Embed Size (px)

Citation preview

Did Policy Experimentation in ChinaAlways Seek Efficiency? A case studyof Wenzhou financial reform in 2012

JINGHAN ZENG*

Policy experimentation has been widely considered a ‘magic bullet’ of policy improvement

and key to economic prosperity in China. This article, however, argues that policy

experimentation in China does not always seek policy efficiency. Rather, it can be

manipulated as a political symbol without actually affecting practices. By taking a case study

on Wenzhou’s financial reform, this article illustrates that local policy experimentation can

serve as a mechanism for the central government to legitimately delay reform practices—in

the case of Wenzhou’s financial reform in 2012, out of a desire to maintain socio-economic

stability during the power succession at the 18th Party Congress. In this reform, socio-

economic stability was deemed more important than developing a sustainable and effective

long-term policy. This article provides a new perspective on understanding policy

experimentation in China by proposing the idea of ‘symbolic reforms’.

Introduction

Thirty years of spectacular economic growth in China suggests that the ChineseCommunist Party (CCP) somehow got its market reforms right. China’s economicprosperity has prompted a plethora of political science and economics literaturelinking the policy experimentation with the economic miracle.1 The existing studies

* Jinghan Zeng is a Lecturer in the Department of Politics and Public Policy at the De Montfort University. Hisresearch focuses on legitimacy, ideology and elite politics of contemporary China and social science researchmethods. His academic papers have appeared in Contemporary Politics, Journal of Chinese Political Science andComparative Economic & Social Systems. For more information, please visit his homepage https://sites.google.com/site/zengjinghan/home. The author would like to thank Shaun Breslin (University of Warwick), Xiao Yuefan(University of Warwick) and the anonymous reviewer of JCC for their valuable comments on the earlier version ofthis article. Special thanks go to Zhou Chunxi (Zhejiang Gongshang University) for his generous sharing of therelevant data. This article was presented at the 9th Annual Graduate Seminar on China held in the Chinese Universityof Hong Kong. The comments from the conference, in particular those from Yan Xiaojun (Hong Kong University),are also highly appreciated. All mistakes are the responsibility of the author. The author can be reached by email [email protected].

1. Yingyi Qian and BarryWeingast, ‘China’s transition tomarkets: market-preserving federalism, Chinese style’,Journal of Policy Reform 2, (1995), pp. 149–185; SharunMukand and Dani Rodrik, ‘In search of the holy grail: policyconvergence, experimentation, and economic performance’, American Economic Review 95(1), (2005), pp. 374–383;Thomas Rawski, ‘Implication of China’s reform experience’, The China Quarterly 144, (1995), pp. 1150–1173;Gerard Roland, Transition and Economics: Politics, Markets, and Firms (Cambridge, MA: MIT Press, 2000).

Journal of Contemporary China, 2014

http://dx.doi.org/10.1080/10670564.2014.932517

q 2014 Taylor & Francis

Dow

nloa

ded

by [

Uni

vers

ity o

f W

arw

ick]

at 1

3:19

04

Oct

ober

201

4

consider policy experimentation as a ‘magic bullet’ of policy improvement and key toeconomic prosperity in China. Though the link seems natural, the existing studieshave underemphasized political dynamics of policy experimentation in China, whichthis article will highlight.This article argues that policy experimentations in China do not always seek

effectiveness and efficiency; nudging policy experiments can allow thegovernment to fake activity regarding problems which can no longer simply beignored. Policy experiments may thus serve only to pay lip service to other partiesinvolved without really tackling the core problems or launching meaningfulreforms.This article proposes the idea of ‘symbolic reform’ to explain why reforms can be

manipulated as a political symbol to maintain the status quo. By taking a case study ofWenzhou’s financial reform, this article illustrates that local policy experimentationcan serve as a mechanism for the central government legitimately to delay reformpractices—in this case, out of the desire to maintain socio-economic stability duringthe power succession at the 18th Party Congress.In Wenzhou’s reform, socio-economic stability was deemed more important

than developing a sustainable and effective long-term policy. This stability-oriented reform succeeded in solving the debt crisis and restoring marketconfidence in the short term. Although it might be argued that maintainingstability was an improvement on the rather chaotic environment that preceded it,this reform did not tackle the core structural problems or significantly increase theefficiency of the financial system as both the local and central governmentpromised.The Wenzhou case was chosen because it has been a pioneer of local policy

experimentation in China for decades, to the extent that it has been referred to ashaving developed a specific ‘Wenzhou model’.2 Financial reform has long beenfar behind other market reforms in China and Wenzhou has a long history of beinga pilot area in which to practice financial reforms.3 The financial reform of 2012in Wenzhou represents a typical case of policy experimentation, but it is alsounique because this reform is closely related to Wenzhou’s debt crisis in 2012 thatclashed with the once-in-a-decade leadership transition. It thus provides a greatopportunity to examine how the central state balances its understanding thatfundamental financial reform is necessary to promote long-term economic stabilityon the one hand, with the need to guarantee short-term socio-political stability onthe other.Notably, the purpose of this article is not to dispute the relationship between

policy experimentation and China’s economic growth, but to explore its impact onregime survival that has been underemphasized by the existing literature.This article provides a new perspective on understanding policy experimentationin China.

2. Ya-Ling Liu, ‘The private economy and local politics in Wenzhou’, The China Quarterly 130, (1992),pp. 293–316. For a detailed analysis of Wenzhou economy, please see Kristen Parris, ‘Local initiative and nationalreform: the Wenzhou model of development’, The China Quarterly 134, (1993), pp. 242–263.

3. For example, in 1987, Wenzhou first launched a floating interest reform. In 2002, Wenzhou was set as acomprehensive financial reform pilot area.

JINGHAN ZENG

2

Dow

nloa

ded

by [

Uni

vers

ity o

f W

arw

ick]

at 1

3:19

04

Oct

ober

201

4

Policy experimentation in China

Institutions of the communist states, as proved by their history, have been widelyregarded as extremely inflexible and rigid.4 China, however, seems to be anexception. Market reforms launched by the CCP leadership have fostered remarkableeconomic growth over the past three decades. The regime has showed greatadaptability in overcoming the complex challenges of large-scale economictransformation while avoiding systematic breakdown. China’s economic prosperityand the poor practices of many developing countries on ‘Washington Consensus’style reforms present constant challenges to the marketization-cum-privatizationparadigm. How to explain the success of Chinese economy and market reforms?Many link it to the decentralized experimentation of policymaking in China, which

has been considered key to encouraging policy innovation and economic growth inChina.5 For example, Heilmann argues that the core of China’s adaptability is ‘theunusual combination of extensive policy experimentation with long-term policyprioritization’.6 This experimentation ‘minimized the risks and the cost to centralpolicymakers by placing the burden on local governments and providing welcomescapegoats in cases of failure’.7 Wang Shaoguang argues that there are learningmodes to explore suitable welfare systems for China.8 The resilience of the Chinesesystem lies in its ‘deep-seated one-size-does-not-fit-all pragmatism’ and theadaptability of decision makers is key to the ‘China model’.9 In this sense, policyexperimentation is at the core of China’s developmental experience.Others, on the contrary, argue that decentralized experimentation is not the primary

cause of the economicmiracle and reform success in China; rather, they consider localpolicy experimentation as a product driven by political factions.10 It is argued that thecentral leaders tend to broaden their bases of political support by provingthe effectiveness of their preferred policies in local states. Cai and Treisman arguethat the pro-reform factions,DengXiaoping and his allies in particular, frequently usedeffective local experiments as opportunities to promote their supporters and replaceanti-reform or conservative officials.11 For example, Deng Xiaoping replaced theconservative local leaders of Fujian with more enthusiastic reform supporters becauseof the slow reformprogress of theXiamen Special Economic Zones in the late 1980s.12

4. Valeria Bunce, Subversive Institutions: The Design and the Destruction of Socialism and the State(New York: Cambridge University Press, 1999).

5. Qian andWeingast, ‘China’s transition to markets’; Mukand and Rodrik, ‘In search of the holy grail’; Rawski,‘Implication of China’s reform experience’; Roland, Transition and Economics.

6. Sebastian Heilmann, ‘Maximum tinkering under uncertainty, unorthodox lessons from China’,Modern China35(4), (2009), pp. 450–462.

7. Sebastian Heilmann, ‘Policy experimentation in China’s economic rise’, Studies in Comparative InternationalDevelopment 43, (2008), pp. 1–26.

8. Shaoguang Wang, ‘学习机制,适应能力与中国模式’ [‘Learning mechanism, adaptability, and Chinesemodel’], 开放时代 [Open Times ] no. 7, (2009).

9. ShaoguangWang, ‘Adapting by learning, the evolution of China’s rural health care financing’,Modern China35(3), (2009), pp. 370–404.

10. Hongbin Cai and Daniel Treisman, ‘Did government decentralization cause China’s economic miracle?’,World Politics 58, (2006), pp. 505–535; Wing Thye Woo, ‘The real reasons for China’s growth’, The China Journal41, (1999), pp. 115–137.

11. Cai and Treisman, ‘Did government decentralization cause China’s economic miracle?’.12. Ibid.

POLICY EXPERIMENTATION IN CHINA

3

Dow

nloa

ded

by [

Uni

vers

ity o

f W

arw

ick]

at 1

3:19

04

Oct

ober

201

4

Above all, both views suggest that local policy experimentations in China arelaunched to explore more efficient policies, either in order to promote economicgrowth or as part of political struggles. As this article will demonstrate, policyexperimentations in China are not always seeking a better policy.There are many kinds of policy experimentation in China and the case study of

this article emphasizes those launched by the central government and practiced inlocal regions. In this kind of policy experimentation, the central state would usuallylaunch reform programs first. The local states then voluntarily practice thoseexperimental programs with some of the successful local experiences later adjustedinto national policy and rolled out countrywide.13 During the process ofexperimentation, the central state usually expresses support for certain localinitiatives or programs, but keeps some distance from local pilots. This distanceencourages the self-innovation of local governments with less intervention from thetop. It also washes the central government’s hands entirely of responsibility forpotential reform failure. The power structure of the regime reduces the costs andrisks of the central state.14 If there is any popular protest caused by reforms, localgovernments might be blamed for ‘mismanagement’ or ‘misleading’, and the centralgovernment will play a moral role of savior. The central government thus retains afavorable position in that it can contain and quell local protests without affecting itsown appearance of legitimacy.15

This model of policy experimentation in China has successfully transformed agreat number of local projects into national policies.16 The agricultural reform, forexample, started the entire reform process in 1978 and later emerged as a nationalpolicy after experimentation in different provinces. The acceptance of privateownership as a legitimate form in China in the 1980s also followed successful localexperimentation in Wenzhou where the case study of this article is based. Policyexperimentation is the process of turning local input into national policy and Chinesestyle local–central interaction. Many noted the local–central interaction as theChinese style of federalism.17 Some argue that it is a model of decentralization.18

13. For a detailed analysis ofChina’s policy experimentation, seeHeilmann, ‘Maximum tinkering under uncertainty’;Heilmann, ‘Policy experimentation in China’s economic rise’; Sebastian Heilmann, ‘From local experiments to nationalpolicy: the origins ofChina’s distinctive policy process’,TheChina Journal 59, (2008), pp. 1–30; Parris, ‘Local initiativeand national reform’. For analysis of decentralization, see Cai and Treisman, ‘Did government decentralization causeChina’s economic miracle?’; Gabriella Montinola, Yingyi Qian and Barry Weingast, ‘Federalism, Chinese style: thepolitical basis for economic success’,World Politics 48(1), (1996), pp. 50–81.

14. Yongshun Cai, ‘Power structure and regime resilience: contentious politics in China’, British Journal ofPolitical Science 38, (2008), pp. 411–432.

15. It protects the central government’s legitimacy to some extent and contributes to the interesting phenomenathat high legitimacy at the central level contrasts with low legitimacy at the local level. Zhengxu Wang, ‘Politicaltrust in China: forms and causes’, in Lynn White, ed., Legitimacy: Ambiguities of Political Success or Failure inEast and Southeast Asia (Singapore: World Scientific Pub. Co. Inc., 2005); Tony Saich, ‘Development and choice’,in Edward Friedman and Bruce Gilley, eds, Asia’s Giants Comparing China and India (New York: PalgraveMacMillan, 2005).

16. Heilmann, ‘Policy experimentation in China’s economic rise’.17. Montinola et al., ‘Federalism, Chinese style’; Qian and Weingast, ‘China’s transition to markets’; Yongnian

Zheng, De Facto Federalism in China: Reforms and Dynamics of Central–Local Relations (Singapore: WorldScientifics, 2007).

18. Chenggang Xu and Juzhong Zhuang, ‘Why China grew: the role of decentralization’, in Peter Boone,Stanislaw Gomulka and Richard Layard, eds, Emerging from Communism: Lessons from Russia, China, and EasternEurope (Cambridge, MA: MIT Press, 1998).

JINGHAN ZENG

4

Dow

nloa

ded

by [

Uni

vers

ity o

f W

arw

ick]

at 1

3:19

04

Oct

ober

201

4

Others argue that neither of the above terms can grasp the essence of China’s local–central interaction. Heilmann defined it as ‘experimentation under hierarchy’ becausethere are no vertical checks and balances in China’s authoritarian system and thecentral government has the unchallengeable authority.19

Theoretical explanation

Symbolic reform

To date, there is no in-depth analysis of symbols on the experiences of policyexperimentation in China, although political symbols of reform have beenextensively studied in the area of public administration.20 Symbols are defined hereas a set of positive normative concepts, which might be embedded into plans toconstruct positive reform languages. Going one step further, this article proposesthe idea of ‘symbolic reforms’ (象征性改革). Symbolic reform refers to thosereforms which merely comprise political symbols without correspondingsubstantive changes. There are many popular sayings expressing similar meanings,such as ‘a change in form but not in content’ (换汤不换药), ‘an old wine in a newbottle’ and ‘loud thunder without rain’ (雷声大,雨点小), among others. Whenthe political actors are either incapable of or unwilling to launch meaningfulreforms but they still make significant reform promises to address pressure forreforms, those reforms are likely to be symbolic. The case of Wenzhou financialreform demonstrates that policy efficiency is not always the primary goal of policyexperimentation; rather, it can be used as a symbol of changes that ironically act tomaintain the status quo instead.Political symbols of reform are particularly important in China where political

marketing is a strength of the CCP. Chinese leaders are keen to portray themselves asbeing more positive and forward looking than their predecessors so as to win popularsupport, despite the fact that they do not necessarily need popular votes. For example,when President Hu Jintao and Premier Wen Jiabao took power, the Chinesegovernment used official propaganda in many ways to portray the new leadership asreformists. In the first few years, it was widely called the ‘new politics of Hu andWen’ (胡温新政). However, Hu’s leadership has achieved very little progress inpolitical system reforms in the past decade and his era is considered by many as a‘lost decade’.21 A similar strategy was subsequently applied to promote the reformcredentials of the new leadership of Xi Jinping and Li Keqiang. After the 18th PartyCongress, official propaganda invested in building an image that suggested that the

19. Heilmann, ‘Policy experimentation in China’s economic rise’.20. Several works mentioned symbols and image-building of local policy experimentation; however, they did not

give an in-depth analysis of this issue. For example, Yongshun Cai, ‘Irresponsible state: local cadres and image-building in China’, Journal of Communist Studies and Transition Politics 20(4), (2004), pp. 20–41. For articles ofpublic administration about political symbols, please see Tom Christensen and Per Laegreid, ‘Administrative reformpolicy: the challenges of turning symbols into practice’, Public Organization Review 3, (2003), pp. 3–27; TomChristensen and Per Laegreid, New Public Management: The Transformation of Ideas and Practice (Aldershot, UK:Ashgate, 2001).

21. Cheng Li and Eve Cary, ‘The last year of Hu’s leadership: Hu’s to blame?’, China Brief 11(23), (2011);Joseph Fewsmith, ‘Xi Jinping’s fast start’, China Leadership Monitor 41, (2013), p. 6.

POLICY EXPERIMENTATION IN CHINA

5

Dow

nloa

ded

by [

Uni

vers

ity o

f W

arw

ick]

at 1

3:19

04

Oct

ober

201

4

new leadership was determined to combat corruption and promote reforms.Xi Jinping’s visit to Guangdong Province has been deliberately publicized in the styleof Deng Xiaoping’s South Visit which launched a new era of reform in China.To what extent this image reflects the reality still needs further observation and willtake some years to become clear.22

Political symbols have been used not only in political system reforms but alsoin Chinese administrative reforms. The importation of the Super-DepartmentReform is a fitting example. The Chinese government launched a superficialSuper-Department Reform to serve domestic purposes by symbolically learningfrom the West.23 Some argue that the Chinese government has been manipulatingthe Super-Department model as a symbol of Western reform ideas with weakimplementation.24

Manipulating broad symbols of reform policies by political actors can produceseveral benefits.25 First, in the short term, symbolic reforms tend to be less costlywhen facing a complicated problem with ambiguous solutions. Second, politicalleadership can gain legitimacy by using reform symbols. Third, the symbols given intalks and plans can have the same effect as practice or reality in shaping people’sreform perceptions, at least at first.Political actors might choose to label their reform in certain positive ways in

order to attract broader public support.26 To embed a set of positive normativeconcepts into a reform plan as reform symbols is a clear way to construct positivereform languages. To a certain extent, reform symbols can substitute for actualpractices.27 In the case of Wenzhou, the central state designed an ambitiousfinancial reform plan to express its determination to implement a complete anddeep reform. As I will explain later, it successfully helped to gain marketconfidence and maintain socio-economic stability without doing a great deal.In this way, a financial reform idea has substituted the actual practices in solvingdebt crisis.

Theoretical framework

The following section reviews theoretical explanations to introduce a context for thecase study. The gap between reform ideas and implementation is widely observed asa ‘loose coupling’.28 It is usually associated with politics in liberal democracies but

22. However, in his interview with Duowei news, Deng Yuwen, who is the deputy editor of the Central PartySchool’s Study Times journal and an influential commentary writer, argues that the content of Xi Jinping’s ‘ChineseDream’ is old but the bottle is new, thus it is ‘an old wine in a new bottle’. Please see http://china.dwnews.com/news/2013-06-28/59248571.html (accessed 14 July 2013).

23. Lisheng Dong, Tom Christensen and Martin Painter, ‘A case study of China’s administrative reform: theimportation of the super-department’, The American Review of Public Administration 40(2), (2010), pp. 170–188.

24. Ibid.25. Christensen and Laegreid, ‘Administrative reform policy’.26. Martha Feldman and James March, ‘Information in organizations as signal and symbol’, Administrative

Science Quarterly 26, (1981), pp. 177–179; John Meyer and Brian Rowan, ‘Institutionalized organizations: formalstructure as myth and ceremony’, American Journal of Sociology 83(2), (1977), pp. 340–363.

27. Nils Brunsson, The Organization of Hypocrisy. Talk, Decisions and Actions in Organizations (Chichester:Wiley, 1989).

28. Christensen and Laegreid, New Public Management.

JINGHAN ZENG

6

Dow

nloa

ded

by [

Uni

vers

ity o

f W

arw

ick]

at 1

3:19

04

Oct

ober

201

4

can also be applied to the authoritarian regimes. Indeed, it is one of the majorgovernance problems shared by both the US and China.29 Pressure from theenvironment is one of the most important factors leading to this ‘loose coupling’,which ‘defines how much leeway political leaders have in making choices aboutreforms’.30 For example, reforms might be initiated or heavily influenced by pressurefrom the environment, such as an economic crisis, in order to maintain the legitimacyof leadership and increase the efficiency of public sectors.Elite reform activity is another important factor which can lead to this ‘loose

coupling’ because reform credentials are closely linked with the legitimacy ofleadership. When political actors are incapable of or unwilling to implement a realreform, political actors might cover it up by promoting ideas of reform to gain publicsupport and ‘to have a broader political effect, hoping that people will care more aboutthe promises of reform than about finding out what really happens to reform inpractice’.31 In this situation, reform outcomes can be far from reform ideas.An understanding that reform combines two central dimensions is used as the

analytical framework in this case study. One dimension is the pressure from theenvironment: strong or weak environmental pressures for reforms (both domestic andinternational). The other is the reform activities of political actors: whether politicalleaders are capable of and active in promoting a systematic reform or are moreconcerned with simply establishing reform credentials when under pressure. Fourpossible combinations are listed in Table 1.Model 1 indicates that the leadership might actively promote a systematic

reform and effectively implement reform ideas. In this case, it is likely that a realreform will be launched. Model 2 suggests that the reform ideas are likely to bemanipulated as hollow symbols to face external pressures for reforms. In thissituation, a symbolic reform would be launched to maintain legitimacy and establish

Table 1. Two dimensions of reform variablesa

Active reform activity: leaders whoare capable of and activein initiating and promoting reforms

Low elite reform activity: leaderswho simply intend to buildreform credentials

Strong external pressure Model 1 Model 2 (highly likely tobe symbolic reforms)

Weak external pressure Model 3 Model 4

Notes: a This table is developed from Lisheng Dong, Tom Christensen and Martin Painter, ‘A case studyof China’s administrative reform: the importation of the super-department’, The AmericanReview of Public Administration 40(2), (2010), pp. 170–188.

29. Yongfei Zhao and B. Guy Peters, ‘The state of the state: comparing governance in China and the UnitedStates’, Public Administration Review 69, (2009), pp. S122–S128.

30. Tom Christensen and Per Laegreid, Transcending New Public Management (Aldershot: Ashgate PublishingLtd, 2007).

31. Christensen and Laegreid, ‘Administrative reform policy’; Tom Christensen and Per Laegreid,‘Administrative reform policy: the challenges of turning symbols into practice’, in The Sixth National PublicManagement Research Conference, School of Public and Environmental Affairs, Indiana University, Bloomington(2001).

POLICY EXPERIMENTATION IN CHINA

7

Dow

nloa

ded

by [

Uni

vers

ity o

f W

arw

ick]

at 1

3:19

04

Oct

ober

201

4

the reform credentials of political leaders, rather than tackle the core problems or seekmeaningful changes. Thus, the reform is likely to remain superficial ‘window-dressing’. In some cases, a political leader might be interested in implementing acomplete reform but is unable to do so in the face of severe resistance from vestedinterests; nonetheless, the leader may still choose to make significant reformpromises in response to reform pressure. It is also a kind of symbolic reform, whichmerely comprises reform promises as political symbols without correspondingsubstantive meaningful changes, and is applied to the low elite reform activitycategory of Model 2. Model 3 indicates that the reform elements will be selectivelypicked to fit in a local context setting. Model 4 suggests that no reform will belaunched and the status quo will be maintained.

The case of Wenzhou financial reform

After discussing the theory, lets return to the case of Wenzhou. Chinese banks haveprivileged large and state enterprises in their lending decisions over small andmedium-sized enterprises (SMEs) even during years of financial expansion. TheSMEs are in an unfavorable position when it comes to gaining loans, which has led tothe prosperity of the underground lending market (民间借贷). The debt crisis ofWenzhou and prosperity of the underground market are mainly caused by the highinterest rate of private finance on the one hand and limited official investmentchannels to attract the private idle fund on the other hand. A meaningful solutionshould not lie in solving specific issues in Wenzhou, but rather in solving thestructural problems in the financial system that force people into shadows. As weshall see, the central government seems not to be interested in reaching the corestructural problems in the financial reform of Wenzhou.

Debt crisis in Wenzhou

Wenzhou has a leading developed private economy in China with abundant privatefunds and financial activities. It is one of the manufacturing powerhouses in China,producing and exporting products including lighters, clothes and shoes. Manysuccessful, privately owned enterprises are based in Wenzhou. In recent years, manySMEs have reduced their investment in traditional business because of decliningprofits.32Windfall profits, on the contrary, weremade in the real estatemarket.33Manylocal entrepreneurs, therefore, took their money out of the struggling industrialmanufacturing sector and put it into the profitable real estate market. In 2011, thecentral government began to tighten monetary policy to curb soaring inflation, whichmade it even harder for SMEs to receive credit from banks.Many SMEs had to look forfinancing from the underground lending market. The interest rate of this undergroundmarket is much higher than the benchmark interest rate and it is usually organized for

32. There were many reasons for this decline in profits, including: appreciation of RMB currency, economicrecession in the US and Europe, and increasing labor costs in China.

33. Interest rates on deposits are so low that simply depositing money in the banks is not an attractive option;therefore, many choose to invest in the housing market.

JINGHAN ZENG

8

Dow

nloa

ded

by [

Uni

vers

ity o

f W

arw

ick]

at 1

3:19

04

Oct

ober

201

4

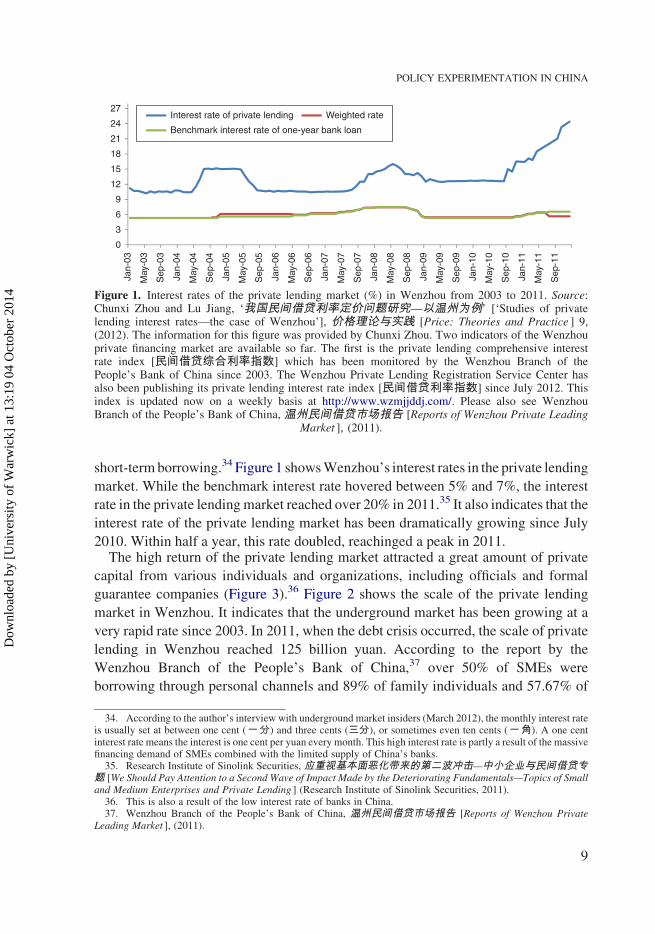

short-termborrowing.34 Figure 1 showsWenzhou’s interest rates in the private lending

market. While the benchmark interest rate hovered between 5% and 7%, the interest

rate in the private lendingmarket reached over 20% in 2011.35 It also indicates that the

interest rate of the private lending market has been dramatically growing since July

2010. Within half a year, this rate doubled, reachinged a peak in 2011.The high return of the private lending market attracted a great amount of private

capital from various individuals and organizations, including officials and formal

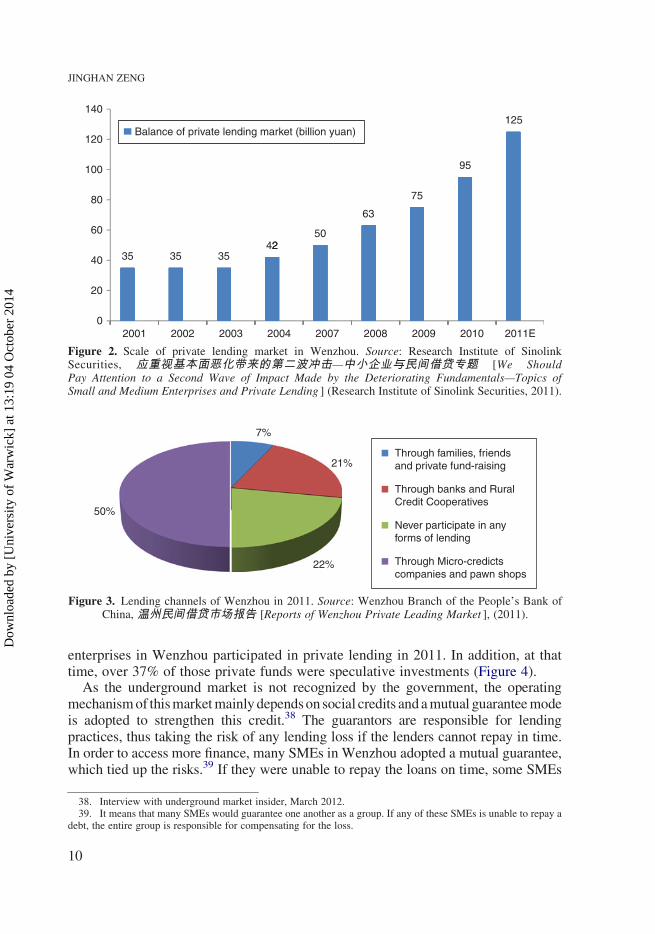

guarantee companies (Figure 3).36 Figure 2 shows the scale of the private lending

market in Wenzhou. It indicates that the underground market has been growing at a

very rapid rate since 2003. In 2011, when the debt crisis occurred, the scale of private

lending in Wenzhou reached 125 billion yuan. According to the report by the

Wenzhou Branch of the People’s Bank of China,37 over 50% of SMEs were

borrowing through personal channels and 89% of family individuals and 57.67% of

0

3

6

9

12

15

18

21

24

27

Jan-

03

May

-03

Sep

-03

Jan-

04

May

-04

Sep

-04

Jan-

05

May

-05

Sep

-05

Jan-

06

May

-06

Sep

-06

Jan-

07

May

-07

Sep

-07

Jan-

08

May

-08

Sep

-08

Jan-

09

May

-09

Sep

-09

Jan-

10

May

-10

Sep

-10

Jan-

11

May

-11

Sep

-11

Interest rate of private lending Weighted rate

Benchmark interest rate of one-year bank loan

Figure 1. Interest rates of the private lending market (%) in Wenzhou from 2003 to 2011. Source:Chunxi Zhou and Lu Jiang, ‘我国民间借贷利率定价问题研究—以温州为例’ [‘Studies of privatelending interest rates—the case of Wenzhou’], 价格理论与实践 [Price: Theories and Practice ] 9,(2012). The information for this figure was provided by Chunxi Zhou. Two indicators of the Wenzhouprivate financing market are available so far. The first is the private lending comprehensive interestrate index [民间借贷综合利率指数] which has been monitored by the Wenzhou Branch of thePeople’s Bank of China since 2003. The Wenzhou Private Lending Registration Service Center hasalso been publishing its private lending interest rate index [民间借贷利率指数] since July 2012. Thisindex is updated now on a weekly basis at http://www.wzmjjddj.com/. Please also see WenzhouBranch of the People’s Bank of China, 温州民间借贷市场报告 [Reports of Wenzhou Private Leading

Market ], (2011).

34. According to the author’s interview with underground market insiders (March 2012), the monthly interest rateis usually set at between one cent (一分) and three cents (三分), or sometimes even ten cents (一角). A one centinterest rate means the interest is one cent per yuan every month. This high interest rate is partly a result of the massivefinancing demand of SMEs combined with the limited supply of China’s banks.

35. Research Institute of Sinolink Securities, 应重视基本面恶化带来的第二波冲击—中小企业与民间借贷专题 [We Should Pay Attention to a Second Wave of Impact Made by the Deteriorating Fundamentals—Topics of Smalland Medium Enterprises and Private Lending ] (Research Institute of Sinolink Securities, 2011).

36. This is also a result of the low interest rate of banks in China.37. Wenzhou Branch of the People’s Bank of China, 温州民间借贷市场报告 [Reports of Wenzhou Private

Leading Market ], (2011).

POLICY EXPERIMENTATION IN CHINA

9

Dow

nloa

ded

by [

Uni

vers

ity o

f W

arw

ick]

at 1

3:19

04

Oct

ober

201

4

enterprises in Wenzhou participated in private lending in 2011. In addition, at thattime, over 37% of those private funds were speculative investments (Figure 4).As the underground market is not recognized by the government, the operating

mechanismof thismarketmainly dependson social credits andamutual guaranteemodeis adopted to strengthen this credit.38 The guarantors are responsible for lendingpractices, thus taking the risk of any lending loss if the lenders cannot repay in time.In order to access more finance, many SMEs in Wenzhou adopted a mutual guarantee,which tied up the risks.39 If they were unable to repay the loans on time, some SMEs

35

0

20

40

60

80

100

120

140

2001 2002 2003 2004 2007 2008 2009 2010 2011E

35 3542

Balance of private lending market (billion yuan)

250

63

75

95

125

Figure 2. Scale of private lending market in Wenzhou. Source: Research Institute of SinolinkSecurities, 应重视基本面恶化带来的第二波冲击—中小企业与民间借贷专题 [We ShouldPay Attention to a Second Wave of Impact Made by the Deteriorating Fundamentals—Topics ofSmall and Medium Enterprises and Private Lending ] (Research Institute of Sinolink Securities, 2011).

50%

7%

21%

22%

Through families, friendsand private fund-raising

Through banks and RuralCredit Cooperatives

Never participate in anyforms of lending

Through Micro-credictscompanies and pawn shops

Figure 3. Lending channels of Wenzhou in 2011. Source: Wenzhou Branch of the People’s Bank ofChina, 温州民间借贷市场报告 [Reports of Wenzhou Private Leading Market ], (2011).

38. Interview with underground market insider, March 2012.39. It means that many SMEs would guarantee one another as a group. If any of these SMEs is unable to repay a

debt, the entire group is responsible for compensating for the loss.

JINGHAN ZENG

10

Dow

nloa

ded

by [

Uni

vers

ity o

f W

arw

ick]

at 1

3:19

04

Oct

ober

201

4

chose toborrowmore fromtheundergroundmarket to payoff the interest and the interestrate on thiswas higher thanonprevious loans: a vicious circle. In fact, the profit from realestate was largely affected by government control policies and it was impossible tosustain such high returns. After the financial chains eventually broke, some of the localentrepreneurs fled and a few even committed suicide, leaving substantial debt behind inWenzhou.While the situationwasmore severe inWenzhou than in other parts of China,this ‘local’ crisis nevertheless had repercussions beyond the immediate environment andvarious reports expressed serious concern about the potential impact of the collapse ofthe Wenzhou private lending scheme on the Chinese economy as a whole.40

After the mass media exposed the flights and suicides of SME owners, the lendersrequested that SMEs pay back their borrowings. The underground lending marketshrunk rapidly, which led to an ever greater number of SMEs collapsing. A chainreaction in Wenzhou’s economy and waves of collapsed SMEs seriously challengedthe local socio-economic stability. In late September 2011, the news reached a climaxwhen the SinceTech chairman was reported to have escaped to the US, leaving a debtof over two billion RMB.41

Response of the government

Soon after the debt crisis, on 3 October 2011, Premier Wen Jiabao visited Wenzhouwith many top finance officials, including Financial Minister Xie Xuren, theGovernor of the Central Bank Zhou Xiaochuan and the CBRC Chairman LiuMingkang. They visited the industry bases and met with many SMEs during theirvisit to Zhejiang. Wen emphasized that ‘local government should properly handle the

19%

19%37%

20%

5%

Investment on Real Estate

General Production and Operation

Lend to agent computer by individuals

Repayment of loan, notes deposits andother short-term revolving funds

Others

Figure 4. Distributions of Wenzhou private capital purposes in 2011. Source: Wenzhou Branch ofthe People’s Bank of China, 温州民间借贷市场报告 [Reports of Wenzhou Private Leading

Market ], (2011).

40. Research Institute of Sinolink Securities, 应重视基本面恶化带来的第二波冲击 [We Should Pay Attentionto a Second Wave of Impact Made by the Deteriorating Fundamentals ].

41. Bing Chen, 传温州最大眼镜厂信泰集团董事长欠款潜逃 [The Chairman of Wenzhou’s Biggest GlassesFactory, Sincetech, Has Fled for Fear of Debt, (2010), available at: http://www.21cbh.com/HTML/2011-9-22/1MMDcyXzM2NzY1MA.html (accessed 10 October 2012).

POLICY EXPERIMENTATION IN CHINA

11

Dow

nloa

ded

by [

Uni

vers

ity o

f W

arw

ick]

at 1

3:19

04

Oct

ober

201

4

recent risky events, protect people’s legal rights, and strengthen marketconfidence’.42 On 28 March 2012, the State Council approved ‘The Overall Programof Wenzhou Financial Comprehensive Reform Pilot Area in Zhejiang Province’.It pointed out that ‘the broken funding chain and the fleeing of local entrepreneurs inWenzhou affected economic and social stability’43 and clarified 12 central tasks ofWenzhou financial reform. Through the ambitious and complete financial reformplan, the central state signaled to the market that it was determined to solve the debtcrisis and funding problems of SMEs. Wenzhou again became a pilot zone forfar-reaching financial reforms.The debt crisis was gradually solved after the announcement by the State

Council. It is notable that the reform announced by the State Council was a vagueplan and the specific implementation measures were left to the Wenzhougovernment to organize. Interestingly, those specific rules were postponed severaltimes after the immediate debt crisis was solved. In July 2012, the WenzhouFinancial Office claimed that the specific rules would be announced on 28 August2012; however, the Office failed to announce them.44 Relevant conferences ofWenzhou financial reform were held on 29 September 2012, just half a year afterthe announcement of the State Council, which seemed to be a good time to releasethe specific rules. Wenzhou Financial Office Director, Zhang Zhengyu, explainedthat specific rules would be released in the press conference on 29 September 2012,but this conference was later cancelled.45 According to a source at Securities Times,it was cancelled because there had been no substantive progress achieved by thisreform in the government’s opinion.46 Not surprisingly, the repeated delays ofspecific rules have made many who had high expectations of this reform feeldisappointed.47

The leadership transition in late 2012 (i.e. the 18th Party Congress) and the needfor stability are among the reasons why the reform rules were postponed. Accordingto a research report by Essence Securities,48 a major reason which led to the slowprogress of the Wenzhou financial reform is that the key target of the localgovernment was to maintain stability. Therefore, they emphasized the risk control.This report expected that progress would be faster after the 18th Party Congress.49

On 23 November 2012, a week after the leadership transition at the 18th PartyCongress, the Wenzhou government finally released the specific rules. As we shallsee, those rules left many insiders disappointed again.

42. Jiabao Wen, ‘Recognize situation, increase confidence and strengthen the good tendency of economicgrowth’, Speech at the meeting with small loan companies, reported by Xinhua news, (2011), available at: http://news.xinhuanet.com/politics/2011-10/05/c_122121534_2.htm (accessed 1 January 2012).

43. Executive meeting of the State Council of China, on 28 March 2012.44. Xiaoping Li, ‘温州金改细则难产民众参与热情大减’ [‘Specific rules of Wenzhou financial reform have not

been announced yet, passion of people’s participation largely decreased’], STCN, (2012), available at: http://kuaixun.stcn.com/2012/1010/10130297.shtml (accessed 25 January 2013).

45. Ibid.46. Ibid.47. Ibid.48. Jianhai Yang and Li He, 温州金融改革进展跟踪 [Tracking Progress of Wenzhou Financial Reform ]

(Essence Securities, 2012).49. Ibid.

JINGHAN ZENG

12

Dow

nloa

ded

by [

Uni

vers

ity o

f W

arw

ick]

at 1

3:19

04

Oct

ober

201

4

Theoretical framework and the Wenzhou financial reform

After introducing the debt crisis and the government response in Wenzhou, lets usethe aforementioned theoretical framework to analyze the Wenzhou financial reform.

External pressures

The immediacy of the Wenzhou debt crisis generated strong pressures from the CCPand social forces. First and foremost, the primary pressure came from the CCP leaders,which was extremely high as it was relevant to the survival of the regime. The crisis ofWenzhou has caused economic difficulties in China’s leading local economy. If itcould not be contained immediately, it might have become a national crisis. Economicsuccess is widely considered as a principal (if not sole) pillar of political legitimacy inChina,50 and Chinese intellectuals are seriously concerned about the negative impactsof bad economic performance on regime legitimacy.51 In this sense, theWenzhou debtcrisis did pose a serious challenge to the legitimacy of the entire regime, and was notjust a local problem in Wenzhou itself.In addition to economic problems, this crisis also undermined social stability—

Wenzhou fell into panic immediately after the media exposure about the flight orsuicide of local entrepreneurs. To maintain a stable social order is highly valued byChinese leaders. According to Deng Xiaoping, ‘in China, the overriding need is forstability.Without a stable environment, we can accomplish nothing andmay even losewhat we have gained’.52 In Jiang Zemin’s speech at the 15th Party Congress, Jiangclearly elaborated that ‘without stability, nothing can be achieved’.53 Hu Jintao alsowarned that ‘we should always keep in mind that there is nothing we can achievewithout social stability; we should properly handle the relationship among reform,development and stability, and maintain the overall social stability’.54 In 2011,a Chinese white paper clearly declared social stability as one of China’s core interests.While this emphasis on stability has been something of a constant in contemporary

Chinese politics, it appears to have been an even greater and urgent consideration in

50. Dingxin Zhao, ‘The mandate of heaven and performance legitimation in historical and contemporary China’,American Behavioral Scientist 53(3), (2009), pp. 416–433; Wang, ‘Political trust in China’; Andre Laliberte andMarc Lanteigne, ‘The issue of challenges to the legitimacy of CCP rule’, in Andre Laliberte and Marc Lanteigne, eds,The Chinese Party-State in the 21st Century: Adaptation and the Reinvention of Legitimacy (London: Routledge,2008); David Shambaugh, ‘The dynamics of elite politics during the Jiang era’, The China Journal 45, (2001),pp. 101–111; Dingxin Zhao, ‘当今中国会不会发生革命?’ [‘Will a revolution happen in China?’], 二十一世纪[21st Century ] 134, (2012); Elizabeth Perry, ‘Chinese conceptions of “rights”: from Mencius to Mao—and now’,Perspectives on Politics 6, (2008).

51. Jinghan Zeng, ‘The debate on regime legitimacy in China: bridging the wide gulf between Western andChinese scholarship, Journal of Contemporary China 23(88), (2014), pp. 612–635.

52. Also, during his talk with leading members of the CCP Central Committee on 24 December 1990, Deng againinsisted that ‘I have said more than once that stability is of overriding importance and that we cannot abandon thepeople’s democratic dictatorship’ [‘我不止一次讲过,稳定压倒一切,人民民主专政不能丢’]. See XiaopingDeng, Selected Works of Deng Xiaoping Vol. 3 [邓小平文选第三卷 ] (Beijing: Foreign Languages Press, 1994),p. 365; English translation is cited from People’s Daily, available at: http://english.peopledaily.com.cn/dengxp/vol3/text/d1170.html (accessed 15 July 2013).

53. ‘没有稳定,什么事也干不成.’ See Jiang Zemin, The Selected Works of Jiang Zemin Vol. 1 [江泽民文选第一卷] (Beijing: People’s Press [人民出版社], 2006), p. 461.

54. ‘我们要始终牢记没有稳定的社会局面,就什么事也干不成,妥善处理好改革发展稳定的关系,保持社会大局的稳定.’ Hu Jintao, excerpt from a talk during Hu’s visit in Brunei, 21 April 2005.

POLICY EXPERIMENTATION IN CHINA

13

Dow

nloa

ded

by [

Uni

vers

ity o

f W

arw

ick]

at 1

3:19

04

Oct

ober

201

4

2012 because of the once-in-a-decade leadership transition. Seven out of the ninemost powerful leaders including President Hu Jintao and Premier Wen Jiabao werereplaced in late 2012. For an authoritarian regime, successfully transferring the toppower and preventing a split in the leadership during this process have always beenextremely challenging. Around 68% of authoritarian leaders have been overthrownby ruling elites rather than by the masses.55 Power succession in China has alwaysbeen a moment of crisis and great change, except for the two most recenttransitions.56

In 2012, the scandal of Bo Xilai, a member of the Politburo and a leading candidateto enter the Politburo Standing Committee, indicated an intense political struggleunder the table. Bo was removed from his post as Chongqing Party Chief severalmonths before the leadership transition because of a ‘disciplinary offence’, and hiswife was charged with murder. As the power transition period has a high incidence ofcrisis and instability, the CCP was very sensitive to any potential risks and tried theirbest to maintain stability during this period in order to perform a smooth and orderlyleadership transition.57 As such, the central leaders could not simply ignore the debtcrisis and they immediately responded with a financial reform idea to establish theirreform credentials and maintain their leadership legitimacy.In addition to intra-party concerns, some pressure also came from domestic private

enterprises, which are in an unfavorable funding position in trying to compete withstate-owned enterprises in the current financial system. The debt crisis was alsooriginally caused by those SMEs that could not gain sufficient loans from Chinesebanks. Not surprisingly, the SMEs expected that the central government could reformthe financial system in order to reduce their financing costs. However, as I willexplain below, this reform neither reduced financing costs for SMEs nor improvedthe efficiency of the financial system as it promised. Although both the party leadersand social forces push for the financial reform, they expected a different outcomefrom the reform. In short, the SMEs attempted to gain greater economic benefits fromthe reform, whilst the central leaders considered it as a mean to restore socio-economic order.

Elite reform activity

As mentioned above, compared with the inefficiency of the current financial system,the leadership of Hu Jintao and Wen Jiabao seemed to be more concerned about theinstability caused by the debt crisis at the sensitive period of leadership transition.They were either incapable or unwilling—perhaps most persuasively both of theabove—to launch a complete reform to solve the structural problems of the financial

55. Milan Svolik, The Politics of Authoritarian Rule (Cambridge: Cambridge University Press, 2012), p. 5.56. For example, the purge of Mao Zedong’s successors Liu Shaoqi and Lin Biao plunged the country into chaos.

The 1989 protest was closely related to Deng Xiaoping’s appointed successors, Zhao Ziyang and Hu Yaobang, whowere also removed.

57. In order to reduce the risks of cruel political struggles and maintain the unity of the leadership, the CCP usedthe ‘seniority’ principle to select its new top leaders in 2012. Please see Jinghan Zeng, ‘What matters most in selectingtop Chinese leaders? A qualitative comparative analysis’, Journal of Chinese Political Science 18(3), (2013),pp. 223–239; Jinghan Zeng, ‘Institutionalization of the Authoritarian Leadership in China: A Power SuccessionSystem with Chinese Characteristics?’ Contemporary Politics 20 (3), (2014), pp. 294–314.

JINGHAN ZENG

14

Dow

nloa

ded

by [

Uni

vers

ity o

f W

arw

ick]

at 1

3:19

04

Oct

ober

201

4

system in China. The primary reason is simple: a market-oriented financial reformmight cause uncertainties and the CCP needed stability in 2012, as I mentioned earlier.Moreover, it was perhaps an awkward time to start a tough reform. Such a complex

reform needs sustainable support and commitment from the central government.Although we can expect the new leadership to adopt a path-dependent approach onmajor issues, whether they will show the same level of support for this financialreform is still questionable.In addition, policy consistency might be affected by the leadership transition.

For example, the new premier Li Keqiang has staked his financial reform plan on the‘China (Shanghai) Pilot Free Trade Zone’ rather than the ‘Wenzhou FinancialComprehensive Reform Pilot Area’. Although the central government claimed thatWenzhou financial reform would be highly valued when it was launched, this reformdid not receive corresponding support from the central government after the debt crisiswas solved—indeed, the support of Li Keqiang’s State Council for pilots in Shenzhenand Shanghai seems to have been much stronger than that for Wenzhou, as I willexplain later.Above all, the above discussion suggests that Wenzhou financial reforms fit the

categorization of Model 2 (strong external pressure with low reform activity) in thetheoretical framework. It indicates that reform remains superficial without meaningfulchanges. This is evidenced byWenzhou’s ambitious reform ideas in contrast with poorreform practices.

Symbolic reform: ‘loud thunder without rain’

The reform ideas in Wenzhou were highly ambitious and positive, which led toanother wave of news coverage after the debt crisis and raised high expectations inthe market. However, its actual practices seemed to deviate from this goal. Afterthe specific rules of reform were released by the Wenzhou government, manyindustry insiders felt very disappointed and used the words ‘loud thunder withoutrain’ (雷声大,雨点小) to describe this reform.58

For instance, the vice president of the SMEs Association and the president ofWenzhou SMEs Development Promotion Association, Zhou Dewen, argue thatWenzhou financial reform did not make any breakthrough and its rules were toovague.59 According to Zhou, the Wenzhou reforms lacked courage and thegovernment restricted itself.60 The vice dean of the Shanghai Advanced FinancialSchool at the Shanghai Jiaotong University, Zhu Ning, argues that the results of thisreform are mixed. Whilst it has helped the economy to recover in Wenzhou, however,the extent to which the reform ideas have been implemented is a serious problem.61

58. Fenfen Tong, ‘温州金改:细则不’细’ 隔靴搔痒’ [‘Wenzhou financial reform: specific rules are not“specific” nowhere near enough’], 民商杂志 [Magazine of Private Business ], (2013); Tan Ye, ‘叶檀:温州金改改皮不改骨’ [‘Wenzhou financial reform changes the skin without improving the core parts’],每日经济新闻 [NationalBusiness Daily ], (2012).

59. Tong, ‘温州金改:细则不’细’ 隔靴搔痒’ [‘Wenzhou financial reform’].60. Li, ‘温州金改细则难产民众参与热情大减’ [‘Specific rules of Wenzhou financial reform have not been

announced yet’].61. Ibid.

POLICY EXPERIMENTATION IN CHINA

15

Dow

nloa

ded

by [

Uni

vers

ity o

f W

arw

ick]

at 1

3:19

04

Oct

ober

201

4

Ye Tan, a prominent Chinese financial analyst, argues that Wenzhou’s financialreform only ‘changes a new dress without improving its body’ (改皮不改骨).62

Ma Guangtuan, a prominent Chinese economist, is more pessimistic. After severalvisits to Wenzhou and communication with local officials and institutions, Ma arguethat the specific rules of Wenzhou financial reform ‘failed badly’ (很失败)63 and thereform ‘only exists in name’ (名存实亡).64 Why were those insiders and analysts sodisappointed about this reform?First of all, many parts of the content of the reform were not new. The second task

of the reform program approved by the State Council, for example, is to ‘acceleratethe development of new financial organizations: encourage and support private fundsto participate in village banks, loan companies, and rural capital unions’.65 Indeed,the China Banking Regulatory Commission (CBRC) released similar policies forvillage banks as far back as 2006. Regarding small loan companies, ‘Suggestions toAdjust Access Policy of Banks and Financial Institutions in Rural Areas’ in 2006 and‘Guidance of Small Loan Companies Pilots’ in 2008 announced by the CBRC alsoformed similar policies.This task has not been well implemented either. According to Zhou Dewen, only

two small loan companies were established in Wenzhou and none of the small loancompanies changed into a bank for the villages and towns after the reform wasannounced.66 The financial reform of 2012 emphasizes the idea of accelerating thedevelopment of new financial organizations, but no specific measures (such asloosening conditions to establish small loan firms or simplified government approvalprocedures) were released to achieve this goal. According to Zhou, this is perhapsbecause the local government restricted itself and lacks courage.67

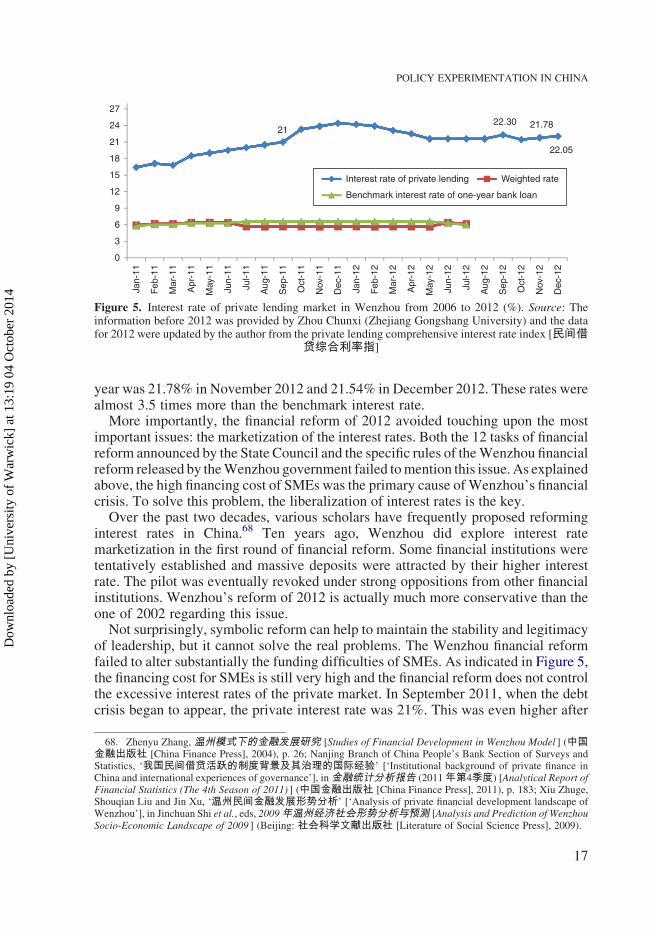

The biggest breakthrough of this reform is perhaps the official recognition ofprivate finance. This policy helps the government to monitor private finance;however, its real impact on the operating mechanism of private finance is verylimited. This issue refers to a more important reason why the financial reform of 2012is symbolic: it deliberately avoids touching upon the core issues. Under the controlpolicies of the interest rate, the official interest rate in China does not respond to themarket and thus it is not very attractive for private idle funds. In this situation, privateidle funds will still be motivated to go to underground markets which offer highinterest rates. This prediction has been confirmed by the latest data. Figure 5 showsthe interest rate of private finance and banks from 2011 to 2012. It indicates that thereis a wide gap between the interest rate of private lending and that of banks after thereform. A year after Wenzhou’s debt crisis, the interest rate of private finance per

62. Ye, ‘叶檀:温州金改改皮不改骨’ [‘Wenzhou financial reform changes the skin without improving the coreparts’].

63. Guangyuan Ma, ‘温州金融综合改革实施细则很失败’ [‘Specific rules of Wenzhou comprehensive financialreform failed badly’], Caijing, (2012), available at: http://blog.caijing.com.cn/expert_article-151268-44179.shtml(accessed 21 January 2013).

64. Guangyuan Ma, ‘马光远:温州金融改革名存实亡’ [‘Wenzhou’s financial reform only exists in name’],Sohu, (2012), available at: http://business.sohu.com/20121128/n358928611.shtml (accessed 21 January 2013).

65. For the contents of the reform, please see http://politics.people.com.cn/GB/1024/17523916.html.66. Li, ‘温州金改细则难产民众参与热情大减’ [‘Specific rules of Wenzhou financial reform have not been

announced yet’].67. Ibid.

JINGHAN ZENG

16

Dow

nloa

ded

by [

Uni

vers

ity o

f W

arw

ick]

at 1

3:19

04

Oct

ober

201

4

year was 21.78% in November 2012 and 21.54% in December 2012. These rates werealmost 3.5 times more than the benchmark interest rate.More importantly, the financial reform of 2012 avoided touching upon the most

important issues: the marketization of the interest rates. Both the 12 tasks of financialreform announced by the State Council and the specific rules of theWenzhou financialreform released by theWenzhou government failed tomention this issue. As explainedabove, the high financing cost of SMEs was the primary cause ofWenzhou’s financialcrisis. To solve this problem, the liberalization of interest rates is the key.Over the past two decades, various scholars have frequently proposed reforming

interest rates in China.68 Ten years ago, Wenzhou did explore interest ratemarketization in the first round of financial reform. Some financial institutions weretentatively established and massive deposits were attracted by their higher interestrate. The pilot was eventually revoked under strong oppositions from other financialinstitutions. Wenzhou’s reform of 2012 is actually much more conservative than theone of 2002 regarding this issue.Not surprisingly, symbolic reform can help to maintain the stability and legitimacy

of leadership, but it cannot solve the real problems. The Wenzhou financial reformfailed to alter substantially the funding difficulties of SMEs. As indicated in Figure 5,the financing cost for SMEs is still very high and the financial reform does not controlthe excessive interest rates of the private market. In September 2011, when the debtcrisis began to appear, the private interest rate was 21%. This was even higher after

0

3

6

9

12

15

18

21

24

27

Jan-

11

Feb

-11

Mar

-11

Apr

-11

May

-11

Jun-

11

Jul-1

1

21

Aug

-11

Sep

-11

Oct

-11

Nov

-11

Dec

-11

Jan-

12

Feb

-12

Mar

-12

Apr

-12

May

-12

Jun-

12

Jul-1

2

22.30 21.78

Aug

-12

Sep

-12

Oct

-12

22.05

Nov

-12

Dec

-12

Interest rate of private lending Weighted rate

Benchmark interest rate of one-year bank loan

Figure 5. Interest rate of private lending market in Wenzhou from 2006 to 2012 (%). Source: Theinformation before 2012 was provided by Zhou Chunxi (Zhejiang Gongshang University) and the datafor 2012 were updated by the author from the private lending comprehensive interest rate index [民间借

贷综合利率指]

68. Zhenyu Zhang, 温州模式下的金融发展研究 [Studies of Financial Development in Wenzhou Model ] (中国金融出版社 [China Finance Press], 2004), p. 26; Nanjing Branch of China People’s Bank Section of Surveys andStatistics, ‘我国民间借贷活跃的制度背景及其治理的国际经验’ [‘Institutional background of private finance inChina and international experiences of governance’], in金融统计分析报告 (2011年第4季度) [Analytical Report ofFinancial Statistics (The 4th Season of 2011) ] (中国金融出版社 [China Finance Press], 2011), p. 183; Xiu Zhuge,Shouqian Liu and Jin Xu, ‘温州民间金融发展形势分析’ [‘Analysis of private financial development landscape ofWenzhou’], in Jinchuan Shi et al., eds, 2009年温州经济社会形势分析与预测 [Analysis and Prediction of WenzhouSocio-Economic Landscape of 2009 ] (Beijing: 社会科学文献出版社 [Literature of Social Science Press], 2009).

POLICY EXPERIMENTATION IN CHINA

17

Dow

nloa

ded

by [

Uni

vers

ity o

f W

arw

ick]

at 1

3:19

04

Oct

ober

201

4

the financial reform and reached 22.3% in September 2012, a year after the debtcrisis. The latest rate of December 2012 provided by the Wenzhou government was22.05%, which is higher than the average rate for 2011.In addition, this reform also fails to improve the investment channels of private idle

funds. Limited official investment channels led to the inefficient allocation of privateidle funds and this is one of the major reasons why the underground market is soprosperous. Various Chinese scholars have proposed building a more diversifiedofficial investment channel for private idle funds.69 This reform promised to ‘build adiversified financial system and encourage development of private funds’,70 but it didnot implement this goal. According to the report by the Economic Herald,71 variousprivate idle funds in Wenzhou were excited by this financial reform; however, theWenzhou government deliberately controlled the progress of the reform, which madethe legal investment channel of the private fund still quite limited. This indicates thatthe government wanted to maintain socio-economic stability. In the words of theWenzhou Finance Office, ‘stability’ is a guiding principle.72 The local officials arealso wary of taking any risk. In the words of the Zhejiang Party Chief, Zhao Hongzhu,and the Wenzhou Financial Office Director, Zhang Zhengyu, ‘Wenzhou financialreform failure will not be tolerated’ (只许成功,不许失败).73

The Chinese Academy of Social Science (CASS) provides a more comprehensiveand authoritative evaluation of Wenzhou financial reform based on its scholars’fieldwork in Wenzhou in August 2013. Although this report acknowledges theprogress of the reform in three aspects—launching various measures to promotefinancing and investment of the SMES, establishing a financial safety net and effortsin building the insurance system—it points out seven major problems that still exist inWenzhou’s financial market.74 It clearly points out that the reform ideas were notwell-implemented. It also argues that the policy support and tax incentives areinsufficient because the central government did not give sufficient to the pilots inWenzhou compared with pilots in Shanghai and Shenzhen. According to the report,the crisis of the mutual guarantee mode is still ‘spreading’ (蔓延) in Wenzhou.A more straightforward expression is given by Zhang Ming—one of the CASSreport’s two authors and a CASS research associate—‘the financial reform failed tosolve big problems’ (金融改革没能解决大问题).75

69. Zhuge et al, ‘温州民间金融发展形势分析’ [‘Analysis of private financial development landscape ofWenzhou’]; Section of Surveys and Statistics, ‘我国民间借贷活跃的制度背景及其治理的国际经验’[‘Institutional background of private finance in China’].

70. Juntao Liu, 国务院会议确定温州市金融综合改革十二项任务 [The State Council Conference Decides theTwelve Tasks of Wenzhou Financial Reform ], (2012), available at: http://politics.people.com.cn/GB/1024/17523916.html (accessed 20 December 2012).

71. Chao Shi, ‘温州金融改革被指尚未见效民资汹涌投资受限’ [‘Wenzhou’s financial reforms are noteffective yet, investment channels of private funding are limited’], 经济导报 [Economic Herald ], (2012).

72. Ibid.73. Xiang Gao and Junhua Hu, ‘温州金改成长记:重点在制度创新’ [‘Development of Wenzhou financial

reform: emphasis should be innovation of institutions’], 每日经济新闻 [National Business Daily ], (2012).74. Jie Liu and Ming Zhang, ‘温州金融改革调研报告’ [‘A research report of Wenzhou financial reform’],

in International Investment Studies (Chinese Academy of Social Science, 2013).75. Ming Zhang, ‘Wenzhou research report II: the financial reform failed to solve big problems’ [‘温州调研报告之

二:金融改革没能解决大问题’], Sohu Blog, (2013), available at: http://zhangming1977.blog.sohu.com/281811200.html (accessed 7 December 2013). This straightforward expression was widely reproduced by various media. Forexample, please see http://comments.caijing.com.cn/2013-11-05/113522827.html (accessed 1 December 2013).

JINGHAN ZENG

18

Dow

nloa

ded

by [

Uni

vers

ity o

f W

arw

ick]

at 1

3:19

04

Oct

ober

201

4

Concluding remarks

As demonstrated by the case of Wenzhou, policy experimentation in China does notalways seek policy efficiency that is at least implied in some of the literature.Reforms can be manipulated as political symbols to restore socio-economic ordersby promoting the ideas of ‘change’ and to maintain the legitimacy of leadership byestablishing their reform credentials.To understand the extent to which policy experimentation in China is used as a

hollow symbol, it is necessary to understand the interests of the centralgovernment. Although economic power has been highly decentralized in China, thecentral state still holds the unchallengeable power in this authoritarian system.It still dominates the power to set policy goals, choose local practices, define the‘success’ of policy practices in local states, and decide whether local practices willbe upgraded into a national policy. In this way, the central state can filter localpractices in its own right, and there is little doubt that this filtering process will beaffected by the interests of the central government. As illustrated in this article, amore efficient and effective policy does not always coincide with the interests ofthe central state. In the case of the Wenzhou financial reform, the priority of thecentral state is to maintain stability, which could be at the expense of policyimprovement. Thus, Wenzhou financial reform is likely to go through a ‘tinkerthrough’ process.As Heilmann argued, the pattern of central–local interaction lies at the core of

China’s policy experimentations.76 In this sense, it is important to understand how theinterests of the central government affect the design of local experimentation.The central government has to step in every time local governments fail, but itmight notalways impose ameaningful solution or tackle the real problems.More importantly, theextent to which symbolic reforms represent the cases of Chinese reforms needs to bestudied carefully given its implications for the development of China.Nowadays, many China watchers tend to find explanations for adaptive

governance from China’s political system. They consider this authoritarian systemas ‘resilient’.77 It implies that China’s political system somehow helps to encouragereform and policy innovation. While there is much room for those arguments, weshould not undermine the limits of the authoritarian system. In democratic countries,alternations of the government will not necessarily lead to the collapse of the politicalsystem. However, in China, the state, the political system and perhaps the economyare combined. The cost of a split leadership during the process of power successionwill be paid for not only by the regime but also by the entire political system. At alltimes, the survival of the government is the first priority for the party-state; it mightbe at the expense of policy and reform merits.

76. Heilmann, ‘Policy experimentation in China’s economic rise’.77. Andrew Nathan, ‘Authoritarian resilience’, Journal of Democracy 14(1), (2003), pp. 6–17; Joseph Fewsmith,

‘Inner-party democracy: development and limitations’, China Leadership Monitor 31, (2006); Kerry Brown, Friendsand Enemies: The Past, Present and Future of the Communist Party of China (New York: Antherm Press, 2009);Bruce Dickson, Red Capitalists in China: The Party, Private Entrepreneurs, and Prospects for Political Changes(New York: Cambridge University Press, 2003); Kellee Tsai, Capitalism without Democracy: The Private Sector inContemporary China (Ithaca, NY: Cornell University Press, 2007); Dali Yang, Remaking the Chinese Leviathan:Market Transition and the Politics of Governance in China (Stanford, CA: Stanford University Press, 2004).

POLICY EXPERIMENTATION IN CHINA

19

Dow

nloa

ded

by [

Uni

vers

ity o

f W

arw

ick]

at 1

3:19

04

Oct

ober

201

4