Embed Size (px)

Citation preview

35 Years of legacy

41 Touch-points

24 Cities across the country

1,450+ AAA

Employees

Credit Rating

03 Subsidiaries operating in capital market

2020 marked the 35th year of IDLC. Our clients, shareholders, employees, partners, regulators, and the community at large, have each been an integral part that made us whole and who we are today; one of the most recognized and the largest financial institution of the country. Hand-in-hand we have trekked over mountains and have attained new heights. Despite many challenges along the way we, as a family, grew together. Thus, at this milestone we reflect on the lives we have touched, gave us a reason to exist and provided us the opportunity to give back to the community. This year we are sharing with you the stories which we consider as our achievements and inspiration for our journey ahead...

CONTENTSHighlights 4

About Our Integrated Report 6

Stakeholders Identification 9

Materiality Determination Process 10

Navigating Through This Report 11

THE COMPANY OPERATING ENVIRONMENT AND RISK MANAGEMENT

MANAGEMENT DISCUSSION & ANALYSIS

STEWARDSHIP

Our Philosophies 13

Key Milestones 14

Products & Services 16

IDLC Integrated Business Model & Activity Models 18

National Footprint 21

Value Chain Activities & Impacts 22

How We Create Value 24

Our Capitals

Financial Capital 26

Human Capital 28

Manufactured Capital 30

Intellectual Capital 32

Social & Relationship Capital 34

Natural Capital 36

Stakeholders Engagement 38

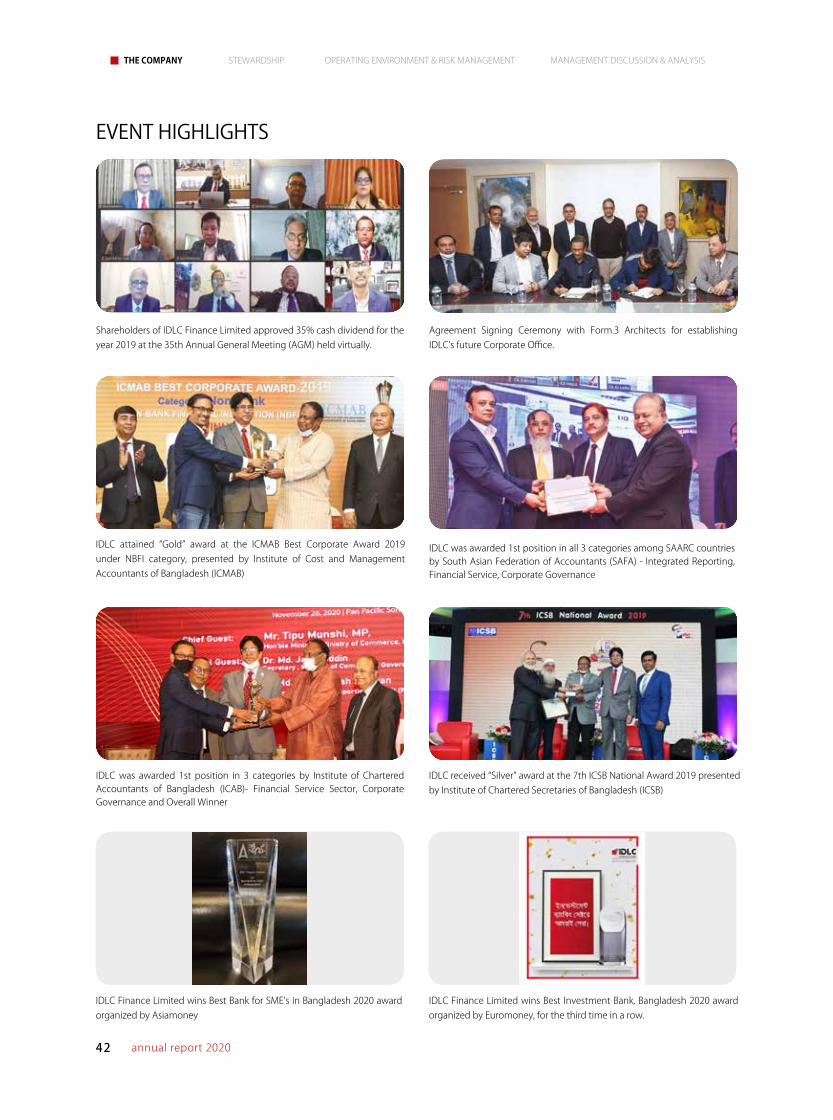

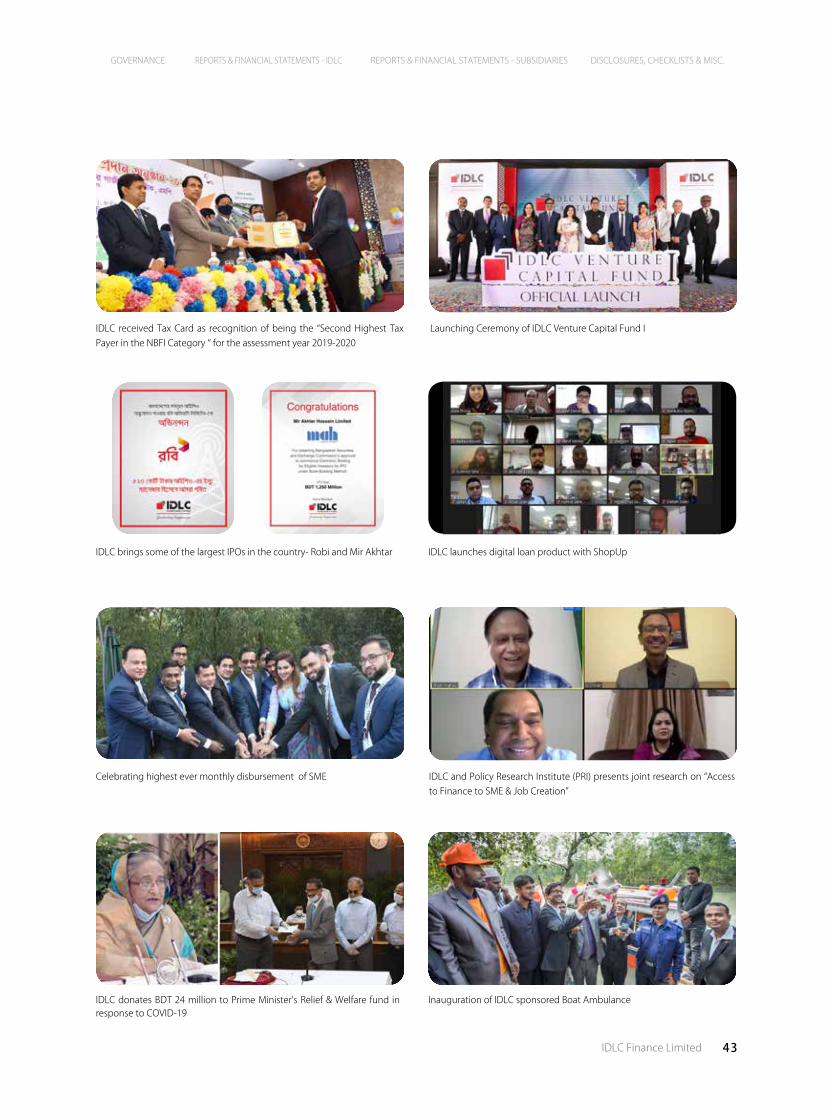

Event Highlights 42

Awards & Accolades 46

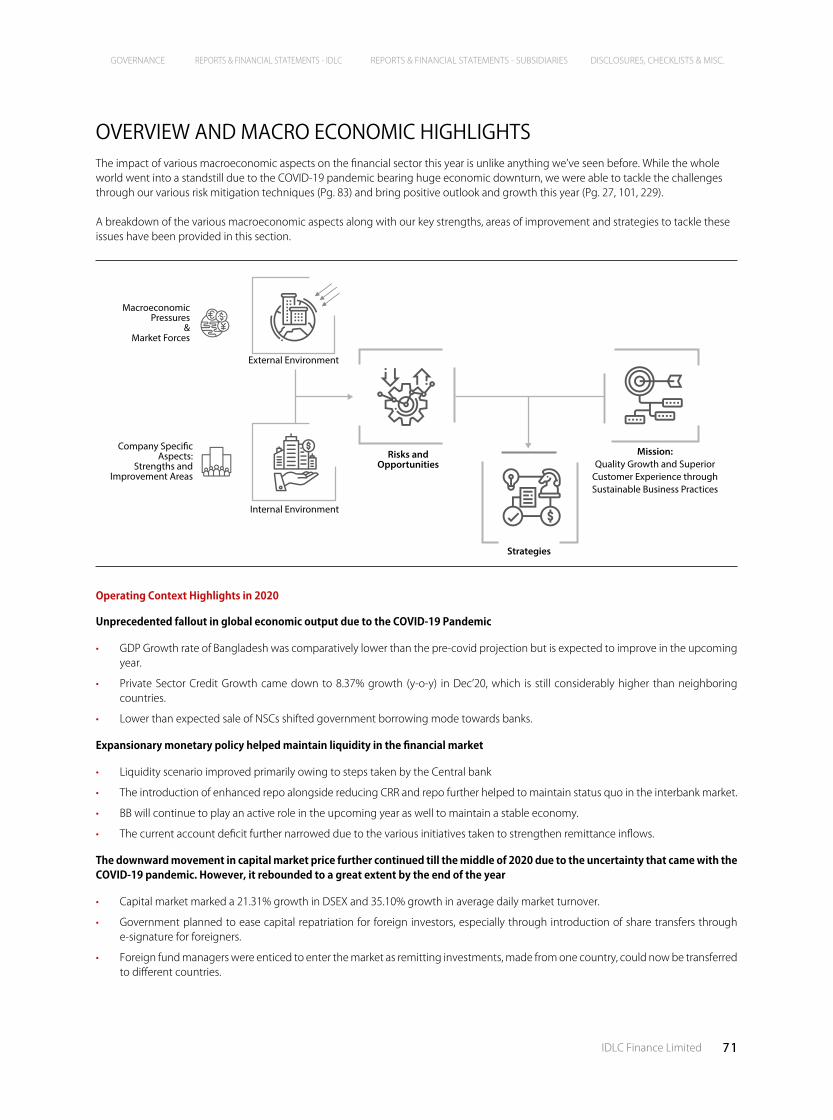

Overview & Macroeconomic Highlights 71

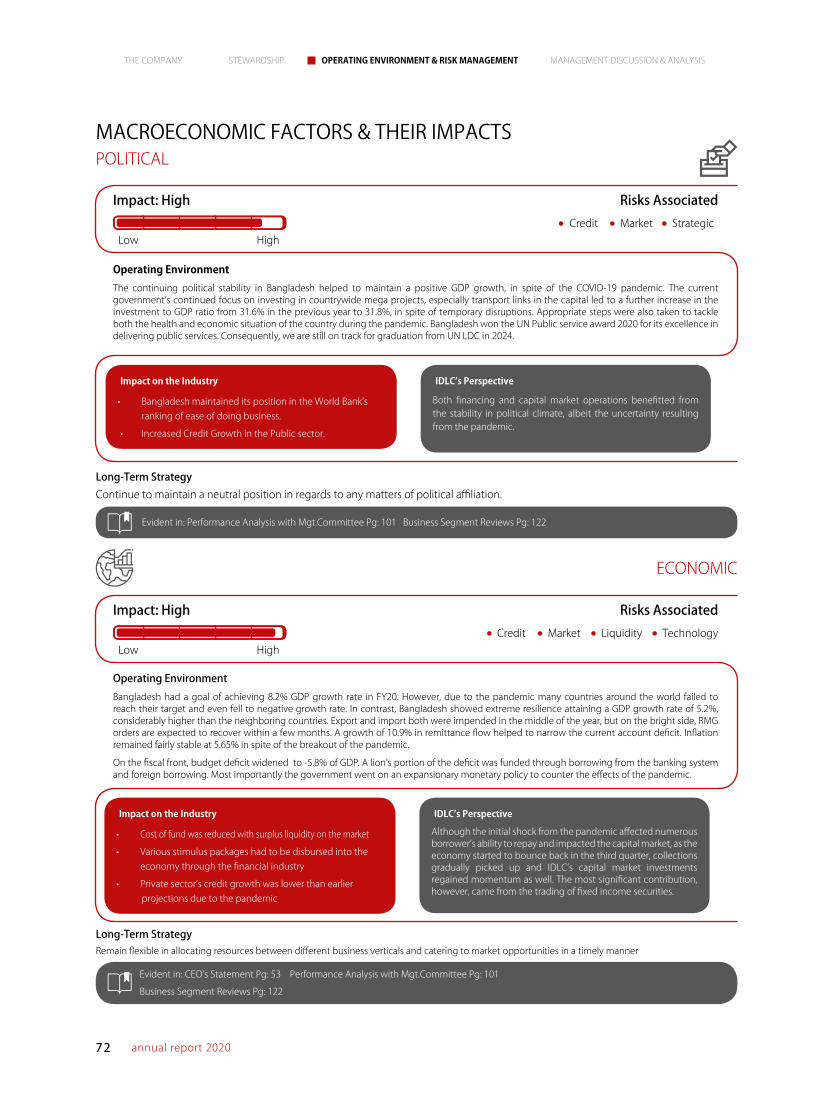

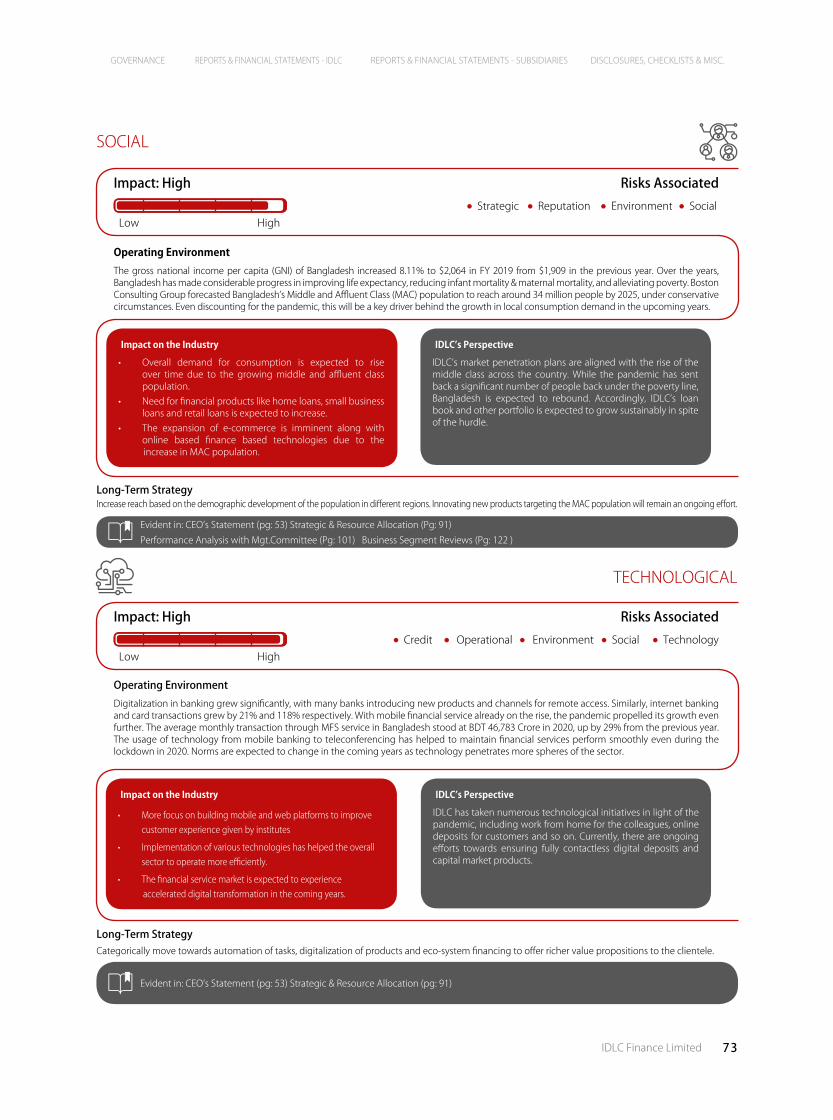

Macroeconomic Factors & Their Impacts 72

Market Forces & Competitive Landscape 75

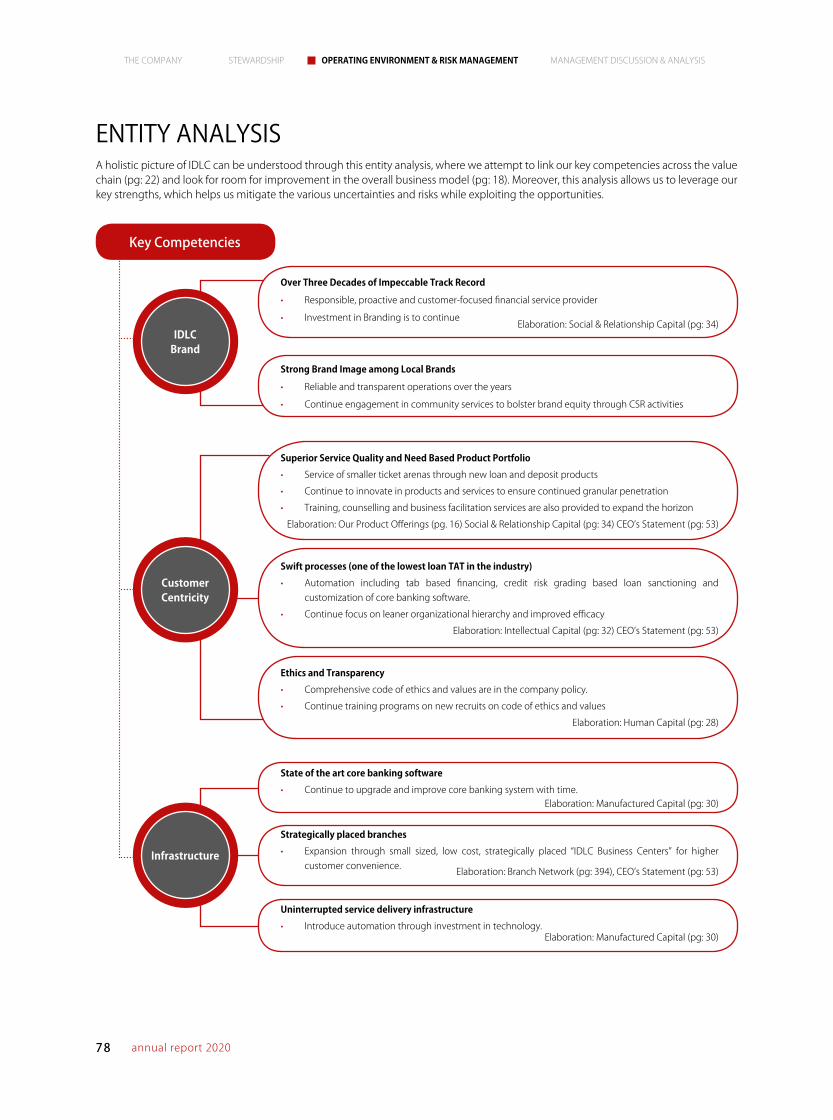

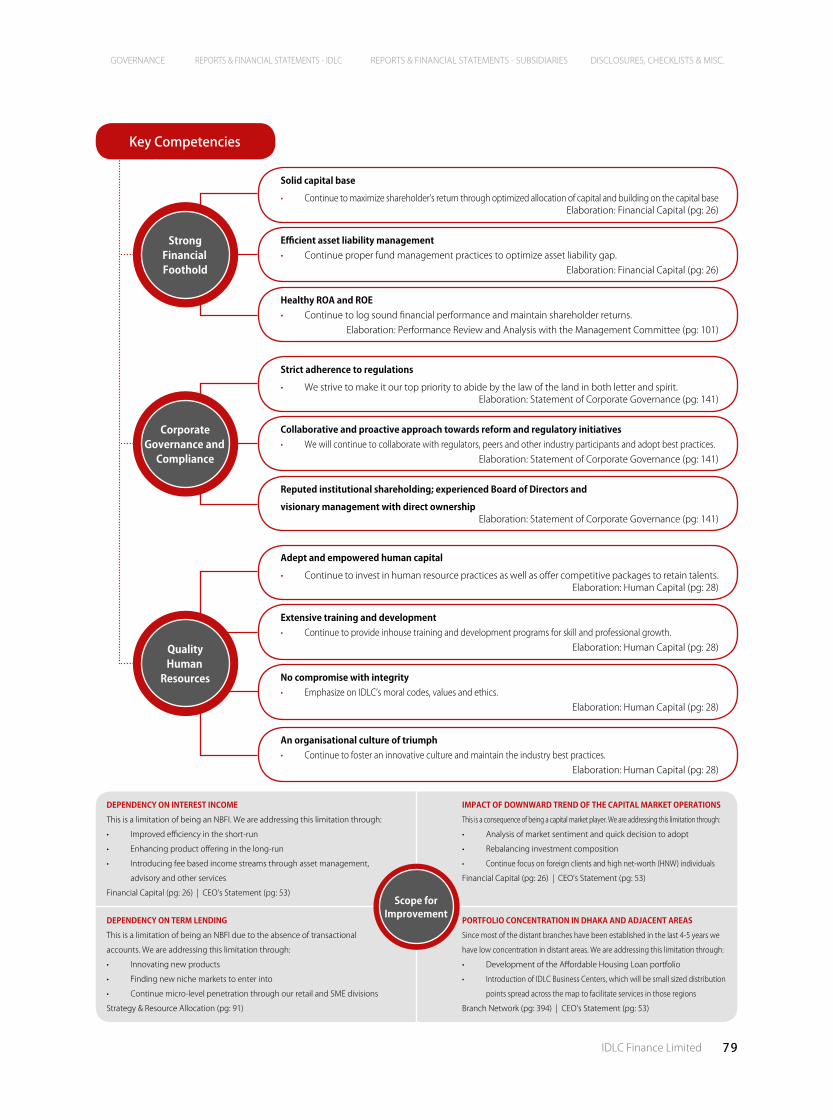

Entity Analysis 78

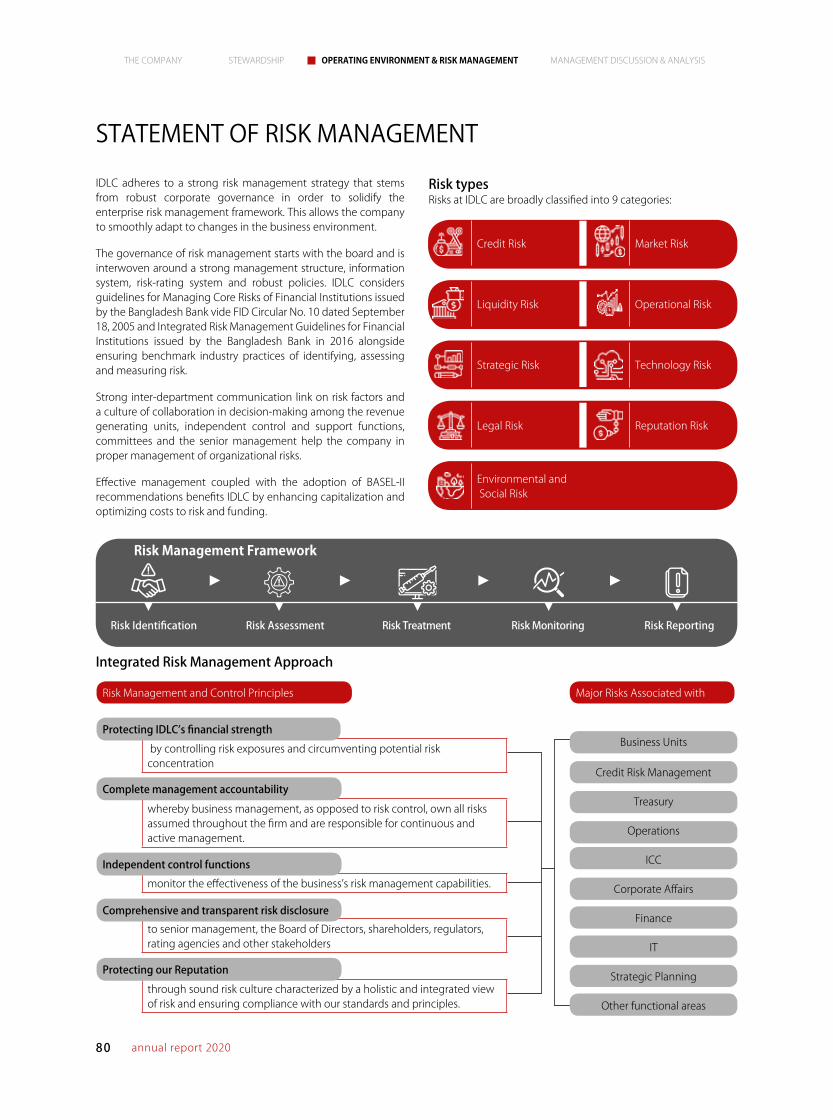

Statement of Risk Management 80

Message from the Chairman 49

CEO's Statement 53

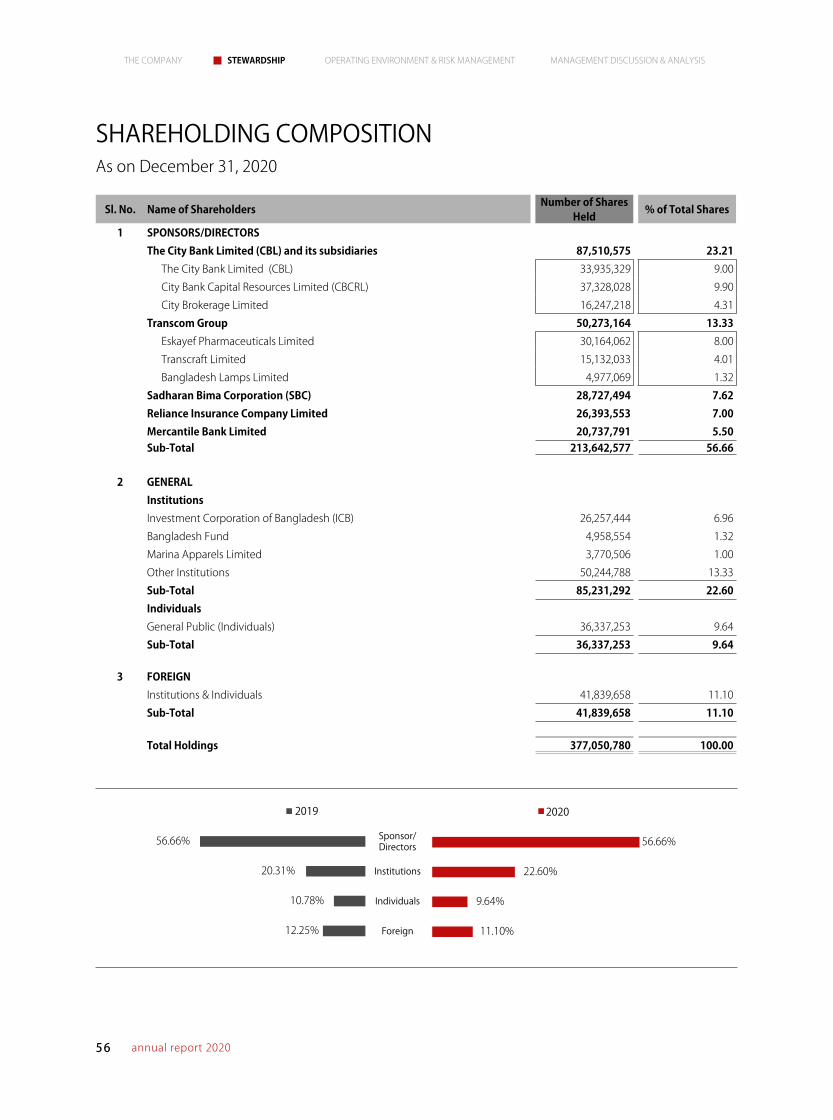

Shareholding Composition 56

Board Composition 57

Organisational Chart 63

Management Committee 64

Senior Executives 68

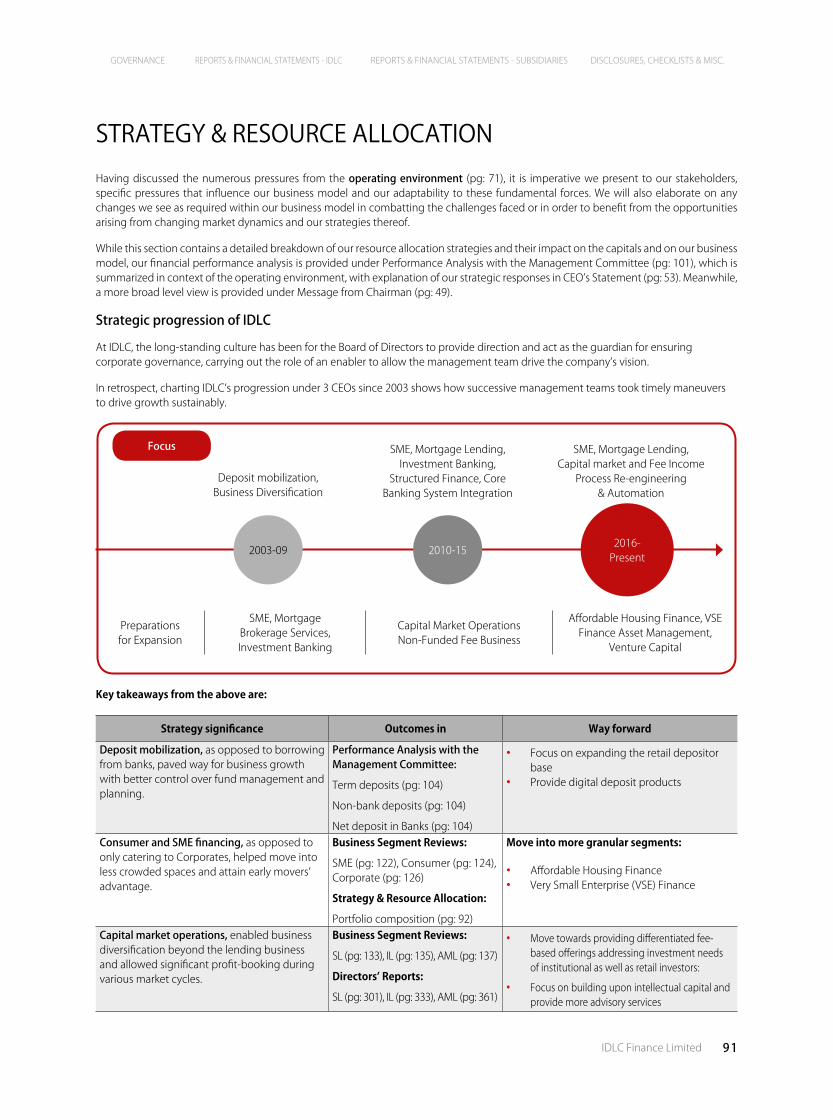

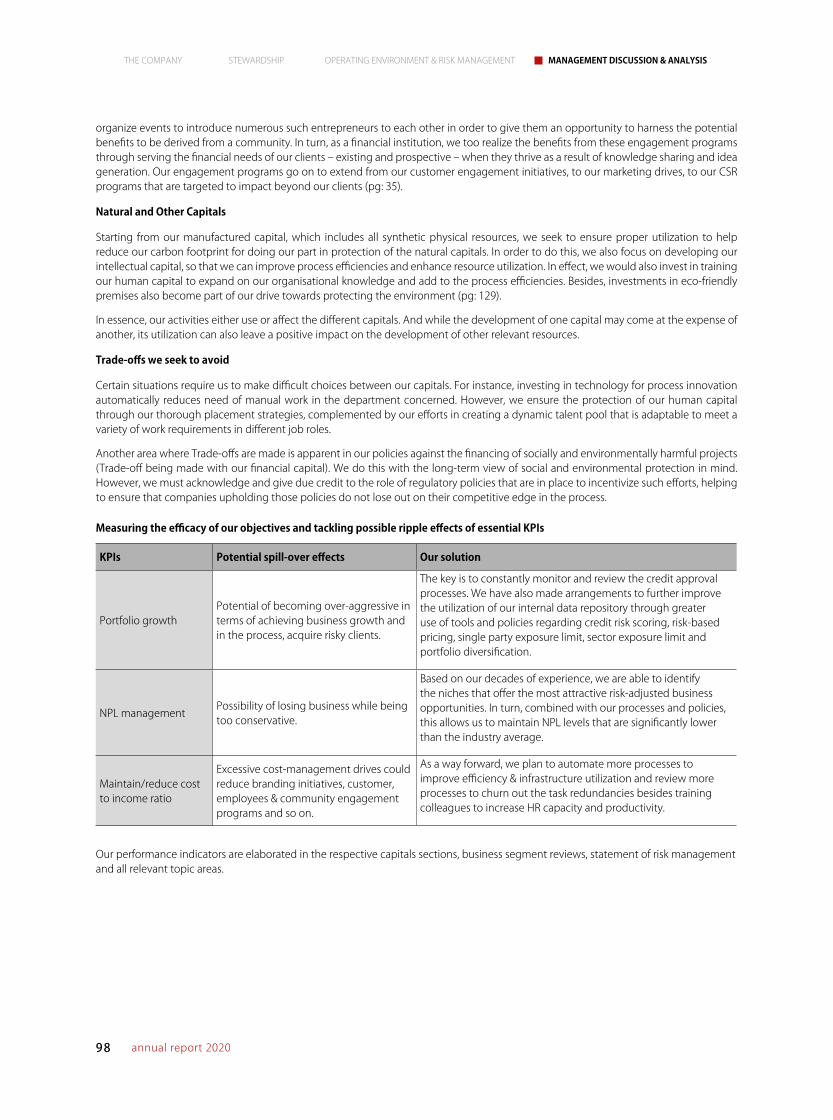

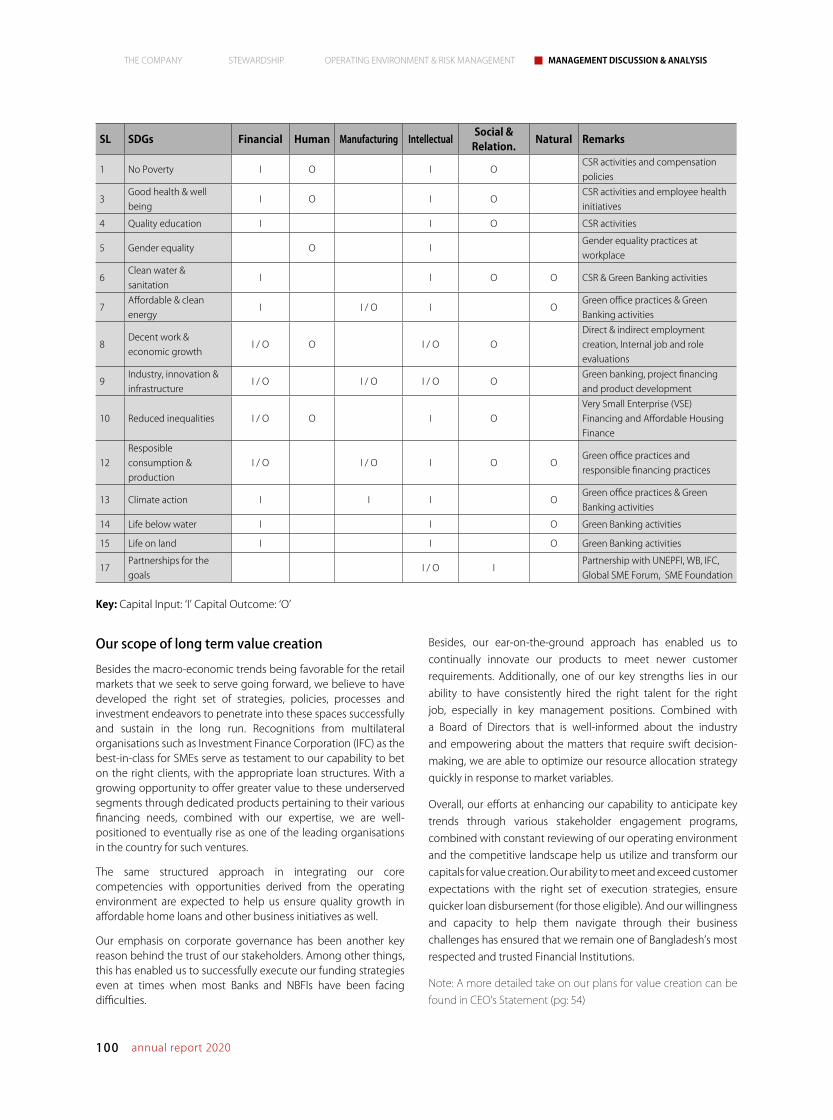

Strategy & Resource Allocation 91

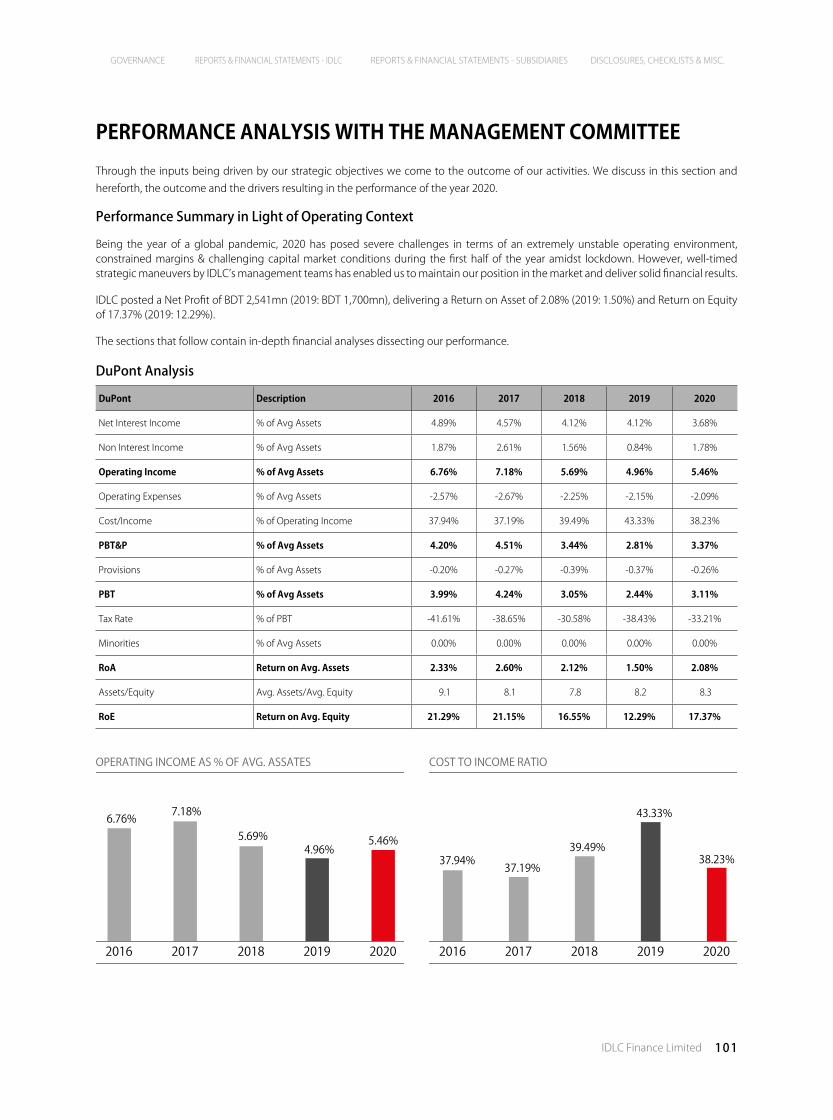

Performance Analysis with the Management Committee 101

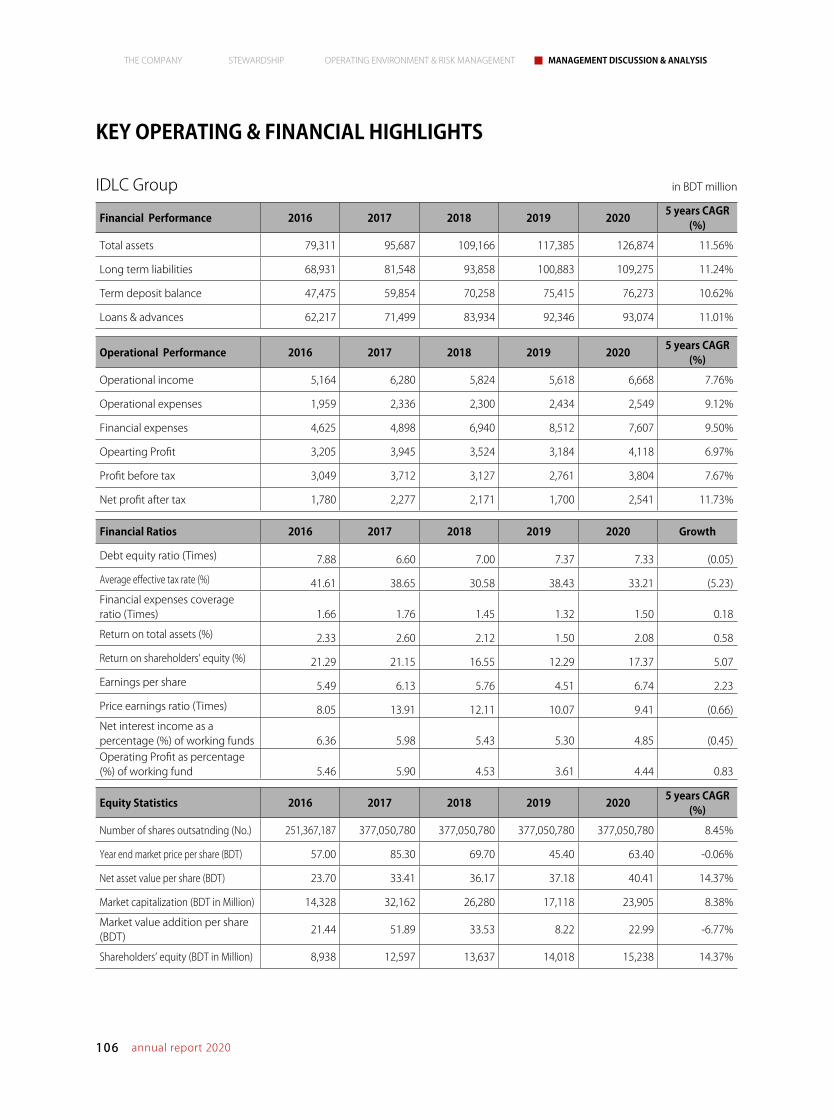

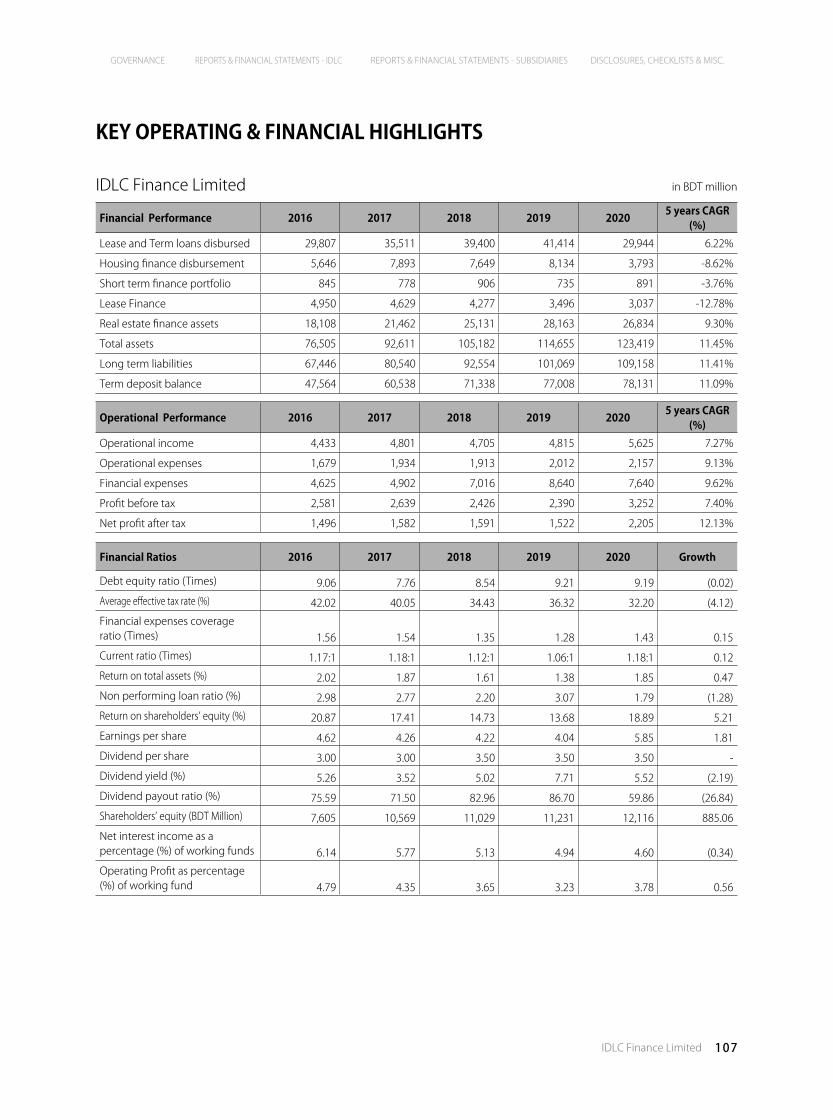

Key Operating & Financial Highlights 106

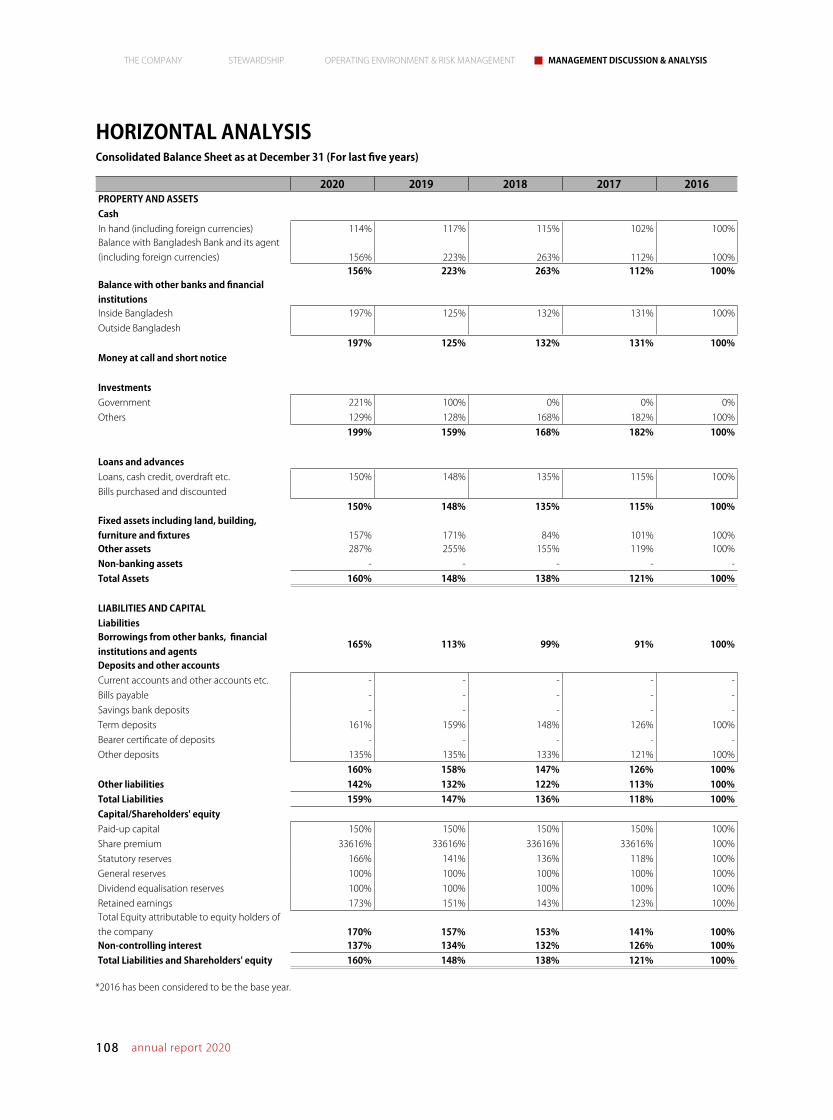

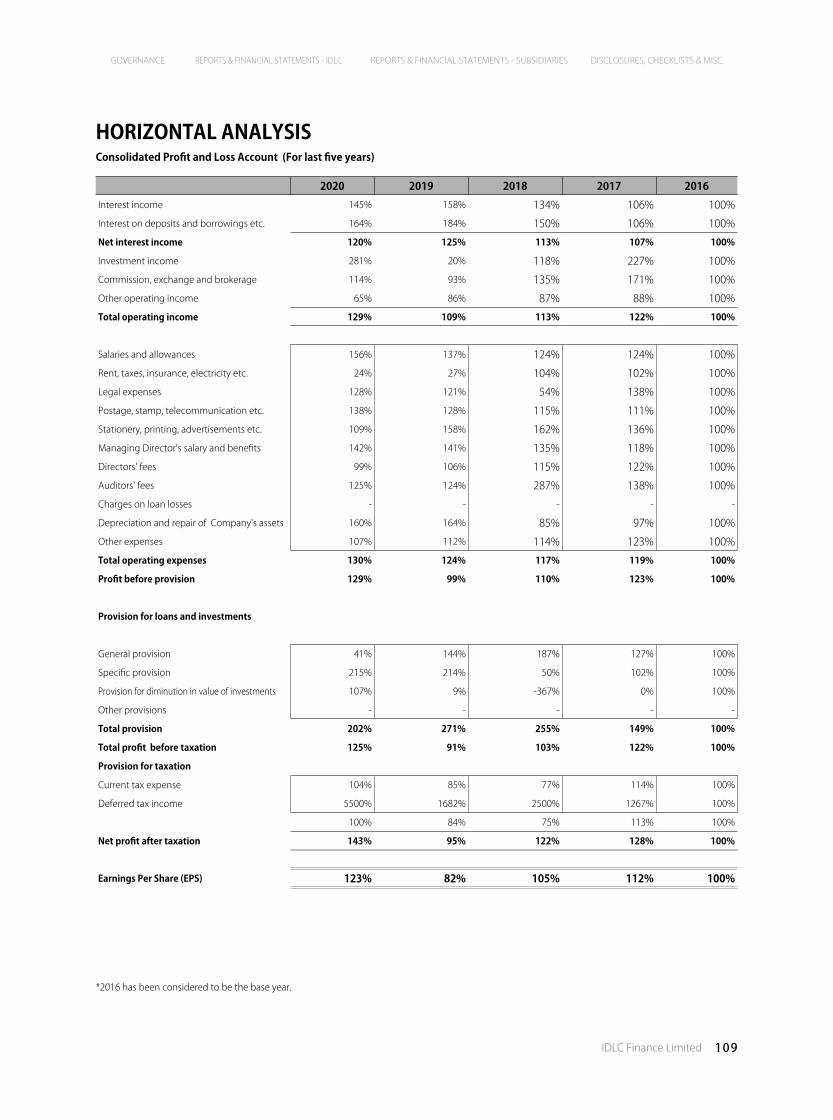

Horizontal Analysis 108

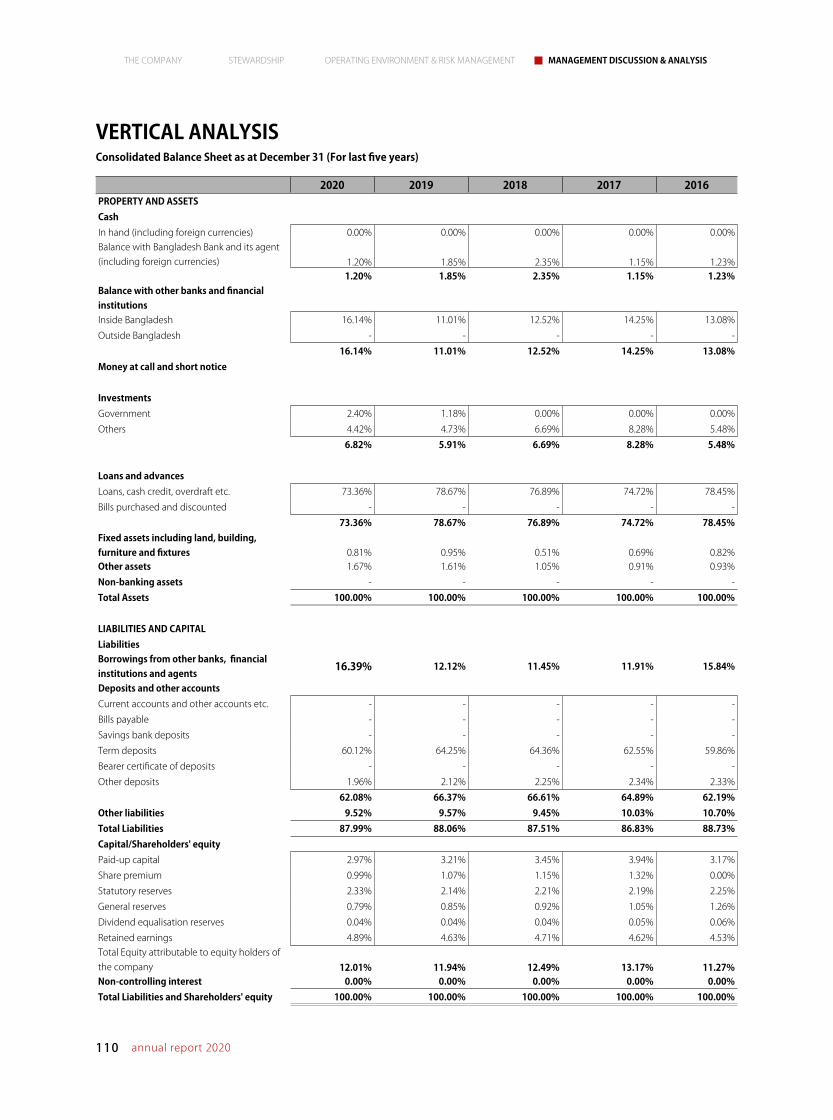

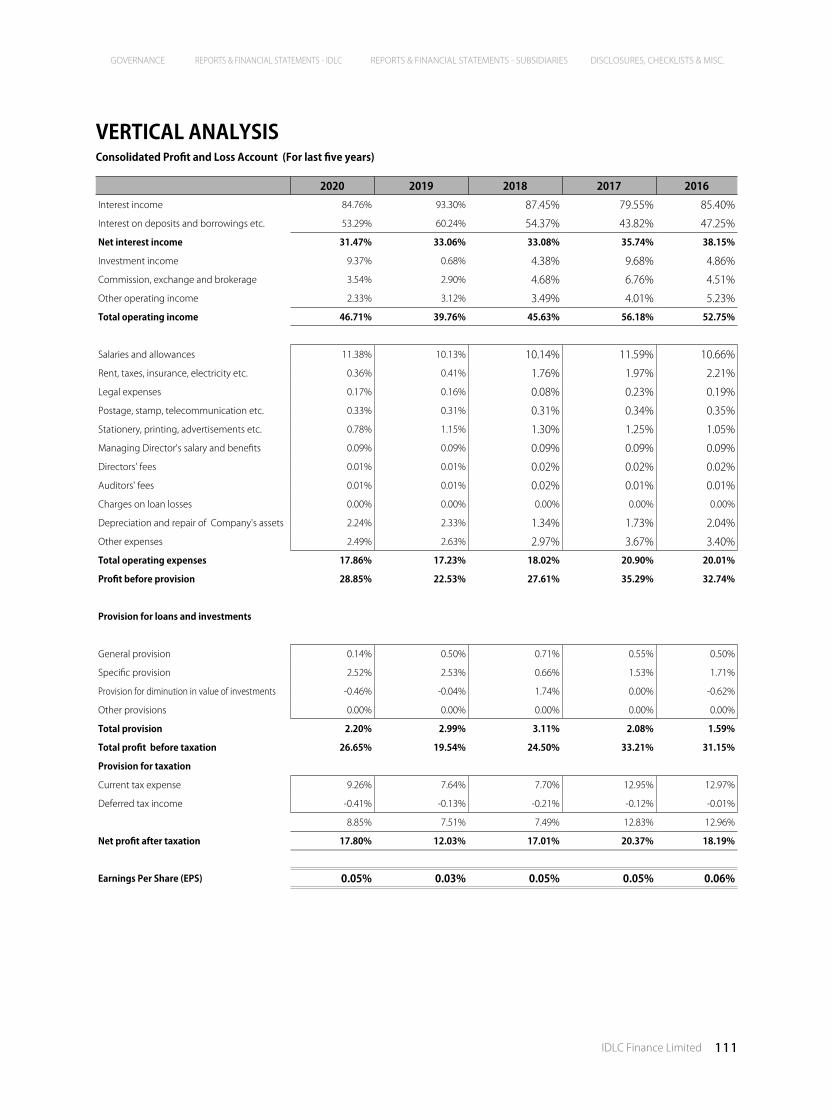

Vertical Analysis 110

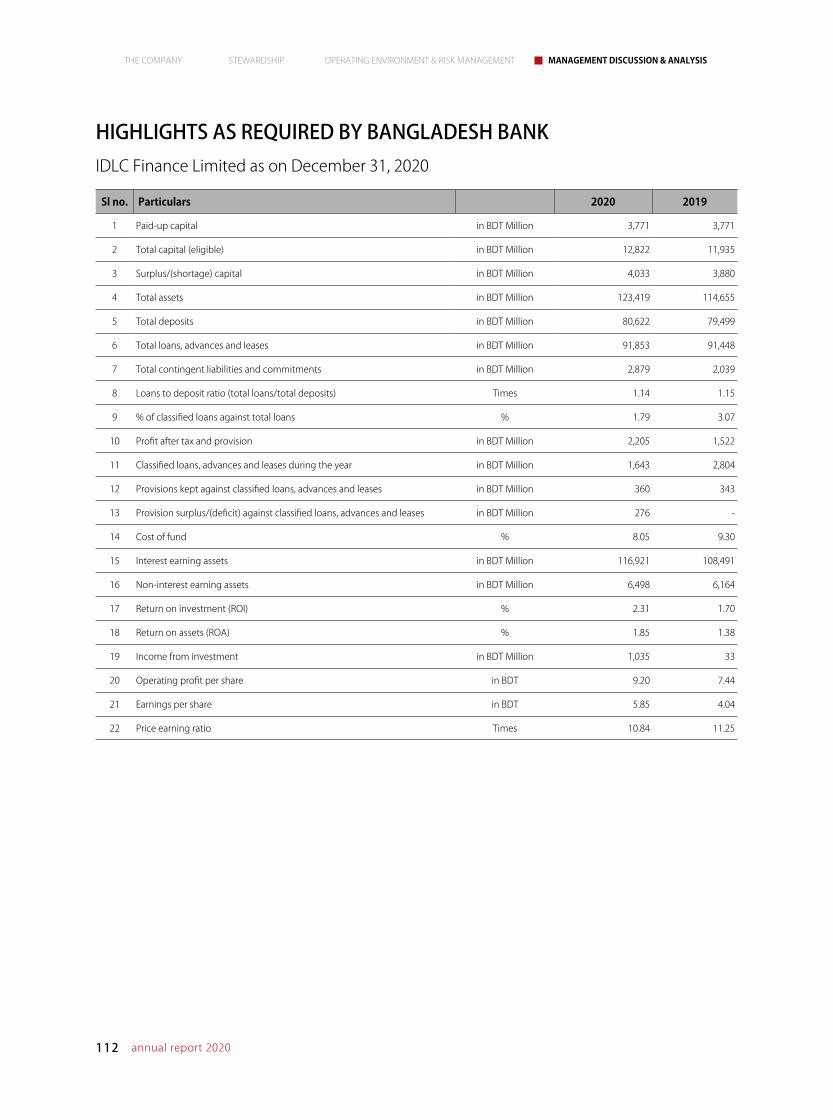

Highlights as Required by Bangladesh Bank 112

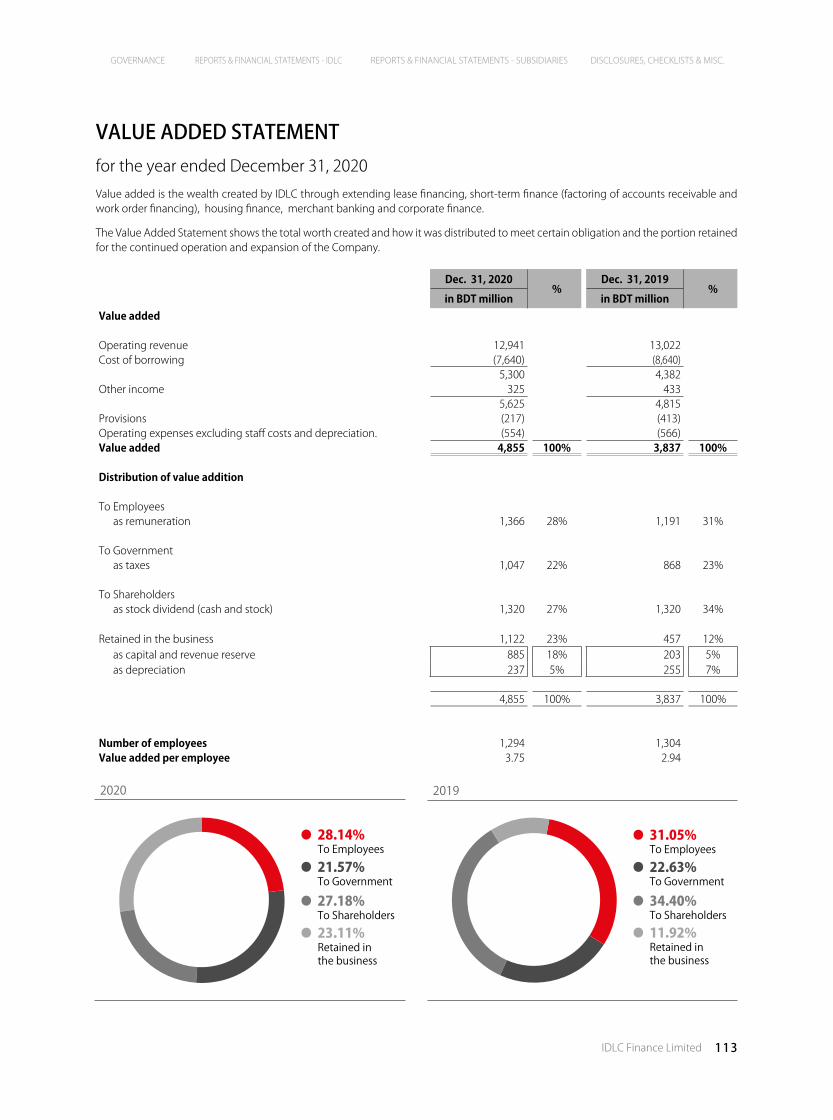

Value Added Statement 113

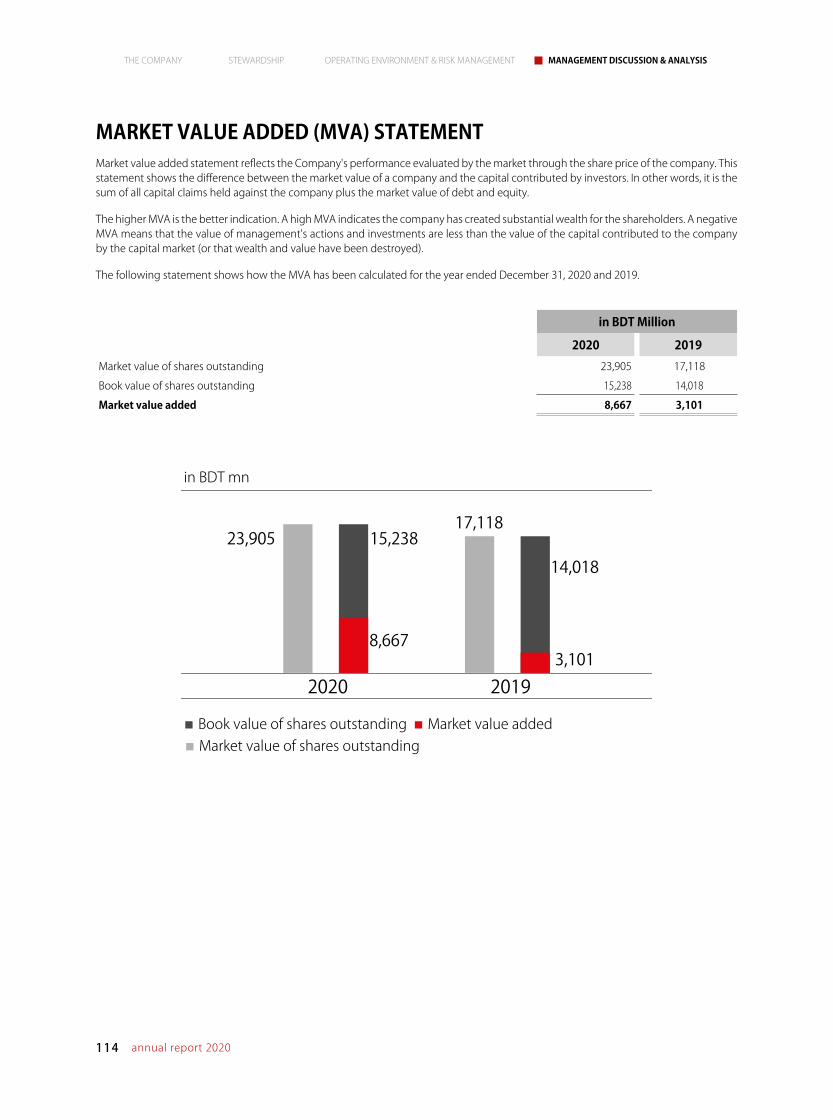

Market Value Added (MVA) Statement 114

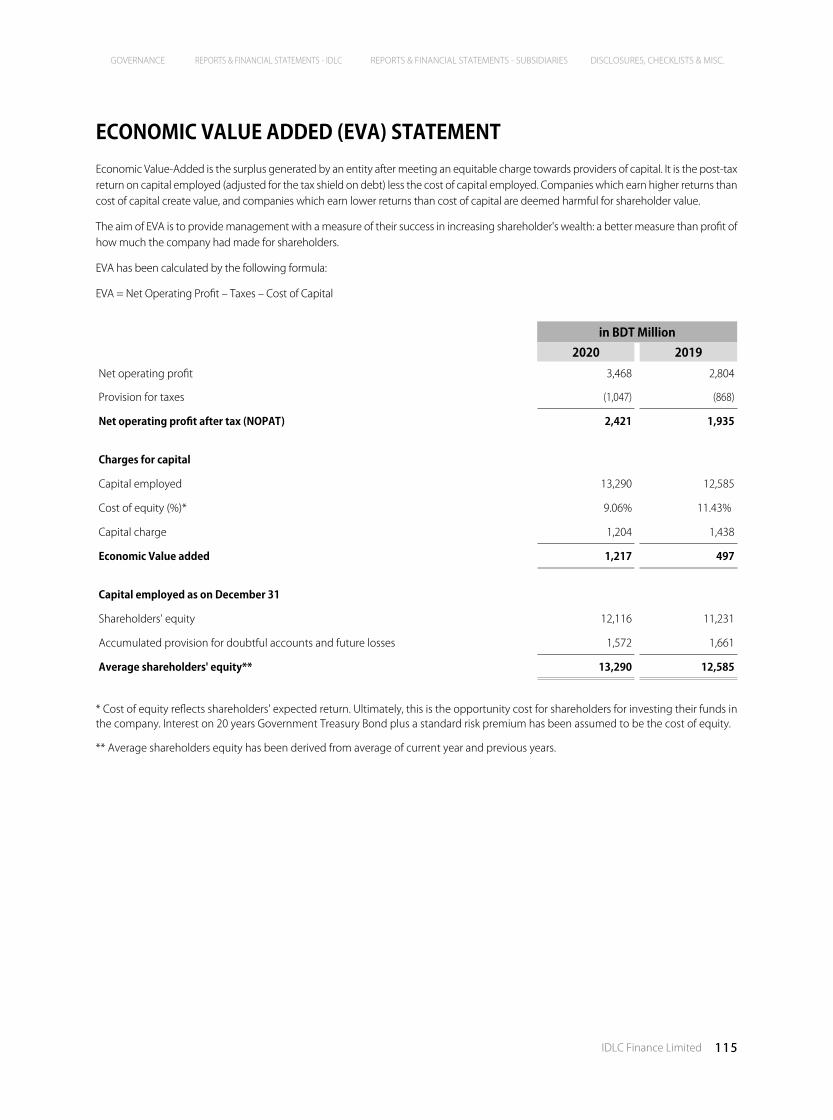

Economic Value Added (EVA) Statement 115

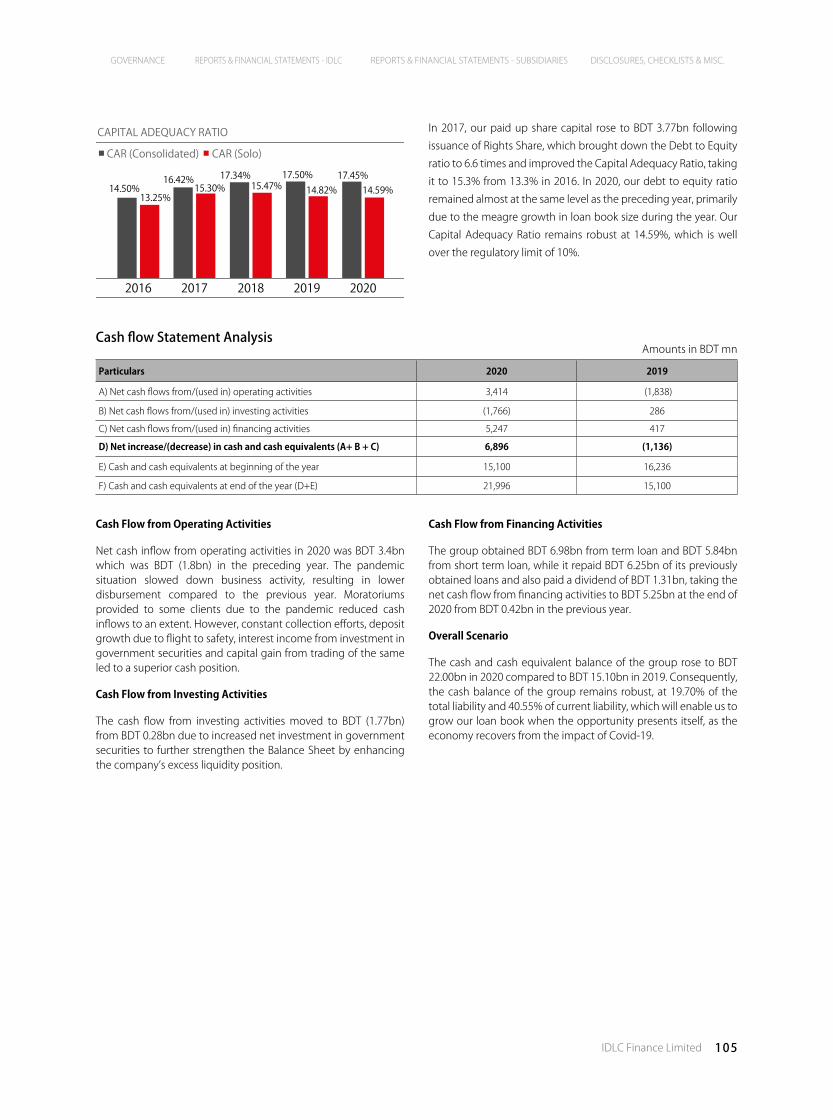

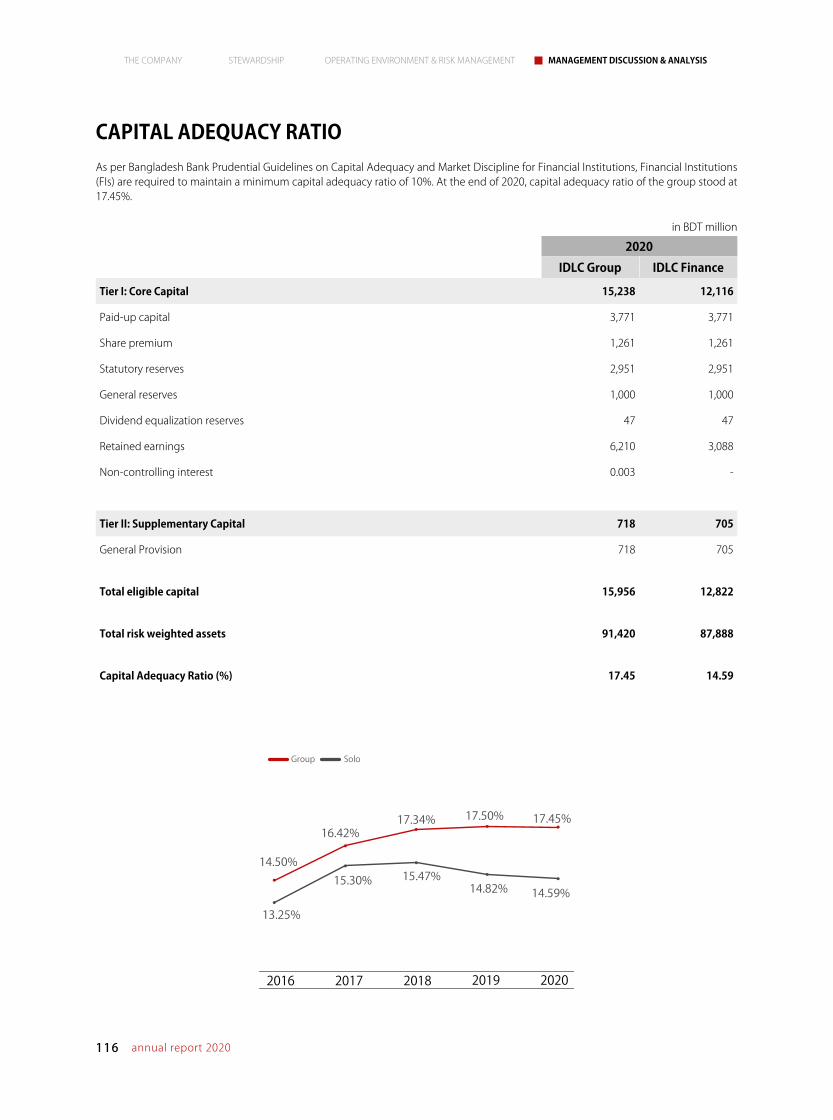

Capital Adequacy Ratio 116

Contribution to the National Economy 117

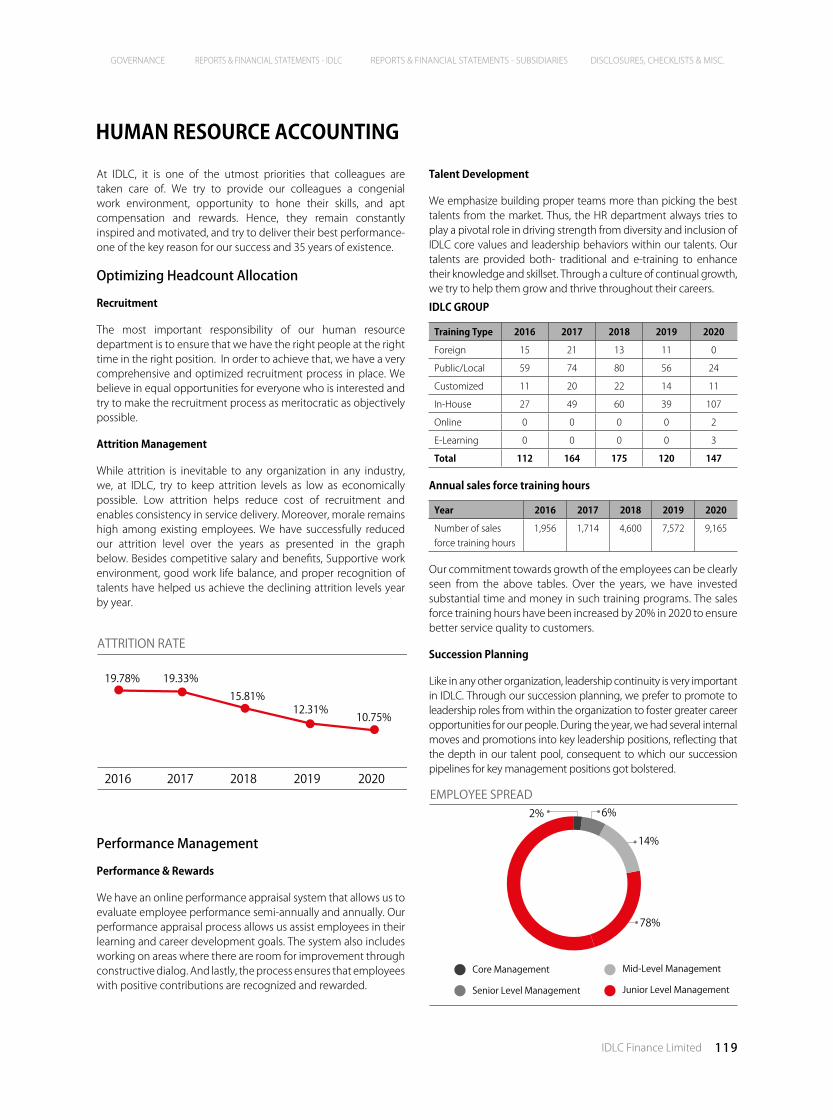

Human Resource Accounting 119

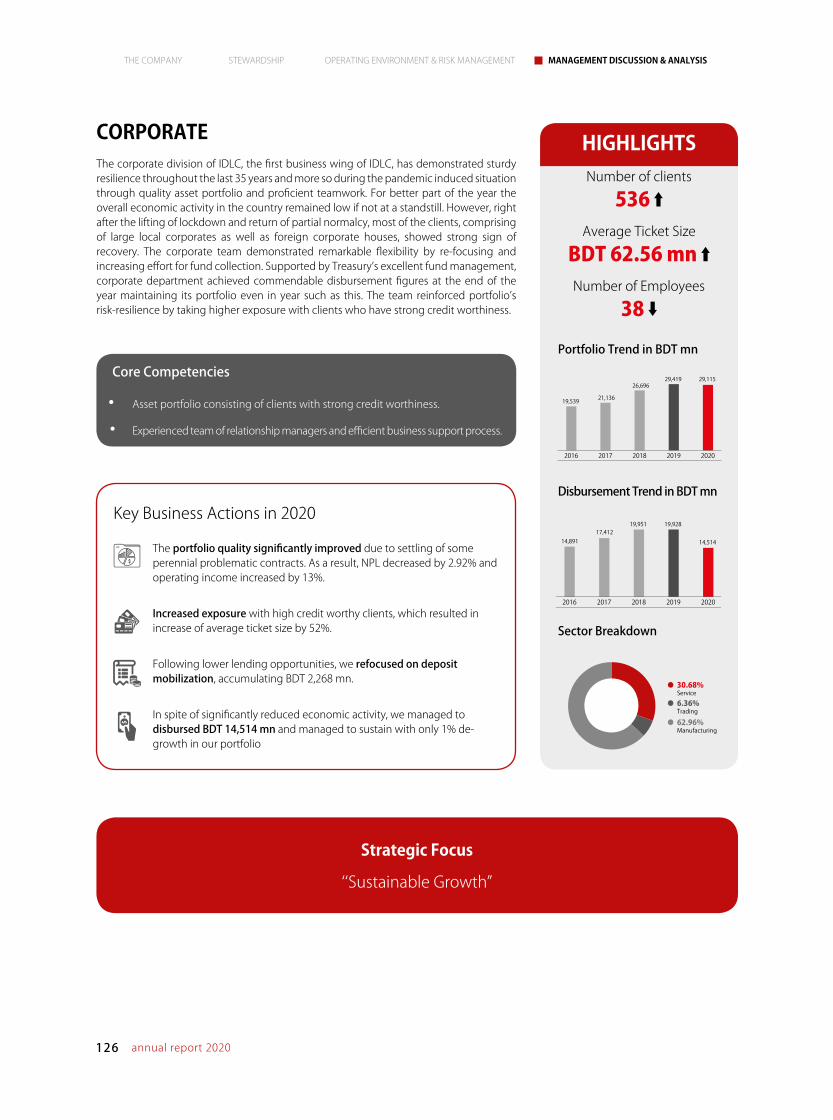

Business Segment Review – Core Financing

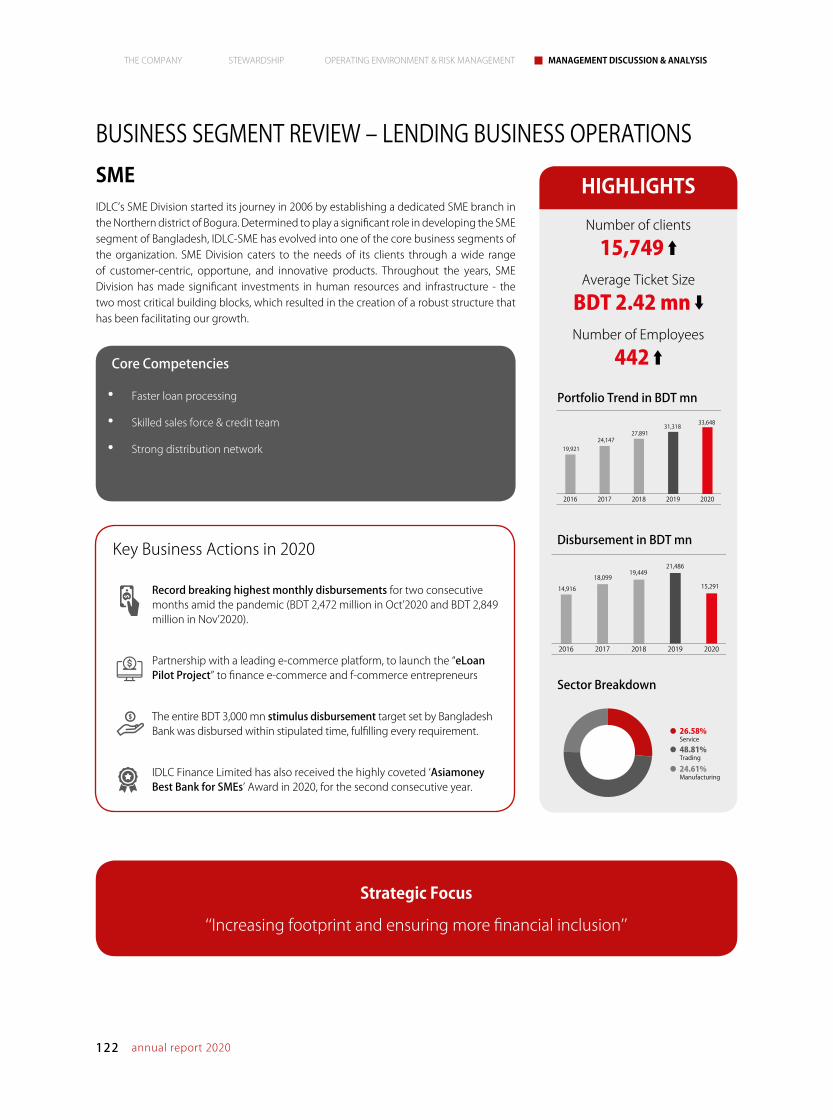

SME 122

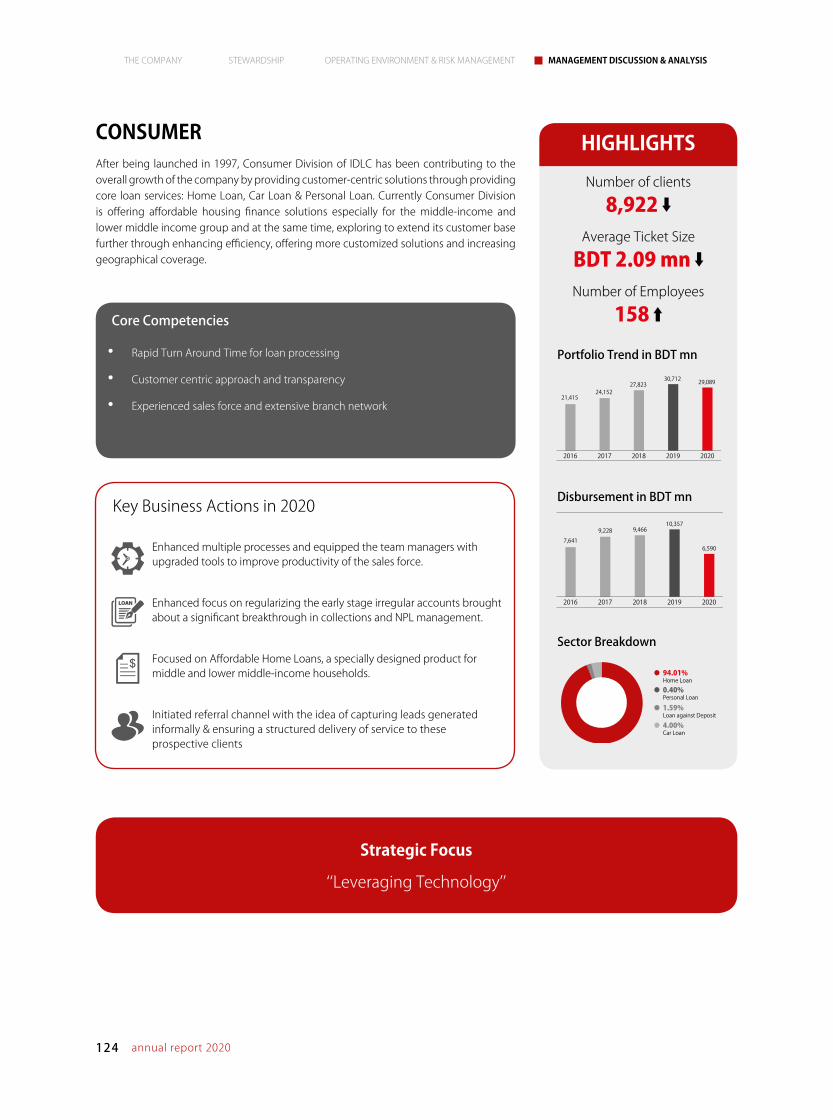

Consumer 124

Corporate 126

Structured Finance 128

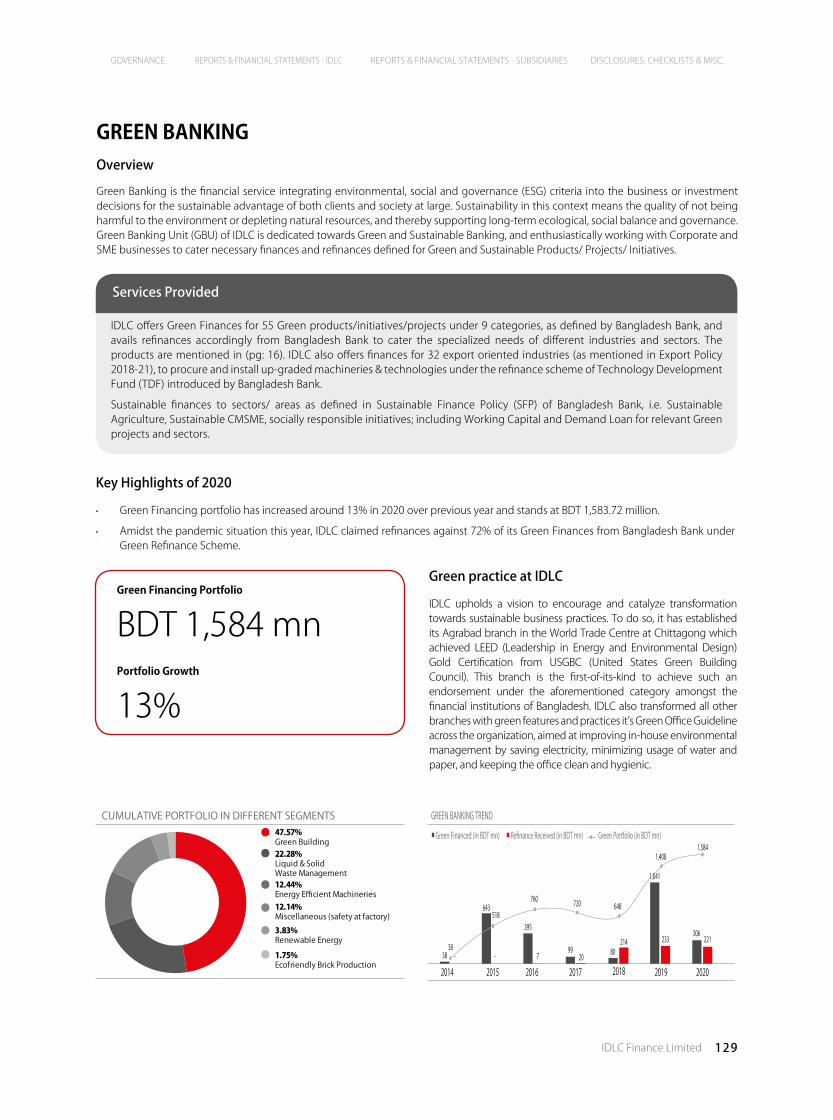

Green Banking 129

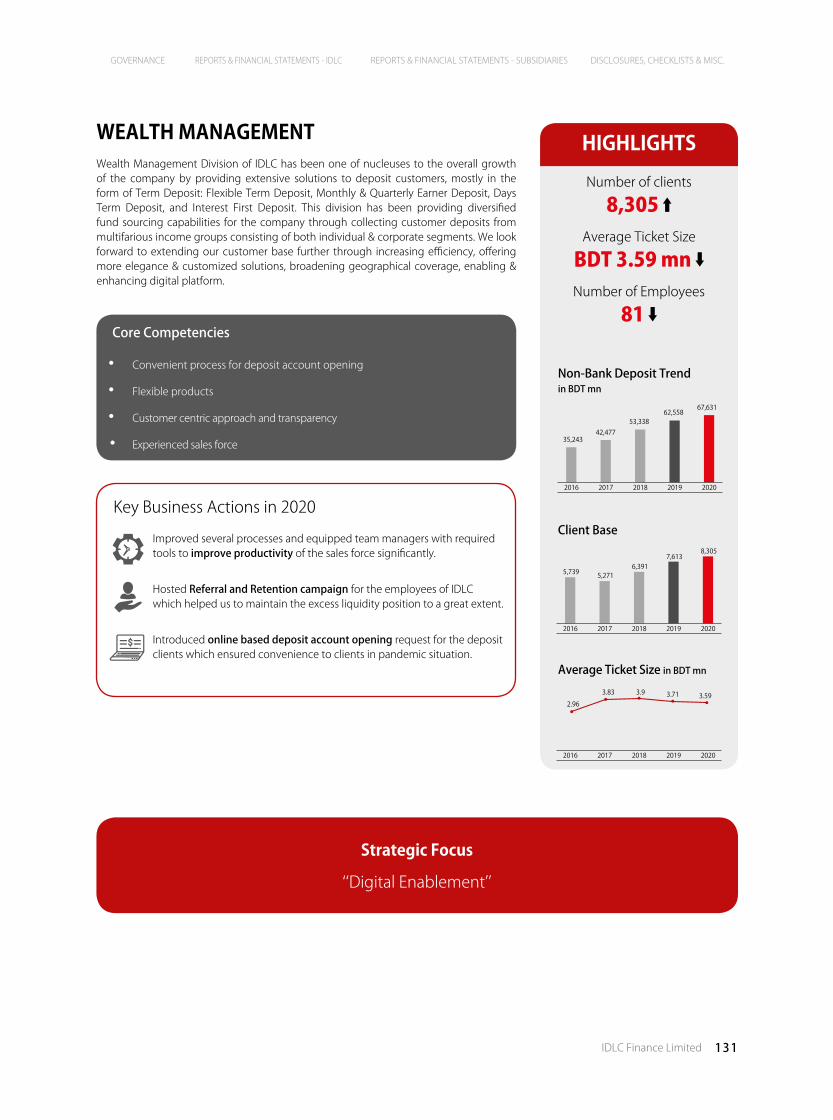

Wealth Management 131

Business Segment Review – Subsidiaries

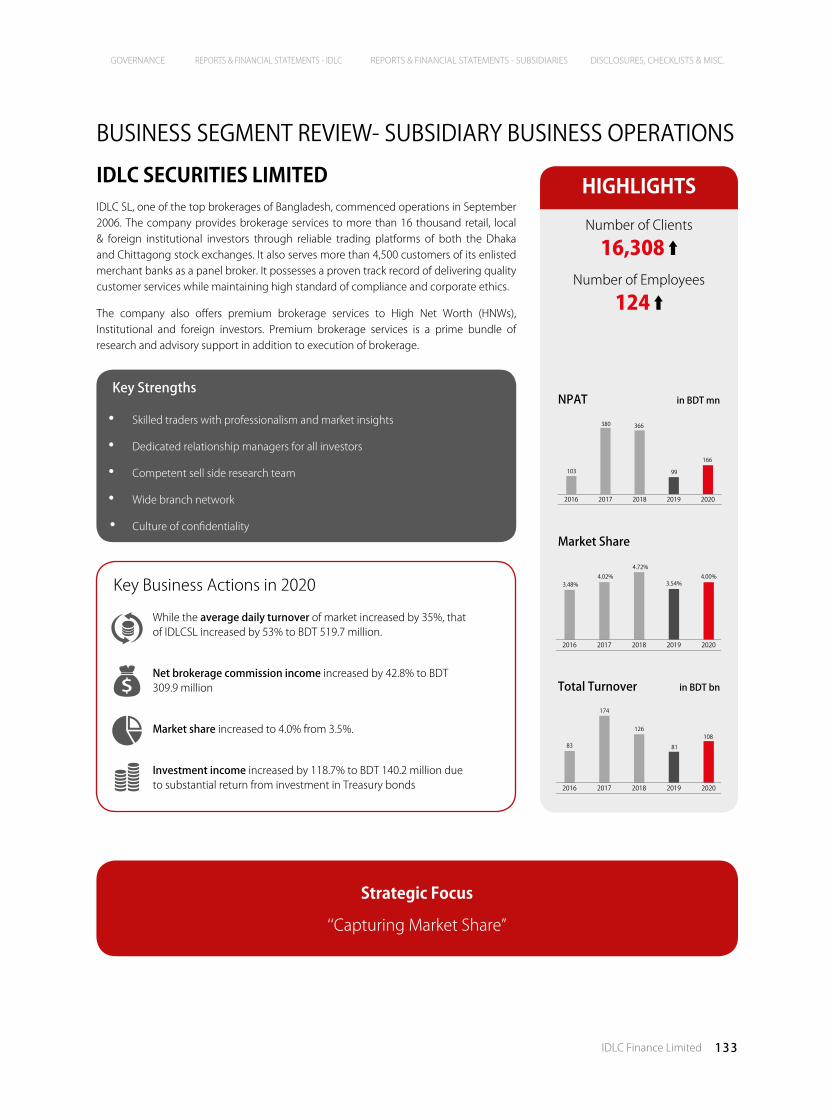

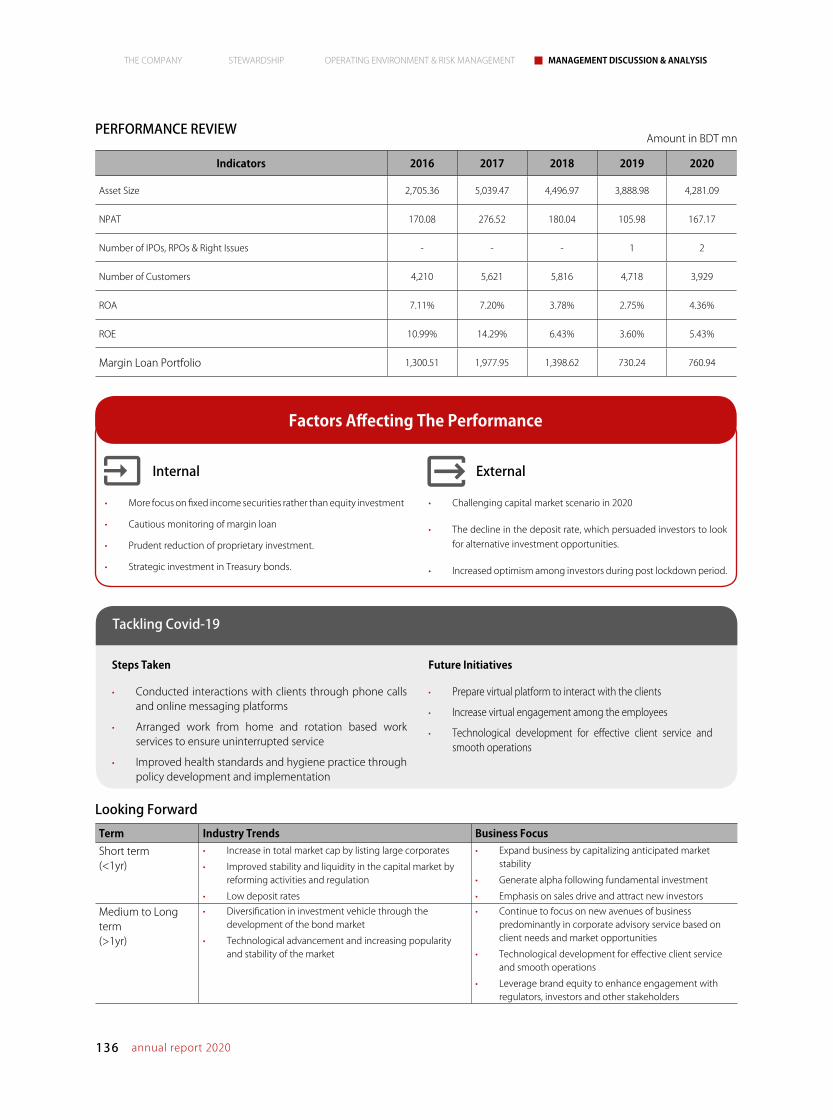

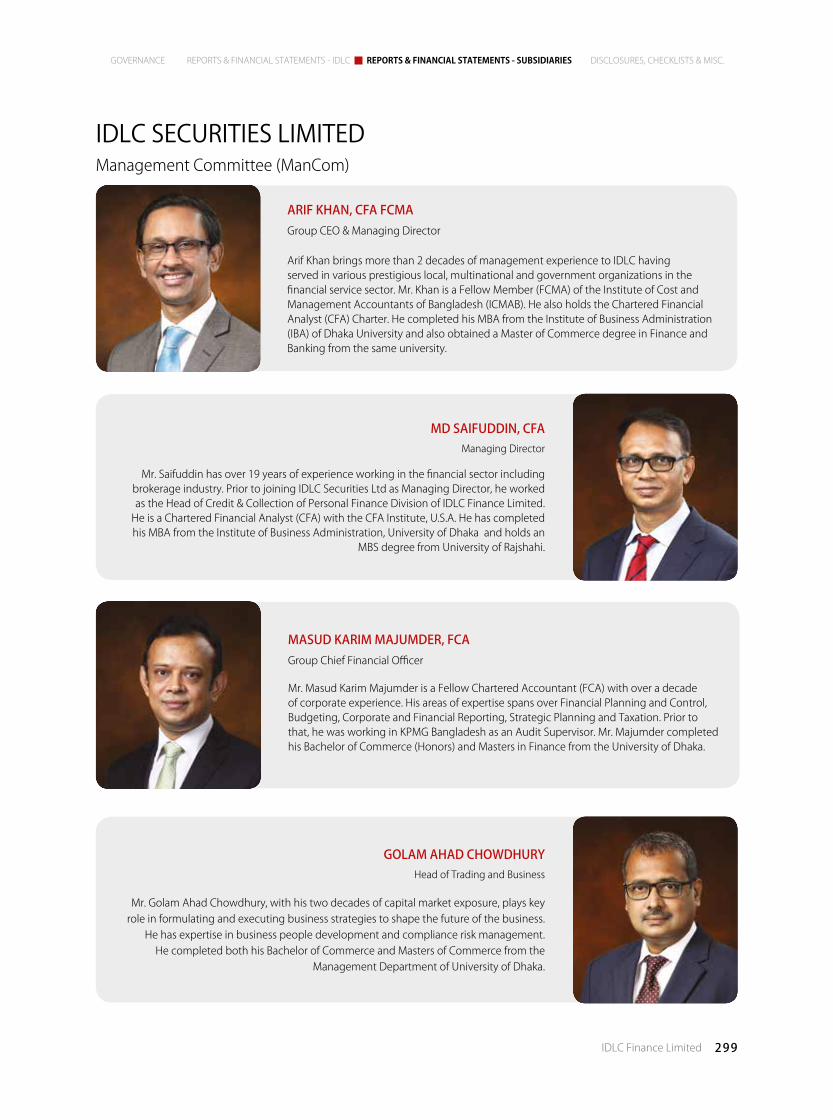

IDLC Securities Limited 133

IDLC Investments Limited 135

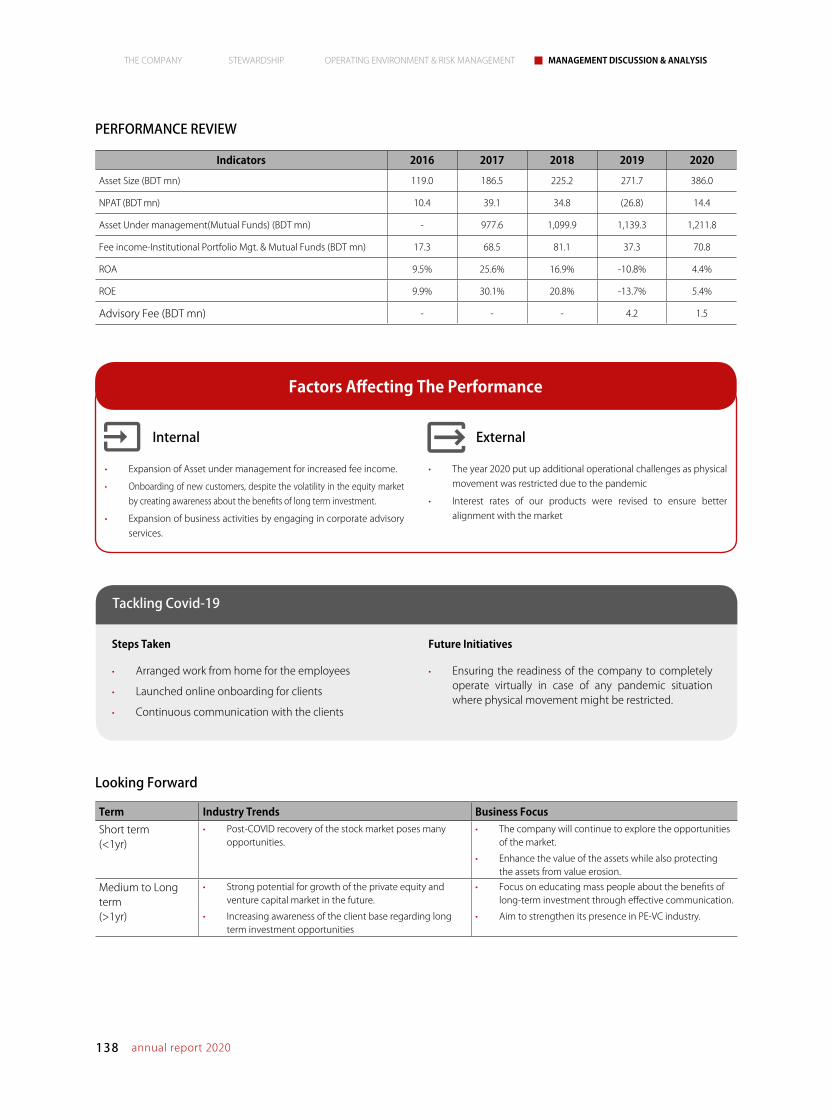

IDLC Asset Management Limited 137

Report of the CEO and Managing Director and the Chief Financial Officer

222

Independent Auditor's Report 223

Consolidated Financial Statements - IDLC Group

Consolidated Balance Sheet 227

Consolidated Profit and Loss Account 229

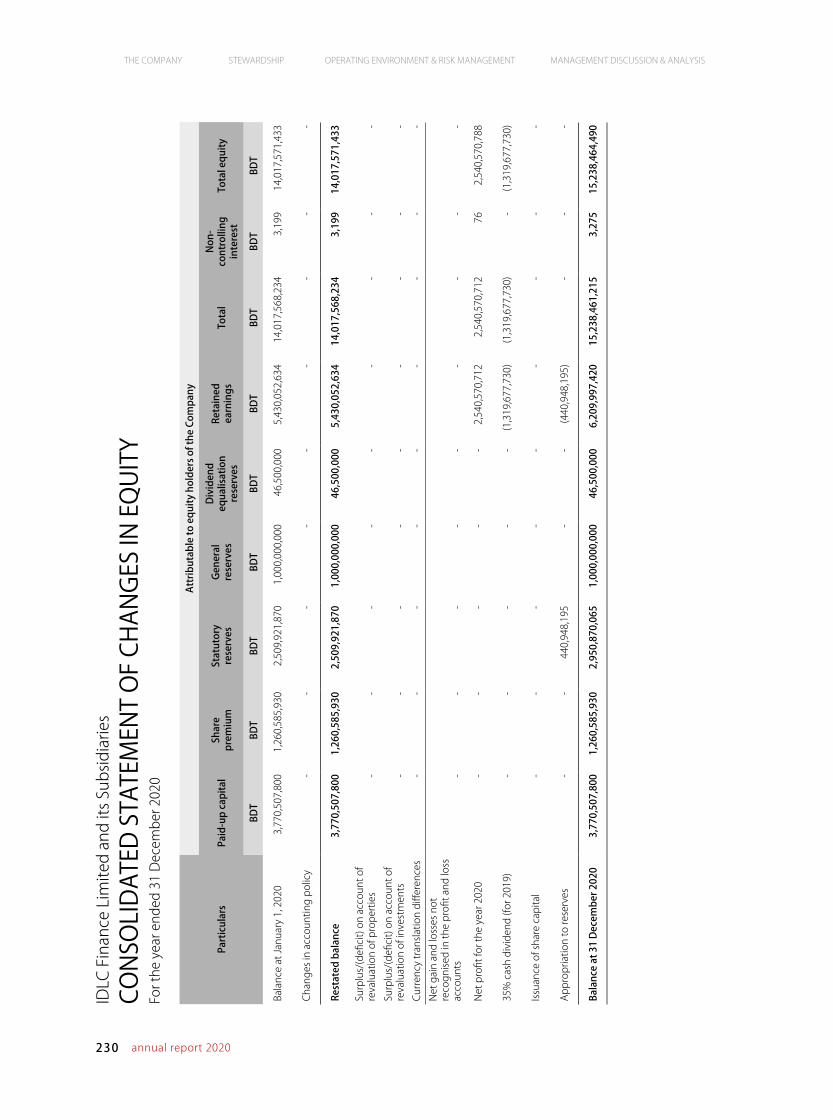

Consolidated Statement of Changes in Equity 230

Consolidated Cash Flow Statement 232

Financial Statements - IDLC Finance Limited

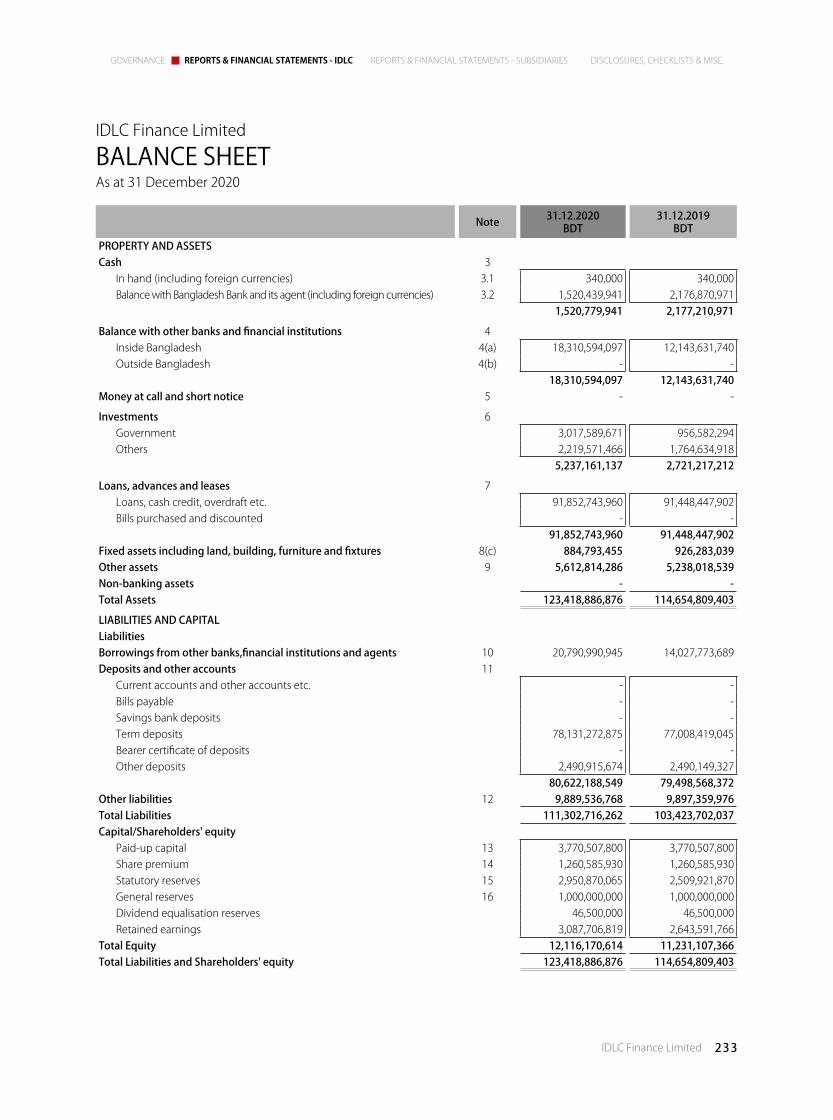

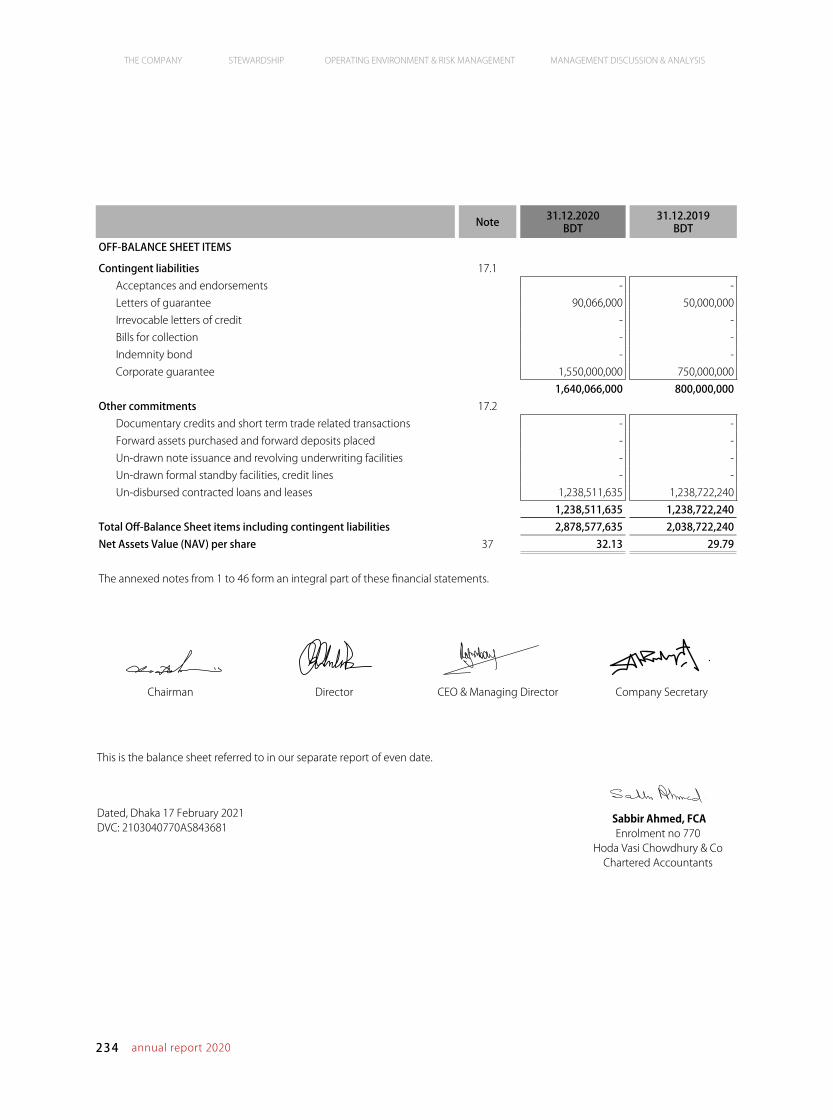

Balance Sheet 233

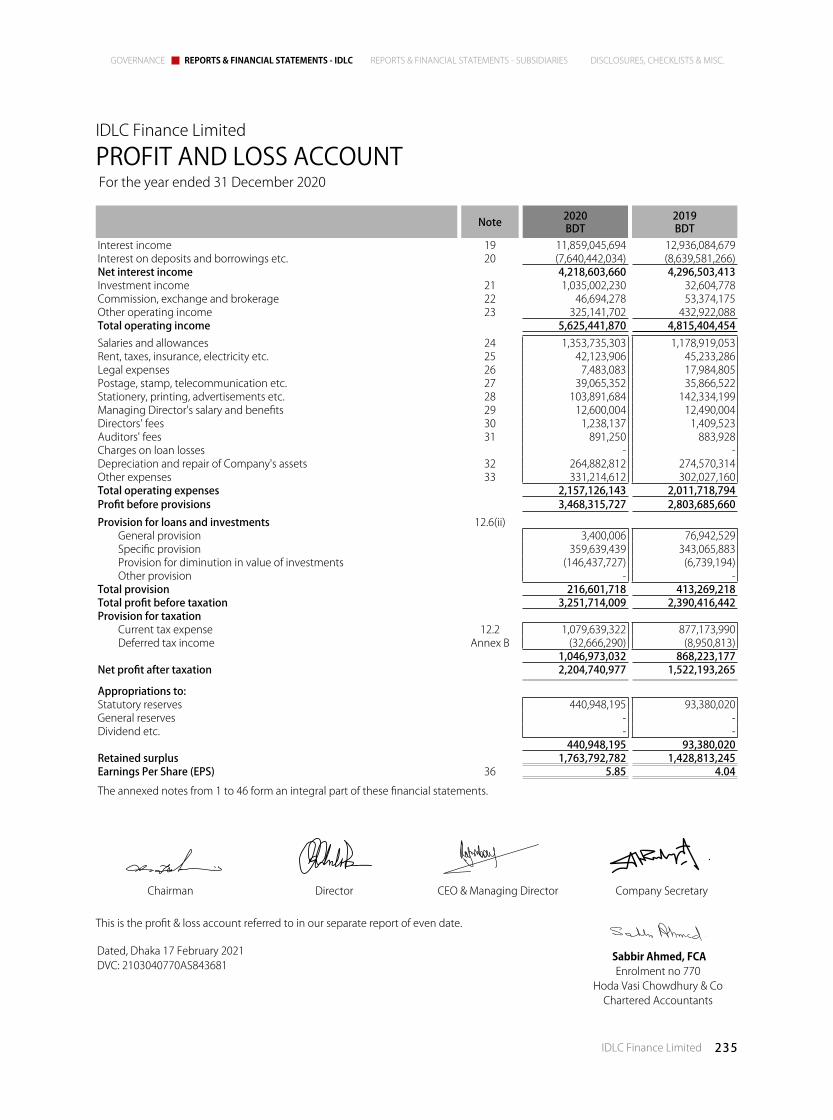

Profit and Loss Account 235

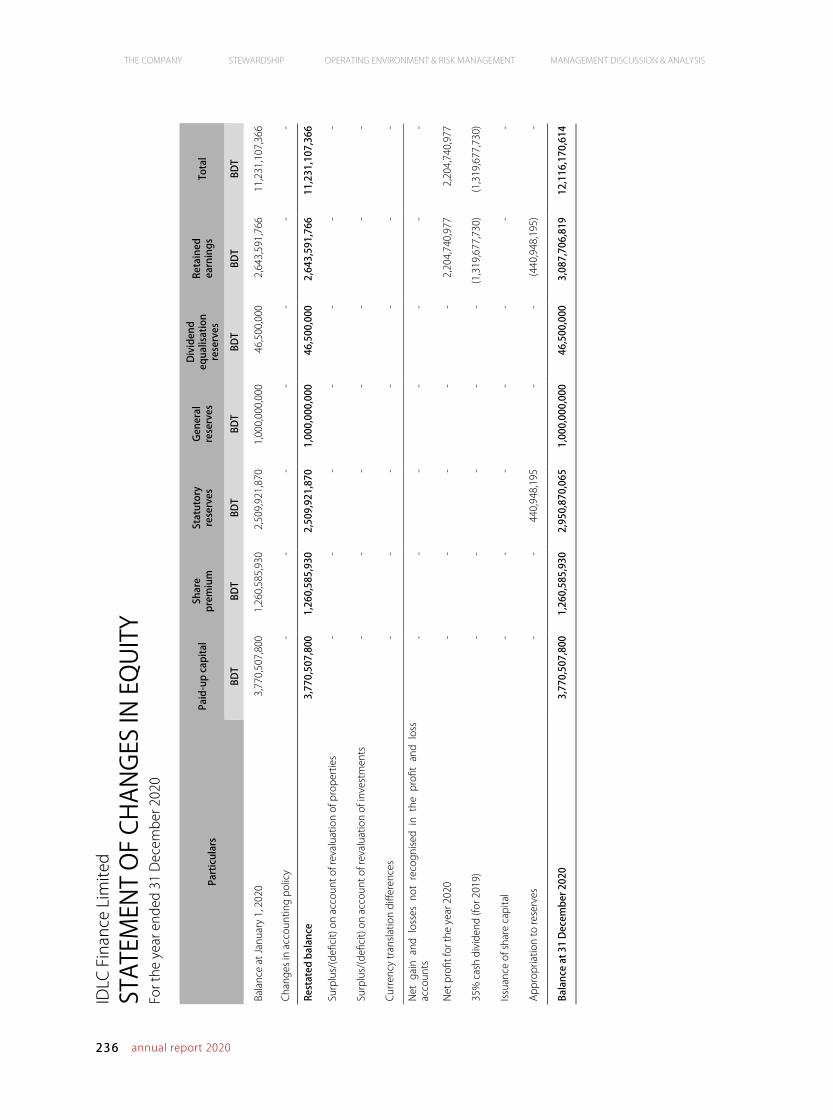

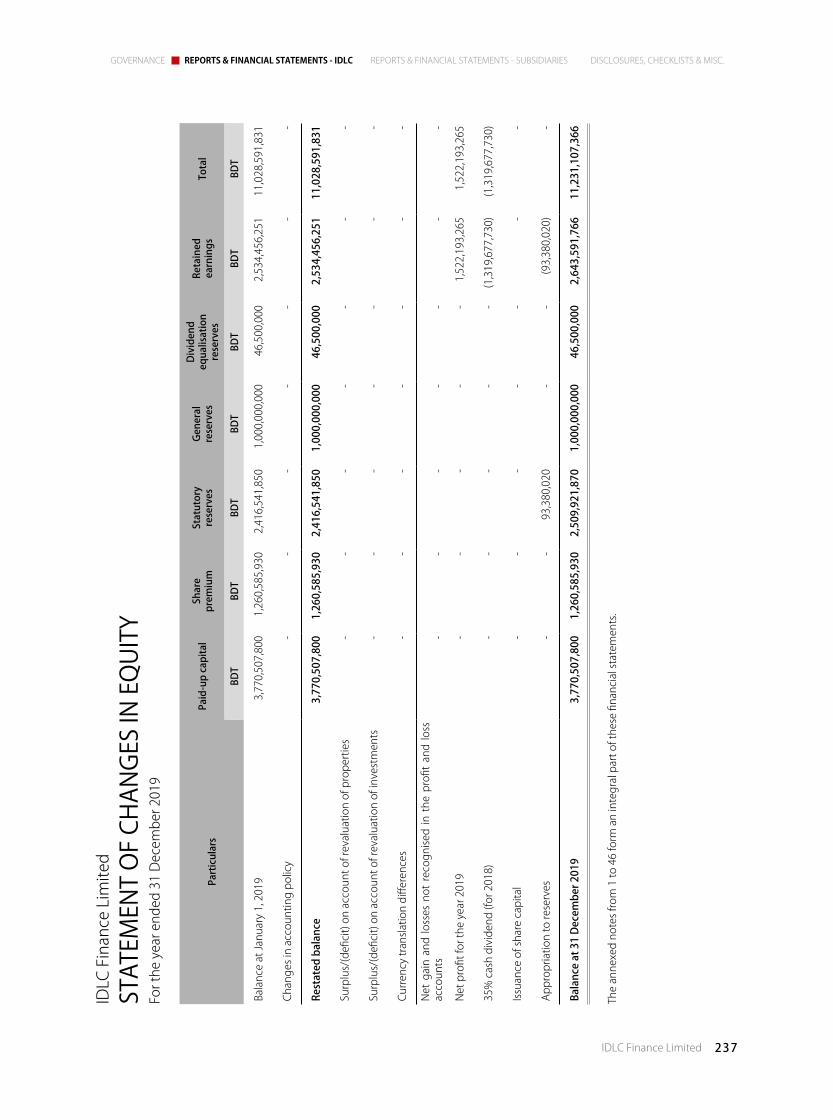

Statement of Changes in Equity 236

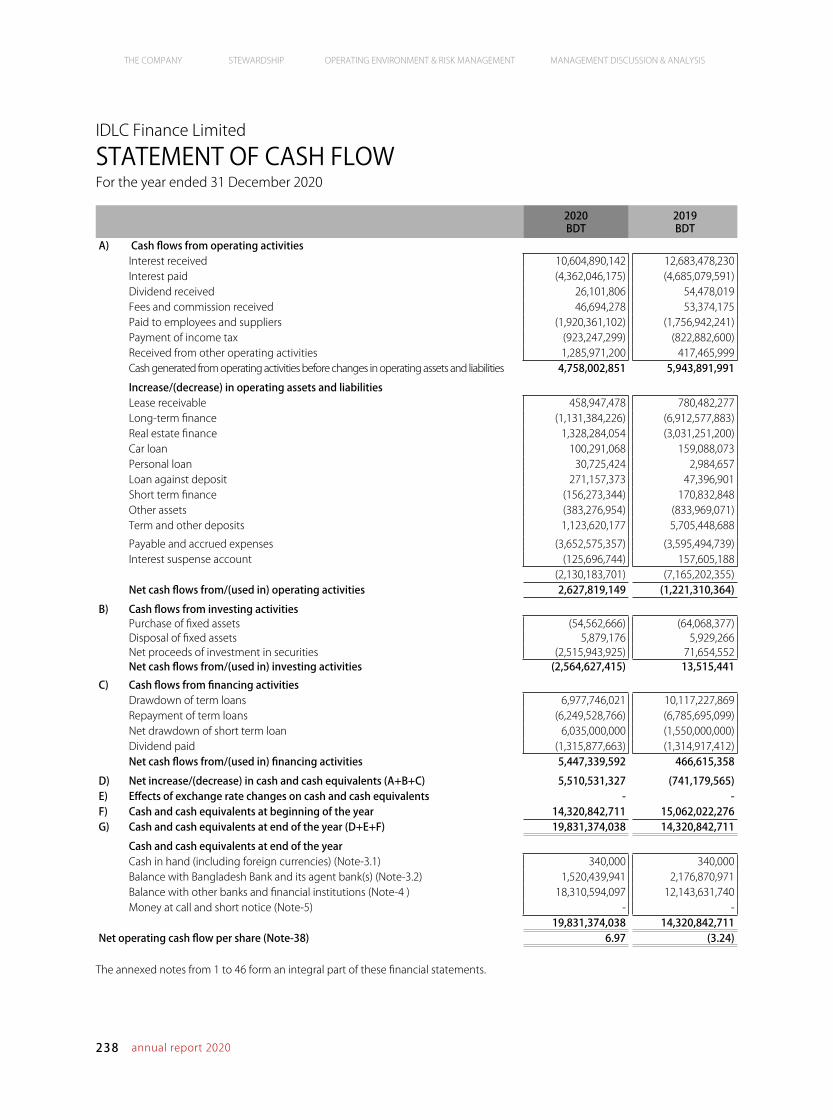

Cash Flow Statement 238

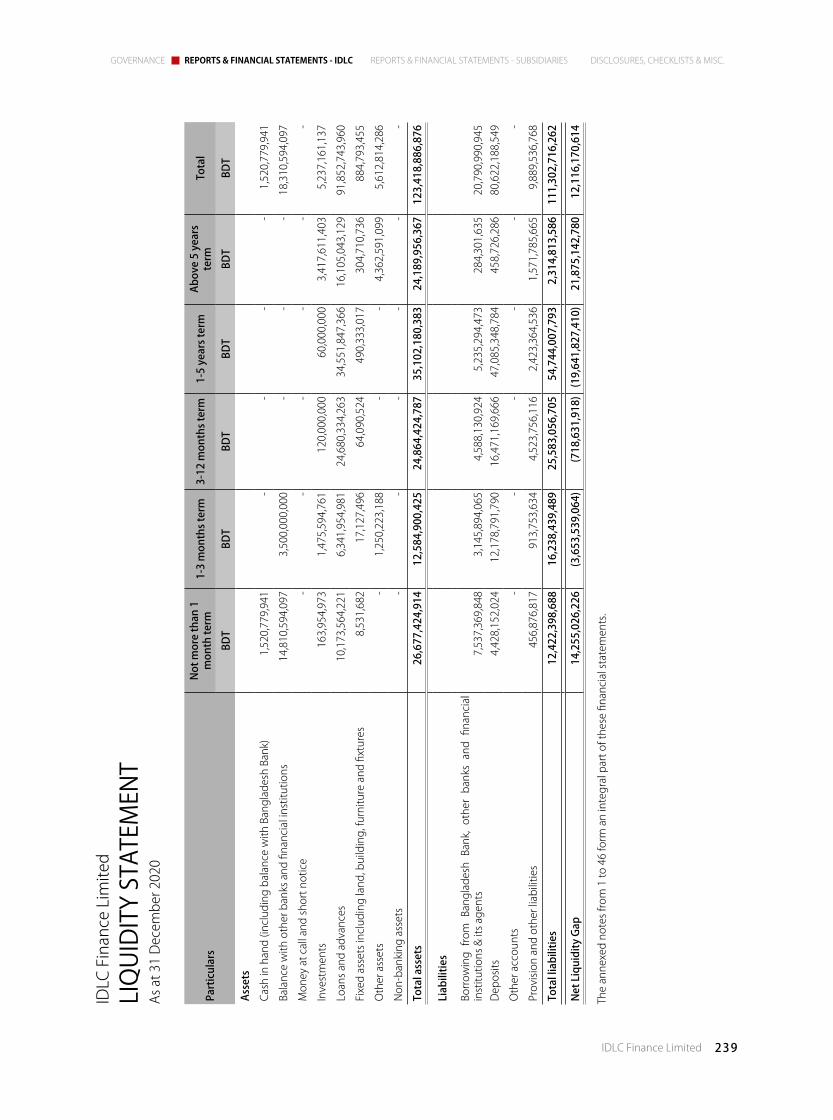

Liquidity Statement 239

Notes to the Consolidated and Separate Financial Statements

240

IDLC Securities Limited

Management Committee 299

Directors' Report to the Shareholders 301

Independent Auditors' Report 306

Statement of Financial Position 308

Statement of Profit and Loss and Other Comprehensive Income

309

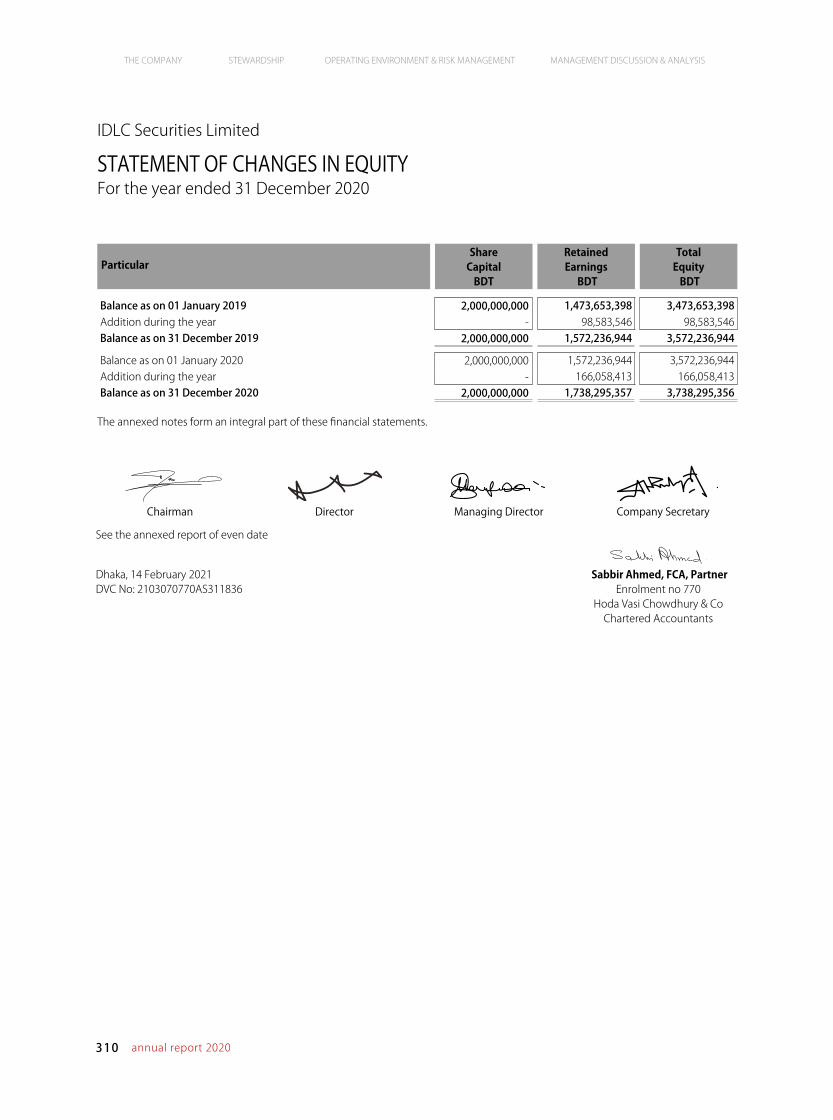

Statement of Changes in Equity 310

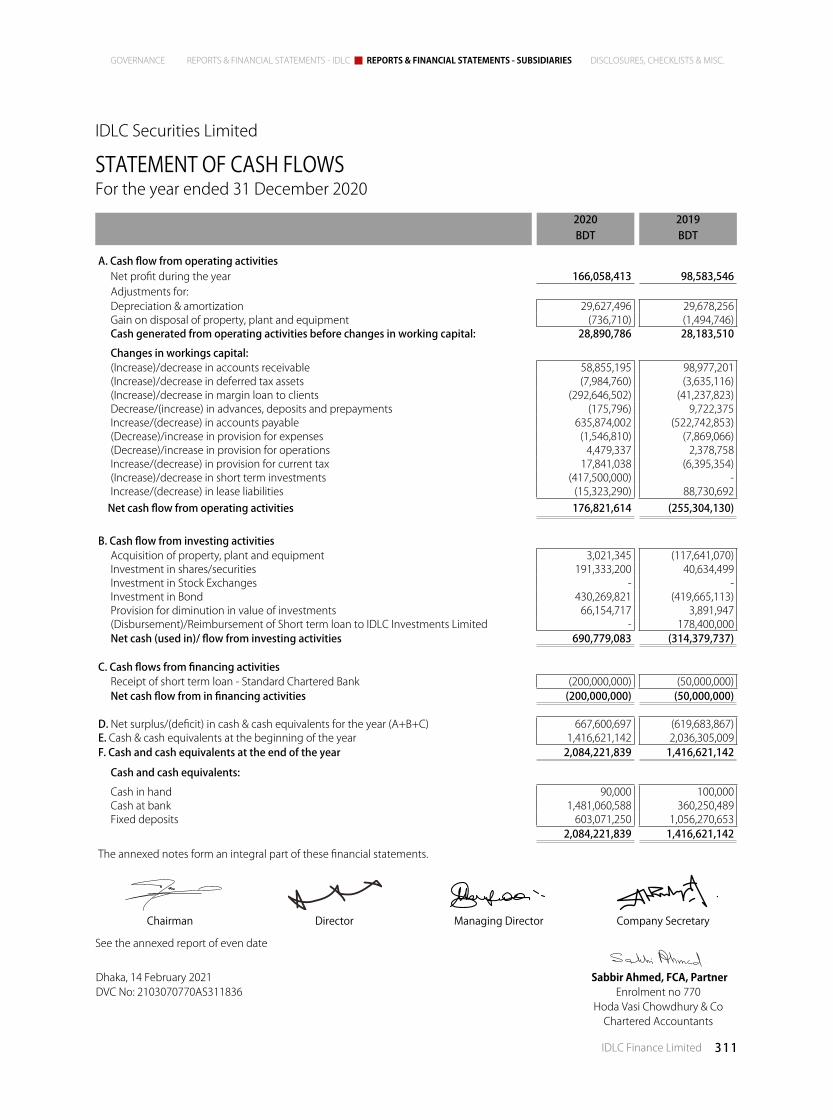

Statement of Cash Flows 311

Notes to the Financial Statements 312

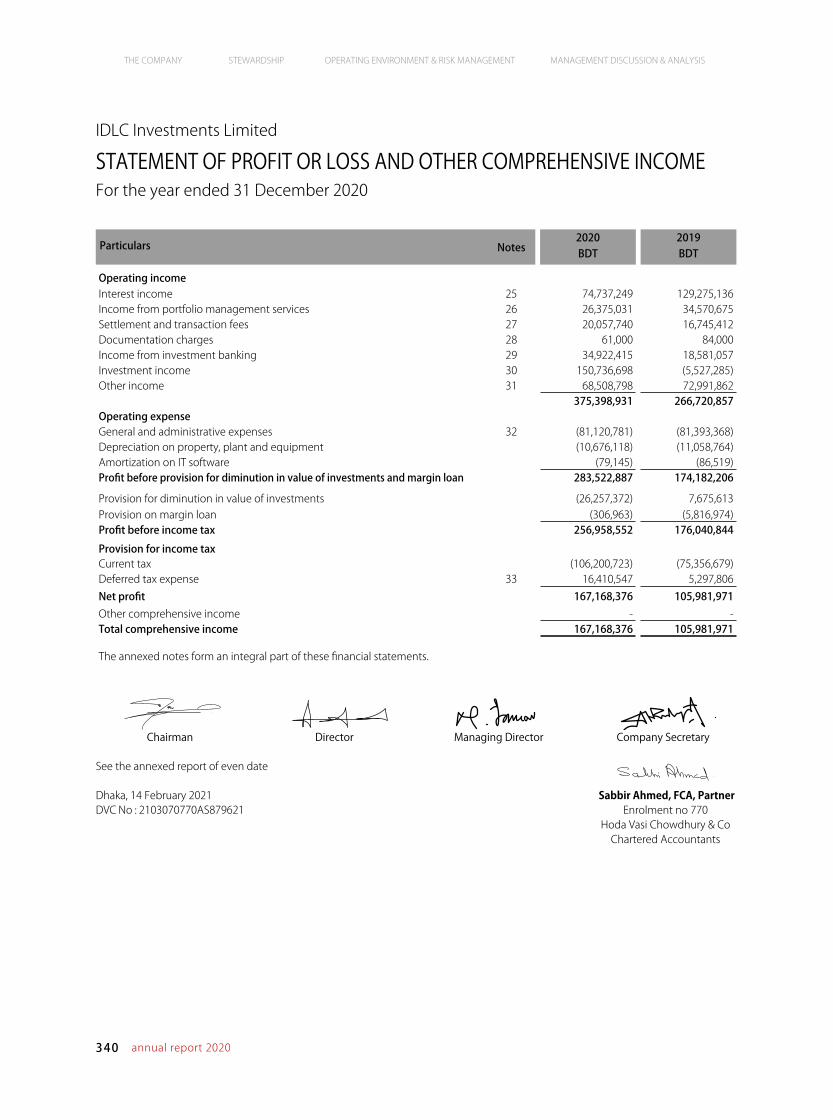

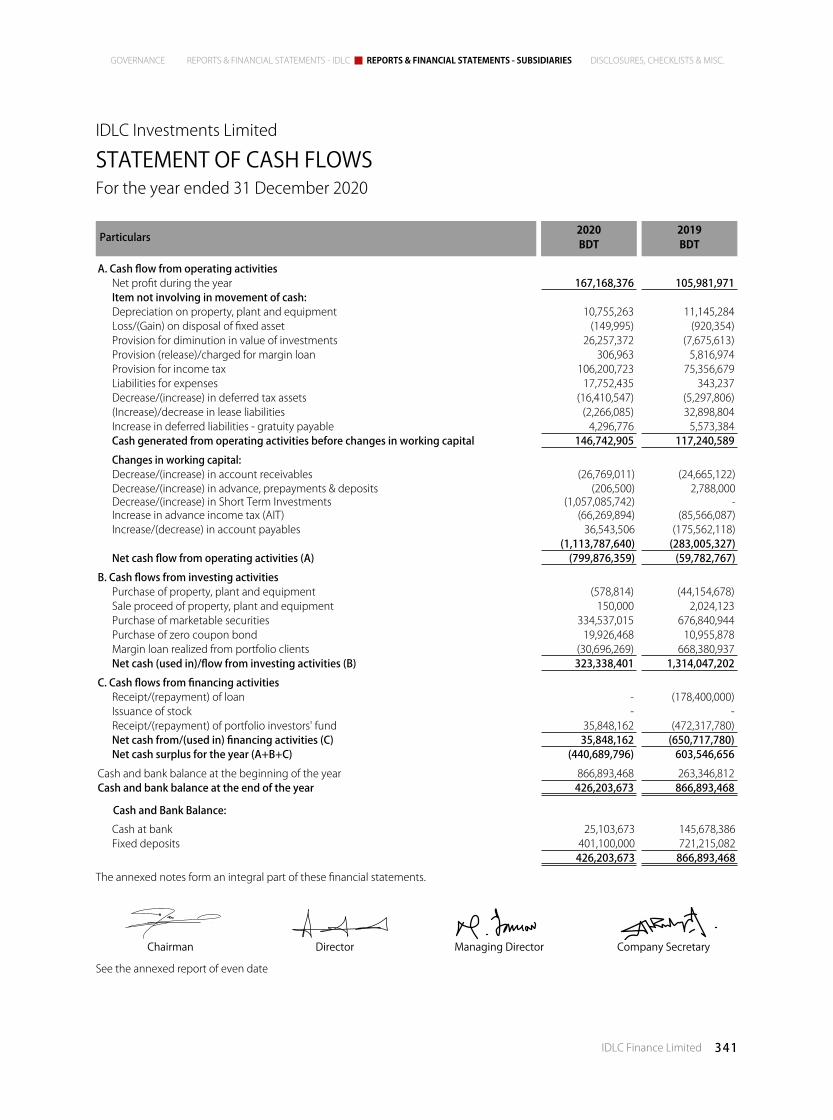

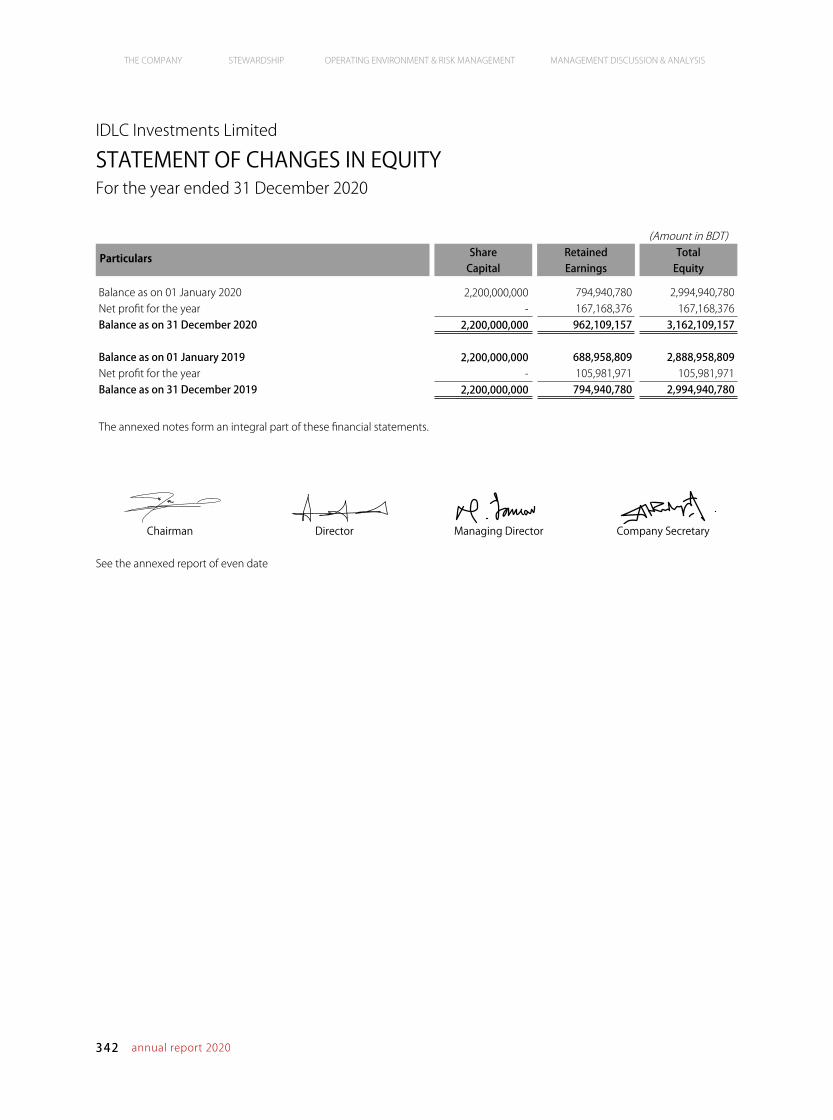

IDLC Investments Limited

Management Committee 331

Directors' Report to the Shareholders 333

Independent Auditors' Report 337

Statement of Financial Position 339

Statement of Profit and Loss and Other Comprehensive Income

340

Statement of Cash Flows 341

Statement of Changes in Equity 342

Notes to the Financial Statements 343

IDLC Asset Management Limited

Management Committee 359

Directors' Report to the Shareholders 361

Independent Auditors' Report 364

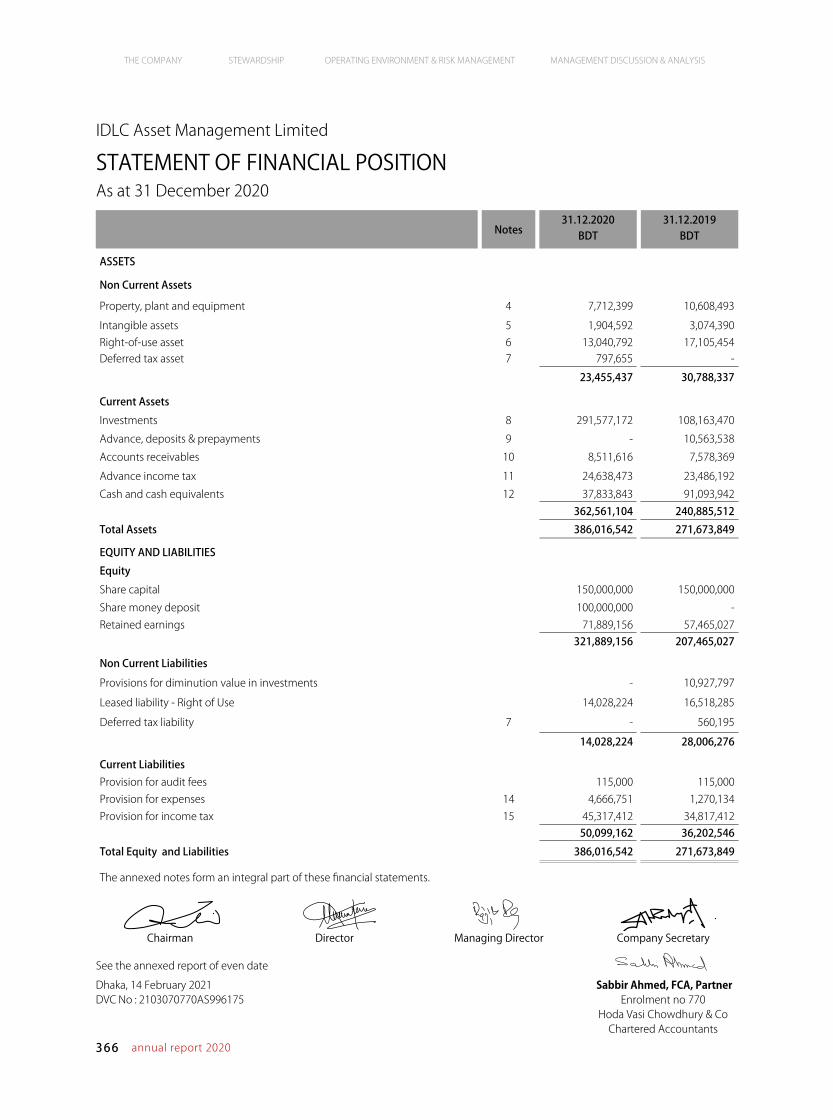

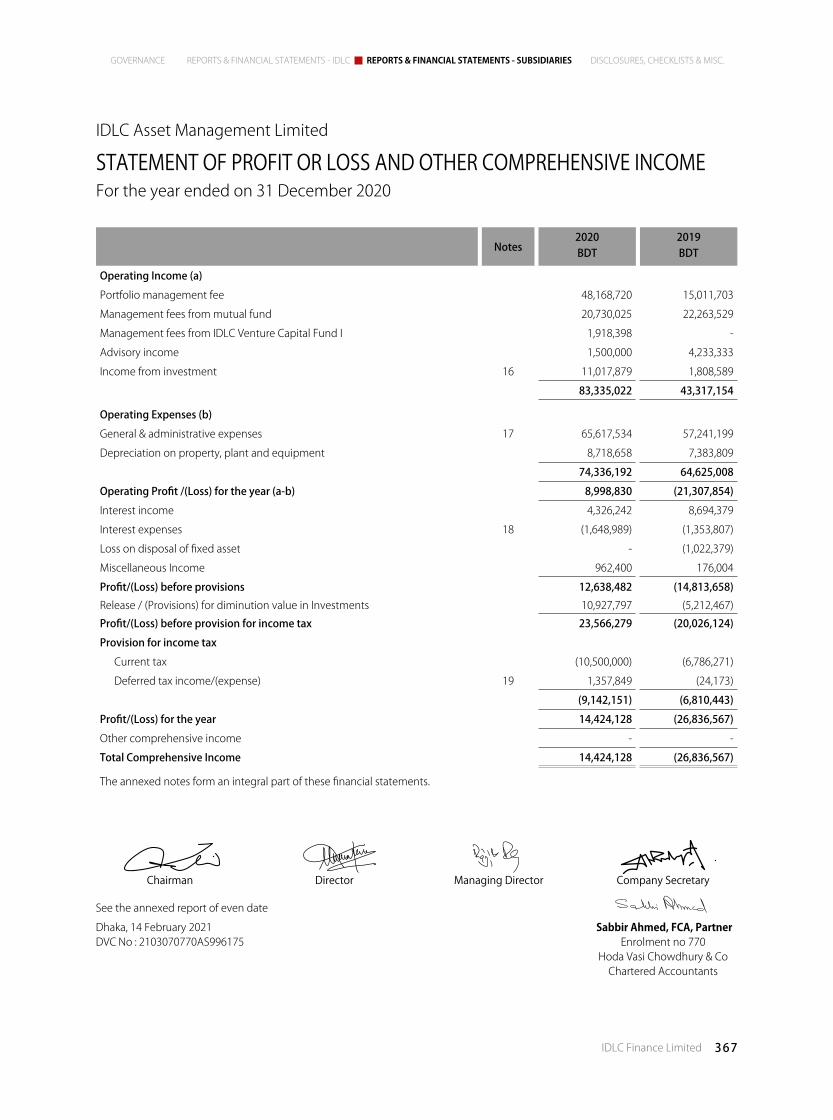

Statement of Financial Position 366

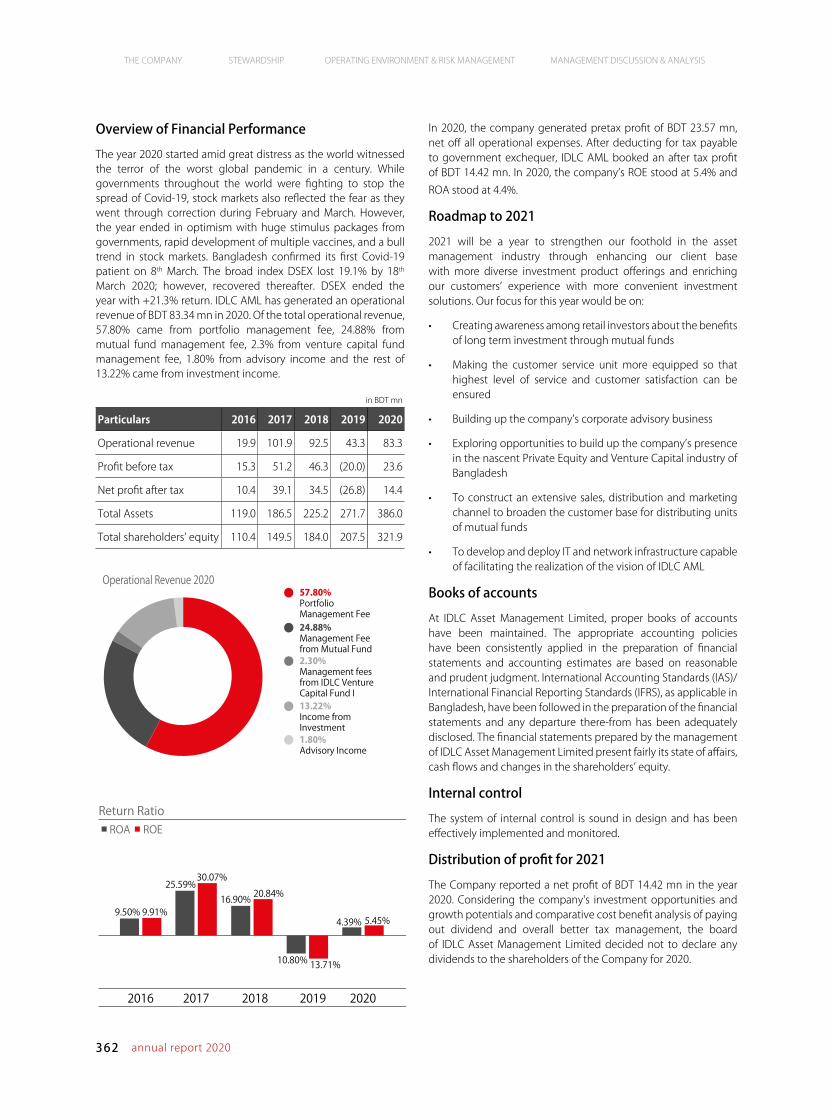

Statement of Profit and Loss and Other Comprehensive Income 367

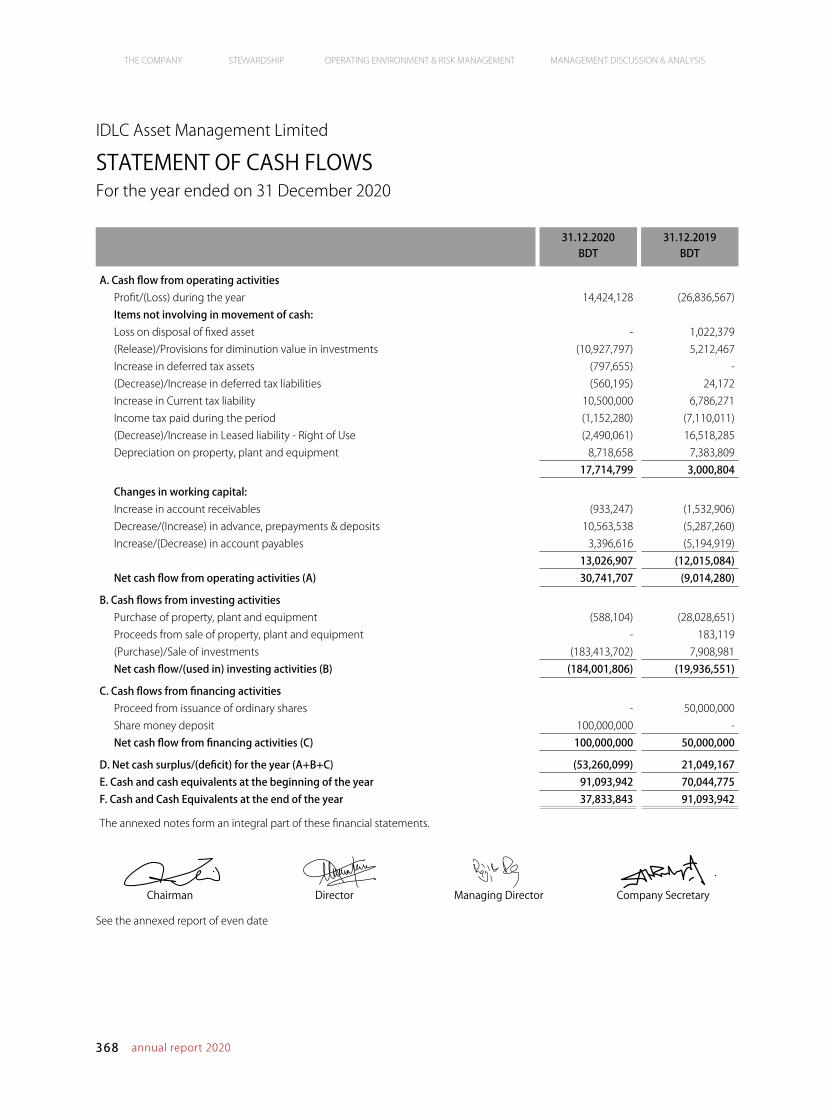

Statement of Cash Flows 368

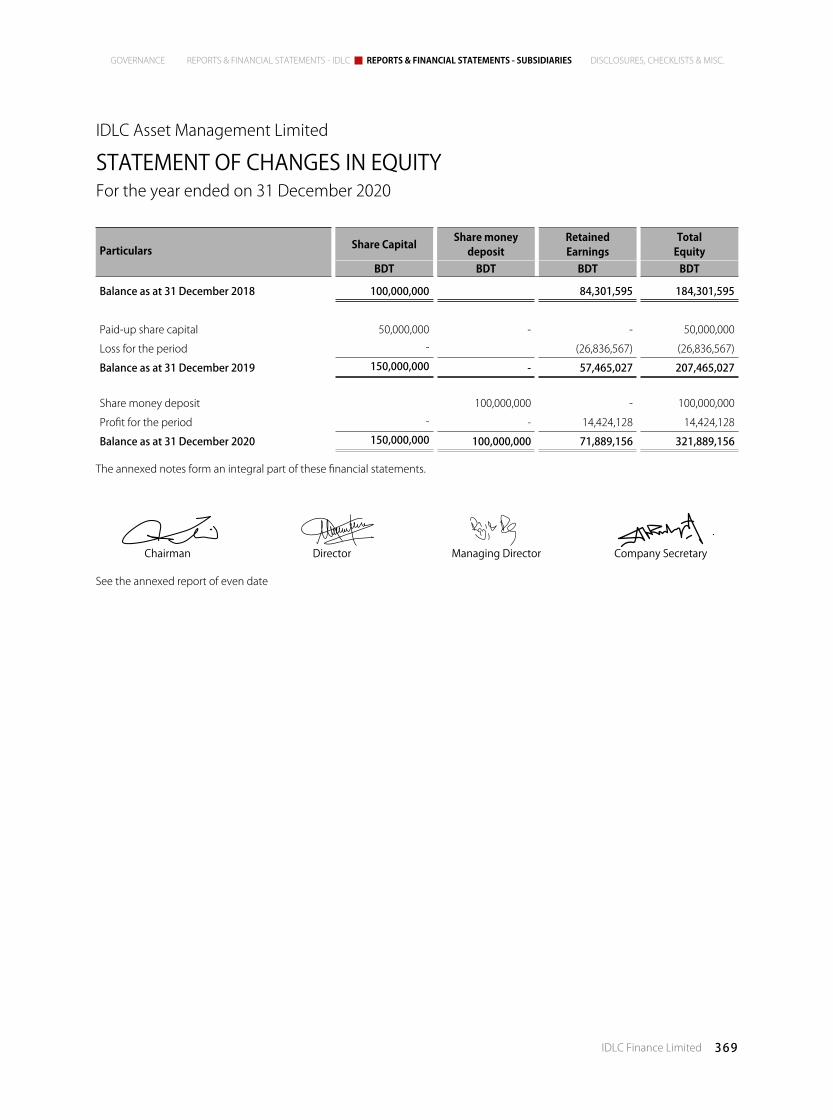

Statement of Changes in Equity 369

Notes to the Financial Statements 370

GOVERNANCE REPORTS & FINANCIAL STATEMENTS SUBSIDIARY COMPANIES

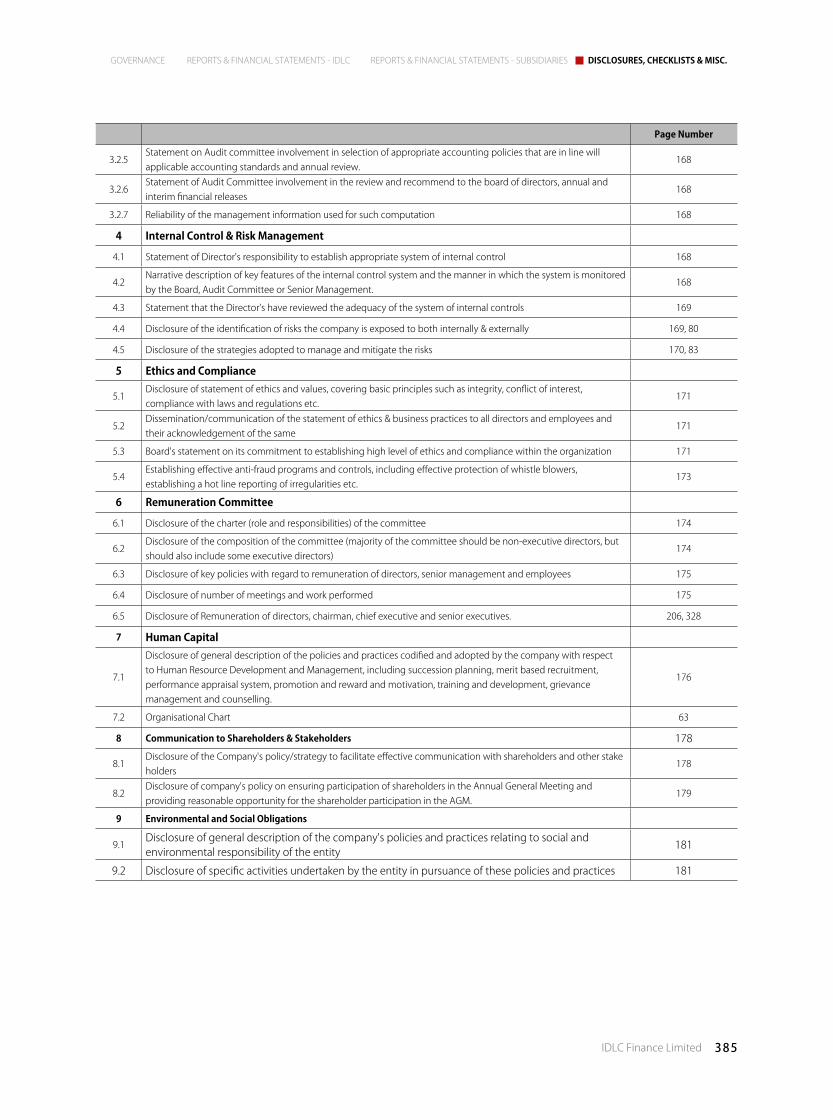

DISCLOSURES, CHECKLISTS & MISCELLANEOUS

REPORTS & FINANCIAL STATEMENTSIDLC GROUP AND IDLC FINANCE LIMITED

Letter from Board of Directors 140

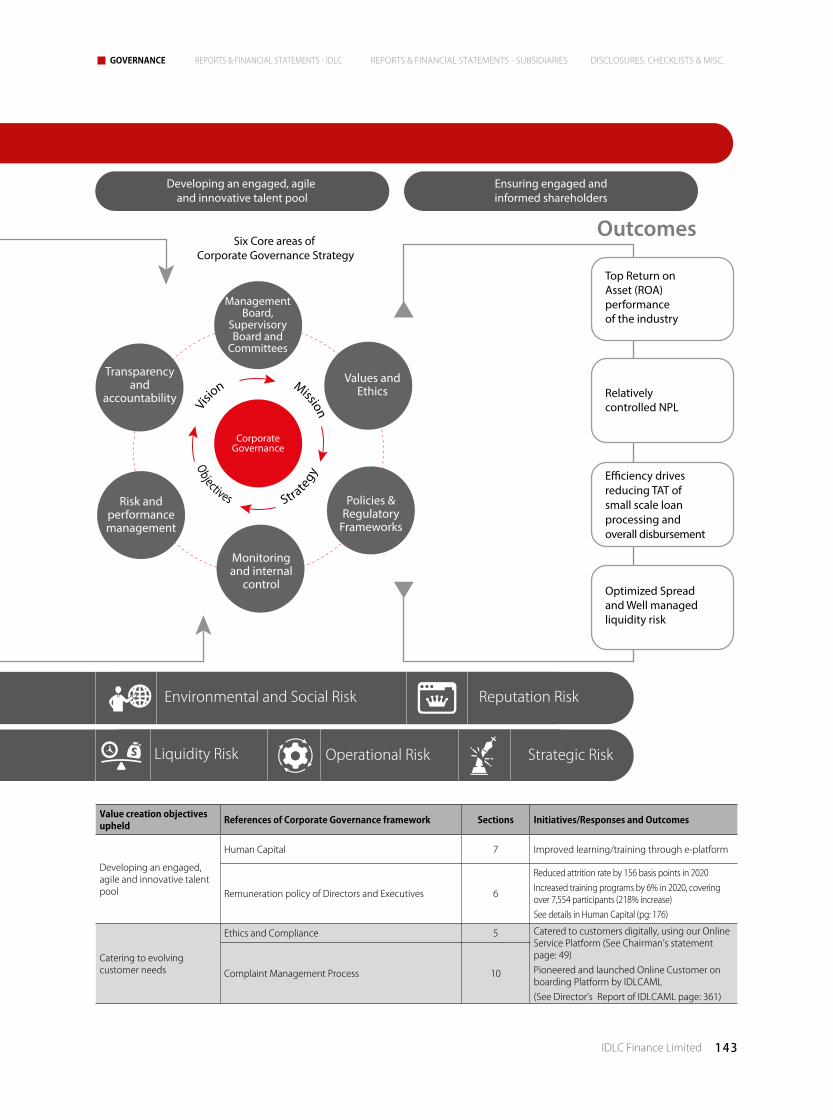

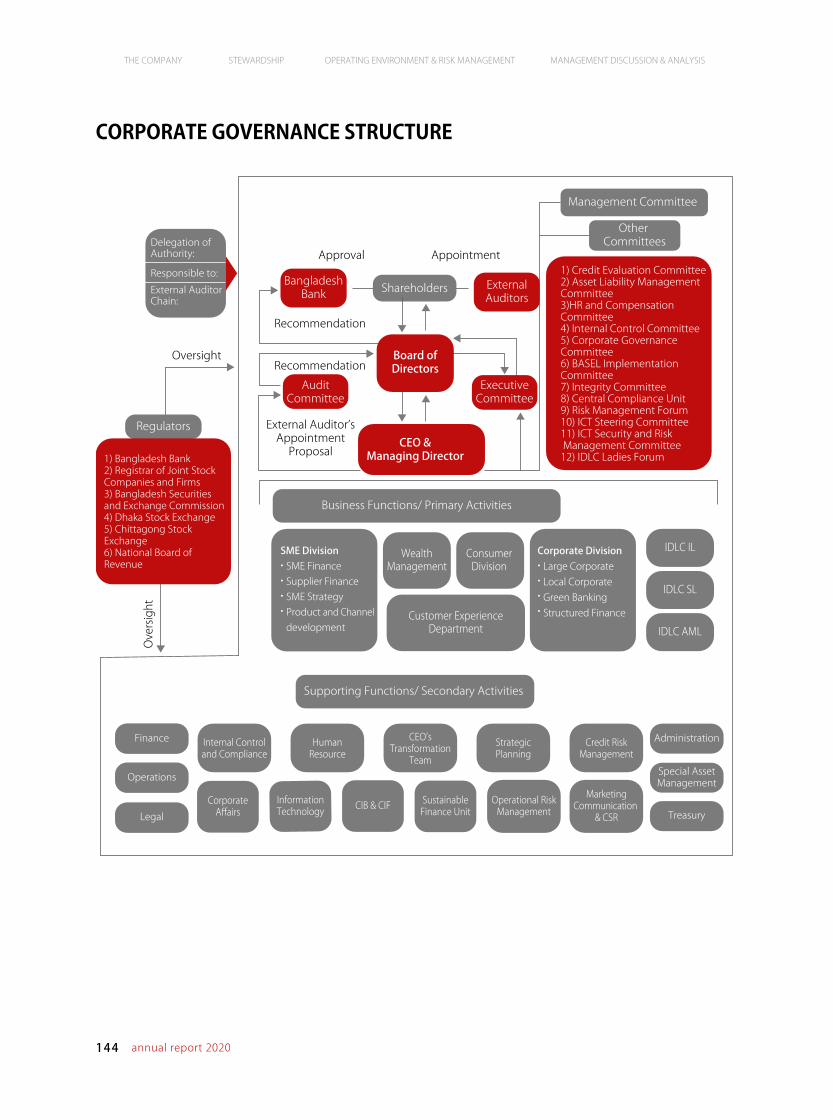

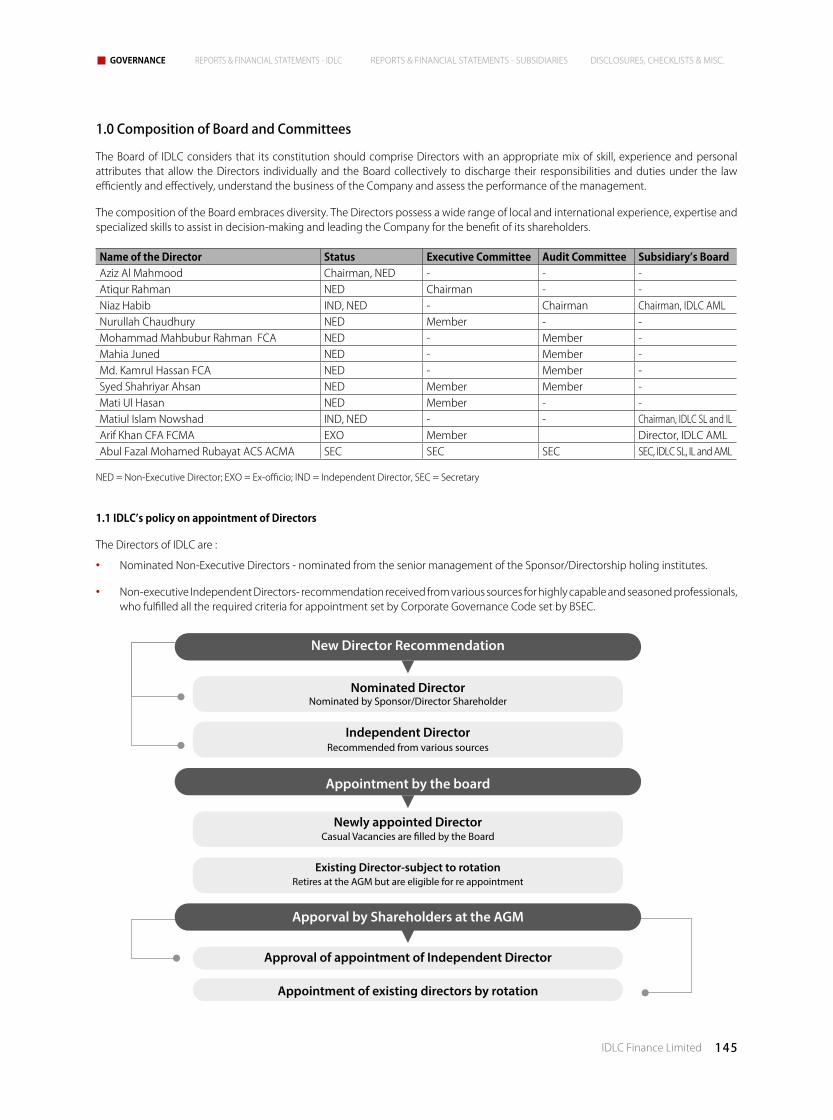

Statement of Corporate Governance 141

Statutory Reporting

Key Pointers for the Stakeholders 182

Disclosures Under Pillar-III Market Discipline 184

Report on Security Custodial Service of IDLC Finance Limited

191

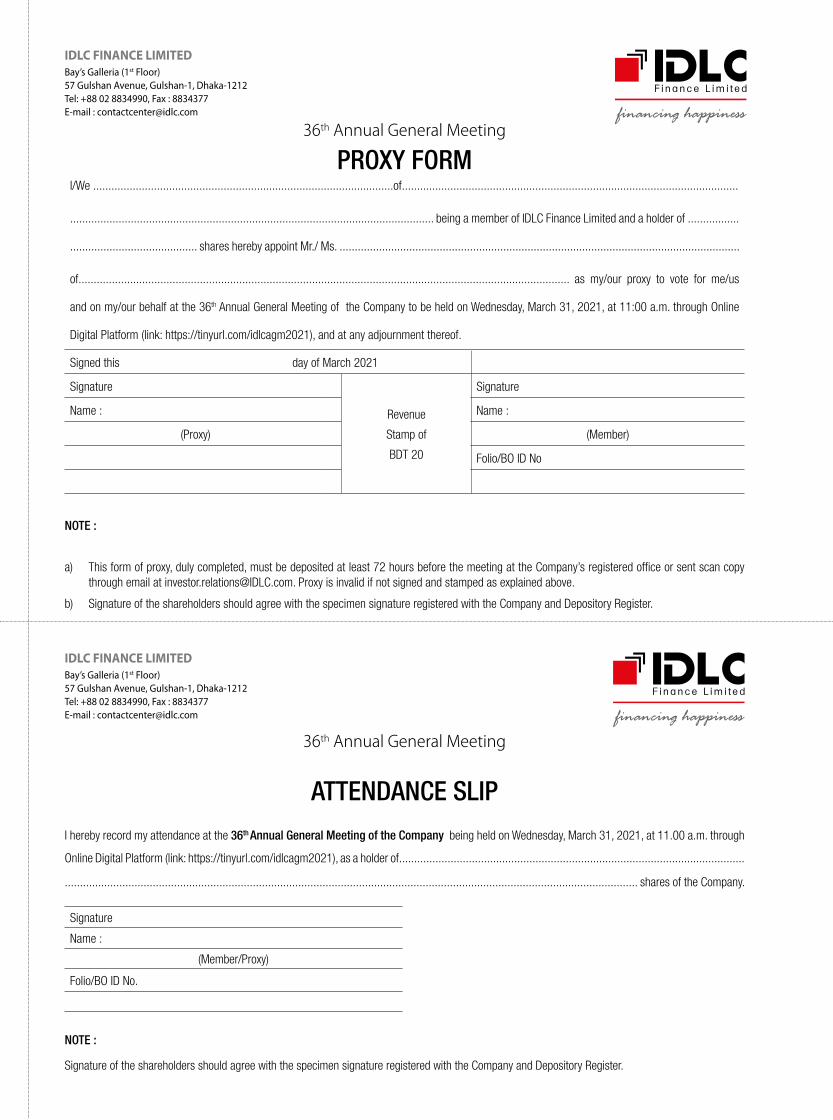

Notice of the 36th Annual General Meeting 192

Report of the Audit Committee 193

Assessment Report on the Going Concern of IDLC Finance Limited

195

Statement of Directors' Responsibilities for Internal Control, Financial Reporting and Corporate Governance

197

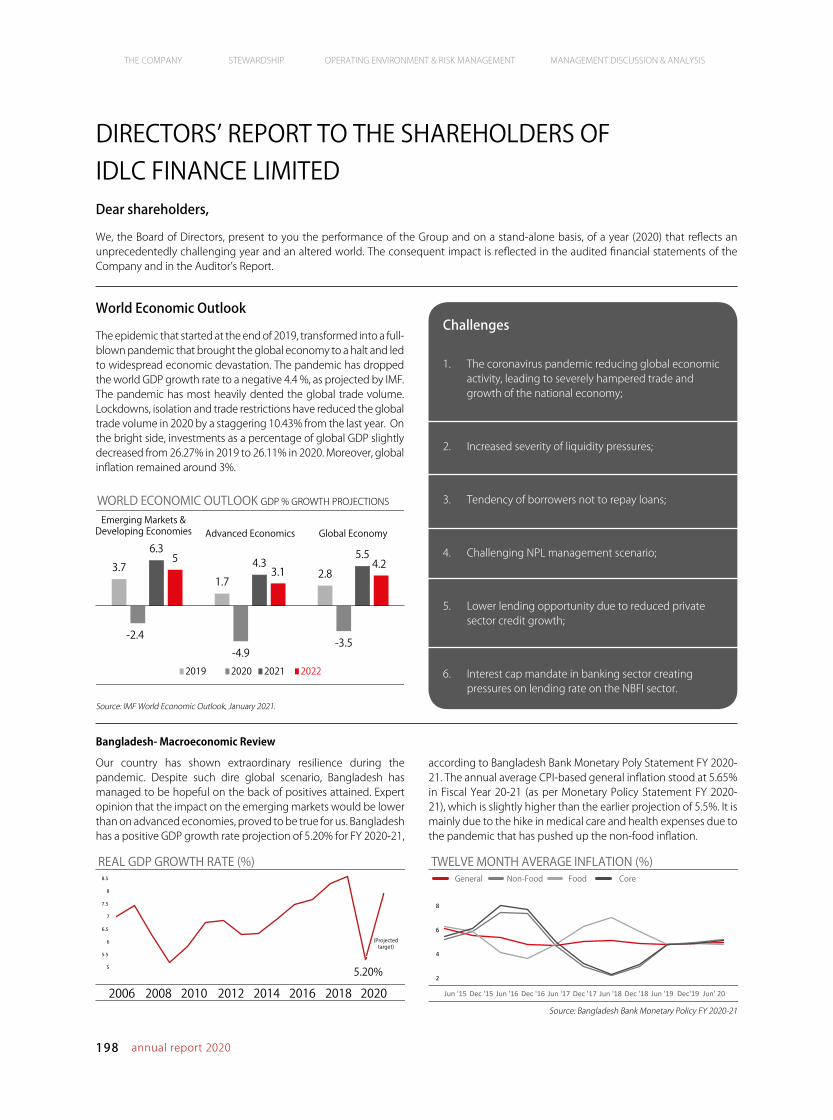

Directors’ Report to the Shareholders 198

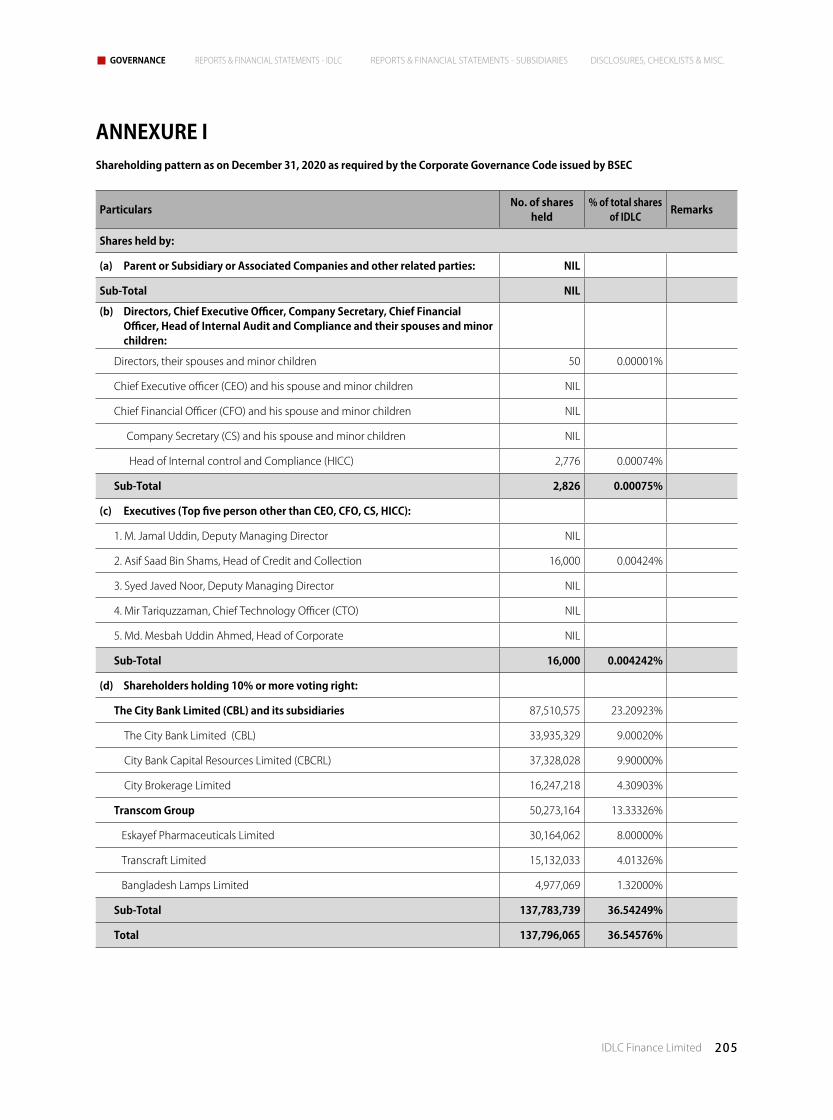

Annexure I: Shareholding pattern as required by the Corporate Governance Code issued by BSEC

205

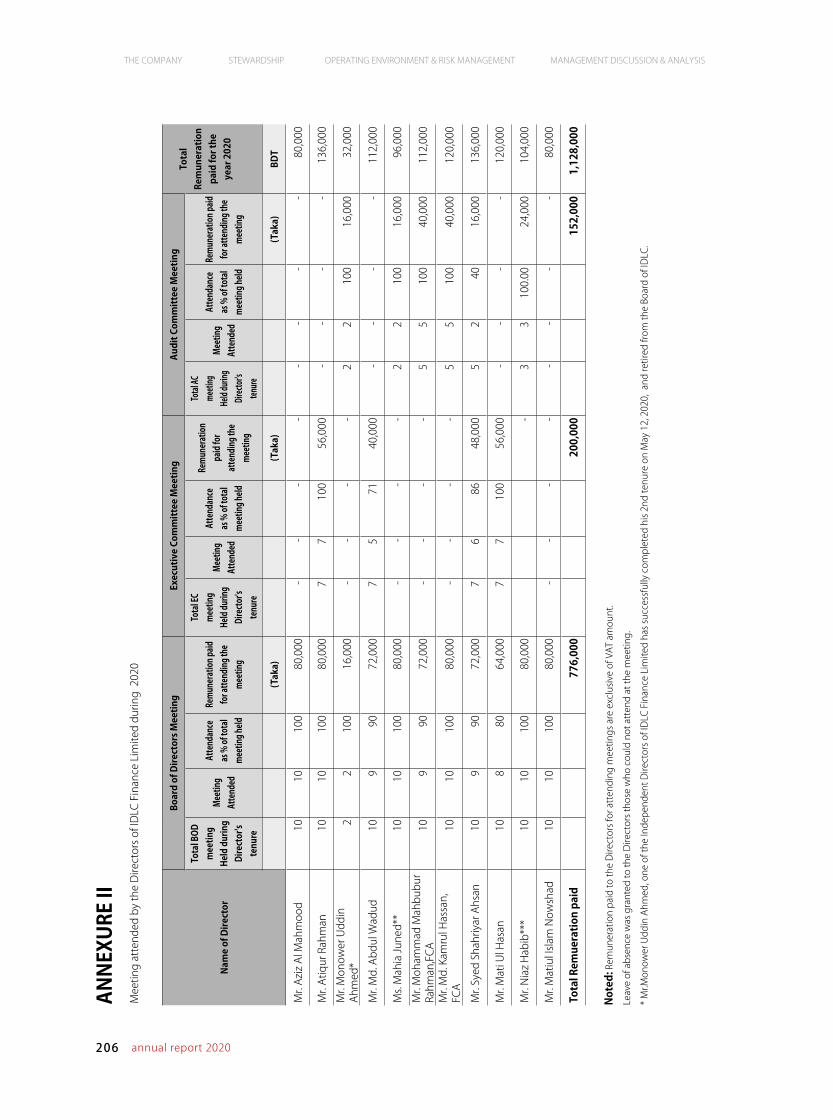

Annexure II: Meeting attended by the Directors 206

Annexure III: Certification on the Compliance with the Corporate Governance Guidelines

207

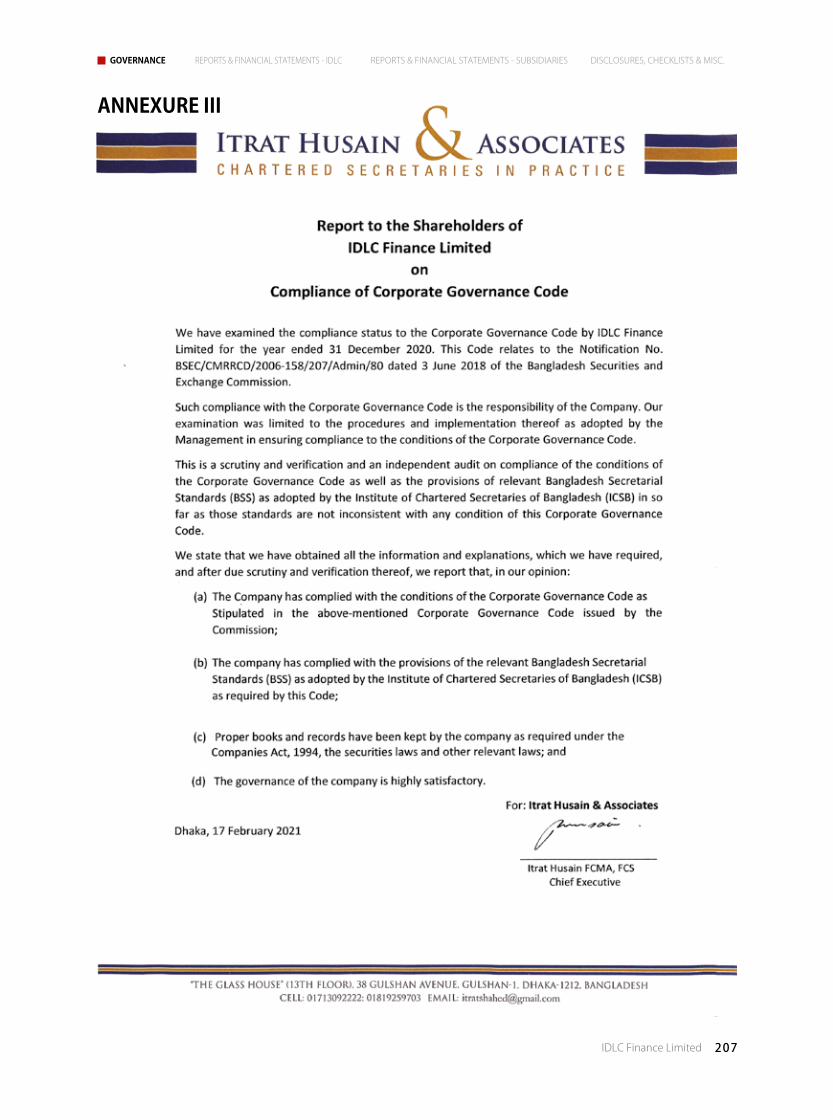

Status of Compliance with the Corporate Governance Guidelines

208

Annexure IV: Statement of Compliance with the the Good Governance Guidelines Issued by the Bangladesh Bank

219

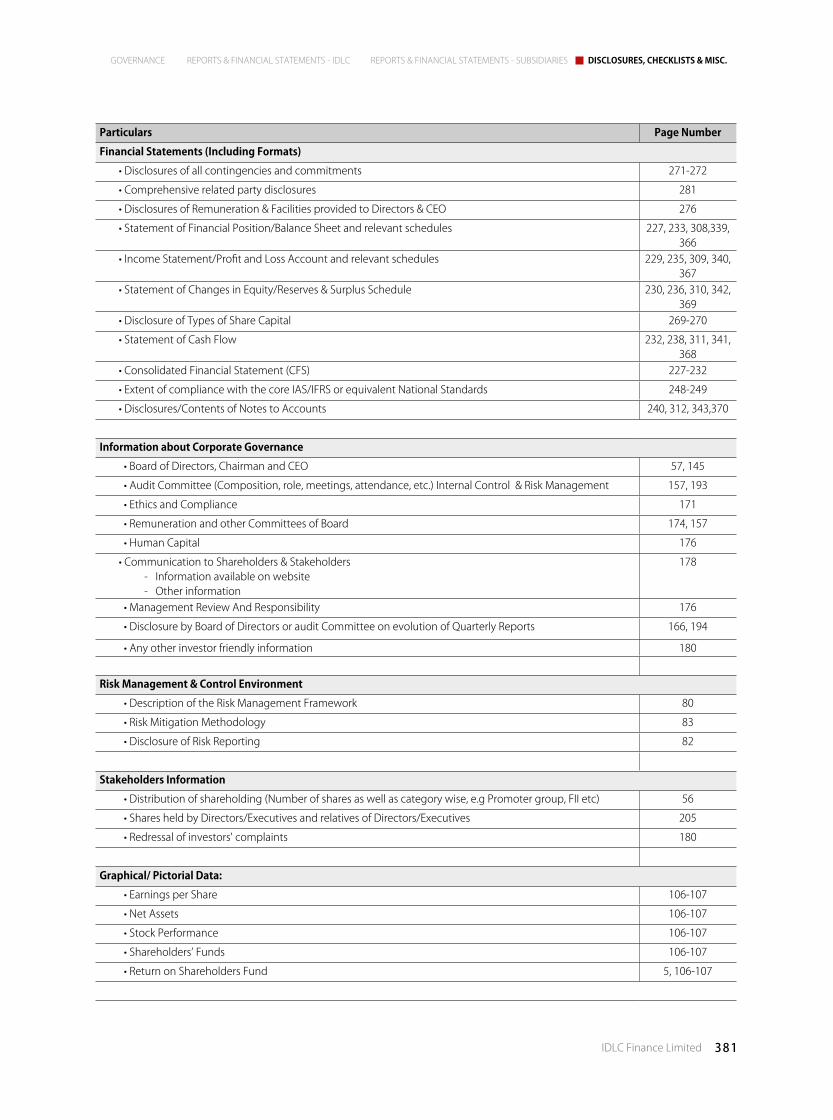

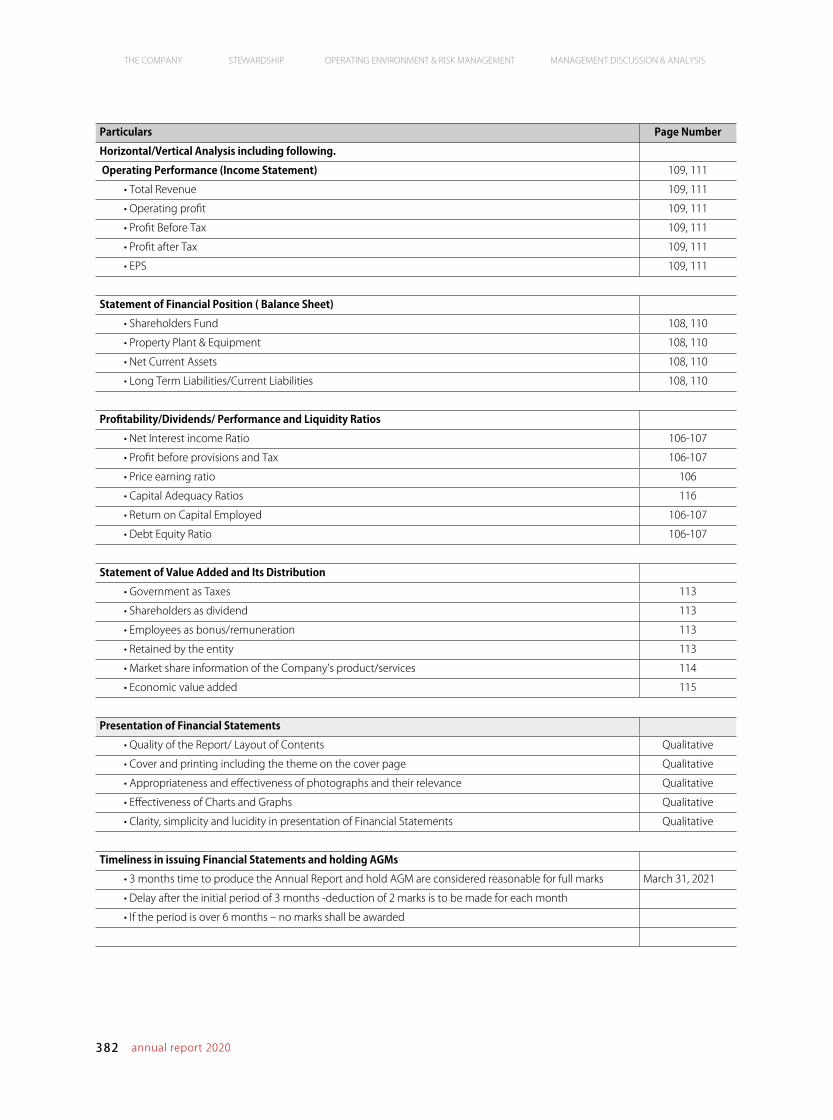

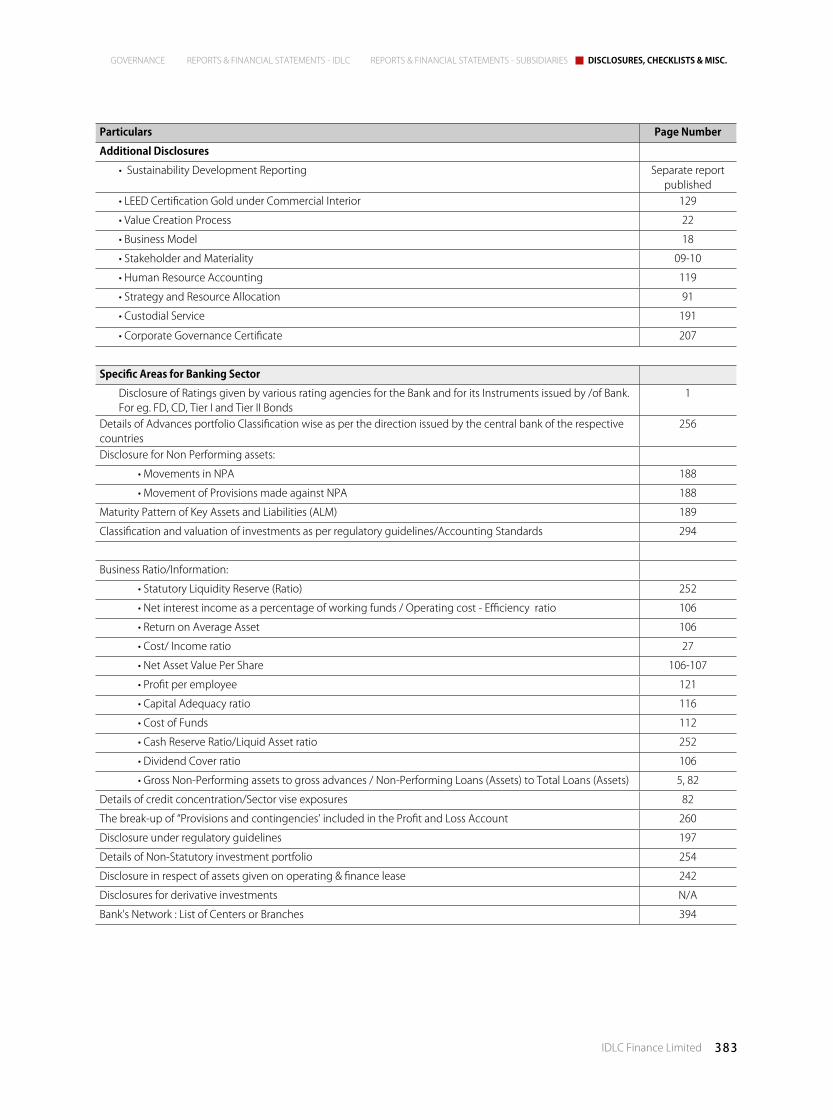

Annual Report Review Checklist 380

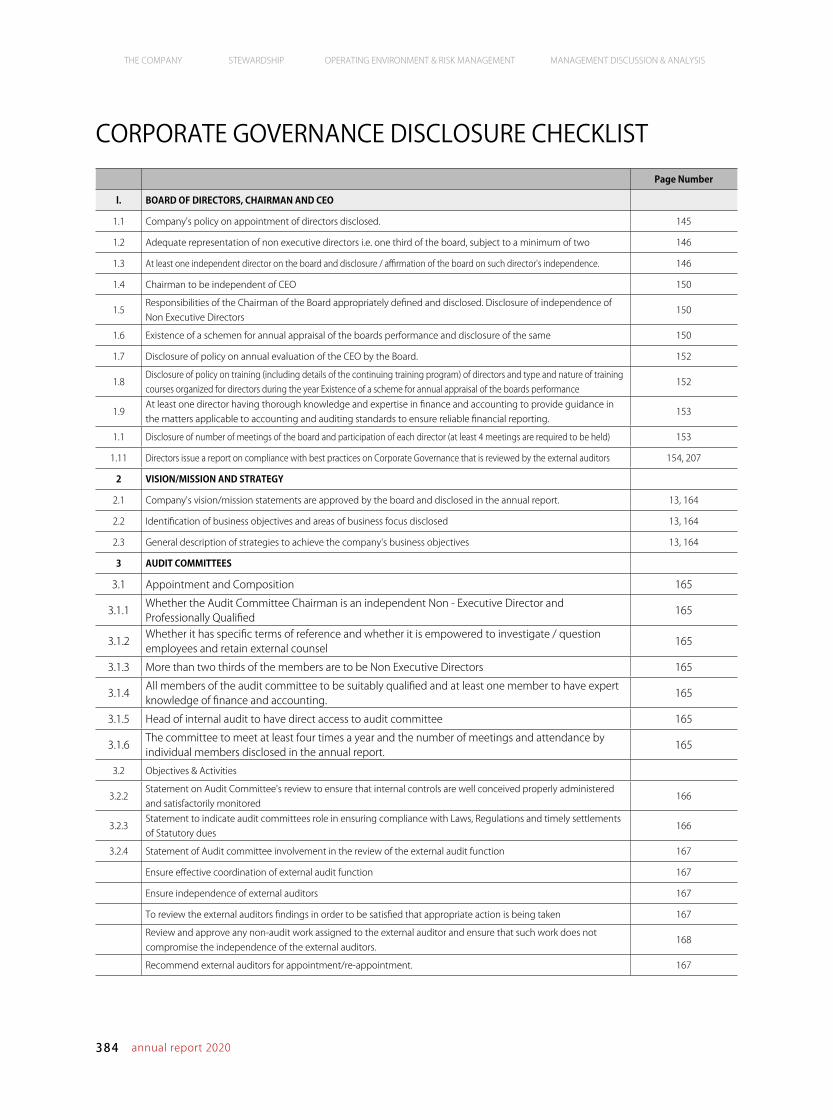

Corporate Governance Checklist 384

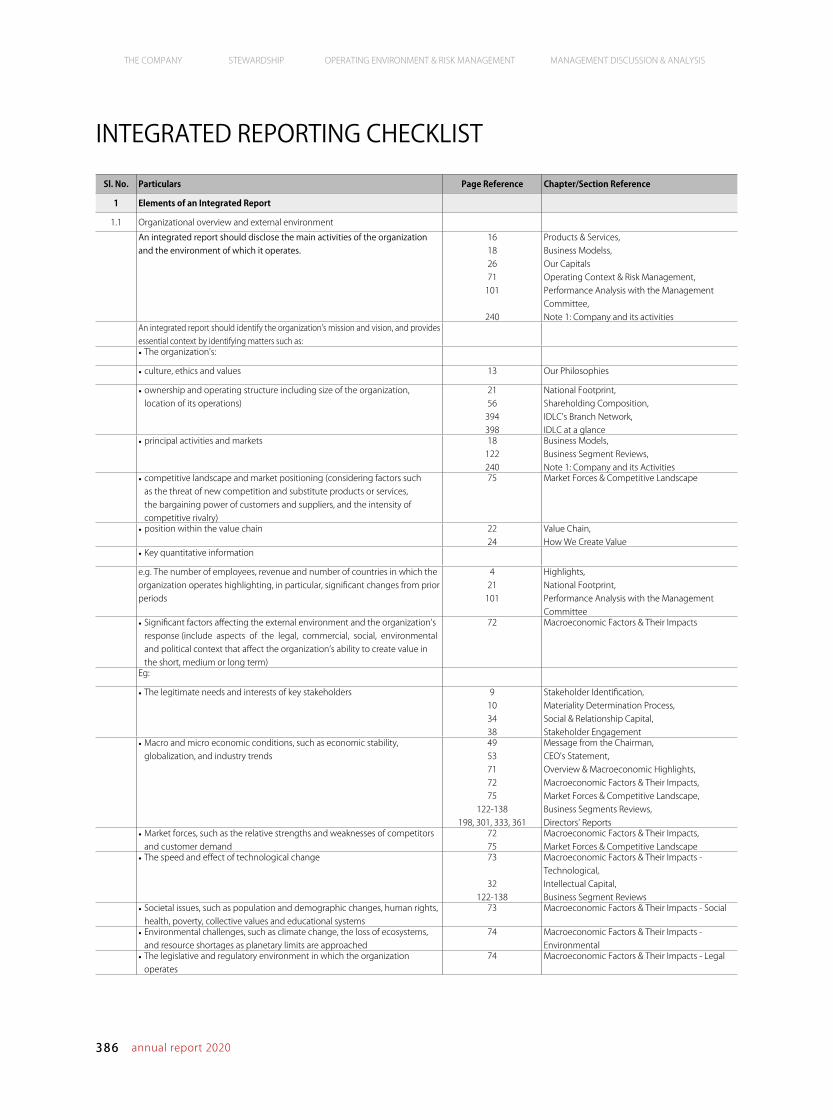

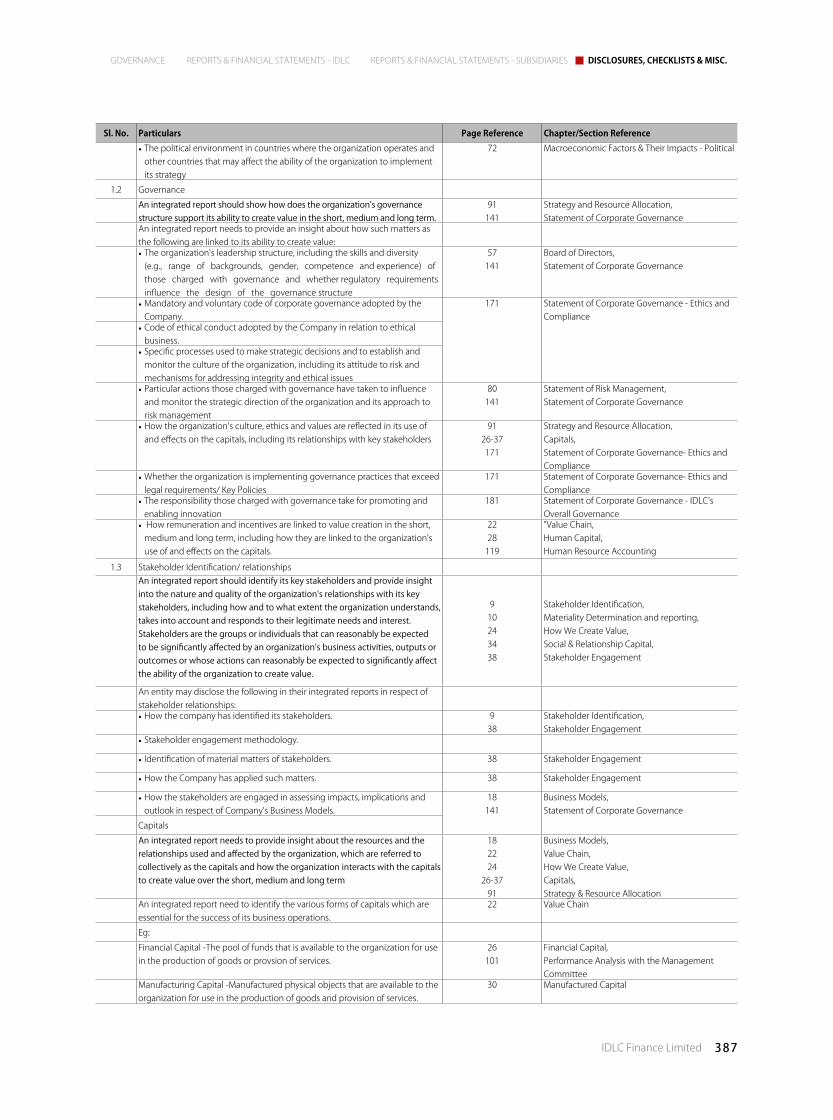

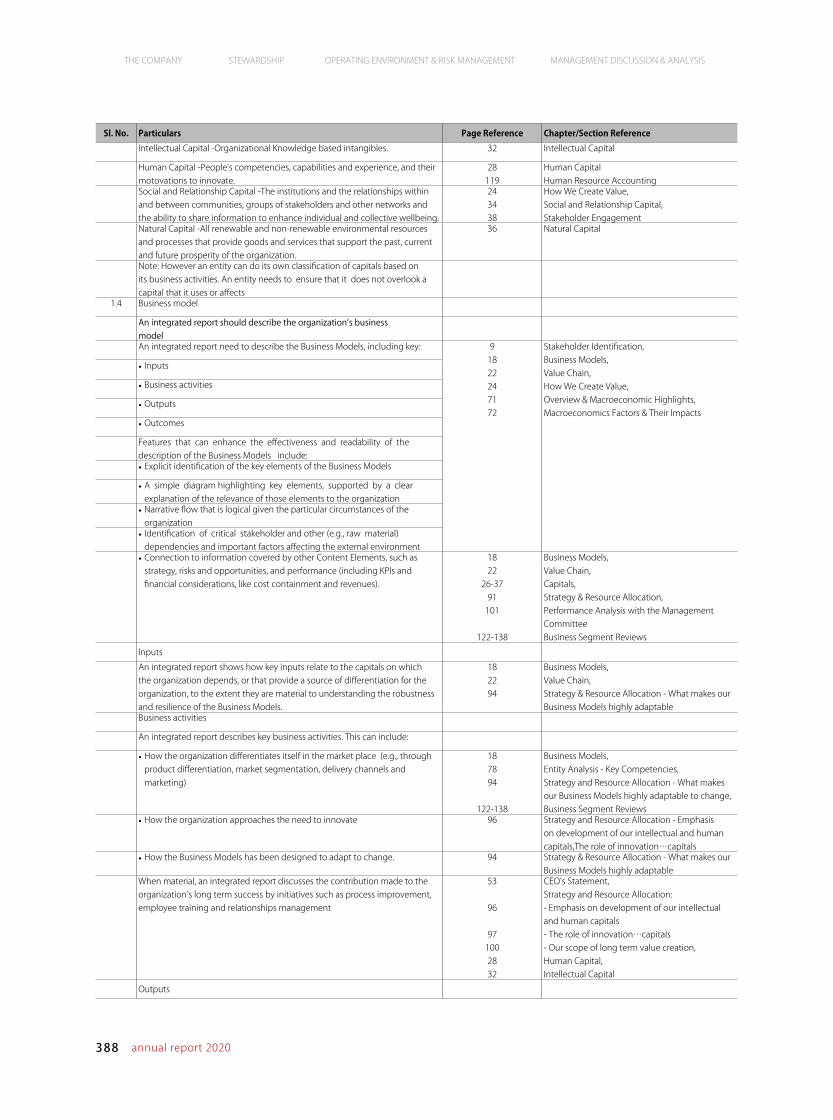

Integrated Reporting Checklist 386

IDLC’s Branch Network 394

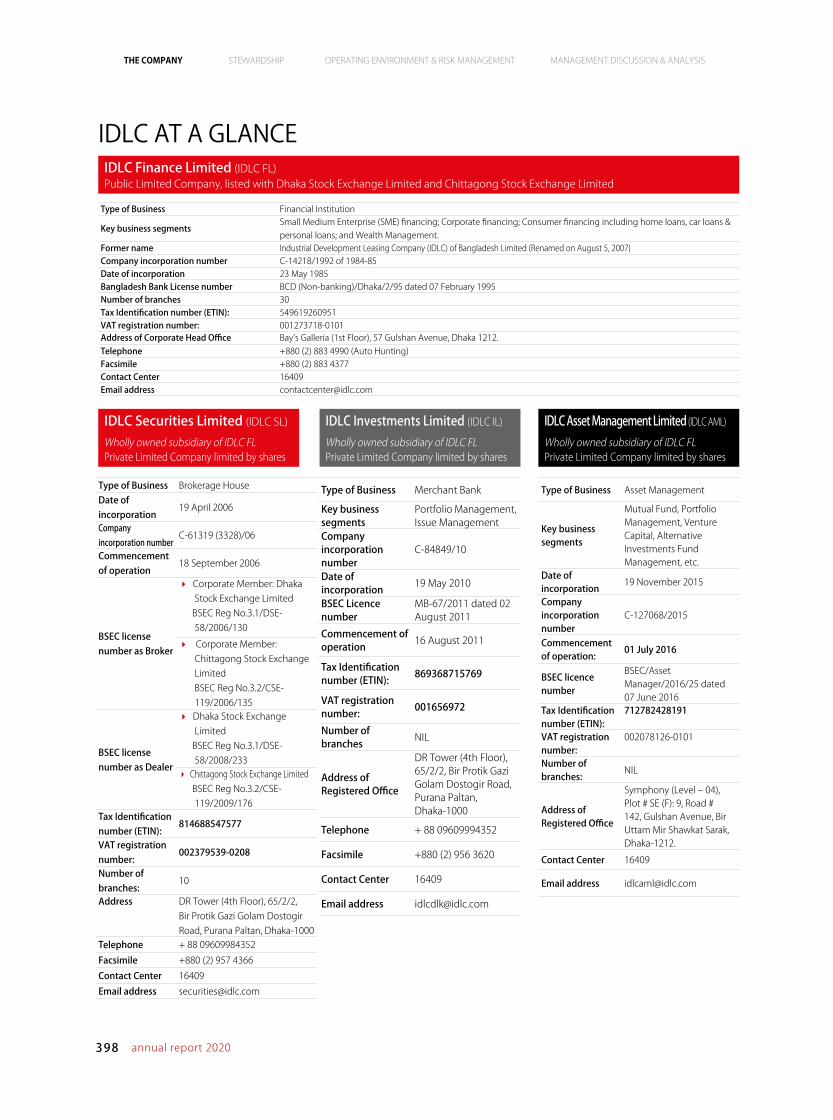

IDLC at a Glance 398

Proxy Form & Attendance Slip 399

4 annual report 2020

THE COMPANY STEWARDSHIP OPERATING ENVIRONMENT & RISK MANAGEMENT MANAGEMENT DISCUSSION & ANALYSIS

HIGHLIGHTS

PILOTED

Deposit Pension Scheme

E-Loan of SME

LAUNCHED IDLC Venture Capital Fund-I

Investors online onboarding platform

CUSTOMERS

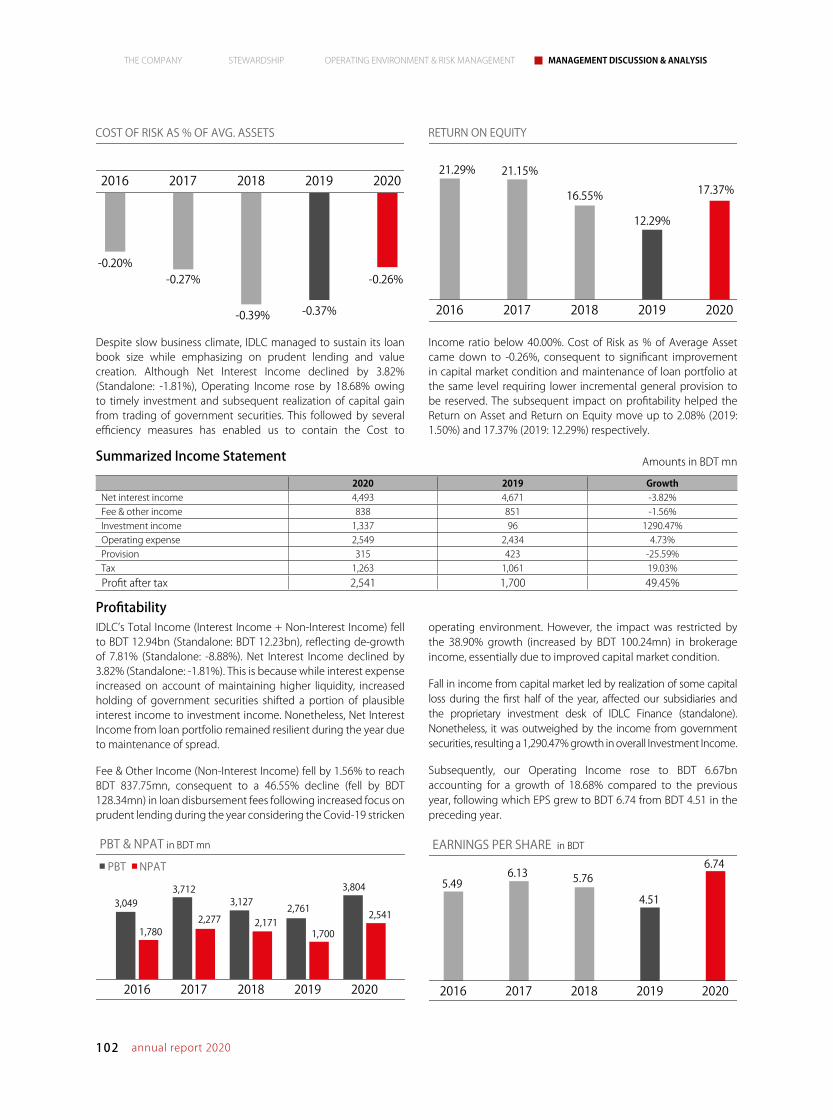

2.08%Return on Asset

35%Proposed Cash Dividend

SHAREHOLDERS

BDT 2,346 million

Contribution through payment of Tax, VAT and Excise Duty

REGULATORS

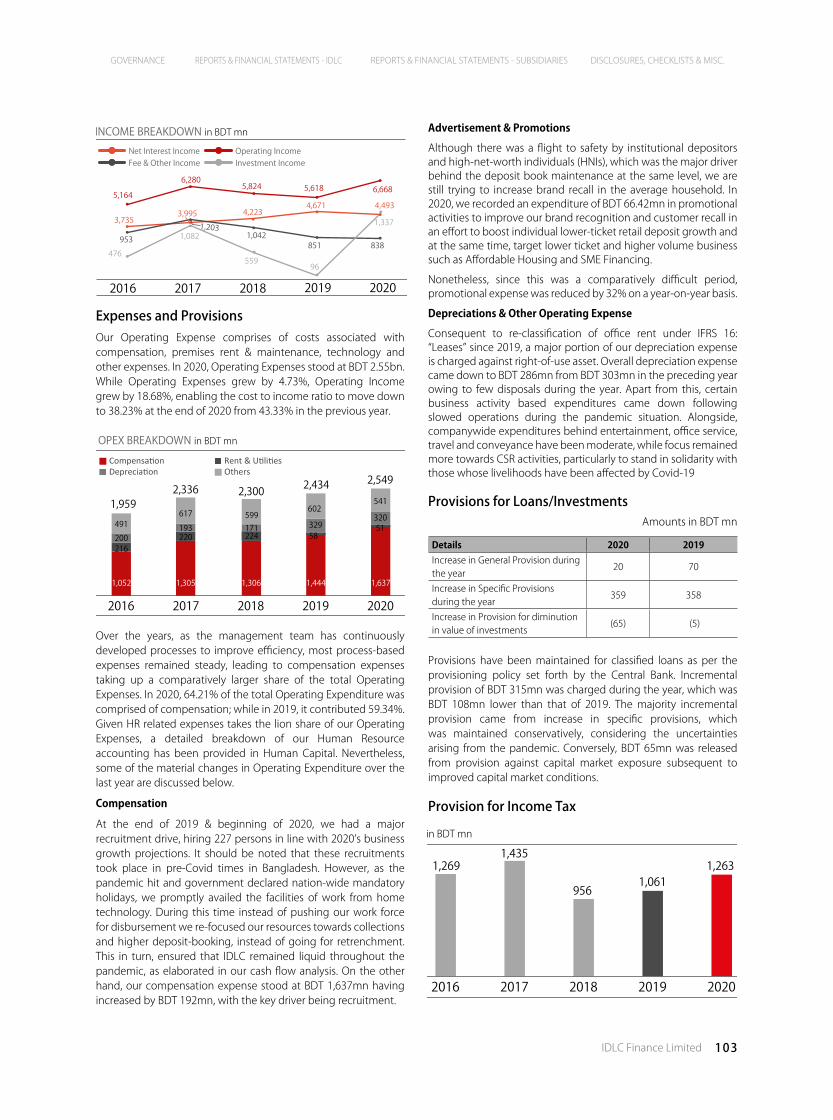

COST TO INCOME RATIO

2016 2017 2018 2019 2020

37.94%37.19%

39.49%

43.33%

38.23%

PROFIT AFTER TAX IN BDT MN

2016 2017 2018 2019 2020

5 year CAGR: 11.73%

1,780

2,277 2,171

1,700

2,541

2016 2017 2018 2019 2020

62,217 71,499

83,934 92,346 93,074

TOTAL LOAN PORTFOLIO in BDT mn5 year CAGR: 11.01%

5IDLC Finance Limited

GOVERNANCE REPORTS & FINANCIAL STATEMENTS - IDLC REPORTS & FINANCIAL STATEMENTS - SUBSIDIARIES DISCLOSURES, CHECKLISTS & MISC.

BDT 31 million

fund contributed to various entities to support the community through the pandemic

32,000+

individuals benefitted through our various CSR activities

COMMUNITY

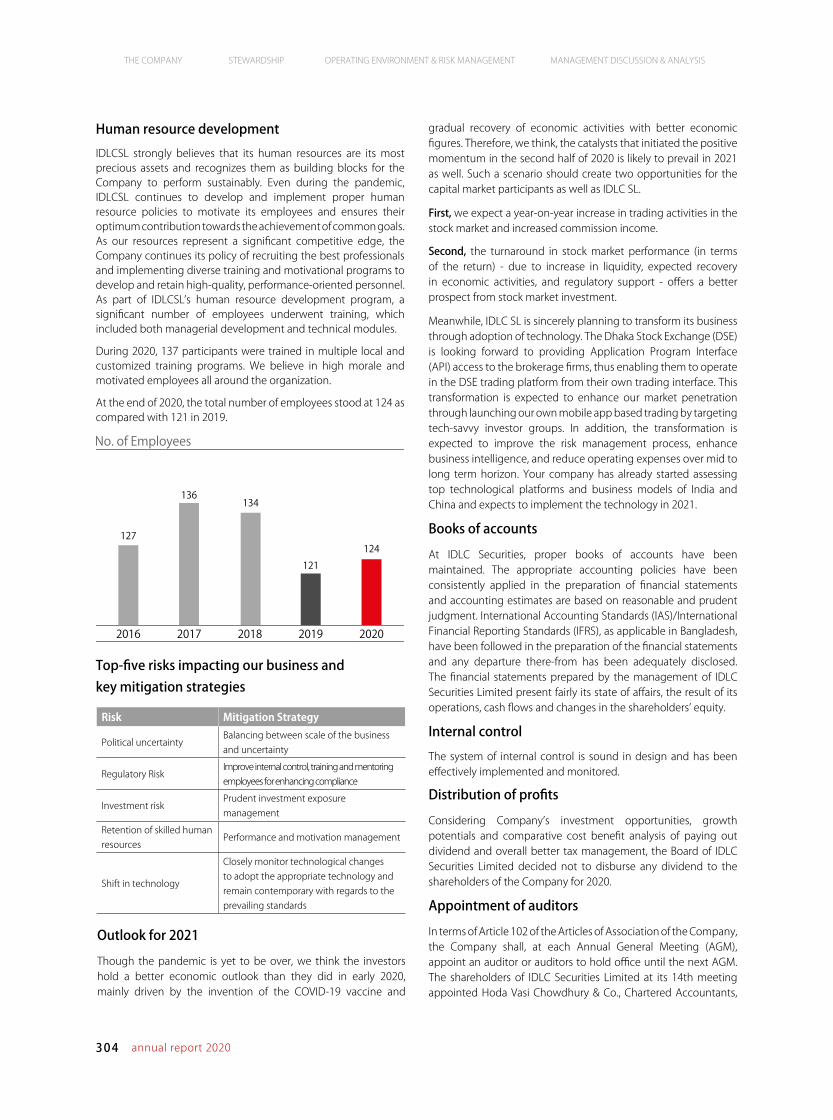

155Number of Training

7,554Number of Attendees

EMPLOYEES

NPL%

2016 2017 2018 2019 2020

2.98%2.77%

2.20%

3.07%

1.79%

RETURN ON ASSET

2016 2017 2018 2019 2020

2.33%2.60%

2.12%

1.50%

2.08%

RETURN ON EQUITY

2016 2017 2018 2019 2020

21.29% 21.15%

16.55%

12.29%

17.37%

6 annual report 2020

THE COMPANY STEWARDSHIP OPERATING ENVIRONMENT & RISK MANAGEMENT MANAGEMENT DISCUSSION & ANALYSIS

ABOUT OUR INTEGRATED REPORT

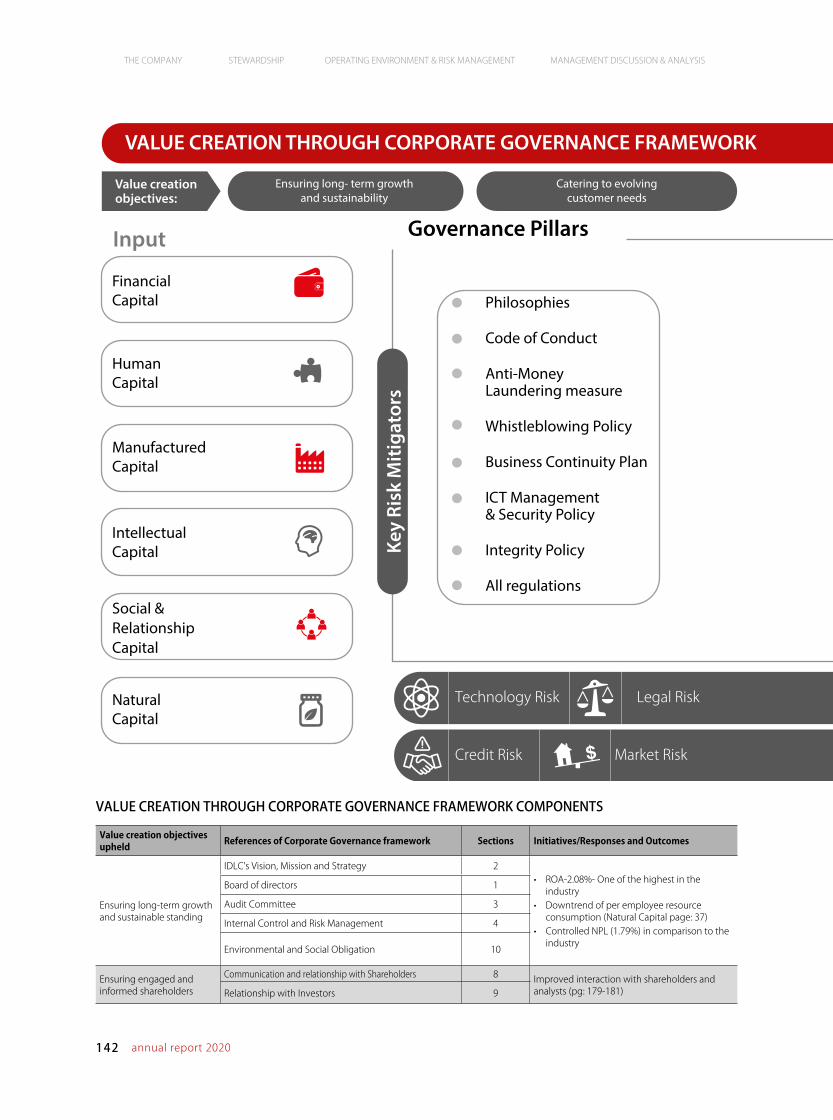

The story presents key aspects of our value creation process which are in the different forms of capital that provide the inputs, business domains and the value creating activities that results in outputs, outcomes and impacts. It also covers risk and the aspect of conformance. In totality, this report ensures

accurate measurement of operational, financial and sustainable performance against our strategy and the matters we consider to be most material to the sustainability of our Group, in a concise manner, so that it ensures comparability with the industry and beyond.

Scope and Boundaries of this Report

The report covers the period from 1 January 2020 to 31 December 2020, which encompasses the activities that have been carried out within the geographical boundaries of Bangladesh, as IDLC does not have operation or subsidiary in other countries.

We have referred to the guidelines of Integrated Report, issued by the Institute of Chartered Accountants of Bangladesh (ICAB) in the form of ‘Integrated Reporting Checklist’, which is in congruence with the integrated reporting framework prototype issued by the International Integrated Reporting Council (IIRC). We have also taken into account recommendations and

guidance from by IFC Toolkits for Disclosure and Transparency, published by International Finance Corporation to improve coherence, and transparency across the report.

In clarifying the Company’s operations and financial performance, we have extracted the financial information from the Audited Financial Statements for the financial year ended 2020 with relevant comparative information. The financial statements consistently comply with the mandated requirements of the laws of the land and of the industry that includes Companies Act 1994, Securities and Exchange Rules 1987, International Financial Reporting Standards, Financial Institutions Act 1993, circulars from Central Bank.

The aim of our integrated reporting approach is to enable our stakeholders, including investors, to make a more informed assessment of the value of IDLC and its prospects as this report is organised around our story of value creation.

REGULATIONS WE FOLLOW

• Companies Act 1994

• Financial Institutions Act 1993

• Securities and Exchange Rules 1987

• Corporate Governance Code

• Relevant rules and regulations of Bangladesh Bank (The Central Bank)

• And other applicable laws and regulations of the land.

REPORTING FRAMEWORKS AND GUIDELINES

• International Accounting Standards (IAS) and International Financial Reporting Standards (IFRS)

• Global Reporting Initiative (GRI)-GR4 Framework

• International Integrated Reporting Framework by International Reporting Council

• SAFA Integrated Reporting Checklist

• ICAB Corporate Governance Checklist

We are pleased to present to our shareholders with the 2020 Annual Report

in the form of an ‘Integrated Report’ for IDLC Finance Limited and its subsidiaries

(collectively referred to as IDLC Group).

7IDLC Finance Limited

GOVERNANCE REPORTS & FINANCIAL STATEMENTS - IDLC REPORTS & FINANCIAL STATEMENTS - SUBSIDIARIES DISCLOSURES, CHECKLISTS & MISC.

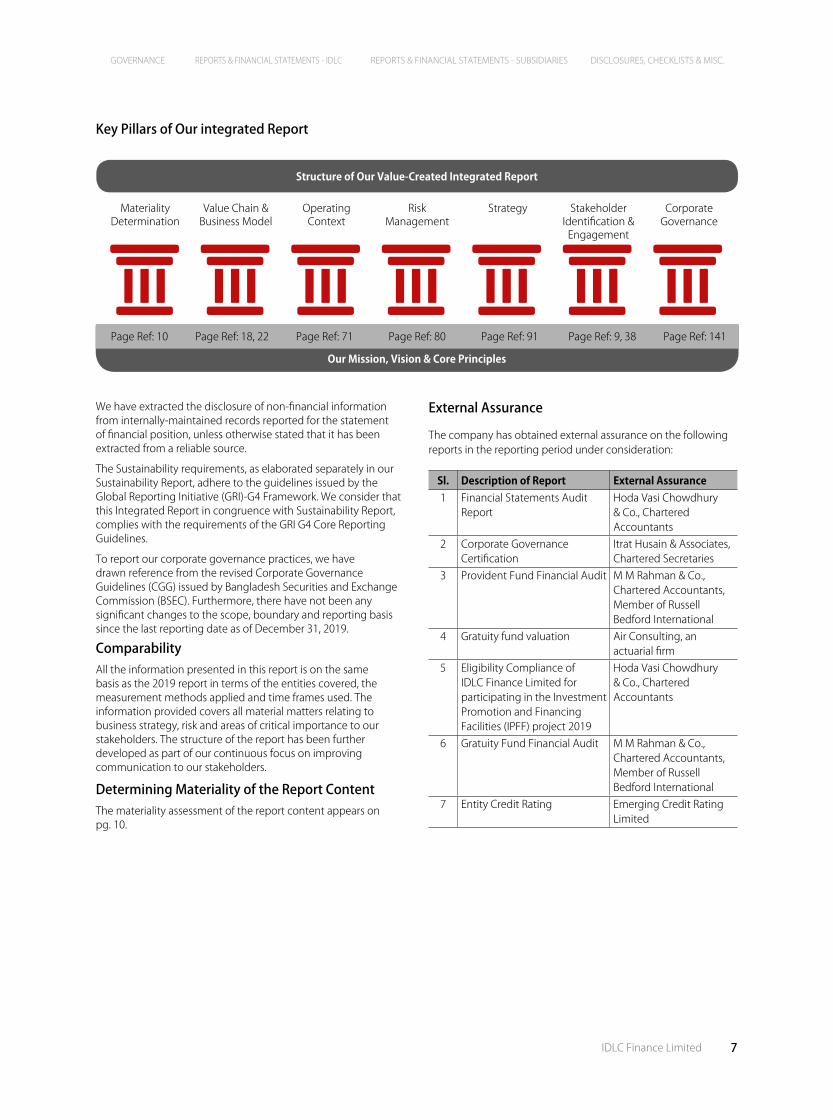

Structure of Our Value-Created Integrated Report

Our Mission, Vision & Core Principles

Materiality Determination

Value Chain & Business Model

Operating Context

Risk Management

Strategy Stakeholder Identification &

Engagement

Corporate Governance

Page Ref: 10 Page Ref: 18, 22 Page Ref: 71 Page Ref: 80 Page Ref: 91 Page Ref: 9, 38 Page Ref: 141

Key Pillars of Our integrated Report

We have extracted the disclosure of non-financial information from internally-maintained records reported for the statement of financial position, unless otherwise stated that it has been extracted from a reliable source.

The Sustainability requirements, as elaborated separately in our Sustainability Report, adhere to the guidelines issued by the Global Reporting Initiative (GRI)-G4 Framework. We consider that this Integrated Report in congruence with Sustainability Report, complies with the requirements of the GRI G4 Core Reporting Guidelines.

To report our corporate governance practices, we have drawn reference from the revised Corporate Governance Guidelines (CGG) issued by Bangladesh Securities and Exchange Commission (BSEC). Furthermore, there have not been any significant changes to the scope, boundary and reporting basis since the last reporting date as of December 31, 2019.

ComparabilityAll the information presented in this report is on the same basis as the 2019 report in terms of the entities covered, the measurement methods applied and time frames used. The information provided covers all material matters relating to business strategy, risk and areas of critical importance to our stakeholders. The structure of the report has been further developed as part of our continuous focus on improving communication to our stakeholders.

Determining Materiality of the Report ContentThe materiality assessment of the report content appears on pg. 10.

External Assurance

The company has obtained external assurance on the following reports in the reporting period under consideration:

Sl. Description of Report External Assurance1 Financial Statements Audit

ReportHoda Vasi Chowdhury & Co., Chartered Accountants

2 Corporate Governance Certification

Itrat Husain & Associates, Chartered Secretaries

3 Provident Fund Financial Audit M M Rahman & Co., Chartered Accountants, Member of Russell Bedford International

4 Gratuity fund valuation Air Consulting, an actuarial firm

5 Eligibility Compliance of IDLC Finance Limited for participating in the Investment Promotion and Financing Facilities (IPFF) project 2019

Hoda Vasi Chowdhury & Co., Chartered Accountants

6 Gratuity Fund Financial Audit M M Rahman & Co., Chartered Accountants, Member of Russell Bedford International

7 Entity Credit Rating Emerging Credit Rating Limited

8 annual report 2020

THE COMPANY STEWARDSHIP OPERATING ENVIRONMENT & RISK MANAGEMENT MANAGEMENT DISCUSSION & ANALYSIS

I, on behalf of the Board, acknowledge our responsibility to ensure the integrity of this Integrated Report, which addresses all material issues and presents fairly the integrated performance of IDLC Group.

Aziz Al MahmoodChairmanIDLC Finance Limited

The Board and the management ensures that reasonable care has been taken in preparation and presentation of this Integrated Annual Report to preserve the disclosure contained in this Integrated Report presented herewith which comprises the discussion, analysis and disclosures pertaining to stewardship, which should be read in conjunction with the audited financial statements. The role of stewardship brings upon it an obligation to be transparent and accountable, which is thoroughly recognised in this report.

Furthermore, we agree that the Integrated Annual Report has been prepared in accordance with the Integrated Reporting Council’s International Integrated Reporting Framework, and it addresses the material matter pertaining to the long term sustainability of the group and presents fairly the integrated performance of IDLC Group and the impacts thereof.

Responsibility over the Integrity of the Integrated Report

Availability of the Annual Report

The soft copy of the Annual Report is sent to all the shareholders, prior to holding the Annual General Meeting, giving due period of notice. Separately, for the benefit of all stakeholders, our report has been made available in the website http://www.idlc.com.

9IDLC Finance Limited

GOVERNANCE REPORTS & FINANCIAL STATEMENTS - IDLC REPORTS & FINANCIAL STATEMENTS - SUBSIDIARIES DISCLOSURES, CHECKLISTS & MISC.

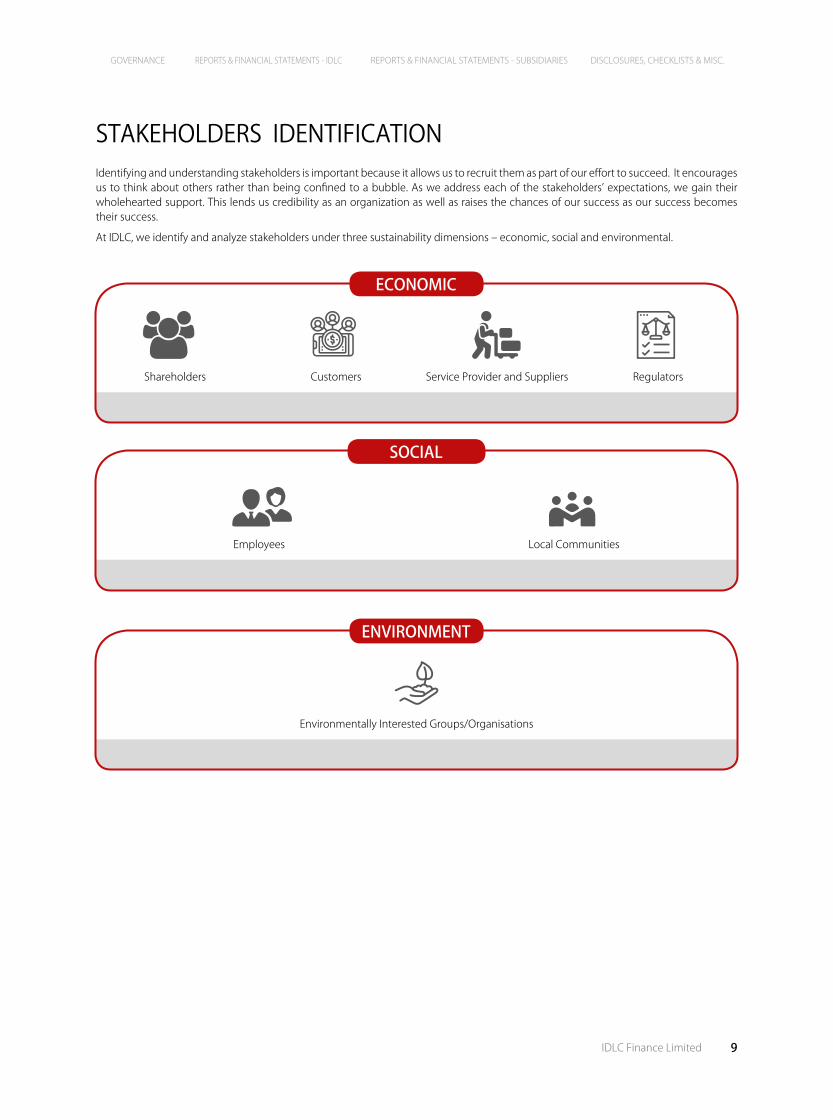

STAKEHOLDERS IDENTIFICATIONIdentifying and understanding stakeholders is important because it allows us to recruit them as part of our effort to succeed. It encourages us to think about others rather than being confined to a bubble. As we address each of the stakeholders’ expectations, we gain their wholehearted support. This lends us credibility as an organization as well as raises the chances of our success as our success becomes their success.

At IDLC, we identify and analyze stakeholders under three sustainability dimensions – economic, social and environmental.

Shareholders Customers Service Provider and Suppliers Regulators

Employees Local Communities

Environmentally Interested Groups/Organisations

ECONOMIC

SOCIAL

ENVIRONMENT

10 annual report 2020

THE COMPANY STEWARDSHIP OPERATING ENVIRONMENT & RISK MANAGEMENT MANAGEMENT DISCUSSION & ANALYSIS

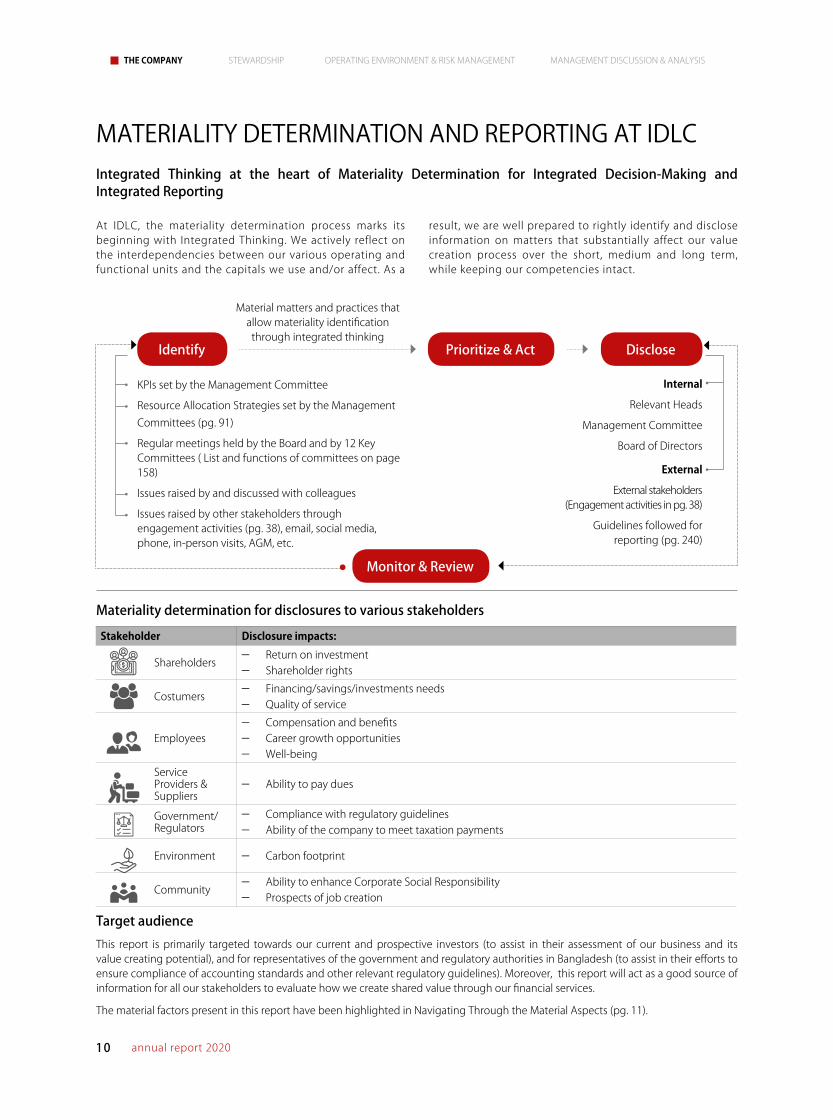

MATERIALITY DETERMINATION AND REPORTING AT IDLC

At IDLC, the materiality determination process marks its beginning with Integrated Thinking. We actively reflect on the interdependencies between our various operating and functional units and the capitals we use and/or affect. As a

result, we are well prepared to rightly identify and disclose information on matters that substantially affect our value creation process over the short, medium and long term, while keeping our competencies intact.

Materiality determination for disclosures to various stakeholders

Target audienceThis report is primarily targeted towards our current and prospective investors (to assist in their assessment of our business and its value creating potential), and for representatives of the government and regulatory authorities in Bangladesh (to assist in their efforts to ensure compliance of accounting standards and other relevant regulatory guidelines). Moreover, this report will act as a good source of information for all our stakeholders to evaluate how we create shared value through our financial services.

The material factors present in this report have been highlighted in Navigating Through the Material Aspects (pg. 11).

Stakeholder Disclosure impacts:

Shareholders- Return on investment- Shareholder rights

Costumers- Financing/savings/investments needs- Quality of service

Employees- Compensation and benefits- Career growth opportunities- Well-being

Service Providers & Suppliers

- Ability to pay dues

Government/Regulators

- Compliance with regulatory guidelines- Ability of the company to meet taxation payments

Environment - Carbon footprint

Community- Ability to enhance Corporate Social Responsibility- Prospects of job creation

Monitor & Review

Identify DisclosePrioritize & Act

Integrated Thinking at the heart of Materiality Determination for Integrated Decision-Making and Integrated Reporting

Material matters and practices that allow materiality identification through integrated thinking

KPIs set by the Management Committee

Resource Allocation Strategies set by the Management Committees (pg. 91)

Regular meetings held by the Board and by 12 Key Committees ( List and functions of committees on page 158)

Issues raised by and discussed with colleagues

Issues raised by other stakeholders through engagement activities (pg. 38), email, social media, phone, in-person visits, AGM, etc.

Internal

Relevant Heads

Management Committee

Board of Directors

External

External stakeholders (Engagement activities in pg. 38)

Guidelines followed for reporting (pg. 240)

11IDLC Finance Limited

GOVERNANCE REPORTS & FINANCIAL STATEMENTS - IDLC REPORTS & FINANCIAL STATEMENTS - SUBSIDIARIES DISCLOSURES, CHECKLISTS & MISC.

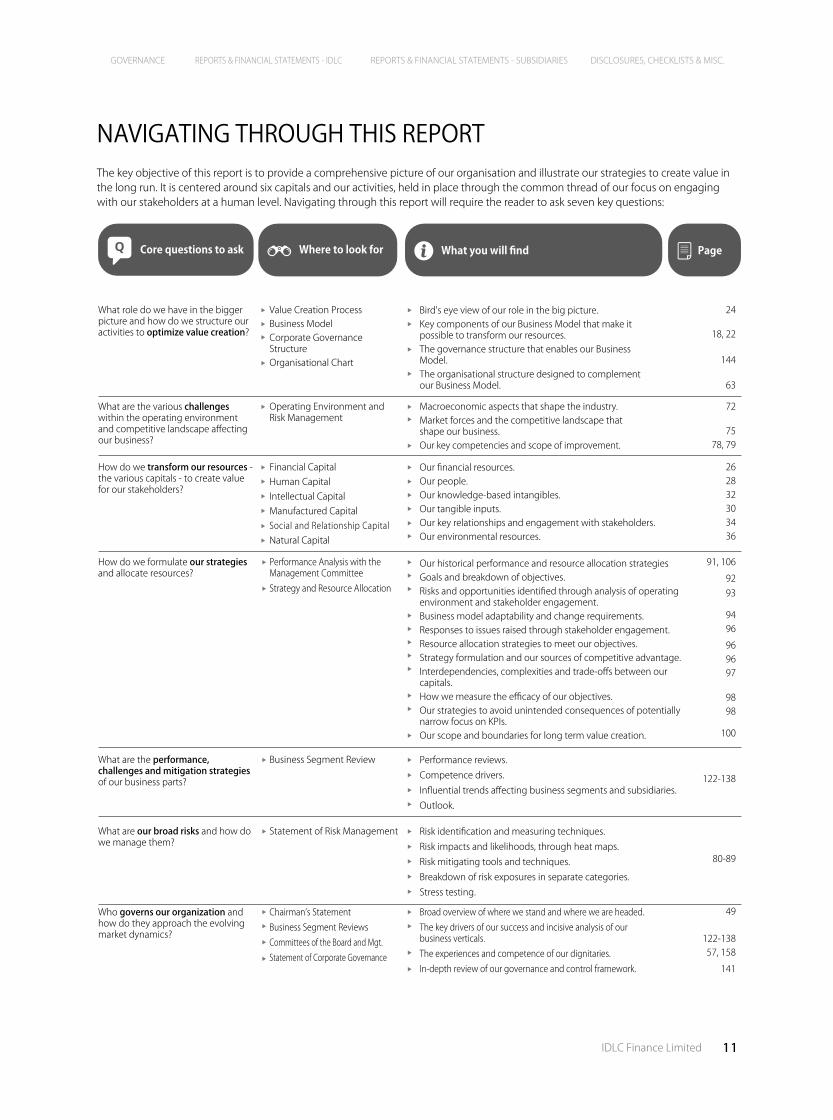

NAVIGATING THROUGH THIS REPORTThe key objective of this report is to provide a comprehensive picture of our organisation and illustrate our strategies to create value in the long run. It is centered around six capitals and our activities, held in place through the common thread of our focus on engaging with our stakeholders at a human level. Navigating through this report will require the reader to ask seven key questions:

What role do we have in the bigger picture and how do we structure our activities to optimize value creation?

Value Creation ProcessBusiness ModelCorporate Governance StructureOrganisational Chart

Bird's eye view of our role in the big picture.Key components of our Business Model that make it possible to transform our resources.The governance structure that enables our Business Model.The organisational structure designed to complement our Business Model.

Core questions to ask Where to look for What you will find Page

24

18, 22

144

63

What are the various challenges within the operating environment and competitive landscape affecting our business?

Operating Environment and Risk Management

Macroeconomic aspects that shape the industry.Market forces and the competitive landscape that shape our business.Our key competencies and scope of improvement.

72

7578, 79

How do we transform our resources - the various capitals - to create value for our stakeholders?

Financial CapitalHuman CapitalIntellectual CapitalManufactured CapitalSocial and Relationship CapitalNatural Capital

Our financial resources.Our people.Our knowledge-based intangibles.Our tangible inputs.Our key relationships and engagement with stakeholders.Our environmental resources.

2628

32303436

How do we formulate our strategies and allocate resources?

Performance Analysis with the Management CommitteeStrategy and Resource Allocation

Our historical performance and resource allocation strategiesGoals and breakdown of objectives.Risks and opportunities identified through analysis of operating environment and stakeholder engagement.Business model adaptability and change requirements.Responses to issues raised through stakeholder engagement.Resource allocation strategies to meet our objectives.Strategy formulation and our sources of competitive advantage.Interdependencies, complexities and trade-offs between our capitals.How we measure the efficacy of our objectives.Our strategies to avoid unintended consequences of potentially narrow focus on KPIs.Our scope and boundaries for long term value creation.

91, 106

9293

9496

969697

9898

100

What are the performance, challenges and mitigation strategies of our business parts?

Business Segment Review Performance reviews.Competence drivers.Influential trends affecting business segments and subsidiaries.Outlook.

122-138

What are our broad risks and how do we manage them?

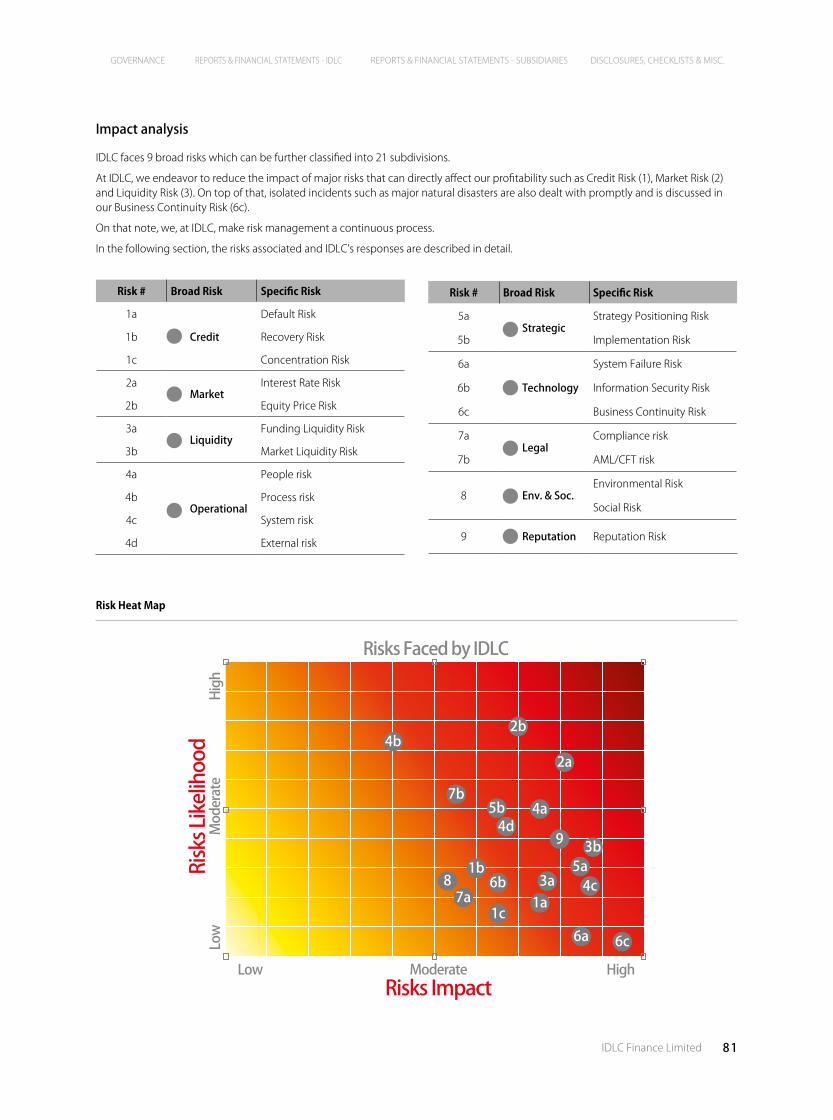

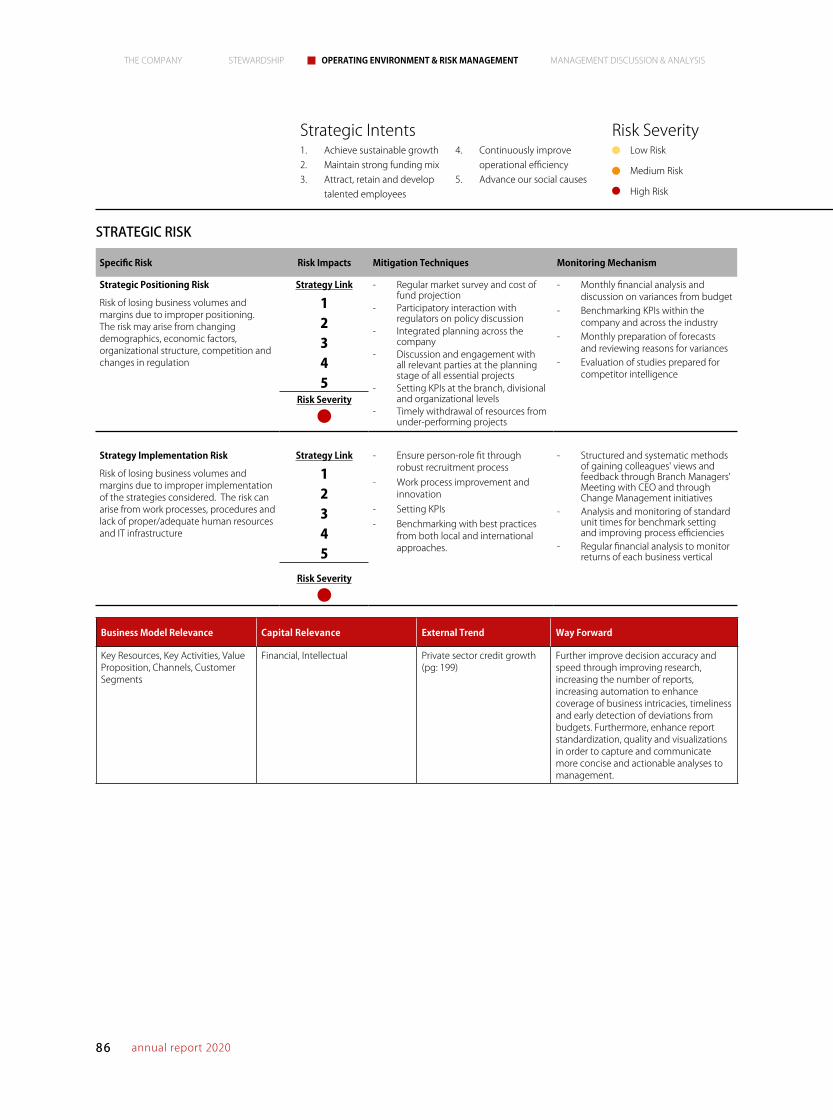

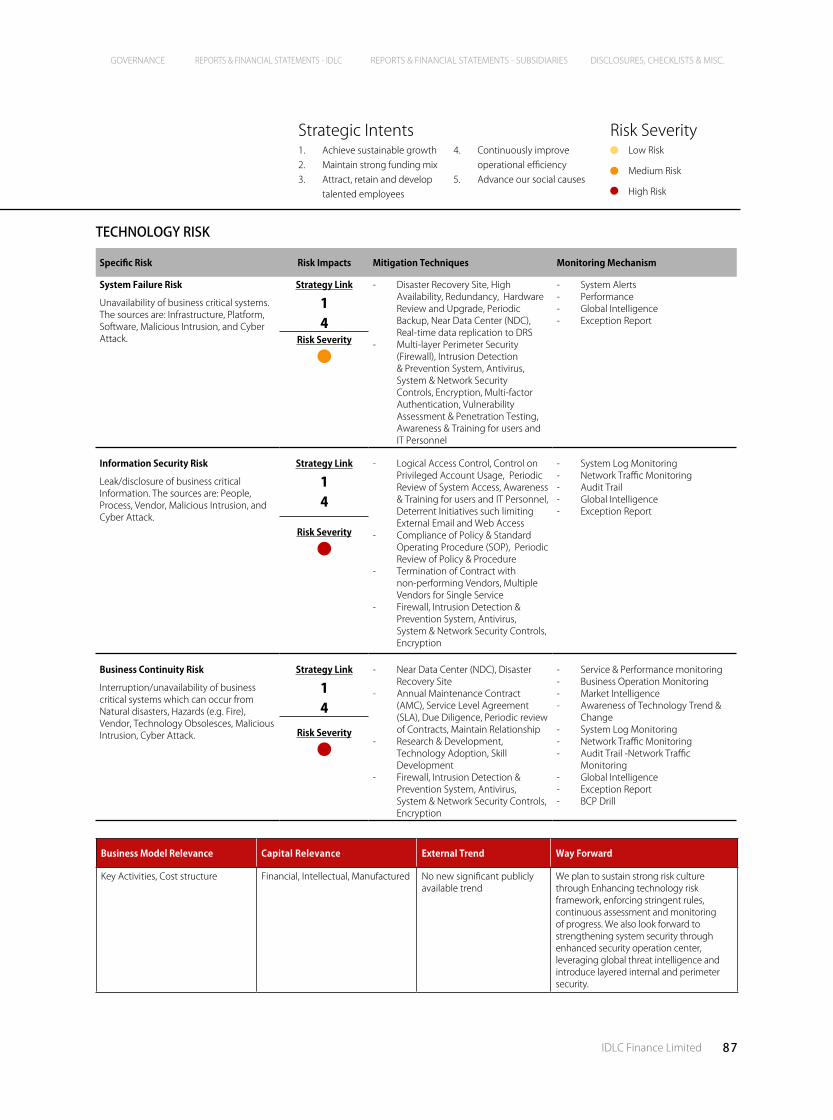

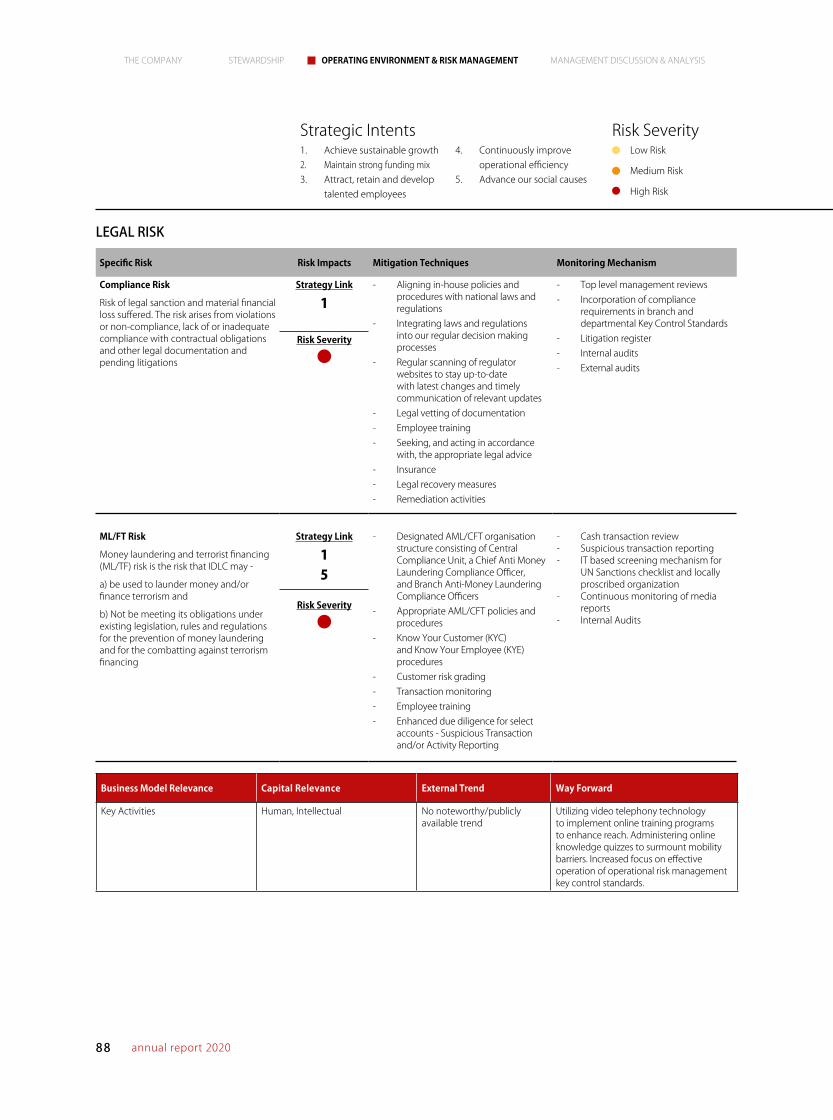

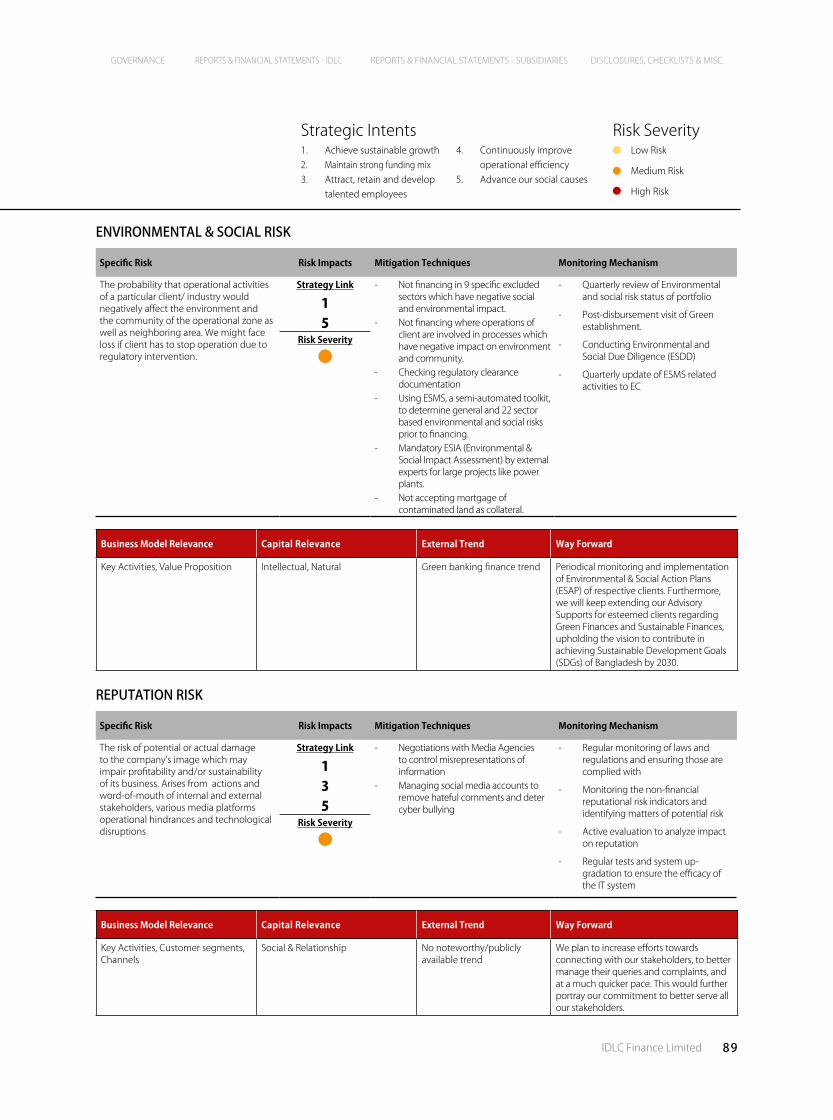

Statement of Risk Management Risk identification and measuring techniques.Risk impacts and likelihoods, through heat maps.Risk mitigating tools and techniques.Breakdown of risk exposures in separate categories.Stress testing.

80-89

Who governs our organization and how do they approach the evolving market dynamics?

Chairman’s StatementBusiness Segment ReviewsCommittees of the Board and Mgt.Statement of Corporate Governance

Broad overview of where we stand and where we are headed.The key drivers of our success and incisive analysis of our business verticals.The experiences and competence of our dignitaries.In-depth review of our governance and control framework.

49

122-13857, 158

141

12 annual report 2020

THE COMPANY STEWARDSHIP OPERATING ENVIRONMENT & RISK MANAGEMENT MANAGEMENT DISCUSSION & ANALYSIS

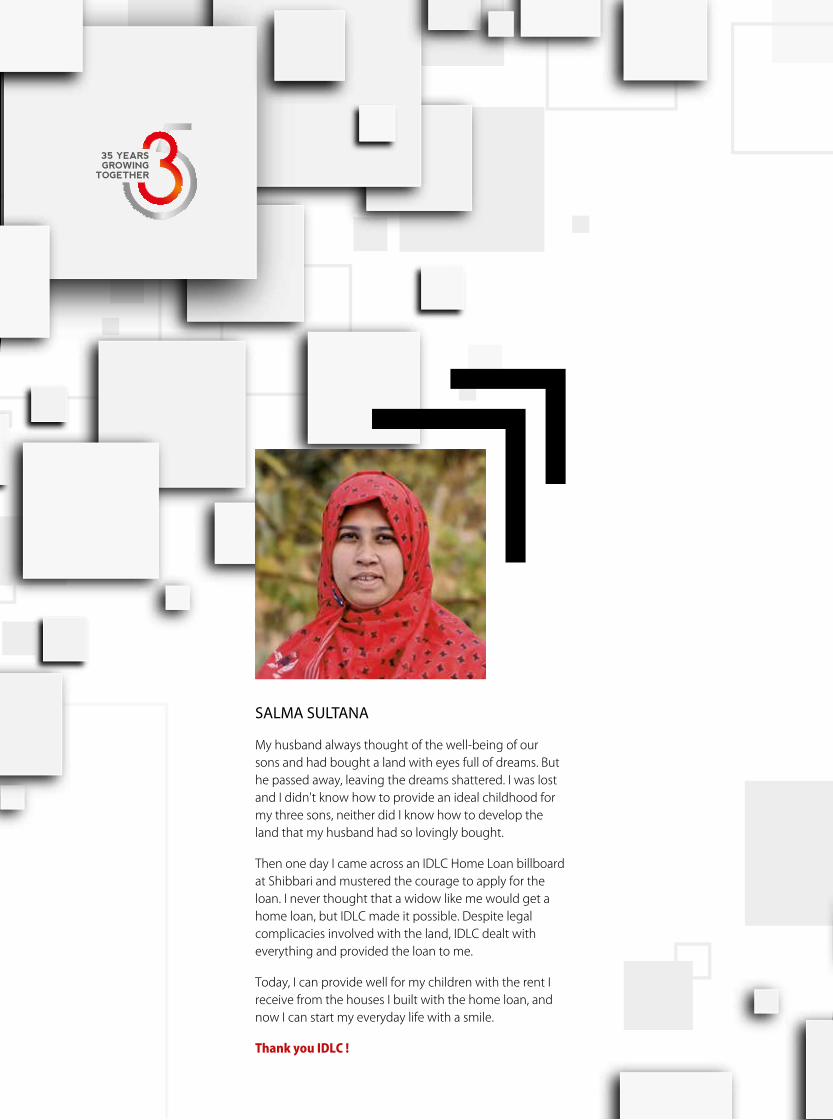

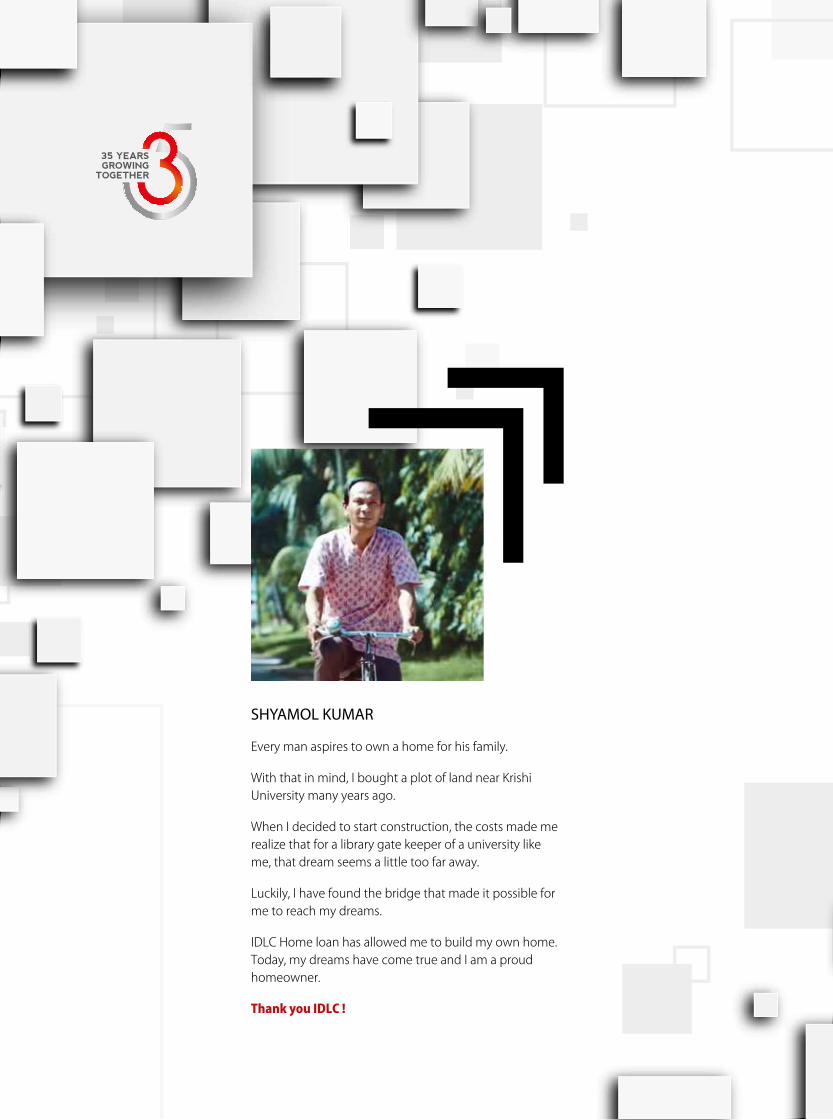

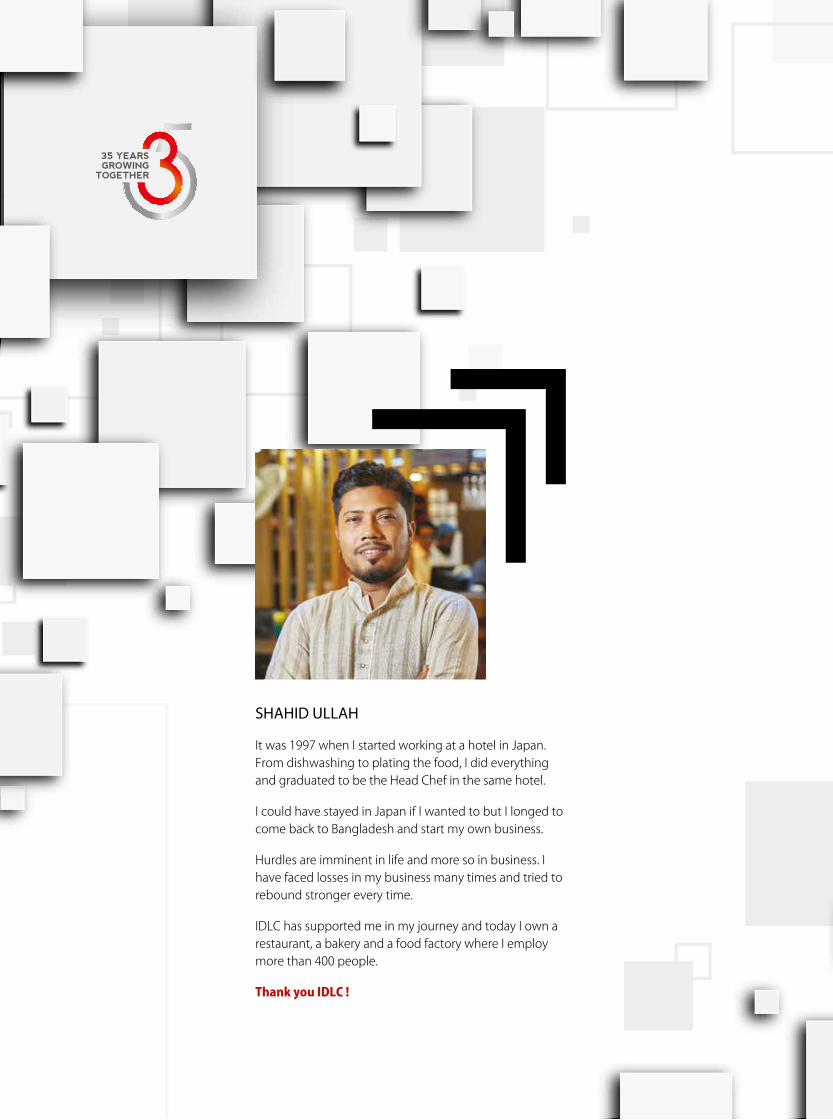

SALMA SULTANA

My husband always thought of the well-being of our sons and had bought a land with eyes full of dreams. But he passed away, leaving the dreams shattered. I was lost and I didn't know how to provide an ideal childhood for my three sons, neither did I know how to develop the land that my husband had so lovingly bought.

Then one day I came across an IDLC Home Loan billboard at Shibbari and mustered the courage to apply for the loan. I never thought that a widow like me would get a home loan, but IDLC made it possible. Despite legal complicacies involved with the land, IDLC dealt with everything and provided the loan to me.

Today, I can provide well for my children with the rent I receive from the houses I built with the home loan, and now I can start my everyday life with a smile.

Thank you IDLC !

13IDLC Finance Limited

GOVERNANCE REPORTS & FINANCIAL STATEMENTS - IDLC REPORTS & FINANCIAL STATEMENTS - SUBSIDIARIES DISCLOSURES, CHECKLISTS & MISC.

SALMA SULTANA

My husband always thought of the well-being of our sons and had bought a land with eyes full of dreams. But he passed away, leaving the dreams shattered. I was lost and I didn't know how to provide an ideal childhood for my three sons, neither did I know how to develop the land that my husband had so lovingly bought.

Then one day I came across an IDLC Home Loan billboard at Shibbari and mustered the courage to apply for the loan. I never thought that a widow like me would get a home loan, but IDLC made it possible. Despite legal complicacies involved with the land, IDLC dealt with everything and provided the loan to me.

Today, I can provide well for my children with the rent I receive from the houses I built with the home loan, and now I can start my everyday life with a smile.

Thank you IDLC !

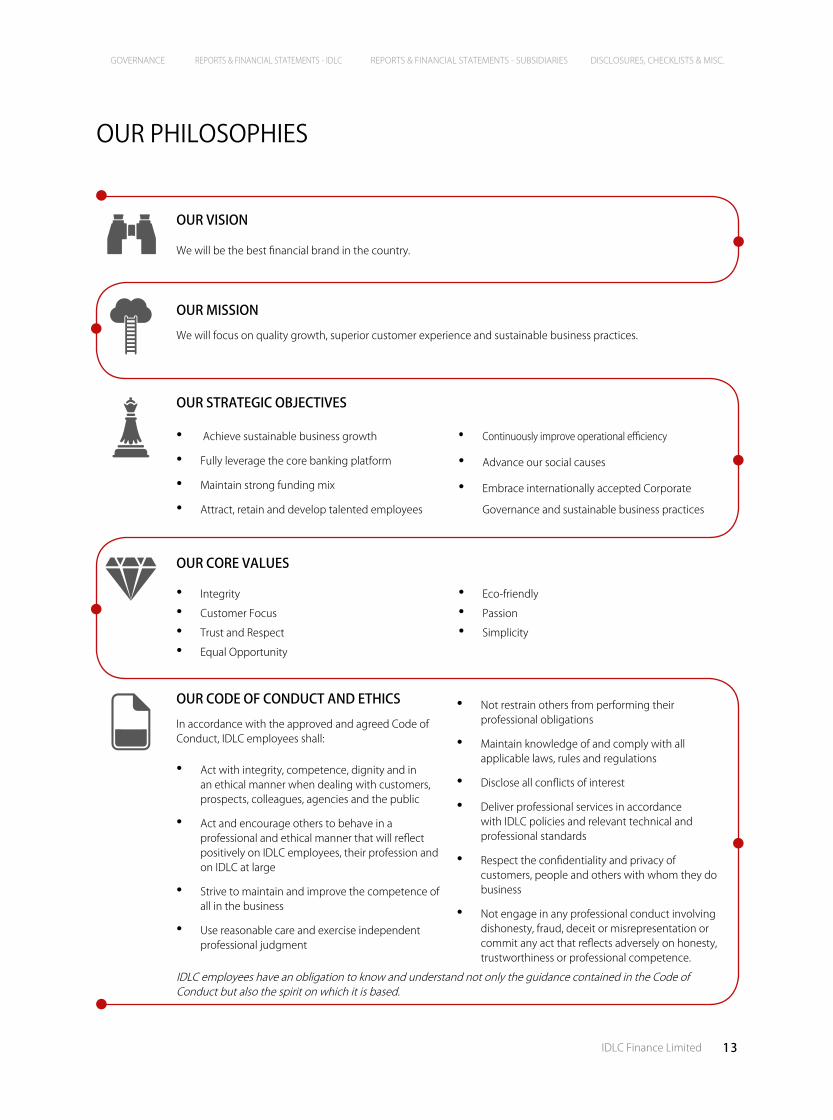

OUR PHILOSOPHIES

OUR CODE OF CONDUCT AND ETHICS

In accordance with the approved and agreed Code of Conduct, IDLC employees shall:

• Act with integrity, competence, dignity and in an ethical manner when dealing with customers, prospects, colleagues, agencies and the public

• Act and encourage others to behave in a professional and ethical manner that will reflect positively on IDLC employees, their profession and on IDLC at large

• Strive to maintain and improve the competence of all in the business

• Use reasonable care and exercise independent professional judgment

• Not restrain others from performing their professional obligations

• Maintain knowledge of and comply with all applicable laws, rules and regulations

• Disclose all conflicts of interest

• Deliver professional services in accordance with IDLC policies and relevant technical and professional standards

• Respect the confidentiality and privacy of customers, people and others with whom they do business

• Not engage in any professional conduct involving dishonesty, fraud, deceit or misrepresentation or commit any act that reflects adversely on honesty, trustworthiness or professional competence.

• Achieve sustainable business growth

• Fully leverage the core banking platform

• Maintain strong funding mix

• Attract, retain and develop talented employees

• Continuously improve operational efficiency

• Advance our social causes

• Embrace internationally accepted Corporate

Governance and sustainable business practices

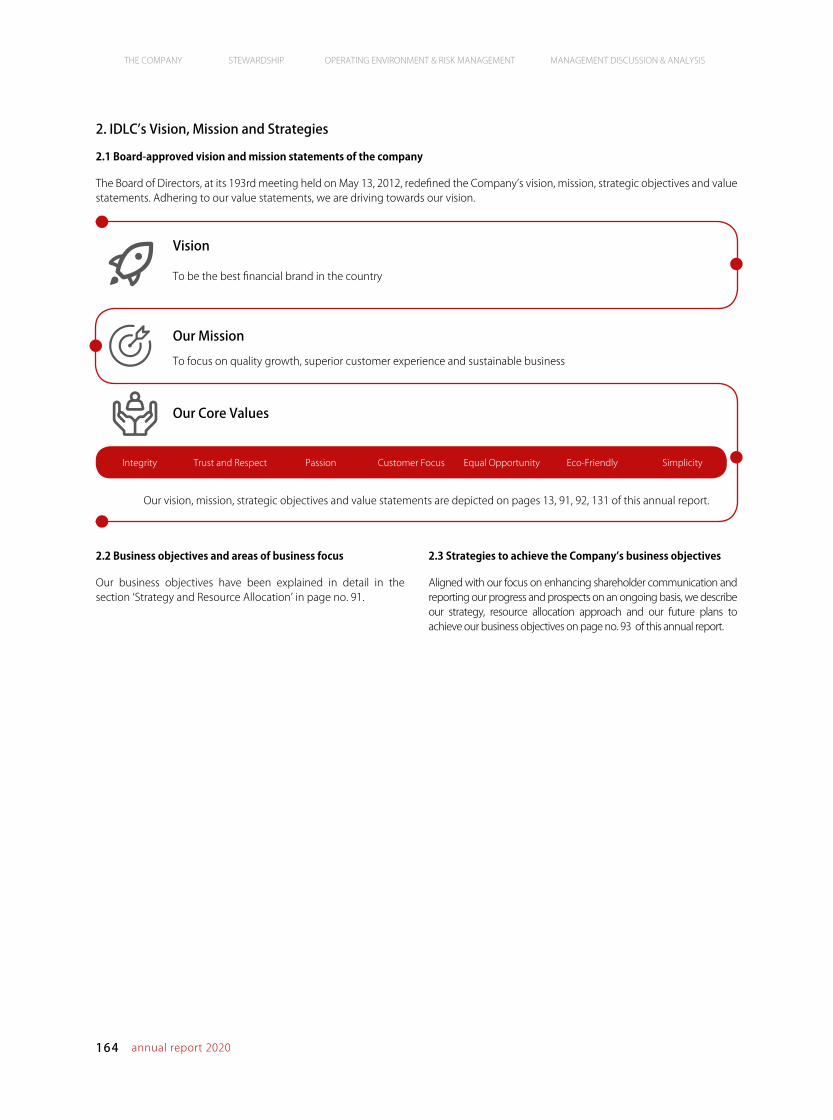

OUR VISION

We will be the best financial brand in the country.

OUR MISSION

We will focus on quality growth, superior customer experience and sustainable business practices.

• Integrity

• Customer Focus

• Trust and Respect

• Equal Opportunity

• Eco-friendly

• Passion

• Simplicity

IDLC employees have an obligation to know and understand not only the guidance contained in the Code of Conduct but also the spirit on which it is based.

OUR STRATEGIC OBJECTIVES

OUR CORE VALUES

14 annual report 2020

THE COMPANY STEWARDSHIP OPERATING ENVIRONMENT & RISK MANAGEMENT MANAGEMENT DISCUSSION & ANALYSIS

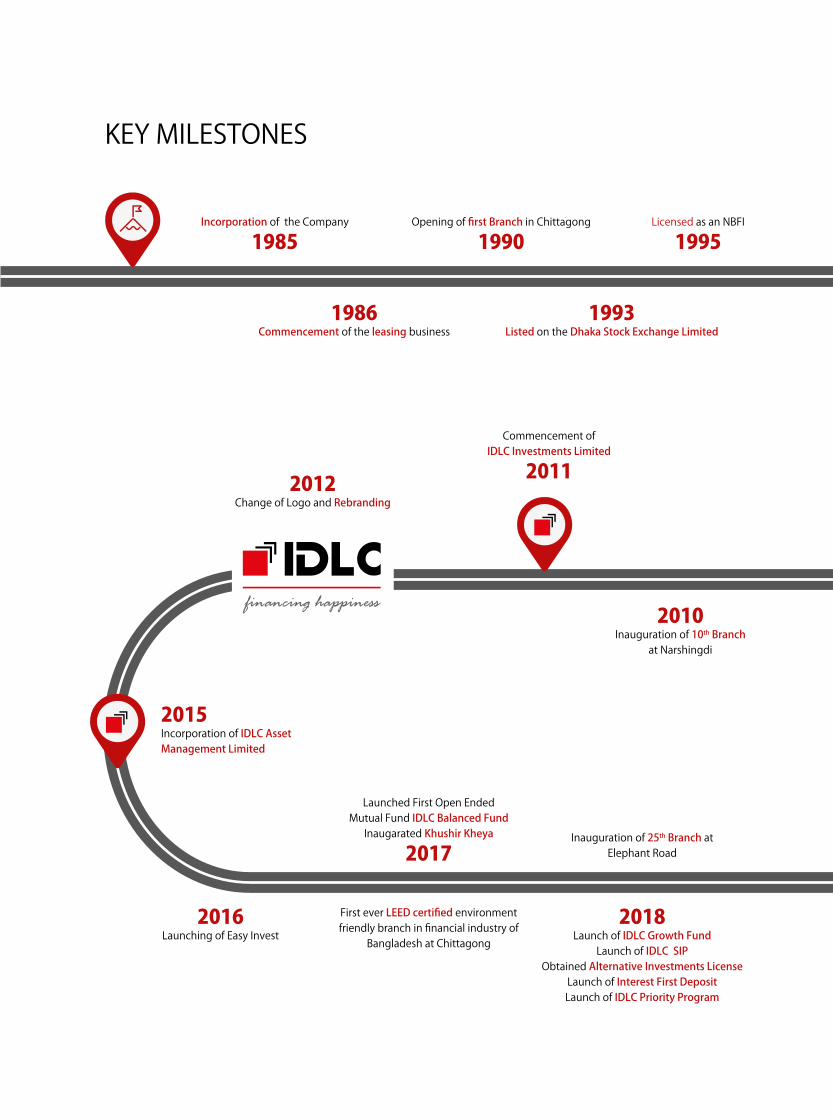

Opening of first Branch in Chittagong

1990

Launched First Open Ended Mutual Fund IDLC Balanced Fund

Inaugarated Khushir Kheya

2017

2019Launch of VSE Finance & Affordable Housing

Received BSEC approval for Venture Capital FundLaunch of IDLC AML Shariah Fund

2020Launch of Venture Capital Fund-I

Launch of Online On-boarding Platform by IDLC AML

Inauguration of 25th Branch at Elephant Road

First ever LEED certified environment friendly branch in financial industry of

Bangladesh at Chittagong

Licensed as an NBFI

1995Incorporation of the Company

1985

Commencement of IDLC Investments Limited

2011

Commencement of home finance and short-term finance operations

1997

Company Name changed to IDLC Finance Limited

2007

Commencement of corporate finance and merchant banking operations

1999

2006Commencement of IDLC Securities Limited

Opening of the first SME focused branch at BoguraRelocation of Head Office to Gulshan Premise

1986Commencement of the leasing business

2016Launching of Easy Invest

2018Launch of IDLC Growth Fund

Launch of IDLC SIPObtained Alternative Investments License

Launch of Interest First Deposit Launch of IDLC Priority Program

1993Listed on the Dhaka Stock Exchange Limited

1996Listed on the Chittagong Stock Exchange Limited

1998Licensed as a merchant

banker by BSEC

2004Opening of first retail focused

branch at Dhanmondi

2012Change of Logo and Rebranding

2015Incorporation of IDLC AssetManagement Limited

2010Inauguration of 10th Branch

at Narshingdi

KEY MILESTONES

15IDLC Finance Limited

GOVERNANCE REPORTS & FINANCIAL STATEMENTS - IDLC REPORTS & FINANCIAL STATEMENTS - SUBSIDIARIES DISCLOSURES, CHECKLISTS & MISC.

Opening of first Branch in Chittagong

1990

Launched First Open Ended Mutual Fund IDLC Balanced Fund

Inaugarated Khushir Kheya

2017

2019Launch of VSE Finance & Affordable Housing

Received BSEC approval for Venture Capital FundLaunch of IDLC AML Shariah Fund

2020Launch of Venture Capital Fund-I

Launch of Online On-boarding Platform by IDLC AML

Inauguration of 25th Branch at Elephant Road

First ever LEED certified environment friendly branch in financial industry of

Bangladesh at Chittagong

Licensed as an NBFI

1995Incorporation of the Company

1985

Commencement of IDLC Investments Limited

2011

Commencement of home finance and short-term finance operations

1997

Company Name changed to IDLC Finance Limited

2007

Commencement of corporate finance and merchant banking operations

1999

2006Commencement of IDLC Securities Limited

Opening of the first SME focused branch at BoguraRelocation of Head Office to Gulshan Premise

1986Commencement of the leasing business

2016Launching of Easy Invest

2018Launch of IDLC Growth Fund

Launch of IDLC SIPObtained Alternative Investments License

Launch of Interest First Deposit Launch of IDLC Priority Program

1993Listed on the Dhaka Stock Exchange Limited

1996Listed on the Chittagong Stock Exchange Limited

1998Licensed as a merchant

banker by BSEC

2004Opening of first retail focused

branch at Dhanmondi

2012Change of Logo and Rebranding

2015Incorporation of IDLC AssetManagement Limited

2010Inauguration of 10th Branch

at Narshingdi

KEY MILESTONES

16 annual report 2020

THE COMPANY STEWARDSHIP OPERATING ENVIRONMENT & RISK MANAGEMENT MANAGEMENT DISCUSSION & ANALYSIS

PRODUCTS AND SERVICES

Small Enterprise Financing• SME Term Loan/Lease• Purnota – Women

Entrepreneur Loan

• Working Capital Loan• Seasonal Loan• Abashan Loan• SME Shombhabona• Commercial Vehicle Loan• IDLC Udbhabon

Supply Chain Finance• Factoring of Accounts

Receivables• Work Order Financing• Distributor Financing

Home Loan• Apartment/Home Purchase• Building Construction• Commercial Space• Home Equity• Affordable Housing

Finance Solution

• ASHA• ULLAS• Semi Paka Loan

Car Loan• Brand New• Reconditioned

Personal Loan• Secured• Unsecured

SME

Consumer

Deposits

Corporate Finance• Lease Financing• Term Loan Financing• Commercial Vehicle

Finance• Commercial Space

Financing• Project Financing• Short Term Loans (to

meet working capital requirements)

• Specialized Products (for meeting seasonal demand)

• Preferred Stock

• Bridge Loan

Structured Finance Solutions• Debt Syndication (Local &

Foreign Currency)• Working Capital

Syndication• Agency & Trusteeship• Fund Raising through

Zero Coupon & Coupon Bearing Bonds

• Commercial Paper• Arrangement of Private

Equity & Preference Shares• Corporate Advisory for

Mergers• Balance Sheet

Restructuring• Preparation of feasibility

Study

Green Banking Solutions• Certified Green Industry/

Building Establishment• Renewable Energy• Energy & Resource

Efficiency• Liquid & Solid Waste

Management• Recycling &

Manufacturing of Recyclable Goods

• Environment-friendly Brick Production

• Occupational Health and Safety

Corporate

• Loan Against Deposits

• Flexible Term Deposit Package

• Regular Earner Package

• Deposit Pension Scheme

IDLC

FINA

NCE

LIM

ITED

17IDLC Finance Limited

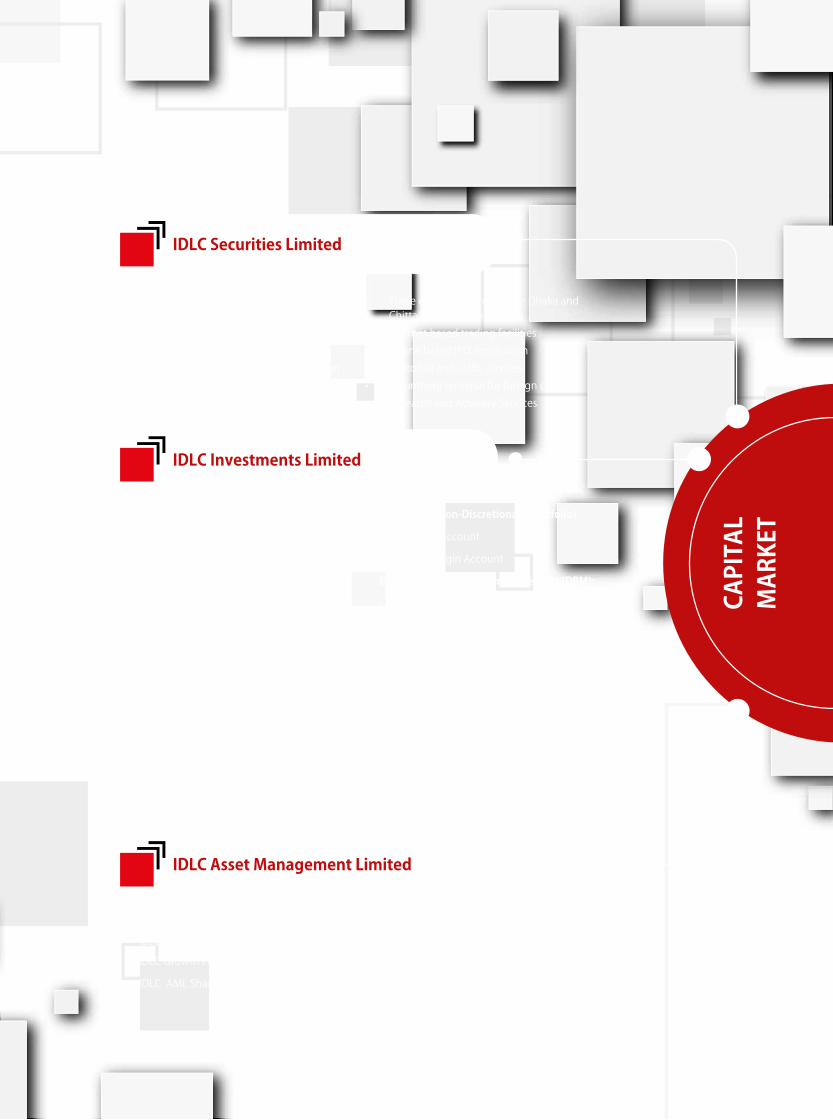

GOVERNANCE REPORTS & FINANCIAL STATEMENTS - IDLC REPORTS & FINANCIAL STATEMENTS - SUBSIDIARIES DISCLOSURES, CHECKLISTS & MISC.

Mutual Funds• IDLC Balanced Fund

• IDLC Growth Fund

• IDLC AML Shariah Fund

Alternate Investment Funds• IDLC Venture Capital Fund 1

Others• Corporate Advisory• Institutional Portfolio Management

• Cash Account• Margin Account • Easy IPO• Premium Brokerage for High Networth

Individuals (HNIs), Institutions and Foreign Investors

• Trade execution through the Dhaka and Chittagong stock exchanges

• Internet based trading facilities• Online based IPO Application• Custodial and CDBL services• Bloomberg terminal for foreign clients• Research and Advisory Services

Investment Banking Services :

• Initial Public Offering (IPO)

• Rights Issue Management

• Repeat Public Offering (RPO)

• Mergers & Acquisitions

• Corporate advisory

• Underwriting

• Arranging pre-IPO placement/ capital raising of forthcoming IPOs

• Substantial share acquisition and take over

• Valuation services for repatriation of sale proceeds of non-resident owned equity in unlisted companies

• Acting as trustee of bond issuances through private placement of debt securities

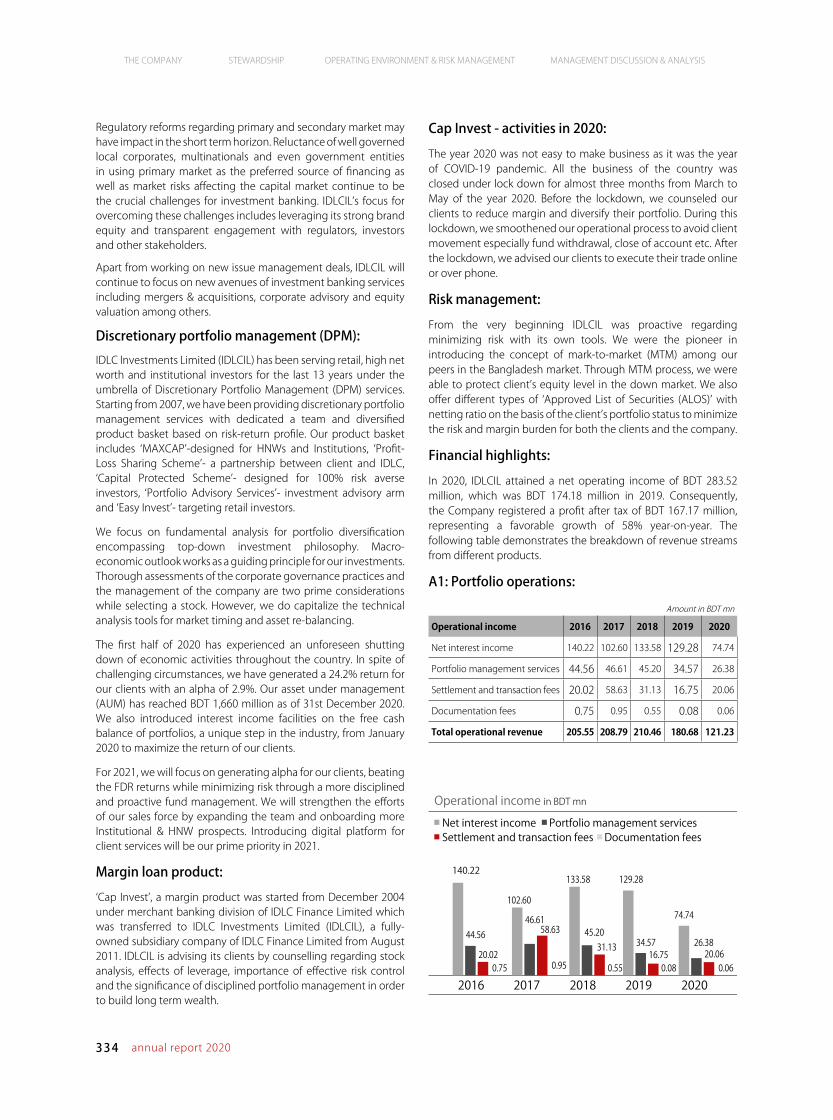

Cap-Invest (Non-Discretionary Portfolio)

• Margin Account

• Non-Margin Account

Discretionary portfolio management (DPM):

• MAXCAP

• Easy Invest

• Profit-Loss Sharing Scheme

• Capital Protected Scheme

• Portfolio Advisory Services

IDLC Asset Management Limited

CAPI

TAL

MAR

KET

IDLC Securities Limited

IDLC Investments Limited

18 annual report 2020

THE COMPANY STEWARDSHIP OPERATING ENVIRONMENT & RISK MANAGEMENT MANAGEMENT DISCUSSION & ANALYSIS

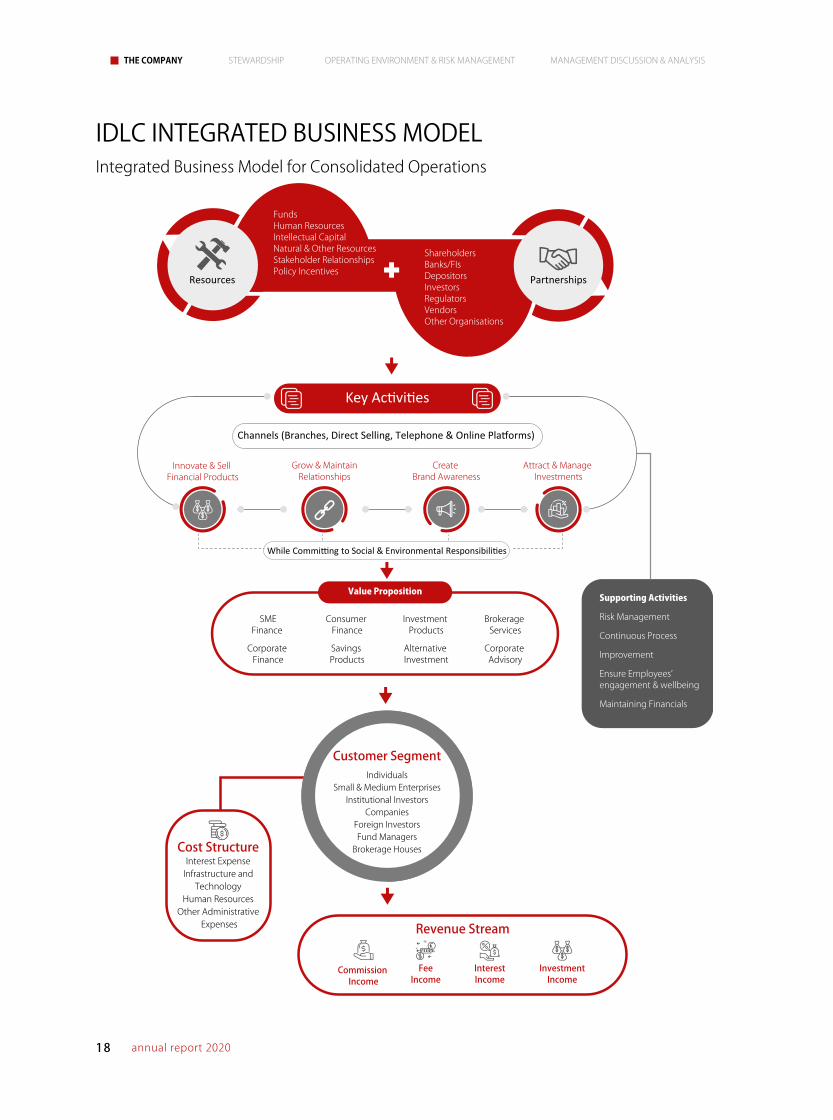

IDLC INTEGRATED BUSINESS MODELIntegrated Business Model for Consolidated Operations

Cost StructureInterest Expense

Infrastructure andTechnology

Human ResourcesOther Administrative

Expenses

ShareholdersBanks/FIsDepositorsInvestorsRegulatorsVendorsOther Organisations

FundsHuman ResourcesIntellectual CapitalNatural & Other ResourcesStakeholder RelationshipsPolicy Incentives

Value Proposition

Resources Partnerships

SMEFinance

Consumer Finance

Investment Products

Brokerage Services

Corporate Finance

Savings Products

Alternative Investment

Corporate Advisory

Key Ac�vi�es

Channels (Branches, Direct Selling, Telephone & Online Pla�orms)

Innovate & Sell Financial Products

Grow & MaintainRelationships

Create Brand Awareness

Attract & Manage Investments

While Commi�ng to Social & Environmental Responsibili�es

Supporting Activities

Risk Management

Continuous Process

Improvement

Ensure Employees’ engagement & wellbeing

Maintaining Financials

Customer SegmentIndividuals

Small & Medium EnterprisesInstitutional Investors

CompaniesForeign InvestorsFund Managers

Brokerage Houses

Commission Income

FeeIncome

InterestIncome

InvestmentIncome

Revenue Stream

19IDLC Finance Limited

GOVERNANCE REPORTS & FINANCIAL STATEMENTS - IDLC REPORTS & FINANCIAL STATEMENTS - SUBSIDIARIES DISCLOSURES, CHECKLISTS & MISC.

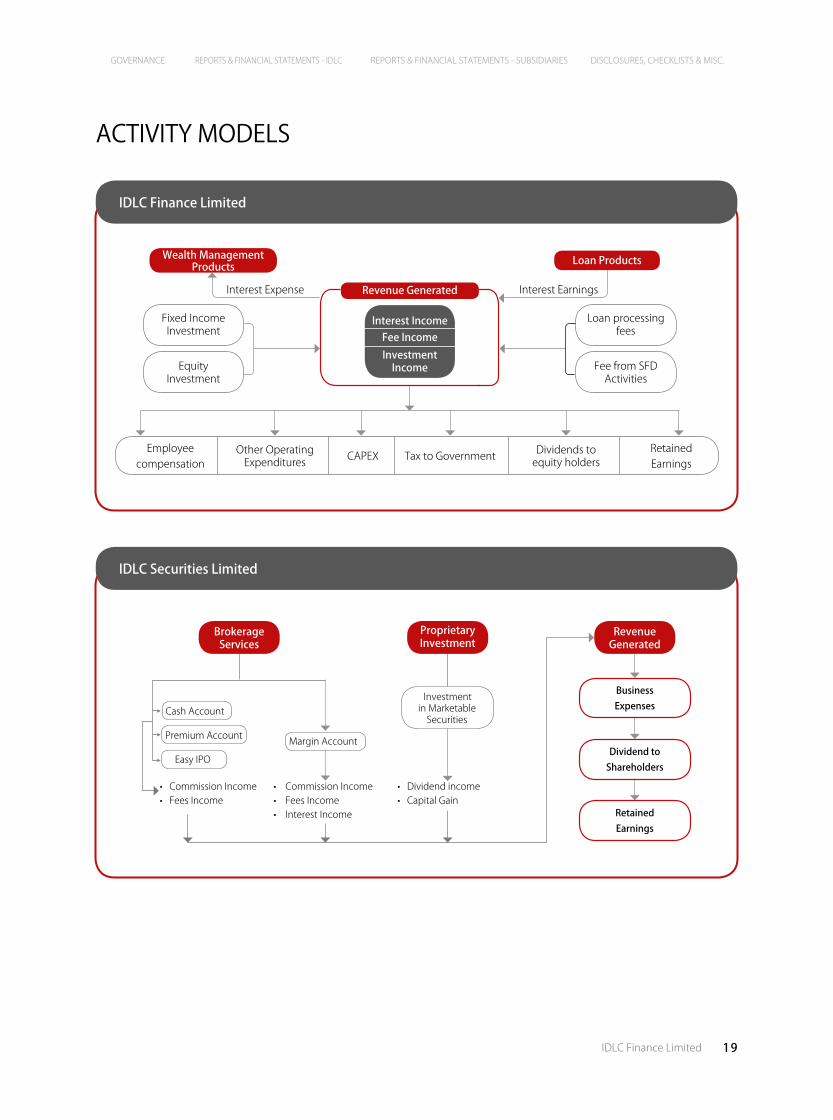

ACTIVITY MODELS

IDLC Finance Limited

IDLC Securities Limited

Interest IncomeFee IncomeInvestment

Income

Revenue GeneratedInterest Expense

Fixed Income Investment

Loan processing fees

Equity Investment

Fee from SFD Activities

Interest Earnings

Employeecompensation

RetainedEarnings

Dividends to equity holdersCAPEX Tax to GovernmentOther Operating

Expenditures

BrokerageServices

Proprietary Investment

Cash Account

Premium Account

Easy IPO

Margin Account

Investment in Marketable

Securities

• Commission Income• Fees Income

• Commission Income• Fees Income• Interest Income

• Dividend income• Capital Gain

Revenue Generated

Retained Earnings

Dividend to Shareholders

Business Expenses

Wealth Management Products Loan Products

20 annual report 2020

THE COMPANY STEWARDSHIP OPERATING ENVIRONMENT & RISK MANAGEMENT MANAGEMENT DISCUSSION & ANALYSIS

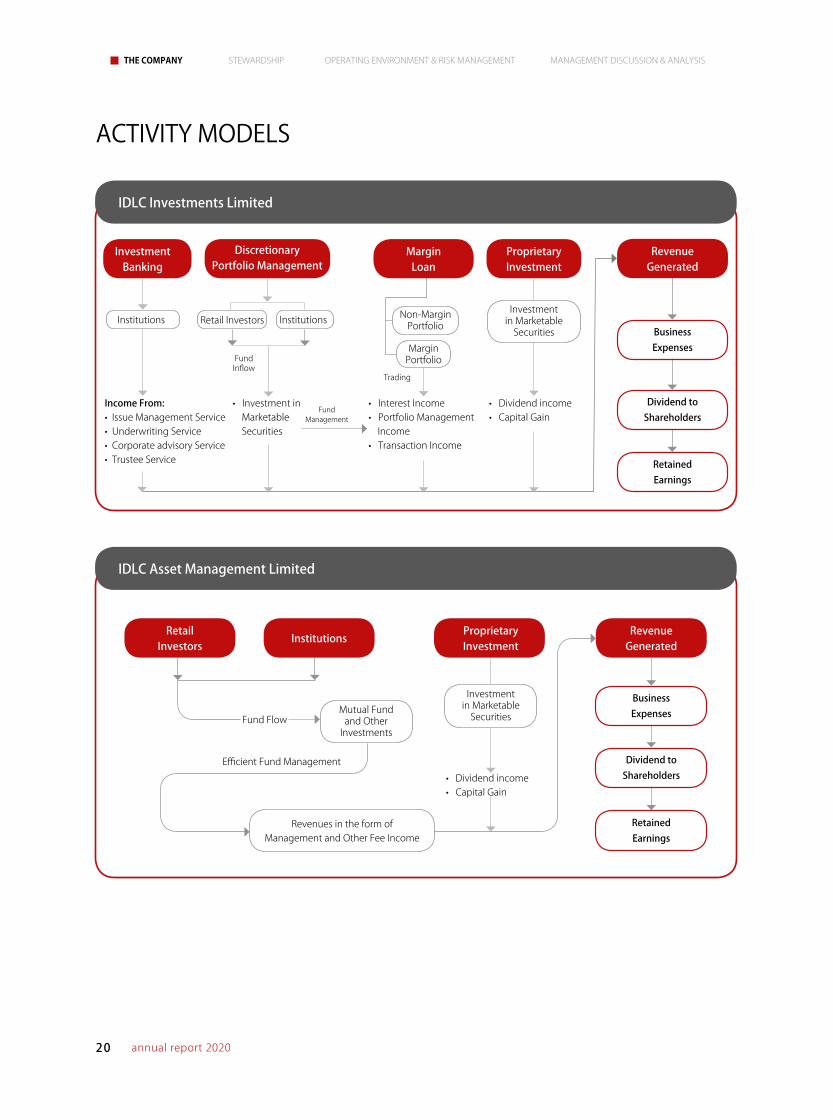

IDLC Investments Limited

IDLC Asset Management Limited

Investment Banking

Margin Loan

DiscretionaryPortfolio Management

Proprietary Investment

Retained Earnings

Dividend to Shareholders

Business Expenses

Revenue Generated

• Dividend income• Capital Gain

• Dividend income• Capital Gain

Income From:• Issue Management Service• Underwriting Service• Corporate advisory Service• Trustee Service

• Investment in Marketable Securities

Fund Management

• Interest Income• Portfolio Management Income• Transaction Income

Institutions Retail Investors InstitutionsInvestment

in Marketable Securities

Investment in Marketable

Securities

Non-Margin Portfolio

Margin PortfolioFund

InflowTrading

Fund FlowMutual Fund

and Other Investments

Revenues in the form ofManagement and Other Fee Income

Efficient Fund Management

Retained Earnings

Dividend to Shareholders

Business Expenses

Revenue Generated

Retail Investors

Institutions

ACTIVITY MODELS

Proprietary Investment

21IDLC Finance Limited

GOVERNANCE REPORTS & FINANCIAL STATEMENTS - IDLC REPORTS & FINANCIAL STATEMENTS - SUBSIDIARIES DISCLOSURES, CHECKLISTS & MISC.

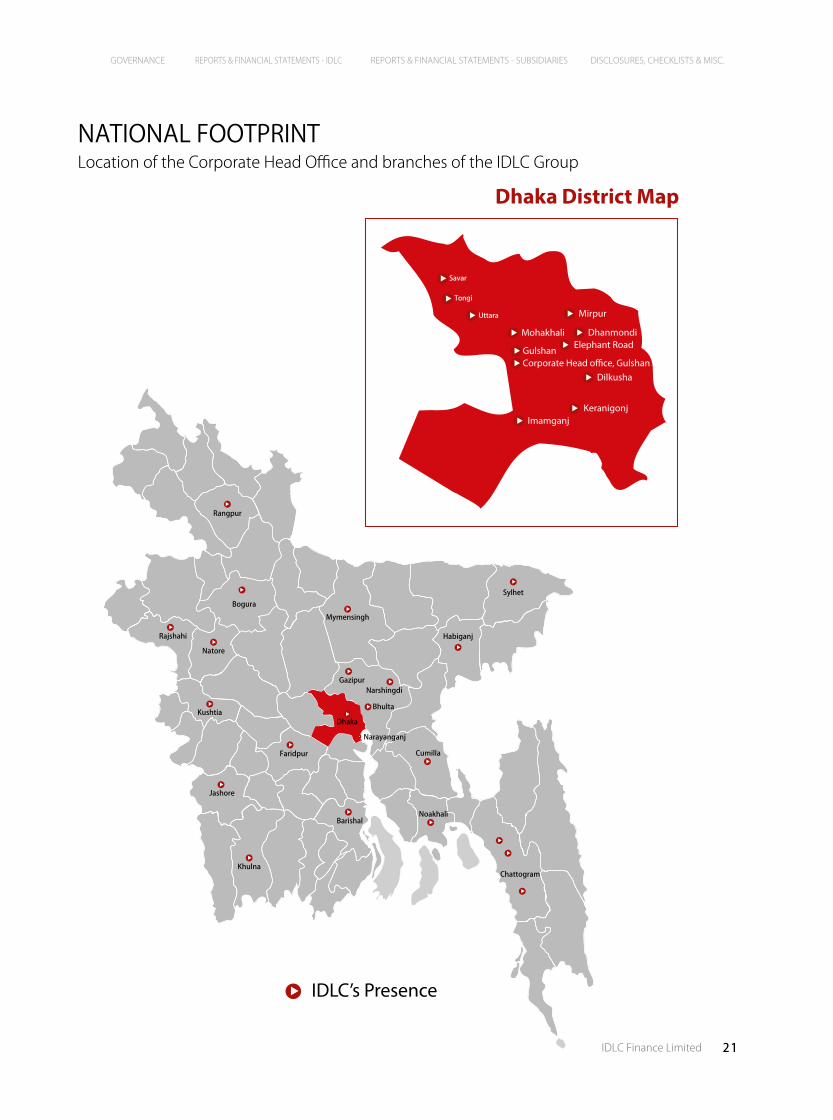

NATIONAL FOOTPRINTLocation of the Corporate Head Office and branches of the IDLC Group

IDLC’s Presence

Dhaka District Map

Bhulta

Narshingdi

Bogura

Rangpur

Mymensingh

Gazipur

Narayanganj

Chattogram

Jashore

Khulna

Barishal

Faridpur Cumilla

Noakhali

Natore

Rajshahi

Kushtia

Sylhet

Habiganj

Tongi

Uttara

Gulshan

Mohakhali

Corporate Head o�ce, Gulshan

Mirpur

DhanmondiElephant Road

Dilkusha

KeranigonjImamganj

Savar

Dhaka

THE COMPANY STEWARDSHIP OPERATING ENVIRONMENT & RISK MANAGEMENT MANAGEMENT DISCUSSION & ANALYSIS

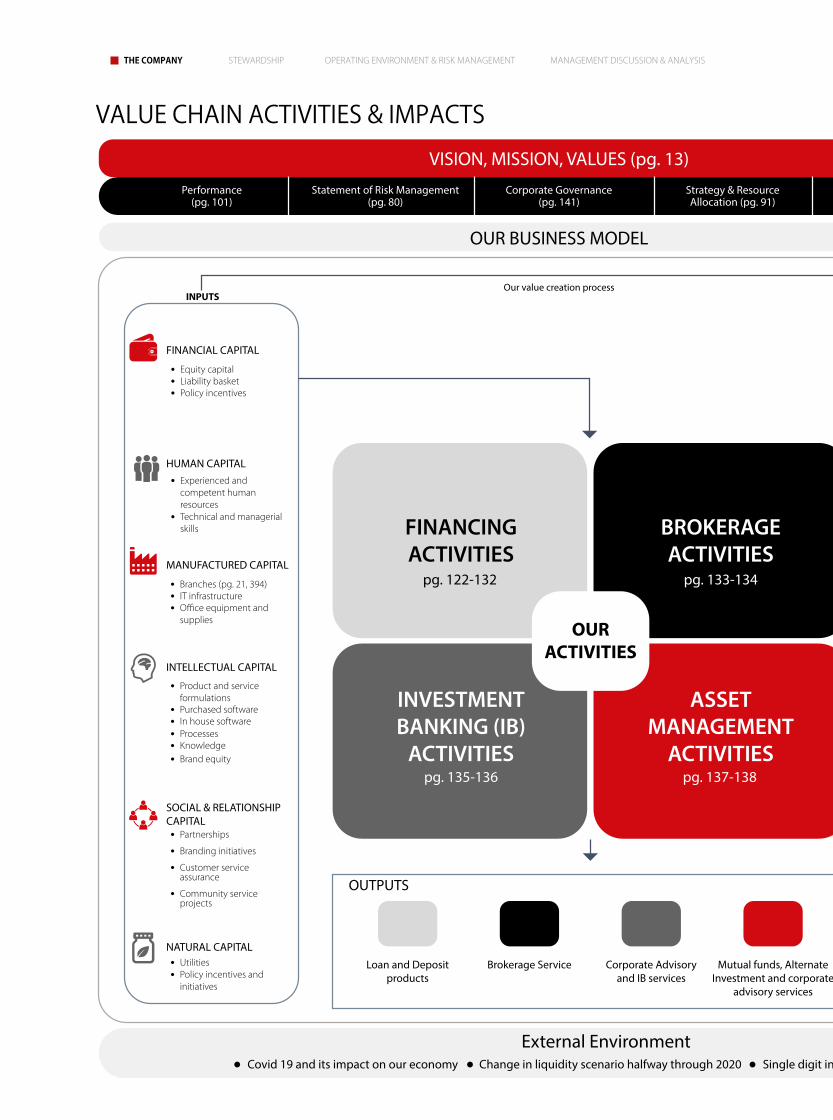

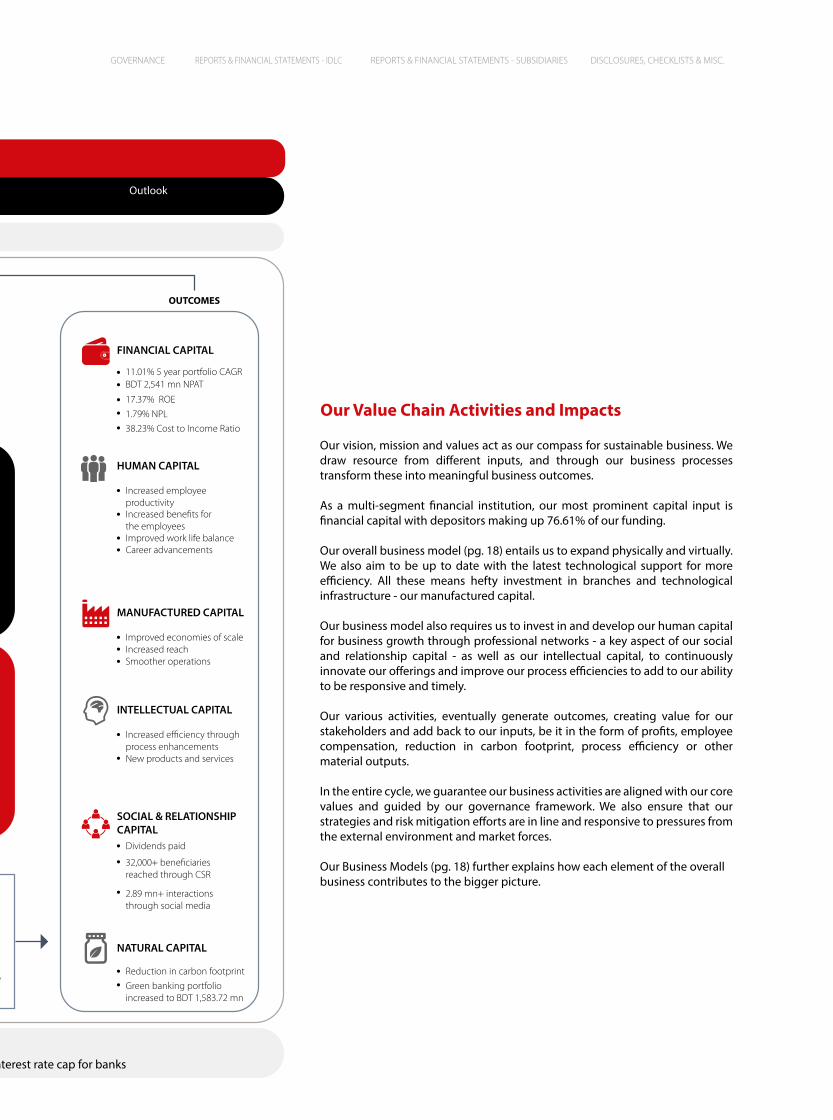

Our Value Chain Activities and Impacts

Our vision, mission and values act as our compass for sustainable business. We draw resource from di�erent inputs, and through our business processes transform these into meaningful business outcomes.

As a multi-segment �nancial institution, our most prominent capital input is �nancial capital with depositors making up 76.61% of our funding.

Our overall business model (pg. 18) entails us to expand physically and virtually. We also aim to be up to date with the latest technological support for more e�ciency. All these means hefty investment in branches and technological infrastructure - our manufactured capital.

Our business model also requires us to invest in and develop our human capital for business growth through professional networks - a key aspect of our social and relationship capital - as well as our intellectual capital, to continuously innovate our o�erings and improve our process e�ciencies to add to our ability to be responsive and timely.

Our various activities, eventually generate outcomes, creating value for our stakeholders and add back to our inputs, be it in the form of pro�ts, employee compensation, reduction in carbon footprint, process e�ciency or other material outputs.

In the entire cycle, we guarantee our business activities are aligned with our core values and guided by our governance framework. We also ensure that our strategies and risk mitigation e�orts are in line and responsive to pressures from the external environment and market forces.

Our Business Models (pg. 18) further explains how each element of the overall business contributes to the bigger picture.

FINANCINGACTIVITIES

pg. 122-132

BROKERAGE ACTIVITIES

pg. 133-134

ASSET MANAGEMENT

ACTIVITIESpg. 137-138

INVESTMENT BANKING (IB)

ACTIVITIESpg. 135-136

OURACTIVITIES

OUTPUTS

Loan and Deposit products

Corporate Advisory and IB services

Mutual funds, Alternate Investment and corporate

advisory services

Brokerage Service

FINANCIAL CAPITAL

Equity capitalLiability basketPolicy incentives

MANUFACTURED CAPITAL

Branches (pg. 21, 394)IT infrastructureO�ce equipment andsupplies

NATURAL CAPITALUtilitiesPolicy incentives andinitiatives

INTELLECTUAL CAPITAL

Product and serviceformulationsPurchased softwareIn house softwareProcessesKnowledge

SOCIAL & RELATIONSHIPCAPITAL

Brand equity

Partnerships

Branding initiatives

Customer serviceassurance

Community serviceprojects

FINANCIAL CAPITAL

11.01% 5 year portfolio CAGRBDT 2,541 mn NPAT

17.37% ROE1.79% NPL38.23% Cost to Income Ratio

MANUFACTURED CAPITAL

Improved economies of scaleIncreased reachSmoother operations

SOCIAL & RELATIONSHIPCAPITAL

Dividends paid

32,000+ bene�ciariesreached through CSR

2.89 mn+ interactionsthrough social media

NATURAL CAPITAL

Reduction in carbon footprintGreen banking portfolioincreased to BDT 1,583.72 mn

INTELLECTUAL CAPITAL

Increased e�ciency throughprocess enhancementsNew products and services

INPUTS OUTCOMES

VISION, MISSION, VALUES (pg. 13)

OUR BUSINESS MODEL

External Environment

Performance (pg. 101)

Statement of Risk Management(pg. 80)

Corporate Governance(pg. 141)

Strategy & ResourceAllocation (pg. 91)

Outlook

Our value creation process

Covid 19 and its impact on our economy Change in liquidity scenario halfway through 2020 Single digit interest rate cap for banks

HUMAN CAPITALExperienced andcompetent humanresourcesTechnical and managerialskills

HUMAN CAPITAL

Increased employeeproductivityIncreased bene�ts for the employeesImproved work life balanceCareer advancements

VALUE CHAIN ACTIVITIES & IMPACTS

GOVERNANCE REPORTS & FINANCIAL STATEMENTS - IDLC REPORTS & FINANCIAL STATEMENTS - SUBSIDIARIES DISCLOSURES, CHECKLISTS & MISC.

Our Value Chain Activities and Impacts

Our vision, mission and values act as our compass for sustainable business. We draw resource from di�erent inputs, and through our business processes transform these into meaningful business outcomes.

As a multi-segment �nancial institution, our most prominent capital input is �nancial capital with depositors making up 76.61% of our funding.

Our overall business model (pg. 18) entails us to expand physically and virtually. We also aim to be up to date with the latest technological support for more e�ciency. All these means hefty investment in branches and technological infrastructure - our manufactured capital.

Our business model also requires us to invest in and develop our human capital for business growth through professional networks - a key aspect of our social and relationship capital - as well as our intellectual capital, to continuously innovate our o�erings and improve our process e�ciencies to add to our ability to be responsive and timely.

Our various activities, eventually generate outcomes, creating value for our stakeholders and add back to our inputs, be it in the form of pro�ts, employee compensation, reduction in carbon footprint, process e�ciency or other material outputs.

In the entire cycle, we guarantee our business activities are aligned with our core values and guided by our governance framework. We also ensure that our strategies and risk mitigation e�orts are in line and responsive to pressures from the external environment and market forces.

Our Business Models (pg. 18) further explains how each element of the overall business contributes to the bigger picture.

FINANCINGACTIVITIES

pg. 122-132

BROKERAGE ACTIVITIES

pg. 133-134

ASSET MANAGEMENT

ACTIVITIESpg. 137-138

INVESTMENT BANKING (IB)

ACTIVITIESpg. 135-136

OURACTIVITIES

OUTPUTS

Loan and Deposit products

Corporate Advisory and IB services

Mutual funds, Alternate Investment and corporate

advisory services

Brokerage Service

FINANCIAL CAPITAL

Equity capitalLiability basketPolicy incentives

MANUFACTURED CAPITAL

Branches (pg. 21, 394)IT infrastructureO�ce equipment andsupplies

NATURAL CAPITALUtilitiesPolicy incentives andinitiatives

INTELLECTUAL CAPITAL

Product and serviceformulationsPurchased softwareIn house softwareProcessesKnowledge

SOCIAL & RELATIONSHIPCAPITAL

Brand equity

Partnerships

Branding initiatives

Customer serviceassurance

Community serviceprojects

FINANCIAL CAPITAL

11.01% 5 year portfolio CAGRBDT 2,541 mn NPAT

17.37% ROE1.79% NPL38.23% Cost to Income Ratio

MANUFACTURED CAPITAL

Improved economies of scaleIncreased reachSmoother operations

SOCIAL & RELATIONSHIPCAPITAL

Dividends paid

32,000+ bene�ciariesreached through CSR

2.89 mn+ interactionsthrough social media

NATURAL CAPITAL

Reduction in carbon footprintGreen banking portfolioincreased to BDT 1,583.72 mn

INTELLECTUAL CAPITAL

Increased e�ciency throughprocess enhancementsNew products and services

INPUTS OUTCOMES

VISION, MISSION, VALUES (pg. 13)

OUR BUSINESS MODEL

External Environment

Performance (pg. 101)

Statement of Risk Management(pg. 80)

Corporate Governance(pg. 141)

Strategy & ResourceAllocation (pg. 91)

Outlook

Our value creation process

Covid 19 and its impact on our economy Change in liquidity scenario halfway through 2020 Single digit interest rate cap for banks

HUMAN CAPITALExperienced andcompetent humanresourcesTechnical and managerialskills

HUMAN CAPITAL

Increased employeeproductivityIncreased bene�ts for the employeesImproved work life balanceCareer advancements

24 annual report 2020

THE COMPANY STEWARDSHIP OPERATING ENVIRONMENT & RISK MANAGEMENT MANAGEMENT DISCUSSION & ANALYSIS

COM

MUN

ITY

C

USTO

MERS

SHAREHOLDERS

REGULATORS SUPPLIES

EMPLOYER

ENVIRONMENT

Lend

mon

ey to

clien

ts, re

ceive

fund

s from

indiv

iduals

and i

nstit

ution

s, mak

einve

stmen

ts, m

anag

e cred

it risk

,

and p

rovid

e syn

dicati

on an

d age

ncy s

ervice

s

Lend money to clients, receive funds from individuals

and institutions, make investments, manage credit

risk, and provide syndication and agency services

Provide merchant banking services, manage portfolios

Provide brokerage services, Produce sell-side research,

Offer margin loans

ACTIVITIESKEYCore

Fina

ncing

Asset Management Investment Banking

Brokerage

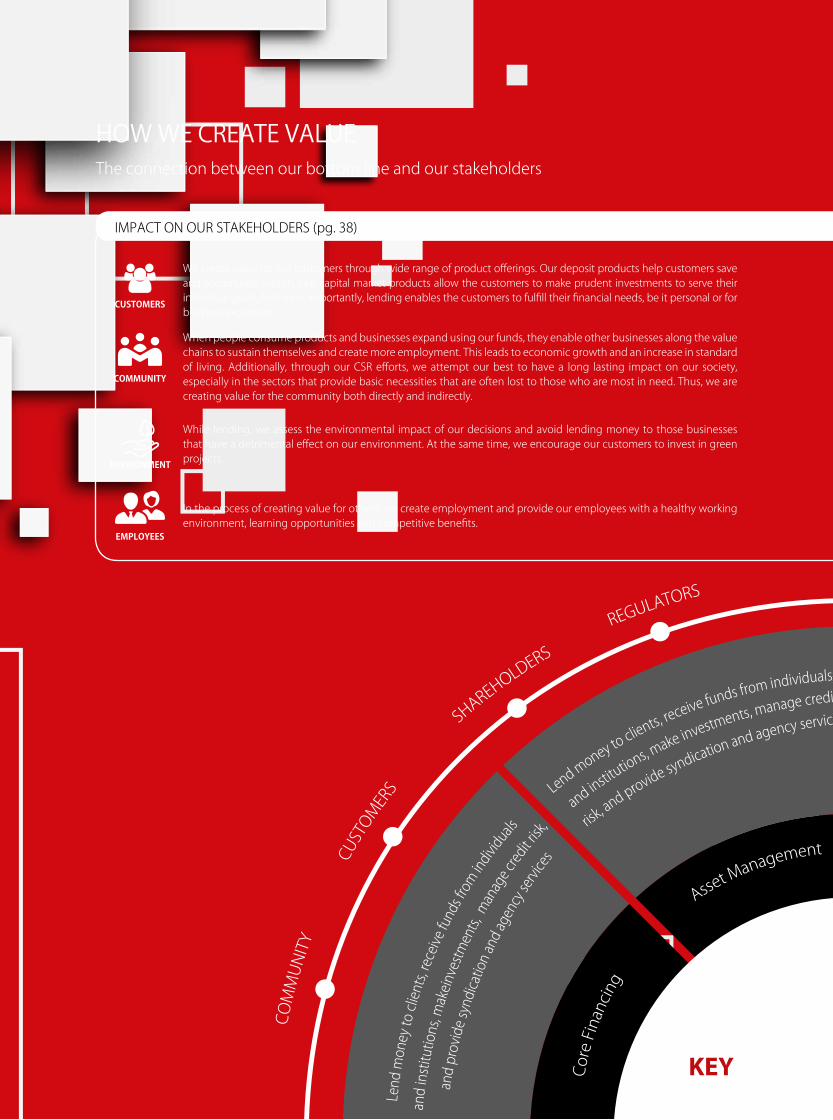

HOW WE CREATE VALUE The connection between our bottom line and our stakeholders

IMPACT ON OUR STAKEHOLDERS (pg. 38)

CUSTOMERS

We create value for our customers through wide range of product offerings. Our deposit products help customers save and accumulate wealth. Our capital market products allow the customers to make prudent investments to serve their individual goals. And most importantly, lending enables the customers to fulfill their financial needs, be it personal or for business expansion.

When people consume products and businesses expand using our funds, they enable other businesses along the value chains to sustain themselves and create more employment. This leads to economic growth and an increase in standard of living. Additionally, through our CSR efforts, we attempt our best to have a long lasting impact on our society, especially in the sectors that provide basic necessities that are often lost to those who are most in need. Thus, we are creating value for the community both directly and indirectly.

While lending, we assess the environmental impact of our decisions and avoid lending money to those businesses that have a detrimental effect on our environment. At the same time, we encourage our customers to invest in green projects.

In the process of creating value for others, we create employment and provide our employees with a healthy working environment, learning opportunities and competitive benefits.

EMPLOYEES

COMMUNITY

ENVIRONMENT

25IDLC Finance Limited

GOVERNANCE REPORTS & FINANCIAL STATEMENTS - IDLC REPORTS & FINANCIAL STATEMENTS - SUBSIDIARIES DISCLOSURES, CHECKLISTS & MISC.

COM

MUN

ITY

C

USTO

MERS

SHAREHOLDERS

REGULATORS SUPPLIES

EMPLOYER

ENVIRONMENT

Lend

mon

ey to

clien

ts, re

ceive

fund

s from

indiv

iduals

and i

nstit

ution

s, mak

einve

stmen

ts, m

anag

e cred

it risk

,

and p

rovid

e syn

dicati

on an

d age

ncy s

ervice

s

Lend money to clients, receive funds from individuals

and institutions, make investments, manage credit

risk, and provide syndication and agency services

Provide merchant banking services, manage portfolios

Provide brokerage services, Produce sell-side research,

Offer margin loans

ACTIVITIESKEYCore

Fina

ncing

Asset Management Investment Banking

Brokerage

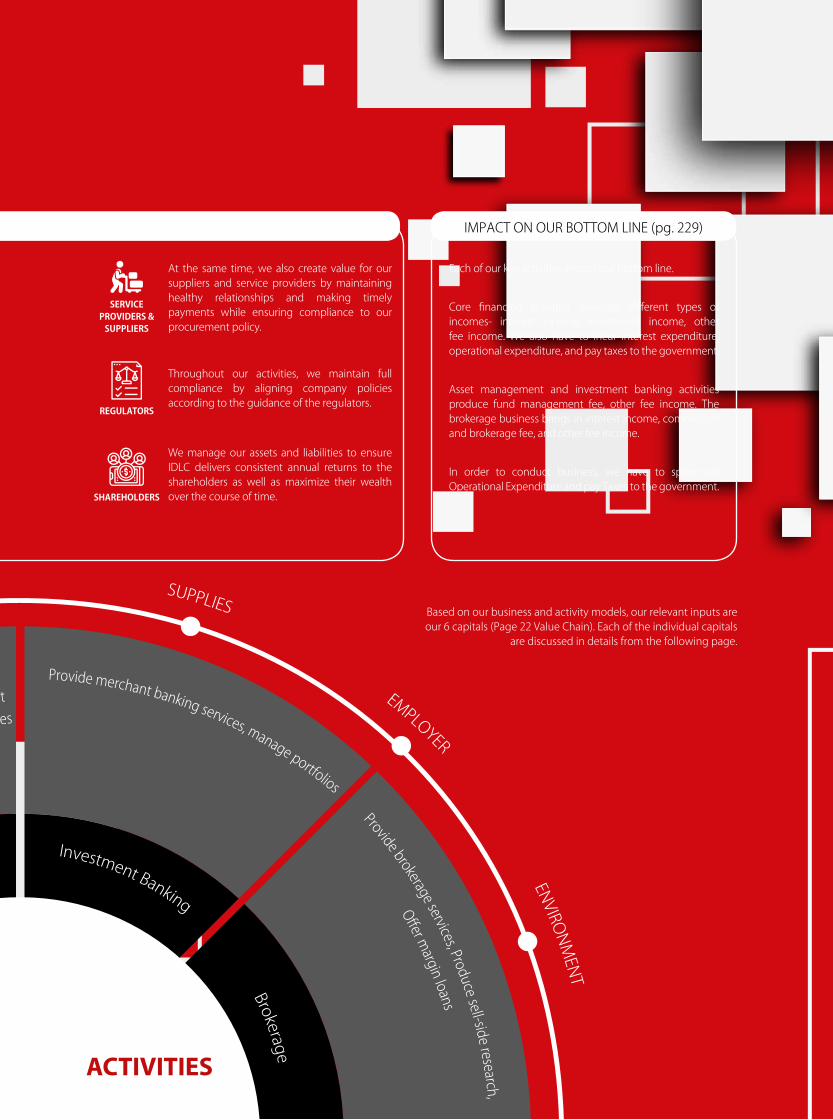

IMPACT ON OUR BOTTOM LINE (pg. 229)

Each of our key activities impact our bottom line.

Core financing activities generate different types of incomes- interest income, investment income, other fee income. We also have to incur interest expenditure, operational expenditure, and pay taxes to the government.

Asset management and investment banking activities produce fund management fee, other fee income. The brokerage business brings in interest income, commission and brokerage fee, and other fee income.

In order to conduct business, we have to spend on Operational Expenditure and pay Taxes to the government.

SERVICE PROVIDERS &

SUPPLIERS

REGULATORS

SHAREHOLDERS

At the same time, we also create value for our suppliers and service providers by maintaining healthy relationships and making timely payments while ensuring compliance to our procurement policy.

Throughout our activities, we maintain full compliance by aligning company policies according to the guidance of the regulators.

We manage our assets and liabilities to ensure IDLC delivers consistent annual returns to the shareholders as well as maximize their wealth over the course of time.

Based on our business and activity models, our relevant inputs are our 6 capitals (Page 22 Value Chain). Each of the individual capitals

are discussed in details from the following page.

26 annual report 2020

THE COMPANY STEWARDSHIP OPERATING ENVIRONMENT & RISK MANAGEMENT MANAGEMENT DISCUSSION & ANALYSIS

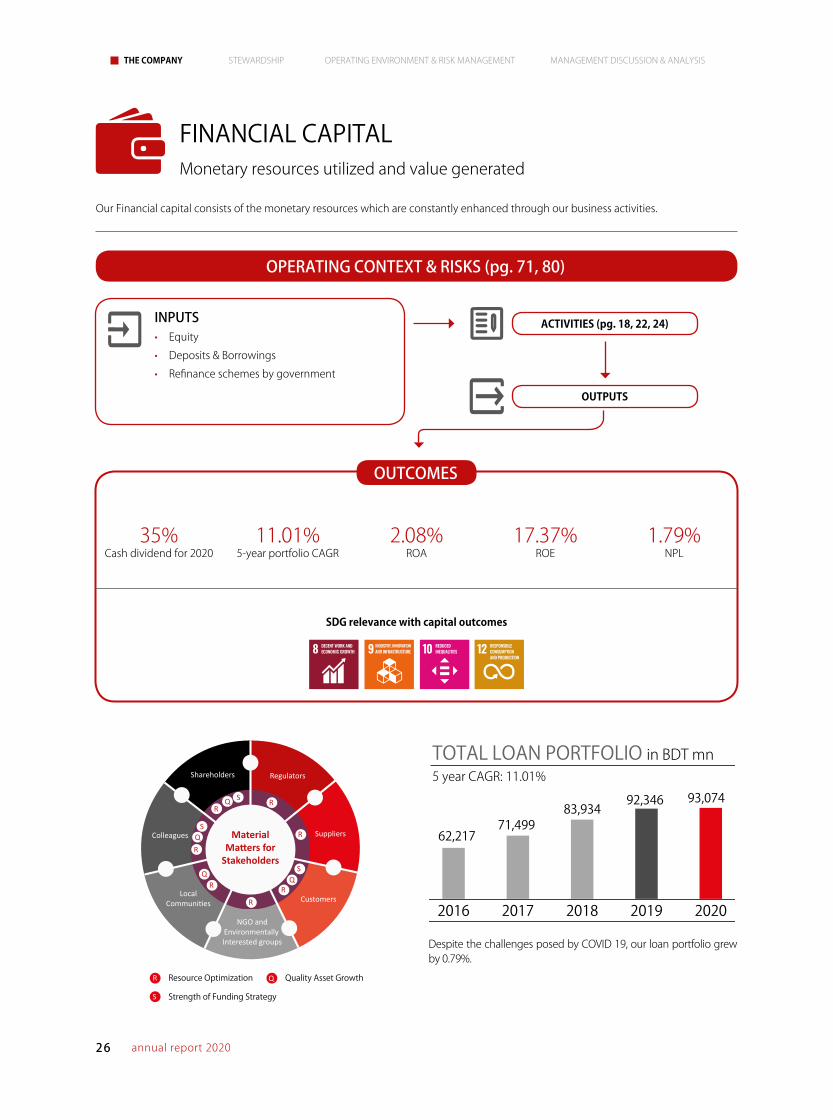

FINANCIAL CAPITALMonetary resources utilized and value generated

Our Financial capital consists of the monetary resources which are constantly enhanced through our business activities.

OPERATING CONTEXT & RISKS (pg. 71, 80)

ACTIVITIES (pg. 18, 22, 24)

OUTPUTS

35%Cash dividend for 2020

11.01%5-year portfolio CAGR

2.08%ROA

17.37%ROE

1.79%NPL

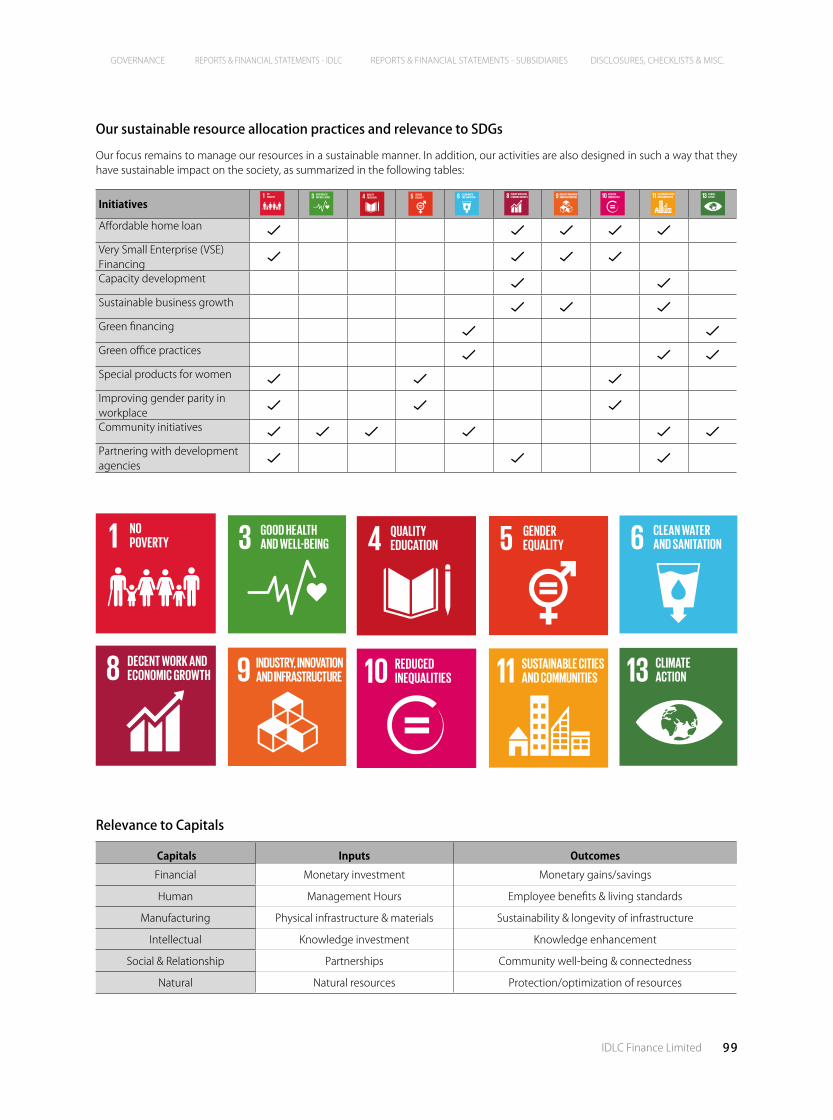

SDG relevance with capital outcomes

INPUTS• Equity

• Deposits & Borrowings

• Refinance schemes by government

OUTCOMES

QR Resource Optimization Quality Asset Growth

S Strength of Funding Strategy

Shareholders Regulators

SuppliersMaterialMatters for

Stakeholders

CustomersLocal

Communi�es

NGO andEnvironmentally Interested groups

Colleagues

RQ

SQ

R

R

R

R

RQ

S

RQ S

Despite the challenges posed by COVID 19, our loan portfolio grew by 0.79%.

TOTAL LOAN PORTFOLIO in BDT mn

2016 2017 2018 2019 2020

5 year CAGR: 11.01%

62,217 71,499

83,934 92,346 93,074

27IDLC Finance Limited

GOVERNANCE REPORTS & FINANCIAL STATEMENTS - IDLC REPORTS & FINANCIAL STATEMENTS - SUBSIDIARIES DISCLOSURES, CHECKLISTS & MISC.

Challenges Responses

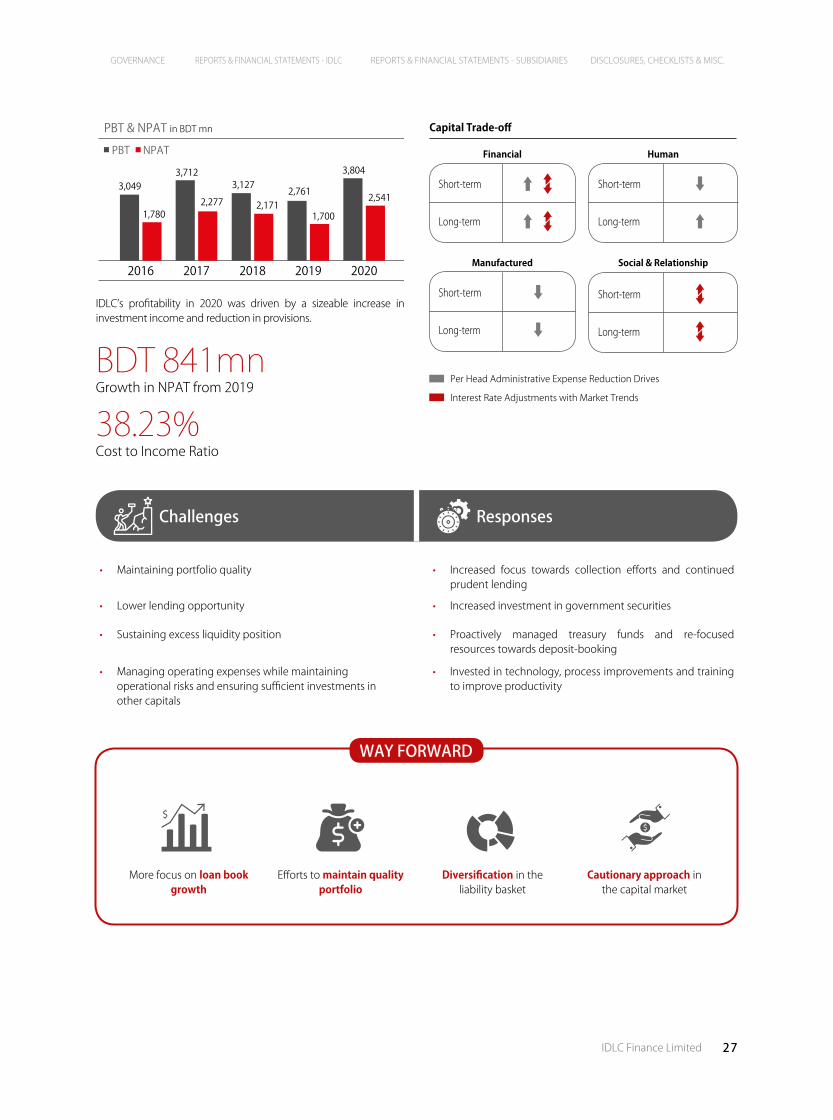

IDLC’s profitability in 2020 was driven by a sizeable increase in investment income and reduction in provisions.

More focus on loan book growth

Efforts to maintain quality portfolio

Diversification in the liability basket

Cautionary approach in the capital market

WAY FORWARD

PBT & NPAT in BDT mn

2016 2017 2018 2019 2020

3,049 3,712

3,127 2,761

3,804

1,780 2,277 2,171

1,700

2,541

PBT NPAT

BDT 841mnGrowth in NPAT from 2019

38.23%Cost to Income Ratio

Per Head Administrative Expense Reduction Drives

Interest Rate Adjustments with Market Trends

Capital Trade-off

Financial Human

Short-term Short-term

Long-term Long-term

Social & Relationship

Short-term

Long-term

Manufactured

Short-term

Long-term

• Maintaining portfolio quality • Increased focus towards collection efforts and continued prudent lending

• Lower lending opportunity • Increased investment in government securities

• Sustaining excess liquidity position • Proactively managed treasury funds and re-focused resources towards deposit-booking

• Managing operating expenses while maintaining operational risks and ensuring sufficient investments in other capitals

• Invested in technology, process improvements and training to improve productivity

28 annual report 2020

THE COMPANY STEWARDSHIP OPERATING ENVIRONMENT & RISK MANAGEMENT MANAGEMENT DISCUSSION & ANALYSIS

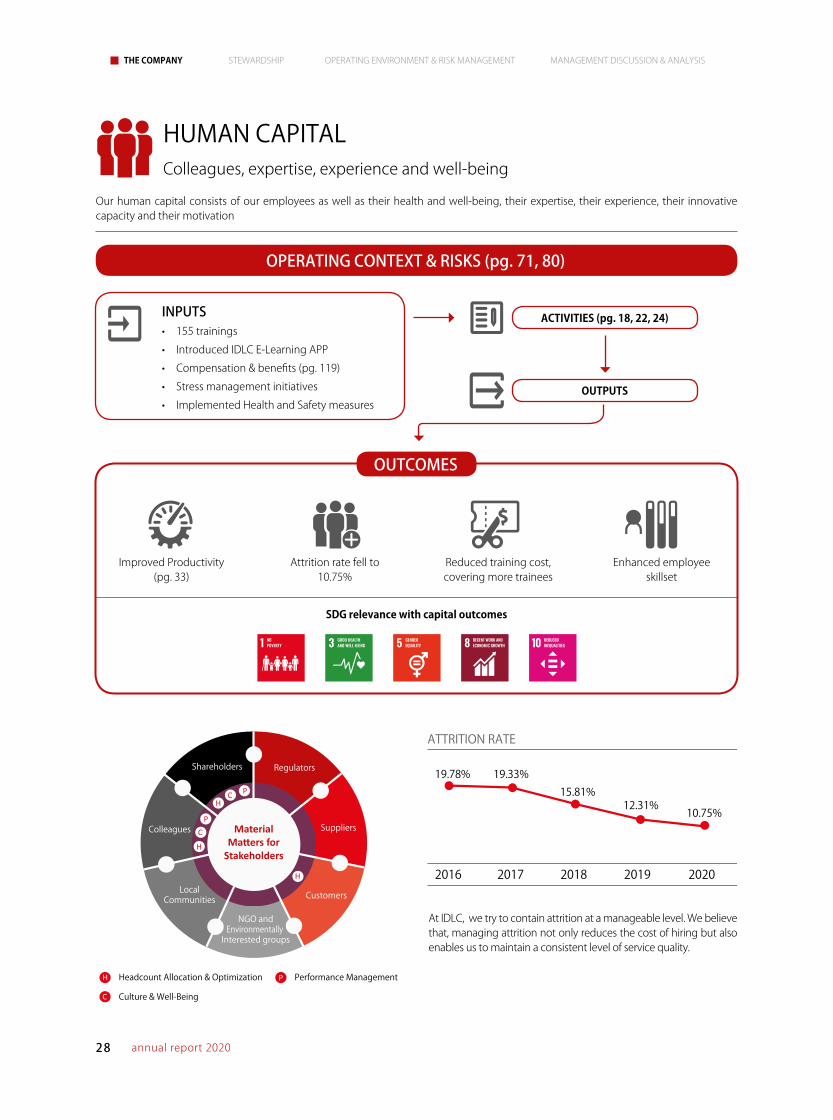

HUMAN CAPITAL Colleagues, expertise, experience and well-being

Our human capital consists of our employees as well as their health and well-being, their expertise, their experience, their innovative capacity and their motivation

OPERATING CONTEXT & RISKS (pg. 71, 80)

ACTIVITIES (pg. 18, 22, 24)

OUTPUTS

Improved Productivity (pg. 33)

Attrition rate fell to 10.75%

Reduced training cost, covering more trainees

Enhanced employee skillset

SDG relevance with capital outcomes

INPUTS• 155 trainings

• Introduced IDLC E-Learning APP

• Compensation & benefits (pg. 119)

• Stress management initiatives

• Implemented Health and Safety measures

OUTCOMES

Shareholders Regulators

SuppliersMaterialMatters for

Stakeholders

CustomersLocalCommunities

NGO andEnvironmentally

Interested groups

Colleagues

H

H

CP

HC P

PH Headcount Allocation & Optimization Performance Management

C Culture & Well-Being

At IDLC, we try to contain attrition at a manageable level. We believe that, managing attrition not only reduces the cost of hiring but also enables us to maintain a consistent level of service quality.

ATTRITION RATE

2016

19.78% 19.33%15.81%

12.31% 10.75%

2017 2018 2019 2020

29IDLC Finance Limited

GOVERNANCE REPORTS & FINANCIAL STATEMENTS - IDLC REPORTS & FINANCIAL STATEMENTS - SUBSIDIARIES DISCLOSURES, CHECKLISTS & MISC.

Build Managerial capabilities to lead more

effectively with coaching & feedback tools

Improving the evaluation process to strengthen the talent recruitment process

Use technology to automate HR Processes

Focus more on individual career plans to develop

the right resources for the right roles

WAY FORWARD

Core Management

Senior Level Management

Mid-Level Management

Junior Level Management

EMPLOYEE SPREAD6%

14%

78%

2%

Training

Increments in compensation & benefits

New Hires

Capital Trade-off

Financial

Intellectual

Human

Social & Relationship

Short-term

Short-term Short-term

Long-term

Long-term

Long-term

Long-term

Short-term

Challenges Responses

• COVID-19 pandemic and health and safety of the employees • Introduced work from home initiatives to ensure health and safety of the employees

• Employee morale and mental health during the pandemic. • Introduced employee health portal and rigorously tracked employee health to maintain a safe environment.

• Enhance employee talents through need base training, coaching and e-learning

• Organized mental health awareness and counselling session for all employees to enhance mental health of employees and boost employee morale.

• Reducing attrition rate & ensuring retention of talent through a culture where people are driven towards achieving personal as well as business goals and objectives

• Supporting the career development plans of all the employees and focus on providing the right training to the right personnel

30 annual report 2020

THE COMPANY STEWARDSHIP OPERATING ENVIRONMENT & RISK MANAGEMENT MANAGEMENT DISCUSSION & ANALYSIS

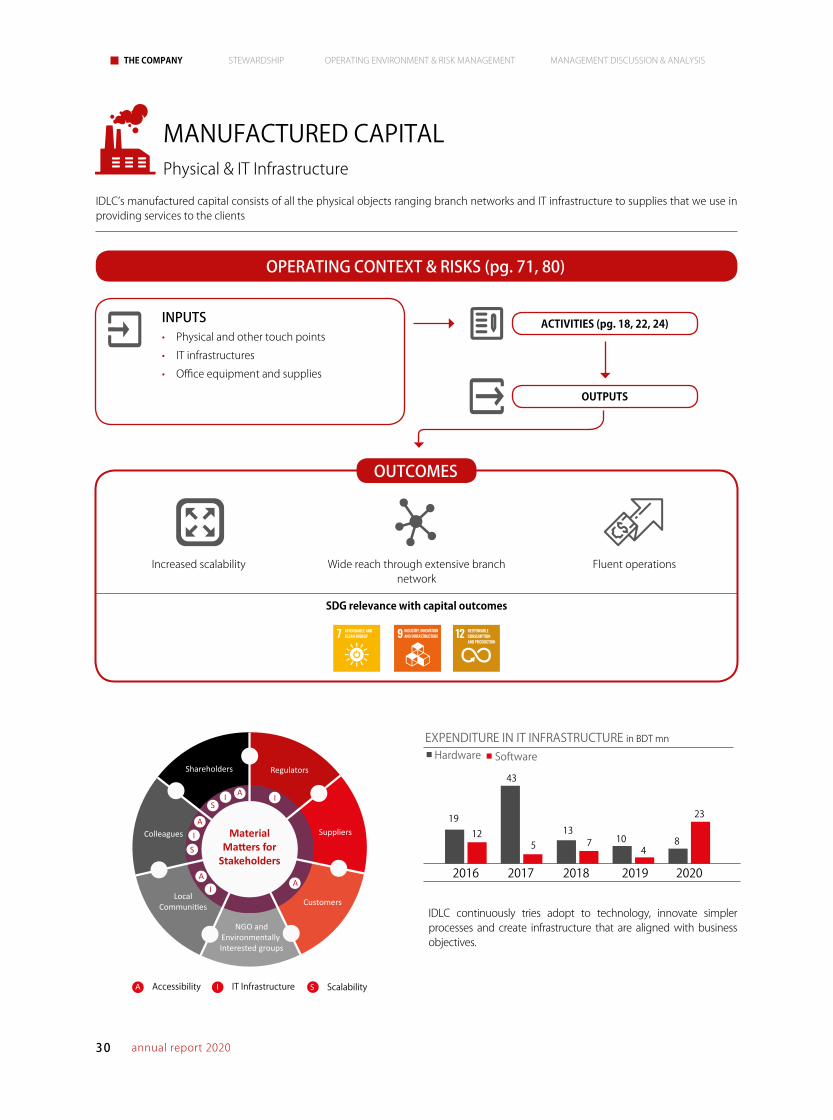

MANUFACTURED CAPITALPhysical & IT Infrastructure

IDLC’s manufactured capital consists of all the physical objects ranging branch networks and IT infrastructure to supplies that we use in providing services to the clients

OPERATING CONTEXT & RISKS (pg. 71, 80)

ACTIVITIES (pg. 18, 22, 24)

OUTPUTS

Increased scalability Wide reach through extensive branch network

Fluent operations

SDG relevance with capital outcomes

INPUTS• Physical and other touch points

• IT infrastructures

• Office equipment and supplies

IDLC continuously tries adopt to technology, innovate simpler processes and create infrastructure that are aligned with business objectives.

IA Accessibility IT Infrastructure S Scalability

Shareholders Regulators

SuppliersMaterialMatters for

Stakeholders

CustomersLocal

Communi�es

NGO andEnvironmentally Interested groups

Colleagues

A

S

IA

IA

SI A I

EXPENDITURE IN IT INFRASTRUCTURE in BDT mn

2016 2017 2018 2019 2020

Hardware Software

19

43

13 10 8

12 5 7

4

23

OUTCOMES

31IDLC Finance Limited

GOVERNANCE REPORTS & FINANCIAL STATEMENTS - IDLC REPORTS & FINANCIAL STATEMENTS - SUBSIDIARIES DISCLOSURES, CHECKLISTS & MISC.

Enhance our accessibility by increasing both geographical and

virtual presence

Extend infrastructure to meet upcoming business needs

Improve process efficiencies to improve utilization of manufactured

capitals

WAY FORWARD

The accessibility network is designed keeping the opportunities, need for proximity to the clients and cost effectiveness in mind. Currently, we are operating from 41 physical touch points across the nation.

IDLC also maintains strong virtual presence in social media. Furthermore, it has dedicated hotlines to deal with customer requests and grievances round the clock.

Rental Expense in BDT mn

2016 2017 2018 2019 2020

163 166

170

184 186

Capital Trade-off

Financial

Intellectual

Manufactured

Social & Relationship

Short-term

Short-term Short-term

Long-term

Long-term

Long-term

Long-term

Short-term

Investment in servers

Branch Expansion

Security measures against possible Intellectual property damage

Challenges Responses

• Ensuring infrastructure adequacy to align with growth ambitions

• Made strategic investments in network expansion

• Finding the right balance in costs & benefits • Conducted regular cost benefit analysis by competent personnel

• Evolving technological needs and timing of investments • Consulted local and international consultants to be updated with best practices

• Ensure timely delivery of services • Maintained/updated systems according to technology and process audits for quick adoption and improvisation

32 annual report 2020

THE COMPANY STEWARDSHIP OPERATING ENVIRONMENT & RISK MANAGEMENT MANAGEMENT DISCUSSION & ANALYSIS

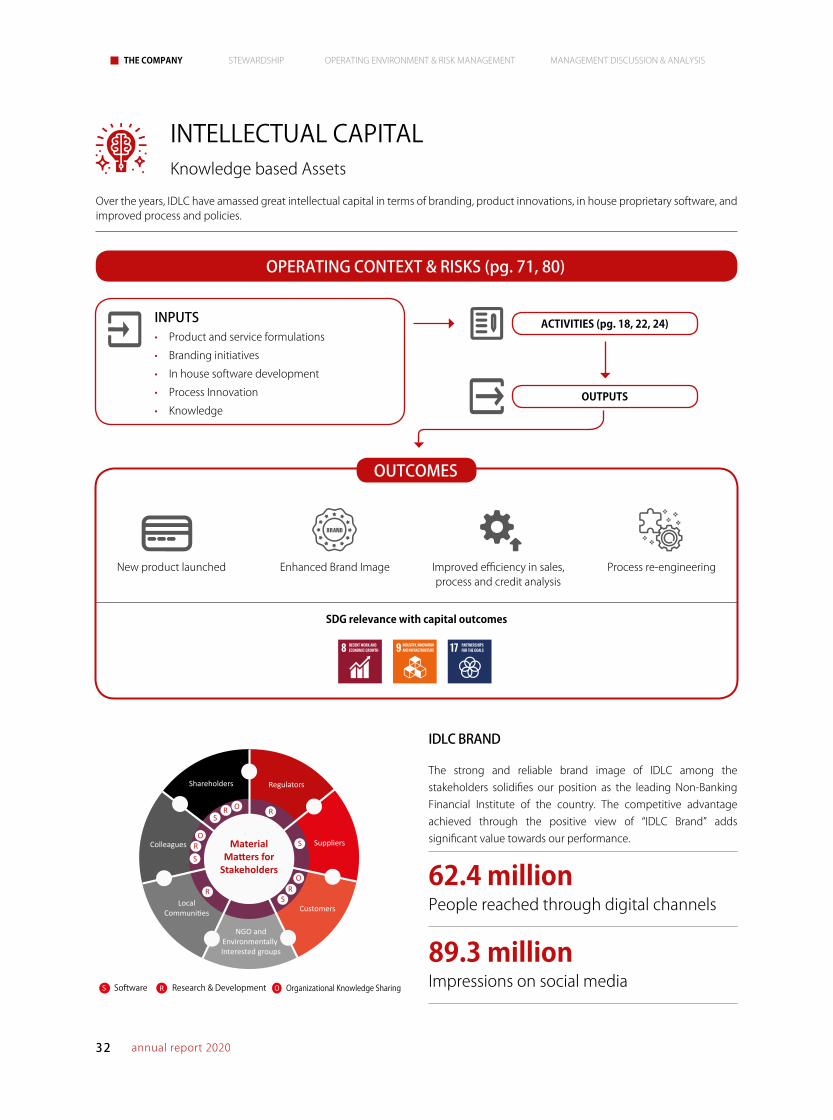

INTELLECTUAL CAPITALKnowledge based Assets

Over the years, IDLC have amassed great intellectual capital in terms of branding, product innovations, in house proprietary software, and improved process and policies.

OPERATING CONTEXT & RISKS (pg. 71, 80)

ACTIVITIES (pg. 18, 22, 24)

OUTPUTS

SDG relevance with capital outcomes

INPUTS• Product and service formulations

• Branding initiatives

• In house software development

• Process Innovation

• Knowledge

RS Software Research & Development O Organizational Knowledge Sharing

Shareholders Regulators

SuppliersMaterialMatters for

Stakeholders

CustomersLocal

Communi�es

NGO andEnvironmentally Interested groups

Colleagues

SR

O

R

R

S

SR

O

SR O

IDLC BRAND

The strong and reliable brand image of IDLC among the stakeholders solidifies our position as the leading Non-Banking Financial Institute of the country. The competitive advantage achieved through the positive view of “IDLC Brand” adds significant value towards our performance.

New product launched Enhanced Brand Image Improved efficiency in sales, process and credit analysis

Process re-engineering

62.4 millionPeople reached through digital channels

89.3 millionImpressions on social media

OUTCOMES

33IDLC Finance Limited

GOVERNANCE REPORTS & FINANCIAL STATEMENTS - IDLC REPORTS & FINANCIAL STATEMENTS - SUBSIDIARIES DISCLOSURES, CHECKLISTS & MISC.

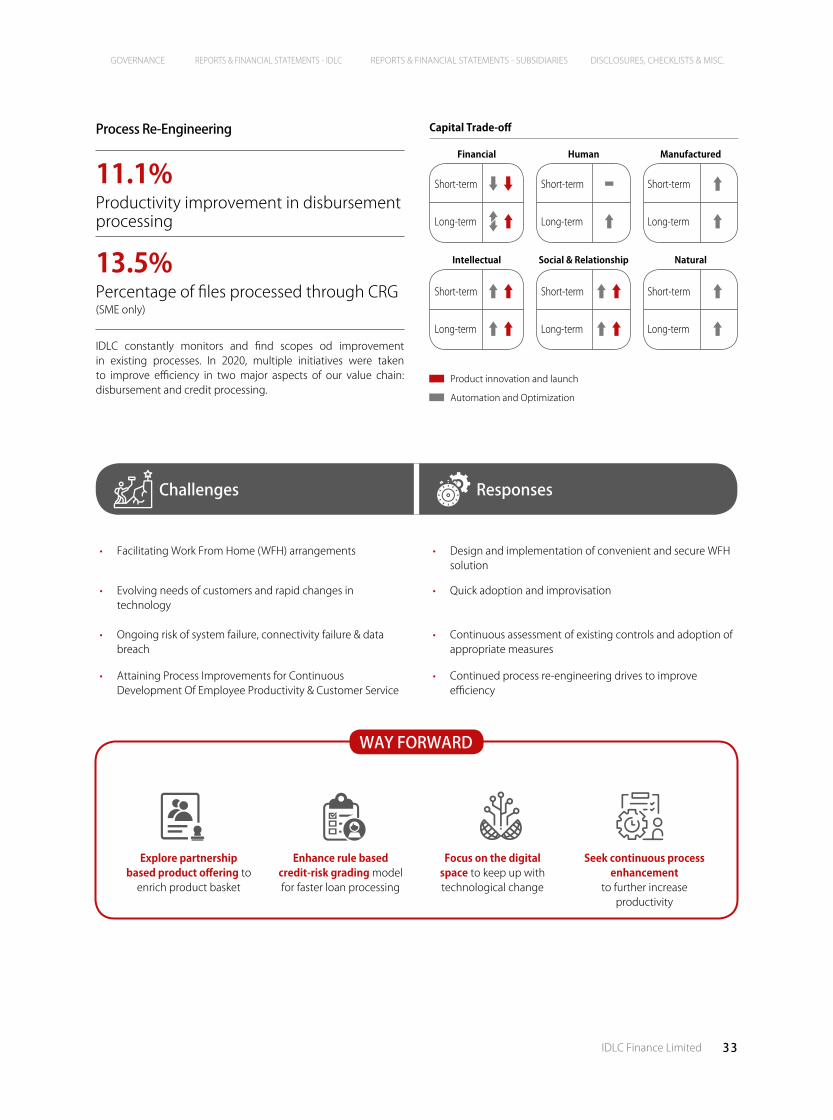

Process Re-Engineering

Explore partnership based product offering to

enrich product basket

Enhance rule based credit-risk grading model for faster loan processing

Focus on the digital space to keep up with technological change

Seek continuous process enhancement

to further increase productivity

WAY FORWARD

11.1% Productivity improvement in disbursement processing

13.5%Percentage of files processed through CRG (SME only)

IDLC constantly monitors and find scopes od improvement in existing processes. In 2020, multiple initiatives were taken to improve efficiency in two major aspects of our value chain: disbursement and credit processing.

Product innovation and launch

Automation and Optimization

Capital Trade-off

Financial

Intellectual

Human

Social & Relationship

Manufactured

Natural

Short-term

Short-term

Short-term

Short-term

Short-term

Short-term

Long-term

Long-term

Long-term

Long-term

Long-term

Long-term

Challenges Responses

• Facilitating Work From Home (WFH) arrangements • Design and implementation of convenient and secure WFH solution

• Evolving needs of customers and rapid changes in technology

• Quick adoption and improvisation

• Ongoing risk of system failure, connectivity failure & data breach

• Continuous assessment of existing controls and adoption of appropriate measures

• Attaining Process Improvements for Continuous Development Of Employee Productivity & Customer Service

• Continued process re-engineering drives to improve efficiency

34 annual report 2020

THE COMPANY STEWARDSHIP OPERATING ENVIRONMENT & RISK MANAGEMENT MANAGEMENT DISCUSSION & ANALYSIS

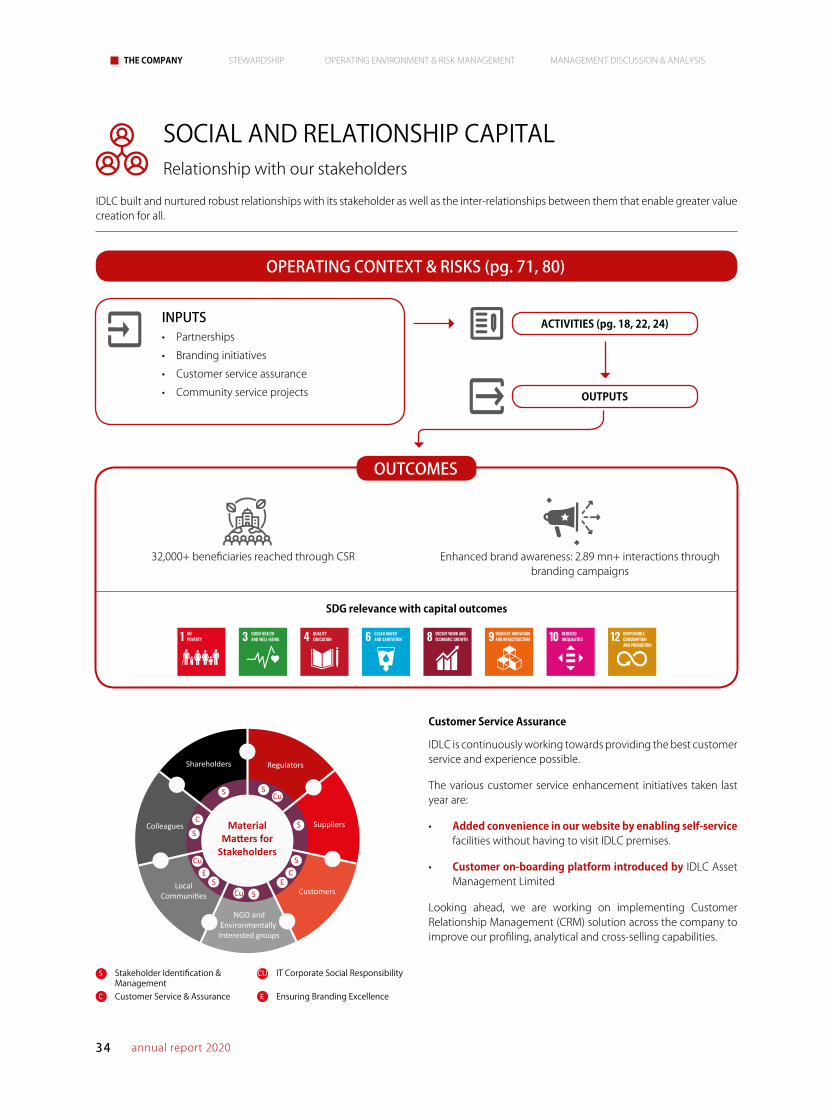

SOCIAL AND RELATIONSHIP CAPITALRelationship with our stakeholders

IDLC built and nurtured robust relationships with its stakeholder as well as the inter-relationships between them that enable greater value creation for all.

OPERATING CONTEXT & RISKS (pg. 71, 80)

ACTIVITIES (pg. 18, 22, 24)

OUTPUTS

32,000+ beneficiaries reached through CSR Enhanced brand awareness: 2.89 mn+ interactions through branding campaigns

SDG relevance with capital outcomes

INPUTS• Partnerships

• Branding initiatives

• Customer service assurance

• Community service projects

Shareholders Regulators

SuppliersMaterialMatters for

Stakeholders

CustomersLocal

Communi�es

NGO andEnvironmentally Interested groups

Colleagues

CS

E

S

C

SE

Cu

S CuS

SCu

S

CU IT Corporate Social ResponsibilityS Stakeholder Identification &Management

C Customer Service & Assurance E Ensuring Branding Excellence

IDLC is continuously working towards providing the best customer service and experience possible.

The various customer service enhancement initiatives taken last year are:

• Added convenience in our website by enabling self-service facilities without having to visit IDLC premises.

• Customer on-boarding platform introduced by IDLC Asset Management Limited

Looking ahead, we are working on implementing Customer Relationship Management (CRM) solution across the company to improve our profiling, analytical and cross-selling capabilities.

Customer Service Assurance

OUTCOMES

35IDLC Finance Limited

GOVERNANCE REPORTS & FINANCIAL STATEMENTS - IDLC REPORTS & FINANCIAL STATEMENTS - SUBSIDIARIES DISCLOSURES, CHECKLISTS & MISC.

Environment

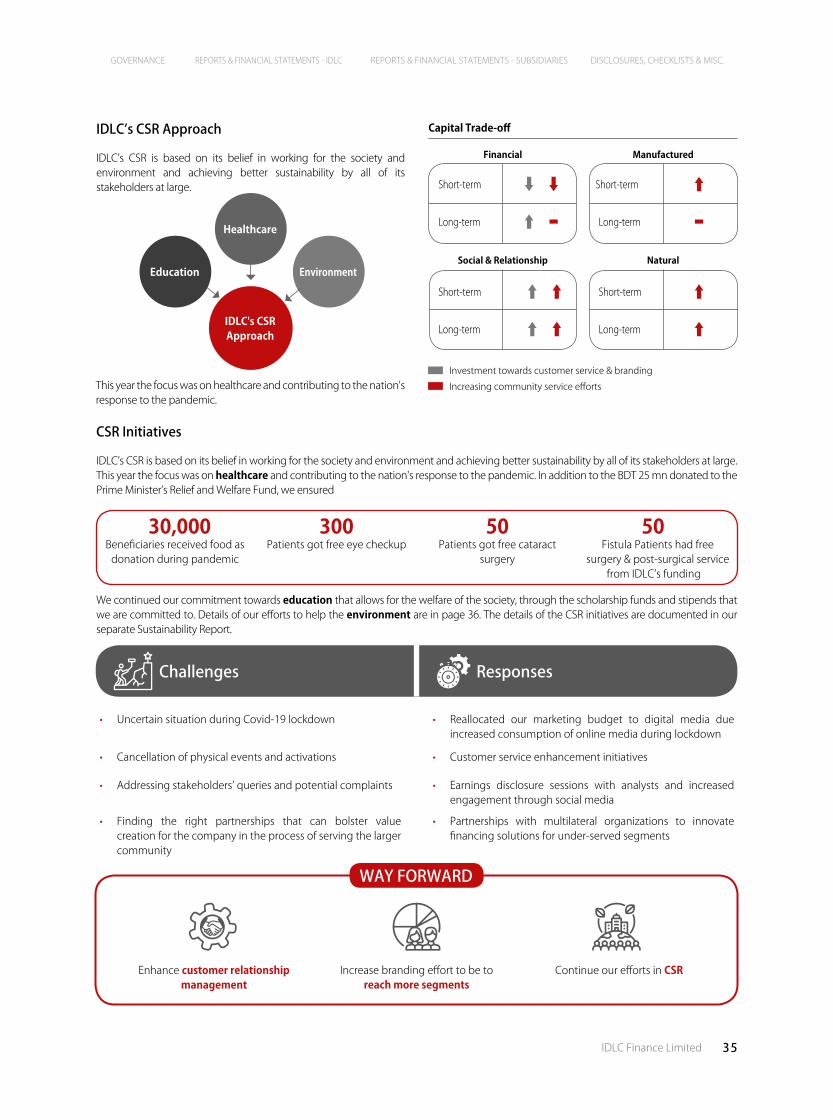

IDLC’s CSR Approach

IDLC’s CSR is based on its belief in working for the society and environment and achieving better sustainability by all of its stakeholders at large.

CSR Initiatives

IDLC’s CSR is based on its belief in working for the society and environment and achieving better sustainability by all of its stakeholders at large. This year the focus was on healthcare and contributing to the nation's response to the pandemic. In addition to the BDT 25 mn donated to the Prime Minister’s Relief and Welfare Fund, we ensured

We continued our commitment towards education that allows for the welfare of the society, through the scholarship funds and stipends that we are committed to. Details of our efforts to help the environment are in page 36. The details of the CSR initiatives are documented in our separate Sustainability Report.

IDLC's CSR Approach

Education

Healthcare

This year the focus was on healthcare and contributing to the nation's response to the pandemic.

Enhance customer relationship management

Increase branding effort to be to reach more segments

Continue our efforts in CSR

WAY FORWARD

Investment towards customer service & branding

Increasing community service efforts

Capital Trade-off

Financial

Social & Relationship

Manufactured

Natural

Short-term

Short-term Short-term

Long-term

Long-term

Long-term

Long-term

Short-term

30,000Beneficiaries received food as

donation during pandemic

300Patients got free eye checkup

50Patients got free cataract

surgery

50Fistula Patients had free

surgery & post-surgical service from IDLC’s funding

Challenges Responses

• Uncertain situation during Covid-19 lockdown • Reallocated our marketing budget to digital media due increased consumption of online media during lockdown

• Cancellation of physical events and activations • Customer service enhancement initiatives

• Addressing stakeholders’ queries and potential complaints • Earnings disclosure sessions with analysts and increased engagement through social media

• Finding the right partnerships that can bolster value creation for the company in the process of serving the larger community

• Partnerships with multilateral organizations to innovate financing solutions for under-served segments

36 annual report 2020

THE COMPANY STEWARDSHIP OPERATING ENVIRONMENT & RISK MANAGEMENT MANAGEMENT DISCUSSION & ANALYSIS

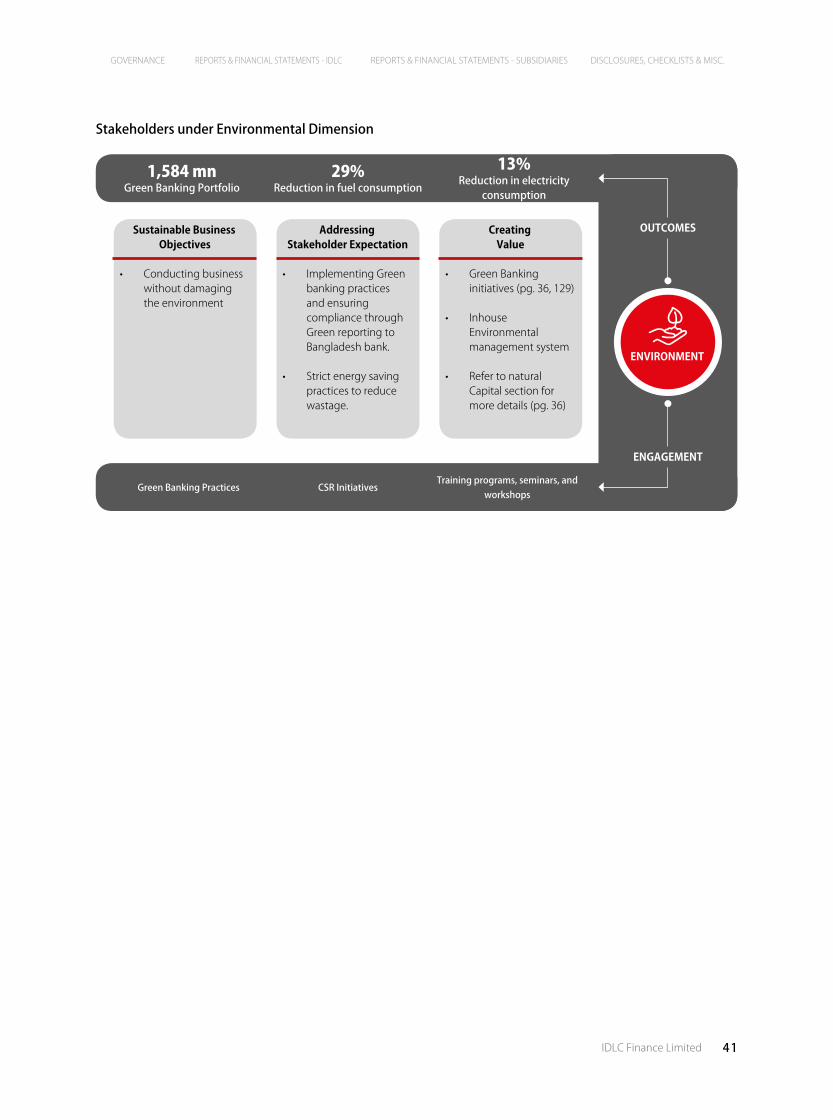

NATURAL CAPITAL Ecosystem and natural resources

IDLC’s natural capital comprises of the ecosystem and natural resources that are directly or indirectly affected by our business initiatives

OPERATING CONTEXT & RISKS (pg. 71, 80)

ACTIVITIES (pg. 18, 22, 24)

OUTPUTS

INPUTS• Utilities

• Policy Incentives from regulators

• Green Initiatives

ES Sustainable Business Practices Environmental Friendly Initiatives

G Green Banking

Shareholders Regulators

SuppliersMaterialMatters for

Stakeholders

CustomersLocal

Communi�es

NGO andEnvironmentally Interested groups

Colleagues

GS

G

E

SG G

GES

ENVIRONMENTAL FRIENDLY INITIATIVES

Through various external and internal initiatives, IDLC tries to bring positive impact to the environment surrounding its business activities. We are one of the Executing Entity (EE) of a Green Climate Fund (GCF) approved project that is worth USD 340.5 million.

Only member of United Nation Environment Program for Financial Institution (UNEP FI) in Bangladesh.

The Initiatives of the Founding signatories of UNEPFI are:

Principles for

Responsible Banking (PRB)

Collective Commitment

to Climate Action (CCCA)

Pledge of Tobacco Free

Portfolios

Green Initiatives Increased Green Banking Portfolio Controlled Carbon Footprint

SDG relevance with capital outcomes

OUTCOMES

37IDLC Finance Limited

GOVERNANCE REPORTS & FINANCIAL STATEMENTS - IDLC REPORTS & FINANCIAL STATEMENTS - SUBSIDIARIES DISCLOSURES, CHECKLISTS & MISC.

Continued focus on organisation wide resource optimization

Increased focus on organisation-wide carbon management

Increase focus on sustainability

WAY FORWARD

IDLC strictly follows our Green Office Guide, which helps us to use natural resources as prudently as possible and maintain a sustainable business environment. Although no natural resources are directly utilized behind our business operations, they are used to aid our day to day operations.

PER EMPLOYEE RESOURCE CONSUMPTION2019 2020

710

21,517

3,837 916 450

18,646

2,716 902

WaterConsumption

ElectricityConsumption

FuelConsumotion

PaperConsumptiom

Green Banking Efforts

Green Office Practices

Capital Trade-off

Financial

Social & Rel.

Manufactured

Natural

Short-term

Long-term Long-term

Short-term

Short-term

Long-term

Short-term

Long-term

Challenges Responses

• Implementing an effective resource optimization system to reduce energy and resource consumption during business operations

• Implemented an organization-wide Carbon Management & Resource Optimization Model

• Creating awareness among clients regarding the benefits of green projects

• Leveraged our relationships with regulators and multilateral organizations to increase green financing

• Ensuring Green Office practices are maintained and internal stakeholders are aware of its benefits

• Conducted training and seminars to increase awareness of our colleagues and stakeholders

38 annual report 2020

THE COMPANY STEWARDSHIP OPERATING ENVIRONMENT & RISK MANAGEMENT MANAGEMENT DISCUSSION & ANALYSIS

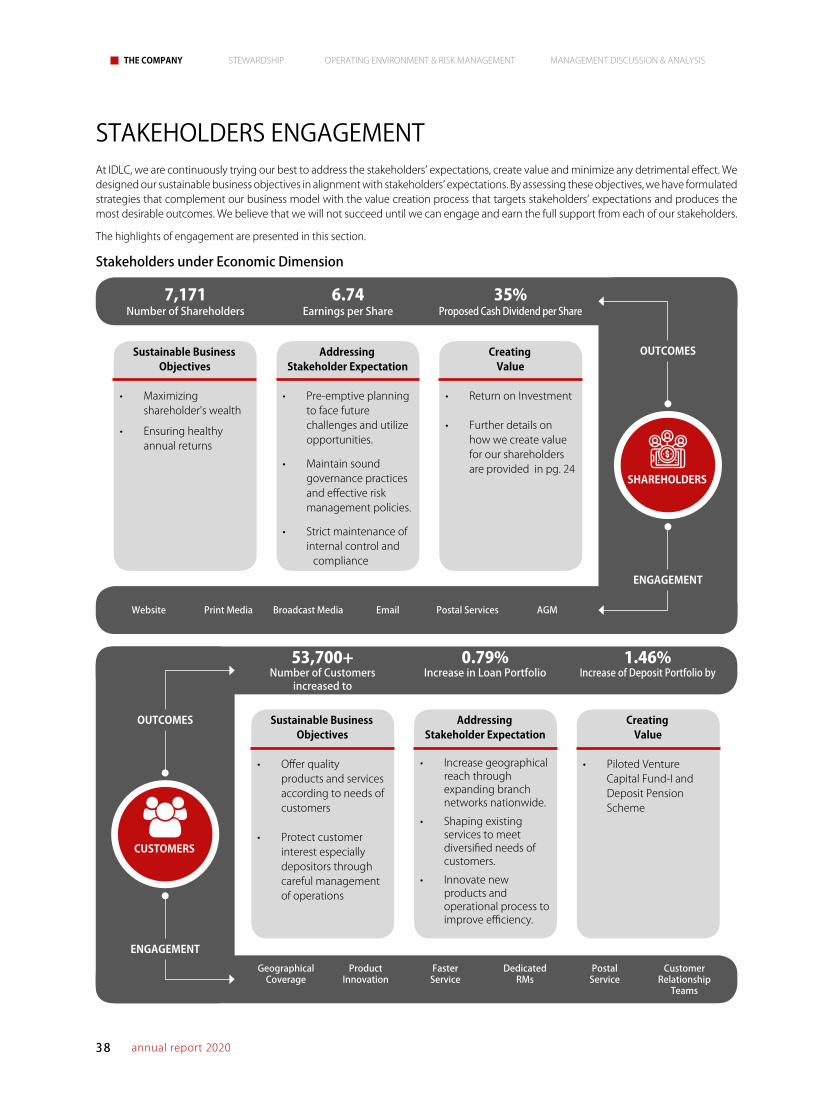

STAKEHOLDERS ENGAGEMENTAt IDLC, we are continuously trying our best to address the stakeholders’ expectations, create value and minimize any detrimental effect. We designed our sustainable business objectives in alignment with stakeholders’ expectations. By assessing these objectives, we have formulated strategies that complement our business model with the value creation process that targets stakeholders’ expectations and produces the most desirable outcomes. We believe that we will not succeed until we can engage and earn the full support from each of our stakeholders.

The highlights of engagement are presented in this section.

Stakeholders under Economic Dimension

SHAREHOLDERS

CUSTOMERS

OUTCOMES

OUTCOMES

ENGAGEMENT

ENGAGEMENT

7,171Number of Shareholders

6.74Earnings per Share

35%Proposed Cash Dividend per Share

53,700+Number of Customers

increased to

0.79%Increase in Loan Portfolio

1.46%Increase of Deposit Portfolio by

Website Print Media Broadcast Media Email Postal Services AGM

Geographical Coverage

Product Innovation

Faster Service

DedicatedRMs

PostalService

Customer Relationship

Teams

Sustainable BusinessObjectives

• Maximizing shareholder's wealth

• Ensuring healthy annual returns

Sustainable BusinessObjectives

• Offer quality products and services according to needs of customers

• Protect customer interest especially depositors through careful management of operations

Addressing Stakeholder Expectation

• Pre-emptive planning to face future challenges and utilize opportunities.

• Maintain sound governance practices and effective risk management policies.

• Strict maintenance of internal control and

compliance

Addressing Stakeholder Expectation

• Increase geographical reach through expanding branch networks nationwide.

• Shaping existing services to meet diversified needs of customers.

• Innovate new products and operational process to improve efficiency.

Creating Value

• Return on Investment

• Further details on how we create value for our shareholders are provided in pg. 24

Creating Value

• Piloted Venture Capital Fund-I and Deposit Pension Scheme

39IDLC Finance Limited

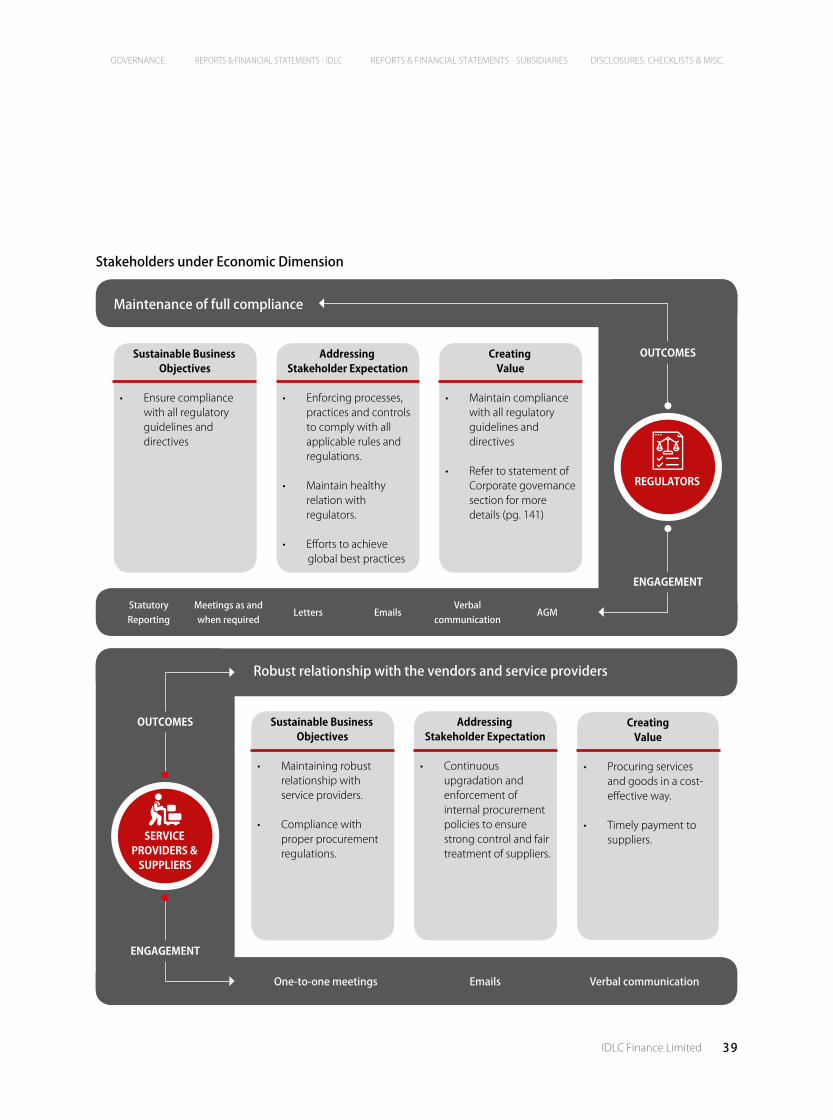

GOVERNANCE REPORTS & FINANCIAL STATEMENTS - IDLC REPORTS & FINANCIAL STATEMENTS - SUBSIDIARIES DISCLOSURES, CHECKLISTS & MISC.

Stakeholders under Economic Dimension

SERVICE PROVIDERS &

SUPPLIERS

OUTCOMES

ENGAGEMENT

Robust relationship with the vendors and service providers

One-to-one meetings Emails Verbal communication

Sustainable BusinessObjectives

• Maintaining robust relationship with service providers.

• Compliance with proper procurement regulations.

Addressing Stakeholder Expectation

• Continuous upgradation and enforcement of internal procurement policies to ensure strong control and fair treatment of suppliers.

Creating Value

• Procuring services and goods in a cost-effective way.

• Timely payment to suppliers.

REGULATORS

OUTCOMES

ENGAGEMENT

Maintenance of full compliance

Statutory Reporting

Meetings as and when required

Letters EmailsVerbal

communicationAGM

Sustainable BusinessObjectives

• Ensure compliance with all regulatory guidelines and directives

Addressing Stakeholder Expectation

• Enforcing processes, practices and controls to comply with all applicable rules and regulations.

• Maintain healthy relation with regulators.

• Efforts to achieve global best practices

Creating Value

• Maintain compliance with all regulatory guidelines and directives

• Refer to statement of Corporate governance section for more details (pg. 141)

40 annual report 2020

THE COMPANY STEWARDSHIP OPERATING ENVIRONMENT & RISK MANAGEMENT MANAGEMENT DISCUSSION & ANALYSIS

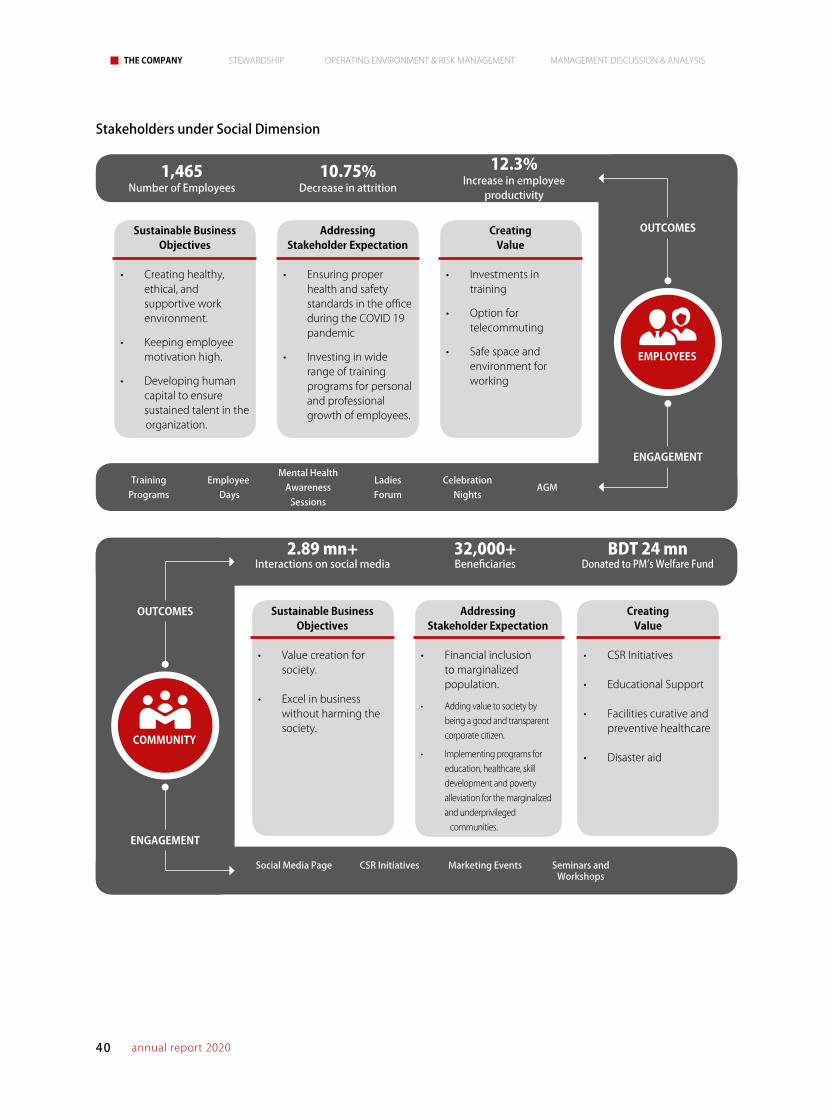

Stakeholders under Social Dimension

EMPLOYEES

COMMUNITY

OUTCOMES

OUTCOMES

ENGAGEMENT

ENGAGEMENT

1,465Number of Employees

10.75%Decrease in attrition

12.3%Increase in employee

productivity

2.89 mn+Interactions on social media

32,000+Beneficiaries

BDT 24 mnDonated to PM’s Welfare Fund

Training Programs

Employee Days

Mental Health Awareness

Sessions

LadiesForum

Celebration Nights

AGM

Social Media Page CSR Initiatives Marketing Events Seminars and Workshops

Sustainable BusinessObjectives

• Creating healthy, ethical, and supportive work environment.

• Keeping employee motivation high.

• Developing human capital to ensure sustained talent in the organization.

Sustainable BusinessObjectives

• Value creation for society.

• Excel in business without harming the society.

Addressing Stakeholder Expectation

• Ensuring proper health and safety standards in the office during the COVID 19 pandemic

• Investing in wide range of training programs for personal and professional growth of employees.

Addressing Stakeholder Expectation

• Financial inclusion to marginalized population.

• Adding value to society by being a good and transparent corporate citizen.

• Implementing programs for education, healthcare, skill development and poverty alleviation for the marginalized and underprivileged