Embed Size (px)

Citation preview

Economic Analysis of Snohvit

Expansion Project

COVER

Trian Hendro Asmoro

51445172

August, 2015

A thesis presented in partial fulfilment of the requirements for

the degree of MSc Petroleum Energy Economics and Finance

at the University of Aberdeen

ii

for Dika, Safa, Aidan

iii

DISCLAIMER

I declare that this thesis has been composed by myself, that it has not been accepted in any

previous application for a degree, that the work of which it is record has been done by

myself, and that all quotations have been distinguished appropriately and the source of

information specifically acknowledged.

Trian Hendro Asmoro

August 10th

, 2015

iv

ABSTRACT

Norway has clear interests in hydrocarbon production in arctic provinces. Barents Sea

in Arctic region has played significant role in producing hydrocarbon for Norway since the

establishment of Snohvit LNG plant in 2007 by Statoil. It was estimated to be a new frontier

for further development projects in the region. Some recent discoveries have likely indicated

a plan to expand current LNG operation. Meanwhile, northern sea route has become more

commercially attractive in connecting North-East Asia countries, e.g. Japan and China, with

their North-Western European counterparts, e.g. Netherlands and Norway, as a result of

melting arctic ice caps.

There would be opportunities in the near future for Snohvit expansion project to supply

LNG to North-East Asia as well as obtaining LNG technology suppliers from North-East

Asia. The project needs therefore to be analysed using key project’s variables, such as

discoverable gas reserve, LNG price and project costs in which Snohvit is one of most

expensive LNG projects. Project economics model with discounted cash flow method and

montecarlo simulation is used to do economic analysis. This research shows that project

scenario, development options and prospects in the LNG market play role to determine the

feasibility of Snohvit expansion project.

v

LIST OF CONTENTS

COVER ....................................................................................................................................... i

DISCLAIMER ......................................................................................................................... iii

ABSTRACT .............................................................................................................................. iv

LIST OF CONTENTS ............................................................................................................... v

LIST OF FIGURES .................................................................................................................. vi

LIST OF TABLES ................................................................................................................... vii

CHAPTER I: INTRODUCTION ............................................................................................... 1

CHAPTER II: LITERATURE REVIEW .................................................................................. 4

2.1. Norwegian Barents Sea ............................................................................................... 4

2.2. Snohvit LNG ............................................................................................................... 7

2.3. Norwegian Petroleum Fiscal System .......................................................................... 9

2.4. LNG Market and Price .............................................................................................. 11

2.5. Northern Sea Route ................................................................................................... 14

CHAPTER III: METHODOLOGY AND DATA ................................................................... 17

3.1. Methodology ............................................................................................................. 17

3.2. Data and Assumptions ............................................................................................... 19

CHAPTER IV: RESULT AND ANALYSIS .......................................................................... 24

4.1. Economic Indicators .................................................................................................. 24

4.2. Sensitivity Analysis ................................................................................................... 24

4.3. Probabilistic Output................................................................................................... 29

4.4. Scenario Analysis ...................................................................................................... 32

4.5. Discussion ................................................................................................................. 35

CHAPTER V: CONCLUSION................................................................................................ 39

BIBLIOGRAPHY .................................................................................................................... 42

APPENDIX 1: MODEL INPUT .............................................................................................. 46

APPENDIX 2: MODEL CALCULATION ............................................................................. 47

APPENDIX 3: MODEL SIMULATION INPUT .................................................................... 51

APPENDIX 4: UNIT COST PROBABILITY ........................................................................ 52

GLOSSARY ............................................................................................................................ 53

vi

LIST OF FIGURES

Figure 1-1 Potential Arctic Oil and Gas Resources ................................................................... 1

Figure 2-1 Norwegian Oil and Gas Provinces ........................................................................... 4

Figure 2-2 Oil and Gas Discoveries in the Barents Sea ............................................................. 5

Figure 2-3 Snohvit Field in the Barents Sea .............................................................................. 7

Figure 2-4 Petroleum Taxation System in Norway ................................................................. 10

Figure 2-5 Natural Gas Prices .................................................................................................. 12

Figure 2-6 Typical LNG Value Chain ..................................................................................... 13

Figure 2-7 NSR and Current SSR ............................................................................................ 14

Figure 2-8 Vessels and Tons Cargo Sailed in the NSR ........................................................... 15

Figure 2-9 Northern Sea Route Detail ..................................................................................... 16

Figure 3-1 Research Framework of Snohvit Expansion Project .............................................. 17

Figure 3-2 Research Methodology........................................................................................... 19

Figure 3-3 Triangular Distribution of Development Cost ....................................................... 20

Figure 3-4 LNG Unit Cost for High Cost Projects .................................................................. 21

Figure 4-1 Sensitivity Chart of NPV ....................................................................................... 25

Figure 4-2 Sensitivity Chart of NPV without Uplift ................................................................ 26

Figure 4-3 Sensitivity Chart of IRR ......................................................................................... 27

Figure 4-4 Sensitivity Chart of IRR without Uplift ................................................................. 28

Figure 4-5 Simulation Result of Project’s NPV ...................................................................... 30

Figure 4-6 Simulation Result of Project’s IRR ........................................................................ 30

Figure 4-7 Simulation Result of Project’s NPV and NPV Capex Ratio .................................. 31

Figure 4-8 Unit Cost Probability for 1.3 MTPA ...................................................................... 36

Figure 4-9 Liquefaction Plant Metric Cost .............................................................................. 37

vii

LIST OF TABLES

Table 4-1 Deterministic Output of Economics Model ............................................................. 24

Table 4-2 Project Scenario ....................................................................................................... 33

Table 4-3 Decision Table for Project’s NPV ........................................................................... 33

Table 4-4 Decision Table for NPV Project and Capex Ratio .................................................. 34

Table 4-5 Project Scenario and Development Cost (Mean Capex) ......................................... 35

Table 4-6 Project Scenario and Decision Table ....................................................................... 35

Table 4-7 Probability of Unit Cost........................................................................................... 36

1

CHAPTER I: INTRODUCTION

In 2008, the U.S. Geological Survey (USGS) completed an appraisal of possible future

additions to world oil and gas reserves from new field discoveries in the Arctic. It resulted in

an assessment of potential undiscovered and technically recoverable crude oil, natural gas,

and natural gas liquid resources in the Arctic region including the Barents Sea Shelf of

Norway. According to USGS, the total mean undiscovered conventional oil and gas resources

of the Arctic are estimated to be approximately 90 billion barrels of oil (BOE), 1,669 trillion

cubic feet (TCF) of natural gas, and 44 billion barrels of natural gas liquids. Converting these

figures to BOE and adding them up, a total of 412 billion BOE could be found (USGS 2008).

The USGS study estimated that the Arctic could hold about 13% of the world’s undiscovered

oil resources and as much as 30% of the world’s undiscovered natural gas resources. In other

words, it was about 22% of the global undiscovered conventional oil and gas resources

(Lindholt, Glomsrød 2012). By allocating the estimated resources/provinces to the nearest

country, Norway is estimated to hold 12% of the total Arctic resources (EY 2013), where

most of it is gas resources as shown in Figure 1-1. However, hydrocarbon exploration and

production (E&P) activities in the Arctic are always challenging and cash-intensive.

Figure 1-1 Potential Arctic Oil and Gas Resources

(Source: EY 2013)

The Barents Sea has played increasingly significant role in producing hydrocarbon for

Norway during the last few years, as the country is experiencing considerable shrinkage of its

hydrocarbon production from Norwegian and North Sea. The Barents Sea has also been

considered as the most exciting new area of oil and gas, along with the northern part of the

2

Norwegian Sea since the establishment of Snohvit LNG plant in Melkoya Island in 2007 by

Statoil (Auran et al. 2012). It is important to note, however, that the significant development

costs have hampered its economics. In addition, harsh winters with extreme temperatures,

combined with limited supply lines to energy consumers, as well as a lack of adequate

infrastructure and delicate environmental issues, provide problematic conditions for

developing oil and gas fields in arctic (Harsem, Eide & Heen 2011). Although LNG transport

from Melkoya is the only gas infrastructure developed in the northern part of the world today,

Snohvit LNG plant was one of the most expensive LNG investments ever (Songhurst 2014).

There have been some discoveries in the Barents Sea in recent years that leads to the

possibility of building the second train of Snohvit LNG plant (Auran et al. 2012, EY 2013).

Norway, one of the world’s largest gas exporters, has clear interests in oil and gas production

in arctic provinces. The country is heavily dependent on the oil and gas sector, as the industry

accounted for 23% of the Norwegian GNP, 30% of the state revenues and 52% of Norway’s

total exports in 2012 (Moe 2013). If Norway wants to continue its current output level, arctic

oil and gas activities must intensify. There is an estimate of 0.3 billion standard cubic meters

of oil equivalents of extractable hydrocarbon identified (mainly gas) in the Norwegian

Barents Sea, with additional estimate of 1 billion standard cubic meters of oil equivalents

resources unidentified (Kullerud 2011). Nevertheless, the country’s aggressiveness in

exploring and developing the Arctic region may also be adversely affected by its caution of

the CO2 emissions impact of the activities (Harsem, Eide & Heen 2011).

The most important factor in exploring the Arctic region, unsurprisingly, is the super-

cooled gas, commonly known as LNG, that is averagely traded at a premium of about US$16

per million British thermal unit (MMBTU) in Far East market (BP 2015). In addition, global

investment in LNG infrastructure and facilities has risen, and they are now spread across

more countries, while the size of the LNG tanker fleet has expanded significantly, and

transport costs have fallen (Ritz 2014). Moreover, the trend of relatively higher LNG prices

in Asian markets is believed to continue further as countries such as Japan, South Korea,

Taiwan, India and China keep experiencing relatively high economic growth (Rogers, Stern

2015). Meanwhile, climate change has played a significant role in expanding access to the

Arctic region. The northern sea route (NSR) has therefore become more commercially

attractive in connecting North-East Asia countries, such as Japan, South Korea, Taiwan and

China, with their North-Western European counterparts, such as Netherlands, Norway, UK

and Germany, as a result of melting arctic ice caps (Bekkers, Francois & Rojas-Romagosa

3

2015). All things considered, there would be opportunity in the near future to supply LNG

from second train of Snohvit LNG plant to North-East Asia in addition to equipment and

services movement from North-East Asia to support the Snohvit expansion project.

In correspondence with research background above, there are three research questions

that have to be answered through the research. First, how main variables of project

economics, e.g. cost, recoverable gas, LNG prices, behave in determining the project

economics output of Snohvit expansion project. Second, how factors within internal project’s

boundaries are required to make the project feasible, given current conditions faced by the

project. Third, how development options or project scenario and prospects in the LNG market

play role to determine the project’s feasibility.

To discuss and answer the research questions, this dissertation is organised as follows:

Chapter 1: Introduction. This chapter mainly describes about background or motivation of

the research.

Chapter 2: Literature Review. This chapter will discuss some relevant literatures to

support the research.

Chapter 3: Methodology and Data. This chapter will explain methodology, data and

assumptions used in the research.

Chapter 4: Result and Analysis. This chapter will present and analyse the results of the

research.

Chapter 5: Conclusion. This chapter will consist of conclusion and recommendation

obtained from the research.

4

CHAPTER II: LITERATURE REVIEW

2.1. Norwegian Barents Sea

Norway is estimated to hold 12% of the total Arctic resources with most of it being gas

resources (USGS 2008, EY 2013). More specifically 0.3 billion standard cubic meters of oil

equivalents of extractable hydrocarbon have been identified (mainly gas) in the Norwegian

Barents Sea, with additional 1 billion standard cubic meters of oil equivalents resources

estimated to be unidentified (Kullerud 2011, Klett, Gautier 2009). In recent years, the

country’s interest in the Barents has picked up significantly as it is estimated to contain up to

42% of Norway’s undiscovered reserves (ECC 2013). Another contributing factor to the

significance of Barents Sea’s activities is that the recent years’ decline of Norwegian

hydrocarbon output. Meanwhile, liquefied natural gas (LNG) production that is processed

from Snohvit and other fields has significantly contributed to Norwegian production level in

mitigating the fast decline of Norwegian hydrocarbon production (Moe 2013). This along

with the maturity of Norwegian Sea and North Sea fields suggest that the development of the

Norwegian Arctic region, e.g. Barents Sea, as new petroleum provinces will attract more

interests from the country government, despite the uncertainties associated with the resource

estimates and their cost (Lindholt, Glomsrød 2012). The Norwegian oil and gas provinces are

shown in Figure 2-1.

Figure 2-1 Norwegian Oil and Gas Provinces

(Source: Heiersted 2005)

5

Oil and gas activities in the Barents Sea had led to a sensitive issue regarding the shared

border between Russia and Norway. The 2010 agreement between the two countries on

Arctic border in Barents Sea generated significant opportunities for resource development

(Wilson Centre 2013). The countries agree to set aside their differences and establish a

maritime border so that they can explore in the region. The treaty represents a compromise,

with the two countries agreeing to a border that splits this area roughly in half (EY 2013).

This has led to increasing activities in the Barents Sea, resulting to several discoveries, such

as Skrugard and Havis during 2011-2012 which is believed to have proven resources of 400-

600 million barrels of recoverable oil (Statoil 2014a). The latest discovery in the Drivis

prospect in the Barents Sea was announced by Statoil, a Norwegian-owned oil and gas

company, in 2014 after conducting exploration program around the Johan Castberg (former

Skrugard) field. The discovery will add the existing portfolio of other discoveries within the

Johan Castberg province as shown in Figure 2-2, so that it creates a basis for further Johan

Castberg development project (Statoil 2014a).

Figure 2-2 Oil and Gas Discoveries in the Barents Sea

(Source: Statoil 2014a)

The development of gas fields will be more challenging if they are contaminated with

CO2 or other pollutants, because it would impact on how oil and gas in the Barents Sea will

be developed. Snohvit LNG is the world’s first LNG plant with CO2 capture and storage,

since the country strongly supports for the Kyoto agreement, and for a worldwide reduction

of carbon emissions (Harsem, Eide & Heen 2011). The government had even deferred the

6

decision to give a green light for further exploration activities in the region due to sensitive

ecological-related issues associated with this area (Wilson Centre 2013). There are

recognised risks related with oil and gas activities particularly in offshore installation and

production, such as hydrocarbon leaks from subsea production systems, pipelines, risers and

subsea well kicks or loss of well control (Vinnem et al. 2006). These risks have risen

significantly, in parallel with the growing offshore oil and gas activities recently. In particular

to LNG operation, most LNG tankers are new and safe, while gas leaks and LNG spills

accidents are infrequent. Risks such as LNG accidents which include collisions and

groundings are small and manageable due to current safety policies and practises (Auran et

al. 2012). An accidental discharge of oil and gas mixture below sea level, for instance, can

instigate a release of toxic chemicals into the water column and sediment pore water. This

may increase morbidity and mortality of marine life of various species in the long-term

(Nazir et al. 2008).

In spite of the increased activity in arctic resources, their development is still both high-

cost and high-risk. The major challenges related with arctic development include harsh

climate effects such as the intense cold for most of the year, long periods of near-total

darkness, and the potential ice-pack damage to offshore facilities, limited existing

infrastructure, spill containment/spill recovery, overlapping/competing economic sovereignty

claims, country-specific environment laws/regulations (EY 2013). On the other hand, the

booming global gas supply, both from conventional and unconventional sources, will

significantly challenge the Arctic gas development. There are increasing estimates of non-

frontier resource potential of which almost all could be developed at less cost and with lower

environmental risk compared with Arctic resources (EY 2013). Therefore, if the Norwegian

government wants to increase the activities in the Barents Sea, there are many things that

should be taken into account regarding the economics feasibility of Arctic development,

environmental concerns, and perhaps most importantly, public opinion (Harsem, Eide &

Heen 2011).

Since Snohvit, the first hydrocarbon development in the Arctic region is viewed as one

of high cost LNG investments (Songhurst 2014), the next section will describe the profile of

Snohvit LNG and Norwegian petroleum fiscal system. Subsequently, LNG market and price

mechanism will be discussed. Finally, northern sea route will be seen as an alternative route

to transport LNG from Barents Sea to Asia.

7

2.2. Snohvit LNG

Snohvit LNG plant is located in Melkoya Island, a dedicated island in the Barents Sea,

near Hammerfest, Norway. It processes natural gas produced from Snohvit, Albatross and

Askeladd field which lie about 140 km northwest of Hammerfest. The Snohvit and Albatross

fields came on stream in 2007, while the Askeladd is due to come on stream in 2014-15

(Hydrocarbon-technology 2012). The total reserve from those producing fields is estimated

190 billion cubic meters (BCM) gas or about 6.8 trillion cubic feet (TCF) (Heiersted 2005).

Those fields have nine production wells and the other 20 production wells are planned to

drill. The wells are producing gas by means of a remote-controlled subsea solution that

includes pipelines to land, while the production plant is located on the seabed between 250

and 345 metres below the sea surface (Statoil 2013a) as depicted in Figure 2-3.

Figure 2-3 Snohvit Field in the Barents Sea

(Source: Norwegian Ministry of Environment 2011)

Large volumes of natural gas are transported through a 143-kilometre multiphase

transport pipeline to shore. It has set a new record for long-distance transportation of

unprocessed well stream (Statoil 2013a). The feed gas has 5-8 % CO2 content. Consequently,

it also has a carbon dioxide capture and storage facility. A 153-km separate pipeline ensures

that CO2 from the plant is returned to the Snohvit field, where it is stored in an appropriate

geological layer located 2.6 km beneath the seabed of the Snohvit field. Snohvit plant was

designed to operate until 2035, started producing gas in October 2007, while the first CO2

was injected in April 2008 (Hydrocarbon-technology 2012) . In addition, it is the first LNG

facility with CO2 capture and storage in the world. A total of nearly 2 million tonnes of CO2

had been stored in the Snohvit field until early 2013 (Statoil 2014a).

8

Regarding the commercial aspects of the project, it requires total investment of US$ 5.6

Billion (NOK 39.5 billion). Most of the capital invested goes to offshore, land and flow

systems 58 %, in which some portion will be spent for further drilling and development in 20

years of 25-year production period. It was constructed for 48 months from its investment

decision (Heiersted 2005). Snohvit has single train LNG with production capacity of 4.3

million tonnes per annum (MTPA) LNG or equivalent to approximately 5.7 BCM of LNG.

Thus, the unit cost of LNG per annum will be about US$ 1,300 per tonne per annum (TPA).

Although it was a green field project, it is regarded as one of high cost LNG projects

compared to the low cost ones that cost below 1,000 US$/TPA (Songhurst 2014). LNG

contracts were agreed with customers for 25 years delivery as follows: 1.8 MTPA to the US

east coast (El Paso), 1.2 MTPA to the Spain (Iberdrola), and the remaining capacity will go to

Gaz de France and Total (Hydrocarbon-technology 2012, Heiersted 2005).

Snohvit is considered by Statoil as a milestone project for further development project

in the Norwegian Barents Sea. The company estimated that Snohvit would be a new frontier

in the Arctic which could cover gas fields within about 250 km from LNG plant (Heiersted

2005). Thus, it can foster an opportunity to expand the Snohvit LNG plant for its second train

in relation to some following discoveries in the Barents Sea. However, the latest discoveries

in the Barents Sea, e.g. Skrugard (2011) and Havis (2012) have been oil discoveries as

compared to the expected gas reservoirs (Auran et al. 2012). As a result, Statoil as main

operator in the Barents Sea and its partners decided in 2013 to stop work on a possible

capacity increase on Snohvit LNG because the gas discoveries had not provided a sufficient

basis for such expansion project. It was also reported that other scenario such as new pipeline

transportation could not make the project profitable (Statoil 2013b).

However, there were some other hydrocarbon discoveries in the following years in

Johan Castberg (former Skrugard) region, e.g. Nunatak (2013), Iskrystall (2013), Skavl

(2013), Kramsno (2014) and Drivis (2014). The first two discoveries proved only gas

reservoirs, whereas the rest proved oil reservoirs as shown in Figure 2-2. Although the

exploration program around the Johan Castberg field has been vital in providing area

knowledge, but the company stated that it has not delivered expected oil volumes to make the

project profitable (Statoil 2014a). Johan Castberg has reflected the possible discovery area

company mentioned before that can actually feed the natural gas for Snohvit expansion

project. It is located in the Barents Sea, about 100 km north of the Snohvit field and nearly

240 km from Melkoya Island (Statoil 2014b). Nevertheless, Statoil and its partners have not

9

amended the last decision they made that they stopped work on possible capacity increase in

Snohvit LNG plant.

2.3. Norwegian Petroleum Fiscal System

After looking at the possible discoverable gas fields, petroleum fiscal system needs to

be taken into account in analysing the project. The ultimate objective of a petroleum fiscal

system is to balance the associated risk and reward between investors and government (state).

The Norwegian government has modified the fiscal system in several versions to achieve the

objective. Oil and gas industry itself have operated in Norway since 1965 when the first

Norwegian licences were awarded. The first discovery was Ekofisk field in 1969, and the first

production commenced in 1971 (Jansen, Bjerke 2012). The country has been heavily

dependent on the oil and gas sector since then, for example it accounted for 23% of the

Norwegian GNP, 30% of the state revenues and 52% of Norway’s total exports in 2012 (Moe

2013). The revenue is derived from petroleum resources partly through direct participation in

the petroleum sector with SDFI (State's Direct Financial Interest) mechanism, and partly

through taxation. The petroleum revenues have contributed significant value to the

Norwegian state over the years, and it will likely continue to do so for years to come (Jansen,

Bjerke 2012, Moe 2013).

The Norwegian petroleum taxation code includes direct and indirect taxation. The

direct taxation relates to company upstream activities comprising 28% general income tax

and an additional 50% special tax on income from petroleum production and pipeline

transportation activities (Jansen, Bjerke 2012). This 50% special tax on petroleum activities is

intended to capture the resource rent, which is defined as the return over and above normal

profits from oil and gas activities after deducted all necessary costs. The idea behind this

special tax is that Norway provides licences to oil and gas companies under the term that the

state can capture this resource rent (Aarsnes, Lindgren 2012). Thus, a total marginal tax rate

78% is levied to oil and gas earnings in Norway. Meanwhile, indirect taxation consists of

carbon dioxide (CO2), nitrogen oxide (NOx) tax, VAT and an area fee charged for acreage.

These indirect taxations play a limited role for companies engaged in exploration and

production as well as having less importance to the state finance compared to direct taxations

(Jansen, Bjerke 2012, Deloitte 2014). Finance cost of interest bearing debt that has relevance

for the petroleum investment is allowed as tax deductible item in the taxation system. To

encourage investment, a special uplift of 7.5% of capital expenditure is provided for 4 years

(totalling 30%). This is intended to protect normal profits from being taxed with the 50%

10

special tax, which can be deducted against the tax base before the special tax of 50% is

applied (Aarsnes, Lindgren 2012). The taxation system is summarised in Figure 2-4.

Figure 2-4 Petroleum Taxation System in Norway

(Source: Aarsnes, Lindgren 2012)

The Norwegian petroleum tax system is regarded as a neutral tax system that performs

well regarding net present value per dollar invested and break-even prices. In addition, it

provides considerably low risk and few distortions to pre-tax economics. The system uses a

company based tax system, not project/field based or ring fence mechanism (Moe 2013).

Most importantly, the state offers some special rules and incentives aside of capital uplift.

Firstly, there is a loss carry-forward in the petroleum tax system, and the loss is allowed to be

carried forward indefinitely with interest based on discount factors as stipulated by

Norwegian Finance Ministry (Aarsnes, Lindgren 2012). Secondly, highly attractive 78% tax

refund will be given by the Norwegian Petroleum Directorate for costs of exploration wells as

alternative to carrying the losses forward. Such costs include all direct and indirect costs

incurred except finance costs. This refund also applies to any unused losses at the point when

a company abandon its Norwegian offshore activities (Deloitte 2014). This tax refund

mechanism clearly shows that the government want to maintain Norway’s present status as a

major and reliable oil and gas producer, and create the basis for the commercial development

of resources in the region (ECC 2013).

Some other incentives have been also applied for very specific projects, such as Snohvit

LNG project. Snohvit had accelerated depreciation that was a three-year straight-line

depreciation from and including the year the investment was made instead of a normal six-

year straight-line depreciation (Aarsnes, Lindgren 2012). Moreover, the scope of the

petroleum taxation actually makes it necessary to distinguish between the activities of a

company which fall within the 78% special tax, and other activities which are only liable to

the general income tax of 28%. The distinction is often referred to as offshore income and

11

onshore income (Jansen, Bjerke 2012). As a result, Snohvit LNG project actually had two

separate tax system, i.e. onshore operations are only liable to 28% corporate tax, while the

offshore are also liable to 50% special tax in addition to the corporate tax (Jansen, Bjerke

2012). The LNG- facilities would most likely fall outside the scope of special tax and be

considered an onshore activity. However, since the Snohvit-project was granted specific tax

benefits in the form of accelerated depreciation and uplift, LNG-facilities were included to be

within the scope of special tax (Jansen, Bjerke 2012).

2.4. LNG Market and Price

The realisation of profit as result of petroleum fiscal system to the investor and the state

relies heavily on LNG price. Thus, the current and future LNG market is extremely important

in analysing the expansion project. Global natural gas demand itself has increased

significantly over the last twenty five years, where global natural gas consumption in 2013

was double than that in 1988. Meanwhile, global LNG business has so far been driven by

Asia, underpinned by consumption in Japan, South Korea and Taiwan. In addition, India,

China, Singapore, Vietnam and Thailand are the newly emerging consumers of LNG in Asia

pacific (Kumar et al. 2011). The growth of natural gas consumption in Asia Pacific from

2013 to 2014 was 2.0%, whereas the global growth of natural gas consumption for the same

period was only 0.4% (BP 2015). The rapid Asian economic growth has become the main

factor of increasing gas demand. The LNG consumption from Asia Pacific is expected to

continue to rise in the upcoming years from three established LNG markets of Japan, Korea

and Taiwan. Although the rate of growth in LNG imports in Japan is expected to slow, it will

remain the largest and one of the most important markets in the region (Kumar et al. 2011).

The Fukushima accident of March 2011 has effectively switched off large parts of Japanese

nuclear power implying to an increase in demand for imported LNG to “fill the gap” (Ritz

2014). In addition, strong growth is also projected in the emerging LNG markets of India and

China as both countries seek LNG imports to complement existing domestic gas supplies and

to fuel expected fast growth in economic output and electricity generation, and to increase the

use of clean energy sources (Kumar et al. 2011). In particular, China has shown strong

growth in LNG demand of 8.6% from 2013 to 2014 (BP 2015).

The LNG prices around the world vary widely, and the increasing LNG demand from

Asian countries causes higher LNG prices in Asia than those in Europe and North America as

shown in Figure 2-5. Moreover, the international LNG trade in Asia has been based on the

Japan Crude Cocktail or Japanese Customs-Cleared Crude Oil (JCC) price mechanism, a

12

monthly published index by the Japanese government representing the average oil import

prices into Japan, over the past 25 years. Due to high natural gas prices in Japan, it attracts

more LNG supplies to Northeast Asia countries, e.g. Japan, South Korea, Taiwan, and China

(Rogers, Stern 2015). Before 2010, Asia Pacific imported LNG from Middle East countries,

such as Abu Dhabi, Qatar, and Oman accounting for only 10–15% of total LNG consumption

(Kumar et al. 2011), but it increased dramatically to about 40% of total LNG consumption in

Asia Pacific during 2014 (BP 2015). In addition, LNG from US is forecasted to start

supplying Asian LNG importers in the post 2015 periods. This may create a tighter LNG

market, and shift LNG pricing mechanism in Asia implying a decrease trend in the LNG

contract prices and in the long term LNG contracts (Rogers, Stern 2015).

Figure 2-5 Natural Gas Prices

(Source: BP 2015)

In the contract side, long-term contracts between exporters and importers of LNG have

been widely used in LNG trades. These contracts provide certainty, and increase the debt

capacity of large, long-lived, capital investments by reducing cash flow variability (Hartley

2013). Despite a decline trend in the dominance of long-term contracts, LNG producers have

preference to long-term contracts because LNG projects are very capital intensive. The

contract prices are determined based on whether LNG is priced free-on-board (FOB) or ex-

ship. The ex-ship contract reflects downstream market prices (Henry Hub for the US or JCC

for Japan) less gasification and other destination terminal costs and shipping, including

insurance. The remainder (netback to producer) must be sufficient enough to cover all costs

associated with developing of natural gas fields, liquefaction plant and export terminal costs

plus yield a sufficient return to equity. The FOB prices are prices of LNG delivered to the

13

tanker at the export terminal at producer’s premise. In this type, shipping and insurance are

the responsibility of the buyer. FOB contracts give buyers greater flexibility regarding

shipping costs and the ability to exploit profit opportunities through arbitrage (Maxwell, Zhu

2011). However, FOB contract prices can be linked to established spot market prices to avoid

big price differentials. In addition, it could have a formula in sales agreement to share any

gains from exercising arbitrage opportunities (Kellas 2008).

Global investment in LNG infrastructure and facilities has risen and diverged across

more countries in accordance with the higher LNG demand in the world. Although cost of

LNG development did fall significantly during the 1990s and early 2000s mostly due to

improved technology, there was a very substantial cost escalation which greatly exceeded the

overall increase in oil and gas production and development costs from the mid-2000s

(Songhurst 2014). Some LNG projects even experienced cost overruns of up to 30% such as

in Australia. The capital costs of existing projects was in the range of US$1,000-1,500 per ton

of LNG per annum (MTPA), while newer projects could be in the range of 2,500-3,600

US$/TPA (Rogers, Stern 2015). However, other less expensive types of LNG projects have

been developed in recent years, such as Floating LNG (FLNG) and smaller scale LNG, i.e.

medium, small, and mini LNG plant (Castillo, Dorao 2010, Marmolejo 2014).

Figure 2-6 Typical LNG Value Chain

(Source: Office of Fossil Energy 2005)

The size of the LNG tanker fleet has expanded significantly as result of increasing LNG

trades, thus transport costs have also fallen (Ritz 2014). For a typical LNG value chain as

shown in Figure 2-6, shipping represents 10 to 30% of total capital costs, exploration and

production of feed gas accounts for 15 to 20%, liquefaction comprises 30 to 45% of costs,

and gasification and storage account for the remainder, 15 to 25% (Office of Fossil Energy

2005). LNG shipping rates are usually sensitive not only to daily charter rates, but also to the

number of days in moving from point of departure to point of destination. Thus, decreases in

shipping costs increase netbacks and returns to equity for producers that deliver LNG on an

ex-ship basis. For FOB contracts, lower shipping costs increase profit margins for buyers

Exploration and Production

Processing and Liquefaction

Shipping Regasification and

Storage

14

(Maxwell, Zhu 2011). However, LNG shipping costs are determined not only by moving

costs on a set of known parameters, but also the level of price spreads between regions across

the global gas market. As global prices have diverged particularly post Fukushima accident,

shipping costs have played important role in recent years in determining the decisions on

cargo diversion to markets with higher price (Timera Energy 2015).

2.5. Northern Sea Route

As Northeast Asian countries would be the main targeted market by all LNG players

including Snohvit expansion project, northern sea route (NSR) could be taken into account as

the shorter shipping route that may lead to cheaper shipping cost to deliver the LNG to the

importers compared to southern south route (SSR) through Suez Canal. By definition, the

NSR, also known as northeast passage (NEP) before the beginning of the 20th century, is a

shipping lane between the Atlantic Ocean and the Pacific Ocean along the Russian coast of

Siberia and the Far East, crossing five Arctic Seas: the Barents Sea, the Kara Sea, the Laptev

Sea, the East Siberian Sea and the Chukchi Sea (Liu, Kronbak 2010), as shown in Figure 2-7.

The NSR has been seen as more viable alternative aside of the current SSR due to global

climate change that has melted arctic ice caps resulting in expanding access to the arctic

region (Bekkers, Francois & Rojas-Romagosa 2013).

Figure 2-7 NSR and Current SSR

(Source: Liu, Kronbak 2010)

NSR offers reductions on shipping distance between Northeast Asia countries, such as

Japan, South Korea, Taiwan and China, with Northern European countries, such as

Netherlands, Belgium, UK and Germany. For instance, the effective distance is reduced by

around 37% from Japan to North European countries, while the same figure is around 31%

for South Korea, 23% for China and 17% for Taiwan (Bekkers, Francois & Rojas-Romagosa

2013). The shipping-distance reductions can even be increased by about 3%, if the route from

Northern Asia countries continues to the region along the Scandinavian countries, such as

15

Norway, Sweden and Denmark (Lee, Song 2014). As a result, it could save 20-30% of

transport costs (Bekkers, Francois & Rojas-Romagosa 2013). In addition, since LNG contract

is preferably based on FOB, the shorter duration of shipping will be considered by the LNG

buyers since it could cut the shipping costs significantly.

The utilisation of NSR has generally shown an increase trend after 2010, though it was

open for navigation only for certain months in a year during summer months. In 2010, the

route was only used by four vessels carrying 111,000 tons of cargo. Then, the traffic

increased extremely with thirty-four vessels carrying 820,000 tons of cargo in 2011. One of

the reasons for the increase is the route that connects Europe to the Asia- Pacific region was

open for 141 days in 2011, one month longer than the norm of three months during a year

(CSIS 2013, Pettersen 2014). The numbers of vessels and tons cargo sailed along the NSR

from 2010 to 2014 is compiled in Figure 2-8 below. A steep downturn in 2014 was caused

by a downfall in bulk cargo transports from natural resources-based companies due to the

lower prices (Pettersen 2014). These figures are however still extremely low compared to the

traffic through the Suez Canal, reported 17,800 ships and about 690 million tons of cargo in

2011 (CSIS 2013). The main reasons of using Suez Canal compared to the NSR are because

the Suez Canal route offers larger vessel capacity, greater predictability, and opportunities to

stop at multiple ports along the way for maintenance and support. Most importantly, it

provides access to multiple markets along highly populated coastal areas, as container ships

rarely unload all cargo at a single destination (Buixadé Farré et al. 2014).

Figure 2-8 Vessels and Tons Cargo Sailed in the NSR

(Source: CSIS 2013, Pettersen 2014)

An economic analysis revealed that a 30% reduction in shipping distance using the

NSR does not correspond to a 30% cost saving. Thus, the benefits from the distance

16

reduction is offset by other factors, e.g. harsh weather, higher building costs for ice-classed

ships, non-regularity of route operation and slower speeds, navigation difficulties and greater

risks that drive to higher insurance fee, as well as the need for extra ice breaker service and

for extra time of obtaining the shipping permit (Liu, Kronbak 2010). The distance-saving

effects do not entirely guarantee the reduction of annual shipping time and cost as well as

increasing annual profit due to seasonal operation (Lee, Song 2014). Nevertheless, shipping

along the NSR depicted in Figure 2-9 still offers greater opportunities for bulk carriage of

resources, i.e. minerals and energy, from the Eurasian Arctic because it is more point to point

shipping that does not access to multiple markets. In addition, extensive exploration and

production activities in the region are likely to drive Arctic resource development, leading to

a growth of shipping traffic along the NSR (Buixadé Farré et al. 2014).

Figure 2-9 Northern Sea Route Detail

(Source: Buixadé Farré et al. 2014)

The NSR utilisation for LNG shipping has actually been initiated. There was a tanker

loaded with LNG first sailing the NSR from Snohvit plant in Hammerfest, Norway to Japan

in 2012. It was only a two-week shipping, an extreme shipping-time reduction up to 20 days

if using SSR (Nilsen 2012). Moreover, LNG Yamal project located on the eastern shore of

the Yamal Peninsula, Russia will also use the NSR to ship LNG to Asian markets. The Yamal

LNG plant will have a capacity of 16.5 MTPA and will be ready in 2017 (Staalesen 2014).

Furthermore, NSR is projected to operate for six months in a year during 2020 to 2024, for

nine months in a year from 2025 to 2029, and for twelve months starting from 2030. It is also

expected that some current barriers in the NSR as mentioned before would reduce after 2020

(Lee, Song 2014).

17

CHAPTER III: METHODOLOGY AND DATA

3.1. Methodology

Based on literature review from previous chapter, the following framework in Figure

3- describes the way of thinking used in the research and how key variables and boundaries in

the research relate to the others. The economic analysis of Snohvit expansion project will be

determined by project scope, fiscal system, project costs, LNG prices and potential gas

discoveries. The discoveries are related to gas reserve and its properties. Although northern

sea route (NSR) might impact to the project on reducing travel and shipping costs between

Norway and North-East Asia countries, it will not include in the economic model.

Figure 3-1 Research Framework of Snohvit Expansion Project

A discounted cash flow (DCF) method will be used to conduct economic analysis of

Snohvit expansion project. This method discounts the stream of asset net cash flows in the

forecast realization of the future at a constant rate. This constant discount rate is typically set

to an estimate of an average discount rate appropriate for valuing the assets of the corporation

as a whole. The discount rate also can represent the composition between external and

internal funding for the project (Berk, DeMarzo 2007). The DCF will be used to analyse and

assess the profitability of the project with various indicators. The estimate of asset or project

value is the sum over time of these discounted net cash flows, called NPV (net present value).

The other outputs of DCF calculation normally are internal rate of return (IRR) and pay out

time (POT) or payback period. IRR is the discount rate (interest) such that NPV equals zero,

and POT is an indicator of the rate at which cash flows are generated early in the project

18

(Newendorp, Schuyler 2000). These outputs are generated using a spread sheet model. In

practice, one-point estimated input of a DCF model is used to estimate the economic

indicators, hence it is called a deterministic method.

Sensitivity analysis will then be performed to test the robustness of the model as well as

investigating on how main variables influence the economic output. The analysis would help

answer one of research questions, i.e. how main variables of project economic, e.g. project

cost, recoverable gas, LNG price, behave in determining the economic output of Snohvit

expansion project. Subsequently, probabilistic method will be undertaken to reflect the risks

associated with the project. Probabilistic inputs of economic models for main variables are

generated using montecarlo simulation. Montecarlo simulation is a type of parametric

simulation in which specific parameters are required prior to do the simulation. This is more

appropriate when the historical data is entirely completed, similar to a project that never

creates equal to the others in terms of project parameters, e.g. scope, time, cost and risk

(Newendorp, Schuyler 2000).

Simulation helps describe risk and uncertainty of input variables in the form of

probability distribution. Triangular distribution is set for project costs since it reflects the

variation in typical project data (Mun 2010). In the triangular distribution, a straight line

relationship is assumed between the minimum value, up to the most likely value, and from

the most likely value down to the maximum value, as profiled in Figure 3-3. It is also used to

reflect asymmetric density of probable values. However, these three inputs are often confused

with the worst-case, moderate-case, and best-case scenarios. This assumption is indeed

incorrect, because the minimum and maximum cases will almost never occur, with a

probability of occurrence set at zero (Mun 2010). Subsequently, montecarlo with 1000 trials

will be performed to result in possible outcomes of project costs as well as the model outputs.

In other words, montecarlo will be used to take a closer look at the risk diversity in a project.

As a result, the probabilistic model can be analysed to complement the deterministic one.

A combination of deterministic and probabilistic analysis is employed in order to

identify factors within internal project’s boundaries required to make the project feasible,

given current conditions faced by the project. Firstly, some scenarios of LNG capacity of

Snohvit expansion project are set to capture variety possible reserve of discovered gas fields.

In addition, some scenarios of LNG FOB prices are set to reflect the LNG market in Asian

countries. These approaches are deterministic method by setting fixed decision variables.

19

Subsequently, probabilistic method is applied into main project costs, i.e. capital and

operation costs. This will create a decision table as guidance in controlling the project on an

economical track. As a result, a guide on how much of the LNG capacity and price should be

required, with a maximum allowable project costs to maintain positive NPV and or any other

investment indicators. Finally, it is required to identify and briefly assess key strategies based

on the results of the second research question. These strategies include development options

and scenario to capture the allowable capital cost, as well as LNG price determination with

regards to prospects of the LNG produced from Snohvit expansion project in the LNG

market. This will address the last research question, i.e. how development options or scenario

including prospects in the LNG market play roles to support the project feasibility. The

methodology is described in the Figure 3-2 below.

Figure 3-2 Research Methodology

3.2. Data and Assumptions

Some data and assumptions required to build the economic model of Snohvit expansion

project as follows:

1. Field and Project Scope

Hypothetical gas-fields will be used to build the economic model. The fields in the

Barents Sea have enough recoverable gas to build a 4.3 million ton per annum (MTPA)

LNG plant as current Snohvit capacity. These assumptions are taken in regards to Statoil

that has discovered hydrocarbon in Johan Castberg province. The gas reserve required for

expansion project is determined by LNG capacity that will be decided by the company. In

other words, the LNG capacity for the project can also be determined by the available gas

reserve in the Barents Sea. In addition, the gas fields are assumed to have similar

hydrocarbon properties or composition as Snohvit producing fields.

The expansion project will cover a complete LNG plant, which consists of

development drilling, subsea gathering line from producing fields to the LNG plant,

20

processing and liquefaction technology and all supporting system or facilities. Like

Snohvit project, the expansion project is assumed to last for 48 months from the time the

investment decision will be made by the company. The plant capacity would be one of

decision variables to make, because it is assumed that the expansion project can have

different capacity compared to the current plant. Total production of LNG is assumed not

to exceed 76.5% of gas reserve referring to the ratio of LNG sales agreement and gas

reserve on current Snohvit LNG operation. This ratio could also reflect the gas required

for LNG cargo and own use, e.g. fuel.

2. Project Cost

a. Development cost

Since the discovered fields have similar gas properties, the expansion LNG plant

would have similar processing and liquefaction technology with current Snohvit plant.

Consequently, the capital cost for building the expansion plant can refer to the Snohvit’s

capital expenditure. The Snohvit project with 4.3 MTPA LNG requires total investment

of US$ 5.6 billion, thus the unit cost is about US$ 1,300 per ton LNG per annum (TPA).

The project will cost 1,500 US$/TPA to incorporate inflation factor. Triangular

distribution is then employed into the unit cost input of such expansion project. The

minimum, most likely and maximum unit cost is 1,000 US$/TPA, 1,500 US$/TPA, and

2,500 US$/TPA respectively as shown in Figure 3-3. These triangular costs are used

since the project will locate in the harsh environment, therefore it belongs to high cost

projects that have had unit cost between 1,000 and 2,500 US$/TPA in recent years

(Songhurst 2014, Ritz 2014), as depicted in Figure 3-4. For example, current capital

expenditure (capex) of green field LNG developments in Australia (includes upstream

development and LNG plant) is between A$ 2,500 and 3,000/TPA or about 1,880 to

2,250 US$/TPA (White, Morgan 2012).

Figure 3-3 Triangular Distribution of Development Cost

21

Figure 3-4 LNG Unit Cost for High Cost Projects

(Modified from: Songhurst 2014)

Another assumption to make is the capital cost will be all incurred in the first five

years of field life, since the capital cost invested in the latter years of field life would have

less significant to the economic indicators rather than in the beginning years of field life.

Furthermore, capacity factor method is used to estimate the capital cost of similar facility

of a known (but usually different) capacity. It relies on the nonlinear relationship between

capacity and cost. In other words, the ratio of costs between the two similar facilities of

different capacities equals the ratio capacities multiplied by an exponent, usually between

0.6 and 0.7 (Amos 2010). In this economic model, 0.7 is used as an exponent factor for

capacity and cost relationship.

b. Operation cost

The operation expenditure (opex) of a LNG plant can generally be divided into

several categories, e.g. personnel, energy, maintenance and other costs including CO2

costs. The opex also depends on the type of liquefaction technology used in the plant, in

which there are two main technology in liquefaction, i.e. mixed refrigerant and expander

technology (Castillo, Dorao 2010). As Snohvit LNG uses refrigerant technology

combined with sea water cooling system (Pettersen et al. 2013), the opex of Snohvit LNG

can therefore be defined as following:

Opex = Makeup refrigerants + Energy costs + CO2 cost + Fixed Cost

Each of those components is used in the economic model. The mixed process of

refrigerants based on a plant of 1 MTPA of LNG can be 644 TPA of ethane with a cost

22

about 1,400 USD/ton and 154 TPA of propane with a cost about 620 USD/ton (Castillo,

Dorao 2010). Regarding to energy costs, Snohvit uses gas turbines as main electricity

generator for supplying power for the plant (Pettersen et al. 2013), so that it is not

required to get electricity suppliers from other parties. Meanwhile, the cost related to CO2

(carbon) production is taken into account as an operation cost. Carbon is produced in

several stages of LNG plant, but it is assumed that only carbon related to energy

consumption for using gas turbine considered that is about 0.7 KgCO2/kWh because CO2

from processing feed gas will be re-injected into the field. Having said that Norway is

highly aware of carbon emission, thus the company should consider the production of

carbon in their operations. Energy consumption for a mixed refrigerants process is 350

kWh/ton LNG, and the price under the European Union Emission Trading System (EU

ETS) for the emission used in the model is assumed 15 US$/ton carbon (Castillo, Dorao

2010). It is based on the historical spot prices of carbon emission allowance in the EU

ETS, where the price was about 30 €/ton carbon in 2008. But it has been around 10 €/ton

carbon since then (Siikamäki, Munnings & Ferris 2012). Moreover, fixed cost includes

personnel, maintenance and other costs that are not directly related to the volume of

production. The annual fixed cost is assumed 2% of total capex. As a result, total annual

opex of the project is slightly below of a rule of thumb for unescalated opex that is 3% of

capex per annum (White, Morgan 2012).

c. Exploration and decommissioning cost

Exploration activities including sunk costs are assumed to cost US$ 1 billion, while

decommissioning cost is 200 US$/TPA or about one seventh of the most likely

development cost. In accordance with petroleum taxation system in Norway, the company

can spread out the decommissioning cost yearly during production period to become

decommissioning schedule, thus it make less tax payment for the company. There is no

three point input for exploration and decommissioning cost. The reason is because

exploration cost incurred prior to investment decision being made, so that there will be no

more uncertainty for it. Meanwhile, decommissioning cost that will incur in the latter

years of field lifetime would intuitively have less impact on the project economic.

3. LNG Price

A long-term contract between producer and buyer is used as an assumption for this

project because LNG projects are very capital intensive in addition to extreme

23

environment of the Snohvit expansion project. The contract will include escalation factor

3% per year over production lifetime. The contracted price would also be free-on-board

(FOB) basis that means that LNG price set at the producer’s export terminal and the

shipping and insurance costs are the responsibility of the buyer. As the plant is projected

to supply LNG to Northeast Asian countries, e.g. Japan, South Korea, Taiwan and China,

the Japan natural gas price is used for reference in determining gas price input for the

economic model because international LNG trade in Asia has been based on the Japanese

Customs-Cleared Crude Oil (JCC) price mechanism (Rogers, Stern 2015). Having said

that the average natural gas prices in Japan with ex-ship basis or CIF (cost, insurance,

freight) contract has been around US$ 16 per million British thermal unit (MMBTU) in

the past three years (BP 2015), the model will use 14 US$/MMBTU as base price to

reflect the possible price at 2020 as baseline year, assumed the cost for a 31-day LNG

shipping to Japan is about 2 US$/MMBTU (Timera Energy 2015, Searates 2015).

The base price will be used in the price scenario combined with the scenario of plant

capacity to create project scenario and eventually to produce the decision tables. The gas

price and the plant capacity will be the two decision variables, and the decision tables will

consist of each combination of decision variable values. Furthermore, some assumptions are

included for inputs of the economic model of Snohvit expansion project attached in in

Appendix 1 as follows:

1. A 10% discount rate is used, and a 3% yearly inflation factor is applied to operation

expenditures, decommissioning schedule and cost, and carbon emission price. There is no

escalation factor on capital cost because the contract for engineering, procurement and

construction (EPC) works is assumed in lump sum basis at the beginning of the project.

2. There is no nitrogen oxide (NOx) tax imposed to the project because there is no

significant nitrogen contaminant in the gas properties, and there is no area tax paid for the

expansion project since it would utilise the existing plant area.

24

CHAPTER IV: RESULT AND ANALYSIS

4.1. Economic Indicators

Investors and companies heavily refer to economic indicators to make decisions on the

investment of a project. Following the methodology as described in the previous chapter, it is

found that Snohvit expansion project results in economic indicators as presented in Table 4-1.

This simply indicates that project is financially feasible for the company due to the positive

NPV (net present value) and the IRR (internal rate of return) above 10% of project discount

rate. NPV presents that the project is able to generate additional value of 5.1 billion US$ after

taking into account all necessary costs and real term (time value of money). In addition, the

project has approximately 7 years of payback period from the beginning of investment and

0.96 of post-tax NPV and NPV capex ratio. The ratio describes that the project could

generate value 96% of capital expenditure (capex) in real terms.

Table 4-1 Deterministic Output of Economics Model

These indicators are the deterministic output since it is obtained from single model

input as shown in Appendix 1. It is then calculated to reach post-tax net cash flow using a

spread sheet attached in Appendix 2. Moreover, the output is from company’s point of view

to reflect the decision that will be made by the company to do the project. In other words, if

the project is seen as an unprofitable one, the company will not make any investment.

Nevertheless, it shall be noted that the model uses input data and assumptions that may differ

from the actual data. Further analysis therefore needs to be performed to look at the project

economics more comprehensively in order to capture the uncertainties that project may face

during executing the project.

4.2. Sensitivity Analysis

After finding that the project is financially feasible, it is important to identify which of

the used variables are more important and how much they can influence the economic output.

Sensitivity analysis is therefore undertaken to investigate on how main variables influence the

25

economic output as well as testing the robustness of the model. It is conducted by giving 20%

range values for each main variable, e.g. gas price, plant capacity, tax rate, and costs. The

20% range is assumed only to capture the influence of variable changes to the output. The

sensitivity charts of post-tax NPV and IRR are shown figures below.

Figure 4-1 Sensitivity Chart of NPV

From sensitivity chart in Figure 4-1, if gas price decreases by 20%, project’s NPV will

decrease from US$ 5.1 billion to US$ 3.3 billion. On the other hand, if gas price increases by

20%, project’s NPV will increase from US$ 5.1 billion to US$ 6.9 billion. Similar response is

shown by changes in plant capacity, if gas price decreases by 20%, project’s NPV will

26

decrease to US$ 3.8 billion and if gas price increases by 20%, project’s NPV will increase to

US$ 6.6 billion. Consequently, gas price and plant capacity are the two most influential

variables that determine the project’s NPV. Furthermore, if capital uplift 7.5% for 4 years

according to offshore taxation system is not applied in the model, gas price and rent tax rate

become the two most influential variables which determine the project’s NPV as shown in

Figure 4-2. The base case NPV falls from US$ 5.1 billion to US$ 4.6 billion indicating that

the company would face early fiscal burden because the system allows the company to

receive 7.5% uplift allowance. In overall, gas price, plant capacity, rent tax rate, development

cost, corporate tax rate, and exploration cost are the significant variables to the NPV.

Figure 4-2 Sensitivity Chart of NPV without Uplift

27

Figure 4-3 Sensitivity Chart of IRR

From sensitivity chart of IRR in Figure 4-3, it indicates that if gas price decreases by

20%, project’s IRR will fall from 18.8% to 16.2%. On the other hand, if gas price rises by

20%, project’s IRR will also rise from 18.8% to 21.1%. Meanwhile, if development cost

decreases by 20%, project’s IRR will increase from 18.8% to 20.8% and if gas price rises by

20%, project’s IRR will fall from 18.8% to 17.1%. For IRR’s sensitivity, the two most

influential variables are gas price and development cost. Nevertheless, if capital uplift 7.5%

28

for 4 years is not applied in the model, unlike in the project’s NPV, capital uplift would not

significantly change the sensitivity chart in which gas price and development cost are still the

two most influential variables which determine the project’s IRR as shown in Figure 4-4.

However, the base case IRR falls from 18.8% to 17.7% indicating that the company would

face early fiscal burden because the system allows the company to receive 7.5% uplift

allowance. In addition, rent tax rate, plant capacity, corporate tax rate and exploration cost

considerably impact on the sensitivity of project’s IRR.

Figure 4-4 Sensitivity Chart of IRR without Uplift

29

These results are reasonable because those variables are key parameters in determining

the project economics. From internal project’s boundaries, gas price, development cost and

plant capacity which is associated with recoverable gas volume are the most three influential

variables. Rent tax and corporate tax rate are also significant variables, but they are outside

project boundaries meaning that the company cannot fully authorise to realise them. There

are some other important variables that could influence the economics, such as capex

spending distribution and construction duration. Intuitively, the more capex spending in the

latter years, the higher the economic output will be. And the shorter construction period or

the quicker production start, the higher the output will be. The company may also exercise

any possible actions to improve the economics.

4.3. Probabilistic Output

Following the deterministic model above, probabilistic model needs to be built to

consider some probable values of variables input. The probabilistic model has probabilistic

inputs, i.e. development cost (capex) that is generated using montecarlo simulation as

explained in the previous chapter. In fact, the actual development cost in the end of the

project’s period is unlikely the same as the cost stated in the beginning of the project. Some

other factors can lead to the deviation of the actual cost from its initial budget or assumption,

such as scope modifications and global market changes. As a result, the simulation has

generated the profile of the project’s NPV and IRR as depicted in Figure 4-5 and Figure 4-6.

The mean of project’s NPV and IRR is US$ 4.8 billion and 18% respectively. The simulation

results in no negative NPV and no IRR less than discount rate 10%.

30

Figure 4-5 Simulation Result of Project’s NPV

Figure 4-6 Simulation Result of Project’s IRR

The project is therefore profitable for company based on this probabilistic approach,

even though the simulated mean of project’s NPV and IRR is lower than the indicators

resulted from the deterministic model in Table 4-1. This is because the most likely input of

31

triangular distribution in the model fell more in the minimum side rather than in the

maximum side as shown in previous chapter, while the simulation generated probable values

of capex from minimum to maximum input to eventually obtain the mean of project’s NPV

and IRR. In addition, these results represent the project economic profile in facing the

probable values of capex (development cost). Moreover, the company may also use other

indicators to make its final investment decision.

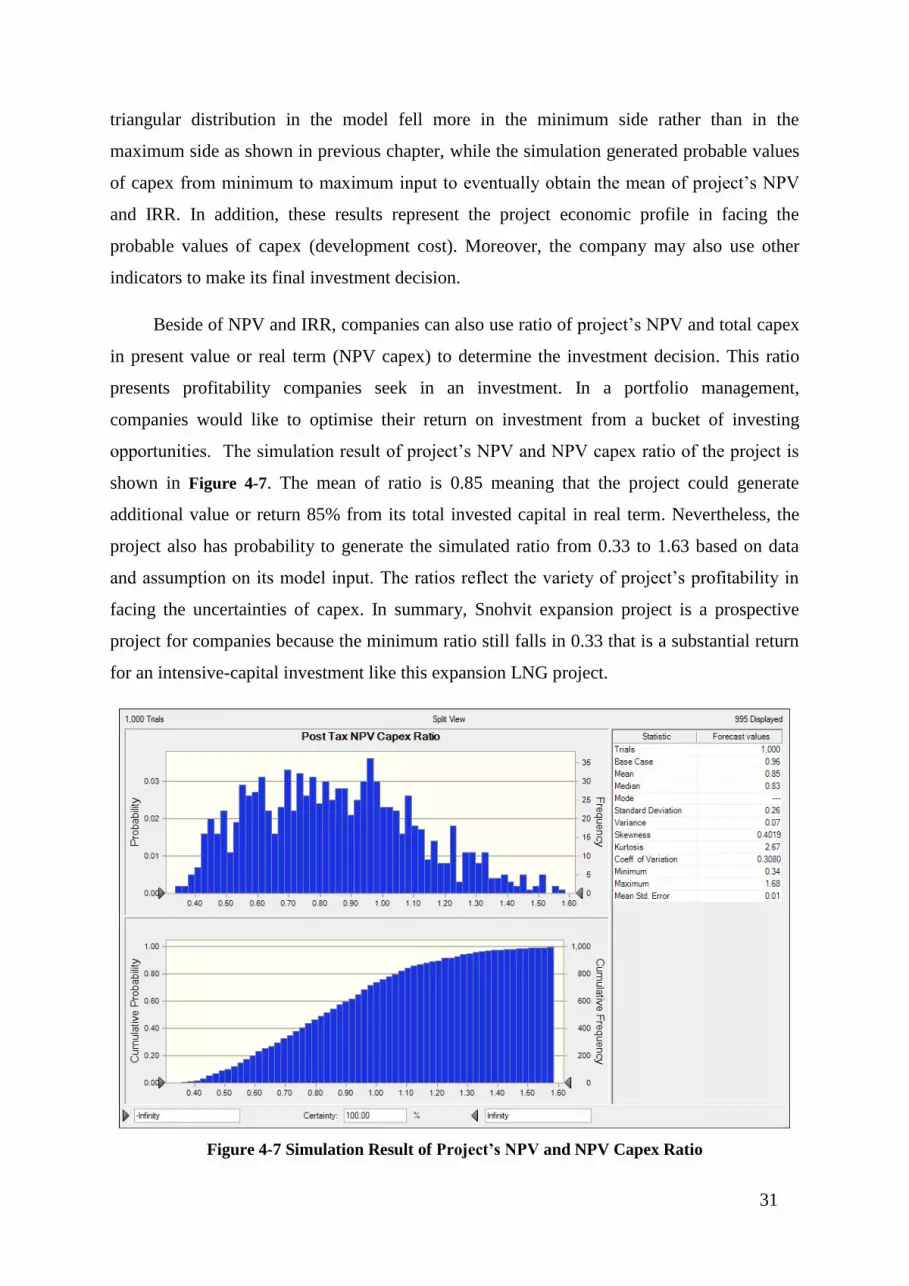

Beside of NPV and IRR, companies can also use ratio of project’s NPV and total capex

in present value or real term (NPV capex) to determine the investment decision. This ratio

presents profitability companies seek in an investment. In a portfolio management,

companies would like to optimise their return on investment from a bucket of investing

opportunities. The simulation result of project’s NPV and NPV capex ratio of the project is

shown in Figure 4-7. The mean of ratio is 0.85 meaning that the project could generate

additional value or return 85% from its total invested capital in real term. Nevertheless, the

project also has probability to generate the simulated ratio from 0.33 to 1.63 based on data

and assumption on its model input. The ratios reflect the variety of project’s profitability in

facing the uncertainties of capex. In summary, Snohvit expansion project is a prospective

project for companies because the minimum ratio still falls in 0.33 that is a substantial return

for an intensive-capital investment like this expansion LNG project.

Figure 4-7 Simulation Result of Project’s NPV and NPV Capex Ratio

32

4.4. Scenario Analysis

In the real world, some values of the project economic variables are uncertain. The

economics of project should be ideally modelled for a wide variety of scenario decisions.

Snohvit expansion project in particular that requires very intensive capital needs to be

assessed using scenario and probabilistic method, so that the project feasibility can be

comprehensively analysed. According to sensitivity analysis, gas prices and recoverable gas

reserve or plant capacity are the most influential variables that lead to the economic output.

Plant capacity and gas price are also the two variables which have to be firstly defined before

taking an investment decision. Therefore, plant capacity and gas price are selected to define

project scenarios. The scenario of plant capacity is determined based on an assumption that

the company can build the plant with capacity less than the current capacity of 4.3 million ton

per annum (MTPA). In this case, there are four scenarios of plant capacity, i.e. 1.3, 2.3, 3.3,

and 4.3 MTPA.

For gas price, there are four scenarios, i.e. US$ 10, 12, 14 and 16 per million British

thermal unit (MMBTU). They are defined referring to the average natural gas prices in Japan

that have been about US$ 16 per million BTU in the last three years for CIF (cost, insurance,

freight) contract, while the European hub prices have been around 10 and 11 US$/MMBTU

since 2011 (BP 2015). In addition, LNG from US forecasted to supply Asian LNG importers

in the post 2015 periods may shift LNG pricing mechanism in Asia, and bring the LNG

prices down (Rogers, Stern 2015). Thus, the gas prices in Asia and Europe as main target

market of the project may fall in the range of 10 to 16 US$/MMBTU for FOB (free-on-board)

contract in the upcoming years. Meanwhile, the baseline of the model uses a scenario with

gas reserve 175 billion cubic meter (BCM), LNG capacity 4.3 MTPA and baseline gas price

14 US$/MMBTU with a 3% escalation per year starting from the year of first cargo shipment

as explained in previous chapter.

The project will have a total of 16 scenarios that combine scenarios of plant capacity

and gas price as shown in Table 4-2. For example, the upside reserve in scenario 4 will have a

recoverable reserve with a volume of 175 billion cubic meter (BCM), thus it will have a 4.3

MTPA plant. The downside reserve in scenario 1 will only have a recoverable reserve of 53

BCM, thus it will have a 1.3 MTPA plant. Then, these scenarios are used to develop a

decision table in which companies can refer to in deciding the investment. The decision table

compiles the results in a table of forecast cells indexed by the decision variables. It is

obtained from a simulation of input variables for each combination of decision variable

33

values. The model for producing decision tables has plant capacity and gas price as decision

variables, and development cost as input variables. Subsequently, the simulation will generate

the model outputs for each scenario, e.g. the mean of project’s NPV, project’s IRR, project’s

NPV and NPV capex ratio. As a result, a decision table for project’s NPV is resulted in Table

4-3, while a decision table for project’s NPV and NPV capex ratio is shown in Table 4-4. This

will eventually identify the required factors within internal project’s boundaries that make the

project financially feasible.

Table 4-2 Project Scenario

Table 4-3 Decision Table for Project’s NPV

Based on Table 4-3 above, it provides the variability in the mean of project’s NPV

according to project scenario. Scenario with capacity 4.3 MTPA and gas price 16

US$/MMBTU clearly results in the highest NPV value, whereas scenario with capacity 1.3

MTPA and gas price 10 US$/MMBTU provides the lowest NPV value. It presents that a 1.3

34

MTPA plant and gas prices up to 12 US$/MMBTU will likely result in negative NPV.

Meanwhile, Table 4-4 describes the variability in the mean of project’s NPV and NPV capex

ratio based on project scenario. Like result in Table 4-3, scenario with capacity 4.3 MTPA

and gas price 16 US$/MMBTU results in the highest ratio value, whereas scenario with

capacity 1.3 MTPA and gas price 10 US$/MMBTU provides the lowest ratio value.

Table 4-4 Decision Table for NPV Project and Capex Ratio

Using the decision tables, companies can decide their investment depending on the real

scenario that would happen, and they have also taken into account project risk analysis in a

form of simulating the probable values of development cost. Companies may use a cut-off

point of NPV project and capex ratio in assessing the project economics, such as using 0.3 as

an investment limit. This implies that only projects which have ratio 0.3 will qualify and go

further for other investment assessments. For instance, if the reserve is big enough to build a

2.3 MTPA plant but the company is failed to secure the gas price at 14 US$/MMBTU in the

baseline year with a 3% escalation per year, then there will be no investment decision for the

project. Consequently, the less reserve discovered, the less capacity can be built, and the

higher the gas price.

Furthermore, the combination of project scenario and montecarlo simulation can result

in the probable values of development cost or capex. Table 4-5 presents the mean of

development cost as a result of montecarlo simulation for each of project scenarios. The

development cost only relies on plant capacity, so that the cost will generate the same

development cost for any gas price scenario. This output can then be used as guidance in

controlling the actual development cost during project execution. As a result, the

development cost for each plant capacity scenario will confine the limit of actual cost to

guide the project on an economical track according to indicators as shown in the decision

tables. For example, if LNG plant is decided with capacity 1.3 MTPA and baseline gas price

35

is set at 14 US$/MMBTU, then the maximum development cost should be US$ 3.1 billion in

order to achieve project’s NPV of US$ 210 million as shown in Table 4-3. In other words, if

the cost significantly exceeds US$ 3.1 billion, it will decrease the project’s NPV and it may

lead to negative NPV implying the project becomes unprofitable for the company.

Table 4-5 Project Scenario and Development Cost (Mean Capex)

4.5. Discussion

Snohvit expansion project is a feasible project based on project economic indicators