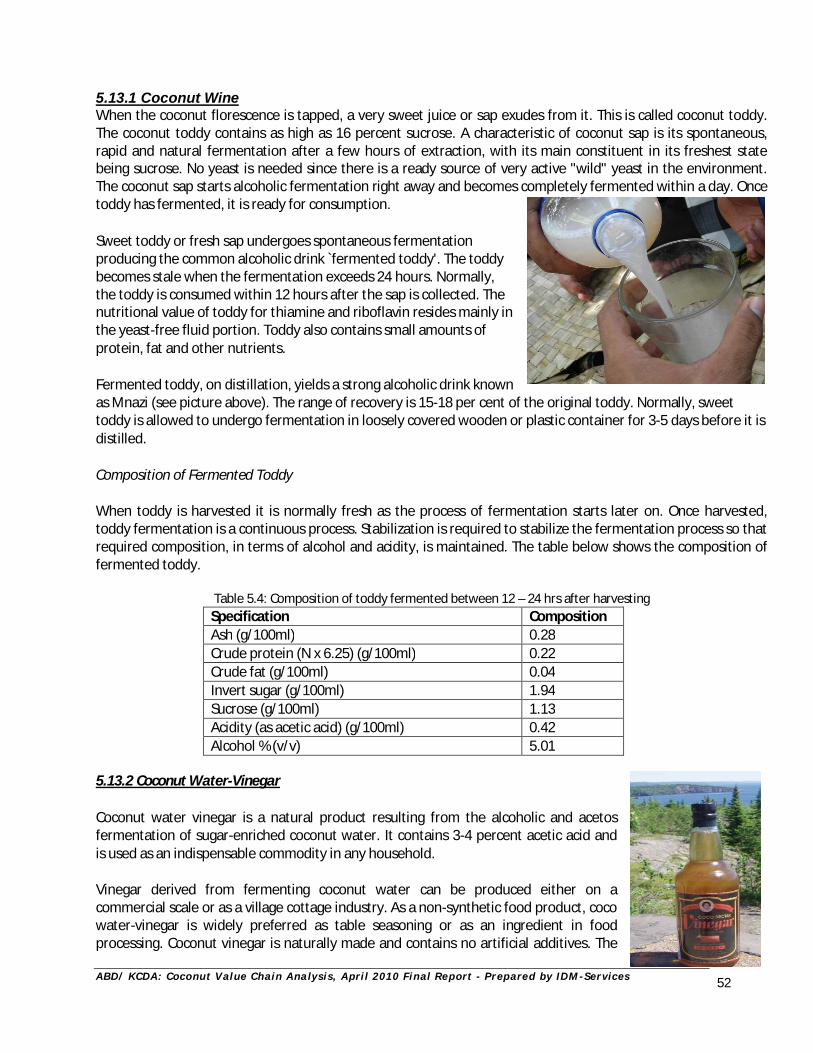

Embed Size (px)

Citation preview

ASPS-ABD/KCDA

COCONUT VALUE CHAIN ANALYSIS REPORT

Conducted By: INSTITUTION DEVELOPMENT & MANAGEMENT SERVICES [IDM]

Ambalal House, South Wing, 2nd Floor; P.O. Box 41825, Mombasa Tel: 041-2225403/ 020 2169840 Fax: 230084,

Cell: 0722 244686, Email: [email protected] Final Report – April 2010

A B D / K C D A : C oc o nu t V al ue C h ai n A na l y s i s , A pr i l 2 0 1 0 F i n a l R e p or t - P r e p ar e d by I D M - Se r v i c e s

ii

ASPS-ABD/KCDA

COCONUT VALUE CHAIN ANALYSIS

FINAL REPORT

Compiled By:

Githende Gachanja Muli Musinga Gitau Ngigi

Norbert Onyango John Bett

April, 2010

A B D / K C D A : C oc o nu t V al ue C h ai n A na l y s i s , A pr i l 2 0 1 0 F i n a l R e p or t - P r e p ar e d by I D M - Se r v i c e s

iii

TABLE OF CONTENTS Table of Contents …….…………………………………………….………………………………………………. iii List of Acronyms …………………………………………………………………………………………………. vi List of Tables …………..…….………………………………………………………………..………………. vii List of Charts …………..…………………………..………………………………………....………………. viii Acknowledgement …....………….…………………………………………………………………………………. ix Executive Summary ….……………………………………………………………………………………………... x 1.0 INTRODUCTION 1.1 Overview ……………………………………………………………………………………………….... 1 1.2 Background Information on the Project ...……………………………………………………..………………..…………………….. 1 1.3 Role of Agricultural Sector Programme Support (ASPS) in Kenya .....…………………………………………………………………………………………… 1 1.4 The Kenya Coconut Development Authority (KCDA) .........……………….................................................................................................... 2 1.5 Coconut Value Chain Analysis – Objectives ...…………………………………………………………………………………………….. 2 1.6 Study Methodology and Approach .....……………….………………………………………………………………………….. 3 2.0 OVERVIEW OF THE COCONUT SUB SECTOR - Trend Analysis 2.1 The Coconut Industry in Kenya - Background Information ……………………………………..………………………………………………………… 4 2.2 Population and Distribution of Coconut Trees within the Coast Province ..................................................................................................................................... 4 2.3 Coconut Products and Production ...............……………………………………………..……..………………………………. 6 2.4 Monetary Value of the Coconut Sub Sector ...…….……………………………………………………………………………………….. 7 2.5 Import and Export figures for Coconut Products 2006 – 2009 ..........………………………………………………………………………………………… 8

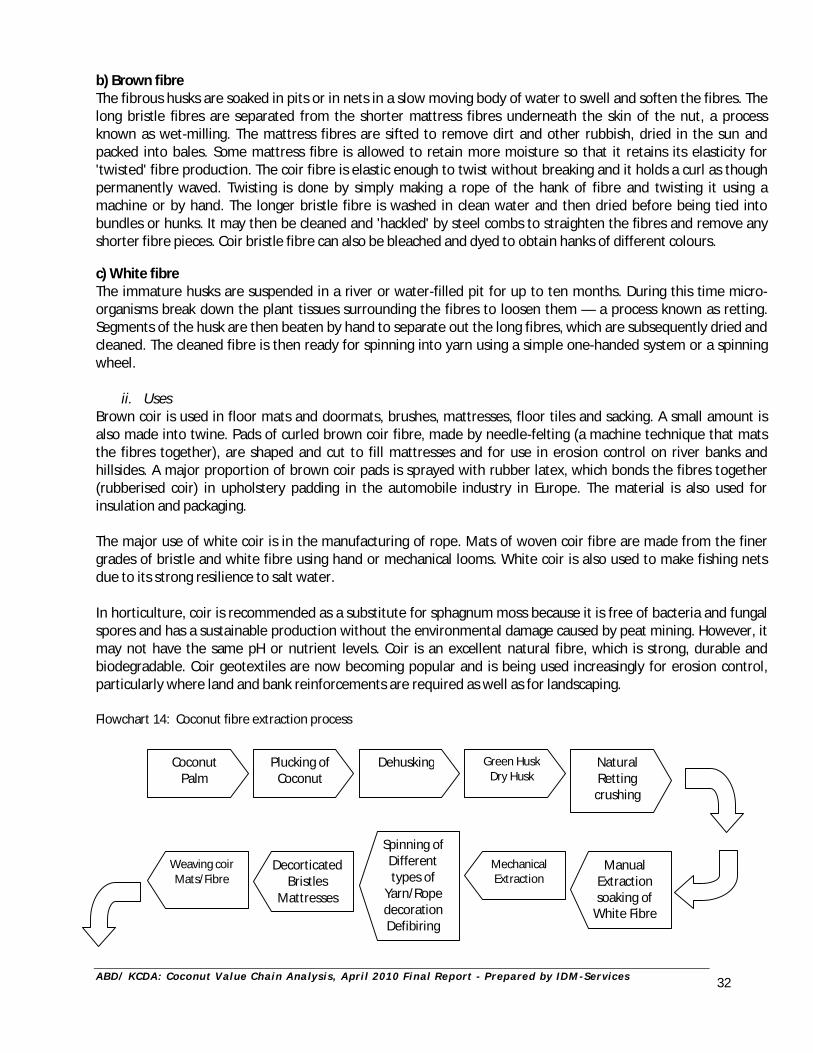

SECTION ONE COCONUT (MATURE NUT) VALUE CHAIN ANALYSIS

3.0 Overview of the Dry Nut Value Chain …………………………………...………………………….…….………………………… 11 3.1 The Nut Production Chain ..........…………………………………………………………..……….………….……….. 11

A B D / K C D A : C oc o nu t V al ue C h ai n A na l y s i s , A pr i l 2 0 1 0 F i n a l R e p or t - P r e p ar e d by I D M - Se r v i c e s

iv

3.2 Coconut Dry Nut Value Chain Actors and Functions ………………………………………………………………………………………………. 14 3.3 Processed Coconut Products and their Uses ..………………………………………………….……………….………………………… 25

3.4 Standards and Quality Control for Coconut Products .…………………………………….…...…................................................................... 32

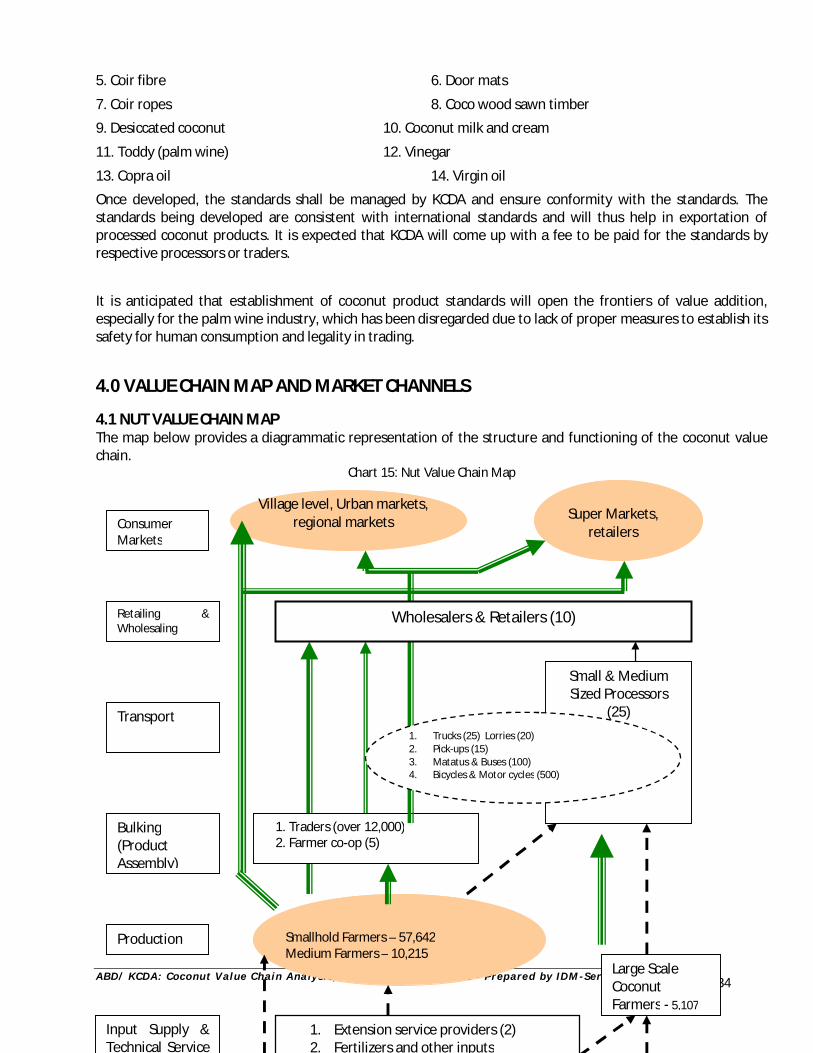

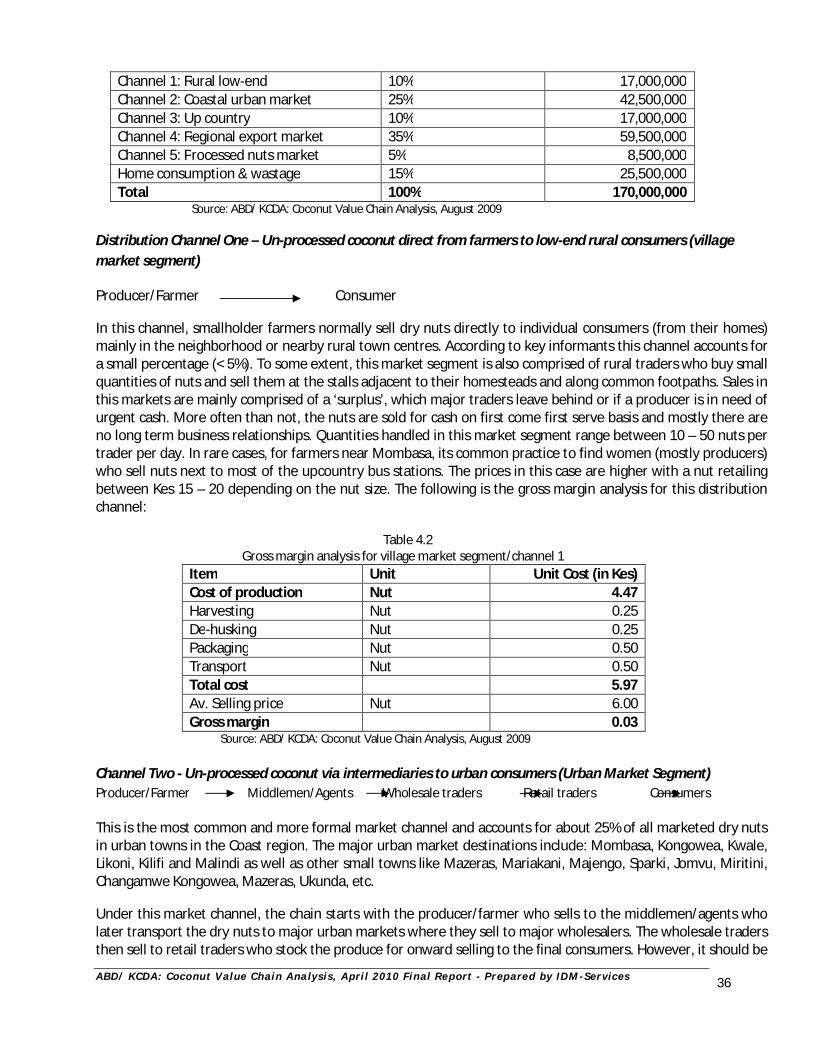

4.0 VALUE CHAIN MAP AND MARKET CHANNELS 4.1 Nut Value Chain Map …………………………………………………………………………………………….... 33 4.2 Dry Nut Marketing and Distribution Channels ……..……………………………………………………………………………………….. 34

SECTION TWO COCONUT WINE INDUSTRY VALUE CHAIN

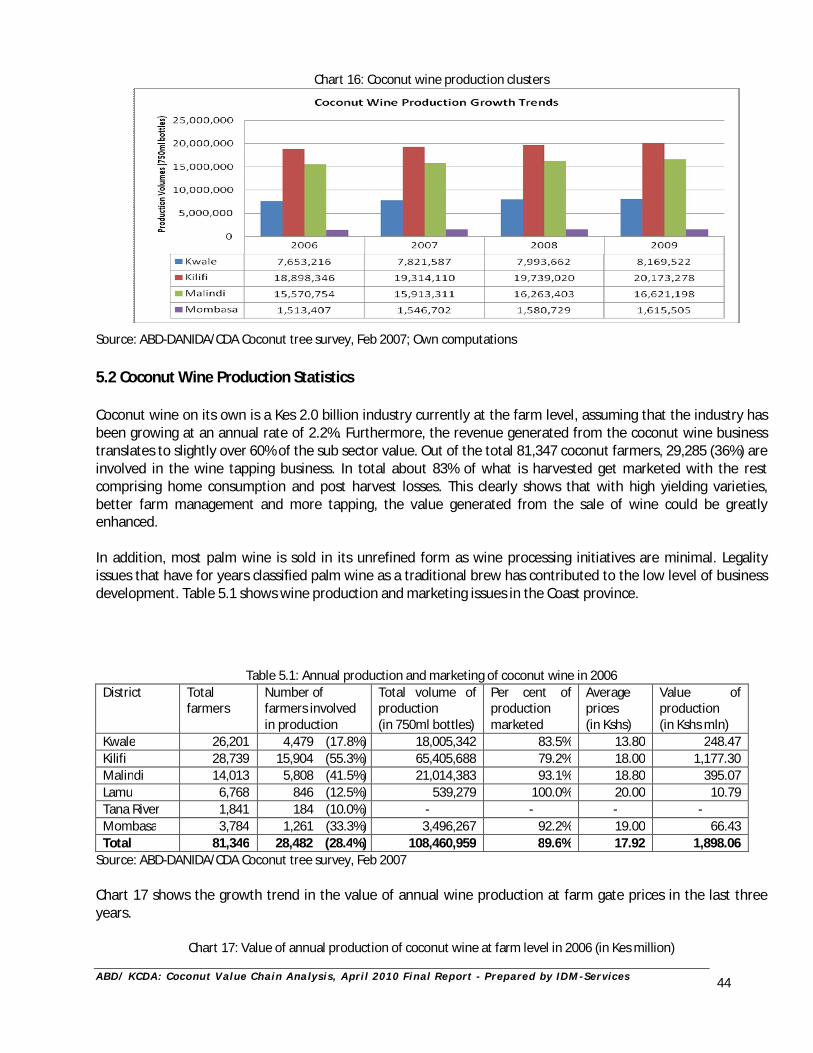

5.0 OVERVIEW OF THE COCONUT WINE CHAIN 5.1 Coconut Wine Production Clusters ……………………………………………………………………….……………………… 42 5.2 Coconut Wine Production Statistics …..………………………………………………………..………….……………………… 42 5.3 Coconut Trees Varieties and Toddy Production ………………………………………………..…….……………………………………….. 43 5.4 The Tapping Process .………………………………………………………………….………….……….………. 43 5.5 Tapping Tools ……………………………………………………………………..…………………..…….. 44 5.6 Toddy Production per Tree .………………………………………………………………………………………..……. 44 5.7 Production Seasonality ..………………………………………………………………………………………..……. 44 5.8 Analysis of Demand and Supply Gaps .………………………………………………………………..……………………………... 45 5.9 Toddy Price Variation across the Seasons .……………………………………………………….……………………………………… 46 5.10 Average Production per Farmer per Day ………………………………………………………………………………………………. 46 5.11 Quality of Toddy ……………………………………………………………………………………………….. 46 5.12 Coconut Wine Production Gross Margin Analysis ..………………………………..…………………………………………………………… 47 5.13 Coconut Toddy Products and Uses .………………………………………………………………….………………………….. 49 6.0 VALUE CHAIN FUNCTIONS AND ACTORS ….…………………………………..………………………………………………………. 53

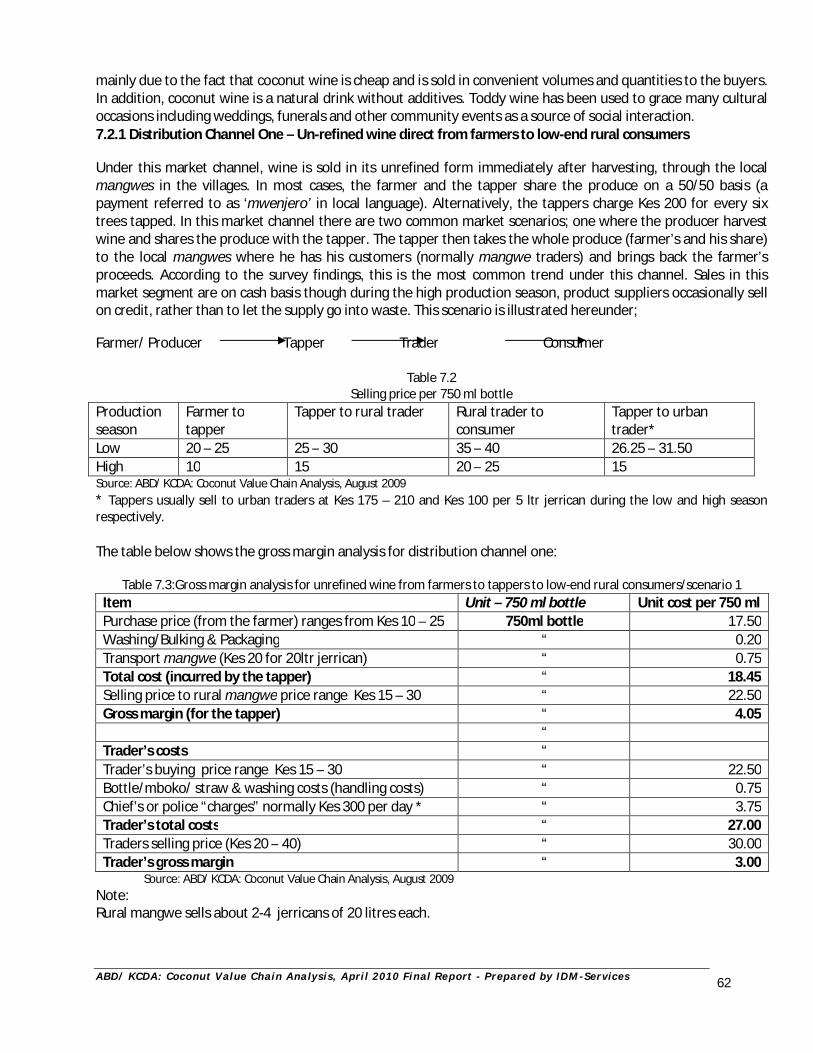

7.0 TODDY VALUE MAP AND MARKET CHANNELS 7.1 Toddy Value Chain Map ……..…………………….…………………………………………………………………… 58

A B D / K C D A : C oc o nu t V al ue C h ai n A na l y s i s , A pr i l 2 0 1 0 F i n a l R e p or t - P r e p ar e d by I D M - Se r v i c e s

v

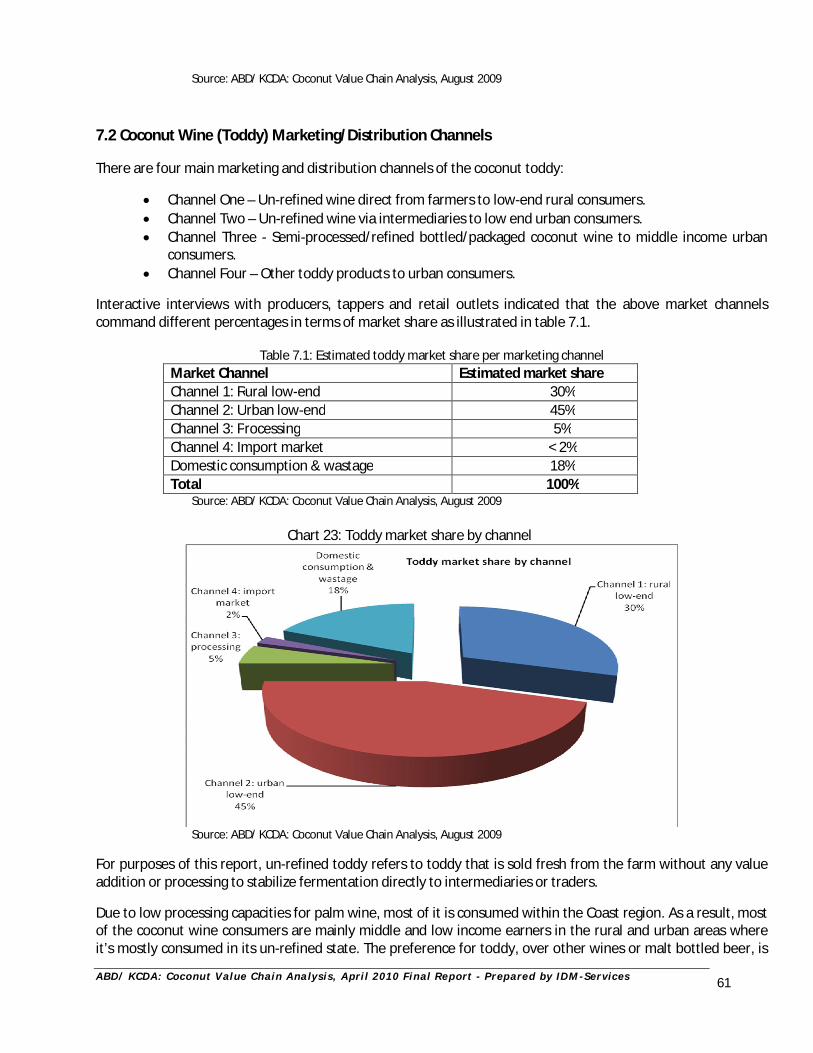

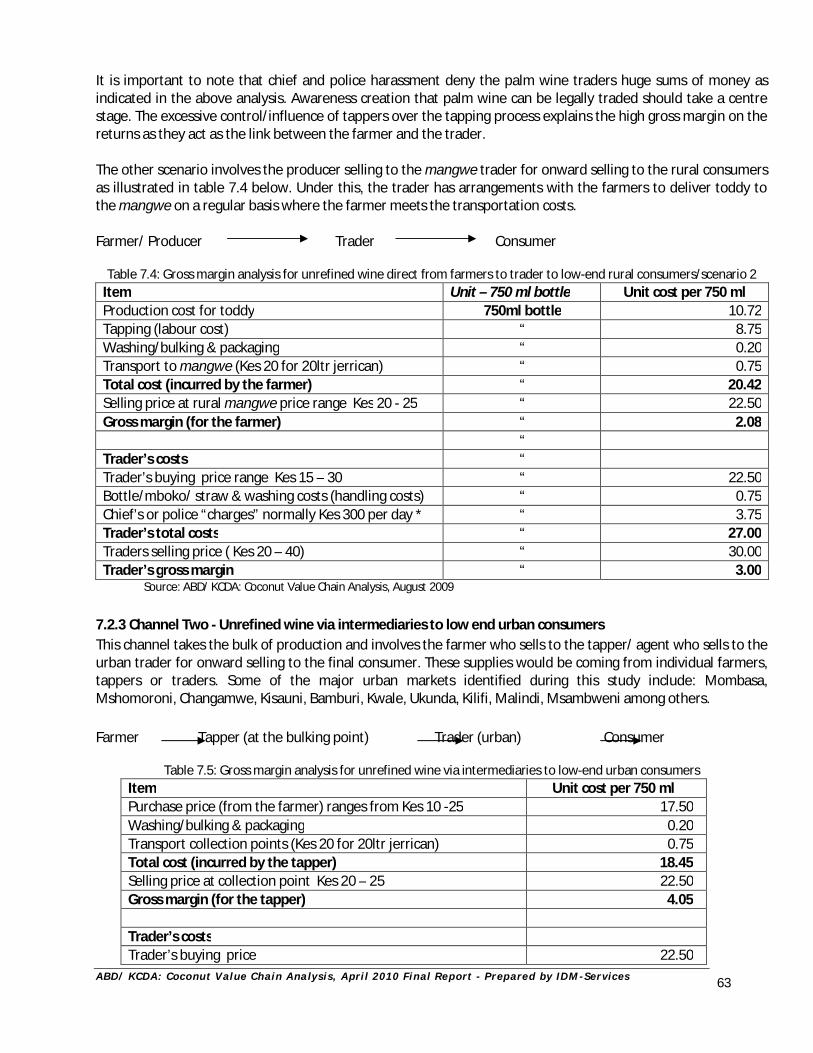

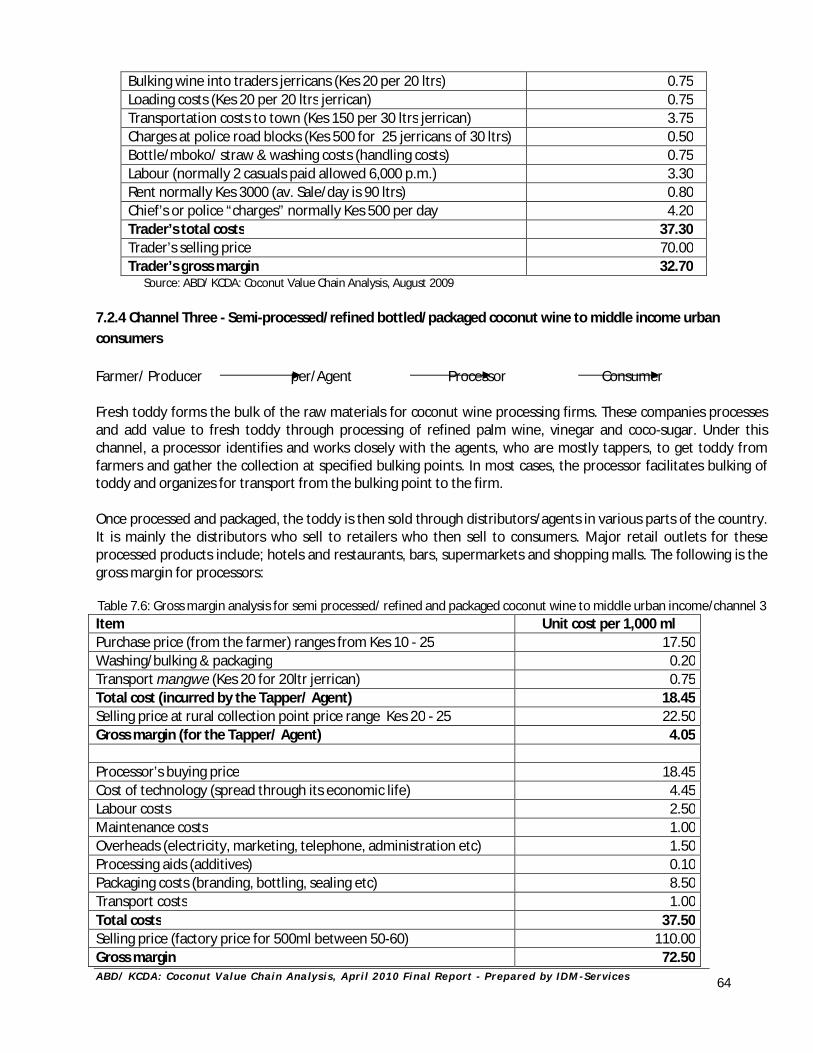

7.2 Coconut Wine (Toddy) Marketing/Distribution Channels ……………………………………….………………………………………………………. 59 8.0 OTHER COCONUT SUPPORTING CHAINS 8.1 Overview ………………………………………………………………………………………………. 64 8.2 The Trunk (Wood) ……………….………………………………………………….………………………….. 64 8.3 The Leaves ………………………………………………………………………………………..…….. 64 9.0 CHALLENGES FACING THE COCONUT VALUE CHAIN ………………………………………………………………………………………………. 66 10. OPPORTUNITIES WITHIN THE COCONUT VALUE CHAIN 10.1 Overview ………………………………………………………………………………………………. 68 10.2 Opportunities …………………………………..…………………………………….……………………. 68 11. SUMMARY OF FINDINGS AND CONCLUSIONS 11.1 Overview …..………………………………………………………………………………………….. 70 11.2 Summary of Key Findings ……………………………………………………………………………………………….. 70 12. RECOMMENDATIONS…..……………………………………………………………. 73

Annexes Annex 1: References Annex 2: Survey Instruments Annex 3: List of Key stakeholders for Draft Report and Dissemination workshop Annex 4: Coconut wine cash flow Annex 5: Nuts cash flow (pure stand) Annex 6: Nut cash flow (Multiple product production) Annex 7: List of Coconut Imports 2007 – 2009 Annex 8: Stakeholders’ Comments

A B D / K C D A : C oc o nu t V al ue C h ai n A na l y s i s , A pr i l 2 0 1 0 F i n a l R e p or t - P r e p ar e d by I D M - Se r v i c e s

vi

LIST OF ACRONYMS

AAEO - Assistant Agricultural Extension Officer

ABD - Agricultural Business Development

AEZ - Agro – Ecological Zones

ASPS - Agricultural Sector Programme Support

CDA - Coast Development Authority

CDO - Community Development Officer

CL - Coastal Lowlands

DAEO - District Agricultural Extension Officer

DANIDA - Danish International Development Agency

DAO - District Agricultural Officer

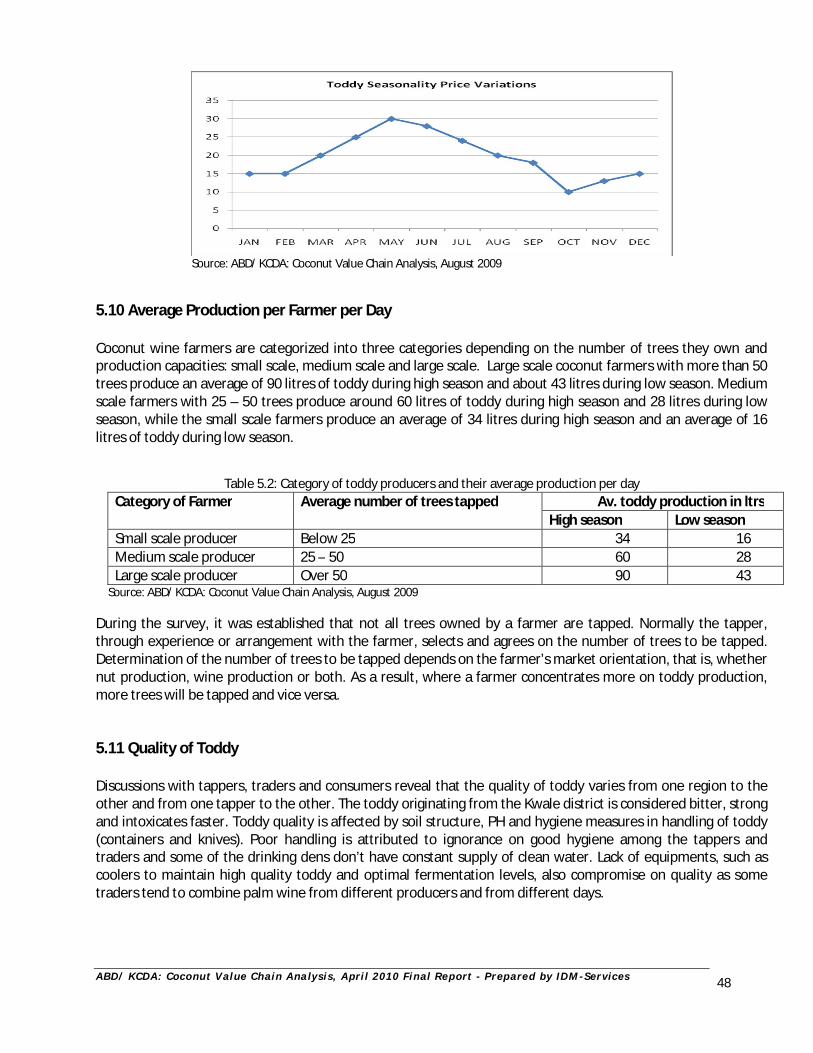

DCDO - District Crop Development Officer

GDP - Gross Domestic Product

KARI - Kenya Agricultural Research Institute

KCDA - Kenya Coconut Development Authority

KEBs - Kenya Bureau of Standards

KEPHIS - Kenya Plant Health Inspection Services

KenInvest - Kenya Investment Authority

KIE - Kenya Industrial Estates

KIRDI - Kenya Industrial Research Institute

KRA - Kenya Revenue Authority

Md - Man day

MoA - Ministry of Agriculture

NACADA - National Agency for the Campaign Against Drugs Abuse

PDA - Provincial Director of Agriculture

R &D - Research and Development ROI - Return on Investment

SMEs - Small and Medium Enterprises

TORs - Terms of Reference

VCA - Value Chain Analysis

VCO - Virgin Coconut Oil

A B D / K C D A : C oc o nu t V al ue C h ai n A na l y s i s , A pr i l 2 0 1 0 F i n a l R e p or t - P r e p ar e d by I D M - Se r v i c e s

vii

LIST OF TABLES TABLE PAGE Table 2.1 Population of Coconut Trees in Coast Province by District ……………………… 5 Table 2.2 Extrapolated Annual Production and Marketed Figures for various Coconut Products in 2006 - 2008 …………………………………………. 7 Table 2.3 Value of Annual Production of various Coconut Products at

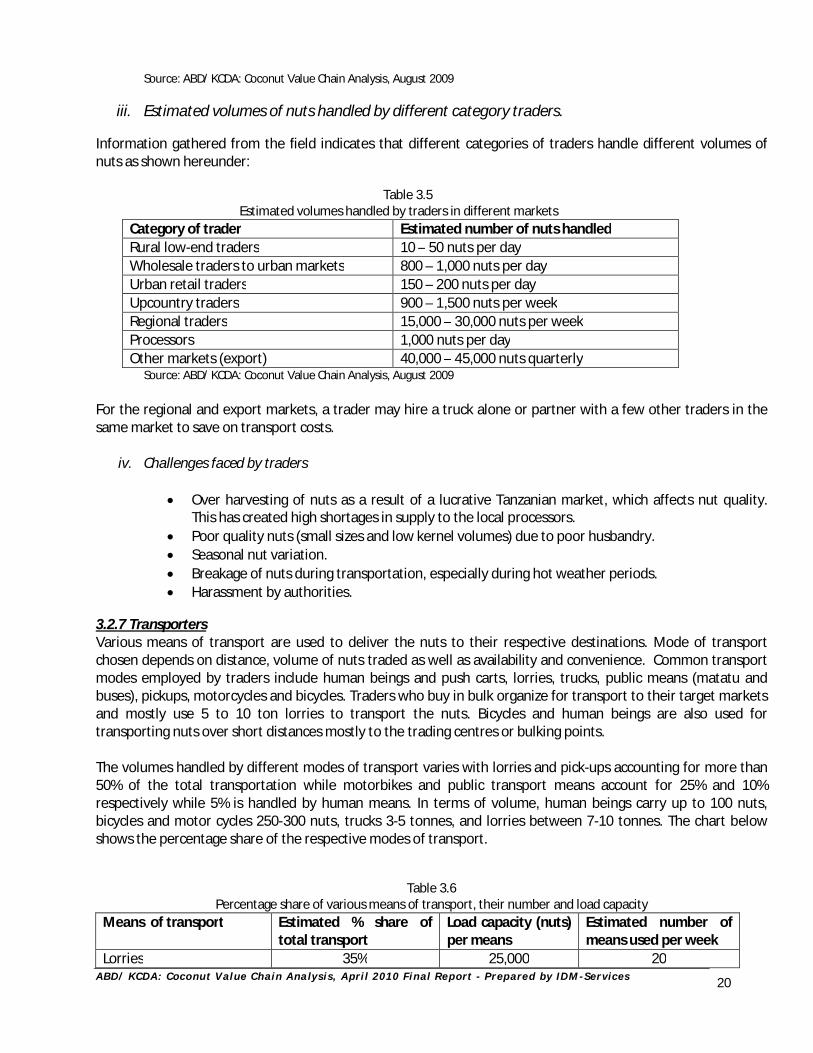

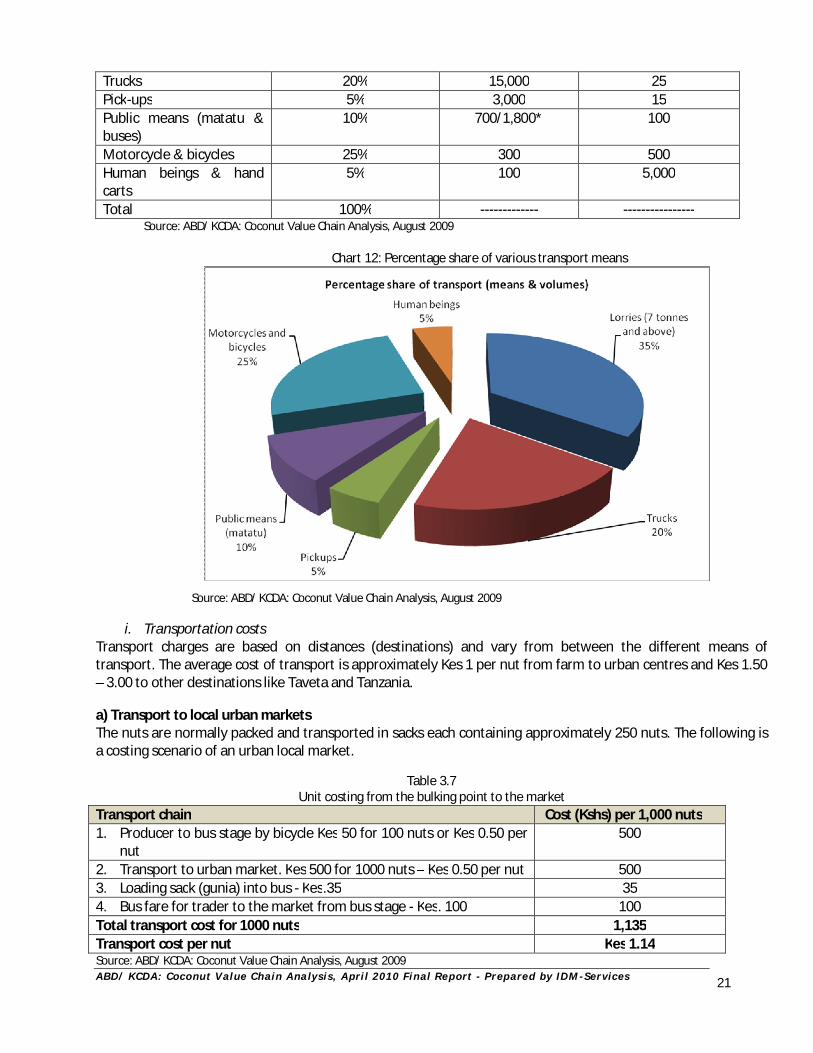

Farm Level in 2006 (in Kes million) ………………………………………………………………………………………….. 8 Table 3.1 Gross Margin Analysis for Coconut Production ……………………………….….. 13 Table 3.2 Categories of Producers based on the Number of Trees Held ………….…….… 15 Table 3.3 Annual Production and Marketing of Mature Nuts in 2006 ………………..…….. 15 Table 3.4 Estimated Number of Traders in different Markets ………………………….…… 18 Table 3.5 Estimated Volumes handled by Traders in different Markets …………….…….. 19 Table 3.6 Percentage Share of various means of Transport, their

Number and Load Capacity ………………………………………………………… 19 Table 3.7 Unit costing from the Bulking Point to the Market ……………………………….. 20 Table 3.8 Unit Costing for Transport to Regional Markets ……………………………….…. 21 Table 4.1 Estimated Annual Nut Market Share per Marketing Channel ………………….. 34 Table 4.2 Gross Margin Analysis for Village Market Segment/Channel 1 …………..…. 35 Table 4.3 Gross Margin Analysis for Unprocessed Dry Nuts for Urban Market Segment/Channel 2 .………………………………………………. 35 Table 4.4 Gross Margin Analysis for Unprocessed Dry Nuts for Upcountry Market Segment/Channel 3 ……………………………………………… 36 Table 4.5 Gross Margin Analysis for Unprocessed Dry Nuts for

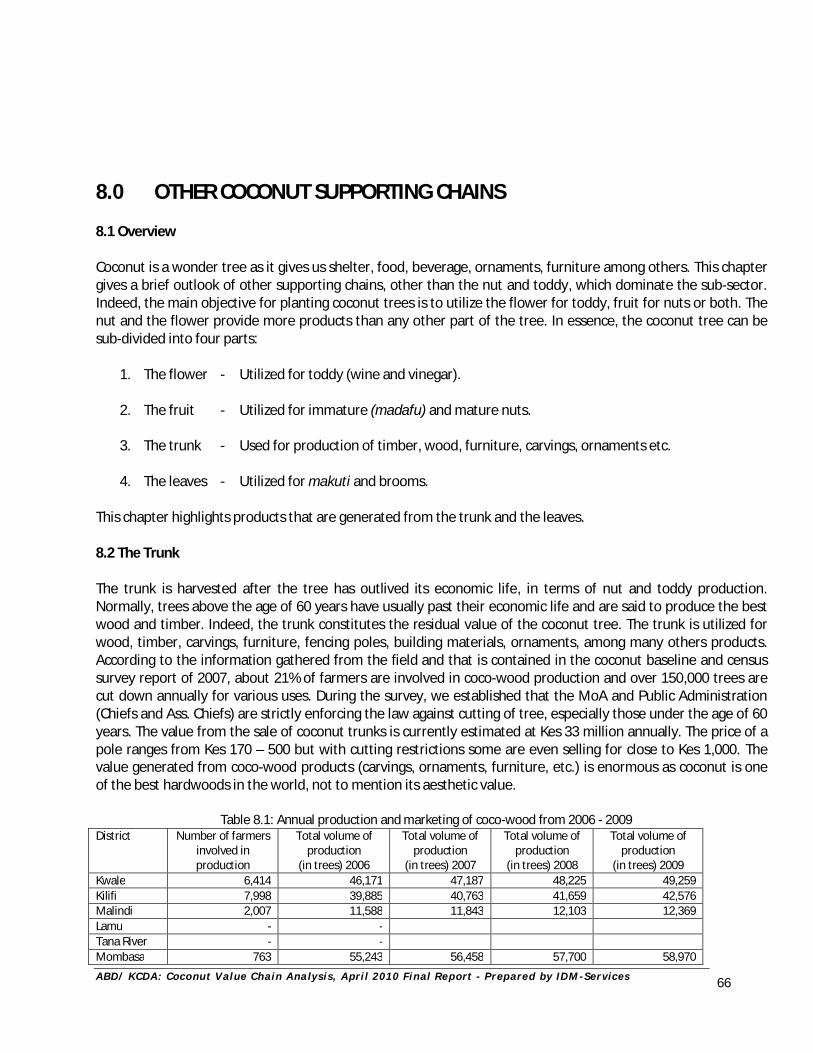

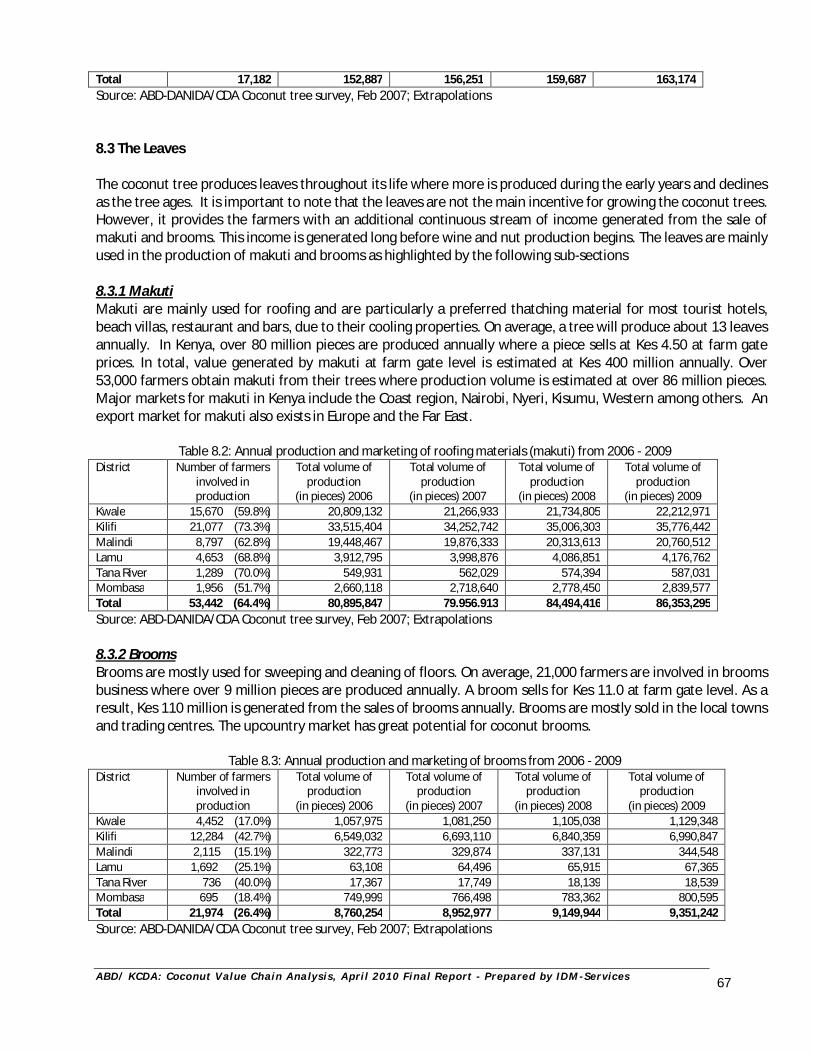

Export Market Segment/Channel 4 …………………………………………………. 37 Table 4.6 Value Added by Traders to Dubai Export Market ………………………….…….. 38 Table 4.7 Gross Margin Analysis for Processed Desiccated Coconut …………………….. 39 Table 4.8 Gross Margin Analysis for Processed Virgin Coconut Oil ……………………….. 40 Table 5.1 Annual Production and Marketing of Coconut Wine in 2006 …………….……… 43 Table 5.2 Category of Toddy Producers and their Average Production per day …………. 46 Table 5.3 Coconut Wine Production Gross Margin Analysis …………………………….…. 48 Table 5.4 Composition of Toddy Fermented between 12 – 24 hrs after Harvesting …….. 50 Table 6.1 Category of Toddy Producers and their Average Production per day …………. 53 Table 6.2 Number of Tappers in Coast Province ……………………………………………… 54 Table 6.3 Estimated Number of Traders in Coast Province ……………………………..…… 55 Table 6.4 Estimated Number of Transporters in Coast Province ……………………….….. 55 Table 7.1 Estimated Toddy Market Share per Marketing Channel ………………..……….. 59 Table 7.2 Selling Price per 750 ml bottle .……………………………………………………… 60 Table 7.3 Gross Margin Analysis for Unrefined Wine direct from Farmers to Low-end Rural Consumers/Scenario 1 …………….………………………………. 60 Table 7.4 Gross Margin Analysis for Unrefined Wine direct from Farmers to Low-end Rural Consumers/Scenario 2 …………………….………………………. 61 Table 7.5 Gross Margin Analysis for Unrefined Wine via Intermediaries to Low-end Urban Consumers …………………………………………………………. 61 Table 7.6 Gross Margin Analysis for Semi Processed/Refined and Packaged Coconut Wine to Middle Urban Income/Channel 3 ..………………… 62 Table 8.1 Annual Production and Marketing of Coco-Wood from 2006 - 2009 ……………………… 64 Table 8.2 Annual Production and Marketing of Roofing Materials (makuti) from 2006 - 2009 ……. 65 Table 8.3 Annual Production and Marketing of Brooms from 2006 - 2009 ……………………………. 65

A B D / K C D A : C oc o nu t V al ue C h ai n A na l y s i s , A pr i l 2 0 1 0 F i n a l R e p or t - P r e p ar e d by I D M - Se r v i c e s

viii

LIST OF CHARTS

CHART PAGE Chart 1: Distribution of Coconut Trees in Coast Province by District ………..……….…. 5 Chart 2: Growth Trend (Population of Coconut Trees) ……………………………………. 6 Chart 3: Monetary Value of Key Coconut Products ………………………………………... 6 Chart 4: Monetary Value of Annual Processed Coconut Imports in Kes ………………... 8 Chart 5: Volume of Annual Processed Coconut Imports in Kgs …………………………. 9 Chart 6: Raw Nuts Exports through Taveta Border ………………………..……………... 10 Chart 7: Nut Export through Lunga Lunga Border ………………………………………… 10 Chart 8: Nut Production Seasonality Chart ……………………………………….………… 12 Chart 9: Nut Seasonality Price Variation Chart …………………………………………….. 12 Chart 10: Comparison between Nuts Demand and Supply ……………………………… 13 Chart 11: Annual Production and Marketing of Mature Nuts for 2006-2009 ……………… 16 Chart 12: Percentage Share of various Transport Means …………………………………. 20 Chart 13: Coconut (Mature Nut) Processing ………………………………………………… 25 Flowchart 14: Coconut Fibre Extraction Process ………………………………………………… 31 Chart 15: Nut Value Chain Map …………………………………………………………….... 33 Chart 16: Coconut Wine Production Clusters ………………………………………………… 42 Chart 17: Value of Annual Production of Coconut Wine at

Farm Level in 2006 (in Kes million) ………………………………………………… 43 Chart 18: Toddy Production Seasonality Chart ………………………………………………. 45 Chart 19: Toddy Supply and Demand Curves ………………………………………………… 45 Chart 20: Toddy price Variations across the Seasons ………………………………………. 46 Flowchart 21: Coconut Processing …………………………………………………………………. 49 Figure 22: Coconut Toddy Value Chain Map ………………………………………………….. 58 Chart 23: Toddy Market Share by Channel …………………………………………………… 59

A B D / K C D A : C oc o nu t V al ue C h ai n A na l y s i s , A pr i l 2 0 1 0 F i n a l R e p or t - P r e p ar e d by I D M - Se r v i c e s

ix

ACKNOWLEDGEMENTS

We would sincerely wish to express our gratitude to many individuals and organizations, who have significantly contributed to the successful conclusion of the Coconut Value Chain Analysis Report. The funding of this project was provided by the Agricultural Business Development (ABD) programme of the Agricultural Sector Programme Support (ASPS) and implemented in collaboration with the Ministry of Agriculture, Government of Kenya. We are also grateful to the support extended by the Kenya Coconut Development Authority (KCDA) and Municipal Council of Mombasa who provided us with vital information that enabled us to compile this report. Special thanks go to the ABD team in the Coast region especially the Regional Coordinator Mr. George Mazuri; District Coordinator Malindi Mr. Genya Nyale; District Coordinator Kwale, Mrs. Claris Kionge; the Managing Director KCDA, Mr. Jonathan Sulubu and the Senior Advisor ABD, Mr. Bjarne Christensen for the support and approval of this project. Special thanks go to the staff of the Kenya Coconut Development Authority (KCDA), especially Mr. Ngugi Ticha, Mr. Patrick Onchieku and Ms Miriam Mutuku, who provided liaison throughout the project. The success of the coconut value chain analysis was a joint effort by the staff of the Ministry of Agriculture from the five targeted districts of the Coast Province, farmers, traders, processors and leading supermarkets in the country. We particularly register our appreciation to the Provincial Director of Agriculture, Mrs Phoebe Odhiambo and the District Agri-Business Development Officers who included; Amos Rukwaro of Malindi, James Njoroge of Kwale , Harrison B Mghana of Msambweni, Fredrick Aoko of Kilifi and John Ouko of Kaloleni district. We further pay special tribute to the team of over 30 research assistants for the many hours put into data collection and information gathering in all the targeted areas. We would also wish to recognize the good work performed by the IDM Team of Officers who worked tirelessly to ensure timely completion of this assignment. It is also important to acknowledge the contribution of the coconut stakeholders who provided valuable critique that shaped the final outcome of the report. We are particularly indebted to Mr. Mwangi Njoya of Msambweni Development Company, Mr Kimathi of Kenya Industrial Estate (KIE), Dr. Linus Kasambo of KIRDI and Mr. Peter Nyachwaya, Regional Co-ordinator of the Export Promotion Council, for their very valuable contributions. While many individuals and organizations have participated in varied ways to the outcome of this report including providing useful comments and observations, the opinions expressed in this report (or any errors therein) are solely those of the authors of the report and should not be misconstrued as the official position of ABD, KCDA, MoA or any other institution or persons that helped in accomplishing this work. To all those mentioned above and others who may in one way or the other have contributed to the success of this project, we are indeed very grateful. Githende Gachanja Project Lead Consultant - IDM SERVICES

A B D / K C D A : C oc o nu t V al ue C h ai n A na l y s i s , A pr i l 2 0 1 0 F i n a l R e p or t - P r e p ar e d by I D M - Se r v i c e s

x

EXECUTIVE SUMMARY The Coconut Value Chain Analysis project was commissioned by ABD and KCDA in May 2009 and contracted to Institution Development and Management (IDM) Services after an open tendering process. This Final Report gives a detailed account of the Coconut Value Chain Analysis that has been undertaken and completed by the consultant since the project was commissioned. The Terms of Reference (ToRs) provided by ABD and KCDA required that IDM undertook the assignment of the Coconut Value Chain Analysis to the satisfaction of the coconut industry stakeholders.

The main objective of this project was to analyze and document credible information within the coconut value chains (nuts and toddy) and other supporting value chains that facilitate business development in the sub-sector. The exercise was expected to identify the key players and actors along the coconut value chain; analyze all major products within the chain from the seedling/conception stage to consumption and disposal of all products generated during the life span of the coconut tree. This process involved in-depth analysis of inputs at the initial stage, thorough reviewing of the production and bulking processes, evaluating transport and storage factors, documenting marketing processes in both whole-selling and retailing, identifying business opportunities, documenting key challenges facing the sub-sector and generating recommendations to guide the way forward. The project was also expected to identify major coconut product chains and assess their respective quantities and market channels as well as analyze production costs and identify key factors that influence market pricing. It was also supposed to evaluate and establish the unit production cost of Nuts and Toddy, taking into consideration the life span of the coconut trees. The project was also required to generate reliable data in regard to coconut products, domestic consumption and export quantities in the last 3 years and identify their respective destinations. It was also expected to document coconut products, which are imported and identify their value and origin.

The Survey used the administrative structures of the Ministry of Agriculture and the coconut sub-sector market structures to collect data from major coconut growing Districts of the Coast region. It was also expected to document bulking and transport facilities, coconut processing units, market outlets in the Coast region and other areas. Primary data collection was done by a team of over 30 trained research assistants and MoA District Agri-business Development Officers, independently recruited and supervised on a daily basis by IDM Research Coordinators. In total, over 100 coconut producers, tappers, processors, retailers, transporters and middlemen were interviewed across the coconut belt of the Coast Province. Other strategically selected areas were also visited i.e. Taveta, Lunga Lunga, Nairobi, Kisumu and Busia. It is important to note that these areas are important coconut product markets and transit outlets for coconut exports. In addition, a thorough literature review was conducted to contextualize and benchmark findings of the survey. Key Findings Coconut Potential From the findings of the study, the coconut value chain has a lot of un-tapped potential. According to a recent baseline survey on the coconut sub sector, the value of the sub sector is estimated at Kes 4 billion at farm gate price. Nut and wine are the key driving products of the coconut sub-sector. It is estimated that the coconut sub-sector could potentially be generating over Kes 20 billion with better production methods and enhanced value addition. Coconut wine production currently stands at 2.5 litres per tree, which is relatively low compared to optimal productivity levels of over 5 litres expected in good yielding varieties. While wine production and marketing contributes to more than half of the sub sector value, only 36% of the coconut farmers are involved in this business. The low participation rate of farmers is generally attributable to poor development of the wine

A B D / K C D A : C oc o nu t V al ue C h ai n A na l y s i s , A pr i l 2 0 1 0 F i n a l R e p or t - P r e p ar e d by I D M - Se r v i c e s

xi

markets in some of the regions in the coconut belt. This is mostly due to religious beliefs and harassments from over zealous law enforcement agencies. The nut chain, on the other hand, reveals great untapped potential as most products are sold in unprocessed form. Information from the study indicates that most of the processed coconut products in our markets are imported at a cost of over Kes 500 million annually. This situation can only be reversed through enhanced processing and value addition; a role that can be effectively played by private sector participants. Value Chain Actors Under the mature nut value chain, the study identified the following actors: Input suppliers and service providers, coconut producers, harvestors, de-huskers, traders and agents, transporters, wholesalers and retailers, government institutions, development agencies and consumers. Similarly, under the coconut wine chain, the following actors were identified: Input suppliers and service providers, coconut wine producers, tappers, traders and agents, transporters, wholesalers and retailers, government agencies and consumers. The number of these value chain actors fluctuates with the availability of other alternative employment opportunities particularly among the young unskilled actors. For instance, many coconut toddy tappers and dehuskers are moving away from the sub-sector to other income generating activities due to the pressure of high cost of living. Socio-Cultural Issues and Coconut Wine Coconut wine is deeply entrenched in the cultural practices and way of life of coastal communities. These cultural values have dictated that almost every farming household in the coconut belt has at least a few trees. This partly explains why some farmers will attempt to grow the crop even in fairly marginal areas. Overall, this cultural attachment has contributed to the large population of trees and seems bound to continue holding ground. The cultural entrenchment is exemplified by the widespread consumption of coconut products, especially the coconut wine. Coconut wine is a local drink of choice, a factor that plays a major part in driving the coconut industry. It is however clear that the coconut product market expansions must go beyond just the coastal region. As a positive mark, this trend is already current and it only needs to be further propelled. Information from the study shows that there is great demand for coconut products in all regions of the country especially wine and mature nuts. Coconut Wine Consumption Coconut wine remains a key driver in the coconut sub-sector with its production and marketing value accounting for more than Kes 2.5 billion of the sub-sector GDP. Similarly, according to the study findings, the consumption volume of wine is believed to be in excess of 100 million litres per year at the Mangwe levels. Information from the study indicated that there are over 3,600 mangwes in all the 1,800 villages in the Coast region. Considering there are over 8 million coconut trees in the coconut belt the potential for coconut wine is enormous. The Kes 42 billion beer industry has a 40% gap that is occupied by illicit brews that can easily be replaced by coconut wine. It is important to note that growth in the wine chain is currently hindered by a variety of drawbacks that include socio-cultural and religious factors, especially in the Islamic dominated areas. Local Markets Potential There is apparent high demand for both coconut (mature nuts) and wine in the up-country markets. It should be noted that the mature nut is popular in the upcountry markets i.e. Nairobi, Kisumu, Busia, Eldoret, etc. where it fetches premium prices. Coconut wine, on the other hand, can conveniently replace the illicit brews that dominate the low end market niche in the up-country. Unfortunately, these products are in short supply in all the up-country markets visited by the survey team. It is conclusive that with proper marketing of coconut products

A B D / K C D A : C oc o nu t V al ue C h ai n A na l y s i s , A pr i l 2 0 1 0 F i n a l R e p or t - P r e p ar e d by I D M - Se r v i c e s

xii

and value addition, the opportunities in these vast areas could be fully exploited thereby enhancing the income levels of sub sector players along the value chains. The private sector can play a lead role by availing the requisite investment for processing and marketing of coconut products. Nuts Export Markets Currently, Tanzania offers the largest market for Kenyan coconut exports. In total, nearly 4 million nuts are exported annually through Taveta and Lunga Lunga border towns. The documented nut export figures through these borders by HCDA and KEPHIS are slightly lower than the 4 million. During the survey, we established that some traders cross over to Tanzania without passing through these offices. Unfortunately, the prices offered to the farmers are relatively low, a factor that is attributable to the low level of farmer organizations, which curtails their bargaining power for better prices. Processing and Product Diversification The coconut is a versatile tree and yields and provides farmers with numerous product opportunities. It is evident from the study that the numerous opportunities within the coconut sub-sector have not been fully exploited, despite the high returns. These opportunities can be realized through processing and value addition. Information from the study indicates that there is need for product diversification using simple and affordable technology. Product diversification would effectively address the issue of import substitution, generate income and create employment. During the survey, it was observed that the income of coconut farmers could be tripled by product diversification and value addition. It is important to note that most of the processed coconut products in the Kenyan markets are imported from Asia. Integration of Stakeholders into the Coconut Industry Whereas there are various stakeholders with vast knowledge and technology to develop the coconut sub sector their integration has been minimal. For example, KIRDI has technologies, which could help to set up cottage industries but sub sector integration and adoption of new ideas and technologies remains limited. There are a number of locally developed coconut processing technologies which can serve as core ideas for potential rural-based enterprises. Establishment of rural based industries will not only increase utilization of coconut products at the domestic level but will also intensify the competitiveness in the industry. Laundry and toilet soaps, for example, are more expensive in the rural than in the urban areas because of distribution and marketing costs. There are still many traditional products that could be produced by small-scale industries, which could generate rural employment, increase utilization of coconut products and enhance farmers' incomes. Some of these products include; Virgin oil, coco sugar, vinegar, coconut milk, desiccated coconut, etc. It is imperative that stakeholders and service providers with critical information and technology are integrated into the coconut growers’ fraternity to facilitate experience sharing and technology transfers at all stages of the coconut value chain. KCDA should provide leadership in this regard. Post Harvest Handling and Losses According to the study, it is evident that there are challenges related to handling of both nuts and coconut wine. Poor handling may cause the nut to crack or damage the shell, thus reducing its quality and value. Some of the key processes in product handling i.e. de-husking, transport, storage, packaging etc. are not prudently managed at various levels along the value chain. The low levels of revenue generation in the sub-sector are attributable to poor handling and inefficient management at most levels along the coconut value chain. For instance, during tapping of coconut toddy, many farmers do not own cooling equipment; hence suffering enormous loses when their products go to waste. Other factors that contribute to post harvest handling and losses include poor market development and poor infrastructure in the coconut belt. Coconut Value Chain Challenges

A B D / K C D A : C oc o nu t V al ue C h ai n A na l y s i s , A pr i l 2 0 1 0 F i n a l R e p or t - P r e p ar e d by I D M - Se r v i c e s

xiii

The main challenges facing farmers at production level include; accessibility of quality planting materials, the menace of pests and diseases, limited extension services and low yield per tree. From a development perspective, this can be viewed as a challenge for finding more drought tolerant and high yielding tree varieties for both nuts and wine which is one of the key research areas that should be focused on. Challenges at market level include, inefficient marketing systems that are dominated by middlemen and brokers who dictate the terms of trade, lack of credit facilities and a general lack of processing facilities within the coconut belt. The above constraints have resulted to below optimal utilization of the sub sector potential. As a result, relevant stakeholders ought to develop proper mechanisms and initiatives to address these challenges so as to revamp the sub sector and fully exploit the economic benefits of the coconut tree. Processing and Value Addition related Challenges From the findings of the study, it is evident that the processing capacity is not properly developed. Coconut wine is generally perceived to be handled, traded and consumed under unhygienic conditions, a factor that discourages the urban up-market consumers. There is therefore need for appropriate initiatives towards reversing this negative trend as price differentials between local Mnazi and packaged wine are wide. With little value addition the lives of the sub sector players would be greatly transformed. From the results of the survey, the processing of the nuts is still limited to a few products despite its enormous potential to generate numerous products. This is a contraction considering that the local supermarkets are flooded with imported coconut products from India and Asia Pacific countries. Apparently, there has been a general lack of innovation in terms of affordable processing technologies that can be applied in rural areas. Similarly, there has been low investment in coconut processing as a result of low participation of the private sector players. Legal and Institutional Framework related Challenges Although the legal related issues have been addressed by the repeal of the Liquor Act and creation of KCDA, the situation on the ground is still shrouded with a lot of hindrances. For instance, the transport, consumption and trading of coconut wine is still conducted in a clandestine way. This has attracted the attention of unscrupulous law enforcement agents who use the advantage to harass and demand bribes from both the Mangwe operators and transporters. It is important that KCDA harmonizes coconut wine licensing with the existing Liquor Licensing Act There is therefore need for KCDA and other stakeholders to carry out awareness creation activities and educate the farmers, as well as wine traders, on their rights. This is probably the most lucrative chain and holds the key to the development and transformation of the coconut sub-sector.

A B D / K C D A : C oc o nu t V al ue C h ai n A na l y s i s , A pr i l 2 0 1 0 F i n a l R e p or t - P r e p ar e d by I D M - Se r v i c e s

1

1.0 INTRODUCTION 1.1 Overview

This report presents findings of a coconut value chain analysis (VCA) in Kenya commissioned in May 2009 by the Agricultural Business Development (ABD) in collaboration with the Kenya Coconut Development Authority (KCDA) contracted to Institution Development and Management Services (IDM Services) a private research and management consulting firm based in Mombasa. The assignment aimed at establishing and providing critical and credible information within the coconut value chain. The assignment was carried out over a three months period using the Ministry of Agriculture (MoA) structures where the firm closely worked with Agricultural Business Development Officers (ABDO) as they were deemed to have a better insight on agri-business issues, which is the main frame of this report. Data and information gathering was carried out in the months of June to August 2009 using a team of trained researchers with requisite knowledge and experience in the coconut sub sector, supervised closely by district coordinators from IDM. The project was undertaken within all the administrative districts of the Coast province i.e. Kwale, Kilifi, Kaloleni, Msambweni, Malindi, Lamu, Tana Delta, Tana River, Taita, Taveta, Kilindini, Mombasa and Kinango. It specifically focused on the local coconut product markets i.e. Mombasa, Malindi, Kilifi, Lamu, Mpeketoni, Kipini, Garsen, Kaloleni, Mazeras, Mariakani, Lungalunga, Taveta, Voi, Kinango, Kwale, Mtwapa, Ukunda etc. Other major coconut product markets outside the Coast region that were also visited included Nairobi and Kisumu and key border towns i.e. Taveta and Busia, where exports pass through. 1.2 Background Information on the Project. Following the successful completion of a baseline survey and census of coconut trees in Kenya and the subsequent formation of the KCDA, there was dare need to establish additional information relating to the coconut value chain. Such information related to establishing the key players within the value chain and their functions, gross margin distribution along the chain, unit production costs, pricing, value addition, domestic consumption and export markets among other issues. On 19th February 2009, during a national workshop held at Mombasa Beach Hotel to validate KCDA’s 5 year Strategic Plan, ABD made a commitment to provide financial support to undertake the Coconut Product VCA to help generate credible information about the sub sector. Indeed, ASPS funded 75% of the project cost with KCDA funding the remaining 25%. The information was deemed necessary if KCDA and other Development Agencies were to promote exploitation of the sub sector potential, which remains grossly untapped. With such information at hand, it would be possible to encourage investors into the sub sector, which is base to this study report. 1.3 Role of Agricultural Sector Programme Support (ASPS) in Kenya The Agricultural Sector Programme Support (ASPS) was initiated in July 2005 as a co-operation between the Government of Kenya and the Government of Denmark (Danida). The programme aims at linking smallholder farmers and Micro and Small Enterprises (MSEs) with the potential to further develop viable agricultural businesses. The programme focuses on improving production, creating employment, increasing income levels through agri- business initiatives, especially in semi arid districts, which are the main areas of focus for the programme. ASPS gives support to farmers in several districts of Eastern and Coast provinces, namely; Kitui, Taita Taveta, Makueni, Kwale, and Kilifi, Mwingi and Malindi districts with more districts being roped in. The ASPS has got three major components through which it supports farmers that includes; Agricultural Policy Support Facility (APSF), Agricultural Business Development Support (ABD) and Decentralized Agricultural Support Structures (DASS). The three components of ASPS were established to facilitate the transition of the agricultural sector where the private sector becomes the vehicle for economic growth while the public sector establishes a conducive environment for this development (asps-ke.org). The coconut value chain analysis project was

A B D / K C D A : C oc o nu t V al ue C h ai n A na l y s i s , A pr i l 2 0 1 0 F i n a l R e p or t - P r e p ar e d by I D M - Se r v i c e s

2

initiated by ASPS and funded through the ABD component, which mainly focuses on improving productivity, initiating agri-businesses and developing market linkages among the producers/farmers, Small and Medium Enterprises (SMEs) and Financial Service Providers. 1.4 The Kenya Coconut Development Authority (KCDA) KCDA was established through a legal notice No. 165 of the Kenya Gazette of 27th August 2007 under the provisions of the State Corporations Act. Its primary mandate is to regulate the coconut industry. Its core functions include:

Provide advisory services on matters related to the coconut industry to the government and to the industry for planning purposes.

Collect and collate data, maintain a database on the coconut industry and document and monitor the industry through registration of all players in the industry.

Assist in the production, processing, grading, storage, collection, transportation and warehousing of all the produce and bi-products destined for markets.

Arbitrate on disputes arising between growers and any of the players or among other players in the industry.

Vet and witness contract agreements between growers and any other players or between other players in the industry before they are executed.

Appoint agents for the implementation or performance of any function of the Authority under this Order.

Monitor imports and exports of coconut produce and bi-products through efficient management of the coconut industry.

1.5 Coconut Value Chain Analysis - Objectives The main objective of the study was to undertake a Coconut Value Chain Analysis and disseminate detailed and credible information on the industry’s main value chains (nuts and toddy) and other supporting value chains for business development by various industry players. Specific objectives/tasks under the assignment as defined by the terms of reference -ToR included the following;

To document the key players along the coconut value chain. To analyze all the key products within the nut value chain from seedling to coco wood and by products

generated during the life span of the tree. To analyze all the key products within the toddy value chain. To identify the major coconut products and assess their respective market values. To analyze coconut products production costs and identify key factors that influence market pricing. To establish the unit production cost of nuts and toddy (litre) taking into consideration the life span of

the trees. To generate reliable data in regard to domestic consumption of coconut product and export quantities in

the last 3 years (2006 – 2008). To identify coconut product export destinations. To identify coconut products, which are imported and from which origin. To make appropriate recommendations to guide the way forward. To prepare a comprehensive coconut value chain report.

A B D / K C D A : C oc o nu t V al ue C h ai n A na l y s i s , A pr i l 2 0 1 0 F i n a l R e p or t - P r e p ar e d by I D M - Se r v i c e s

3

1.6 Study Methodology and Approach More often than not, value chain analyses are mainly qualitative opposed to quantitative. The coconut value chain analysis largely employed a survey methodology with a qualitative approach. To gather the required information, the following major activities were carried out:

Literature Review of relevant documents from various sources relating to the topic under study. Field Interviews with selected respondents/players drawn from a wide range of stakeholders and actors

from the coconut sub sector who included coconut farmers, cooperative societies, input suppliers, processors, local administration, tappers, traders, staff from the Ministry of Agriculture, Kenya Coconut Development Authority and transporters among others.

Focused Group Discussions (FDGs) with selected groups and stakeholders. The study covered seven districts of the Coastal region of Kenya, namely Kaloleni, Kilifi, Malindi, Mombasa, Taveta, Msambweni and Kwale. The main tools used for the study included an interview guide for the various value chain players and participatory observation guides during the harvesting, de-husking, bulking and transport, processing and marketing discussions with the concerned farmers, harvestors, de-huskers, traders, transporters, government agencies (Ministry of Agriculture and KCDA) and other relevant stakeholders. Telephone interviews were also used to collect vital information from key informants though on a limited scale. Stratified sampling was adopted for the study to identify all key sub sector players so as to have a sample, which is as representative as possible, to facilitate a comprehensive analysis on the coconut value chain.

A B D / K C D A : C oc o nu t V al ue C h ai n A na l y s i s , A pr i l 2 0 1 0 F i n a l R e p or t - P r e p ar e d by I D M - Se r v i c e s

4

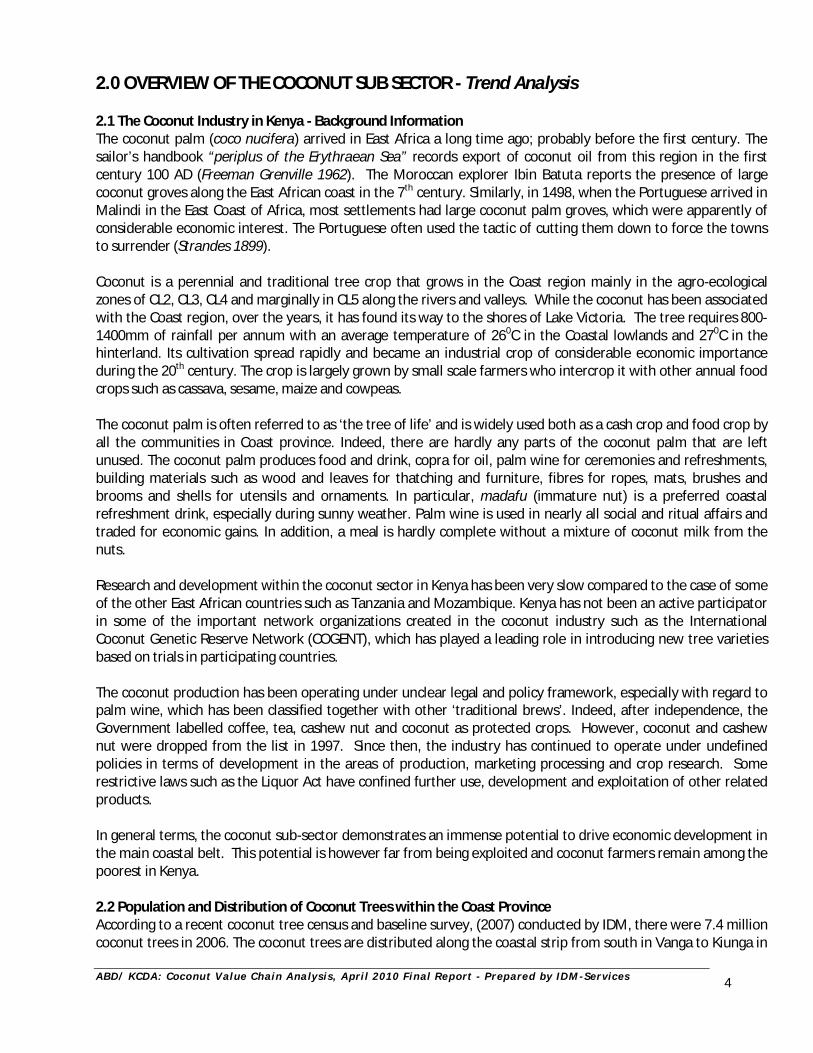

2.0 OVERVIEW OF THE COCONUT SUB SECTOR - Trend Analysis 2.1 The Coconut Industry in Kenya - Background Information The coconut palm (coco nucifera) arrived in East Africa a long time ago; probably before the first century. The sailor’s handbook “periplus of the Erythraean Sea” records export of coconut oil from this region in the first century 100 AD (Freeman Grenville 1962). The Moroccan explorer Ibin Batuta reports the presence of large coconut groves along the East African coast in the 7th century. Similarly, in 1498, when the Portuguese arrived in Malindi in the East Coast of Africa, most settlements had large coconut palm groves, which were apparently of considerable economic interest. The Portuguese often used the tactic of cutting them down to force the towns to surrender (Strandes 1899). Coconut is a perennial and traditional tree crop that grows in the Coast region mainly in the agro-ecological zones of CL2, CL3, CL4 and marginally in CL5 along the rivers and valleys. While the coconut has been associated with the Coast region, over the years, it has found its way to the shores of Lake Victoria. The tree requires 800-1400mm of rainfall per annum with an average temperature of 260C in the Coastal lowlands and 270C in the hinterland. Its cultivation spread rapidly and became an industrial crop of considerable economic importance during the 20th century. The crop is largely grown by small scale farmers who intercrop it with other annual food crops such as cassava, sesame, maize and cowpeas. The coconut palm is often referred to as ‘the tree of life’ and is widely used both as a cash crop and food crop by all the communities in Coast province. Indeed, there are hardly any parts of the coconut palm that are left unused. The coconut palm produces food and drink, copra for oil, palm wine for ceremonies and refreshments, building materials such as wood and leaves for thatching and furniture, fibres for ropes, mats, brushes and brooms and shells for utensils and ornaments. In particular, madafu (immature nut) is a preferred coastal refreshment drink, especially during sunny weather. Palm wine is used in nearly all social and ritual affairs and traded for economic gains. In addition, a meal is hardly complete without a mixture of coconut milk from the nuts. Research and development within the coconut sector in Kenya has been very slow compared to the case of some of the other East African countries such as Tanzania and Mozambique. Kenya has not been an active participator in some of the important network organizations created in the coconut industry such as the International Coconut Genetic Reserve Network (COGENT), which has played a leading role in introducing new tree varieties based on trials in participating countries. The coconut production has been operating under unclear legal and policy framework, especially with regard to palm wine, which has been classified together with other ‘traditional brews’. Indeed, after independence, the Government labelled coffee, tea, cashew nut and coconut as protected crops. However, coconut and cashew nut were dropped from the list in 1997. Since then, the industry has continued to operate under undefined policies in terms of development in the areas of production, marketing processing and crop research. Some restrictive laws such as the Liquor Act have confined further use, development and exploitation of other related products. In general terms, the coconut sub-sector demonstrates an immense potential to drive economic development in the main coastal belt. This potential is however far from being exploited and coconut farmers remain among the poorest in Kenya. 2.2 Population and Distribution of Coconut Trees within the Coast Province According to a recent coconut tree census and baseline survey, (2007) conducted by IDM, there were 7.4 million coconut trees in 2006. The coconut trees are distributed along the coastal strip from south in Vanga to Kiunga in

A B D / K C D A : C oc o nu t V al ue C h ai n A na l y s i s , A pr i l 2 0 1 0 F i n a l R e p or t - P r e p ar e d by I D M - Se r v i c e s

5

the north. While the tree is symbolic of the Coastal region, distributions are not even as there are areas with higher concentrations than others. In some areas of high tree population concentration, there are clearly identifiable production clusters (defined as areas with high concentrations of coconut trees and its producers/ farmers within a short distance of a radius of 5 - 8 km). This makes it easy to enjoy economies of scale, such as joint sourcing of services and attracting customers to the market, due to large volumes of production. Table 2.1 below shows the coconut tree population and distribution by districts where Kwale is the leading district closely followed by the Kilifi district. The average tree holding per farmer stands at 91.5 coconut trees.

Table 2.1: Population of coconut trees in Coast Province by district District Number of coconut trees Number of farmers Average trees

per farmer Number Per cent Number Per cent Kwale 2,895,427 39.0% 26,201 32.2% 111 Kilifi 2,831,978 38.1% 28,739 35.3% 99 Malindi 986,997 13.3% 14,013 17.2% 70 Lamu 434,105 5.8% 6,768 8.3% 64 Tana River 140,414 1.9% 1,841 2.3% 76 Mombasa 136,938 1.8% 3,784 4.7% 36 Total 7,425,859 99.9% 81,346 100% 91.5

Source: ABD-DANIDA/CDA Coconut tree survey, February 2007 Chart 1: Distribution of coconut trees in Coast Province by district

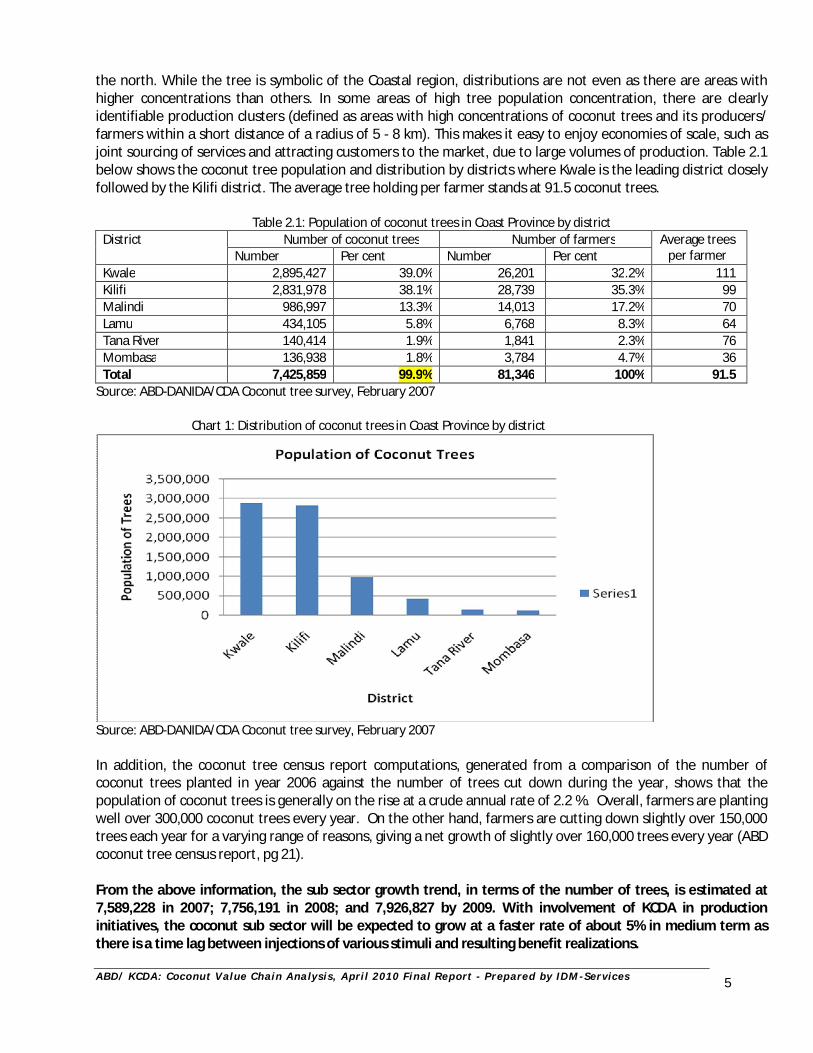

Source: ABD-DANIDA/CDA Coconut tree survey, February 2007 In addition, the coconut tree census report computations, generated from a comparison of the number of coconut trees planted in year 2006 against the number of trees cut down during the year, shows that the population of coconut trees is generally on the rise at a crude annual rate of 2.2 %. Overall, farmers are planting well over 300,000 coconut trees every year. On the other hand, farmers are cutting down slightly over 150,000 trees each year for a varying range of reasons, giving a net growth of slightly over 160,000 trees every year (ABD coconut tree census report, pg 21). From the above information, the sub sector growth trend, in terms of the number of trees, is estimated at 7,589,228 in 2007; 7,756,191 in 2008; and 7,926,827 by 2009. With involvement of KCDA in production initiatives, the coconut sub sector will be expected to grow at a faster rate of about 5% in medium term as there is a time lag between injections of various stimuli and resulting benefit realizations.

A B D / K C D A : C oc o nu t V al ue C h ai n A na l y s i s , A pr i l 2 0 1 0 F i n a l R e p or t - P r e p ar e d by I D M - Se r v i c e s

6

Chart 2: Growth Trend (Population of Coconut Trees)

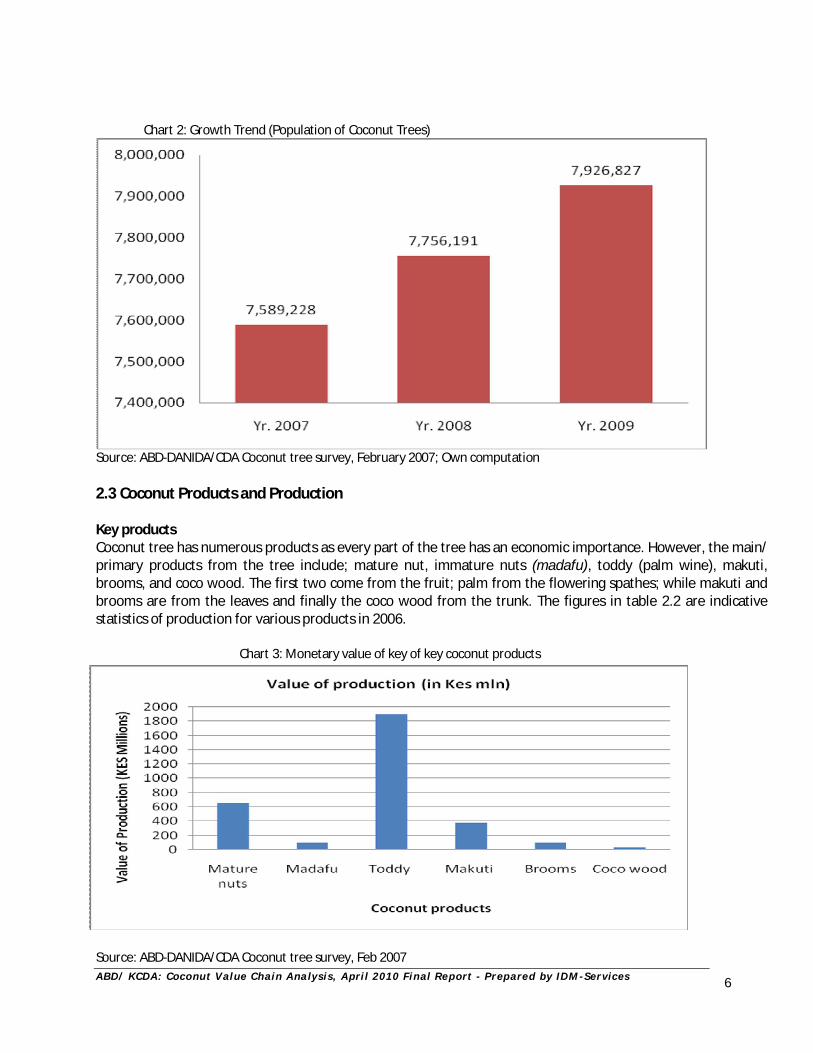

Source: ABD-DANIDA/CDA Coconut tree survey, February 2007; Own computation 2.3 Coconut Products and Production Key products Coconut tree has numerous products as every part of the tree has an economic importance. However, the main/ primary products from the tree include; mature nut, immature nuts (madafu), toddy (palm wine), makuti, brooms, and coco wood. The first two come from the fruit; palm from the flowering spathes; while makuti and brooms are from the leaves and finally the coco wood from the trunk. The figures in table 2.2 are indicative statistics of production for various products in 2006. Chart 3: Monetary value of key of key coconut products

Source: ABD-DANIDA/CDA Coconut tree survey, Feb 2007

A B D / K C D A : C oc o nu t V al ue C h ai n A na l y s i s , A pr i l 2 0 1 0 F i n a l R e p or t - P r e p ar e d by I D M - Se r v i c e s

7

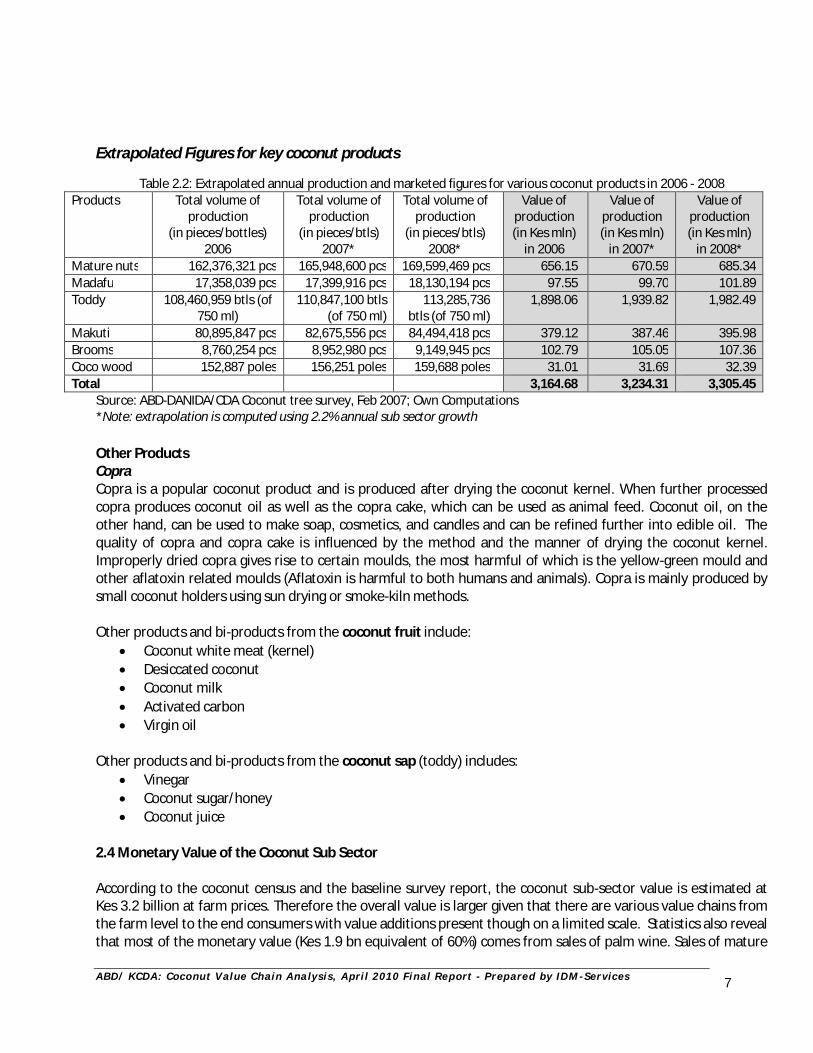

Extrapolated Figures for key coconut products

Table 2.2: Extrapolated annual production and marketed figures for various coconut products in 2006 - 2008 Products Total volume of

production (in pieces/bottles)

2006

Total volume of production

(in pieces/btls) 2007*

Total volume of production

(in pieces/btls) 2008*

Value of production (in Kes mln)

in 2006

Value of production (in Kes mln)

in 2007*

Value of production (in Kes mln)

in 2008* Mature nuts 162,376,321 pcs 165,948,600 pcs 169,599,469 pcs 656.15 670.59 685.34 Madafu 17,358,039 pcs 17,399,916 pcs 18,130,194 pcs 97.55 99.70 101.89 Toddy 108,460,959 btls (of

750 ml) 110,847,100 btls

(of 750 ml) 113,285,736

btls (of 750 ml) 1,898.06 1,939.82 1,982.49

Makuti 80,895,847 pcs 82,675,556 pcs 84,494,418 pcs 379.12 387.46 395.98 Brooms 8,760,254 pcs 8,952,980 pcs 9,149,945 pcs 102.79 105.05 107.36 Coco wood 152,887 poles 156,251 poles 159,688 poles 31.01 31.69 32.39 Total 3,164.68 3,234.31 3,305.45

Source: ABD-DANIDA/CDA Coconut tree survey, Feb 2007; Own Computations *Note: extrapolation is computed using 2.2% annual sub sector growth Other Products Copra Copra is a popular coconut product and is produced after drying the coconut kernel. When further processed copra produces coconut oil as well as the copra cake, which can be used as animal feed. Coconut oil, on the other hand, can be used to make soap, cosmetics, and candles and can be refined further into edible oil. The quality of copra and copra cake is influenced by the method and the manner of drying the coconut kernel. Improperly dried copra gives rise to certain moulds, the most harmful of which is the yellow-green mould and other aflatoxin related moulds (Aflatoxin is harmful to both humans and animals). Copra is mainly produced by small coconut holders using sun drying or smoke-kiln methods. Other products and bi-products from the coconut fruit include:

Coconut white meat (kernel) Desiccated coconut Coconut milk Activated carbon Virgin oil

Other products and bi-products from the coconut sap (toddy) includes:

Vinegar Coconut sugar/honey Coconut juice

2.4 Monetary Value of the Coconut Sub Sector According to the coconut census and the baseline survey report, the coconut sub-sector value is estimated at Kes 3.2 billion at farm prices. Therefore the overall value is larger given that there are various value chains from the farm level to the end consumers with value additions present though on a limited scale. Statistics also reveal that most of the monetary value (Kes 1.9 bn equivalent of 60%) comes from sales of palm wine. Sales of mature

A B D / K C D A : C oc o nu t V al ue C h ai n A na l y s i s , A pr i l 2 0 1 0 F i n a l R e p or t - P r e p ar e d by I D M - Se r v i c e s

8

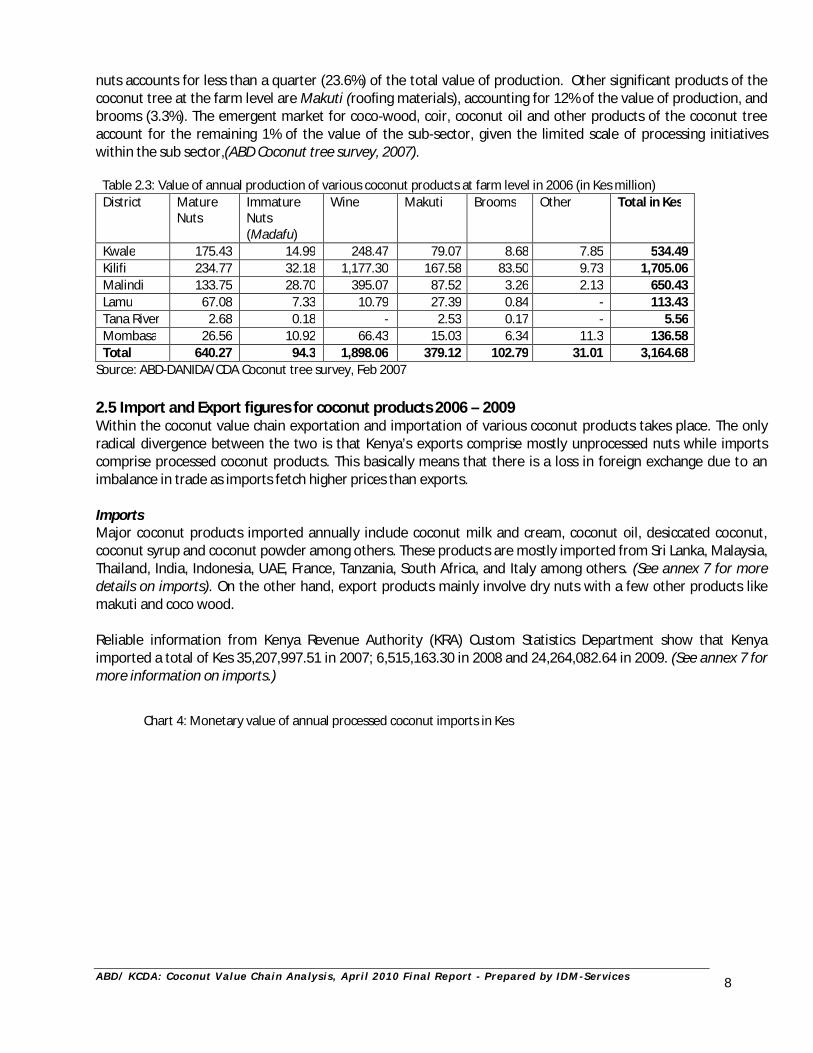

nuts accounts for less than a quarter (23.6%) of the total value of production. Other significant products of the coconut tree at the farm level are Makuti (roofing materials), accounting for 12% of the value of production, and brooms (3.3%). The emergent market for coco-wood, coir, coconut oil and other products of the coconut tree account for the remaining 1% of the value of the sub-sector, given the limited scale of processing initiatives within the sub sector,(ABD Coconut tree survey, 2007). Table 2.3: Value of annual production of various coconut products at farm level in 2006 (in Kes million)

District Mature Nuts

Immature Nuts (Madafu)

Wine Makuti Brooms Other Total in Kes

Kwale 175.43 14.99 248.47 79.07 8.68 7.85 534.49 Kilifi 234.77 32.18 1,177.30 167.58 83.50 9.73 1,705.06 Malindi 133.75 28.70 395.07 87.52 3.26 2.13 650.43 Lamu 67.08 7.33 10.79 27.39 0.84 - 113.43 Tana River 2.68 0.18 - 2.53 0.17 - 5.56 Mombasa 26.56 10.92 66.43 15.03 6.34 11.3 136.58 Total 640.27 94.3 1,898.06 379.12 102.79 31.01 3,164.68

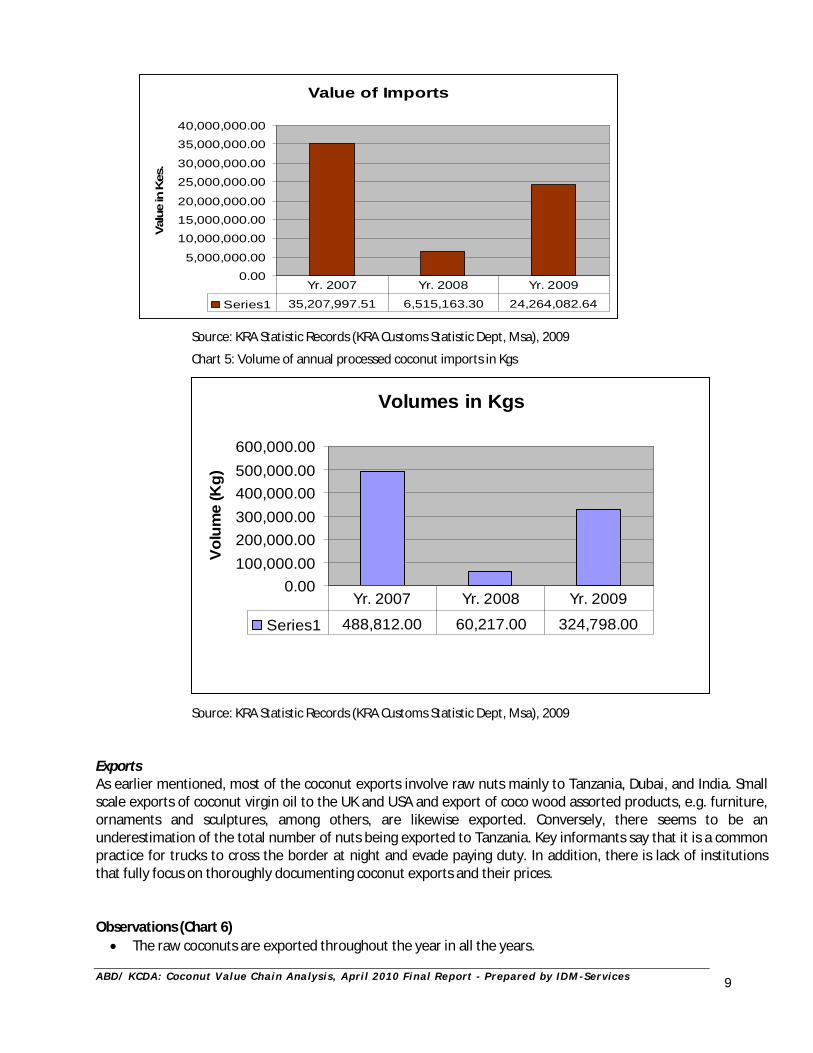

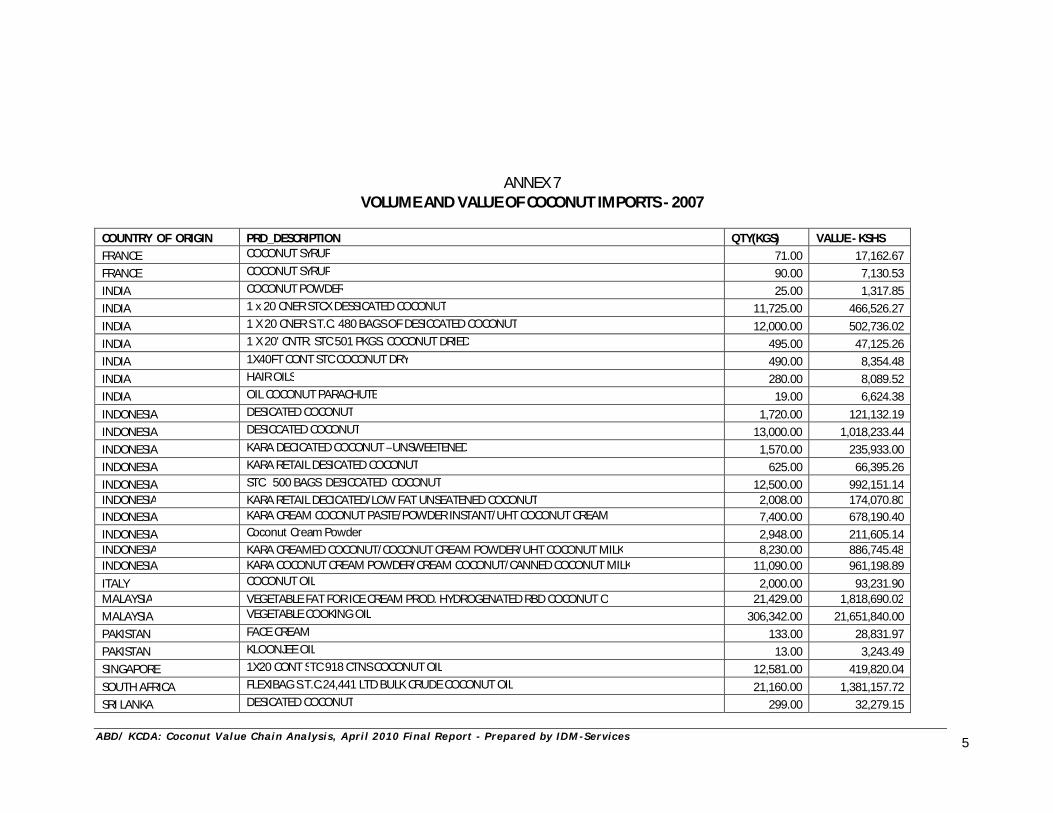

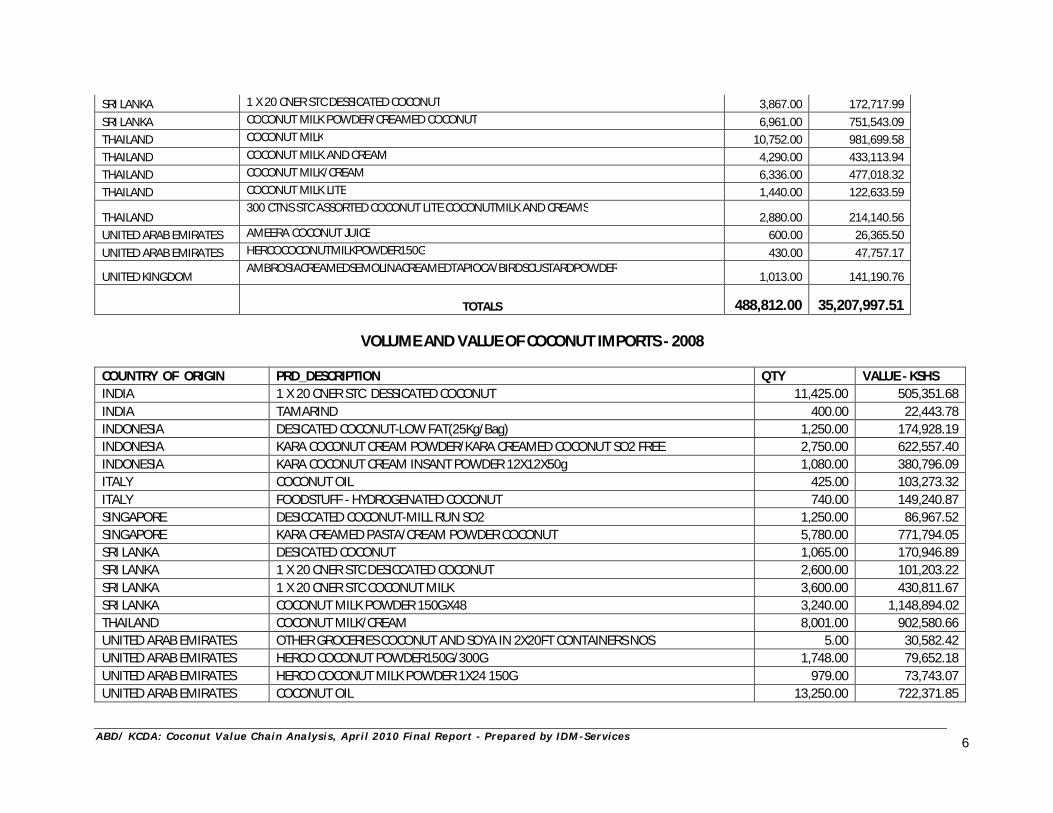

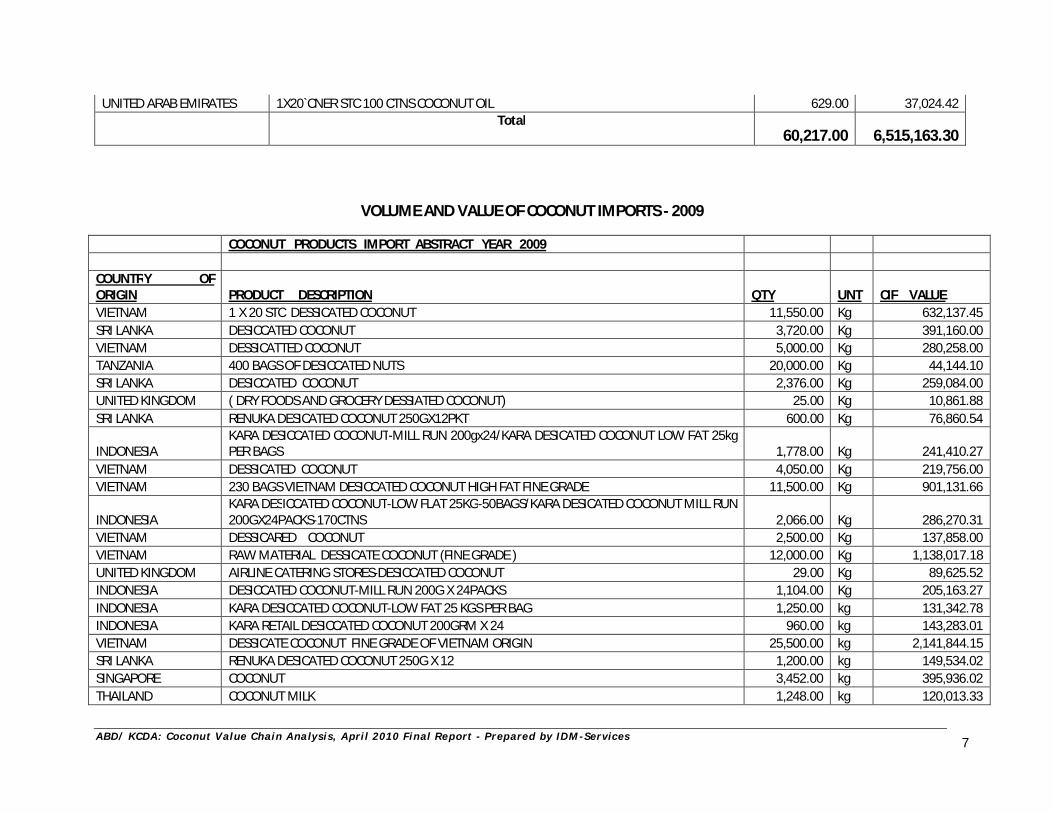

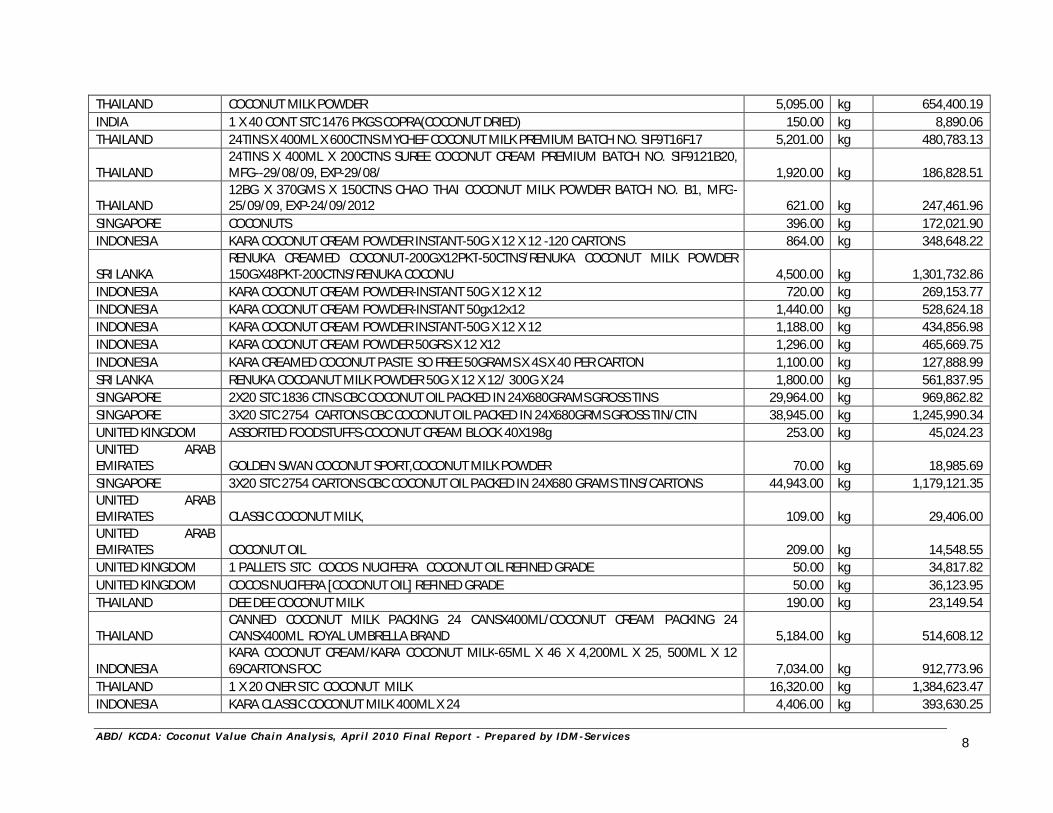

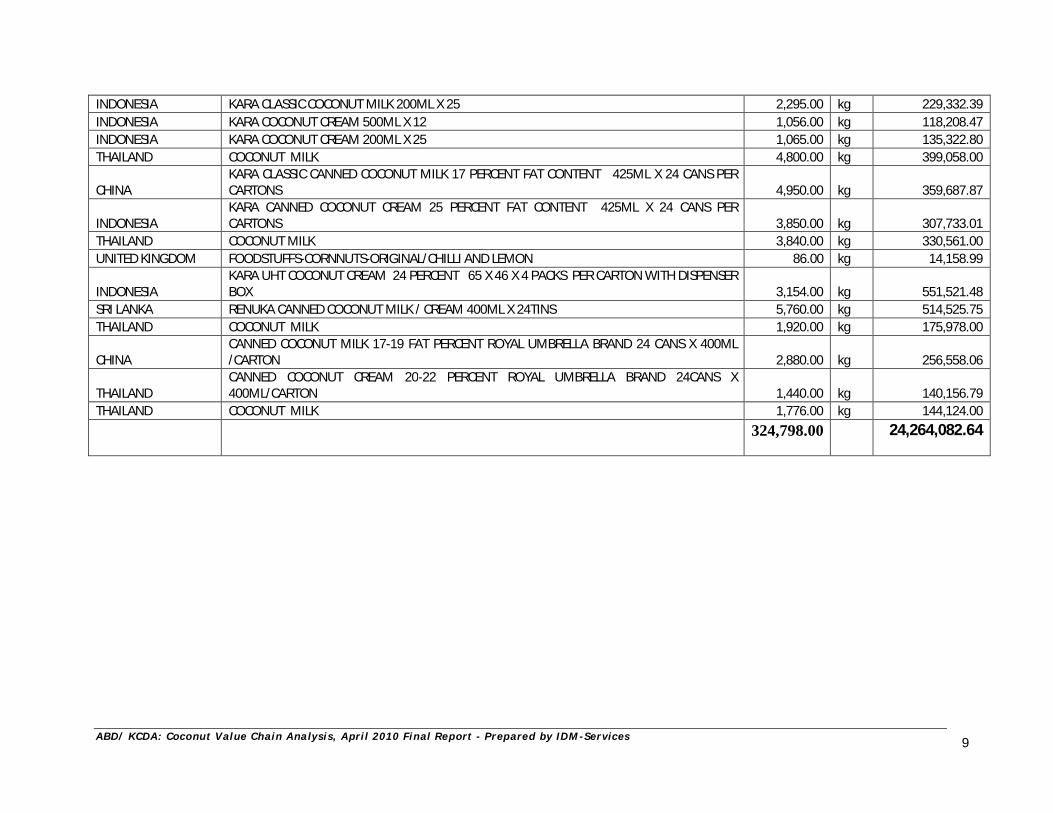

Source: ABD-DANIDA/CDA Coconut tree survey, Feb 2007 2.5 Import and Export figures for coconut products 2006 – 2009 Within the coconut value chain exportation and importation of various coconut products takes place. The only radical divergence between the two is that Kenya’s exports comprise mostly unprocessed nuts while imports comprise processed coconut products. This basically means that there is a loss in foreign exchange due to an imbalance in trade as imports fetch higher prices than exports. Imports Major coconut products imported annually include coconut milk and cream, coconut oil, desiccated coconut, coconut syrup and coconut powder among others. These products are mostly imported from Sri Lanka, Malaysia, Thailand, India, Indonesia, UAE, France, Tanzania, South Africa, and Italy among others. (See annex 7 for more details on imports). On the other hand, export products mainly involve dry nuts with a few other products like makuti and coco wood. Reliable information from Kenya Revenue Authority (KRA) Custom Statistics Department show that Kenya imported a total of Kes 35,207,997.51 in 2007; 6,515,163.30 in 2008 and 24,264,082.64 in 2009. (See annex 7 for more information on imports.)

Chart 4: Monetary value of annual processed coconut imports in Kes

A B D / K C D A : C oc o nu t V al ue C h ai n A na l y s i s , A pr i l 2 0 1 0 F i n a l R e p or t - P r e p ar e d by I D M - Se r v i c e s

9

Value of Imports

0.00

5,000,000.00

10,000,000.00

15,000,000.00

20,000,000.00

25,000,000.00

30,000,000.00

35,000,000.00

40,000,000.00

Valu

e in

Kes

.

Series1 35,207,997.51 6,515,163.30 24,264,082.64

Yr. 2007 Yr. 2008 Yr. 2009

Source: KRA Statistic Records (KRA Customs Statistic Dept, Msa), 2009

Chart 5: Volume of annual processed coconut imports in Kgs

Volumes in Kgs

0.00100,000.00200,000.00300,000.00400,000.00500,000.00600,000.00

Volu

me

(Kg)

Series1 488,812.00 60,217.00 324,798.00

Yr. 2007 Yr. 2008 Yr. 2009

Source: KRA Statistic Records (KRA Customs Statistic Dept, Msa), 2009

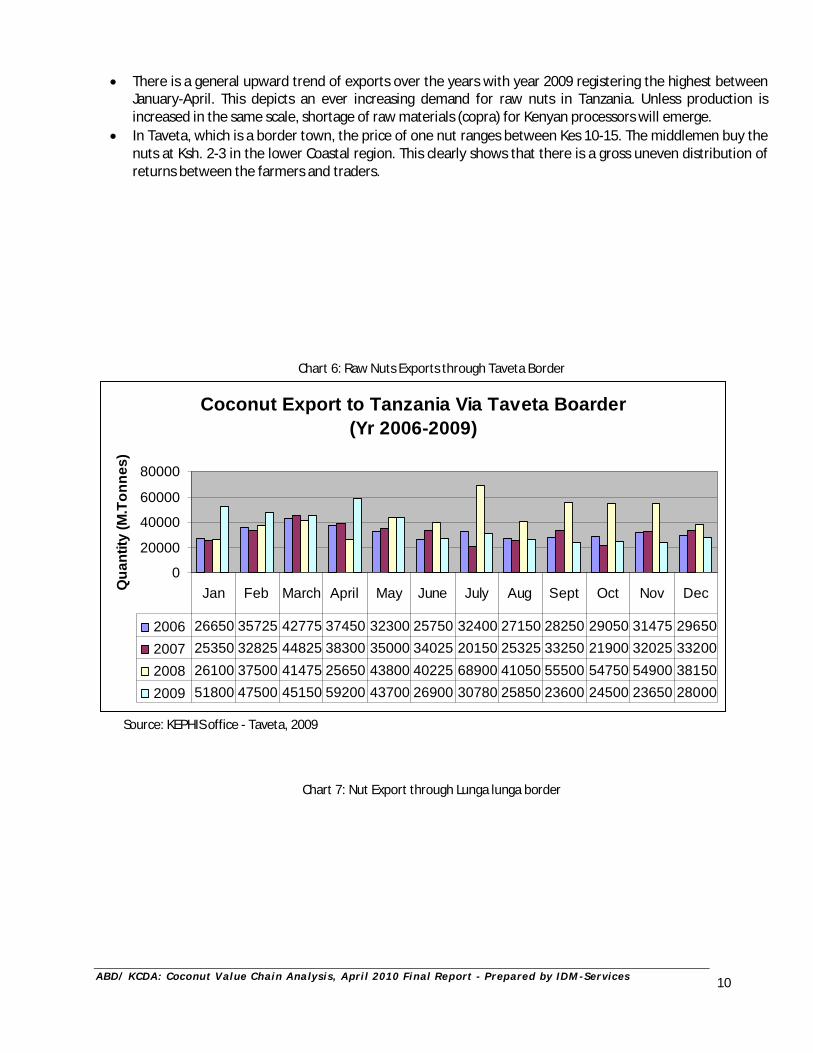

Exports As earlier mentioned, most of the coconut exports involve raw nuts mainly to Tanzania, Dubai, and India. Small scale exports of coconut virgin oil to the UK and USA and export of coco wood assorted products, e.g. furniture, ornaments and sculptures, among others, are likewise exported. Conversely, there seems to be an underestimation of the total number of nuts being exported to Tanzania. Key informants say that it is a common practice for trucks to cross the border at night and evade paying duty. In addition, there is lack of institutions that fully focus on thoroughly documenting coconut exports and their prices. Observations (Chart 6) The raw coconuts are exported throughout the year in all the years.

A B D / K C D A : C oc o nu t V al ue C h ai n A na l y s i s , A pr i l 2 0 1 0 F i n a l R e p or t - P r e p ar e d by I D M - Se r v i c e s

10

There is a general upward trend of exports over the years with year 2009 registering the highest between January-April. This depicts an ever increasing demand for raw nuts in Tanzania. Unless production is increased in the same scale, shortage of raw materials (copra) for Kenyan processors will emerge.

In Taveta, which is a border town, the price of one nut ranges between Kes 10-15. The middlemen buy the nuts at Ksh. 2-3 in the lower Coastal region. This clearly shows that there is a gross uneven distribution of returns between the farmers and traders.

Chart 6: Raw Nuts Exports through Taveta Border

Coconut Export to Tanzania Via Taveta Boarder (Yr 2006-2009)

0

20000

40000

60000

80000

Qua

ntity

(M.T

onne

s)

2006 26650 35725 42775 37450 32300 25750 32400 27150 28250 29050 31475 296502007 25350 32825 44825 38300 35000 34025 20150 25325 33250 21900 32025 332002008 26100 37500 41475 25650 43800 40225 68900 41050 55500 54750 54900 381502009 51800 47500 45150 59200 43700 26900 30780 25850 23600 24500 23650 28000

Jan Feb March April May June July Aug Sept Oct Nov Dec

Source: KEPHIS office - Taveta, 2009

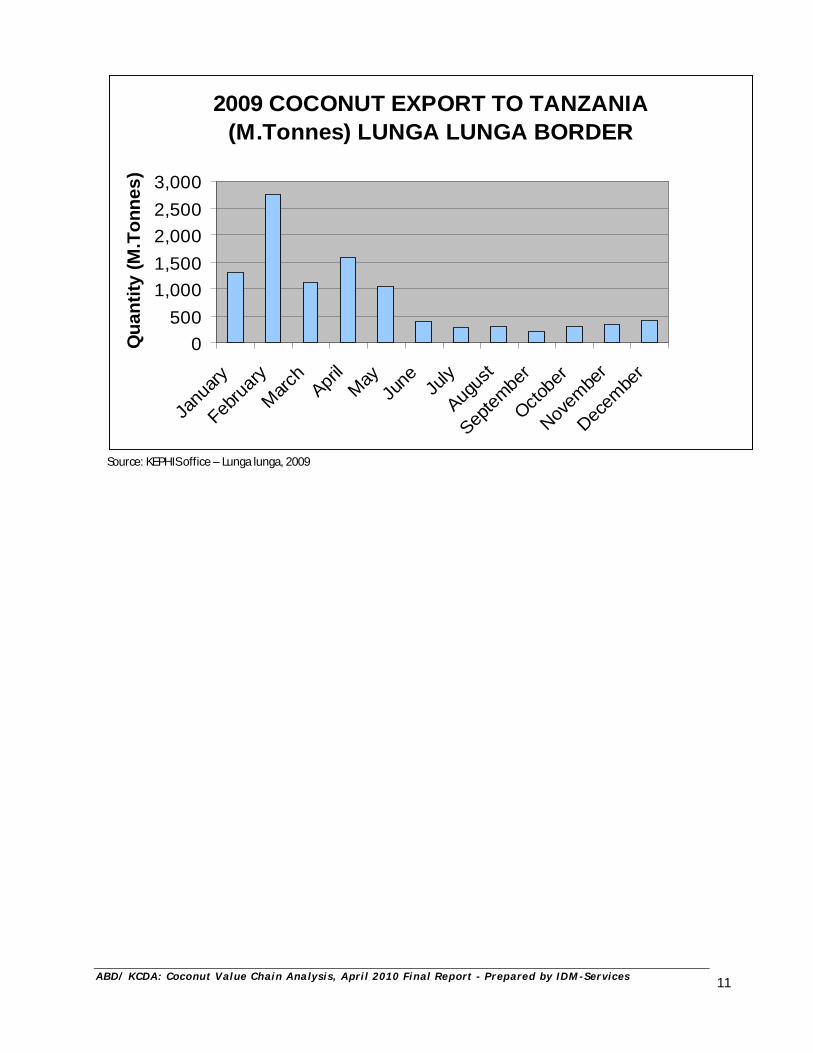

Chart 7: Nut Export through Lunga lunga border

A B D / K C D A : C oc o nu t V al ue C h ai n A na l y s i s , A pr i l 2 0 1 0 F i n a l R e p or t - P r e p ar e d by I D M - Se r v i c e s

11

2009 COCONUT EXPORT TO TANZANIA (M.Tonnes) LUNGA LUNGA BORDER

0500

1,0001,5002,0002,5003,000

Janu

ary

Februa

ryMarc

hApri

lMay

June Ju

ly

Augus

t

Septem

ber

Octobe

r

Novem

ber

Decem

ber

Qua

ntity

(M.T

onne

s)

Source: KEPHIS office – Lunga lunga, 2009

A B D / K C D A : C oc o nu t V al ue C h ai n A na l y s i s , A pr i l 2 0 1 0 F i n a l R e p or t - P r e p ar e d by I D M - Se r v i c e s

12

SECTION ONE COCONUT (MATURE NUT) VALUE CHAIN ANALYSIS

3.0 Overview of the Dry Nut Value Chain This section of the report provides resourceful information in regard to the mature nuts value chain by analyzing the various segments from input suppliers and producers to the end consumers. This information relates to key actors along the nut chain, products under the nut value chain, production costs for the nut, gross margin analysis, market pricing, challenges faced at each stage, and opportunities for growth among many others. However, it is important to note that owing to the numerous products that the coconut tree has, it was not possible to analyze all the mature nut products. Notwithstanding, effort was made to provide a detailed value chain analysis for most nut products that are processed locally. Critical leverage points that hold the key to unlocking the sub sector potential are also well documented in the section as well as areas that require urgent attention. 3.1 The Nut Production Chan During the value chain analysis about 95% of the farmers stated that they obtain their seedlings from their own farms. A few (5%) obtain seedlings from established private commercial nurseries and from neighbouring farmers where little seed selection is done from trees that have exhibited high production performance in the past. In most cases farmers will give the seedlings for free to their neighbours who may wish to plant some. They also buy from each other at an average price of Kes 50 to Kes 80 per seedling. Production and management of coconut is labour intensive and is provided mainly by family members at the small scale to medium scale level of farming. However, in most of the large scale farms, hired labourers are engaged. Most of these labourers are casuals and are engaged in managing the orchards and includes; harvesters, dehuskers and assemblers among others. 3.1.1 Nut production per tree From a list of the farmers interviewed, the average nut production per tree stands at about 30 – 60 nuts depending on the level of management. However, some indicated that production per tree may at times be as low as 20 nuts. Current nut production among most farmers seldom involves fertilizer application or use of pest and disease control measures. Normally, trees are intercropped or left to grow in grassy and bushy fields. Nuts production is mainly influenced by the management practices such as weeding, manure and fertilizer application and pests and disease control. Quality of planting materials/varieties also has a major impact on nut production.

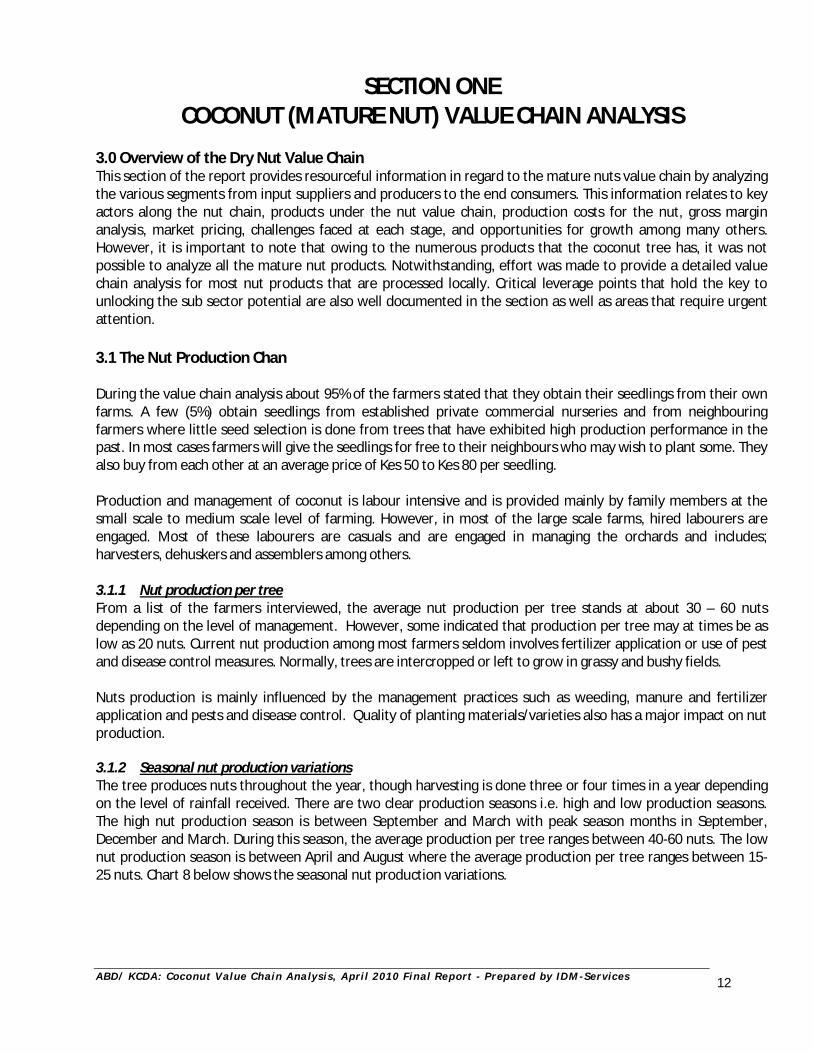

3.1.2 Seasonal nut production variations The tree produces nuts throughout the year, though harvesting is done three or four times in a year depending on the level of rainfall received. There are two clear production seasons i.e. high and low production seasons. The high nut production season is between September and March with peak season months in September, December and March. During this season, the average production per tree ranges between 40-60 nuts. The low nut production season is between April and August where the average production per tree ranges between 15-25 nuts. Chart 8 below shows the seasonal nut production variations.

A B D / K C D A : C oc o nu t V al ue C h ai n A na l y s i s , A pr i l 2 0 1 0 F i n a l R e p or t - P r e p ar e d by I D M - Se r v i c e s

13

Chart 8: Nut production seasonality chart

Source: ABD/ KCDA: Coconut Value Chain Analysis, August 2009

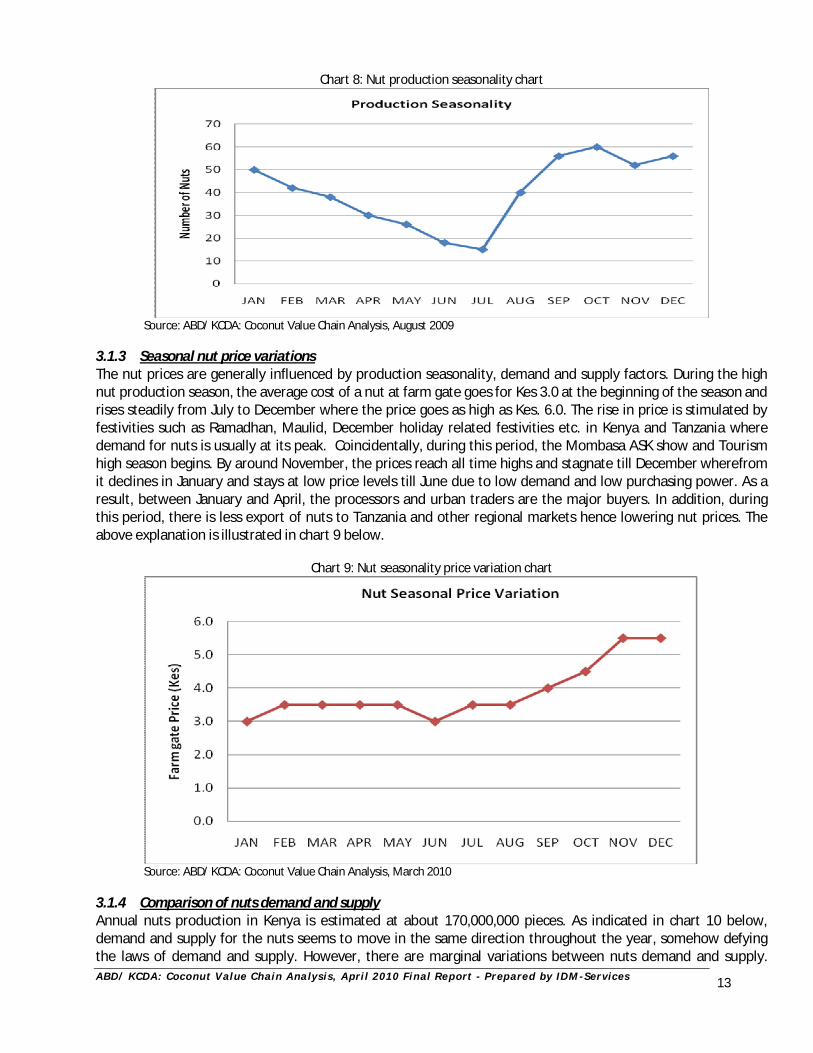

3.1.3 Seasonal nut price variations The nut prices are generally influenced by production seasonality, demand and supply factors. During the high nut production season, the average cost of a nut at farm gate goes for Kes 3.0 at the beginning of the season and rises steadily from July to December where the price goes as high as Kes. 6.0. The rise in price is stimulated by festivities such as Ramadhan, Maulid, December holiday related festivities etc. in Kenya and Tanzania where demand for nuts is usually at its peak. Coincidentally, during this period, the Mombasa ASK show and Tourism high season begins. By around November, the prices reach all time highs and stagnate till December wherefrom it declines in January and stays at low price levels till June due to low demand and low purchasing power. As a result, between January and April, the processors and urban traders are the major buyers. In addition, during this period, there is less export of nuts to Tanzania and other regional markets hence lowering nut prices. The above explanation is illustrated in chart 9 below.

Chart 9: Nut seasonality price variation chart

Source: ABD/ KCDA: Coconut Value Chain Analysis, March 2010

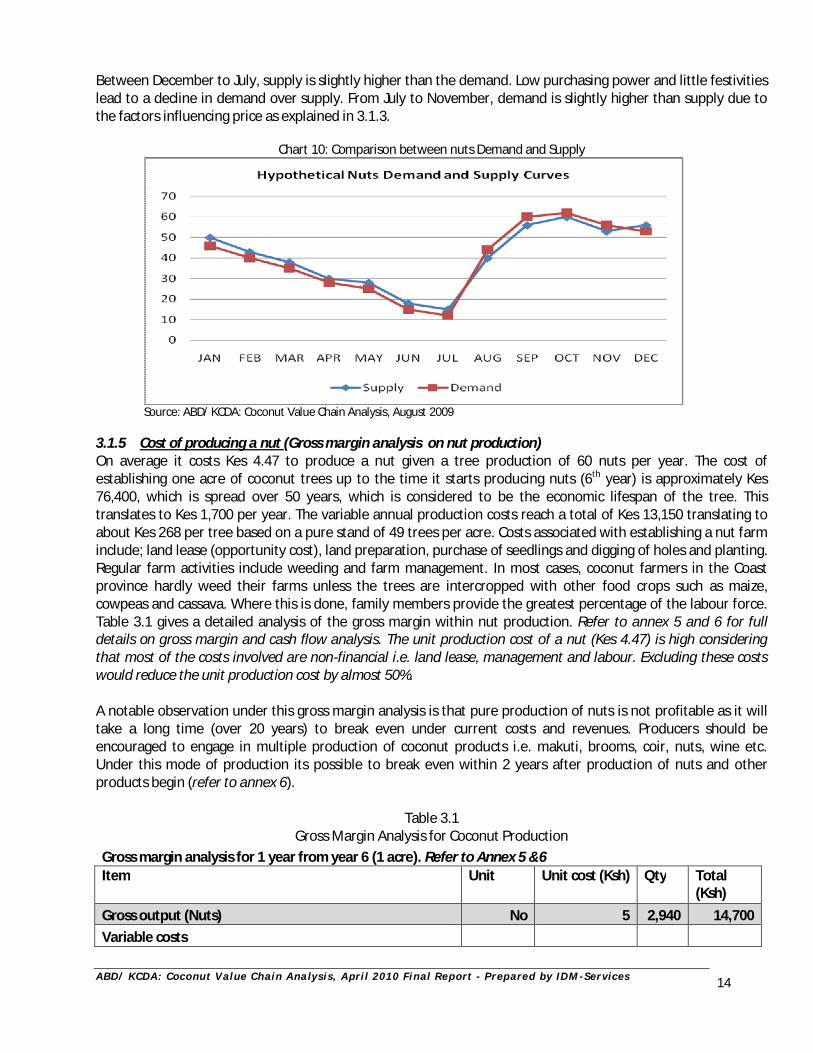

3.1.4 Comparison of nuts demand and supply Annual nuts production in Kenya is estimated at about 170,000,000 pieces. As indicated in chart 10 below, demand and supply for the nuts seems to move in the same direction throughout the year, somehow defying the laws of demand and supply. However, there are marginal variations between nuts demand and supply.

A B D / K C D A : C oc o nu t V al ue C h ai n A na l y s i s , A pr i l 2 0 1 0 F i n a l R e p or t - P r e p ar e d by I D M - Se r v i c e s

14

Between December to July, supply is slightly higher than the demand. Low purchasing power and little festivities lead to a decline in demand over supply. From July to November, demand is slightly higher than supply due to the factors influencing price as explained in 3.1.3.

Chart 10: Comparison between nuts Demand and Supply

Source: ABD/ KCDA: Coconut Value Chain Analysis, August 2009

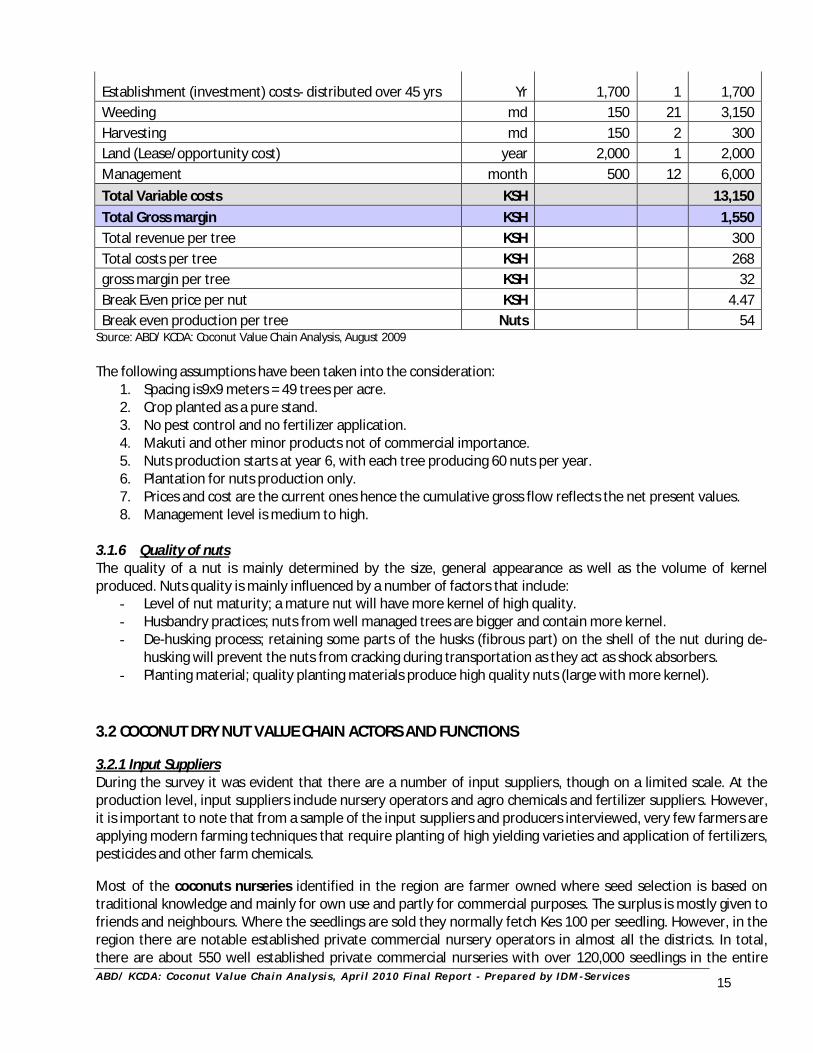

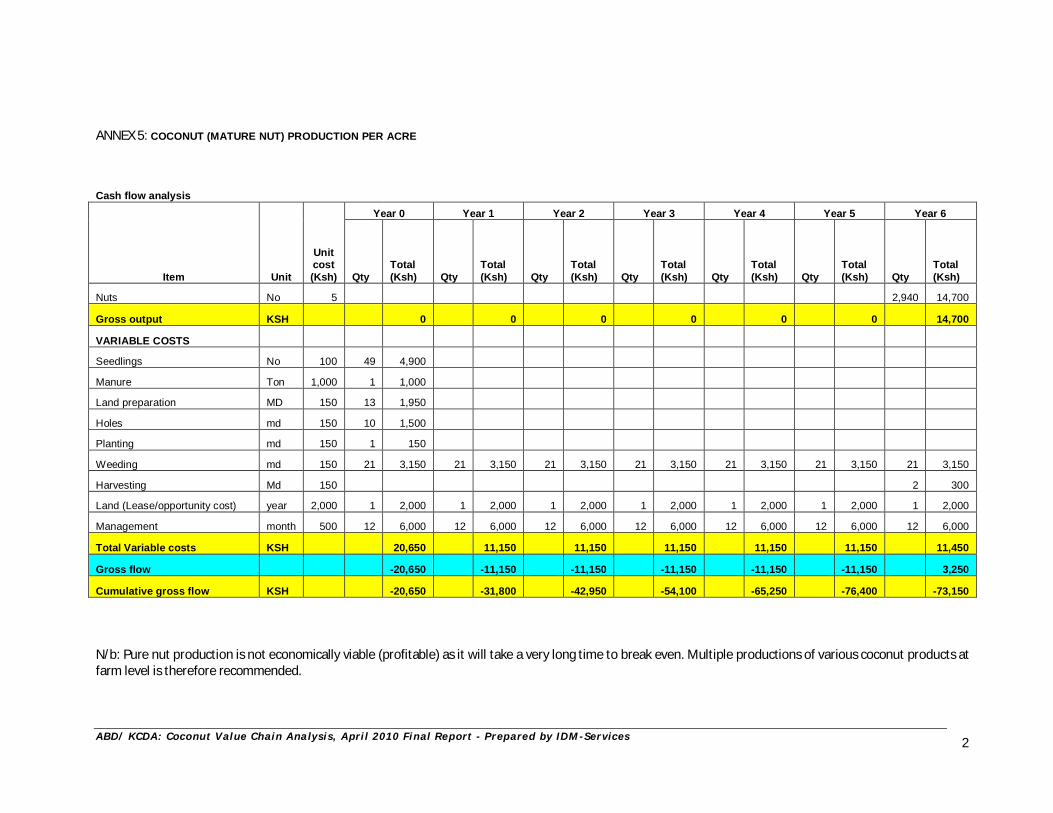

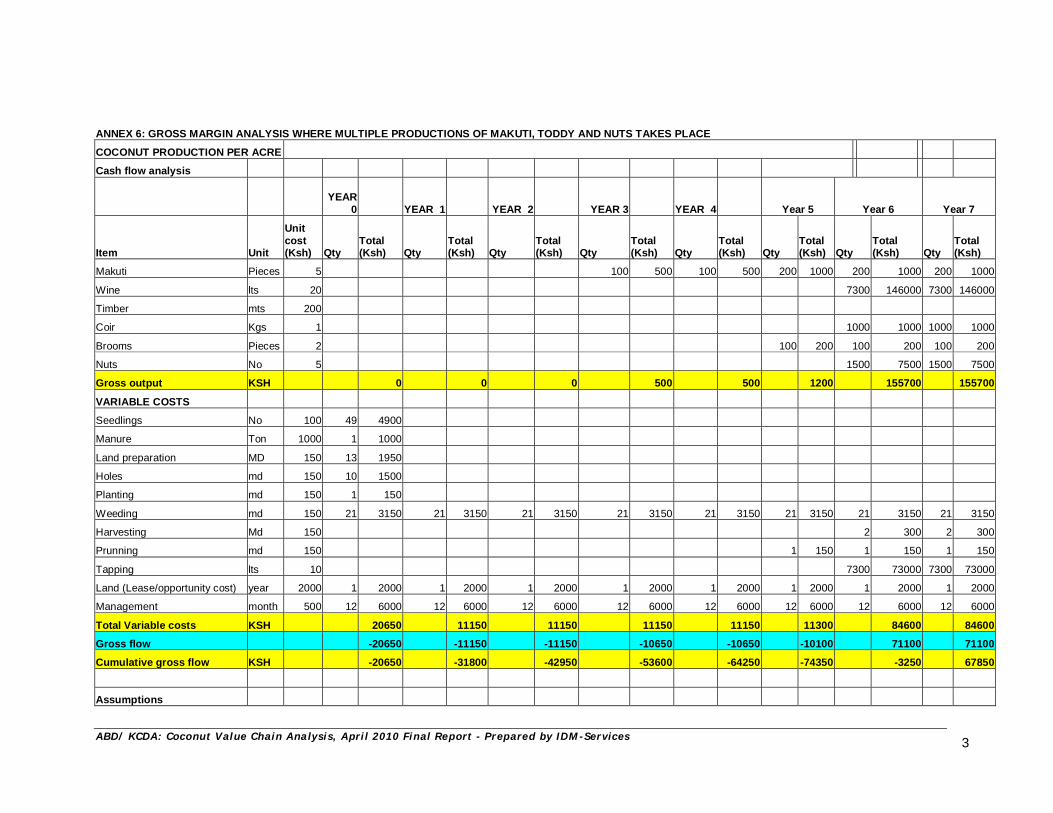

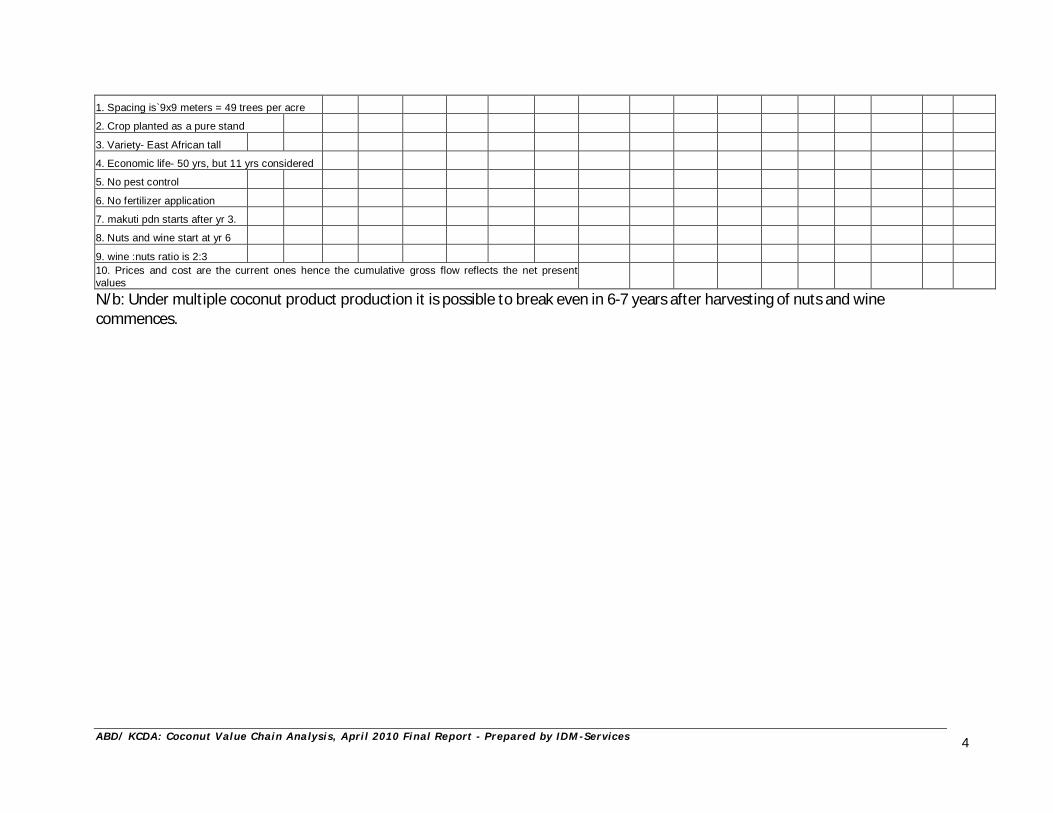

3.1.5 Cost of producing a nut (Gross margin analysis on nut production) On average it costs Kes 4.47 to produce a nut given a tree production of 60 nuts per year. The cost of establishing one acre of coconut trees up to the time it starts producing nuts (6th year) is approximately Kes 76,400, which is spread over 50 years, which is considered to be the economic lifespan of the tree. This translates to Kes 1,700 per year. The variable annual production costs reach a total of Kes 13,150 translating to about Kes 268 per tree based on a pure stand of 49 trees per acre. Costs associated with establishing a nut farm include; land lease (opportunity cost), land preparation, purchase of seedlings and digging of holes and planting. Regular farm activities include weeding and farm management. In most cases, coconut farmers in the Coast province hardly weed their farms unless the trees are intercropped with other food crops such as maize, cowpeas and cassava. Where this is done, family members provide the greatest percentage of the labour force. Table 3.1 gives a detailed analysis of the gross margin within nut production. Refer to annex 5 and 6 for full details on gross margin and cash flow analysis. The unit production cost of a nut (Kes 4.47) is high considering that most of the costs involved are non-financial i.e. land lease, management and labour. Excluding these costs would reduce the unit production cost by almost 50%. A notable observation under this gross margin analysis is that pure production of nuts is not profitable as it will take a long time (over 20 years) to break even under current costs and revenues. Producers should be encouraged to engage in multiple production of coconut products i.e. makuti, brooms, coir, nuts, wine etc. Under this mode of production its possible to break even within 2 years after production of nuts and other products begin (refer to annex 6).

Table 3.1

Gross Margin Analysis for Coconut Production Gross margin analysis for 1 year from year 6 (1 acre). Refer to Annex 5 &6 Item Unit Unit cost (Ksh) Qty Total

(Ksh) Gross output (Nuts) No 5 2,940 14,700 Variable costs

A B D / K C D A : C oc o nu t V al ue C h ai n A na l y s i s , A pr i l 2 0 1 0 F i n a l R e p or t - P r e p ar e d by I D M - Se r v i c e s

15

Establishment (investment) costs- distributed over 45 yrs Yr 1,700 1 1,700 Weeding md 150 21 3,150 Harvesting md 150 2 300 Land (Lease/opportunity cost) year 2,000 1 2,000 Management month 500 12 6,000 Total Variable costs KSH 13,150 Total Gross margin KSH 1,550 Total revenue per tree KSH 300 Total costs per tree KSH 268 gross margin per tree KSH 32 Break Even price per nut KSH 4.47 Break even production per tree Nuts 54

Source: ABD/ KCDA: Coconut Value Chain Analysis, August 2009 The following assumptions have been taken into the consideration:

1. Spacing is9x9 meters = 49 trees per acre. 2. Crop planted as a pure stand. 3. No pest control and no fertilizer application. 4. Makuti and other minor products not of commercial importance. 5. Nuts production starts at year 6, with each tree producing 60 nuts per year. 6. Plantation for nuts production only. 7. Prices and cost are the current ones hence the cumulative gross flow reflects the net present values. 8. Management level is medium to high.

3.1.6 Quality of nuts The quality of a nut is mainly determined by the size, general appearance as well as the volume of kernel produced. Nuts quality is mainly influenced by a number of factors that include:

- Level of nut maturity; a mature nut will have more kernel of high quality. - Husbandry practices; nuts from well managed trees are bigger and contain more kernel. - De-husking process; retaining some parts of the husks (fibrous part) on the shell of the nut during de-

husking will prevent the nuts from cracking during transportation as they act as shock absorbers. - Planting material; quality planting materials produce high quality nuts (large with more kernel).

3.2 COCONUT DRY NUT VALUE CHAIN ACTORS AND FUNCTIONS 3.2.1 Input Suppliers During the survey it was evident that there are a number of input suppliers, though on a limited scale. At the production level, input suppliers include nursery operators and agro chemicals and fertilizer suppliers. However, it is important to note that from a sample of the input suppliers and producers interviewed, very few farmers are applying modern farming techniques that require planting of high yielding varieties and application of fertilizers, pesticides and other farm chemicals. Most of the coconuts nurseries identified in the region are farmer owned where seed selection is based on traditional knowledge and mainly for own use and partly for commercial purposes. The surplus is mostly given to friends and neighbours. Where the seedlings are sold they normally fetch Kes 100 per seedling. However, in the region there are notable established private commercial nursery operators in almost all the districts. In total, there are about 550 well established private commercial nurseries with over 120,000 seedlings in the entire

A B D / K C D A : C oc o nu t V al ue C h ai n A na l y s i s , A pr i l 2 0 1 0 F i n a l R e p or t - P r e p ar e d by I D M - Se r v i c e s

16

Coast region with most of them being located in Kwale, Kilifi and Kaloleni districts. The major constraint is the low number of farmers buying from these commercial nurseries as evidenced by a large number of unsold seedlings in the nurseries resulting in high prices (ranging between Kes 80 -100 per seedling). Currently the Kenya Coconut Development Authority is promoting coconut tree nurseries in selected districts of the Coast province. For instance, in Kaloleni District there are 18 coconut seedling nurseries that KCDA have helped to establish and through which they subsidize the cost of seedlings. The cost of a coconut seedling from these nurseries is estimated at Kes 50 where KCDA pays Kes 30 and the farmer pays Kes 20. Most of these nurseries are owned and managed by farmers. In relation to production, there are extension officers from the MoA who provide farmers with extension services on coconut production and management. Their services have not been consistent due to logistical challenges though the trend is changing slowly. Other suppliers include farm tool suppliers who are mostly hardware dealers and agrovet dealers. 3.2.2 Producers Coconut farmers in the entire coastal region can be categorized into three groups; small scale, medium scale and large scale farmers depending on the number of coconut trees they hold. Based on this categorization, small scale producers own less than 100 trees. Medium scale producers on the other hand own between 101 – 300 trees while the larger scale producers are farmers with land holdings with over 300 trees on a plantation such as Msambweni Development Company and others.

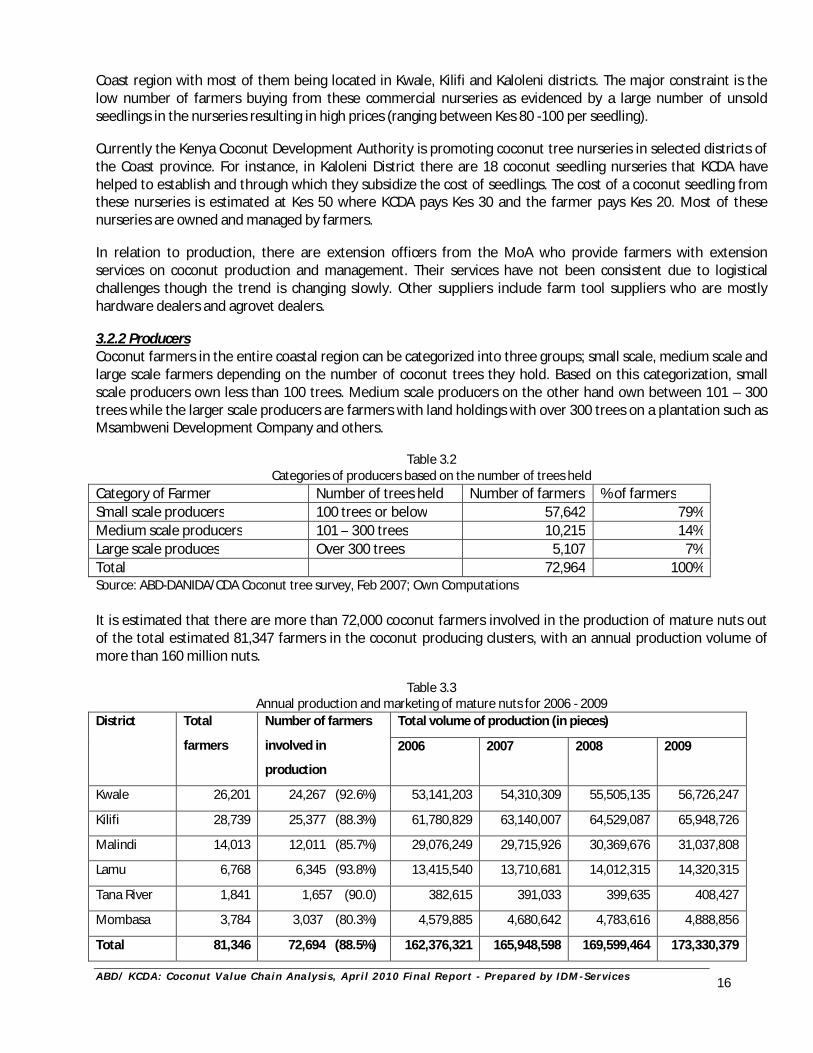

Table 3.2

Categories of producers based on the number of trees held Category of Farmer Number of trees held Number of farmers % of farmers Small scale producers 100 trees or below 57,642 79% Medium scale producers 101 – 300 trees 10,215 14% Large scale produces Over 300 trees 5,107 7% Total 72,964 100% Source: ABD-DANIDA/CDA Coconut tree survey, Feb 2007; Own Computations It is estimated that there are more than 72,000 coconut farmers involved in the production of mature nuts out of the total estimated 81,347 farmers in the coconut producing clusters, with an annual production volume of more than 160 million nuts.

Table 3.3

Annual production and marketing of mature nuts for 2006 - 2009 District Total

farmers

Number of farmers

involved in

production

Total volume of production (in pieces)

2006 2007 2008 2009

Kwale 26,201 24,267 (92.6%) 53,141,203 54,310,309 55,505,135 56,726,247

Kilifi 28,739 25,377 (88.3%) 61,780,829 63,140,007 64,529,087 65,948,726

Malindi 14,013 12,011 (85.7%) 29,076,249 29,715,926 30,369,676 31,037,808

Lamu 6,768 6,345 (93.8%) 13,415,540 13,710,681 14,012,315 14,320,315

Tana River 1,841 1,657 (90.0) 382,615 391,033 399,635 408,427

Mombasa 3,784 3,037 (80.3%) 4,579,885 4,680,642 4,783,616 4,888,856

Total 81,346 72,694 (88.5%) 162,376,321 165,948,598 169,599,464 173,330,379

A B D / K C D A : C oc o nu t V al ue C h ai n A na l y s i s , A pr i l 2 0 1 0 F i n a l R e p or t - P r e p ar e d by I D M - Se r v i c e s

17

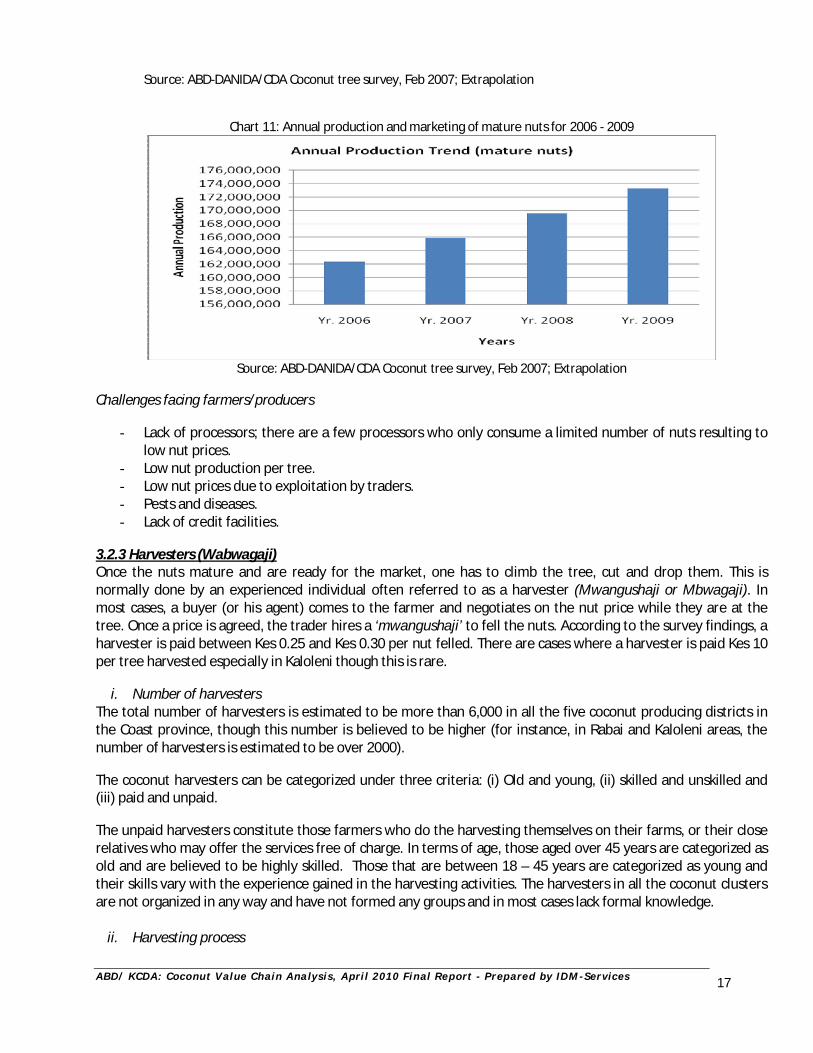

Source: ABD-DANIDA/CDA Coconut tree survey, Feb 2007; Extrapolation

Chart 11: Annual production and marketing of mature nuts for 2006 - 2009

Source: ABD-DANIDA/CDA Coconut tree survey, Feb 2007; Extrapolation

Challenges facing farmers/producers

- Lack of processors; there are a few processors who only consume a limited number of nuts resulting to low nut prices.

- Low nut production per tree. - Low nut prices due to exploitation by traders. - Pests and diseases. - Lack of credit facilities.

3.2.3 Harvesters (Wabwagaji) Once the nuts mature and are ready for the market, one has to climb the tree, cut and drop them. This is normally done by an experienced individual often referred to as a harvester (Mwangushaji or Mbwagaji). In most cases, a buyer (or his agent) comes to the farmer and negotiates on the nut price while they are at the tree. Once a price is agreed, the trader hires a ‘mwangushaji’ to fell the nuts. According to the survey findings, a harvester is paid between Kes 0.25 and Kes 0.30 per nut felled. There are cases where a harvester is paid Kes 10 per tree harvested especially in Kaloleni though this is rare.

i. Number of harvesters The total number of harvesters is estimated to be more than 6,000 in all the five coconut producing districts in the Coast province, though this number is believed to be higher (for instance, in Rabai and Kaloleni areas, the number of harvesters is estimated to be over 2000). The coconut harvesters can be categorized under three criteria: (i) Old and young, (ii) skilled and unskilled and (iii) paid and unpaid. The unpaid harvesters constitute those farmers who do the harvesting themselves on their farms, or their close relatives who may offer the services free of charge. In terms of age, those aged over 45 years are categorized as old and are believed to be highly skilled. Those that are between 18 – 45 years are categorized as young and their skills vary with the experience gained in the harvesting activities. The harvesters in all the coconut clusters are not organized in any way and have not formed any groups and in most cases lack formal knowledge.

ii. Harvesting process

A B D / K C D A : C oc o nu t V al ue C h ai n A na l y s i s , A pr i l 2 0 1 0 F i n a l R e p or t - P r e p ar e d by I D M - Se r v i c e s

18

The nut harvesting process is simple as it involves the harvester climbing the tree using a rope, (if the tree has no ladders (engraves on the trunk)). On reaching the top, a bunch of mature nuts are cut, which is normally brown in colour, using a sharp knife. Harvesting per tree takes between 5 - 12 minutes.

iii. Volumes handled by Harvesters A harvester can harvest up to 40 trees in a day though the average is 25 trees a day. The number of trees harvested in a day is influenced by the strength of an individual, height of the tree, weather conditions, and the number of nuts to be harvested from a tree. Depending on the number of nuts per tree, a harvester can handle 400-1,500 nuts per day.

iv. Costs incurred by the harvester Costs incurred by a harvester relate to purchase of harvesting knife which costs Kes 60 for the ordinary knife and Kes 200 for good steel knife. This is only bought once lasts for many years. Sisal ropes are purchased on need basis and costs about Kes 50 and file for sharpening the knife that costs about Kes 100.

v. Challenges/issues facing harvesters According to views expressed by several harvesters the following are the main challenges facing their trade:

Low prices offered per tree or nut harvested. High risks associated with harvesting; accidental falling from trees while harvesting have been reported

including the risk of being bitten by wasps, snakes and other insects. Similarly, there is difficulty in climbing during rainy seasons as the trees get wet and slippery.

Inconsistency of harvesting exercise; Unlike tapping which is a daily activity, harvesting of nuts is not and a harvester can take a long time before getting work.

Low production per tree affects income generation. Injuries (sometimes fatal) from falling.

3.2.4 De-huskers (Wafuaji) Once the nuts are cut from the tree, the next step is to de-husk them. Under-husked nuts are normally bulky and require removal of the husk to facilitate bulking and transportation to the market. This task is carried out by individuals often referred to as dehuskers using a sharp piece of metal (‘tarimbo’ or ‘Kifulio’).

i. Number of de-huskers Since de-husking does not involve special skills and associated risks are minimal, the estimated number of de-huskers is higher than that of harvesters though it fluctuates depending on nut productivity and availability of buyers. It is estimated that there could be well over 10,000 de-huskers with the majority being located in Kilifi, Kaloleni, Malindi, Lunga Lunga, Msambweni and Kwale. In most cases, it is a trader who hires the de-huskers to collect the felled nuts, de-husk them and package them into sacks in readiness for transportation.

ii. De-husking process The process involves collecting and dehusking the felled nuts by ‘wafuaji’ using a sharp piece of metal locally referred to as ‘tarimbo’ or ‘kifulio’. In the absence of a sharp piece of metal, some de-huskers use sharpened pieces of wood with a pointed end. There are rare instances where harvesters are involved in de-husking, especially where only limited number of nuts is being harvested. In de-husking there is a gender mix unlike harvesting where it’s entirely carried out by men though the number of women de-huskers is small. During this process, care must be taken to avoid breaking the nut. Once the nuts have been de-husked, they are assembled at one point and counting is done in the presence of the farmer who is then paid. The nuts are then packaged into sacks where a sack carries about 250 – 300 nuts. A de-husker is normally paid an average of Kes 25 for every 100 nuts de-husked i.e. Kes 0.25 per nut.

A B D / K C D A : C oc o nu t V al ue C h ai n A na l y s i s , A pr i l 2 0 1 0 F i n a l R e p or t - P r e p ar e d by I D M - Se r v i c e s

19

iii. Volumes handled by a de-husker

A de-husker can de-husk an average of 500 - 600 nuts per day using the traditional de-husking methods. The average number of de-husked nuts per day will depend on the tools used in de-husking, that is, the shape and material used to make the tool.

iv. Costs related to de-husking The only major cost incurred by a de-husker is that of acquiring the sharp piece of metal which is at times negligible given that it’s cheap to acquire and takes a long time to be replaced.

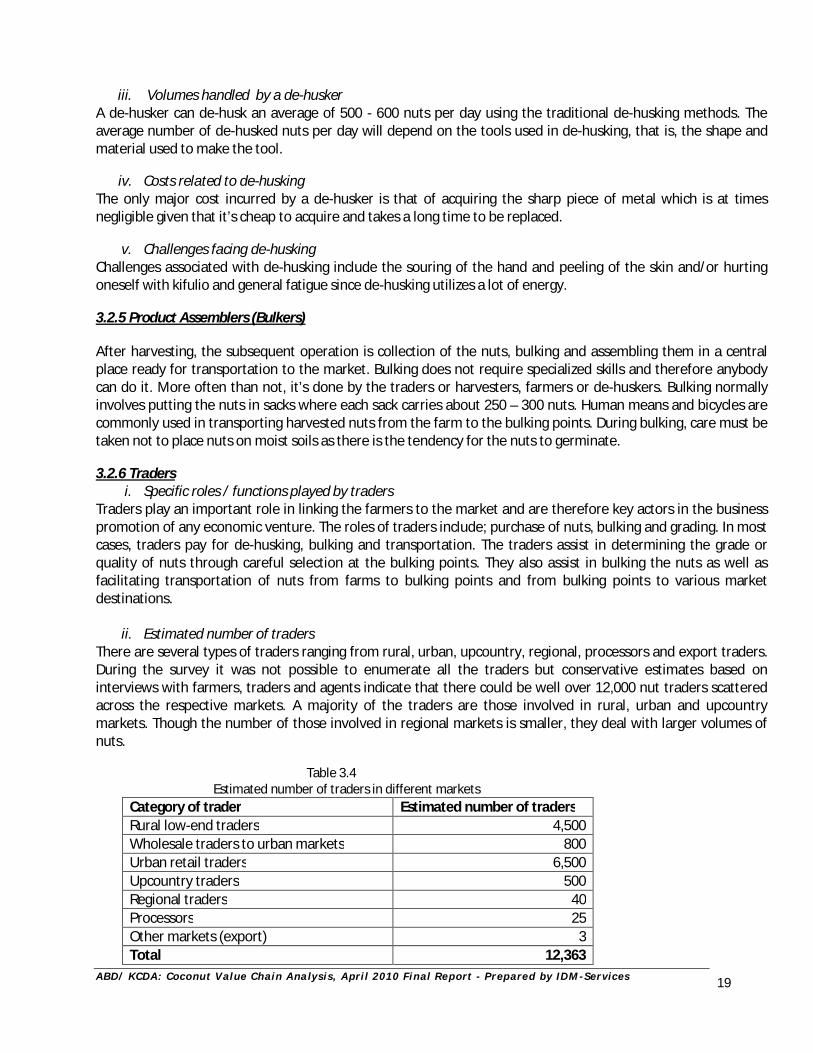

v. Challenges facing de-husking Challenges associated with de-husking include the souring of the hand and peeling of the skin and/or hurting oneself with kifulio and general fatigue since de-husking utilizes a lot of energy. 3.2.5 Product Assemblers (Bulkers) After harvesting, the subsequent operation is collection of the nuts, bulking and assembling them in a central place ready for transportation to the market. Bulking does not require specialized skills and therefore anybody can do it. More often than not, it’s done by the traders or harvesters, farmers or de-huskers. Bulking normally involves putting the nuts in sacks where each sack carries about 250 – 300 nuts. Human means and bicycles are commonly used in transporting harvested nuts from the farm to the bulking points. During bulking, care must be taken not to place nuts on moist soils as there is the tendency for the nuts to germinate. 3.2.6 Traders