Embed Size (px)

Citation preview

*BUSINESS INCOME SECTION 4(a)

HASNANILIZA BINTI SABRI UK24824

AIN NUR ADILAH BT ZAKARIA UK26159NUR SYAIDATUL AMIRAH BT YAHYAUK26458

• Income Statement is prepared in order to assess the financial performance of a business.

• Getting profit or suffering losses does not exclude a business from tax obligation.

• A business may have to pay tax even though they experience financial loss in that financial year.

• The act provides preferential treatment to business income and it is therefore important to understand its scope.

*Introduction

*WHAT is mean by business income?

*Definition-Section 2 of the Act defines ‘business’ to include profession, vocation, and trade and every manufacture, adventure or concern in the nature of trade, but excludes employment. -Under the Act, a taxpayer can have more than one business source within a YA.

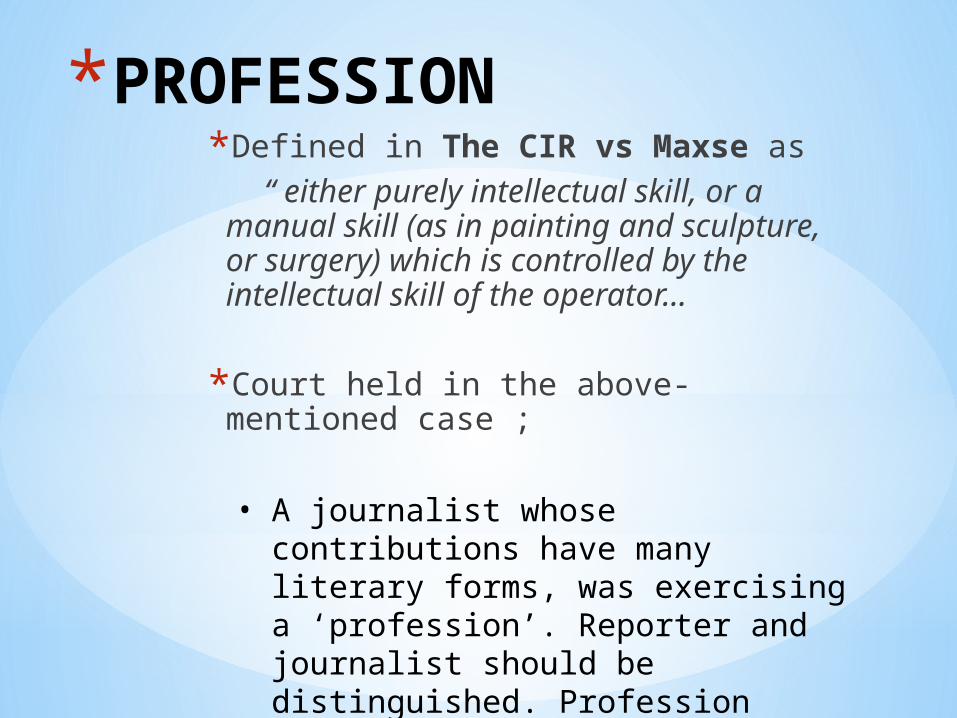

*PROFESSION*Defined in The CIR vs Maxse as “ either purely intellectual skill, or a

manual skill (as in painting and sculpture, or surgery) which is controlled by the intellectual skill of the operator…

*Court held in the above-mentioned case ;

• A journalist whose contributions have many literary forms, was exercising a ‘profession’. Reporter and journalist should be distinguished. Profession (journalist) can be carried out either by a company or an individual.

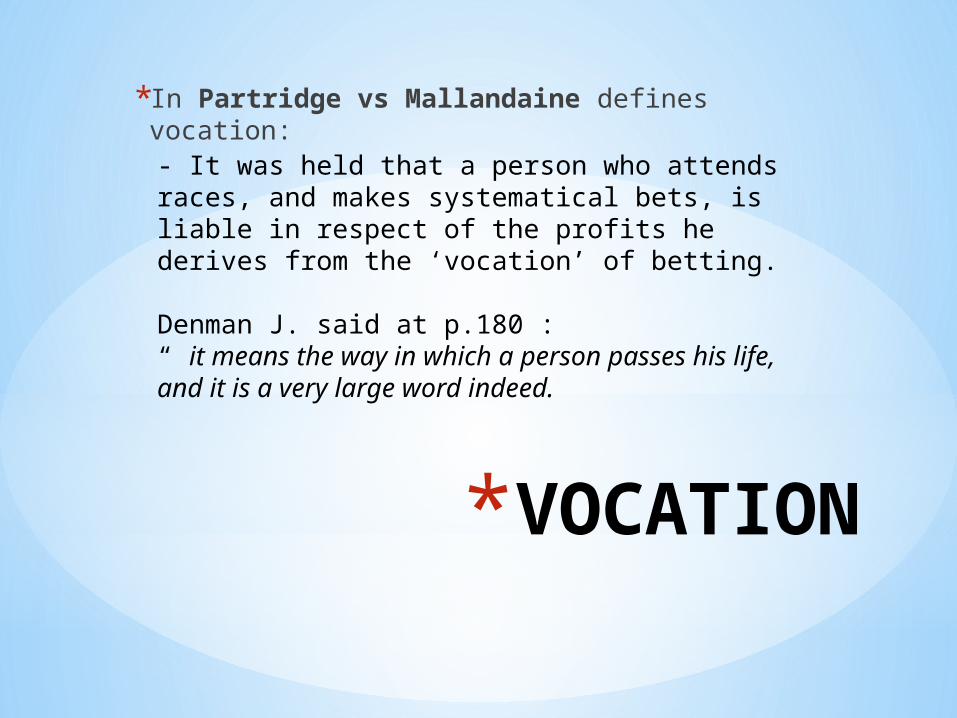

*VOCATION

*In Partridge vs Mallandaine defines vocation:- It was held that a person who attends races, and makes systematical bets, is liable in respect of the profits he derives from the ‘vocation’ of betting.

Denman J. said at p.180 :“ it means the way in which a person passes his life, and it is a very large word indeed.

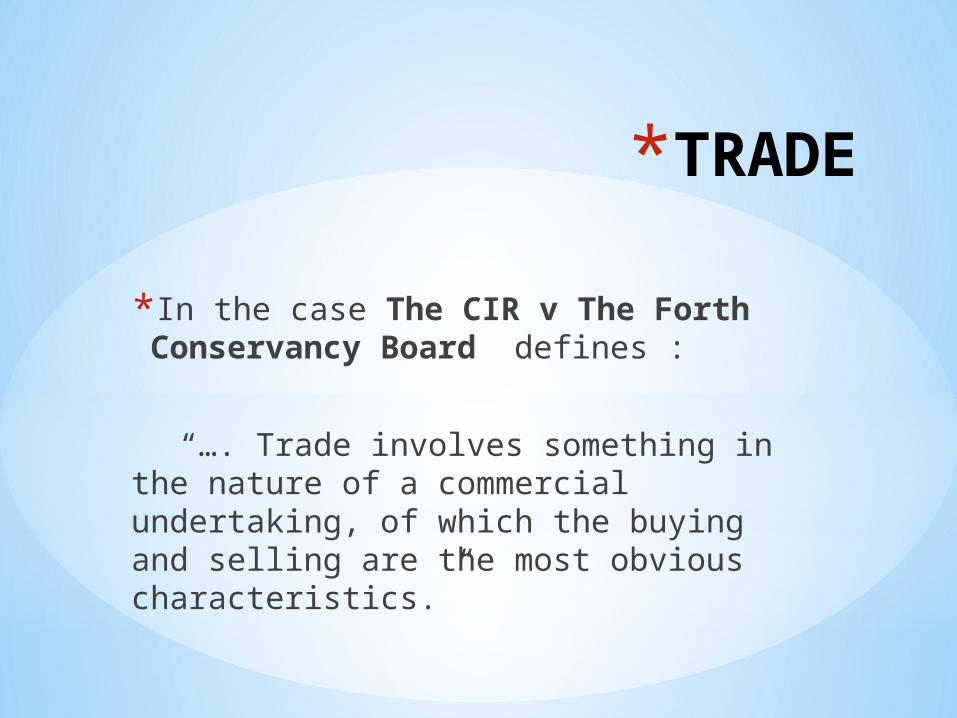

*TRADE*In the case The CIR v The Forth Conservancy Board defines :

“…. Trade involves something in the nature of a commercial undertaking, of which the buying and selling are the most obvious characteristics.”

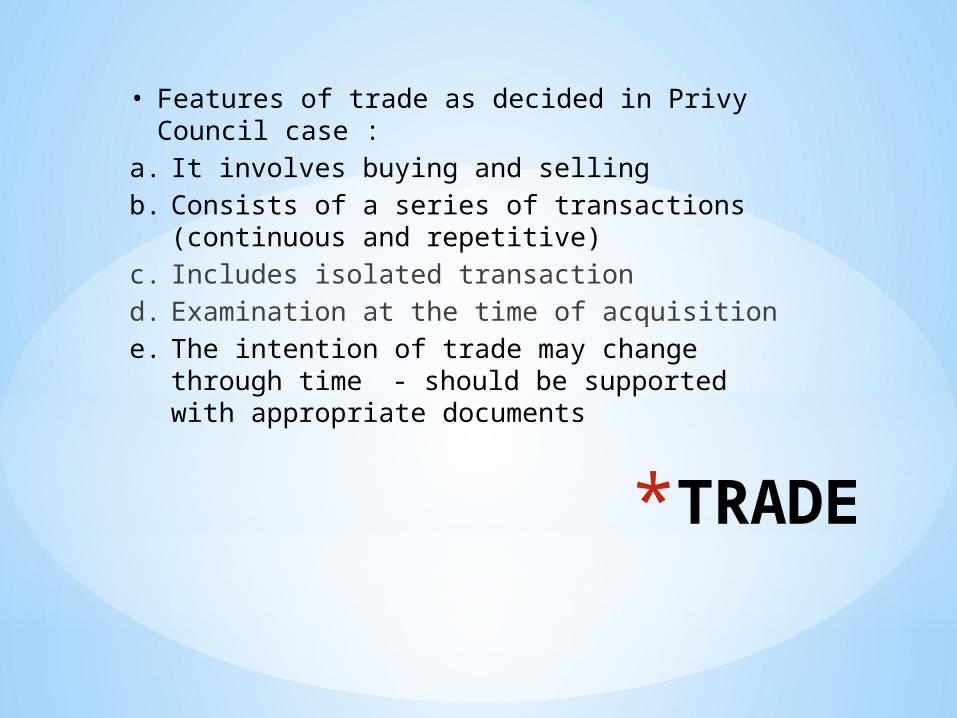

*TRADE

• Features of trade as decided in Privy Council case :

a. It involves buying and sellingb. Consists of a series of transactions

(continuous and repetitive)c. Includes isolated transactiond. Examination at the time of acquisitione. The intention of trade may change

through time - should be supported with appropriate documents

*MANUFACTURE• Explained in Aditya Mills Ltd vs Union of India:

- Manufacture is a process where the original material must undergo a transformation so that a new and different article or product emerges. The new substance or article must have a distinct name, character or use……

*ADVENTURE OR CONCERN IN THE NATURE OF TRADE

*Deals with isolated buying and selling (trade) transactions.*Difficult to hold such transactions as trade activities due to their isolated nature.*However, possible to hold them as an “adventure or concern in the nature of trade” and apply income tax upon them

*ADVENTURE OR CONCERN IN THE NATURE OF TRADE

• A guide to evaluate a transaction is an adventure or concern in the nature of trade

In Leeming vs Jones :

(i)The existence of an organization

(ii) Activities which lead to the maturing of the asset to be sold

(iii) The existence of special skill, opportunities

(iv) The fact that the nature of the asset itself should lend itself to commercial transaction.

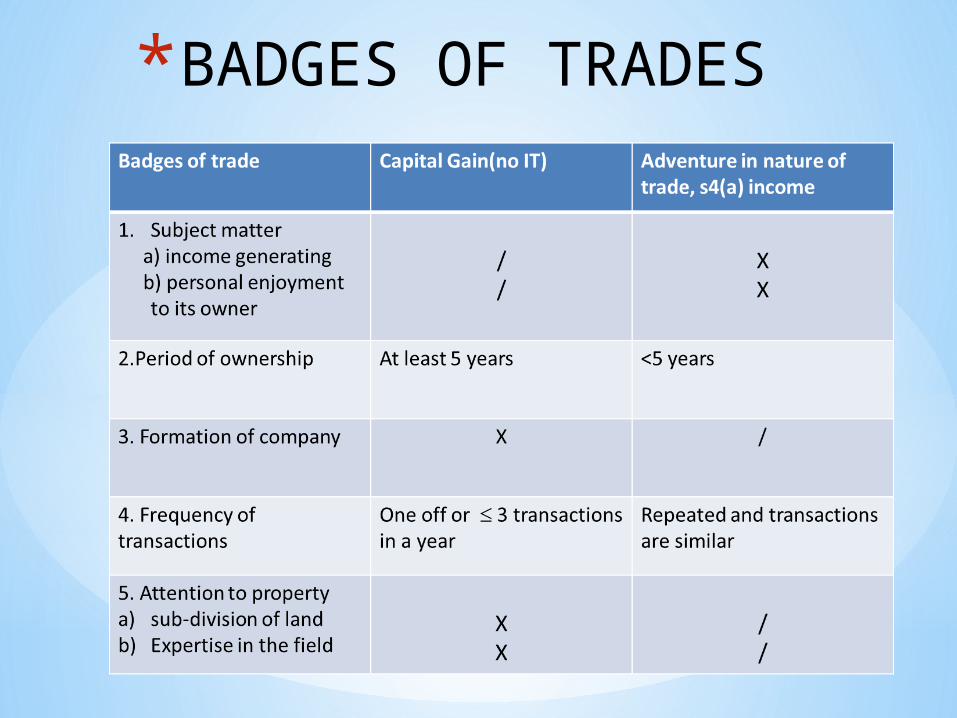

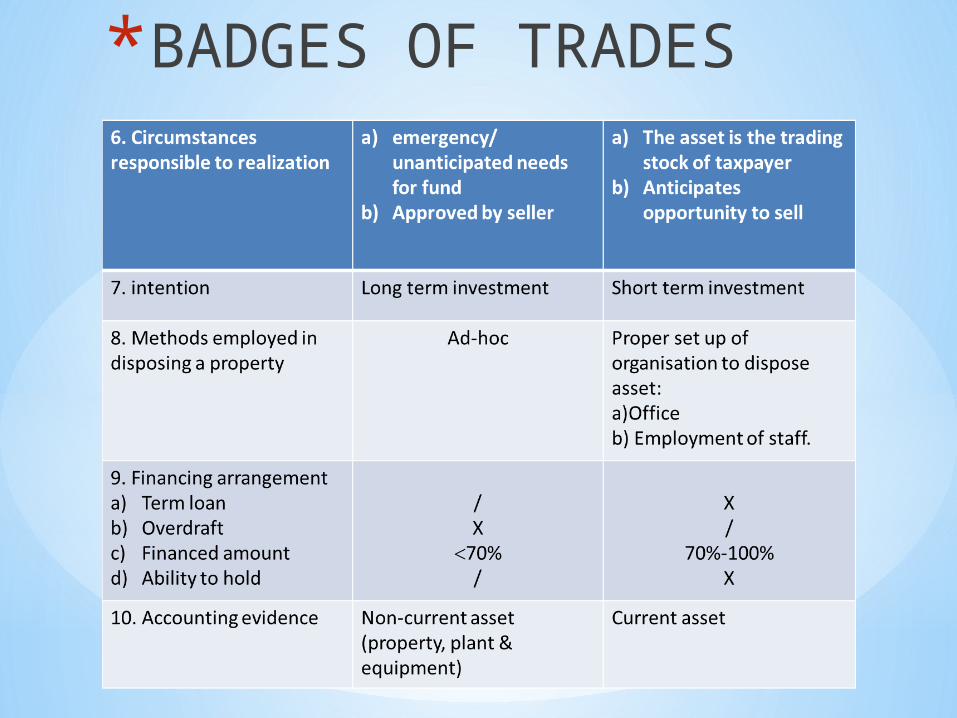

*BADGES OF TRADE• Used as a guide to distinguish gains arising from disposal of an investment and gains from trading or from an adventure or concern in the nature of trade

• Gains from disposal of an investment not taxable

• Gains from trading and an adventure or concern in the nature of trade taxable

*BADGES OF TRADES

*BADGES OF TRADES

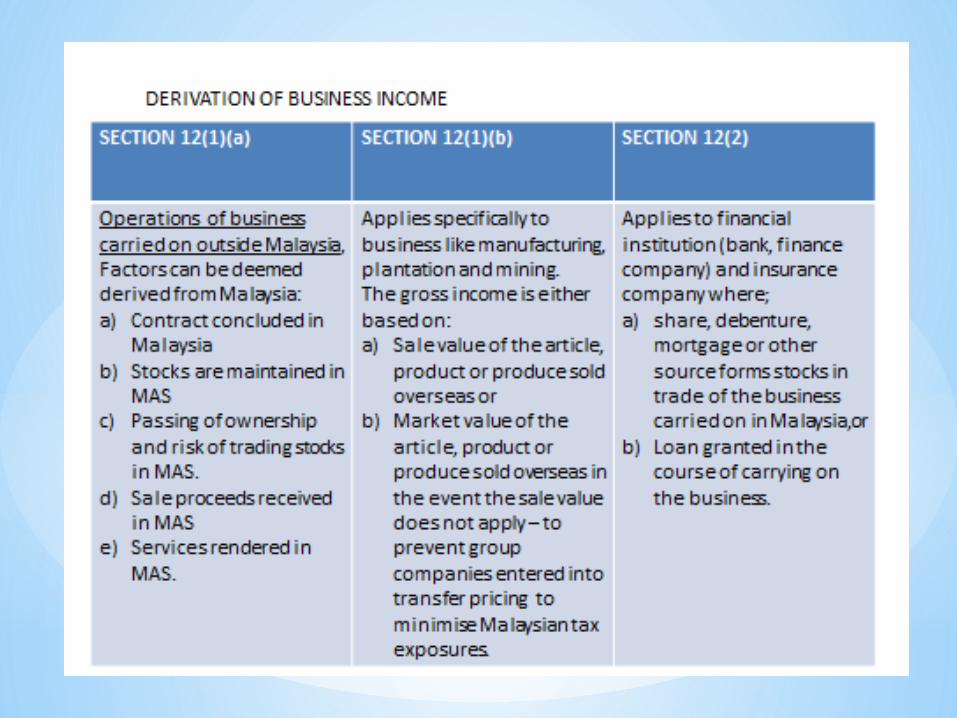

WHEN business income is derived?

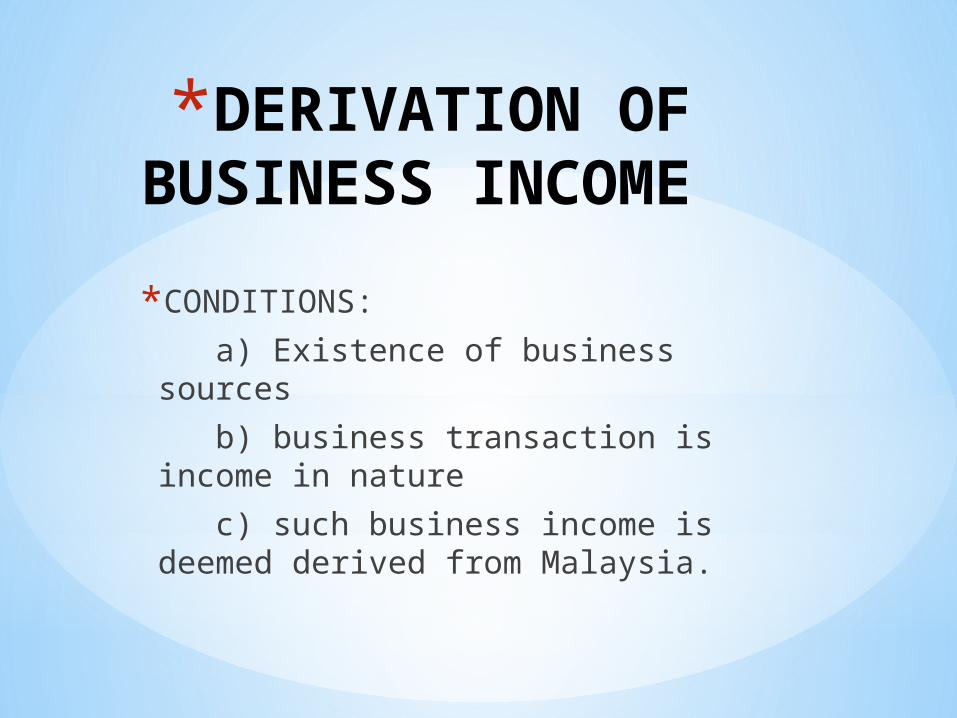

*DERIVATION OF BUSINESS INCOME*CONDITIONS: a) Existence of business sources b) business transaction is income in nature c) such business income is deemed derived from Malaysia.

*cases

*Director-General of Inland Revenue vs Hypergrowth Sdn Bhd (MALAYSIA)*Mount Elizabeth Ltd vs Comptroller of Income Tax (SINGAPORE)

*Director-General of Inland Revenue

vs Hypergrowth Sdn Bhd

The taxpayer (Hypergrowth Sdn Bhd) was a company incorporated under the Companies Act 1965 controlled by an individual who owned 91% of the share capital of the company.

The taxpayer had acquired certain shares in Ngiu Kee Berhad (“Ngiu Kee”) which was subsequently listed on the second board of the then KLSE.

The listing was prompted by the need to raise financing for the expansion of Ngiu Kee.

*One of the taxpayer’s objects that “take, buy or otherwise acquire shares, stocks, debentures or other securities issued by any other company to invest upon or without security and deal with the moneys of the company in such manner as may from time to time be determined and to hold any such shares securities or investments or at any time or times to sell realize and to re-invest the proceeds.” *Subsequently, the taxpayer entered into an agreement for the sale of shares in Ngiu Kee, which was triggered by the sudden and unanticipated deterioration in the local and regional economy.

*The crucial issue for determination before the Special Commissioners of Income Tax (“SCIT”) whether the taxpayer’s purchase of shares and the disposal constituted of an adventure in the nature of trade that bring gains from the sale of shares by incurred charge of income tax.*Or the disposal is a realization of capital asset which not be taxable.

*Decision by Special Commisioners of

Income Tax

*SCIT that the taxpayer’s acquisition of Ngiu Kee’s shares was a long term investment.*Taxpayer not a trader in shares.*The shares were not acquired as part of taxpayer’s trade.*SCIT decide that, the taxpayer’s investment was not an “adventure in the nature of trade” and profit motive seeking is absent.

*Decision by High Court

*Affirmed the SCIT decision.*Conclusion SCIT were right and the taxpayer cannot be disturbed on appeal.

*Mount Elizabeth Ltd vs Comptroller of

Income Tax*The appellant ME developed a block of 59 high-rise apartments of which 51 were sold between 1971 and 1973 and eight of which were retained by ME. *Six of the retained flats were sold in 1980. *On 27 November 1981 the Comptroller of Income Tax (‘the Comptroller’) made an additional assessment for the year of assessment 1981 against ME in respect of the profits derived from the sale of six flats. *ME objected to the additional assessment and appealed to the Income Tax Board of Review (the Board) arguing that the surplus from the sale of the six flats was a capital accretion as ME’s intention from the start was to develop some flats for sale and to retain some flats for investment.

*ME was carrying on two activities: *(a) the principal activity of property development for sale which came to an end in 1973* (b) a subsidiary activity of letting out flats.

*The Comptroller, however, argued that the surplus arising from the sale of the six flats was a trading receipt since ME was carrying on the business of property development, and that the flats were constructed in the course of such business.

*Judgement

*The income derived from the letting of the eight flats for each of the relevant years had been assessed to tax under s 10(1)(a) of the Income Tax Act on the basis that it was part of trading profits and not investment income and no objection was raised by the appellant to each of the said assessments.

*Decision *The Income Tax Board of Review dismissing the appeal of the appellant against the additional assessment made by the Comptroller of Income Tax for the YA 1981.

*THAT’S ALLTHANK YOU