Embed Size (px)

Citation preview

Qatalum_Qatalum_Mettal bulletin.indd 1 11/11/12 11:09 AM

www.metalbulletin.com

supplements

Qatalum_Managing_Mettal bulletin.indd 1 11/11/12 11:10 AM

supplements

OVERVIEW04 A tricky yearWhile the fundamental advantages of producing and processing primary aluminium in the Mena region remain strong, global forces at play in international aluminium markets have had some impact on Arab aluminium smelters and the region’s downstream sector this year. What is the outlook now?

SMELTER FACT-FILES07 Smelter output climbsFact-files for each of the major operational smelters record some key steps in the region’s expansion of production, and list present capacities and products, plus plans for more to come

PROJECT PROFILE15 Ma’aden-Alcoa’s first metal dueThe smelter at Ma’aden-Alcoa’s joint venture integrated aluminium complex in Saudi Arabia will soon be producing its first metal. A project profile gives updates on progress and describes the further steps to come

TECHNOLOGY19 Recent contractsThe Arab aluminium industry continues to invest in the latest technology for production capacity upstream and downstream

DOWNSTREAM20 Downstream developmentsMills, extruders and alloy producers, often set up close by primary smelters, are aiming to supply steady markets at home, while looking to future domestic and regional demand growth and hoped-for recovery in export markets further afield

November 2012 | Arab aluminium | 3

Published by the Metals, Minerals and Mining division of Metal Bulletin Ltd.Metal Bulletin Ltd, Nestor House, Playhouse Yard, London EC4V 5EX. UK registration number: 00142215. Editorial headquarters: 5-7 Ireland Yard, London EC4V 5EX. Tel: +44 20 7827 9977. Fax: +44 20 7928 6892 and +44 20 7827 6495. E-mail: [email protected] Website: http://www.metalbulletin.comMetal Bulletin Focus: Editor: Richard Barrett Associate Editor: Steve Karpel Tel: +44 (0)20 7827 9977Magazine design: Paul RackstrawPublisher: Spencer WicksManaging Director: Raju DaswaniCustomer Services Dept: Tel +44 (0)20 7779 7390Advertising: Tel: +44 20 7827 5220 Fax: +44 20 7827 5206E-mail: [email protected] Sales Director: Mary ConnorsAdvertising Sales Team: Julius Pike, Abdul Zaidi, Susan Zou, Darren ElliottUSA Editorial & Sales: Metal Bulletin, 225 Park Avenue South, 8th Floor, New York, NY 10003.Tel: +1 (212) 213 6202. Toll free: 1-800-METAL-25. Editorial Fax: +1 (212) 213 6617. Sales Fax:+1 (212) 213 6273.

Metal Bulletin:Editor: Alex HarrisonSteel Editor: Vera BleiDeputy Editor, Non-ferrous: Fleur RitzemaRaw Materials Editor: Michelle MadsenEuropean Editor, Steel First: Naomi ChristieSpecial Correspondent: Andrea HotterSenior Correspondents: Stacy Irish, Janie Davies, Shivani Singh, Jethro WookeyCorrespondent: Mark BurtonReporters: Christopher Rivituso, Claire Hack, Alexandra Chapman, Elfi Middelbeek, Nina NasmanNewsdesk Manager: Rod GeorgeSenior Sub-editors: Jeff Porter, Tony Pettengell, James Heywood, Matthew DupuyProduction Designer: Hayley KilminsterPrices Manager: Mary HigginsAssistant Prices Co-ordinator: Joanne WoodNorth American Editor (Steel): Jo IsenbergSingapore: Catalpa Suite 11/F 9 Battery Road, Straits Trading Building, Singapore 049910. Tel: +65 6597 0923. Fax: +65 6597 7099 Asia Editor: Martin RitchieSenior Correspondents: Shivani Singh, Weilyn LooReporter: Daisy TsengSenior Sub-editors: Catherine Yates, Cecil FungSub-editor: Deepali SharmaShanghai: Metal Bulletin Research, Room 305, 3/F,

Azia Center, 1233 Lujiazui Ring Road, Shanghai 200120.Tel: +86 21 5877 0857. Fax: +86 21 5877 0856São Paulo: Rua Tabapua 422, 4th Floor CJ 43/44, CEP: 04533-001, Sao Paulo, Brazil. Tel: +55 11 3078 9331. Fax: +55 11 3168 5867.Latin America Correspondent: Juan WeikLatin America reporter: Carolina GuerraAnnual Subscription: Metal Bulletin is only available on subscription at: UK delivery only: £1,468.15 (£1,330 + £138.15 VAT); North, Central and South America: US$2,850; Europe eurozone*: €2,330; Rest of the World: US$2,850.Single copies: UK delivery only: £60; North, Central and South America: US$155; Europe eurozone*: €110; Rest of the World: US$155.*For subscriptions to European addresses, please quote your sales tax number, otherwise VAT may be charged.Subscription EnquiriesSales Tel: +44 (0)20 7779 7999Sales Fax: +44 (0)20 7246 5200Sales E-mail: [email protected] sales Tel: +1 212 224 3570Asia Pacific sales Tel: +61 3 5229 5445Asia Pacific E-mail: [email protected] sales: [email protected] Fulfilment administrator: Paul Abbott

Metal Bulletin Ltd is a part of Euromoney Institutional Investor PLC: Nestor House, Playhouse Yard, London EC4V 5EX.Directors: Sir Patrick Sergeant, The Viscount Rothermere, Richard Ensor (Executive Chairman), Christopher Fordham (Managing Director), Neil Osborn, Dan Cohen, John Botts, Colin Jones, Diane Alfano, Jaime Gonzalez, Jane Wilkinson, Martin Morgan, David Pritchard, Bashar Al-Rehany.

COPYRIGHT NOTICE: © Metal Bulletin Limited, 2012. All rights reserved. No part of this publication (text, data or graphic) may be reproduced, stored in a data retrieval system, or transmitted, in any form whatsoever or by any means (electronic, mechanical, photocopying, recording or otherwise) without obtaining Metal Bulletin Ltd’s prior written consent. Unauthorised and/or unlicensed copying of any part of this publication is in violation of copyright law. Violators may be subject to legal proceedings and liable for substantial monetary damages for each infringement as well as costs and legal fees. Brief extracts may be used for the purposes of publishing commentary or review only provided that the source is acknowledged. (Registered as a Newspaper at the Post Office. ISSN 0026-0533. Printed by The Magazine Printing Company plc, Enfield, EN3 7NT, UK.)

4 | Arab aluminium | November 2012

Arab aluminium 2012

Overview

It has been a difficult year for the global aluminium industry. While the aluminium markets of the past 12 months have not fallen as hard on the smelters of the Arab world as the likes of Lynemouth in the UK, Kurri Kurri in Australia or Zalco in the Netherlands, as elsewhere 2012 will not be remembered as an ideal year for the region’s aluminium industry to prosper.

Particularly low LME aluminium prices naturally impact every smelter, so a period in which the LME 3-month daily official price plummeted from a $2,000-2,300/tonne band during November-May towards $1,800 at the end of July this year has occupied the management minds of all aluminium producers.

A short-term rally to more than $2,100 brought some temporary relief in early September, but a subsequent fall back to less than $2,000 brought little cheer. The aluminium world remains gripped in an unusual – and unusually long – period in which inventories in LME warehouses hover around the 5 million tonne level – with much of that stock tied up in finance deals.

Although analysts estimate that as much material again could be held in stocks off-exchange, a lot of that additional inventory is similarly tied up, and so physical supply of metal to end-users has generally stayed tight. Much publicised queues to remove metal from LME warehouses are said to have exacerbated a tight physical market.

“The LME system has to be reviewed for the benefit of the industry,” Yousuf Bastaki, projects vice-president at Emirates Aluminium (Emal), told delegates at MB’s 27th International Aluminium Conference in mid-September. “It really affects what happens in the market, especially with the waiting factor to get metal out of warehouses.”

Market analysts consistently point out that all the while interest rates stay low and an LME aluminium contango persists, purchasers needing physical material will continue to compete with investors to buy metal.

The overall effect of very high premiums

resulting from tight markets has been the salvation of some smelters towards the upper end of the cost curve, but even those at the lower end, such as the Middle East’s, are not complacent. High power costs and relatively weak local markets have greatly increased pressure on European smelters, so international aluminium producers with multiple sites like Norsk Hydro have welcomed the fruits of their investment in production in the Middle East – a 50:50 joint venture with Qatar Petroleum in its case. Alcoa looks forward to the cost advantages of its joint venture project with Ma’aden in Saudi Arabia.

“Prices are low and that won’t change any time soon,” Norsk Hydro cfo Jørgen Rostrup told Metal Bulletin at MB’s September conference. “It’s a cost game. We’re focused on the things we can do something about, and it will be much the same as long as the price situation is like it is now.”

At the same event, Laurent Schmitt, then Alba ceo, also stressed efficiency: “We’re located in a region where we have access to competitive

energy, but we’re still working very hard on optimising our energy efficiency,” he said. “Costs will go up all over the world, and even in the Middle East energy is an area where we have to increase efficiency.”

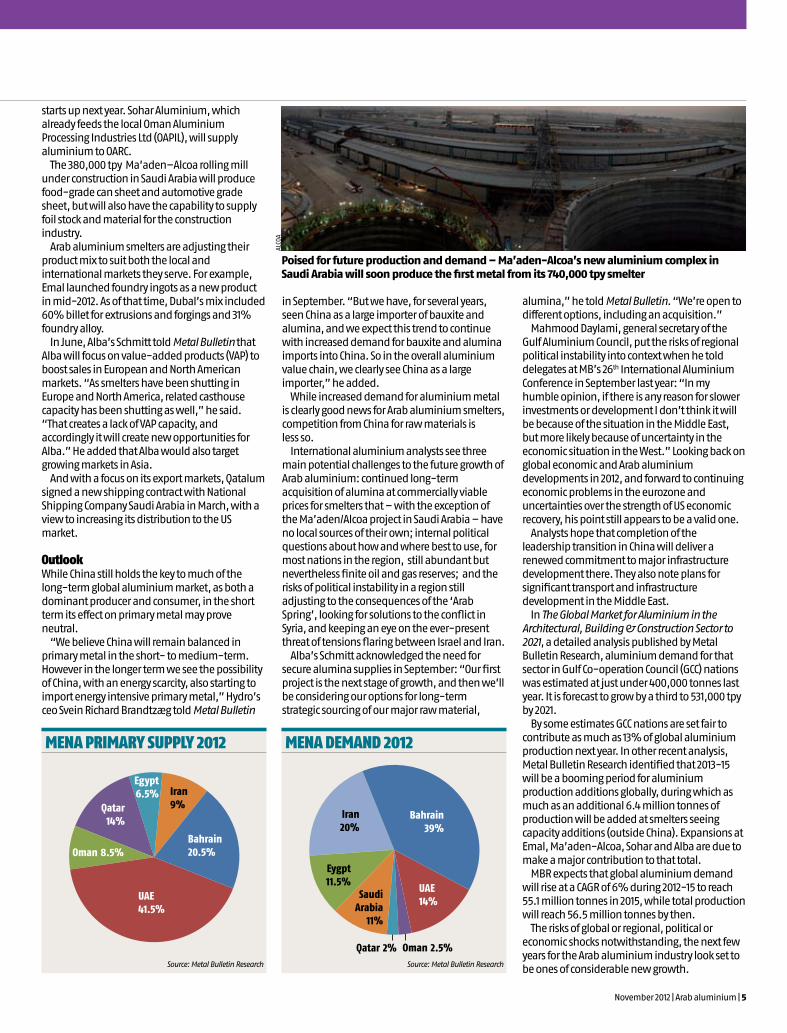

Expansion progress and plansDespite the factors affecting global aluminium markets, progress has been made by the Arab aluminium industry upstream and downstream. As smelter output is curtailed or shut elsewhere, the relative importance of aluminium supply from the Middle East and North Africa continues to climb.

First metal from the 740,000 tpy smelter at Alcoa-Ma’aden’s aluminium complex in Saudi Arabia is due to flow ahead of schedule in December (see page 15). The project’s access to bauxite and alumina from its own mine and refinery upstream, its own natural gas field for energy production, and its ability to produce flat rolled products on site at its own mill – due to come on stream at the end of next year – are expected to maximise cost advantages.

Emirates Aluminium (Emal) has been upgrading the current in its existing Phase 1 potlines to increase production capacity by 50,000 tpy to 800,000 tpy. Work to build Emal’s Phase 2 expansion to 1.3 million tpy also moved forward, with both concrete poured and structural steelwork erected this year for what will become a 520,000 tpy, 1.7 km long potline due to cast first metal in March 2014.

Alba hired BNP Paribas in July this year to assess financing requirements for a sixth potline. With an estimated capex of $2.5 billion, a bankable feasibility study is due to begin by year-end 2012. Additional capacity of 400,000 tpy is planned to bring total capacity to almost 1.3 million tpy.

Qatalum’s output has crept up a little to 600,000 tpy but, although the smelter’s site was designed with subsequent expansion in mind, no build decision has been made on a major extension of capacity as yet. And while smaller than its neighbours in the Arabian Gulf, Egyptalum is reported to have plans to increase production from 320,000 tpy to a full capacity of 400,000 tpy.

Downstream developmentAlthough companies downstream have felt the pressure of high premiums and generally weak international export markets this year, the widely adopted regional strategy to build local businesses as smelter customers, provide employment and make products from aluminium for growing national markets continues implementation. This is sometimes achieved with the energy-saving and logistical benefits of liquid metal transfer from the nearby smelter.

Construction by the Oman Aluminium Rolling Company (OARC, see page 19) is well under way. It will supply flat rolled product markets when it

A tricky yearThe fundamental advantages of producing and processing primary aluminium in the Middle East and North Africa remain strong, but global forces at play in the international aluminium markets have affected Arab aluminium smelters and the region’s downstream sector this year. Richard Barrett reviews the year and considers the outlook

In addition to increasing production capacity, Arab aluminium smelters are putting extra emphasis on value-added products

NORS

K H

YDRO

4 | Arab aluminium | November 2012

Arab aluminium 2012

Overview

It has been a difficult year for the global aluminium industry. While the aluminium markets of the past 12 months have not fallen as hard on the smelters of the Arab world as the likes of Lynemouth in the UK, Kurri Kurri in Australia or Zalco in the Netherlands, as elsewhere 2012 will not be remembered as an ideal year for the region’s aluminium industry to prosper.

Particularly low LME aluminium prices naturally impact every smelter, so a period in which the LME 3-month daily official price plummeted from a $2,000-2,300/tonne band during November-May towards $1,800 at the end of July this year has occupied the management minds of all aluminium producers.

A short-term rally to more than $2,100 brought some temporary relief in early September, but a subsequent fall back to less than $2,000 brought little cheer. The aluminium world remains gripped in an unusual – and unusually long – period in which inventories in LME warehouses hover around the 5 million tonne level – with much of that stock tied up in finance deals.

Although analysts estimate that as much material again could be held in stocks off-exchange, a lot of that additional inventory is similarly tied up, and so physical supply of metal to end-users has generally stayed tight. Much publicised queues to remove metal from LME warehouses are said to have exacerbated a tight physical market.

“The LME system has to be reviewed for the benefit of the industry,” Yousuf Bastaki, projects vice-president at Emirates Aluminium (Emal), told delegates at MB’s 27th International Aluminium Conference in mid-September. “It really affects what happens in the market, especially with the waiting factor to get metal out of warehouses.”

Market analysts consistently point out that all the while interest rates stay low and an LME aluminium contango persists, purchasers needing physical material will continue to compete with investors to buy metal.

The overall effect of very high premiums

resulting from tight markets has been the salvation of some smelters towards the upper end of the cost curve, but even those at the lower end, such as the Middle East’s, are not complacent. High power costs and relatively weak local markets have greatly increased pressure on European smelters, so international aluminium producers with multiple sites like Norsk Hydro have welcomed the fruits of their investment in production in the Middle East – a 50:50 joint venture with Qatar Petroleum in its case. Alcoa looks forward to the cost advantages of its joint venture project with Ma’aden in Saudi Arabia.

“Prices are low and that won’t change any time soon,” Norsk Hydro cfo Jørgen Rostrup told Metal Bulletin at MB’s September conference. “It’s a cost game. We’re focused on the things we can do something about, and it will be much the same as long as the price situation is like it is now.”

At the same event, Laurent Schmitt, then Alba ceo, also stressed efficiency: “We’re located in a region where we have access to competitive

energy, but we’re still working very hard on optimising our energy efficiency,” he said. “Costs will go up all over the world, and even in the Middle East energy is an area where we have to increase efficiency.”

Expansion progress and plansDespite the factors affecting global aluminium markets, progress has been made by the Arab aluminium industry upstream and downstream. As smelter output is curtailed or shut elsewhere, the relative importance of aluminium supply from the Middle East and North Africa continues to climb.

First metal from the 740,000 tpy smelter at Alcoa-Ma’aden’s aluminium complex in Saudi Arabia is due to flow ahead of schedule in December (see page 15). The project’s access to bauxite and alumina from its own mine and refinery upstream, its own natural gas field for energy production, and its ability to produce flat rolled products on site at its own mill – due to come on stream at the end of next year – are expected to maximise cost advantages.

Emirates Aluminium (Emal) has been upgrading the current in its existing Phase 1 potlines to increase production capacity by 50,000 tpy to 800,000 tpy. Work to build Emal’s Phase 2 expansion to 1.3 million tpy also moved forward, with both concrete poured and structural steelwork erected this year for what will become a 520,000 tpy, 1.7 km long potline due to cast first metal in March 2014.

Alba hired BNP Paribas in July this year to assess financing requirements for a sixth potline. With an estimated capex of $2.5 billion, a bankable feasibility study is due to begin by year-end 2012. Additional capacity of 400,000 tpy is planned to bring total capacity to almost 1.3 million tpy.

Qatalum’s output has crept up a little to 600,000 tpy but, although the smelter’s site was designed with subsequent expansion in mind, no build decision has been made on a major extension of capacity as yet. And while smaller than its neighbours in the Arabian Gulf, Egyptalum is reported to have plans to increase production from 320,000 tpy to a full capacity of 400,000 tpy.

Downstream developmentAlthough companies downstream have felt the pressure of high premiums and generally weak international export markets this year, the widely adopted regional strategy to build local businesses as smelter customers, provide employment and make products from aluminium for growing national markets continues implementation. This is sometimes achieved with the energy-saving and logistical benefits of liquid metal transfer from the nearby smelter.

Construction by the Oman Aluminium Rolling Company (OARC, see page 19) is well under way. It will supply flat rolled product markets when it

A tricky yearThe fundamental advantages of producing and processing primary aluminium in the Middle East and North Africa remain strong, but global forces at play in the international aluminium markets have affected Arab aluminium smelters and the region’s downstream sector this year. Richard Barrett reviews the year and considers the outlook

In addition to increasing production capacity, Arab aluminium smelters are putting extra emphasis on value-added products

NORS

K H

YDRO

November 2012 | Arab aluminium | 5

starts up next year. Sohar Aluminium, which already feeds the local Oman Aluminium Processing Industries Ltd (OAPIL), will supply aluminium to OARC.

The 380,000 tpy Ma’aden–Alcoa rolling mill under construction in Saudi Arabia will produce food-grade can sheet and automotive grade sheet, but will also have the capability to supply foil stock and material for the construction industry.

Arab aluminium smelters are adjusting their product mix to suit both the local and international markets they serve. For example, Emal launched foundry ingots as a new product in mid-2012. As of that time, Dubal’s mix included 60% billet for extrusions and forgings and 31% foundry alloy.

In June, Alba’s Schmitt told Metal Bulletin that Alba will focus on value-added products (VAP) to boost sales in European and North American markets. “As smelters have been shutting in Europe and North America, related casthouse capacity has been shutting as well,” he said. “That creates a lack of VAP capacity, and accordingly it will create new opportunities for Alba.” He added that Alba would also target growing markets in Asia.

And with a focus on its export markets, Qatalum signed a new shipping contract with National Shipping Company Saudi Arabia in March, with a view to increasing its distribution to the US market.

OutlookWhile China still holds the key to much of the long-term global aluminium market, as both a dominant producer and consumer, in the short term its effect on primary metal may prove neutral.

“We believe China will remain balanced in primary metal in the short- to medium-term. However in the longer term we see the possibility of China, with an energy scarcity, also starting to import energy intensive primary metal,” Hydro’s ceo Svein Richard Brandtzæg told Metal Bulletin

in September. “But we have, for several years, seen China as a large importer of bauxite and alumina, and we expect this trend to continue with increased demand for bauxite and alumina imports into China. So in the overall aluminium value chain, we clearly see China as a large importer,” he added.

While increased demand for aluminium metal is clearly good news for Arab aluminium smelters, competition from China for raw materials is less so.

International aluminium analysts see three main potential challenges to the future growth of Arab aluminium: continued long-term acquisition of alumina at commercially viable prices for smelters that – with the exception of the Ma’aden/Alcoa project in Saudi Arabia – have no local sources of their own; internal political questions about how and where best to use, for most nations in the region, still abundant but nevertheless finite oil and gas reserves; and the risks of political instability in a region still adjusting to the consequences of the ‘Arab Spring’, looking for solutions to the conflict in Syria, and keeping an eye on the ever-present threat of tensions flaring between Israel and Iran.

Alba’s Schmitt acknowledged the need for secure alumina supplies in September: “Our first project is the next stage of growth, and then we’ll be considering our options for long-term strategic sourcing of our major raw material,

alumina,” he told Metal Bulletin. “We’re open to different options, including an acquisition.”

Mahmood Daylami, general secretary of the Gulf Aluminium Council, put the risks of regional political instability into context when he told delegates at MB’s 26th International Aluminium Conference in September last year: “In my humble opinion, if there is any reason for slower investments or development I don’t think it will be because of the situation in the Middle East, but more likely because of uncertainty in the economic situation in the West.” Looking back on global economic and Arab aluminium developments in 2012, and forward to continuing economic problems in the eurozone and uncertainties over the strength of US economic recovery, his point still appears to be a valid one.

Analysts hope that completion of the leadership transition in China will deliver a renewed commitment to major infrastructure development there. They also note plans for significant transport and infrastructure development in the Middle East.

In The Global Market for Aluminium in the Architectural, Building & Construction Sector to 2021, a detailed analysis published by Metal Bulletin Research, aluminium demand for that sector in Gulf Co-operation Council (GCC) nations was estimated at just under 400,000 tonnes last year. It is forecast to grow by a third to 531,000 tpy by 2021.

By some estimates GCC nations are set fair to contribute as much as 13% of global aluminium production next year. In other recent analysis, Metal Bulletin Research identified that 2013-15 will be a booming period for aluminium production additions globally, during which as much as an additional 6.4 million tonnes of production will be added at smelters seeing capacity additions (outside China). Expansions at Emal, Ma’aden-Alcoa, Sohar and Alba are due to make a major contribution to that total.

MBR expects that global aluminium demand will rise at a CAGR of 6% during 2012-15 to reach 55.1 million tonnes in 2015, while total production will reach 56.5 million tonnes by then.

The risks of global or regional, political or economic shocks notwithstanding, the next few years for the Arab aluminium industry look set to be ones of considerable new growth.

MENA PRIMARY SUPPLY 2012

Iran9%

Egypt6.5%

Qatar14%

Bahrain20.5%

UAE41.5%

Oman 8.5%

MENA DEMAND 2012

SaudiArabia

11%

Iran20%

Eygpt11.5%

Qatar 2% Oman 2.5%

UAE14%

Bahrain39%

Source: Metal Bulletin ResearchSource: Metal Bulletin Research

Poised for future production and demand – Ma’aden-Alcoa’s new aluminium complex in Saudi Arabia will soon produce the first metal from its 740,000 tpy smelter

ALCO

A

Driven byInnovationInnovation is in everything we do and in all the equipment we design and build.

For over 60 years, ECL™ has been the benchmark for reliable, high quality and cost-effective equipment for aluminium smelters, for all technologies.

We will maintain that focus now and in the future.

www.ecl.fr

Arab aluminium 2012

Smelter fact-files

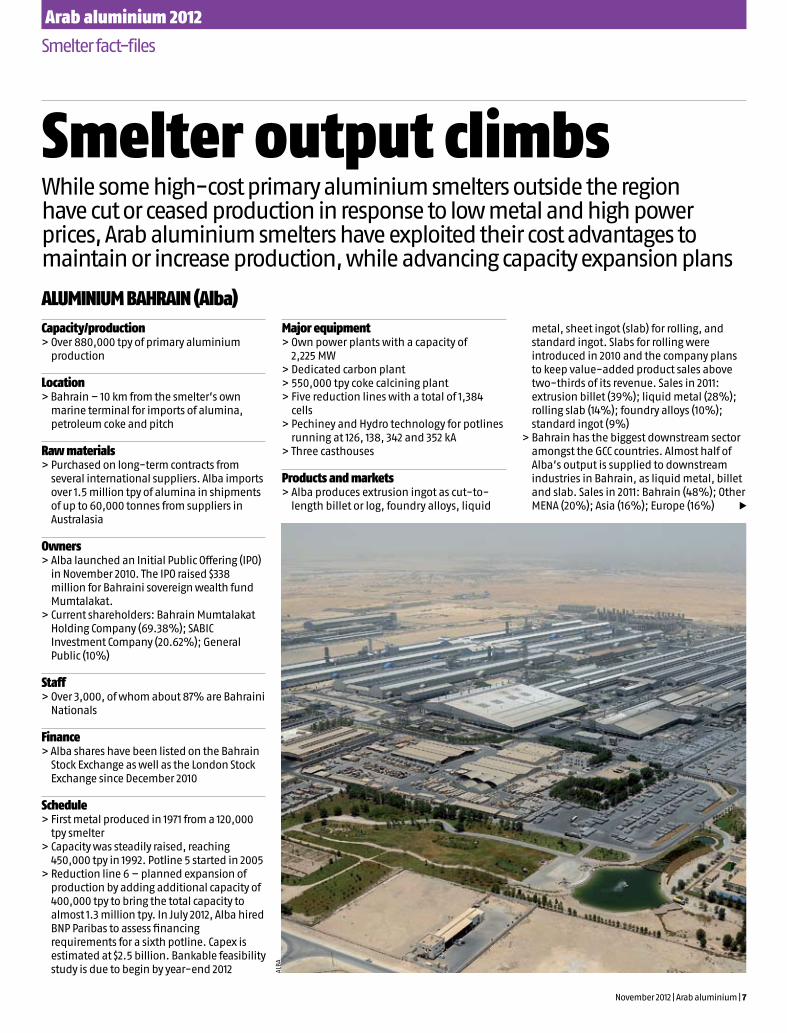

November 2012 | Arab aluminium | 7

Capacity/production> Over 880,000 tpy of primary aluminium

production

Location> Bahrain – 10 km from the smelter’s own

marine terminal for imports of alumina, petroleum coke and pitch

Raw materials> Purchased on long-term contracts from

several international suppliers. Alba imports over 1.5 million tpy of alumina in shipments of up to 60,000 tonnes from suppliers in Australasia

Owners> Alba launched an Initial Public Offering (IPO)

in November 2010. The IPO raised $338 million for Bahraini sovereign wealth fund Mumtalakat.

> Current shareholders: Bahrain Mumtalakat Holding Company (69.38%); SABIC Investment Company (20.62%); General Public (10%)

Staff> Over 3,000, of whom about 87% are Bahraini

Nationals

Finance> Alba shares have been listed on the Bahrain

Stock Exchange as well as the London Stock Exchange since December 2010

Schedule> First metal produced in 1971 from a 120,000

tpy smelter> Capacity was steadily raised, reaching

450,000 tpy in 1992. Potline 5 started in 2005> Reduction line 6 – planned expansion of

production by adding additional capacity of 400,000 tpy to bring the total capacity to almost 1.3 million tpy. In July 2012, Alba hired BNP Paribas to assess financing requirements for a sixth potline. Capex is estimated at $2.5 billion. Bankable feasibility study is due to begin by year-end 2012

Major equipment> Own power plants with a capacity of

2,225 MW> Dedicated carbon plant> 550,000 tpy coke calcining plant> Five reduction lines with a total of 1,384

cells> Pechiney and Hydro technology for potlines

running at 126, 138, 342 and 352 kA> Three casthouses

Products and markets> Alba produces extrusion ingot as cut-to-

length billet or log, foundry alloys, liquid

metal, sheet ingot (slab) for rolling, and standard ingot. Slabs for rolling were introduced in 2010 and the company plans to keep value-added product sales above two-thirds of its revenue. Sales in 2011: extrusion billet (39%); liquid metal (28%); rolling slab (14%); foundry alloys (10%); standard ingot (9%)

> Bahrain has the biggest downstream sector amongst the GCC countries. Almost half of Alba’s output is supplied to downstream industries in Bahrain, as liquid metal, billet and slab. Sales in 2011: Bahrain (48%); Other MENA (20%); Asia (16%); Europe (16%)

Smelter output climbsWhile some high-cost primary aluminium smelters outside the region have cut or ceased production in response to low metal and high power prices, Arab aluminium smelters have exploited their cost advantages to maintain or increase production, while advancing capacity expansion plans

ALUMINIUM BAHRAIN (Alba)

u

ALBA

Arab aluminium 2012

Smelter fact-files

November 2012 | Arab aluminium | 9

Capacity/production> Completed phase 1: 750,000 tpy (upgrading

current to produce 800,000 tpy by end of 2012) > Phase 2: 520,000 tpy

Location> A 6 sq km site in Al Taweelah, Abu Dhabi> Has a purpose-built wharf at Khalifa Port

Raw materials> Emal has a contract with the Abu Dhabi

government to supply natural gas for both phases of the project and has long-term contracts in place for alumina supply

Owners> Joint venture of Dubai Aluminium, Dubal (50%),

and Mubadala Development Company (50%), the Abu Dhabi state investment company

Staff> 2,000 staff employed for phase 1. Another 1,000

staff to be employed for phase 2

Finance> Phase 1 development: $5.7 billion> Phase 2 development: $4.5 billion

Schedule> Joint venture formed in 2007 and construction

commenced in May 2007

> Phase 1 produced first metal at end of 2009 and reached full capacity in January 2011

> Phase 1 DX technology to be upgraded to 380 kA to increase production to 800,000 tpy by the end of 2012

> Phase 2 expansion to increase production to 1.3 million tpy approved in July 2011, commenced implementation in September 2011 and expected to be fully operational by the end of

2014. First potroom concrete poured in April 2012 and first structural steel erected in July 2012. Phase 2 will create an additional potline to the existing two lines. First cast metal from phase 2 expected in March 2014

Major equipment> Phase 1 uses Dubal’s DX smelting technology

running at 350 kA. Engineering, procurement, and construction management (EPCM) contract awarded to the joint venture SNC-Lavalin and Worley Parsons (SLWP) for phase 1 and to SNC-Lavalin for phase 2. Phase 1 has 756 cells in two potlines and a 2,000 MW power plant

> Phase 2 to comprise a single 1.7 km long, 444 reduction cell potline deploying upgraded DX technology (DX+ running at 420 kA) and an additional 1,000 MW to the current power plant

Products> Production includes sow, standard ingots, sheet

ingots and extrusion billets (also Tee ingot). Foundry ingots launched as a new product in mid-2012. Emal also supplies liquid metal to downstream companies based next to the smelter, in Kizad, Khalifa Industrial Zone

Markets> Emal supplies domestic and global markets,

shipping aluminium to 280 customers in 36 countries

EMIRATES ALUMINIUM (Emal), UAE

Capacity/production> Production exceeds 1 million tpy of primary

aluminium from 7 operational potlines> Casthouse capacity exceeds 1 million tpy

Location> A 480 hectare site (including residential area) at

Jebel Ali

Raw materials> Consumes approximately 1,956,000 tpy of

alumina, 300,000 tpy of petroleum coke and 70,000 tpy of coal tar pitch

> Dubal has part shares in alumina refinery projects in Brazil (with Hydro), Guinea (with BHP Billiton, Mubadala and Global Alumina) and Cameroon (with Hindalco and Hydromine of the USA)

Owners> Dubai Aluminium is 100% state owned. Dubal

has a 50% share in Emal in Abu Dhabi

Staff> About 3,800 (as of July 2012), of which almost

16% are UAE nationals

Schedule > First pot for potlines 1-3 started up in October

1979> Potlines 4-9 started up in sequential phases

between October 1990 and February 2008

Major equipment> Power station with a capacity of 2,350 MW

(at 30˚C)> 1,573 reduction cells of five different types: D18,

CD20, D20, DX and DX+, running at 200 kA (D18) up to 420 kA (DX+)

Products and markets> Dubal supplies more than 300 customers in

over 50 countries. The product mix in mid-2012 comprised 60% billet for extrusions and forging, 31% foundry alloy, 7% high purity primary aluminium for electronics and aerospace, and 2% for other applications, including busbar and anode bar. The company’s products were exported to Asia (37%); countries of the Gulf Cooperation Council, Middle East, Africa and the Indian sub-continent (23%); Europe (24%); and the Americas (16%)

DUBAI ALUMINIUM (Dubal), UAE

u

EMAL

DU

BAL

With more than 50 furnaces supplied over the last 10 years to Alba, Sohar Aluminium, Alcoa Fjardaal, Nordural, Qatalum, Hulamin, Novelis, Ma’aden Alcoa Aluminium, Emal and RTA Kitimat, Fives Solios is recognized worldwide for its expertise in furnaces. Fives Solios has delivered some of the largest capacity furnaces in the world with 135t nominal capacity and molten metal capacity up to 169t.To share its customers’ objectives, Fives Solios continues to develop innova-tive solutions that combine technology with industrial and environmental performances.

Fives Solios, designing today the aluminium plants of the future

What about the performance of your furnaces?

More than 50 years of experience in developing solutions for the casthouse

Driving progresswww.fivesgroup.com

Arab aluminium 2012

Smelter fact-files

November 2012 | Arab aluminium | 11

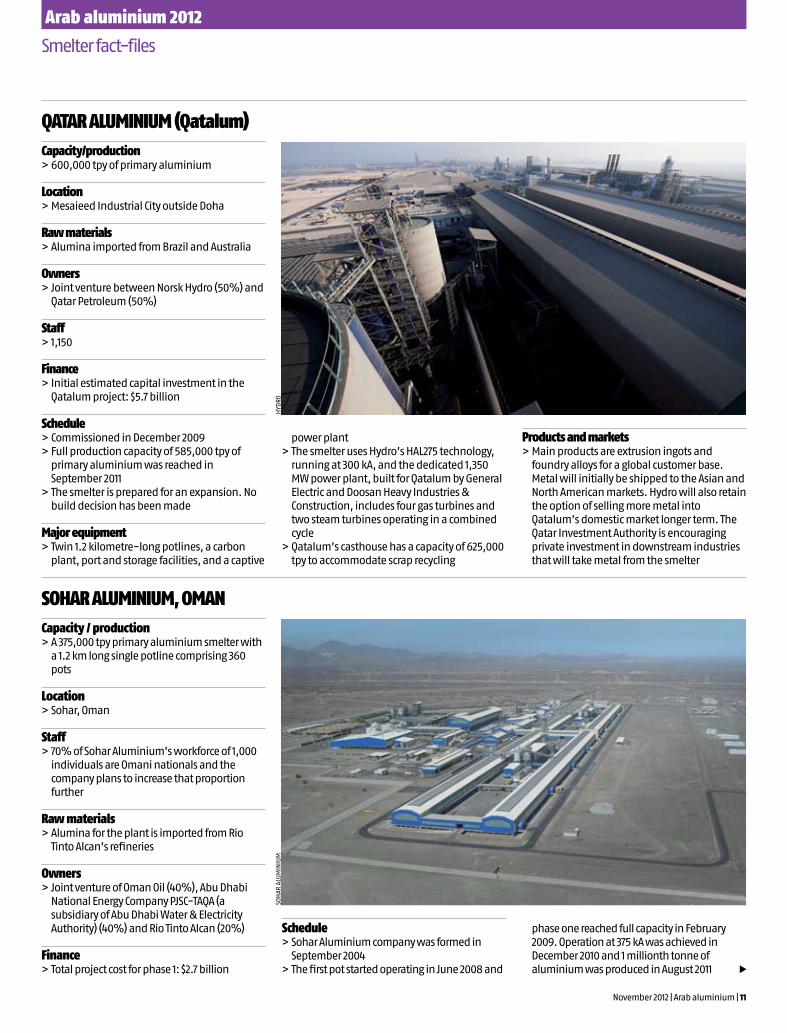

Capacity / production> A 375,000 tpy primary aluminium smelter with

a 1.2 km long single potline comprising 360 pots

Location> Sohar, Oman

Staff> 70% of Sohar Aluminium’s workforce of 1,000

individuals are Omani nationals and the company plans to increase that proportion further

Raw materials> Alumina for the plant is imported from Rio

Tinto Alcan’s refineries

Owners> Joint venture of Oman Oil (40%), Abu Dhabi

National Energy Company PJSC-TAQA (a subsidiary of Abu Dhabi Water & Electricity Authority) (40%) and Rio Tinto Alcan (20%)

Finance> Total project cost for phase 1: $2.7 billion

Schedule> Sohar Aluminium company was formed in

September 2004> The first pot started operating in June 2008 and

phase one reached full capacity in February 2009. Operation at 375 kA was achieved in December 2010 and 1 millionth tonne of aluminium was produced in August 2011

Capacity/production> 600,000 tpy of primary aluminium

Location> Mesaieed Industrial City outside Doha

Raw materials> Alumina imported from Brazil and Australia

Owners> Joint venture between Norsk Hydro (50%) and

Qatar Petroleum (50%)

Staff> 1,150

Finance> Initial estimated capital investment in the

Qatalum project: $5.7 billion

Schedule> Commissioned in December 2009> Full production capacity of 585,000 tpy of

primary aluminium was reached in September 2011

> The smelter is prepared for an expansion. No build decision has been made

Major equipment> Twin 1.2 kilometre-long potlines, a carbon

plant, port and storage facilities, and a captive

power plant> The smelter uses Hydro’s HAL275 technology,

running at 300 kA, and the dedicated 1,350 MW power plant, built for Qatalum by General Electric and Doosan Heavy Industries & Construction, includes four gas turbines and two steam turbines operating in a combined cycle

> Qatalum’s casthouse has a capacity of 625,000 tpy to accommodate scrap recycling

Products and markets> Main products are extrusion ingots and

foundry alloys for a global customer base. Metal will initially be shipped to the Asian and North American markets. Hydro will also retain the option of selling more metal into Qatalum’s domestic market longer term. The Qatar Investment Authority is encouraging private investment in downstream industries that will take metal from the smelter

SOHAR ALUMINIUM, OMAN

QATAR ALUMINIUM (Qatalum)

u

SOH

AR A

LUM

INIU

MH

YDRO

Arab aluminium 2012

Smelter fact-files

November 2012 | Arab aluminium | 11

Capacity / production> A 375,000 tpy primary aluminium smelter with

a 1.2 km long single potline comprising 360 pots

Location> Sohar, Oman

Staff> 70% of Sohar Aluminium’s workforce of 1,000

individuals are Omani nationals and the company plans to increase that proportion further

Raw materials> Alumina for the plant is imported from Rio

Tinto Alcan’s refineries

Owners> Joint venture of Oman Oil (40%), Abu Dhabi

National Energy Company PJSC-TAQA (a subsidiary of Abu Dhabi Water & Electricity Authority) (40%) and Rio Tinto Alcan (20%)

Finance> Total project cost for phase 1: $2.7 billion

Schedule> Sohar Aluminium company was formed in

September 2004> The first pot started operating in June 2008 and

phase one reached full capacity in February 2009. Operation at 375 kA was achieved in December 2010 and 1 millionth tonne of aluminium was produced in August 2011

Capacity/production> 600,000 tpy of primary aluminium

Location> Mesaieed Industrial City outside Doha

Raw materials> Alumina imported from Brazil and Australia

Owners> Joint venture between Norsk Hydro (50%) and

Qatar Petroleum (50%)

Staff> 1,150

Finance> Initial estimated capital investment in the

Qatalum project: $5.7 billion

Schedule> Commissioned in December 2009> Full production capacity of 585,000 tpy of

primary aluminium was reached in September 2011

> The smelter is prepared for an expansion. No build decision has been made

Major equipment> Twin 1.2 kilometre-long potlines, a carbon

plant, port and storage facilities, and a captive

power plant> The smelter uses Hydro’s HAL275 technology,

running at 300 kA, and the dedicated 1,350 MW power plant, built for Qatalum by General Electric and Doosan Heavy Industries & Construction, includes four gas turbines and two steam turbines operating in a combined cycle

> Qatalum’s casthouse has a capacity of 625,000 tpy to accommodate scrap recycling

Products and markets> Main products are extrusion ingots and

foundry alloys for a global customer base. Metal will initially be shipped to the Asian and North American markets. Hydro will also retain the option of selling more metal into Qatalum’s domestic market longer term. The Qatar Investment Authority is encouraging private investment in downstream industries that will take metal from the smelter

SOHAR ALUMINIUM, OMAN

QATAR ALUMINIUM (Qatalum)

u

SOH

AR A

LUM

INIU

MH

YDRO

ABB’s history of powering primary aluminium plants started 45 years ago. Ever since, we have been supplying complete electrification solutions and substations to more than 60 aluminium smelters worldwide. Demands for improved environmental performance and increased energy efficiency, price fluctuations and intense competition are the major challenges aluminium producers face today. ABB meets these challenges by providing state-of-the-art electrification, automation and process optimization solutions – always with the objective to increase your productivity and maximize your return on investment. For more information, visit us at www.abb.com/aluminium

Maximize your return on investment?

Absolutely.

Main Technology Center for electrical,control and instrumentation systems5405 Baden 5 Dättwil, [email protected]

Arab aluminium 2012

Smelter fact-files

November 2012 | Arab aluminium | 13

Major equipment> Bechtel (for the EPCM contract) and Alstom

were major contractors for the construction of the smelter, which has its own 1,000 MW dedicated power plant. The power plant would be expanded should phase 2 come on line. The smelter uses AP36 technology running at 375 kA

Products and markets> The casthouse produces ingots, sows and

liquid metal. The ingots and sows are sold to Rio Tinto Alcan for delivery to markets including China, Malaysia and Indonesia

> Sohar Aluminium’s long-term plan is to use around 60% of the smelter’s aluminium production for local companies and to export the balance. Oman Aluminium Processing Industries Ltd (OAPIL) is one of the smelter’s downstream customers that is currently operational

> A second downstream customer, Oman Aluminium Rolling Company (OARC) is under construction and once commissioned will supply to the food container and food-preservation foil markets, as well as automotive and air conditioner markets. Italy’s Fata EPC was

awarded the contract to build the aluminium rolling mill in Sohar. The 160,000 tpy plant will contain a Hazelett continuous caster, while Fata Hunter, a division of Fata SpA, will supply a hot rolling mill with cold rolling and finishing equipment. The first production from OARC is expected to start in 2013.

> Oman’s downstream aluminium sector

continues development and space has been set aside at Sohar for more industries to take liquid metal from the smelter. Development of the Sohar Free Zone is expected to attract further partners to Oman. Sohar Aluminium has its own dedicated port facility in the Sohar Industrial Port Complex (a joint venture between Oman and the Port of Rotterdam)

Capacity/production> 320,000 tpy

Location> Nag Hammady HQ. Smelter 100 km north

of Luxor

Finance> Listed on the Egyptian Stock Exchange

Schedule> Initiated in 1972 with an inaugural capacity

of 100,000 tpy.> First two potlines constructed in 1975 and

expanded to five in 1983. New prebaked

potline no. 6 started in October 1997. Plans to expand capacity to 400,000 tpy

Major equipment> Operates 12 potrooms

Products and markets> Smelter produces slab, ingot, T-bar, billet

and wire rod. Associated rolling mill produces hot and cold rolled sheet, coil and plate for Egyptian aluminium fabricators and international markets. Exports from the port in Alexandria. Markets include Europe, the USA, the Arab Gulf, Turkey and Asia

EGYPTIAN ALUMINIUM (Egyptalum), EGYPT

14 | Arab aluminium | November 2012

Arab aluminium 2012

Project profile

November 2012 | Arab aluminium | 15

The long-awaited Ma’aden-Alcoa integrated aluminium joint venture in Saudi Arabia is about to become a reality with the first metal expected to be poured on 12 December 2012, to be followed by the first coil from its rolling mill in December 2013 and production from its bauxite mine and alumina refinery in 2014.

At the end of 2009 the joint venture of Alcoa of the USA and Saudi Arabian Mining Company (Ma’aden) entered into an agreement to build the largest and world’s lowest-cost integrated aluminium complex in the highly populated Middle East, where there is growing aluminium demand in markets such as packaging, automotive and building/construction.

Ma’aden has majority ownership (74.9%) of the $10.8 billion project, which is expected to gain efficiencies from not only integrating the bauxite mine, alumina refinery, aluminium smelter and rolling mills but also from low energy costs. Alcoa has the remaining share of the project (25.1%)

and has the option to increase its ownership to 40%.

The joint venture partners maintain that this will indeed be the lowest-cost integrated aluminium complex in the world.

“One of the reasons why this project is so low on the cost curve is because it includes its own natural gas field,” Klaus Kleinfeld, Alcoa’s chairman and chief executive officer, explained earlier this month at the company’s Investor Day in New York.

In addition, the partners are bringing in the best technologies in their class throughout the complex and developing the local skills and operational routines to extract the most efficient, high-quality production from them, an Alcoa spokeswoman says.

She adds that conservation of resources is a key design factor throughout the facility. For example, the refinery will utilise an advanced system to treat, recycle and conserve significant

volumes of water. “Conserving resources is crucial to maintenance of low operating costs,” she says.

Both partners are expected to reap considerable benefits from this project, which is aimed at capitalising on growth in the Mena region. Kay Meggers, Alcoa’s executive vp and group president of its Global Rolled Products unit, says that while the major end-use market served will be packaging (providing body-, end- and tab-stock for aluminium beverage cans), it will also serve the foil stock, building/construction and automotive industries in the region and beyond.

Diversification Kleinfeld points out that the project is particularly important to the Kingdom of Saudi Arabia and its focus on diversifying the economy and creating jobs.

“This … will place Saudi Arabia among the world’s foremost aluminium producers by combining the highest standards of quality with the exceptional cost competitiveness of this world-class project,” Khalid Mudaifer, Ma’aden’s president and chief executive officer, said in a statement. “These new capabilities will help establish downstream industries in Saudi Arabia, using aluminium that has been mined, refined, smelted and rolled in the Kingdom. It is also fully compatible with the national strategy of developing national resources to create sustainable wealth and employment for Saudis, as well as enabling the replacement of a wide range of imports with cost-effective, high-quality domestic products.”

The joint venture is also expected to help Alcoa meet its goal of lowering its position on the cost curve, the company spokeswoman says. “Our strategy in our upstream businesses has remained consistent – to move down the refining cost curve from the 30th percentile to the 23rd percentile and to move down the smelting cost curve from the 51st percentile to the 41st percentile by 2015,” she says, observing that, company-wide, Alcoa is now holding steady on the refining cost curve at the 30th percentile and has already moved four points down the smelting curve to the 47th percentile.

The Ma’aden-Alcoa project is expected to move Alcoa down two percentage points on the refining cost curve as well as two points down on the smelting cost curve. “On the smelting side we have a clear plan to close, curtail or fix our high cost capacity,” she says, observing that the company has already made progress in doing so. “We were the first in the industry to announce production cuts and since the beginning of 2012 we have taken 14% of our highest-cost capacity offline.”

Lower costs Meanwhile, she says that Alcoa is also bringing the lowest-cost capacity in the world, including Ma’aden, on-stream: “That is helping to further lower our overall production cost base.”

Ma’aden – Alcoa’s first metal due

The potroom of the 740,000 tpy smelter in Ras Al Khair will start up next month

The Ma’aden-Alcoa integrated aluminium complex in Saudi Arabia is poised to produce its first metal. The project will supply products to the packaging, automotive and construction sectors in the region and beyond. Myra Pinkham reviews progress and the next steps forward

ALCO

A

Integrating shredding with steelmaking

u

16 | Arab aluminium | November 2012

www.aidaalloys.com

Aluminum grain refiner.

Aluminum master alloys: altib, alsr10, alsi50, almn20, alti10, alv10, alzr10 in ingot, rod or castcut forms.

Alloying compact as tablet and briquette form: Elements available are Cu, Cr, Ni, Fe, Mn, Zn, Ti.

Ceramic foam filter: We can produce all kinds of size CFF to satisfy customers’ needs.

Aluminum melting fluxes: Available in powder, granular and tablet form.

Silicon metal lumps & Ferro Alloys: Manganese Metal Lumps/Powder/Briquette.

The products have been exported to many countries in Asia, Europe, American, Japan and Asia.

SIHUI AIDA ALLOYS CO., LTDAdd: Nanjiang Industrial Park, Sihui,

Guangdong Province. P. R. China 526241Tel: 86 758 3855723/3851721 Fax: 86 758 3851719

Mobile: 86 18666511033/ 13509958238/ 13902892161E-mail: [email protected]

SHENZHEN AIDA ALUMINUM ALLOYS CO., LTD

16 | Arab aluminium | November 2012

www.aidaalloys.com

Aluminum grain refiner.

Aluminum master alloys: altib, alsr10, alsi50, almn20, alti10, alv10, alzr10 in ingot, rod or castcut forms.

Alloying compact as tablet and briquette form: Elements available are Cu, Cr, Ni, Fe, Mn, Zn, Ti.

Ceramic foam filter: We can produce all kinds of size CFF to satisfy customers’ needs.

Aluminum melting fluxes: Available in powder, granular and tablet form.

Silicon metal lumps & Ferro Alloys: Manganese Metal Lumps/Powder/Briquette.

The products have been exported to many countries in Asia, Europe, American, Japan and Asia.

SIHUI AIDA ALLOYS CO., LTDAdd: Nanjiang Industrial Park, Sihui,

Guangdong Province. P. R. China 526241Tel: 86 758 3855723/3851721 Fax: 86 758 3851719

Mobile: 86 18666511033/ 13509958238/ 13902892161E-mail: [email protected]

SHENZHEN AIDA ALUMINUM ALLOYS CO., LTD

Arab aluminium 2012

Project profile

November 2012 | Arab aluminium | 17

The alumina refinery, smelter and rolling mill are located within the new industrial zone of Ras Al Khair on the east coast of Saudi Arabia, where they can utilise the infrastructure there. The Alcoa spokeswoman explains that not only includes low-cost, clean power generation, but also port and rail facilities.

The Ras Al Khair industrial zone is a 77 square km site located 90 km north of Al Jubail on the Arabian Gulf coast, which, in addition to housing the three joint venture facilities, is where the Ma’aden Phosphate Company’s integrated chemical and fertilizer facility is located. That complex consists of a phosphoric acid plant, a

sulphuric acid plant, a diammonium phosphate (DAP) granulation plant, a power co-generation plant and desalination plant, as well as related infrastructure.

Once the new 4 million tpy bauxite mine in Al Ba’itha, near Quiba in the north, is operational in 2014, bauxite feedstock from the mine, which has over 30 years of reserves, will be transported by rail to the alumina refinery, which will initially produce 1.8 million tpy of alumina. This refinery, which is also expected to be up and running in 2014, has been designed to be able to increase its capacity.

The joint venture partners say the fact that the

740,000 tpy aluminium smelter, which is co-located with the rolling mill, will be commissioning the first 180 of its total 740 pots in mid-December, as opposed to doing so next year, is a significant accomplishment, especially given that they will be able to do so safely and on budget. The smelter is expected to progress from first concrete poured to first hot metal in 25 months.

“For a big capital project such as this one, the ability to get revenue and earnings from that project in advance of when you anticipated is very good for the return of the project,” Chris Ayers, Alcoa’s executive vp and group president of its Global Primary Products unit, told investors. “But as important as the first hot metal, is the last hot metal,” he says. “We are not doing anything to sacrifice that either.”

The Alcoa spokeswoman says that the Ma’aden-Alcoa smelter will be the lowest-cost smelter within the Alcoa system, and is being delivered as a complete package, with a carbon plant, ingot caster and associated infrastructure. Like the alumina refinery, it is designed for expansion.

Alumina quality critical Until the dedicated bauxite mine and refinery comes on line in 2014, Alcoa will be supplying the joint venture’s smelter with alumina. In fact, at the end of October the first shipment of alumina –about 47,000 tonnes – departed from Alcoa’s Bunbury Port facility in Western Australia for the Ras Al Khair smelter.

Ken Wisnoski, president of Alcoa Global Primary Products Growth, says that the supply of uniformly high-quality alumina is essential for the efficient operation of a smelter at any time, but it is even more important during the critical commissioning and early operational periods. “The ability to source alumina that can be relied on for its consistent quality, shipment after shipment, is a critical advantage to us,” he says in a statement. “It’s reassuring for us that Alcoa’s West Australian operations are solidly behind us in this joint venture.”

The complex’s rolling mill, which will initially produce 380,000 tpy of food-grade can sheet, and will also be able to produce automotive grade sheet, building/construction sheet and foil stock sheet, is right in the flow path of the smelter in Ras Al Khair. Alcoa says that this technologically advanced rolling mill, which will be the first in the Middle East capable of producing food-grade can sheet, is to produce its first coil by December 2013, which is approximately when Alcoa’s automotive sheet expansion in Davenport, Iowa, is expected to come on-stream at about the same time.

“This is a good, solid project for us,” Ayers says. “It is exciting that we will be getting the project on line this quickly and that we will be the lowest cost producer out there.”

The author is a specialist writer based in New York.

BASIC PROJECT FACTSLocations> Bauxite mine at Al Bai’itha, near Quiba, Saudi Arabia> Alumina refinery, aluminium smelter and hot rolling mill at Ras Al Khair on the Gulf Coast of Saudi Arabia, 90 km north of Jubail. Ras Al Khair is the location for Ma’aden’s 77 sq km minerals industry complex

Initial capacity> 4 million tpy bauxite mine, expected to be operational in 2014> 1.8 million tpy alumina refinery, expected to be operational in 2014> 740,000 tpy aluminium smelter, first hot metal expected 12 December 2012> 380,000 tpy rolling mill, first coil expected by December 2013

Ownership> Ma’aden, the Saudi Arabian Mining Co. (74.9%) > Alcoa 25.1% (with a right to increase its share to 40%)

InvestmentTotal $10.8 billion including: > $202 million engineering, procurement and construction management (EPCM) contract for the mine and refinery with Worley Parsons and Fluor Enterprises > $73 million contract for engineering and oversight services with Fluor Enterprises > $590 million EPC-LSTK contract for the execution of the rolling mill> $74 million contract with Fluor Arabia for overall project management services and engineering/procurement services for the infrastructure at Ras Al Khair

Finance> Phase 1: The joint venture partners signed $4.0 billion of the financing for the smelter and rolling mill project with 17 financial institutions, including Saudi Arabia’s Public Investment Fund in 2010 > Futher funding of around $320 million by the

Saudi Industrial Development Fund for Phase 1 was executed in October 2012 > Phase 2: On 16 October 2011, Ma’aden and Alcoa signed a financing agreement for $1 billion for the mining and refinery project, in addition to $1 billion loan approval from Saudi Arabia’s Public Investment Fund. > Further funding of around $160 million by the Saudi Industrial Development Fund was to be evaluated

Major equipment> Ingot and billet casting systems from Wagstaff and Alcoa> Hot and cold rolling mills from SMS Siemag> Coating line from Germany’s BWG Bergwerk- und Walzwerk-Maschinenbau > Preheat furnaces from Ebner

Raw materials> Bauxite feedstock for the planned alumina refinery will be transported by rail from the new mine at Al Ba’itha> Alcoa will supply alumina to the smelter from its Bunbury Port facility in Western Australia until the mine and refinery start up

Products and markets> While packaging, including body-, end- and tab-stock for aluminium beverage cans, will be the major end-use market sector, it will also serve the foil stock, building/construction and automotive industries for the Middle East and beyond

Other details> It is expected to be the lowest cost aluminium production facility globally, partly due to its ownership of its own natural gas field> It is proceeding on time (and in some cases ahead of schedule) and on budget> It is expected to contribute to Alcoa’s goal of moving down the cost curve by seven points for refining and 10 points for smelting by 2015, and is expected to move Alcoa down two points on both the refining and the smelting cost curves

Using our innovative diagnostic methods, we quickly track down the causes of any plant malfunctions. After all, the best brains in the business are behind our Technical Service. Our experts systematically check your plant components and get straight to the heart of the problem. That ensures the performance of your entire plant.

Innovative X-Cellize® service modules andhighly qualifi ed service technicians are the vital factors that ensure stable overall productivity of plants at low maintenance costs. To fi nd out more, go to www.sms-siemag.com.

SMS Siemag – service is in our genes.

X-Cellize® – service modules. Effective and effi cient

Focused on quality and reliability.

SMS SIEMAG AG

Eduard-Schloemann-Strasse 4 Phone: +49 211 881-0 E-mail: [email protected] Düsseldorf, Germany Fax: +49 211 881-4902 Internet: www.sms-siemag.com

Service_209x274_e.indd 1 12.10.12 12:59

Arab aluminium 2012

Technology

November 2012 | Arab aluminium | 19

Ma’aden-Alcoa, Saudi ArabiaAs a large integrated aluminium complex, the Saudi Arabian Ma’aden-Alcoa joint venture project has called on international engineering businesses and plantmakers.

One example for upstream work is ABB, which earlier this year won orders worth around $24 million from Ma’aden Aluminium Company (MAC) to execute a fast-track transmission substation project. ABB’s contract is for the design, engineering and supply of a new 380 kV outdoor gas-insulated switchgear (GIS) substation at the Ras Al Khair power plant that will export 800 megawatt (MW) of power from the plant to the national transmission grid and feed the new aluminium smelter.

ABB’s scope of supply includes high-voltage outdoor gas-insulated switchgear, communication and auxiliary systems and IEC 61850 compliant substation automation, control and protection. These ‘containerised’ systems are factory assembled and pre-commissioned to speed up on-site installation.

Downstream, SMS Siemag will supply the 380,000-400,000 tpy hot and cold rolling complex for aluminium strip. The complex comprises a hot rolling mill with roughing stand and four-stand finishing mill plus a four-stand tandem cold rolling mill with coil transport system.

SMS Siemag will supply the complete electrics, and the automation systems already fully tested in the plantmaker’s new ‘test field’ at its works in Germany before shipping.

Much of the mills’ output will be for beverage cans, but SMS Siemag is also supplying an additional single-stand cold rolling mill, ordered in March this year, to produce material as thin as 0.15 mm for the automotive industry. Maximum coil width will be 2,100 mm. A new 50,000 tpy annealing and coating line, which “paves the way for Ma’aden-Alcoa to enter the market for aluminium car body sheets,” states SMS Siemag, will also be supplied.

OARC, Oman

In April 2011, FATA EPC, a division of FATA SpA, was awarded the US$380 million turnkey EPC contract for the Oman Aluminium Rolling Company (OARC) facility in Sohar, Oman.

This complete aluminium flat product plant will be the largest downstream user of metal from Sohar Aluminium. FATA’s total project manpower is approximately 1,600 people as construction of the facility is progressing.

Partial hand-over is scheduled for August 2013 to begin initial production, leading to production ramp up to the 160,000 tpy design capacity. The project will provide 275 direct jobs at full production and will also generate many other jobs required to support the operation of the plant.

Equipment being installed in the plant will comprise: a Hazelett belt caster; a hot rolling mill, a cold rolling mill and a tension levelling line by FATA Hunter; furnaces provided by GNA and filters by STAS; coil annealers by Otto Junker; slitter by Kampf; roll grinding equipment by Tenova Pomini.

This plant will enable OARC to produce aluminium sheet of very thin gauges and high surface quality with shorter product delivery time and world class production costs, says

FATA. The rolling mill will serve the aluminium food-container and food-preservation foil markets, along with material for the automotive heat exchanger and commercial and residential air conditioning markets. The mill is well positioned for the growing regional demand, and sales are expected to reach international markets as well.

Based in Turin, Italy, FATA SpA (a Finmeccanica Company) is an engineering, technology, procurement and construction company. In the aluminium sector, FATA is focusing its efforts in the GCC market, providing its EPC services to the primary, secondary and downstream industries.

Qatalum, QatarAs one of the EPC contractors involved in the Qatalum primary aluminium project, Italy’s FATA implemented, on a full LSTK EPC basis, both the casthouse and the anode baking plant. The casthouse has a capacity of 350,000 tpy of extrusion ingot and 250,000 tpy of foundry ingots. The anode baking plant has a production capacity of 368,000 anodes per year, and the storage facility can handle 18,000 green anodes and 13,000 baked anodes. Both projects were executed on schedule.

Recent contractsThe Arab aluminium industry continues to invest in the latest technology for production capacity and quality upstream and downstream

SMS

SIEM

AG

Integrating shredding with steelmaking

Hot and cold rolling mill stands for Ma’aden-Alcoa under assembly at SMS Siemag’s workshop in Germany

ABB high-voltage switchgear similar to the substation it is supplying for Ma’aden-Alcoa’s Saudi aluminium project

ABB

Qatalum’s casthouse can produce both extrusion and foundry ingots

FATA

FATA

Using our innovative diagnostic methods, we quickly track down the causes of any plant malfunctions. After all, the best brains in the business are behind our Technical Service. Our experts systematically check your plant components and get straight to the heart of the problem. That ensures the performance of your entire plant.

Innovative X-Cellize® service modules andhighly qualifi ed service technicians are the vital factors that ensure stable overall productivity of plants at low maintenance costs. To fi nd out more, go to www.sms-siemag.com.

SMS Siemag – service is in our genes.

X-Cellize® – service modules. Effective and effi cient

Focused on quality and reliability.

SMS SIEMAG AG

Eduard-Schloemann-Strasse 4 Phone: +49 211 881-0 E-mail: [email protected] Düsseldorf, Germany Fax: +49 211 881-4902 Internet: www.sms-siemag.com

Service_209x274_e.indd 1 12.10.12 12:59

Arab aluminium 2012

Technology

November 2012 | Arab aluminium | 19

Ma’aden-Alcoa, Saudi ArabiaAs a large integrated aluminium complex, the Saudi Arabian Ma’aden-Alcoa joint venture project has called on international engineering businesses and plantmakers.

One example for upstream work is ABB, which earlier this year won orders worth around $24 million from Ma’aden Aluminium Company (MAC) to execute a fast-track transmission substation project. ABB’s contract is for the design, engineering and supply of a new 380 kV outdoor gas-insulated switchgear (GIS) substation at the Ras Al Khair power plant that will export 800 megawatt (MW) of power from the plant to the national transmission grid and feed the new aluminium smelter.

ABB’s scope of supply includes high-voltage outdoor gas-insulated switchgear, communication and auxiliary systems and IEC 61850 compliant substation automation, control and protection. These ‘containerised’ systems are factory assembled and pre-commissioned to speed up on-site installation.

Downstream, SMS Siemag will supply the 380,000-400,000 tpy hot and cold rolling complex for aluminium strip. The complex comprises a hot rolling mill with roughing stand and four-stand finishing mill plus a four-stand tandem cold rolling mill with coil transport system.

SMS Siemag will supply the complete electrics, and the automation systems already fully tested in the plantmaker’s new ‘test field’ at its works in Germany before shipping.

Much of the mills’ output will be for beverage cans, but SMS Siemag is also supplying an additional single-stand cold rolling mill, ordered in March this year, to produce material as thin as 0.15 mm for the automotive industry. Maximum coil width will be 2,100 mm. A new 50,000 tpy annealing and coating line, which “paves the way for Ma’aden-Alcoa to enter the market for aluminium car body sheets,” states SMS Siemag, will also be supplied.

OARC, Oman

In April 2011, FATA EPC, a division of FATA SpA, was awarded the US$380 million turnkey EPC contract for the Oman Aluminium Rolling Company (OARC) facility in Sohar, Oman.

This complete aluminium flat product plant will be the largest downstream user of metal from Sohar Aluminium. FATA’s total project manpower is approximately 1,600 people as construction of the facility is progressing.

Partial hand-over is scheduled for August 2013 to begin initial production, leading to production ramp up to the 160,000 tpy design capacity. The project will provide 275 direct jobs at full production and will also generate many other jobs required to support the operation of the plant.

Equipment being installed in the plant will comprise: a Hazelett belt caster; a hot rolling mill, a cold rolling mill and a tension levelling line by FATA Hunter; furnaces provided by GNA and filters by STAS; coil annealers by Otto Junker; slitter by Kampf; roll grinding equipment by Tenova Pomini.

This plant will enable OARC to produce aluminium sheet of very thin gauges and high surface quality with shorter product delivery time and world class production costs, says

FATA. The rolling mill will serve the aluminium food-container and food-preservation foil markets, along with material for the automotive heat exchanger and commercial and residential air conditioning markets. The mill is well positioned for the growing regional demand, and sales are expected to reach international markets as well.

Based in Turin, Italy, FATA SpA (a Finmeccanica Company) is an engineering, technology, procurement and construction company. In the aluminium sector, FATA is focusing its efforts in the GCC market, providing its EPC services to the primary, secondary and downstream industries.

Qatalum, QatarAs one of the EPC contractors involved in the Qatalum primary aluminium project, Italy’s FATA implemented, on a full LSTK EPC basis, both the casthouse and the anode baking plant. The casthouse has a capacity of 350,000 tpy of extrusion ingot and 250,000 tpy of foundry ingots. The anode baking plant has a production capacity of 368,000 anodes per year, and the storage facility can handle 18,000 green anodes and 13,000 baked anodes. Both projects were executed on schedule.

Recent contractsThe Arab aluminium industry continues to invest in the latest technology for production capacity and quality upstream and downstream

SMS

SIEM

AG

Integrating shredding with steelmaking

Hot and cold rolling mill stands for Ma’aden-Alcoa under assembly at SMS Siemag’s workshop in Germany

ABB high-voltage switchgear similar to the substation it is supplying for Ma’aden-Alcoa’s Saudi aluminium project

ABB

Qatalum’s casthouse can produce both extrusion and foundry ingots

FATA

FATA

20 | Arab aluminium | November 2012

Arab aluminium 2012

Downstream

Much of the downstream sector in the Gulf Co-operation Council (GCC) countries of Bahrain, Kuwait, Oman, Qatar, Saudi Arabia and UAE is slowing – trapped between shrinking export demand and rising metal prices due to increased premiums.

The outlook for 2013 is worse than it was six months ago, but this may prove to be a temporary phenomenon since domestic business in the Gulf is as yet relatively unaffected by the world’s market troubles.

Even a slow revival in the export markets and a resolution of uncertainties about premiums could markedly improve downstream prospects next year.

There are four major downstream sectors in the GCC region: flat rolled products (including foil); extrusions; cable, wire and rod; and secondary ingot and casting alloys.

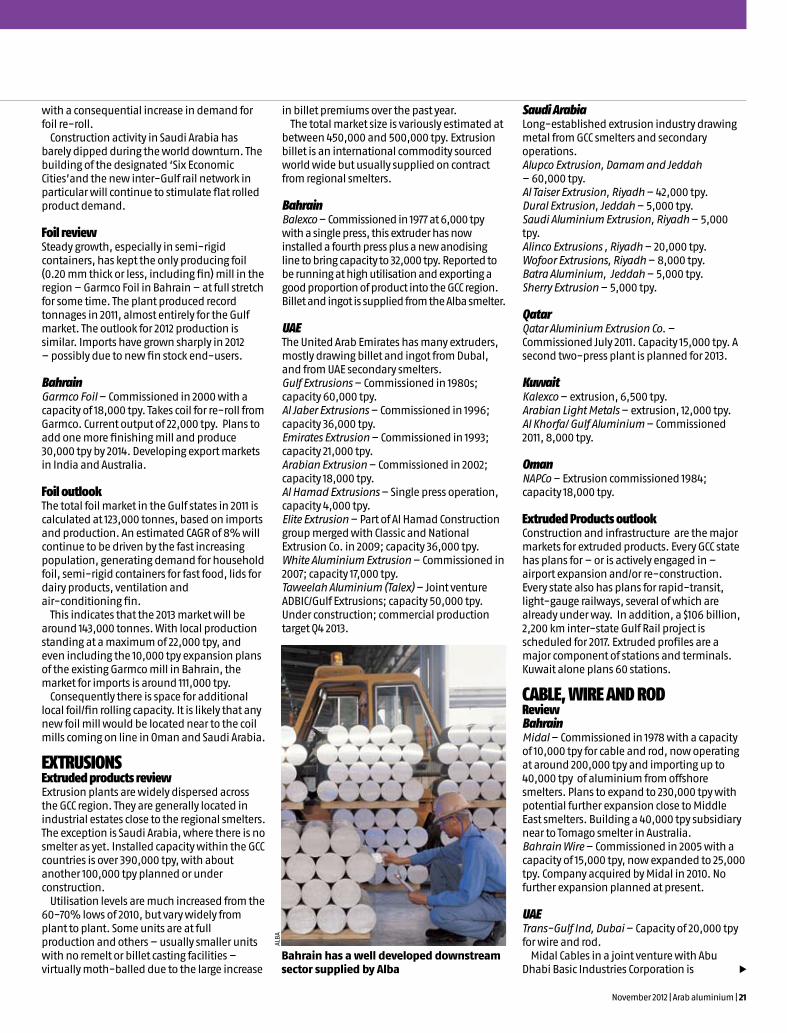

FLAT ROLLED PRODUCTSPlate, sheet and strip review Today there are three working sheet and coil plants in the Gulf with a combined production capacity approaching 250,000 tpy.

BahrainGulf Aluminium Rolling Mills (Garmco) – Commissioned in 1986 with a capacity of 40,000 tpy for sheet and coil. Now operating at 165,000 tpy – all direct-chill hot rolled slab. Around 70% of output is for export outside the Gulf. Installed a new tension levelling/de-greasing line in 2012. Plans to expand by 30,000 tpy and install 100% in- house slab casting capacity over the next five years. Has subsidiaries in Australia, USA, Singapore, China, South Korea, Hong Kong and Europe.

UAEProfiles RHF, Sharjah – Commenced operation in 1991. Sheet and coil mill capacity 70,000 tpy – all continuous-cast (CC) mostly for in-house coil coater and profiled building cladding for the Gulf market. Alumill Tech Gulf, Raz al Khaimah – Commenced operation in early 2012. Sheet and coil mill capacity 15,000 tpy – all CC mostly for in-house coil coater for Gulf market. Plans to expand to 30,000 tpy in the near future.

Plate, sheet and strip outlook Over the next 2-3 years, flat rolled product business in the Gulf will be transformed by new capacity under construction.

Saudi ArabiaMAC– Ma’aden Aluminium Company, Raz az Zawr (Alcoa/Saudi joint venture) – Scheduled for commissioning in 2013 and commercial

production ramp up in 2014. Rated capacity: 380,000 tpy from new state-of-the-art mills. Targeting can stock, automotive heat-treated and non-heat-treated sheet, building and construction sheet and foil stock markets. Casthouse is due to commission shortly.

OmanOARC– Oman Aluminium Rolling Company, Sohar (Takamul) – Scheduled for commissioning in 2013 and commercial production in 2014. Rated capacity: 160,000 tpy from Hazelett Super Caster. Targeting sheet and coil, fin and foil re-roll markets. Fin coating line under consideration.

Flat rolled product marketsTotal annual market demand in the GCC states for plate, sheet and strip in 2012 is estimated at 287,000 tonnes, including around 110,000 tonnes of can stock. At present 145,000 tpy is exported. When all new plants are in full production by 2015, total capacity will be approaching 800,000 tpy, which will leave an ‘overhang’ of about 370,000 tonnes. However, growth within the Gulf states – estimated at 8% CAGR – will account for some 60,000 tonnes and new major end-users may make significant inroads into the remainder.

India’s Tata Motors has indicated a possibility of building a Jaguar Land Rover assembly plant with press shop to utilise car body sheet from Ma’aden.

Existing can lines in Saudi Arabia, Kuwait and UAE sourced around 110,000 tonnes in 2011 from USA, Europe, Australia and Japan. Sourcing from MAC –the region’s only can stock capable mill – would cut freight costs by up to $100/tonne. Although sea freight rates are currently at an all-time low, this will not always be the case.

The Gulf foil market (see below) is undersupplied and it is likely that there will be major investment in foil rolling capacity,

Downstream developments

Bahrain’s Bamco is one of the world’s major master alloy suppliers

While aluminium processors in Gulf Co-operation Council countries are not immune from today’s softer global market trends, they have relatively unaffected domestic demand for their products to serve. Andrew J. Robinson summarises the shape of, and outlook for, the region’s evolving downstream aluminium sector

BAM

CO

Integrating shredding with steelmaking

November 2012 | Arab aluminium | 21

with a consequential increase in demand for foil re-roll.

Construction activity in Saudi Arabia has barely dipped during the world downturn. The building of the designated ‘Six Economic Cities’and the new inter-Gulf rail network in particular will continue to stimulate flat rolled product demand.

Foil review Steady growth, especially in semi-rigid containers, has kept the only producing foil (0.20 mm thick or less, including fin) mill in the region – Garmco Foil in Bahrain – at full stretch for some time. The plant produced record tonnages in 2011, almost entirely for the Gulf market. The outlook for 2012 production is similar. Imports have grown sharply in 2012 – possibly due to new fin stock end-users.

BahrainGarmco Foil – Commissioned in 2000 with a capacity of 18,000 tpy. Takes coil for re-roll from Garmco. Current output of 22,000 tpy. Plans to add one more finishing mill and produce 30,000 tpy by 2014. Developing export markets in India and Australia.

Foil outlookThe total foil market in the Gulf states in 2011 is calculated at 123,000 tonnes, based on imports and production. An estimated CAGR of 8% will continue to be driven by the fast increasing population, generating demand for household foil, semi-rigid containers for fast food, lids for dairy products, ventilation and air-conditioning fin.

This indicates that the 2013 market will be around 143,000 tonnes. With local production standing at a maximum of 22,000 tpy, and even including the 10,000 tpy expansion plans of the existing Garmco mill in Bahrain, the market for imports is around 111,000 tpy.

Consequently there is space for additional local foil/fin rolling capacity. It is likely that any new foil mill would be located near to the coil mills coming on line in Oman and Saudi Arabia.

EXTRUSIONSExtruded products review Extrusion plants are widely dispersed across the GCC region. They are generally located in industrial estates close to the regional smelters. The exception is Saudi Arabia, where there is no smelter as yet. Installed capacity within the GCC countries is over 390,000 tpy, with about another 100,000 tpy planned or under construction.

Utilisation levels are much increased from the 60-70% lows of 2010, but vary widely from plant to plant. Some units are at full production and others – usually smaller units with no remelt or billet casting facilities – virtually moth-balled due to the large increase

in billet premiums over the past year.The total market size is variously estimated at

between 450,000 and 500,000 tpy. Extrusion billet is an international commodity sourced world wide but usually supplied on contract from regional smelters.

BahrainBalexco – Commissioned in 1977 at 6,000 tpy with a single press, this extruder has now installed a fourth press plus a new anodising line to bring capacity to 32,000 tpy. Reported to be running at high utilisation and exporting a good proportion of product into the GCC region. Billet and ingot is supplied from the Alba smelter.

UAEThe United Arab Emirates has many extruders, mostly drawing billet and ingot from Dubal, and from UAE secondary smelters.Gulf Extrusions – Commissioned in 1980s; capacity 60,000 tpy.Al Jaber Extrusions – Commissioned in 1996; capacity 36,000 tpy.Emirates Extrusion – Commissioned in 1993; capacity 21,000 tpy.Arabian Extrusion – Commissioned in 2002; capacity 18,000 tpy.Al Hamad Extrusions – Single press operation, capacity 4,000 tpy.Elite Extrusion – Part of Al Hamad Construction group merged with Classic and National Extrusion Co. in 2009; capacity 36,000 tpy.White Aluminium Extrusion – Commissioned in 2007; capacity 17,000 tpy.Taweelah Aluminium (Talex) – Joint venture ADBIC/Gulf Extrusions; capacity 50,000 tpy. Under construction; commercial production target Q4 2013.

Saudi ArabiaLong-established extrusion industry drawing metal from GCC smelters and secondary operations.Alupco Extrusion, Damam and Jeddah – 60,000 tpy. Al Taiser Extrusion, Riyadh – 42,000 tpy.Dural Extrusion, Jeddah – 5,000 tpy.Saudi Aluminium Extrusion, Riyadh – 5,000 tpy.Alinco Extrusions , Riyadh – 20,000 tpy.Wofoor Extrusions, Riyadh – 8,000 tpy.Batra Aluminium, Jeddah – 5,000 tpy.Sherry Extrusion – 5,000 tpy.

QatarQatar Aluminium Extrusion Co. – Commissioned July 2011. Capacity 15,000 tpy. A second two-press plant is planned for 2013.

KuwaitKalexco – extrusion, 6,500 tpy.Arabian Light Metals – extrusion, 12,000 tpy.Al Khorfa/ Gulf Aluminium – Commissioned 2011, 8,000 tpy.

OmanNAPCo – Extrusion commissioned 1984; capacity 18,000 tpy.

Extruded Products outlook Construction and infrastructure are the major markets for extruded products. Every GCC state has plans for – or is actively engaged in – airport expansion and/or re-construction. Every state also has plans for rapid-transit, light-gauge railways, several of which are already under way. In addition, a $106 billion, 2,200 km inter-state Gulf Rail project is scheduled for 2017. Extruded profiles are a major component of stations and terminals. Kuwait alone plans 60 stations.

CABLE, WIRE AND RODReviewBahrainMidal – Commissioned in 1978 with a capacity of 10,000 tpy for cable and rod, now operating at around 200,000 tpy and importing up to 40,000 tpy of aluminium from offshore smelters. Plans to expand to 230,000 tpy with potential further expansion close to Middle East smelters. Building a 40,000 tpy subsidiary near to Tomago smelter in Australia.Bahrain Wire – Commissioned in 2005 with a capacity of 15,000 tpy, now expanded to 25,000 tpy. Company acquired by Midal in 2010. No further expansion planned at present.

UAETrans-Gulf Ind, Dubai – Capacity of 20,000 tpy for wire and rod.

Midal Cables in a joint venture with Abu Dhabi Basic Industries Corporation is

Bahrain has a well developed downstream sector supplied by Alba

ALBA

u

Arab aluminium 2012

Downstream

22 | Arab aluminium | November 2012

developing a wire rod facility near the Emal smelter in UAE with a proposed capacity of 50,000 tpy.

OmanSAG (Takamul) – Commissioned 2008. Capacity of 30,000 tpy for busbar.OAPIL (Takamul) – Commissioned mid-2010 with a capacity of 48,000 tpy for rod and conductor.

OutlookConstruction of the GCC power grid has been a major driver of conductor and cable demand over the past ten years. However, the final phase of interstate connection is due for completion over the next two years; after that it will be necessary for producers to seek new markets, probably offshore. The most likely contender is India, which is relatively close, where the need for power grid development is massive compared with the Gulf and is becoming a political imperative.

INGOT AND CASTING ALLOYSReviewRegional smelters in Dubai, Bahrain and Qatar all have capacity to produce casting alloys. Total output in 2011 was around 280,000 tonnes. In addition there are major casting alloy and secondary ingot producers in Bahrain , UAE and Saudi Arabia.

BahrainBamco – Commissioned in 1996 with capacity of 8,000 tpy for foundry, casting and master alloys. Now producing at 30,000 tpy. One of the world’s major master alloy suppliers.Aluwheel – Commissioned in 1992 with capacity of 15,000 tpy for cast wheels. Current capacity 20,000 tpy. Secondary ingot production closed in 2012.

UAESherif Metals, Sharjah – Gulf –wide non-ferrous scrap recycling company