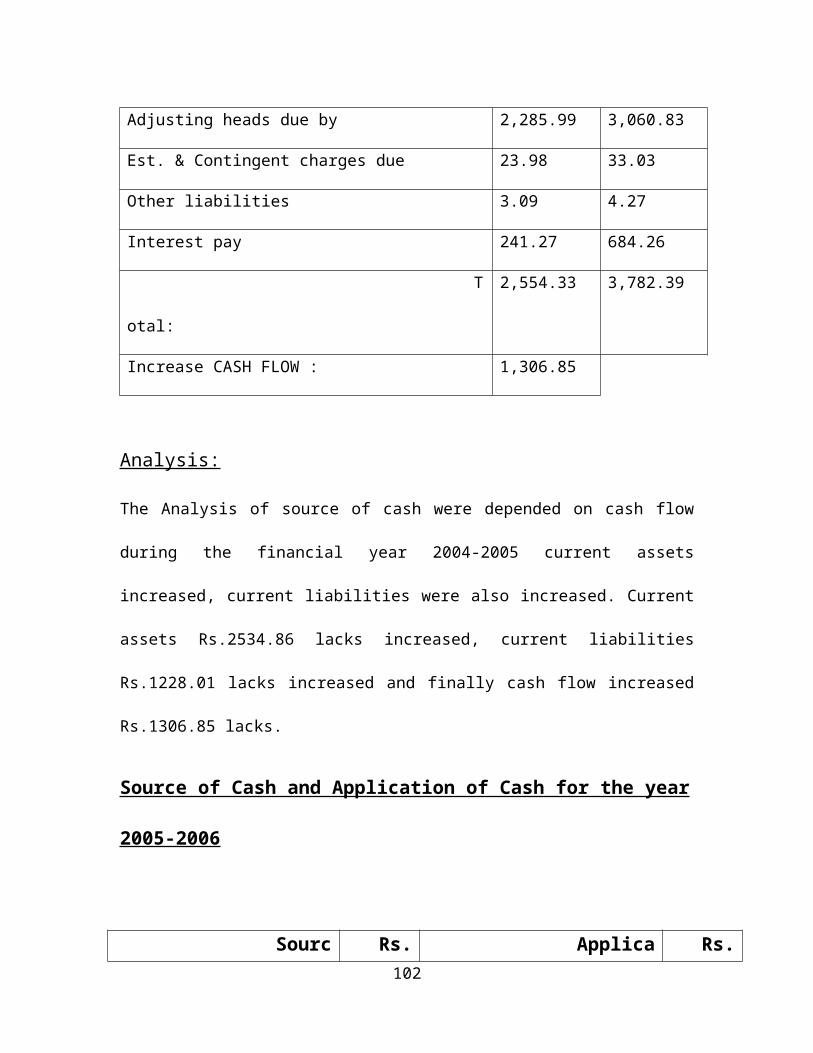

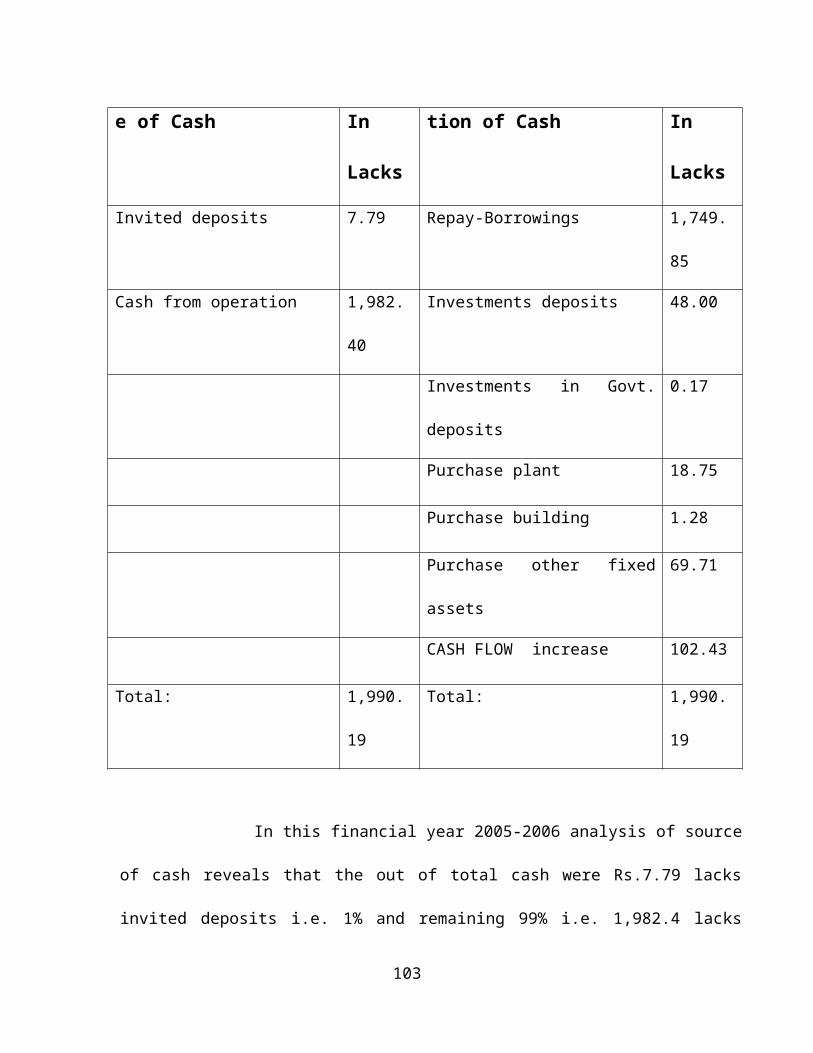

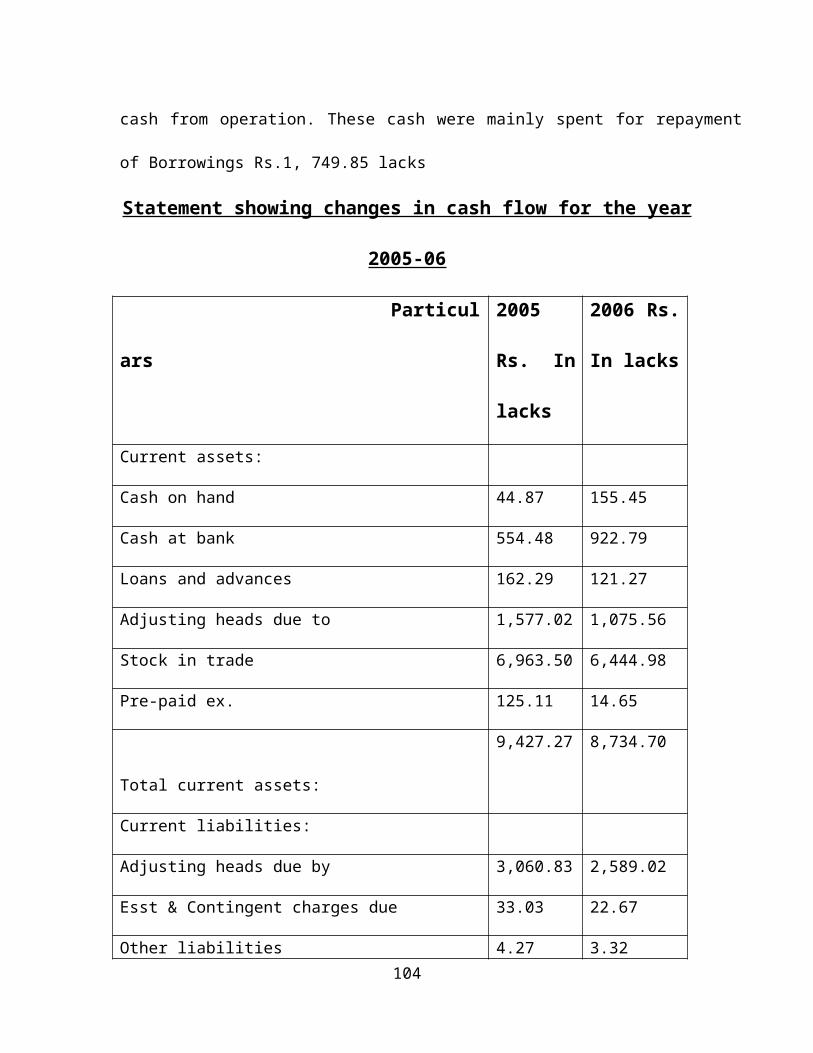

Embed Size (px)

Citation preview

CHAPTER-I

INTRODUCTION

1

INTRODUCTION TO FINANCIAL

MANAGEMENT INTRODUCTION:

Financial Management in the small firm is

characterized, in many different cases, by the need to

confront a somewhat different set of problems and

opportunities than those confronted by a large

corporation. One immediate and obvious difference is

that a majority of smaller firms do not normally have

the opportunity to publicly sell issues of stocks or

bonds in order to raise funds. The owner-manager of a

smaller firm must rely primarily on trade credit, bank

financing, lease financing, and personal equity to

finance the business. One therefore faces a much more

severely restricted set of financing alternatives than

2

those faced by the financial vice president or treasurer

of a large corporation

The business manager must continually be alert to

changes in working capital accounts, the cause of these

changes and the implications of these changes for the

financial health of the company.

MEANING OF FINANCIAL MANAGEMENT

Financial management is the most specialized branch of

the general management, which is related to the

procurement of finance and its efficient utilization for

the achievement of a common goal., for example the

analysis required for a long-term investment decision

such as the purchase of heavy machinery or the

evaluation of lease-buy alternatives, is essentially the

same regardless of the size of the firm.

DEFINITIONS

3

Financial management is an area of financial

decision making, harmonizing individual motives and

enterprise goals.

--- Weston and Birg.

Finance management is the application of the planning

and control function to the finance functions.

--- Howard and Upon.

Financial management is the operational activity of a

business that is responsible for obtaining and

effectively utilizing the funds necessary for efficient

operations.

--- Joseph and Massie.

NATURE OF FINANCIAL MANAGEMENT

The finance functions are acquisitions of funds and

efficient use of available resources. The managerial

4

activity of the financial management is concerned with

the planning and controlling of the firm’s financial

resources. Finance in the modern business world is

lifeblood of the business economy. Every business

transaction is directly of indirectly connected with the

finance. The financial management is concentrated on

three major aspects,

FINANCIAL MANAGEMENT

1.Investment Decision

2.Financing Decision

3.Dividend Decision

INVESTMENT DECISION

It relates to the allocation of capital

are involve to decision to commit funds to long-term

assets which would yield benefits in future. It is one

very significant aspect is the task of measuring the

5

prospective profitability of new investments future

benefits are difficult to measure and cannot be

predicted with continuity because of the uncertain

future capital budgeting involves risk

FINANCING DECISION

Broadly a finance manager must declare when, where

and how to acquire funds to meet the firms investments

needs. The finance manager must strive to obtain the

best financing mix or optimum capital structure of this

firm. The use of debt affects the return and rise of

shareholders. It may increase the return of the equity

funds. A proper balance will have to be struck between

rises and retain.

DIVIDEND DECISION

The finance manager must decide whether the firm

should distribute all profits or certain term or

distribute a portion and retain the balance. The

dividend policy should be determined in terms of its

impact on the market value of the firms share.

6

SCOPE OF FINANCIAL MANAGEMENT

Finance plays an important role in the progress of the

business in keeps the enterprise dynamic.

1. Successful promotion depends upon Financial

Administration,

2. Smooth running of an Enterprise,

3. Determinant of business success,

4. Measure of performance,

5. Focal point of decision making.

FUNCTIONS OF FINANCIAL MANAGEMENT

EXECUTIVE FINANCE FUNCTIONS:

Financial Forecasting

Establishing asset management policies

Allocation of net profit

Cash flow and requirements

Dividing upon borrowing policy

Negotiations for new outside financing

Checking upon financial performance

7

Profit maximization

Wealth maximization

RESPONSIBILTIES OF FINANCIAL MANAGEMENT

Financial planning

Rising of necessary funds

Controlling the use of funds

Other Responsibilities

FIELD OF STUDY

Cash flow Management & Analysis in SVG

COOPERATIVE SUGARS LTD

Due to Globalization of the Industries, the need

for establishing the Industries have grown consequently.

In general the Individual how much wealthy he might be,

cannot fund the entire project cost and he have to

necessarily look for outside financial resources for the

project. In addition to the project cost, funds have to

8

be arranged to meet the cash flow requirements for the

project. Cash flow is the capital required for day-to-

day management of the business and in accounting terms

it represents excess of current assets over the current

liabilities. In other words we can say that is the cash

required to run the daily activities. However, in day-

to-day operations, the factors of uncertainty and risk

play a great role and accordingly the entrepreneur will

have to depend on different sources of finance.

The basic financial statements, i.e., the balance sheet

and profit and loss account or income statement of

business, reveal the net effect of the various

transactions on the operational and financial position

of the company. The balance sheet gives a summary of the

assets and liabilities of an undertaking at a particular

point of time. It reveals the financial status of the

company. The assets side of a balance sheet shows the

deployment of resources of an undertaking while the

liabilities side indicates its obligations, i.e., the

manner in which these resources were obtained. The

9

profit and loss account reflects the results of the

business operations for a period of time. It contains a

summary of expenses incurred and the revenue realized in

an accounting period. Both of these statements provide

the essential basic information on the financial

activities of a business, but their usefulness is

limited for analysis and planning purposes. The balance

sheet gives a static view of the resources (liabilities)

of a business and the uses (assets) to which these

resources have been put at a certain point of time. It

does not disclose the causes for changes in the assets

and liabilities between two different points of time.

The profit and loss account, in a general way, indicates

the resources provided by operations. But there are many

transactions that take place in an undertaking and which

do not operate through profit and loss account.

Thus, another statement has to be

prepared to show the change in the assets and

liabilities from the end of one period of time to the

end of another period of time. The statement is called a

10

statement of changes in Financial Position or a Cash

flow Statement.

The Cash flow Statement is a statement,

which shows the movement of cash and is a report of

financial operations of the business undertaking. It

indicates various means by which cash were obtained

during a particular period and the ways in which these

cash were employed. In simple words, it is a statement

of sources and applications of cash

NEED FOR STUDY:

Financial statement analyses enable a firm to the

dimension into account. It facilities the management

to know where the firms financial position is

improving are determination on over the years.

Cash flow statements are a needful tool for the

management planning and forecasting and controlling.

Financial statement analysis indicates the overall

profitability of the firm. It ensures a fair return to

11

its owners and secures optimum utilization of the

firm’s assets.

It is also helpful in forewarning the corporate

sickness and helps the managements to take corrective

action.

There is a need to prepare analysis for estimating the

cash flow requirements of an organization.

OBJECTIVES OF THE STUDY:

To study the analysis of cash management in the

organization.

To study the safety level of cash in the

organization.

To analyze the sources and application

To suggest suitable measures for better

performance.

METHODOLOGY:

12

Data can be collected from two sources Primary and

secondary. Classified on the basis of purpose of

collection of sources.

Primary Data: Primary data are those collected

specially for the research situation at hand. It is the

firm harm information that researches get from various

sources like respondents, analogous and research

experiments. The primary data will be collected from

personal interview of employees in the organization.

Secondary Data: Secondary data are already published

data collected for some purpose from officials at a

given point to time. The secondary data will be

collected from annual reports, books, journals etc.

LIMITATIONS:

The study of availability of bank finance for the

working capital requirement is an ocean and fund of

experience of lifetime and hence it is in adequate

to cover the entire aspects of the study

13

I have limited the study to the facts obtaining in

the company where I am being employed. Working

Capital Management and dependency on banking

finance is one of the biggest problems faced by the

company

The problems faced by the company are similar to

that of other organizations. The company can

express its problems and request the banks to

provide for the finance enable them to meet its

financial requirements. It can only request the

banks but however it cannot compel the banks to

provide any financial assistance in the regular

course of business. This is a major limitation of

the study

In addition, I have also covered the

recommendations of the Tan don Committee Report as

well as Chore Committee Report released by the

Reserve Bank of India on the subject of Working

capital Management

14

A study is also made on the recommendations made by

Dehejia Committee on the subject

SIGNIFICANCE:

Today the term “Management of cash flow” has been

acquired greatest importance in the Indian scenario.

Either it may be manufacturing Industry or a service

Industry. In this connection, many of the organizations

fail due to poor maintenance of cash flow management.

Gross cash flow and net cash flow .Net cash flow refers

to the difference between current assets and current

liabilities

A positive net cash flow arises when current assets

exceed current liabilities. A negative cash flow occurs

when current liabilities are in excess of current

assets. The investment in current assets should be just

adequate not more not more not less to the needs of the

business firm. Excessive investment in current assets

should be avoided, because it impairs the firms

profitability as idle investment earns nothing, on the

15

other hand, inadequate amount of cash flow can threaten

the solvency of the firm, it is fails to meet its

current obligations. It should be realized that the cash

flow needs of the firm might be fluctuating with

changing business activity. The management should be too

prompt to initiate on action and correct the imbalances.

A negative cash flow and excessive liquidity are

also bad. It may be due to mismanagement of current

assets. Therefore prompt and timely action should be

taken by the management to improve and correct the

unbalance in the liquidity position of the firm. Every

firm should have minimum amount of net cash flow which

is permanent after liberalization role of the cash flow

is improved.

16

CHAPTER -II

INDUSTRY PROFILE

17

AN OVERVIEW OF INDIAN SUGAR INDUSTRY

India has been known as the original home of

sugarcane and sugar. Indians knew the art of making

sugar since the 4th century. However the advent of

modern sugar industry in India dates back to mid

1930’s when a few vacuum pan units were established in

the sub-tropical belts of Uttar Pradesh and Bihar.

Until the mid 50’s the sugar industry was almost

wholly confined to the states of Uttar Pradesh and

Bihar. After late fifties or early sixties the industry

dispersed into Southern India, Western India and other

parts of Northern India.

India is the largest consumer and second largest

producer of sugar in the world. The sufficient and

well distributed monsoon rains, rapid population

growth and substantial increases in sugar production

capacity have combined to make India the largest

consumer and second largest producer of sugar in the

world.

18

The Indian sugar industry has not only achieved

the singular distinction of being one of the largest

producer of white plantation crystal sugar in the world

but has also turned out to be a massive enterprise of

gigantic dimensions. With over 450 sugar factories

located throughout the country, the sugar industry is

amongst the largest agro processing industries, with

an annual turnover of Rs 150 billions. It plays a

major role in rural development and its importance for

India stretches far beyond the role of a sweetener

supplier.

The sugar factories located in various parts of

the country work for development of rural areas by

mobilizing rural resources and generating employment,

transport and communication facilities. Over 45

farmers, their dependants and a large mass of

agricultural labor are involved in sugarcane

cultivation, harvesting and ancillary activities

constituting 7.5% of the rural population. The sugar

19

industry employs over 0.5 million skilled and

unskilled workmen, mostly from the rural areas.

Since the beginning of planning , sugar industry

operated under a policy of partial control in 1950-

51 and 1951-52 , followed by a continuous period of

six years of decontrol between 1952-53 to 1957-58.

This policy was followed under the pragmatic leadership

of the Minister of Food, Shri. Rafi Ahmed Kidwai.

However, with his departure, the perception of decontrol

was lost.

After alternating between control and

decontrol , the government adopted the policy of

partial decontrol in 1967-68, which has since been

the ministry of government policy except for two

short periods of decontrol in the 1970’s .Under the

policy, the government procures 40% of production

at controlled prices based on the Statutory Minimum

Price for sugarcane, for supply through the Public

Distribution System and the balance 60% is

allowed to be sold by the mills in free market

20

subject the monthly release mechanism. The details

of past government policies for sugar industry are

provided in annexure1.

The levy quota for sugar mills has been brought

down from the peak levels of 70% in 1968-69 to the

present levels of40% as a gradual process of

deregulation of sugar industry.

The number of operating sugar mills in the

country has increased from 29 in sugar year (sy)

1930-31 to 412 by SY 1996-97 ( sugar year= October

1st t o September 30th ). The addition in number of

mills was added between 1970 and 1980 to increase

the number of operating units to 300. The development

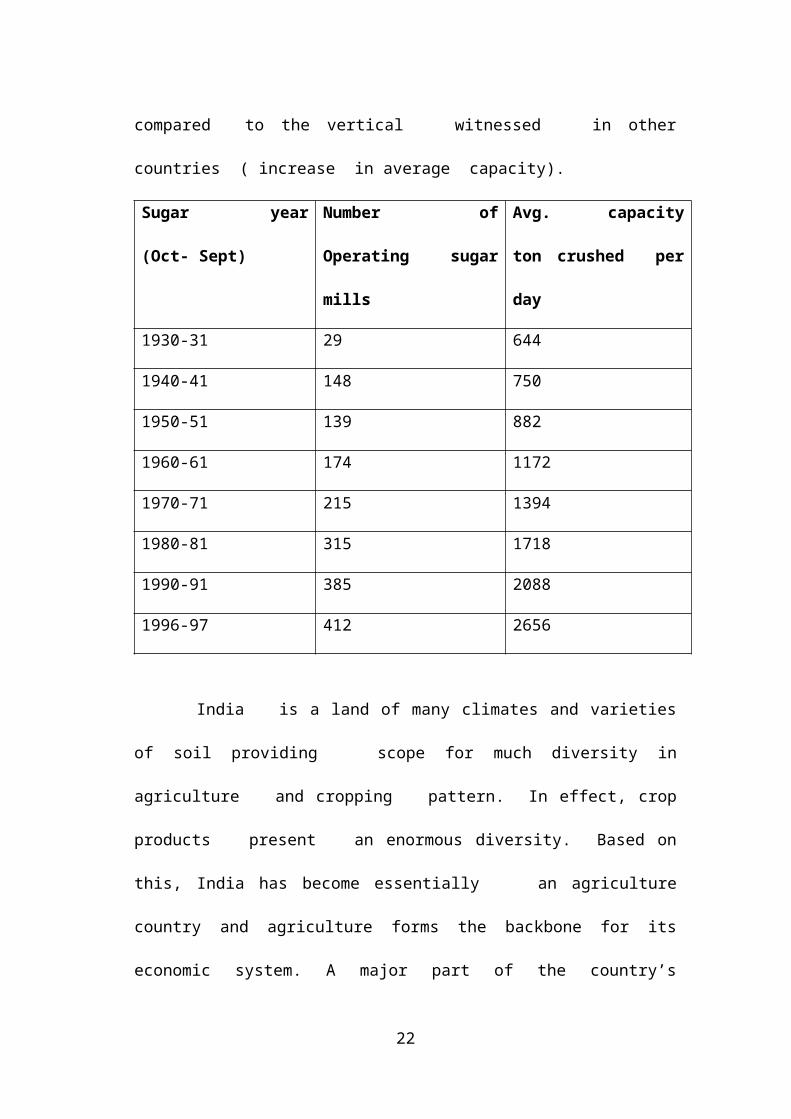

of industry in the past is as given in table below.

The average capacity of the sugar mills in the

industry has considerably moved up from just 644 ton per

day in SY 1930-31 to 2656 ton per day. But still the

growth in the Indian sugar industry was driven by

horizontal growth ( increase in number of units)

21

compared to the vertical witnessed in other

countries ( increase in average capacity).

Sugar year

(Oct- Sept)

Number of

Operating sugar

mills

Avg. capacity

ton crushed per

day

1930-31 29 644

1940-41 148 750

1950-51 139 882

1960-61 174 1172

1970-71 215 1394

1980-81 315 1718

1990-91 385 2088

1996-97 412 2656

India is a land of many climates and varieties

of soil providing scope for much diversity in

agriculture and cropping pattern. In effect, crop

products present an enormous diversity. Based on

this, India has become essentially an agriculture

country and agriculture forms the backbone for its

economic system. A major part of the country’s

22

populations depends directly or indirectly for

sustenance on agriculture. Agricultural sector has

been given top priority in order to feed it’s ever -

growing population. This sector also provides

necessary raw material for the principal food

manufacturing industries. Further, this sector

provides a substantial portion of country’s exports

and hence this sector has become an important foreign

exchange earner. Agriculture is the main occupation for

a major part of population until a few years ago. In

recent years, there has been a tremendous progress

in the field of industrial establishments and soon

this sector has become the backbone for the present

day economic development of the country.

Currently, India is self- sufficient in a large

number of consumer goods and has reached to a

stage that it is able to export a variety of

manufactured or processed goods to different

countries in Asia , Africa, and Europe.

23

India is in outstanding position in the

world with regard to many agricultural products such

as tea, sugar cane , millets, rice , jute , etc. Of

these, sugar cane is important as a non- food grain

crop. It is an industrial crop, because it is used as

a non-food grain crop. It is an industrial crop, because

it is used as raw material in sugar industry. India is

producing more than 2900 lakhs tones of sugar cane. The

principal sugar cane producing states are Uttar

Pradesh , Madhya Pradesh, Maharastra , Tamil Nadu ,

Andhra Pradesh , Bihar, Haryana and Punjab. Sugar is

also grown in other states such as Orissa, Assam,

Gujarat, West Bengal etc. Uttar Pradesh alone produce

37% of total sugar cane produced in the country

every year .In Andhra Pradesh , sugar can is

cultivated in the districts of Srikakulam,

Vizianagaram, Vizag , East Godavari, West Godavari,

Kurnool, Anantapur, Nizamabad, Chitoor, Cuddapah,

Guntur, and Adilabad. Altogether 2 lakh hectors of

land is under sugarcane cultivation in the entire

24

State of Andhra Pradesh. The total annual production

touches 140 lakh tons in Andhra Pradesh alone.

Sugarcane is a tropical plant (Saccharin

officinarum) that is able to grow over a prolonged

season. It thrives well under the temperature ranging

from 25-30 C and under the rainfall ranging from

100-500cm. Under warm humid conditions it can

continue its growth unless terminated by flowering.

However, its height is strongly influenced by the

age of the crop and season. Temperatures above 50

C arrest its growth, those below 20 C slow it down

markedly and severe frost proves fatal. Sugarcane

is a Kharif crop planted between December and

February period. About 10-12 month gestation

period is required for the harvest of sugarcane

crop. Different varieties have been developed over

a period of time and they are being classified into

early varieties, mid varieties and late varieties.

The early varieties reach maturity at the age of 10th

month, mid variety at 11th month and late variety

25

at the 12th or 13th month. Earlier planting of sugarcane

in the season gives higher yields and better

quality cane, the late plantings apart from

giving lower yields are usually badly attacked

by the shoot borer which caused gaps in the

stand of sugarcane and setback to the plant growth.

Since crops planted in different months ripen in

succession, by a suitable adjustments of planning,

the necessary areas in different seasons, and a

planned supply of cane to the factory, a

satisfactory recovery of sugar in factories can be

ensured over a reasonably long crushing season.

It is important note that the harvested sugarcane

should be crushed within 24 hours for getting

good quality sugar. Sugarcane is a heavy feeder. A70 -

ton crop removes from the soil 85-110 kgs of

nitrogen.180-330 kgs of phosphoric acid, 60-90 kgs

of potash and 70-80 kgs of calcium. Adequate manuring

therefore is essential for sustaining high yields. At

26

present, only 10% of sugarcane crop is manured and in

most cases inadequately.

Sugar factories in India are classified based

on their cane crushing capacity per day.

Small Up to 1500 tones

Medium 1501to 3000tones

Large 3001 to above tones

Today the sugar industry is the third largest

industry in the country and ranks next to the

iron steel, and cotton industries. The area

under sugar cultivation in India is larger

than in any other country in the world, but the

average yield per acre is low. Until recently

India depended on imports of cheap foreign sugar,

but with the increase of domestic production, India

could not only achieve self – sufficiency in sugar but

also has surplus for export.

India has a record production of 8.4 million tones in

1981-82 and record earning of Rs. 800 Crores in 1975-

76 by exporting. Sugar industry in India is playing an

27

important role in the economic development of the

country. The by-products find value as raw material

in other industries such as distilleries.

History:

The discovery of sugarcane, from which sugar as it

is known today, is derived dates back unknown thousands

of years. It is thought to have originated in New

Guinea, and was spread along routes to Southeast Asia

and India. The process known for creating sugar, by

pressing out the juice and then boiling in into

crystals, was developed in India around 5000 BC. Its

cultivation was not introduced into Europe until the

middle-ages, when it was brought to Spain by Arabs.

Columbus took the plant, dearly held, to the West

28

Indies, where it began to thrive in a most favorable

climate.

It was not until the eighteenth century that

sugarcane cultivation was began in the United States,

where it was planted in the southern climate of New

Orleans. The very first refinery was built in New York

City 1690; the industry was established by the 1830s.

Earlier attempts to create a successful industry in the

U.S. did not fare well; from the late 1830s, when the

first factory was built. Until 1872, sugar factories

closed down almost as quickly as they had opened. It was

1872 before a factory, built in California, was finally

able to successfully produce sugar in a profitable

manner. At the end of that century, more than thirty

factories were in operation in the D.S.Sugar (sucrose)

is a carbohydrate that occurs naturally in every fruit

and vegetables. It is a major product of photosynthesis,

the process by which plants transform the sun’s energy

into food. Sugar occurs in greatest quantities in

sugarcane and sugar beets from which it is separated for

29

commercial use. The natural sugar stored in the cane

stalk or beet root is separated from rest of the plant

material through a process known as refining Beet sugar

processing is similar, but it is done in one continuous

process without the raw sugar stage. The sugar beets are

washed, sliced and soaked in hot water to separate the

sugar -contain juice from the beet fiber. The sugar-

laden juice is then purified, filtered, concentrated and

dried in a series of steps similar to cane sugar

processing.

For the sugar industry, capacity utilization is

conceptually different from that applicable to

industries in general. It depends on three crucial

factors the actual number of ton of sugarcane crushed in

a day, the recovery rate which generally depends on the

quality of the cane and actual length of the crushing

season.

Since cane is not transported to any great extent,

the quality of the cane that a factory receives depends

on its location and is outside its control. The length

30

of the crushing season also depends upon location with

the maximum sugarcane in India is used to make sugar,

khandsari or Gur.

However, sugar products produced worldwide are

divided into four basic categories: granulated, brown,

liquid sugar and invert sugar. Granulated: granulated

sugar is the pure crystalline sucrose. It can be

classified into seven types of sugar based on the

crystal size. Most of these are used only by food

processors and professional bakers. Each crystal size

provides unique functional characteristics that make the

sugar appropriate for the food processor’s special need.

Mission & Values:

Mission

31

To build entrepreneurial organizations that makes a

difference to society through creation of value.

Values

Humility

We value intellectual modesty and dislike false

pride and arrogance

Entrepreneurship

We seek opportunities – they are everywhere

Teamwork and Relationships

Going beyond the individual – encouraging boundary

less behavior

Deliver the promise, we value a deep sense of

responsibility and self discipline, to meet and

surpass on commitments made.

Learning

Nurturing active curiosity – to question, share,

and improve

32

Social responsibility

Anticipating and meeting relevant and emerging

needs of society and,

DEVELOPMENT – AGRICULTURE:

Just after India attained freedom, 50yeears ago,

Indian governments’ first and immediate concern was food

production. In the words of the first Prime Minister of

India – “Everything can wait, agriculture can not”. The

words expressed common concern as population was growing

at a much faster rate than food production.

That the country became self sufficient in food

grains was a demonstration of unprecedented

collaboration between policy makers, administration,

scientist and response of farmers. To give further

boost Farmer was provided incentive by way of an

attractive support price and disposal mechanism by way

of procurement of the food grains by the Government

Agencies.The agricultural thrust continued in other

agriculture commercial crops as we like oil seeds, sugar

33

cane where Government. appointed technology missions and

where India became self sufficient from a net importer.

In sugar, it became an exporter, exporting as much as

1Million Tones in 1995-96. Today India has made a place

for itself in the world agricultural map where it enjoys

a prominent position with rest of the world.

ISSUES RELATING TO SUGAR INDUSTRY

Central government measure Licensing:

Sugar Industry is a schedule industry under

Industrial Development regulation Act requiring

License to manufacturer.

o Gestation period has been reduced from 3 years

to 1 year.

Minimum capacity of a new sugar mill is 2500 TCD

and expandable up to 5000TCD.

34

Minimum distance between 2 sugar mills is now 15

kms- which used to be 40 km.

Cane availability is now not so critical

requirement.

Government gives incentives where in new mills can

sell up to 100% of the sugar in free market against

60% of existing mills – Government has also

announced such incentive for expansion up to 5000

TCD.

The impact has been horizontal growth – causing

cane shortage – higher per unit processing cost

etc.,

PRODUCTION MONITORING:

The sugar (control) Order 1966- regulates the

production- sale of sugar- stock limit. It also

prescribed standard of quality – to which sugar must

conform at the time of delivery.

SUGAR CANE PRICING:

Sugar cane (control) Order 1966- was issued to

promote sugar industry and to ensure fair deal to cane

35

growers by fixings minimum price payable by sugar mills

Act provided cane price fixation basis 50%profit

sharing. Not enforced in some states where such state

fix its own price.

SUGAR SUPPLIES FOR PUBLIC DISTRIBUTION:

The Levy Sugar Supply (control) Order 1979 was

issued empowering the Government. To direct sugar mills

to supply levy sugar to authorized persons /

organization etc., at a price fixed for the season.

DUAL SUGAR PRICING POLICY:

Under the provision of the Sugar Control Order,

Govt has been regulating the sugar supplies for

distribution under PDS and free market. Several times in

the past, industry has gone through complete control or

partial control to complete decontrol and back to

partial control.

Under the current policy 10% of the sugar

produced is to be delivered by mills, for public

distribution, at a price fixed from season to season.

Balance 90% can be sold in the free market as per

36

quantity decided by government. on month-to-month basis

for each mill. Also mill has to sell minimum 47.5% in

the first fortnight and 52.5 in second.

QUALITY / PACKAGING:

Governed by Indian Standards. Grade 31, 30, 29, and

packaging only in 100 kgs jute bags. Consumer packs

allowed in 1, 2, 5 kg in any packaging. Exports packing

can be in 50 Kg and in any packaging material and so

also imports.

STATE GOVERNMENT REGULATIONS:

Over and above the central government control,

each state government enforces it sown regulatory

measures to protect the state / farmers. Following are

some typical controls in the state of Uttar Pradesh,

which are there in other states in some form or other.

RESTRICTION ON SUGAR CANE PURCHASE ORDER, 1966

This order provides for restriction on purchase of

sugarcane by producers. It also provides for permits for

purchase of sugarcane by a khandsari manufacturer

holding a license.

37

SUGAR CANE CESS ACT, 1956

This Act has been promulgated for imposition of

cess on cane sold to a sugar factory. At present the

rate of cess is Rs. 140 PMT on sugar, which is collected

at the time of delivery of sugar.

SUGAR CANE (PURCHASE TAX) ACT, 1961:

This Act proposes to impose a tax on the purchase of

sugarcane by the owner of a sugar factory. A sugar

factory is not allowed to remove any sugar until

Purchase tax has been paid thereupon. At present the

rate of Purchase Tax is Rs. 220 MT on sugar.

SUGAR CANE (REGULATION OF SUPPLY & PURCHASE)

ACT, 1953

This Act regulated the supply and purchase of sugarcane

required for use in a sugar factory, khandsari unit and

for manufacture of gur, it provides for:

Declaration of reserved area / assigned area for

the purpose of supply of cane to sugar factory.

38

Speedy payment of the price of cane (action for

delays)

Cane purchase by mill through cane grower’s Co-

operative Societies.

Payment of commission to cane grower’s Co-

operative societies.

Power to declare some cane unsuitable for sugar

mills.

SUGAR CANE (SUPPLY& PURCHASE) ORDER, 1954

It provides for rules and regulations governing

purchase of cane in a reserved area /assigned area

and purchase for cane at cane purchasing centers

within the reserved area of a sugar factory

MOLASSES CONTROL ORDER

39

While the central Government has decontrolled the

molasses, the State Governments, had imposed its

regulations like:

Ban on interstate movement

Restriction on end use i.e. Sale to a specific

consumer.

Ratio of control fixed rate and free market

rate.

Also specify consumers who will get a control

price.

SUGAR- DISTRIBUTION AND TRADING PRACTICES

Under the dual pricing policy government

announces from time to time portion of the sugar that

can be sold in the free market and what is to be

supplied at the fixed price under the public

distribution system called levy sugar.

LEVY SUGAR SALES/ DISTRIBUTION SYSTEM

Currently, 40% of production (effectively due to

non- levy unit 33%). Quantity for distribution per month

40

fixed unit per kg/ family etc. Varies basis additional

requirement arising due to important festivals.

Food Ministry issues allocation of various food

departments/ corporations. Such departments approach

individual mills to lift the sugar and for onwards

supply to various public distribution system (ration

shops) appointed by the State Government.

MARKET MAKING

The Indian sugar industry is worth 25000 crore and

lies only with Brazil for the position of the world’s

leading sugar producer. Currently, about 4 million

hectares of land in India is under sugarcane cultivation

with an average yield of 70 tones per hectare. The

cumulative production during October 2002 – May 2003

stood at 19.65 million tones -- 8.6% higher than the

output during the corresponding sugar production is

likely to continue at these high levels into next

year, given that the returns to farmers are higher in

sugarcane than in other crops, in spite of the delay in

payments for cane arrears.

41

SUGAR PRICES

The Indian sugar industry operates under a dual

pricing system for its sugar output. These are levy

prices and free market prices.

Levy prices- the government procures 10% of the

sugar for the public distribution system (PDS) at a

subsidized price called the “levy price”, which varies

from region to region. The government announces PDS

sugar prices based on levy sugar prices fixed by it and

the subsidy is provided through budgetary system.

FREE MARKET PRICES

The remaining 90% of the production by sugar

mills can be sold in the open market, but only up to

a fixed quantity as decided by the government for

each factory each month(monthly release quotas),

based on the demand – supply situation in the

country.

During October 2002 to June 2003, the average price

of free Market sugar was Rs. 12050 per tons as

compared to Rs. 14130 per tons during the corresponding

42

period of 2001-02. This implies a steep 14.7% falls as

against a nominal 2.2% decline recorded in the

corresponding period of 2001-02. The March, April

and May 2003 prices witnessed a year – on- year fall

of 18% , 16% and 16% respectively. May 2003 was

the fifteenth consecutive month that registered a

price fall. Sugar prices dropped to these low levels due

to the dumping of sugar in the open market by the mills.

SUGARCANE PRICES

Each Year, The Government of India declares a

Statutory Minimum Price (SMP) for cane. In some states,

such as Punjab, Haryana, and Uttar Pradesh the sugar

mills have to pay the effective State Advised Price

(SAP) for the sugarcane, which is 20-25% above the

minimum support price (MSP.). The successive increase

in cane prices in the past years has translated into

an abnormally high cost for the production of sugar,

now estimated at $ 270- 280 per tone, in addition to

causing the current supply glut in sugarcane and

sugar.

43

SUGAR EXPORTS

The huge amount of standing sugar stocks has

forced the Indian Government to encourage exports by

offering a reimbursement of the cost of surface

transport of exportable sugar from factories to ports.

(As agreed in July 2002) and an ocean freight subsidy of

Rs. 350 per tones. The benefits also include a state

subsidy on exports and an exemption from levy

obligations on the quantity of sugar exported.

The exports in2001-02 were 1.06 million tones,

while in 2002-03 (October –May) the figures have so

far reached 1.43 million tones. The export for 2002-03,

total, is estimated at 2 million tones. The prices

received by exporters for world market sales are

unlikely to improve in the near future. The world sugar

output in 2002-03 is expected to be, at 143.1 million

tons ( September –August) from 138.2 million tons

last year, and the current structure of the world

white sugar futures suggested that prices will

44

continue to be under pressure for the coming

year.

IMPORTS

Sugar imports are negligible in India as there is a

high customs duty of 60% plus a countervailing duty of

RS. 850 per tons. In addition, the governments’ policy

is to subject imported sugar to a levy requirement and

market release quotas, while tightening the norms for

duty- free import against re- exports.

SUGAR PRODUCTION

sugar cane and sugar beet are the two main crops

that contribute approximately 56% and 44%

respectively of the total sugar production in the

world. Sugar cane is the main source of sugar

production in India and holds a prominent position as

a cash crop. Sugar cane is a crop of the tropics while

sugar beet is essentially a crop of temperature regions.

Sugar is pure sucrose in solid crystalline form. It is

an essential commodity and has innumerable uses. It is

45

the common sweetener. One cannot ignore the use of sugar

in the daily life as the day starts with coffee or tea.

Sugar is used in the preparation of many sweets, bakery,

confectioneries, soft drinks, chocolate industries, etc.

It means that it has wide importance domestically and

industrially. Sugar has highest place in the indigenous

market and also in the export sector. Sugar is being

exported to USA, Canada, UK, Malaysia, Sri Lanka, and

Middle East countries.

Sugar industry is one of the important industries

in India. Among the agro- based industries, textile

industry is the first and foremost important industry

and the second most important industry is the sugar

industry. India stands second in the production of

sugar in the world. India has more than 396 sugar

factories. Overall, the sugar industry provided

employment to 2.5lakh people, which include skilled and

unskilled workers. Further, it sustains over 2.5 crore

agriculturists and their families. The sugar industry is

largely confined to the northern part of the country,

46

especially in Uttar Pradesh and Bihar, this parties

regarded as sugar, belt. In recent years, sugar

industries have come up in the states of

Maharashtra, Andhra Pradesh, West Bengal , tamilnadu ,

Punjab , etc. sugar industries are developed as co-

operative sector industries.

With sugar cane crushing in sugar factories,

the main product obtained is crystal sugar. Along with

it, the by- products, namely, bagasse, molasses, and

filter cake are also obtained. The by – products find

value as raw material in other industries. The biogas is

used as fuel to heat boilers for power production. The

molasses are widely used in distillery industries.

Like any other manufacturing industry, sugar

industry is also responsible for the release of

pollutants, which degrades the local a real environment.

Although no serious health hazards are associated with

pollutants from the sugar industry, over a period of

time, pollution may cause health problems to living

organisms including man. Apart from this, there are some

47

occupational health problems among sugar factory

workers, which will be detailed in the pages to follow

at the appropriate place. Nevertheless the pollution

problems associated with sugar production from sugar

cane is not that serious when compared to those

associated with other industries..

48

CHAPTER-III

COMPANY PROFILE

49

SRI VIJAYA RAMA GAJAPATHI CO- OPERATIVE

SUGAR LTD

This sugar factory is situated in

Bhimasinghi of vizianagaram district. It was

established in the year1960 and production began in

1976 it was established with a view encourage the

nearby sugar cane farmers for growing sugar cane in

their crop fields and also to better their economic

welfare. The factor has a jurisdiction of 601 villages

distributed in 20 mandals out of which only 9 mandals

supply sugar cane for the production of sugar by this

factory, sugarcane is cultivated in 9,908 hectors .The

total sugarcane production from this land amounts to

1, 90,000 metric tons per year .Out of this 25,000

metric tons of sugarcane are kept aside for raising

50

the new crop in the subsequent season and the

remaining 1, 65,000 tons of sugar cane are crushed to

produce sugar by the factory. The factory has an

installed capacity of 1,250 tons of sugar cane per

day. The factory operated from November /December to

may/June and produces 1, 70,250 quintals of sugar from

the total supply of sugar cane (1, 65,000 metric tons)

during this period.

Location:

The factory is situated in Jami mandal,

which is 11kms from vizianagaram. This factory is

provided with good transport facilities like road and

railway station. Korukonda is the nearest railway

station. This is just 4 kms from the plant. About

140days is the optimum crushing duration. Since the

wet weather up to November and sever drought and high

day temperatures in summer months of may restrict

economics of crushing. The cane crush is estimated

about 35,000 M.T per month. Main raw material used in

51

sugar cane only with in the capacity of the plant of

1250 m tones of cane per day.

Objectives of the organization:

The objects of the society shall

be to promote the economic interests on members by

encouraging proper development of agricultural

industries on co-operative lines and through co-

operative principles with a view to ensure to the

agriculturists ,with special attention to and

performance to small farmers as far as possible ,the

advantages of scientific.

Agricultural production and the benefits large

scale industries and for the said purpose it shall be

competent to the society.

To purchase from members or non-members sugarcane

and or other raw materials and also to undertake

cultivation of sugarcane.

To construct or take on rent go downs at the place

of manufacture as well as outside for storage and

sale of the products.

52

To do all other things incidental to or necessary

for the establishment and running of the factory.

To process and sell sugar and other by-products

produced.

To undertake measures for the development of

sugarcane including supply of seed , fertilizer

agricultural implements, irrigation facilities and

other production requirements including

agricultural credit and to provide technical advice

on improved cultivation methods .

To hire or purchase land for the purpose of

undertaking research and to take necessary measures

to disseminate knowledge to members.

To purchase or take on hire tractors, boring sets

and other agricultural implements and hire them to

members.

To issue loans to members for productive and other

similar purposes.

SUGAR CANE YIELD AND CRUSHING:

53

Under the jurisdiction of the

sugar factory, different varieties of sugar cane are

advocated for cultivation. They include early

varieties, mid varieties and late varieties. The early

varieties are co6907, 85A261, 87A298, 88A189, 86V96,

91V83, the mid varieties are co7805, 86A146, 88A162,

90a272, and late varieties are co7219, co7706. Out of

these varieties, early varieties yield quality sugar

cane and quality sugar after crushing. Different

varieties, especially, the mid and the late varieties

are advocated by the factory management for sugar cane

cultivation in order to get a continuous supply of

sugar cane during the operation period of the factory.

The sugar cane growers are largely small and marginal

farmers. The average holding of the land by and

individual farmer ranges from 0.5-2acres. Over 8,000

farmers are involved in sugar cane cultivation under

the jurisdiction of factory.

In order to draw sugarcane for crushing, the

factory conducts pre-harvest survey one month before

54

starting of crushing season. Taking into

consideration the entire sugarcane area, the area is

divided into four groups on the basis of the month,

the variety and ration / plant, etc., early varieties

are surveyed and grouped accordingly to know the

maturity of the crop. Once the pre-harvest survey of

the early varieties of sugarcane is completed and

based on the results of the survey, the factory

management then recommends took the farmers to harvest

the crop. After the harvest of early varieties of

sugarcane and subsequent crushing of the same at the

factory, the mid and the late varieties of sugarcane

and harvested and crushed in succession.

At the factory, 160 skilled and

unskilled workers are engaged for crushing and for the

production of sugar during the entire period of

factory operation. Further, the factory management

engages additional number of seasonal workers as daily

wage laborers (unskilled). Apart from this, 300

55

employees are engaged in Administration, Accounts, and

Agriculture and Engineering sections of the factory.

1. Raw materials:

Raw materials are those basic input materials that

are converted into finished product through the

manufacturing process.

2. Working in progress:

This includes those materials, which have been

committed to production process but have not yet been

completed.

3. Finished goods:

These are completed products a waiting sale .they are

the final output of the production process in a

manufacturing firm. The level of three kinds of

inventories differs depending on the nature of business.

A manufacturing firm will have substantially high level

of the finished goods inventories are no raw material

and work in progress inventory

56

PROCESS OF SUGAR PRODUCTION:

Sugar cane and sugar beet is the main crops

that contribute approximately 56% and 44% respectively

of the total sugar production in the world. Sugar cane

is the main source of sugar production in India and

holds a prominent position as a cash crop. Sugar cane

is a crop of the tropics while sugar beet is

essentially a crop of temperate regions. Sugar cane

from the fields is brought to the factory through

Lorries, tractors, and bullock carts. Sugar cane of

5 to 6 feet length is unloaded into the cane

trolleys and weighted in the automatic electric

weighing bridges and convey the trolled to the

tilting tables by the pushers, sugar cane is

unloaded into the cane carried by trunk tilting

system. Cash is prepared to 80-85% broken cells

with the help of two sets of cane canvas and

shredder, this process is called cane preparation.

In this process of manufacturing of white sugar

there are six stages. They are:

57

Juice Extraction

Juice Clarification

Evaporation

Crystallization

Centrifugation

Grading and Bagging

Packaging

Manuring

transporting

JUICE EXTRACTION:

The juice will be heated to 70 C

and then So2 gas and milk of lime are added. The

sulphited juice will be further heated to 105 C to 108C

in juice heater. Adding magnafloc to this hot

juice fed to the clarifiers helps in quicker

settling of muds in evaporators.

JUICE CLARIFICATION

This muddy juice is mixed with bagacillo and

fed to the vacuum filters.

58

EVAPORATION

Filtered juice will be sent back to the

process and the filter cake will be sent out. Filter

cake is a by- product with which we can make waxes

and can be used as manure to the cane fields.

The clear juice is sent to the

evaporators in which 75% of the water is

evaporated and syrup at around 60 brick is sent

to the pan floor through syrup sulphites in

which So2 will be added.

CRYSTALLIZATION:

The syrup is boiled in the pans till we get the

required size of crystal formation and masscults will

be allowed into the crystallizes for cooling and

exhaustion. After the masscults is

Cooled to the required level, it is sent to the

pug mills where the masscults is reheated for

better mobility.

CENTRIFUGATION

59

The masscults, is a mixture of sugar crystals and

molasses is sent from the pug mills to the centrifugals,

where the sugar and molasses are separated. The

molasses will then be sent to distillery, for the

manufacture of rectified spirits. If there is no

distillery they will send the molasses to private

parties.

The final molasses is a by- product of

sugar industry that can be used as raw materials

for distillery and for making cattle feed etc.

The sugar from centrifugals is dried and cooled

while passing through the hoppers to bucket

elevators.

GRADING AND BAGGING

Sugar is graded according to its crystal

sizes and stored in the bins. The sugar will be

bagged through automatic weighers, stitched and stored

in the god owns through belt conveyors and

stackers.

60

Different varieties of sugar cane are advocated for

cultivation. They include early varieties, mid

varieties and late varieties.

1. Avoiding losses of sales:

If a firm maintains adequate inventories it can

avoid losses on account of losing the customers for non-

supply of goods in time.

2. Reducing order cost:

The variable cost associated with individual order

e.g. Typing, checking, approving, mailing etc. can be

reduced if a firm places a few larger rather than

numerous small order.

61

CHAPTER-IV

CASH FLOW

ANALYSIS

62

CASH FLOW ANALYSIS

THE CO-OPERATIVE SUGARS Ltd, BHIMASINGI:

Procedure for preparing for cash flow statement

Cash flow statement is a method by which we

study changes in the financial position of a business

enterprise between beginning and ending financial statements

dates. Hence, the cash flow statement is prepared by

comparing two balance sheets and with the helps of such

other information derived from the accounts as may be

needed. Broadly speaking, the preparation of a cash flow

statement consists of two pans:

1.Statement or Schedule of changes in cash flow

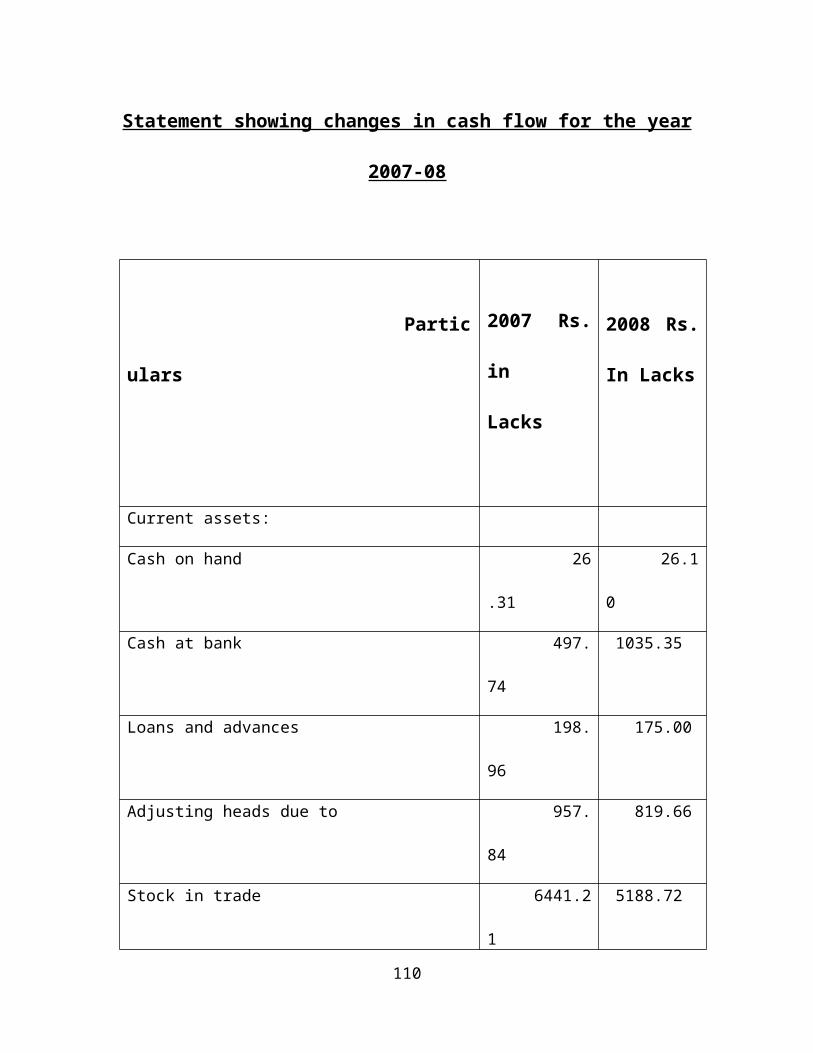

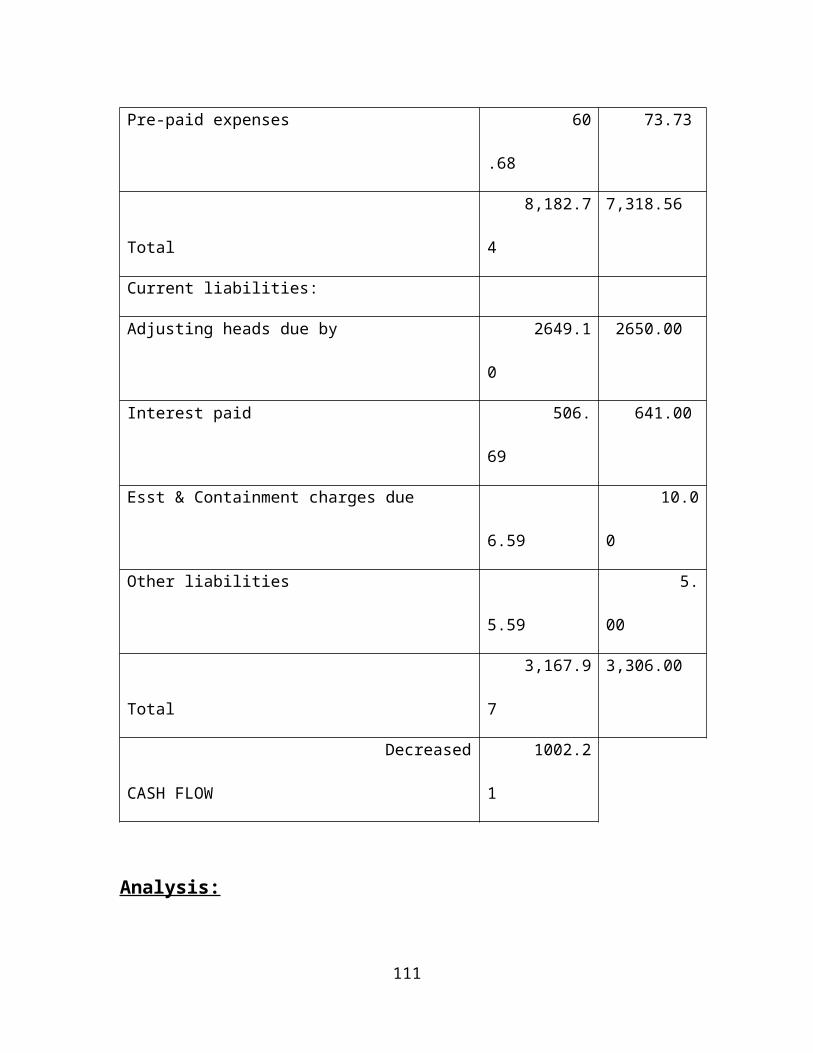

63

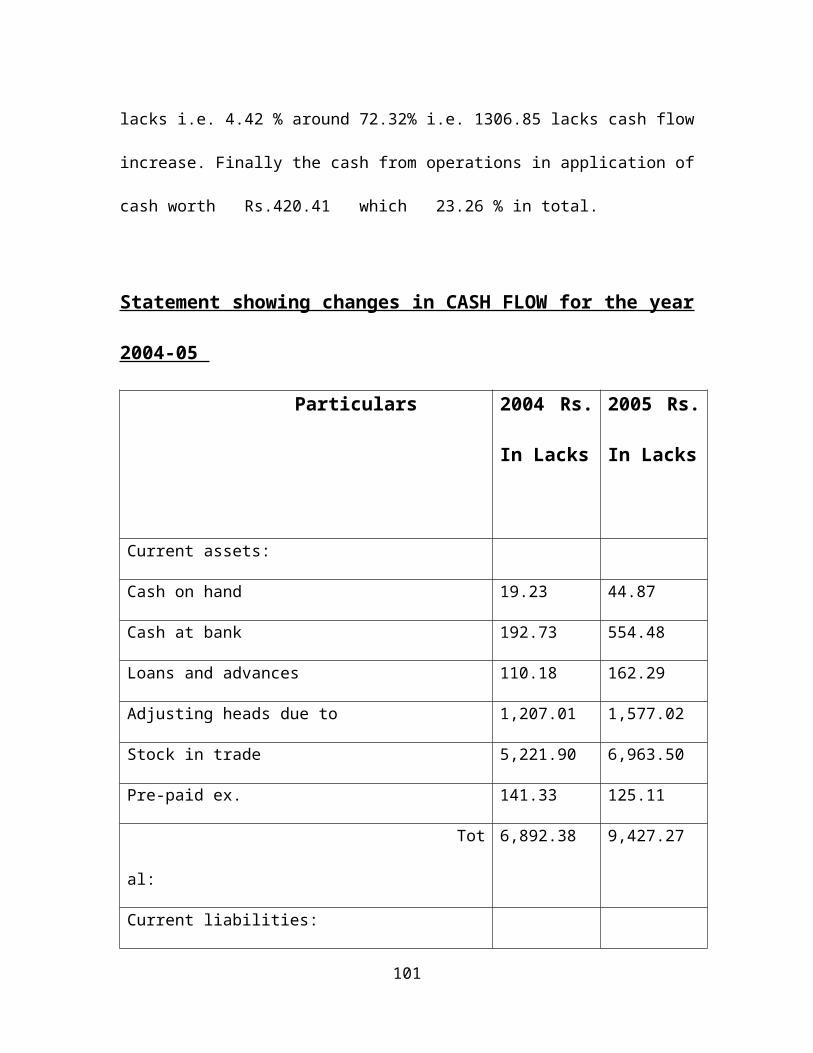

Cash flow means the excess of current assets

over current liabilities. Statement of changes in cash flow

is prepared to show the changes in the cash flow between the

two balance sheet dates. This statement is prepared with

the help of current assets and current liabilities derived

from the two balance sheets.

CASH FLOW =CURRENT ASSETS-CURRENT LIABILITIES.

2. Statement of sources and applications of cash

(I) an increase in current assets increases cash

flow.

(ii) A decrease in current assets decrease,

cash flow

(iii) An increase in current liabilities

decreases cash flow

(iv) A decrease in current liabilities

increases cash flow

The change in the amount of any current asset or current

liability in the current balance sheet as compared to that

of the previous balance sheet either results in increase or

64

decrease in cash flow. The difference is recorded for each

individual current asset and current liability. In case a

current asset in the current period is more than in the

previous period, the effects an increase in cash flow and it

is recorded in the increase column. But if a current

liability in the current period is more than in the previous

period, the effect is decrease in cash flow and it is

recorded in the decrease column or vice versa. The total

increase and the total decrease are compared and the

difference shows the net increase or net decrease in cash

flow It is worth nothing that schedule of changes in cash

flow is prepared only from current assets and current

liabilities and the other information is not of any use for

preparing this statement. A typical form of statement or

schedule of changes in cash flow is as follows:

MANAGEMENT OF CASH

Theoretical aspects of cash management

65

One of the main tasks of financial management is to

hoard and maintain adequate, but not excessive cash

position. Cash is an obvious and inescapable in sufficient

doses according to needs on a continuing basis. Cash is also

the major and much awaited output or result of the companies

operations and there is the need for effective plan to

deploy these liquid resources to utmost productive use.

A company that is growing fast and every turning out

hand some profits may be continuously faced with a state of

production. So finding adequate funds for operation needs is

an unending pre-occupation for the company’s finance manager

in adequacy of cash, even for short period is source of

trouble for most enterprise. It is not wise to have a lot

of cash which is idle, cash is not and earning assets.

It is the duty of the finance manager to provide

adequate cash to all segments of the organization .The has

also to ensure that no funds are blocked in idle cash since

this involve cost in terms of interest to the business a

66

sound cash management schemes, maintain the balance between

the objective of liquidity and cash.

The term cash with reference to cash management is used

in the sense it includes coins, currency notes, cheques,

bank drafts held by within in the banks. In broader sense,

it also include near cash, assets such as marketable

securities and time deposits with bank.

Motives for holding cash:

LORD Keynes, the noted economist has attributed 3 motives

for holding cash.

The transaction motive

The precautionary motive

The speculative motive

The transaction motive

The transaction motive arises from the need for

ready funds to make payment falling due in the ordinary

course of day to day business .Such as payments for

67

purchase, pay for wages, payment of operating expenses and

payment of these and dividends .The aim of cash management

to ensure functioning of day to day business by judicious

direction of the operation of the operating and contractual

payment are promptly.

Precautionary motive

The precautionary motive comes from the closer to keep

a cash caution or buffer to meet un expected contingencies

the degree of precautionary will normally bear an inverse

relationship to the degree of predictability of cash flows

of the business. As a matter abundant caution many companies

have learnt the art of establishing and maintaining good

lasting link with progressive banking institution .Thus,

having a ready borrowing power, the firm can release

available cash resources for remunerative applications.

Speculative motive

The speculative motive covers instances were the

intention is to hold cash to be able to take advantage of68

shifts insecurity prices, rising from changes in interest

and other factors .Thus it is not a common feature of

corporate financial management except in case of finance and

installment companies.

Cash management concern with the management, the cash

flows into and out of the organization. Management of cash

flows with in the firm and management of cash and balances

held by the firm at point of time.

Objective of cash management:

There are two basic objectives of the cash management

To meet the cash disbursement need as per the payment

schedule

To minimize the amount locked up as cash balance

As a matter of fact both the objectives are mutually

contradictory and therefore it is challenge task for the69

finance manager to reconcile them and to have the best in

process.

Meeting cash disbursement

The first basic objective of cash management is to meet

the payment schedule. In other words, the firm should have

sufficient cash to meet the various requirements of the firm

at different time periods. The business has to make payment

for purchase activity may come to grinding half, if the

payment schedule is not maintain cash has therefore been

aptly described as the” oil to lubricate the ever turning

wheels of business, without it the process grinds to a

stop”.

Permanent/Long-term working capital

Permanent working capital should be financial in such a way

that the enterprise may have its uninterrupted use for

sufficiently longer periods.

The sources of long-term working capital are

70

1. Shares: A company can issue various type of shares as

equity shares, preference shares and deferred shares.

Equity shares do not have any fixed commitment,

preference shares have a fixed rate and deferred shares

cannot be issued by a public company.

2. Debentures: Debenture holders are to be paid a fixed

rate of interest. The debentures may be of various

kinds such as simple, naked or unsecured debentures,

secured or mortgaged debentures, redeemable,

irredeemable debentures, convertible, non-convertible

debentures. Interests on debentures have to be paid on

certain predetermined intervals at fixed rate and also

debentures get priority on repayment at the time of

liquidation.

3. Public Deposits: Public deposits are the fixed deposits

accepted by a business enterprise directly from the

public. Public deposits have advantages such as very

simple and convenient source of finance, taxation

benefits, trading on equity, inexpensive source of

finance but non-banking concerns cannot borrow by way71

public deposits more than 25% of its paid up capital

and free reserves.

4. Pouching Back of Profits : This means the reinvestment

by a concern of its surplus earnings in its business.

This method has a number of advantages as it is the

cheapest, no need to keep securities; it ensures stable

dividend policy and gains confidence of the public.

But excessive report may lead to monopolies, over

capitalization and speculation, etc.

5. Long from Financial Institutions: Financial institution

such as commercial Bank, life insurance corporation

(LIC), Industrial Financial Corporation of India

(IFCI), Industrial Development Bank of India (IDBI) etc

provide short-term, medium-term and long-term loans.

Interest is charged at a fixed rate and repayment

should be done by way of installments.

6. Temporary/short-term working capital: Some amount of

working capital may be required to meet the seasonal

demands and rise in prices, strikes etc. this

72

proportion of working capital given rise to temporary

or variable working capital.

The sources of short-term working capital are:

a). Commercial banks: The major portion of working

capital loans are provided by commercial banks through a

wide variety of loans tailored to meet the specific

requirements of a concern.

The different forms for providing loans and advances are:

a. Loans

b. Cash credits

c. Overdrafts

d. Purchasing and discounting of bills

b) Indigenous Bankers: Private money-lenders and other

country bankers used to be only source of finance prior to

the establishment of commercial banks. But even today some

business sources have to depend upon indigenous bankers for

obtaining loans to meet their working capital requirements.

c) Trade Credits: Trade credit arrangements of a concern

with its suppliers an important source of short-term73

finance. The main advantages of this source are; it is very

convenient method of finance, flexible but this method

charges high prices and loss of cash discount.

d) Installment Credit: This is another method by which the

assets are purchased and the possession of goods is taken

immediately but the payment is made in installments over a

predetermined period of time.

e) Advances: Some business houses get advances from their

customers and agents against orders and this source of

finance for them and it is also a cheaper source

Minimizing funds locked up as cash balances

The second basic object of cash management is to

minimize the amount locked up as cash balances. In the

process of minimizing cash balances the financial manager is

confronted with to conflicting aspects.

A higher cash balance ensures proper presents with all

it advantages. But this will result in a large balance of

cash remaining idle low level of cash balance may result in

failure of the firm to meet the payment schedule the74

financial manager should therefore, try to have an optimum

amount of cash balance keep above facts in view.

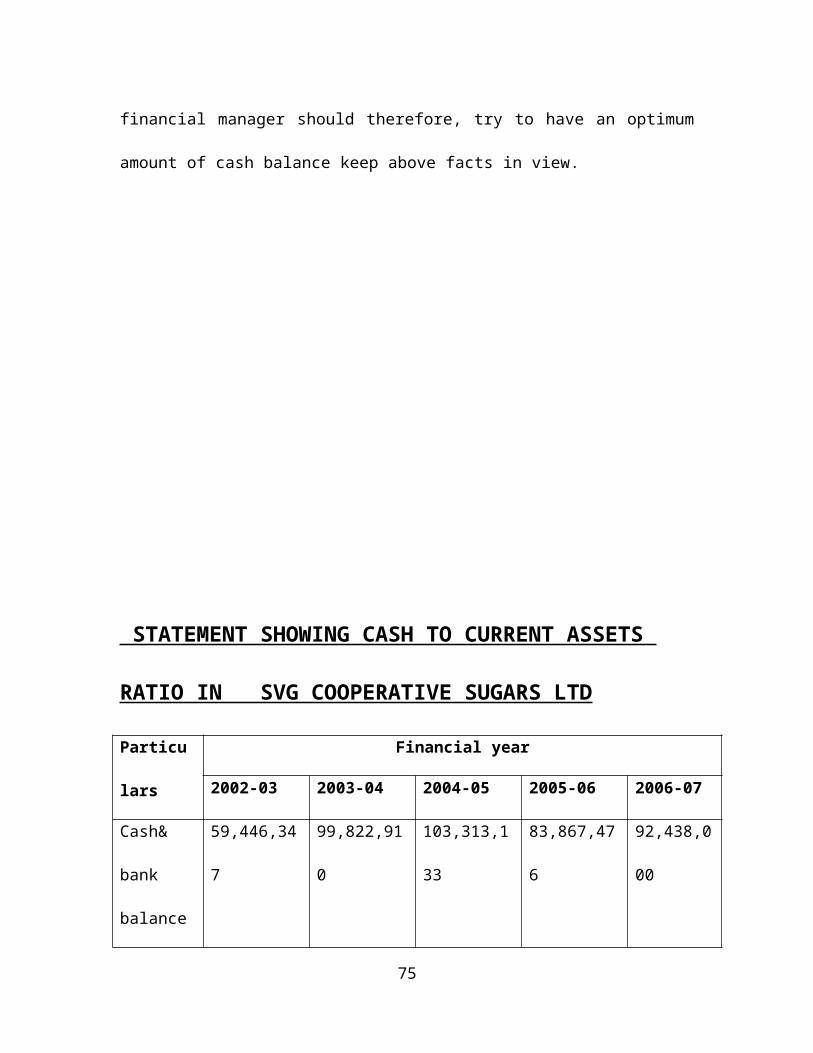

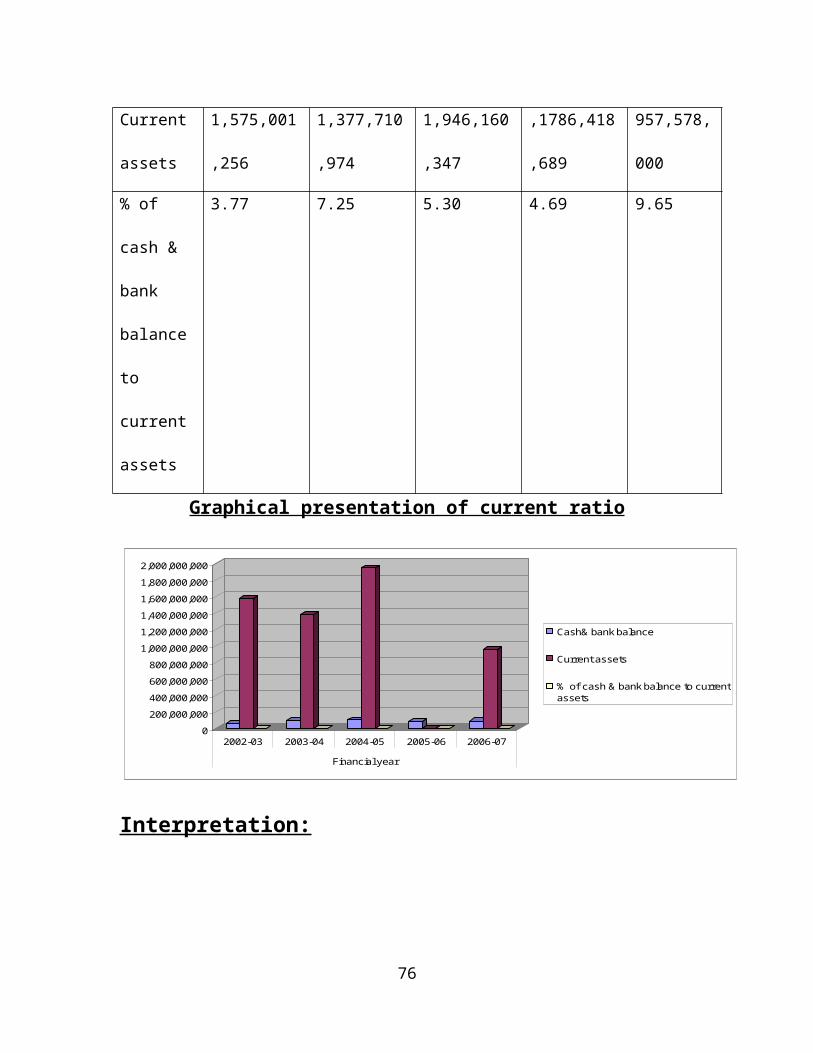

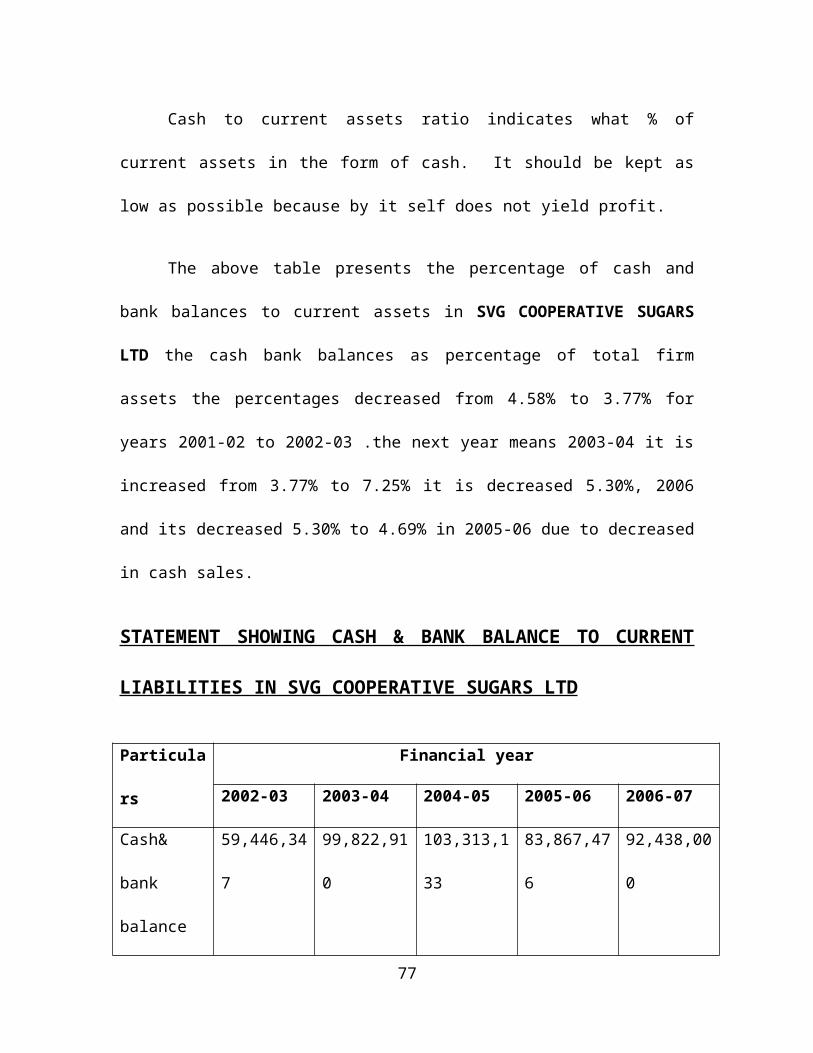

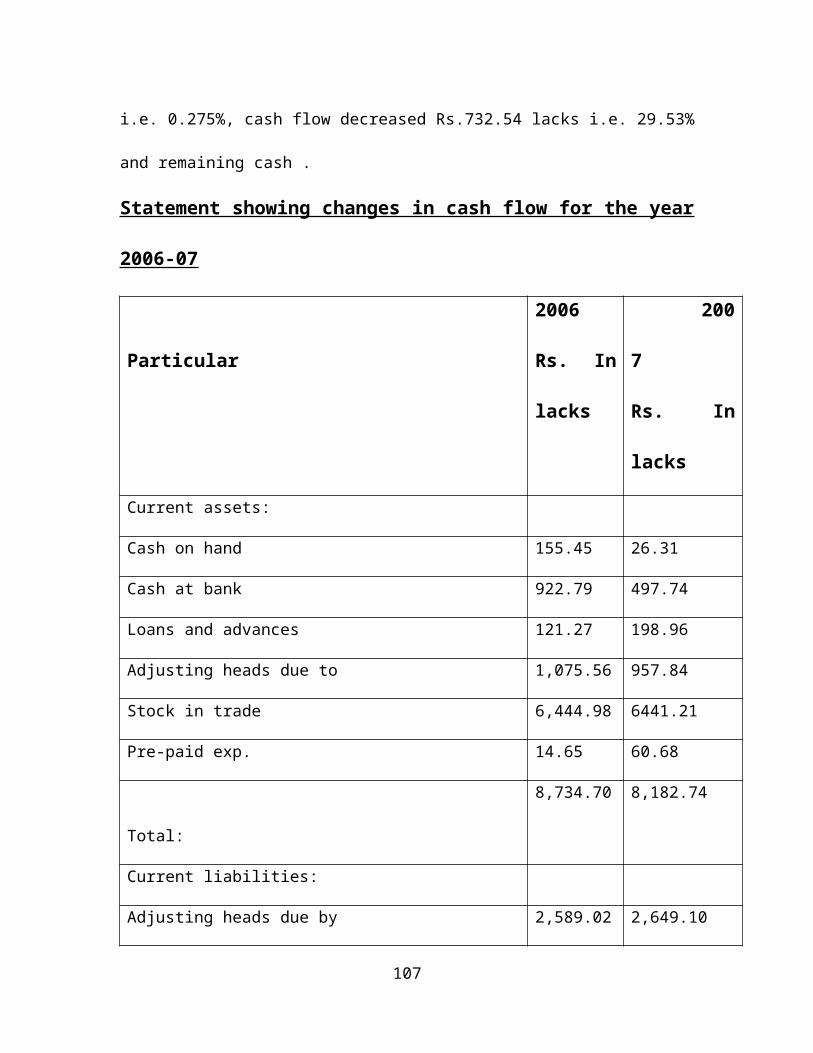

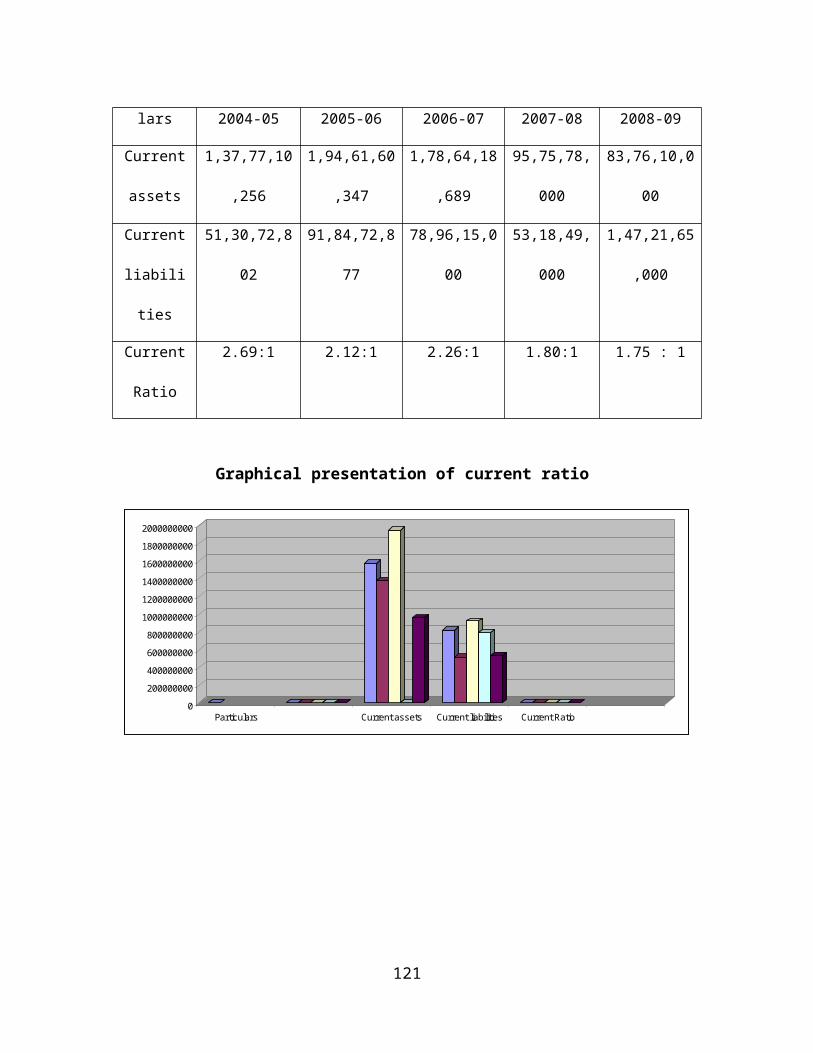

STATEMENT SHOWING CASH TO CURRENT ASSETS

RATIO IN SVG COOPERATIVE SUGARS LTD

Particu

lars

Financial year

2002-03 2003-04 2004-05 2005-06 2006-07

Cash&

bank

balance

59,446,34

7

99,822,91

0

103,313,1

33

83,867,47

6

92,438,0

00

75

Current

assets

1,575,001

,256

1,377,710

,974

1,946,160

,347

,1786,418

,689

957,578,

000

% of

cash &

bank

balance

to

current

assets

3.77 7.25 5.30 4.69 9.65

Graphical presentation of current ratio

0200,000,000400,000,000600,000,000800,000,000

1,000,000,0001,200,000,0001,400,000,0001,600,000,0001,800,000,0002,000,000,000

2002-03 2003-04 2004-05 2005-06 2006-07

Financial year

Cash& bank balance

Current assets

% of cash & bank balance to currentassets

Interpretation:

76

Cash to current assets ratio indicates what % of

current assets in the form of cash. It should be kept as

low as possible because by it self does not yield profit.

The above table presents the percentage of cash and

bank balances to current assets in SVG COOPERATIVE SUGARS

LTD the cash bank balances as percentage of total firm

assets the percentages decreased from 4.58% to 3.77% for

years 2001-02 to 2002-03 .the next year means 2003-04 it is

increased from 3.77% to 7.25% it is decreased 5.30%, 2006

and its decreased 5.30% to 4.69% in 2005-06 due to decreased

in cash sales.

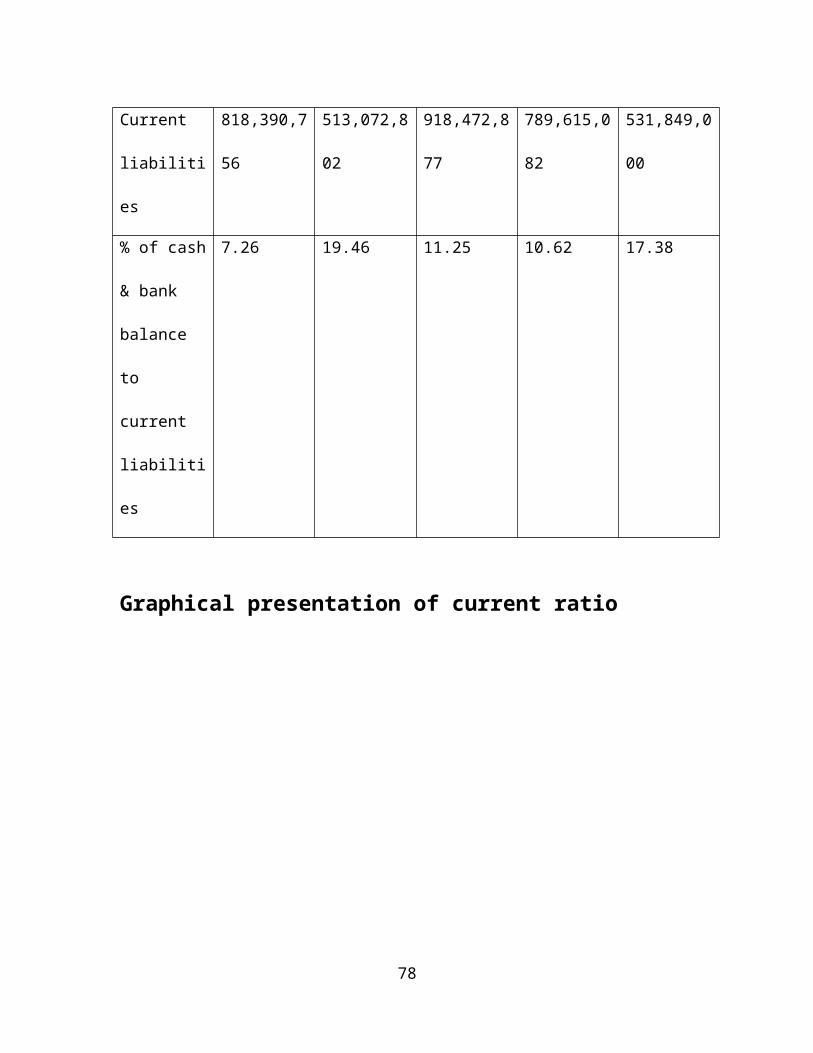

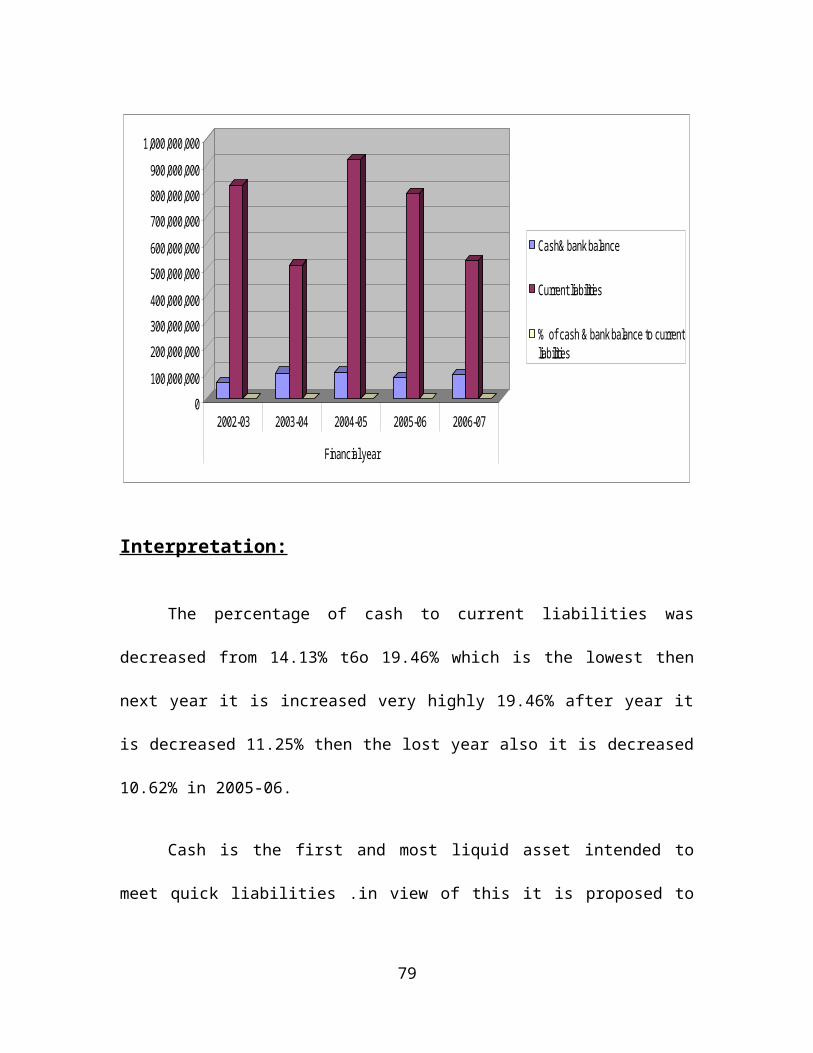

STATEMENT SHOWING CASH & BANK BALANCE TO CURRENT

LIABILITIES IN SVG COOPERATIVE SUGARS LTD

Particula

rs

Financial year

2002-03 2003-04 2004-05 2005-06 2006-07

Cash&

bank

balance

59,446,34

7

99,822,91

0

103,313,1

33

83,867,47

6

92,438,00

0

77

Current

liabiliti

es

818,390,7

56

513,072,8

02

918,472,8

77

789,615,0

82

531,849,0

00

% of cash

& bank

balance

to

current

liabiliti

es

7.26 19.46 11.25 10.62 17.38

Graphical presentation of current ratio

78

0100,000,000200,000,000300,000,000400,000,000500,000,000600,000,000700,000,000800,000,000900,000,000

1,000,000,000

2002-03 2003-04 2004-05 2005-06 2006-07

Financial year

Cash& bank balance

Current liabilities

% of cash & bank balance to currentliabilities

Interpretation:

The percentage of cash to current liabilities was

decreased from 14.13% t6o 19.46% which is the lowest then

next year it is increased very highly 19.46% after year it

is decreased 11.25% then the lost year also it is decreased

10.62% in 2005-06.

Cash is the first and most liquid asset intended to

meet quick liabilities .in view of this it is proposed to

79

compare the trends in cash holding with the trend in the

quick liabilities.

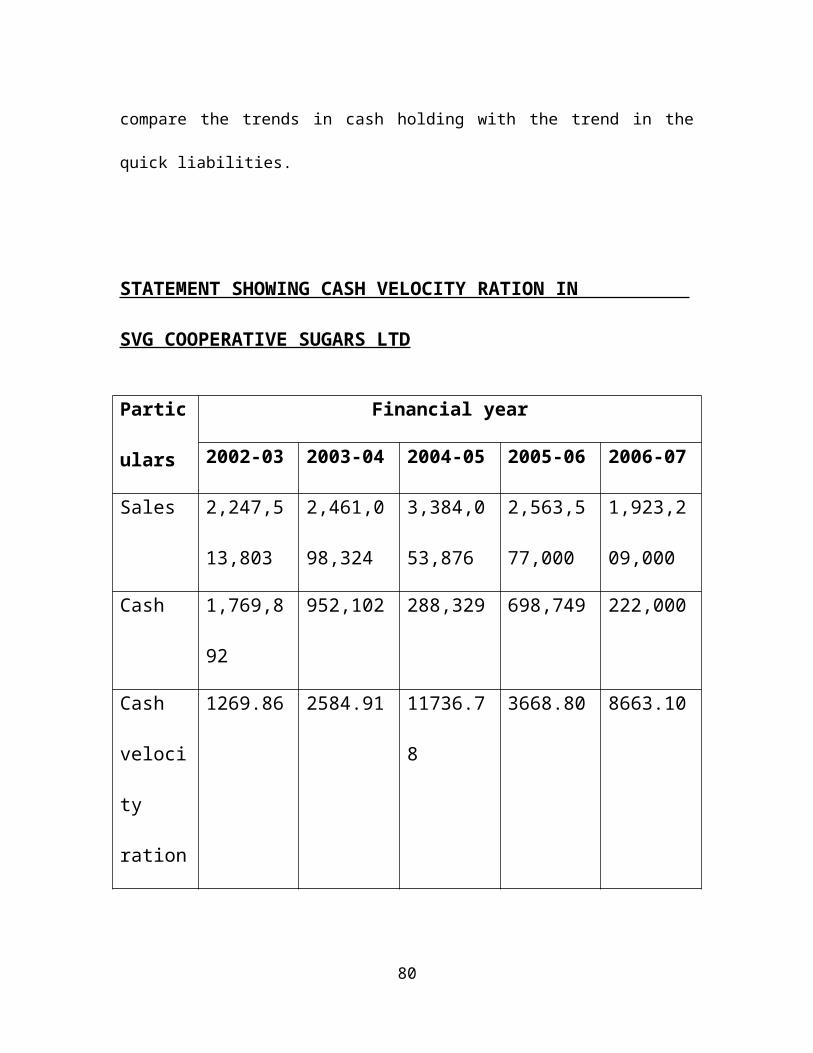

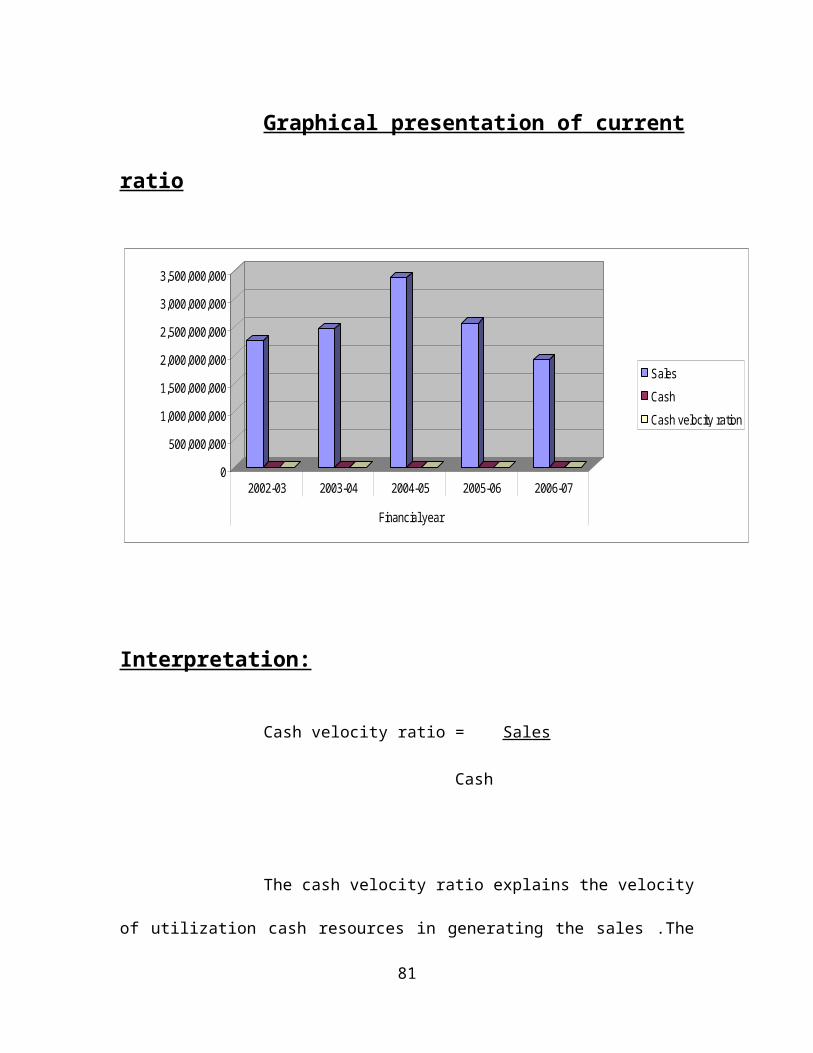

STATEMENT SHOWING CASH VELOCITY RATION IN

SVG COOPERATIVE SUGARS LTD

Partic

ulars

Financial year

2002-03 2003-04 2004-05 2005-06 2006-07

Sales 2,247,5

13,803

2,461,0

98,324

3,384,0

53,876

2,563,5

77,000

1,923,2

09,000

Cash 1,769,8

92

952,102 288,329 698,749 222,000

Cash

veloci

ty

ration

1269.86 2584.91 11736.7

8

3668.80 8663.10

80

Graphical presentation of current

ratio

0

500,000,000

1,000,000,000

1,500,000,000

2,000,000,000

2,500,000,000

3,000,000,000

3,500,000,000

2002-03 2003-04 2004-05 2005-06 2006-07

Financial year

SalesCashCash velocity ration

Interpretation:

Cash velocity ratio = Sales

Cash

The cash velocity ratio explains the velocity

of utilization cash resources in generating the sales .The

81

high cash velocity is desirable but at the same time it

adversely effects the short term liquidity position of the

business unit .In the year 2004-2005 generation of rupees

3,384,053,876 of sales .

The company having only 2,88,329 worth of cash

resources with the merge cash balances .The sample unit is

unable to discharge its liabilities so that there is high

average payment period when the company is following a too

liberal credit policy .It is adversely effective the cash

position.

THE MANAGEMENT OF FIXED ASSETS AND CURRENT ASSETS

DIFFER UN THREE IMPORTANT WAYS

1. In managing fixed assets the three factors is very

important that is why discounting compounding play a very

important role in any capital budgeting decision. But

because the time frames of current assets is only of

money it less significant in the management of current

assets.

82

2. The liquidity positions of firm’s dependent on the

investment in current assets then more then better where

as the role of fixed as for as liquidity is concerned

reliable.

Any short run immediate need of the company whether it be

used for cash or adjustments to fluctuation in safes can be

made only through adjustments. The level of the various

components of the current assets. The calls for efficient

management of current assets which from part of management

of working capital.

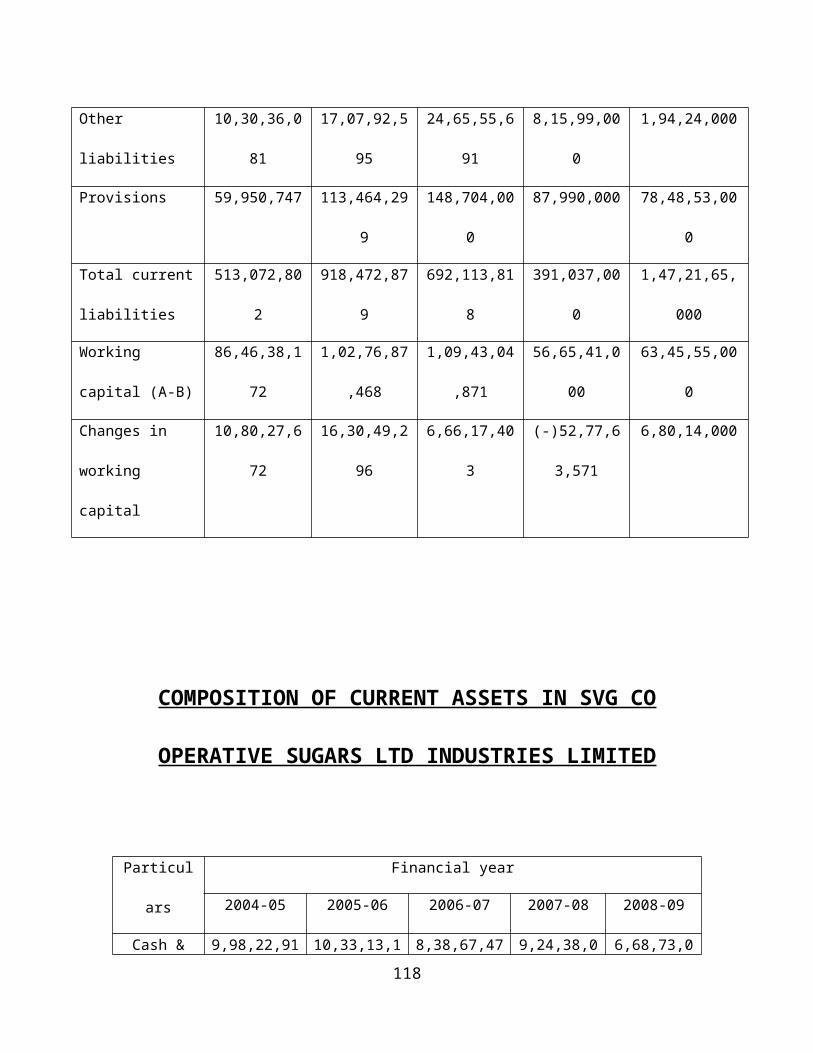

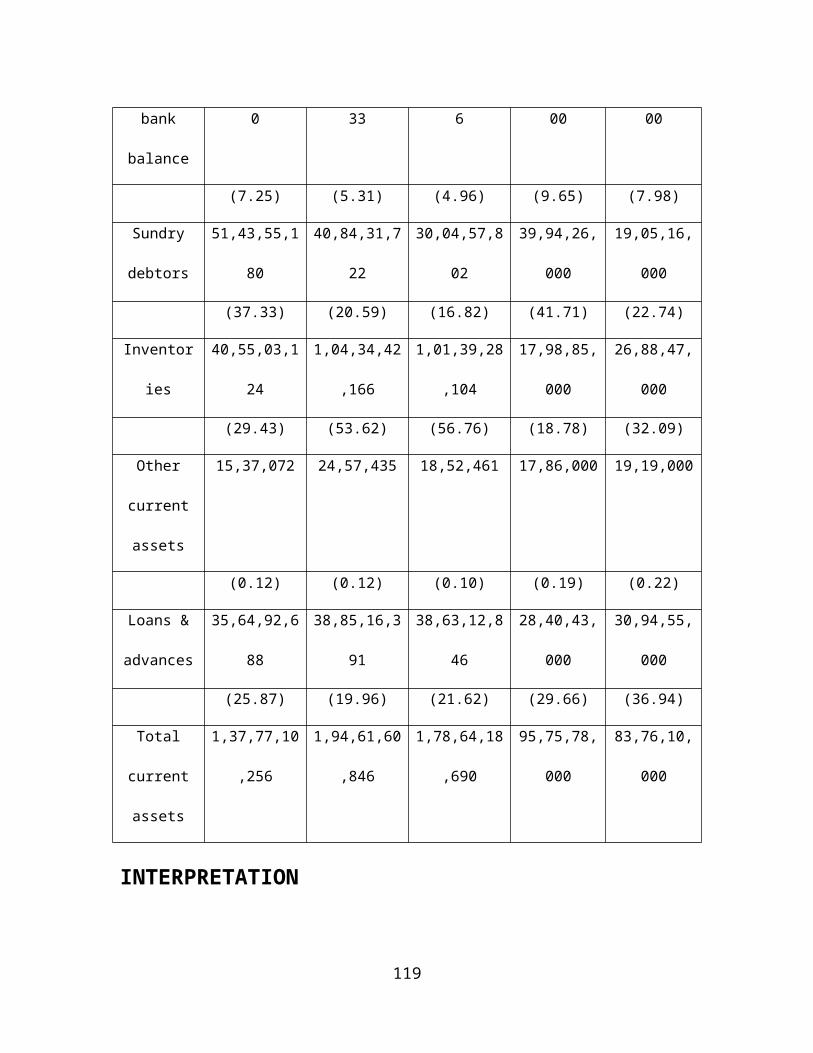

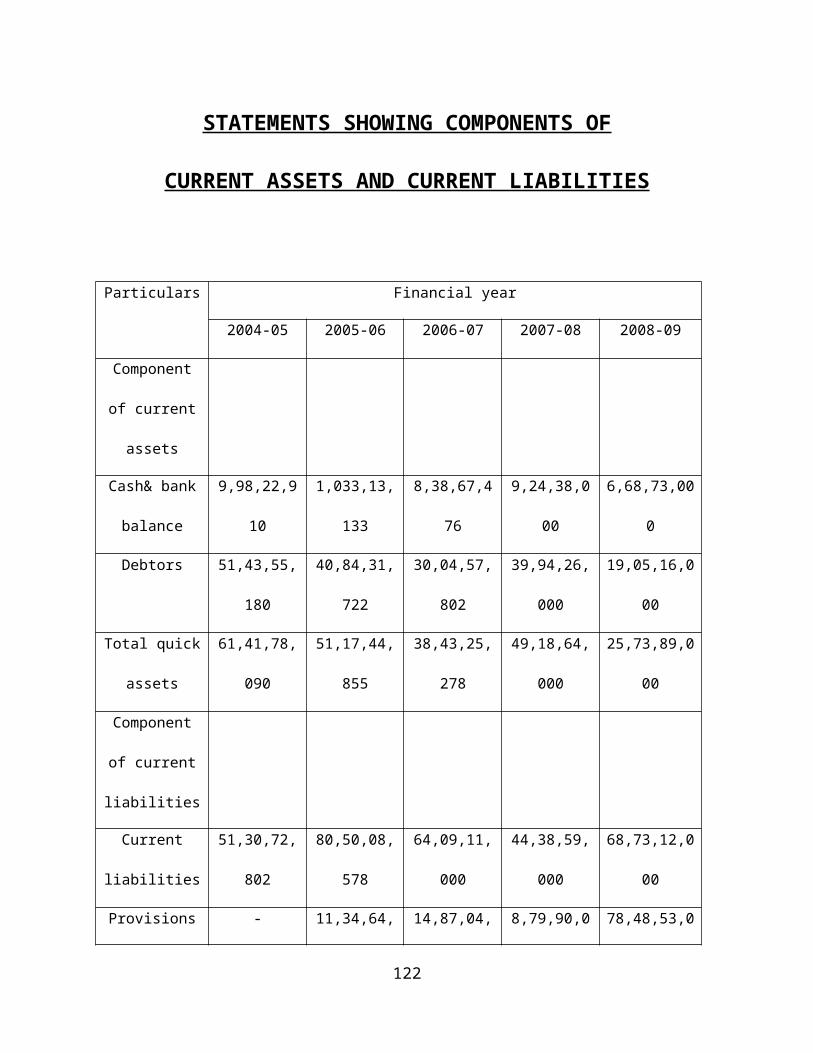

CURRENT ASSETS:

The term current assets refers to those assets which in

the ordinary course of business will be turned into cash

with in one year

The major current assets of cash marketable securities

account receivable and inventories close securities of the

above table no: 1 shows that

83

In the three years of 2004-05, 2006-07, 2007-08&2008-09

the study period inventories from major portion in the

current assets of the enterprise.

In the two years of 2005-06 & 2006-07 the study period

debtors form major portion in the C.A of the

enterprise.

There is some up & down in cash & bank balance from

2004-05 to 2008-09.totally it is increases from 9, 98,

22,910 to 6, 68, 73,000.

There is decrease in inventories from 40,55,03,124 to

26,88,47,000 the portion of inventories as percentage

of total current assets declined from 53.62% to 29.33%

and after that it is increased finally 56.76% in 2007-

08

There is an decrease debtors from 2004-05 to 2006-07

due to credit sales increased on that period after

2007-2008 it is decreases every year due to credit

sales decrease on that period.

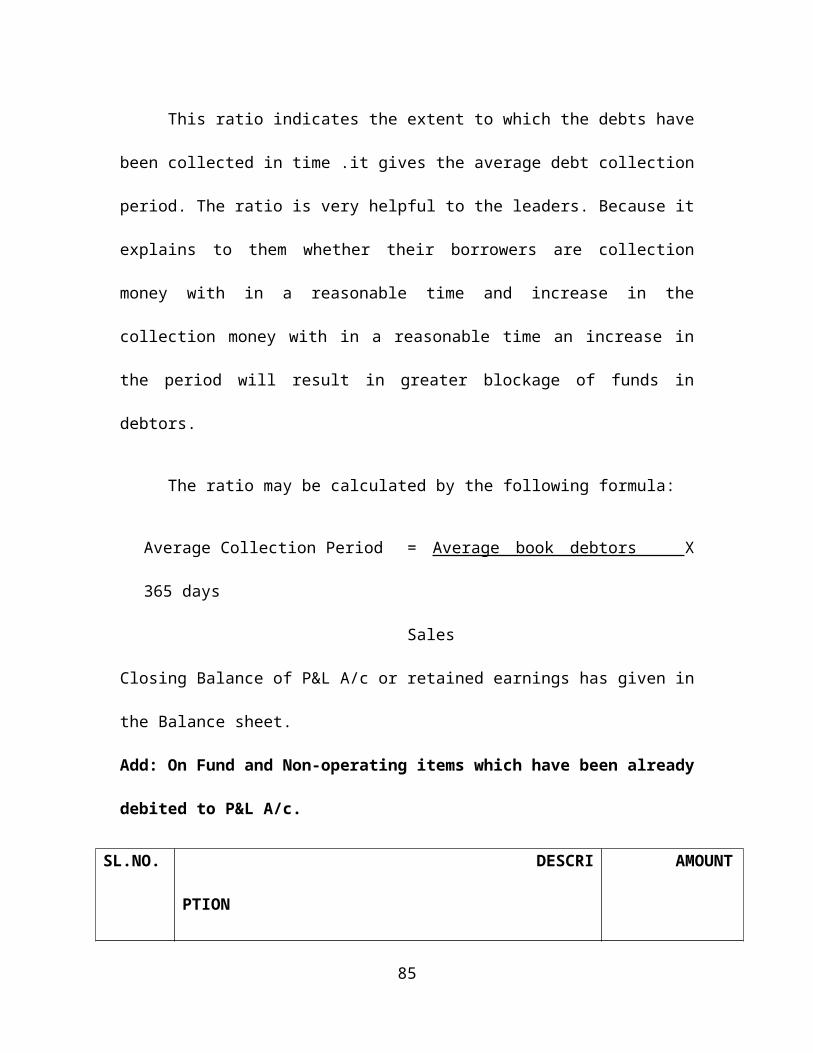

Average collection period:

84

This ratio indicates the extent to which the debts have

been collected in time .it gives the average debt collection

period. The ratio is very helpful to the leaders. Because it

explains to them whether their borrowers are collection

money with in a reasonable time and increase in the

collection money with in a reasonable time an increase in

the period will result in greater blockage of funds in

debtors.

The ratio may be calculated by the following formula:

Average Collection Period = Average book debtors X

365 days

Sales

Closing Balance of P&L A/c or retained earnings has given in

the Balance sheet.

Add: On Fund and Non-operating items which have been already

debited to P&L A/c.

SL.NO. DESCRI

PTION

AMOUNT

85

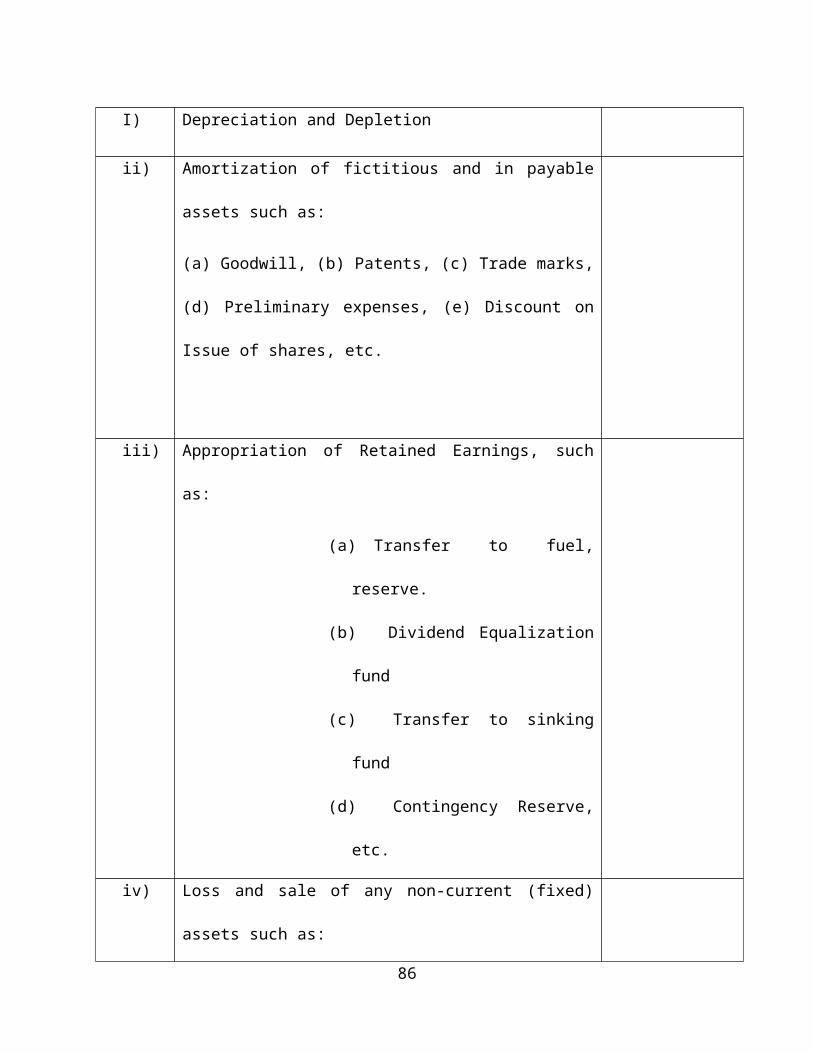

I) Depreciation and Depletion

ii) Amortization of fictitious and in payable

assets such as:

(a) Goodwill, (b) Patents, (c) Trade marks,

(d) Preliminary expenses, (e) Discount on

Issue of shares, etc.

iii) Appropriation of Retained Earnings, such

as:

(a) Transfer to fuel,

reserve.

(b) Dividend Equalization

fund

(c) Transfer to sinking

fund

(d) Contingency Reserve,

etc.

iv) Loss and sale of any non-current (fixed)

assets such as:

86

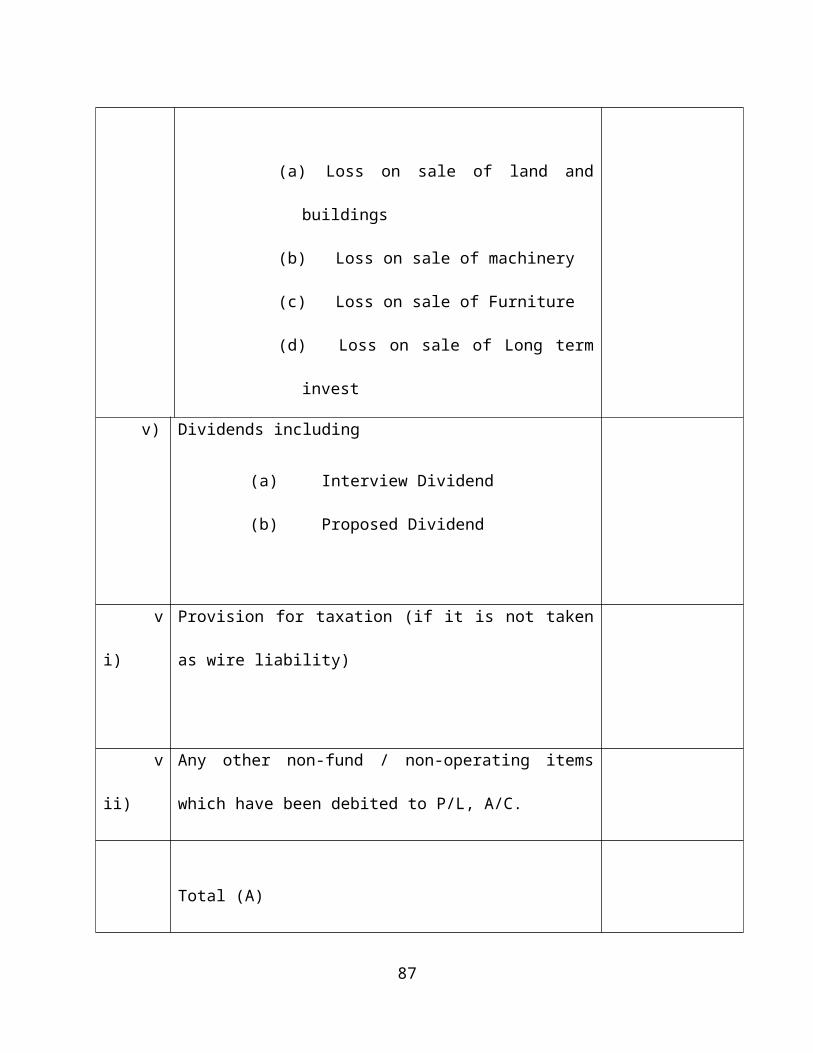

(a) Loss on sale of land and

buildings

(b) Loss on sale of machinery

(c) Loss on sale of Furniture

(d) Loss on sale of Long term

invest

v) Dividends including

(a) Interview Dividend

(b) Proposed Dividend

v

i)

Provision for taxation (if it is not taken

as wire liability)

v

ii)

Any other non-fund / non-operating items

which have been debited to P/L, A/C.

Total (A)

87

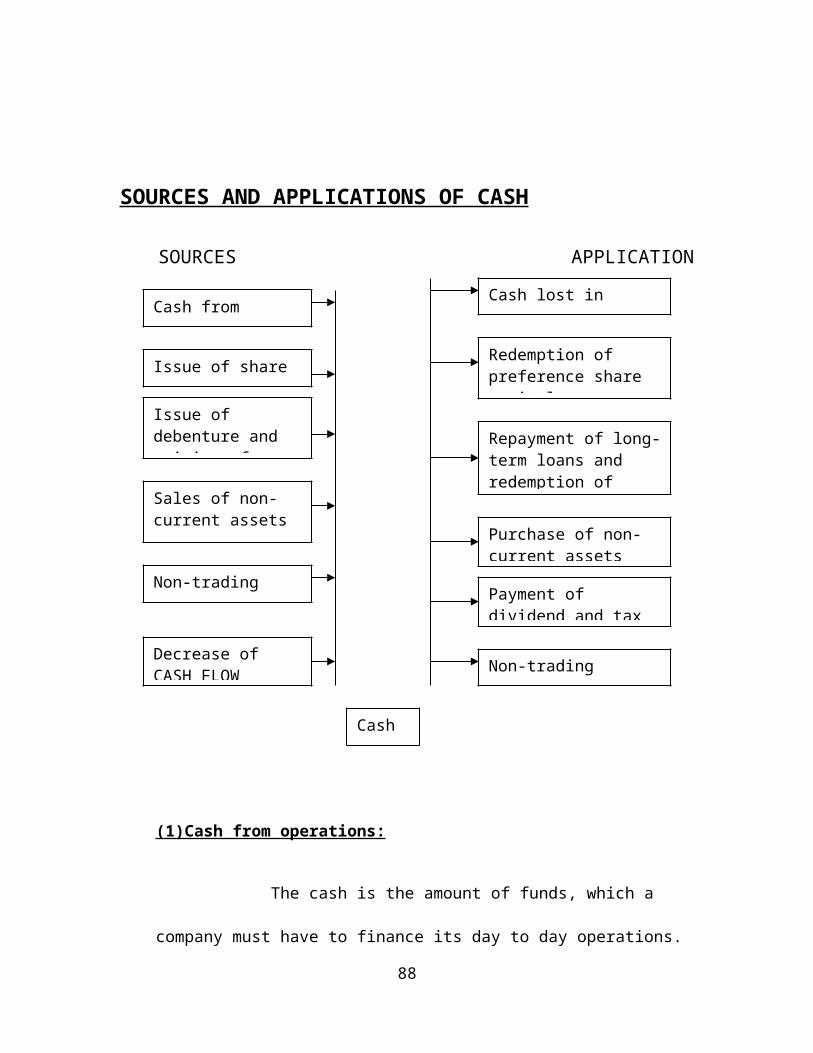

SOURCES AND APPLICATIONS OF CASH

SOURCES APPLICATION

(1)Cash from operations:

The cash is the amount of funds, which a

company must have to finance its day to day operations.

88

Cash from operations

Issue of share capitalIssue of debenture and raising of

Sales of non-current assets

Non-trading receipts Payment of

dividend and tax

Purchase of non-current assets

Repayment of long-term loans and redemption of

Redemption of preference share capital

Cash lost in operations

Decrease of CASH FLOW Non-trading

payment

Cash

It can also be regarded as that operation of the

Companies total capital which is employed in short term

operations. It can take the form of cash near cash and

other assets are stock of raw material and suppliers

needed for manufacturing. Stock of finished goods a

waiting sale, semi-process items or components that will

soon emerges as final products. Sundry debtors spending

collection against credit sales and short term

investment if any.

The current assets are those assets which can be converted

into cash within a short period of time, generally not

exceeding one year without diminution in the value of assets

and include cash, bank, marketable securities inventory of

raw material, semi-finished goods and finished goods.

Debtors, bills receivable and prepaid expenses

(2) Issue of share capital:

If during the year there is any increase in the

share capital, whether preference or equity, it means

capital has been raised during the year. Issue of shares is

89

a source of cash, as it constitutes inflow of cash. Even the

calls received from partly paid shares constitute an inflow

of cash. It should also be remembered that it is the net

proceeds from the issue of share capital, which amounts to a

source of cash and hence in case shares are issued at

premium, even the amount of premium collected shall become a

source of cash. The same is true when shares are issued at

discount; kit will not be the nominal value of shares but

the actual realization after deduction discount that shall

amount to inflow of cash. But sometimes shares are issued

otherwise than in cash the following rules must be followed:

i. Issue of shares or making of partly paid shares is

fully paid out of accumulated profits in tile form/of

bonus shares is not a source of cash.

ii. Issues of shares for consideration other than current

assets such as against purchase of land, machines, and

etc. does not amount to inflow of cash.

90

iii. Conversion of debentures or loans into shares also does

not amount to inflow of cash. In all the three cases

mentioned above, both the

iv. Amounts involved are non-current and do not involve any

current assets or cash.

(3) Issue of Debentures and Raising of Loans, etc.

Issue of debentures or rising of loans (long-term),

whether secured or unsecured results in the flow of cash

into the business. The inflow of cash is the; actual

proceeds from the issue of such debentures or rising of

loans, i.e., including the amount of premium or excluding

discount, if any. However, loans rose for consideration

other than a current asset, such as for purchase of

building, will not constitute inflow of cash because in

that case the accounts involved are only fixed or non-

current.

91

(4) Sale of Fixed (non-current) Assets and Long-term

or Trade investments .

When any fixed or non –current asset like land, building,

plant and Machinery, furniture, long-term investments etc.

Are sold it “C411- 1 racts cash and becomes a source of

cash. However, it must be remembered that if one fixed

asset is exchanged for another fixed asset, it does not

constitute an inflow of cash because no current assets

are involved.

(5) Non-Trading receipts.

Any non-trading receipt like dividend received, refund flax;

rent received, etc. also increases cash and is treated as a

sources of cash because such an income is not included in

the cash from operations.

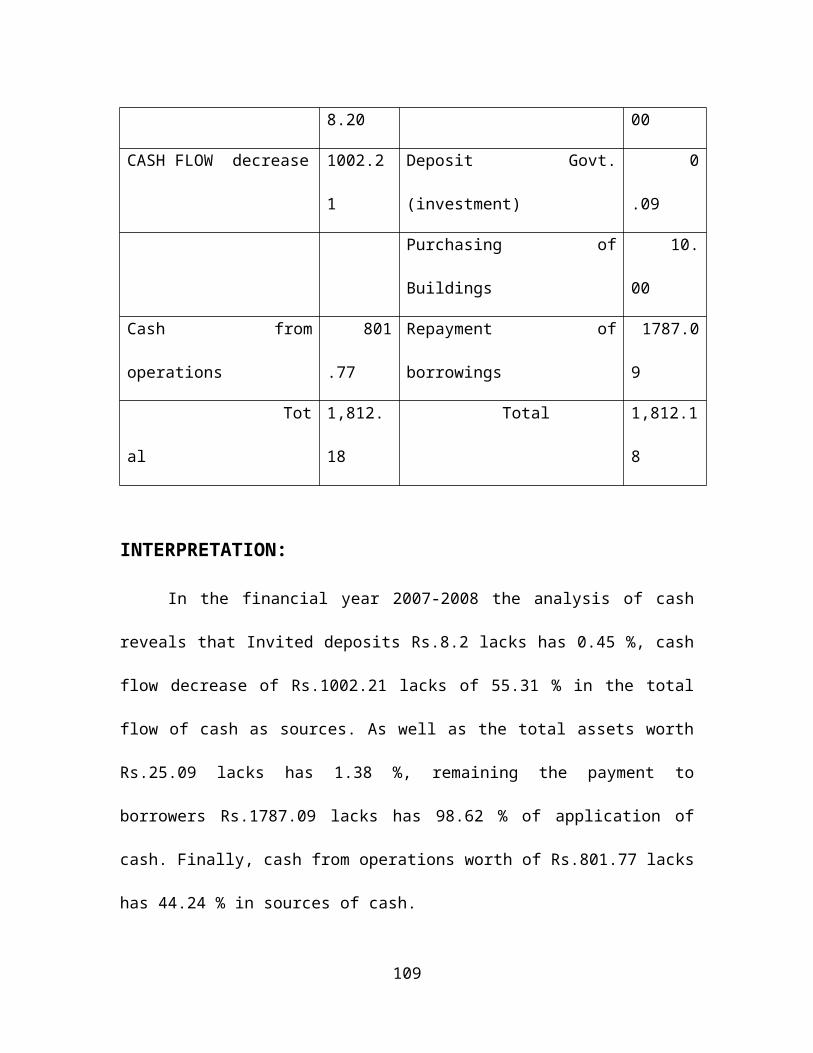

(6) Decrease in cash flow

92

If the cash flow decreases during the current period as

compared to the previous period, it means that there has

been a release of cash from cash flow and it constitutes a

source of fund

APPLICATION OR USES OF CASH

1) Cash lost in operations.

Some times the result of trading in a certain year

is a loss and some cash are lost during that period in

trading operations 1 such loss of cash in trading amounts

to an outflow of cash and is treated as an application of

cash.