Embed Size (px)

Citation preview

A Guide to Irish Private Equity Funds

1

A Guide to Irish Private Equity Funds

Contents

Introduction Page 2 Available Structures to house an Irish Private Equity Fund Page 2 Available Irish Regulated Fund Structures Page 3 Available Irish Unregulated Fund Structures Page 10 Regulatory Regime Applicable to Irish Fund Managers Page 13 Taxation of Irish Regulated Fund Schemes Page 14 Taxation of Irish Limited Partnerships Page 17 Appendix – Regulated Fund Structure Diagram Charts Page 19 Contact Us Page 20

2

A GUIDE TO IRISH PRIVATE EQUITY FUNDS

Introduction

Ireland, as a domicile for private equity funds, offers a variety of potential fund structures both

regulated and unregulated, with differing levels of investment flexibility, minimum subscription

requirements, differing tax regimes and regulatory requirements for service providers depending on

which structure is chosen as the appropriate vehicle for a particular project.

Regulated vehicles include unit trusts, variable capital investment companies and common

contractual funds, each of which can be open-ended, limited liquidity or more frequently closed-

ended schemes, with the level of investment and borrowing restrictions and permitted investment

mechanics being set by the targeted investor profile – retail, professional or qualifying investor – with

strict rules as to custody, asset management and fund administration.

Unregulated structures are generally housed within limited partnership structure established under

the Limited Partnership Act, 1907.

Available Structures to house an Irish Private Equity Fund

As would be the case for any new fund proposal, any consideration of the available structures within

which to house a private equity fund should include the following factors:

- whether prospective investors have a preference for a regulated over an unregulated

structure;

- the investment flexibilities provided by regulated and by unregulated structures;

- the investment strategies to be followed, including the nature of the portfolio of investments;

- any relevant limitations on investor profile or investor numbers;

- regulation of the Fund Managers; and

- taxation.

These factors are addressed separately below.

3

Available Irish Regulated Fund Structures

Given that a portfolio of private equity investments will normally be relatively or highly illiquid, the

available Irish regulated fund structures are what are referred to as non-UCITS structures – UCITS

structures are not appropriate given their focus on liquid assets and their requirement to provide at

least twice monthly redemption facilities.

It should be noted that non-UCITS products, unlike UCITS, do not benefit from the principle of

mutual recognition within the European Economic Area and cannot be publicly marketed in most

other Member States. They are private placement vehicles in practice.

However, an important caveat is that the public marketing of true closed-ended non-UCITS within

the European Economic Area is possible under Directive 2003/71/EC (the “Prospectus Directive” or

“PD”). Although our experience to date is that most promoters of this type of product do not consider

the PD regime to offer marketing advantage particularly for the sophisticated or institutional market

place, in any event QIFs (the most popular Irish regulated vehicle - see further below) can generally

be placed quite widely without using the PD regime, provided that the placing respects each

individual target country’s private placement rules.

Non-UCITS are available in three principal legal forms - variable capital investment companies, unit

trusts and tax transparent common contractual funds. [Note that neither individuals (nor their

nominees) can invest in common contractual funds without undermining their tax transparency].

Note also that whilst regulated investment limited partnerships are also available, to our knowledge

none have been used / authorized for at least a decade and we have not accordingly considered

them further given that the Central Bank of Ireland (the “Central Bank”) would not be familiar with

them in practice.

The choice of legal structure for a regulated fund will usually depend on a number of issues,

including:

- investor familiarity;

- investor capacity to invest (e.g. Japanese investors seem to be able to invest higher

proportions of their portfolios in unit trusts);

- willingness of promoter to set up Irish management company (required for unit trust and

common contractual fund but not for investment company);

- portfolio diversification;

- borrowing/leverage proposals (available in all structures but legal arrangements clearer in

investment companies);

4

- reporting requirements (all regulated funds must prepare annual audited accounts and semi-

annual unaudited accounts, save that QIF investment companies no longer required to

produce semi-annual unaudited accounts);

- operational flexibility (more with unit trusts than with investment companies - i.e. no AGM for

unit trusts and easier to amend constitutional documentation for non-material issues).

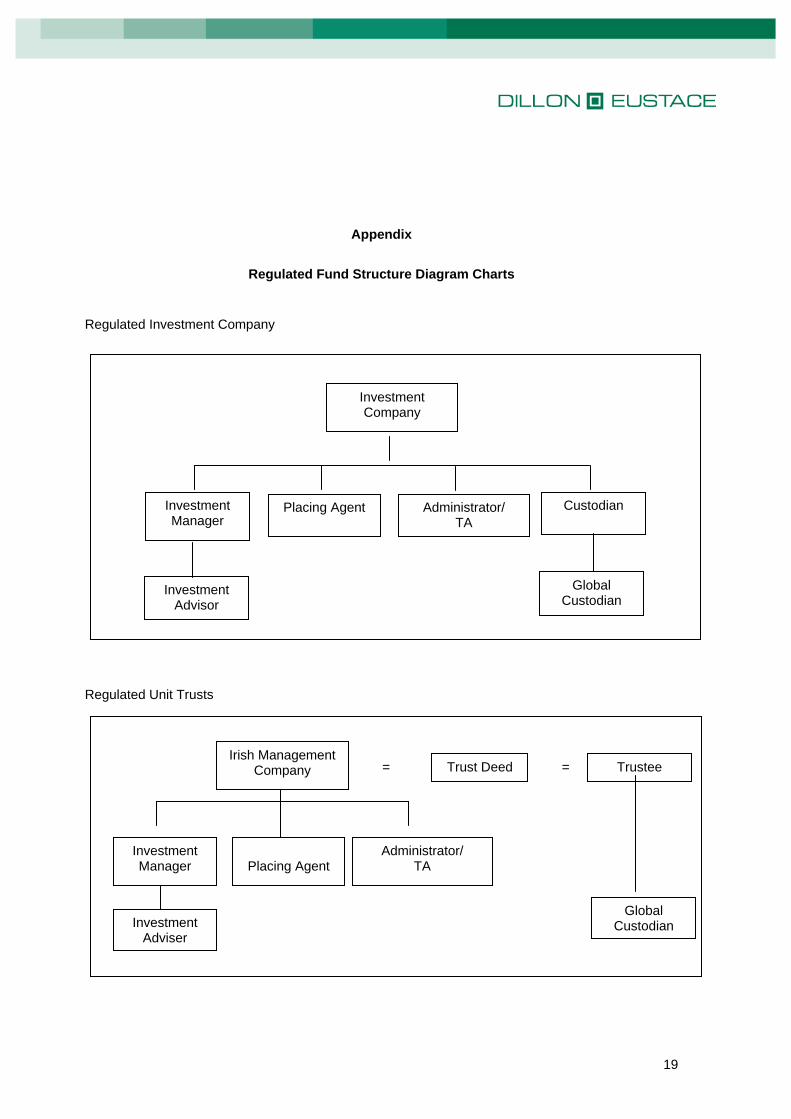

The two main regulated fund structures are shown in diagrammatical format in the Appendix.

The Central Bank is the Irish competent authority entity responsible for authorising and for the

ongoing supervision of all regulated fund structures.

(i) Approval Process for Promoter/Service Providers

For all Irish regulated funds, the initial regulatory requirement is that the principal service providers to

the fund must be approved in advance. This requirement applies to each of the promoter, the

management company (if any), the directors, the investment manager and the Irish administrator

and custodian.

Promoter : The Central Bank regards the promoter of a fund as being the driving force behind the

product. Promoters of an Irish regulated fund must submit an application seeking the Central Bank’s

approval to promote the fund which application must include, inter alia, details of shareholders, latest

audited accounts and details of overseas regulatory status. The Central Bank must be satisfied as to

the promoter’s expertise, integrity and adequacy of financial resources (the promoter must have

minimum shareholder’s funds of €635,000 for as long as it acts as promoter to an Irish collective

investment scheme).

The Central Bank will carry out a due diligence process including contacting the promoter’s regulator

in its home jurisdiction, asking the service providers to confirm their due diligence checks, etc. in

order to ensure that the promoter is sufficiently reputable and experienced.

As a rule, only regulated entities will be accepted by the Central Bank to act as promoters of

regulated Irish fund vehicles.

Management Company (Unit Trust/CCF only) : Where an Irish management company is established

(required for unit trusts and common contractual funds), the Central Bank must be satisfied as to the

competence and probity of its management, that it has sufficient financial resources at its disposal to

enable it to conduct its business effectively and meet its liabilities, that it will be in a position to

comply with any conditions imposed by the Central Bank and that the effective control over its affairs

5

and of the trustee or custodian will be exercised independently of one another. A minimum of two

directors of the management company must be Irish resident.

A management company must have a minimum paid-up share capital equivalent to €125,000 or one-

quarter of its proceeding years fixed overheads, whichever is the greater. The minimum capital

requirement must be held as eligible assets in a form that is easily accessible and must be free from

any liens or charges. A management company that is a member of a group must maintain its

minimum capital requirements outside of the group and must be in a position to demonstrate its

ongoing compliance with this requirement.

Adequate information on the expertise and the reputation of the proposed directors and managers of

the management company must be provided, and names of the company secretary and of the

shareholders must be furnished with audited accounts overseas regulatory status (if any) and

appointments to the office of director of the management company must be approved by the

regulator. The management company is also required to consult the Central Bank before engaging

in significant new activities and is not permitted to manage collective investment schemes not

managed by the Central Bank. Approval from the Central Bank is required in respect of any

proposed change in ownership or in significant shareholdings (10 per cent or more in the

management company).

Directors : The Directors of the fund/management company are required to meet certain standards

of competence and probity which requires them to submit a detailed questionnaire to the Central

Bank seeking prior approval for that appointment.

Investment Manager : Irish regulated funds have to have an investment manager responsible for

discretionary portfolio management. Such entities must be regulated entities in their home

jurisdiction under MiFID or equivalent (i.e. regulated by the US SEC, Hong Kong SFC etc). If Irish

they would have to be regulated under Irish MiFID Regulations. Very few exceptions are available

for unregulated investment managers.

Administrator/Trustee/Custodian : Additionally, Irish regulated non-UCITS fund require an Irish

based fund administrator (responsible for NAV calculation, fund accounting and transfer agency type

functions) and an Irish custodian responsible for safekeeping of assets and performance of various

fiduciary/trustee type functions to be appointed.

(ii) Investment and Borrowing Limits

The Central Bank sets investment and borrowing limits for Irish regulated funds based on the type of

investor targeted, breaking the categorization down into three – retail investors, professional

6

investors and qualifying investors. Quite stringent portfolio diversification requirements and

limitations on borrowing/leverage are imposed on a retail investor funds, with those limits relaxed

partially for professional investor funds, whereas most (but not all) investment limits are disapplied in

the case of a fund targeting qualifying investors.

Minimum Subscription/Commitment : The minimum subscription for a retail investor private equity

type scheme is Euro 12,500. For a professional investor scheme, a minimum subscription per

investor is Euro 125,000 (pension funds can satisfy over a 12 month period) and in the case of

qualifying investor funds the investors must not only subscribe a minimum of Euro 100,000 per

investor but additionally must meet appropriate expertise/understanding tests, they must either be:

(a) an investor who is a professional client within the meaning of Annex II of Directive

2004/39/EC (Markets in Financial Instruments Directive); or

(b) an investor who receives an appraisal from an EU credit institution, a MiFID firm or a UCITS

management company that the investor has the appropriate expertise, experience and

knowledge to adequately understand the investment in the QIF; or

(c) an investor who certifies that they are an informed investor by providing the following:

confirmation (in writing) that the investor has such knowledge of and experience in

financial and business matters as would enable the investor to properly evaluate the

merits and risks of the prospective investment; or

confirmation (in writing) that the investor’s business involves, whether for its own

account or the account of others, the management, acquisition or disposal of property of

the same kind as the property of the QIF.

In the context of funds issuing partly paid units/shares, the minimum subscription amounts refer to

the commitment made, not the initial drawdown.

Investment Limits : As indicated above, the Central Bank sets investment and borrowing limits for

regulated funds by reference to the investor to whom the Fund is sold – retail investor, professional

investor or qualifying investor.

For a retail investor type private equity scheme no more than 20% of net assets may be invested in

any one company or group of companies (derogation for 1 year following launch provided one

observes the principle of risk spreading). Legal and management control of underlying investments

may be taken subject to appropriate prospectus disclosure. Prospectus disclosure must also

7

address suitability of the type of investment and a recommendation that not more than 5% of an

investor’s portfolio be invested in the fund etc.

For a professional investor scheme, it is a matter for negotiation but normally 25 -35% of net assets

can be invested in a single company or group.

In the case of a qualifying investor fund established as a unit trust, there are no risk spreading rules.

If established as an investment company, there is a requirement to spread risk although this is a

statutory requirement not one imposed by the Central Bank and therefore it is up to the Board of

Directors of the qualifying investor type investment company to determine what they consider to be

risk spreading.

Borrowing Limits: The general rule for a retail scheme is that borrowing may be up to 25% of net

assets, 50% to 100% for professional investor funds (subject to negotiation with the Central Bank)

whereas in the case of a qualifying investor scheme borrowing is unlimited, subject simply to

appropriate prospectus disclosure.

Where a fund is investing in other funds, there are specific rules dealing with the nature of the

underlying funds and the maximum exposure that can be taken to individual funds. Again, there is

more flexibility for professional investor and qualifying investors than for retail investor schemes.

Our experience is that regulated private equity (or quasi private equity) funds which have been

established in Ireland to date have mainly used the qualifying investor structure.

Bear in mind, however, that these funds have been targeted from an investment and an investor

perspective at the international not Irish domestic market.

(iii) Operational Issues

As indicated above, whilst private equity funds represent only a small proportion of Irish regulated

collective investment schemes, those that have been established have primarily been established as

qualifying investor schemes. In that context, the Central Bank is familiar, with and has permitted:

- partly paid units/shares and drawdown mechanics;

- use of the EVCA or IVCA rules for valuation purposes;

- flexible investment parameters;

- use of carried interest/waterfall mechanisms;

- closed-ended/limited liquidity schemes;

- use of foreign and Irish subsidiary / intermediary vehicles for investment purposes;

8

- joint venture arrangements, co-investment arrangement

- investor committees.

One point to note is that care needs to be taken in structuring partly paid / commitment

arrangements in closed-ended investment companies as there are particular rules relating to both

allotment of partly paid shares and rules which only allow redemption of fully paid shares.

(iv) Closed-Ended / Limited Liquidity/Open-Ended with Limited Liquidity

Regulated private equity funds can be structured as open-ended, open-ended with limited liquidity,

limited liquidity or closed-ended schemes with the choice very much dependent on the nature of the

portfolio (principally liquidity) and the promoter/investment manager’s intentions regarding returns to

investors.

In summary, an open-ended scheme is one which provides redemption facilities for investors (at

their request) on at least a quarterly basis. Open-ended with limited liquidity is one which provides

redemption facilities at least annually, limited liquidity is one which provides that at some stage

during the life of the fund a option for investors to request redemption, whereas closed-ended

schemes are those which do not provide any capacity for investors to request redemption during the

life of the fund. The choice will very much depend on the portfolio liquidity and therefore the

expectation of the Central Bank would be that a private equity fund would be limited liquidity or

closed-ended.

For closed-ended funds, there must be a finite closed-ended period provided for in the constitutional

documentation. Retail schemes can have an initial closed-ended period of up to 5 years (can be

raised to 10 years where there is realistic provision for liquidity in the units (bear in mind this refers

to realistic provisions for liquidity so listing is unlikely to be sufficient where there is no secondary

market). There is also a provision to increase the initial closed-ended period up to 15 years for retail

schemes where they provide for specific opportunities for redemption after 10 years.

Qualifying investor funds schemes can have an initial duration of up to 15 years and professional

schemes up to 10 years, extending this to 15 years where they have made realistic provision for

liquidity.

At the end of the closed-ended period the fund is required to either:

- wind-up and apply for revocation of authorisation;

- redeem all outstanding units and apply for revocation of authorisation;

- convert into an open-ended scheme; or

9

- obtain investor approval (generally 75% of more of unitholders in favour) to extend the closed

period for a further period.

There are two other key considerations in the context of closed-ended and limited liquidity schemes.

Firstly, closed-ended schemes (as opposed to limited liquidity schemes) are subject to the

Prospectus Directive unless that they can avail of an exemption (professional investor and qualifying

investor schemes should generally be able to avail of an exemption provided that they do not list).

Secondly, it also needs to be borne in mind that closed-ended schemes (as opposed to limited

liquidity schemes) may be subject to quite a number of other European Directives including the

Transparency Directive, the Takeovers Directive, etc. In some cases, promoters seek to avoid

closed-ended schemes (using limited liquidity schemes instead) for this reason but they can be dealt

with with advance preparation.

(v) Eight Year Deemed Disposal Rule

A further important point to note in the context of a fund on Irish investors is that, in the case of

regulated funds, Irish tax law applies a deemed disposal for Irish tax purposes for Irish investors

after eight years from date of investment. In other words, Irish investors are taxed on the basis of a

deemed realisation of their investment after eight years from the date of investment even if no actual

liquidity has been provided. See taxation section for more detail.

(vi) Authorisation Process / Documentation

For regulated funds there is an authorisation process to be completed before they can be launched.

In addition to the service providers to the fund - the promoter, directors, investment manager,

administrator and custodian - the fund itself has to be authorised. What this means is that for retail

and professional funds the fund documentation (prospectus, constitutive documentation, asset

management / administration / custody agreements and certain ancillary documentation) has to be

submitted for prior consideration by the Central Bank and then go through a process of addressing

Central Bank comments on the documentation, leading to a final set of negotiated documentation

with the Central Bank and then filing for formal approval. This process generally takes six weeks

from filing (assuming promoter approval has already obtained).

In the case of a qualifying investor scheme, however, the position is radically different. There is no

prior filing with or review by the Central Bank. Instead, there is a self certification regime

(certification has to be given by the board of the fund / management company and by the Irish legal

advisers). Once those certifications can be given, the fund documentation is simply negotiated

between the promoter, the legal advisers and the other service providers and then executed and

filed with the Central Bank. Once the documentation is filed by 3 p.m. on the day prior to the date for

10

which authorisation is sought, the fund will be authorised on the requested date without a prior

review. A post authorisation review will normally take place.

If any specific derogations from the Central Bank’s requirements for qualifying investor funds are

being sought for the particular product these have to be cleared in advance. In other words this is a

very much a fast track process but again assumes that promoter approval has been obtained.

Available Irish Unregulated Fund Structures

Turning now to the available Irish unregulated fund structures, it is important that care be taken in

establishing/structuring Irish unregulated fund structures to ensure not only that the fund structure

itself falls outside of the regulatory regime but also to consider how the regulatory regime may apply

to the various service providers to the unregulated fund structure and how the fund is

commercialised.

Unregulated unit trust structures are not available (other than for sale to pension funds/charities) and

even those exempt unit trust structures (sold to pension funds/charities) are now being reviewed by

the Central Bank in the context of possibly bringing them within the regulatory regime.

Unregulated corporate structures do not benefit from the variable capital mechanism which makes

investment into and returns from such vehicles difficult to structure as well as having to take into

account the corporate tax regime, the regime dealing with public offers of securities etc.

For these reasons, the 1907 Limited Partnership structure (“LP”) is the favoured Irish unregulated

fund structure for private equity type funds. Although the legislation dealing with regulated fund

structures does not provide any clear exemption from the regulatory regime for 1907 LPs, provided

they are not seen as “public participation” type schemes they should not require regulation. Many

1907 LPs have been and continue to be established and we do not believe that the Central Bank

does or could consider them to be subject to its regulatory regime.

The LP is structured via a partnership agreement entered into between the general partner ("GP")

and the limited partners. The GP would normally be an Irish private limited liability company

(although it does not in fact have to be an Irish entity at all). It is important to ensure that it is a

limited liability entity given that a GP has unlimited liability in contrast to the limited partners whose

liability is limited to the amount of their investment in the LP.

11

There is a strict limit on the number of partners that an LP can have. For most LPs, the limit is set at

20 partners (GP plus 19 limited partners) but this can be raised to 50 where the LP is formed for the

purpose of, and whose main business consists of, the provision of investment and loan finance and

ancillary facilities and services to persons engaged in industrial or commercial activities.

Where an LP breaches these limits not only would it result in breaches of company and partnership

law, but it would also remove the limited liability of the limited partners.

It is also important to appreciate that LPs are private placement vehicles only. There should be no

public type of solicitation of investors as otherwise there would be a risk of the LP being considered

to fall foul of Section 9 of the Unit Trusts Act, 1990 which applies the regulatory regime to a wide

spectrum of arrangements “which are made for the purpose of, or have the effect, solely or mainly, of

providing facilities for the participation by the public, as beneficiaries (otherwise than under a trust or

through membership of a company, a building society, a friendly society or an industrial and

provident society) in profits or income arising from acquisition, holding, management or disposal of

securities or any other property whatsoever”.

Accordingly, one always needs to consider how many investors (as limited partners) one believes

that you will have. In the event that it is more than 50 (including the GP), then consideration would

need to be given to having a second LP. We are aware that this has been dealt with previously by

having, for example, 2 LPs with a co-investment agreement entered into between them. Our view is

that such an approach could result in the co-investment arrangement itself falling foul of the Unit

Trusts Act, 1990 and of company/partnership law so care needs to be taken with any such proposal.

It may be better to deal with this via separate investing LPs where they would have different GPs

and would bind themselves together as investors under shareholder agreements rather than co-

investment arrangements.

Given that an LP is an unregulated structure, there is no promoter approval process, no requirement

to have an Irish administrator or custodian, no investment or borrowing restrictions and no minimum

subscription requirements. There are no particular restrictions on the method by which an LP can be

funded, engage in borrowing/leverage or make investments. The key concern is to ensure that a tax

efficient model is used. This will often involve the routing of investment through conduit vehicles

including, for example, Luxembourg vehicles.

Whilst not subject to the Central Bank’s regulatory regime, 1907 LPs are subject to provision of the

Limited Partnership Act, 1907 from which a number of key points are of note

12

- where a limited partner draws out or receives back directly or indirectly any part of his

“contribution” during the life of the partnership then he will remain liable for the debts and

obligations of the partnership up to the amount so drawn out or received back

- a body corporate can be a limited partner

- a limited partner is not permitted to take part in the management of the partnership and has

no power to bind the partnership

- partnership details have to be registered with the Companies Registration Office (“CRO”).

The disclosure should include the LPs name, the general nature of its business, the principal

place of business, the full name of each of the partners, the term, if any, for which the

partnership is entered into and the date of its commencement, a statement that the

partnership is limited and the description of every limited partner as such and the sum

contributed by each LP and whether paid in cash or otherwise

- if there are also any changes during the life of a limited partnership those particulars also

have to be filed with the CRO

- the rules of the LP are set out in the partnership agreement

To date, the common view, which appears to be accepted by the Central Bank, is that the GP of an

LP does not require to be regulated for investment services on the basis that it is not providing

investment services to third parties but rather to its fellow partners. There are numerous limited

partnerships established which rely on such an interpretation. We have recently obtained some

(limited) comfort on this from the Central Bank who referred to partners in an LP having a

“communality of interest …… the assets would legally be those of the partnership and therefore

assets of each limited partner)."

In that regard, where the GP has a carried interest that would in our view be beneficial from a

regulatory standpoint as that would reinforce the "communality of interests" argument.

In the event that an Irish administrator or custodian is chosen to carry out the day-to-day

administration and/or safekeeping of the LP’s assets, such activities are likely to be regulated

activities and require those service providers to themselves to be authorised under the Irish MiFID or

IIA regimes or corresponding foreign regimes.

The actual process of placing the limited partnership interests can itself be considered to be a

regulated activity involving either the receipt and transmission of orders or the placing of investment

or financial instruments under either MiFID or the IIA. Arguably it falls outside the IIA (as it only

refers to investment limited partnership interests under a 1994 Act) but the list of "transferable

securities" under the MiFID Regulations does include "… other securities equivalent to shares in

companies, partnerships or other entities".

13

Accordingly, we would recommend that only regulated financial intermediaries be used for

placement process and that any such placement process be conducted on very much a private (not

public) basis to avoid application of the Unit Trusts Act, 1990 referred to above

We would expect that an information memorandum would be prepared for the LP as well as normal

investor documentation.

Regulatory Regime Applicable to Irish Fund Managers

Irish entities which provide portfolio management and/or investment advisory services to third parties

on a professional basis are subject to regulation under either the Irish MiFID regime (European

Communities (Markets and Financial Instruments) Regulations 2007) or under the more domestically

focused Investment Intermediaries Act, 1995 (as amended) (the “IIA”).

These regimes regulate the provision of a variety of investment services to third parties in respect of

one or more investment or financial instruments.

In the context of private equity investment, it is worth noting that the MiFID regime includes within the

list of financial instruments “transferable securities” which are defined as meaning with the exception

of instruments of payment, those classes of securities which are negotiable on the capital market,

such as the following:

(a) shares in companies and other securities equivalent to shares in companies, partnerships or

other entities, and depositary receipts in respect of shares;

(b) bonds or other forms of securitised debt, including depositary receipts in respect of such

securities;

(c) any other securities giving the right to acquire or sell any such transferable securities or

giving rise to a cash settlement determined by reference to transferable securities,

currencies, interest rates or yields, commodities or other indices or measures;

The IIA also refers to “transferable securities” in its list of “investment instruments” where it refers to

“transferable securities including shares, warrants, debentures including debenture stock, loan stock,

bonds, certificates of deposit and other instruments creating or acknowledging indebtedness issued

by or on behalf of any body corporate or mutual body, government and public securities, including

loan stock, bonds and other instruments creating or acknowledging indebtedness issued by or on

behalf a government, local authority or public authority, bonds or other instruments creating or

acknowledging indebtedness, certificates representing securities, [or money market instruments].”

14

Whilst some commentators have taken the view that shares which are not transferable would not fall

within this definition, we consider that view to be reasonably aggressive. At the very least, the

definition under the IIA which we consider to be broader than that under the MiFID Regulations apply

to shares in companies which were capable of transfer, irrespective of whether they were capable of

being negotiated on the capital markets.

It is our view therefore that any Irish entity (or presence in Ireland) which is providing the services of

portfolio management and/or investment advice to third parties on a professional basis in relation to

a portfolio of shares / bonds / debt instruments in companies where those are capable of transfer

(which would normally be the case) is likely to be considered to be carrying on a regulated activity

requiring prior authorisation.

However, as noted above, the commonly held view is that the provision by a general partner of

portfolio management series to a LP is not the provision of services to third parties and therefore

falls outside the regulatory regime. We note that this appears to be the position accepted by the

Central Bank also.

Taxation of Irish Regulated Collective Investment Funds

All Irish regulated funds whether they are constituted as corporate entities or unit trusts are subject

to the same taxation regime so long as they are designated as Investment Undertakings under

Section 739B of the Taxes Consolidation Act, 1997 (as amended) (the “TCA”).

Irish Direct Tax & Withholding Tax

Investment Undertakings (“Funds”) are not subject to Irish taxation on any income or gains they may

realise from their investments. In addition, no withholding tax arises on dividend or interest payments

made by Irish companies to Funds. The exemption in respect of dividend withholding tax in the case

of Funds is subject to a standard declaration being in place.

In addition, there are no Irish withholding taxes in respect of a distribution of payments in respect of

units or any encashment, redemption, cancellation or transfer of units by the Fund in respect of:-

(A) unitholders who are neither Irish resident nor ordinarily resident in Ireland provided either:

(i) they have provided the Fund with the appropriate relevant declaration of non-Irish

residence; or

(ii) the Fund has availed of the Appropriate Equivalent Measures (“AEM”) regime as

introduced by Finance Act 2010 which when applicable effectively removes the need

15

for non-resident declarations (see further below under “Taxation of non-Irish

residents”);

(B) unitholders which fall within the category of exempt Irish investors (e.g. approved pension

schemes, charities, other Funds, etc) who have also made an appropriate relevant

declaration to the fund.

However when a distribution is made by the Fund to Irish resident unitholders (or an ordinarily Irish

resident unitholder) who do not fall within any of the exempt Irish investor categories, or such a

unitholder disposes of units and realises a gain, tax must be deducted by the Fund at a rate of 25%

on distributions (where payments are made annually or at more frequent intervals) or 28% on any

other distribution or gain arising to the unitholder.

Taxation of Irish residents

Irish resident individual investors pay no further tax on distributions made to them unless the units

are denominated in a currency other than euro in which case they may be liable to tax on foreign

currency gains.

Irish corporate unitholders who receive distributions from which tax has been deducted will not be

subject to further Irish tax on the payments received. However where such units are held by the

unitholder on a trading account in connection with a trade then that unitholder will be taxable on any

income or gains (grossed up for any tax deducted) as part of that trade (thereby taxable at 12.5%)

with a set off against corporation tax payable for any tax deducted by the Fund (i.e. set-off for 25% or

28% withholding tax). Such unitholders may also be liable to tax on foreign currency gains as

outlined above.

Any corporate unitholders who receive a payment from a Fund from which tax has not been

deducted will be taxable on that payment at 25% (except where the units are held on a trading

account – see above). However, where the payment is in respect of the cancellation, redemption,

repurchase or transfer of units or the ending of an 8 year period, such income shall be reduced by

the amount of the consideration in money or money’s worth given by the unitholders for the

acquisition of the units. Again such unitholders may also be liable to tax on foreign currency gains.

Taxation of non-Irish residents

As above, there would be no withholding tax on distributions made to non-residents (provided they

complete a non-Irish tax resident declaration) or alternatively the Fund has availed of the AEM

16

regime. The AEM regime is subject to approval by the Irish Tax Authority (“ITA”) but in general

should apply to all Funds which are not actively promoted in Ireland. For Funds that avail of this

exemption, it essentially means that non-resident tax resident declarations would not be required in

respect of non-Irish resident unitholders. For more on the AEM regime please see publication on our

website entitled “Funds - An Alternative to NRDs, Equivalent Measures”.

8 Year Rule

Ireland introduced in 2006 legislation to counteract Irish investors being able to roll-up (indefinitely)

their share of the underlying income and gains of a Fund for more than 8 years. Therefore, every

time an Irish investor invests in a Fund, an 8 year clock starts running in relation to that particular

investment in the Fund and if that investment is not returned before the 8th anniversary of making (or

acquiring) that investment (being shares/units) in the Fund, then certain Irish investors will be taxed

as if they had made a redemption or disposal (at market value) of their investment (being

shares/units) in the Fund and consequently will be taxed on any deemed gain at 28%. This 8 year

rule does not apply to non-Irish resident investors.

Stamp Duty

No stamp duty is payable in Ireland on the issue, transfer, repurchase or redemption of units in a

Fund. Furthermore, no stamp duty is payable by the Fund on the conveyance or transfer of stock or

marketable securities provided that the stock or marketable securities in question have not been

issued by a company registered in Ireland and provided that the conveyance or transfer does not

relate to any immovable real estate situated in Ireland or any right over or interest in such real estate

or to any stocks or marketable securities of a company (other than a company which is a fund) which

is registered in Ireland. Where Irish securities or land is involved, Irish stamp duty will apply.

Where any subscription for or redemption of units is satisfied by the in specie transfer of

securities, real estate or other types of assets, consideration should be given to whether Irish

stamp duty may arise on the transfer of such assets.

VAT

There are wide ranging VAT exemptions with regard to the provision of services to Funds (e.g.

administration, transfer agency, investment management, custodial, etc) and to the extent that a

Fund suffers Irish VAT on certain services it receives (e.g. audit and legal fees) the Fund may

recover this VAT based on its recovery rate. The recovery rate will be based on either (i) the extent

that investments of the Fund are invested outside the EU or (ii) the extent that the investors in the

Fund are located outside the EU. The ITA prefer to base the Fund’s VAT recovery position by

17

reference to where the investments of the Fund are invested, rather than where the investors in the

Fund are located. Nevertheless, whichever basis is used, it must be applied consistently from one

period to the next.

Certain services received from abroad (e.g. the service of non-Irish lawyers or accountants) will

require a Fund to register and self account for VAT in Ireland. However, depending on the Fund’s

VAT recovery rate, the Fund may be able to recover some or all of this Irish VAT (although in respect

of EU investments, no VAT recovery would be available). Once registered for Irish VAT the normal

VAT filing and recording keeping obligations under Irish VAT law will apply.

Compliance requirements

Funds have an obligation to register with the ITA so as to obtain a tax reference number as each

Fund must file bi-annual tax returns. These tax returns should be accompanied by the payment of

appropriate tax (if applicable) for the period in question. On the basis that there are no Irish resident

or ordinarily resident unitholders (or such unitholders are exempt Irish investors) the appropriate tax

should be nil.

Taxation of Irish Limited Partnerships

(i) Direct Tax/Withholding Tax

An Irish 1907 Limited Partnership (the “Partnership”) is treated for Irish tax purposes as “tax

transparent”. The limited partners (rather than the Partnership itself) will be subject to taxation on

their share of underlying income and gains of the Partnership itself. Each limited partner will be

solely responsible for paying any Irish tax due on its own share of the Partnership’s profits or gains.

Effectively, for Irish limited partners, the underlying characteristic of the income and gains earned by

the Partnership will remain unchanged (i.e. the limited partners will be taxed as if they had invested

directly in the underlying securities of the partnership). So to the extent the Partnership has capital

gains, dividends or interest income, Irish tax resident limited partners will be taxed as if they earned

their share of income and gains directly. For Irish tax resident individuals it would mean that capital

gains would be taxed at 25% and dividends and interest income would be taxed at their marginal

rate of income tax (plus applicable levies).

For non-resident limited partners they will also be liable to Irish tax as if they had invested directly

(with one caveat below regarding withholding taxes). Therefore capital gains from the sale of shares

(to the extent those shares do not derive substantially their value from Irish real estate) will not be

18

subject to Irish tax. Any interest income from mezzanine debt (issued by Irish companies) or

dividends from Irish companies would also not be subject to income tax (provided the Partnership

was not regarded as carrying on a trade for Irish tax purposes – that is unlikely but that is a facts

based opinion that needs to be looked at in each case). However, Irish withholding tax may arise in

respect of any dividends and interest payments (made by Irish companies) if they arose to the

Partnership. If such withholding tax was to arise, the non-resident limited partners would have to

obtain a refund of their share of any Irish withholding tax on interest and/or dividend payments by

filing appropriate tax refund claims to Authorities.

(ii) Stamp Tax

Transfers of LP interests in the Partnership are subject to prohibitive Irish stamp duty taxes. It may

be possible to minimize the stamp duty charge with appropriate planning. For the avoidance of

doubt the stamp duty tax we refer to above is a cost for the new LP investor on an acquisition of the

LP interest and not the disponer of the LP interest.

(iii) VAT

One needs to look at the VAT implications in respect of services received by the Partnership as

unlike regulated funds there are no specific VAT exemptions. However, any fees earned by the GP

from the Partnership may be VAT exempt.

(iv) Eight year Rule

The eight year deemed disposal rule does not apply to LPs. This document does not address all

applicable tax issues which need to be considered on a project by project basis. DISCLAIMER: This document is for information purposes only and does not purport to represent legal or tax advice. If you have any queries or would like further information relating to any of the above matters, please refer to the contacts above or your usual contact in Dillon Eustace.

19

Appendix

Regulated Fund Structure Diagram Charts

Regulated Investment Company

Regulated Unit Trusts

Investment Company

Investment Manager

Placing Agent Administrator/ TA

Custodian

Investment Advisor

Global Custodian

Irish Management

Company

Investment Manager

Placing Agent

Administrator/ TA

Trustee

Investment Adviser

Global Custodian

Trust Deed = =

CONTACT US

Our Offices

Dublin 33 Sir John Rogerson’s Quay, Dublin 2, Ireland. Tel: +353 1 667 0022 Fax.: +353 1 667 0042 Boston 26th Floor, 225 Franklin Street, Boston, MA 02110, United States of America. Tel: +1 617 217 2866 Fax: +1 617 217 2566 New York 245 Park Avenue 39th Floor New York, NY 10167 United States Tel: +1 212 792 4166 Fax: +1 212 792 4167 Tokyo 12th Floor, Yurakucho Itocia Building 2-7-1 Yurakucho, Chiyoda-ku Tokyo 100-0006, Japan Tel: +813 6860 4885 Fax: +813 6860 4501 e-mail: [email protected] website: www.dilloneustace.ie

Contact Points

Date: October 2010 For more details on how we can help you, to request copies of most recent newsletters, briefings or articles, or simply to be included on our mailing list going forward, please contact any of the team members below. Andrew Bates e-mail: [email protected] Tel : +353 1 667 0022 Fax: + 353 1667 0042 DISCLAIMER: This document is for information purposes only and does not purport to represent legal or tax advice. If you have any queries or would like further information relating to any of the above matters, please refer to the contacts above or your usual contact in Dillon Eustace. Copyright Notice: © 2010 Dillon Eustace. All rights reserved.