Embed Size (px)

Citation preview

Applied Econometrics and International Development Vol. 14-1 (2014)

EFFECTS OF CORPORATE TAXATION AND BILATERAL TAX TREATIES ON EUROPEAN MULTINATIONALS’ INVESTMENT, 2005-2009. A MULTI-

COUNTRY ANALYSIS MARQUES, Mario *

PINHO, Carlos Abstract This paper analyzes the effects of corporate tax rates and tax treaties on multinationals foreign activity. First, it examines whether host country corporate tax rate and tax treaties influence the probability of a multinational to choose a particular country to locate a new foreign subsidiary. Second, it evaluates to what extent the investment level is determined by taxation. We use data of new foreign subsidiaries located in Europe and take a two-step estimation. The estimated semi-elasticity of effective tax rate is of -1.516. At the intensive margin of investment findings indicate significant effects of both tax treaties and corporate tax rates on the number of employees. Keywords: foreign investment, corporate taxation; tax treaties JEL classification: F23, H25, H32 ________________________________________________________________________ 1. Introduction With the globalization of economies, an increasing number of companies invest abroad and develop international activities (Barrios et al., 2009). Moreover, in the European context the EU enlargement to Central and Eastern countries may boosted the capital mobility across countries (v.g. Finkenzeller Spengel, 2004; Frias et al., 2005). In the literature of international trade it is well known that market size, productivity, labor costs among other factors are determinants of the multinationals investment activities. Also, corporate taxation seems to play a role when a company decides where to locate its investment abroad and how much should be invested. Aware of these effects, last decades have witnessed a strong tax competition of countries for firms, capital and profits, which consequently had generated some important changes on the international aspects of national tax system all over the world and particularly in Europe. Two of the mentioned international aspects are corporate tax rates and bilateral tax treaties: countries engaged in a race to the bottom regarding corporate tax rate and expanded the bilateral tax treaties network. This paper considers these two important aspects of tax systems and assesses to what extent they really influence where European multinationals locate their foreign subsidiaries and how much multinational firms invest abroad. In a cross-section multi-country study we examine using a two-part model if corporate taxation and bilateral tax treaties exert effects on the foreign investment at both extensive and intensive margins. Based on the contribution of Huizinga et al. (2008), we also propose and test an effective tax rate, which is taken as a proxy for the existence of bilateral tax treaties and for the tax

* Mário Marques [email protected], and Carlos Pinho, University of Minho, Portugal

Applied Econometrics and International Development Vol. 14-1 (2014)

34

burden of multinationals in each potential host country. This tax measure is a function of both home and host countries corporate tax rate and non-resident withholding tax rate. For the first part model we found that the probability of a multinational to have a subsidiary in a particular country is higher if both tax treaty exists and a given host country decreases its corporate tax rate. The estimated effect of effective tax rate is also negative on the probability of location. Results suggest a corporate tax rate semi-elasticity of -2.224 and a tax treaty semi elasticity of 0.463. In the second part of the model we take fixed assets and the number of employees as proxies of the level of investment. We obtained evidence that the corporate tax rate and the existence of tax treaties have influence on the number of employees. The corporate tax rate and tax treaty semi-elasticities are -24.232 and 2.675, respectively. This paper is organised as follows. In section 2 we analyze some important aspects of international taxation and existing literature, and also propose and define an alternative tax measure. Section 3 provides an overview of the estimation approach and describes the sample. Section 4 presents and discusses the empirical results. The last section concludes. 2. International taxation and existing literature 2.1 Corporate tax rates, bilateral tax treaties and multinationals’ activity The last decades have seen important changes on the international aspects of national tax systems all over the world, partially as a consequence of countries’ tax competition. These international aspects of income taxation are rooted in the taxation of foreign-source income of multinationals and in the existence of bilateral tax treaties (Egger and Merlo, 2011:146). The increasing competition for foreign investment has forced countries for a race to the bottom regarding corporate income tax rates. The average corporate tax rate in European countries in 2000 was 31 per cent and it has declined until 2009 around eleven percentage points (the combined corporate statutory tax rates in 2005 in Europe are provided below in the annexes). The corporate tax rate average is around 25 per cent. The dispersion of tax rates is close to 15 percentage points, over half of the corporate tax rate average. Cyprus and Ireland are the countries with the lowest corporate income tax rates, while Germany, Spain and Malta imposed in 2005 a corporate tax rate equal or greater than 35 per cent. Simultaneously, the growing international trade and markets globalization led countries to settle a large bilateral tax agreements network. Around 50 per cent of bilateral treaties effective all around the world have taken place during decade 2000 (see the Annexes for the European bilateral tax treaties network in 2005). Bilateral tax treaties usually decrease the withholding tax rates on dividends and interest payments, and eliminate or mitigate international double taxation. It would be then expected that the distortion of investment induced by taxation decreases when a tax treaty enters into force. This argument has been examined mainly at an aggregate level of foreign investment and authors generally find either an insignificant or a weakly negative effect of treaties on foreign investment (see Blonigen and Davies, 2002, 2004; Davies, 2003; Barthel et al., 2009; Neumayer, 2007; Millimet and Kumas, 2007; Louie and Rousslang, 2008). More recently, there have been some studies reassessing the effects of tax treaties formation on foreign investment using firm-level data (see Davies et al., 2009; Egger and Merlo, 2011). The empirical work have shown that the existence of tax treaties have

Marques, M., Pinho, C. Effects of Corporate Taxation on European Multinationals’ Investment

35

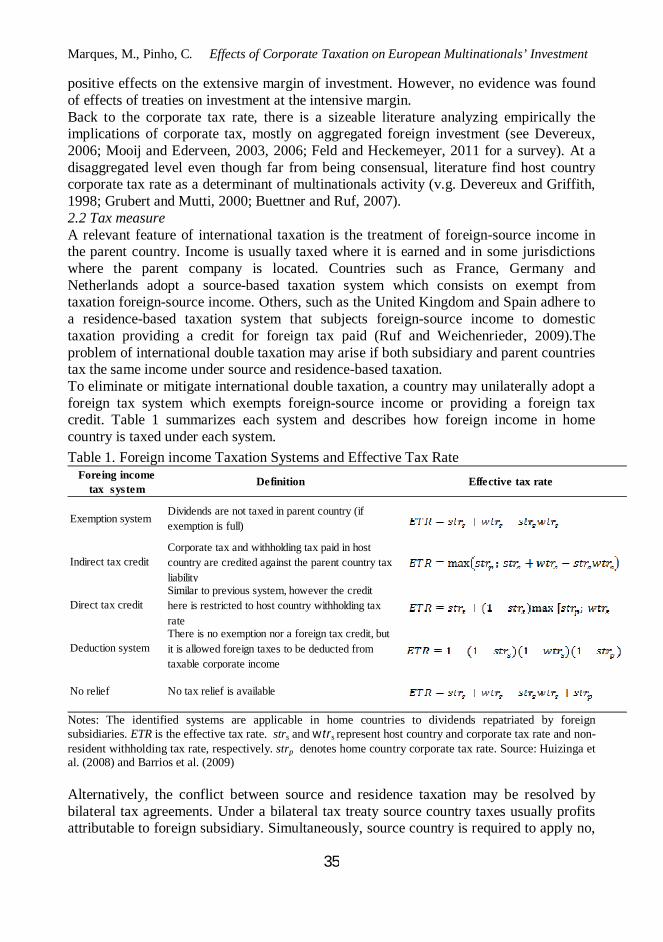

positive effects on the extensive margin of investment. However, no evidence was found of effects of treaties on investment at the intensive margin. Back to the corporate tax rate, there is a sizeable literature analyzing empirically the implications of corporate tax, mostly on aggregated foreign investment (see Devereux, 2006; Mooij and Ederveen, 2003, 2006; Feld and Heckemeyer, 2011 for a survey). At a disaggregated level even though far from being consensual, literature find host country corporate tax rate as a determinant of multinationals activity (v.g. Devereux and Griffith, 1998; Grubert and Mutti, 2000; Buettner and Ruf, 2007). 2.2 Tax measure A relevant feature of international taxation is the treatment of foreign-source income in the parent country. Income is usually taxed where it is earned and in some jurisdictions where the parent company is located. Countries such as France, Germany and Netherlands adopt a source-based taxation system which consists on exempt from taxation foreign-source income. Others, such as the United Kingdom and Spain adhere to a residence-based taxation system that subjects foreign-source income to domestic taxation providing a credit for foreign tax paid (Ruf and Weichenrieder, 2009).The problem of international double taxation may arise if both subsidiary and parent countries tax the same income under source and residence-based taxation. To eliminate or mitigate international double taxation, a country may unilaterally adopt a foreign tax system which exempts foreign-source income or providing a foreign tax credit. Table 1 summarizes each system and describes how foreign income in home country is taxed under each system. Table 1. Foreign income Taxation Systems and Effective Tax Rate

Foreing income tax system

Definition Effective tax rate

Exemption systemDividends are not taxed in parent country (if exemption is full)

Indirect tax creditCorporate tax and withholding tax paid in host country are credited against the parent country tax liability

Direct tax credit Similar to previous system, however the credit here is restricted to host country withholding tax rate

Deduction systemThere is no exemption nor a foreign tax credit, but it is allowed foreign taxes to be deducted from taxable corporate income

No relief No tax relief is available

Notes: The identified systems are applicable in home countries to dividends repatriated by foreign subsidiaries. ETR is the effective tax rate. strs and wtrs represent host country and corporate tax rate and non-resident withholding tax rate, respectively. strp denotes home country corporate tax rate. Source: Huizinga et al. (2008) and Barrios et al. (2009) Alternatively, the conflict between source and residence taxation may be resolved by bilateral tax agreements. Under a bilateral tax treaty source country taxes usually profits attributable to foreign subsidiary. Simultaneously, source country is required to apply no,

Applied Econometrics and International Development Vol. 14-1 (2014)

36

or only a low, withholding tax rate on payments to non-residents such as interests and dividends paid (Avi-Yonah, 2009). Furthermore, the residence country agrees to adopt a foreign tax relief system giving a credit or a deduction on expenses for taxes paid in subsidiary’s country or exempting foreign income from taxes (Avi-Yonah, 2009). In the present paper using firm-level data we investigate for the importance of both corporate taxation and bilateral tax treaties on foreign investment decisions. Following Huizinga et al. (2008), we compute and propose an alternative tax measure (i.e. effective tax rate) which intends to capture the most important international tax features, particularly the corporate tax rate and the existence of a tax treaty. The The combined corporate ( ) and withholding ( ) tax rates in the host country is

(see Huizinga et al., 2008). Let us consider that = 25 per cent and that country s subjects dividends repatriation to a non-resident withholding tax rate of 5 per cent, the combined tax in host country would be 28.75 per cent (i.e.

). Furthermore, if the parent country adopts residence-based other than source-based taxation regime, the dividends may be taxed at the parent country as illustrated in the Table 1. In the proposed tax measure we put in some important specifications of a tax system together: corporate tax rate; non-resident withholding tax rate; foreign income system and the bilateral tax treaties. Consider again the previous example. The corporate tax rate in countries s and p are respectively 25 percent and 30 percent. The withholding tax rate on dividends repatriated from s to parent country is 5 per cent. The effective tax rates are as follows for each of foreign tax system. The effective tax rate is built on the parent company perspective under the assumption that dividend repatriation is not deferred. In the case of home country adhere to the exemption system, the effective tax rate would be 28.75 per cent as previously determined. If instead the home country adopts the residence regime taxing worldwide repatriated income to domestic taxation, a credit is provided by home country for foreign tax paid. Under the indirect tax credit, the effective tax rate would be 30 percent as a consequence of . In the direct system it is provided only credit for foreign withholding tax rate on dividends. In our example the effective tax rate would be , that is 47.5%. Finally, in the deduction system although it is not allowed to use the foreign tax paid against home country tax liability, foreign tax paid is deductible on taxable income of parent country. For the previous example, if country p adopts a deduction system the effective tax rate would be 50.13 per cent. 3. Data and empirical approach 3.1. Data and descriptive statistics For the empirical analysis we use data on European multinationals foreign investment to examine the effects of taxation on investment decisions at extensive and intensive margins. The firm-level data is taken from Amadeus database. The extensive margin of investment is related with the probability of investment in a particular country (see Davies et al., 2009; Egger and Merlo, 2011), thus the outcome variable is binary which takes the value 1 if throughout the period 2005-2009 multinational firm i has incorporated at least one subsidiary in host country j. As far as the level of investment (intensive

Marques, M., Pinho, C. Effects of Corporate Taxation on European Multinationals’ Investment

37

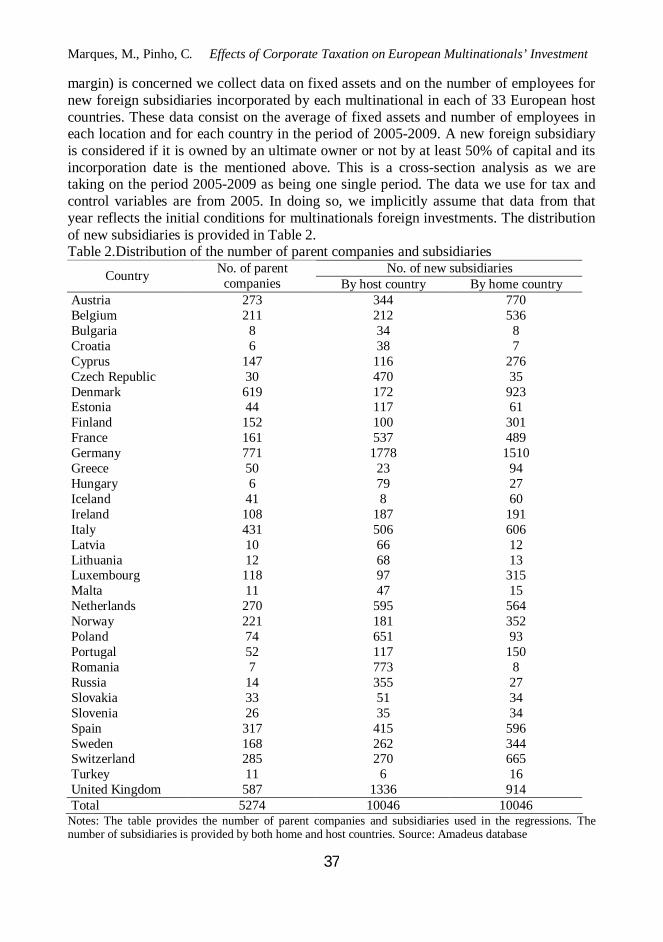

margin) is concerned we collect data on fixed assets and on the number of employees for new foreign subsidiaries incorporated by each multinational in each of 33 European host countries. These data consist on the average of fixed assets and number of employees in each location and for each country in the period of 2005-2009. A new foreign subsidiary is considered if it is owned by an ultimate owner or not by at least 50% of capital and its incorporation date is the mentioned above. This is a cross-section analysis as we are taking on the period 2005-2009 as being one single period. The data we use for tax and control variables are from 2005. In doing so, we implicitly assume that data from that year reflects the initial conditions for multinationals foreign investments. The distribution of new subsidiaries is provided in Table 2. Table 2.Distribution of the number of parent companies and subsidiaries

No. of new subsidiaries Country No. of parent companies By host country By home country

Austria 273 344 770 Belgium 211 212 536 Bulgaria 8 34 8 Croatia 6 38 7 Cyprus 147 116 276 Czech Republic 30 470 35 Denmark 619 172 923 Estonia 44 117 61 Finland 152 100 301 France 161 537 489 Germany 771 1778 1510 Greece 50 23 94 Hungary 6 79 27 Iceland 41 8 60 Ireland 108 187 191 Italy 431 506 606 Latvia 10 66 12 Lithuania 12 68 13 Luxembourg 118 97 315 Malta 11 47 15 Netherlands 270 595 564 Norway 221 181 352 Poland 74 651 93 Portugal 52 117 150 Romania 7 773 8 Russia 14 355 27 Slovakia 33 51 34 Slovenia 26 35 34 Spain 317 415 596 Sweden 168 262 344 Switzerland 285 270 665 Turkey 11 6 16 United Kingdom 587 1336 914 Total 5274 10046 10046

Notes: The table provides the number of parent companies and subsidiaries used in the regressions. The number of subsidiaries is provided by both home and host countries. Source: Amadeus database

Applied Econometrics and International Development Vol. 14-1 (2014)

38

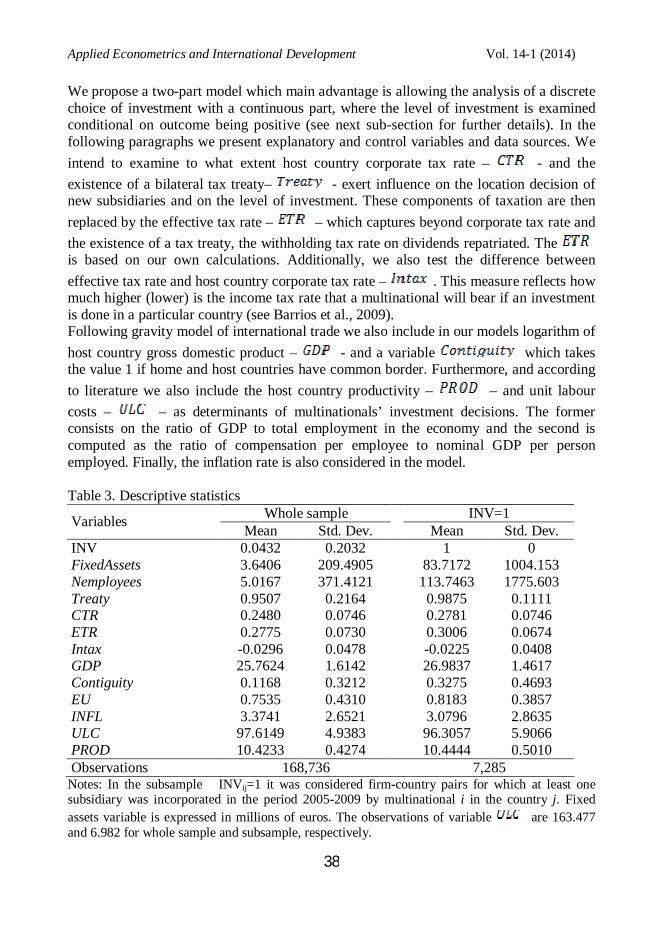

We propose a two-part model which main advantage is allowing the analysis of a discrete choice of investment with a continuous part, where the level of investment is examined conditional on outcome being positive (see next sub-section for further details). In the following paragraphs we present explanatory and control variables and data sources. We intend to examine to what extent host country corporate tax rate – - and the existence of a bilateral tax treaty– - exert influence on the location decision of new subsidiaries and on the level of investment. These components of taxation are then replaced by the effective tax rate – – which captures beyond corporate tax rate and the existence of a tax treaty, the withholding tax rate on dividends repatriated. The is based on our own calculations. Additionally, we also test the difference between effective tax rate and host country corporate tax rate – . This measure reflects how much higher (lower) is the income tax rate that a multinational will bear if an investment is done in a particular country (see Barrios et al., 2009). Following gravity model of international trade we also include in our models logarithm of host country gross domestic product – - and a variable which takes the value 1 if home and host countries have common border. Furthermore, and according to literature we also include the host country productivity – – and unit labour costs – – as determinants of multinationals’ investment decisions. The former consists on the ratio of GDP to total employment in the economy and the second is computed as the ratio of compensation per employee to nominal GDP per person employed. Finally, the inflation rate is also considered in the model. Table 3. Descriptive statistics

Whole sample INV=1 Variables Mean Std. Dev. Mean Std. Dev. INV 0.0432 0.2032 1 0 FixedAssets 3.6406 209.4905 83.7172 1004.153 Nemployees 5.0167 371.4121 113.7463 1775.603 Treaty 0.9507 0.2164 0.9875 0.1111 CTR 0.2480 0.0746 0.2781 0.0746 ETR 0.2775 0.0730 0.3006 0.0674 Intax -0.0296 0.0478 -0.0225 0.0408 GDP 25.7624 1.6142 26.9837 1.4617 Contiguity 0.1168 0.3212 0.3275 0.4693 EU 0.7535 0.4310 0.8183 0.3857 INFL 3.3741 2.6521 3.0796 2.8635 ULC 97.6149 4.9383 96.3057 5.9066 PROD 10.4233 0.4274 10.4444 0.5010 Observations 168,736 7,285

Notes: In the subsample INVij=1 it was considered firm-country pairs for which at least one subsidiary was incorporated in the period 2005-2009 by multinational i in the country j. Fixed assets variable is expressed in millions of euros. The observations of variable are 163.477 and 6.982 for whole sample and subsample, respectively.

Marques, M., Pinho, C. Effects of Corporate Taxation on European Multinationals’ Investment

39

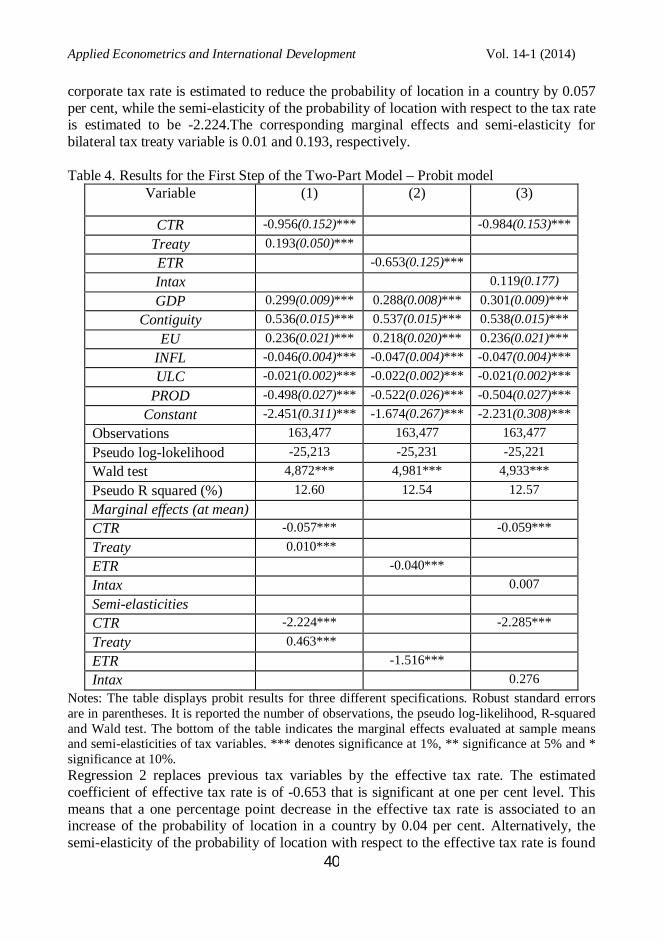

Data on bilateral tax treaties, corporate income tax rate and withholding tax rate and other specifications of European tax systems were collected from International Bureau of Fiscal Documentation, Worldwide Corporate Tax Guide by Ernst & Young, and websites of various fiscal authorities and ministries. The data on GDP, productivity and inflation rate come from World Bank database. Finally, the unit labour cost is provided by Ameco database from European Commission. Table 3 provides the descriptive statistics for the whole sample and for the subsample. The firm-country pairs taking value of 1 is around 4.3 per cent. For the whole sample, the mean of host-country corporate tax rate is 24.8 per cent while the effective is as expected higher reaching 27.8 per cent. Surprisingly, the mean of corporate tax rate, and effective tax rate, in the subsample is higher than for the whole sample, however for treaty variable the existence of a treaty is higher in the subsample of firm-country pairs . Regarding means of control variables and are higher for the subsample comparing to whole sample while means of and are lower. 3.2 Estimation method The purpose of this paper is twofold. First, we examine whether taxation influences the probability of a multinational to choose a particular country to locate a new foreign subsidiary. Second, we evaluate to what extent the level of the investment in the new foreign subsidiary is determined by corporate taxation. We take a two-step estimation approach which reflects a two-part decision-making process, where each part is considered a model of one decision. The two-part approach relaxes the assumption that the zeros and the positives come from the same data-generating process (Cameron and Trivedi, 2010:583). The first step consists on a probit model, where the outcome variable is a binary variable - - consisting in whether or not multinational firm has a new foreign subsidiary located in host country . Then, for the second decision we use a model which outcome is conditional on being positive. Fixed assets and the number of employees are taken as proxies of the level of investment. There are problems in using the ordinary least squares estimation method. One of them is that the logarithm of fixed assets and of number of employees would force to drop a large number of observations as there are a large number of zero assets and employees (Rud and Weichenrieder, 2009). Therefore, we use for the second part a Poisson quasi-maximum likelihood model (see Egger and Merlo, 2011; Ruf and Weicenrieder, 2009; Santos Silva and Tenreyro, 2006). 4. Results and discussion As mentioned before, for the first part of the two-part model we only use a binary as outcome variable to assess the effects of corporate tax rates and tax treaties on the extensive margin of investment. In the second part we examine the impact of taxation on the intensive margin of investment. The results for the probit model are displayed in the Table 4. Regression 1 includes the corporate tax rate and treaty, yielding significant coefficients of -0.956 and 0.193, respectively. A one percentage point increase in the host country

Applied Econometrics and International Development Vol. 14-1 (2014)

40

corporate tax rate is estimated to reduce the probability of location in a country by 0.057 per cent, while the semi-elasticity of the probability of location with respect to the tax rate is estimated to be -2.224.The corresponding marginal effects and semi-elasticity for bilateral tax treaty variable is 0.01 and 0.193, respectively. Table 4. Results for the First Step of the Two-Part Model – Probit model

Variable (1) (2) (3)

CTR -0.956(0.152)*** -0.984(0.153)*** Treaty 0.193(0.050)*** ETR -0.653(0.125)*** Intax 0.119(0.177) GDP 0.299(0.009)*** 0.288(0.008)*** 0.301(0.009)***

Contiguity 0.536(0.015)*** 0.537(0.015)*** 0.538(0.015)*** EU 0.236(0.021)*** 0.218(0.020)*** 0.236(0.021)***

INFL -0.046(0.004)*** -0.047(0.004)*** -0.047(0.004)*** ULC -0.021(0.002)*** -0.022(0.002)*** -0.021(0.002)***

PROD -0.498(0.027)*** -0.522(0.026)*** -0.504(0.027)*** Constant -2.451(0.311)*** -1.674(0.267)*** -2.231(0.308)***

Observations 163,477 163,477 163,477 Pseudo log-lokelihood -25,213 -25,231 -25,221 Wald test 4,872*** 4,981*** 4,933*** Pseudo R squared (%) 12.60 12.54 12.57 Marginal effects (at mean) CTR -0.057*** -0.059*** Treaty 0.010*** ETR -0.040*** Intax 0.007 Semi-elasticities CTR -2.224*** -2.285*** Treaty 0.463*** ETR -1.516*** Intax 0.276

Notes: The table displays probit results for three different specifications. Robust standard errors are in parentheses. It is reported the number of observations, the pseudo log-likelihood, R-squared and Wald test. The bottom of the table indicates the marginal effects evaluated at sample means and semi-elasticities of tax variables. *** denotes significance at 1%, ** significance at 5% and * significance at 10%. Regression 2 replaces previous tax variables by the effective tax rate. The estimated coefficient of effective tax rate is of -0.653 that is significant at one per cent level. This means that a one percentage point decrease in the effective tax rate is associated to an increase of the probability of location in a country by 0.04 per cent. Alternatively, the semi-elasticity of the probability of location with respect to the effective tax rate is found

Marques, M., Pinho, C. Effects of Corporate Taxation on European Multinationals’ Investment

41

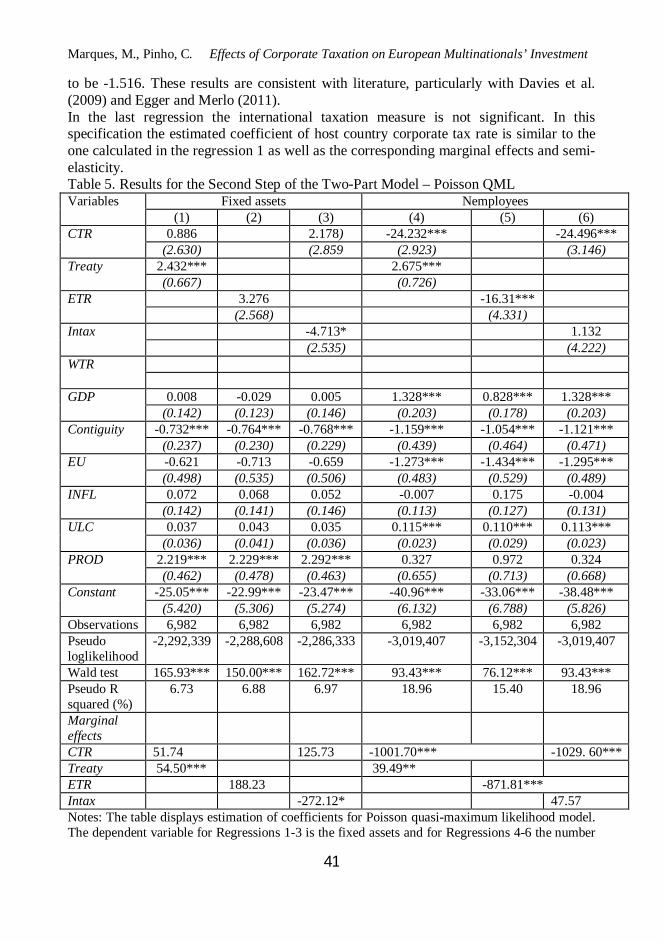

to be -1.516. These results are consistent with literature, particularly with Davies et al. (2009) and Egger and Merlo (2011). In the last regression the international taxation measure is not significant. In this specification the estimated coefficient of host country corporate tax rate is similar to the one calculated in the regression 1 as well as the corresponding marginal effects and semi-elasticity. Table 5. Results for the Second Step of the Two-Part Model – Poisson QML

Fixed assets Nemployees Variables (1) (2) (3) (4) (5) (6)

0.886 2.178) -24.232*** -24.496*** CTR (2.630) (2.859 (2.923) (3.146)

2.432*** 2.675*** Treaty (0.667) (0.726)

3.276 -16.31*** ETR (2.568) (4.331) -4.713* 1.132 Intax (2.535) (4.222) WTR

0.008 -0.029 0.005 1.328*** 0.828*** 1.328*** GDP (0.142) (0.123) (0.146) (0.203) (0.178) (0.203)

-0.732*** -0.764*** -0.768*** -1.159*** -1.054*** -1.121*** Contiguity (0.237) (0.230) (0.229) (0.439) (0.464) (0.471) -0.621 -0.713 -0.659 -1.273*** -1.434*** -1.295*** EU (0.498) (0.535) (0.506) (0.483) (0.529) (0.489) 0.072 0.068 0.052 -0.007 0.175 -0.004 INFL

(0.142) (0.141) (0.146) (0.113) (0.127) (0.131) 0.037 0.043 0.035 0.115*** 0.110*** 0.113*** ULC

(0.036) (0.041) (0.036) (0.023) (0.029) (0.023) 2.219*** 2.229*** 2.292*** 0.327 0.972 0.324 PROD (0.462) (0.478) (0.463) (0.655) (0.713) (0.668)

-25.05*** -22.99*** -23.47*** -40.96*** -33.06*** -38.48*** Constant (5.420) (5.306) (5.274) (6.132) (6.788) (5.826)

Observations 6,982 6,982 6,982 6,982 6,982 6,982 Pseudo loglikelihood

-2,292,339 -2,288,608 -2,286,333 -3,019,407 -3,152,304 -3,019,407

Wald test 165.93*** 150.00*** 162.72*** 93.43*** 76.12*** 93.43*** Pseudo R squared (%)

6.73 6.88 6.97 18.96 15.40 18.96

Marginal effects

CTR 51.74 125.73 -1001.70*** -1029. 60*** Treaty 54.50*** 39.49** ETR 188.23 -871.81*** Intax -272.12* 47.57 Notes: The table displays estimation of coefficients for Poisson quasi-maximum likelihood model. The dependent variable for Regressions 1-3 is the fixed assets and for Regressions 4-6 the number

Applied Econometrics and International Development Vol. 14-1 (2014)

42

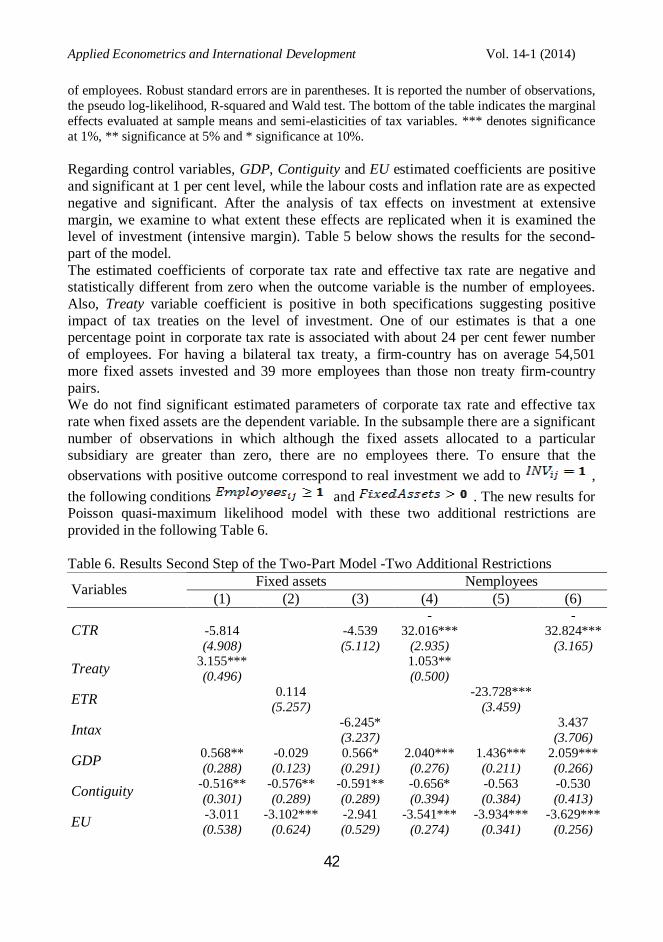

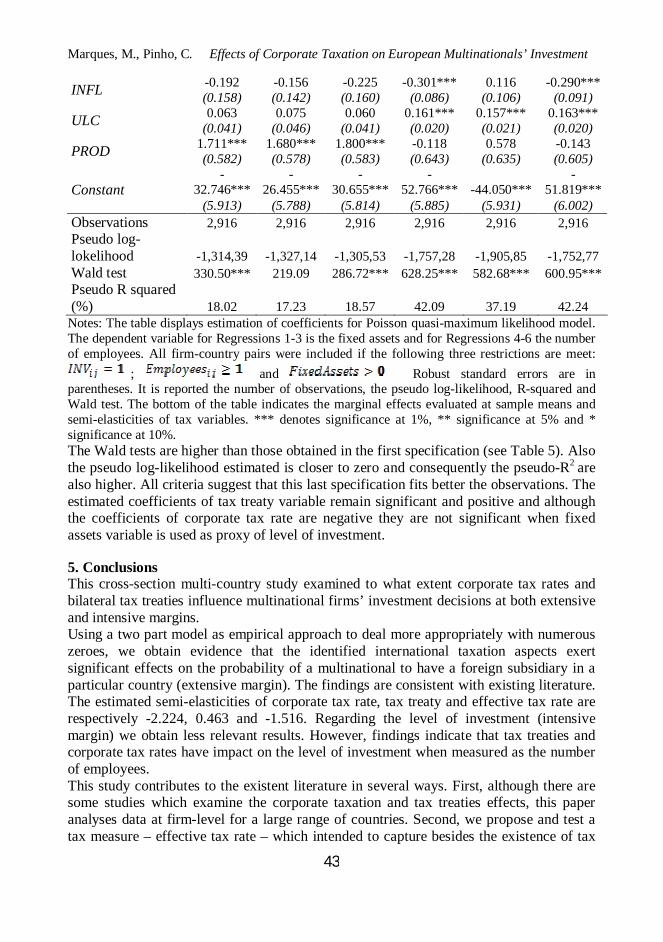

of employees. Robust standard errors are in parentheses. It is reported the number of observations, the pseudo log-likelihood, R-squared and Wald test. The bottom of the table indicates the marginal effects evaluated at sample means and semi-elasticities of tax variables. *** denotes significance at 1%, ** significance at 5% and * significance at 10%. Regarding control variables, GDP, Contiguity and EU estimated coefficients are positive and significant at 1 per cent level, while the labour costs and inflation rate are as expected negative and significant. After the analysis of tax effects on investment at extensive margin, we examine to what extent these effects are replicated when it is examined the level of investment (intensive margin). Table 5 below shows the results for the second-part of the model. The estimated coefficients of corporate tax rate and effective tax rate are negative and statistically different from zero when the outcome variable is the number of employees. Also, Treaty variable coefficient is positive in both specifications suggesting positive impact of tax treaties on the level of investment. One of our estimates is that a one percentage point in corporate tax rate is associated with about 24 per cent fewer number of employees. For having a bilateral tax treaty, a firm-country has on average 54,501 more fixed assets invested and 39 more employees than those non treaty firm-country pairs. We do not find significant estimated parameters of corporate tax rate and effective tax rate when fixed assets are the dependent variable. In the subsample there are a significant number of observations in which although the fixed assets allocated to a particular subsidiary are greater than zero, there are no employees there. To ensure that the observations with positive outcome correspond to real investment we add to , the following conditions and . The new results for Poisson quasi-maximum likelihood model with these two additional restrictions are provided in the following Table 6. Table 6. Results Second Step of the Two-Part Model -Two Additional Restrictions

Fixed assets Nemployees Variables (1) (2) (3) (4) (5) (6)

-5.814 -4.539 -

32.016*** -

32.824*** CTR (4.908) (5.112) (2.935) (3.165)

3.155*** 1.053** Treaty (0.496) (0.500) 0.114 -23.728*** ETR (5.257) (3.459) -6.245* 3.437 Intax (3.237) (3.706)

0.568** -0.029 0.566* 2.040*** 1.436*** 2.059*** GDP (0.288) (0.123) (0.291) (0.276) (0.211) (0.266) -0.516** -0.576** -0.591** -0.656* -0.563 -0.530 Contiguity (0.301) (0.289) (0.289) (0.394) (0.384) (0.413) -3.011 -3.102*** -2.941 -3.541*** -3.934*** -3.629*** EU (0.538) (0.624) (0.529) (0.274) (0.341) (0.256)

Marques, M., Pinho, C. Effects of Corporate Taxation on European Multinationals’ Investment

43

-0.192 -0.156 -0.225 -0.301*** 0.116 -0.290*** INFL (0.158) (0.142) (0.160) (0.086) (0.106) (0.091) 0.063 0.075 0.060 0.161*** 0.157*** 0.163*** ULC (0.041) (0.046) (0.041) (0.020) (0.021) (0.020)

1.711*** 1.680*** 1.800*** -0.118 0.578 -0.143 PROD (0.582) (0.578) (0.583) (0.643) (0.635) (0.605) -

32.746*** -

26.455*** -

30.655*** -

52.766*** -44.050*** -

51.819*** Constant (5.913) (5.788) (5.814) (5.885) (5.931) (6.002)

Observations 2,916 2,916 2,916 2,916 2,916 2,916 Pseudo log-lokelihood -1,314,39 -1,327,14 -1,305,53 -1,757,28 -1,905,85 -1,752,77 Wald test 330.50*** 219.09 286.72*** 628.25*** 582.68*** 600.95*** Pseudo R squared (%) 18.02 17.23 18.57 42.09 37.19 42.24

Notes: The table displays estimation of coefficients for Poisson quasi-maximum likelihood model. The dependent variable for Regressions 1-3 is the fixed assets and for Regressions 4-6 the number of employees. All firm-country pairs were included if the following three restrictions are meet:

; and Robust standard errors are in parentheses. It is reported the number of observations, the pseudo log-likelihood, R-squared and Wald test. The bottom of the table indicates the marginal effects evaluated at sample means and semi-elasticities of tax variables. *** denotes significance at 1%, ** significance at 5% and * significance at 10%. The Wald tests are higher than those obtained in the first specification (see Table 5). Also the pseudo log-likelihood estimated is closer to zero and consequently the pseudo-R2 are also higher. All criteria suggest that this last specification fits better the observations. The estimated coefficients of tax treaty variable remain significant and positive and although the coefficients of corporate tax rate are negative they are not significant when fixed assets variable is used as proxy of level of investment. 5. Conclusions This cross-section multi-country study examined to what extent corporate tax rates and bilateral tax treaties influence multinational firms’ investment decisions at both extensive and intensive margins. Using a two part model as empirical approach to deal more appropriately with numerous zeroes, we obtain evidence that the identified international taxation aspects exert significant effects on the probability of a multinational to have a foreign subsidiary in a particular country (extensive margin). The findings are consistent with existing literature. The estimated semi-elasticities of corporate tax rate, tax treaty and effective tax rate are respectively -2.224, 0.463 and -1.516. Regarding the level of investment (intensive margin) we obtain less relevant results. However, findings indicate that tax treaties and corporate tax rates have impact on the level of investment when measured as the number of employees. This study contributes to the existent literature in several ways. First, although there are some studies which examine the corporate taxation and tax treaties effects, this paper analyses data at firm-level for a large range of countries. Second, we propose and test a tax measure – effective tax rate – which intended to capture besides the existence of tax

Applied Econometrics and International Development Vol. 14-1 (2014)

44

treaty some other international aspects of a tax system (withholding tax rate and corporate tax rate). Finally, our findings shed more light on the effects of a tax policy consisting on reductions of corporate tax rates combined with a more extensive bilateral tax treaties network. References Avi-Yonah (2009), "Double Tax Treaties: An Introduction." in K. P. Sauvant and L. E. Sachs (ed.), The Effect of Treaties on Foreign Direct Investment: Bilateral Investment Treaties, Double Taxation Treaties and Investment Flows, Oxford University Press. Barrios, S., H. Huizinga, L. Laeven, and G. Nicodème (2009), “International Taxation and Multinational Firm Location Decisions”, Taxation Papers, European Commission. Barthel, F., M. Busse, and E. Neumayer (2009), “The Impact of Double Taxation Treaties on Foreign Direct Investment: Evidence from Large Dyadic Panel Data”, Contemporary Economic Policy, 28, 366-377. Blonigen, B. and R. Davies (2004),“The effects of bilateral tax treaties on U.S. FDI activity”, International Tax and Public Finance, 11, 601-622. Blonigen, B. and R. Davies, (2002), “Do bilateral tax treaties promote foreign direct investment?”, Working paper 8834, National Bureau of Economic Research. Buettner, T. and M. Ruf (2007), “Tax incentives and the location of FDI: Evidence from a panel of German multinationals”, International Tax and Public Finance, 47, 151-165. Cameron, A. and P. Trivedi (2010), Microeconometrics Using Stata (Texas, Stata Press Publication, Revised Edition). Davies, R. (2003), “Tax treaties, renegotiations, and foreign direct investment”, Economic Analysis and Policy, 33, 251-273. Davies, R., P. Norback and A. Koru, (2009), “The Effect of Tax Treaties on Multinational Firms: New Evidence from Microdata”, The World Economy, 32, 77-110. Devereux, M. (2006), “The Impact of Taxation on the Location of Capital, Firms and Profit: A Survey of Empirical Evidence”, Working Paper 07/02, University of Oxford. Devereux, M. and R. Griffith, (1998), “Taxes and the Location of Production: Evidence from a Panel of U.S. Multinationals”, Journal of Public Economics, 68, 335-367. Egger, P. and V. Merlo (2011), “Statutory Corporate Tax Rates and Double-Taxation Treaties as Determinants of Multinational Firm Activity”, FinanzArchiv/Public Finance Anlysis, 67, 145-170. Feld, L. P. and J. H. Heckemeyer (2011), “FDI and Taxation: A Meta-Study”, Journal of Economic Surveys, 25, 233-272. Finkenzeller, M. and C. Spengel (2004), “Measuring the effective levels of company taxation in the new member states: A quantitative analysis”, Working paper Taxation papers, European Commission. Frias, I., A. Iglesias, and E. Vasquez-Rozas (2005), “The effects of the enlargement of the EU: The mobility of factors of Production”, Applied Econometrics and International Development, 5-1, 93-112. Grubert, H. and J. Mutti (2000), “Do Taxes Influence Where U.S. Corporation Invest?”, National Tax Journal, 53, 825-840. Huizinga, H., L. Laeven, and G. Nicodème (2008), “Capital Structure and International Debt Shifting”, Journal of Financial Economics, 88, 80-118. Louie, H. and D. Rousslang (2008), “Host-Country Governance, Tax Treaties and U.S. Direct Investment Abroad”, International Tax and Public Finance, 15, 256-273. Millimet, D. and A. Kumas (2007), “Reassessing the Effects of Bilateral Tax Treaties on U.S. FDI Activity”, Working Paper, Southern Methodist University.

Marques, M., Pinho, C. Effects of Corporate Taxation on European Multinationals’ Investment

45

Mooij, R. and S. Ederveen (2003), “Taxation and Foreign Direct Investment: A Synthesis of Empirical Research”, International Tax and Public Finance, 10, 673-693. Mooij, R., andS. Ederveen (2006), “What a Difference Does It Make? Understanding the Empirical Literature on Taxation and International Capital Flows”. Economic Papers no. 261, European Commission. Neumayer, E. (2007), “Do Double Taxation Treaties Increase Foreign Direct Investment to Developing Countries?”, Journal of Developing Studies, 43, 1501-1519. Ruf, M. and A. Weichenrieder (2009), “The Taxation of Passive Foreign Investment. Lessons from German Experience”, CESifo Working Paper no. 2624. Santos Silva, J. and S. Tenreyro (2006), The Log ofGravity, The Review of Economics and Statistics, 88, 641-658.

Annexes

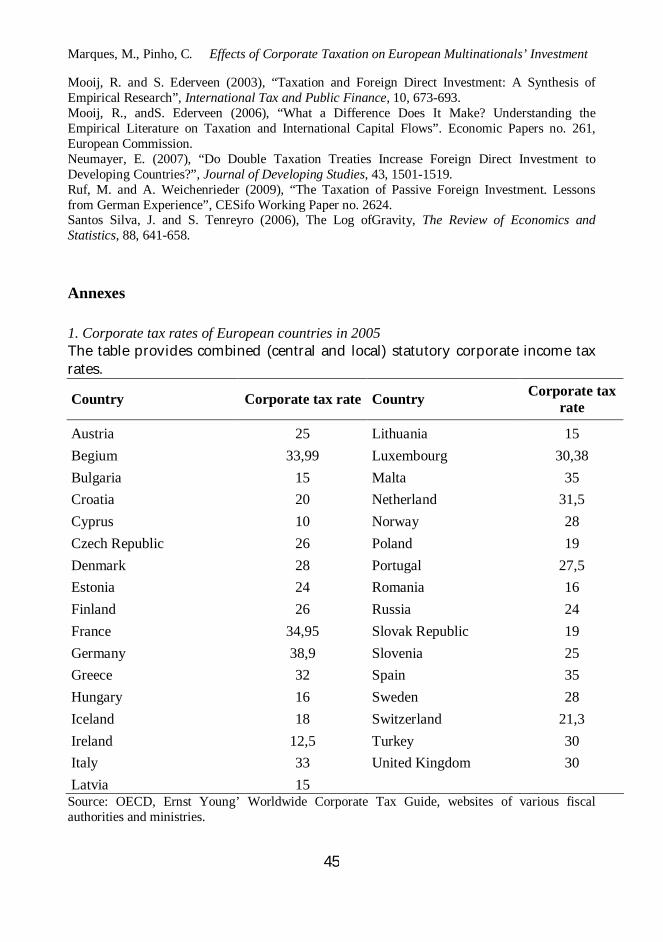

1. Corporate tax rates of European countries in 2005 The table provides combined (central and local) statutory corporate income tax rates.

Country Corporate tax rate Country Corporate tax rate

Austria 25 Lithuania 15 Begium 33,99 Luxembourg 30,38 Bulgaria 15 Malta 35 Croatia 20 Netherland 31,5 Cyprus 10 Norway 28 Czech Republic 26 Poland 19 Denmark 28 Portugal 27,5 Estonia 24 Romania 16 Finland 26 Russia 24 France 34,95 Slovak Republic 19 Germany 38,9 Slovenia 25 Greece 32 Spain 35 Hungary 16 Sweden 28 Iceland 18 Switzerland 21,3 Ireland 12,5 Turkey 30 Italy 33 United Kingdom 30 Latvia 15

Source: OECD, Ernst Young’ Worldwide Corporate Tax Guide, websites of various fiscal authorities and ministries.

Applied Econometrics and International Development Vol. 14-1 (2014)

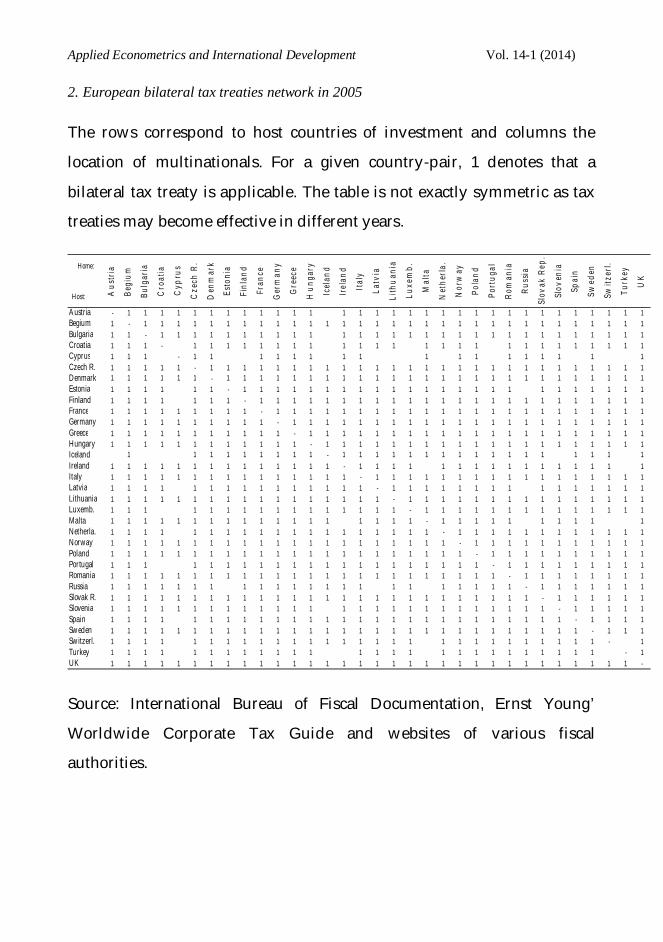

2. European bilateral tax treaties network in 2005

The rows correspond to host countries of investment and columns the

location of multinationals. For a given country-pair, 1 denotes that a

bilateral tax treaty is applicable. The table is not exactly symmetric as tax

treaties may become effective in different years.

Aus

tria

Begi

um

Bulg

aria

Cro

atia

Cyp

rus

Cze

ch R

.

Den

mar

k

Esto

nia

Finl

and

Fran

ce

Ger

man

y

Gre

ece

Hun

gary

Icel

and

Irel

and

Italy

Latv

ia

Lith

uani

a

Luxe

mb.

Mal

ta

Net

herla

.

Nor

way

Pola

nd

Port

ugal

Rom

ania

Russ

ia

Slov

ak R

ep.

Slov

enia

Spai

n

Swed

en

Switz

erl.

Turk

ey

UK

Austria - 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1Begium 1 - 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1Bulgaria 1 1 - 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1Croatia 1 1 1 - 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1Cyprus 1 1 1 - 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1Czech R. 1 1 1 1 1 - 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1Denmark 1 1 1 1 1 1 - 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1Estonia 1 1 1 1 1 1 - 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1Finland 1 1 1 1 1 1 1 - 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1France 1 1 1 1 1 1 1 1 1 - 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1Germany 1 1 1 1 1 1 1 1 1 1 - 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1Greece 1 1 1 1 1 1 1 1 1 1 1 - 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1Hungary 1 1 1 1 1 1 1 1 1 1 1 1 - 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1Iceland 1 1 1 1 1 1 1 1 1 - 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1Ireland 1 1 1 1 1 1 1 1 1 1 1 1 1 1 - 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1Italy 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 - 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1Latvia 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 - 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1Lithuania 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 - 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1Luxemb. 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 - 1 1 1 1 1 1 1 1 1 1 1 1 1 1Malta 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 - 1 1 1 1 1 1 1 1 1 1Netherla. 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 - 1 1 1 1 1 1 1 1 1 1 1 1Norway 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 - 1 1 1 1 1 1 1 1 1 1 1Poland 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 - 1 1 1 1 1 1 1 1 1 1Portugal 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 - 1 1 1 1 1 1 1 1 1Romania 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 - 1 1 1 1 1 1 1 1Russia 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 - 1 1 1 1 1 1 1Slovak R. 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 - 1 1 1 1 1 1Slovenia 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 - 1 1 1 1 1Spain 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 - 1 1 1 1Sweden 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 - 1 1 1Switzerl. 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 - 1Turkey 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 - 1UK 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 -

Home:

Host:

Source: International Bureau of Fiscal Documentation, Ernst Young’

Worldwide Corporate Tax Guide and websites of various fiscal

authorities.