Embed Size (px)

Citation preview

University of Calgary

PRISM: University of Calgary's Digital Repository

Graduate Studies The Vault: Electronic Theses and Dissertations

2019-06-12

Cluster analysis of correlated non-Gaussian

continuous data via finite mixtures of Gaussian

copula distributions

Burak, Katherine L.

Burak, K. L. (2019). Cluster analysis of correlated non-Gaussian continuous data via finite

mixtures of Gaussian copula distributions (Unpublished master's thesis). University of Calgary,

Calgary, AB.

http://hdl.handle.net/1880/110497

master thesis

University of Calgary graduate students retain copyright ownership and moral rights for their

thesis. You may use this material in any way that is permitted by the Copyright Act or through

licensing that has been assigned to the document. For uses that are not allowable under

copyright legislation or licensing, you are required to seek permission.

Downloaded from PRISM: https://prism.ucalgary.ca

UNIVERSITY OF CALGARY

Cluster analysis of correlated non-Gaussian continuous data via finite mixtures of Gaussian

copula distributions

by

Katherine L. Burak

A THESIS

SUBMITTED TO THE FACULTY OF GRADUATE STUDIES

IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE

DEGREE OF MASTER OF SCIENCE

GRADUATE PROGRAM IN MATHEMATICS AND STATISTICS

CALGARY, ALBERTA

JUNE, 2019

c© Katherine L. Burak 2019

Abstract

Model-based cluster analysis in non-Gaussian settings is not straightforward due to a lack of

standard models for non-Gaussian data. In this thesis, we adopt the class of Gaussian cop-

ula distributions (GCDs) to develop a flexible model-based clustering methodology that can

accommodate a variety of correlated, non-Gaussian continuous data, where variables may

have different marginal distributions and come from different parametric families. Unlike

conventional model-based approaches that rely on the assumption of conditional indepen-

dence, GCDs model conditional dependence among the disparate variables using the matrix

of so-called normal correlations. We outline a hybrid approach to cluster analysis that com-

bines the method of inference functions for margins (IFM) and the parameter-expanded

EM (PX-EM) algorithm. We then report simulation results to investigate the performance

of our methodology. Finally, we highlight the applications of this research by applying this

methodology to a dataset regarding the purchases made by clients of a wholesale distributor.

ii

Acknowledgements

I would like to express my gratitude to my supervisor, Dr. A.R. de Leon, for his guidance

throughout this entire process. I am very grateful for the extensive knowledge and leadership

he has provided me during my master’s degree.

I would also like to thank my co-supervisor, Dr. J. Wu, and Drs. X. Lu and K. Kopciuk

for acting as my committee members and providing valuable feedback on my thesis.

Finally, I would like to thank my parents for their endless support; without them, this

truly would not have been possible.

iii

Table of Contents

Abstract ii

Acknowledgements iii

Table of Contents iv

List of Figures and Illustrations vi

List of Tables vii

1 Introduction 11.1 Joint models for non-Gaussian continuous data . . . . . . . . . . . . . . . . . 1

1.1.1 Gaussian copula distributions . . . . . . . . . . . . . . . . . . . . . . 31.2 Cluster analysis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51.3 EM algorithm . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

1.3.1 PX-EM algorithm . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 91.4 Inference functions for margins . . . . . . . . . . . . . . . . . . . . . . . . . 101.5 Overview of thesis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

2 Model-based clustering with Gaussian copula distributions 122.1 Finite mixtures of GCDs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 122.2 PXEM-IFM algorithm . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 142.3 Discussion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

3 Simulations 193.1 Simulation design . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

3.1.1 Parameter settings . . . . . . . . . . . . . . . . . . . . . . . . . . . . 203.2 Model selection criterion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

3.2.1 Bayesian information criterion . . . . . . . . . . . . . . . . . . . . . . 233.2.2 Clustering indices . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 243.2.3 Relative bias . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

3.3 Results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 263.3.1 Simulation 1 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 263.3.2 Simulation 2 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 283.3.3 Simulation 3 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 303.3.4 Discussion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33

iv

4 Application 354.1 Overview of dataset . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 354.2 Results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 374.3 Discussion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38

5 Conclusion 425.1 Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 425.2 Future work . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43

Bibliography 44

v

List of Figures and Illustrations

3.1 Plot of true clusters (K = 3, high separation) . . . . . . . . . . . . . . . . . 203.2 Plot of true clusters (K = 2, moderate separation) . . . . . . . . . . . . . . . 213.3 Plot of true clusters (K = 3, mild separation) . . . . . . . . . . . . . . . . . 223.4 Plot of clusters obtained via GCD (K = 3, high separation) . . . . . . . . . 273.5 Plot of clusters obtained via GCD (K = 2, moderate separation) . . . . . . . 293.6 Plot of clusters obtained via GCD (K = 3, mild separation) . . . . . . . . . 32

4.1 Histograms of continuous variables (wholesale dataset) . . . . . . . . . . . . 394.2 Plot of clusters obtained via GCD (wholesale dataset) . . . . . . . . . . . . . 404.3 Plot of data coloured by channel variable (wholesale dataset) . . . . . . . . . 41

vi

List of Tables

3.1 Parameter settings (K = 3, high separation) . . . . . . . . . . . . . . . . . . 203.2 Parameter settings (K = 2, moderate separation) . . . . . . . . . . . . . . . 213.3 Parameter settings (K = 3, mild separation) . . . . . . . . . . . . . . . . . . 223.4 Average parameter estimates and relative bias after R = 100 repeats (K = 3,

high separation) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 263.5 Number of components, BIC, Rand index, Jaccard index and Fowlkes-Mallows

index (K = 3, high separation) . . . . . . . . . . . . . . . . . . . . . . . . . 273.6 Number of components, BIC, Rand index, Jaccard index and Fowlkes-Mallows

index assuming conditional independence (K = 3, high separation) . . . . . . 283.7 Average parameter estimates and relative bias after R = 100 repeats (K = 2,

moderate separation) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 283.8 Number of components, BIC, Rand index, Jaccard index and Fowlkes-Mallows

index (K = 2, moderate separation) . . . . . . . . . . . . . . . . . . . . . . . 293.9 Number of components, BIC, Rand index, Jaccard index and Fowlkes-Mallows

index assuming conditional independence (K = 2, moderate separation) . . . 303.10 Average parameter estimates and relative bias after R = 50 repeats (K = 3,

mild separation) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 313.11 Number of components, BIC, Rand index, Jaccard index and Fowlkes-Mallows

index (K = 3, mild separation) . . . . . . . . . . . . . . . . . . . . . . . . . 313.12 Number of components, BIC, Rand index, Jaccard index and Fowlkes-Mallows

index assuming conditional independence (K = 3, mild separation) . . . . . 32

4.1 Number of components and BIC (wholesale dataset) . . . . . . . . . . . . . . 374.2 Component parameter estimates (wholesale dataset) . . . . . . . . . . . . . . 374.3 Number of components and BIC assuming componentwise conditional inde-

pendence between variables (wholesale dataset) . . . . . . . . . . . . . . . . 37

vii

Chapter 1

Introduction

Non-Gaussian continuous data pertains to data comprised of a mixture of continuous dis-

parate variables with a variety of marginal distributions. Such data is ubiquitous in many

disciplines such as medicine and health care, genetics, marketing and finance. Although

non-Gaussian data commonly arises, there are a lack of standard models for data of this

nature and some current techniques assume conditional independence between the variables,

which can be problematic with regards to the data analysis. In this chapter, we review the

literature on current techniques for the analysis of non-Gaussian continuous data, as well as

introduce copula models as a flexible model for such data. We introduce the Expectation-

Maximization (EM) algorithm with applications in cluster analysis. Additionally, we outline

the methodology behind the parameter-expanded EM algorithm, a variant of the EM al-

gorithm, and inference functions for margins. Furthermore, we provide an overview of this

thesis and its objectives.

1.1 Joint models for non-Gaussian continuous data

In order to analyze multivariate data, we must first specify a joint distribution of the data.

However, in practice, this can be difficult to construct, especially if the variables have different

marginal distributions. Some current techniques, such as generalized linear mixed models

1

(GLMMs), rely on the assumption of conditional independence (Wu, 2013). A definition of

conditional independence from Dawid (1979) follows.

Definition 1.1. Consider random variables X,Y and Z. We say that X is conditionally

independent of Y given Z, denoted X ⊥⊥ Y | Z, if we can write

fX,Y (x,y | z) = fX(x | z)fY (y | z),

where fX,Y (x,y | z) represents the joint probability density function (PDF) of X and Y

given Z, fX(x | z) represents the conditional PDF of X given Z, and fY (y | z) represents

the conditional PDF of Y given Z. That is, X and Y are independent in their joint

distribution given Z = z, for any z.

Kosmidis and Karlis (2016) noted that models that assume conditional independence may

have limitations. Indeed, the consideration of the dependence structure between variables

can be a critical tool in multivariate data analysis and can provide valuable insight into

inter-variable relationships.

Another approach to the construction of joint models for non-Gaussian continuous data is

factorization. This technique involves the factoring of the joint PDF into a product of a con-

ditional and marginal PDF (Wu, 2013). Hence, we can write fX,Y (x,y) = fX(x | y)fY (y)

or, alternatively, fX,Y (x,y) = fY (y | x)fX(x), where fX(x) represents the marginal PDF

of X, fY (y) represents the marginal PDF of Y , fX(x | y) represents the conditional PDF

of X given Y and fY (y | x) represents the conditional PDF of Y given X. However, as

the direction of conditioning must be selected by the researcher, a hierarchy on the data is

induced (Jiryaie et al., 2016). Thus, different factorization models may result in different

estimates, as these models are not invariant to the direction of conditioning adopted (Jiryaie

et al., 2016). Furthermore, Wu (2013) noted that in high-dimensional settings, factorization

models may not be computationally tractable.

2

1.1.1 Gaussian copula distributions

Copula models are a flexible alternative to jointly model non-Gaussian continuous data.

As illustrated by Ren (2016), the objective is to specify the joint distribution of the data

by transforming the disparate variables into uniform variables via the probability integral

transform (PIT), and then using a copula to ‘glue’ together the margins (Jiryaie et al., 2016).

This section follows the work presented in Jiryaie et al. (2016) and Ren (2016).

LetX = (X1, ..., XP )> be a vector of continuous variables with corresponding cumulative

distribution functions (CDFs) FX1(X1), . . . , FXP(XP ). Recall that, via the PIT, FXj

(Xj) =

Uj ∼ uniform[0, 1], ∀j ∈ 1, . . . , P . Hence, as defined by Ren (2016), we can specify the P -

dimensional joint distribution function FX(x) = FX1,...,XP(x1, . . . , xP ) via the P -dimensional

copula C(u1, . . . , uP ) as

FX(x) = FU (u) = C(u1, . . . , uP ), (1.1)

where uj = FXj(xj) is a realization of Uj, j = 1, . . . , P . Thus, we can construct the joint

distribution of X1, ..., XP from their respective marginal distributions and the joint CDF

of U1, ..., UP , FU (u) = FU1,...,UP(u1, . . . , uP ), which we call a copula. Therefore, a copula is

simply the joint CDF of, possibly dependent, identically distributed uniform[0, 1] random

variables (Ren, 2016). Jiryaie et al. (2016) states that copulas allow great flexibility in mixed

data analysis as the margins do not need to come from the same parametric family. A formal

definition by Nelsen (2006) is provided below.

Definition 1.2. Let I = [0, 1] and IP = [0, 1]P , the P -dimensional unit hyperrectangle. A

P-dimensional copula is a function C(·) from IP to I with the following properties:

1. For every u in IP , C(u) = 0 if at least one coordinate of u is 0, and if all coordinates of

u are 1 except uj, then C(u) = uj.

3

2. For every hyperrectangle [a, b] = [a1, b1] × · · · × [aP , bP ], such that 0 ≤ aj ≤ bj ≤ 1, for

all j = 1, . . . , P ,

VC([a, b]) ≥ 0,

where VC([a, b]) is the volume of [a, b]. That is, C(u) is P -increasing.

Thus, we can construct a joint model for disparate continuous variables with a variety

of marginal distributions that need not be from the same parametric family. The copula is

a powerful and flexible tool in constructing joint multivariate distributions that do not rely

on limiting distributional assumptions.

Choosing an appropriate copula to join together the variable’s marginal distributions is

contingent upon the sufficiency of the copula’s dependence parameter to represent the data’s

dependency structure (Jiryaie et al., 2016). The Gaussian copula is a popular choice due to

its attractive mathematical properties. Given continuous variables X1 ∼ FX1(x1), . . . , XP ∼

FXP(xP ) with joint distribution function FX1,...,XP

(x1, . . . , xP ), the P -dimensional Gaussian

copula distribution (GCD) is defined as

FX(x; Θ,R) = ΦP (Φ−1(u1), . . . ,Φ−1(uP ); R), (1.2)

where Φ−1(u) is the standard normal quantile function, ΦP (u1, . . . , uP ; R) is the P -

dimensional Gaussian CDF with mean vector 0 and correlation matrix R, u1, . . . , uP are re-

alizations of their respective PITs U1 = FX1(X1;θ1) ∼ uniform[0, 1], . . . , UP = FXP(XP ;θP )

∼ uniform[0, 1], Θ = (θ>1 , . . . ,θ>P )>, and R is the correlation matrix of normal scores

Q1 = Φ−1(U1) ∼ N(0, 1), . . . , QP = Φ−1(UP ) ∼ N(0, 1). Here, θj can be a vector or a

scalar depending on the parameter of FXj(xj); for example, if X1 ∼ Gamma(α, β) and

X2 ∼ Exponential(λ), Θ = (θ>1 , θ2)>, where θ1 = (α, β)> and θ2 is simply the scalar λ. The

PDF fX(x; Θ,R) corresponding to the GCD defined in (1.2) is given by

4

fX(xi; Θ,R) =φP (qi1, . . . , qiP ; 0,R)∏P

j=1 φ(qij)

P∏j=1

fXj(xij;θj), (1.3)

where φ(qij) is the standard Gaussian PDF, φP (qi1, . . . , qiP ; 0,R) is the P -dimensional Gaus-

sian PDF with mean vector 0 and correlation matrix R, qij = Φ−1(uij) = Φ−1(FXj(xij;θj)),

and fXj(xij;θj) is the marginal PDF of Xij.

GCDs are a useful and flexible tool in the analysis of non-Gaussian data as they describe

dependence between variables in a similar fashion as Gaussian distributions (Jiryaie et al.,

2016).

1.2 Cluster analysis

Cluster analysis is the process of identifying meaningful groups in data. The main objective of

cluster analysis is to determine the underlying structure of the data without having any prior

information on what this structure might be. Typically, cluster analysis is either performed

via a distance-based or model-based approach. However, over the last ten years, the use of

mixture models for cluster analysis has dramatically increased (Andrews and McNicholas,

2012). A random vector X is from a parametric finite mixture distribution if, for all X = x,

we can write the PDF of X as

f(x; Θ,π) =K∑k=1

πkfk(x;θk), (1.4)

where π = (π1, . . . , πK)>, πk > 0 is the kth mixing proportion such that∑K

k=1 πk = 1,

fk(x;θk) is the PDF of the kth component, and Θ = (θ>1 , . . . ,θ>K)>, where θk = (θ>k1, . . . ,

θ>kP )> is the vector of parameters for component k = 1, . . . , K (Franczak, 2014). Typi-

cally, component densities are chosen to be of the same type (McNicholas, 2016); that is,

fk(x;θk) = f(x;θk) for all k = 1, ..., K. Historically, the multivariate Gaussian has been a

popular choice for the component densities due to its mathematical tractability and flexibil-

5

ity (Franczak, 2014). However, such approaches may not be suitable when we are concerned

with the analysis of non-Gaussian data, which can be comprised of a mixture of possibly

a large number of disparate variables with a variety of marginal distributions. Unlike con-

ventional model-based approaches that rely on the assumption of conditional independence,

GCDs model conditional dependence for each component among the disparate variables us-

ing the matrix of so-called normal correlations. Thus, we introduce a mixture of GCDs

as a flexible clustering methodology for the non-Gaussian continuous data. The PDF of a

mixture of GCDs is given by

f(xi; Θ,R1, . . . ,RK ,π) =K∑k=1

πkfk(xi;θk,Rk), (1.5)

where

fk(xi;θk,Rk) =φP (qik; 0,Rk)∏P

j=1 φ(qikj)

P∏j=1

fXj(xij;θkj) (1.6)

is the PDF of the kth component, πk is the kth mixing proportion, qik = (qik1, . . . , qikP )> =

(Φ−1(FX1(xi1;θk1)), . . . ,Φ−1(FXP

(xiP ;θkP )))>, and Rk is the correlation matrix of normal

scores for the kth component (Ren, 2016). The log-likelihood `(Θ,R1, . . . ,RK ,π) for a finite

mixture of GCDs is then

n∑i=1

K∑k=1

log πkφP (qik; 0,Rk)−n∑

i=1

K∑k=1

P∑j=1

(log φ(qikj)− log fXj(xij;θkj)). (1.7)

It should be noted that, if marginal parameters Θ are known, say, Θ = Θ0 = (θ>01, . . . ,θ>0K)>,

the log-likelihood in (1.7) will simply reduce to the profile log-likelihood `prof(R1, . . . ,RK ,π)

= `(Θ0,R1, . . . ,RK ,π) for R1, . . . ,RK and π given by

`prof(R1, . . . ,RK ,π) =n∑

i=1

K∑k=1

log πkφP (q0ik; 0,Rk), (1.8)

where q0ik = (q0ik1, . . . , q0ikP )> = (Φ−1(FX1(xi1;θ0k1), . . . ,Φ−1(FXP

(xiP ;θ0kP ))>, such that

6

θ0k = (θ>0k1, . . . ,θ>0kP )> is a vector of the known marginal parameters for each component.

For more information regarding model-based clustering of data using copulas, see Kosmidis

and Karlis (2016).

1.3 EM algorithm

The Expectation-Maximization (EM) algorithm is a technique used to obtain parameter

estimates via maximum likelihood estimation when there is missing or incomplete data

(Dempster et al., 1977). As highlighted in Ren (2016), the theory behind the EM algo-

rithm was first formally condensed by Dempster et al. (1977). In this section, we refer to

the EM algorithm in the context of cluster analysis illustrated in Franczak (2014). The EM

algorithm is an iterative procedure that alternates between an expectation step (E-step) and

a maximization step (M-step) until some convergence criterion is reached. The algorithm

utilizes the complete-data, where complete-data refers to the combination of the unobserved

or ‘missing’ data together with the observed data. In the E-step, we calculate the conditional

expectation of the complete-data log-likelihood given the observed data, and in the M-step

we maximize the complete-data log-likelihood with respect to our model parameters.

In the cluster analysis setting, we may not have incomplete data in the traditional sense.

However, since the cluster membership of each observation is unobserved, we can treat

this as ‘missing’ data and apply the EM algorithm in this setting. The complete-data is

comprised of our observed data, the observations xi, and our unobserved data, the cluster

memberships. Denote the complete-data likelihood as Lcomp(Θ), where Θ is the vector of

parameters. For example, let the conditional distribution of Xi, given that it belongs to

component k, be NP (µk,Σk), for k = 1, ..., K. The complete-data likelihood Lcomp(Θ) =

Lcomp(µ1, ...,µK ,Σ1, ...,ΣK , π1, . . . , πK) =∏n

i=1

∏Kk=1 (πkφP (xi;µk,Σk))zik is given by

n∏i=1

K∏k=1

{πk

(2π)P/2|Σk|1/2exp

(− 1

2(xi − µk)>Σ−1k (xi − µk)

)}zik

, (1.9)

7

where zik is a cluster membership indicator variable where

zik =

1, if xi belongs to cluster k

0, otherwise.

The complete-data log-likelihood `comp(Θ) = logLcomp(Θ) is then

K∑k=1

nk log πk −nP

2log 2π − 1

2

K∑k=1

nk|Σk| −1

2

n∑i=1

K∑k=1

zik(xi − µk)>Σ−1k (xi − µk), (1.10)

where nk =∑n

i=1 zik. The EM algorithm for a Gaussian mixture is detailed below.

E-step: Given the current estimate of the model parameters Θ(t) at iteration t, t = 0, 1, . . .,

calculate the conditional expectation

z(t+1)ik = E [Zik | xi] = P (Zik = 1 | xi) =

π(t)k φP (xi; µ

(t)k , Σ

(t)k )∑K

k′=1 π(t)k′ φP (xi; µ

(t)k′ , Σ

(t)k′ )

. (1.11)

M-step: Maximize E[`(t+1)comp(Θ) | x1, . . . ,xn], where `

(t+1)comp(Θ) is the complete-data log-

likelihood at the (t + 1)th iteration, with respect to the model parameters to obtain the

following MLEs:

π(t+1)k =

1

nn(t+1)k , (1.12)

µ(t+1)k =

1

n(t+1)k

n∑i=1

z(t+1)ik xi, (1.13)

Σ(t+1)k =

1

n(t+1)k

n∑i=1

zik(xi − µ(t+1)k )(xi − µ(t+1)

k )>. (1.14)

The algorithm iterates until some convergence criterion is reached, for example,

|Lcomp(Θ)(t+1) − Lcomp(Θ)(t)| < ε, (1.15)

8

where ε = 0.001, say.

The EM algorithm is indeed a useful tool for cluster analysis. However, if initial parame-

ters are chosen poorly, the EM algorithm may have slow convergence rates or, in some cases,

even nonconvergence (McLachlan and Krishnan, 2008). Moreover, as asserted by Everitt

et al. (2011), the use of finite mixture models can yield multiple maxima and, consquently,

may result in the EM algorithm converging to suboptimal MLEs.

1.3.1 PX-EM algorithm

In multivariate data analysis, researchers are often interested in estimating the correlation

between variables. In the context of GCDs, we aim to estimate the correlation matrix R

between normal scores, which must be positive definite (i.e., R > 0) and whose elements

are constrainted to lie in the interval [−1, 1] (Ren, 2016). When the parameter space is

constrained, issues of computational tractability and convergence may arise, particularly in

high-dimensional settings (Ren, 2016).

Liu et al. (1998) were the first to develop the methodology behind the parameter-

expanded EM (PX-EM) algorithm, which allows for improved convergence rates. Adopting

the parameter expansion technique, Xu and Craig (2010) proposed expanding the covariance

matrix Σ as

Σ = V1/2RV1/2, (1.16)

where V = diag(Σ) and R is the corresponding correlation matrix. We can then recover R

as

R = V−1/2ΣV−1/2. (1.17)

The PX-EM algorithm maintains the stability of the ordinary EM algorithm, but with

faster convergence rates (Liu et al., 1998). The parameter expansion technique provides us

9

with a more computationally efficient method to obtain an estimate of the matrix of normal

correlations.

1.4 Inference functions for margins

This section follows from the work done on inference functions for margins by Joe and

Xu (1996). When there are many parameters in a model, the estimation of all of these

parameters simultaneously can be difficult computationally. This is why the estimation

method of inference functions for margins (IFM) for multivariate models was introduced.

Their approach associates each model parameter with a lower-dimensional margin, which

allows parameters to be estimated from their corresponding marginal distribution.

As noted by Joe and Xu (1996), “the estimation method applies to models in which

the univariate margins are separated from the dependence structure,” which is the case for

GCDs. The IFM method is outlined below.

For example, let X = (X1, . . . , XP )> be a vector of continuous random variables with

respective marginal parameters Θ = (θ>1 , . . . ,θ>P )>. Consider the joint log-likelihood

`(Θ,R) =n∑

i=1

log fX(xi; Θ,R), (1.18)

where R is the dependence parameter, and the jth marginal log-likelihood

`j(θj) =n∑

i=1

log fXj(xij;θj), j = 1, . . . , P. (1.19)

Step 1: Maximize the univariate marginal log-likelihoods `j(θj) separately to obtain estimates

Θ = (θ>1 , . . . , θ>P )>.

Step 2: Maximize the joint log-likelihood evaluated at the marginal estimates calculated in

Step 1, `(Θ,R), over R to obtain the estimate R.

10

This methodology is advantageous as the optimization of several models with fewer pa-

rameters is more computationally efficient than the optimization of one model with many

parameters (Joe and Xu, 1996).

1.5 Overview of thesis

In this thesis, we demonstrate a clustering methodology that is a combination of IFM (Joe

and Xu, 1996) and the PX-EM algorithm (Liu et al., 1998) for GCDs. We outline a unified

model-based approach to clustering non-Gaussian continuous data based on flexible Gaussian

copula-based models for the joint distribution of the disparate variables.

In Chapter 2, we introduce a hybrid approach to clustering non-Gaussian continuous

data via GCDs that combines the methodologies of IFM and the PX-EM algorithm.

In Chapter 3, simulations are conducted to evaluate the performance of GCDs in a variety

of settings.

In Chapter 4, we apply our methodology to a real dataset that contains information

about the purchases by clients of a wholesale distributor.

In Chapter 5, we conclude the thesis by discussing our results and highlighting the

strengths and weaknesses of the GCD in clustering non-Gaussian continuous data, as well

as suggesting future areas of research in this field.

11

Chapter 2

Model-based clustering with Gaussian

copula distributions

In this chapter, we outline model-based cluster analysis of non-Gaussian continuous data

modelled according to a finite mixture of GCDs. In the estimation of the parameters of the

finite mixture model, we adopt a hybrid approach that combines IFM (Joe and Xu, 1996)

with the PX-EM algorithm (Liu et al., 1998) for computational efficiency.

2.1 Finite mixtures of GCDs

Let X1, . . . ,Xn be a random sample from a finite mixture of K GCDs, with common PDF

f(xi; Θ,R1, . . . ,RK ,π) given in equation (1.5), and with common PDF fk(xi;θk,Rk) for

component k = 1, . . . , K, given by the PDF of the GCD in equation (1.6). Note that

fk(xi;θk,Rk) is the conditional PDF of Xi = (Xi1, . . . , XiP )>, given that Xi belongs to

component k = 1, ..., K. Here, Θ contains all the marginal parameters θk = (θ>k1, . . . ,θ>kP )>,

for k = 1, . . . , K.

A natural question that arises from adopting a finite mixture of GCDs is that of identifi-

ability. Label switching is a common problem in cluster analysis, and having the component

labels switched on different iterations of the EM algorithm may be problematic with regards

12

to the estimates we obtain (Everitt et al., 2011). Not only do we need to ensure that our

mixture of GCDs is identifiable, but also that the finite mixture for each continuous vari-

able is identifiable. Everitt et al. (2011) suggest that imposing identifiability constraints on

certain model parameters can help overcome the problem of label switching and allow us to

meaningfully interpret the components. Thus, we impose identifiability constraints on the

marginal parameters of the disparate continuous variables to address this issue. For exam-

ple, for a mixture of K univariate Gaussian components, we can impose the identifiability

constraint µ1 < µ2 < · · · < µK (Everitt et al., 2011) on the mean vector µ = (µ1, . . . , µK)>

containing the means of the Gaussian components.

To construct the complete-data likelihood Lcomp(Θ,R1, . . . ,RK ,π), let

zik =

1, if xi belongs to cluster k

0, otherwise

,

so that the complete-data log-likelihood `comp(Θ,R1, . . . ,RK ,π) = logLcomp(Θ,R1, . . . ,

RK ,π) becomes

`comp(Θ,R1, . . . ,RK ,π) =n∑

i=1

K∑k=1

zik log πk +n∑

i=1

K∑k=1

zik log φP (qik;θk,Rk)

−n∑

i=1

K∑k=1

P∑j=1

zik(log φ(qikj)− log fXj

(xij;θkj)). (2.1)

For computational efficiency, we estimate the marginal parameter Θ by IFM, and upon

replacing Θ with its IFM estimate in (2.1), note that `comp(Θ,R1, . . . ,RK ,π) reduces to the

usual log-likelihood of a finite mixture of P -dimensional Gaussian distributions for the normal

scores Qik = (Qik1, . . . , QikP )>, where Qikj = Φ−1(Uikj), such that Uikj = FXj(Xij;θkj) ∼

uniform[0, 1] is the (conditional) PIT, with FXj(xij;θkj) being the (conditional) marginal

CDF of Xij for component k. Here, we assume that FXj(xij;θkj) belongs to the same

parametric family for all k, for simplicity, with only the parameters θkj different across the

13

K components.

We can then easily estimate the component-specific normal correlation matrix Rk via

the conventional EM algorithm for Gaussian mixture models. As Rk is a correlation ma-

trix, we adopt parameter expansion to transform Rk into a conventional covariance matrix.

In addition, to simplify the M-step, we modify the PX-EM algorithm by adopting IFM

and replacing the maximization of the conditional expectation of the complete-data log-

likelihood function, given the observed data, with separate maximizations of the complete-

data marginal log-likelihood functions to estimate the marginal parameters. Note that in

the case of Gaussian mixture models, the M-step does not require actually maximizing the

expectation of the complete-data log-likelihood function because the parameter updates are

all in closed-form; this is because the complete-data log-likelihood function is linear in the

so-called complete-data sufficient statistics, and the updates are all functions of just these

sufficient statistics. However, for a finite mixture of GCDs, the normal scores, which trans-

form the complete-data into standard normal random variables, are not linear functions of

the complete-data, and, therefore, the M-step of the PX-EM algorithm will entail numeri-

cally maximizing the complete-data log-likelihood function. Thus, the nice computational

simplicity of the PX-EM algorithm in the case of Gaussian mixture models is lost in the case

of mixtures of GCDs, necessitating the modification we adopted via the IFM. We outline

this hybrid PXEM-IFM algorithm in what follows.

2.2 PXEM-IFM algorithm

This section follows the work of Ren (2016). In the case of a finite mixture of GCDs, due to

the fact that the elements of Rk are constrained to lie in the interval [−1, 1], this calculation

may not be computationally tractable and there may be issues with convergence. Thus, we

adopt the parameter expansion technique to obtain the estimate of Rk, for k = 1, . . . , K.

We have that normal scores Qikiid∼ NP (0,Rk), and, given an estimate Θ is available (e.g.,

14

via IFM), we treat this as the true value of Θ. Using parameter expansion, define Wik =

(Wik1, . . . ,WikP )> = {diag(Σk)}1/2Qik = (√σk11Qik1, . . . ,

√σkPPQikP )> and it follows that

Wikiid∼ NP (0,Σk = {diag(Σk)}1/2Rk{diag(Σk)}1/2), (2.2)

where diag(Σk) = diag(σk11, . . . , σkPP ) is the P×P diagonal matrix of the diagonal elements

σk11, . . . , σkPP of Σk.

As we already have the estimate Θ of Θ, we need only estimate R1, . . . ,RK and π. The

complete-data profile log-likelihood `comp-prof(R1, . . . ,RK ,π) = `comp(Θ,R1, . . . ,RK ,π)

for R1, . . . ,RK and π is then

`comp-prof(R1, . . . ,RK ,π) =n∏

i=1

K∏k=1

{πk

(2π)p/2|Rk|1/2exp

(− 1

2q>ikR

−1k qik

)}zik

. (2.3)

After applying parameter expansion, the complete-data profile log-likelihood

`comp-prof(Σ1, . . . ,ΣK ,π) for Σ1, . . . ,ΣK and π is then

`comp-prof(Σ1, . . . ,ΣK ,π) =n∏

i=1

K∏k=1

{πk

(2π)p/2|Σk|1/2exp

(− 1

2w>ikΣ

−1k wik

)}zik

. (2.4)

In (2.3) and (2.4), wik = (wik1, . . . , wikP )> = diag(Σk)1/2qik and qik = (qik1, . . . , qikP )>

are the respective realizations of Wik and Qik. We outline the PXEM-IFM algorithm below.

• Initialization: Initialize cluster membership indicator z(0)ik by performing k-means clus-

tering on the data using the kmeans function in R. Also, let the initial estimates be π(0)k ,

θ(0)k and Σ

(0)k (i.e., R

(0)k ), which are calculated based on the initial cluster memberships

obtained from z(0)ik .

• E-step: Given current estimates π(t)k , θ

(t)k and Σ

(t)k (i.e., R

(t)k ), calculate q

(t+1)ikj , z

(t+1)ik and

w(t+1)ik as follows:

15

z(t+1)ik =

π(t)k f

(t)k (xi; Θ, R

(t)1 , . . . , R

(t)K )∑K

k′=1 π(t)k′ f

(t)k′ (xi; Θ, R

(t)1 , . . . , R

(t)K )

, (2.5)

q(t+1)ikj = Φ−1(FXj

(xij; θ(t)kj )), (2.6)

w(t+1)ik = {diag

(Σ

(t)k

)}1/2q(t+1)

ik . (2.7)

The observation xi is then assigned to component k if

z(t+1)ik = max

k′=1,...,Kz(t+1)ik′ . (2.8)

• M-step: Denote the number of observations assigned to component k at iteration t + 1

by n(t+1)k =

∑ni=1 z

(t+1)ik . The updated estimates π

(t+1)k , Σ

(t+1)k and R

(t+1)k are given by

π(t+1)k =

1

nn(t+1)k , (2.9)

Σ(t+1)k =

1

n(t+1)k

n∑i=1

z(t+1)ik

(w

(t+1)ik − 1

n(t+1)k

n∑i=1

z(t+1)ik w

(t+1)ik

)

×

(w

(t+1)ik − 1

n(t+1)k

n∑i=1

z(t+1)ik w

(t+1)ik

)>, (2.10)

R(t+1)k = {diag(Σ

(t+1)k )}−1/2Σ(t+1)

k {diag(Σ(t+1)k )}−1/2. (2.11)

For the update θ(t+1)kj , we adopt the IFM, which especially suits GCDs since the univariate

margins fXj(xij;θkj) do not depend on the correlation matrix Rk, for each component k

16

(Joe and Xu, 1996). If the marginal MLE θ(t+1)kj of θkj exists as a closed-form solution of

the marginal likelihood equation for component k, we use it to update the corresponding

marginal parameters; for example, if the marginal distribution of Xj for component k is

Gaussian with mean µkj, the updated estimate for µkj at iteration t+ 1 is simply

µ(t+1)kj =

1

n(t+1)k

n∑i=1

z(t+1)ik xij.

If there is no closed-form solution to the marginal likelihood equations, we can construct

estimating equations based on the moments of Qikj|zik = 1 ∼ N(0, 1) to obtain the updated

estimates θ(t+1)kj . For example, if θkj is scalar, then we can estimate θkj as the solution of the

unbiased estimating equation

q(t+1)kj =

1

n(t+1)k

n∑i=1

z(t+1)ik q

(t+1)ikj = 0. (2.12)

Note that (2.12) is unbiased because E(Qkj | z1k, . . . , znk) = E(Qikj | z1k, . . . , znk) = 0,

where Qkj = 1nk

∑ni=1 zikQikj; this follows from the fact that Qikj|z1k, . . . , znk ∼ N(0, 1). If

θkj = (θkj1, θkj2)>, then we add another unbiased estimating equation given by

1

n(t+1)k − 1

n∑i=1

z(t+1)ik (q

(t+1)ikj − q(t+1)

kj )2 − 1 = 0. (2.13)

As E(

1nk−1

∑ni=1 zik(Qikj −Qkj)

2∣∣∣ z1k, . . . , znk) = 1, since Qikj|z1k, . . . , znk ∼ N(0, 1), the

estimating equation (2.13) is unbiased. Using the divisor nk is also possible, provided nk is

large enough; otherwise, (2.13) is only asymptotically unbiased.

We can use as many moments of Qikj as there are parameters in θkj to construct estimat-

ing equations for θkj. We can then use the multiroot function in the rootSolve package

(Soetaert, 2015) to solve the estimating equations, such as those in (2.12) and (2.13). Note

that solving the estimating equations in (2.12) and (2.13) is easier than maximizing the

conditional expectations of the marginal complete-data log-likelihood functions given the

17

observed data.

The algorithm continues iterating between the E- and M-steps until the following con-

vergence criterion is reached

||Θ(t+1) −Θ(t)|| < ε, (2.14)

where ε = 0.001. In this scenario, we consider parameter convergence instead of log-likelihood

convergence because our estimates are obtained based on a “pseudo-log-likelihood” and not

on the full likelihood based on the observed data x1, . . . ,xn; consequently, the parameter

estimates we obtain from the PXEM-IFM algorithm are not technically MLEs. However,

as detailed in Ren (2016) and Joe and Xu (1996), although these estimates may not be as

efficient as their respective MLEs, they exhibit the same nice asymptotic properties (e.g.,

asymptotic unbiasedness, asymptotic normality) that MLEs do.

2.3 Discussion

In this chapter, we discussed our proposed methodology for model-based clustering with

GCDs. Using GCDs provides us with a flexible way to model the joint distribution of

disparate continuous variables, since we can model the variables’ marginal distributions

independently, while still accounting for the data’s dependence structure via the Gaussian

copula. The use of IFM in combination with the PX-EM algorithm increases computational

efficiency and mitigates potential issues with convergence.

In the next chapter, we provide simulation results to assess the performance of GCDs in

clustering non-Gaussian continuous data.

18

Chapter 3

Simulations

In this chapter, a variety of simulation studies are carried out to evaluate the performance

of GCDs in clustering non-Gaussian continuous data.

3.1 Simulation design

In this simulation study, we consider disparate, continuous variables X1, . . . , XP and we aim

to determine the performance of GCDs in clustering these data. Moreover, we investigate

the impact that assuming componentwise conditional independence between variables has on

our results. When simulating the data, we consider such factors as the degree of separation

between components, number of components, number of variables, marginal distribution of

variables, correlation between variables and sample size. Note that the components in each

simulation have equal mixing proportions; that is, for K clusters, π1 = . . . = πK .

The BIC is used to select the optimal number of clusters, and we measure the clustering

accuracy using a variety of clustering indicies, both of which are discussed in Section 3.2.

Additionally, we compute the relative bias of our parameter estimates, which is also defined

in Section 3.2.

19

3.1.1 Parameter settings

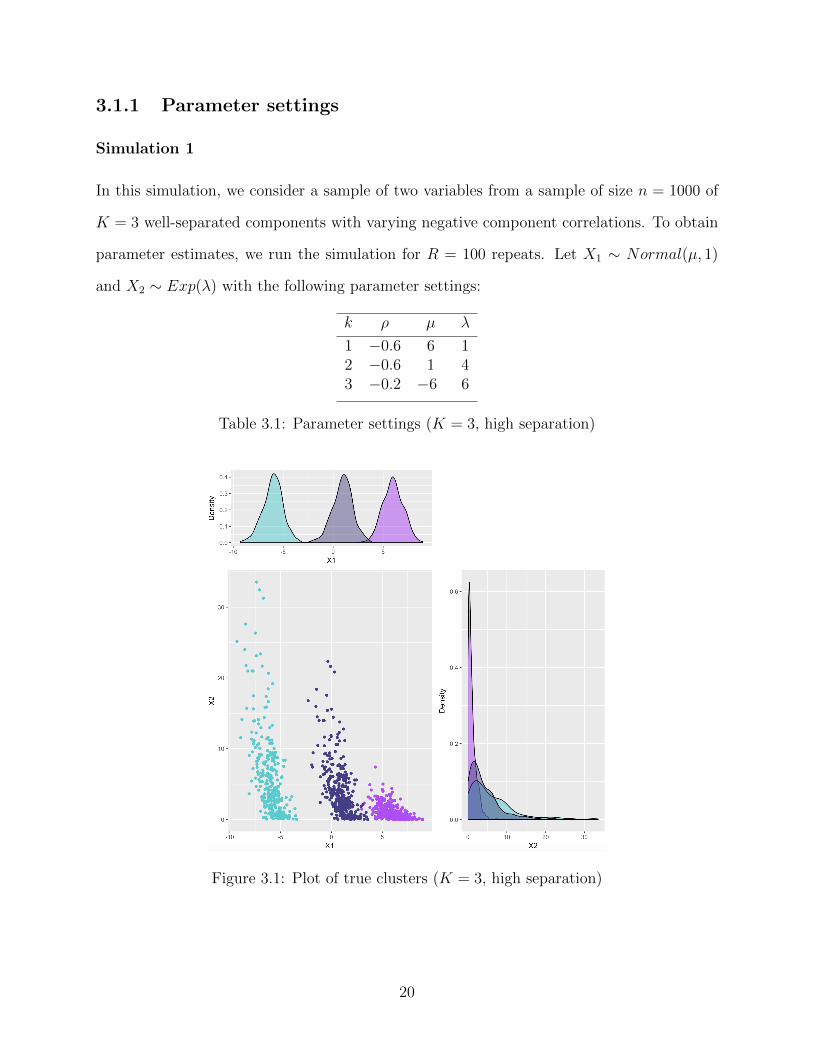

Simulation 1

In this simulation, we consider a sample of two variables from a sample of size n = 1000 of

K = 3 well-separated components with varying negative component correlations. To obtain

parameter estimates, we run the simulation for R = 100 repeats. Let X1 ∼ Normal(µ, 1)

and X2 ∼ Exp(λ) with the following parameter settings:

k ρ µ λ

1 −0.6 6 12 −0.6 1 43 −0.2 −6 6

Table 3.1: Parameter settings (K = 3, high separation)

Figure 3.1: Plot of true clusters (K = 3, high separation)

20

Simulation 2

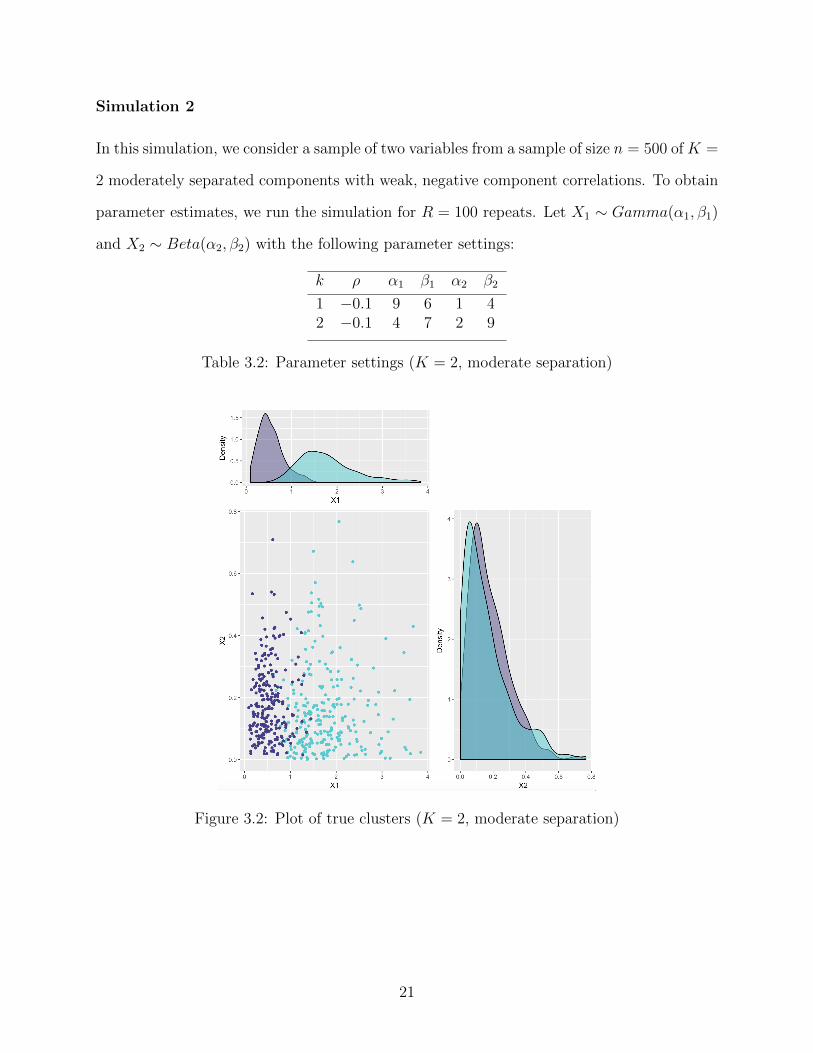

In this simulation, we consider a sample of two variables from a sample of size n = 500 of K =

2 moderately separated components with weak, negative component correlations. To obtain

parameter estimates, we run the simulation for R = 100 repeats. Let X1 ∼ Gamma(α1, β1)

and X2 ∼ Beta(α2, β2) with the following parameter settings:

k ρ α1 β1 α2 β2

1 −0.1 9 6 1 42 −0.1 4 7 2 9

Table 3.2: Parameter settings (K = 2, moderate separation)

Figure 3.2: Plot of true clusters (K = 2, moderate separation)

21

Simulation 3

In this simulation, we consider a sample of three variables from a sample size of n = 1000 of

K = 3 mildly separated components with moderately strong, positve component correlations.

To obtain parameter estimates, we run the simulation for R = 50 repeats. Let X1 ∼

Gamma(α1, β1), X2 ∼ Normal(µ, 1) and X3 ∼ Beta(α3, β3) with the following parameter

settings:

k ρ12 ρ13 ρ23 α1 β1 µ α3 β3

1 0.5 0.5 0.5 8 4 0 10 12 0.5 0.5 0.5 5 8 −3 5 33 0.5 0.5 0.5 1 1 −2 7 5

Table 3.3: Parameter settings (K = 3, mild separation)

Figure 3.3: Plot of true clusters (K = 3, mild separation)

22

3.2 Model selection criterion

3.2.1 Bayesian information criterion

In cluster analysis, one challenge researchers face is the selection of the optimal number of

clusters given the data. This can be difficult in practice, especially when the clusters are

highly latent. Schwarz (1978) was one of the first to introduce the concept of model selection

using a Bayesian approach. The Bayesian Information Criterion (BIC) is widely used and,

as asserted by Franczak (2014), is shown to have advantageous asymptotic properties. The

BIC is defined as

BIC = −2`(x; Θ) + q log(n), (3.1)

where `(x; Θ) is the maximized log-likelihood, Θ is the MLE of Θ, q is the number of free

parameters and n is the sample size (Franczak, 2014). Thus, we select the optimal number of

components based on the model which minimizes the BIC. The BIC can be more conservative

than other model selection criterion as it penalizes both the number of free parameters in

the model as well as the sample size.

In this thesis, we use the BIC to identify the optimal number of clusters in the data. For

P variables and a mixture of K components, the number of free parameters, q, is calcualted

as

q = m+ (K − 1) +KP (P − 1)

2, (3.2)

where m is the number of marginal parameters needed to be estimated, (K−1) accounts for

the estimation of the mixing proportions, πk, and KP (P − 1)/2 accounts for the estimation

of K correlation matrices. Although the BIC is a popular means for model selection, the

number of components it selects may not necessarily be optimal (McNicholas, 2016), and a

deep comprehension of the subject matter is also highly valuable when choosing the number

23

of clusters.

3.2.2 Clustering indices

In order to assess the performance of GCDs in clustering data, we use a variety of clustering

indices to measure the similarity between groups (Desgraupes, 2017). In this section, we

outline three popular clustering indices: the Rand index, the Jaccard index and the Fowlkes-

Mallows index. These clustering indices lie in the interval [0, 1], where indices close to 1

indicate strong agreement of clustering and indices close to 0 indicate poor agreement of

clustering. Definitions obtained from Desgraupes (2017) and Ruan (2015) follow.

Let P1 represent partition 1 and P2 represent partition 2. For a pair of points, there are

four possibilities:

• the two points belong to the same cluster, according to both P1 and P2

• the two points belong to the same cluster according to P1, but not P2

• the two points belong to the same cluster according to P2, but not P1

• the two points do not belong to the same cluster, according to both P1 and P2

Denote A,B,C, and D the number of points belonging to each of the four categories,

respectively. We measure the similarity of the true cluster and computed cluster by counting

the number of pairs of points that are in A,B,C and D. Let n be the number of observations

and nt be the total number of pairs of points. Hence, we have

nt = A+B + C +D =n(n− 1)

2. (3.3)

Rand index

The Rand index is defined as

24

R =A+D

nt

, (3.4)

which measures the agreement of clustering by the proportion of pairs of points that belong

to the same cluster or do not belong to the same cluster, according to both P1 and P2.

Jaccard index

The Jaccard index is defined as

J =A

A+B + C, (3.5)

which measures the agreement of clustering by the proportion of pairs of points that belong

to the same cluster, according to both P1 and P2, relative to the number of pairs of points

that belong to the same cluster in at least one of the partitions.

Fowlkes-Mallows index

The Fowlkes-Mallows index is defined as

FM =A√

(A+B)(A+ C), (3.6)

which measures the agreement of clustering by the geometric mean of the proportion of

pairs of points that belong to the same cluster, according to both P1 and P2, relative to the

number of pairs of points that belong to the same cluster in at least one of the partitions.

In this chapter, we use these three clustering indices to measure the GCDs accuracy of

clustering. The adjustedRand function in the clues package (Chang et al., 2016) is used to

calculate these indices.

25

3.2.3 Relative bias

In order to measure the percentage that a parameter estimate differs from its true value, we

use relative bias. We define the relative bias (in %) of the estimate θ as

Relative bias of θ =Mean of θ − θ

θ× 100%, (3.7)

where the mean of θ is obtained by taking the average of θ after R repeats (Ruan, 2015).

3.3 Results

Note that plots of clusters obtained via GCD and values of BIC and clustering indices are

based on one run of the algorithm.

3.3.1 Simulation 1

Below are the clustering results of simulated data from the parameter settings outlined in

Section 3.1 for simulation 1. The lowest BIC indicating the optimal number of clusters is

bolded.

Parameter Mean RB (%)

µ1 = 6 6.012 0.200µ2 = 1 1.006 0.600µ3 = −6 −5.642 −5.967λ1 = 1 0.974 −2.600λ2 = 4 3.984 −0.400λ3 = 6 5.846 −2.567

ρ1 = −0.6 −0.582 −3.000ρ2 = −0.6 −0.584 −2.667ρ3 = −0.2 −0.224 12.000

Table 3.4: Average parameter estimates and relative bias after R = 100 repeats (K = 3,high separation)

26

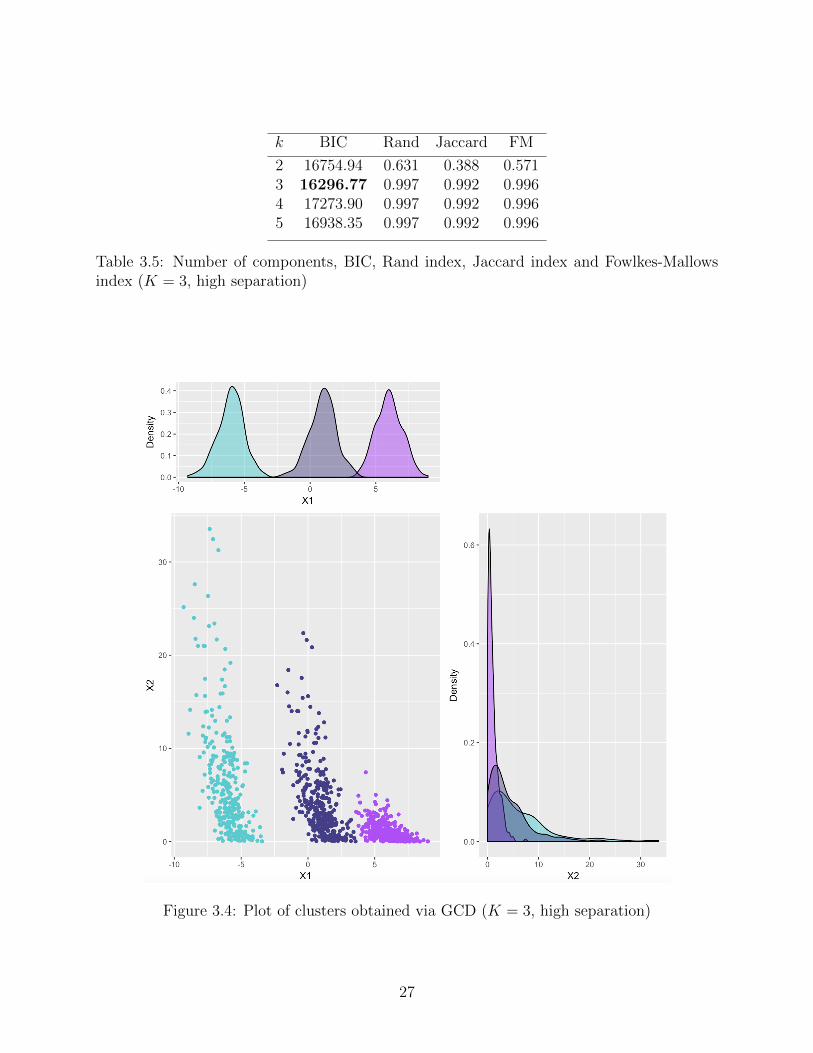

k BIC Rand Jaccard FM

2 16754.94 0.631 0.388 0.5713 16296.77 0.997 0.992 0.9964 17273.90 0.997 0.992 0.9965 16938.35 0.997 0.992 0.996

Table 3.5: Number of components, BIC, Rand index, Jaccard index and Fowlkes-Mallowsindex (K = 3, high separation)

Figure 3.4: Plot of clusters obtained via GCD (K = 3, high separation)

27

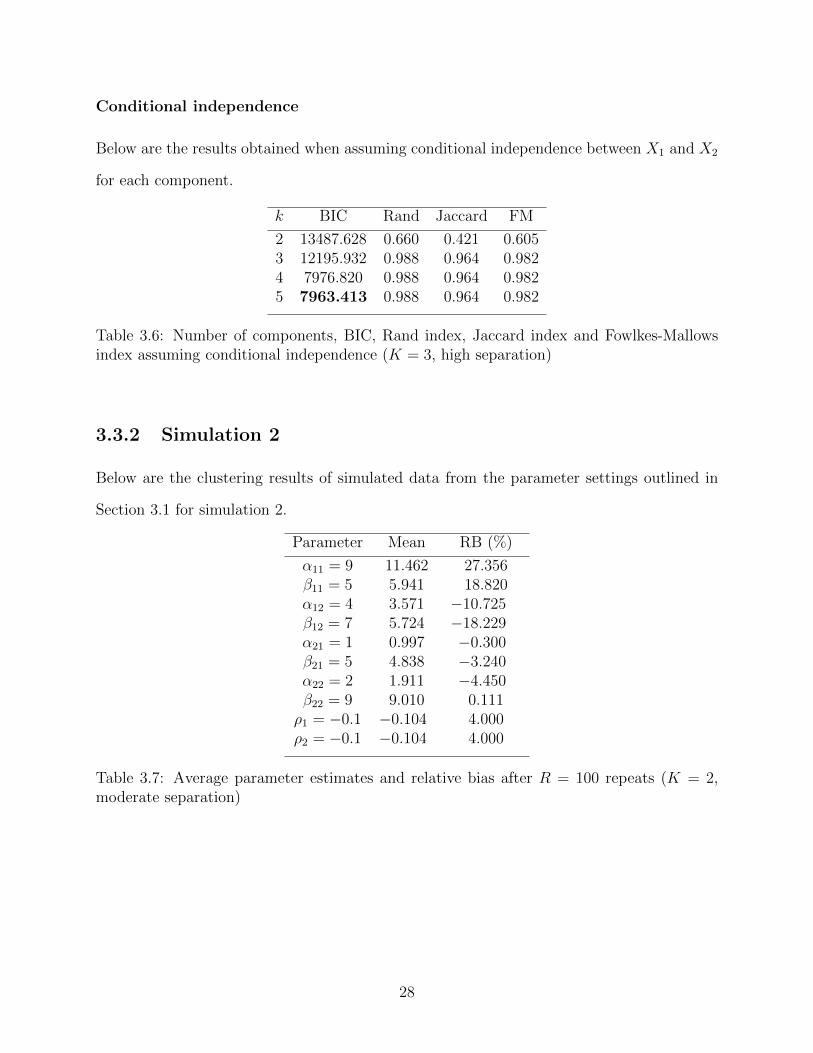

Conditional independence

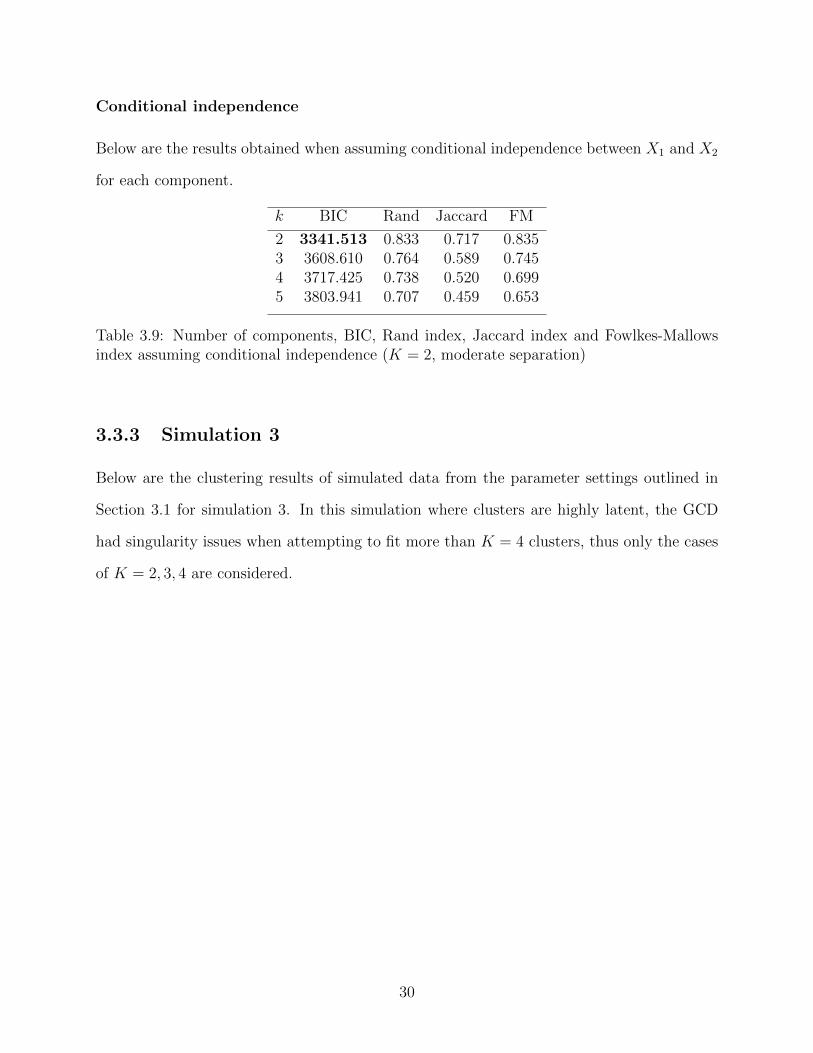

Below are the results obtained when assuming conditional independence between X1 and X2

for each component.

k BIC Rand Jaccard FM

2 13487.628 0.660 0.421 0.6053 12195.932 0.988 0.964 0.9824 7976.820 0.988 0.964 0.9825 7963.413 0.988 0.964 0.982

Table 3.6: Number of components, BIC, Rand index, Jaccard index and Fowlkes-Mallowsindex assuming conditional independence (K = 3, high separation)

3.3.2 Simulation 2

Below are the clustering results of simulated data from the parameter settings outlined in

Section 3.1 for simulation 2.

Parameter Mean RB (%)

α11 = 9 11.462 27.356β11 = 5 5.941 18.820α12 = 4 3.571 −10.725β12 = 7 5.724 −18.229α21 = 1 0.997 −0.300β21 = 5 4.838 −3.240α22 = 2 1.911 −4.450β22 = 9 9.010 0.111ρ1 = −0.1 −0.104 4.000ρ2 = −0.1 −0.104 4.000

Table 3.7: Average parameter estimates and relative bias after R = 100 repeats (K = 2,moderate separation)

28

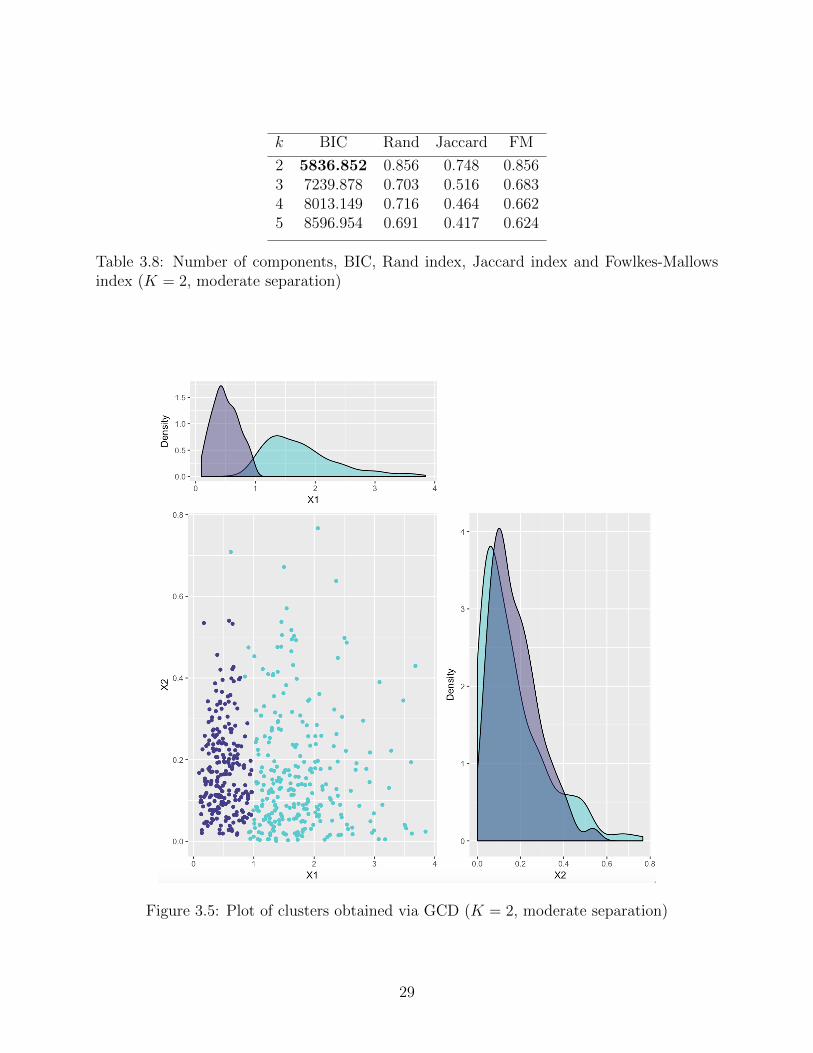

k BIC Rand Jaccard FM

2 5836.852 0.856 0.748 0.8563 7239.878 0.703 0.516 0.6834 8013.149 0.716 0.464 0.6625 8596.954 0.691 0.417 0.624

Table 3.8: Number of components, BIC, Rand index, Jaccard index and Fowlkes-Mallowsindex (K = 2, moderate separation)

Figure 3.5: Plot of clusters obtained via GCD (K = 2, moderate separation)

29

Conditional independence

Below are the results obtained when assuming conditional independence between X1 and X2

for each component.

k BIC Rand Jaccard FM

2 3341.513 0.833 0.717 0.8353 3608.610 0.764 0.589 0.7454 3717.425 0.738 0.520 0.6995 3803.941 0.707 0.459 0.653

Table 3.9: Number of components, BIC, Rand index, Jaccard index and Fowlkes-Mallowsindex assuming conditional independence (K = 2, moderate separation)

3.3.3 Simulation 3

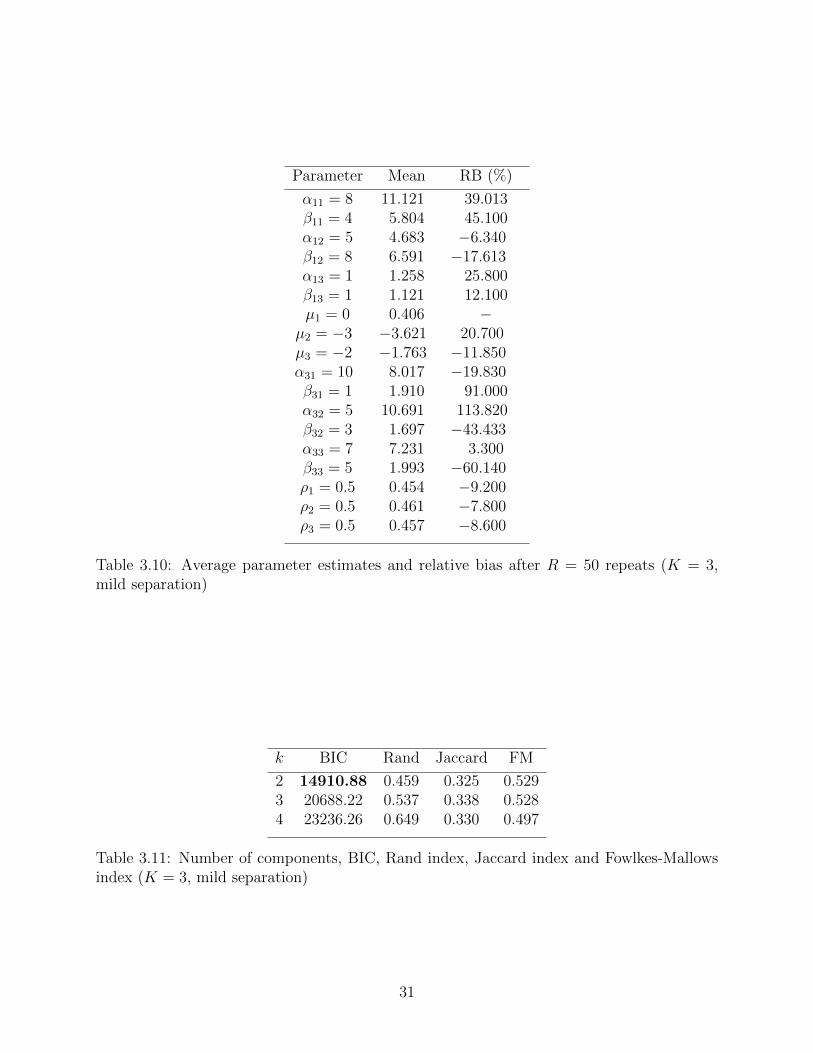

Below are the clustering results of simulated data from the parameter settings outlined in

Section 3.1 for simulation 3. In this simulation where clusters are highly latent, the GCD

had singularity issues when attempting to fit more than K = 4 clusters, thus only the cases

of K = 2, 3, 4 are considered.

30

Parameter Mean RB (%)

α11 = 8 11.121 39.013β11 = 4 5.804 45.100α12 = 5 4.683 −6.340β12 = 8 6.591 −17.613α13 = 1 1.258 25.800β13 = 1 1.121 12.100µ1 = 0 0.406 −µ2 = −3 −3.621 20.700µ3 = −2 −1.763 −11.850α31 = 10 8.017 −19.830β31 = 1 1.910 91.000α32 = 5 10.691 113.820β32 = 3 1.697 −43.433α33 = 7 7.231 3.300β33 = 5 1.993 −60.140ρ1 = 0.5 0.454 −9.200ρ2 = 0.5 0.461 −7.800ρ3 = 0.5 0.457 −8.600

Table 3.10: Average parameter estimates and relative bias after R = 50 repeats (K = 3,mild separation)

k BIC Rand Jaccard FM

2 14910.88 0.459 0.325 0.5293 20688.22 0.537 0.338 0.5284 23236.26 0.649 0.330 0.497

Table 3.11: Number of components, BIC, Rand index, Jaccard index and Fowlkes-Mallowsindex (K = 3, mild separation)

31

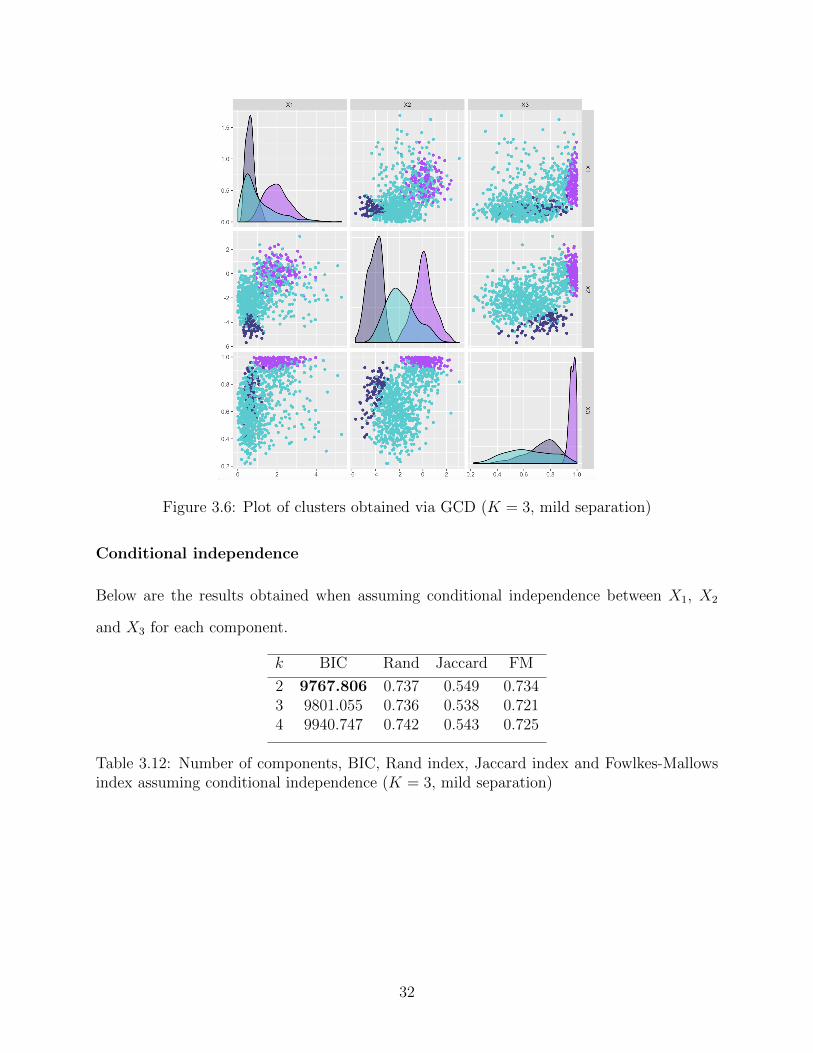

Figure 3.6: Plot of clusters obtained via GCD (K = 3, mild separation)

Conditional independence

Below are the results obtained when assuming conditional independence between X1, X2

and X3 for each component.

k BIC Rand Jaccard FM

2 9767.806 0.737 0.549 0.7343 9801.055 0.736 0.538 0.7214 9940.747 0.742 0.543 0.725

Table 3.12: Number of components, BIC, Rand index, Jaccard index and Fowlkes-Mallowsindex assuming conditional independence (K = 3, mild separation)

32

3.3.4 Discussion

In the case of K = 3 well-separated components, the GCD performs well and correctly

identifies the number of clusters. Clustering indices close to 1 reflect nearly perfect agreement

of clusters. The GCD is able to identify a maximum of K = 3 clusters, which is why the

clustering indices for the cases of K = 4 and K = 5 clusters are the same as K = 3, as

there were 0 observations assigned to the fourth and fifth component. After R = 100 repeats,

parameter estimates are close to their true values with relatively low bias. Additionally, under

the assumption of componentwise conditional independence, the GCD incorrectly selects the

number of clusters and has slightly lower clustering indices for K = 3 components.

For K = 2 moderately separated components, based on the BIC, the GCD correctly

selects the number of components. As expected, clustering indices are lower than the case

of well-separated components, but are still relatively close to 1. When assuming componen-

twise conditional independence, the GCD is able to identify the correct number of clusters.

However, in this case, clustering indices are slightly lower than when we take into account

the dependence between variables. After R = 100 repeats, parameter estimates are still

reasonably close to their true values, although with typically higher relative biases. Also,

since closed-form solutions for the MLEs of the marginal parameters do not exist, the use of

the multiroot function is more computationally intensive and is sometimes sensitive to the

initial values selected.

When considering the case of K = 3 components with mild separation, the GCD mis-

specifies the number of clusters and has much lower clustering indices than when there is

greater compenent separation. As a result of the mild component separation, parameter

estimates generally have higher bias and, due to computational tractability and efficiency,

we only consider R = 50 repeats. The high component latency also results in more singu-

larity issues and, in combination with the use of the multiroot function, results in much

slower calculations. Assuming conditional independence, we also have an incorrect selection

of components, but with higher clustering indices than when we do not make this assump-

33

tion. These results may be attributed to the fact that high component latency can lead to

an increased difficulty in identifying clusters and, consequently, their parameter estimates.

Overall, the GCD performs well in identifying the underlying structure of the data,

including parameter estimation and assigning cluster memberships. The GCD struggles

as the separation between clusters decreases, as this overlap makes it more challenging to

identify the true components, which is to be expected. From the simulation study, one may

also reasonably conclude that ignoring the componentwise dependence between variables

may yield misleading results.

In the next chapter, we apply this methodology to a dataset to further assess its perfor-

mance.

34

Chapter 4

Application

In this chapter, we apply the methodology outlined in Chapter 2 to perform cluster analysis

on a dataset involving the purchases made by clients of a wholesale distributor in Portugal

(Cardoso, 2013; Abreu, 2011).

4.1 Overview of dataset

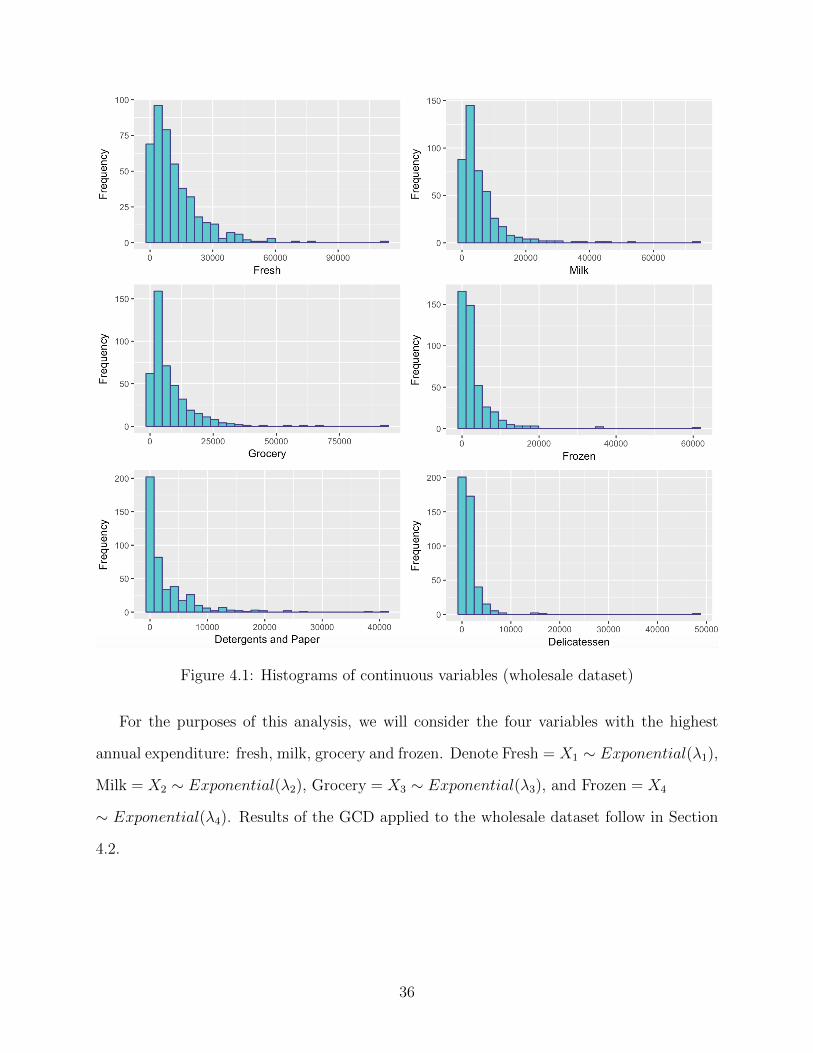

This dataset is comprised of measurements on 440 clients of a wholesale distributor in Por-

tugal. There are 8 variables in the dataset: 6 continuous and 2 nominal. The 6 continuous

variables reflect the annual spending in monetary units on the following categories: fresh

products, milk products, grocery products, frozen products, detergents and paper products,

and delicatessen products. Of the 2 nominal variables, one indicates the customer’s channel,

which is either a horeca (hotel/restaurant/cafe) channel or a retail channel. The other nom-

inal variable indicates the customer’s region, which is one of three options: Lisbon, Oporto,

or other. As noted by Saunders (1980), cluster analysis is widely used in marketing and can

be an effective technique in market segmentation.

We are interested in determining the underlying group structure of the dataset. Looking

at the marginal distributions of the continuous variables, one can see that each variable

appears to follow an exponential distribution.

35

Figure 4.1: Histograms of continuous variables (wholesale dataset)

For the purposes of this analysis, we will consider the four variables with the highest

annual expenditure: fresh, milk, grocery and frozen. Denote Fresh = X1 ∼ Exponential(λ1),

Milk = X2 ∼ Exponential(λ2), Grocery = X3 ∼ Exponential(λ3), and Frozen = X4

∼ Exponential(λ4). Results of the GCD applied to the wholesale dataset follow in Section

4.2.

36

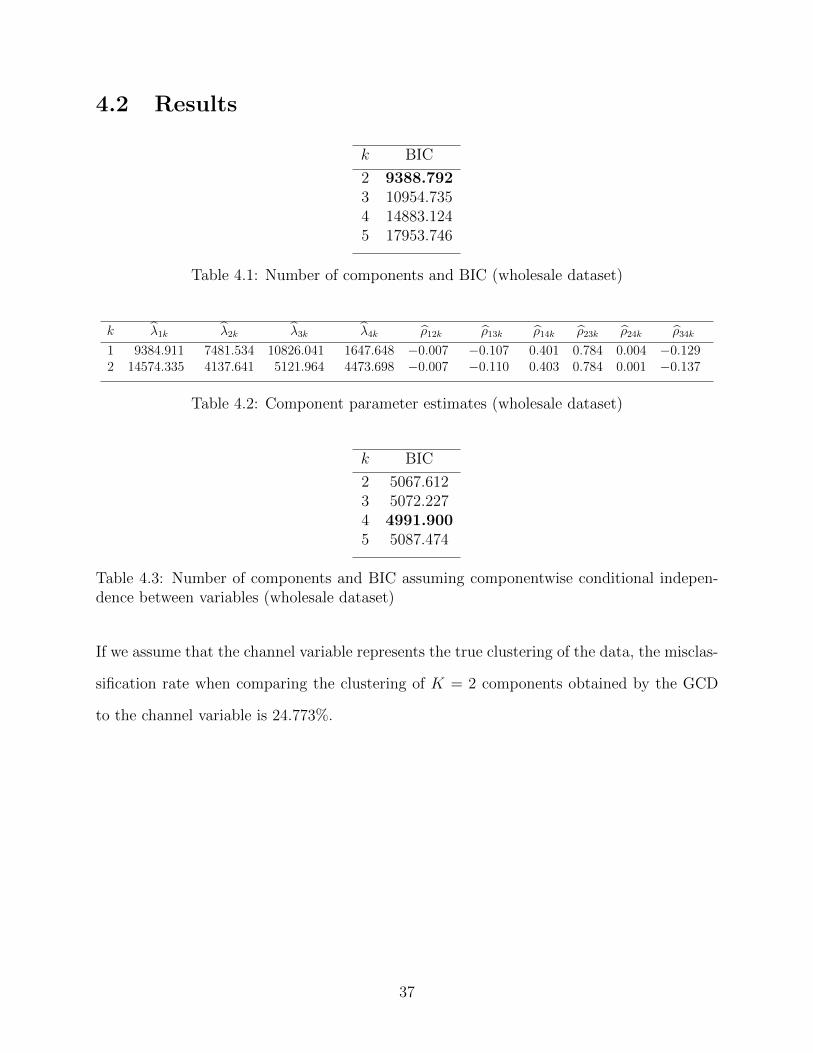

4.2 Results

k BIC

2 9388.7923 10954.7354 14883.1245 17953.746

Table 4.1: Number of components and BIC (wholesale dataset)

k λ1k λ2k λ3k λ4k ρ12k ρ13k ρ14k ρ23k ρ24k ρ34k

1 9384.911 7481.534 10826.041 1647.648 −0.007 −0.107 0.401 0.784 0.004 −0.1292 14574.335 4137.641 5121.964 4473.698 −0.007 −0.110 0.403 0.784 0.001 −0.137

Table 4.2: Component parameter estimates (wholesale dataset)

k BIC

2 5067.6123 5072.2274 4991.9005 5087.474

Table 4.3: Number of components and BIC assuming componentwise conditional indepen-dence between variables (wholesale dataset)

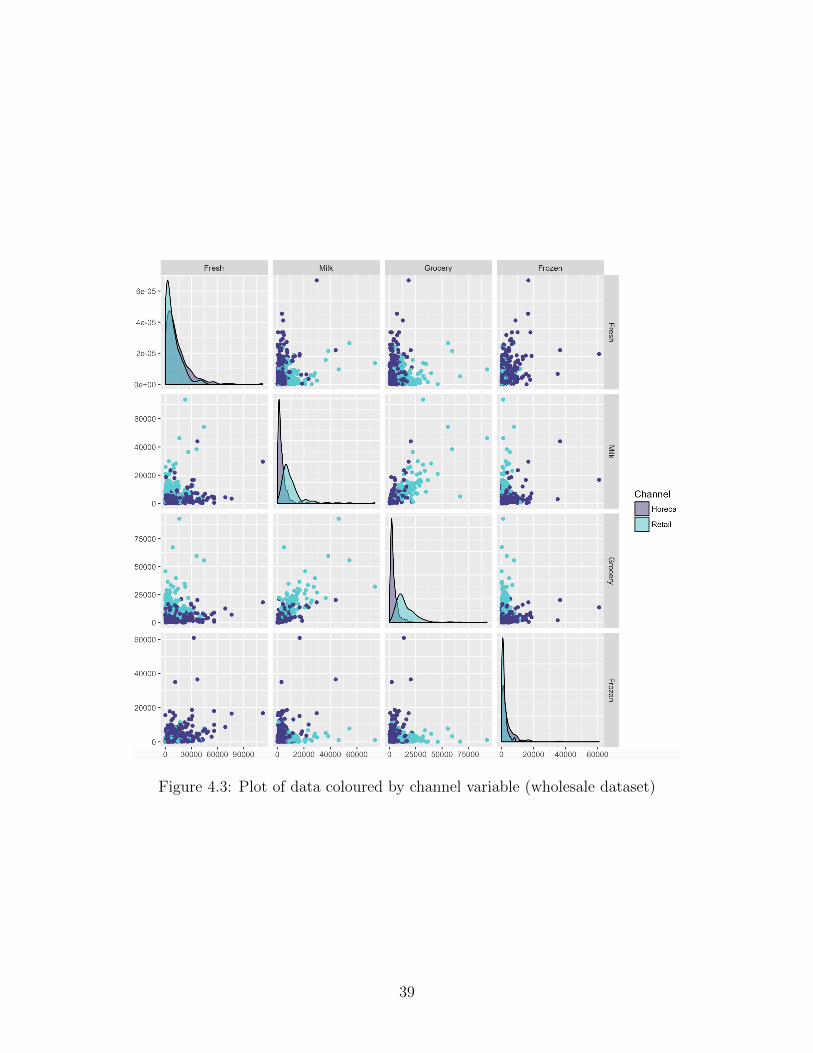

If we assume that the channel variable represents the true clustering of the data, the misclas-

sification rate when comparing the clustering of K = 2 components obtained by the GCD

to the channel variable is 24.773%.

37

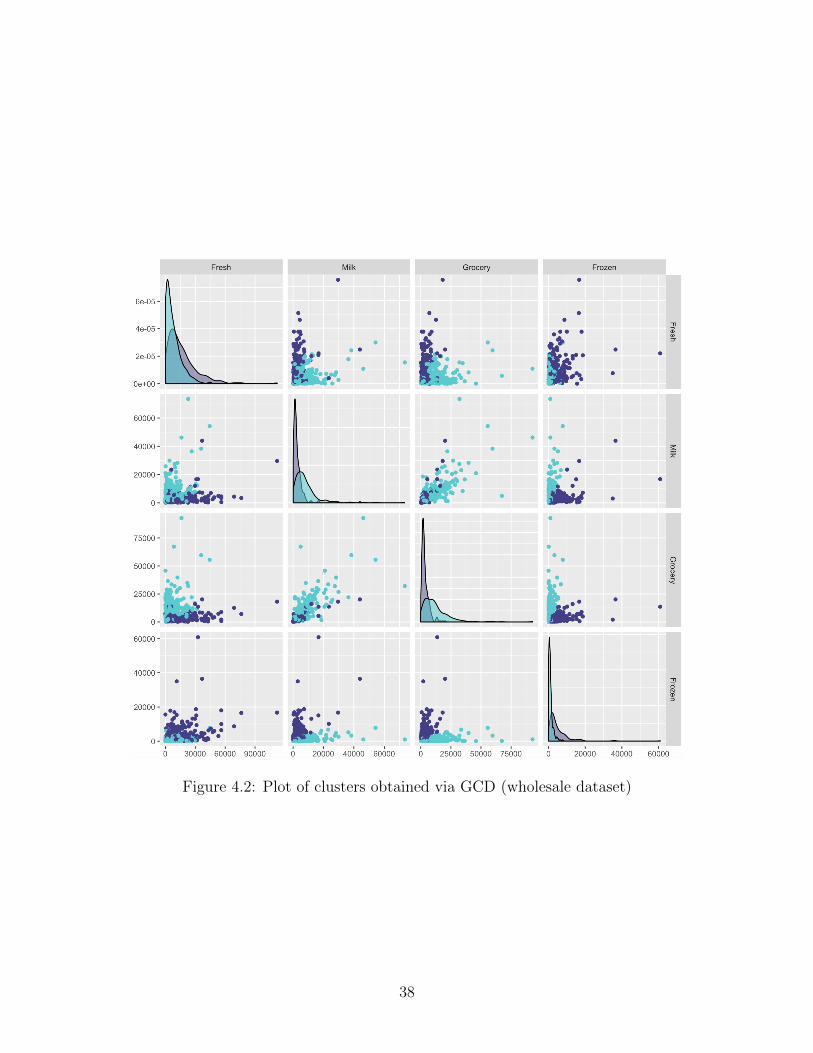

Figure 4.2: Plot of clusters obtained via GCD (wholesale dataset)

38

Figure 4.3: Plot of data coloured by channel variable (wholesale dataset)

39

4.3 Discussion

The GCD selects K = 2 as the optimal number of clusters, which agrees with the fact that

there are two types of customer channels. Comparing the clusters obtained via the GCD

with the grouping from the channel variable, the GCD performs well in identifying the group

structure of the data with a relatively low misclassification rate considering the latency of

the clusters.

Furthermore, when assuming componentwise conditional independence between the vari-

ables, the GCD selects K = 4 components as the optimal number of clusters, which do

not have a straightforward explanation in the context of this data. This demonstrates the

potential issues that may arise when the dependence structure of the data is ignored.

40

Chapter 5

Conclusion

In this chapter, we summarize the thesis and provide a discussion of its results, as well as

consider possible related future work.

5.1 Summary

This thesis explores the use of a hybrid approach to cluster analysis of correlated non-

Gaussian continuous data via GCDs. GCDs provide us with a flexible way to model the

joint distribution of a variety of non-Gaussian continuous data, while not relying on the

assumption of conditional independence between variables.

We adopt a methodology that combines the approaches of IFM and the PX-EM algo-

rithm. The use of IFM enables us to maximize marginal parameter estimates separately,

while still maximizing the correlation between normal scores jointly (Joe and Xu, 1996).

This increases the computational efficiency of the algorithm and still allows us to account

for the relationship between variables. Having a constrained parameter space poses addi-

tional challenges for parameter estimation, but adopting the PX-EM algorithm allows us to

overcome these convergence issues, while preserving the desirable properties of the ordinary

EM algorithm (Liu et al., 1998).

Simulations were performed to evaluate the performance of GCDs in clustering disparate

41

continuous data. From these simulations, we can see that, overall, the GCD performs well

in identifying components and obtaining parameter estimates. Furthermore, these simula-

tions highlight the potential issues that may arise when assuming conditional independence

between variables. When closed-form expressions for MLEs of marginal parameters are not

available, the use of the multiroot function may decrease the computational efficiency of

the algorithm. Also, this function is dependent on initial values, and poor selection of these

initial values may lead to slower convergence rates or even non-convergence. As expected,

when component latency is increased, the GCD does not perform as well. Ultimately, GCDs

appear to be a useful tool in the cluster analysis of non-Gaussian continuous data.

To demonstrate the potential applications of our methodology, we apply the GCD to a

dataset on the client’s of a wholesale distributor. The GCD identifies K = 2 clusters from

the data that could correspond to the customer channel variable. Comparing the clustering

we obtain to the grouping from the channel variable, the GCD does well in identifying the

underlying structure of the data. Moreover, when assuming conditional independence, the

GCD selects K = 4 clusters, which does not have an obvious interpretation for this dataset.

5.2 Future work

A natural extension of this work would be to consider the case of mixed data; that is, data

comprised of both continuous and discrete variables. Extending our methodology to the

mixed data setting could be useful in a variety of statistical settings. See Jiryaie et al.

(2016) for a comprehensive review of GCDs for mixed data.

One could also consider the use of a different copula with which to join together the

margins. For example, one could adopt a class of t copulas. As noted by Demarta and McNeil

(2007), a t copula may be able to capture more heterogeneity and extreme observations in

the data. There are a variety of copulas one could select, depending on the nature of the

data and how one wishes to model the dependence between variables.

42

Bibliography

Abreu, N. (2011). Analise do perfil do cliente Recheio e desenvolvimento de um sistema

promocional. Mestrado em Marketing, ISCTE-IUL, Lisbon.

Andrews, J. L. and McNicholas, P. D. (2012). Model-based clustering, classification, and dis-

criminant analysis via mixtures of multivariate t-distributions. Statistics and Computing,

22(5):1021–1029.

Cardoso, M. (2013). Wholesale customers data set. http://archive.ics.uci.edu/ml/

datasets/Wholesale+customers#.

Chang, F., Qiu, W., Carey, V., Zamar, R., Lazarus, R., and Wang, X. (2016). Package

‘clues’. https://cran.r-project.org/web/packages/clues/clues.pdf.

Dawid, A. (1979). Conditional independence in statistical theory. Journal of the Royal

Statistical Society. Series B (Methodological), 41(1):1–31.

Demarta, S. and McNeil, A. (2007). The t copula and related copulas. International Statis-

tical Review, 73(1):111–129.

Dempster, A., Laird, N., and Rubin, D. (1977). Maximum likelihood from incomplete data

via the EM algorithm. Journal of the Royal Statistical Society. Series B (Methodological),

39(1):1–38.

Desgraupes, B. (2017). Clustering indices. University Paris Ouest, Lab Modal’X.

43

Everitt, B., Landau, S., Leese, M., and Stahl, D. (2011). Cluster Analysis. Wiley, 5th ed.

Franczak, B. (2014). Mixtures of shifted asymmetric Laplace distributions. Doctoral Thesis,

University of Guelph.

Jiryaie, F., Withanage, N., Wu, B., and de Leon, A. (2016). Gaussian copula distributions

for mixed data, with application in discrimination. Journal of Statistical Computation and

Simulation, 86(9):1643–1659.

Joe, H. and Xu, J. (1996). The estimation method of inference functions for margins for

multivariate models. UBC Faculty Research and Publications.

Kosmidis, I. and Karlis, D. (2016). Model-based clustering using copulas with applications.

Statistics and Computing, 26(5):1079–1099.

Liu, C., Rubin, D., and Wu, Y. (1998). Parameter expansion to accelerate EM: the PX-EM

algorithm. Biometrika, 85(4):755–770.

McLachlan, G. and Krishnan, T. (2008). The EM Algorithm and Extensions. Wiley, 2nd ed.

McNicholas, P. (2016). Model-based clustering. Journal of Classification, 33(3):331–373.

Nelsen, R. (2006). An Introduction to Copulas. Springer.

Ren, M. (2016). Likelihood analysis of Gaussian copula distributions for mixed data via a

parameter-expanded Monte Carlo EM (PX-MCEM) algorithm. Master’s Thesis, Univer-

sity of Calgary.

Ruan, J. (2015). Cluster analysis of gene expression profiles via flexible count models for

RNA-seq data. Master’s Thesis, University of Calgary.

Saunders, J. (1980). Cluster analysis for market segmentation. European Journal of Mar-

keting, 14(7):422–435.

44

Schwarz, G. (1978). Estimating the dimension of a model. The Annals of Statistics, 6(2):461–

464.

Soetaert, K. (2015). Package ‘rootSolve’. https://cran.r-project.org/web/packages/

rootSolve/vignettes/rootSolve.pdf.

Wu, B. (2013). Contributions to copula modeling of mixed discrete-continuous outcomes.

Doctoral Thesis, University of Calgary.

Xu, H. and Craig, B. (2010). Likelihood analysis of multivariate probit models using a

parameter expanded MCEM algorithm. Technometrics, 52(3):340–348.

45