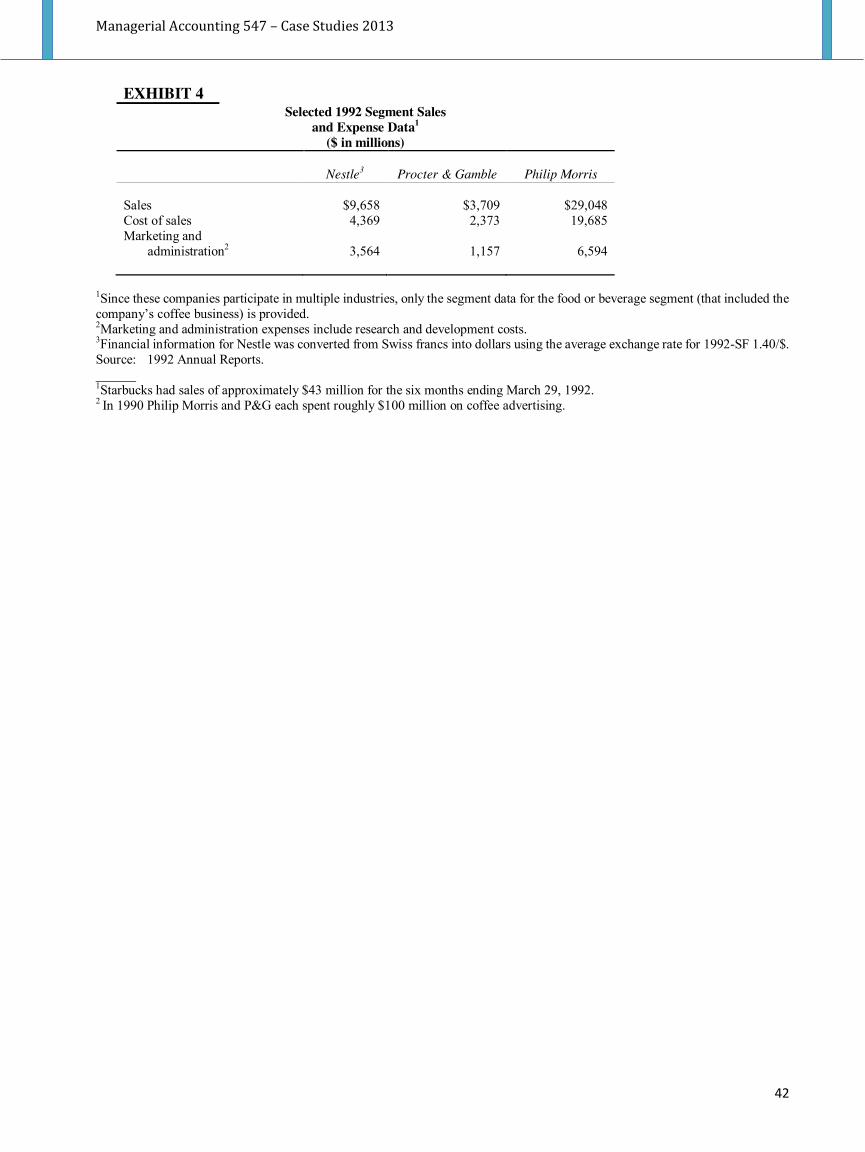

Embed Size (px)

Citation preview

Case Studies

2013

Managerial Accounting 547

Study Package Number: 313419 Credits: 25 Pre-requisite: Nil

Curtin Business School School of Accounting

Managerial Accounting 547 – Case Studies 2013

2

ASM Lithography

An anonymous-looking set of low-rise buildings outside Eindhoven in the Netherlands represents one of Europe’s biggest hopes in high technology. It is the headquarters of ASM Lithography, a company poised, on the back of an agreed takeover of a US rival, to become the world’s biggest maker of wafer-steppers, machines that play a vital role in manufacturing microchips. The go-ahead for ASM’s $1.6bn (£1.1bn) takeover of Silicon Valley Group, which is being delayed by a US government inquiry, would continue a success story that has few parallels in Europe, where in the past 25 years companies in electronics-related technologies have generally been outmanoeuvred by competitors from the US and south-east Asia. WAFER-STEPPER TECHNOLOGY The mass proliferation of digital devices – from personal notebooks to mobile telephones – is the result of increasingly powerful and cheap silicon chips. Driving on these changes has been the ability of engineers to cram more electronic devices on to a small piece of silicon. The wafer-stepper is the key to this development. Largely because of advances in wafer-steppers, the number of transistor-equivalents that can be squeezed on to a microchip has increased 250,000-fold over the past 30 years, while the price paid by the customer for each bit of information stored on the chip has fallen 30,000-fold (see Exhibit 1). The wafer-stepper takes its name from the step-and-repeat process by which the lens system in the machine shuttles across the surface of a 300mm-diameter wafer. This is how it can expose, with light passed through a photo-mask, each small part of the wafer. In a typical high-speed photo-lithography procedure, each wafer (which will later be dissected to give between 100 and 1,000 identical chips, depending on size) stays inside the wafer-stepper for only about half a minute for each process to print a specific layer of circuitry. In most microcircuits, a wafer will have to return to the machine several times, to print further layers of circuits that are built up on top of the first one. This means that, each time the wafer is inside the machine, it may have to make a slight sideways movement every half a second or so, while the lens system also moves, possibly in a different direction and at a different speed. This translates into an almost unbelievably complicated mechanical problem. The lens system and wafer have to be aligned with a precision of one nanometre and in a fraction of a second, immediately after the wafer has been shifted with a force equivalent to several times gravitational acceleration. The wafer is then flooded with ultraviolet light, before a further step-and-repeat process takes place. Under ASM Lithography’s partnership strategy, it does not tackle all the technology behind this by itself. Devising the precision mechanics of ASM’s wafer system is left to one of its four main partners – Philips, the Dutch electrical goods and electronics company that was ASM’s original parent and continues to hold a small stake. The sensor and positioning technology (metrology) is the preserve of Agilent, a US instrumentation company, formerly part of the Hewlett-Packard computer company. While the optics in each wafer-stepper is left to Zeiss of Germany, the light sources in ASM’s machines come mainly from a fourth partner – Cymer, a US manufacturer of high-frequency lasers that emit light in the ultraviolet range at a wavelength of 248 nanometres. Exhibit 1 How the performance and price of microchips have changed

Source: ASM Lithography.

Year

Minimum feature size for an advanced chip (micrometres)

Price per bit of random access memory (1,000th of US¢)

Bit capacity for random access

memory

1970 1980 1990 10.00 1.30 0.50 492 15 0.48 1,000 64,000 4m 2000 0.18 0.015 256m 2010 (forecast) 0.05 0.00047 64bn

Managerial Accounting 547 – Case Studies 2013

3

ASM AND WAFER STEPPERS Behind ASM’s success is the brain-box model: an approach apparent in other areas of high-tech manufacturing. It involves the company maintaining strong links with customers and retaining a crucial role in technology development while leaving to partner businesses much of the manufacturing and design of subcomponents. Incongruously, an important contributor to ASM making this strategy work in the microelectronics age turns out to be a 155-year-old German business steeped in the mechanical engineering principles of the nineteenth century. Carl Zeiss, a large, privately owned optics group, is the Dutch company’s sole supplier of the complex lens systems that are an essential part of its machines and account for about a quarter of its manufactured costs. Costing up to $10m and weighing about 15 tonnes, wafer-steppers are among the most complicated machines on earth. They use optics, precision engineering and lasers to define with mind-boggling precision the dimensions of integrated circuits. ‘Just about everything we do involves technologies at the limits of human capability,’ says Doug Dunn, ASM’s chief executive. Worldwide sales of wafer-steppers – also called silicon lithography machines – last year came to nearly $6bn. The machines radiate ultraviolet light through a lens system and photographic mask. The light rays print (using a photoresist) complicated patterns on to silicon wafers in which the lines are about 0.15 micrometres thick. The lines define the positions of transistors – of which tens of millions, assuming the lithographic patterns are fine enough, can be positioned through manufacturing steps on to a thumbnail-sized chip. Because the accuracy and operating efficiency of wafer-steppers are vital to microchip production, the companies that make them influence the global $1,500bn-a-year electronics business. Wafer-stepper manufacture is dominated by four companies, accounting for more than 95 per cent of world sales. With a market share estimated at 34 per cent, ASM is number two behind Nikon of Japan, with 37 per cent. But through the deal announced last October to buy Silicon Valley Group – now in number four position – ASM is due to become the world leader, with a share of more than 40 per cent, roughly twice as much as Canon of Japan. The deal is being delayed by an investigation into whether US national security would be endangered by allowing foreign control of Tinsley, a small subsidiary of Silicon Valley Group. As well as making lenses for lithography applications, Tinsley produces optical systems for surveillance satellites, including those operated by the US Defense Department. The results of the inquiry are expected in late April or early May (2001). Assuming the deal goes through – and ASM is hopeful, saying it is ready to guarantee to the US government that the availability of Tinsley’s technology will not be compromised – ASM hopes it can build on its position to take more than 50 per cent of the world market within a few years. The company remains confident about the longer-term prospects, in spite of warnings in March that profits would be hit this year by the expected slowdown in investment in the $200bn-a-year microchip industry. ASM’S DEVELOPMENT ASM’s strong run started only relatively recently. Formed in 1984 as a unit of Philips, the Dutch electronics company, it was spun out as a quoted company in 1995. Since then, revenues have risen fivefold to £2.2bn (£1.35bn) last year – with sales outside the Netherlands accounting for 85 per cent of itsrevenues. The company has more than doubled its market share in wafer-steppers since the early 1990s, when its US and Japanese competitors were in the ascendancy. ASM’s story underlines that in high technology, early movers do not necessarily end up strongest. Microchip lithography was invented by Perkin-Elmer, a US instrumentation business, which brought out its first machine in 1973. The machines defined lines 4 micrometres thick, making their resolving power roughly one-twenty-fifth of today’s systems. In the mid-1980s, GCA, a US company, was dominant in wafer-steppers, having entered the business in 1976. But both companies lost their lead in the 1990s to Nikon (which introduced its first machine in 1980) and Canon. A key to this was that the Japanese companies offered superior lens systems to the US competitors (both of which later quit the

Managerial Accounting 547 – Case Studies 2013

4

wafer-stepper business). Both Nikon and Canon had in-house optics technologies, developed as a result of their respective backgrounds in cameras and office equipment. It is in this context that the ASM/Zeiss partnership, which started in the late 1980s, has been vital. The durability of this partnership – and the world-class optics technology that Zeiss provides – has been crucial to ASM’s success. Zeiss, whose centre for semiconductor optics technology is at its headquarters in Oberkochen, a small town near Stuttgart, employs several hundred people who work solely for ASM. They make lens stacks: 1-metre-tall systems of up to 30 lenses, each ground, sometimes with ion beams, to immense accuracy. The lens stacks are at the heart of each wafer-stepper, making sure the radiation is directed on to the wafers with the required precision. The nature of the link with Zeiss has caused some heart-searching at ASM. Mr Dunn, an Englishman who took the top job at ASM in January 2000 after a career in the electronics industry with Plessey, Motorola and Philips, says it is ‘risky’ to have just one supplier for such a critical sub-component – ‘but we don’t have any other choice’. Such is the rarefied nature of this technology, Mr Dunn explains, that it would be virtually impossible to have a back-up supplier that could provide the same quality as Zeiss. Also, by guaranteeing to Zeiss that it will buy lenses from no one else, ASM has made the importance of the link transparent, which Mr Dunn thinks spurs the German company to greater effort on its behalf. ‘We fight a lot but underneath we have a good relationship’, he says. ASM has three other critical partnerships, as a result of which, under its brain-box strategy, it can divert most of its energies into machine development, marketing and building up links with customers, leaving in-depth technical know-how in the area of precision mechanics, metrology and light sources to others. Of ASM’s 4,300 employees (a figure that has increased by 2,000 in the past two years and of which 1,000 are based outside the Netherlands), nearly one in three works in research and development – a field that accounted for 10.8 per cent of sales last year. A similar number is in marketing or customer support, liaising with the big semiconductor companies that are the company’s customers. Only about 800 work in manufacturing – and of these only half are traditional manufacturing and assembly workers, with the rest involved in buying subcomponents or organising shipments of finished goods. ASM’S FUTURE CHALLENGES Mr Dunn says that one of his biggest challenges is to make sure that the spirit of the company – where the average age is only 32 – is kept at the same high pitch as during these years of rapid high growth. Meanwhile, he says that – assuming his US deal is approved and he is left, in effect, with just two competitors – he cannot afford to relax. He says: ‘Every day when I wake up I am paranoid about what the Japanese are doing.’ The next few years, Mr Dunn intimates, are unlikely to be easy for ASM – even if its record in building up a rare European strength in high technology is second to none.

Managerial Accounting 547 – Case Studies 2013

5

Glamour Plastics Glamour Plastics Pty Ltd manufactures plastic kitchenware at its Castle Hill factory. Its manufacturing equipment consists of large plastic extrusion machines that were purchased 15 years ago. Glamour Plastics produces in small production runs, and although the machine is old, it is reliable. The company’s products are much sought after by specialty gift stores and up-market department stores such as David Jones. It also sells its products to Saks of Fifth Avenue in New York. While Glamour Plastics has many products, among the most popular is the Puchi salad bowl and servers. This product is made of clear plastic with gold specks, and competes very favourably with the latest Italian salad bowls. Glamour Plastics has just begun its first benchmarking activity. It has subscribed to an international benchmarking group that provides benchmarking data specifically tailored to different industries. The benchmarking data supplied by the agency, relating to the plastics industry, include product cost per kilogram of finished product; cycle time; reject rate; and direct labour and raw material costs per kilogram of product. The manufacturing manager, Pascale Grinwald, suspects that the benchmark data must relate to the famous Speedy Plastics, renowned as the world’s best plastics manufacturer. This company is a mass-producer of multi-coloured lunch boxes and picnic cutlery, and uses high-speed, computer-controlled plastic extrusion machines. The management accountant of Glamour Plastics, Bruce Hogan, has prepared a report comparing the performance of Glamour Plastics with the benchmark data:

Pascale is concerned about the size of some of the performance gaps between Glamour Plastics’ measures and best practice, and has asked Bruce to investigate.

Performance measure Glamour Plastics Benchmark data

Product cost per kilogram of product $85 $66

Direct labour per kilogram of product $20 $10

Raw material cost per kilogram of product $45 $10

Cycle time per 100 units 60 minutes 15 minutes

Reject rate 2% 3%

Managerial Accounting 547 – Case Studies 2013

6

Topps International Ltd

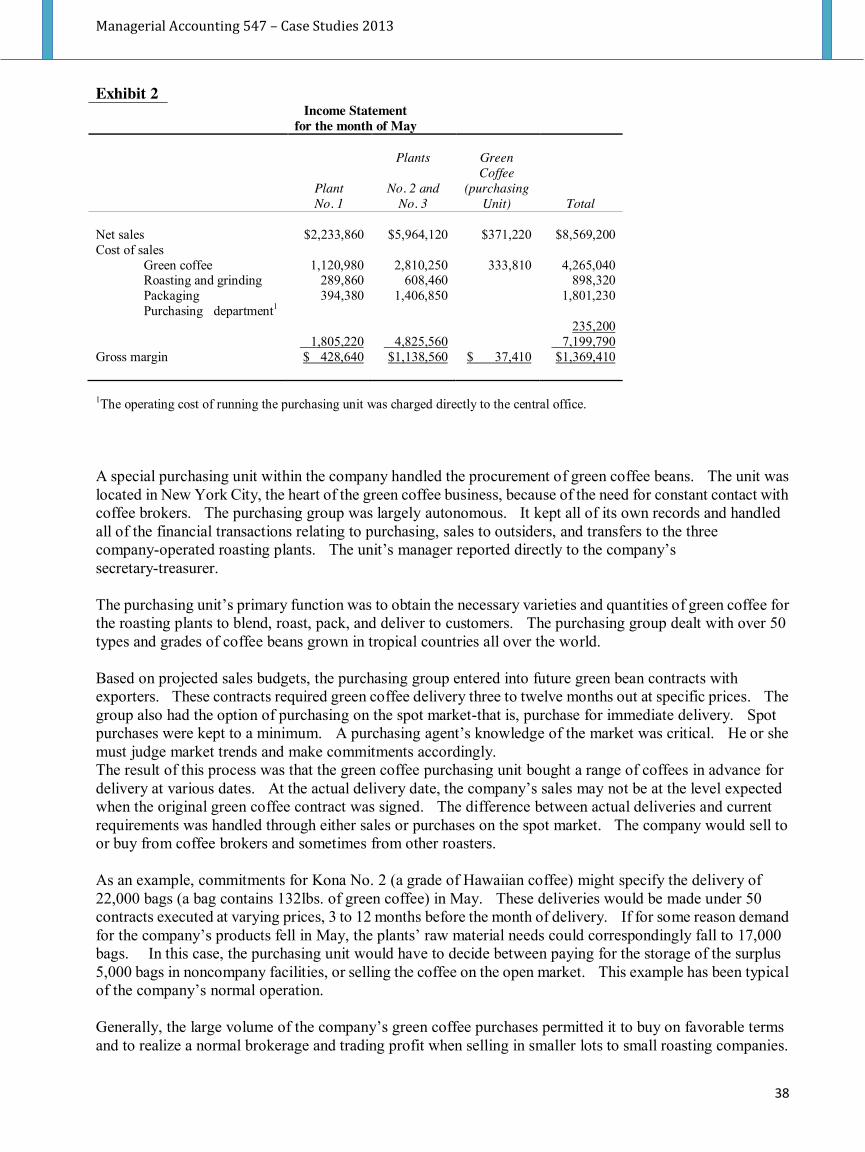

TOPPS INTERNATIONAL LTD, 1995 Topps International Ltd has been operating since 1977 and is a subsidiary of a US-owned multinational company, the Topps Company Inc. Topps is an international marketer of entertainment products – principally collectable trading cards, confectionery, and sticker and album collections – and was founded in 1938. Topps created Bazooka bubblegum in 1947 and marketed the first baseball cards in 1951. Nowadays, Topps is a major player in the children’s entertainment business on the European market and describes its business as the marketing and distribution of fashion items for the children’s market. Hence, Topps is not a typical manufacturing company. Some of the most famous products on which Topps success has been built, the Bazooka chewing gums and the Push-Pops lollipops, have now become household names. Topps has also become famous for adding an entertainment component to its confectionery products in the shape of ‘Casper the friendly ghost’ toy containers, containing gum or sweets. Recently, Topps has been particularly successful with its purchase of the rights to make Pokémon-branded products, including the sale of stickers and albums. The emphasis of its business has changed substantially over the years from a heavily manufacturing perspective to an approach based more on the trade of goods imported from the Far East. By 1995, 20 per cent of its products were manufactured locally, the remainder being imported from China, Thailand and other countries. This represented a significant shift from the position even five years earlier when less than 20 per cent of products were imported. This switch in business emphasis allowed sales growth to mushroom with corresponding increases in the import/export activities. The product life cycle of some of the products was extremely short so the company needed to react quickly to change, emphasising the company’s requirement for accurate information that was readily available. This acceleration of the business flows was aggravated by the rapid development of the new trading element of Topps’ business. Topps products were distributed out of three warehouses – Cork (Ireland), Liverpool (UK) and Rotterdam (Holland). The Cork plant stored the products manufactured in Cork while the Rotterdam depot stored imported products and the Liverpool depot maintained stocks required to serve the UK market. All activities were managed from Cork1

with outside companies providing warehousing and distribution facilities at both external locations. The UK was the biggest market and a team of sales representatives handled sales to multiple stores and wholesalers. Ireland and the rest of Europe were serviced through distributors in each country. Products were sold mainly on a sale or return basis, making it vital that returns were identified quickly and resold within the life cycle where possible. Sales campaigns were not launched simultaneously in all countries and regions so it was often possible to pass unsold products on to another, less saturated market. Identifying the critical success factors for Topps in 1995 Topps’ business success revolved around making correct management decisions quickly. Information technology (IT) supported the vital provision of rapid, accurate information on which to base these decisions. Spreadsheets were used extensively (on a limited number of PCs used in the company) to create mini profit and loss accounts representing scenario analyses on specific markets or for specific products and to identify windows of opportunity aimed at maximising the rotation of stock. The main business tools centred on the strategic plan and operational budgets derived therefrom which were based on a number of spreadsheet models developed in a PC-based software package. The majority of information was gathered manually and the non-strategic data processing services (payroll, invoicing, inventory control, and other nonstrategic transactions processing systems) were provided by software supplied by an external supplier. Both the software and the computer used to run it were completely obsolete – Topps was the final customer using these services, which were becoming increasingly expensive and unreliable. Management at Topps had repeatedly complained to its parent company about the failure of their largely manual systems, but each time clearance to purchase a new system was requested, it was refused by headquarters (in New York). Topps’ management realised that too much replication and duplication was taking place and that a fully integrated financial, manufacturing and distribution system was required to both:

support the basic business processes, and automate basic flows of information.

A more reliable information basis was required to speed up the reporting processes across the organisation. A need for the capability of downloading all required information from a central system into existing information systems was 1 While three separate locations existed, all activities were processed through the Cork offices.

Managerial Accounting 547 – Case Studies 2013

7

identified to improve and make the production of crucial management reports more reliable. Such an approach would require the implementation of a network of PCs to enable data collection and screen enquiries throughout the different business functions (new hardware), selection and implementation of appropriate financial, distribution and manufacturing modules (new software), and staff training. In March 1995, Topps International Ltd again attempted to purchase such an integrated software package that would cover the financial, distribution and manufacturing aspects of their business. The business was growing rapidly across all European markets and it was also looking to expand into a number of South American countries. It had been mainly a manufacturing organisation, but 75 per cent of its turnover was now coming from trading in goods produced by Far East suppliers. The most significant problem for Topps was identified as the lack of online stock control for key personnel as the basic computerised stock system used tracked only goods manufactured and stored in Cork. There were also occasional failures to meet shipping deadlines because of paperwork delays. The robustness of the cash flow was compromised by the lack of control of debtors’ balances and invoice due dates. In addition, there were also problems with reporting to the US headquarters due to the unavailability of information on territory and product profitability. Compliance with requirements for regular monthly and quarterly reports on EU movements of goods was slow. As described by the then financial controller, the company was vulnerable in the shipping, credit-control and treasury departments. He concluded that too much information was contained in employees’ heads rather than in the company’s information systems. Reports that were written at this time pointed out that hiring extra staff would not solve these problems and that the availability of a fully integrated system of the enterprise resource planning type would be required (see, for example, the Consultants’ Report in the Appendix). In addition to this operational data layer, a powerful report generation application would also be required to generate better quality managerial reporting. At the time, a number of potential failures were threatening:

Sales order processing required attention as it was feared that Topps might begin to lose a significant portion of the ever-growing business due to orders not being met on time or not being processed at all.

Invoicing is always a crucial element of a business, but Topps’ management sometimes had no clear idea how much had been shipped to a particular customer. In fact, some shipping deadlines were not met due to paperwork delays.

Convincing HQ Over twenty months of time and effort (in tendering, and development) was involved in the process that culminated in the selection of the required ERP system and the local software vendor who was to supply it. Consultants had argued that local support would be a significant asset during the implementation phase as people in Topps had little experience with large computer systems (there were no full-time IT personnel in Topps at the time). The next step in the process was to commit the money to this investment of roughly £180,000 and the signs were good when the IT director at HQ responded favourably to the request and agreed with the conclusions of the final report he had been sent. Topps’ parent company then purchased Merlin Publishing, a UK-based company similar in size to Topps but operating in the complementary children’s entertainment market (e.g. the production of stickers of players in the English premiership and other major European soccer leagues). Due to uncertainties regarding the sharing of business between Topps and Merlin and the relations to be developed between the two companies, HQ decided, again, to block the ERP investment in Topps. Following a number of meetings with equivalent personnel in Merlin, a new strand of reports was sent to HQ to indicate how the systems in both Topps and Merlin could operate and the processes that could be shared between the two companies. A joint report signed by Topps and Merlin was even sent to the US to emphasise the support that Merlin were ready to give Topps in its implementation of the system selected. A further series of negotiations took place but the project was put on hold while a global IT strategy for Topps was developed by the IT director at HQ. More than two years after the first reports had been written and sent to the US about the weaknesses of the systems in Topps, nothing had been done and the manual systems were still holding on. A computerised system for Topps International had never seemed so far away. In a final attempt to demonstrate that there were no managerial grounds for postponing the commitment of Topps to the purchase of a system (software and hardware) another report was sent to HQ. The report emphasised that a global IT strategy for the company made little sense as no truly shared processes requiring integration of computer systems had been identified either between Ireland and the US or between Topps and Merlin (the computing cultures differed significantly as Merlin had full-time IT personnel and a networked IT infrastructure with its international subsidiaries; no such common processes existed between Merlin and Topps – no consolidation of financial information was required;;

Managerial Accounting 547 – Case Studies 2013

8

finally, using a UK-based supplier of software services would lead to significant cost increases in IT provision). Compatibility of each organisation’s systems would, however, be required to enable the smooth exchange of information, and for example, reports on the performance of various Topps and Merlin products. In addition, the implementation of a global strategy meant that Topps would have to sacrifice the possibility of using local support for the software, an added – and potentially very costly – difficulty for a company without full-time resident IT expertise. This report was to change the minds of managers in the parent company. In mid-December 1995, news from HQ indicated that management should start implementing the decision to purchase an integrated computer system covering the financial and distribution activities. Before the end of January, the cabling had been put in place and system installation began in earnest. ERP teething troubles following implementation Management at Topps found that committing to a solution was not the only important aspect of the decision making in relation to deciding to implement its ERP system. Actual implementation involved enacting the choices made on the basis of management expertise and consultants’ advice, and raised new issues and fresh questions which were overlooked or ignored throughout the previous stages. Such difficulties have frequently been reported in the management of ERP projects around the world. More specifically, there were problems with the support provided by the system for the manufacturing operations of Topps’ business. ERP systems are an extension of the materials requirement planning (MRP) systems of the 1970s and most of them are based on some MRP logic. This means that companies should have an MRP-organised factory before they can implement an ERP system that also supports their manufacturing. At the time, Topps had reduced its manufacturing to a small number of products (most originating in the Far East) but the factory floor had never been MRP-oriented. In fact, there had never been any just-in-time requirement in the factory and it was not known how useful it would be to switch to MRP at that stage. This issue was increasingly relevant as the manufacturing operations of Topps’ activities were being phased out. As a result, ‘workarounds’ had to be implemented at the interface between the ERP and the manufacturing activities. Workarounds were portions of business processes that had to be ‘invented’ in the computer system and in reality to ensure that the ERP software could be used even though it did not exactly match the way activities were carried out. Developing the workarounds was not likely to compromise the success of the ERP implementation because the products being made in the factory represented a very small fraction of Topps’ turnover but it did take some time that had not been planned for. There were also problems with the lack of familiarity of Topps’ staff with the software. Such problems are very common with enterprise-wide software such as ERP and most companies who implement them find themselves on a steep learning curve from the moment their new system goes live. No amount of training is ever going to provide staff with the confidence needed to use their ERP to its full extent from the outset. Thus, even though training was quite extensive, it took a while before staff became accustomed to the new ways of doing business through the ERP system. Topps’ business, like any other, includes a certain level of idiosyncrasy and, in the ERP area, software providers can never become so familiar with a company that they would be able to anticipate every detail of the business processes. Some are replaced by new processes suggested by the package, but some remain and require workarounds that take a while to establish and to integrate into day-to-day routines. After a few weeks, staff became more comfortable with their systems, and after a few months, they became true experts at exploiting the functionality of their ERP software to develop Topps’ business. Another problem that arose was that of data migration, which is also common with ERP systems. ERP systems are organised around very large databases that contain all the data required for the systems to operate properly and to link up with other information systems the company may have decided to keep. These data must often be uploaded from previous systems (which is referred to as migration). This applies to the more stable data a business uses, such as bills of material (describing the recipe of the company’s products), customer data, but also some much needed transactional information such as invoicing data, sales data and any other accounting-based data. In the case of Topps, the previous system was an obsolete integrated package running on an even more archaic computer. The data proved difficult to extract on account of the lack of flexibility of the old system. Also, the data did not always have the proper level of detail, as modern ERP systems offer far greater depths of information and far more schemes to classify and organise data. Thus, a substantial amount of manual data entry was originally required before the system could go live. After a few months, however, it became clear to the managers in Topps that their ERP system was a sound investment and that the benefits obtained in terms of inventory management and acceleration of business processes would far outweigh these initial teething problems.

Managerial Accounting 547 – Case Studies 2013

9

Using the ERP system – January 2001 According to the financial controller in 2001, the ERP project had been very useful and positive from the first year of its implementation and Topps had progressed in leaps and bounds in terms of its information systems. Before the implementation of the ERP system, production of the complete month’s end results took two weeks and even then did not allow managers to drill down into products, geographical areas and activities with any flexibility. This time had been halved after the implementation of the ERP system and the system also enabled managers to investigate sales figures to a much greater level of detail, drilling down into each market and each product far more accurately than ever before. The main strength of the ERP system was that it provided managers with the full set of live data regarding the inventory and shipment elements of the business, whereas managers used to rely on suppliers to establish accurate quantities shipped. The sales function, by contrast, was not improved to the same exent, but the purchase of an additional software package (called Adaytum™) enabled managers to achieve significant improvements in this area. This added flexibility in understanding the business and controlling the flows of goods had been achieved despite enormous growth of sales from IR£20m in 1996 to over IR£50m in 2000. The greatest advantage of the ERP system identified was how it allowed managers to control stocks, sales volumes and quality control in a way that was never possible before. Slow-moving lines were exposed, quality problems could be traced down to specific consignments and first-in first-out stock movements could be strictly enforced. Such was the accuracy of the ERP system that managers in Ireland could tell operators in the Rotterdam warehouse which cases should be shipped first and the exact location (or bin number) where they were located in the warehouse. In practice, however, they did not need to do so because the Rotterdam operators had a separate system which tallied with Topps’ ERP system. A new project is currently under way which will enable staff in the Liverpool and Rotterdam facilities to access Topps’ ERP system remotely through its e-business module so as to increase the integration of the companies and reduce the extent of duplication of work. These represented very significant improvement from a quality control point of view because the appearance of sweets disimproves over time (even though they are extremely slow to perish) and become impossible to sell. Since the implementation of the ERP system, products no longer had to be destroyed on a regular basis. As far as reporting was concerned the ERP package was not initially sufficient to cater for Topps’ needs. Even though all the required information was available, the report generation capabilities of the system were not sufficiently flexible. This problem was solved in 2000 by the purchase of the additional package (Adaytum

TM

) which used the data contained in the ERP system to provide the drill-down and reporting capabilities required by Topps’ managers. Reports could then be produced on every single line or item sold by Topps and customer profitability analyses could be carried out to an extent never possible before. At this point, the ERP system could cater for all the actual orders and the Adaytum software could handle the forecasting and planning of demand. These two key sources of data could then be aggregated to produce the overall plan for the company.

Case Appendix: Topps International Ltd2

CONSULTANTS’ REPORT (1995) Goals of information system implementation for Topps As an introduction, it should be acknowledged that Topps is currently a healthy organisation with a clear management structure and a very good knowledge of its market. This does not mean, however, that the performance of Topps could not be improved significantly. Topps possesses a combination of up-to-date managerial thinking but rather out-dated administration. It is therefore certain that the introduction of state-of-the art computing in Topps could have a significantly positive impact on the performance of the business and create a more reliable administration of the organisation as a whole, especially given the recent increases in the volume of transactions dealt with by Topps International Ltd. Additional benefits arising from such an introduction could include:

an advance towards ISO certification (and the potential resulting benefits);; freeing of manpower for either higher-level analytical tasks or improved customer service; an administrative system less reliant on individuals, thereby providing more permanent and consistent

long-run company operations. Given that Topps’ business success revolves around making correct management decisions quickly, it is important that information technology (IT) is applied more efficiently to provide the rapid, accurate information on which to base these 2

The issues described in this report are expanded in Adam and Doherty, 2000.

Managerial Accounting 547 – Case Studies 2013

10

decisions. This occurs to a degree with the extensive use of spreadsheets but these are not centrally available and sometimes are not preserved for reuse such that substantial duplication of work arises. Reports take more time to produce than they should and the standard of presentation suffers as a result. Time better spent in utilising the information creatively and efficiently to exploit opportunities and be aware of threats is currently spent on gathering basic information. Required systems for Topps As an initial step, the application of a modern software package would substantially improve the quality of managerial reports. However, from the investigations carried out, excessive replication and duplication of work (e.g. data entry) also need to be addressed. A fully integrated financial and distribution system would support both the basic business processes carried out at Topps and automate the basic flows of information within the organisation. All modules of the system need not be implemented simultaneously and a phased approach to implementation should suffice, once commitment to implement all modules in the medium term is established. Enterprise resource planning systems Such a system may be classified as an enterprise resource planning (ERP) system which is an integrated enterprise-wide software package designed to support the key functional areas of the organisation. ERP systems have inherent strengths and weaknesses, and are therefore better suited to certain types of organisations and certain circumstances. Management at Topps should, therefore, understand the inherent trade-offs of an ERP system before they make any decision regarding the potential appropriateness of the ERP concept for their organisation. While many consultants and media reports are prompt to emphasise the benefits of ERP implementations, the key issue resides in understanding the specific needs of an organisation and the business model best suited to its operations. The added difficulty in ERP projects is that few companies, if any, could possibly contemplate developing such vast applications in-house. For the majority of companies, the decision to implement ERP functionalities will mean buying a software package from one of the major suppliers on the ERP market 3 .

The software selection phase is not straightforward and managers must understand what ERP packages are on offer, how they differ, and what is at stake in selecting one ERP over another. Each ERP package uses a business model as an underlying framework and can be quite different relative to competitors’ products in terms of how they operate or the business processes they support. The problem for Topps’ management is that not all business models fit all organisations and the cost of failing to recognise the relationship between the nature of one’s business and the ERP system to be purchased can be very high indeed. Quite literally, selecting the right software package, i.e. the right blueprint for one’s organisation, is a critical failure factor in ERP projects. An analysis of the strengths and weakness of ERP systems can help managers facing such decisions. Strengths and weaknesses of ERP systems The case for ERP systems In many ways ERP systems represent the implementation of a managerial dream of unifying and centralising (or at least under one name) all the information systems required by the firm in one single system. Most notably, ERP systems support the recording of all business transactions from purchase orders to sales orders and the scheduling and monitoring of manufacturing activities. Most ERP systems are based on an inventory control module that records the movements of goods in and out of the company which makes them particularly suited to organisations seeking to rationalise their internal processes and obtain higher performance from their operations. ERP systems provide employees within organisations with a common language and a common pool of data. At a practical level, ERP systems have very beneficial effects that remove the need for often disparate and unreliable end-user applications, operating and reporting procedures can be standardised and some of the key processes of the firm (e.g. order acquisition and processing or inventory control) can be optimised. In addition, these systems offer high levels of portability and reasonable flexibility in adapting to the requirements of specific organisations. One of the key strengths of ERP systems is that they are built on top of a relational database4

which enables a reliable and rapid circulation of the data between the modules and eliminates the need for multiple data entry. Thus, ERP systems simplify, accelerate and automate much of the data transfers that must take place in organisations to guarantee the proper execution of operational tasks. The relational database underlying an ERP can be quite large, depending on

3 For example, SAP, Baan, JD Edwards, Peoplesoft, Oracle or MFG/PRO. 4 A relational database is a collection of items organised as a set of formally described tables from which data can be accessed or reassembled in many different ways without having to reorganise the database tables.

Managerial Accounting 547 – Case Studies 2013

11

company and operational complexity (some SAP applications implemented are reported to have in excess of one thousand different tables). Currently, the case for ERP systems seems compelling and the development of more powerful and user-friendly platforms makes it now possible to integrate many large systems in a way that was not possible up to very recently. This is clear from the fact that Microsoft spent 10 months and $25m replacing 33 existing systems in 26 sites with ERP systems. Managers in Microsoft claim to save $18m annually as a result and Bill Gates reportedly expressed great satisfaction with the system. Microsoft had reportedly grown so fast that it could not keep up with itself – the number of applications developed to support the company’s operations and their lack of integration meant that information systems staff had lost control over the complexity of the systems they administered. Moving to a single ERP architecture enabled better linkages between business areas as well as with suppliers and customers. The case against ERP systems The strengths of ERP packages are matched by the high level of risk associated with ERP projects. ERP projects are complex and require the reliance on many different types of expertise often sourced outside the organisation. Consultants often advise managers to undertake some degree of re-engineering of key processes before acquiring ERP systems and this adds to the complexity and political character of the projects. There is empirical evidence of the dangers inherent in such vast projects5.

These difficulties have led to some researchers taking a negative view of ERP systems. Some researchers argue that the current interest in ERP in the business community is justified more by political reasons than by sound managerial reasoning. Relevant surveys show low levels of satisfaction of firms having implemented ERP systems, with 45 per cent of firms perceiving no improvements whatever from implementation and 43 per cent claiming that no cycle reduction had been obtained. The difficulty inherent in ERP implementations is largely due to the fact that organisations implementing them should typically only hold on to 20 per cent of their previous applications. But the extensive replacement of previous systems may be a requirement if the major benefits of ERP implementation – greater integration of functional areas and, in the case of multinational firms, greater co-ordination between entities and between sites – are to be obtained. The consequence of this ‘clean slate’ approach is that organisations find it virtually impossible to revert to their pre-ERP situation and, in any case, their investment either cannot be recouped or generates very low returns. Finally, there is anecdotal evidence that many companies were pushed into ERP projects by the much-publicised fears of what might have happened to legacy systems during the year 2000 change. Conclusions for Topps These arguments paint a very mixed picture of the potential of ERP packages which may be portrayed as silver bullets as often as villains. The message to be taken from the potential strengths and weaknesses of ERP systems for Topps’ management is that they would be well advised to conduct a detailed analysis of proposed benefits and costs of their ERP system prior to going down the implementation road to ensure that the system can appropriately meet the organisational requirements. Of vital importance in this process is the consideration of the business strategy needs of Topps and the specific improvements that an enterprise-wide integrated software package can provide. Articles consulted to support report Adam, F. and Doherty, P. (2000) ‘Do ERP implementations have to be lengthy? Lessons from Irish SMEs’, 5th Conference of the Information and

Management Association, Montpellier, France, November. Bancroft, N. (1996) Implementing SAP/R3: How to introduce a large system into a large organisation, Manning/Prentice Hall, London, UK. Bingi, P., Sharma, M. and Godla, J. (1999) ‘Critical issues affecting an ERP implementation’, Information Systems Management, Summer, 7–14. Forrest, P. (1999) ‘Les ERP à l’épreuve de l’organisation’, Systèmes d’Information et Management, 4(4), 71–90. Kalatoka, R. and Robinson, M. (1999) E-business – Roadmap to success, Addison-Wesley, Reading, MA. Rowe, F. (1999) ‘Cohérence, Intégration informationnelle et changement: esquisse d’un programme de recherche à partir des Progiciels Intégrés

de Gestion’, Systèmes d’Information et Management, 4(4), 3–20. Wood, T. and Caldas, M. (2000) Stripping the ‘big brother’: unveiling the backstage of the ERP fad,

http://www.gv.br/prof_alunos/thomaz/ingles/paper5.htm. White, B., Clark, D. and Ascarely, S. (1997) ‘Program of pain’, Wall Street Journal, 14 March 6.

5 Kalatoka and Robinson (1999) detail the case of Foxmayer which went bankrupt in 1996 after three years of unsuccessful implementation of SAP – suing SAP’s US subsidiary and Arthur Andersen in the process. This is illustrative of what can happen to the largest organisations when ERP implementations go wrong.

Managerial Accounting 547 – Case Studies 2013

12

Irish Ports THE INTERNATIONAL TREND TOWARDS PORT REFORM The tendency to reform the operational and institutional structures of ports is a matter of strategic interest within the maritime sector internationally. Ports are critical nodes which facilitate trade flows and, to a lesser extent, tourism flows. In turn, their operational efficiency can have a considerable impact upon the wider economy. Alfred Baird of Napier University in Scotland described the four different models of port administration which are in place variously in different countries and these are shown in Exhibit 1.

Exhibit 1 Four models of port administration

Port functions Models Land ownership Regulation Cargo handling

1. Pure public sector public public public 2. PUBLIC/private public public private 3. PRIVATE/public private public private 4. Pure private sector private private private

As can be seen from Exhibit 1, ports can have any combination of three different functions. Land ownership concerns the physical assets such as vessel berths, terminals, parking areas etc. which comprise the port. Regulation concerns vessel navigation, ensuring compliance with various regulations such as waste disposal and crew safety. Cargo handling concerns the loading and unloading of vessels, storage of freight, provision of value added services, etc. Much debate surrounded the question of what combinations of these functions should be controlled by the state and what combinations should be left to the free market and be controlled by the private sector. STRUCTURE OF THE IRISH MARKET The Republic of Ireland, a member of the European Union (EU) since 1973, is an island country geographically located in the north-west of Europe with a population of some 3.6 million people. The island of Ireland comprises both the Republic of Ireland, established initially as a Free State under a treaty with the United Kingdom in 1922, and Northern Ireland which remains part of the United Kingdom. A feature of the whole island of Ireland is that, since the opening of the Channel Tunnel linking England with Continental Europe, Ireland is now the only EU member country without a landlink to the rest of the EU and is thus totally dependent on both the air and maritime transport modes for external access and egress. In addition, Ireland has both a large economic dependence on external trade and is in a peripheral location vis-à-vis the economic centre of gravity of the EU. Consequently, ports are of special importance to the Irish economy. The Celtic tiger Economic conditions in Ireland in recent years have been so positive that it has been dubbed the ‘Celtic tiger’ (the once-vibrant economies of South East Asia were referred to as ‘tiger’ economies;; the term ‘Celtic’ refers to the earliest immigrants to Ireland, the Celts, who arrived from central Europe in the period up to 150 BC and who fashioned the course of Irish life and culture for the next 1,000 years). This economic success has resulted from growth in both the manufacturing and service sectors and is a consequence of, inter alia, a combination of careful economic planning, investment in infrastructure, high standards of education and, not least, EU grant aid. A member of the EU since 1973, Ireland was one of the first qualifiers for European Monetary Union (EMU) and became a member of the single currency (Irish pound IR£ = a1.27). Over the last decade many multinational companies have located high-tech manufacturing facilities in Ireland. Ireland became an essential node in the global value chains of many of the world’s leading manufacturers. In recent years there has been significant growth, in particular in exports of high-value products such as electronics and pharmaceuticals which are exported to diverse overseas locations. In 1997 exports were valued at ca. IR£35 billion and imports at ca. IR£26 billion, yielding a balance of trade surplus of ca. IR£9 billion. Unemployment has fallen sharply in recent years and now stands at a record low of ca. 6 per cent. Inflation, previously relatively high, has fallen to a low of 2 per cent, although there was some evidence pointing to overheating in the economy leading to potential rises. Lastly, in 1998, gross national product (GNP) stood at IR£46.8 billion (having grown by 50 per cent in real terms since 1993) and gross domestic product (GDP) per capita was US$21,500 (GDP per capita was substantially lower, however, because of profit repatriation by foreign firms and interest payments on the national debt).

Managerial Accounting 547 – Case Studies 2013

13

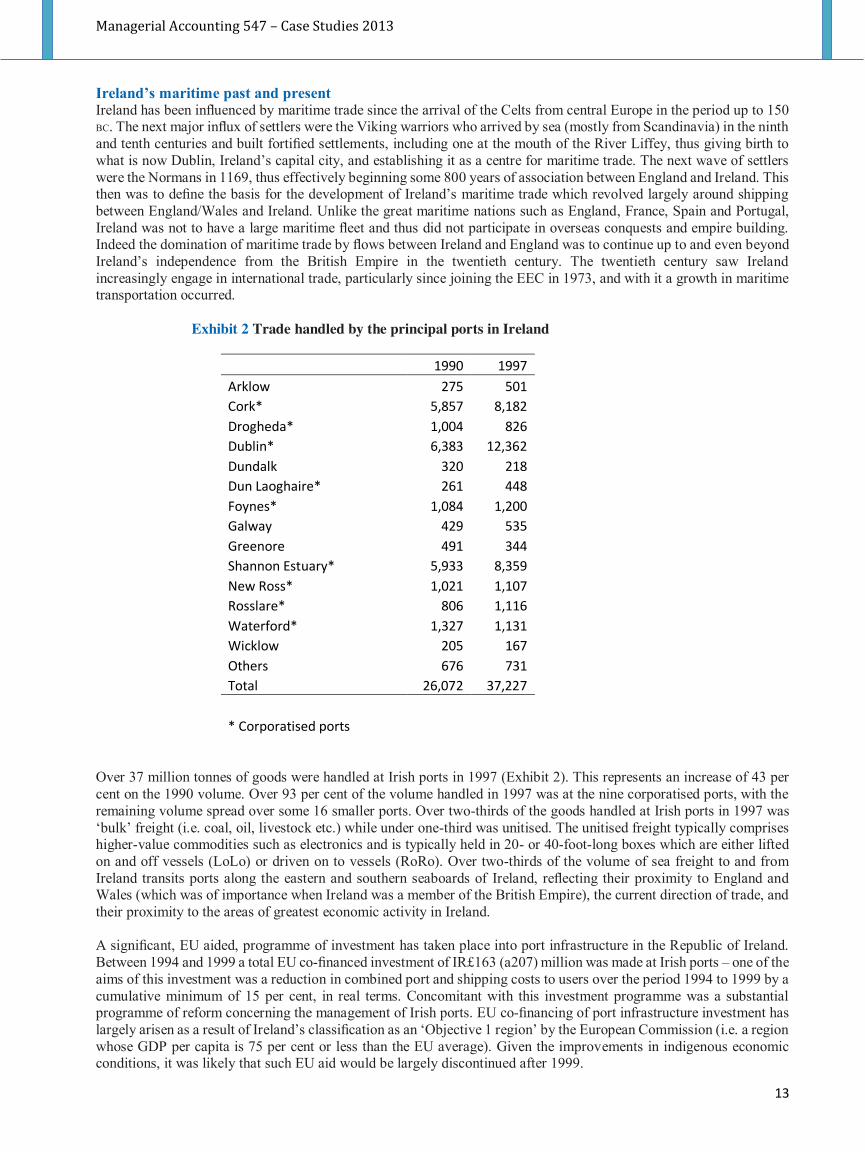

Ireland’s maritime past and present Ireland has been influenced by maritime trade since the arrival of the Celts from central Europe in the period up to 150 BC. The next major influx of settlers were the Viking warriors who arrived by sea (mostly from Scandinavia) in the ninth and tenth centuries and built fortified settlements, including one at the mouth of the River Liffey, thus giving birth to what is now Dublin, Ireland’s capital city, and establishing it as a centre for maritime trade. The next wave of settlers were the Normans in 1169, thus effectively beginning some 800 years of association between England and Ireland. This then was to define the basis for the development of Ireland’s maritime trade which revolved largely around shipping between England/Wales and Ireland. Unlike the great maritime nations such as England, France, Spain and Portugal, Ireland was not to have a large maritime fleet and thus did not participate in overseas conquests and empire building. Indeed the domination of maritime trade by flows between Ireland and England was to continue up to and even beyond Ireland’s independence from the British Empire in the twentieth century. The twentieth century saw Ireland increasingly engage in international trade, particularly since joining the EEC in 1973, and with it a growth in maritime transportation occurred.

Exhibit 2 Trade handled by the principal ports in Ireland

1990 1997 Arklow 275 501 Cork* 5,857 8,182 Drogheda* 1,004 826 Dublin* 6,383 12,362 Dundalk 320 218 Dun Laoghaire* 261 448 Foynes* 1,084 1,200 Galway 429 535 Greenore 491 344 Shannon Estuary* 5,933 8,359 New Ross* 1,021 1,107 Rosslare* 806 1,116 Waterford* 1,327 1,131 Wicklow 205 167 Others 676 731 Total 26,072 37,227 * Corporatised ports

Over 37 million tonnes of goods were handled at Irish ports in 1997 (Exhibit 2). This represents an increase of 43 per cent on the 1990 volume. Over 93 per cent of the volume handled in 1997 was at the nine corporatised ports, with the remaining volume spread over some 16 smaller ports. Over two-thirds of the goods handled at Irish ports in 1997 was ‘bulk’ freight (i.e. coal, oil, livestock etc.) while under one-third was unitised. The unitised freight typically comprises higher-value commodities such as electronics and is typically held in 20- or 40-foot-long boxes which are either lifted on and off vessels (LoLo) or driven on to vessels (RoRo). Over two-thirds of the volume of sea freight to and from Ireland transits ports along the eastern and southern seaboards of Ireland, reflecting their proximity to England and Wales (which was of importance when Ireland was a member of the British Empire), the current direction of trade, and their proximity to the areas of greatest economic activity in Ireland. A significant, EU aided, programme of investment has taken place into port infrastructure in the Republic of Ireland. Between 1994 and 1999 a total EU co-financed investment of IR£163 (a207) million was made at Irish ports – one of the aims of this investment was a reduction in combined port and shipping costs to users over the period 1994 to 1999 by a cumulative minimum of 15 per cent, in real terms. Concomitant with this investment programme was a substantial programme of reform concerning the management of Irish ports. EU co-financing of port infrastructure investment has largely arisen as a result of Ireland’s classification as an ‘Objective 1 region’ by the European Commission (i.e. a region whose GDP per capita is 75 per cent or less than the EU average). Given the improvements in indigenous economic conditions, it was likely that such EU aid would be largely discontinued after 1999.

Managerial Accounting 547 – Case Studies 2013

14

Many of the ferry companies in the Irish market who carry RoRo freight also carry passengers. Between four and five million passengers travel on RoRo ferries between Britain and Ireland each year, while in contrast over eight million travel by air; a relatively small number (approximately three hundred thousand) travel on ferries between Ireland and France. Deregulation in the air transport market has led to considerable growth in this sector and the ferry companies now face stiff competition from the air mode. One major cloud on the horizon of the passenger travel market was the intended abolition of duty-free sales in late June 1999. GOVERNMENT POLICY Together with the investment programme in port infrastructure there has been a substantial programme of reform concerning the management of Irish ports. Irish ports had been governed by relatively old legislation, namely the Harbours Acts 1946–1976. A government-appointed Review Group was established in 1991 to review the policy and legislation governing commercial ports in Ireland. The Review Group was chaired by Patrick Murphy, a highly successful Irish industrialist, and comprised eight other members who represented the various stakeholders’ interests. The Review Group’s report noted that ‘Ireland’s ports have been severely constrained in their ability to respond commercially because of the restricted legislation under which they operate’. Prior ministerial approval was, for example, required for matters such as setting rates and charges, borrowing money, carrying out harbour improvements, and acquiring and disposing of property. The Review Group considered four alternative structures for Irish ports in order to bring about greater commercialisation:

privatisation; amalgamation/regionalisation of ports; a national seaports company, on the model of Aer Rianta (the state-owned company which operated

Ireland’s three main airports);; separate state companies to operate individual ports on a commercial footing (i.e. the state remains the

sole shareholder). The Review Group recommended that commercial state companies should be set up to manage twelve key (in effect the largest) Irish ports. Consequently the Harbours Act 1996 was passed with the purpose of ‘freeing Ireland’s key ports from direct Departmental control and giving them the commercial freedom they need to be able to operate as modern, customer-oriented service industries’. In March 1997 the first eight ports (see Exhibit 3) out of a planned twelve ports were corporatised and vested as commercial harbour companies (previously they were known as harbour authorities). The port of Waterford was subsequently corporatised in January 1999. There were a number of reasons for the delay in corporatising Waterford, which included the port’s largest customer going out of business, storm damage to two cranes (key assets in any ports infrastructure and which are not possible to replace over a short period), and an outstanding loan from the European Investment Bank (EIB). It was intended to corporatise a further three ports (Arklow, Dundalk and Wicklow) but this did not subsequently happen. PROGRESS TO DATE The government department responsible for the ports sector, the Department of the Marine and Natural Resources, was committed to enhancing the effectiveness of Irish maritime transport infrastructure and services, especially in the context of the critical role which maritime transport played in Ireland’s geographically peripheral island economy. The Department in their strategy statement for the period 1998–2000 stressed that sea transport and port services must be efficient, adequate, responsive and competitive. Dr Michael Woods TD, the Minister for Marine and Natural Resources, stated at a national ports conference in late 1998 that ‘freeing up our key ports from direct state control gave them the commercial freedom to operate as modern, customer-oriented service industries, while tightening up accountability for operational and financial procedures’. Dr Woods, a noted scientist and long-serving politician, was regarded by his peers as a hard-working minister (he also served as Minister for the Marine in a previous government) who achieved results, aided and abetted by a new breed of astute and commercially focused civil servants. By mid-1999 the corporatised ports were enjoying significant successes, buoyed up by very healthy domestic economic conditions. Whether these ports would have been as successful had economic conditions not been so good was a moot point. Many of the ports had made strides to becoming much more commercially focused and began to explore other value-adding and non-core commercial activities. Areas of business being developed included the development of marinas, industrial parks, transhipment facilities, car park developments, and the cruise liner business. A number of ports also introduced leading-edge navigation technologies for vessels (VTIMS) using their ports and also introduced quality standards. In addition, the corporatised ports submitted five-year development plans to the Department of the Marine and Natural Resources. Invariably, it would take some time for matters to settle and for the ports to further develop and prosper under their new status.

Managerial Accounting 547 – Case Studies 2013

15

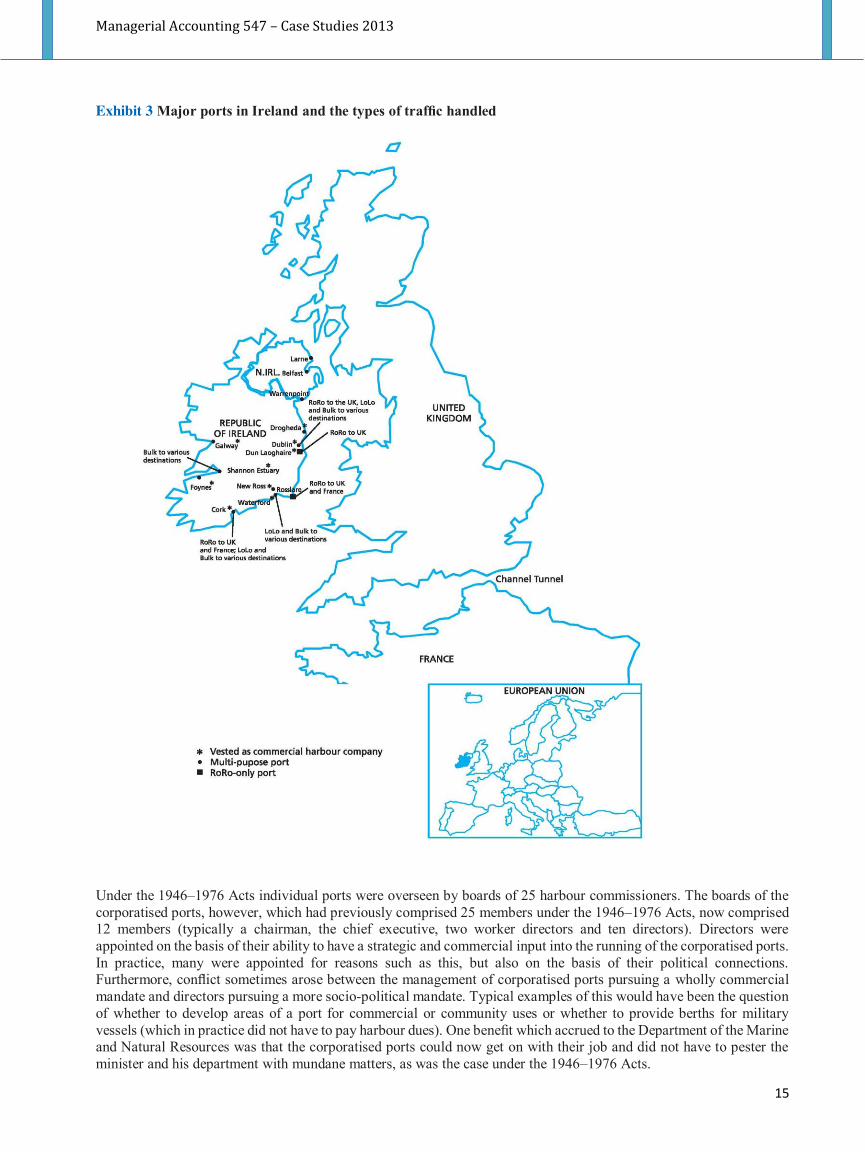

Exhibit 3 Major ports in Ireland and the types of traffic handled

Under the 1946–1976 Acts individual ports were overseen by boards of 25 harbour commissioners. The boards of the corporatised ports, however, which had previously comprised 25 members under the 1946–1976 Acts, now comprised 12 members (typically a chairman, the chief executive, two worker directors and ten directors). Directors were appointed on the basis of their ability to have a strategic and commercial input into the running of the corporatised ports. In practice, many were appointed for reasons such as this, but also on the basis of their political connections. Furthermore, conflict sometimes arose between the management of corporatised ports pursuing a wholly commercial mandate and directors pursuing a more socio-political mandate. Typical examples of this would have been the question of whether to develop areas of a port for commercial or community uses or whether to provide berths for military vessels (which in practice did not have to pay harbour dues). One benefit which accrued to the Department of the Marine and Natural Resources was that the corporatised ports could now get on with their job and did not have to pester the minister and his department with mundane matters, as was the case under the 1946–1976 Acts.

Managerial Accounting 547 – Case Studies 2013

16

The corporatised ports did, however, inherit certain difficulties with their change of status. Many port employees had been guaranteed that there would be no threat to their jobs. Pensions provisions were complex and in some instances lacking. The new corporatised ports had to deal with certain restrictive work practices and other issues such the results of a lack of investment in staff training over previous years. In addition, the corporatised ports were expected to be cognisant of various externalities which might affect the many varied stakeholder groups. Issues which arose here included noise pollution from cargo handling disturbing local communities, marine engineering works affecting aquaculture developments and fishing interests, and the introduction of new services disturbing marine leisure users. Confusion also arose over ownership of the foreshore (i.e. that part of the shore between the high- and low-tide marks) which was governed by very dated legislation, namely the 1933 Foreshore Act. Finally, difficulties with surface transport access (primarily congestion) also affected some ports. ISSUES FOR THE FUTURE It had been intended to corporatise a further three ports (Arklow, Dundalk and Wicklow) but this did not happen. In addition, the question arose in the late 1990s as to what should be done with the thirteen other smaller ports. This combined group of sixteen ports still operated under the rather dated 1946–1976 Harbours Acts. Exhibit 2 illustrated the relatively small volumes handled by these ports. In effect, policy makers had six options, which were not mutually exclusive, to choose from with regard to the future of these ports, namely:

1. Allow the status quo to remain and make small legislative changes as necessary to the 1946–1976 Acts (this would of course involve these ports still being quite dependent upon the Department of the Marine and Natural Resources).

2. Corporatise the ports under the 1996 Harbours Act as was done with the nine larger ports (one pragmatic issue which would have to be addressed was board remuneration: the chairman of a corporatised port received an annual fee of IR£4,000 and each director received IR£2,500; some of the smaller ports had annual revenues below IR£100,000 and could not afford such a structure. It should be noted that fees payable to directors under the 1946–1976 Acts were insignificant in comparison).

3. Transfer ownership of ports to local authorities. 4. Sell ports to the largest customer (in some instances the bulk of the traffic through the smaller ports was derived

from one large customer). 5. Develop the ports jointly with the private sector on a public–private partnership (PPP) basis – there were

precedents elsewhere in Ireland for such an undertaking (e.g. toll roads etc.). 6. Stipulate that mergers or alliances are made between different combinations of ports.

Key aspects of whatever strategy would be chosen included ensuring that public expenditure would be kept to a minimum, and also ensuring that traffic would not merely be displaced from one small port to another, but instead that real growth would occur and would be of benefit to the port hinterland and the wider economy. Furthermore, policy makers also decided that they would review progress under the Harbours Act 1996 with regard to the nine corporatised ports by completing statutory audits on these ports in March 2000. References Baird, A. (1995) Privatisation of trust ports in the UK: review and analysis of the first sales. Transport Policy, 2 (2) 135–143. Mangan, J. and Hannigan, K. (eds), (2000) Logistics and Transport in a Fast Growing Economy, Blackhall Publishing, Dublin. The following websites are recommended for further information concerning the Irish economy: Irish Government (with links to Government departments) www.irlgov.ie Irish Economic and Social Research Institute www.esri.ie Irish Central Statistics Office www.cso.ie Irish Industrial Development Authority www.idaireland.com Economic Review and Outlook 2000, Department of Finance, Dublin, available at www.irlgov.ie/finance/econ2000.pdf The Irish Times (daily newspaper with various links) www.ireland.com

Managerial Accounting 547 – Case Studies 2013

17

The Royal Hotel Introduction It is said that the difference between an Irish summer and Irish winter is that in summer the rain is warm! Recalling this, Pascal Burke smiled as the rain drops gathered on and lazily meandered down the window pane outside. It was mid-afternoon but the dark, heavy rain clouds outside necessitated the use of desk lamps for those working indoors. Pascal had not expected to be at his desk this Friday afternoon. Indeed, Pascal had not expected to be at his desk at this time! He should have been on holiday. He had just finished his MBA degree, as a full-time student and had graduated near the top of his class and had been voted by his fellow students as ‘the person most likely to be famous’. While the award was made slightly tongue in cheek, Pascal, nevertheless, took it seriously. Pascal took most things seriously - especially work. On leaving school, seven years earlier, he studied for and earned a degree in hotel management. His father owned a hotel in a provincial town in Ireland in which Pascal spent most of his school holidays working. He developed a keen interest in the hospitality industry and his decision to study hotel management was a logical progression from his schoolboy times. His studies were a combination of theory and practice and he acquired good experience both within Ireland and Europe. On graduation, he joined the Smith Group which was a family run hotel chain in Ireland. It was a private company, unlike Irish publicly quoted hotel chains of Jurys Hotel Group plc or Ryan Hotels plc. After three years he had progressed as far as he could and felt it was time to broaden his horizons. A full-time MBA offered the greatest challenge and opportunity. After one year of study his perspective had been considerably expanded and changed. He enjoyed his time studying in Dublin and looked forward, after a brief holiday, to a job search in the area of promoting the Irish tourism industry to the European market. However, it was not to be after the recent phone call from his mother ... The scenario A few days earlier his mother had phoned to convey the bad news of his father's heart attack. Thankfully it was not fatal and his father, even at sixty years of age, was expected to make a full recovery in due course. In the meanwhile, the hotel was effectively without a manager, so Pascal promised to return home immediately to try to sort things out. Before he left for home he phoned his girlfriend to apologize for the cancellation of their holiday. It was a ‘special offer’ holiday so he didn't lose too much money - he didn't have much money to lose. The Royal Hotel is situated in a provincial town on the east coast of Ireland, about an hour's drive from the capital city, Dublin. The town is situated in what the tourist brochures describe as ‘the Garden of Ireland’. The hotel is an ideal location for exploring the Dublin/Wicklow mountains. The hotel is only a short distance from the sea although only a few of the town's hardy souls swam during summer months. Rather, walking along the sea front with the invigorating ocean air was the preferred option for many. The town had a population of about 5,000. This population, coupled with a significant hinterland and number of tourists, provided a reasonable trade for the other three hotels in the immediate vicinity. The Royal, like the three other hotels in the locality, is a fifty-bedroom, two-star hotel and can be described as being in the mid-price range. Each guest room is comfortable, includes a telephone and most have a private bathroom. With its traditional Irish pub - named the ‘Lady Gray’ after a rather notorious inhabitant of the town during the previous century - together with the restaurant and function room, the Royal Hotel offers the cost-conscious guest excellent value and good food. Unlike the other hotels, the Royal Hotel was situated in the town. A few years ago, most of its gardens were replaced by tarmac in order to provide ample parking space for its patrons. Thus, its physical scope for expansion was restricted and any proposed developments to the hotel were likely to encounter resistance from local residents and the planning authorities. Some immediate problems and issues currently occupied Pascal's mind. Over the past few days he had introduced himself to employees as the acting General Manager of the hotel. He had also read or at least glanced at all the correspondence and reports on this father’s desk. The one that interested him the most was the summarized management accounts for the year ended 31 October 1996 (Table 1). Although it was only mid-October, Pascal had asked the hotel accountant, Pat Doyle, to prepare them for the past year, including projections for the last weeks in October. Pat Doyle was not a qualified accountant and his role in the hotel was effectively that of bookkeeper. He operated, with a good degree of accuracy, debtors and creditors ledgers, the payroll function, and prepared bank reconciliation statements. He was also responsible for tax compliance of the hotel, mainly the operation of VAT and the deduction of payroll tax under the PAYE system.

Managerial Accounting 547 – Case Studies 2013

18

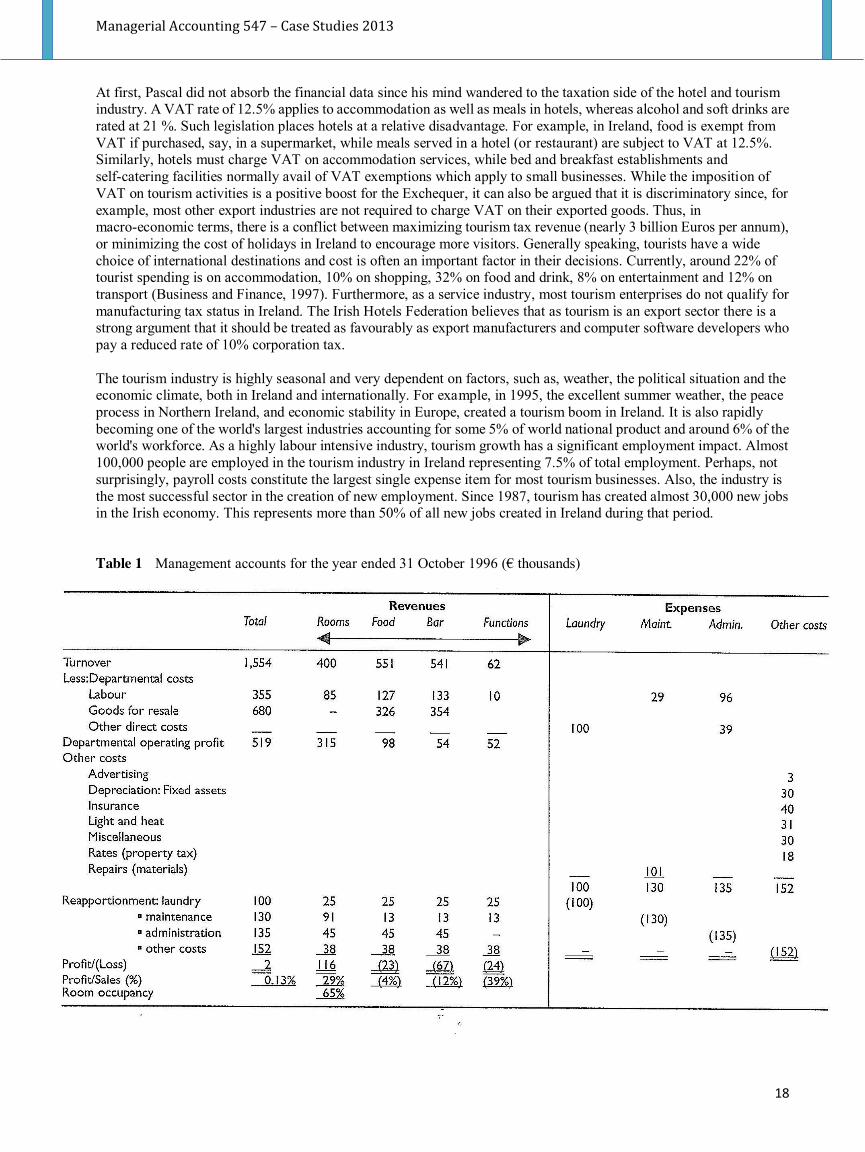

At first, Pascal did not absorb the financial data since his mind wandered to the taxation side of the hotel and tourism industry. A VAT rate of 12.5% applies to accommodation as well as meals in hotels, whereas alcohol and soft drinks are rated at 21 %. Such legislation places hotels at a relative disadvantage. For example, in Ireland, food is exempt from VAT if purchased, say, in a supermarket, while meals served in a hotel (or restaurant) are subject to VAT at 12.5%. Similarly, hotels must charge VAT on accommodation services, while bed and breakfast establishments and self-catering facilities normally avail of VAT exemptions which apply to small businesses. While the imposition of VAT on tourism activities is a positive boost for the Exchequer, it can also be argued that it is discriminatory since, for example, most other export industries are not required to charge VAT on their exported goods. Thus, in macro-economic terms, there is a conflict between maximizing tourism tax revenue (nearly 3 billion Euros per annum), or minimizing the cost of holidays in Ireland to encourage more visitors. Generally speaking, tourists have a wide choice of international destinations and cost is often an important factor in their decisions. Currently, around 22% of tourist spending is on accommodation, 10% on shopping, 32% on food and drink, 8% on entertainment and 12% on transport (Business and Finance, 1997). Furthermore, as a service industry, most tourism enterprises do not qualify for manufacturing tax status in Ireland. The Irish Hotels Federation believes that as tourism is an export sector there is a strong argument that it should be treated as favourably as export manufacturers and computer software developers who pay a reduced rate of 10% corporation tax. The tourism industry is highly seasonal and very dependent on factors, such as, weather, the political situation and the economic climate, both in Ireland and internationally. For example, in 1995, the excellent summer weather, the peace process in Northern Ireland, and economic stability in Europe, created a tourism boom in Ireland. It is also rapidly becoming one of the world's largest industries accounting for some 5% of world national product and around 6% of the world's workforce. As a highly labour intensive industry, tourism growth has a significant employment impact. Almost 100,000 people are employed in the tourism industry in Ireland representing 7.5% of total employment. Perhaps, not surprisingly, payroll costs constitute the largest single expense item for most tourism businesses. Also, the industry is the most successful sector in the creation of new employment. Since 1987, tourism has created almost 30,000 new jobs in the Irish economy. This represents more than 50% of all new jobs created in Ireland during that period. Table 1 Management accounts for the year ended 31 October 1996 (€ thousands)

Managerial Accounting 547 – Case Studies 2013

19

Generally speaking, the current worldwide trend away from sun destinations and towards cultural and activity-based holidays has proved to be very beneficial to the Irish tourism industry. Recognizing this, the National Development Plan 1994-1999, sets three key targets for the tourism sector. It aims to increase foreign tourist revenue by about 1.5 billion Euros, to increase visitor numbers to Ireland by 1.7 million and to create 35,000 new jobs in tourism. Indeed, the Irish Tourism Board (Bord Fáilte, 1994) hoped to attract 4.4 million visitors per annum to Ireland by 1999. The climate for development of the tourism industry in Ireland is ideal at present. For example, government funds are available under the National Development Plan and there have been recent beneficial changes in tax legislation. Tax incentives are particularly important to the hotel and tourism industries, because of low profit margins and volatile earnings. The most pervasive and attractive tax incentives were introduced by the 1995 Finance Act. The government's objective for the scheme is 'to revitalise and update the tourist amenities and facilities in the resort areas designated'. The pilot scheme is exclusively targeting seaside resorts and the scheme has hence become known as the ‘seaside resorts scheme’, but the Finance Act does not refer to the scheme being specifically for seaside resorts. The incentives available for resort areas include (a) accelerated capital allowances, (b) double rent allowances and (c) relief for expenditure on certain rented residential accommodation. In addition, financial support is increasingly available from banks and financial institutions, and the industry itself is experiencing the effects of growing maturity and independence (Ernst and Young/AIB, 1995). However, Pascal realized that the hotel sector is as vulnerable to painful shakeout as any other industry. He remembered that in the US and UK during the 1980s there was a huge increase in the supply of hotel rooms followed by a dramatic contraction in demand. Declining tourism numbers were certainly a factor. In the UK alone, hundreds of hotels became insolvent in the early 1990s. Resale values of hotels collapsed. Pascal's thoughts returned to the summarized management accounts prepared by Pat Doyle (Table 1). Pascal was slightly amused that what were referred to as the ‘management accounts’, were so simple but they made grim and surprising reading. The hotel reported a profit of only 2,000 Euros for the year. Clearly, the overall profitability of the hotel would have to be improved. In his father's temporary absence this would be Pascal's responsibility and he intended to upgrade the hotel to three-star status. However, this aspiration would require significant expenditure to ensure that all guest rooms had a private bathroom with a bath and/or shower. Table d'hôte and a la carte menus would be introduced to provide a high standard of cuisine in relaxed surroundings. In general, the Royal Hotel would need to offer a range of services to satisfy the cost-conscious client. Closing down the hotel for the forthcoming winter season might allow some changes to be made. Another alternative would be to sell the hotel as a going concern. Either way the decision would require clear and unambiguous thinking and this was what Pascal was resolved to do. But, first he had to get a better overall picture of the situation. The management accounts had been prepared to conform with the Uniform System of Accounts for Hotels. The Uniform System originated in the USA and was first published in 1926. It sets out recommendations on how particular transactions should be dealt with in accounting terms. Results of hotels are reported in a particular way, using standard formats, and are therefore comparable with results of other hotels. One of the main principles of the Uniform System is that results are reported by each department of the hotel, in line with the traditional organization structure which is found in most hotel operations. All expenses that are attributable to (and controllable by) a particular department are allocated against the revenue of that department to arrive at a departmental operating profit. The allocation of revenues and costs enables the General Manager to allocate responsibility for results to individual department heads who can directly influence, and be accountable for, the results of their department. For management accounting purposes, the Royal Hotel operated four departments, i.e. Rooms, Food (Restaurant), Bar and a Function Room which generated rental income for weddings, social and other functions, including business meetings. Any revenues generated by such functions from food or bar sales were directly attributed to their respective departments. This function room, tastefully decorated, offers a much-needed facility for local business and commercial clients. It can accommodate up to 200 guests in total. The various cost headings used in the management accounts were relatively straightforward and self-explanatory. The bulk of cost items (excluding the direct costs of the four revenue departments) were charged to one of four cost headings, i.e. Laundry (which was an externally purchased rather than in-house service), Maintenance, Administration and Other Costs. In turn, these costs were reapportioned by Pat Doyle to the four revenue departments as follows:

Cost item Basis ofre-apportiomnent Laundry • Equally to all four departments. Maintenance • Space occupied by four departments i.e. 7/10; 1/10; 1/10; 1/10, Administration • Equally between three departments. Other costs • Equally between four departments.

Managerial Accounting 547 – Case Studies 2013

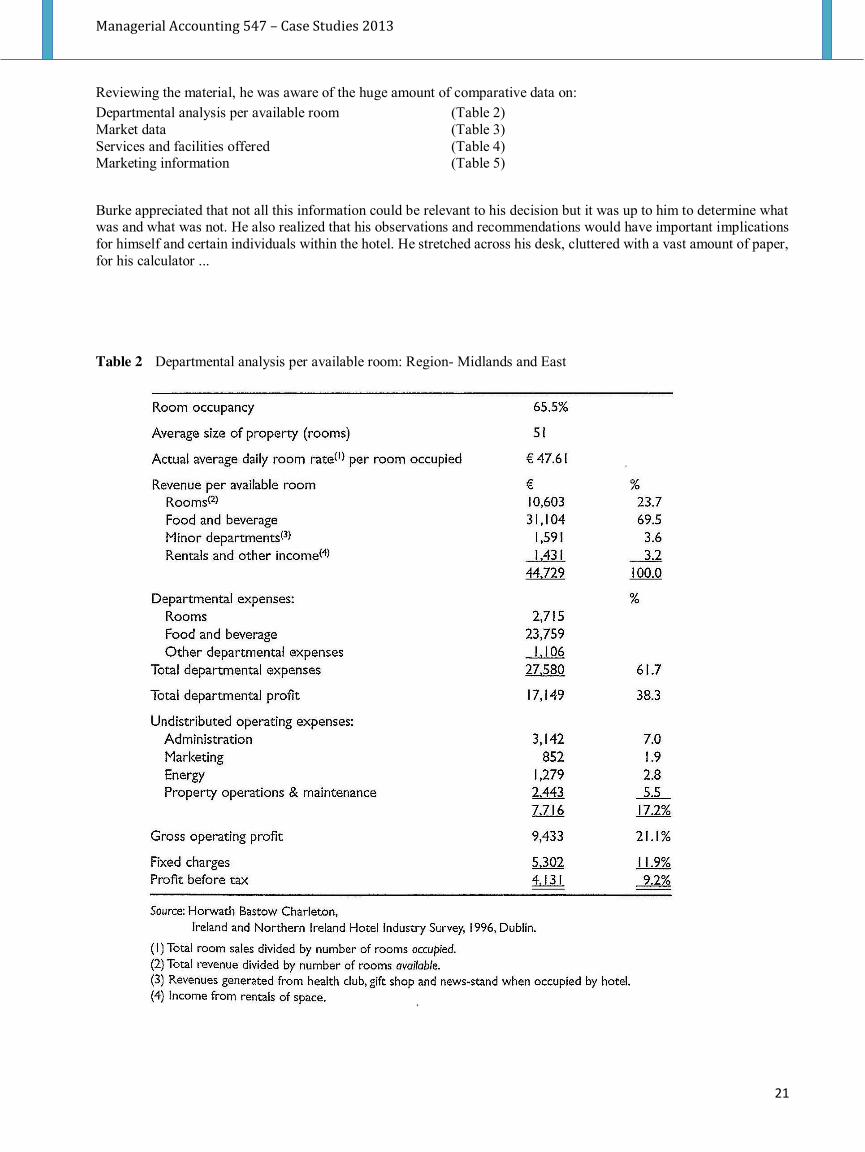

20