Embed Size (px)

Citation preview

This article was downloaded by: [University of La Laguna Vicerrectorado]On: 01 September 2014, At: 02:31Publisher: RoutledgeInforma Ltd Registered in England and Wales Registered Number: 1072954 Registered office: MortimerHouse, 37-41 Mortimer Street, London W1T 3JH, UK

Click for updates

Regional StudiesPublication details, including instructions for authors and subscription information:http://www.tandfonline.com/loi/cres20

Banks and Regional Development: An EmpiricalAnalysis on the Determinants of Credit Availability inBrazilian RegionsMarco Croccoa, Fernanda Faria-Silvaa, Luiz Paulo-Rezendea & Carlos J. Rodríguez-Fuentesb

a CEDEPLAR, Avenida Antonio Carlos, 6627, FACE – UFMG, Belo Horizonte, Minas Gerais31270 – 901, Brazilb Department of Applied Economics, Faculty of Economics and Business Studies,University of La Laguna, Campus Guajara s/n, E-38071 – S/C de Tenerife, Spain.Published online: 12 Jul 2012.

To cite this article: Marco Crocco, Fernanda Faria-Silva, Luiz Paulo-Rezende & Carlos J. Rodríguez-Fuentes (2014) Banksand Regional Development: An Empirical Analysis on the Determinants of Credit Availability in Brazilian Regions, RegionalStudies, 48:5, 883-895, DOI: 10.1080/00343404.2012.697141

To link to this article: http://dx.doi.org/10.1080/00343404.2012.697141

PLEASE SCROLL DOWN FOR ARTICLE

Taylor & Francis makes every effort to ensure the accuracy of all the information (the “Content”) containedin the publications on our platform. However, Taylor & Francis, our agents, and our licensors make norepresentations or warranties whatsoever as to the accuracy, completeness, or suitability for any purpose ofthe Content. Any opinions and views expressed in this publication are the opinions and views of the authors,and are not the views of or endorsed by Taylor & Francis. The accuracy of the Content should not be reliedupon and should be independently verified with primary sources of information. Taylor and Francis shallnot be liable for any losses, actions, claims, proceedings, demands, costs, expenses, damages, and otherliabilities whatsoever or howsoever caused arising directly or indirectly in connection with, in relation to orarising out of the use of the Content.

This article may be used for research, teaching, and private study purposes. Any substantial or systematicreproduction, redistribution, reselling, loan, sub-licensing, systematic supply, or distribution in anyform to anyone is expressly forbidden. Terms & Conditions of access and use can be found at http://www.tandfonline.com/page/terms-and-conditions

Banks and Regional Development: An EmpiricalAnalysis on the Determinants of Credit Availability

in Brazilian Regions

MARCO CROCCO*, FERNANDA FARIA-SILVA*, LUIZ PAULO-REZENDE* andCARLOS J. RODRÍGUEZ-FUENTES†

*CEDEPLAR, Avenida Antonio Carlos, 6627, FACE – UFMG, Belo Horizonte, Minas Gerais 31270 – 901, Brazil.Emails: [email protected], [email protected] and [email protected]

†Department of Applied Economics, Faculty of Economics and Business Studies, University of La Laguna, Campus Guajara s/n,E-38071 – S/C de Tenerife, Spain. Email: [email protected]

(Received January 2011: in revised form April 2012)

CROCCO M., FARIA-SILVA F., PAULO-REZENDE L. and RODRÍGUEZ-FUENTES C. J. Banks and regional development: anempirical analysis on the determinants of credit availability in Brazilian regions, Regional Studies. This paper studies the influencethat liquidity preference and bank lending strategies might have played in the determination of bank credit availability in Brazilianregions during the period 1999–2008. It puts forward the argument that in remoter and less developed regions, the liquidity pre-ference of agents is higher and fluctuates along business cycles, reducing regional credit availability in downturns (due to both acontraction in supply and the demand for credit in remoter regions), and producing a more unstable pattern for credit availabilityalongside business cycles. Empirical evidence for the Brazilian regions during the period 1999–2008 is provided to supportthis view.

Regional economy (Brazil) Banking system Regional credit availability Liquidity preference Regional growth

CROCCO M., FARIA-SILVA F., PAULO-REZENDE L. and RODRÍGUEZ-FUENTES C. J. 银行与区域发展:巴西区域信贷可及

性决定因子的经验分析,区域研究。本文研究巴西区域自 1999 至 2008 年间,流动性偏好(liquidity preference)与银行借贷策略对于决定银行信贷可及性可能产生的影响。本研究进一步主张:在较为偏远且发展较低的区域,代理人的流动性偏好较高,且随着商业周期波动,在经济不景气时减低了区域信贷的可及性(同时由供给的紧缩以及偏远地区的信贷需求所导致),并且随着商业周期产生更为不稳定的信贷可及性模式。巴西 1999 年至 2008 年间的区

域经验证据将提供用以支持该论点。

区域经济(巴西) 银行系统 区域信贷可及性 流动性偏好 区域成长

CROCCO M., FARIA-SILVA F., PAULO-REZENDE L. et RODRÍGUEZ-FUENTES C. J. Les banques et l’aménagement du territoire:une analyse empirique des déterminants de l’offre de crédit dans les régions brésiliennes, Regional Studies. Cet article cherche àexaminer l’influence éventuelle de la préférence pour la liquidité et les opérations de prêt bancaires quant à la détermination del’offre de crédit bancaire dans les régions brésiliennes entre 1999 et 2008. On avance l’argument selon lequel la préférence desagents pour la liquidité s’avère plus élevée et varie en fonction des cycles d’activité dans les régions plus isolées et moinsdéveloppées, réduisant l’offre de crédit régionale au moment des ralentissements économiques (ce qui s’explique à la fois parune baisse de l’offre et de la demande de crédit dans les régions plus isolées), et déstabilisant l’offre de crédit en fonction descycles d’activité. On fournit des preuves empiriques auprès des régions brésiliennes pour la période allant de 1999 à 2008 afinde justifier cet argument.

Économie régionale (Brésil) Système bancaire Offre de crédit régionale Préférence pour la liquidité Croissancerégionale

CROCCO M., FARIA-SILVA F., PAULO-REZENDE L. und RODRÍGUEZ-FUENTES C. J. Banken und Regionalentwicklung: eineempirische Analyse über die Determinanten für die Verfügbarkeit von Darlehen in brasilianischen Regionen, Regional Studies. Indiesem Beitrag wird untersucht, welche Rolle Liquiditätspräferenzen und Bankkreditstrategien für die Entscheidungen über dieVerfügbarkeit von Bankdarlehen in brasilianischen Regionen im Zeitraum von 1999 bis 2008 gespielt haben könnten. Wir argu-mentieren, dass die Liquiditätspräferenzen der Akteure in abgelegeneren und weniger entwickelten Regionen höher ausfallen undmit den Geschäftszyklen fluktuieren, wodurch sich die regionale Verfügbarkeit von Darlehen bei einem Abschwung (aufgrundeines verringerten Angebots und der Nachfrage nach Darlehen in abgelegeneren Regionen) verringert und ein instabileres

Regional Studies, 2014

Vol. 48, No. 5, 883–895, http://dx.doi.org/10.1080/00343404.2012.697141

© 2012 Regional Studies Associationhttp://www.regionalstudies.org

Dow

nloa

ded

by [

Uni

vers

ity o

f L

a L

agun

a V

icer

rect

orad

o] a

t 02:

31 0

1 Se

ptem

ber

2014

Muster von Darlehensverfügbarkeit gemäß den Geschäftszyklen entsteht. Zur Unterstützung dieser These werden empirischeBelege für die brasilianischen Regionen im Zeitraum von 1999 bis 2008 geliefert.

Regionalwirtschaft (Brasilien) Banksystem Regionale Verfügbarkeit von Darlehen Liquiditätspräferenzen RegionalesWachstum

CROCCO M., FARIA-SILVA F., PAULO-REZENDE L. y RODRÍGUEZ-FUENTES C. J. Bancos y desarrollo regional: un análisisempírico sobre los factores que determinan la disponibilidad de créditos en regiones brasileñas, Regional Studies. En este artículoestudiamos qué influencia han tenido la preferencia de liquidez y las estrategias de los préstamos bancarios en la determinaciónde la disponibilidad de créditos bancarios en las regiones brasileñas durante el periodo entre 1999 y 2008. Presentamos el argumentode que en las regiones más remotas y menos desarrolladas, la preferencia de liquidez de los agentes es superior y fluctúa junto con losciclos comerciales, reduciendo la disponibilidad regional de los créditos en época de recesión (debido a la contracción de la oferta yla demanda de créditos en regiones más remotas) y produciendo un modelo más inestable en la disponibilidad de los créditos juntocon los ciclos comerciales. Para respaldar esta tesis mostramos pruebas empíricas para las regiones brasileñas durante el periodo entre1999 y 2008.

Economía regional (Brasil) Sistema bancario Disponibilidad regional de créditos Preferencia de liquidez Crecimientoregional

JEL classifications: E60, G21, R12

INTRODUCTION

Studies on the relationship between financial systemsand economic growth have consolidated in recentdecades. Authors such as LEVINE (1997) and DEMIR-

GUC-KUNT and LEVINE (2004) have made importantcontributions to the literature on the relationshipbetween economic growth and financial developmentin the long-term, and have provided empirical evidenceof the existence of bidirectional causality between them.LAWRENCE (2006) also stressed the importance of therole of state intervention (through regulation) toensure proper channelling of resources so that it stimu-lates regional growth.

Other contributions, based on a Post-Keynesiantheoretical perspective, have also emphasized the rel-evance of money (and the banking system) for regionaldevelopment from a theoretical perspective (DOW,1987a, 1987b; CHICK and DOW, 1988; RODRÍGUEZ-FUENTES, 1998, 2006). Although these contributionsexplicitly recognize the endogeneity of money supply,they also identify the importance of banking develop-ment and liquidity preference in determining theamount of available credit at a regional level. In thissense, these authors believe that supply and creditdemand are determined largely by the level of financialdevelopment achieved in each region and by thechanges that occur in the liquidity preference of agents(banks and public in general).

This paper follows this second approach and analysesthe influence of the main determinants of bank creditavailability in Brazilian regions between 1999 and2008. Some indicators and proxies are introduced withthe aim to capture the influence from four sources: (1)the liquidity preference of agents, (2) access to banks,(3) bank portfolio choices and (4) unstable growth pat-terns of gross domestic product (GDP). The difference

in effect between more and less developed regions isalso studied. To reflect this effect, a variable (Giniindex) is introduced to capture the inequality in distri-bution of income by region. The results of the estimatessuggest that the liquidity preference of banks and thepublic, bank access, bank portfolio choices, and thedynamics of GDP affect the supply and demand ofcredit among Brazilian regions. Another importantresult was obtained with the identification of higheramplitude of fluctuation in the poorer regions.

Including this Introduction, the paper is structuredinto five sections and it also contains an Appendixwhich provides details on the empirical variables. Thesecond section briefly describes the theoretical frame-work of the paper and pays particular attention to theinfluence of liquidity preference and the stages ofbanking development on the dynamics of peripheralregions, with particular reference to the Brazilian states.The third section presents some empirical evidence onthe determinants of regional credit availability in Brazil.Finally, the fourth and fifth sections discuss the empiricalresults and summarize the conclusions, respectively.

THE ROLE OF CREDIT IN REGIONALDEVELOPMENT

Over the last decades, there has been a growing interestin the economic literature for the role that money andbanks play in the process of regional economic develop-ment (for a survey of the literature, see DOW andRODRÍGUEZ-FUENTES, 1997; RODRÍGUEZ-FUENTES

and DOW, 2003; and RODRÍGUEZ-FUENTES, 2006,pp. 73–113). This growing interest has questioned, tosome extent, the orthodox assumption that neithermoney nor banks have ever played a relevant role inthe regional development process, since orthodox

884 Marco Crocco et al.

Dow

nloa

ded

by [

Uni

vers

ity o

f L

a L

agun

a V

icer

rect

orad

o] a

t 02:

31 0

1 Se

ptem

ber

2014

monetary theory always considered (and still does) thatmoney is a separate variable whose only role is to easethe exchange of goods already produced. Consequently,all that money (and monetary policy) can do is to affectthe general level of prices (when it is supplied in excessfor exchange purposes) but not the real output (at leastin the long run). In addition, according to the orthodoxview, the credit supplied by the financial intermediariescan never restrain regional growth thanks to the efficientwork of the banking system, which allocates (efficientand passively) scarce financial resources among regions,once the central bank has set the money supply (inaccordance with the real needs and the transactionmotive in the demand for money) and the money mul-tiplier has determined the available supply of bank creditfor the whole economy.1

The New Keynesian theoretical perspective2 providesa general equilibrium model where credit-market fric-tions can amplify, through the ‘financial accelerator’,both nominal and real shocks (BERNANKE et al., 1999,pp. 1341–1393), whereby credit-market friction is under-stood as incomplete information (AKERLOF, 1970).According to this view, the supply of credit can berationed when local banks cannot supply credit due to achange in their net worth and this is not offset by a move-ment of either banks into a region or new capital intoexisting banks. Credit rationing is therefore seen as a con-sequence of both imperfect information (that makescapital less mobile than expected) and the existence ofweak financial local institutions that segment the market(STIGLITZ and GREENWALD, 2003, ch. XII). TheNew Keynesian explanation for credit rationing inregional markets is based, as noted by DOW (1998), ontwo assumptions: the loanable funds theory and the exist-ence of asymmetric (or imperfect) information. The firstassumption leads to the conclusion that banks only redis-tribute regionally a maximum fixed amount of creditavailable at the national level (DOW, 1998, p. 218). Thesecond assumption considers that only information(facts) on the side of banks (the supply side), and not‘knowledge’ (processes) on the supply (banks and savers)and demand (local borrowers), determines credit avail-ability in one particular region (DOW, 1998, p. 221).3

The two assumptions upon which the orthodox tra-ditional view described above (New Keynesian) is builthave been always challenged by the contributions that,built on the basic principles of Post-Keynesian monetarytheory, have broadened the scope of the analysis bytaking into account the underlying factors determiningregional credit creation: the stage of banking developmentand the liquidity preferenceoffinancial agents (CHICK andDOW, 1988; DOW, 1990, 1993;DOW andRODRÍGUEZ-FUENTES, 1997; RODRÍGUEZ-FUENTES, 1998, 2006).4

From this theoretical perspective, regional credit avail-ability is determined not only by the ‘efficient allocationprocess’ (the loanable funds traditional view) carriedout by banks, but also (and more importantly) by thechanges in liquidity preference along business cycles

and the regional differences in terms of bankingdevelopment.

The stage of banking development determines both localand nationwide banks’ ability to extend credit regardlesstheir deposit base (either regional or national)

implying that

regions having banking systems in lower stages of develop-ment would be more constrained by low saving or depositratios than other.

(DOW and RODRÍGUEZ-FUENTES, 1997, p. 914)

The liquidity preference affects both supply and demandfor credit. From the supply side, changes in liquiditypreference influences the willingness to lend withinthe region when regional perceived risk is higher or itsassessment is more difficult.5 But changes in liquiditypreference can also affect the supply of credit throughits influence on savers’ behaviour, since a rise in liquiditypreference might also produce in remoter regions finan-cial outflows to central financial markets that supplyfinancial assets that are considered less risky. A rise inliquidity preference can also lower the regionaldemand for credit when, due to poorer expectationsabout future investment projects returns, investors areless willing to run into debt (DOW and RODRÍGUEZ-FUENTES, 1997, p. 915).

One important implication that arises from thePost-Keynesian view is that credit availability may sys-tematically fluctuate along business cycles, as liquiditypreference does, this pattern being more pronouncedfor the less developed regions (RODRÍGUEZ-FUENTES,1998; RODRÍGUEZ-FUENTES and DOW, 2003). Conse-quently, rather than focusing on why a perfect flow offinancial resources among regions does not exist, thePost-Keynesian literature on regional money and credittakes market imperfection as the norm, and focuses onthe study of regional patterns of credit creation, andhow these may vary from one region to another. In sodoing, Post-Keynesian theory makes use of bothChick’s stages of banking development (CHICK, 1986,1988, 1993) and the Keynesian principle of liquiditypreference.6

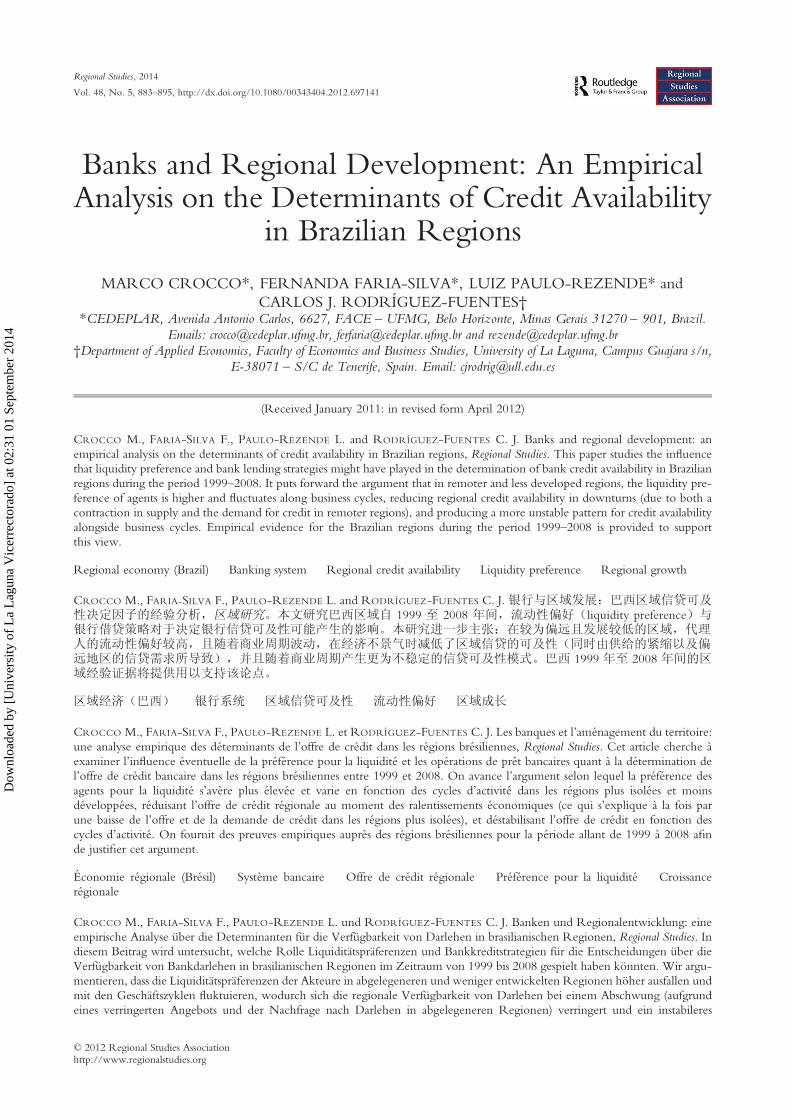

A particular feature of the Post-Keynesian theory isthat its analysis addresses both the supply-side and thedemand-side of the regional credit market (Fig. 1). Forthat reason Post-Keynesian analysis does not see regionalcredit rationing as a unicausal situation explained byregional discriminatory behaviour on the part of thefinancial system (mainly banks), which, in turn, leadsto an uneven regional distribution of credit, but as amulticausal situation in which all sectors in the regionare involved.

One of the implications that follow from the theoreti-cal framework described so far is that having sound anddeveloped regional financial institutions is important forsecuring the supply of the necessary credit to finance

Banks and Regional Development: Determinants of Credit Availability in Brazilian Regions 885

Dow

nloa

ded

by [

Uni

vers

ity o

f L

a L

agun

a V

icer

rect

orad

o] a

t 02:

31 0

1 Se

ptem

ber

2014

regional investment and growth. However, as DOW

(1992) has noted, this is only a necessary conditionsince banks can always choose to ration the localdemand for credit when they have strong preferencesfor liquid assets. Thus, when uncertainty rises, banksmight try to satisfy their preferences by replacing therisky assets in their portfolios (bank credit) for others,which may not be available locally (if they are only sup-plied in central regions) or, if they are, they might not beserving the needs for working capital or productiveinvestment. When this happens, the ‘defensive financialbehaviour’ of banks (DOW, 1992), which leads them tofocus on short-term and riskless operations, might inter-fere with the availability of credit for working capital aswell as for new long-term profitable investment projectsin the region. Consequently, the ‘financial defensive be-haviour’ of banks may become an important obstacle forsecuring funds for many small and medium-sized enter-prises simply because they have no other option offunding sources besides bank credit (CROCCO et al.,2005).

In the case of peripheral regions, it is important tohighlight two important aspects in relation to thecredit dynamics. The first is concerned with microeco-nomic implications, specifically with the formal credit-risk assessment processes, which are more difficult andcostly to carry out in remoter regions, and the liquiditypreference of economic agents, which tends to behigher than in central regions. Thus, in these regions(periphery) more rigid and rationed credit markets arelikely to be found, with their corresponding higherinterest rates and required major credit collaterals.

The second point, being more macroeconomic innature, is related to the procyclical and more pro-nounced changes in the liquidity preferences of allagents, which reinforces (reduces) the agents willingnessto borrow (public) and lend (banks) in expansions(recessions) and it interferes in the business cycles.Thus, in these regions (periphery) the financial systemreinforces the volatile character of such economiesrather than promoting economic growth in the long

run (by producing a more unstable pattern in creditavailability) because the credit creation process fuelsexpansions and enhances recessions (RODRÍGUEZ-FUENTES, 2006, pp. 100–103).

The following section of this paper is devoted to thestudy of some of the determinants of credit availability inthe states that make up the five major regions of Brazil.7

BANKS AND REGIONAL DEVELOPMENT:THE CASE OF THE BRAZILIAN STATES

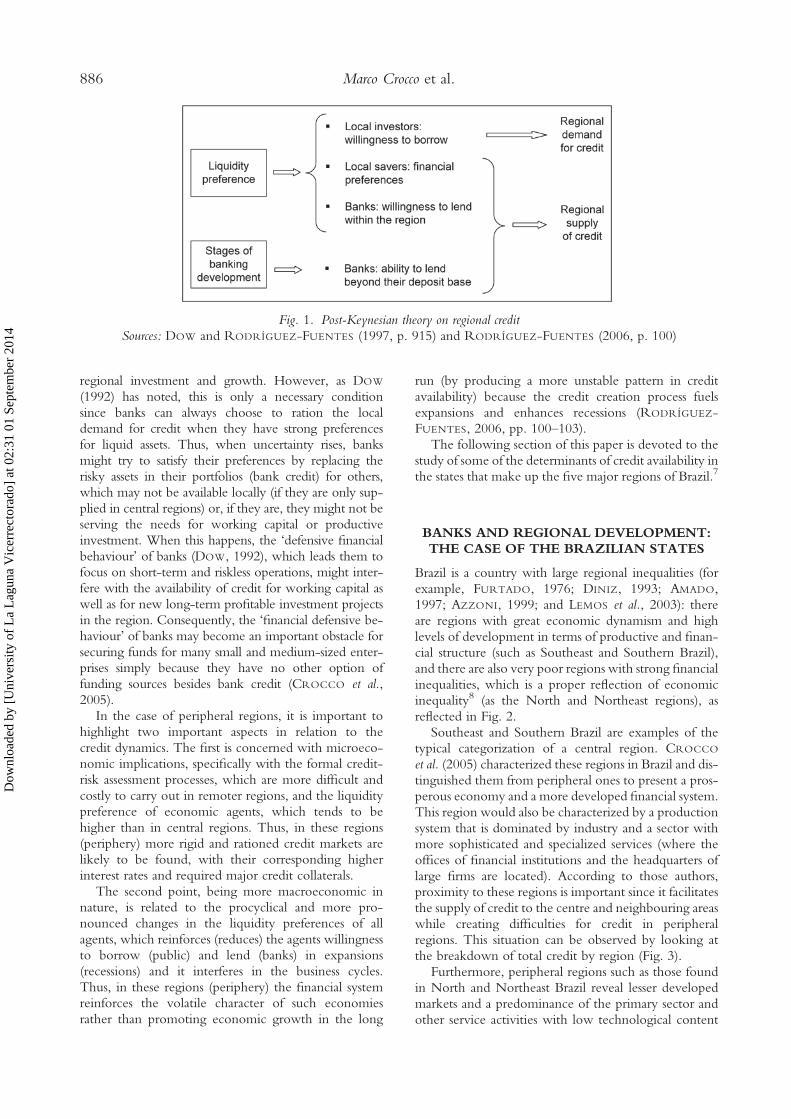

Brazil is a country with large regional inequalities (forexample, FURTADO, 1976; DINIZ, 1993; AMADO,1997; AZZONI, 1999; and LEMOS et al., 2003): thereare regions with great economic dynamism and highlevels of development in terms of productive and finan-cial structure (such as Southeast and Southern Brazil),and there are also very poor regions with strong financialinequalities, which is a proper reflection of economicinequality8 (as the North and Northeast regions), asreflected in Fig. 2.

Southeast and Southern Brazil are examples of thetypical categorization of a central region. CROCCO

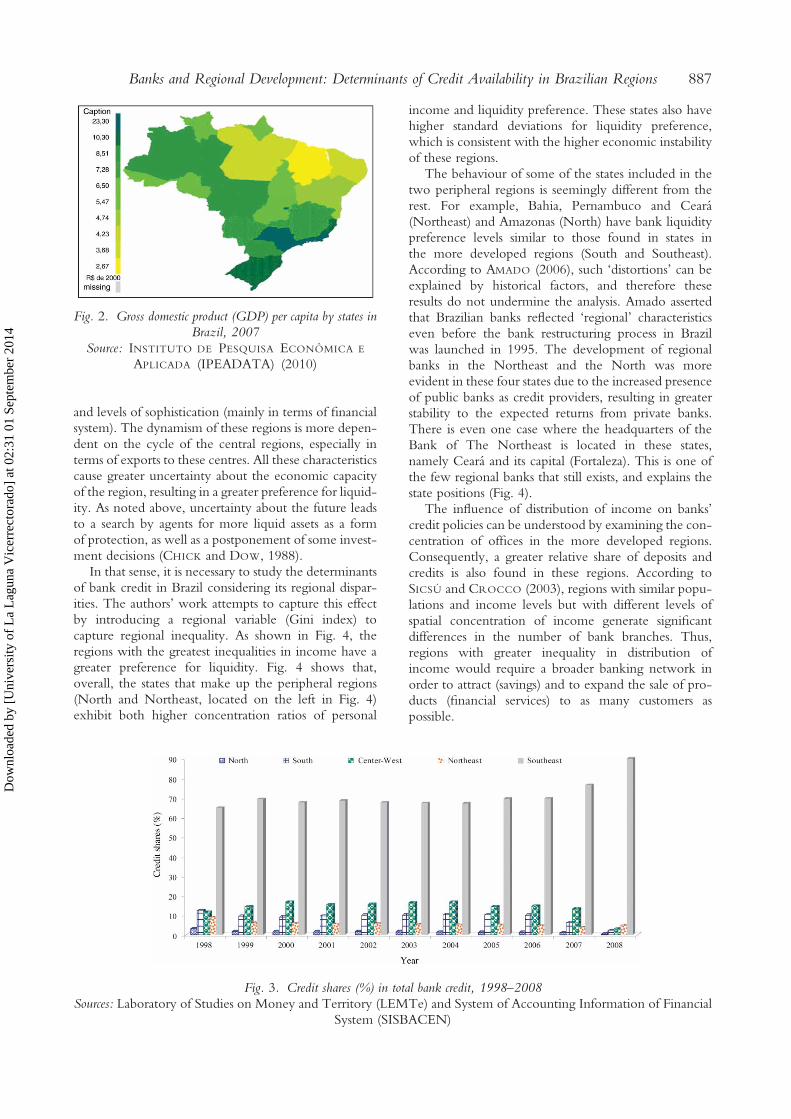

et al. (2005) characterized these regions in Brazil and dis-tinguished them from peripheral ones to present a pros-perous economy and a more developed financial system.This region would also be characterized by a productionsystem that is dominated by industry and a sector withmore sophisticated and specialized services (where theoffices of financial institutions and the headquarters oflarge firms are located). According to those authors,proximity to these regions is important since it facilitatesthe supply of credit to the centre and neighbouring areaswhile creating difficulties for credit in peripheralregions. This situation can be observed by looking atthe breakdown of total credit by region (Fig. 3).

Furthermore, peripheral regions such as those foundin North and Northeast Brazil reveal lesser developedmarkets and a predominance of the primary sector andother service activities with low technological content

Fig. 1. Post-Keynesian theory on regional creditSources: DOW and RODRÍGUEZ-FUENTES (1997, p. 915) and RODRÍGUEZ-FUENTES (2006, p. 100)

886 Marco Crocco et al.

Dow

nloa

ded

by [

Uni

vers

ity o

f L

a L

agun

a V

icer

rect

orad

o] a

t 02:

31 0

1 Se

ptem

ber

2014

and levels of sophistication (mainly in terms of financialsystem). The dynamism of these regions is more depen-dent on the cycle of the central regions, especially interms of exports to these centres. All these characteristicscause greater uncertainty about the economic capacityof the region, resulting in a greater preference for liquid-ity. As noted above, uncertainty about the future leadsto a search by agents for more liquid assets as a formof protection, as well as a postponement of some invest-ment decisions (CHICK and DOW, 1988).

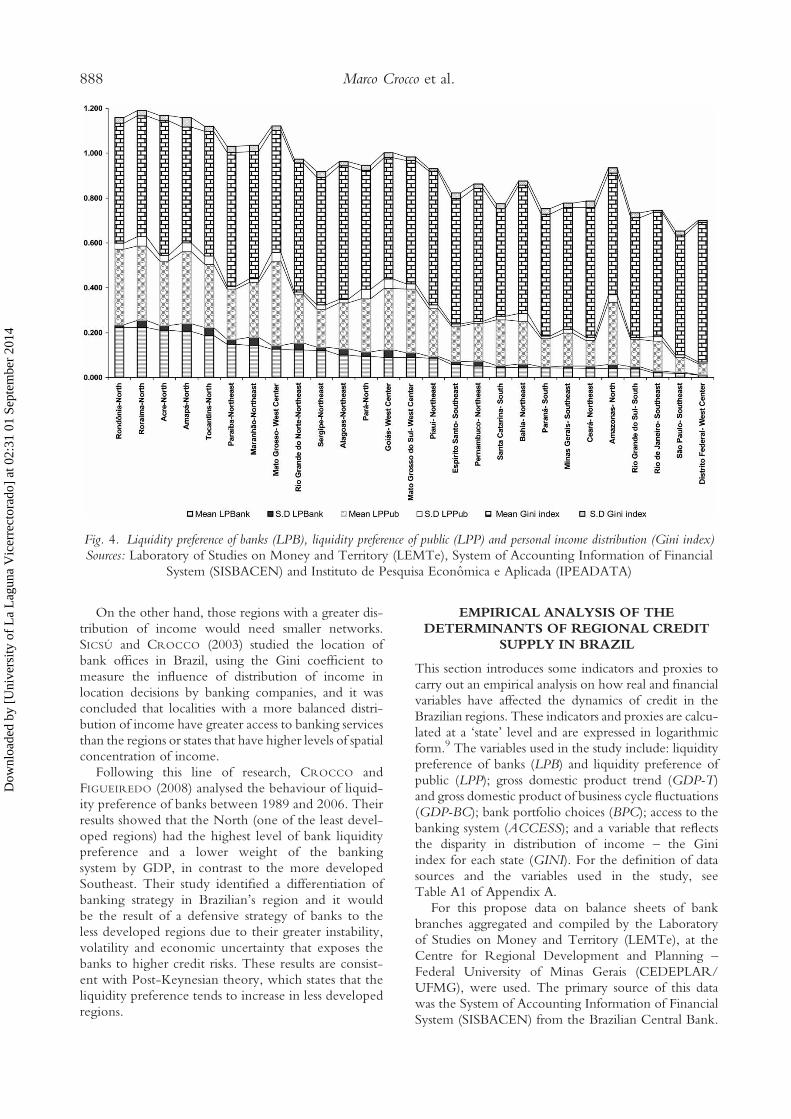

In that sense, it is necessary to study the determinantsof bank credit in Brazil considering its regional dispar-ities. The authors’ work attempts to capture this effectby introducing a regional variable (Gini index) tocapture regional inequality. As shown in Fig. 4, theregions with the greatest inequalities in income have agreater preference for liquidity. Fig. 4 shows that,overall, the states that make up the peripheral regions(North and Northeast, located on the left in Fig. 4)exhibit both higher concentration ratios of personal

income and liquidity preference. These states also havehigher standard deviations for liquidity preference,which is consistent with the higher economic instabilityof these regions.

The behaviour of some of the states included in thetwo peripheral regions is seemingly different from therest. For example, Bahia, Pernambuco and Ceará(Northeast) and Amazonas (North) have bank liquiditypreference levels similar to those found in states inthe more developed regions (South and Southeast).According to AMADO (2006), such ‘distortions’ can beexplained by historical factors, and therefore theseresults do not undermine the analysis. Amado assertedthat Brazilian banks reflected ‘regional’ characteristicseven before the bank restructuring process in Brazilwas launched in 1995. The development of regionalbanks in the Northeast and the North was moreevident in these four states due to the increased presenceof public banks as credit providers, resulting in greaterstability to the expected returns from private banks.There is even one case where the headquarters of theBank of The Northeast is located in these states,namely Ceará and its capital (Fortaleza). This is one ofthe few regional banks that still exists, and explains thestate positions (Fig. 4).

The influence of distribution of income on banks’credit policies can be understood by examining the con-centration of offices in the more developed regions.Consequently, a greater relative share of deposits andcredits is also found in these regions. According toSICSÚ and CROCCO (2003), regions with similar popu-lations and income levels but with different levels ofspatial concentration of income generate significantdifferences in the number of bank branches. Thus,regions with greater inequality in distribution ofincome would require a broader banking network inorder to attract (savings) and to expand the sale of pro-ducts (financial services) to as many customers aspossible.

Fig. 2. Gross domestic product (GDP) per capita by states inBrazil, 2007

Source: INSTITUTO DE PESQUISA ECONÔMICA E

APLICADA (IPEADATA) (2010)

Fig. 3. Credit shares (%) in total bank credit, 1998–2008Sources: Laboratory of Studies on Money and Territory (LEMTe) and System of Accounting Information of Financial

System (SISBACEN)

Banks and Regional Development: Determinants of Credit Availability in Brazilian Regions 887

Dow

nloa

ded

by [

Uni

vers

ity o

f L

a L

agun

a V

icer

rect

orad

o] a

t 02:

31 0

1 Se

ptem

ber

2014

On the other hand, those regions with a greater dis-tribution of income would need smaller networks.SICSÚ and CROCCO (2003) studied the location ofbank offices in Brazil, using the Gini coefficient tomeasure the influence of distribution of income inlocation decisions by banking companies, and it wasconcluded that localities with a more balanced distri-bution of income have greater access to banking servicesthan the regions or states that have higher levels of spatialconcentration of income.

Following this line of research, CROCCO andFIGUEIREDO (2008) analysed the behaviour of liquid-ity preference of banks between 1989 and 2006. Theirresults showed that the North (one of the least devel-oped regions) had the highest level of bank liquiditypreference and a lower weight of the bankingsystem by GDP, in contrast to the more developedSoutheast. Their study identified a differentiation ofbanking strategy in Brazilian’s region and it wouldbe the result of a defensive strategy of banks to theless developed regions due to their greater instability,volatility and economic uncertainty that exposes thebanks to higher credit risks. These results are consist-ent with Post-Keynesian theory, which states that theliquidity preference tends to increase in less developedregions.

EMPIRICAL ANALYSIS OF THEDETERMINANTS OF REGIONAL CREDIT

SUPPLY IN BRAZIL

This section introduces some indicators and proxies tocarry out an empirical analysis on how real and financialvariables have affected the dynamics of credit in theBrazilian regions. These indicators and proxies are calcu-lated at a ‘state’ level and are expressed in logarithmicform.9 The variables used in the study include: liquiditypreference of banks (LPB) and liquidity preference ofpublic (LPP); gross domestic product trend (GDP-T)and gross domestic product of business cycle fluctuations(GDP-BC); bank portfolio choices (BPC); access to thebanking system (ACCESS); and a variable that reflectsthe disparity in distribution of income – the Giniindex for each state (GINI). For the definition of datasources and the variables used in the study, seeTable A1 of Appendix A.

For this propose data on balance sheets of bankbranches aggregated and compiled by the Laboratoryof Studies on Money and Territory (LEMTe), at theCentre for Regional Development and Planning –Federal University of Minas Gerais (CEDEPLAR/UFMG), were used. The primary source of this datawas the System of Accounting Information of FinancialSystem (SISBACEN) from the Brazilian Central Bank.

Fig. 4. Liquidity preference of banks (LPB), liquidity preference of public (LPP) and personal income distribution (Gini index)Sources: Laboratory of Studies on Money and Territory (LEMTe), System of Accounting Information of Financial

System (SISBACEN) and Instituto de Pesquisa Econômica e Aplicada (IPEADATA)

888 Marco Crocco et al.

Dow

nloa

ded

by [

Uni

vers

ity o

f L

a L

agun

a V

icer

rect

orad

o] a

t 02:

31 0

1 Se

ptem

ber

2014

This system makes it mandatory for all bank branches tosupply the Central Bank with balance-sheet informationof their monthly operations. The Central Bank pub-lishes the data, aggregated by municipality. TheLEMTe organized the information for the periodbetween 1988 and 2008 for all Brazilian municipalities;it was then aggregated into states.

Estimates were made using econometric panel data.According to BALTAGI (2005), this technique has theadvantage of providing more information, greatervariability and efficiency of estimates while reducingcollinearity among the variables and degrees offreedom. Panel data are also better when studying theadjustment dynamics of the econometric model.

As stated by WOOLDRIDGE (2001), this techniquecan also work with multiple observations in the sameunit, leading to the control of certain unobservedcharacteristics of the studied agents. Thus, this toolcould help in the analysis of the influence of banks’(supply) and borrowers’ (demand) behaviour in the cre-ation of credit in Brazil, given the high level of hetero-geneity found in the characteristics of the affected states(regions). The aim was to identify which variables weremost significant in determining the amount of bankcredit in the Brazilian states.

The heterogeneity of the Brazilian data due to thestructural differences in each state can cause heteroske-dasticity due to the higher variability. The use of serialdata can also generate possible problems of residualautocorrelation. The heteroskedasticity is a minorproblem because it only affects the efficiency of the esti-mator but does not cause bias. But if the estimation pre-sents a lack of significance, it may be due to a modelmisspecification (omitted variables), which could gener-ate a problem of endogeneity.

In order to solve these types of problem, estimationwasmade using a robust estimation in a dynamic panel datamodel (ARELLANO and BOVER, 1995). ARELLANO andBOVER (1995) suggest including a generalized methodof moments (GMM)10 estimation with variables in thefirst lag (delay) and the original-level equations in thesystem. This context not only improves the accuracy ofthe estimators, but also reduces the sample bias.

The robust estimation in a dynamic panel datamodel, the delayed dependent and exogenous variablesare used as an instrument with the aim of correcting theproblem of serial autocorrelation of errors over time andit treats some problems of endogeneity due to unob-served effects (CAMERON and TRIVEDI, 2010).

To ensure the consistency of the estimates, the val-idity of the instruments from the Sargan test and theserial autocorrelation test was compared. The first testaims to verify the validity of the instruments throughthe validation of restrictions on an over-identificationof the model. The second test examines the hypothesisthat the residual is not serially correlated.

A dynamic panel method was used to study theeffects of liquidity preference and bank concentration

on the supply of credit in Brazil, based on the work ofMENEZES et al. (2007). The justification for using sucha technique was to take into account the path depen-dence assumed in Post-Keynesian theory on regionalcredit, where liquidity preference and bank concen-tration have a significant influence on credit supplyand, to the extent that these factors also contribute toreinforce agents’ expectations to lend/borrow lesscredit in less developed regions, they would alsoreinforce the unstable pattern of credit availability forthe less developed regions, and so contribute to themaintenance of income gaps between less and moredeveloped regions. Under this assumption, this paperaims to estimate the following equation:

CREDit = c + b1LPPit + b2LPBit + b3GDP-Tit

+ b4GDP-BCit + b5ACCESSit+ b6BPCit + b7GINIit + U (1)

The liquidity preference of bank (LPB) variablemeasures the proportion of liquid assets in the bank’sbalance sheet. The inclusion of this variable aims atmeasuring changes in banks’ credit strategies: whenuncertainty rises, banks are less willing to supply credit(particularly in some regions) so there is an increase inthe proportion of more liquid assets in the balancesheet (CROCCO et al., 2005).11

Similarly, and following CROCCO et al. (2005), theliquidity preference of the public (LPP) shows therelationship between demand deposits and total depos-its. While demand deposits are the most liquid assetfor the public (leaving aside cash holdings), time depositsrepresent for banks a liability that allows them to allocatetheir resources into assets with a longer maturity – as isthe case of credit operations. The higher are these twoindices (LPP and LPB), the greater the preference forliquidity and, therefore, more liquid assets will be main-tained or required.

Regarding the GDP variable, the aim is to capturethe influence of both growth and business cycle onbanks’ credit strategies, primarily in terms of theamount of credit that the bank system is willing tosupply and its allocation (both sectorial and spatially).Consequently, the influence of GDP was divided intotwo components: the trend component (GDP-T); andfluctuations alongside business cycles (GDP-BC).GDP-T aims to take into account the investmentopportunities that vary across regions having differenttrends in GDP growth. The regions with higher GDPaverage growth rates are more attractive to investmentsand to supply credit. GDP-BC, which is calculated bythe Hodrick Prescott filter, measures the business cycledynamics. The sign of the coefficient for the GDP fluc-tuations is negative, which reinforces the theoreticalhypothesis that in regions with higher fluctuations inbusiness cycles, the liquidity preference of banks ishigher and therefore the supply credit is lower.

Banks and Regional Development: Determinants of Credit Availability in Brazilian Regions 889

Dow

nloa

ded

by [

Uni

vers

ity o

f L

a L

agun

a V

icer

rect

orad

o] a

t 02:

31 0

1 Se

ptem

ber

2014

The ‘access to the banking system’ variable (ACCESS),following the work of SICSÚ and CROCCO (2003), is ameasure of the concentration of banking services in thestates. It is understood as an indication of the access ofthe population to the banking system, and it could bestated that more developed regions also concentratemore branches, thus the availability of credit is facilitated.

The variable ‘bank portfolio choices’ (BPC) measurestransactions in securities and derivatives in banks’ port-folios and it aims to identify the influence of banks’ port-folio strategies on lending.12 The capital market in Brazilis still underdeveloped and in this case this measure canbe a good proxy to capture the problematic relationshipbetween economic growth and financial stability due tothe lack of funding.

Finally, the GINI variable was introduced into themodel in order to classify the Brazilian states accordingto their respective levels of inequality in the distributionof income. The Federal District, where the capital islocated, is an outlier (in terms of regional inequality asbeing the financial and administrative headquarters ofpublic banks). These two features give this state a verystrong concentration of banks and a large ratio incredit volumes. It is important to consider the FederalDistrict in the sample mainly because the public banksare important institutions in the Brazilian financialsystem and decide to invest large quantities in financialinnovations and support credit operations.13

Based on the above variables previously defined, thepresent study aims to estimate a panel model covered atotal of ten years (120 months) for all twenty-seven Bra-zilian states, leading to a total of 270 observations.Finally, all estimates were made using STATA statisticalsoftware version 10 (STATACORP, 2008).

DISCUSSION

According to the model and the theoretical explanationsprovided in the proceeding former section, Table 1shows the estimates for the variables influencing thesupply of credit in the Brazilian states during theperiod 1999–2008.14 The empirical results shown inTable 1 seem to give support to the arguments putforward in this paper, namely that liquidity preference(of banks and public) had played an important role indetermining regional credit availability in the Brazilianstates, which in turn confirms a significant (and notneutral) role of banks in regional development inBrazil during that period.

The inverse relationship between liquidity prefer-ence and credit volume seems to confirm the assump-tion that regions with lower liquidity preference andgreater bank development are those that have a morestable pattern of credit availability over time, whereasthere are fewer opportunities in regions with higherlevels of liquidity preference (DOW and RODRÍGUEZ-

FUENTES, 1997; CROCCO et al., 2005; RODRÍGUEZ-FUENTES, 2006).

Liquidity preference by the public is also significantwhen explaining the supply of credit in the model, asevidenced by the strong interaction between supplyand demand for credit. Thus, according to RODRÍ-

GUEZ-FUENTES (2006, p. 65), an increase in theliquidity preference of agents reduces their demand forcredit because they would be less willing to borrow,while the supply of credit is reduced because banks aremore risk averse, or because they prefer to invest inmore liquid assets and higher profitability. Additionally,in most bank branches in Brazil, their portfolio decisionsare more constrained and dependent of theirheadquarters.

It is interesting to note that this is characteristic of aself-reinforcing situation, where the low regional avail-ability of credit is due to both a weak demand andsupply of credit, which is the result of the ‘financialdefensive behaviour’ of both lenders and borrowers,which is more common in the less developed regionsdue to the increasing uncertainty of the worsening ofeconomic expectations (DOW, 1992).

Table 1. Results of the estimates (dynamic panel) and tests

LPB –0.9077(0.0305)***

LPP –0.0989(0.0536)*

GDP-T 0.4192(0.0422)***

GDP-BC –0.0483(0.0291)*

ACCESS 0.1642(0.0352)***

BPC –0.0157(0.0056)***

GINI –1.5990(0.2075)***

CREDt−1 0.3686(0.0566)***

CREDt−2 0.0191(0.0433)

c (constant term) 4.7315(0.4398)***

Number of years 10Sargan testa (195.8156)

Serial correlation test (Arellano–Bond)First order (–2.1272)**Second order (–0.32667)

Wald test (4595.82)+

Notes: aThe Sargan test does not reject the null hypothesis of over-identification restrictions being valid, therefore it guarantees thevalidity of the instruments.

Absolute value of t-statistics are given in parentheses:*Statistically significant at the 10% level; **statistically significant atthe 5% level; and ***statistically significant at the 1% level (*p<0.1; **p < 0.05; and ***p< 0.01). Absolute value of Chi2 statisticsare given in parentheses: +, significant at 1%.Source: Authors’ own results and performed tests.

890 Marco Crocco et al.

Dow

nloa

ded

by [

Uni

vers

ity o

f L

a L

agun

a V

icer

rect

orad

o] a

t 02:

31 0

1 Se

ptem

ber

2014

Changes in liquidity preference explain the variationsin credit and, therefore, may have an influence onregional income in those economies with a high financialdependence on bank credit. The negative coefficientfound in the liquidity preference of banks indicates thata reduction in this variable would cause credit growth.That is also one of the factors that explains why moneysupply cannot be exogenous, or fully controlled by theCentral Bank through its traditional managerial instru-ments of bank reserves (which would be very difficult,if not impossible, in the current stage of banking develop-ment, financial globalization and the financialization ofeconomic activity).

Thus, most developed banking systems have a greatcapacity to expand credit in a context of positive expec-tations and lower uncertainty, regardless of theirdeposit base, by making transactions with their bankliabilities (off-balance sheet operations) or by financialinnovations.

The variable GDP-BC shows a negative coefficient,according to the hypothesis that business cycle fluctu-ations reduce credit availability by producing a raise inbanks’ liquidity preference in some particular regions.In this way, KEYNES (1936) asserted that the long-term expectation, upon which investment decisionsare based, does not solely depend on the most prob-able forecast on expected return. It also depends onthe degree of confidence with which the agentsmake this forecast. If the agents expect large changesbut are very uncertain as to the precise form thesechanges will take, then the state of confidence willbe weak. On the contrary, in central regions thisstate of confidence will be strong and stable becauseof prevailing conditions that generate littleuncertainty.

The results for GDP-T show a positive coefficient, asexpected. Economic growth reduces the uncertainty ofthe agents and confirms the optimistic expectationsabout the future, thereby driving the expansion of credit.

Following AMADO (2006), this positive relationshipis stronger in more developed regions, characterizedby greater and more stable GDP growth rate, aswell as having greater endogenous dynamics. Theopposite occurs in the peripheral regions, where GDPgrowth rate is lower and more volatile economies arepresent, which cause a high degree of uncertainty thatmay lead to a reduction in credit supply. Thus, whena region is characterized by economic stagnation, theformation of future expected returns on the part ofbanks could cause a contraction in regional creditsupply.

Therefore, the liquidity preference of banks and thepublic is lower in central regions than in the peripherybecause money multipliers are greater in the formerregion. In addition, the financial resources of peripheralareas tend to move to central regions, reinforcing thenegative relationship between credit creation andliquidity preference (AMADO, 1997, 2006).

The Gini index has an expected negative sign, asexpected. It represents greater inequality, which istypical for the less developed states in socio-economicterms. In less developed areas there are not only lowersaving rates which make financing long-term projectinvestments more difficult for local banks, but alsoextra-regional investment opportunities which mayoffer similar returns but with lower expected risks(public sector or large corporations’ assets). This may bethe case for Brazil, where more developed states arecharacterized by a process of endogenous growth withstronger financial institutions and more developed finan-cial markets which offer more liquid financial assets. Inaddition, these states concentrate production in the sec-ondary and tertiary sectors, and also have a more conso-lidated information system, which results in lowerliquidity preference and a higher bank multiplier. Thismight explain why the more developed regions con-stantly tend to have a greater supply of credit.

The ‘access to the banking system’ (ACCESS) vari-able shows a positive relationship with the rate ofcredit growth, especially in states where agents havegreater access to bank branches or more diversified ser-vices. According to ROMERO and JAYME JR (2008),regions with low access may restrict bank credit,which can be interpreted as a measure of financialexclusion. MENEZES et al. (2007) found a positiverelationship between the concentration of banks andincreased funding, confirming the estimates of thiswork.

According to the conventional approach, the pro-cesses of financial innovation are beneficial for econ-omic growth of regions, since it would increasedomestic savings rates and, therefore, the supply ofcredit.15 However, the proliferation of financial inno-vations can also reinforce the processes of ‘excessive’creation (destruction) of credit in periods of economicexpansion (recession), and so reinforce the instabilityin the temporal credit availability pattern in backwardareas. The negative sign found in the estimates for thevariable BPC, which measures bonds and derivativesin banks’ portfolios, seems to support the hypothesisthat short-term and market-driven logic of banking’sstrategies – which are particularly reinforced whenuncertainty rises – forces banks to replace credit (inthe asset side) for other more liquid and less risky finan-cial assets (but less suitable for the current needs ofworking capital of firms or the new planned investmentsto increase future productive capital). No doubtthe ‘financialization’ of banking lending can help indi-vidual banks (micro-level) to achieve higher rates ofreturn while reducing the risks of their portfolios.However, financial innovations can also stronglyaffect the availability of credit (macro-level), particularlyfor those regions and economic activities thatcannot offer the same combination of return and riskthat banks can get in assets traded in global financialmarkets.

Banks and Regional Development: Determinants of Credit Availability in Brazilian Regions 891

Dow

nloa

ded

by [

Uni

vers

ity o

f L

a L

agun

a V

icer

rect

orad

o] a

t 02:

31 0

1 Se

ptem

ber

2014

The Brazilian financial system that emerged fromthis process of restructuring was more internationa-lized, concentrated (in terms of the number of insti-tutions operating in the country and the total assets)and competitive (in terms of profitability); itremained functionally underdeveloped as it was lessconcerned with the provision of credit to investmentsthan with the gaining of handsome profits in thetrading (particularly government bonds of highreturn and low risk). In other words, banks movedto a far more speculative posture by seeking assetsof higher liquidity or, alternatively, by showing ahigher degree of liquidity preference (CROCCO andFIGUEIREDO, 2008).

Most of the credit operations are of a short-termnature or directed to consumption. Moreover, in thecase of domestic and foreign private banks, there is aclear preference for very short-term bonds and securi-ties. This shows the speculative nature of private banksin Brazil and their high liquidity preference. The Brazi-lian financial system is still functionally underdevelopedas it is unable to provide financing for development andit is highly speculative because it operates in the veryshort-term. According to STUDART (1996) andCROCCO et al. (2005) it has been an obstacle to economicgrowth and to financial stability due to the lack offunding, which heavily penalizes peripheral regionswhen compared with central ones, and so contributes tothe maintenance of the regional economic disparities inBrazil.

CONCLUSIONS

This paper studied the influence that liquidity prefer-ence and banks’ portfolio strategies have played inthe determination of bank credit availability in Brazi-lian regions during the period 1999–2008. Theempirical relationships that have been tested in thispaper are based on the theoretical assumptions pro-vided by the Post-Keynesian regional credit avail-ability literature, which was briefly discussed in thepaper. This theory states that in the remoter andless developed regions, liquidity preference of agentsis higher and fluctuates along business cycles, redu-cing regional credit availability in downturns andproducing a more unstable pattern for credit avail-ability alongside business cycles. In addition, thepaper also considered that bank portfolio choicesmight have reinforced the unstable pattern in creditavailability in the less developed regions in Brazilby facilitating the spatial reallocation of funds in themore ‘central’ and stable economies.

The empirical results provided in this paper seem tosupport the above-mentioned assumptions. On the onehand, the estimates show an inverse relationshipbetween liquidity preference and bank credit availabilityin the Brazilian states during 1999–2008. Bank portfoliochoices and income inequality also exert a negativeeffect on regional credit availability. Consequently, forthe less developed regions in Brazil, both the higherliquidity preference and the higher inequality in the per-sonal distribution of income have negatively influencedcredit availability. The negative influence of bonds andderivates in banks’ portfolios for credit availability foundin this paper reinforces the hypothesis expressed inworks such as those by CARVALHO (2005) andCROCCO and FIGUEIREDO (2008), which havesuggested that banks follow their management strategiesseeking to reconcile assets with high profitability andlower risk, making decisions based on expected returns.Such returns affect their liquidity preference, creatingregional differentiation by the bank, choosing othertypes of operations at the expense of credit, and compro-mising its supply and other kinds of longer-term invest-ment. This result is, however, less than surprising forBrazil, where the participation of private banks in provid-ing credit for the productive sector is historically smallerthan that of public banks, because private banks preferto concentrate their operations in government bonds(due to its high liquidity and high returns), so thatpublic banks are responsible for financing strategicsectors and profitability in the longer-term.

On the other hand, the positive sign for the growthvariable and the banking access found in this paperalso suggests that remoter regions, with lower rates ofgrowth and banking accessibility, have faced a reductionin credit availability.

Overall, the empirical results shown in this paper raisethe question of what can be done to increase the creditavailability in remoter regions, particularly in countriessuch as Brazil, with such large regional economic dispar-ities. Under these particular circumstances, the market-driven logic of ‘financial efficiency’ which constantlyforces banks to look for higher returns and lower risksto allocate funds might not be the best alternative toachieve higher levels of growth and economic cohesion.In this case, as many authors have pointed out(CARVALHO, 2005), the ‘banking functionality view’might be more helpful to achieve the objective ofreducing regional economic disparities.

Acknowledgements – The authors acknowledge thefinancial support provided by the National Council forScientific and Technological Development (CNPq) and theBrazilian Federal Agency for Support and Evaluation ofPostgraduate Education (CAPES).

892 Marco Crocco et al.

Dow

nloa

ded

by [

Uni

vers

ity o

f L

a L

agun

a V

icer

rect

orad

o] a

t 02:

31 0

1 Se

ptem

ber

2014

NOTES

1. Only when markets are segmented does this view con-sider the possibility for the banking system to interferein the process (ROBERTS and FISHKIND, 1979;MOORE and HILL, 1982); otherwise, there will be equi-librating interregional financial flows which, in turn,would mean that money and credit are of no significanceat the regional level (BORTS, 1968; MOORE andNAGURNEY, 1989).

2. The New Keynesian theory is applied to the regionallevel by GREENWALD et al. (1993) and STIGLITZ andGREENWALD (2003, ch. XII).

3. According to DOW (1998),

the term ‘knowledge’ refers more to processes than tofacts; information on facts is thus a subset of knowl-edge. The knowledge-information distinction is thusparallel to the distinction between ‘knowing how’and ‘knowing that’.

(p. 221)

4. For the explanation of the New Keynesian and Post-Keynesian approaches to regional credit markets, as wellas their differences, see DOW and RODRÍGUEZ-FUENTES (1997, pp. 913–914 and 914–915, respectively).

5. Note the Post-Keynesian distinction between infor-mation and knowledge in the credit creation process,outlined by DOW (1998) as follows:

This distinction [information versus knowledge] hasprofound implications for credit market analysis.First, the range of potential knowledge is notknown in advance (or even in retrospect). The cleareststatement of this is Shackle’s (1972) argument thatfirms’ investment projects are crucial experiments;there is in general no relevant frequency distributionon which to estimate risk. More generally, insti-tutional evolution and human creativity mean thatthe future is not like the past in ways which cannotpossibly be predicted. Keynes’s (1973e) Treatise onProbability builds on the argument that the range ofknowledge which can be captured by frequency dis-tributions is small; most knowledge is subject touncertainty in the sense of unquantifiable risk.Keynes classified knowledge as being direct (basedon pure logic and/or direct experience) and indirect(based on theorizing, referring to direct knowledgeas evidence.

(p. 221)

6. For a fuller account of this approach, see RODRÍGUEZ-FUENTES (2006, pp. 100–103).

7. The ‘state’ refers to the geographical unit that makes upeach region in Brazil. Brazil has twenty-six states (plus theFederal District) divided into five geographical regions:(1) ‘North’ – seven states: Amazonas, Pará, Rondônia,Roraima, Amapá, Acre and Tocantins; (2) ‘Northeast’ –nine states: Alagoas, Sergipe, Bahia, Pernambuco, RioGrande do Norte, Paraíba, Maranhão, Piauí and Ceará;

Table A1. Description of variables and data sources: period: 1999–2008 – level of disaggregation: Brazilian states

Proxies Variables/indicators Sources

Bank credit (CRED) Log of total banking system credit – by state (constant2008). Total credit includes all types of credit to thesectors of the economy captured by the account 1600of the Brazilian Central Bank System (SISBACEN).Deflator: consumer price index (IPCA)

LEMTe of CEDEPLAR/UFMG through the datacollected in SISBACEN/Central Bank of Brazil

Liquidity preference of banks(LPB)

Log of the ratio: demand deposit/total credit (constant2008). Deflator: consumer price index (IPCA)

LEMTe of CEDEPLAR/UFMG through the datacollected in SISBACEN/Central Bank of Brazil

Liquidity preference of public(LPP)

Log of the ratio: demand deposit/total deposit (constant2008). Deflator: consumer price index (IPCA)

LEMTe of CEDEPLAR/UFMG through the datacollected in SISBACEN/Central Bank of Brazil

Gross domestic product: trend(GDP-T) and businesscycles (GDP-BC)a

Log of GDP (constant 2008). Deflator: consumer priceindex (IPCA)

IBGE

Bank portfolio choices (BPC) Log of the total value of bonds and derivatives. Deflator:consumer price index (IPCA)

LEMTe of CEDEPLAR/UFMG through the datacollected in SISBACEN/Central Bank of Brazil

Access bank system(ACCESS)

Log of the ratio: total branches/population Branches banks: LEMTe – (CEDEPLAR/UFMG) bySISBACEN/Central Bank of Brazil. Populationdata: Demographical Census (2000) – IBGE

Personal income distribution(GINI)

Log of the Gini index Instituto de Pesquisa Econômica e Aplicada(IPEADATA)

Notes: aCalculated by the Hodrick Prescott filter.CEDEPLAR/UFMG, Centre for Regional Development and Planning – Federal University of Minas Gerais; IBGE, Instituto Brasileiro de

Geografia e Estatística; LEMTe, Laboratory of Studies on Money and Territory; SISBACEN, System of Accounting Information of FinancialSystem.

APPENDIX

Banks and Regional Development: Determinants of Credit Availability in Brazilian Regions 893

Dow

nloa

ded

by [

Uni

vers

ity o

f L

a L

agun

a V

icer

rect

orad

o] a

t 02:

31 0

1 Se

ptem

ber

2014

(3) ‘Midwest’ – three states plus the Federal District: MatoGrosso, Mato Grosso do Sul and Goiás; (4) ‘Southeast’ –four states: Minas Gerais, São Paulo, Rio de Janeiro andEspírito Santo; and (5) ‘South’ – three states: Rio Grandedo Sul, Paraná and Santa Catarina. For purposes of thispaper, the names of the regions are not translated fromthe original Portuguese.

8. Some ‘peripheral’ states such as Amazonas and MatoGrosso (as shown in Fig. 2) have a higher income percapita. This fact is due to the presence of areas withsome degree of economic dynamism in these two states(such as the ‘Zona Franca de Manaus’ in Amazonas andprimary-export (agriculture and pecuary) activities inMato Grosso), and is also due to its large geographicaland low population densities which, according toFig. 2, do not accurately reflect the economic situationof less developed states.

9. Except for the Gini variable.10. This method is appropriate when the independent vari-

ables used in regressions are endogenous and requiresome type of control for the simultaneity or reverse caus-ality and endogeneity.

11. Since the variable liquidity preference of banks (LPB) ismeasured at the bank branch level, and in the remoterregions the portfolio allocation decision might be limitedto more basic financial assets (such as loans or deposits), arise in bank liquidity preference (during expansions) maydrive banks tobuymore liquid and less risky assets in national

financial markets and therefore reduce the supply of creditregionally. In the reverse case, a reduction in liquidity prefer-ence (during recessions) contributes to higher instability incredit availability alongside business cycles.

12. The information on bonds and derivatives was extractedfrom account 1300 of the Information System of theCentral Bank of Brazil (SISBACEN).

13. Some authors (MENEZES et al., 2007) opt for exclusionfrom the Federal District due to this being the capital ofBrazil and the headquarters of the major public banks.Some transactions are carried out (both asset and liability)that produce values which do not necessarily correspondto the behaviour of banks, but are due to the specificcharacteristics of the government.

14. The authors tried to add a default measure to the modelin order to capture greater sensitivity on the demand side(the capacity of default of borrowers), as well as the pro-vision for credit (once it interferes with the risk of banks,therefore, it affects their decision in offering moreresources or even renegotiating debt). Since the dataseries from the Brazilian Central Bank was not availablefor all years considered, the default measure was notincluded in the estimates.

15. For example, BERGER (2003) argued that the expansionof technology would increase productivity and alter thestructure of the financial system in terms of loanvolume and variety of banking services, as well as redu-cing the costs (economies of scale).

REFERENCES

AKERLOF G. A. (1970) The market for ‘lemons’: quality uncertainty and the market mechanism,Quarterly Journal of Economics 84(3),488–500.

AMADO A. (1997) Disparate Regional Development in Brazil. Ashgate, Aldershot.AMADO A. M. (2006) Impactos regionais do processo de reestruturação bancária do início dos anos 1990, in JAIME JR F. G. and

CROCCO M. (Eds)Moeda e território: uma interpretação da dinâmica regional brasileira, pp. 147–168. Autêntica, Belo Horizonte, MG.ARELLANO M. and BOVER O. (1995) Another look at the instrumental variable estimation of error-components models, Journal of

Econometrics 68, 29–51.AZZONI C. R. (1999) Concentração regional e dispersão das rendas per capita estaduais: análise a partir das séries históricas estaduais

de PIB, 1939–95, Estudos Econômicos 27(3), 341–393.BALTAGI B. H. (2005) Econometric Analysis of Panel Data, 3rd Edn. Wiley, Chichester.BERGER A. N. (2003) The economic effects of technological progress: evidence from the banking industry, Journal of Money, Credit,

and Banking 35(2), 141–176.BERNANKE B., GERTLER M. and GILCHRIST S. (1999) The financial accelerator and the flight to quality, Review of Economics and

Statistics 78(1), 1–15.BORTS G. H. (1968) Regional economic models. Growth and capital movements among US regions in the post-war period,

American Economic Review 58(2), 155–161.CAMERON A. C. and TRIVEDI P. K. (2010) Microeconometrics using Stata, Revd Edn. Stata Press, College Station, TX.CARVALHO F. J. C. (2005) Sobre a preferência pela liquidez dos bancos, in DE PAULA L. F. and OREIRO J. L. C. (Eds) Eficiência do

Sistema Financeiro: avaliando a funcionalidade do setor bancário brasileiro, pp. 3–21. Elsevier.CHICK V. (1986) The evolution of the banking system and the theory of saving, investment and interest, Économies et Sociétés (Série

Monnaie et Production, 3) 20(8–9), 111–127.CHICK V. (1988) The evolution of the banking system and the theory of monetary policy. Paper presented at the Symposium on

‘Monetary Theory and Monetary Policy: New Tracks for the 1990s’, Berlin, Germany, 1988.CHICK V. (1993) The evolution of the banking system and the theory of monetary policy, in FROWEN S. F. (Ed.) Monetary Theory

and Monetary Policy: New Tracks for the 1990s, pp. 79–92. Macmillan, London.CHICK V. and DOW S. C. (1988) Post-Keynesian perspective on the relation between banking and regional development, in

ARESTIS P. (Ed.) Post-Keynesian Monetary Economics: New Approaches to Financial Modelling. Elgar, Aldershot.CROCCO M., CAVALCANTE A. and BARRA C. (2005) The behavior of liquidity preference of banks and public and regional devel-

opment: the case of Brazil, Journal of Post-Keynesian Economics 28(2), 217–240.

894 Marco Crocco et al.

Dow

nloa

ded

by [

Uni

vers

ity o

f L

a L

agun

a V

icer

rect

orad

o] a

t 02:

31 0

1 Se

ptem

ber

2014

CROCCOM. and FIGUEIREDO A. T. L (2008) Estratégias, bancárias diferenciadas no território: uma análise exploratória, XIII EncontroNacional de Economia Política (available at: http://www.sep.org.br/artigo/1261_0c91861b6ab6b4d79d0adb55d195c2e1.pdf)(accessed February 2010).

DEMIRGUC-KUNT A. and LEVINE R. (2004) Financial Structure and Economic Growth: A Cross-Country Comparison of Banks, Markets,and Development. MIT Press, Cambridge, MA.

DINIZ C. C. (1993) Desenvolvimento poligonal no Brasil: nem desconcentração nem contínua polarização, Nova Economia 3(1),35–64.

DOW S. C. (1987a) Money and regional development, Studies in Political Economy 23(2), 73–94.DOW S. C. (1987b) The treatment of money in Regional Economics, Journal of Regional Science 27(1), 13–24.DOW S. C. (1990) Financial Markets and Regional Economic Development: The Canadian Experience. Avebury, Aldershot.DOW S. C. (1992) The regional financial sector: a Scottish case study, Regional Studies 26(7), 619–631.DOW S. C. (1993) Money and the Economic Process. Edward Elgar, Cambridge.DOW S. C. (1998) Knowledge, information and credit creation, in ROTHEIM R. (Ed.) New Keynesian Economics/Post-Keynesian

Alternatives, pp. 214–226. Routledge, London.DOW S. C. and RODRÍGUEZ-FUENTES C. J. (1997) Regional Finance: a survey, Regional Studies 31(9), 903–920.FURTADO C. (1976) Formação econômica do Brasil. Editora Nacional, São Paulo.GREENWALD B. C., LEVINSON A. and STIGLITZ J. E. (1993) Capital market imperfections and regional economic development, in

GIOVANNINI A. (Ed.) Finance and Development: Issues and Experience, pp. 63–93. Cambridge University Press, Cambridge.INSTITUTO BRASILEIRO DE GEOGRAFIA E ESTATÍSTICA (IBGE) (n.d) Homepage (available at: http://www.ibge.gov.br) (accessed

February 2010).INSTITUTO DE PESQUISA ECONÔMICA E APLICADA (IPEADATA) (2010) Homepage (available at: http://www.ipeadata.gov.br)

(accessed February 2010).KEYNES J. M. (1936) The General Theory of Employment, Interest and Money. Macmillan, London.LAWRENCE P. (2006) Finance and development: why should causation matter?, Journal of International Development 18, 997–1016.LEMOS M. B., DINIZ C. C., GUERRA L. P. and MORO S. (2003) A nova configuração regional Brasileira e sua geografia econômica,

Estudos Econômicos 33(4), 665–700.LEVINE R. (1997) Financial development and economic growth: views and agenda, Journal of Economic Literature 35(2), 688–726.MENEZES M., CROCCO M., SANCHES E. and AMADO A. (2007) Sistema financeiro e desenvolvimento regional: notas explicativas, in

OREIRO J. L. and PAULA L. F. (Eds) Sistema financeiro: uma análise do setor bancário. Elsevier, Rio de Janeiro.MOORE C. L. and HILL J. M. (1982) Interregional arbitrage and the supply of loanable funds, Journal of Regional Science 22(4),

499–512.MOORE C. L. and NAGURNEY A. (1989) A general equilibrium model of interregional monetary flows, Environment and Planning A

21(3), 397–404.ROBERTS R. B. and FISHKIND H. (1979) The role of monetary forces in regional economic activity: an econometric simulation

analysis, Journal of Regional Science 19(1), 15–29.RODRÍGUEZ-FUENTES C. J. (1998) Credit availability and regional development, Papers in Regional Science 77(1), 63–75.RODRÍGUEZ-FUENTES C. J. (2006) Regional Monetary Policy. Routledge, New York, NY.RODRÍGUEZ-FUENTES C. J. and DOW S. C. (2003) EMU and the regional impact of monetary policy, Regional Studies 37(9),

973–984.ROMERO J. P. and JAYME JR F. G. (2008) Sistema financeiro, inovação e desenvolvimento regional: um estudo sobre a relação entre

preferência pela liquidez e inovação no Brasil. Paper presented at the Annual Meeting of Economics – ANPEC Brasil, 2008.SICSÚ J. and CROCCOM. (2003) Em busca de uma teoria da localização das agências bancárias: algumas evidências do caso brasileiro,

Revista de Economia 4(1), 85–112.STATACORP (2008) Stata Statistical Software: Release: 10. StataCorp LP, College Station, TX.STIGLITZ J. E. and GREENWALD B. C. N. (2003) Towards a New Paradigm in Monetary Economics. Cambridge University Press,

Cambridge.STUDART R. (1996) The efficiency of financial systems, liberalization and economic development, Journal of Post-Keynesian

Economics 18(2), 269–292.WOOLDRIDGE J. M. (2001) Econometrics Analysis of Cross-Section and Panel Data. MIT Press, Cambridge, MA.

Banks and Regional Development: Determinants of Credit Availability in Brazilian Regions 895

Dow

nloa

ded

by [

Uni

vers

ity o

f L

a L

agun

a V

icer

rect

orad

o] a

t 02:

31 0

1 Se

ptem

ber

2014