Embed Size (px)

Citation preview

Community Based Health Insurance Practices in Nepal

Rabindra Ghimire1

Abstract

This paper critically reviews the micro health insurance practices in Nepal practices by governmental and

nongovernmental sectors. The purpose of this paper is to review the existing community based health

insurance practices, assess the opportunities and challenges of micro health scheme and suggest the better

alternatives in Nepalese context. The paper has prepared based on available literature and it is qualitative

in nature. The micro health insurance intervention nominal in Nepal is in infant stage.

Government health post and hospital provides limited health services to public. Most of the Nepalese are far

from the health insurance services. Six community based health insurance schemes have been initiated by

government in 2003. These schemes are running by hospital, health centre, NGOs, Cooperatives, Business

Association and Trade union. Some schemes are self sustained economically whereas most of the schemes

are supported by government and international donor agencies. Micro Health Insurance Schemes are

running in different parts of Nepal which covers almost 50,000 people. From 400 to 18000 clients are

covered by different micro health insurance schemes. are getting health insurance facility. The paper

concludes that the impact of community based social health schemes in Nepal is not significant but it is

essential for poor and marginalized group.

1. INTRODUCTION

1.1 An Overview of Health Insurance in Nepal

Health insurance is new phenomena in Nepalese context even though commercial insurers have been sold health

insurance package since many years. Government have been provided health insurance, medical allowance and free of

health check, consultation and medical treatment through its own organizational structure and resources. Population

having age below 15 and above 75 also get some treatment facilities from state owned hospital. Still large number of

population is outside the schemes of proper health care facilities.

Community health insurance in Nepal had began by international NGO more than 30 years back initiated by the United

Mission to Nepal as “Lalitpur Medical Insurance Scheme" which is regarded as first non-profit health insurance schemes

in Nepal. In 2000, BP Koirala Institute of Health Science (BPKIHS) in Dharan, started health insurance which covered

urban and rural populations, offering the same benefit package at different premium rates. The scheme covered the

organised sector (cooperatives, business groups) and unorganised groups (such as farmers and self-employed groups),

1 Assistant Professor, Pokhara University and currently Research Scholar, Faculty of Commerce, BHU, Varanasi. [email protected]

______________________________________________________________________________ Community Based Health Insurance Practices in Nepal Page 2 of 15

but was unable to expand because of high costs and low premium collection, which created a deficit. Now, more than a

dozen of schemes operated by private sector are in operations by NGOs, Cooperatives and Hospital.

Health insurance providers in Nepal are basically categorized in two broad sectors: Non subsidized (Commercial insurers

and self managed schemes) and subsidized (government managed CBHI schemes, hospital, cooperatives and NGOs

managed schemes). Besides unorganized sector, health insurance is provided by the commercial insurers as per the need

of the customers. Currently, 17 non life insurers are selling health and accidental insurance policies. The rate of health

insurance penetration by commercial insurers is very low due to small volume of risk exposures, lack of awareness and

high claim ratio.

Major health and accidental policies are: Hospital and surgical expenses insurance, medical and health insurance, Group

Medical Insurance, Group Personnel Accident, Medical & Travel Insurance, Medical Aid Insurance, Traveling Medical

Insurance, mediclaim for senior citizen, Overseas Mediclaim, Hospital Cash Plan, Children health policy etc. (Ghimire,

2012). Under the self managed schemes, Health cooperative societies have been providing their members charging

certain premium. The total numbers of such schemes are not well documented either by the Department of Cooperatives

or Insurance Board.

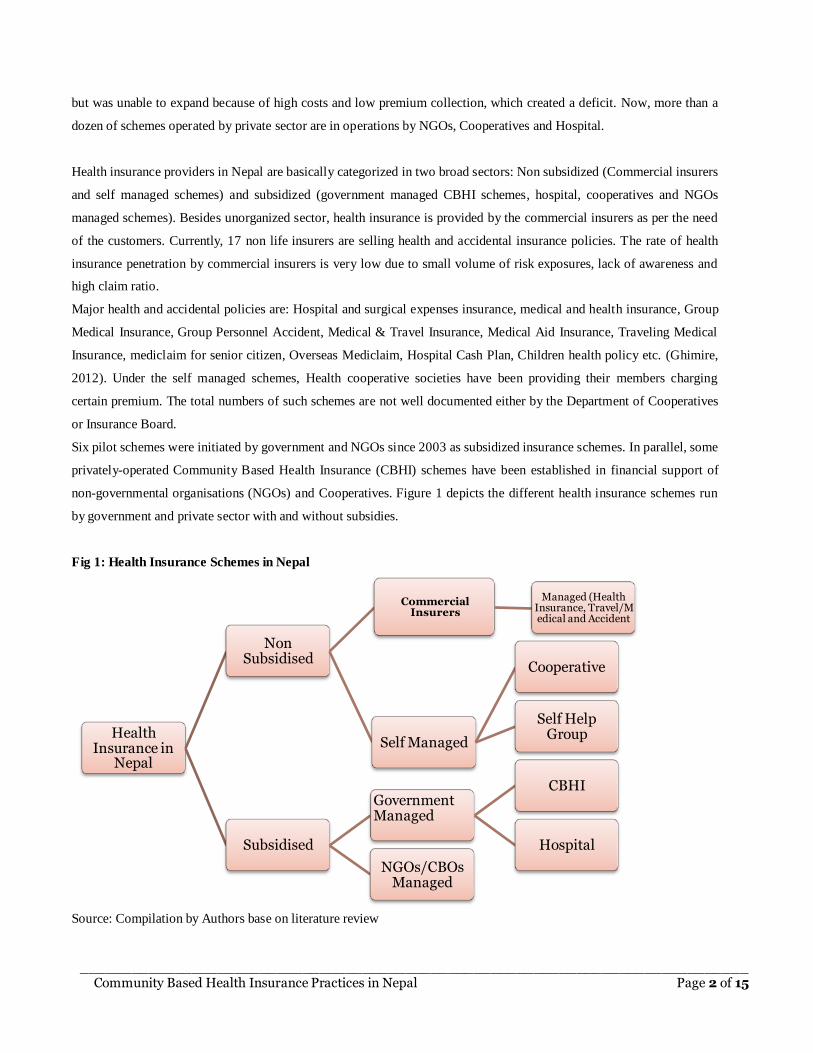

Six pilot schemes were initiated by government and NGOs since 2003 as subsidized insurance schemes. In parallel, some

privately-operated Community Based Health Insurance (CBHI) schemes have been established in financial support of

non-governmental organisations (NGOs) and Cooperatives. Figure 1 depicts the different health insurance schemes run

by government and private sector with and without subsidies.

Fig 1: Health Insurance Schemes in Nepal

Source: Compilation by Authors base on literature review

Health Insurance in

Nepal

Non Subsidised

Commercial Insurers

Managed (Health Insurance, Travel/Medical and Accident

Self Managed

Cooperative

Self Help Group

Subsidised

Government Managed

CBHI

Hospital

NGOs/CBOs Managed

______________________________________________________________________________ Community Based Health Insurance Practices in Nepal Page 3 of 15

1.2 Health Financing in Nepal

Major characteristics of public health delivery system of Nepal are poor health facilities rendering by government

hospitals even in cities and capital, unavailability of workable equipments, skilled human resources, effective medicine

in most of the hospital outside the Kathmandu valley and limited services available even in a regional and zonal hospital

committed in policy and programs.

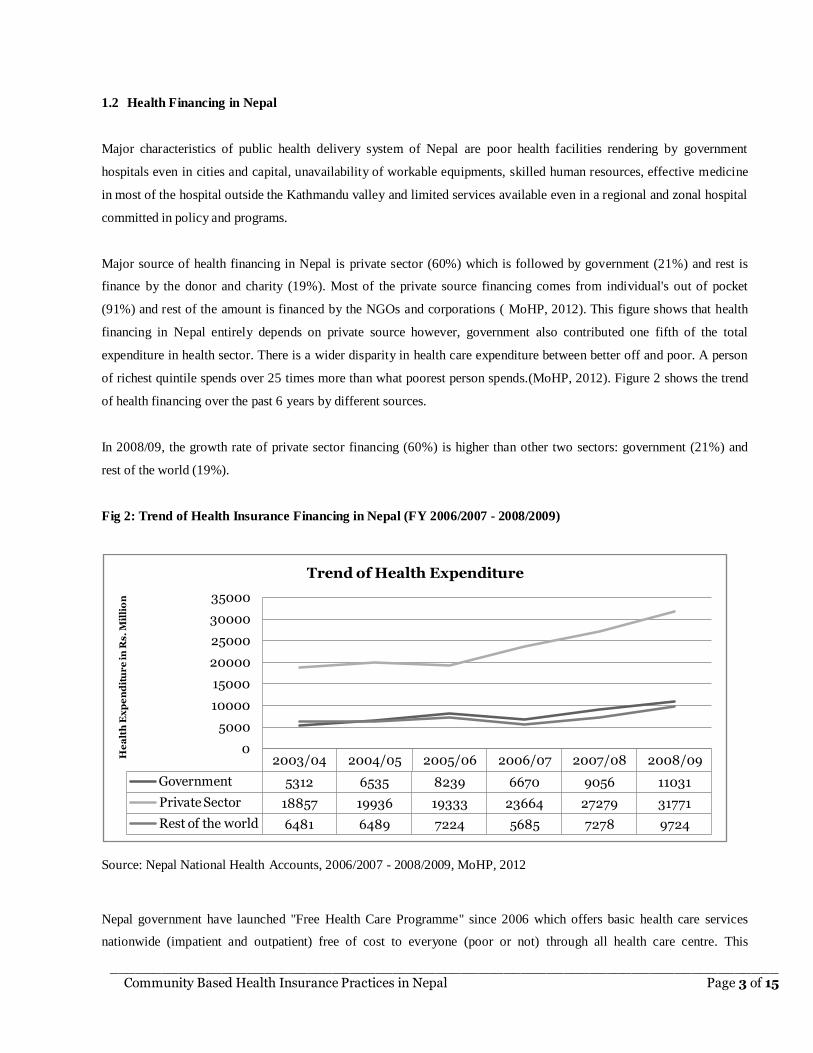

Major source of health financing in Nepal is private sector (60%) which is followed by government (21%) and rest is

finance by the donor and charity (19%). Most of the private source financing comes from individual's out of pocket

(91%) and rest of the amount is financed by the NGOs and corporations ( MoHP, 2012). This figure shows that health

financing in Nepal entirely depends on private source however, government also contributed one fifth of the total

expenditure in health sector. There is a wider disparity in health care expenditure between better off and poor. A person

of richest quintile spends over 25 times more than what poorest person spends.(MoHP, 2012). Figure 2 shows the trend

of health financing over the past 6 years by different sources.

In 2008/09, the growth rate of private sector financing (60%) is higher than other two sectors: government (21%) and

rest of the world (19%).

Fig 2: Trend of Health Insurance Financing in Nepal (FY 2006/2007 - 2008/2009)

Source: Nepal National Health Accounts, 2006/2007 - 2008/2009, MoHP, 2012

Nepal government have launched "Free Health Care Programme" since 2006 which offers basic health care services

nationwide (impatient and outpatient) free of cost to everyone (poor or not) through all health care centre. This

2003/04 2004/05 2005/06 2006/07 2007/08 2008/09

Government 5312 6535 8239 6670 9056 11031

Private Sector 18857 19936 19333 23664 27279 31771

Rest of the world 6481 6489 7224 5685 7278 9724

0

5000

10000

15000

20000

25000

30000

35000

He

alt

h E

xp

en

dit

ur

e i

n R

s.

Mil

lio

n

Trend of Health Expenditure

______________________________________________________________________________ Community Based Health Insurance Practices in Nepal Page 4 of 15

programme provides 22 to 40 different medicines free of cost to all. But, additional service (consultations and treatment,

minor surgery, emergency obstetric care (either comprehensive or basic), x-rays and laboratory services) are provided to

target groups only (poor, ultra poor, helpless, disabled, senior citizens above 60 years of age and female community

health volunteers) only.

2. SYNOPSIS OF LITERATURE REVIEW

Most of the poor people in the world are suffering from the health related expenses. Microinsurance is emerging as a

global solution for breaking the cycle of poverty and vulnerability. Locally, it provides an opportunity to plan for ill

health by organizing regular payments, making health expenses predictable and affordable. Micro health insurance is

especially designed to poor and vulnerable people to provide them health and medical facilities since they couldn't afford

the cost of medicine and hospitalization as other normal income people from the ordinary market. The poorest citizens of

the poorest countries are typically exposed to the greatest risks (Murdoch, 1995). They are inherently more vulnerable to

illness due to their living conditions, limited resources and exclusion from social security systems.

In Nepal, families face multiple barriers in accessing healthcare. Delays in the decision to seek care arise from financial

constraints as 72% of people finance health costs “out-of-pocket” (World Bank, 2011). In order to cope with these costs

families may borrow money with interest or sell productive assets, pushing them further into poverty. Access to micro

health insurance has been shown to decrease out-of-pocket expenditure, especially for catastrophic health events, and

improve access to care for insured members (Carrin, Waelkens and Criel 2012). As health insurance coverage is only

5% in Nepal, the opportunity to deliver an innovative solution is substantial (Stoermer et al., 2011).

Illness and crop failure often cause severe economic damage to rural households in Cambodia that more farmer sell their

land due to illness than due to crop failure (Kanjiro, 2005). Crop failure is generally considered to be a common shock,

while illness is considered idiosyncratic. According to recent World Health Organization estimates, every year 25

million households (more than 100 million people) are forced into poverty by illness.

According to WHO (2005) 100 million people every year are driven into poverty due to catastrophic health expenditure.

It is imaginable that most reside in resource poor settings such as Sub Saharan Africa with very weak modern health care

systems and in most cases without any functioning health insurance schemes (WHO, 2003; Carrin et al, 2005).

The highest demand from poor people was for health products and life products, followed by property insurance and

accidental death and disability cover. Roth, Michael and Liber (2007) states that Micro Health Insurance schemes over

the world are found in large numbers but their membership is limited in numbers and growth of membership is slow.

Community Based Health Insurance Schemes (CBHISs) are promising alternatives for a cost sharing health care system

which hopefully also leads to better utilization of health care services, reduce illness related income shocks and

______________________________________________________________________________ Community Based Health Insurance Practices in Nepal Page 5 of 15

eventually lead to a sustainable and fully functioning universal health care system (Shimeles, 2010). But, the experience

of CBHI in different places is different, however, the objective is the same to deliver the health service to poor and

marginalized population in affordable price.

CBHI schemes as observed in different regions of developing world are quite diverse. Nevertheless, certain features

common to most of the schemes can be readily identified, such as, the voluntary participation of the people, not-for-

profit objective in organizing the scheme, scheme management by the community itself, and some degree of risk

pooling. These schemes are reported to have made positive contribution in terms of financial protection, resource

mobilization, social exclusion, and in health care provision (Ahuja, et al. 2003).

Tobor (2005) in his study concludes that the main weaknesses of CBHI are the low level of revenues that can be

mobilized from poor communities, the frequent exclusion of the poorest of the poor from participation in such schemes

without some form of subsidy, the small size of the risk pool, the limited management capacity that exists in rural and

low-income contexts, and their isolation from the more comprehensive benefits that are often available through more

formal health financing mechanisms and provider networks.

CBHI schemes are run in different modalities in international practices such as community owned, run by local or central

government or both, run by hospitals or clinics, run by international NGOs or donors, by cooperatives or trade unions.

3. OBJECTIVES AND METHODOLOGY

Objective of this paper is to review the existing community based health insurance practices in Nepal, assess

effectiveness of health insurance program run by government and private sector and provide suggestions regarding the

suitable model for the better delivery of the health insurance to the poor and vulnerable community with the best possible

way. The paper also shed lights the prospects and challenges of community based micro health insurance schemes.

The paper has been prepared based on secondary information available from different literature. Sufficient literature has

been reviewed and required data have been gathered from the various relevant publications published from Department

of Health Services, bilateral and multilateral development organizations, INGOs, NGOs. Relevant literature in the field

of community based health insurance in Nepal and health insurance financing in Nepal has been collected. Government’s

health related rules, strategic plan and policy have been also been consulted. The study is descriptive and qualitative in

nature based on available secondary information from the published and unpublished sources including the web search.

Experts in the field were consulted to validate the information.

We have taken total 22 CBHI schemes for this study. Six CBHI schemes are run by government run and 16 are privately

run. For government run CBHI, medicine, diagnosis, hospitalization and total benefits variables are taken for analysis

______________________________________________________________________________ Community Based Health Insurance Practices in Nepal Page 6 of 15

whereas in private owned CBHI scheme, Number of Beneficiaries and coverage of area, types of beneficiaries and

supporting agency are taken as variables for discussion.

4. COMMUNITY BASED HEALTH INSURANCE PRACTICES

Micro Health Insurance schemes have been run in different name and modality in Nepal but they are still not operated as

per the insurance guidelines and not registered under Insurance Board. Government and private sector run different

schemes are discussed in this section.

4.1 Government Run CBHI

Health insurance has gained momentum among policy makers in Nepal over the last couple of years. The Ministry of

Health and Population is in the process of drafting a health insurance policy and a new health financing strategy. At the

implementation level, the Ministry of Health and Population has been piloting community-based health insurance

schemes since 2003/04 and for the effective implementation of the scheme, Community Health Insurance Operational

Guidelines, 2006 is on operation.

Currently, CBHI are run either in two modalities: low cost high frequency of illness and high cost low frequency of

illness model.

i. Low cost high frequency of illness model: This model covers the primary health care services at

Dumkauli,Tikapur, Lamahi, Chandranigahapur and Katari PHC.

ii. High cost, low frequency of illness model: This model covers primary health care services with referral services

at Mangalbare.

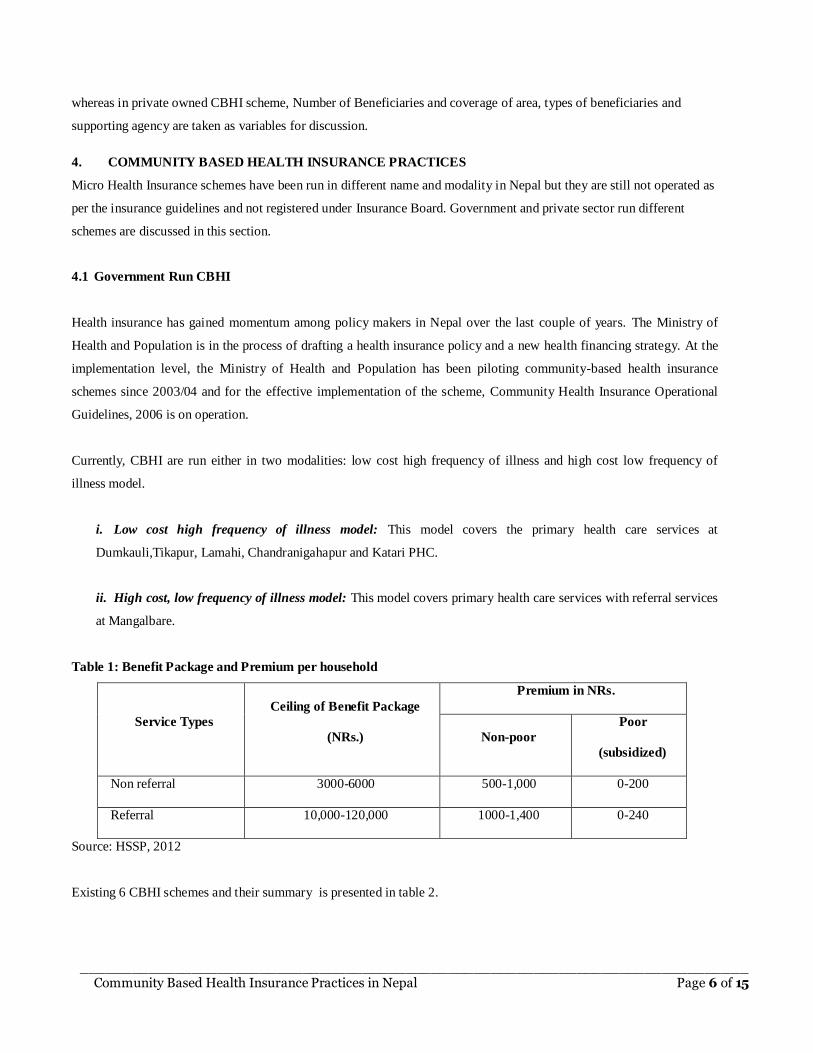

Table 1: Benefit Package and Premium per household

Service Types

Ceiling of Benefit Package

(NRs.)

Premium in NRs.

Non-poor

Poor

(subsidized)

Non referral 3000-6000 500-1,000 0-200

Referral 10,000-120,000 1000-1,400 0-240

Source: HSSP, 2012

Existing 6 CBHI schemes and their summary is presented in table 2.

______________________________________________________________________________ Community Based Health Insurance Practices in Nepal Page 7 of 15

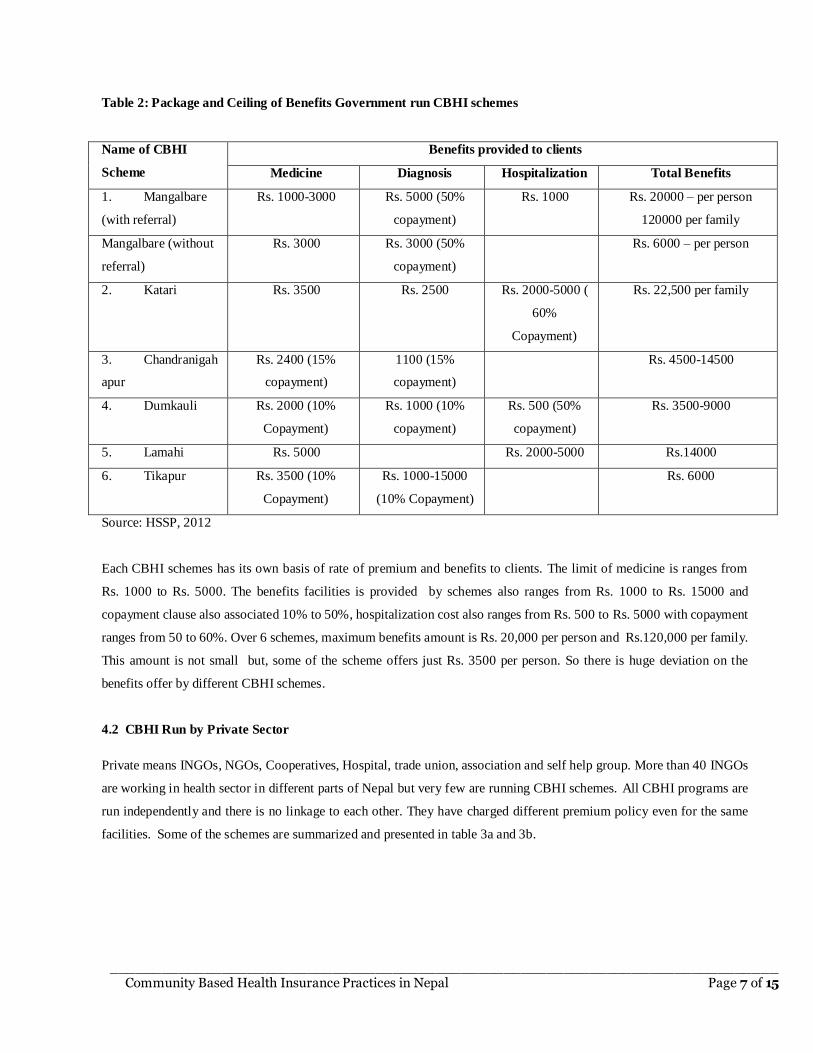

Table 2: Package and Ceiling of Benefits Government run CBHI schemes

Name of CBHI

Scheme

Benefits provided to clients

Medicine Diagnosis Hospitalization Total Benefits

1. Mangalbare

(with referral)

Rs. 1000-3000 Rs. 5000 (50%

copayment)

Rs. 1000 Rs. 20000 – per person

120000 per family

Mangalbare (without

referral)

Rs. 3000 Rs. 3000 (50%

copayment)

Rs. 6000 – per person

2. Katari Rs. 3500 Rs. 2500 Rs. 2000-5000 (

60%

Copayment)

Rs. 22,500 per family

3. Chandranigah

apur

Rs. 2400 (15%

copayment)

1100 (15%

copayment)

Rs. 4500-14500

4. Dumkauli Rs. 2000 (10%

Copayment)

Rs. 1000 (10%

copayment)

Rs. 500 (50%

copayment)

Rs. 3500-9000

5. Lamahi Rs. 5000 Rs. 2000-5000 Rs.14000

6. Tikapur Rs. 3500 (10%

Copayment)

Rs. 1000-15000

(10% Copayment)

Rs. 6000

Source: HSSP, 2012

Each CBHI schemes has its own basis of rate of premium and benefits to clients. The limit of medicine is ranges from

Rs. 1000 to Rs. 5000. The benefits facilities is provided by schemes also ranges from Rs. 1000 to Rs. 15000 and

copayment clause also associated 10% to 50%, hospitalization cost also ranges from Rs. 500 to Rs. 5000 with copayment

ranges from 50 to 60%. Over 6 schemes, maximum benefits amount is Rs. 20,000 per person and Rs.120,000 per family.

This amount is not small but, some of the scheme offers just Rs. 3500 per person. So there is huge deviation on the

benefits offer by different CBHI schemes.

4.2 CBHI Run by Private Sector

Private means INGOs, NGOs, Cooperatives, Hospital, trade union, association and self help group. More than 40 INGOs

are working in health sector in different parts of Nepal but very few are running CBHI schemes. All CBHI programs are

run independently and there is no linkage to each other. They have charged different premium policy even for the same

facilities. Some of the schemes are summarized and presented in table 3a and 3b.

______________________________________________________________________________ Community Based Health Insurance Practices in Nepal Page 8 of 15

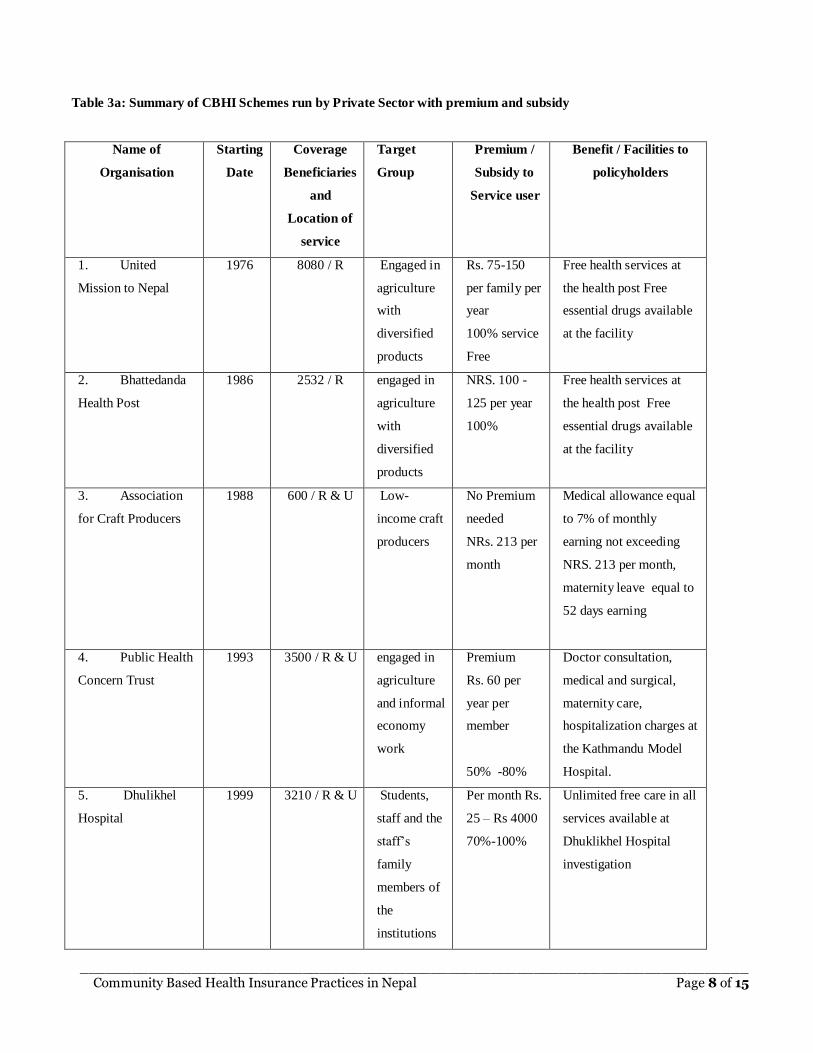

Table 3a: Summary of CBHI Schemes run by Private Sector with premium and subsidy

Name of

Organisation

Starting

Date

Coverage

Beneficiaries

and

Location of

service

Target

Group

Premium /

Subsidy to

Service user

Benefit / Facilities to

policyholders

1. United

Mission to Nepal

1976 8080 / R Engaged in

agriculture

with

diversified

products

Rs. 75-150

per family per

year

100% service

Free

Free health services at

the health post Free

essential drugs available

at the facility

2. Bhattedanda

Health Post

1986 2532 / R engaged in

agriculture

with

diversified

products

NRS. 100 -

125 per year

100%

Free health services at

the health post Free

essential drugs available

at the facility

3. Association

for Craft Producers

1988 600 / R & U Low-

income craft

producers

No Premium

needed

NRs. 213 per

month

Medical allowance equal

to 7% of monthly

earning not exceeding

NRS. 213 per month,

maternity leave equal to

52 days earning

4. Public Health

Concern Trust

1993 3500 / R & U engaged in

agriculture

and informal

economy

work

Premium

Rs. 60 per

year per

member

50% -80%

Doctor consultation,

medical and surgical,

maternity care,

hospitalization charges at

the Kathmandu Model

Hospital.

5. Dhulikhel

Hospital

1999 3210 / R & U Students,

staff and the

staff’s

family

members of

the

institutions

Per month Rs.

25 – Rs 4000

70%-100%

Unlimited free care in all

services available at

Dhuklikhel Hospital

investigation

______________________________________________________________________________ Community Based Health Insurance Practices in Nepal Page 9 of 15

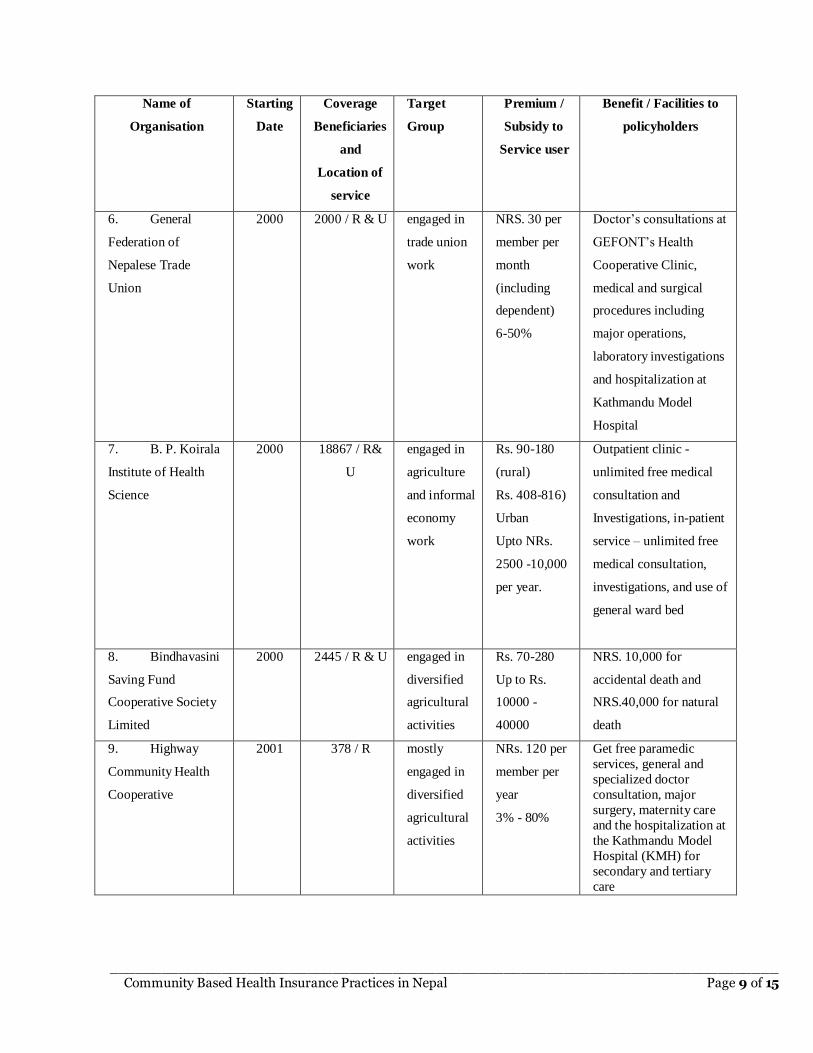

Name of

Organisation

Starting

Date

Coverage

Beneficiaries

and

Location of

service

Target

Group

Premium /

Subsidy to

Service user

Benefit / Facilities to

policyholders

6. General

Federation of

Nepalese Trade

Union

2000 2000 / R & U engaged in

trade union

work

NRS. 30 per

member per

month

(including

dependent)

6-50%

Doctor’s consultations at

GEFONT’s Health

Cooperative Clinic,

medical and surgical

procedures including

major operations,

laboratory investigations

and hospitalization at

Kathmandu Model

Hospital

7. B. P. Koirala

Institute of Health

Science

2000 18867 / R&

U

engaged in

agriculture

and informal

economy

work

Rs. 90-180

(rural)

Rs. 408-816)

Urban

Upto NRs.

2500 -10,000

per year.

Outpatient clinic -

unlimited free medical

consultation and

Investigations, in-patient

service – unlimited free

medical consultation,

investigations, and use of

general ward bed

8. Bindhavasini

Saving Fund

Cooperative Society

Limited

2000 2445 / R & U engaged in

diversified

agricultural

activities

Rs. 70-280

Up to Rs.

10000 -

40000

NRS. 10,000 for

accidental death and

NRS.40,000 for natural

death

9. Highway

Community Health

Cooperative

2001 378 / R mostly

engaged in

diversified

agricultural

activities

NRs. 120 per

member per

year

3% - 80%

Get free paramedic

services, general and

specialized doctor

consultation, major

surgery, maternity care

and the hospitalization at

the Kathmandu Model

Hospital (KMH) for

secondary and tertiary

care

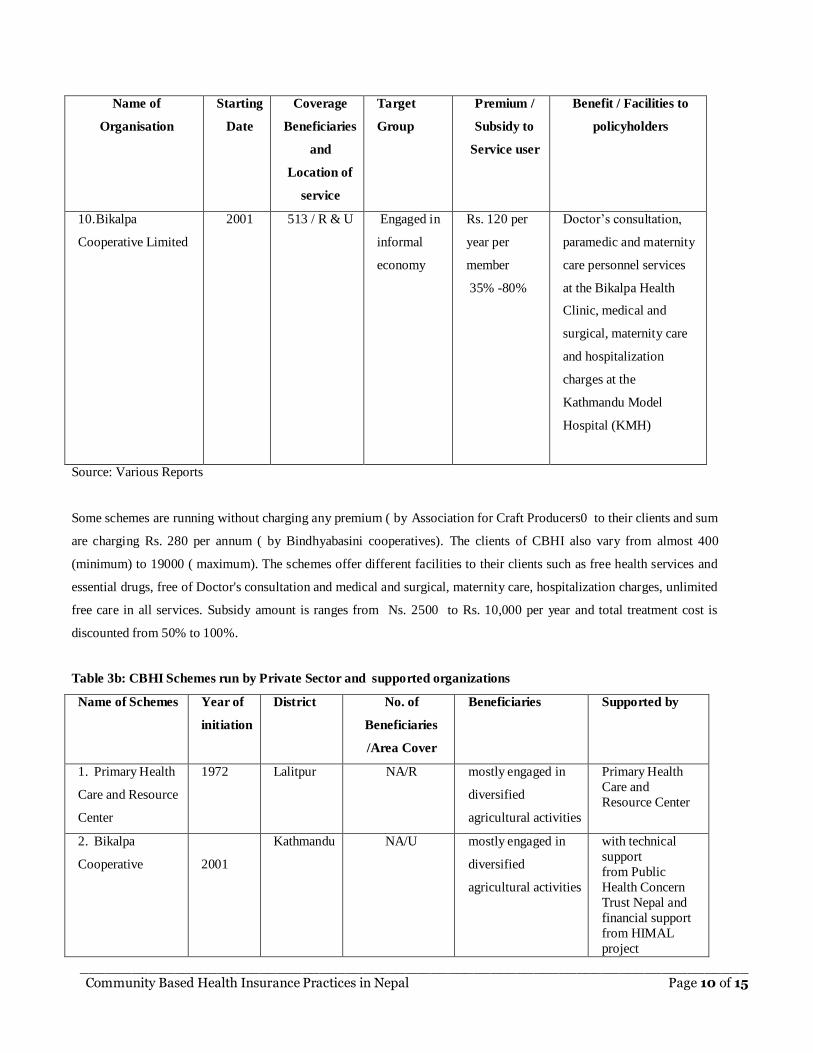

______________________________________________________________________________ Community Based Health Insurance Practices in Nepal Page 10 of 15

Name of

Organisation

Starting

Date

Coverage

Beneficiaries

and

Location of

service

Target

Group

Premium /

Subsidy to

Service user

Benefit / Facilities to

policyholders

10. Bikalpa

Cooperative Limited

2001 513 / R & U Engaged in

informal

economy

Rs. 120 per

year per

member

35% -80%

Doctor’s consultation,

paramedic and maternity

care personnel services

at the Bikalpa Health

Clinic, medical and

surgical, maternity care

and hospitalization

charges at the

Kathmandu Model

Hospital (KMH)

Source: Various Reports

Some schemes are running without charging any premium ( by Association for Craft Producers0 to their clients and sum

are charging Rs. 280 per annum ( by Bindhyabasini cooperatives). The clients of CBHI also vary from almost 400

(minimum) to 19000 ( maximum). The schemes offer different facilities to their clients such as free health services and

essential drugs, free of Doctor's consultation and medical and surgical, maternity care, hospitalization charges, unlimited

free care in all services. Subsidy amount is ranges from Ns. 2500 to Rs. 10,000 per year and total treatment cost is

discounted from 50% to 100%.

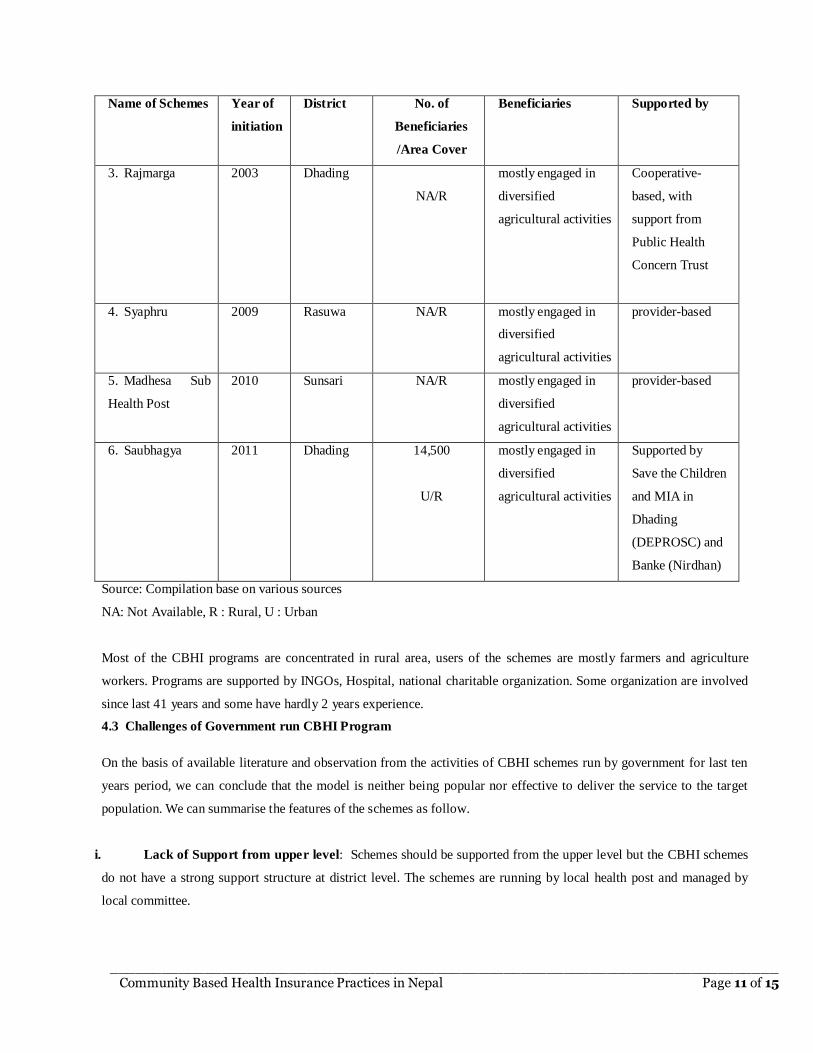

Table 3b: CBHI Schemes run by Private Sector and supported organizations

Name of Schemes Year of

initiation

District No. of

Beneficiaries

/Area Cover

Beneficiaries Supported by

1. Primary Health

Care and Resource

Center

1972 Lalitpur NA/R mostly engaged in

diversified

agricultural activities

Primary Health

Care and

Resource Center

2. Bikalpa

Cooperative

2001

Kathmandu NA/U mostly engaged in

diversified

agricultural activities

with technical

support

from Public

Health Concern

Trust Nepal and

financial support

from HIMAL

project

______________________________________________________________________________ Community Based Health Insurance Practices in Nepal Page 11 of 15

Name of Schemes Year of

initiation

District No. of

Beneficiaries

/Area Cover

Beneficiaries Supported by

3. Rajmarga 2003 Dhading

NA/R

mostly engaged in

diversified

agricultural activities

Cooperative-

based, with

support from

Public Health

Concern Trust

4. Syaphru

2009

Rasuwa NA/R mostly engaged in

diversified

agricultural activities

provider-based

5. Madhesa Sub

Health Post

2010 Sunsari NA/R mostly engaged in

diversified

agricultural activities

provider-based

6. Saubhagya 2011 Dhading 14,500

U/R

mostly engaged in

diversified

agricultural activities

Supported by

Save the Children

and MIA in

Dhading

(DEPROSC) and

Banke (Nirdhan)

Source: Compilation base on various sources

NA: Not Available, R : Rural, U : Urban

Most of the CBHI programs are concentrated in rural area, users of the schemes are mostly farmers and agriculture

workers. Programs are supported by INGOs, Hospital, national charitable organization. Some organization are involved

since last 41 years and some have hardly 2 years experience.

4.3 Challenges of Government run CBHI Program

On the basis of available literature and observation from the activities of CBHI schemes run by government for last ten

years period, we can conclude that the model is neither being popular nor effective to deliver the service to the target

population. We can summarise the features of the schemes as follow.

i. Lack of Support from upper level: Schemes should be supported from the upper level but the CBHI schemes

do not have a strong support structure at district level. The schemes are running by local health post and managed by

local committee.

______________________________________________________________________________ Community Based Health Insurance Practices in Nepal Page 12 of 15

ii. Financial efficiency: Most CBHI schemes do not have any data to monitor their financial viability. They are not

aware of their operating expenses as expenses are born by government. So, the incurred expense ratio (incurred

expenses/earned premium) is very high.

iii. Pro Poor Challenges: Another major question is that micro health program does serve the real poor and vulnerable

class? It is said that program are community-based, but they are governed by government not community. The

premium of these schemes is not determined on the actuarial base and risk is not reinsured. The premium is

subsidized in the same rate to rich and poor which is not justifiable.

iv. Sustainability: These schemes need to regulate by Insurance Board otherwise, there is the question of solvency and

sustainability for long run. Schemes are not reinsured and the adverse selection cases are more than normal cases.

v. Limited Coverage: The population of Nepal is 26.6 million, more than 25 percent are below the poverty line and

almost 83 percent are living in rural area. The schemes are running in very small scale and scaling up is also not

done. The impact of micro health insurance over the country is meaningless.(Economic Survey, 2012; CBS, 2011)

vi. Poor Health Care: The reasons behind such poor health care services can be listed as: limited fund available for the

health care services, lack of commitment of professional to work outside the capital city and corruption,

mismanagement and bureaucratic hurdles. The difficult landscape has also contributed to the poor level of access to

healthcare, with rural areas having little or no form of medical treatment available. The healthcare facilities available

in remote areas, the medical professionals are normally poorly trained (Oxfam, 2008)

5. MICRO HEALTH INSURANCE MODEL

Government capacity to deliver free health care to its citizen largely depends on willingness to offer and capacity to

offer. It is also called the fiscal space of government which means “room in a government’s budget that allows it to

provide resources for a desired purpose without jeopardizing the sustainability of its financial position or the stability of

the economy” (Heller P, 2006).

Sustainable sources of government revenue are tax but the tax base is very narrow. The tax to GDP ratio in 2009/10 was

14.3% (average of OECD was 35%). Government has no priority to Health sector since Health Budget to National

Budget ratio never increased than 7.16%. In this context, existing ongoing universal free health care program, maternity

program and other free targeted health care programs might be affected and difficult to maintain and sustain in coming

years.

Worldwide health insurance models are either out of pocket based or government revenue based or mix of the both. Most

of the developing countries, people cannot afford health insurance. In Nepal, more than 80 percent people living in

village and livelihood of 75 percent people is subsistence agriculture so that they cannot purchase life insurance.

Government has not sufficient fund to finance the 100 percent health expenditure to 100 percent population.

______________________________________________________________________________ Community Based Health Insurance Practices in Nepal Page 13 of 15

We have already four different models of health insurance in practices: 1) Private Health Insurance is offering by

commercial insurers for middle and high income class, 2) Micro health insurance is available to low income group by

private sector but the outreach is very poor; 3) Community Based Health Insurance (CBHI) is recently introduced by

government in limited cluster and 4) Social Health Insurance is available to government and corporate employees. None

of the model is perfect and can give the solution of diverse demographic structure having a different income level, health

status, culture and needs. Mix of the above models may give the best result and serve the need of the target population.

According to the objective of this paper, we discuss on the model of micro health insurance. Government should abide

by some fundamental principles while implementing the health insurance program to the poor and vulnerable group.

Need to focus on vulnerable groups, such as women, poor and elderly people, and people suffering to chronic

diseases who are most likely to be excluded by insurance mechanisms.

Need to increase national budgets as well as portion of health budget by increasing the tax base and proper

utilisation of international development budget.

Gradually increase the government support and subsidy to poor and at the same time decrease the amount of

premium. This could be a more promising and more equitable route to universal access.

Among the existing various models to deliver the health insurance to low income people, none of the model is perfect

and ideal. Single model may not be enough to address the people having diverse income, culture and demographic

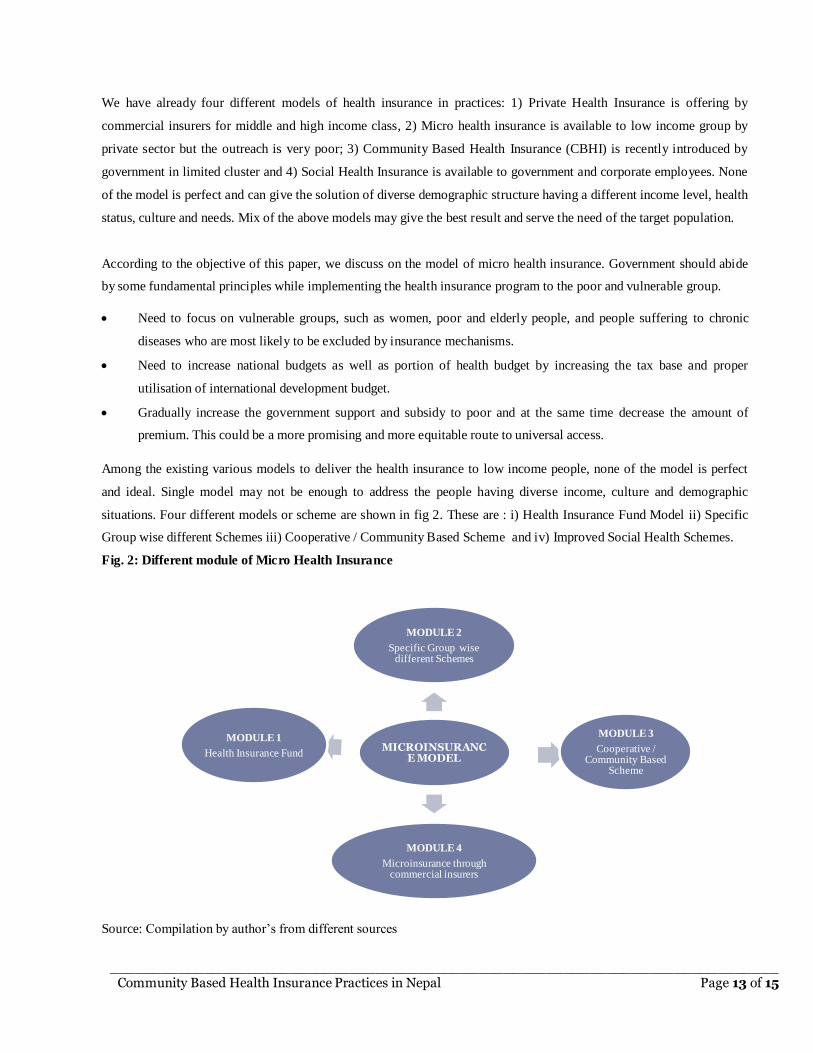

situations. Four different models or scheme are shown in fig 2. These are : i) Health Insurance Fund Model ii) Specific

Group wise different Schemes iii) Cooperative / Community Based Scheme and iv) Improved Social Health Schemes.

Fig. 2: Different module of Micro Health Insurance

Source: Compilation by author’s from different sources

MICROINSURANCE MODEL

MODULE 2

Specific Group wise different Schemes

MODULE 3

Cooperative / Community Based

Scheme

MODULE 4

Microinsurance through commercial insurers

MODULE 1

Health Insurance Fund

______________________________________________________________________________ Community Based Health Insurance Practices in Nepal Page 14 of 15

The best solution can be Mix Model. In mix model, there is government contribution (tax revenue) and personal

contribution (insurance) for health care financing. This can be implemented through different schemes such as through

separate health insurance fund, through association formed by the people of same profession, forming the cooperatives or

CBHI and microinsurance through commercial insurers where subsidies on premium is provided by the government.

Due to the constraints of the length of the paper, detail of each scheme is not possible to discuss in the same paper. These

four schemes can be lunched parallel way as per the situation.

6. CONCLUDING REMARKS

Community Based Health Insurance Nepal was initiated 30 years back but still it is in infant stage. Government of Nepal

has started some CBHI schemes as a pilot study. Moreover, private sector also has offered health insurance in different

modality but the coverage of insurance to public is very limited. There is urgent need of expansion of such services from

Himalayan to Terai and East to West focusing the poor and marginalized community. Since 2006, government has been

providing the different medicines and treatments to public and special groups of people became the milestone in the

history of health care management in Nepal.

It is obvious that CBHI schemes have positive impact on community through various ways for example, it has increased

consciousness on their health, increases utilization rate, increase service coverage, it has provided health security to the

poor, people are getting timely treatment and they are using drug, quality of care improved, community participation and

ownership increased, built referral system. The schemes bear some weakness also which also better to mention for

further improvement of the schemes. These are: inadequate community mobilization for creating awareness on the

benefit of health insurance, low population coverage, high adverse selection Inadequate and weak Monitoring and

Supervision of DOHS and MOHP, increase the trend of moral hazards, higher administration cost, no linkage with other

income generating activities, inadequate ownership taken by community, additional workload for health staffs,

inefficient fund management and there is no legal backing found.

In conclusion, the analysis of community-based health insurance schemes in Nepal shows that their scope and impact is

very limited. In the view of the evaluation team, community-based health insurance, the way it is currently being

implemented, does not look promising in terms of building a comprehensive, equitable, empowering and sustainable

social health insurance system in Nepal, particularly as CBHI schemes do not have a strong support structure at a higher

level. Even though, players and providers in micro insurance sector are big in numbers, their coverage and impact in

Nepal is not significant. Hardly less than 1 per cent get the micro health insurance facilities over the country. Unless and

until all schemes are run under the umbrella of single organized and systematic institution, the result will not be fruitful

and successful.

______________________________________________________________________________ Community Based Health Insurance Practices in Nepal Page 15 of 15

REFFERENCES:

Ahuja, R. And Jutting J. (2003). Design of incentives in community based health insurance schemes. Indian Council For

Research On International Economic Relations. New Delhi.

Carrin ,G.,Waelkens,M. and Criel B. (2005).Community –based health insurance in developing countries: a study of its

contribution to the performance of health financing systems. Tropical Medicine and International Health, Vol

10,No.8, pp 799-811

CBS (2011). Nepal Population Report- 2012. Central Bureau of Statisitcs. Kathmandu

Ghimire, R. (2012). Principles of Insurance and Risk Management. Asmita Books:Kathmandu.

Heller, P. S. (2005). Understanding Fiscal Space. International Monetary Fund.

HSSP(2012).Review of Community-based Health Insurance Initiatives in Nepal. Health Sector Support Programme

Kenjiro, Y. ( )Why Illness Causes More Serious Economic Damage than Crop Failure in Rural Cambodia

MoF (2012). Economic Survey, 2011/12. Government of Nepal. Kathmandu.

MoHP (2011). Nepal Demographic and Health Survey, 2011

MoHP (2012) Nepal national health accounts, 2006/07–2008/09. Kathmandu: Health Economics and Financing Unit,

Ministry of Health and Population, Government of Nepal

MoHP (2012). Nepal National Health Accounts, 2006/2007 - 2008/2009. Ministry of Health and Population

Murdoch, J. (1995), Income Smoothing and Consumption Smoothing, in: Journal of Economic Perspectives, 9, 103–114.

OECD (2011).Health at a Glance, 2011: OECD Indicators.

Oxfam (2008). Government of Nepal scraps user fees for basic health care [Online]. 2008 [cited 2009 Feb 2]; Available

from: URL:http://www.oxfam.org.uk/applications/blogs/policy/2008/01

Roth, J., Michael J. and Liber D. (2007). The landscape of Microinsurance in the world's 100 poorest countries. The

Microinsurance Centre.

Shimeles, A. (2010). Community Based Health Insurance Schemes in Africa: the Case of Rwanda. AFRICAN

DEVELOPMENT BANK GROUP

Stoermer, M; Sharma, SS; Napierala, C; Silwal, PR (2009) Essential drug procurement and supply management system

in Nepal. Options for improvement. Kathmandu: GIZ/GFA Consulting Group GmbH, Health Sector Support

Programme

Tabor, S. R. (2005). Community-Based Health Insurance and Social Protection Policy. World Bank Institute.

WHO (2003).Drug and Money: Price, Affordability and Cost Containment. Amsterdam: IOS Press,

2003.http://archives.who.int/tbs/global/s4912e.pdf

World Bank (2011) Assessing Fiscal Space for Health in Nepal. Health Nutrition and Population, South Asia Region,

The World Bank.

World Health Organization, Geneva , (2003), “ Community based health insurance schemes in developing countries:

facts problems and perspectives”, Discussion Paper.