigger the lending and investments

portfolio can be maintained by the banks to sustain its expansion and future growth. The banks

must have adequate deposits to meet the lending volume required by the public and at the same

time maintain extra cash for withdrawals by depositors. The cash reserve is a component of

liquidity reserves which measure the ability of the bank to meet its expected withdrawals and

recurring withdrawals. The withdrawals made from there serves are oddly-offset against new

deposits which the banks should continuously mobilize. The inability to get sufficient deposits

could result in negative fund situation. The level of deposits growth also indicates the bank's

performance in relation to customers' satisfaction on interest payout and services rendered.

The fast growing economy of the country, which is proactively investing in road infrastructure,

building hydropower dams, constructing thousands of housing condominiums and expanding

agricultural and other investments in the country are hugely relying on the commercial banks for

loans and credits. Moreover, there have been multiple small enterprises incubated in the last

decades and increasing number of import and export companies, heavily relying on commercial

banks for loans, foreign currency and trade assurances. This call for an increased demand for

deposit mobilization from public institutions, private sector and other potential contributors

(Hibret, 2015).However, Ethiopian banking industry is still in its growing stage. The deposit

generated by the county economy not yet been mobilized as much as expected. NBE indicates

that from deposits that should be mobilized by banks only 7% is mobilized as of 2012 (Wubitu,

2012). This indicates that from the money that should be deposited in the bank 93% of it was not

mobilized. Moreover, in the context of Ethiopian, the previous related research has mostly focus

on similar determinant variables to assess the factors that affects the deposit of commercial

banks.

5

For instance; Inflation Rate taken as explanatory variable by (Andinet, 2016) the result of his

study indicates inflation has a negative relation and insignificant to Privets Commercial Bank

Deposit. (Giagn, 2015) also used the variable in his study to determine the effect of inflation to

Commercial Bank Deposit Growth result of the study was positive relation and significant for

deposit. Finally (Shemsu, 2014) used Inflation rate as an explanatory variable to determine the

effect on the Commercial bank of Ethiopia deposit result was positive relation and insignificant

to the dependent variable deposit. Interest rate: was taken as an explanatory variable by (Andinet,

2016), the result is positive and significant to deposit. (Shemsu, 2014) the result is positive and

insignificant and (Giragn, 2015) the result is negative and insignificant and lastly (Wubit, 2012)

result shows positive and insignificant. Therefore, the findings of the study were incompatible

andwhich revealed mixed result which stimulates further study. There were gaps in the

identification of factors that affects deposit of commercial banks. This meansthere are many

factors that affect commercial banks‟ banks financial performance. These are broadly

categorized as internal and external factors (Choong,Thim, &Kyzy, 2012; Sehrish&Zaman,

2011). Internal factors are mainly influenced by a bank‟s management decisions and policy

objectives whereas external factors focus on industry related and macroeconomic variables

reflected in the economic and legal environment where banks operate (Kijjambu, 2015). Since

CBE has been playing a significant role in the economic development of the country, the bank

has not yet been mobilized as much as expected. This is because of, there are institutional and

external factors affecting deposit mobilization of the bank. The institutional factors: lack of

good saving policy, low employees motivation, lack of good marketing strategy, which will lead

lower market share and the external factors; high competition of other deposit taking banks, low

income level of society, persistent increase of commodity price & unattractive interest rate,

which will discourse deposit mobilization. Hence, the aim of this study was designed to assess

the extent of influence of such factors and to generate valuable information on internal saving

policy, employees‟ motivation & product/service promotion strategy. And external factors like

other banks competition, interest rate, income level & inflation rate that affecting deposit

mobilization of commercial bank of Ethiopia, targeted at Hawassa District city branches.

6

1.3. Objectives of the study

1.3.1General Objectives

The overall objective of the study was aimed to assess factors that affecting the deposit

mobilization of commercial bank of Ethiopia, Hawassa city branches.

1.3.2. The specific objectives

1. To determine the influence of internal saving policy on deposit mobilization of CBE

2. To determine the influence of clients income on deposit mobilization of CBE.

3. To determine the influence of new product promotional strategy on deposit mobilization of

CBE.

4. To determine the influence of interest rate changes on deposit mobilization of CBE.

5. To establish the current status and trend of deposit mobilization by CBE for the period 2012-

2017.

1.3.3 Research hypothesis

Research hypothesis is a predictive statement, capable of being tested by scientific methods,

that relates an independent variable to some dependent variable (kothari, 2004).It is the null

hypothesis is assumed to be correct, until research demonstrate that the null hypothesis is

incorrect (mathers, Fox&Hunn2007).

Based on the objectives the following hypotheses are set for the study under consideration:

H1: Internal saving policy has significant effect on deposit mobilization of commercial banks.

H2: Customers‟ income has significant effect on deposit mobilization of commercial banks.

H3: New product promotional strategy has significant effect on deposit mobilization of CBE.

H4: An interest rate change has significant effect on deposit mobilization of CBE.

H5; performance incentives system has significant effect on deposit mobilization of CBE.

7

1.4 Research questions

This study was intended to address the following questions

1. To what extent is the internal saving policy is affecting the deposit mobilization of CBE?

2. To what extent do the clients‟ income is affecting the deposit mobilization of CBE?

3. What is the effect of the new product strategy on deposit mobilization of CBE?

4. What is the effect of interest rate changes on deposit mobilization CBE?

5. What is the current status and trend of deposit mobilization of commercial bank of Ethiopia?

1.5 Significance of the study

The study conduct on assessment of factors affects commercial banks deposit mobilization

would be an important input to all stakeholder. Accordingly, the following are the significances

that are attained from the study.

1. It would contribute to the well-being of the financial sector of the economy and the society as

a whole. To the financial sectors, it is hoped that the results obtained from the study would serve

as a veritable material to deal with the issues and problems associated with deposit mobilization

in commercial banks.

2. It provides information for all stakeholders especially for management of the commercial

banks in order to minimize the impact of factors affects deposits mobilization by making them to

design effective strategies.

3. Furthermore, it serves as source of reference for academic staffs of the country for further

studies in the area of deposit mobilization. To the students and academics the study would be a

contribution to knowledge and literature as well as a guide for further research.

4. Lastly, this study gives good idea to the researcher about this specific topic and general

knowledge about any research.

1.6. Scope of the study

In line with the overall theme, the study in terms of geographical coverage is delimited to CBE,

Hawassa District selected city branches. In accordance with conceptual delimitation, the

assessment of deposit mobilization influencing factors drew limits to the institutional and the

external environmental factors that drawing from the theoretical and conceptual framework of

8

the study. In terms methodology, the study employed descriptive research, which is survey

design. The study also used survey data collection both quantitative and qualitative methods by

designing semi-structured questionnaire and structured interview to managers and employees

under Hawassa District city branches. Regarding the time scope, the study based on the analysis

of savings mobilization extended to the previous six years (2012-2017) deposit trend of

Hawassa District.

1.7. Limitation of the study

1. A limitation of a research study identifies potential weaknesses in the research. Hence, the

study confined to the following constraints during the research process:

2. The study limited by empirical data which is previously done on the areas of deposit

mobilization in the commercial bank of Ethiopia.

3. The study limited by the ethical consideration of respondents to conduct a research honestly

and with integrity to get bias free data.

4. The scope of the study area was also limited by finance, time and resource constraints.

1.8 Organization of the thesis

This paper organized into five chapters. The first chapter is introductory chapter and is

focused on the introductory part, background of the study, statement of the Problem,

significance of the study, objective of the study, search question, scope of the Study and

limitation of the study& the organization of the study. The second chapter is deals with

literature review, definition of deposit mobilization, theoretical conceptualization the role

financial institution on deposit mobilization, deposit mobilization in commercial banks; the

review also extends to concepts & empirical literature on institutional &environmental factors

that affects deposit mobilization of commercial banks. it also details the conceptual

framework of the study. The third chapter concerns with research methodology, Description

of the study area, sampling technique (procedure) data collection method and data analysis

procedure. The fourth chapter deals with data analysis, findings and discussion of the study.

The fifth chapter focused on Summary of findings, conclusions and recommendations.

9

1.9. Operational definition of the study

1. Deposit mobilization: This is defined as taking of money from clients for storage into their

bank account which is later withdrawn for consumption or investments.

2.Institutional factors: This are the attributes of the saving system internal in the commercial

banks that create an environment that foster or deter performance by the actors/staffs of the

commercial banks .The regulatory environment is defined by policies, strategies, guidelines that

create incentive for performance.

3. External factors: This is defined as the attributes of the external environment to the

commercial banks. The regulatory environment is defined by regulatory policies, competition

and income status of potential deposit clients.

10

CHAPTER TWO

2. LITERATURE REVIEW

2.1 Chapter overview

This chapter preset the reviewed literature on deposit mobilization accordance with the study

objectives. it presents the theoretical conceptualization the role of financial institutions in deposit

mobilization, deposit mobilization trend in Ethiopia and empirical evidence on factors that

influence saving mobilization. The review also extends to the empirical literature on deposit

mobilization influencing factors in developing countries like Ethiopia and focus on institutional

and environmental factors. Finally, a summery will identify the gap and justify the relevancy of

this study is presented.

2.2. Theoretical conceptualization of deposit

According to Bello (2005), banking system is the backbone of financial intermediation through

the mobilization and channeling of financial resources. Banks in performing their pivotal role in

the economy, facilitate financial settlement through the payment system, influence money

market rates and provide a means for international payment. The sector mobilizes funds from the

surplus spending units into the economy and by on-lending such funds to the deficit spending

units for investment, banks in the process increase the quantum of national savings and

investment (Mordi, 2004)

Commercial banks as well as the sector in general do depend on customer‟s deposit to advance

its clients. According to Sharma (2009), the bank credit and bank deposits are very closely

related with each other that they represent, roughly speaking, two sides of the same coin, and the

balance sheets of banks. With regard to the question whether loans make deposits or deposits

make loans, two kinds of answers have been given for the puzzle. Banks, the world over, thrive

on their ability to generate income through their lending activities. The lending activity is made

possible only if the banks can mobilize enough funds from their customers. Since commercial

banks depend on depositor‟s money as a source of funds, it means that there are some

relationships between the ability of the banks to mobilize deposits and the amount of credit

granted to the customers. Thus, the main function of financial institutions of mobilizing funds

from the surplus economic agents to the deficit economic agents is put to test in order to generate

11

economic growth. However, the efficiency of performing this function depends on the level of

development of the financial system. The finance literature provides support for the argument

that countries with better/efficient financial systems grow faster, while inefficient financial

systems bear the risk of bank failure. (Kasekende, 2008)

Mohan (2012), Mobilization of deposits is one of the important functions of banking business. It

is an important source of working fund for the bank. Deposit mobilization is an indispensable act

or to increase the sources of the banks to serve effectively. Mobilization of deposit plays an

important role in providing satisfactory service to different sectors of the economy. The success

of the banking greatly lies on the deposit mobilization.

Mobilization of deposits is one of the important functions of banking business. It is an important

source of working fund for the bank. Deposit mobilization is an indispensable factor to increase

the sources of the banks to serve effectively. Mobilization of deposit plays an important role in

providing satisfactory service to different sectors of the economy. The success of the banking

greatly lies on the deposit mobilization. Performances of the bank depend on deposits, as the

deposits are normally considered as a cost effective source of working fund. There are different

types of deposits, with different maturity pattern carrying different rates of interests. Deposit

mobilization is depending on the cost of deposits. Mobilization of deposits for a bank is as

essential as oxygen for human being. To enhance profitability, banks take steps to minimize the

expenditure and are forced to mobilize low cost deposits. (Sylvester, 2010)

In the present context banks‟ performance is measured on several indicators, including the

deposit mix and the quantum of low cost deposits in the mix among others. In the present era of

competition and with the emergence of private and multinational banks, an ideal mix of deposits

is a must to survive. Since the interest paid on deposit forms a big burden on bank, the

mobilization of low cost deposits, like current account and savings bank deposit is the urgent

need for the bank. Banks borrow and lend, they borrow money by accepting deposits from the

public including members of the bank. Deposit mobilization is the chief source of funds to

undertake lending operations, for profitable operation, the amount of deposits is very important.

The banks should introduce various deposits schemes to attract the public to deposit. It is the size

of the deposits that largely decides the lending potential of a bank.(Rajeshwari,2014

12

2.3 The role of commercial Banks in Financial Systems

Commercial bank deposits are major liabilities for commercial banks. (Kelvin, 2001) said that

deposits of commercial banks account for about 75% of commercial banks liabilities.

Commercial banks keep lending as long as they possess adequate deposit.

Therefore, banks will be better off if they are mobilizing more deposits. However, as (N.

Desinga, 1975) indicates deposit mobilization is a very difficult task. The cost of intermediation

for mobilizing deposits is also very important part of overall intermediation cost of the banking

system as (E.A. Shaw 1995) indicates. In spite of the difficulties, deposits play an important role

not only to the banking sector but also the overall economy.

All the financial performance of most of the commercial banks in one way or the other related to

the deposit it managed to be mobilized. Deposits provide limits to the working capital of the

bank. The higher the deposit, the higher will be the funds at the disposal of a bank to lend and

earn profits (N. Desinga, 1975). Therefore, to maximize its profit the bank should increase its

deposit. (Mahendra, 2005) had also mentioned deposits as a foundation up on which banks thrive

and grow and deposit is unique items on a bank‟s balance sheet that distinguish them from other

type of business organizations.

Commercial banking is a service industry with a high degree of built in profit potential

(Meenakshi, 1975). Commercial banks mainly depend on the funds deposited with them by the

public to lend it out to others in order to earn interest income (Davinaga, 2010). However, banks

attract deposits by paying a risk free return to the savers. Interest expense is number one expense

on the income statement of most commercial banks. (Hamid 2011) said that if banks lose their

deposit base they rely on non-deposit based funding that is very expensive and consequently

minimizes the profit margin.

2.4 Major Types of Deposit products

Deposit account is a savings account, current account or any other type of bank account that

allows money to be deposited and withdrawn by the account holder. These transactions are

recorded on the bank's books, and the resulting balance is recorded as a liability for the bank and

represents the amount owed by the bank to the customer. Some banks may charge a fee for this

service, while others may pay the customer interest on the funds deposited. The account holder

13

has the right to withdraw any deposited funds, as set forth in the terms and conditions of the

account. The following are most common type of bank deposit.

Demand Deposit: it consists of funds held in an account from which deposited funds can be

withdrawn at any time without any advance notice to the depository institution. Demand deposits

can be "demanded" by an account holder at any time. Many checking accounts today are demand

deposits and are accessible by the account holder through a variety of banking options, including

teller, ATM and online banking.

Savings Account: is a deposit account held at a bank or other financial institution that provides

principal security and a modest interest rate. Depending on the specific type of savings account,

the account holder may not be able to write checks from the account (without incurring extra fees

or expenses) and the account is likely to have a limited number of free transfers/transactions.

Time Deposit: time deposit or certificate of deposit (CD) held for a fixed-term, with the

understanding that the depositor can make a withdrawal only by giving notice. A time deposit is

an interest-bearing bank deposit that has a specified date of maturity. Generally speaking, the

longer the term the better the yield on the money (Dereje, 2017)

2.5 .Importance of Deposit mobilization

A. a source of investment

According to(Ongore&Kusa, 2013) Intermediation function of banks play a vital role in the

efficient allocation of resources of countries by mobilizing resources for productive activities.

They transfer funds from those who don't have productive use of it to those with productive

venture. (Nwanko, Ewuim, &Asoya, 2013) States that, savings are resources which one decides

to put aside for investment purposes and not for luxury. What people save, avoiding toconsume

all their income, is called "personal savings". These savings can remain on the bank accounts for

future use or be actively invested in houses, real estate, bonds, shares and other financial

instruments.

B. Low cost

According to (Shettar&Sheshgiri, 2014) the success of the banking greatly lies on the deposit

mobilization. Performances of the bank depend on deposits, as the deposits are normally

considered as a cost effective source of working fund.

14

Elser, Hannig, &Wisniwski, (1999) savings are a source of funds with low financial costs i.e.,

interest costs, Compared to other commercial funds. With regard to financial costs, most of the

institutions apply a differentiated interest rate schedule, compensating for the higher

administrative costs with no or low interest rates on small savings and increasing them according

to the size of the deposit.

C. A source of profit

According to (Varman, 2005) the ability of a bank„s management and staff to attract checking

and saving accounts from business and individuals is an important measure of the bank„s

acceptance by the public. Deposits provide most of the raw materials for bank loans and thus

represent the ultimate source of bank profits and growth.

Tuyishime, Memba, &Mbera, (2015) also affirmed that, Deposits are an indispensable tool

commercial banks use to enhance its profitability through advancing deposits mobilized to its

customers in form of loans which make in return interest to commercial banks.

D. Economic Growth and Development

According to (Ongore&Kusa, 2013), In addition to resource allocation good bank performance

rewards the shareholders with sufficient return for their investment. When there is return there

shall be an investment which, in turn, brings about economic growth. On the other hand, poor

banking performance has a negative repercussion on the economic growth and development.

Poor performance can lead to runs, failures and crises. Banking crisis could entail financial crisis

which in turn brings the economic meltdown.

2.6 Factors that affects the deposit mobilization of commercial banks in Ethiopia

The factors that influence the commercial banks deposit are categorized into two main parties as

institutional (internal) and the external environmental factors.

2.6.1 Institutional factors and saving mobilization

2.6.1.1 Internal saving policy

Luara et al.(1999) argues that people are willing and have capacity to save with commercial

institutions but can only do so if the institution offer appropriate saving products and an

appropriate institutional structure and regulatory environment to guarantee safety of their funds,

easy of immediate access and positive real return to savings. A number of empirical literature

15

open insights into crucial factors that are likely to affect the role played by financial institutions

in saving mobilization. These are: institutional type, governance organizational structure,

appropriateness of saving products the regulatory environment .the elements have been analyzed

and specific strategies on how to successfully mobilize savings identified in context of financial

institutions in the other countries. Similarly, Maimbo&Movrotas (2003) observed a changing

trend in aggregate as well as private saving &government saving in overtime in Zambia. This

change was attributed to the financial institutional reform as well as in decline in government

foreign debt. Bank outreach is also a key factor in saving mobilization .most saving especially in

the rural area probably are not efficiently mobilized as a result of factors, which amongst others;

include bank spread otherwise referred to as commercial bank branches distribution .the poor

bank distribution lead to the development of strong informal financial sectors, which now

competes with the formal sector at an almost equal strength (Anza, 2005; Ngendakuriyo et al.,

2014) Performance of commercial banks in saving mobilization can also be linked with the

general performance management literature which underscores a significant link between

employees‟ competence ,motivation ,rewards, remuneration, and punitive actions with

performance(Chubbe ,Reilly &Brown,2011Strebler,Robinson, & Bevan(2001) observed that

organization can improve performance by adopting either a developmental approach or punitive

action .The former concerns interventions to build staff capacity to perform better trough fitting

people to roles that would allow them to perform better, adopting reward system, encouraging

&motivating poor performers(Locke &Latham,1990;Likert , 1959;Karuhagna,2010;Chubbe et

al.(2011) .the later entails adoption of more punitive method of identifying and weeding out

those who are seen as nonperformers.

2.6.1.2 Employees attitude, incentives, promotion &monitoring

Deposit mobilization is the most important function of commercial banks since their successful

functioning depends on the extent of funds mobilized. In Nigeria, the government has directed

banks from time to time to make all possible efforts to mobilize new deposits, which can

expedite the pace of lending activities. Historically, monetary incentives have been used to

reward bank employees for good job performance. Monetary rewards have been tied to the

achievement of sales or target deposits (Bonner and Sprinkle 2002).

16

Thus staff financial incentive scheme in the banking industry are mostly designed to have

positive and powerful effects on productivity in terms of deposit mobilization. According to

Omolayo and Owolabi (2010), most financial incentive schemes or bonuses in banks are

designed in a manner that only better performing staff (especially marketers) are rewarded with

higher salaries or bonuses. In the banking sector in Nigeria marketers are given higher

compensation for working better and harder in meeting or exceeding targets given to them. As a

marketer, your ability to mobilize more deposits earns you financial reward.

Similarly, Suleiman (2011) observed that salaries of bank staff are tied to their performance in

bringing deposits. Thus, incentives are designed to motivate staff to achieve high performance

levels, change behaviors and attitudes. He described financial bonus or incentives in the banking

sector as rewards for achieving certain targets or making a certain effort toward mobilization of

deposit. Financial incentive scheme is a potential tool for boosting the deposit mobilization

efforts of marketers and managers of bank branches. Those performances are monitored on a

monthly, quarterly or yearly basis depending on the bank.

Ahmed (2010), asserted that the purpose of target deposit and the financial implication in terms

of staff incentive is to improve marketers efforts in deposit mobilization. He stated that most

banks in Nigeria implement individual performance based monetary staff incentive which

considers only the amount of deposits brought to the bank. He opined that one major “lever” for

increasing individual efforts is money. Monetary incentives have a direct impact on employees

income, regardless of the payment‟s frequency (i.e. whether the incentive “package” is paid out

monthly or quarterly, or at other intervals). Therefore, the staff members targeted by a monetary

incentive scheme will feel a direct impact on their own incomes and ultimately, on their

livelihoods. He submitted that it is only logical that a financial institutions employee will take a

keen interest in any financial incentive scheme designed (or planed) for them. After all, they are

the ones who are most directly affected by such schemes.

According to Hartman (2011), in most financial institutions both in developed and developing

economies, financial incentives or bonuses are typically designed for marketers and staff

involved in attracting deposits. These incentives measure and reward performance in the short-

term, focus on target deposit mobilization, and bonuses make a significant difference to the

remuneration of the staff affected. He opined that incentives transform best into improved

performance if:

17

1. Staff perceives a strong link between their individual effort and reward; a) performance is

measured and rewarded in the short term (monthly or quarterly); b) the performance of

individual employees (marketers) is measured and rewarded;

2. Rewards are monetary and make a significant change to the employee‟s total remuneration;

bonuses are not capped. Clark and Condly (2003), sees economic and money reward as the

greatest motivator for marketers and bank staff in general. They conducted a meta-analytic

review of all adequately designed field and laboratory research on the use of incentives to

motivate performance. They reported that in all the studies, money was found to result in higher

performance gains than non-monetary incentives. The literature on target deposit and its

financial implication for marketers and individuals is well documented. In a study on the way in

which United Kingdom banks practice internal marketing, Omon- Donkakis (2011) discovered

that banks set sales targets for the majority of contact personnel and the branch as a whole.

Internal marketing is used to direct people‟s efforts towards achieving higher sale. Everyone has

to get their sales targets in order to get the bonuses and a salary increase at the end of the year.

Omon- Donkatis (2011), noted that banks in the United Kingdom tie monetary rewards to the

achievement of sale targets. Front line personnel have more monetary incentives than back-up

personnel because of their selling role. As part of internal marketing banks design and promote a

program called “Pentathlon” in which the banks reward individual performance in terms of the

sales targets achieved. The monetary rewards are between 20 pounds and 1000 pounds. The

banks also reward two managers who achieve the highest performance results in terms of sales

nationally. This creates competition within the branch network. Branch personnel receive

literature on a quarterly basis which emphasizes the importance of meeting their sales and profit

targets in order to gain the monetary rewards. These are also monetary rewards given for

individual performances in terms of (a) the highest number of new accounts opened and (b) the

highest sales figures for specific products including loans, cards and insurance services.

Impact of target Deposit on Individual Promotion

Constant and due promotion is a way by which employees climb to the top of their career and

achieve by joining an organization. He posited that everything that will enable the employee to

achieve his ambition of promotion and self-actualization will motivate him to put in his best in

18

his work. Thus, there is significant effect on the quality of performance when personal ambition

in joining an organization is not achieved.

In any organization career progression is mostly based on promotion and is of paramount

importance to the employees. Thus, promotion is necessary for climbing to the top in any chosen

career. However, organizations differ in their criteria for staff promotion. In the mainstream civil

service, promotion of civil servants is upon mandatory duration of certain number of years,

favorable scores in performance evaluation, and passing of written examination. In the tertiary

institutions (especially for academics), it is mainly through additional qualification and

publications, while in the banking sector it is based on performance. Whatever the organization

may be, promotion can be a powerful motivating force just as monetary compensation or

intrinsic rewards. Milkorich and Newman (2008) opined that the most important human resource

management issue nowadays is reward structure. They stated that due to global competition and

environmental uncertainty most employers have shifted from traditional ways of reward structure

and design them on the basis of performance, skills knowledge and competency. This they

concluded is to attract, retain and motivate talented employees to achieve their objectives.

Gunu(2009),reported that in the Nigeria banking industry there is relationship between “target

deposit‟ and promotion of bank staff. He asserted that promotion in most of the banks both in the

pre-consolidation and post consolidation eras to a large extent depend on the value of deposits a

bank staff could mobilize. This he concluded has given rise to the emergence of unprofessional

bankers especially in the top management levels. According to Farooq and Ullah (2010), money

is not the only effective motivator in business. Employees may also see factors aside from money

as prime motivators. They noted that in the banking sector motivation can be increased by given

employees more responsibility so that they can feel their contribution is more valuable to the

business and that their contribution is appreciated. They further observed that banks also promise

staff the chance of promotion if they reach a certain standard or target. Thus, promotion of bank

staff is mostly based on meeting deposit mobilization target.

In the same vein, Dauda and Akingbade (2010) noted that financial institutions especially

commercial banks have introduced the process of appraisal which is a huge motivator to

employees. This is because they will be recognized for the value they add (or do not add) to the

business by reviewing their progress and achievements over a certain period. However measures

of financial performance, such as targets based on revenue or deposit mobilization, profit or

19

income, cash flow or interest on loans, are still frequently used for performance measurement in

the banking sector. Haerdle, et al (2011), observed that the main instrument used by banks to

raise their deposit is giving incentives and promotion to staff, who works in the deposit area,

should they have widened the number of depositors by promoting the bank‟s products. Because

of this fact, nowadays financial institutions/banks use the level of deposit in the branch as

standard measuring tool of staff performance. They also noted that since bank staff has

considered the promotion incentive as a benefit, in most instances, clients have been obliged by

concerned staff to open a deposit account to get in turn the bank credit facilities. Obliging clients

either directly or indirectly to deposit their money in the banks in such a way has benefited the

banks in deposit mobilization. Adegbaju and Olokoyo (2008) asserted that the opportunity for

promotion in the banking sector is a powerful motive for good performance. They observed that

most marketers or bank staff works harder to meet or exceed their target deposit so that they can

move to a higher rank within the organization. In his contribution to the impact of target deposit

on promotion, Oyewole (2011) emphasized that most often banks in Nigeria have a policy of

filling all vacant managerial positions from within the organization. This is intended as a signal

to employees that it pays to work hard since the best employees can move up through the ranks.

He however noted that as a result of stiff competition and the consolidation program, banks in

Nigeria start seeking for “hot” high profile marketers even in other banks to make managers of

their banks. It is documented that high performing marketers in the banking sector move from

one bank to the other as they will, and are easily promoted to the next level or two steps ahead of

their present position by other banks. In most cases these marketers use their skills, connections

to increase the deposit of their new employers. Some even go to the extent of moving the high

profile customers they introduced to the former bank to the new bank by all means. It is therefore

no secret that promotion of marketers and bank staff is nowadays highly dependent on meeting

or exceeding deposit mobilization targets.

2.6.1.3. Marketing strategy and deposit mobilization

A marketing strategy combines product development, promotion, distribution, pricing,

relationship management and other elements; identifies the firm's marketing goals, and explains

how they will be achieved, ideally within a stated timeframe. Marketing strategy determines the

choice of target market segments, positioning, marketing mix, and allocation of resources. It is

20

most effective when it is an integral component of overall firm strategy, defining how the

organization will successfully engage customers, prospects, and competitors in the market arena

of corporate strategies, corporate missions, and corporate goals. As the customer constitutes the

source of a company's revenue, marketing strategy is closely linked with sales. As per the

research conducted by TIebbar (1988) studied marketing strategies of banks aimed at inculcating

the habit of thrift among the people. The suggestion is that keeping the rural branches open on

Sundays can augment savings. Direct marketing is also suggested to reduce waiting time

exponentially and enhance customer satisfaction. Erratic behavior of the employees, suspicious

looks of the staff, vague knowledge of the products, undynamic promotional methods etc., may

hamper the banking business in rural areas. In the process of study, Mehta (2010) in his article”

Personal Selling-A Strategy for promoting Bank Marketing “reported that there is lack of

Marketing Communication in Indian Banks .He suggested for adopting banks suitable marketing

promotion strategies for better business. He emphasized that on adoption of personal selling as a

strategy for marketing promotion in Banks the banking business can improve considerably.

In another study made by Gupta, and Mittal (2008), in their article” Comparative Study of

Promotional Strategies of Public and Private Sectors Banks in India “stated that a well -designed

promotional strategy is very important to promote banking services effectively .They studied that

the promotional strategies of private and public sector banks are almost similar. Both types of

banks take the help of almost all type of media to promote their services. The major difference in

the promotional strategies adopted by banks is in the two techniques of the promotion and they

are "Personal Selling" and "Direct Marketing". The difference is that public sector banks do not

adopt the strategies of promotion as personal selling and direct marketing; on the other hand the

same are adopted by private sector banks.

According to A.S.Mohanrani and C.Mahavi, Feb (2007) conducted an empirical study on,

―Product related characteristics, Promotion and Marketing Mix are key tools in determining

Purchase Behavior of Purchase Decision by Teenagers. Results suggest that teenagers are

influenced by updated information of the product and hence they go for information search,

collect information from different dealers on various aspects like price, technology etc. They are

also influenced by peer compulsion of sales talk of the dealers. Teenager„s employees two

strategies- Emotionally convincing & logically convincing to convincer their parents. Logical

teenagers give importance to sales promotion factors like offers & schemes, while emotional

21

teenagers gives importance to aesthetic appearance, color, brand value, popularity &social image

on selecting the products. Marketing strategies comprises of marketing mix which involves 7Ps

to organize business in effective manner. In the process of that a detailed review is collected with

regard to 7Ps and presented in following paragraphs includes - product, price, place, promotion,

people, process and physical evidence.

Vashist (1987), in his doctoral work, evaluated the performance of PSBs with regard to six

indicators, i.e., branch expansion, deposits, credit, priority sector advances, differential rate of

interest, advances and net profits, over the period 1971-83. The study has ranked Indian

Overseas Bank at the top and Dena Bank at the bottom. To improve the performance of

commercial banks, the study has suggested development of marketing strategy for deposit

mobilization, profit planning and strengths, weaknesses, opportunities and threats analysis in

banks.

Robert A.W. Kole& BAS Hillebrand (2003) conducted the study on ―What makes product

development market oriented? Towards a conceptual frame work, author presents a conceptual

frame work detailing the elements of market oriented product development and the relationship

between these elements.

RajaniSofat&PreetiHiro, (2007) conducted a comparative study on Creativity and Innovations in

retail banking- A comparative analysis of financial product offered by ICICI & HDFC bank.

Results suggests that now challenge for banking sector in the current scenario is to design and

innovate the financial product which are convenient to use & continuously meet financial goals

of the customers.

Dixit, V.C. (2004) concludes that for successful marketing and to make it more effective,

identify the customer needs by way of designing new products to suit the customers. The staff

should be well equipped with adequate knowledge to fulfill the customer‟s needs. We should

adopt long-term strategies to convert the entire organization into a customer-oriented one.

Dwivedi, R. (2007) explained that finance functions are important but not as important as the

marketing functions. Friction between the marketing and finance functions would be detrimental

to the smooth development and functioning of any business organization. Finance objectives like

value maximization to shareholders are integral parts of any new strategy adopted by the

organization. But this objective seems to have been lost amidst the flurry of marketing activities

22

focusing on market share. Conscious efforts must be taken to avoid the missing core objective

and for sales growth.

Goerge J. Avlonitis and Kostis A. Indounas ( 2005 ) conducted the study on Pricing objectives

and pricing methods in the services sector, the findings of the study reveal that the objectives,

which are pursued, are fundamentally qualitative rather than quantitative in their nature with a

particular emphasis given on the company„s customers. The pricing methods, which are adopted

by the majority of the companies, refer to the traditional cost-plus method and the pricing

accounts to the market„s average prices.

SubbaRao (1982) conducted a study to find out the influence of different media of advertisement

and different forms of personal selling on the deposit mobilization of commercial banks both in

urban and rural areas. The study suggested that the medium of English Newspapers need not be

used widely as its impact is very little on urban customers and it is almost negligible on rural

depositors. Personal selling or direct contact has been found to be more powerful method, since

it educates the potential rural customers into the bargain.

Chidambaram (1994) studied the promotional mix available to bankers for the marketing of

services such as direct marketing, public relations, social banking and customer meets. The study

concludes that a good promotional mix is one that a) that takes into account the objectives of the

bank and lays emphasis on those services which are of current significance, b) reaches various

customer segments very effectively, c) creates a desire to seek out the services offered, d) builds

a positive image for the bank, and e) strike a balance between cost and effectives

Booz Allen Hamilton (2005) conducted the study on ―Improve productivity to make the most of

branch popularity study has created a framework for understanding the drivers of performance.

As well as staff roles and time-spend, it has identified four other drivers: network size and

structure, sales process effectiveness, performance measurement and management and process

efficiency.