Embed Size (px)

Citation preview

ed: CK/ sa: PY, CS

Resilient packaging demand despite COVID-19 pandemic • Packaging demand to grow at CAGR of c.3-4%

• Upstream chemical players more affected by

environmental concerns than packaging producers

• Strong demand for hygiene and medical products can

boost the prices of certain chemicals in short-run

• PTL, SCGP and UTP are the winners

Packaging demand to grow at CAGR of c.3-4% over 2019-2022F, driven by megatrend of i) booming e-commerce, ii) low packaging penetration rate, iii) rising transportation/logistic activity, iv) COVID-19 pandemic concerns, v) demographics and lifestyle changes, vi) uptrend for fast-moving consumer goods (FMCGs), and vii) uptrend for parcel delivery services.

Upstream chemical players hit by environmental concerns and single-use plastic ban. Polystyrene (PS), Polyethylene (PE) and Polypropylene (PP) are the key raw materials of single-use plastic and are slated to be banned in the near future. As a result, upstream chemical players such as IRPC Plc (IRPC TB) and PTT Global Chemical (PTTGC TB) will be the most affected.

Increasing awareness of cleanliness and hygiene driven by COVID-19 pandemic. During the outbreak of COVID-19, there was a shortage of medical equipment and hygiene products – thanks to a spike in demand during 1H20. In turn, this has led to a surge in demand for certain chemical materials that are the key components for producing medical equipment and hygiene products, such as PE, PP, Polyethylene Terephthalate (PET) and butadiene, as there are still no signs that the coronavirus can be contained, at least in short-run.

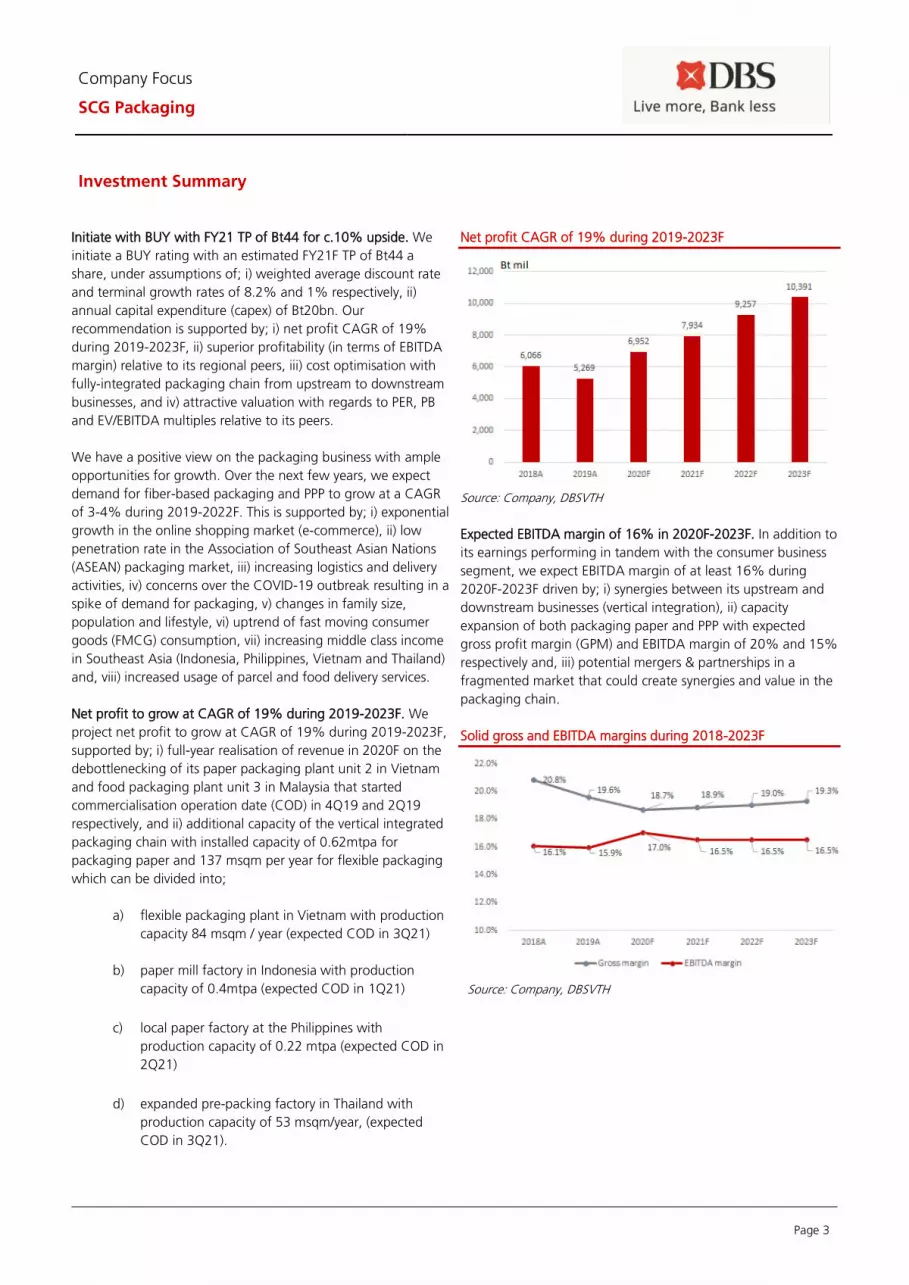

PTL, SCGP and UTP are clear winners. According to 2Q20 results, sales of consumer products dropped by c.20% q-o-q, due to mall closures and travel restrictions caused by the COVID-19 pandemic. However, the packaging business’s performance was rather resilient than the overall consumer sector, as c.50-70% of the former’s sales volumes involve consumer staple goods. Additionally, packaging players are less affected by environmental concerns due to the higher recyclability of their products.

SET : 1,433.56

Analyst

Duladeth BIK, CFA, FRM, CAIA +66 28577833

Thailand Research Team +66 28577833; [email protected]

Index performance (year-to-date basis)

Source: SETSMART, DBSVTH, data as of 18 Nov 2020

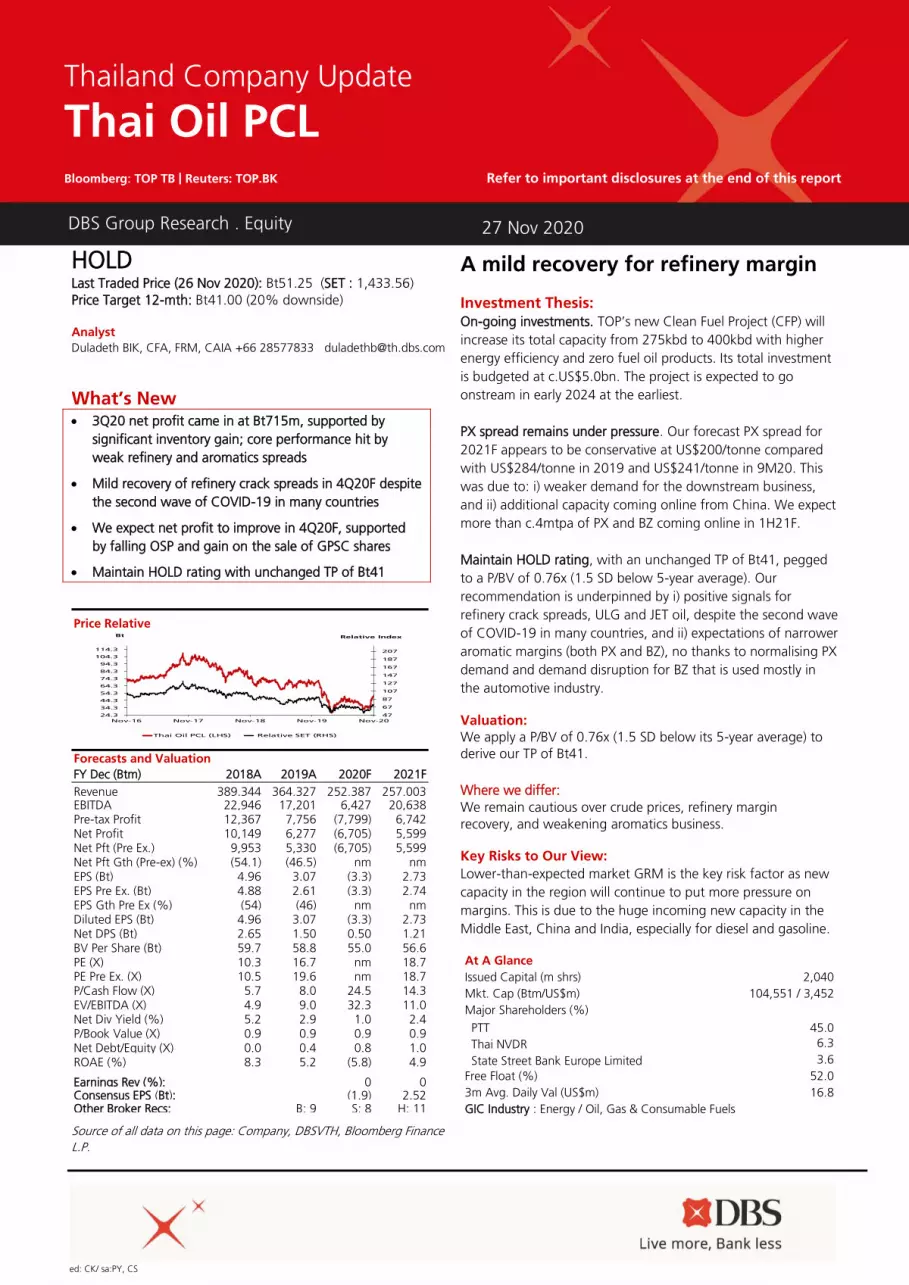

DBS Group Research . Equity

27 Nov 2020

Asian Insights SparX: Resilient packaging demand while

sustainability principles remain intact

Chemical/Packaging/Paper Refer to important disclosures at the end of this report

STOCKS

12-mth

Price Mkt Cap Target Price Performance (%)

Bt US$m Bt 3 mth 12 mth Rating

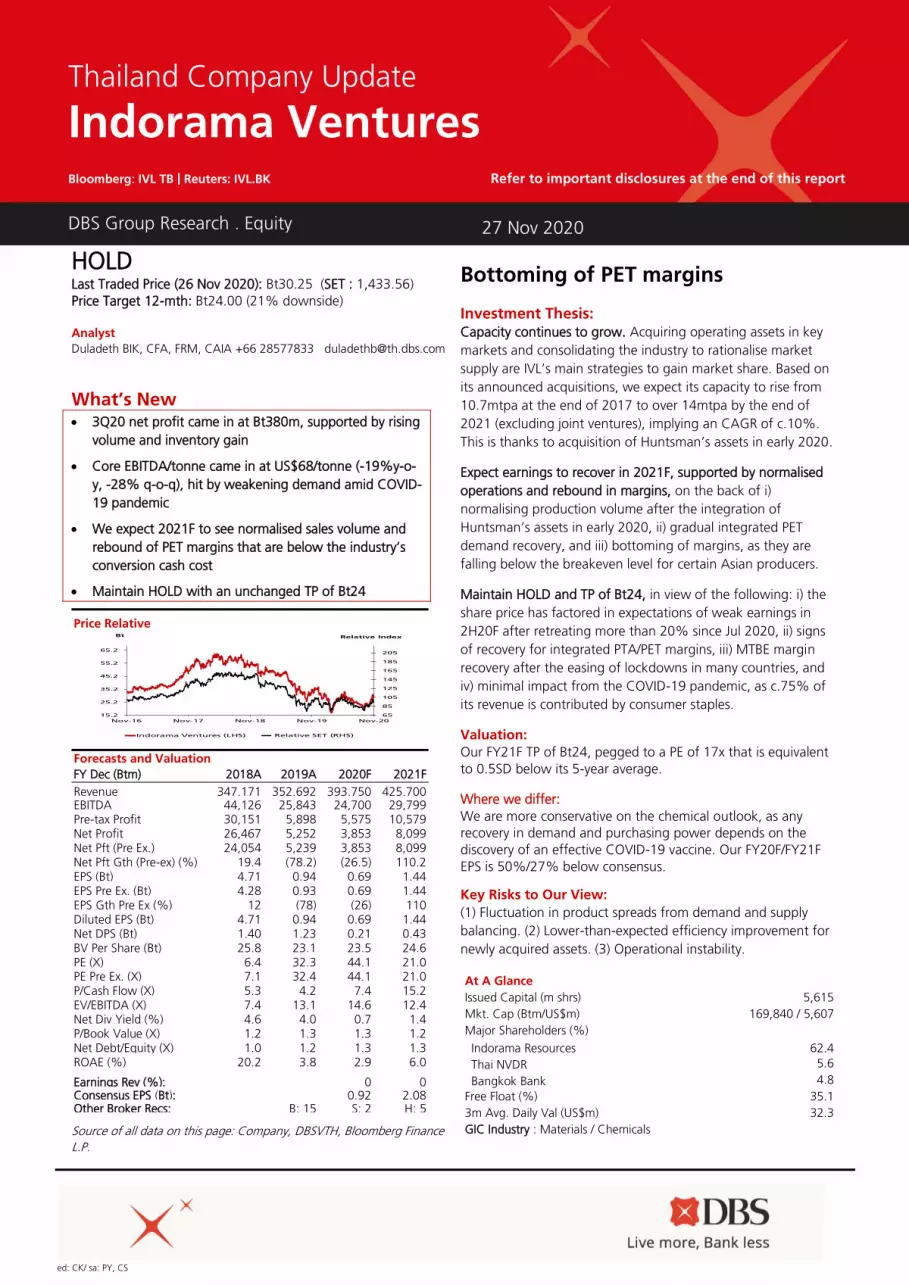

Indorama Ventures 30.25 5,607 24.00 24.5 (13.6) HOLD

IRPC PCL 2.88 1,943 2.30 18.0 (17.7) HOLD

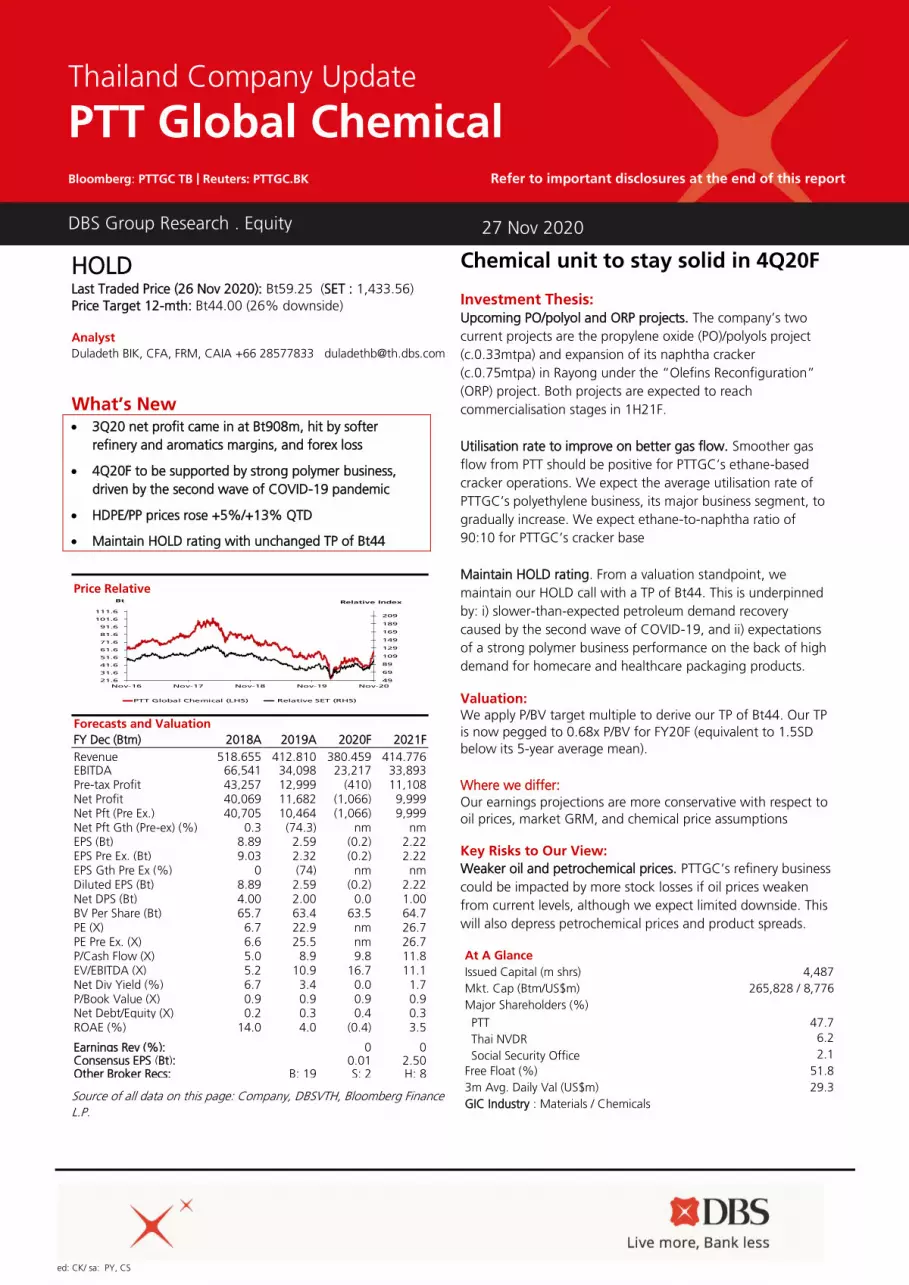

Polyplex (Thailand) 22.30 663 27.50 (10.8) 58.2 BUY

PTT Global

Chemical 59.25 8,776 44.00 24.7 8.7 HOLD

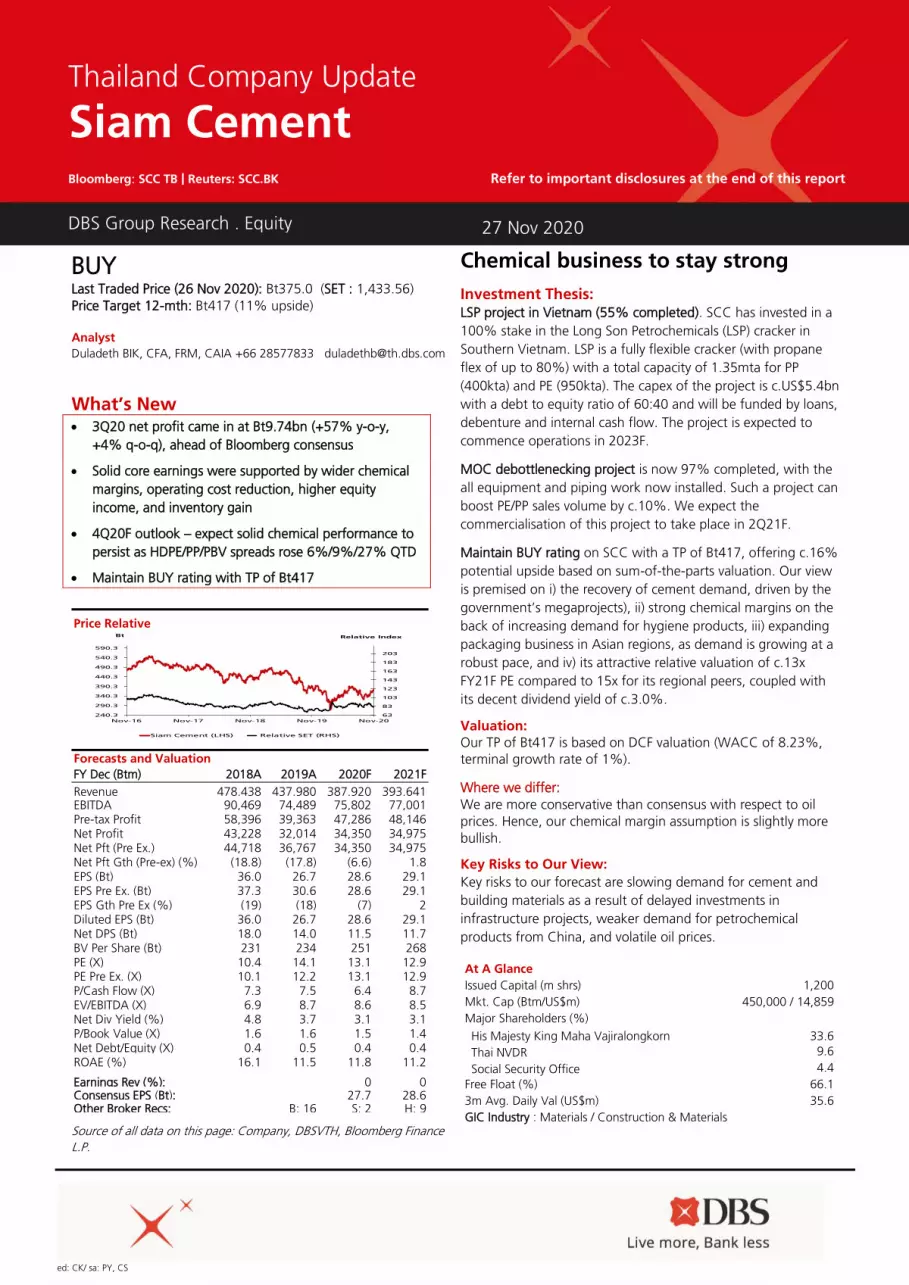

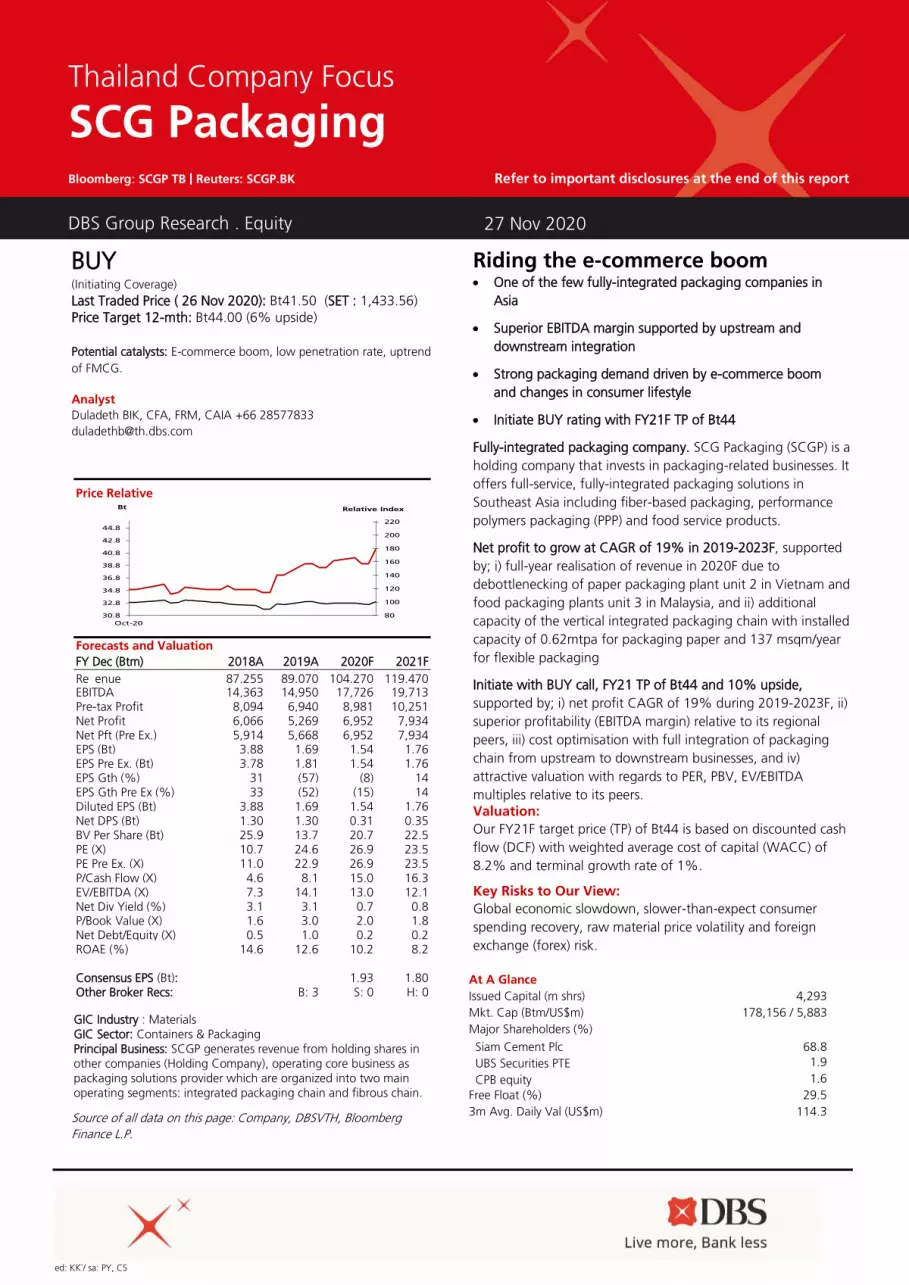

Siam Cement 375 14,855 417 7.8 (4.6) BUY

SCG Packaging

PCL 41.50 5,881 44.00 N.A N.A BUY

Thai Oil PCL 51.25 3,451 41.00 19.2 (27.3) HOLD

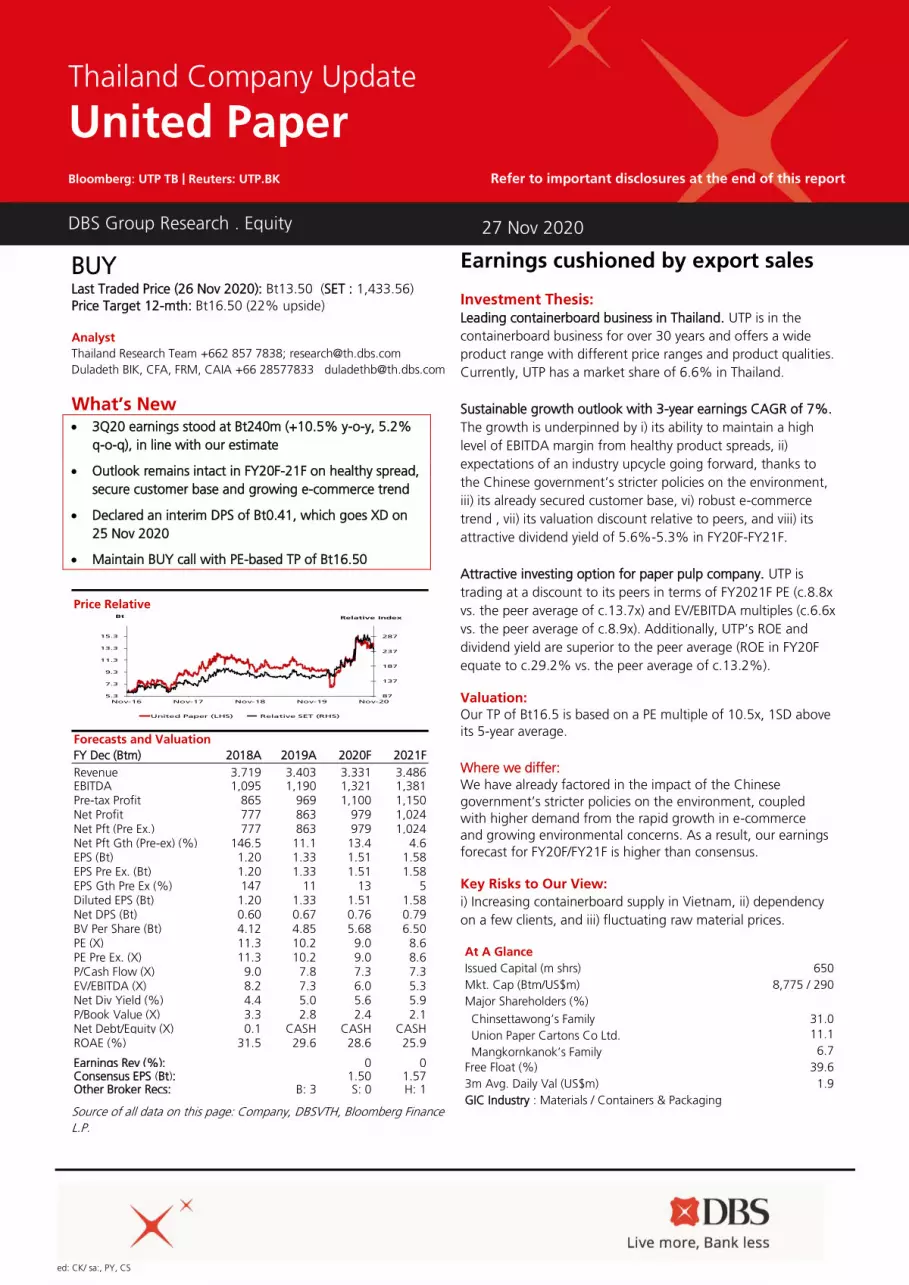

United Paper 13.50 290 16.50 (8.8) 37.8 BUY

Asian Insights SparX: Resilent packaging

demand while sustainability remains intact

Chemical/Packaging/Paper

Page 2

The DBS Asian Insights SparX report is a deep dive look into thematic angles impacting the longer term investment thesis for a sector, country or the region. We view this as an ongoing conversation rather than a one off treatise on the topic, and invite feedback from our readers, and in particular welcome follow on questions worthy of closer examination.

Table of Contents

Executive Summary 3

What is packaging? 8

Part 1: Resilient packaging demand driven by megatrends 9

Part 2: Long-run impact from environmental concern and sustainability principles 20

Part 3: Outbreak of COVID-19 boosts demand for certain types of plastic 26

Part 4: Implications and selection of winners 29

Stock Profile 37

Indorama Ventures 38

IRPC PCL 44

Polyplex (Thailand) 50

PTT Global Chemical 57

Siam Cement 63

SCG Packaging PCL 69

Thai Oil PCL 94

United Paper 101

Asian Insights SparX: Resilent packaging

demand while sustainability remains intact

Chemical/Packaging/Paper

Page 3

Executive Summary

Resilient packaging business amid COVID-19 pandemic. While

the global economy is being hit by the pandemic of COVID-

19, we think business segments related to consumer staples

goods and consumption, such as packaging, will be more

resilient than those related to cyclicality and exports such as

commodities and tourism. According to the 2Q20 results of

the consumer/commerce sectors, the revenue of key

consumer players such as HomePro, CPALL and Robinson

Department Store, to name a few, dropped by c.20% q-o-q,

weighed down by travel restrictions, city lockdowns, malls

closures during Mar-May 2020. On the other hand, the

packaging business was rather resilient than the overall

consumer sector with the former’s total sales volume, on

average, coming in flat. We believe that the reasons behind

the packaging business’s resilient sales volume are i) c.70% of

packaging sales volume came from consumer staples which

were least affected by the pandemic, ii) packaging cost

accounted for only c.3-4% of the total cost of finished

products, and iii) demand stickiness from food and beverage

manufacturers that are reluctant to change packaging

supplies for the fear of eroding the quality of their product

packaging.

Evidently, based on the data compiled by McKinsey, online

sales of grocery and fresh food in China doubled within a 10-

day period in Jan 2020, at the early stage of the country’s

outbreak of COVID-19. Moreover, there is a spike in volume

of online shopping as well as rising demand for delivery

services (both food and beverage and parcel), due to work-

from-home policies, and the high demand for medical care

and hygiene products. Hence, packaging products such as

corrugated paper, flexible, and rigid plastic were in high

demand.

Expect resilent packaging demand during 2020-2022F, driven

by megatrends. The outbreak of the COVID-19 pandemic in

early 2020 has caused disruptions to businesses and economic

activities the world over. This has temporarily led to a global

economic slowdown, and the packaging business is no

exception. However, we believe the adverse impact on

packaging demand would be limited in view of i) c.70% of

packaging material is used in consumer stable goods which

were least affected by the pandemic, ii) demographics and

lifestyle changes that will lead to a gradual increase in

packaging demand over time, and iii) the boom of e-

commerce that is supported by internet network

advancements and greater internet penetration rate.

As a result, we expect the demand for packaging, both paper-

based and polymer-based products, to remain solid and grow

at a CAGR of 3-4% in during 2019-2022F, driven by the

following factors: i) the boom of online shopping (e-

commerce), ii) low packaging penetration rate in ASEAN, iii)

rising transportation activity, iv) COVID-19 pandemic

concerns, v) demographic and lifestyle changes, vi) uptrend

for FMCG, vii) rising income from the middle class in

Southeast Asia (Indonesia, the Philippines, Vietnam and

Thailand), viii) improving Internet network and penetration

rate, ix) increasing digital banking transactions, x) uptrend for

parcel delivery services and cheaper delivery fee, and xi)

growing popularity of social and mobile commerce services.

More negative impact for chemical players than packaging

producers with respect to environmental concerns and

sustainability principles

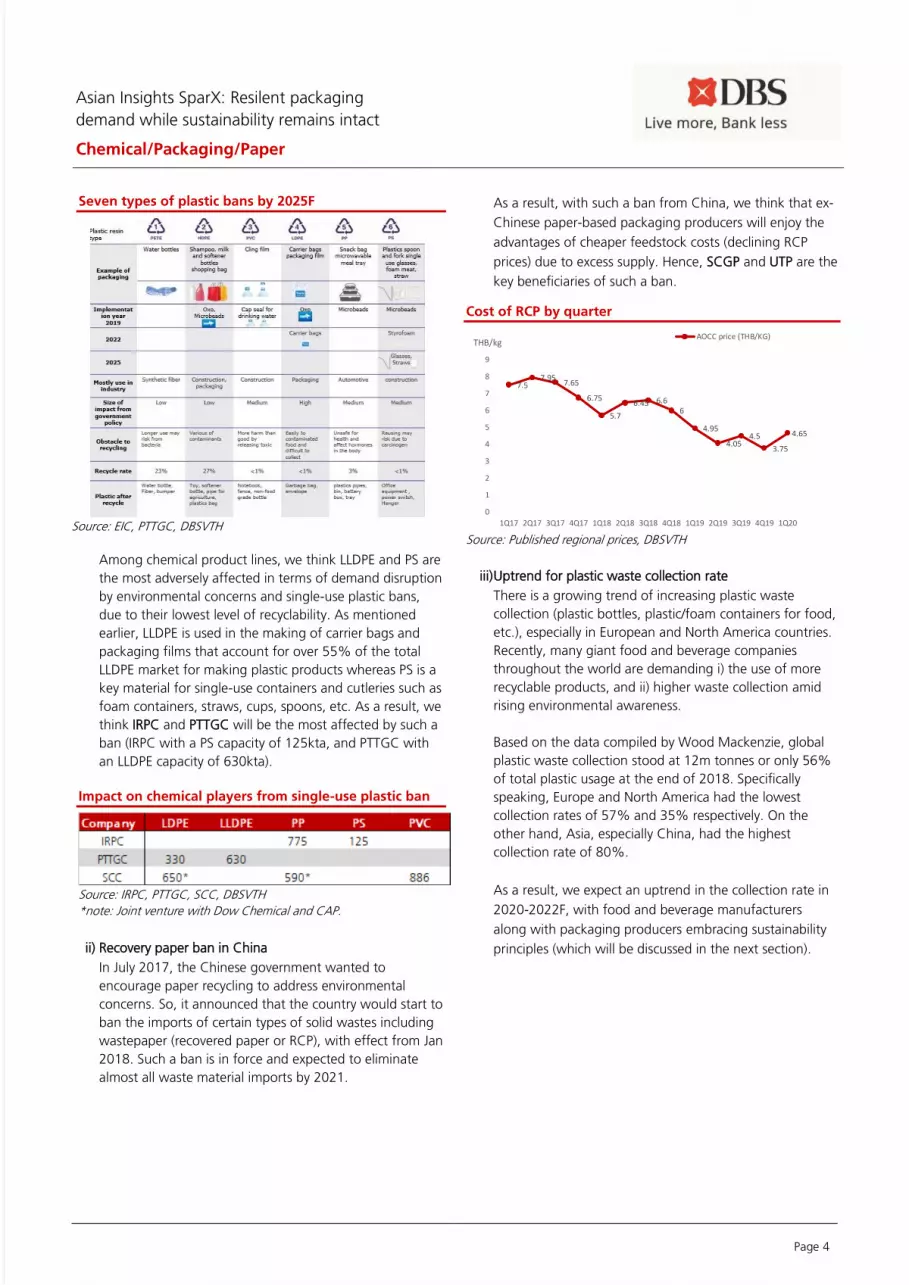

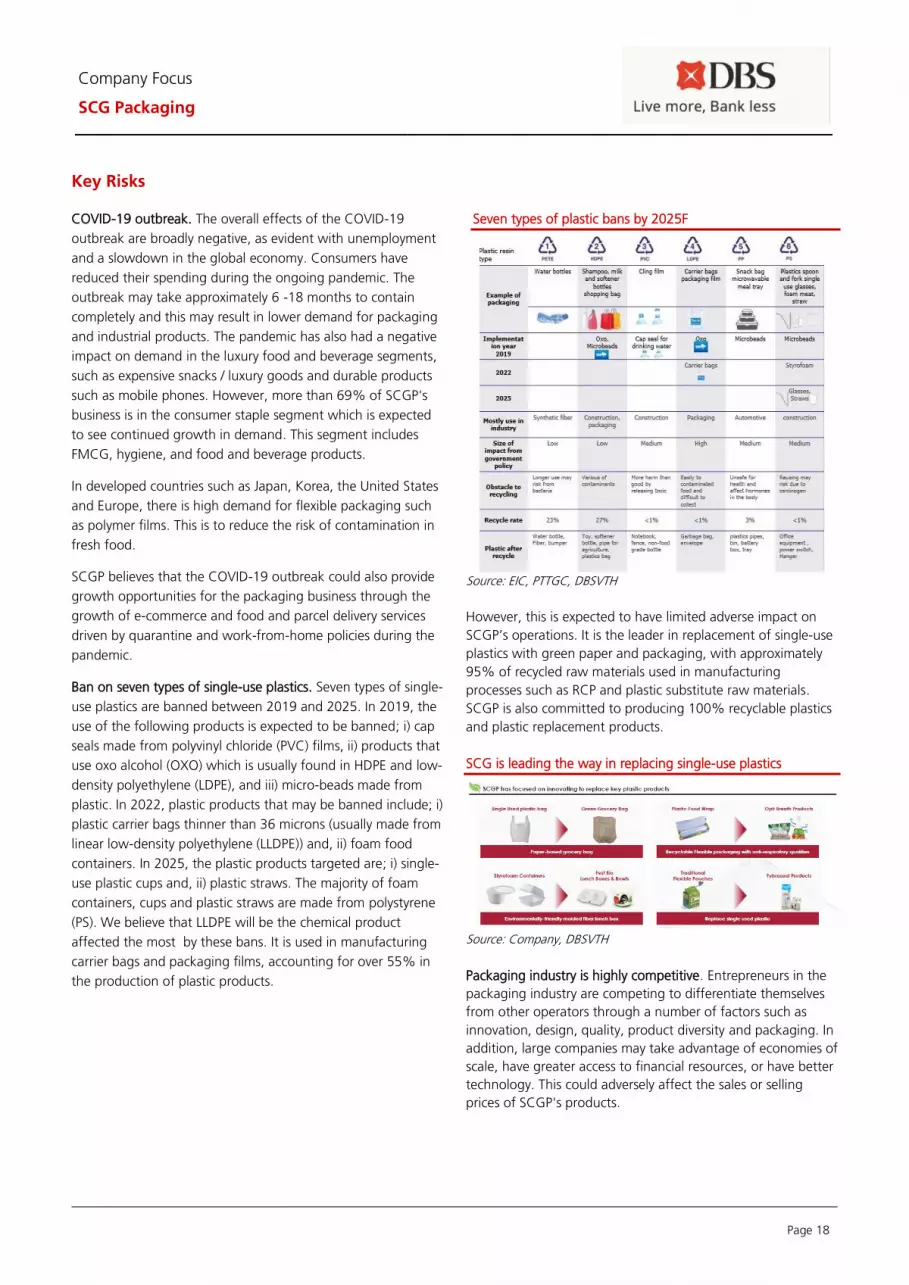

i) Ban on seven types of single-use plastics

In 2018, the sub-committee on plastic waste management

looked at the plan of action on reducing and banning the

use of seven types of single-use plastics between 2019

and 2025. In 2019, the use of the following products is

expected to be banned i) cap seals made from PVC films,

ii) products that use Oxo alcohol (OXO), which is usually

found in HDPE and LDPE, and iii) micro-beads made from

plastic. In 2022, the targeted plastic products to be

banned include i) plastic carrier bags that are thinner than

36 microns (usually made from LLDPE), and ii) foam food

containers. As for 2025, the plastic products being

targeted are i) single-use plastic cups and ii) plastic straws.

The majority of foam containers, cups, and plastic straws

are made from PS. We believe LLDPE will be the most

affected chemical product. This because it is used in the

making of carrier bags and packaging films, accounting

for over 55% in the process of producing plastic products.

Asian Insights SparX: Resilent packaging

demand while sustainability remains intact

Chemical/Packaging/Paper

Page 4

Seven types of plastic bans by 2025F

Source: EIC, PTTGC, DBSVTH

Among chemical product lines, we think LLDPE and PS are

the most adversely affected in terms of demand disruption

by environmental concerns and single-use plastic bans,

due to their lowest level of recyclability. As mentioned

earlier, LLDPE is used in the making of carrier bags and

packaging films that account for over 55% of the total

LLDPE market for making plastic products whereas PS is a

key material for single-use containers and cutleries such as

foam containers, straws, cups, spoons, etc. As a result, we

think IRPC and PTTGC will be the most affected by such a

ban (IRPC with a PS capacity of 125kta, and PTTGC with

an LLDPE capacity of 630kta).

Impact on chemical players from single-use plastic ban

Source: IRPC, PTTGC, SCC, DBSVTH

*note: Joint venture with Dow Chemical and CAP.

ii) Recovery paper ban in China

In July 2017, the Chinese government wanted to

encourage paper recycling to address environmental

concerns. So, it announced that the country would start to

ban the imports of certain types of solid wastes including

wastepaper (recovered paper or RCP), with effect from Jan

2018. Such a ban is in force and expected to eliminate

almost all waste material imports by 2021.

As a result, with such a ban from China, we think that ex-

Chinese paper-based packaging producers will enjoy the

advantages of cheaper feedstock costs (declining RCP

prices) due to excess supply. Hence, SCGP and UTP are the

key beneficiaries of such a ban.

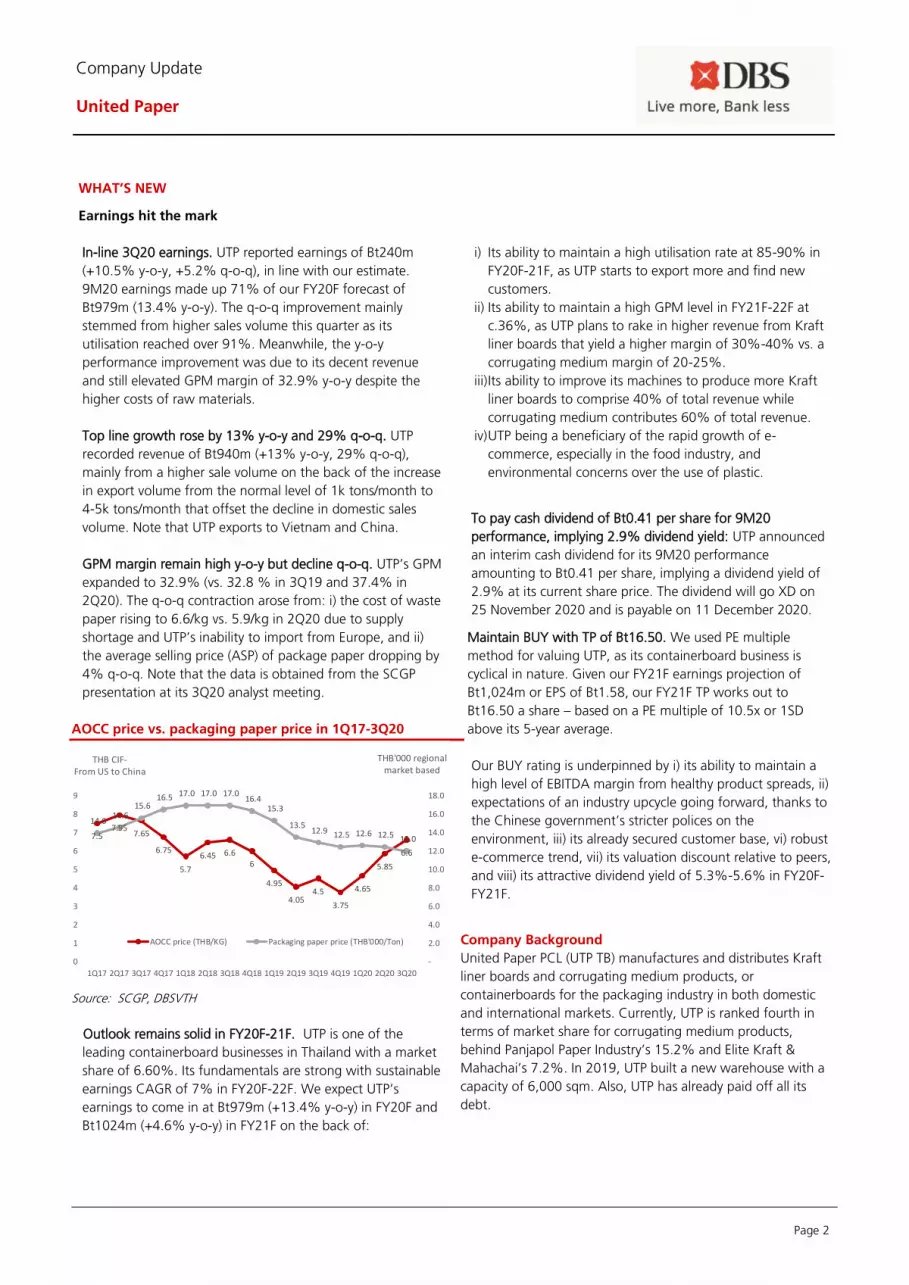

Cost of RCP by quarter

Source: Published regional prices, DBSVTH

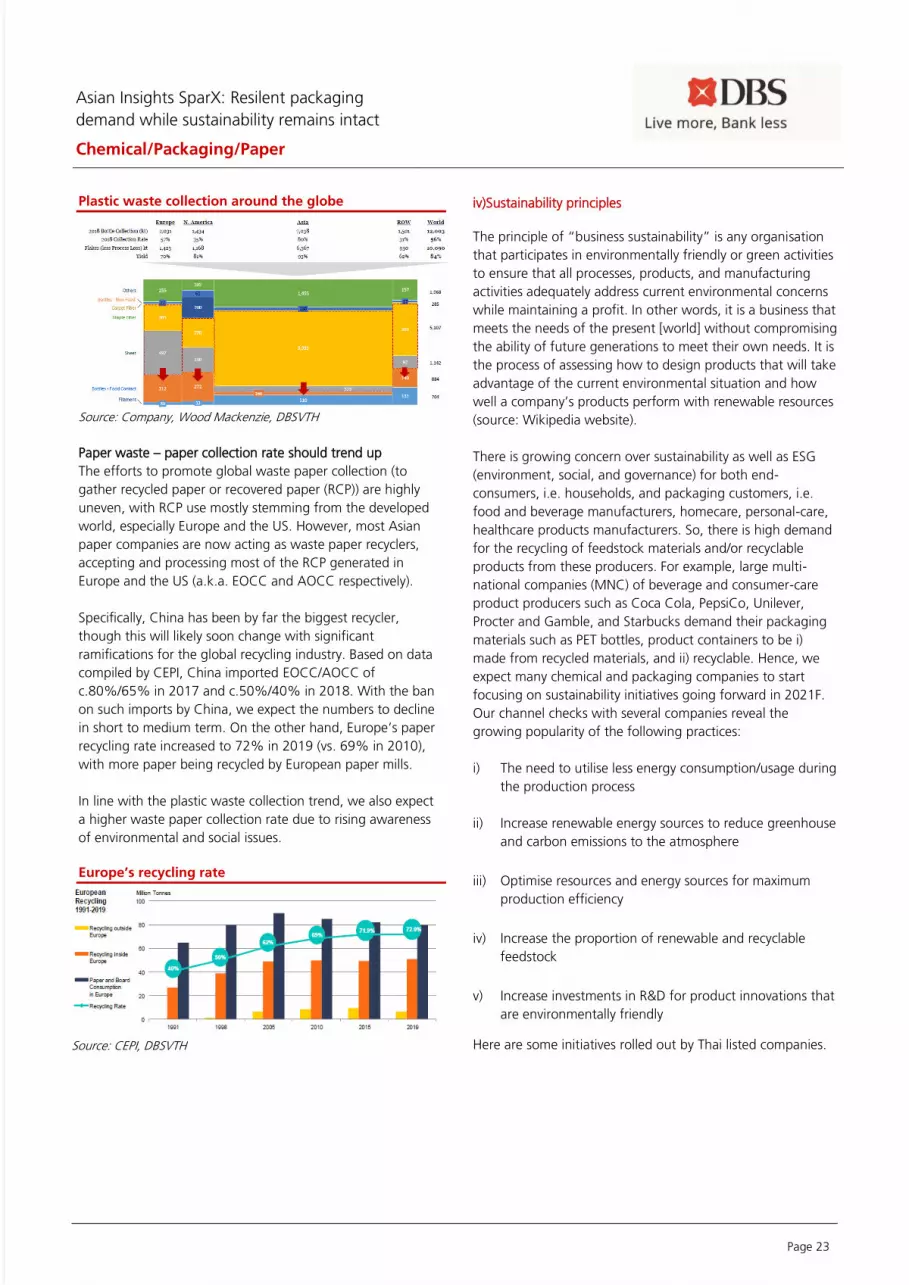

iii) Uptrend for plastic waste collection rate

There is a growing trend of increasing plastic waste

collection (plastic bottles, plastic/foam containers for food,

etc.), especially in European and North America countries.

Recently, many giant food and beverage companies

throughout the world are demanding i) the use of more

recyclable products, and ii) higher waste collection amid

rising environmental awareness.

Based on the data compiled by Wood Mackenzie, global

plastic waste collection stood at 12m tonnes or only 56%

of total plastic usage at the end of 2018. Specifically

speaking, Europe and North America had the lowest

collection rates of 57% and 35% respectively. On the

other hand, Asia, especially China, had the highest

collection rate of 80%.

As a result, we expect an uptrend in the collection rate in

2020-2022F, with food and beverage manufacturers

along with packaging producers embracing sustainability

principles (which will be discussed in the next section).

7.57.95

7.65

6.75

5.7

6.45 6.66

4.95

4.054.5

3.75

4.65

0

1

2

3

4

5

6

7

8

9

1Q17 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18 4Q18 1Q19 2Q19 3Q19 4Q19 1Q20

THB/kgAOCC price (THB/KG)

Asian Insights SparX: Resilent packaging

demand while sustainability remains intact

Chemical/Packaging/Paper

Page 5

Plastic waste collection around the globe

Source: Company, Wood Mackenzie, DBSVTH

iv) Sustainability principles

There is growing concern over sustainability as well as ESG

(environment, social, and governance) for both end-

consumers, i.e. households, and packaging customers, i.e.

food and beverage manufacturers, homecare, personal-

care, healthcare products manufacturers. So, there is high

demand for the recycling of feedstock materials and/or

recyclable products from these producers. For example,

large multi-national companies (MNC) of beverage and

consumer-care product producers such as Coca Cola,

PepsiCo, Unilever, Procter and Gamble, and Starbucks

demand their packaging materials such as PET bottles,

product containers to be i) made from recycled materials,

and ii) recyclable. Hence, we expect many chemical and

packaging companies to start focusing on sustainability

initiatives going forward in 2021F. Our channel checks

with several companies reveal the growing popularity of

the following practices:

a) The need to utilise less energy

consumption/usage during the production

process

b) Increase renewable energy sources to reduce

greenhouse and carbon emissions to the

atmosphere

c) Optimise resources and energy sources for

maximum production efficiency

d) Increase the proportion of renewable and

recyclable feedstock

e) Increase investments in R&D for product

innovations that are environmentally friendly

As a result, most packaging companies are in the process of i)

improving their energy usage and production process

efficiency, ii) investing in projects to reduce their carbon

footprint, iii) developing environmentally friendly and

degradable products, and iv) investing in renewable energy

sources. Hence, we believe they might incur additional cost

that can erode their profitability as a result of complying with

sustainability principles.

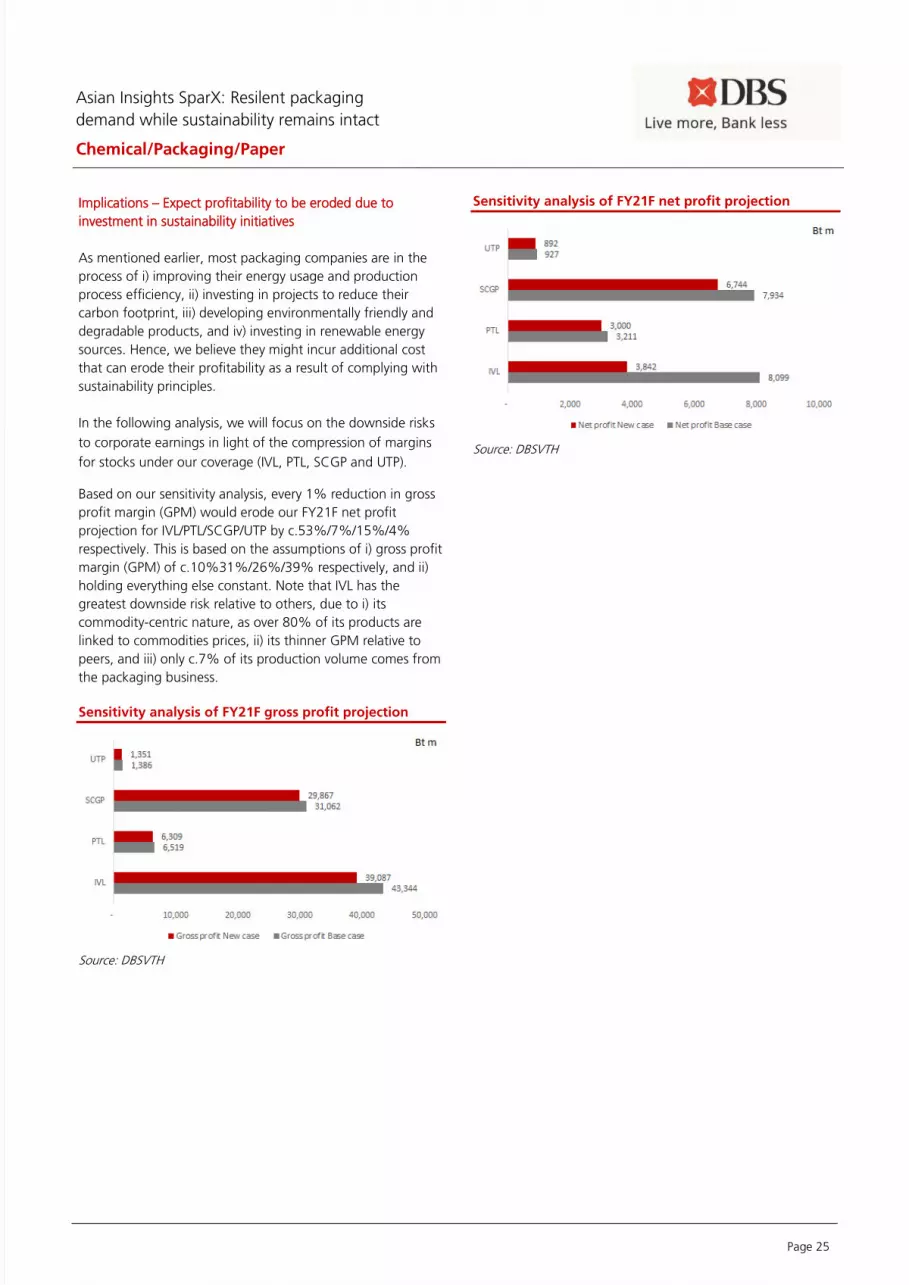

In the following analysis, we will focus on the downside risks

to corporate earnings in light of the compression of margins

for stocks under our coverage (IVL, PTL, SCGP and UTP).

Based on our sensitivity analysis, every 1% reduction in gross

profit margin (GPM) would erode our FY21F net profit

projection for IVL/PTL/SCGP/UTP by c.53%/7%/15%/4%

respectively. This is based on the assumptions of i) gross profit

margin (GPM) of c.10%31%/26%/39% respectively, and ii)

holding everything else constant. Note that IVL has the

greatest downside risk relative to others, due to i) its

commodity-centric nature, as over 80% of its products are

linked to commodities prices, ii) its thinner GPM relative to

peers, and iii) only c.7% of its production volume comes from

the packaging business.

Sensitivity analysis of FY21F net profit

Source: DBSVTH

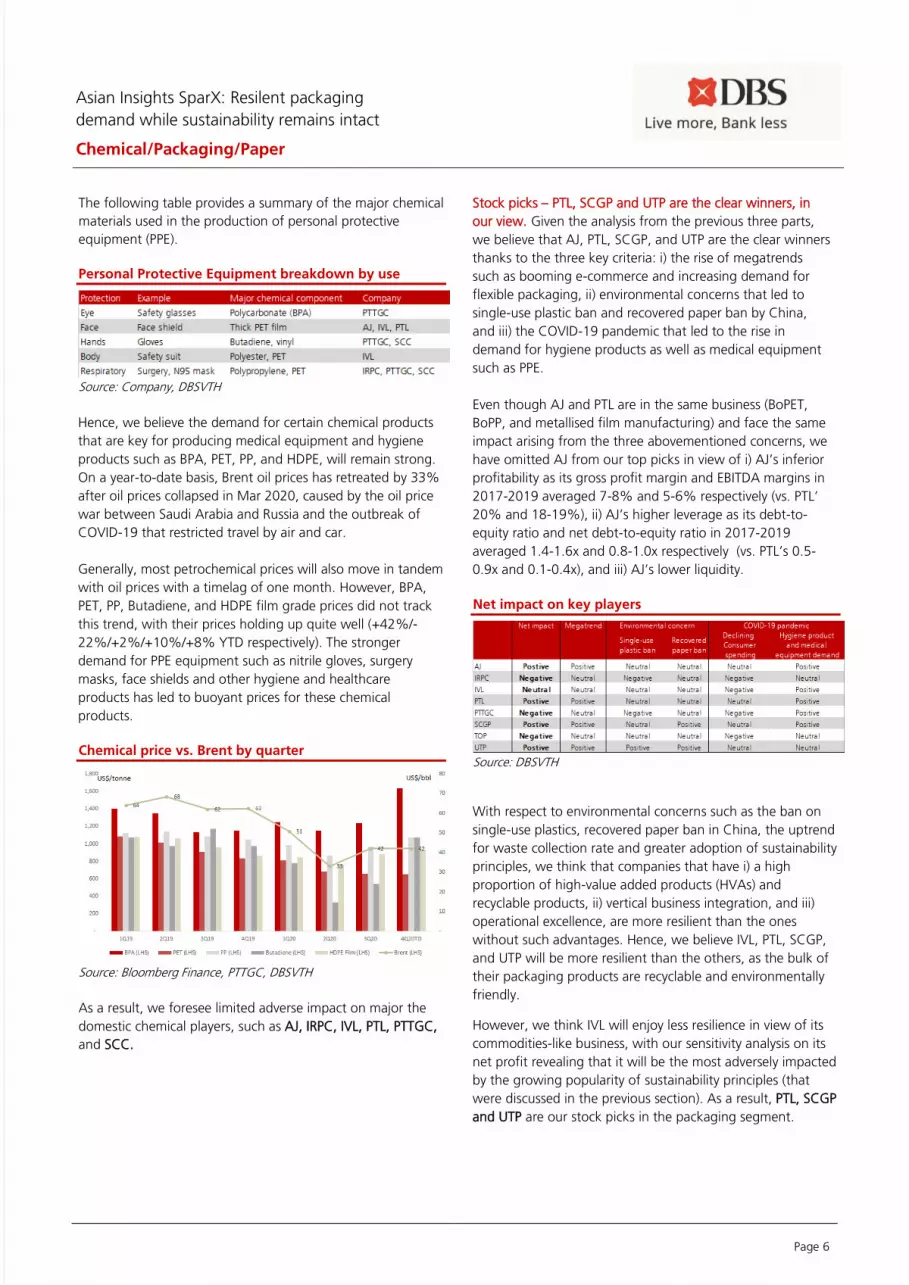

Increasing awareness of cleanliness and hygiene driven by

COVID-19 pandemic. During the outbreak of COVID-19, there

was a shortage of medical, surgery, and personal protective

equipment for the eye and face (safety glasses, and face

shields), hand (natural latex gloves, nitrile gloves, vinyl gloves),

body, and respiratory system (surgery masks, N95 masks, and

full-face respirators). Moreover, there is a spike in demand for

hygiene products in developing countries in Africa, Southeast

Asia, and South America, where the healthcare spending per

capita is relatively lower than the global averages and peers.

Asian Insights SparX: Resilent packaging

demand while sustainability remains intact

Chemical/Packaging/Paper

Page 6

The following table provides a summary of the major chemical

materials used in the production of personal protective

equipment (PPE).

Personal Protective Equipment breakdown by use

Source: Company, DBSVTH

Hence, we believe the demand for certain chemical products

that are key for producing medical equipment and hygiene

products such as BPA, PET, PP, and HDPE, will remain strong.

On a year-to-date basis, Brent oil prices has retreated by 33%

after oil prices collapsed in Mar 2020, caused by the oil price

war between Saudi Arabia and Russia and the outbreak of

COVID-19 that restricted travel by air and car.

Generally, most petrochemical prices will also move in tandem

with oil prices with a timelag of one month. However, BPA,

PET, PP, Butadiene, and HDPE film grade prices did not track

this trend, with their prices holding up quite well (+42%/-

22%/+2%/+10%/+8% YTD respectively). The stronger

demand for PPE equipment such as nitrile gloves, surgery

masks, face shields and other hygiene and healthcare

products has led to buoyant prices for these chemical

products.

Chemical price vs. Brent by quarter

Source: Bloomberg Finance, PTTGC, DBSVTH

As a result, we foresee limited adverse impact on major the

domestic chemical players, such as AJ, IRPC, IVL, PTL, PTTGC,

and SCC.

Stock picks – PTL, SCGP and UTP are the clear winners, in

our view. Given the analysis from the previous three parts,

we believe that AJ, PTL, SCGP, and UTP are the clear winners

thanks to the three key criteria: i) the rise of megatrends

such as booming e-commerce and increasing demand for

flexible packaging, ii) environmental concerns that led to

single-use plastic ban and recovered paper ban by China,

and iii) the COVID-19 pandemic that led to the rise in

demand for hygiene products as well as medical equipment

such as PPE.

Even though AJ and PTL are in the same business (BoPET,

BoPP, and metallised film manufacturing) and face the same

impact arising from the three abovementioned concerns, we

have omitted AJ from our top picks in view of i) AJ’s inferior

profitability as its gross profit margin and EBITDA margins in

2017-2019 averaged 7-8% and 5-6% respectively (vs. PTL’

20% and 18-19%), ii) AJ’s higher leverage as its debt-to-

equity ratio and net debt-to-equity ratio in 2017-2019

averaged 1.4-1.6x and 0.8-1.0x respectively (vs. PTL’s 0.5-

0.9x and 0.1-0.4x), and iii) AJ’s lower liquidity.

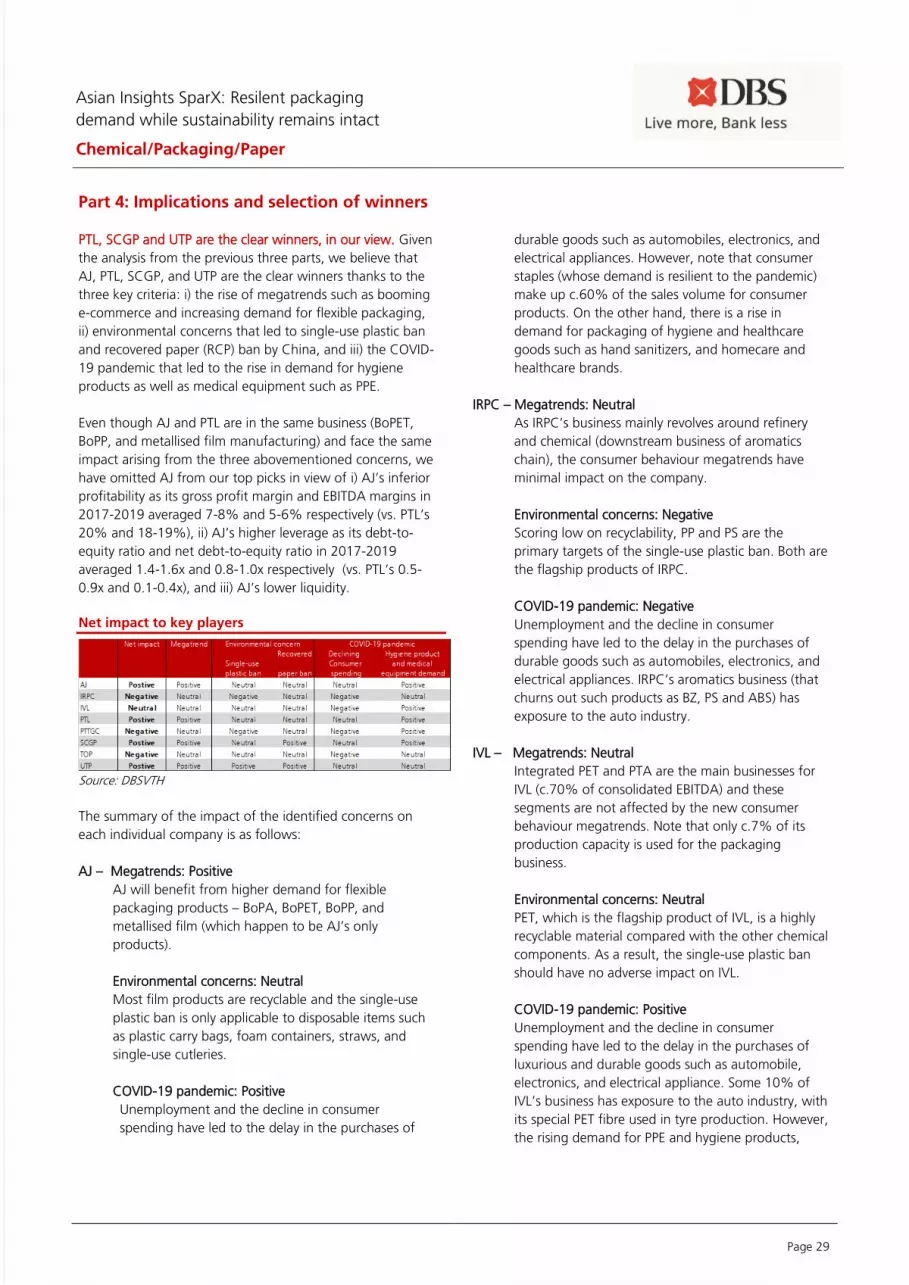

Net impact on key players

Source: DBSVTH

With respect to environmental concerns such as the ban on

single-use plastics, recovered paper ban in China, the uptrend

for waste collection rate and greater adoption of sustainability

principles, we think that companies that have i) a high

proportion of high-value added products (HVAs) and

recyclable products, ii) vertical business integration, and iii)

operational excellence, are more resilient than the ones

without such advantages. Hence, we believe IVL, PTL, SCGP,

and UTP will be more resilient than the others, as the bulk of

their packaging products are recyclable and environmentally

friendly.

However, we think IVL will enjoy less resilience in view of its

commodities-like business, with our sensitivity analysis on its

net profit revealing that it will be the most adversely impacted

by the growing popularity of sustainability principles (that

were discussed in the previous section). As a result, PTL, SCGP

and UTP are our stock picks in the packaging segment.

Asian Insights SparX: Resilent packaging

demand while sustainability remains intact

Chemical/Packaging/Paper

Page 7

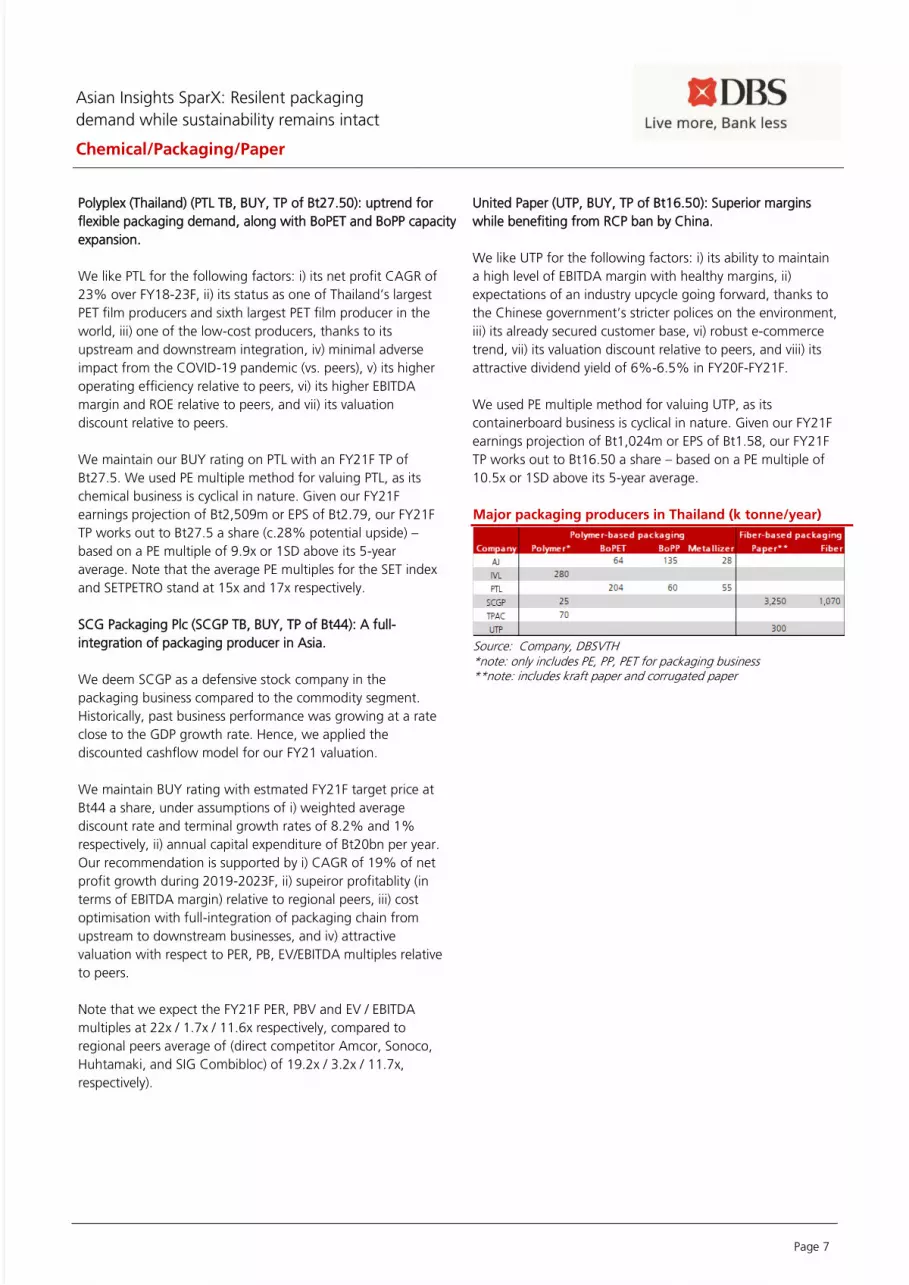

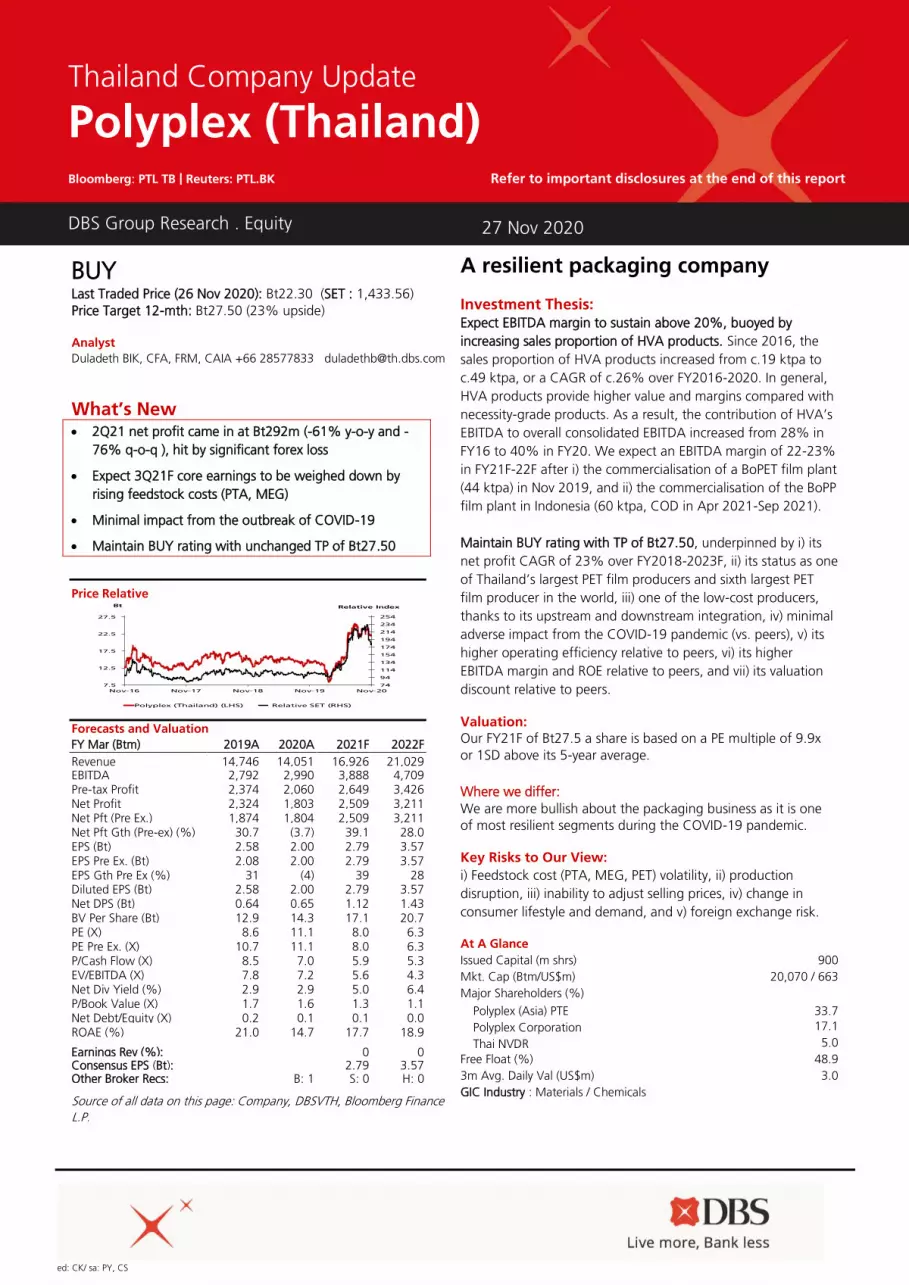

Polyplex (Thailand) (PTL TB, BUY, TP of Bt27.50): uptrend for

flexible packaging demand, along with BoPET and BoPP capacity

expansion.

We like PTL for the following factors: i) its net profit CAGR of

23% over FY18-23F, ii) its status as one of Thailand’s largest

PET film producers and sixth largest PET film producer in the

world, iii) one of the low-cost producers, thanks to its

upstream and downstream integration, iv) minimal adverse

impact from the COVID-19 pandemic (vs. peers), v) its higher

operating efficiency relative to peers, vi) its higher EBITDA

margin and ROE relative to peers, and vii) its valuation

discount relative to peers.

We maintain our BUY rating on PTL with an FY21F TP of

Bt27.5. We used PE multiple method for valuing PTL, as its

chemical business is cyclical in nature. Given our FY21F

earnings projection of Bt2,509m or EPS of Bt2.79, our FY21F

TP works out to Bt27.5 a share (c.28% potential upside) –

based on a PE multiple of 9.9x or 1SD above its 5-year

average. Note that the average PE multiples for the SET index

and SETPETRO stand at 15x and 17x respectively.

SCG Packaging Plc (SCGP TB, BUY, TP of Bt44): A full-

integration of packaging producer in Asia.

We deem SCGP as a defensive stock company in the

packaging business compared to the commodity segment.

Historically, past business performance was growing at a rate

close to the GDP growth rate. Hence, we applied the

discounted cashflow model for our FY21 valuation.

We maintain BUY rating with estmated FY21F target price at

Bt44 a share, under assumptions of i) weighted average

discount rate and terminal growth rates of 8.2% and 1%

respectively, ii) annual capital expenditure of Bt20bn per year.

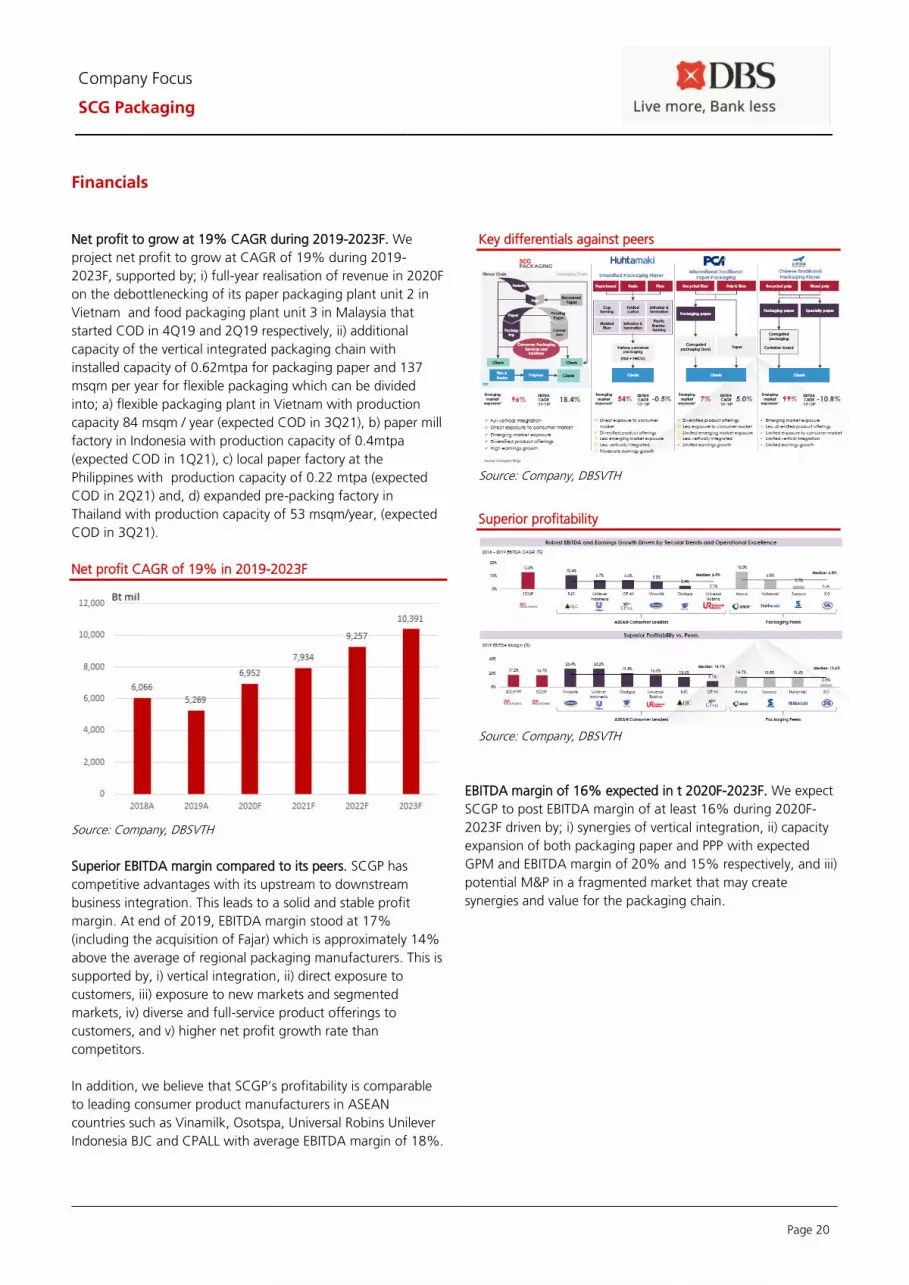

Our recommendation is supported by i) CAGR of 19% of net

profit growth during 2019-2023F, ii) supeiror profitablity (in

terms of EBITDA margin) relative to regional peers, iii) cost

optimisation with full-integration of packaging chain from

upstream to downstream businesses, and iv) attractive

valuation with respect to PER, PB, EV/EBITDA multiples relative

to peers.

Note that we expect the FY21F PER, PBV and EV / EBITDA

multiples at 22x / 1.7x / 11.6x respectively, compared to

regional peers average of (direct competitor Amcor, Sonoco,

Huhtamaki, and SIG Combibloc) of 19.2x / 3.2x / 11.7x,

respectively).

United Paper (UTP, BUY, TP of Bt16.50): Superior margins

while benefiting from RCP ban by China.

We like UTP for the following factors: i) its ability to maintain

a high level of EBITDA margin with healthy margins, ii)

expectations of an industry upcycle going forward, thanks to

the Chinese government’s stricter polices on the environment,

iii) its already secured customer base, vi) robust e-commerce

trend, vii) its valuation discount relative to peers, and viii) its

attractive dividend yield of 6%-6.5% in FY20F-FY21F.

We used PE multiple method for valuing UTP, as its

containerboard business is cyclical in nature. Given our FY21F

earnings projection of Bt1,024m or EPS of Bt1.58, our FY21F

TP works out to Bt16.50 a share – based on a PE multiple of

10.5x or 1SD above its 5-year average.

Major packaging producers in Thailand (k tonne/year)

Source: Company, DBSVTH *note: only includes PE, PP, PET for packaging business **note: includes kraft paper and corrugated paper

Asian Insights SparX: Resilent packaging

demand while sustainability remains intact

Chemical/Packaging/Paper

Page 8

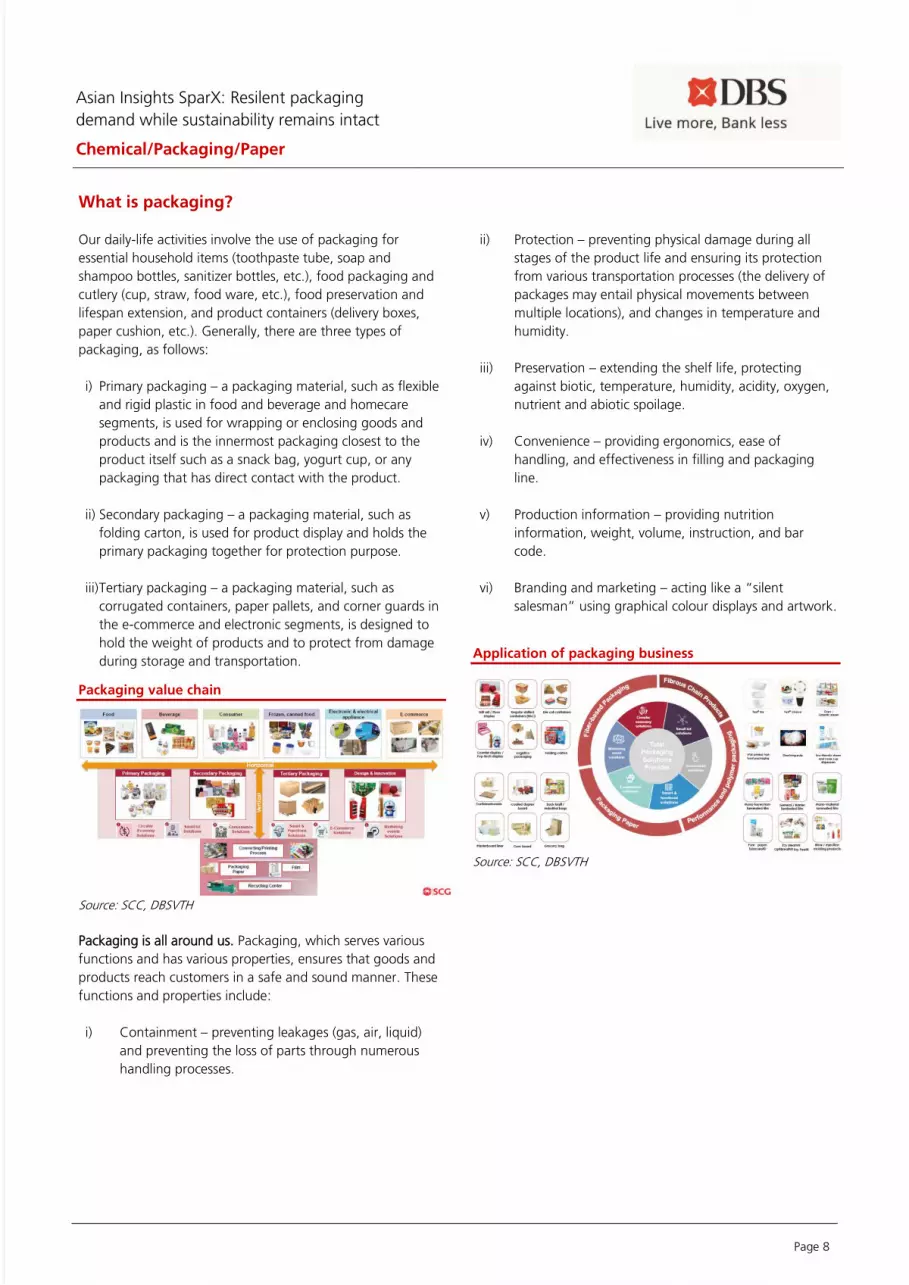

What is packaging?

Our daily-life activities involve the use of packaging for

essential household items (toothpaste tube, soap and

shampoo bottles, sanitizer bottles, etc.), food packaging and

cutlery (cup, straw, food ware, etc.), food preservation and

lifespan extension, and product containers (delivery boxes,

paper cushion, etc.). Generally, there are three types of

packaging, as follows:

i) Primary packaging – a packaging material, such as flexible

and rigid plastic in food and beverage and homecare

segments, is used for wrapping or enclosing goods and

products and is the innermost packaging closest to the

product itself such as a snack bag, yogurt cup, or any

packaging that has direct contact with the product.

ii) Secondary packaging – a packaging material, such as

folding carton, is used for product display and holds the

primary packaging together for protection purpose.

iii) Tertiary packaging – a packaging material, such as

corrugated containers, paper pallets, and corner guards in

the e-commerce and electronic segments, is designed to

hold the weight of products and to protect from damage

during storage and transportation.

Packaging value chain

Source: SCC, DBSVTH

Packaging is all around us. Packaging, which serves various

functions and has various properties, ensures that goods and

products reach customers in a safe and sound manner. These

functions and properties include:

i) Containment – preventing leakages (gas, air, liquid)

and preventing the loss of parts through numerous

handling processes.

ii) Protection – preventing physical damage during all

stages of the product life and ensuring its protection

from various transportation processes (the delivery of

packages may entail physical movements between

multiple locations), and changes in temperature and

humidity.

iii) Preservation – extending the shelf life, protecting

against biotic, temperature, humidity, acidity, oxygen,

nutrient and abiotic spoilage.

iv) Convenience – providing ergonomics, ease of

handling, and effectiveness in filling and packaging

line.

v) Production information – providing nutrition

information, weight, volume, instruction, and bar

code.

vi) Branding and marketing – acting like a “silent

salesman” using graphical colour displays and artwork.

Application of packaging business

Source: SCC, DBSVTH

Asian Insights SparX: Resilent packaging

demand while sustainability remains intact

Chemical/Packaging/Paper

Page 9

Part 1: Resilient packaging demand to be driven by megatrends

Expect resilient packaging demand during 2020-2022F, driven

by megatrends.

The outbreak of the COVID-19 pandemic has led to

disruptions in businesses and economic activities the world

over. This has temporarily led to a global economic

slowdown, and the packaging business is no exception.

However, we believe the adverse impact on packaging

demand would be limited in view of i) c.70% of packaging

material is used in consumer stable goods which were least

affected by the pandemic, ii) demographics and lifestyle

changes that will lead to a gradual increase in packaging

demand over time, and iii) the boom of e-commerce that is

supported by Internet network advancements and greater

Internet penetration rate.

As a result, we expect the demand for packaging, both paper-

based and polymer-based products, to remain resilient and

grow at a CAGR of 3-4% in during 2019-2022F, driven by

the following factors: i) the boom of online shopping (e-

commerce), ii) low packaging penetration rate in ASEAN, iii)

rising transportation/logistic activity, iv) COVID-19 pandemic

concerns, v) demographic and lifestyle changes, vi) uptrend

for FMCG, vii) rising income from the middle class in

Southeast Asia (Indonesia, the Philippines, Vietnam and

Thailand), viii) improving Internet network and penetration

rate, ix) increasing digital banking transactions, x) uptrend for

parcel delivery services and cheaper delivery fee, and xi)

growing popularity of social and mobile commerce services.

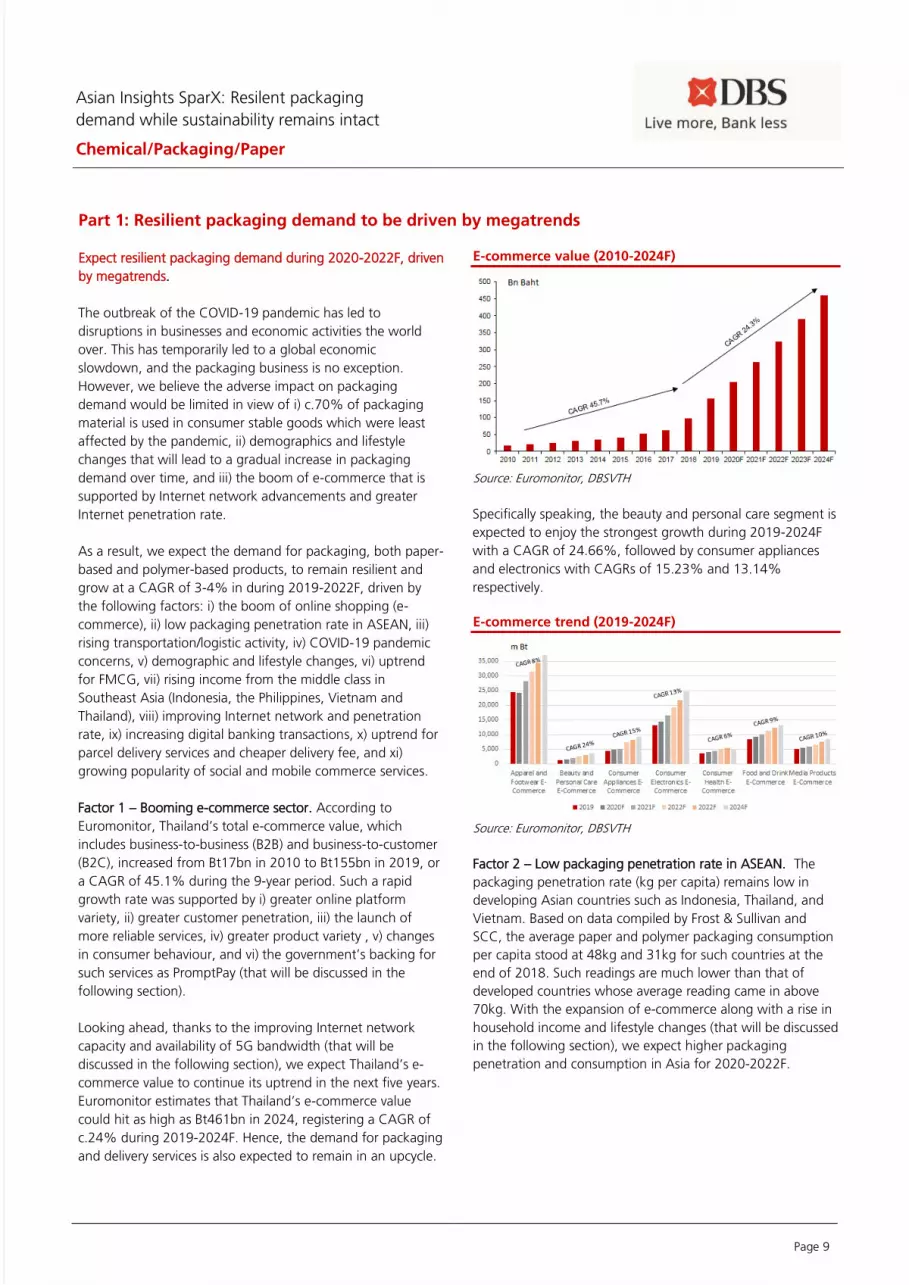

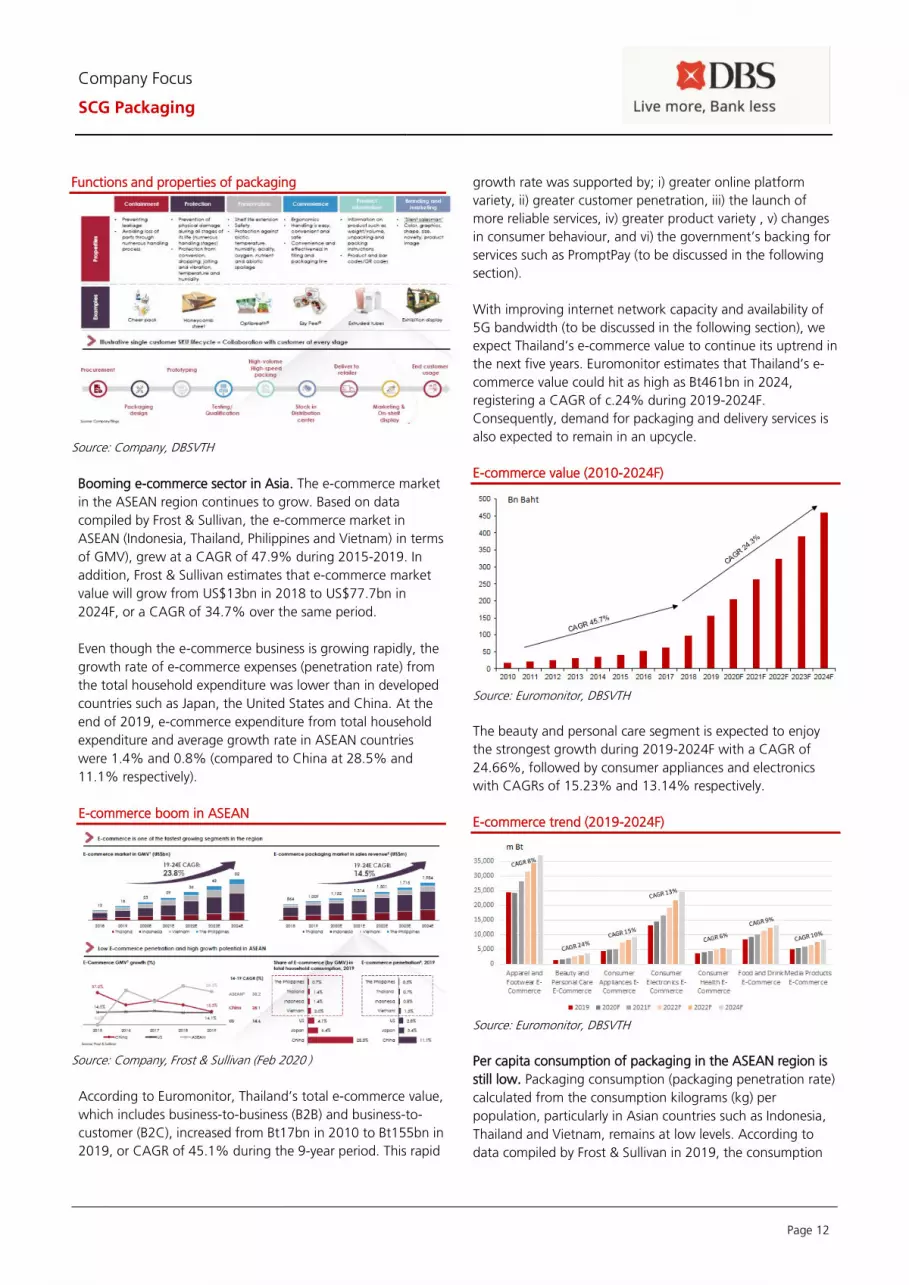

Factor 1 – Booming e-commerce sector. According to

Euromonitor, Thailand’s total e-commerce value, which

includes business-to-business (B2B) and business-to-customer

(B2C), increased from Bt17bn in 2010 to Bt155bn in 2019, or

a CAGR of 45.1% during the 9-year period. Such a rapid

growth rate was supported by i) greater online platform

variety, ii) greater customer penetration, iii) the launch of

more reliable services, iv) greater product variety , v) changes

in consumer behaviour, and vi) the government’s backing for

such services as PromptPay (that will be discussed in the

following section).

Looking ahead, thanks to the improving Internet network

capacity and availability of 5G bandwidth (that will be

discussed in the following section), we expect Thailand’s e-

commerce value to continue its uptrend in the next five years.

Euromonitor estimates that Thailand’s e-commerce value

could hit as high as Bt461bn in 2024, registering a CAGR of

c.24% during 2019-2024F. Hence, the demand for packaging

and delivery services is also expected to remain in an upcycle.

E-commerce value (2010-2024F)

Source: Euromonitor, DBSVTH

Specifically speaking, the beauty and personal care segment is

expected to enjoy the strongest growth during 2019-2024F

with a CAGR of 24.66%, followed by consumer appliances

and electronics with CAGRs of 15.23% and 13.14%

respectively.

E-commerce trend (2019-2024F)

Source: Euromonitor, DBSVTH

Factor 2 – Low packaging penetration rate in ASEAN. The

packaging penetration rate (kg per capita) remains low in

developing Asian countries such as Indonesia, Thailand, and

Vietnam. Based on data compiled by Frost & Sullivan and

SCC, the average paper and polymer packaging consumption

per capita stood at 48kg and 31kg for such countries at the

end of 2018. Such readings are much lower than that of

developed countries whose average reading came in above

70kg. With the expansion of e-commerce along with a rise in

household income and lifestyle changes (that will be discussed

in the following section), we expect higher packaging

penetration and consumption in Asia for 2020-2022F.

Asian Insights SparX: Resilent packaging

demand while sustainability remains intact

Chemical/Packaging/Paper

Page 10

Packaging penetration rate as of 2018

Source: Frost & Sullivan, SCC, DBSVTH

According to a Frost and Sullivan report, consumption per

capita of containerboard packaging in developing countries is

still very low as compared to the matured markets, e.g.

Thailand’s consumption of containerboard is only 48 per

kg/person/year compared to South Korea’s 91 per

kg/person/year.

Containerbord comsumption by countries (as of 2019)

Source: Frost and Sullivan, DBSVTH

Factor 3 – Rise in transportation/logistic activities. Over 2015-

2018, total transported goods, both domestically and

internationally, increased from c.804m tonnes in 2015 to

c.962m tonnes in 2018, or a CAGR of c.4.6%, with rapid

growth of 6-8% seen during 2017-2018. Such growth was

driven by a rise in demand for consumer staple goods,

agricultural products, electronic devices, and construction

materials. Additionally, this was also supported by increasing

demand for door-to-door delivery services that was in tandem

with the growing e-commerce business.

Logistics activities (2015-2018)

Source: NESDC, DBSVTH

Moreover, the logistics business for e-commerce posted a

solid CAGR of 26% over 2015-2017, rising from Bt64.1bn in

2015 to Bt126bn in 2017. Such growth was driven by i)

Alibaba and Jingdong’s (JD) logistics developments, and ii)

increasing delivery activities by Thailand Post, Lazada, Kerry

and Sokochan. Hence, we also expect the uptrend to

continue in the near future.

E-commerce value of the logistics business (2015-2018)

Source: NESDC, DBSVTH

Factor 4 – COVID-19 pandemic concerns. We believe the

impact on packaging demand and supply from the outbreak

of COVID-19 pandemic is mixed, depending on the product

segment and portfolio position of the packaging players.

However, we think the high demand for food, grocery,

healthcare products, personal-care products, food delivery

and e-commerce transportation will continue, as COVID-19

has turned out to be a hard-to-contain virus with second

waves appearing in many countries. Based on the data

compiled by Mckinsey, the online sales of grocery and fresh

food in China doubled within a 10-day period in Jan 2020,

during the early stages of the outbreak. Hence, demand was

high for packaging materials such as corrugated paper,

flexible, and rigid plastic. On the other hand, demand for

packaging materials for the industrial, luxury, alcohol and

business-to-business (B2B) segments such as bulk and

91

87

73

70

48

35

22

15

11

0 20 40 60 80 100

South Korea

USA

Germany

Japan

Thailand

China

Vietnam

Indonesia

Philiphine

kg/person/year

Asian Insights SparX: Resilent packaging

demand while sustainability remains intact

Chemical/Packaging/Paper

Page 11

transportation packaging could see a downward trend, as the

demand for such segments is highly correlated with the

domestic GDP performance. Note that the Bank of Thailand

(BOT) has revised down Thailand’s 2020F GDP growth

forecast to -8.1% in June 2020.

Thailand GDP growth rate (2010-2020F)

Source: BOT, DBSVTH

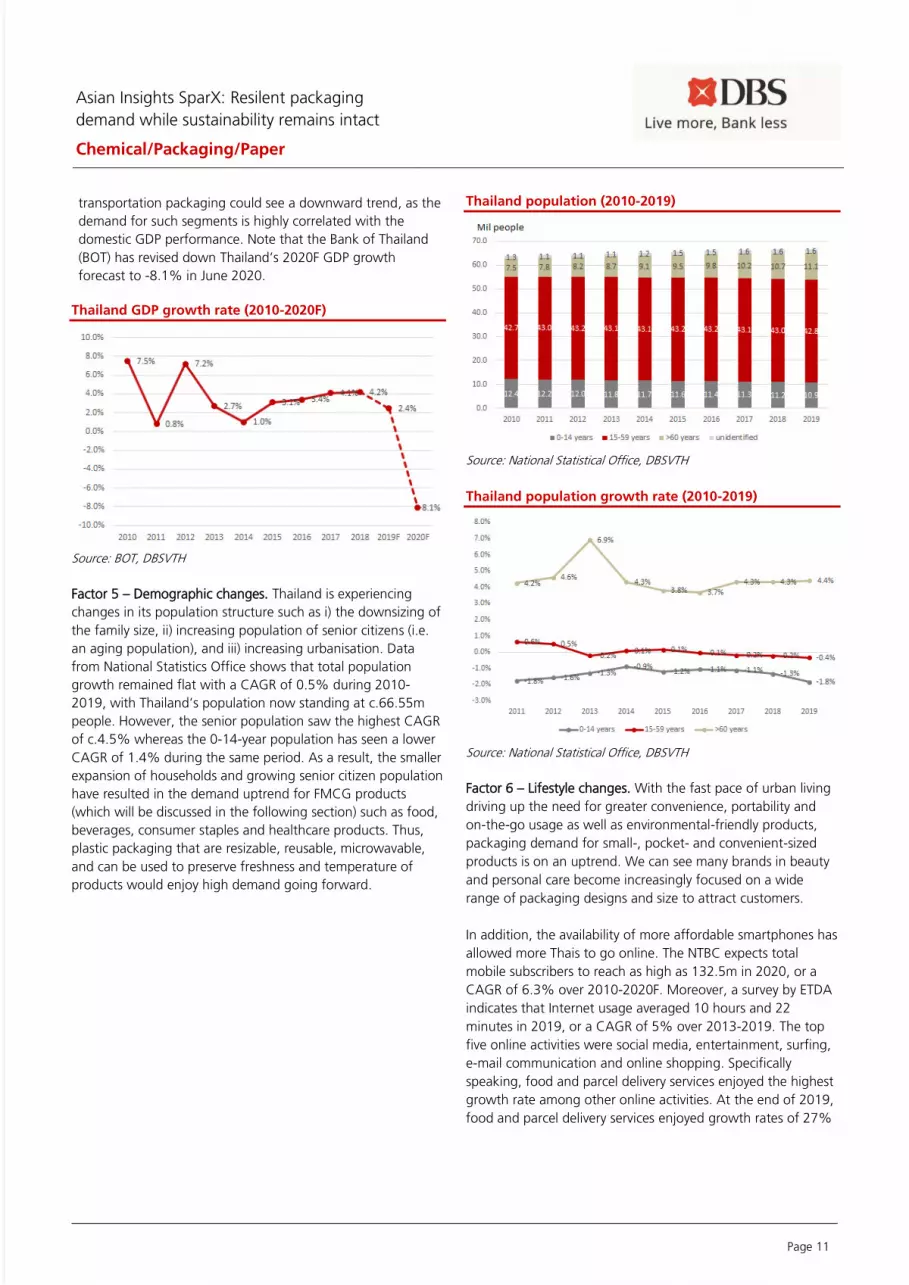

Factor 5 – Demographic changes. Thailand is experiencing

changes in its population structure such as i) the downsizing of

the family size, ii) increasing population of senior citizens (i.e.

an aging population), and iii) increasing urbanisation. Data

from National Statistics Office shows that total population

growth remained flat with a CAGR of 0.5% during 2010-

2019, with Thailand’s population now standing at c.66.55m

people. However, the senior population saw the highest CAGR

of c.4.5% whereas the 0-14-year population has seen a lower

CAGR of 1.4% during the same period. As a result, the smaller

expansion of households and growing senior citizen population

have resulted in the demand uptrend for FMCG products

(which will be discussed in the following section) such as food,

beverages, consumer staples and healthcare products. Thus,

plastic packaging that are resizable, reusable, microwavable,

and can be used to preserve freshness and temperature of

products would enjoy high demand going forward.

Thailand population (2010-2019)

Source: National Statistical Office, DBSVTH

Thailand population growth rate (2010-2019)

Source: National Statistical Office, DBSVTH

Factor 6 – Lifestyle changes. With the fast pace of urban living

driving up the need for greater convenience, portability and

on-the-go usage as well as environmental-friendly products,

packaging demand for small-, pocket- and convenient-sized

products is on an uptrend. We can see many brands in beauty

and personal care become increasingly focused on a wide

range of packaging designs and size to attract customers.

In addition, the availability of more affordable smartphones has

allowed more Thais to go online. The NTBC expects total

mobile subscribers to reach as high as 132.5m in 2020, or a

CAGR of 6.3% over 2010-2020F. Moreover, a survey by ETDA

indicates that Internet usage averaged 10 hours and 22

minutes in 2019, or a CAGR of 5% over 2013-2019. The top

five online activities were social media, entertainment, surfing,

e-mail communication and online shopping. Specifically

speaking, food and parcel delivery services enjoyed the highest

growth rate among other online activities. At the end of 2019,

food and parcel delivery services enjoyed growth rates of 27%

Asian Insights SparX: Resilent packaging

demand while sustainability remains intact

Chemical/Packaging/Paper

Page 12

y-o-y and 20% y-o-y respectively. Hence, we expect such solid

growth to continue, on the back of COVID-19.

Thailand’s mobile subscribers (2010-2020F)

Source: NBTC, DBSVTH

Mobile usage per day (2013-2019)

Source: ETDA, DBSVTH

Growth of top five online activities (2018-2019)

Source: ETDA, DBSVTH

Factor 7 – Growing FMCG trend. Consumer goods are

products purchased for consumption by the average

consumer. They are divided into three different categories:

durable, non-durable goods, and services. Durable goods

have a shelf life of three years or more while non-durable

goods have a shelf life of less than one year. FMCGs – a.k.a.

packaged consumer goods – form the largest segment of

consumer goods. They fall into the non-durable category, as

they are consumed immediately and have a short shelf life

(source: Investopedia). FMCGs are purchased frequently on a

daily basis, consumed rapidly, priced affordably and sold in

large quantities, and have low cost of production. They also

have a high turnover and will not stay long on store shelves.

They can be categorised in the following broad segments: i)

processed foods, ii) ready-to-eat meals, iii) beverages, iv)

groceries, v) frozen and dry foods, and vi) home-care

products.

Since FMCGs are mostly substitute products and have low

cost of production, the major manufacturers such as Coca-

Cola, Pepsi, Unilever, Procter & Gamble (P&G), Nestlé,

Johnson & Johnson, L’Oreal, Colgate, and Ajinomoto, need to

differentiate their products to gain market share at the

expense of their competitors.

Hence, we believe packaging formats will play an important

role in the production process as well as marketing campaigns

of the FMCG companies. Generally, logistics and distribution

systems often require secondary and tertiary packaging to

maximise efficiency, whereas attractive product displays and

pleasant user experience can also play a key role in selling

products. The unit pack or primary package is critical for

product protection and shelf life, and also provides

information and sales incentives to consumers.

Different types of packaging

Source: SCC, DBSVTH

Asian Insights SparX: Resilent packaging

demand while sustainability remains intact

Chemical/Packaging/Paper

Page 13

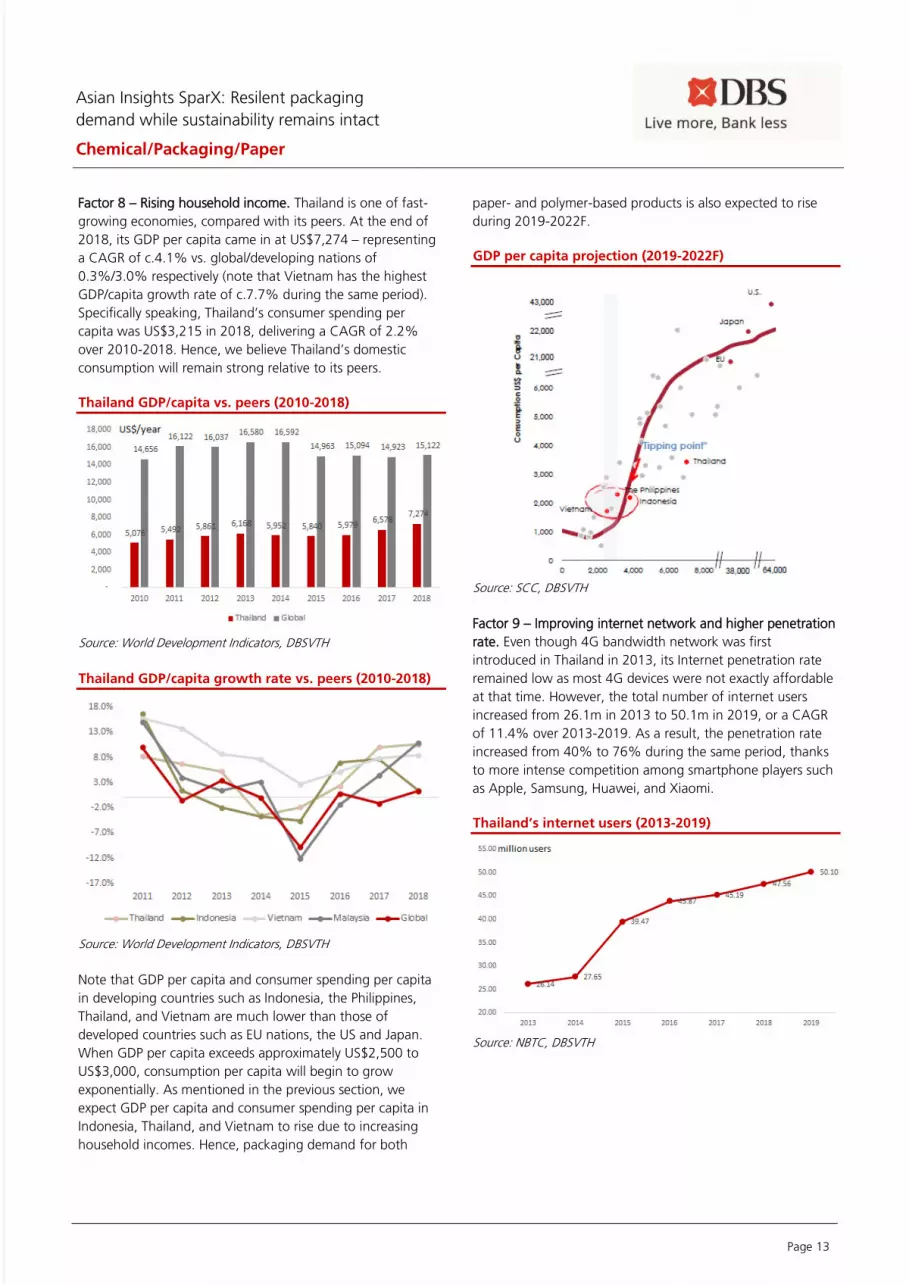

Factor 8 – Rising household income. Thailand is one of fast-

growing economies, compared with its peers. At the end of

2018, its GDP per capita came in at US$7,274 – representing

a CAGR of c.4.1% vs. global/developing nations of

0.3%/3.0% respectively (note that Vietnam has the highest

GDP/capita growth rate of c.7.7% during the same period).

Specifically speaking, Thailand’s consumer spending per

capita was US$3,215 in 2018, delivering a CAGR of 2.2%

over 2010-2018. Hence, we believe Thailand’s domestic

consumption will remain strong relative to its peers.

Thailand GDP/capita vs. peers (2010-2018)

Source: World Development Indicators, DBSVTH

Thailand GDP/capita growth rate vs. peers (2010-2018)

Source: World Development Indicators, DBSVTH

Note that GDP per capita and consumer spending per capita

in developing countries such as Indonesia, the Philippines,

Thailand, and Vietnam are much lower than those of

developed countries such as EU nations, the US and Japan.

When GDP per capita exceeds approximately US$2,500 to

US$3,000, consumption per capita will begin to grow

exponentially. As mentioned in the previous section, we

expect GDP per capita and consumer spending per capita in

Indonesia, Thailand, and Vietnam to rise due to increasing

household incomes. Hence, packaging demand for both

paper- and polymer-based products is also expected to rise

during 2019-2022F.

GDP per capita projection (2019-2022F)

Source: SCC, DBSVTH

Factor 9 – Improving internet network and higher penetration

rate. Even though 4G bandwidth network was first

introduced in Thailand in 2013, its Internet penetration rate

remained low as most 4G devices were not exactly affordable

at that time. However, the total number of internet users

increased from 26.1m in 2013 to 50.1m in 2019, or a CAGR

of 11.4% over 2013-2019. As a result, the penetration rate

increased from 40% to 76% during the same period, thanks

to more intense competition among smartphone players such

as Apple, Samsung, Huawei, and Xiaomi.

Thailand’s internet users (2013-2019)

Source: NBTC, DBSVTH

Asian Insights SparX: Resilent packaging

demand while sustainability remains intact

Chemical/Packaging/Paper

Page 14

In addition, we expect online shopping activities and

packaging demand to continue enjoying strong growth, as

the latest 5G bandwidth technology will enter the

commercialisation stage nationwide by the end of 2020F. This

technology could give rise to a safer online shopping

experience as well as cost savings arising from the use of

drones for logistics and delivery. Consumers will also get to

experience new online shopping platforms with 4K 360-

degree live video streaming, which bodes well for e-

commerce sales volume and revenue. Thus, demand for

packaging will also rise on the back of improving Internet

network capability.

Factor 10 – Increasing digital banking transactions. There is a

growing use of digital banking for payment of goods and

services, transfer of money, and payment of utility bills. This is

mainly thanks to the Bank of Thailand’s (BOT) decision to

waive digital banking fees in 2017. As a result, total e-

payment value increased from Bt8,425bn in 1Q15 to

Bt12,690bn in 3Q18.

Total e-payments (1Q15-3Q18)

Source: Bank of Thailand, DBSVTH

In particular, total internal banking transactions and value

increased from 43.4m orders and Bt5,275bn in 1Q15 to

227,114m orders and Bt7,587bn in 1Q20 respectively.

Similarly, total mobile banking transactions and value

increased from 48.3m orders and Bt545bn in 1Q15 to

1,637m orders and Bt7,010bn in 1Q20 respectively. The rapid

growth of online shopping and cashless activities is one of the

megatrends that will boost the demand for packaging.

Internet banking transaction and value (1Q15-1Q20)

Source: Bank of Thailand, DBSVTH

Mobile banking transaction and value (1Q15-1Q20)

Source: Bank of Thailand, DBSVTH

Moreover, the BOT has also introduced the PromptPay service,

an online transfer payment with a use of either a mobile

phone or national identification number instead of a bank

account. Such services offer convenience, time savings and

ease of use for money transfer between accounts. Thus, they

also facilitate and boost online shopping activities.

Statistically, PromptPay’s total transactions and value

increased from 2.1m orders and Bt12.16bn in 1Q17 to

865.6m orders and Bt4,221bn in 1Q20 respectively.

Asian Insights SparX: Resilent packaging

demand while sustainability remains intact

Chemical/Packaging/Paper

Page 15

PromptPay transactions and value (1Q17-1Q20)

Source: Bank of Thailand, DBSVTH

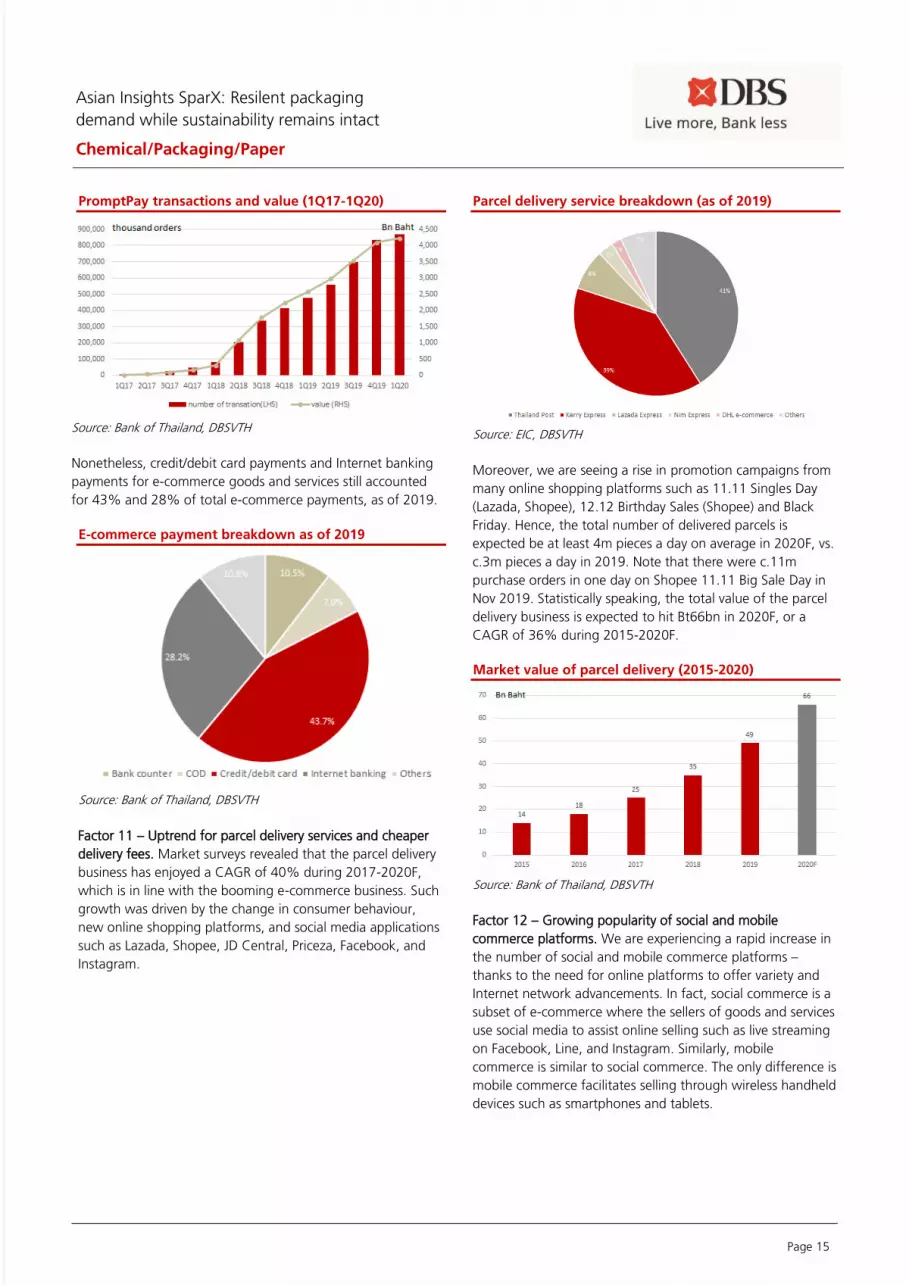

Nonetheless, credit/debit card payments and Internet banking

payments for e-commerce goods and services still accounted

for 43% and 28% of total e-commerce payments, as of 2019.

E-commerce payment breakdown as of 2019

Source: Bank of Thailand, DBSVTH

Factor 11 – Uptrend for parcel delivery services and cheaper

delivery fees. Market surveys revealed that the parcel delivery

business has enjoyed a CAGR of 40% during 2017-2020F,

which is in line with the booming e-commerce business. Such

growth was driven by the change in consumer behaviour,

new online shopping platforms, and social media applications

such as Lazada, Shopee, JD Central, Priceza, Facebook, and

Instagram.

Parcel delivery service breakdown (as of 2019)

Source: EIC, DBSVTH

Moreover, we are seeing a rise in promotion campaigns from

many online shopping platforms such as 11.11 Singles Day

(Lazada, Shopee), 12.12 Birthday Sales (Shopee) and Black

Friday. Hence, the total number of delivered parcels is

expected be at least 4m pieces a day on average in 2020F, vs.

c.3m pieces a day in 2019. Note that there were c.11m

purchase orders in one day on Shopee 11.11 Big Sale Day in

Nov 2019. Statistically speaking, the total value of the parcel

delivery business is expected to hit Bt66bn in 2020F, or a

CAGR of 36% during 2015-2020F.

Market value of parcel delivery (2015-2020)

Source: Bank of Thailand, DBSVTH

Factor 12 – Growing popularity of social and mobile

commerce platforms. We are experiencing a rapid increase in

the number of social and mobile commerce platforms –

thanks to the need for online platforms to offer variety and

Internet network advancements. In fact, social commerce is a

subset of e-commerce where the sellers of goods and services

use social media to assist online selling such as live streaming

on Facebook, Line, and Instagram. Similarly, mobile

commerce is similar to social commerce. The only difference is

mobile commerce facilitates selling through wireless handheld

devices such as smartphones and tablets.

Asian Insights SparX: Resilent packaging

demand while sustainability remains intact

Chemical/Packaging/Paper

Page 16

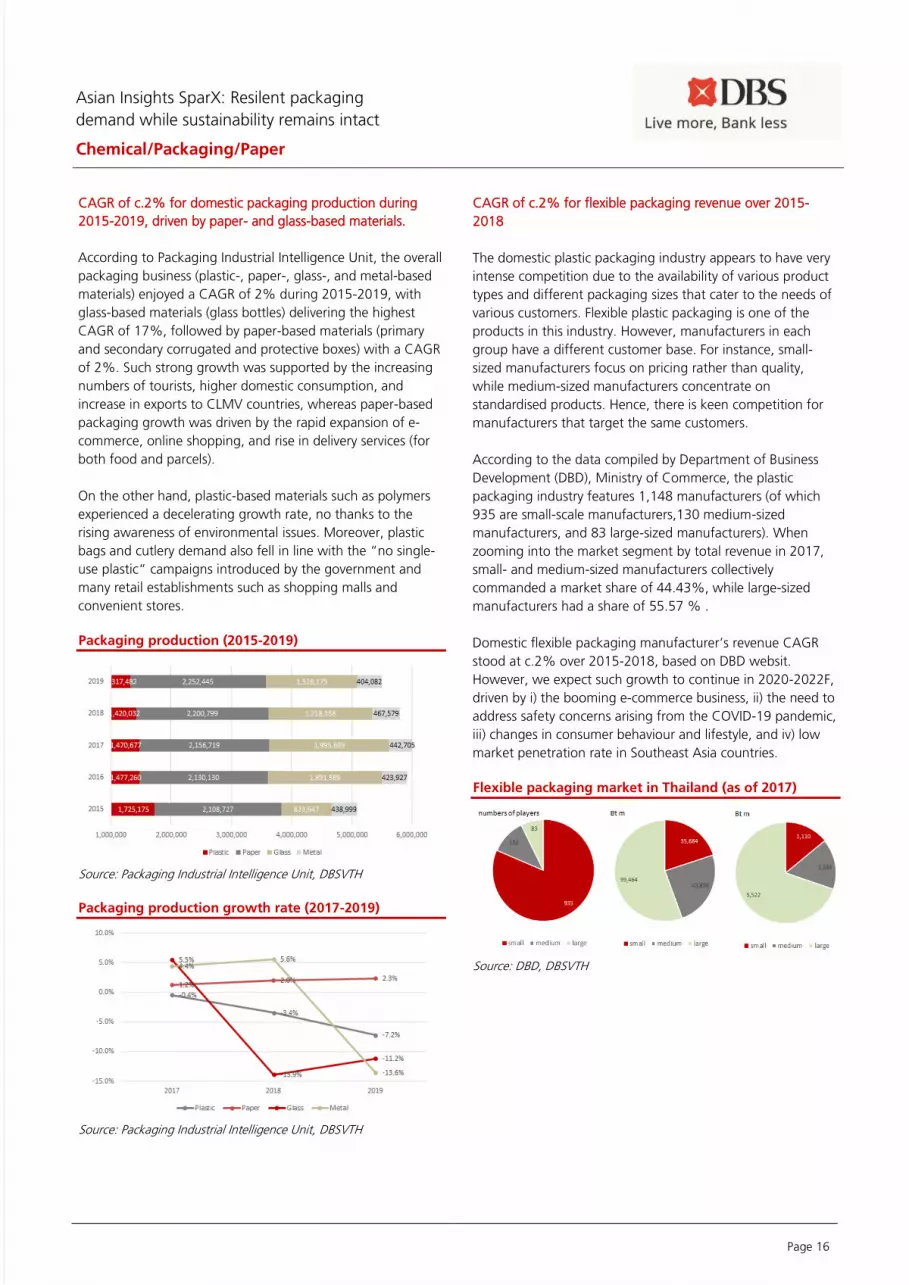

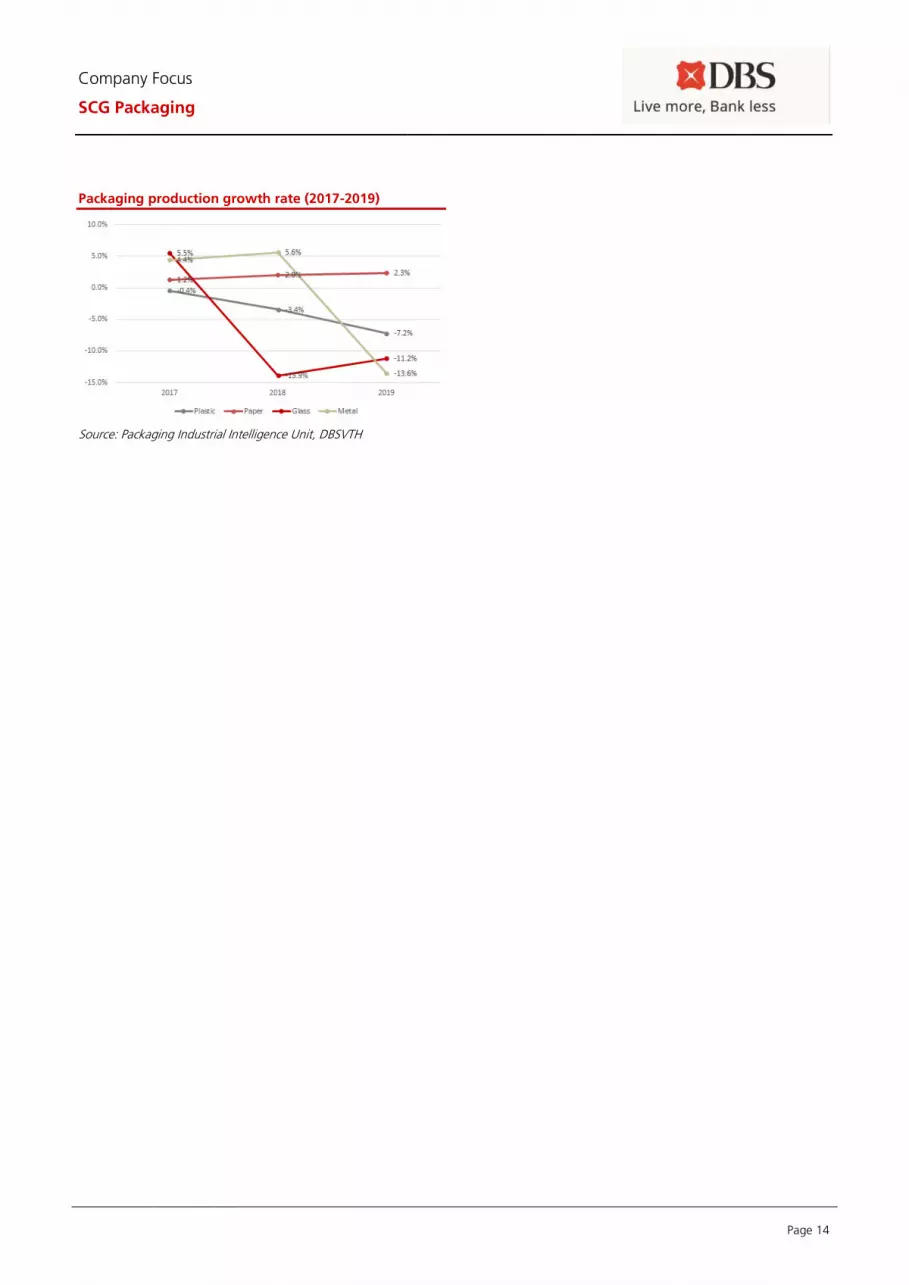

CAGR of c.2% for domestic packaging production during

2015-2019, driven by paper- and glass-based materials.

According to Packaging Industrial Intelligence Unit, the overall

packaging business (plastic-, paper-, glass-, and metal-based

materials) enjoyed a CAGR of 2% during 2015-2019, with

glass-based materials (glass bottles) delivering the highest

CAGR of 17%, followed by paper-based materials (primary

and secondary corrugated and protective boxes) with a CAGR

of 2%. Such strong growth was supported by the increasing

numbers of tourists, higher domestic consumption, and

increase in exports to CLMV countries, whereas paper-based

packaging growth was driven by the rapid expansion of e-

commerce, online shopping, and rise in delivery services (for

both food and parcels).

On the other hand, plastic-based materials such as polymers

experienced a decelerating growth rate, no thanks to the

rising awareness of environmental issues. Moreover, plastic

bags and cutlery demand also fell in line with the “no single-

use plastic“ campaigns introduced by the government and

many retail establishments such as shopping malls and

convenient stores.

Packaging production (2015-2019)

Source: Packaging Industrial Intelligence Unit, DBSVTH

Packaging production growth rate (2017-2019)

Source: Packaging Industrial Intelligence Unit, DBSVTH

CAGR of c.2% for flexible packaging revenue over 2015-

2018

The domestic plastic packaging industry appears to have very

intense competition due to the availability of various product

types and different packaging sizes that cater to the needs of

various customers. Flexible plastic packaging is one of the

products in this industry. However, manufacturers in each

group have a different customer base. For instance, small-

sized manufacturers focus on pricing rather than quality,

while medium-sized manufacturers concentrate on

standardised products. Hence, there is keen competition for

manufacturers that target the same customers.

According to the data compiled by Department of Business

Development (DBD), Ministry of Commerce, the plastic

packaging industry features 1,148 manufacturers (of which

935 are small-scale manufacturers,130 medium-sized

manufacturers, and 83 large-sized manufacturers). When

zooming into the market segment by total revenue in 2017,

small- and medium-sized manufacturers collectively

commanded a market share of 44.43%, while large-sized

manufacturers had a share of 55.57 % .

Domestic flexible packaging manufacturer’s revenue CAGR

stood at c.2% over 2015-2018, based on DBD websit.

However, we expect such growth to continue in 2020-2022F,

driven by i) the booming e-commerce business, ii) the need to

address safety concerns arising from the COVID-19 pandemic,

iii) changes in consumer behaviour and lifestyle, and iv) low

market penetration rate in Southeast Asia countries.

Flexible packaging market in Thailand (as of 2017)

Source: DBD, DBSVTH

Asian Insights SparX: Resilent packaging

demand while sustainability remains intact

Chemical/Packaging/Paper

Page 17

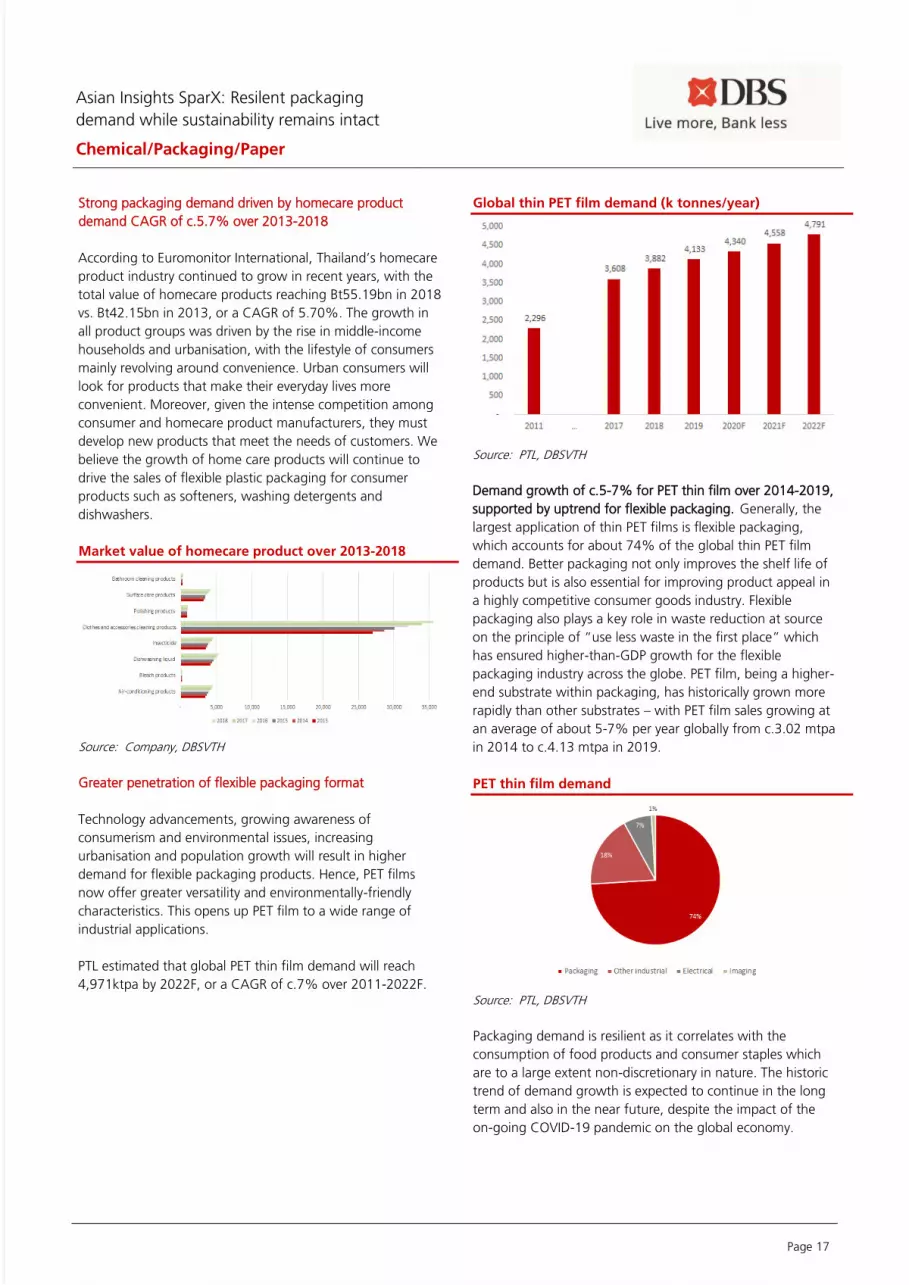

Strong packaging demand driven by homecare product

demand CAGR of c.5.7% over 2013-2018

According to Euromonitor International, Thailand’s homecare

product industry continued to grow in recent years, with the

total value of homecare products reaching Bt55.19bn in 2018

vs. Bt42.15bn in 2013, or a CAGR of 5.70%. The growth in

all product groups was driven by the rise in middle-income

households and urbanisation, with the lifestyle of consumers

mainly revolving around convenience. Urban consumers will

look for products that make their everyday lives more

convenient. Moreover, given the intense competition among

consumer and homecare product manufacturers, they must

develop new products that meet the needs of customers. We

believe the growth of home care products will continue to

drive the sales of flexible plastic packaging for consumer

products such as softeners, washing detergents and

dishwashers.

Market value of homecare product over 2013-2018

Source: Company, DBSVTH

Greater penetration of flexible packaging format

Technology advancements, growing awareness of

consumerism and environmental issues, increasing

urbanisation and population growth will result in higher

demand for flexible packaging products. Hence, PET films

now offer greater versatility and environmentally-friendly

characteristics. This opens up PET film to a wide range of

industrial applications.

PTL estimated that global PET thin film demand will reach

4,971ktpa by 2022F, or a CAGR of c.7% over 2011-2022F.

Global thin PET film demand (k tonnes/year)

Source: PTL, DBSVTH

Demand growth of c.5-7% for PET thin film over 2014-2019,

supported by uptrend for flexible packaging. Generally, the

largest application of thin PET films is flexible packaging,

which accounts for about 74% of the global thin PET film

demand. Better packaging not only improves the shelf life of

products but is also essential for improving product appeal in

a highly competitive consumer goods industry. Flexible

packaging also plays a key role in waste reduction at source

on the principle of “use less waste in the first place” which

has ensured higher-than-GDP growth for the flexible

packaging industry across the globe. PET film, being a higher-

end substrate within packaging, has historically grown more

rapidly than other substrates – with PET film sales growing at

an average of about 5-7% per year globally from c.3.02 mtpa

in 2014 to c.4.13 mtpa in 2019.

PET thin film demand

Source: PTL, DBSVTH

Packaging demand is resilient as it correlates with the

consumption of food products and consumer staples which

are to a large extent non-discretionary in nature. The historic

trend of demand growth is expected to continue in the long

term and also in the near future, despite the impact of the

on-going COVID-19 pandemic on the global economy.

Asian Insights SparX: Resilent packaging

demand while sustainability remains intact

Chemical/Packaging/Paper

Page 18

Demand growth of c.4-5% for PET thick films over 2014-

2019. Electrical and Industrial are the key segments in the PET

thick film industry. During 2014-2019, PET thick film demand

has been growing at a CAGR of about 4-5%. New

innovations and usage new applications in the electrical

segments (like flat screen panels, PV solar cells, etc.) have

been driving the growth in the past and would help this

industry to continue to grow at a healthy CAGR of about 4-

6% in the long term, although there is a temporary

contraction in demand due to the impact of COVID-19.

PET thick film global demand

Source: PTL, DBSVTH

Uptrend for flexible packaging demand that will unleash

higher value added

Currently, Thailand is importing plastic film packaging such as

plastic bags with aseptic aluminium lining that have high

value (due to demographics and lifestyle changes as

mentioned in the previous sections) while exporting

fundamental plastic goods including plastic carrier bags with

low added value. Therefore, when comparing the value of

plastic per tonne against plastic exporters in Asia, which are

China, Korea, Vietnam, Taiwan, Indonesia, and Japan,

Thailand is severely disadvantaged in the value of plastic

packaging per tonne. Thus, we believe there is an opportunity

for producers to develop the market for a plastic film that can

be used for flexible plastic packaging that will enjoy high

demand both domestically and internationally.

Based on the data collected by Packaging Intelligence Unit,

the amount of imported and exported plastic packaging

materials enjoyed CAGRs of 7% and 4% during 2013-2019.

This confirms our view that demand for flexible, reusable and

microwavable packaging that can be used to preserve

freshness and temperature of products, is on an uptrend.

Import/export of plastic packaging materials (2013-2019)

Source: Packaging Industrial Intelligence Unit, DBSVTH

Key listed domestic packaging players

AJ Plast Plc – (AJ TB) - AJ is a bi-axially-oriented film

manufacturer (BoPET, BoPP, and BoPA) that meets world-class

quality and standards, and ensures customer satisfaction via

its experience, innovations and advanced technologies. It has

a production capacity of 261,000 tonnes per year.

Indorama Ventures Plc (IVL TB, HOLD, TP of Bt24) – IVL is a

vertically integrated chemical player in the aromatics (PX, PTA,

PET) and olefins (EO, EG, IPA, MEG, MTBE) businesses. IVL has

an effective PET capacity of 12.05 mtpa, which is used to

produce a wide range range of products such as polyester,

PET bottle, specialty chemical, packaging (c.0.3mtpa), and

HVA products.

Polyplex (Thailand) Plc (PTL TB, BUY, TP of Bt27.5) – PTL has

the sixth largest capacity PET film globally and produces both

thin and thick PET films with various surface properties

covering a wide spectrum of applications. It has also

diversified into BOPP, Blown PP/PE and CPP films that are

produced in its state-of-the-art plants with economies of

scale. Its integrated downstream business covers metallizing,

silicone coating (offline chemical coating), extrusion coating

and transfer of metallized paper that offer further value

added.

SCG Packaging Plc (SCGP TB, BUY, TP of Bt44) – SCG

Packaging (SCGP), a subsidiary of SCC that will be listed ion

the Stock Exchange of Thailand, is a holding company that

offers packaging solutions through innovative products &

services and embraces sustainable business practices. SCGP

engages in fibre-based packaging, performance and polymer

packaging, as well as food service product and corrugated

containers, offering capacities of 4.0 and 1.1 mtpa

respectively. Moreover, it also has a flexible packaging

capacity of c.820m sqm per year.

Asian Insights SparX: Resilent packaging

demand while sustainability remains intact

Chemical/Packaging/Paper

Page 19

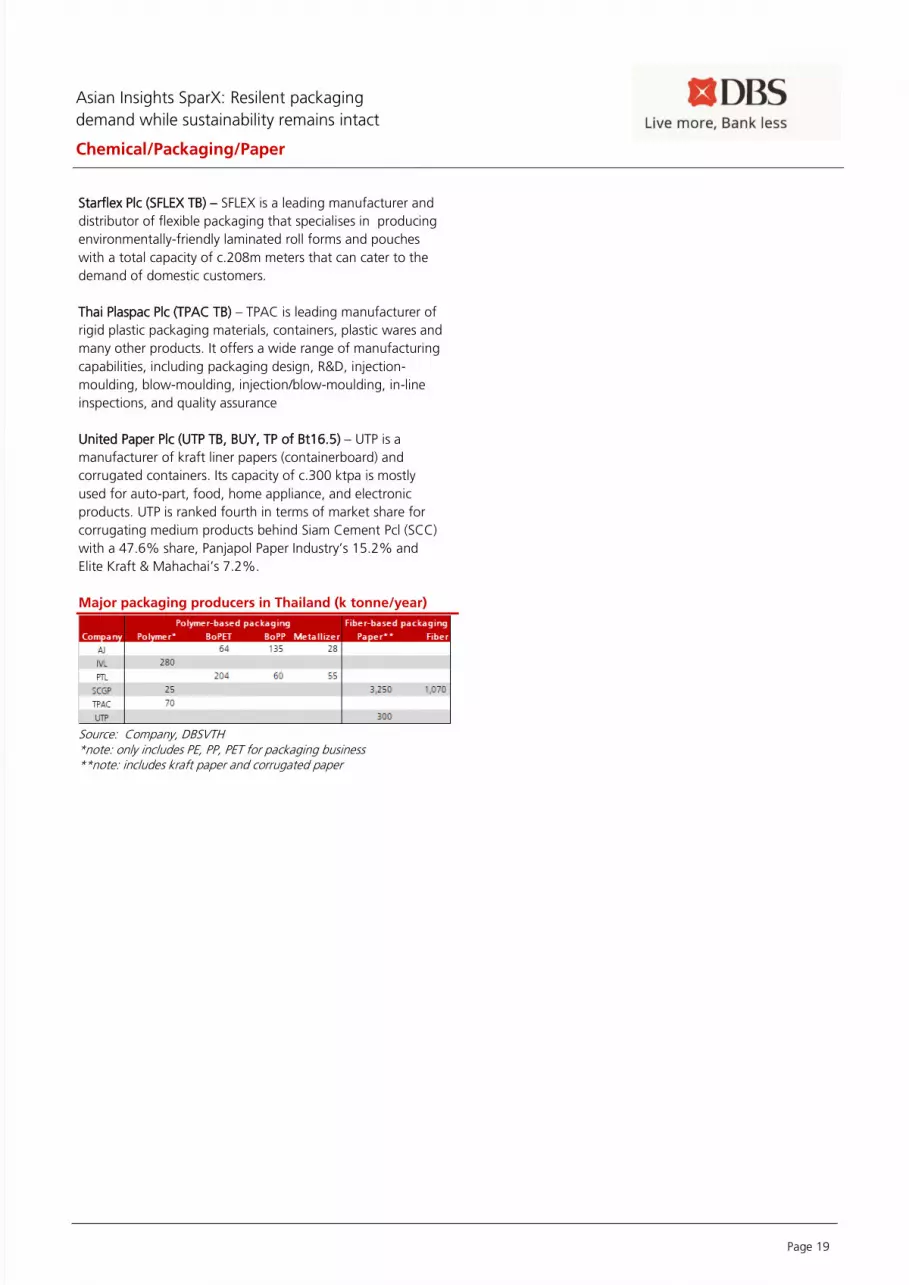

Starflex Plc (SFLEX TB) – SFLEX is a leading manufacturer and

distributor of flexible packaging that specialises in producing

environmentally-friendly laminated roll forms and pouches

with a total capacity of c.208m meters that can cater to the

demand of domestic customers.

Thai Plaspac Plc (TPAC TB) – TPAC is leading manufacturer of

rigid plastic packaging materials, containers, plastic wares and

many other products. It offers a wide range of manufacturing

capabilities, including packaging design, R&D, injection-

moulding, blow-moulding, injection/blow-moulding, in-line

inspections, and quality assurance

United Paper Plc (UTP TB, BUY, TP of Bt16.5) – UTP is a

manufacturer of kraft liner papers (containerboard) and

corrugated containers. Its capacity of c.300 ktpa is mostly

used for auto-part, food, home appliance, and electronic

products. UTP is ranked fourth in terms of market share for

corrugating medium products behind Siam Cement Pcl (SCC)

with a 47.6% share, Panjapol Paper Industry’s 15.2% and

Elite Kraft & Mahachai’s 7.2%.

Major packaging producers in Thailand (k tonne/year)

Source: Company, DBSVTH *note: only includes PE, PP, PET for packaging business **note: includes kraft paper and corrugated paper

Asian Insights SparX: Resilent packaging

demand while sustainability remains intact

Chemical/Packaging/Paper

Page 20

Part 2: Long-run impact from environmental concerns

i) Single-use plastic ban

Since 2013, the usage of plastic packaging in Thailand has

shown signs of a downtrend, in contrast to the strong growth

enjoyed by the plastic packaging industry previously. Based on

the data compiled by EIC, the usage of plastic packaging

grew at a CAGR of 7% over 2008-2012 before decelerating

to a CAGR of 3% between 2013-2017. When assessing the

share of plastic packaging usage, it was found that the use of

rigid plastic packaging that has decelerated in the past five

years. It share was eroded by the use of flexible plastic

packaging, due to demographic and lifestyle changes, and

rising awareness of environmental issues.

More than 8m tonnes per year of plastic waste being dumped

into water sources around the world. The Ocean

Conservancy, a non-profit organisation that studies the

conservation of marine resources, estimated that there are

currently c.150m tonnes of plastic waste circulating in the

oceans, seas and water sources and such waste can be traced

all the way back to 1950. The amount of plastic waste is also

likely to increase due to the ineffective management of waste

and the low amount of plastic recycling, especially in

developing countries. Subsequently, a considerable amount of

plastic waste will flow into water sources and into the sea,

and subsequently the ocean. As for Thailand, the pollution

control department estimated that there are more than 2m

tonnes of plastic waste amounting to 12% of the total waste

in the country annually. Although a proportion of the waste is

destroyed or recycled, c.1m tonnes of waste would be

dumped into the sea.

Acceleration of phase-out of single-use plastic spurred by

government and private businesses. The government has

three important and integrative goals in reducing plastic

waste, which are i) reducing the volume of waste plastic, ii)

developing innovative new plastic packaging materials that

are re-usable and more environmentally friendly, and iii)

increasing the re-use of post-consumption plastic to 60% by

2021. In this vein, the government will revisit the concept of

collecting taxes or introducing fees associated with the use of

plastic packaging such as a plastic bag or packaging tax.

Additionally, the Pollution Control Department of the Ministry

of Natural Resources and Environment has signed an MOU

with bottled water producers to stop using cap seals with the

aim of reducing plastic waste of 520 tonnes per year, or

260,000 kilometres of waste that could circle the earth 6.5

times, from 1 April 2018.

Meanwhile, the Department of Medical Services, Ministry of

Public Health, also announced that it has stopped using

plastic bags for storing medicines in every unit from 1 October

2018. This measure will reduce the annual usage of plastic

bags in hospitals under the department by more than 9m

bags. Similarly, the Thai private retail sector has its own

initiatives to reduce plastic packaging, involving grocery and

convenient stores like Tops Daily, Tesco Lotus, 7-11 as well as

shopping malls like Central Department Store, The Malls and

Starbucks.

We believe such measures being introduced by both the

public and private sectors may not have serious consequences

in the short term, as Thai people use more than 7bn plastic

bags per year. However, should the government be able to

achieve the goal of re-using plastic bags by 60% after their

initial consumption and the campaign of reducing the use of

such bags persist, producers of single-use plastic packaging

such as carrier bags and water bottles will be impacted rather

significantly.

Ban on seven types of single-use plastics by 2025. In 2018,

the sub-committee on plastic waste management looked at

the action plan of reducing and banning the use of seven

types of single-use plastics between 2019 and 2025. In 2019,

the use of the following products is expected to be banned i)

cap seals made from PVC films, ii) products that use Oxo

alcohol (OXO), which is usually found in HDPE and LDPE, and

iii) micro-beads made from plastic. In 2022, the targeted

plastic products to be banned include i) plastic carrier bags

that are thinner than 36 microns (usually made from LLDPE),

and ii) foam food containers. As for 2025, the plastic products

being targeted are i) single-use plastic cups and ii) plastic

straws. The majority of foam containers, cups, and plastic

straws are made from polystyrene (PS). We believe LLDPE will

be the most affected chemical product. This because it is used

in the making of carrier bags and packaging films, accounting

for over 55% in the process of producing plastic products.

Asian Insights SparX: Resilent packaging

demand while sustainability remains intact

Chemical/Packaging/Paper

Page 21

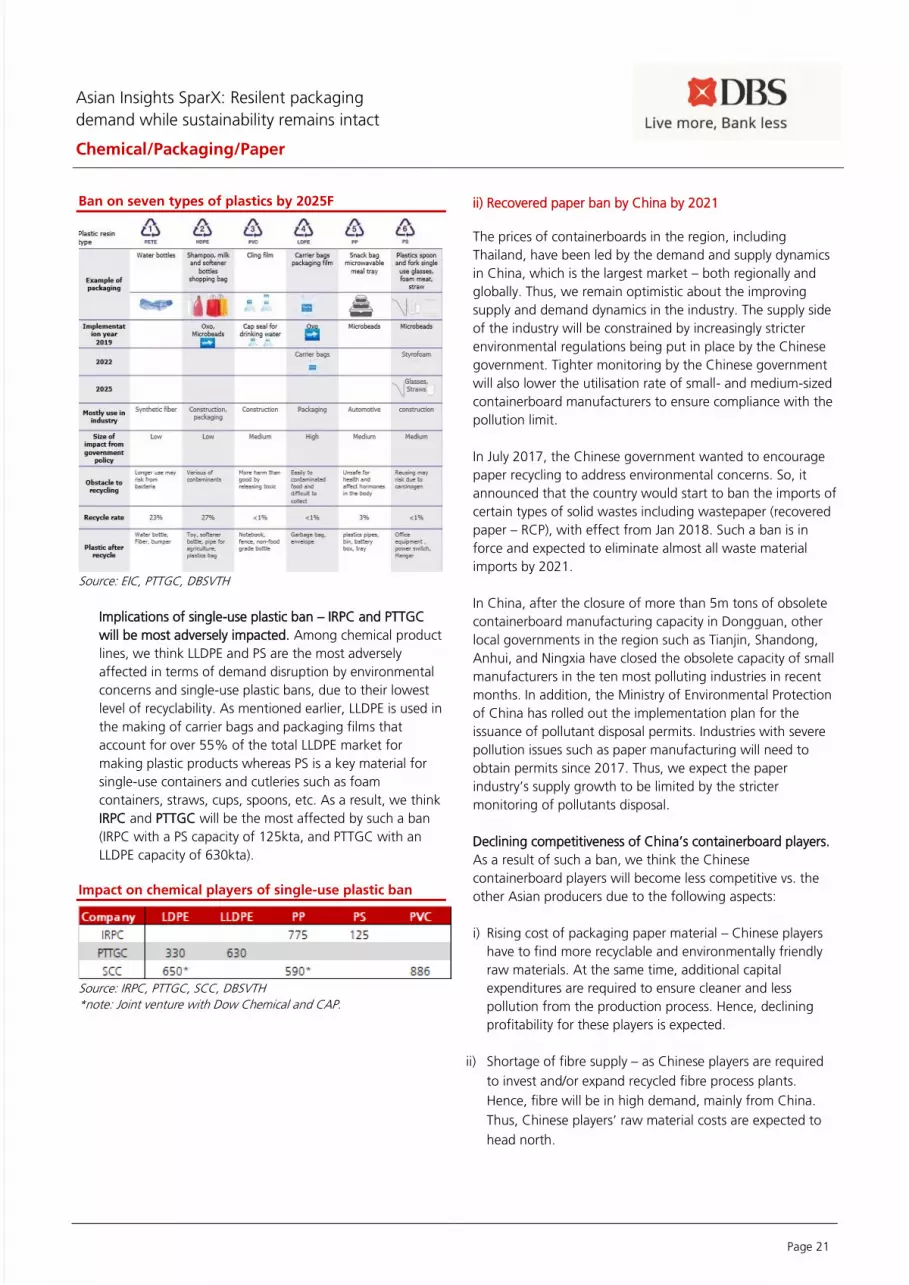

Ban on seven types of plastics by 2025F

Source: EIC, PTTGC, DBSVTH

Implications of single-use plastic ban – IRPC and PTTGC

will be most adversely impacted. Among chemical product

lines, we think LLDPE and PS are the most adversely

affected in terms of demand disruption by environmental

concerns and single-use plastic bans, due to their lowest

level of recyclability. As mentioned earlier, LLDPE is used in

the making of carrier bags and packaging films that

account for over 55% of the total LLDPE market for

making plastic products whereas PS is a key material for

single-use containers and cutleries such as foam

containers, straws, cups, spoons, etc. As a result, we think

IRPC and PTTGC will be the most affected by such a ban

(IRPC with a PS capacity of 125kta, and PTTGC with an

LLDPE capacity of 630kta).

Impact on chemical players of single-use plastic ban

Source: IRPC, PTTGC, SCC, DBSVTH

*note: Joint venture with Dow Chemical and CAP.

ii) Recovered paper ban by China by 2021

The prices of containerboards in the region, including

Thailand, have been led by the demand and supply dynamics

in China, which is the largest market – both regionally and

globally. Thus, we remain optimistic about the improving

supply and demand dynamics in the industry. The supply side

of the industry will be constrained by increasingly stricter

environmental regulations being put in place by the Chinese

government. Tighter monitoring by the Chinese government

will also lower the utilisation rate of small- and medium-sized

containerboard manufacturers to ensure compliance with the

pollution limit.

In July 2017, the Chinese government wanted to encourage

paper recycling to address environmental concerns. So, it

announced that the country would start to ban the imports of

certain types of solid wastes including wastepaper (recovered

paper – RCP), with effect from Jan 2018. Such a ban is in

force and expected to eliminate almost all waste material

imports by 2021.

In China, after the closure of more than 5m tons of obsolete

containerboard manufacturing capacity in Dongguan, other

local governments in the region such as Tianjin, Shandong,

Anhui, and Ningxia have closed the obsolete capacity of small

manufacturers in the ten most polluting industries in recent

months. In addition, the Ministry of Environmental Protection

of China has rolled out the implementation plan for the

issuance of pollutant disposal permits. Industries with severe

pollution issues such as paper manufacturing will need to

obtain permits since 2017. Thus, we expect the paper

industry’s supply growth to be limited by the stricter

monitoring of pollutants disposal.

Declining competitiveness of China’s containerboard players.

As a result of such a ban, we think the Chinese

containerboard players will become less competitive vs. the

other Asian producers due to the following aspects:

i) Rising cost of packaging paper material – Chinese players

have to find more recyclable and environmentally friendly

raw materials. At the same time, additional capital

expenditures are required to ensure cleaner and less

pollution from the production process. Hence, declining

profitability for these players is expected.

ii) Shortage of fibre supply – as Chinese players are required

to invest and/or expand recycled fibre process plants.

Hence, fibre will be in high demand, mainly from China.

Thus, Chinese players’ raw material costs are expected to

head north.

Asian Insights SparX: Resilent packaging

demand while sustainability remains intact

Chemical/Packaging/Paper

Page 22

iii) Inventory build-up by customers – In anticipation of

increasing RCP prices, most customers have built up their

RCP inventory. However, as the Chinese government

becomes stricter on environment protection and US-China

trade war tensions become more intense, a number of

customers are destocking their inventory and dumping their

RCP stock.

iv) High cost producers will exit the market – We expect some

producers to exit the market, especially the ones with

higher operating cost and/or those without vertical

packaging business integration.

Implications for other Southeast Asia players – ample

opportunities abound

We see huge opportunities for fibre-based packaging players

in Southeast Asia in light of the abundant supply of RCP and

marketing opportunities in the Chinese market. The following

outlines the key implications for non-Chinese players:

i) Declining RCP price – As mentioned earlier, a large amount

of RCP supply will flow from China to Southeast Asia. This

will drive down the cost of raw material for fibre-based

packaging producers.

ii) Better RCP quality – Southeast Asia players will gain access

to better quality RCP at low prices, which bodes well for

their profitability.

iii) Geographical proximity – Countries in Southeast Asia

would be best positioned to fill the gap of undersupply of

processed recycled fibre, as recycled pulp can be

transported in wet form vs. the need to ship pulp in dry

form from the US.

iv) Market opportunities in China – Southeast Asia players are

able to provide cheaper packaging paper alternatives and

to look for new markets for Chinese customers.

v) Relocation of Chinese plants – Chinese producers are likely

to re-locate their recycled fibre plants to other counties in

Southeast Asia. However, such process will take some time,

as they could struggle to adapt to an unfamiliar local

culture, and new regulations, laws, customs, etc.

vi) Environmental footprint – China’s ban of RCP signals that

the country is serious about addressing environmental

issues. This could spur other Asian countries to introduce

similar measures to incentivise localised recycling efforts

going forward.

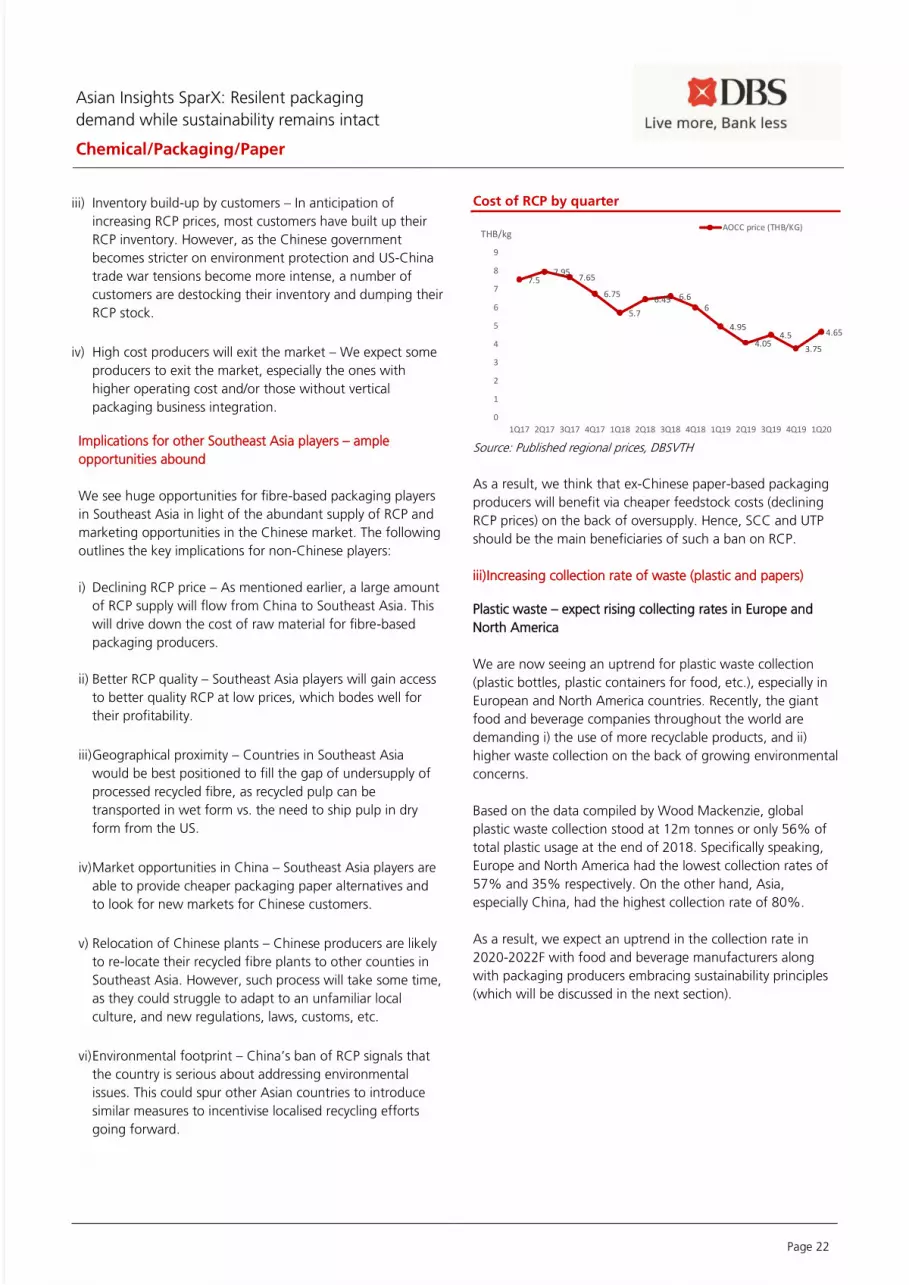

Cost of RCP by quarter

Source: Published regional prices, DBSVTH

As a result, we think that ex-Chinese paper-based packaging

producers will benefit via cheaper feedstock costs (declining

RCP prices) on the back of oversupply. Hence, SCC and UTP

should be the main beneficiaries of such a ban on RCP.

iii) Increasing collection rate of waste (plastic and papers)

Plastic waste – expect rising collecting rates in Europe and

North America

We are now seeing an uptrend for plastic waste collection

(plastic bottles, plastic containers for food, etc.), especially in

European and North America countries. Recently, the giant

food and beverage companies throughout the world are

demanding i) the use of more recyclable products, and ii)

higher waste collection on the back of growing environmental

concerns.

Based on the data compiled by Wood Mackenzie, global

plastic waste collection stood at 12m tonnes or only 56% of

total plastic usage at the end of 2018. Specifically speaking,

Europe and North America had the lowest collection rates of

57% and 35% respectively. On the other hand, Asia,

especially China, had the highest collection rate of 80%.

As a result, we expect an uptrend in the collection rate in

2020-2022F with food and beverage manufacturers along

with packaging producers embracing sustainability principles

(which will be discussed in the next section).

7.57.95

7.65

6.75

5.7

6.45 6.66

4.95

4.054.5

3.75

4.65

0

1

2

3

4

5

6

7

8

9

1Q17 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18 4Q18 1Q19 2Q19 3Q19 4Q19 1Q20

THB/kgAOCC price (THB/KG)

Asian Insights SparX: Resilent packaging

demand while sustainability remains intact

Chemical/Packaging/Paper

Page 23

Plastic waste collection around the globe

Source: Company, Wood Mackenzie, DBSVTH

Paper waste – paper collection rate should trend up

The efforts to promote global waste paper collection (to

gather recycled paper or recovered paper (RCP)) are highly

uneven, with RCP use mostly stemming from the developed

world, especially Europe and the US. However, most Asian

paper companies are now acting as waste paper recyclers,

accepting and processing most of the RCP generated in

Europe and the US (a.k.a. EOCC and AOCC respectively).

Specifically, China has been by far the biggest recycler,

though this will likely soon change with significant

ramifications for the global recycling industry. Based on data

compiled by CEPI, China imported EOCC/AOCC of

c.80%/65% in 2017 and c.50%/40% in 2018. With the ban

on such imports by China, we expect the numbers to decline

in short to medium term. On the other hand, Europe’s paper

recycling rate increased to 72% in 2019 (vs. 69% in 2010),

with more paper being recycled by European paper mills.

In line with the plastic waste collection trend, we also expect

a higher waste paper collection rate due to rising awareness

of environmental and social issues.

Europe’s recycling rate

Source: CEPI, DBSVTH

iv)Sustainability principles

The principle of “business sustainability” is any organisation

that participates in environmentally friendly or green activities

to ensure that all processes, products, and manufacturing

activities adequately address current environmental concerns

while maintaining a profit. In other words, it is a business that

meets the needs of the present [world] without compromising

the ability of future generations to meet their own needs. It is

the process of assessing how to design products that will take

advantage of the current environmental situation and how

well a company’s products perform with renewable resources

(source: Wikipedia website).

There is growing concern over sustainability as well as ESG

(environment, social, and governance) for both end-

consumers, i.e. households, and packaging customers, i.e.

food and beverage manufacturers, homecare, personal-care,

healthcare products manufacturers. So, there is high demand

for the recycling of feedstock materials and/or recyclable

products from these producers. For example, large multi-

national companies (MNC) of beverage and consumer-care

product producers such as Coca Cola, PepsiCo, Unilever,

Procter and Gamble, and Starbucks demand their packaging

materials such as PET bottles, product containers to be i)

made from recycled materials, and ii) recyclable. Hence, we

expect many chemical and packaging companies to start

focusing on sustainability initiatives going forward in 2021F.

Our channel checks with several companies reveal the

growing popularity of the following practices:

i) The need to utilise less energy consumption/usage during

the production process

ii) Increase renewable energy sources to reduce greenhouse

and carbon emissions to the atmosphere

iii) Optimise resources and energy sources for maximum

production efficiency

iv) Increase the proportion of renewable and recyclable

feedstock

v) Increase investments in R&D for product innovations that

are environmentally friendly

Here are some initiatives rolled out by Thai listed companies.

Asian Insights SparX: Resilent packaging

demand while sustainability remains intact

Chemical/Packaging/Paper

Page 24

Indorama Ventures Plc (IVL TB, HOLD, TP of Bt24) – To ensure

economic prosperity and sustainability

The goal is to ensure economic prosperity and sustainability

for all its stakeholders in the energy business. IVL measures its

success not just by economic gains but by the achievements in

preserving the environment, thereby benefiting the society at

large. IVL undertook several initiatives in 2018 that are in line

with the commitment to increase its focus on long-term

sustainability through recycling, lowering its carbon footprint,

increasing the use of renewable energy, and developing

human capital.

By 2020F, IVL aims to achieve the following sustainability

goals: i) investing in recycled PET products in its portfolio (with

a targeted capacity of 750ktpa), ii) reducing its carbon

footprint by 10%, iii) reducing its energy consumption by 5%,

iv) increasing its renewable energy resources by 10%, and v)

reducing its water consumption by 10%. Moreover, one of its

directors has been directly assigned to spearhead IVL’s

sustainability initiatives.

SCG Packaging Plc (SCGP TB, BUY, TP of Bt44) – ESG in its

core DNA

Generally, SCGP is leading the change to replace single-use

plastic with paper and green packaging. Its business model is

compatible with the green trend, as it embarks on replacing

plastic by using 95% RCP and building out plastic

replacements. Moreover, it aims to achieve 100% recyclable

plastic and plastic substitute products.

Additionally, SCGP will also focus on maximising packaging

material lifecycle through the following processes:

i) Production stage – Reduce raw material usage while

maintaining product strength, improve the tensile and

burst strength of fibre-based products, improve barrier

properties, improve product shelf life and recyclability.

ii) Manufacturing stage – Build 10MW waste-to-energy

facility that can recycle up to 100k tonnes of waste paper

per year, with 95% of its raw materials sourced from RCP

and 25% of its water consumption coming from internal

water treatment systems.

iii) Recovery and recycling stage – Collaborate with retail