Embed Size (px)

Citation preview

CORPORATE GOVERNANCE

• Corporate Governance aims to balance the interests of the various

parties involved.

• By balancing the interests of all the stakeholders- management,

shareholders, consumers etc, it formulates ways to attain company’s

objectives.

• Clause 49 of the Listing Agreement by Securities Exchange Board of

India elaborates on the issue of Corporate Governance and prescribes

the norms under which the Companies are mandated to operate

SEBI• On April 12, 1988, the Securities and Exchange Board of India

(SEBI)was established with a dual objective of protecting the rights of

small investors and regulating and developing the stock markets in

India

• In 1992, the Bombay Stock Exchange (BSE),the leading stock exchange

in India, witnessed the first major scam masterminded by Harshad

Mehta.

• Analysts unanimously felt that if more powers had been given to SEBI,

the scam would not have happened.

• As a result the Government of India (GoI) brought in a separate

legislation by the name of ‘SEBI Act 1992’and conferred statutory

powers to it.

• Since then, SEBI had introduced several stock market reforms. These

reforms significantly transformed the face of Indian Stock Markets

SEBI and Clause 49

• SEBI asked Indian firms above a certain size to implement Clause 49,

a regulation that strengthens the role of independent directors serving

on corporate boards.

• On August 26, 2003, SEBI announced an amended Clause 49 of the

listing agreement which every public company listed on an Indian

stock exchange is required to sign. The amended clauses come into

immediate effect for companies seeking a new listing.

CLAUSE 49 ON SHAREHOLDER RIGHTS • Participate in and be sufficiently informed on decisions concerning

fundamental corporate changes.

• Vote in shareholder meetings.

• Ask questions to the Board and propose resolutions.

• Participate in nomination and election of Board members.

• Exercise their ownership rights.

• Put forward their grievances to the Company.

• Be protected from abusive actions in the interest of controlling

shareholders.

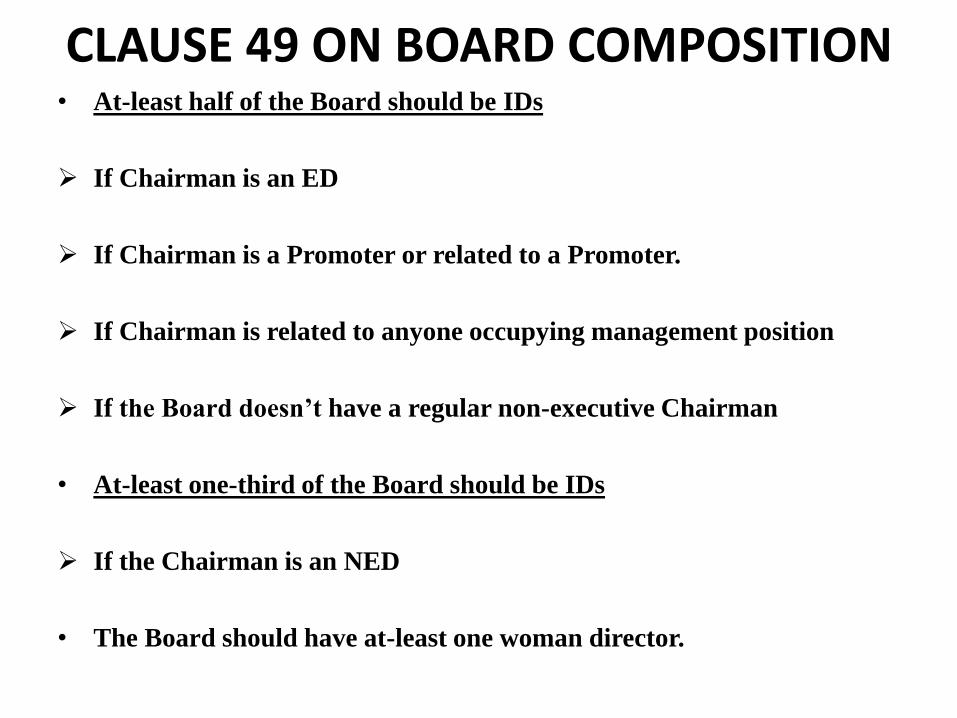

CLAUSE 49 ON BOARD COMPOSITION • At-least half of the Board should be IDs

If Chairman is an ED

If Chairman is a Promoter or related to a Promoter.

If Chairman is related to anyone occupying management position

If the Board doesn’t have a regular non-executive Chairman

• At-least one-third of the Board should be IDs

If the Chairman is an NED

• The Board should have at-least one woman director.

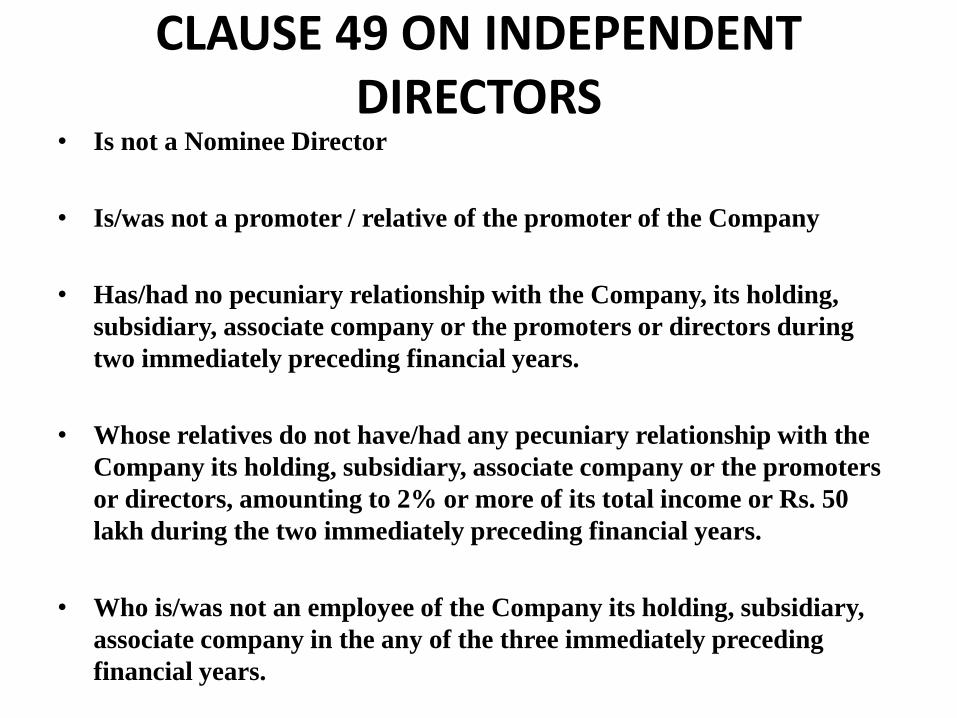

CLAUSE 49 ON INDEPENDENT DIRECTORS

• Is not a Nominee Director

• Is/was not a promoter / relative of the promoter of the Company

• Has/had no pecuniary relationship with the Company, its holding,

subsidiary, associate company or the promoters or directors during

two immediately preceding financial years.

• Whose relatives do not have/had any pecuniary relationship with the

Company its holding, subsidiary, associate company or the promoters

or directors, amounting to 2% or more of its total income or Rs. 50

lakh during the two immediately preceding financial years.

• Who is/was not an employee of the Company its holding, subsidiary,

associate company in the any of the three immediately preceding

financial years.

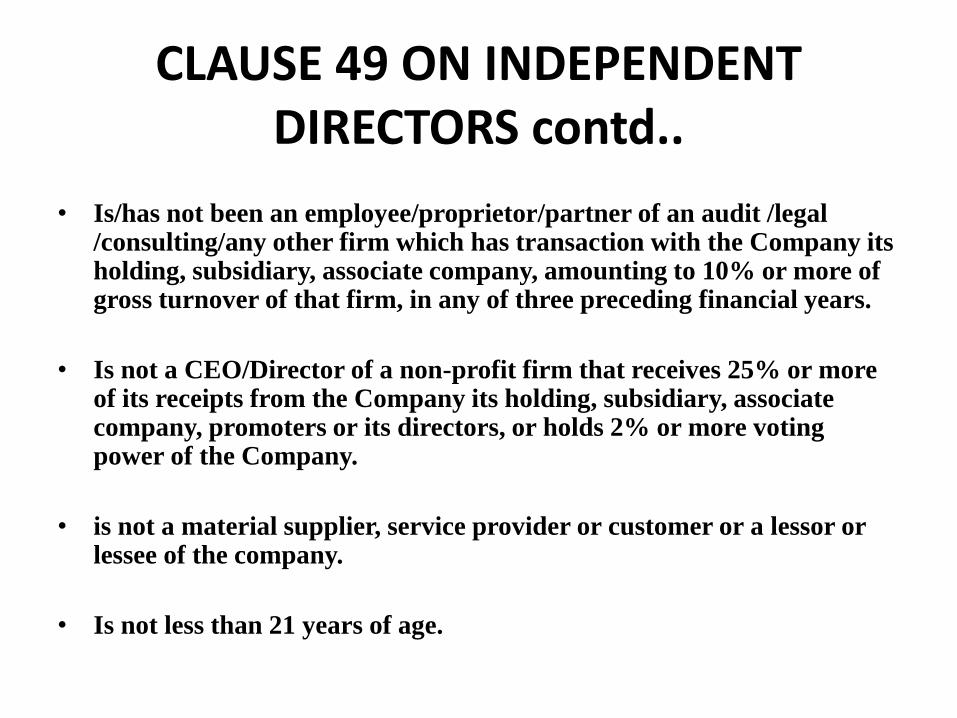

CLAUSE 49 ON INDEPENDENT DIRECTORS contd..

• Is/has not been an employee/proprietor/partner of an audit /legal /consulting/any other firm which has transaction with the Company its holding, subsidiary, associate company, amounting to 10% or more of gross turnover of that firm, in any of three preceding financial years.

• Is not a CEO/Director of a non-profit firm that receives 25% or more of its receipts from the Company its holding, subsidiary, associate company, promoters or its directors, or holds 2% or more voting power of the Company.

• is not a material supplier, service provider or customer or a lessor or lessee of the company.

• Is not less than 21 years of age.

CLAUSE 49 ON DIRECTORIAL REMUNERATION

• Disclosure of all pecuniary relationships of non-executive directors

with the company.

• Disclosure of detailed information on remuneration to directors.

• Disclosure of criteria of making payments to non-executive directors.

• Disclosure of shares/other instruments held by non-executive directors.

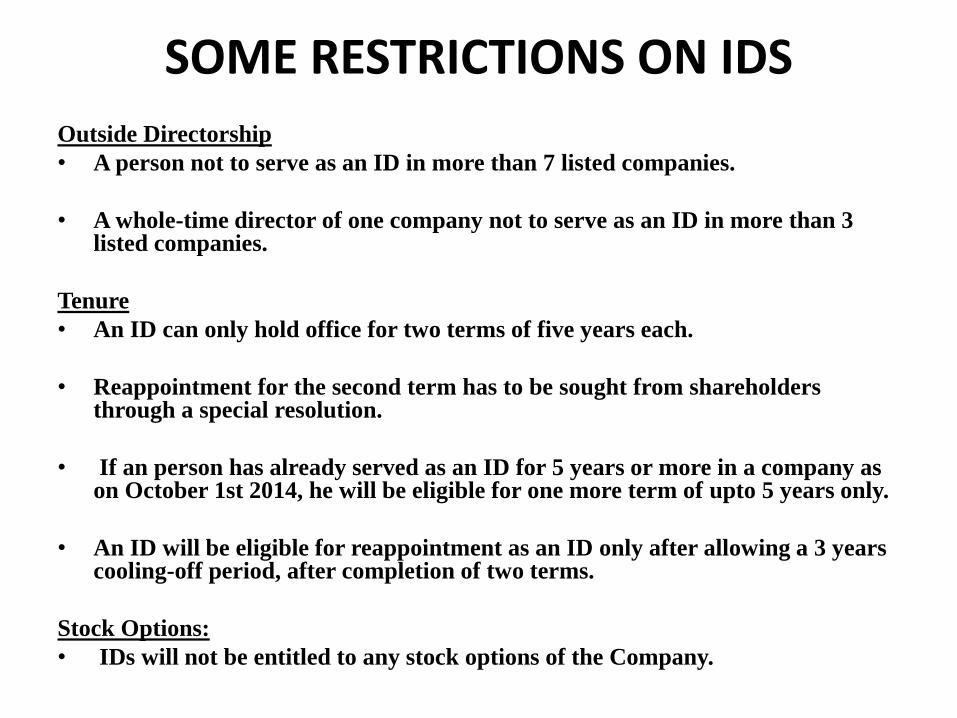

SOME RESTRICTIONS ON IDS

Outside Directorship

• A person not to serve as an ID in more than 7 listed companies.

• A whole-time director of one company not to serve as an ID in more than 3 listed companies.

Tenure

• An ID can only hold office for two terms of five years each.

• Reappointment for the second term has to be sought from shareholders through a special resolution.

• If an person has already served as an ID for 5 years or more in a company as on October 1st 2014, he will be eligible for one more term of upto 5 years only.

• An ID will be eligible for reappointment as an ID only after allowing a 3 years cooling-off period, after completion of two terms.

Stock Options:

• IDs will not be entitled to any stock options of the Company.

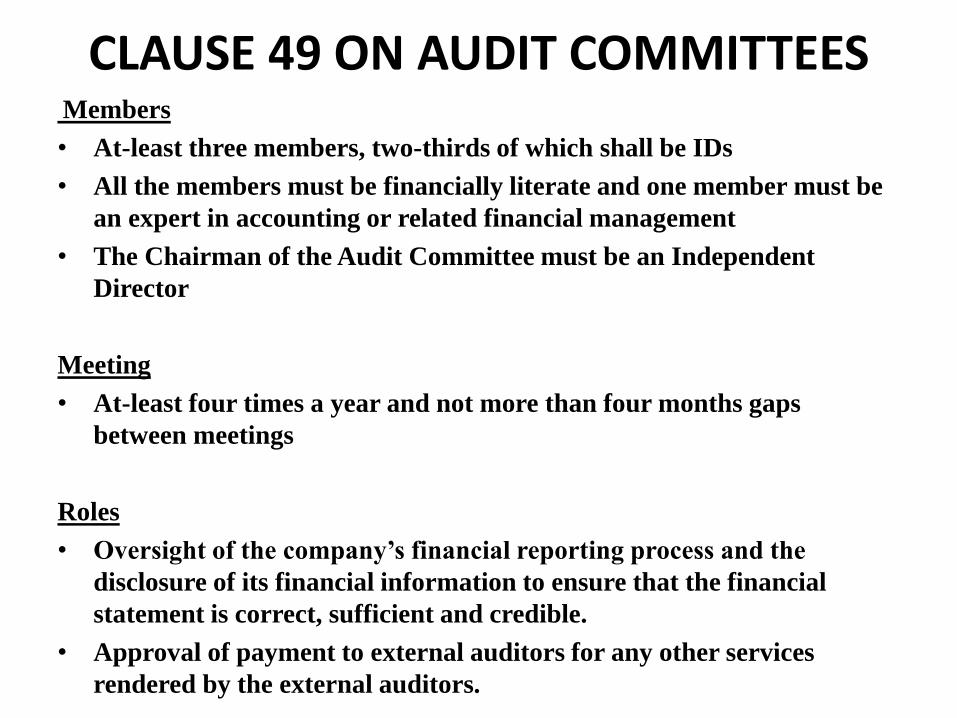

CLAUSE 49 ON AUDIT COMMITTEESMembers

• At-least three members, two-thirds of which shall be IDs

• All the members must be financially literate and one member must be

an expert in accounting or related financial management

• The Chairman of the Audit Committee must be an Independent

Director

Meeting

• At-least four times a year and not more than four months gaps

between meetings

Roles

• Oversight of the company’s financial reporting process and the

disclosure of its financial information to ensure that the financial

statement is correct, sufficient and credible.

• Approval of payment to external auditors for any other services

rendered by the external auditors.

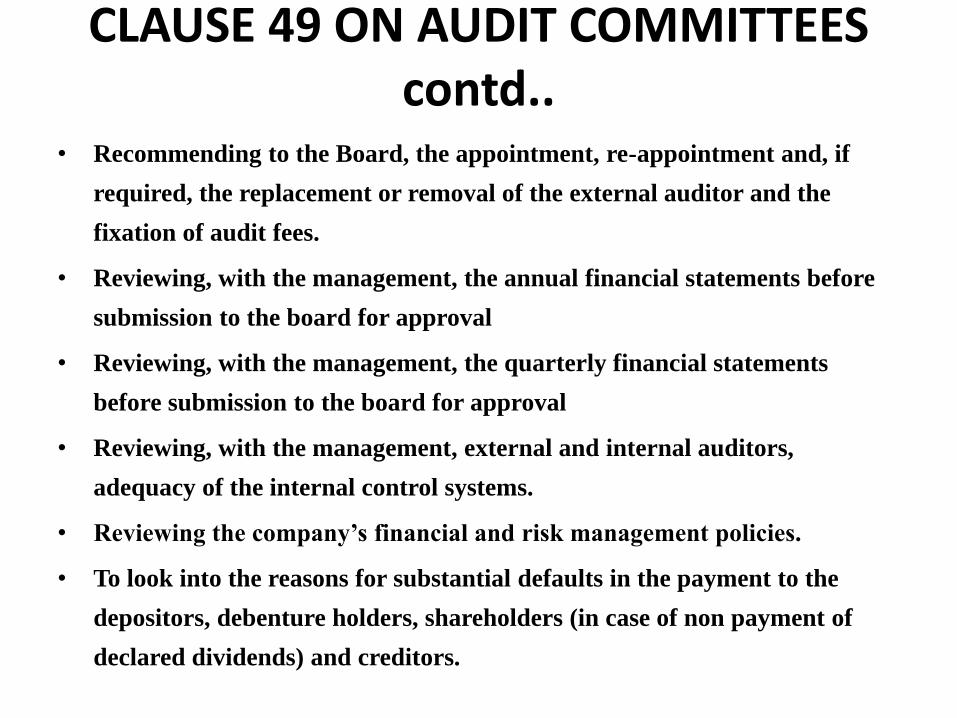

CLAUSE 49 ON AUDIT COMMITTEES contd..

• Recommending to the Board, the appointment, re-appointment and, if

required, the replacement or removal of the external auditor and the

fixation of audit fees.

• Reviewing, with the management, the annual financial statements before

submission to the board for approval

• Reviewing, with the management, the quarterly financial statements

before submission to the board for approval

• Reviewing, with the management, external and internal auditors,

adequacy of the internal control systems.

• Reviewing the company’s financial and risk management policies.

• To look into the reasons for substantial defaults in the payment to the

depositors, debenture holders, shareholders (in case of non payment of

declared dividends) and creditors.

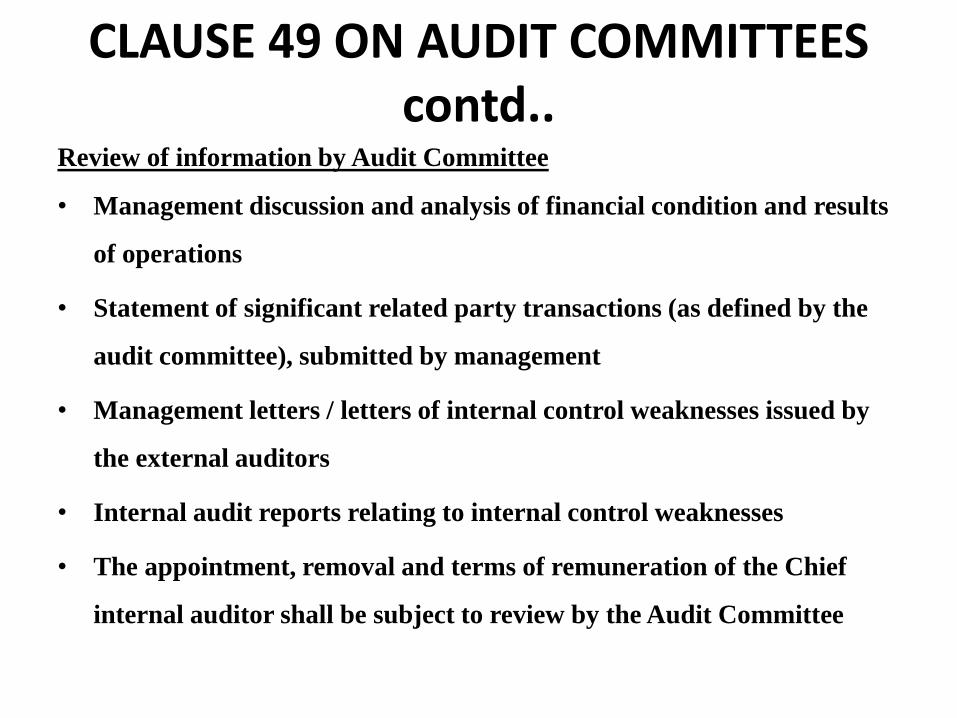

CLAUSE 49 ON AUDIT COMMITTEES contd..

Review of information by Audit Committee

• Management discussion and analysis of financial condition and results

of operations

• Statement of significant related party transactions (as defined by the

audit committee), submitted by management

• Management letters / letters of internal control weaknesses issued by

the external auditors

• Internal audit reports relating to internal control weaknesses

• The appointment, removal and terms of remuneration of the Chief

internal auditor shall be subject to review by the Audit Committee

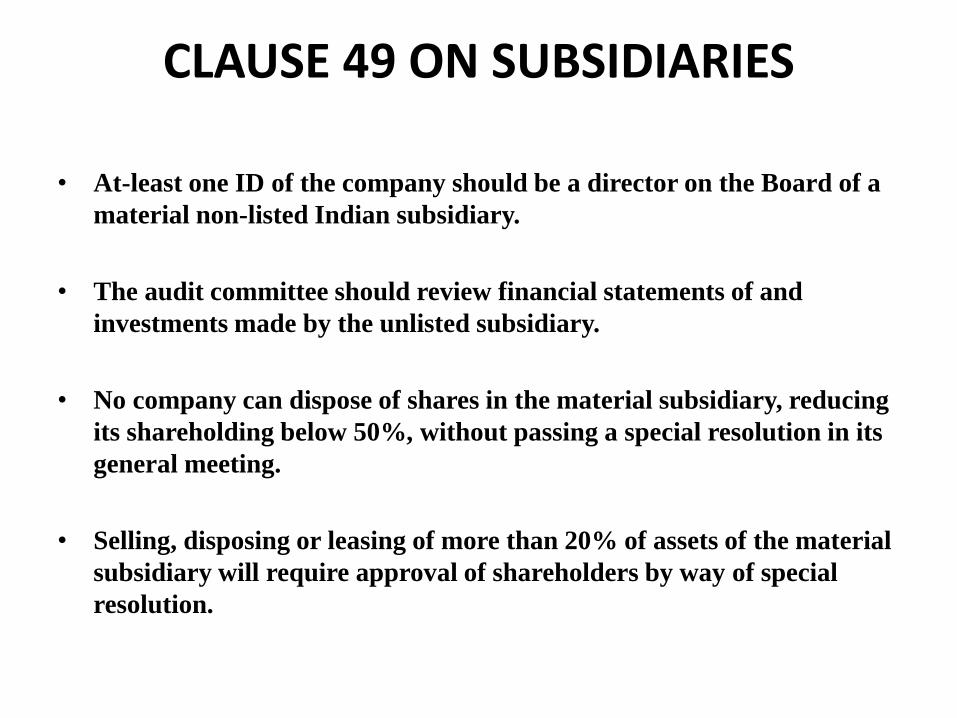

CLAUSE 49 ON SUBSIDIARIES

• At-least one ID of the company should be a director on the Board of a

material non-listed Indian subsidiary.

• The audit committee should review financial statements of and

investments made by the unlisted subsidiary.

• No company can dispose of shares in the material subsidiary, reducing

its shareholding below 50%, without passing a special resolution in its

general meeting.

• Selling, disposing or leasing of more than 20% of assets of the material

subsidiary will require approval of shareholders by way of special

resolution.

CLAUSE 49 ON RELATED PARTY TRANSACTIONS

• RPTs to require prior approval of the audit committee.

• Material RPTs to require shareholder approval though special

resolution and concerned related parties to abstain from voting on

such resolutions.

• Disclosure of all material RPTs on a quarterly basis with compliance

report on corporate governance.

• Disclosure of policies on dealing with RPTs, in website and Annual

Report.

CLAUSE 49 ON OTHER BOARD PROVISIONS

• A director can’t be a member in more than 10 committees and

Chairman of more than 5 committees across all the Boards of Indian

listed companies.

• IDs who resign or are removed, are to be replaced with new IDs within

3 months or immediate next Board meeting, whichever is earlier, in

case the requirement of IDs is not met.

• Board members have to affirm compliance with a ‘Code of Conduct’

on an annual basis.

• IDs to be held liable in acts of omission or commission, which occurs in

their knowledge.

• Company has to mandatorily establish a whistle blower mechanism.

CLAUSE 49 ON DISCLOSURE AND TRANSPARENCY

• The Company should ensure timely and accurate disclosure of information

to its shareholders.

• The information should be prepared and disclosed in accordance with the

prescribed standards and rules.

• Channels for dissemination of information should provide for equal,

timely and cost efficient access to relevant information by users

• The company should maintain minutes of the meeting explicitly recording

dissenting opinions.

CLAUSE 49 ON OTHER DISCLOSURES • Directorial Resignation: Disclosure of letter of resignation of directors

along with reasons, on the company website and stock exchange,

within one working day of receipt of the letter.

• Letter of Appointment: Disclosure of letter of appointment of an ID

along with detailed profile, on the company website and stock

exchange, within one working day of date of appointment.

• Disclosure of training imparted to IDs, in the Annual Report.

• Disclosure of details of establishment of vigil mechanism, in company

website and Board’s report.

• Disclosure of the remuneration policy and the evaluation criteria in the

Annual Report.

MAJOR SCAMS

BHANSALI SCAM

• Between the years of 1992 - 1996, Chain Roop Bhansali was running a

lot of financial firms like CRB Capital Markets, CRB Mutual Fund

and CRB Share Custodial Services

• He offered lot of attractive schemes and made the public and big

organizations to invest in his financial outfits.

• Once investment was made Bhansali very conveniently transferred the

money to imaginary companies.

• Thus he easily owned money worth Rs 900 crores from all the sources.

• It was only when his capital grew from Rs.2 crores in 1992 to Rs.430

crores in 1996 there was a suspicion.

BHANSALI SCAM

• Thus Chain Roop Bhansali was soon charged under various grounds

like fraud, cheating, siphoning off funds from SBI and much more.

• Bhansali made several misleading companies to float in the market like

the CRB Capital Markets, CRB Mutual Fund & CRB Share Custodial

Services and nearly 133 subsidiaries and unlisted companies which

were truly dummy.

• The above three mentioned companies played a major role in

attracting a huge chunk of public money through various attractive

schemes with fixed deposits, bonds and debentures

TELGI SCAM• Abdul Karim Telgi from Belgaum in Karnataka is the main accused in

the major Telgi scam which is worth more than 43,000 crores

• The scam involved the printing and circulation of duplicate stamps

and stamp papers

• In the year 2003, Abdul Karim Telgi started printing fake stamp paper

and also along with this appointed nearly 300 agents for selling the

duplicate stamp papers to bulk purchasers like banks, financial

institutions, insurance companies and share broking firms.

• A shortage of stamp paper engineered with the help of a few officials of

the Indian Security Press at Nashik enabled Telgi to expand his illegal

business throughout the country

• There were also records which clearly state that there were lot of illegal

support from various other organizations and departments of the

Government which were helping in the production and the selling of

the high security stamps.

TELGI SCAM

• Telgi had appointed lot of agents who worked to explore the loopholes

or inadequacies in the law and when the right time emerged Telgi and

his team established a well- knitted network

• Telgi's methodology was that he used a special type of chemical to wash

the cancelled stamp papers.

• Once the stamp papers were washed it used to give a fresh look after

which they were sold at even discount prices by his network of people

to big corporations such as Indian Oil or the Life Insurance

Corporation

HARSHAD MEHTA SCAM

• Harshad Mehta was making waves in the stock market. He had been

buying shares heavily since the beginning of 1990.

• The crucial mechanism through which the scam was effected was

the ready forward (RF) deal.

• Another instrument used in a big way was the bank receipt (BR).

• The money which was got due to manipulation was used to drive up

the prices of stocks in the stock market.

Thank you