Embed Size (px)

Citation preview

Go Onlinewww.matthey.com/AR12To view our online annual report

JOHNSON MATTHEY IS A LEADING SPECIALITYCHEMICALS COMPANY UNDERPINNED BYSCIENCE, TECHNOLOGY AND OUR PEOPLE.

The group is a leader in sustainabletechnologies and many of ourproducts enhance the quality of lifefor millions through their beneficialimpact on the environment, healthand wellbeing. Technologyleadership forms the basis ofJohnson Matthey’s strategy to deliversuperior long term growth and wecontinue to invest in R&D to developthe next generation of sustainableproducts for our customers. To us,good performance is not just aboutprofit. It’s about running our businessin the most sustainable andresponsible way and so we haveidentified five elements of sustainabilitywhich have a material impact on ourbusiness. In this report we will updateyou on our progress.

DELIVERINGVALUE

FinancialMust be profitable to be sustainableSustainability initiatives can be cost efficient too

Health and SafetyProtecting employees, customers and communitiesBeneficial products

EnvironmentResponsible operationsBeneficial products

GovernanceWell run businessTransparent reporting

SocialEmployee development and wellbeing, recruitment Supporting communities, safeguarding reputation

Building a Sustainable Business

ANNUAL REPORT & ACCOUNTS

Johnson Matthey

Annual R

eport & Accounts 2012

5th Floor25 Farringdon StreetLondon EC4A 4ABUnited KingdomTel: +44 (0)20 7269 8400Fax: +44 (0)20 7269 8433

2012

VALUEdeveloping products that enhance the quality of life

for millions of people around the world

Go Onlinewww.matthey.comTo view our online annual report

DELIVERING

Go Onlinewww.matthey.com/AR12To view our online annual report

JOHNSON MATTHEY IS A LEADING SPECIALITYCHEMICALS COMPANY UNDERPINNED BYSCIENCE, TECHNOLOGY AND OUR PEOPLE.

The group is a leader in sustainabletechnologies and many of ourproducts enhance the quality of lifefor millions through their beneficialimpact on the environment, healthand wellbeing. Technologyleadership forms the basis ofJohnson Matthey’s strategy to deliversuperior long term growth and wecontinue to invest in R&D to developthe next generation of sustainableproducts for our customers. To us,good performance is not just aboutprofit. It’s about running our businessin the most sustainable andresponsible way and so we haveidentified five elements of sustainabilitywhich have a material impact on ourbusiness. In this report we will updateyou on our progress.

DELIVERINGVALUE

FinancialMust be profitable to be sustainableSustainability initiatives can be cost efficient too

Health and SafetyProtecting employees, customers and communitiesBeneficial products

EnvironmentResponsible operationsBeneficial products

GovernanceWell run businessTransparent reporting

SocialEmployee development and wellbeing, recruitment Supporting communities, safeguarding reputation

Building a Sustainable Business

ANNUAL REPORT & ACCOUNTS

Johnson Matthey

Annual R

eport & Accounts 2012

5th Floor25 Farringdon StreetLondon EC4A 4ABUnited KingdomTel: +44 (0)20 7269 8400Fax: +44 (0)20 7269 8433

2012

VALUEdeveloping products that enhance the quality of life

for millions of people around the world

Go Onlinewww.matthey.comTo view our online annual report

DELIVERING

Johnson Matthey Annual Report & Accounts 2012

Johnson Matthey at a Glance

Environmental Technologies

Emission ControlTechnologies

Process Technologies

Fuel Cells

Environmental Technologies Division’sproducts and services are used globally inapplications which benefit the environment.It supplies catalysts and technologieswhich contribute to pollution control,cleaner fuels, greener power and the moreefficient use of hydrocarbon resources.Its emission control catalysts are fitted toabout one in three cars around the world.

Return on sales excluding 11.3%precious metalsReturn on invested capital (ROIC) 14.2%Capital expenditure £97.1mCapex / depreciation 1.2Average invested capital £1,492mEmployees 5,640

Key Statistics

2009

1,135*

124.3

1,252

120.9

1,566

164.7

1,876

211.8

2010 2011 2012Sales excludingprecious metals

Underlyingoperatingprofit

0

500

1,000

1,500

2,000

£ million

* Excluding inter-segment sales.

Precious Metal Products

Services

Platinum Marketing and DistributionRefining

Manufacturing

Noble MetalsColour Technologies

Catalysts and Chemicals

Precious Metal Products Divisionadds value to precious metals. Its wideranging activities include the marketing,distribution and fabrication of preciousmetals and the manufacture of catalystsand precious metal chemicals. It is alsoa world leading refiner of precious metals,ensuring these valuable materials areefficiently recovered and reused.

Return on sales excluding 34.5%precious metalsReturn on invested capital (ROIC) 58.9%Capital expenditure £31.6mCapex / depreciation 1.4Average invested capital £341mEmployees 2,894

Key Statistics

2009

447*

143.0

454

116.7

541

172.9

582

200.8

2010 2011 2012Sales excludingprecious metals

Underlyingoperatingprofit

0

200

400

600

£ million

Fine Chemicals

API Manufacturing

Macfarlan SmithPharmaceutical Materials and Services

Research Chemicals

Fine Chemicals Division supplies activepharmaceutical ingredients, fine chemicalsand other speciality chemicals to a widerange of pharmaceutical and chemicalindustry customers and research institutesglobally. Its products help relieve pain, treat cancer and other medical conditions,improving the quality of life for many peoplearound the world.

Return on sales excluding 24.5%precious metalsReturn on invested capital (ROIC) 16.7%Capital expenditure £15.8mCapex / depreciation 0.9Average invested capital £418mEmployees 1,090

Key Statistics

2009

215*

49.5

221

55.8

245

56.2

285

69.7

2010 2011 2012Sales excludingprecious metals

Underlyingoperatingprofit

0

100

200

300

£ million

March2007

March2008

March2009

March2011

March2010

March2012

Total accident rate

> 3-day lost timeaccident rate

0

3

6

9

12

2007* 2009 2010 2011 2012

Tonnes CO2

equivalent (’000)Tonnes /£ million sales

0

100

200

300

400

500

0

50

100

150

200

250

300

2008

89.6

37.1

89.5

36.6

86.4

39.0

119.0

46.0

153.7

55.0

2009 20112010 2012Underlying earnings per share

Ordinary dividend per share

0

40

80

120

160

Performance Highlights

* Calendar year.

Johnson Matthey continued its strong performance in 2011/12 withgood growth across all three of its divisions.

Year to 31st March2012 2011 % change

FinancialRevenue £ million 12,023 9,985 +20

Sales excluding precious metals (sales) £ million 2,679 2,280 +17

Profit before tax £ million 409.3 259.32 +58

Total earnings per share pence 148.7 85.22 +75

Underlying1:

Profit before tax £ million 426.0 345.5 +23

Earnings per share pence 153.7 119.0 +29

Dividends per share:

Ordinary pence 55.0 46.0 +20

Special pence 100.0 – –

SocialAverage number of employees 9,914 9,388 +6

Voluntary employee turnover % 6.4 5.6 +1

Training spend per employee £ 335 390 -14

Charitable donations £ thousands 645 517 +25

Health and SafetyGreater than three day accidents per 1,000 employees 2.07 2.992 -31

Total accident rate per 1,000 employees 5.69 7.892 -28

Occupational illness cases per 1,000 employees 3.5 3.5 –

EnvironmentEnergy consumption thousands GJ 4,726 4,749 –

Global warming potential thousand tonnes CO2 equivalent 417 415 –

Total waste tonnes 120,363 113,671 +6

Water consumption thousands m3 2,201 2,076 +6

Total acid gas emissions tonnes SO2 equivalent 444 318 +40

1 Before amortisation of acquired intangibles, major impairment and restructuring charges, profit or loss on disposal of businesses and, where relevant, related tax effects.

2 Restated.

Delivering Superior Valuepence

> Reducing Carbon IntensityTonnes CO2 Tonnes /equivalent (’000) £ million sales

> Safety is a Key Priorityper 1,000 employees

>

The paper in this report contains material sourced from responsibly managed forests, certified inaccordance with the FSC® (Forest Stewardship Council) and is totally recyclable and acid-free.

Fulmar Colour is FSC certified, PEFC certified and ISO 14001 certified showing that it is committedto all round excellence and improving environmental performance is an important part of thisstrategy. Fulmar Colour aims to reduce at source the effect its operations have on the environmentand is committed to continual improvement, prevention of pollution and compliance with anylegislation or industry standards.

Fulmar Colour is a Carbon Neutral Printing Company.

Designed and produced by MAGEEwww.magee.co.ukPrinted by Fulmar Colour

Johnson Matthey is grateful to the following for their help in providing illustrations:

Fruits, page 65 – © Ene | Dreamstime.com

Johnson Matthey Annual Report & Accounts 2012

Johnson Matthey at a Glance

Environmental Technologies

Emission ControlTechnologies

Process Technologies

Fuel Cells

Environmental Technologies Division’sproducts and services are used globally inapplications which benefit the environment.It supplies catalysts and technologieswhich contribute to pollution control,cleaner fuels, greener power and the moreefficient use of hydrocarbon resources.Its emission control catalysts are fitted toabout one in three cars around the world.

Return on sales excluding 11.3%precious metalsReturn on invested capital (ROIC) 14.2%Capital expenditure £97.1mCapex / depreciation 1.2Average invested capital £1,492mEmployees 5,640

Key Statistics

2009

1,135*

124.3

1,252

120.9

1,566

164.7

1,876

211.8

2010 2011 2012Sales excludingprecious metals

Underlyingoperatingprofit

0

500

1,000

1,500

2,000

£ million

* Excluding inter-segment sales.

Precious Metal Products

Services

Platinum Marketing and DistributionRefining

Manufacturing

Noble MetalsColour Technologies

Catalysts and Chemicals

Precious Metal Products Divisionadds value to precious metals. Its wideranging activities include the marketing,distribution and fabrication of preciousmetals and the manufacture of catalystsand precious metal chemicals. It is alsoa world leading refiner of precious metals,ensuring these valuable materials areefficiently recovered and reused.

Return on sales excluding 34.5%precious metalsReturn on invested capital (ROIC) 58.9%Capital expenditure £31.6mCapex / depreciation 1.4Average invested capital £341mEmployees 2,894

Key Statistics

2009

447*

143.0

454

116.7

541

172.9

582

200.8

2010 2011 2012Sales excludingprecious metals

Underlyingoperatingprofit

0

200

400

600

£ million

Fine Chemicals

API Manufacturing

Macfarlan SmithPharmaceutical Materials and Services

Research Chemicals

Fine Chemicals Division supplies activepharmaceutical ingredients, fine chemicalsand other speciality chemicals to a widerange of pharmaceutical and chemicalindustry customers and research institutesglobally. Its products help relieve pain, treat cancer and other medical conditions,improving the quality of life for many peoplearound the world.

Return on sales excluding 24.5%precious metalsReturn on invested capital (ROIC) 16.7%Capital expenditure £15.8mCapex / depreciation 0.9Average invested capital £418mEmployees 1,090

Key Statistics

2009

215*

49.5

221

55.8

245

56.2

285

69.7

2010 2011 2012Sales excludingprecious metals

Underlyingoperatingprofit

0

100

200

300

£ million

March2007

March2008

March2009

March2011

March2010

March2012

Total accident rate

> 3-day lost timeaccident rate

0

3

6

9

12

2007* 2009 2010 2011 2012

Tonnes CO2

equivalent (’000)Tonnes /£ million sales

0

100

200

300

400

500

0

50

100

150

200

250

300

2008

89.6

37.1

89.5

36.6

86.4

39.0

119.0

46.0

153.7

55.0

2009 20112010 2012Underlying earnings per share

Ordinary dividend per share

0

40

80

120

160

Performance Highlights

* Calendar year.

Johnson Matthey continued its strong performance in 2011/12 withgood growth across all three of its divisions.

Year to 31st March2012 2011 % change

FinancialRevenue £ million 12,023 9,985 +20

Sales excluding precious metals (sales) £ million 2,679 2,280 +17

Profit before tax £ million 409.3 259.32 +58

Total earnings per share pence 148.7 85.22 +75

Underlying1:

Profit before tax £ million 426.0 345.5 +23

Earnings per share pence 153.7 119.0 +29

Dividends per share:

Ordinary pence 55.0 46.0 +20

Special pence 100.0 – –

SocialAverage number of employees 9,914 9,388 +6

Voluntary employee turnover % 6.4 5.6 +1

Training spend per employee £ 335 390 -14

Charitable donations £ thousands 645 517 +25

Health and SafetyGreater than three day accidents per 1,000 employees 2.07 2.992 -31

Total accident rate per 1,000 employees 5.69 7.892 -28

Occupational illness cases per 1,000 employees 3.5 3.5 –

EnvironmentEnergy consumption thousands GJ 4,726 4,749 –

Global warming potential thousand tonnes CO2 equivalent 417 415 –

Total waste tonnes 120,363 113,671 +6

Water consumption thousands m3 2,201 2,076 +6

Total acid gas emissions tonnes SO2 equivalent 444 318 +40

1 Before amortisation of acquired intangibles, major impairment and restructuring charges, profit or loss on disposal of businesses and, where relevant, related tax effects.

2 Restated.

Delivering Superior Valuepence

> Reducing Carbon IntensityTonnes CO2 Tonnes /equivalent (’000) £ million sales

> Safety is a Key Priorityper 1,000 employees

>

The paper in this report contains material sourced from responsibly managed forests, certified inaccordance with the FSC® (Forest Stewardship Council) and is totally recyclable and acid-free.

Fulmar Colour is FSC certified, PEFC certified and ISO 14001 certified showing that it is committedto all round excellence and improving environmental performance is an important part of thisstrategy. Fulmar Colour aims to reduce at source the effect its operations have on the environmentand is committed to continual improvement, prevention of pollution and compliance with anylegislation or industry standards.

Fulmar Colour is a Carbon Neutral Printing Company.

Designed and produced by MAGEEwww.magee.co.ukPrinted by Fulmar Colour

Johnson Matthey is grateful to the following for their help in providing illustrations:

Fruits, page 65 – © Ene | Dreamstime.com

Johnson Matthey Annual Report & Accounts 2012

>DeliveringValue

1

CAUTIONARY STATEMENT

The Business Review and certain other sections of this annual report contain forward looking statements that are subject to risk factors associatedwith, amongst other things, the economic and business circumstances occurring from time to time in the countries and sectors in which the groupoperates. It is believed that the expectations reflected in these statements are reasonable but they may be affected by a wide range of variableswhich could cause actual results to differ materially from those currently anticipated.

This annual report aims to demonstrate how we deliver superiorvalue for our stakeholders. It combines our financial, social, health andsafety, environmental and governance performance into one documentand reflects the five elements of sustainability which we believe have amaterial impact on our business.

Consequently…

Our 2012 Annual Report and Accounts is divided into eight sections:

Contents

Overview: introduces Johnson Matthey and summarises our performance in the year. It also outlines the group’s strategy fordelivering superior value.

Financial: details the financial performance of the group and its three divisions during the year.

Social: highlights initiatives involving our people, our communities andother stakeholder groups. It also contains performance data relating toemployees and community investment.

Health and Safety: outlines our performance in the year, our approach to health, safety and product stewardship and the programmes we havein place to drive continuous improvement.

Environment: provides more detail on the impact of our business on theenvironment. It details the environmental performance of our operationsin the year and highlights the beneficial impact of our products.

Governance: introduces our board of directors and details the corporategovernance structures that are in place to ensure we manage ourbusiness in a responsible and transparent way.

Accounts: includes the consolidated and parent company accountsand related notes, as well as the statement on responsibility of directorsand the independent auditor’s report on the financial accounts.

Other Information: contains the assurance statement on our non-financialdata and a checklist against the Global Reporting Initiative. It alsoprovides further information for shareholders, a glossary and an indexto help the reader locate information in the relevant sections.

In addition to this integrated Annual Report and Accounts we publish case studies andfurther information on sustainability on the internet. Links to this supplementary informationare highlighted in the relevant chapter of this report with the symbol.

Johnson Matthey Annual Report & Accounts 20122

Go Onlinewww.matthey.com/AR12To view our online annual report

3

Report of the DirectorsBusiness Review

What we mean by Delivering ValueOverview:>

Johnson Matthey at a Glance (inner flap) Performance Highlights 2011/12 (inner flap) 6 Chairman’s Statement 8 Chief Executive’s Statement 10 Our Business 12 Our Strategy 16 Group Performance Review 18 Group Key Performance Indicators 20 Risks and Uncertainties

Linking profitability and sustainabilityFinancial:>

26 Financial Review of Operations 26 Environmental Technologies 34 Precious Metal Products 40 Fine Chemicals 43 Financial Review 47 Treasury Policies 47 Liquidity and Going Concern

Investing in our people and ourcommunities around the world

Social:>

50 Social Performance Summary 50 Stakeholder Engagement 52 Building a Sustainable Workforce 56 Community Investment 58 Social Aims and Targets

A key priorityHealth and Safety:>

62 Health and Safety Performance Summary 62 Managing Performance and Driving Continuous Improvement 62 Health Performance in 2011/12 63 Sustainable Health Improvement Priorities for 2012/13 63 Safety Performance in 2011/12 64 Safety Priorities for 2012/13 64 Product Stewardship 65 Product Stewardship Performance in 2011/12 65 Product Stewardship Priorities for 2012/13 66 Animal Testing 67 Responsible Care 67 Regulatory Matters

Environment:>

70 Environmental Performance Summary 70 Managing Performance and Driving Continuous Improvement 70 Environmental Performance in 2011/12 74 Environmental Aims and Targets 75 Biodiversity

Managing our business in the right wayGovernance:>

78 Letter from the Chairman 79 Governance and Sustainability 82 Board of Directors 84 Corporate Governance Report100 Other Statutory Information105 Nomination Committee Report106 Audit Committee Report108 Remuneration Report

The details behind ourfinancial performance

Accounts

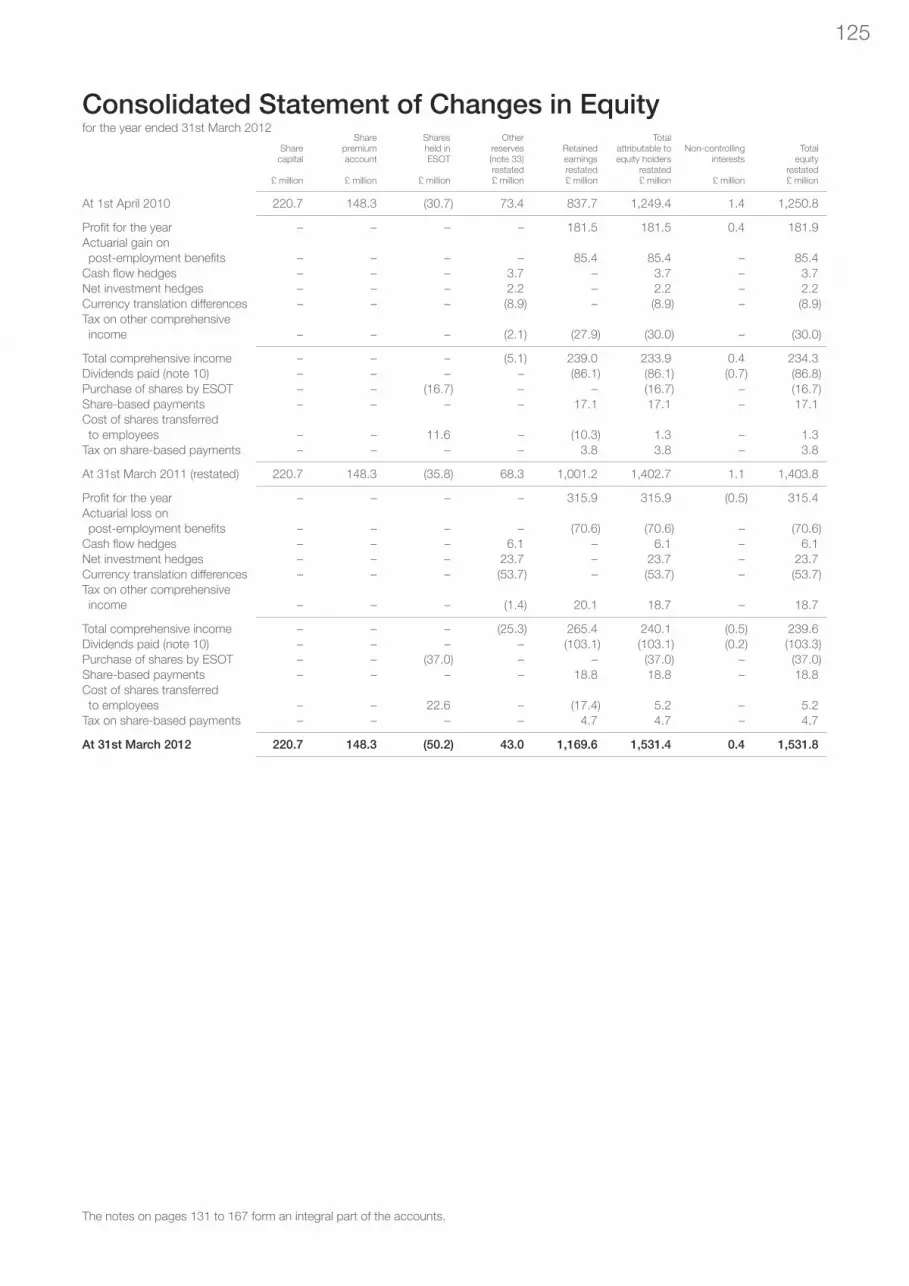

120 Responsibility of Directors121 Independent Auditor’s Report122 Consolidated Income Statement122 Consolidated Statement of Total Comprehensive Income123 Consolidated and Parent Company Balance Sheets124 Consolidated and Parent Company Cash Flow Statements125 Consolidated Statement of Changes in Equity126 Parent Company Statement of Changes in Equity127 Accounting Policies131 Notes on the Accounts

Shareholdings, summaries,the glossary and index

Other Information

170 Five Year Record – Financial Data171 Five Year Record – Non-Financial Data172 Basis of Reporting – Non-Financial Data173 Verification and Assurance – Non-Financial Data174 Shareholder Information176 Global Reporting Initiative (GRI) Summary177 Glossary of Terms178 Index179 Financial Calendar 2012/13180 Company Details

Governance

Reducing the impact of our operations anddeveloping beneficial products

Johnson Matthey Annual Report & Accounts 2012Report of the Directors – Business ReviewOverview

4

What wemean byDeliveringValue

Contents

6 Chairman’s Statement 8 Chief Executive’s Statement 10 Our Business 12 Our Strategy 16 Group Performance Review 18 Group Key Performance Indicators 20 Risks and Uncertainties

OverviewThis section introduces Johnson Matthey and summarises our performance in the year. It also outlines the group’s strategyfor delivering superior value.

. The washcoat preparation area at our Smithfield facility in Pennsylvania, USA.

. Inspecting heavy duty diesel catalysts. . State of the art technologies at Smithfield formanufacturing heavy duty diesel catalysts.

> Leading the Way inHDD CatalystsThe market for catalysts to control harmfulemissions from heavy duty diesel (HDD)vehicles, such as trucks and buses, is growing rapidly driven by tightening legislationfor both on road and non-road applicationsaround the world.

Johnson Matthey has developed worldleading catalyst technology for HDD applicationsand, as a result, has established a very strongmarket position thanks to sustained investmentin R&D and state of the art manufacturingfacilities, including at our plant in Smithfield,USA (pictured). 2011/12 marked anotherstrong year for Johnson Matthey’s HDDcatalyst business where sales grew by 48%to £438 million and operating profit morethan doubled.

New and tighter legislation will imposeincreasing technical demands on the emissioncontrol catalyst systems required for HDDapplications and technologies must cope withcontrolling oxides of nitrogen and particulatematter to extremely low levels. This inevitablyresults in increasing value for JohnsonMatthey. Furthermore, as legislation extendsto cover more vehicles and additional regionsof the world, the group’s commitment tomaintaining technology leadership in this fieldpositions us well to benefit from future growthin demand.

Delivering Value

Chairman’s Statement

In my first statement as Chairman, I amdelighted to report that Johnson Mattheyperformed very strongly in 2011/12. Duringthe year the company benefited from gooddemand for its products as well as robustprecious metal prices, particularly in thefirst half. The group’s continuing strongperformance is enabled by our long terminvestment in research and development(R&D) and our strategy of organic growth,complemented by bolt-on acquisitions.Together these have enabled the companyto achieve leading positions in a number of rapidly growing markets. The result isanother year of strong growth in underlyingearnings per share, which were up 29%to 153.7 pence.

The group’s cash generation has also been strong: at 31st March 2012 the group’s net debt (including post taxpension deficits) to EBITDA ratio was1.0 times. As a result of this very goodperformance the board has carried outa review of the group’s balance sheetstructure. The outlook for the groupremains strong; we believe it has ampleresources to fund forecast capitalexpenditure and a further increase in R&D.The board is therefore recommendinga special dividend to shareholders of100 pence per share, which represents atotal payment of approximately £212 million.

Sustainability continues to be a keyelement of the company’s strategy andI am very pleased to be introducing this,Johnson Matthey’s first ‘integrated’ annualreport, which describes all aspects of ourfinancial and non-financial performance.I believe that this reflects both our valuesand our determination to build a sustainablebusiness, as well as communicating to allof our stakeholders our commitment tosustainable growth. In this year’s annualreport we have also included morecomprehensive governance reporting,including in the Corporate GovernanceReport on pages 84 to 99 which formsa key part of the Report of the Directors.

Johnson Matthey Annual Report & Accounts 2012Report of the Directors – Business ReviewOverview

6

Tim StevensonChairman

“Welcome to this, our firstintegrated annual report,which I hope will provide youwith a deeper understandingof the many aspects of ourbusiness, its performance,its long term prospects, itsgovernance and, ultimately,how we deliver value to ourstakeholders.”

This is in light of changes introducedby the UK Corporate Governance Code(the Code), which replaced the CombinedCode on Corporate Governance in June2010. While we reflected certain aspectsof the Code on a voluntary basis in lastyear’s annual report, this year’s CorporateGovernance Report fully reflects a numberof substantial changes in corporategovernance reporting. I hope that thisintegrated annual report will provide youwith a deeper understanding of the manyaspects of our business, its performance,its long term prospects, its governanceand, ultimately, how we deliver value to ourcustomers and to other stakeholders.

I joined the board as ChairmanDesignate in March 2011 and was verypleased to have been appointed asChairman of your company at the close oflast year’s annual general meeting (AGM).

I recognise that an effective boardis central to the long term sustainablesuccess of the company. In the Governancesection of this year’s annual report wedescribe the structures and measures inplace which are designed to ensure itscontinued effectiveness and we reviewhow the principles of the Code have beenapplied in the year, focusing on the roleand effectiveness of the board. Wedescribe in particular the board andcommittee performance evaluationscompleted last year and underway thisyear. These have been especially importantfor me in my first year as Chairman.

I chair the board at an exciting stageof Johnson Matthey’s development. Notonly are its businesses making excellentprogress, realising the benefits of thecompany’s long term strategy andinvestment in R&D and facilities, but ourSustainability 2017 programme continuesto achieve good progress towards meetingits objectives and targets. Its focus onimproving resource efficiency in ourmanufacturing operations and developingmore sustainable products for ourcustomers should make a majorcontribution to growth in the years ahead.

Since joining the company, I have meta number of Johnson Matthey’s majorshareholders and received positive feedbackon the company and its strategy. I am keento maintain regular dialogue with ourshareholders and look forward to meetingmany of you at this year’s AGM when therewill be an opportunity for us to discuss thecompany’s business and achievements.

This is my opportunity to thank mypredecessor, Sir John Banham, for hisstrong leadership of the board and manyefforts on behalf of the company overthe five years that he was Chairman.John brought to the board his wideranging experience of both corporate andpublic sector leadership and governance.He was also a tireless ambassador for thecompany and an eloquent and enthusiasticadvocate of its achievements andpotential. On behalf of all of us at JohnsonMatthey, I thank him for his importantcontribution and wish him all the very bestfor his retirement.

Sir Thomas Harris retires from theboard at the close of this year’s AGMhaving served as a non-executive directorsince April 2009. I would like to thank Tomfor his wise counsel and contribution to thework of the board over the last three yearsand wish him the best for the future.

There is no doubt that our mostimportant investment is that which wemake in our people. The training,development and, most importantly, thewellbeing of our employees is vital to thesuccess of our business. In this respect I am delighted that we have made suchgood progress towards achieving ourtarget of zero accidents during the year.

Since joining the company I have metmany of our employees around the world.I have been repeatedly impressed by theirenthusiasm, professionalism and dedicationat every level of the organisation. Onbehalf of all our stakeholders, I thank ouremployees for their hard workingcontribution to another successful year.

To conclude: as you will read in thisannual report, Johnson Matthey is in verygood shape and continues to make goodprogress in delivering value to itsshareholders and other stakeholders.The drivers of our business remain firmlyin place. Despite current global economicuncertainties, I am confident that we willcontinue to benefit in the years ahead fromour continuing and increasing investmentin R&D, our emphasis on efficientmanufacturing infrastructure and thequality of our people around the world.

Tim StevensonChairman

7

Chief Executive’s Statement

Johnson Matthey Annual Report & Accounts 2012Report of the Directors – Business ReviewOverview

8

I am very pleased to say that JohnsonMatthey had a good year in 2011/12,continuing our strong financial performanceand making good progress towardsimproving our environmental, health andsafety performance. We have alsoincreased our focus on developing ourpeople and on defining and disseminatingour culture, both of which are key to thesuccess of our growing global business.The year has also seen us making goodprogress on our strategy of deliveringsuperior value to our stakeholders throughtechnology leadership, continuing toincrease our investment in research anddevelopment and in state of the artmanufacturing facilities around the world.

The year saw good growth across allthree of our divisions. Sales excludingprecious metals (sales) were substantiallyahead of last year, up 17% at £2.7 billion,and the rate of growth in underlyingoperating profit was higher, at 23%.

Our Environmental TechnologiesDivision had a very good year. Its EmissionControl Technologies (ECT) businessbenefited from good growth in sales of lightduty catalysts, ahead of growth in globalvehicle production, and a substantialincrease in demand for heavy duty dieselcatalysts, particularly in North America. OurProcess Technologies business performedwell boosted by another excellent yearfrom Davy Process Technology (DPT) anda good contribution from our Additivesbusiness (formerly Intercat), which wasacquired in November 2010.

Precious Metal Products Division alsoperformed well, especially in the first sixmonths of the year. After a very strong firsthalf, precious metal prices softened inresponse to concerns over the globaleconomy which adversely impacted thedivision’s Services businesses. ItsManufacturing businesses saw gooddemand across their product range.

Fine Chemicals Division exceeded ourexpectations, delivering excellent results in2011/12, supported by a very strongperformance from its Active PharmaceuticalIngredient (API) Manufacturing businesses.Its global Research Chemicals businessalso grew well in the year.

Neil CarsonChief Executive

“We have made goodprogress this year onour strategy of deliveringsuperior value to ourstakeholders throughtechnology leadership,continuing to increase ourinvestment in research anddevelopment and state ofthe art manufacturingfacilities around the world.”

9

For the group as a whole, revenuewas 20% up on last year at £12 billion and sales were £2.7 billion, 17% higherthan last year. Underlying operating profitwas 23% higher at £450.1 million, whileunderlying profit before tax was also 23% up at £426.0 million. The group’sunderlying return on sales increased to16.8% from 16.1% last year, primarily dueto operational leverage, particularly in ourheavy duty diesel catalyst business, andthe excellent performance from our highermargin DPT business.

Sustainability is a key element of ourstrategy for growth and is well embeddedin all of our businesses and embraced byour employees around the world. Wecontinue to make good progress towardsachieving our Sustainability 2017 Vision viathe challenging targets that we setourselves when we launched it back inDecember 2007. Our sustainability strategyand targets are subject to continuousreview and during the year we have madesome changes to our targets which areoutlined on page 15 of this annual report.In particular we have taken a detailed lookat our commitment to reduce carbonemissions from our operations.

Over the last few years we havegained a much better understanding ofcarbon legislation, markets and emissionsfrom our processes and we have come tothe conclusion that carbon neutrality is notan appropriate target for a growingmanufacturing business like ours. However,we remain committed to driving down ourcarbon emissions as much as is realisticallypossible and with effect from 1st April2012 we have replaced carbon neutralitywith a new target to halve our carbonintensity, relative to our 2007 baselinefigure, by 2017. I believe that this continuesto be a stretching target.

Johnson Matthey is extremely wellplaced to benefit from a combination ofimprovements to the efficiency andenvironmental performance of its ownmanufacturing operations and fromdeveloping new products that bringsignificant sustainability benefits to ourcustomers. Operational improvements andincreased efficiency have undoubtedlybeen making a significant contribution to

the growth and success of the companyin the last few years. Manufacturing is atthe very heart of our business. It is howwe bring our science and technology tolife and deliver what our customers want,when they want it. During the year weestablished and launched a groupwideManufacturing Excellence programme.I believe that this important initiative willbetter equip us to produce high technologyproducts for our customers in the mostsustainable and efficient way and will bringmajor benefits to our business in the yearsahead.

Our people play a vital role in thesuccess of our business, they truly are ourmost valuable resource. Their training anddevelopment and protection of their health,safety and wellbeing have long been, andremain, key priorities. We have continuedto make good progress during the year indeveloping our systems and improvingperformance in these very important areas.

Outlook

After another year of strong growth, thegroup is well positioned for the year ahead.However, once again, it is difficult toassess with any degree of confidence howthe global economy, especially in Europe,will develop in the short term. Thisuncertainty has resulted in a substantialfall in precious metal prices over the lastfew months, despite robust demand.Nonetheless, we remain confident that ourstrong position in markets with structuralgrowth will allow us to make furtherprogress in Environmental Technologiesand Fine Chemicals in 2012/13. This,however, will be offset by a weakerperformance from Precious Metal Products, if precious metal prices remain at current levels.

The outlook for our EnvironmentalTechnologies Division remains positive.Emission Control Technologies shouldbenefit from the continued development ofthe heavy duty diesel catalyst market andanticipated growth in light duty vehicleproduction in North America and Asia.However, we remain cautious about theoutlook for European car and truckmarkets. Notwithstanding that, the removal

of the headwinds in the first half of2011/12 associated with higher rare earthmaterial prices and the Japaneseearthquake should ensure that ECT willperform well in the first six months of thisyear. Process Technologies is also wellplaced for another year of growth,benefiting from the ongoing strongdemand for DPT’s licences and foradditives.

Precious Metal Products Division’sperformance is, as we have outlinedbefore, more dependent upon preciousmetal prices and their recent falls, ifmaintained, will impact the division’sServices businesses. In addition, thesebusinesses suffer from relatively toughcomparatives as metal prices and refiningintakes were strong in the first half of2011/12. Therefore, if precious metalprices remain at current levels, theperformance of the Services businesses inthe first half of 2012/13 will be significantlylower than in 2011/12. The Manufacturingbusinesses are expected to make progressduring 2012/13.

The performance of our FineChemicals Division in 2011/12 exceededour expectations and the strong drivers forthe business remain in place. Continueddemand for our existing APIs, theintroduction of new products and furthergeographic expansion of our ResearchChemicals business’ footprint shouldensure that we have another strong year.

In the longer term, we are continuingto expand our manufacturing capacityaround the world and to invest in R&D.Together, this should enable us to provideproducts that satisfy tightening globallegislation and that meet the growingdemand from our customers. We havestrong positions in markets that will seestructural growth over the next few yearsand, despite current global economicuncertainties, we are confident of thegroup’s continuing growth potential.

Neil CarsonChief Executive

Our Business

Johnson Matthey Annual Report & Accounts 2012Report of the Directors – Business ReviewOverview

10

Johnson Matthey is a global speciality chemicals company.We have operations in over 30 countries and employ around10,000 people worldwide.

The group is organised into three global divisions: > Environmental TechnologiesRead more on page 26.

> Precious Metal ProductsRead more on page 34.

> Fine ChemicalsRead more on page 40.

> Johnson Matthey is a leader insustainable technologies. We focuson clean air, clean energy and lowcarbon technologies and are expertsin the application and recycling ofprecious metals. We invest in R&Dto develop products that enhancethe quality of life for millions of peoplearound the world.

Wellpositionedfor futuregrowth

11

Europe35%

North America34%

China8%

Rest of Asia11%

Rest of World12%

Sales by Region

A Truly Global CompanyJohnson Matthey sells its productsglobally which provides stability in times ofregional market uncertainty. Year on yearwe are increasing our sales to developingmarkets and expanding our operations tosupport this global growth.

19%Sales in Asia in 2011/12.Read more on pages 26 to 42.

>

>

DELIVERINGVALUE

FinancialMust be profitable to be sustainableSustainability initiatives can be cost efficient too

Health and SafetyProtecting employees, customers and communitiesBeneficial products

EnvironmentResponsible operationsBeneficial products

GovernanceWell run businessTransparent reporting

SocialEmployee development and wellbeing, recruitment Supporting communities, safeguarding reputation

Building a Sustainable Business

£128.6mGross spend on R&D in 2011/12.Read more on pages 14 and 15.

Light dutyvehicles

39%

Heavy duty diesel vehicles17%

Pharmaceutical13%

Petrochemical15%

Precious metal services

6%

Other10%

Sales by Key Market

Focused on Key MarketsJohnson Matthey is focused on its keymarkets where we can add value throughapplying our expertise in catalysis andplatinum group metal chemistry. Thisapproach enables us to maintaindifferentiation through technology andachieve leading industry positions withhigh margin products.

48%Growth in heavy duty diesel catalyst sales in2011/12. Read more on pages 30 and 31.

>

>

>£28mSavings from sustainability initiatives to date.Read more on pages 13 to 15 and page 17.

Environment55%

Health10%

Resourceefficiency

21%

Social / lifestyle5%

Other9%

Sales by Area of Beneficial Impact

A Leader in Sustainable TechnologiesJohnson Matthey is focused on developingproducts that deliver sustainability benefitsto our customers and to society. Today,some 86% of the group’s sales representproducts and services which providesustainability benefits through their positiveimpact on the environment, resourceefficiency or our health.

86%Sales from products providing sustainability benefitsin 2011/12. Read more on pages 26 to 42.

>

>

60%Employees working in manufacturing operations.Read more on pages 14 and 15.

A Vision for SustainabilityOur goal at Johnson Matthey is to growour business – but to grow it sustainably.Sustainability is a key element of our strategyfor continued growth and we believe thatthe resource efficient, environmentallyresponsible manufacturing of products thatoffer sustainability benefits for our customerscan leverage commercial advantage for thegroup and deliver superior value.

All across the group, employees areengaged in sustainability programmesfocused on designing and manufacturingour products more efficiently using fewerresources and on developing improved,more efficient products for our customers.

Read more on page 13.

Investing in R&DAt Johnson Matthey, we invest heavily inresearch and development (R&D). Werecognise that this investment is vital if weare to realise new market opportunitiesover the years ahead. Our ability toinnovate and differentiate throughtechnology underpins our future success.

Sustainability 2017Sustainability 2017 is Johnson Matthey’svision for building a sustainable businessand includes challenging targets to supportfuture growth. We aim to double ourunderlying earnings per share while cuttingcarbon intensity by half, achieving zerowaste to landfill and halving the keyresources that we consume per unit ofoutput by 2017, the 200th anniversaryof the company’s foundation.

Manufacturing ExcellenceManufacturing is the way we bring ourscience to life and our ManufacturingExcellence programme is focused onensuring we run our manufacturingoperations with the highest efficiency.Through Manufacturing Excellencewe aim to boost efficiency, reducemanufacturing costs, develop our peopleand support delivery of our Sustainability2017 targets.

There are five major themes directing Johnson Matthey’s strategy:

Focus on leading edge catalysisWe will continue to focus upon the science of catalysis which underpins the majority of Johnson Matthey’s products andenables the group to develop high performance solutions for our customers.

Differentiation through technologyEnhanced investment in R&D in our core markets will enable the group to provide the very best products and maintain acompetitive edge.

Strong position in platinum group metalsAround 70% of Johnson Matthey’s businesses involve platinum group metals (pgms) and we will continue to apply ourexpertise in exploiting their chemical and physical properties to deliver high technology added value products.

Organic growthOrganic growth remains our primary focus however the group will make bolt-on acquisitions where they will accelerate thedelivery of our strategy.

New business developmentWe will increase our investment in new markets and sectors to target further growth from areas that are aligned with thegroup’s technological expertise and commercial interests.

Delivering superior long termgrowth through technology leadership

OurStrategicIntent:

Focus on leading edge catalysis

Differentiation through technology

Strong position in platinum group metals

Organic growth New business development

Our Strategy:

Supported by: Globaldrivers Sustainability R&D

ManufacturingExcellence

Our peopleand culture

In late 2010 the group reviewed its strategy. This review involved adetailed examination of the group’s past performance, its keystrengths and the attributes that make it successful. Globalmegatrends impacting the world around us that will drive growthfor the company were considered and the key strategicopportunities arising from these were identified. From this, thegroup’s strategic direction for the next ten years was defined.

Read more on the strategy review process onpages 8 to 13 of our 2011 Annual Report andAccounts or online at www.matthey.com/AR11.

Our Strategy

Johnson Matthey Annual Report & Accounts 2012Report of the Directors – Business ReviewOverview

12

> Johnson Matthey’s strategic intentis to deliver superior long term growththrough technology leadership. For us,delivering ‘superior long term growth’means growing our business aheadof the underlying growth rates of ourkey markets.

Strategicintent

13

Global Drivers Impacting the Chemical Industry

Johnson MattheyActivities

Industry Sector GLOBAL DRIVERS Johnson MattheyActivities

Industry Sector

Emissioncontrol catalysts

Obscurationenamels

Pharma-ceuticals

Agriculturalchemicals

Emissioncontrol

Clean fuel

Low carbon

PgmsPetrochemicalcatalysts andprocesses

Gas / coal to productstechnology

CatalystsPgm

refining

Automotive Electronics

Construction Bulkchemicals

Population Growth

Urbanisation

Increasing Wealth

Health and Nutrition

Ageing Population

Natural Resource Constraints

Environmental Factors

Climate Change

Regulation

Energysecurity

Alternativeenergy

Resourceefficiency

Recycling

APIsMedical

components

Pgm catalysts

Ammoniasynthesis andnitric acidcatalysts

Fine chemicals

Emissioncontrolcatalysts

Abatementtechnologies

Hydrogencatalysts

Purificationproducts

Fuel cellsCarbon

capture andstorage (CCS)

>

>

<

<

>

>

<

<

There are five fundamental key enablers toour strategy. We now examine each ofthese in more detail to understand theimpact they have on our business and theirrole in enabling future growth.

1. Global Drivers that Support FutureGrowthThere are four major global driverswhich we believe have a major impacton Johnson Matthey’s business:

> Environmental factors, climatechange, regulation

> Natural resource constraints

> Population growth, urbanisation,increasing wealth

> Health and nutrition, ageingpopulation

The figure below illustrates howthese macro level trends impact theindustries into which Johnson Mattheysupplies its products and technologies.All four global drivers provideopportunities for growth in many ofour businesses. For example:

• Projected population growthrates and increasing urbanisationand wealth, particularly inemerging markets, will drive anincrease in the number of carson our roads and therefore linksthrough to growth in JohnsonMatthey’s automotive emissioncontrol catalyst business.

• Projections on how naturalresources will become moredepleted provide estimates ondemand for recycling which inturn will benefit the group’s PgmRefining business.

These global level trends alsooffer opportunities for the group toleverage its expertise in catalysis andplatinum group metals to delivergrowth across its businesses, aheadof underlying market rates.

2. A Vision for SustainabilitySustainability is a key element of ourstrategy for future growth where theresource efficient, environmentallyresponsible manufacturing of hightechnology products that deliversustainability benefits can leveragecommercial advantage for the group.

The group’s Sustainability 2017Vision, launched in December 2007,sets out our direction and aspirationsfor building a more sustainablebusiness. Our long term sustainabilitystrategy is underpinned by twobusiness drivers, five key elementsand six sustainability targets.

Two Business DriversThere are two key business driversfor sustainability which engenderresponsible business practices andsupport future growth. The first

focuses on our internal operationsand on designing and manufacturingour products more efficiently usingfewer resources. This approach helpsus to reduce our costs and at thesame time reduces our impact on theplanet. The second driver concernsour products and services andfocuses on developing improved,more efficient solutions for ourcustomers. By doing this we canenhance our customers’ performanceand improve their sustainabilityfootprint which, in turn, will improveour competitiveness. Together thesedrivers support the development ofproducts and services which have a beneficial impact on the planet, be it through health, social orenvironmental improvements.

Five Key ElementsGrowing our business throughsustainability is not only about ouroperations and products. We arealso committed to best practice ingovernance, to creating a positiveworking environment for employeesand to being a responsible partnerfor our customers, suppliers,communities and other stakeholders.As such, we manage sustainabilityacross the group according to fiveelements: financial; governance; social;health and safety; and environment.Delivering good performance in all fiveareas is vital to our long term success.

Six Sustainability TargetsOur Sustainability 2017 Vision issupported by six challenging targetsas illustrated in the figure above. Ourprogress towards them in 2011/12 issummarised on page 17 and furtherdetails are provided in the Financial,Social, Health and Safety andEnvironment sections of this report.

Read more on sustainabilityat Johnson Matthey atwww.matthey.com/sustainability.

3. Research and DevelopmentContinued investment in R&Dunderpins the future growth ofJohnson Matthey. It is this investment,together with our ability to recruit themost talented scientists, that willensure we maintain the expertise andleadership in the science of catalysis,materials chemistry and pgms thatdrive the development of hightechnology products andmanufacturing processes.

Around 1,200 of our employeeswork in R&D representing around12% of the total workforce andinclude many highly skilled scientistsand engineers. Around 80% of ourR&D staff work within the group’sbusinesses in dedicated R&D andtechnical centres around the world.In our businesses, work is mainlyfocused on delivery of shorter termbusiness specific projects or toaddress particular marketdevelopments or customer needs.

Alongside these activities,Johnson Matthey also has centralcapability on strategic R&D, locatedat two Technology Centres, whichworks on behalf of all of the group’sbusinesses.

We maintain a close link betweenour central R&D activities and thedevelopment work carried out directlyby Johnson Matthey’s businesses.This interaction is key in ensuring the rapid transfer of technology tosupport the continued development ofinnovative new products and servicesfor our customers. Examples of ourcurrent projects are highlighted as‘Innovation in Action’ case studiesthroughout this report.

As previously described, majorglobal drivers provide significantopportunities for Johnson Mattheyto grow and develop its existingbusiness areas over the years aheadand R&D will play an important role inrealising these opportunities.

In 2011/12 Johnson Mattheyincreased its gross investment in R&D by 17% to £128.6 million.

Read more on R&D atJohnson Matthey atwww.matthey.com/innovation.

4. Manufacturing ExcellenceManufacturing is a key contributor toJohnson Matthey’s success and willunderpin our growth in the future. It isa major part of our business in terms ofthe group’s global spend and providesjobs for 60% of our employees.Improving our manufacturingperformance can therefore have asignificant impact on our business.

The 2010/11 strategic reviewidentified that there were opportunitiesfor us to improve our operations andenhance our competitiveness.

Manufacturing Excellence is along term investment in our people,manufacturing processes, engineeringand technology. Lean principles arebecoming integrated at all sites toincrease manufacturing efficiency andimprove overall performance. Technicalcentres of excellence are beingdeveloped to provide opportunitiesfor manufacturing teams around theworld to trial and test new equipment.Engineering teams are working toidentify and develop best practice forour key processes.

The programme offers opportunitiesfor us to increase efficiency, reduce ourcosts, capture our global expertise andimprove our capacity with minimumcapital expenditure.

Our Strategy continued

Johnson Matthey Annual Report & Accounts 2012Report of the Directors – Business ReviewOverview

14

CentralResearch

21%

EnvironmentalTechnologies

61%

PreciousMetal

Products13%

FineChemicals

5%

Research and DevelopmentEmployees

Six Sustainability Targets (from April 2012)

At least double earnings per share

Halve carbon intensity

Achieve zero waste to landfill

Halve key resources consumed per unit of output

Reduce annual incidence of occupationalillness cases by at least 30% over the five yearsto 2013/14

Achieve a zero ‘greater than three day accidents’safety target

Innovation in ActionRead more on our R&D activities throughoutthis annual report:> Staying Ahead of the

Legislation page 29> Deeper Knowledge of

NOx Removal Catalysts page 30> An Insight on the Inside page 32> Looking Inside a Fuel Cell page 33> Sustainable Catalysts to

Replace Mercury page 39

15

5. People and CultureRecruiting the right people, developingthem and providing an environmentwhich motivates them to contributeand stay with the company isfundamental to the group’s long termperformance. A ten year humanresources strategy, developedalongside the group strategy, isfocused on ensuring we can recruit,retain and develop the highly skilledpeople that will be needed to supportour global growth.

The group recognises that ourpeople and culture are a particularstrength and, although the culture ofan organisation is not easy to define,there is a distinctive culture inJohnson Matthey, irrespective ofdivision, business, function orgeographic location. Sustaining andintegrating our culture as we growthe business is a challenge we areembracing on a global scale.

Progress in 2011/12 andFuture Developments

Having established and communicatedits ten year strategy in 2010/11, thegroup has now focused on theprocess of embedding the strategyand on its delivery. During the year, allbusinesses were required to reviewand report on their long term strategicplans and key developments werediscussed.

As a result of the strategic review,the group concluded that it wouldplace more emphasis on newbusiness development and work isnow underway to identify newopportunities and leverage our R&Dexpertise to drive growth. A team hasbeen established, tasked with findingnovel applications outside our currentproducts and markets but which alignwith our technology bases and widercapabilities. A rigorous market basedapproach has been adopted andduring 2011/12, two main areas wereexplored. Opportunities within thewater industry were investigated anda number of potential areas wereidentified where Johnson Matthey’stechnology and capabilities could beapplied. The team also looked at theimplications of the introduction ofelectric automotive powertrains,considering a range of optionsincluding battery materials and othertechnologies. This has identified arange of possible new businessactivities for the company. As a result,we have formed a team who aredeveloping and executing the group’splans to address these markets. It isstill early days, but we hope to makefurther progress during 2012/13.

Two additional sectors will beinvestigated during the year. This workis consistent with our overall objectiveof developing a new business withsales of more than £200 million withinten years.

Work has commenced this yearto explore how we can moreeffectively articulate and communicatethe group’s culture and values. Thiswill continue in 2012/13 and theiralignment with employee behavioursand performance management will beexplored further.

During 2011/12 the grouplaunched its global ManufacturingExcellence programme to support itsstrategic intent. Work will continue toimplement and embed theprogramme and from the start of the2012/13 financial year, performanceagainst a number of key metrics willbe reported by all manufacturing siteson a monthly basis and used internallyto track progress and direct actions.

As discussed in last year’s annualreport, in February 2011 the groupreviewed its sustainability strategy toassess progress and ensure that itstargets were still appropriate tobusiness needs. The reviewconcluded that there was no need toradically change direction, buthighlighted areas where we couldevolve our strategy to better supportthe future growth of the company.These were further investigated during2011/12 and as a result, twoamendments to our Sustainability2017 targets have been introduced.

From April 2012 our target toachieve ISO 14001 at all majormanufacturing facilities has beenremoved as all sites included in theoriginal target have now achieved this.This requirement has now beenincluded in our environment, healthand safety (EHS) management system.

In 2012/13 we will continue toreview the appropriateness of ourtarget to achieve zero waste to landfill.We have made steady progresstowards this target but recognise thatwaste to landfill is only a proportion ofthe waste generated by our operations.Therefore we will consider how wecan broaden this target to encompass

a wider definition of waste andresource efficiency with an overall goalof reducing waste across our business.

One aspect of the strategy weconsidered in detail was ourcommitment to reduce carbonemissions from our operations. Thefeedback from employees hadsuggested that our aspirational targetto achieve carbon neutrality was aconcept that was difficult to understandand was causing confusion internally.Furthermore, over four years into oursustainability programme, we have amuch greater understanding andknowledge of carbon legislation,markets and emissions from ourprocesses. Consequently, we nowdo not believe that carbon neutralityis an appropriate target for us.

As a manufacturing business anda business that is growing, this targetcannot be achieved without purchasingcarbon offsets. We have conducted alot of research into offsets and are notconvinced they offer an appropriateway of mitigating our carbon emissions.We have therefore concluded this isnot an approach we wish to take.

As a group we remain committedto driving down our carbon emissionsas far as is realistically possible andthat any increase will be at a rate thatis below the rate of business growth.

To support this commitment,from 1st April 2012 we have replacedour target to achieve carbon neutralitywith a new target to halve our carbonintensity by 2017, relative to our 2007baseline figure. Our carbon intensity isthe group’s global warming potential(GWP) per £ million of sales excludingprecious metals (sales). In 2007, ourcarbon intensity was 294 tonnes CO2

equivalent / £ million sales and so wehave set a target to halve our carbonintensity to 147 tonnes CO2 equivalent/ £ million sales by 2017.

Many of our products alreadyreduce greenhouse gas emissions forour customers and we continue tofocus on the development of productsthat mitigate climate change. Our ownlife cycle experts group is working tobetter quantify the in service benefitsof our products.

Delivering ValueRead more about how we deliver value throughout this annual report:> Leading the Way in HDD Catalysts pages 4 and 5> Davy Process Technology pages 24 and 25> Growing Our People pages 48 and 49> Investing in New Capacity pages 60 and 61> Developing the Next Generation of Sustainable Products pages 68 and 69> Supporting Our Strategy in Fine Chemicals pages 76 and 77> Customer Focus at Colour Technologies pages 118 and 119> Managing Metals for Our Businesses and Our Customers pages 168 and 169

Johnson Matthey has delivered another year of strong growth witha good contribution from all of its divisions. This performance wasparticularly enhanced by our leading position in heavy duty dieselcatalysts, a very strong year from Davy Process Technology (DPT) andexcellent progress in our North American API Manufacturing business.

Sales

Revenue for the year ended 31st March 2012 was 20% up on lastyear at £12.0 billion. The group’s sales were 17% higher than last yearat £2.7 billion. Translated at constant exchange rates, revenue for theyear was 21% ahead and sales grew by 18%.

Operating Profit

For the group as a whole, underlying operating profit (beforeamortisation of acquired intangibles, major impairment and restructuringcharges) was 23% higher than last year at £450.1 million, whileunderlying profit before tax was also 23% up at £426.0 million. Thegroup’s underlying return on sales increased to 16.8% from 16.1%last year, primarily due to operational leverage, particularly in ourheavy duty diesel catalyst business, and the excellent performancefrom our higher margin DPT business.

The performance of the individual businesses is explained in moredetail in the Financial Review of Operations section on pages 26 to 42.

Group Performance Review

Financial Performance

Johnson Matthey Annual Report & Accounts 2012Report of the Directors – Business ReviewOverview

16

Year to 31st March 2012 2011 % change restated

Revenue £ million 12,023 9,985 +20

Sales excluding precious metals (sales) £ million 2,679 2,280 +17

Operating profit £ million 433.4 279.9 +55

Profit before tax £ million 409.3 259.3 +58

Total earnings per share pence 148.7 85.2 +75

Underlying*:

Operating profit £ million 450.1 366.2 +23

Profit before tax £ million 426.0 345.5 +23

Earnings per share pence 153.7 119.0 +29

* Before amortisation of acquired intangibles, major impairment and restructuring charges, profit or loss on disposal of businesses and, where relevant, related tax effects.

Fine Chemicals10%

Precious MetalProducts

21%

EnvironmentalTechnologies

69%

Group Sales by Division

Europe35%

North America34%

China8%

Rest of Asia11%

Rest of World12%

Group Sales by Destination

2009*

EnvironmentalTechnologies

Precious MetalProducts

FineChemicals

2010 2011 20120

500

1,000

1,500

2,000

2,500

3,000

Divisional Sales£ million

2009

EnvironmentalTechnologies

Precious MetalProducts

FineChemicals

2010 2011 20120

100

200

300

400

500

Divisional Underlying Operating Profit£ million

* Excluding inter-segment sales.

Our Progress

Johnson Matthey has made good progresstowards its Sustainability 2017 targets thisyear.

In 2011/12 our financial performancewas strong with underlying earnings pershare (EPS) at 153.7 pence and we believethe group remains on track to achieve itstarget to double underlying EPS from the2007 baseline by 2017. As outlined in thestrategy section on page 15, the group hasamended its target on carbon this year andprogress towards the new target, to halvecarbon intensity, has been very good.Similarly, initiatives across the group’sbusinesses to improve resource efficiencyare paying off and we remain well on trackto achieve our target to halve keyresources per unit of output by 2017.Steady progress is being made to reducethe amount of waste we send to landfill,although year on year waste to landfillincreased in 2011/12, as explained in theEnvironment section on page 72. Work todrive continuous improvement in health andsafety is reflected by the good progress wehave made this year in further reducing ournumber of greater than three day accidentstowards our target of zero accidents, and inmaintaining our incidence of occupationalillness cases below our target.

Further details of the group’sperformance towards its Sustainability 2017targets are explained in the strategy sectionon pages 13 to 15, the Health and Safetysection on pages 60 to 67, theEnvironment section on pages 68 to 75and on the company’s website atwww.matthey.com/sustainability.

Economic Impact and Distributionof Value to Stakeholders

2011/12 marked another strongperformance from Johnson Matthey withgood growth across all three divisions.

The group generated an underlyingoperating profit of £450.1 million andrevenue of £12.0 billion in the year. Of thisrevenue, £9.3 billion represents the value of precious metals in our products whichin many cases is passed directly on to ourcustomers. As a result, we may see quitelarge year on year swings in the revenue linedepending on the movements in the marketprices of precious metals during the year.Sales excluding the value of precious metalsis thus a better measure of the salesgrowth in our business.

Of the £12 billion revenue, the costsof goods and services were £11 billion(including £9 billion for precious metals)while our own operations created anestimated £1 billion in underlying addedvalue.

Employees received the largest shareof this underlying added value, some 49%of the total, reflecting the fact that JohnsonMatthey is a high technology companyemploying many highly skilled employeesacross the globe. Amounts payable toproviders of capital, i.e. our shareholdersand financiers, were 35% of the total(including the proposed special dividend of£212 million), and corporate income taxesof 10% were payable to governments. In2011/12 we retained / invested 5% in thebusiness for future growth and £0.6 millionwas invested in our local communities.

This community investment representscash donations made by Johnson Mattheyand does not include the value of employeetime donated during working hours. Weare continuing to develop our systemsto capture further information on ourcontribution to local communities, suchas employees’ time from volunteering.

17

Sustainability 2017Sustainability 2017 Target Key Performance Indicators Baseline 2007 20121 Target Progress

At least double Underlying earnings 82.22 153.7 164.4earnings per share per share (pence)

Halve carbon intensity Global warming potential 2943 156 147(tonnes CO2 eq / £ million sales)

Achieve zero waste to landfill Waste to landfill (tonnes) 16,5553 10,708 0

Halve key resources per unit Electricity consumption 1,0983 626 549of output (GJ / £ million sales)

Natural gas consumption 1,6043 1,012 802(GJ / £ million sales)

Water consumption 1.4263 0.822 0.713(m3 ’000 / £ million sales)

Achieve zero greater than Annual greater than three day n/a 2.07 0three day accidents accident rate per 1,000 employees

Reduce occupational illness cases Annual incidence of occupational 5.34 3.5 3.7by at least 30% by 2013/14 illness cases per 1,000 employees

1 Data presented is for the period 1st April 2011 to 31st March 2012.2 Data presented is for the period 1st April 2006 to 31st March 2007.3 Data presented is for the period 1st January 2006 to 31st December 2006.4 Baseline is incidence of occupational illness cases per 1,000 employees in calendar year 2008.

Progress Towards Sustainability 2017

Local communities0.1%

Retained by /invested in business

for future growth5%

Governments10%

Providers of capital

36%

Employees49%

Special dividend

Ordinary dividend

and interest

Johnson Matthey – Distribution ofUnderlying Added Value 2011/12

Group Key Performance Indicators

Johnson Matthey Annual Report & Accounts 2012Report of the Directors – Business ReviewOverview

18

Johnson Matthey uses a range of key performanceindicators (KPIs) to monitor the group’s performance overtime in line with its strategy.

These include key measures of the group’s financialperformance as well as indicators to monitor ongoinginvestment in facilities and in R&D. In addition, the groupalso uses KPIs to track the carbon footprint of itsoperations and to measure and drive continuousimprovement in the safety, wellbeing and developmentof its employees.

The KPIs weuse to monitorand driveperformance

> These principal KPIs, together with the group’s performance against them in 2011/12,are described below:

Sales Excluding Precious Metals£ million

2008

1,7971,7501,886

2,280

2,679

2009 20112010 20120

500

1,000

1,500

2,000

2,500

3,000

Monitoring sales provides a measure ofthe growth of the business. In measuringthe growth of the group, we focus on salesexcluding the value of precious metalsbecause total revenue can be heavilydistorted by year on year fluctuations inprecious metal prices. Not only that, inmany cases, variations in the value of theprecious metal contained within ourproducts are passed directly on to ourcustomers.

Performance in 2011/12In 2011/12 sales excluding preciousmetals grew by 17% with good growthacross all three divisions as described inthe Financial Review of Operations onpages 26 to 42.

Underlying Earnings per Sharepence

2008

89.689.5 86.4

119.0

153.7

2009 20112010 20120

40

80

120

160

Underlying earnings per share is theprincipal measure used by the board toassess the overall profitability of the group.The following items are excluded fromunderlying earnings because they candistort the trend in measuring results:• Amortisation and impairment ofintangible assets arising on acquisitionof businesses (acquired intangibles).

• Major impairment or restructuringcharges.

• Profit or loss on disposal of businesses.• Tax on the above and major tax itemsarising from changes in legislation.

Performance in 2011/12This year underlying earnings per sharerose by 29% to 153.7 pence supported bya strong performance across the group.Further details are provided on pages 26to 46.

Return on Invested Capital%

In a business as capital intensive asJohnson Matthey’s, profitability alone isa poor measure of performance; it ispossible to generate good operatingmargins but poor value for shareholders ifassets are not used efficiently. Return oninvested capital (ROIC) is therefore usedalongside profit measures to ensure focusupon the efficient use of the group’sassets. ROIC is defined for the group asunderlying operating profit divided byaverage capital employed (equity plus netdebt). ROIC for individual divisions iscalculated using average segmental netassets as the denominator.

Performance in 2011/12The group’s ROIC increased from 19.4%to 22.3%, exceeding our target of 20%.

2008 2009 20112010 20128

10

14

16

20

22

18

12

24

Cost of Capital

Target

19

Safety – Annual Rate of >3 DayAccidentsper 1,000 employees

Johnson Matthey is a manufacturingbusiness and a significant proportionof our employees work in productionenvironments with chemicals and processmachinery. Rigorous safety systems applyacross all facilities and are essential if thegroup is to avoid accidents which couldcause injury to people or damage to ourproperty, both of which can impact thegroup’s performance. We actively manageour safety performance through monitoringthe incidence and causes of accidents thatresult in more than three days lost time.

Performance in 2011/12The group’s annual accident rate of greaterthan three day accidents reduced this yearto 2.07 per 1,000 employees. Furtherdetails of our safety improvementprogrammes are provided in the Healthand Safety section on pages 60 to 67.

Occupational Health – AnnualIncidence of Occupational Illnesscases per 1,000 employees

2007*

5.55.8

5.2

3.5 3.5

2009 20112010 20120

1

2

3

4

5

6

* Calendar year.

The health and wellbeing of our employeesis a priority for Johnson Matthey and weare committed to minimising workplacerelated negative health effects. Wemanage our performance in this area bymeasuring the number of occupationalillness cases arising as a result of exposureto workplace health hazards.

Performance in 2011/12The annual incidence of occupationalillness cases was unchanged this yearat 3.5 per 1,000 employees, below ourtarget of 3.7 cases per 1,000 employees,as a result of our initiatives to promoteemployee wellbeing across the group.Further details are provided in the Healthand Safety section on pages 60 to 67.

Voluntary Employee Turnover%

Europe

4.74.8

14.9

8.5

6.4

NorthAmerica

Rest ofWorld

Asia Group0

4

8

12

16

The success of Johnson Matthey is partlydependent upon the extent that we areable to attract and retain talentedemployees. This means that being anattractive employer is a prerequisite ina competitive environment. We monitorour success in retaining our staff usingvoluntary employee turnover statistics.

Performance in 2011/12In 2011/12 the group’s voluntary employeeturnover increased to 6.4% from 5.6% in2010/11.

Capital Expenditure£ million capex / depn (times)

0

1

2

3

2008

203.5

145.0134.4 137.9

149.6

2009 20112010 20120

30

60

90

120

150

180

210

To enable the group to continue to grow,Johnson Matthey invests significantamounts in maintaining and improving ourexisting plants and in adding new facilitiesto provide additional capacity wherenecessary. All new capital expenditure issubject to detailed review to ensure that itsinvestment case passes internal hurdles.Annual capital expenditure is measured asthe cost of property, plant and equipmentand intangible assets purchased duringthe year. The ratio of capital expenditureto depreciation gives an indication of therelative level of investment.

Performance in 2011/12In 2011/12 the group’s capital expenditurewas £149.6 million which represented1.2 times depreciation (2010/11 1.1).

Gross Research andDevelopment Expenditure£ million

2008

87.6

73.0

91.7

109.8

128.6

2009 20112010 20120

20

40

60

80

120

100

140

Johnson Matthey is fundamentally atechnology company. To maintain ourcompetitive position, we need to keepinvesting in research and development.Whilst absolute levels of research anddevelopment expenditure do notnecessarily indicate how successful weare, that success rapidly feeds through tohigher sales as lead times in our businesscan be quite short.

Performance in 2011/12In 2011/12 the group increased itsresearch and development expenditureby 17% to £128.6 million. Further detailsof the group’s research and developmentactivities are described throughout theBusiness Review.

Sustainability – Global WarmingPotentialthousand tonnes CO2 equivalent

2007** Calendar year.

372390 377

415 417

2009 20112010 20120

90

180

270

360

450

We measure our progress towards reducingthe carbon footprint of our operations bylooking at the group’s total global warmingpotential (GWP). Total GWP is based on ourdirect and indirect energy usage and CO2

equivalence which provide a strong platformfor monitoring the impacts associated withenergy use in our operations. We areworking to broaden the scope of our GWPmeasurement to include all aspects of ourbusiness and to consider the beneficialimpacts of our products and services.

Performance in 2011/12This year the group’s GWP increased onlyslightly from 415,000 to 417,000 tonnesCO2 equivalent despite increased activityand a full year’s contribution from twooperations acquired during 2010/11.Further information on the group’s GWPis given in the Environment section onpages 68 to 75.

March2007

March2008

March2009

March2011

March2010

March2012

0

4

2

6

Risks and Uncertainties

Johnson Matthey Annual Report & Accounts 2012Report of the Directors – Business ReviewOverview

20

Risk Description Impact

STRATEGICFailure to grow in the longer The group’s existing activities are well placed to deliver Failure to identify new business areas or extend the term, to take advantage of good growth over the coming years. New business group’s portfolio could impact the ability of the group new opportunities or to have areas will help to sustain the group’s growth beyond to continue to grow in the long term. sufficient capacity to meet that period. demand

Inability to deliver anticipated The group’s strategy is based upon organic growth. Unsuccessful integration of an acquired business benefits from acquisitions, However, acquisitions and investment in capital projects or project time or cost over-runs could result in the capital projects and other will accelerate the achievement of our strategic goals. failure to realise the expected benefits and hence initiatives impact the group’s results.

The realisation of anticipated benefits depends on: • the performance of acquired businesses after

acquisition and their successful integration into thegroup; and

• the delivery of capital projects on cost and to plan.

Changes to future Approximately 50% of the group’s revenue is driven by A curtailment in environmental legislation around the environmental legislation environmental legislation, particularly legislation over world could limit the group’s growth potential and

emissions from light and heavy duty vehicles. Further undermine profit margins. tightening of global emissions legislation generally requires improved technological solutions and the extension of emissions legislation to new applications can create opportunities for the group.