Embed Size (px)

Citation preview

A COMPREHENSIVE STUDY OF MARBLE INDUSTRY IN AFGHANISTAN

Abdul Ghafar Rassin

April 2012

Research & Statistics Department Afghanistan Investment Support Agency

Research & Statistics Department, AISA

ii

The views expressed in this paper are those of the author and do not necessarily reflect the official position of AISA (Afghanistan Investment Support Agency).

Research & Statistics Department, AISA

iii

Acknowledgement

This paper reflects the work, ideas, and generosity of many individuals and organizations within the Afghan government and particularly at Afghanistan Investment Support Agency (AISA).

At AISA, I would like to thank the top management, especially Naseem Akbar the Acting CEO, for their continuous support to the Research & Statistics department. I should express my gratitude to all colleagues in the department, particularly to Omar Joya and Mir Tawfiq Ansari who provided insightful comments and guidance throughout this study.

At the Ministry of Mines, my special thanks go to Marzia Akbari for her endless cooperation with our department, to Sayed Zaman Hashemi for supplying us information on legal aspects, and to the staff of Cadastre department.

At AMGPA (Afghanistan Marble Granite Processing Association), I am especially grateful to Engineer Rahmatullah Rahmat and Haji Kamali who frequently provided me with helpful information. I should acknowledge that without Engineer Rahmat’s help, this report would not have been as informative at it is now.

At AMIA (Afghanistan Marble Industry Association), my great appreciation goes to Nasim Doost and Mr. Mohebi for sharing all information that helped me to complete this report. I also thank Mr. Daqiq who explained in every detail the marble process at the factory of Nasim Doost.

Finally, Daryosh Tabesh, Ahmad Shah Momin, Abdul Samad Katawazy and Qudratullah Halimi have assisted in the research through surveys, onsite visits, and data collection, to whom I am grateful.

Abdul Ghafar Rassin

Research & Statistics Department, AISA

iv

Executive Summary

Since 2003, there have been huge private investments in Afghanistan – $1.8 billion foreign and $3.8 billion domestic investments. Most of these investments are allocated to the construction, telecommunications, banking, and transportation sectors. Other industries, such as the marble and granite industry, despite having huge potential for investors, have been overlooked. Therefore this report thrived to examine the hypothesis that those industries which received no attention from the government and investors – in this case the marble industry – have good potential to grow and can have high return for investors.

The objectives of this paper are to study the market structure and performance of marble industry, to look at the potential opportunities from an investor’s prospective, to identify the constraints and factors of market failure, and to finally recommend measures and actions for the development of this industry.

In order to serve the objectives of this paper, we relied in my methodology on using the SCP (structure-conduct-performance) model to study the market structure and performance, whilst we employed a more general approach for the identification of market opportunities and constraints. Data and information was collected through onsite visits to businesses and factories, interviews and discussions with business owners, heads of associations and officials at the Ministry of Mines, and previous studies and reports made on marble industry in Afghanistan and in the neighbouring countries.

The paper argues that given the strong growth of the global market for marble and the increasing demand in most regions of the world, there is strong potential for marble exports – and thus production – in Afghanistan. Estimates show that the annual growth rate of marble production in the world is over 8 percent. Average world annual production of marble is over 100 million metric tonnes and world consumption is equivalent to $40 billion. Almost half of world’s marble output is consumed in the Middle East, Far-East and in European countries.

The Afghan marble industry has grown by 60 percent since 2008, and it should be a good reason for the government to place this sector at its top priority for support. Based on the data collected by the Ministry of Mines, our projections show that marble industry in Afghanistan in terms of number of employees, size of production, and share in GDP could grow fivefold over the next five years. However, these projections are based on some hypotheses discussed in Chapter 4 of this paper under the Recommendations.

Using an SCP model, we found that although the marble industry is fragmented in Afghanistan, few big players control the market price. Due to lack of competition – which is the result of a non-efficient market structure – firms’ performance and conduct

Research & Statistics Department, AISA

v

are not desirable; while their prices are very high, the quality of their finished products in terms of polishing and finishing is dire. As a result, Afghan market is dominated by foreign products. Moreover, there is no tendency among the Afghan firms to acquire new technology and to improve their industrial and marketing management.

To resolve all these problems arising from market deficiencies, the paper recommends that the government (i.e. Ministry of Mines and Ministry of Finance) provide incentives for firms operating in marble quarrying to increase their output and acquire technological upgrading. Since the supply chain for marble production has two major stages, namely quarrying and processing, any incentive designed to increase the production will result for firms operating in both quarrying and processing to employ standard and more modern technology (to be able to produce more). An increased supply of goods at the first stage of supply chain will increase the supply of goods at the latter stage. Thus, the processing plants will equally employ more standard technology to catch up with the extra supply of quarrying firms. When the amount of final product in the market is increased, the prices will fall. The incentive to encourage quarrying firm to increase production will have the following effects:

Fall in the prices – this can increase share of Afghan firms in domestic markets Usage of more standard and modern technology which increases productivity of

Afghan firms, and allow them to benefit from economies of scale Increase quality of Afghan products due to the usage of standard machinery, this

in turn may increase the exports of Afghan marble at the global market Finally, increase competitiveness of Afghan firms (through higher quality and

lower prices)

To identify investment opportunities and constraints in the marble industry in Afghanistan, we look at the marble market from supply and demand prospective. Over half of the world marble output is consumed in regional and European countries, and Afghanistan can potentially supply these markets – given the unique quality of Afghan marbles. Almost 85 percent of domestic market is dominated by Pakistani marble; this is only due to lower prices. Therefore, there is huge external and internal market for Afghan marble products. However, looking from the supply side, despite the fact that Afghanistan has almost infinite reserves of best quality marble, the industry is still very small. The main constraints are attached to the factors of production; shortage of land for processing plants, lack of skilled labour, lack of capital, lack of technology and modern machinery, and finally lack of entrepreneurial skills. In order to respond to these constraints, the paper recommends various institutional arrangements (such as creating an independent agency for the development of industrial parks, providing capital to firms in need of liquidity, establishing training schools for mining workers, etc.).

Research & Statistics Department, AISA

vi

AISA Afghanistan Investment Support Agency

List of abbreviations

AMGPA Afghanistan Marble Granite Processing Association

AMIA Afghanistan Marble Industry Association

BGS British Geological Survey

DFID Department for International Development EPAA Export Promotion Agency of Afghanistan

GDP Gross Domestic Product

MoM Ministry of Mines

R&D Research and Development

SCP Structure-Conduct-Performance

UNDP United Nation Development Program

USAID United States Agency for International Development

USGS United State Geological Survey

Note: The conversion rate used in this paper for converting Afghanis to US dollars is AFN 50 = $1.

A billion means a thousand million.

Research & Statistics Department, AISA

vii

Contents Pages

• Introduction 1 • Methodology 2

Chapter One 1. Overview of marble industry 3

1.1 The world marble markets 4

1.2 Regional markets 6

1.3 Pakistan marble industry 7

1.4 Afghanistan marble industry 8

1.5 Comparison of Afghanistan and Pakistan marble industries 10

1.7 Five years projection of Afghan marble industry 11

Chapter Two

2. Market Analysis 12 2.1 Market structure 13

• Number and size distribution of firms

• Type of product

• Ease of entry and exit

• Information flow between buyers and sellers

• Vertical integration

• Control over prices by established firms 2.2 Firms conduct 14

• Policy objectives

• Pricing objectives

• Marketing strategy

• Research and development

2.3 Firms performance 15 • Profit margin

• Efficiency

Research & Statistics Department, AISA

viii

• Product quality

Chapter Three

3. Market Opportunities 19 3.1 Raw materials 20

3.2 Demand within internal and external markets 22

4.2 Factors of production 24

• Land

• Labour

• Capital

• Entrepreneurial skills

• Technology

Chapter Four

4. Recommendations 31 4.1 Role of government 32

4.2 Role of private sector 34

4.3 Role of donors 35

5. Conclusion 37 6. References 38

Appendix A List of marble association members

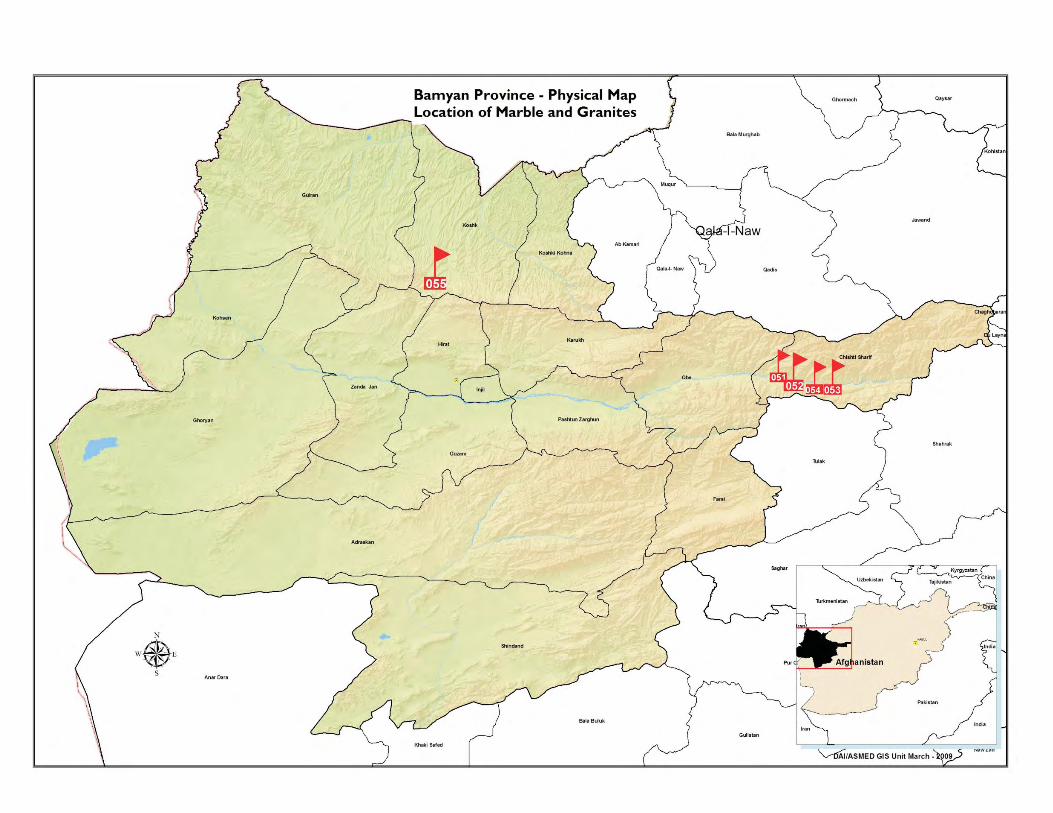

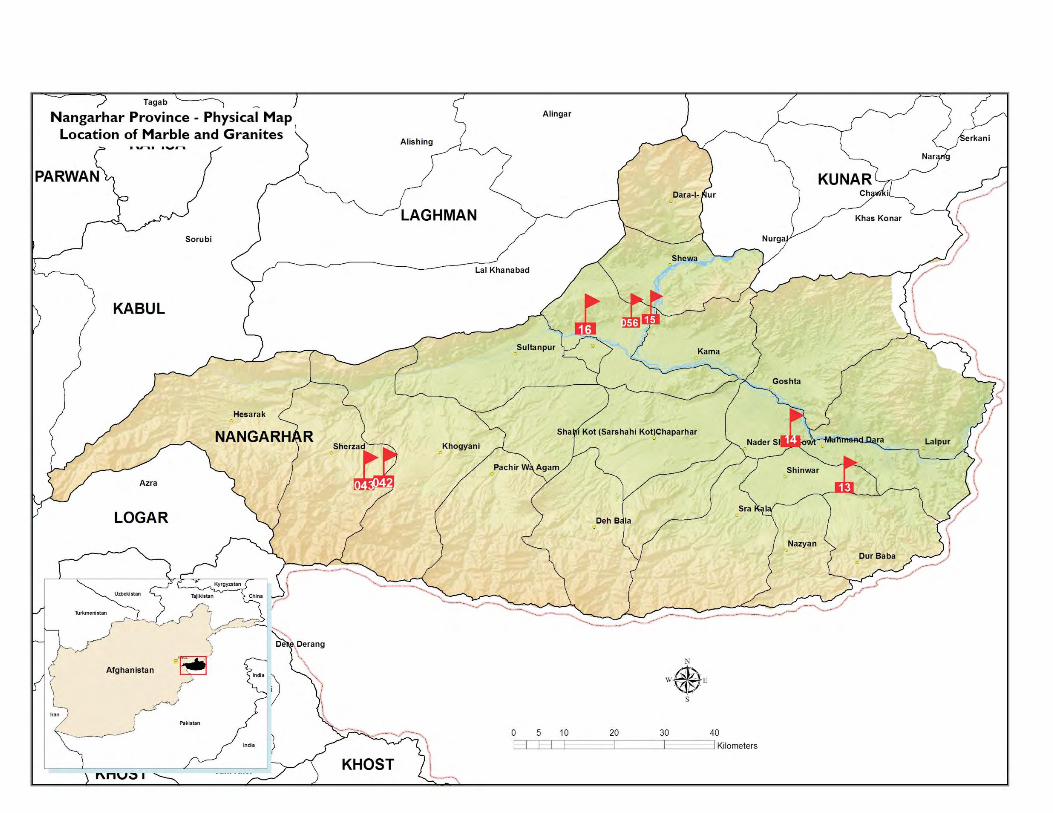

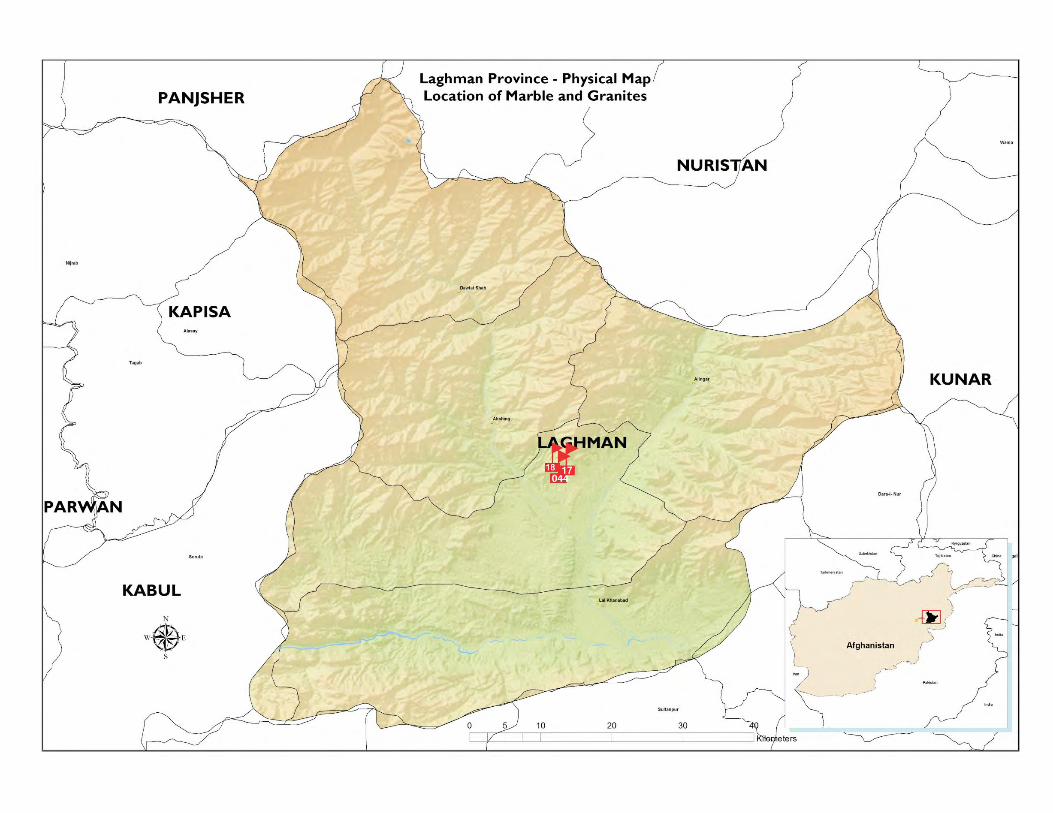

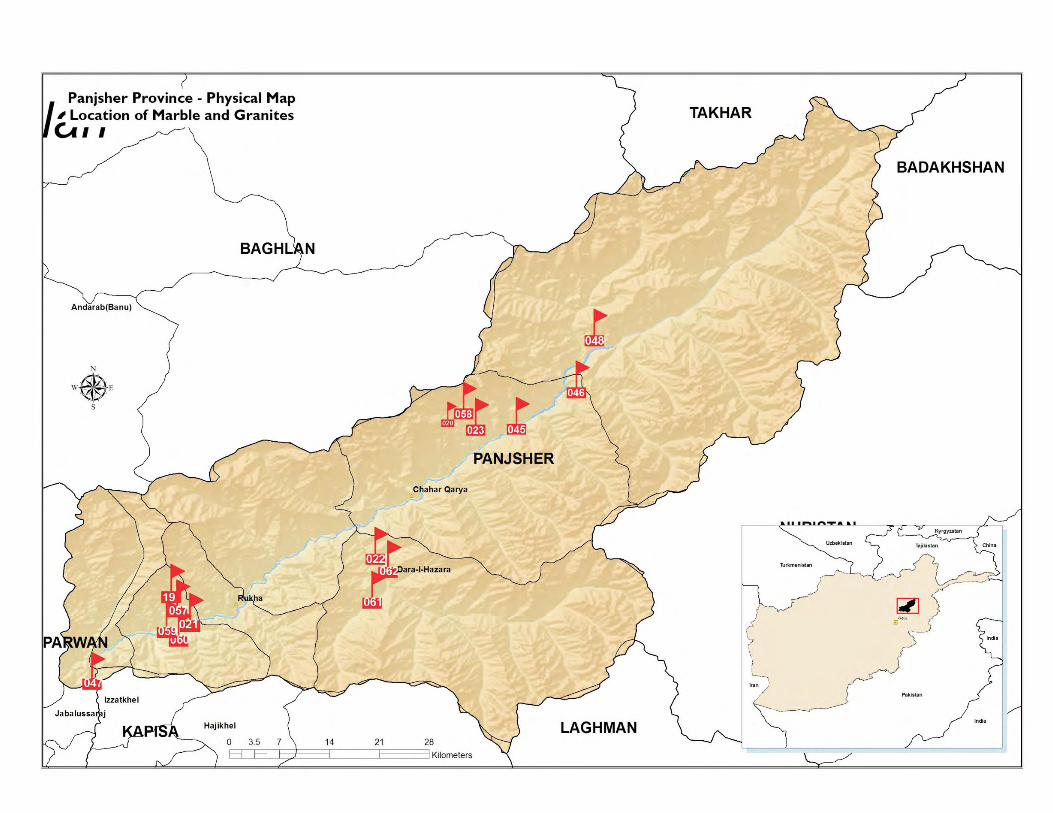

Appendix B Calculations Appendix C Location of marble reserves throughout Afghanistan

Research & Statistics Department, AISA

1

I. Introduction Thirty years of war not only destroyed the physical infrastructures in Afghanistan

but also eradicated the regulatory, social, political and economic institutions which guarantee for an efficient environment for investment. Fortunately, since the fall of Taliban regime in 2001, the government has been engaged in establishing and developing the institutional requirements and arrangements which are necessary for investors to do business in Afghanistan. As a result, many investment opportunities heaved up in the country and investors are increasingly investing in all sectors. However, some sectors such as construction, telecommunications, banking, and transportation sectors have received most of the investments, whereas other potential sectors – such as marble production – have not attracted much attention.

There are many papers and reports, written by various institutions, which address the quality and quantity of Afghan marble. ASMED (2010), Afghanistan Marble Industry Directory, argues that Afghanistan has over 400 varieties of marble with total value of around $150 billion up to $200 billion. Mitchell (2008) discusses the size of marble reserves in Afghanistan, and asserts that Afghanistan can supply marble to regional and international markets almost for indefinite period of time. This means that Afghanistan has endless amount of marble reserves. Moreover, other studies such as the OTF Group (2006), Stephen (2007) and EPAA (2006) discussed the potential of marble industry in Afghanistan that can be a driving force of the Afghan economy. The paper by Yahya (2009), using Porter’s Diamond Analysis model, found a series of problems such as absence of cluster. His paper thoroughly analysed the weakness and strength of Afghan marble industry. The model he employed was a management model – more helpful for existing firms to draw strategy for future.

These studies also addressed the issues that marble industry faces in a crude way. A critical assessment of these reports would suggest that they all focus on the quality, quantity and the potential demand and supply of Afghan marble within domestic and foreign markets. Neither these reports rigorously study the market characteristics in order to find all underlying problems that curb potential growth of the industry; nor do they look at the market from an investor’s perspective, by adopting a clear cost-benefit approach or simply explaining the profitability of this business for investors.

This paper, however, touches to those issues which are left undiscussed by previous studies. The main objectives of this paper are to:

• understand the overall nature of marble business in the world, regional and Afghan markets;

• study the characteristics of the marble industry in Afghanistan, particularly the market structure and performance;

Research & Statistics Department, AISA

2

• identify potential investment opportunities in marble industry, by taking a clear cost-benefit approach and demonstrating the profitability of this business from an investor’s viewpoint;

• have recommendations to both public and private actors in order to correct market deficiencies and to improve the market conditions to reach its optimal productivity, competitiveness and profitability.

The perceived value of this paper is to get a clear picture of current marble business, both from an investor’s prospective to invest in Afghanistan and from the governments prospective to support the industry.

The next section explains the methodology used in this paper for studying the marble industry. Chapter 1 makes an overview of marble business in the world and in the region. Chapter 2 studies the marble market in Afghanistan, mainly the market structure and performance. Chapter 3 looks at potential investment opportunities in Afghanistan for marble production. Chapter 4 presents some recommendations to both public and private actors for further enhancement of the marble market in Afghanistan. Finally, the last section concludes this paper.

II. Methodology

The methodology employed in this paper is based on two distinct approaches. Chapter 2 uses the SCP (Structure-Conduct-Performance) model to study the structure and performance of the marble market in Afghanistan. The SCP model is usually used to analyze the relation among firms’ performance, firms’ conduct, and market structure. The model states that market structure determines the firms’ conduct, and thereby sets the level of firm’s performance. On the other hand, firms’ performance is determined by their conduct, which in return depends on market structure. However, in this paper, we do not focus on the nature of relation between the market structure and firms’ conduct and performance. Instead, we simply use the SCP model to study the basic market characteristics.

On the other hand, Chapter 2 adopts a clear cost-benefit approach to identify the market opportunities. It looks at basic supply and demand conditions of the market and determines the profitability of the business from an investor’s perspective.

For the data collection, we relied on both primary research through field surveys and on secondary research on previous studies and reports. For field surveys, we visited marble processing units and marble quarrying sites in Kabul, Nangarhar and Herat provinces. Interviews and discussions with marble associations and MoM’s officials were another main source of information. To find out how much the Afghan marble industry has the potential for growth in terms of value addition and employment opportunities, we will gather the required information and present them in conclusive manner.

Research & Statistics Department, AISA

3

Chapter 1:

An overview of world marble industry

Research & Statistics Department, AISA

4

1. An overview of world marble industry

This section first talk about the world marble industry in terms of total production, total consumption, and rate of growth, and will find out the top dominant countries in the global marble market. In the second step, the paper will study the regional market for marble production including Afghanistan. By using a supply and demand model, we can get insight into the potential of this industry.

1.1. The world marble market

According to Mehdi (2006), the world total production of marble and granite reaches over 100 million tons and total consumption is valued about $40 billion per year. In 2010, the world export value of marble and granite was $62 billion. Since 1999, world marble production grew at a high rate of 8.7 percent and the industry is expected to grow over 8 percent till 2025.

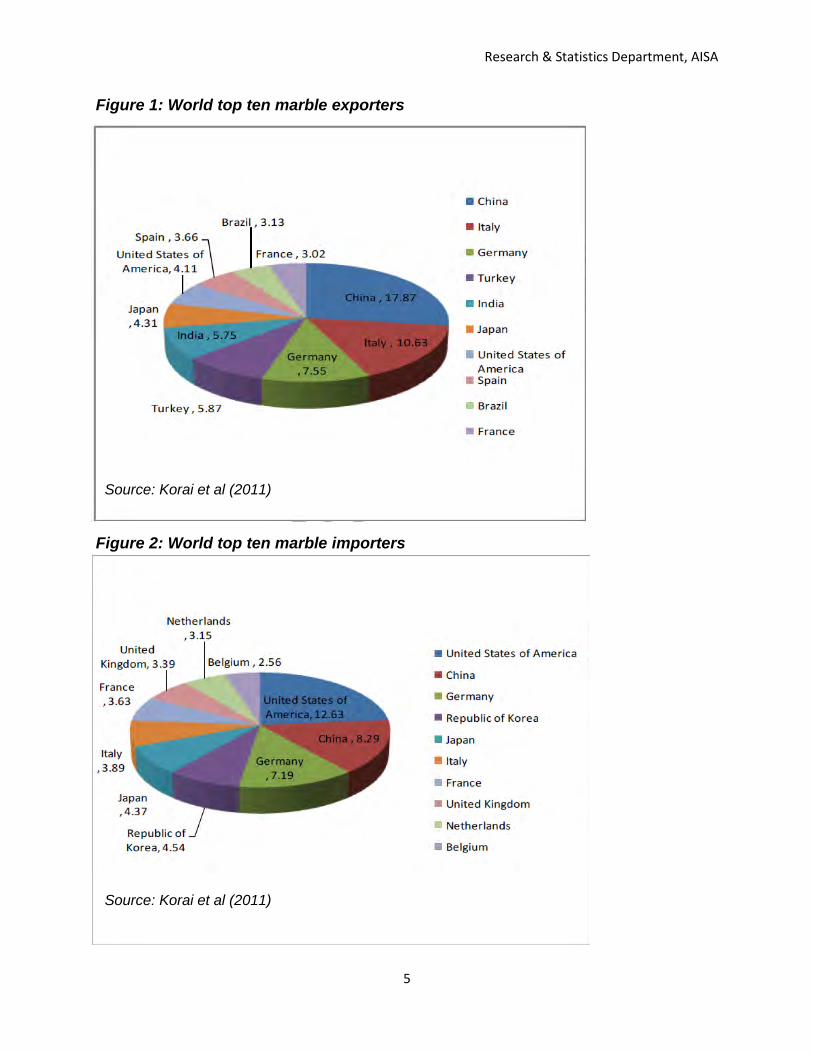

Marble and granite are produced in more than 40 countries in the world. Italy, Turkey, Spain, India and China are the top five dominant countries in terms of marble production. These countries control over half of the world market – only Italy produces over 17 percent of world marble. A major part of production is consumed locally by producing countries, and only a small percentage of total production is exported. This fact indicates that local supply of marble remains less costly, while the transportation cost increases the price of exported marble products. Therefore, Afghan firms can win the domestic market with least effort. Figure 1 and 2 show world top ten marble exporters and importers.

Research & Statistics Department, AISA

5

Figure 1: World top ten marble exporters

Source: Korai et al (2011)

Figure 2: World top ten marble importers

Source: Korai et al (2011)

Research & Statistics Department, AISA

6

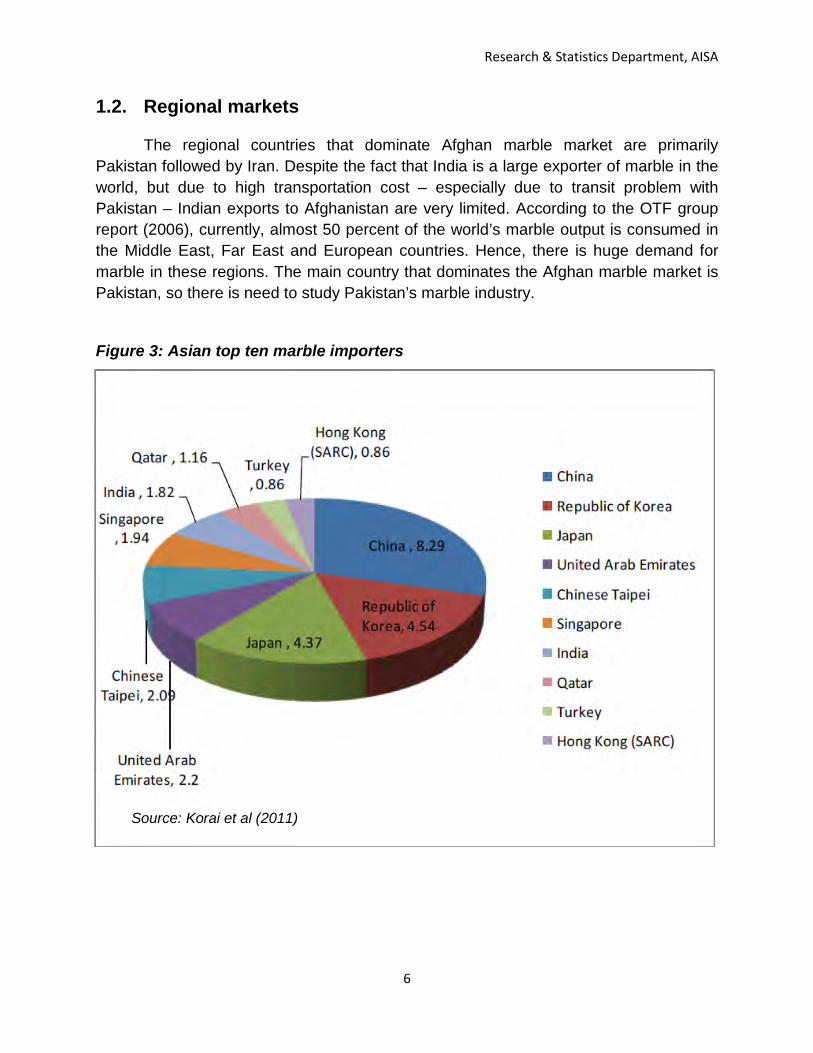

1.2. Regional markets

The regional countries that dominate Afghan marble market are primarily Pakistan followed by Iran. Despite the fact that India is a large exporter of marble in the world, but due to high transportation cost – especially due to transit problem with Pakistan – Indian exports to Afghanistan are very limited. According to the OTF group report (2006), currently, almost 50 percent of the world’s marble output is consumed in the Middle East, Far East and European countries. Hence, there is huge demand for marble in these regions. The main country that dominates the Afghan marble market is Pakistan, so there is need to study Pakistan’s marble industry.

Figure 3: Asian top ten marble importers

Source: Korai et al (2011)

Research & Statistics Department, AISA

7

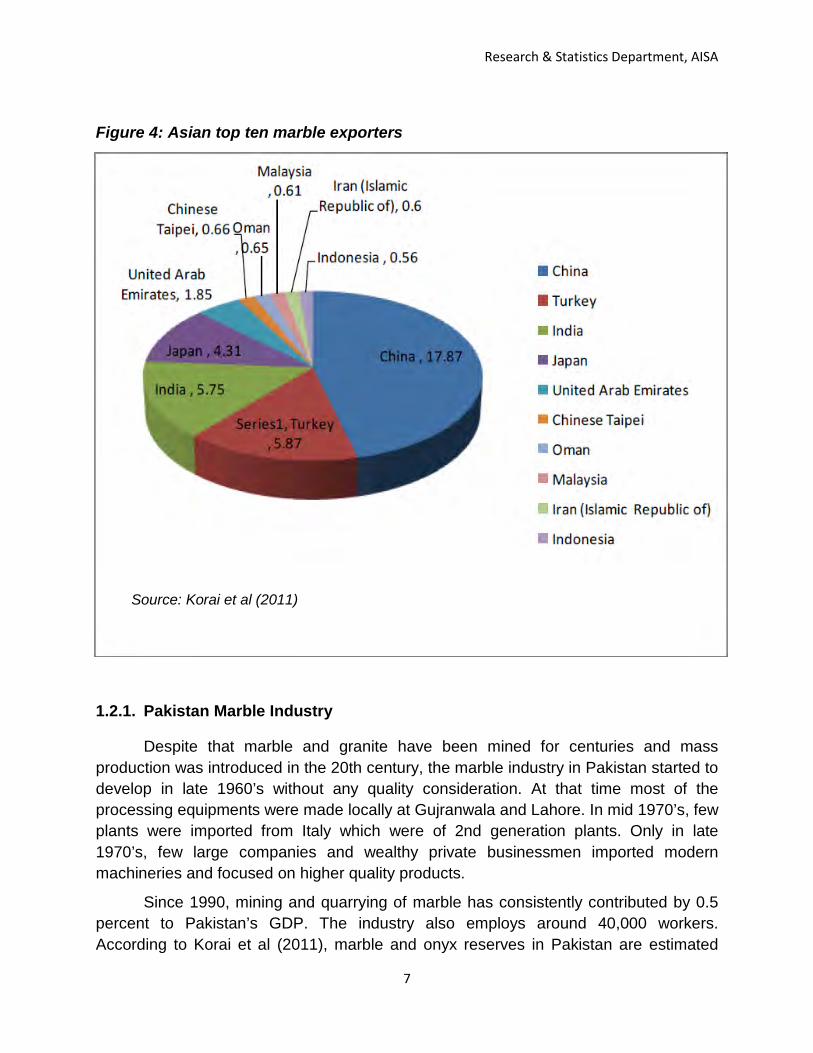

Figure 4: Asian top ten marble exporters

Source: Korai et al (2011)

1.2.1. Pakistan Marble Industry

Despite that marble and granite have been mined for centuries and mass production was introduced in the 20th century, the marble industry in Pakistan started to develop in late 1960’s without any quality consideration. At that time most of the processing equipments were made locally at Gujranwala and Lahore. In mid 1970’s, few plants were imported from Italy which were of 2nd generation plants. Only in late 1970’s, few large companies and wealthy private businessmen imported modern machineries and focused on higher quality products.

Since 1990, mining and quarrying of marble has consistently contributed by 0.5 percent to Pakistan’s GDP. The industry also employs around 40,000 workers. According to Korai et al (2011), marble and onyx reserves in Pakistan are estimated

Research & Statistics Department, AISA

8

more than 300 billion tons. There are around 17 active quarries and 1600 processing plants. Around 150 to 160 processing plants are equipped with appropriate machineries (Korai et al, 2011). By producing more than 900,000 tons of marble, Pakistan only contributes by 1 percent to world total production. In 2010, Pakistan’s marble and granite exports reached $60 million.

1.2.2. Afghanistan Marble Industry

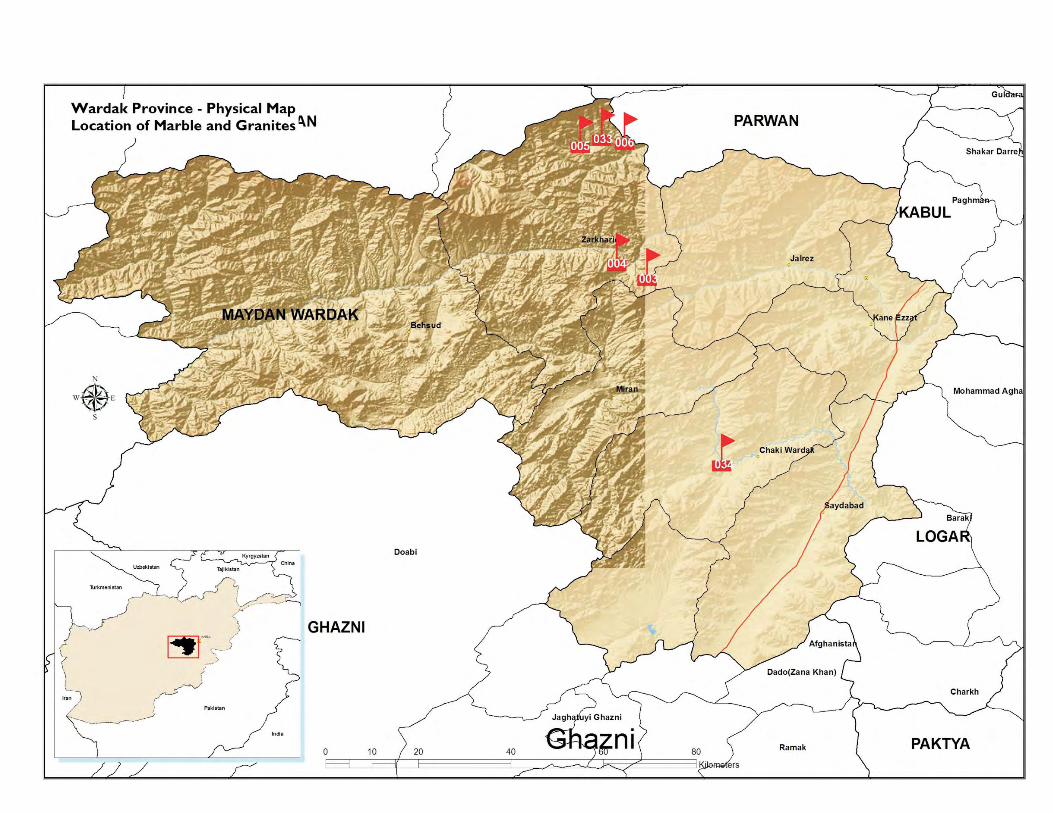

According to Mitchell (2008) Afghanistan has the potential to supply Middle Eastern and Asian markets with an almost unlimited amount of marble. It is important to mention that, as of now, not all Afghan marble deposits are discovered or surveyed properly. According to some unverified reports, total estimated marble deposits in Afghanistan reach over 9 billion tons as described in Table 1 below.

The US geological survey has discovered 66 marble and granite reserves in Afghanistan, which are shown in Table 2 below.

Table 1: Estimated marble reserves in Afghanistan

Province Marble (million m3)

Granite (million m3)

Wardak 1,500 / Jalalabad 3,500 / Bamyan / 2,400 Badakhshan 1,300 Herat 30 / Helmand 300 / Others 2,500 / Total 9,130 2,400

Table 2: Number of marble and granite reserves per province

Kabul Parwan Nangarhar Wardak Bamyan Panjshir Laghman Herat Balkh

13 (M) 4 (T) 1 (OX)

5 (M) 2 (G)

2 (M) 1 (G)

3 (TRA)

2 (M) 3 (G)

5 (TRA) 8 (M) 7 (G)

2 (M) 1 (G)

4 (M) 1(OT)

1 (M)

Source: USGS, GPS Survey 2009 M: marble; G: granite; TRA: travertine; OX: onyx; OT: others Figures in front of the brackets are number of reserves.

Research & Statistics Department, AISA

9

Afghanistan annual marble production is around 124,000 to 155,000 tons. But over half of unprocessed marble goes to Pakistan and Iran. Total consumption of finished marble in Afghanistan is around 270,000 tons. Around 80 to 85 percent of Afghan market is dominated by Pakistani marble. Currently the total value added of the Afghan marble industry is around $105 million which makes 0.6 percent of GDP

According to the Minister of Mines, Wahidullah Shahrani, “Afghanistan marble boasts more than 100 high quality varieties, spanning diverse colors and patterns. Current marble exports are estimated at $15 million per year. With improved extraction, processing, infrastructure, and investments, the industry could grow into a $450 million per year business” (US embassy, 2010)

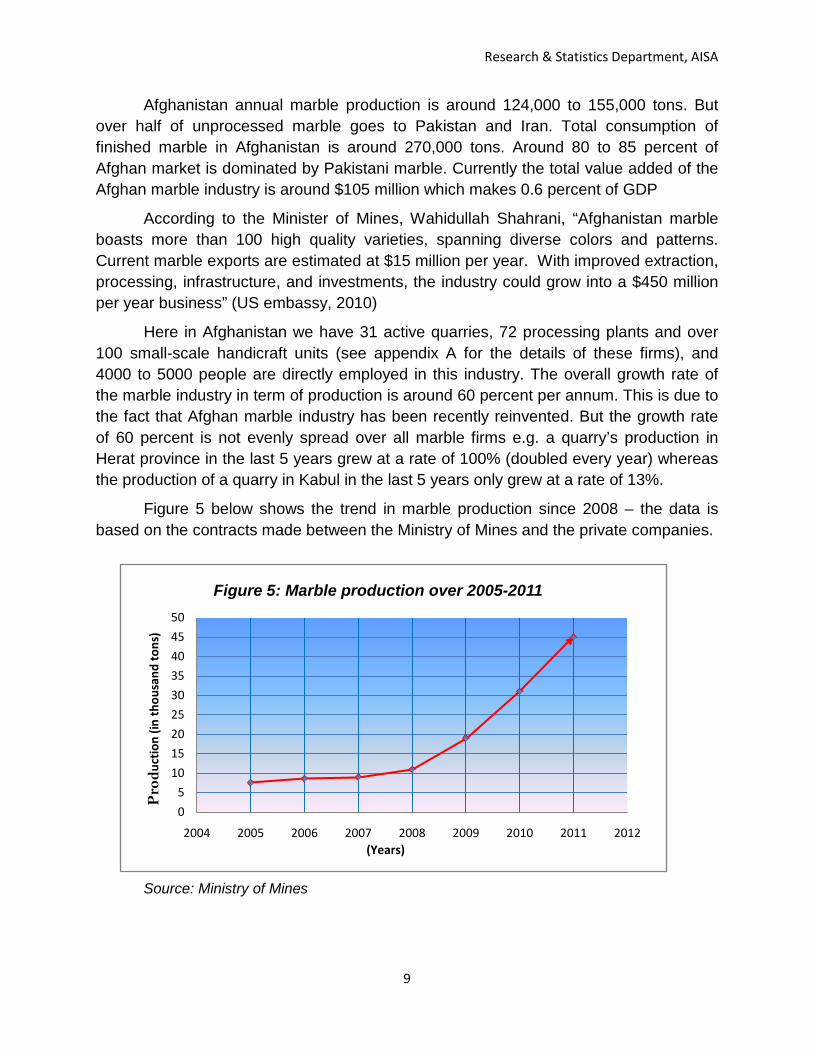

Here in Afghanistan we have 31 active quarries, 72 processing plants and over 100 small-scale handicraft units (see appendix A for the details of these firms), and 4000 to 5000 people are directly employed in this industry. The overall growth rate of the marble industry in term of production is around 60 percent per annum. This is due to the fact that Afghan marble industry has been recently reinvented. But the growth rate of 60 percent is not evenly spread over all marble firms e.g. a quarry’s production in Herat province in the last 5 years grew at a rate of 100% (doubled every year) whereas the production of a quarry in Kabul in the last 5 years only grew at a rate of 13%.

Figure 5 below shows the trend in marble production since 2008 – the data is based on the contracts made between the Ministry of Mines and the private companies.

Source: Ministry of Mines

05

101520253035404550

2004 2005 2006 2007 2008 2009 2010 2011 2012

Pro

duct

ion

(in th

ousa

nd to

ns)

(Years)

Figure 5: Marble production over 2005-2011

Research & Statistics Department, AISA

10

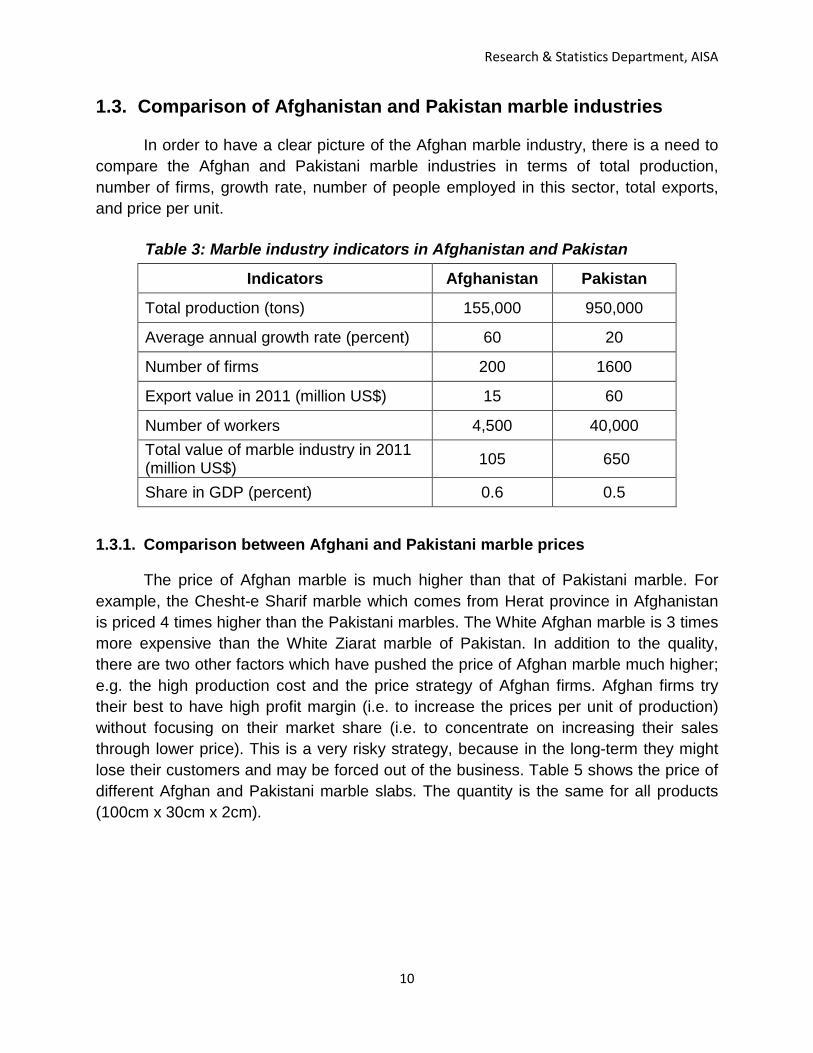

1.3. Comparison of Afghanistan and Pakistan marble industries

In order to have a clear picture of the Afghan marble industry, there is a need to compare the Afghan and Pakistani marble industries in terms of total production, number of firms, growth rate, number of people employed in this sector, total exports, and price per unit.

1.3.1. Comparison between Afghani and Pakistani marble prices

The price of Afghan marble is much higher than that of Pakistani marble. For example, the Chesht-e Sharif marble which comes from Herat province in Afghanistan is priced 4 times higher than the Pakistani marbles. The White Afghan marble is 3 times more expensive than the White Ziarat marble of Pakistan. In addition to the quality, there are two other factors which have pushed the price of Afghan marble much higher; e.g. the high production cost and the price strategy of Afghan firms. Afghan firms try their best to have high profit margin (i.e. to increase the prices per unit of production) without focusing on their market share (i.e. to concentrate on increasing their sales through lower price). This is a very risky strategy, because in the long-term they might lose their customers and may be forced out of the business. Table 5 shows the price of different Afghan and Pakistani marble slabs. The quantity is the same for all products (100cm x 30cm x 2cm).

Table 3: Marble industry indicators in Afghanistan and Pakistan

Indicators Afghanistan Pakistan

Total production (tons) 155,000 950,000

Average annual growth rate (percent) 60 20

Number of firms 200 1600

Export value in 2011 (million US$) 15 60

Number of workers 4,500 40,000 Total value of marble industry in 2011 (million US$) 105 650

Share in GDP (percent) 0.6 0.5

Research & Statistics Department, AISA

11

1.4. Five year projection of Afghan marble industry

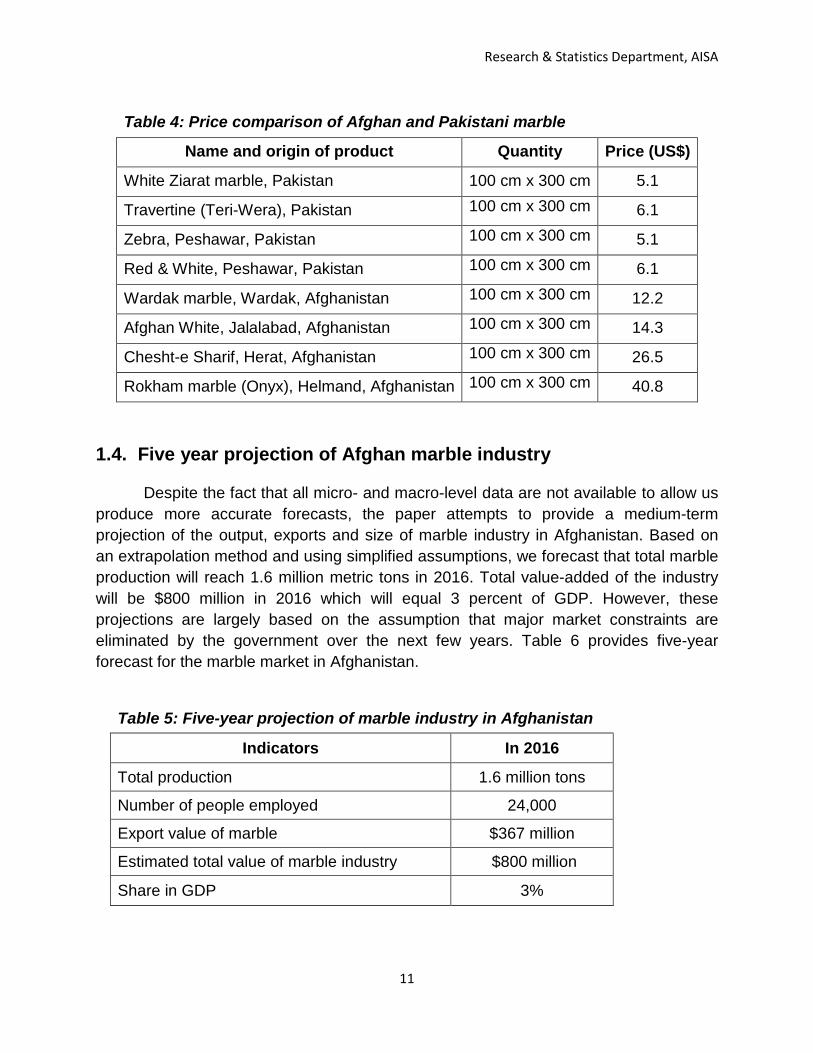

Despite the fact that all micro- and macro-level data are not available to allow us produce more accurate forecasts, the paper attempts to provide a medium-term projection of the output, exports and size of marble industry in Afghanistan. Based on an extrapolation method and using simplified assumptions, we forecast that total marble production will reach 1.6 million metric tons in 2016. Total value-added of the industry will be $800 million in 2016 which will equal 3 percent of GDP. However, these projections are largely based on the assumption that major market constraints are eliminated by the government over the next few years. Table 6 provides five-year forecast for the marble market in Afghanistan.

Table 4: Price comparison of Afghan and Pakistani marble

Name and origin of product Quantity Price (US$)

White Ziarat marble, Pakistan 100 cm x 300 cm 5.1

Travertine (Teri-Wera), Pakistan 100 cm x 300 cm 6.1

Zebra, Peshawar, Pakistan 100 cm x 300 cm 5.1

Red & White, Peshawar, Pakistan 100 cm x 300 cm 6.1

Wardak marble, Wardak, Afghanistan 100 cm x 300 cm 12.2

Afghan White, Jalalabad, Afghanistan 100 cm x 300 cm 14.3

Chesht-e Sharif, Herat, Afghanistan 100 cm x 300 cm 26.5

Rokham marble (Onyx), Helmand, Afghanistan 100 cm x 300 cm 40.8

Table 5: Five-year projection of marble industry in Afghanistan

Indicators In 2016

Total production 1.6 million tons

Number of people employed 24,000

Export value of marble $367 million

Estimated total value of marble industry $800 million

Share in GDP 3%

Research & Statistics Department, AISA

12

Chapter 2:

Market analysis

Research & Statistics Department, AISA

13

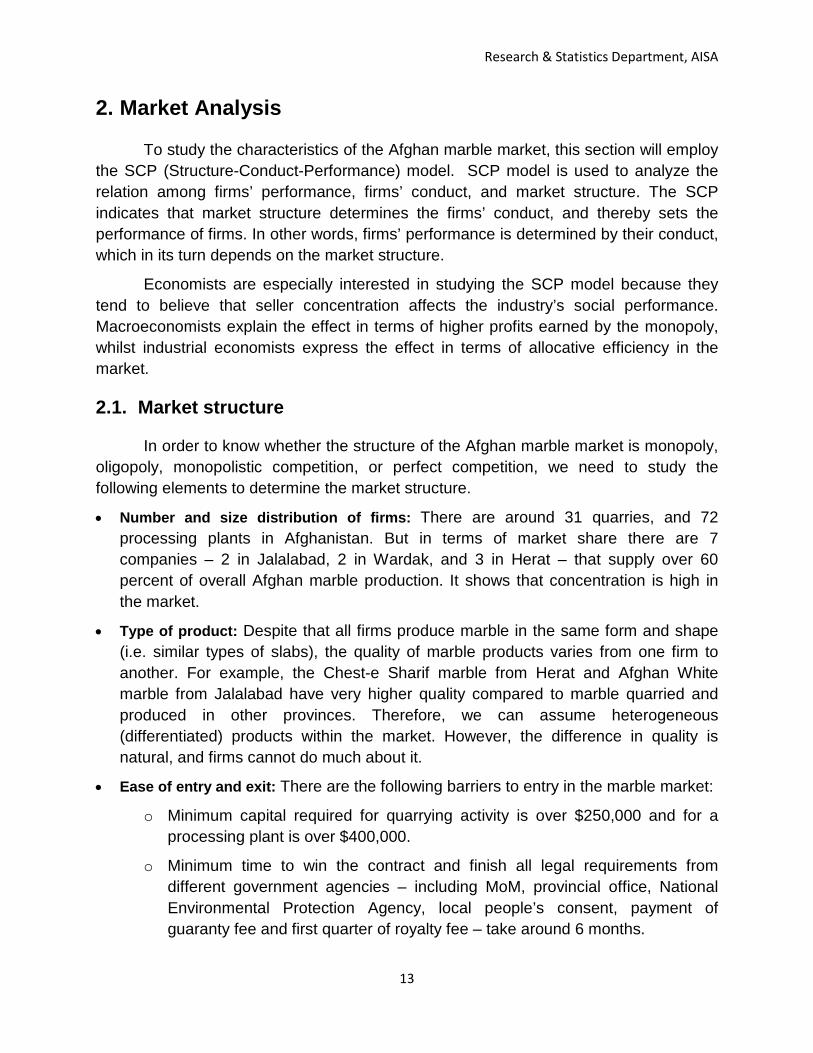

2. Market Analysis

To study the characteristics of the Afghan marble market, this section will employ the SCP (Structure-Conduct-Performance) model. SCP model is used to analyze the relation among firms’ performance, firms’ conduct, and market structure. The SCP indicates that market structure determines the firms’ conduct, and thereby sets the performance of firms. In other words, firms’ performance is determined by their conduct, which in its turn depends on the market structure.

Economists are especially interested in studying the SCP model because they tend to believe that seller concentration affects the industry’s social performance. Macroeconomists explain the effect in terms of higher profits earned by the monopoly, whilst industrial economists express the effect in terms of allocative efficiency in the market.

2.1. Market structure

In order to know whether the structure of the Afghan marble market is monopoly, oligopoly, monopolistic competition, or perfect competition, we need to study the following elements to determine the market structure.

• Number and size distribution of firms: There are around 31 quarries, and 72 processing plants in Afghanistan. But in terms of market share there are 7 companies – 2 in Jalalabad, 2 in Wardak, and 3 in Herat – that supply over 60 percent of overall Afghan marble production. It shows that concentration is high in the market.

• Type of product: Despite that all firms produce marble in the same form and shape (i.e. similar types of slabs), the quality of marble products varies from one firm to another. For example, the Chest-e Sharif marble from Herat and Afghan White marble from Jalalabad have very higher quality compared to marble quarried and produced in other provinces. Therefore, we can assume heterogeneous (differentiated) products within the market. However, the difference in quality is natural, and firms cannot do much about it.

• Ease of entry and exit: There are the following barriers to entry in the marble market:

o Minimum capital required for quarrying activity is over $250,000 and for a processing plant is over $400,000.

o Minimum time to win the contract and finish all legal requirements from different government agencies – including MoM, provincial office, National Environmental Protection Agency, local people’s consent, payment of guaranty fee and first quarter of royalty fee – take around 6 months.

Research & Statistics Department, AISA

14

o Minimum time to set up machineries and build office on quarry site is around 6 months which makes the total time spent around a year.

o Once you bid for a quarry contract, there is no guaranty that you will win – most bidders have no intention to extract marble but to win the contract and then resell it to others, or even to just sabotage the bidding process.

o You have to get the consent of local people; mostly the quarry plant must pay to local influentials

• Exit barriers: To exit the market, a firm bears the following costs:

o It is difficult to sell second-hand machineries at a good price – there is no market for specialized second-hand machineries in Afghanistan.

o The network you build over the years will vanish.

o The government does not pay for the infrastructure you built at your quarrying site.

• Information flow between buyers and sellers: there is no perfect information flow between the buyers and the sellers in both activities (quarrying and processing). The sellers don’t focus on consumer needs as they have inward looking strategy instead of outward focus.

• Vertical integration: Mostly large producers of primary marble products (i.e. quarry firms) own downstream firms with processing, polishing, finishing and distribution activities. But those firms that only process more often face difficulties such as lack of supply from quarry firms.

• Control over prices by established firms: The biggest producers not only use their market power but they also use other instruments to control the market price. For example, the biggest producers are influential members of marble associations (director, deputy director, and management member), and therefore they engage in price setting activities.

Despite that there are numerous firms; only few have over 60 percent of market share. Products are differentiated, entry-exit condition is limited, information flow is imperfect, and firms engage in a price-setting mechanism. Therefore, the Afghan marble market is close to an oligopoly.

2.2. Firms conduct

In this section, the objective is to study the conduct of firms (both quarries and processing plants) in terms of policy objective, pricing strategies, marketing strategies, and R&D activities. Furthermore, to evaluate the question that how market structure affects the way the firms compete.

Research & Statistics Department, AISA

15

• Policy objectives: Unfortunately, firms in this market are short-sighted – their main objective and focus is instant profit. They have no long-term plan for growth and market share. This is why 80 to 85 percent of Afghan market is dominated by Pakistani marbles.

• Pricing objectives: This study found that firms in marble market have no other strategy for pricing except to adopt a price discrimination policy. These strategies give them the chance to earn higher profits than what they would have received if they had a competitive pricing strategy. However, with such a strategy, they will lose a large number of their customers in the long-run.

• Marketing strategy: Firms in this industry neither have market research nor effective advertising activities. Mostly the managers and owners of marble firms do not understand the importance of marketing activities.

• Research and development (R&D): This study found no R&D activities, neither at the level of an individual firm, nor at the level of industry association, which is a significant barrier to the industry’s growth. Absence of innovation in production and product development is mainly due to the lack of R&D – this in turn is the reason why Afghan marble products cover 15 to 20 percent of the market and level of exports is low.

Among many other factors, one is lack of competition between the firms this due to the oligopolistic structure of the market. This shapes an environment in which Afghan firms behave in a way that is neither optimal for themselves nor for consumers – price is high, quality of finished marble in terms of processing and polishing is dire, innovation lacks, market is dominated by foreign products, etc. In upcoming sections, we will provide recommendation for relevant bodies to improve this situation.

2.3. Firms performance

It is very obvious in theory that, when there is no competition in the market, firms profitability is high. But on the other hand, there is no tendency for firms to bring efficiency, improve product quality and make technological upgrading. But to prove this theory is right, we present the following findings.

• Profit margin: In the next paragraphs, we assume that firms have both quarry and processing plants – looking at different levels of value chain as a single value-added process.

Because of difference in product quality and size of production, profitability of Afghan marble business differs within the market. But we would like to look at the profitability of three different products, namely Chest-e Sharif, Afghan White (from

Research & Statistics Department, AISA

16

Khogiani in Jalalabad) and Sang-e Tara Khel (from Kabul), assuming that they are all produced around 5000 tons per year.

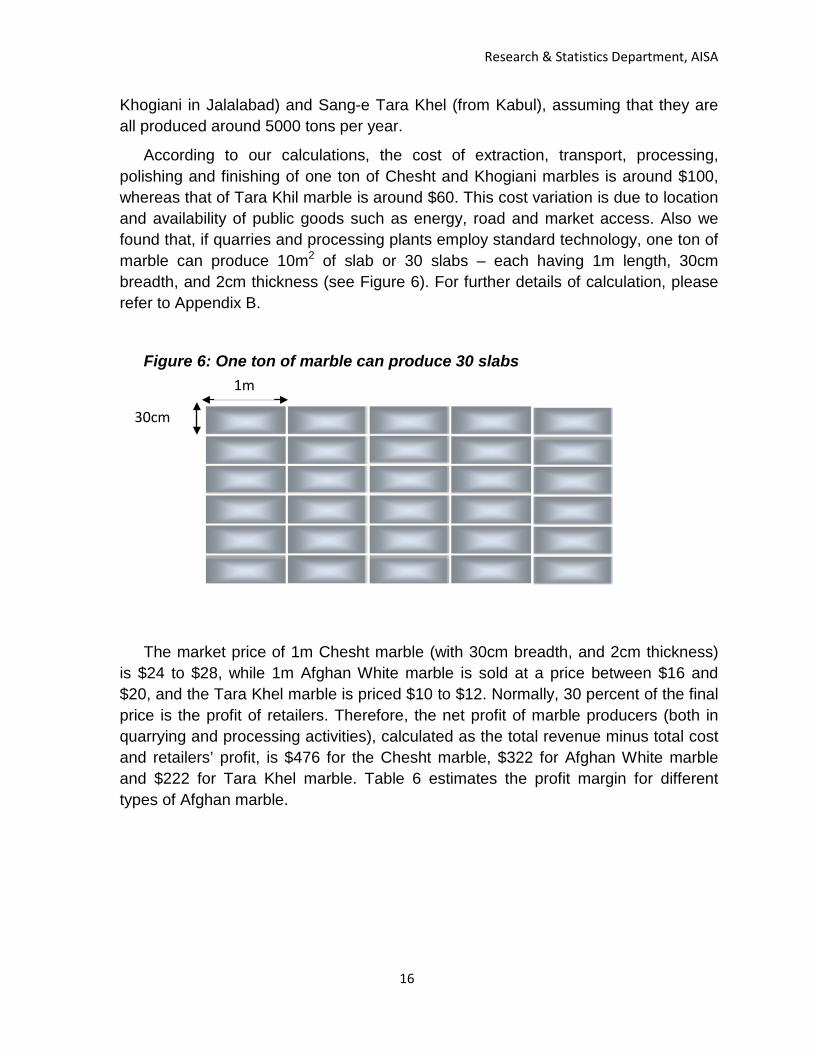

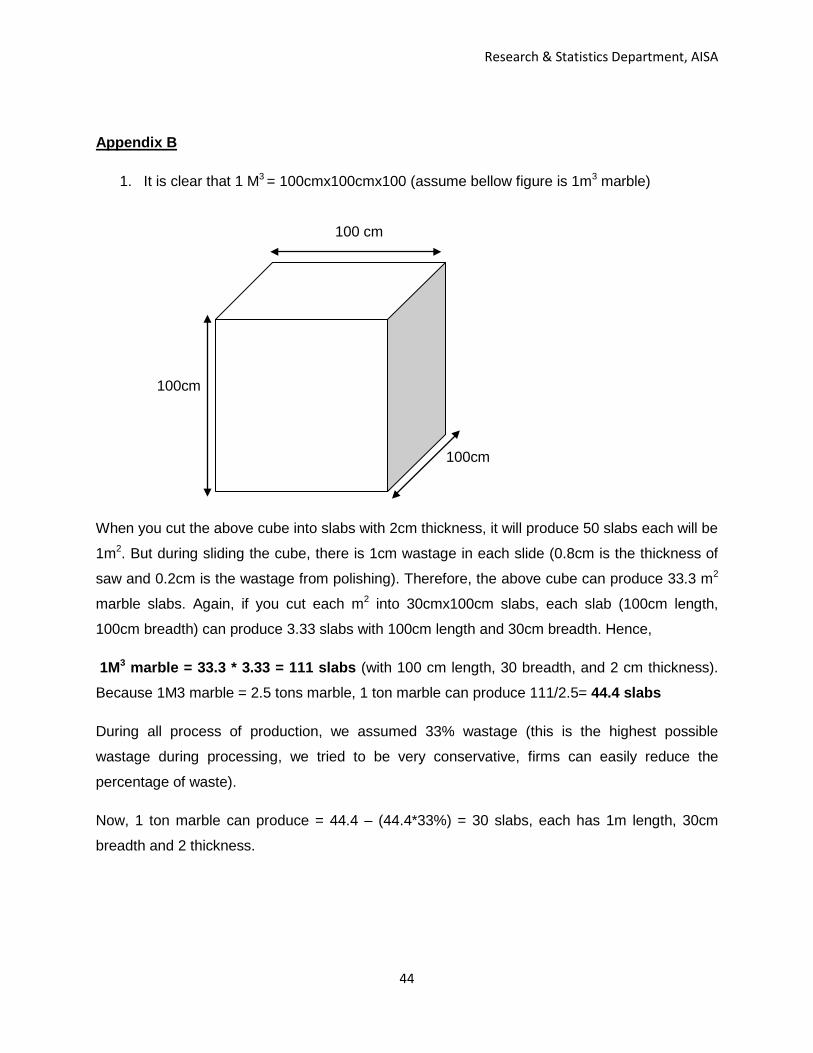

According to our calculations, the cost of extraction, transport, processing, polishing and finishing of one ton of Chesht and Khogiani marbles is around $100, whereas that of Tara Khil marble is around $60. This cost variation is due to location and availability of public goods such as energy, road and market access. Also we found that, if quarries and processing plants employ standard technology, one ton of marble can produce 10m2 of slab or 30 slabs – each having 1m length, 30cm breadth, and 2cm thickness (see Figure 6). For further details of calculation, please refer to Appendix B.

Figure 6: One ton of marble can produce 30 slabs

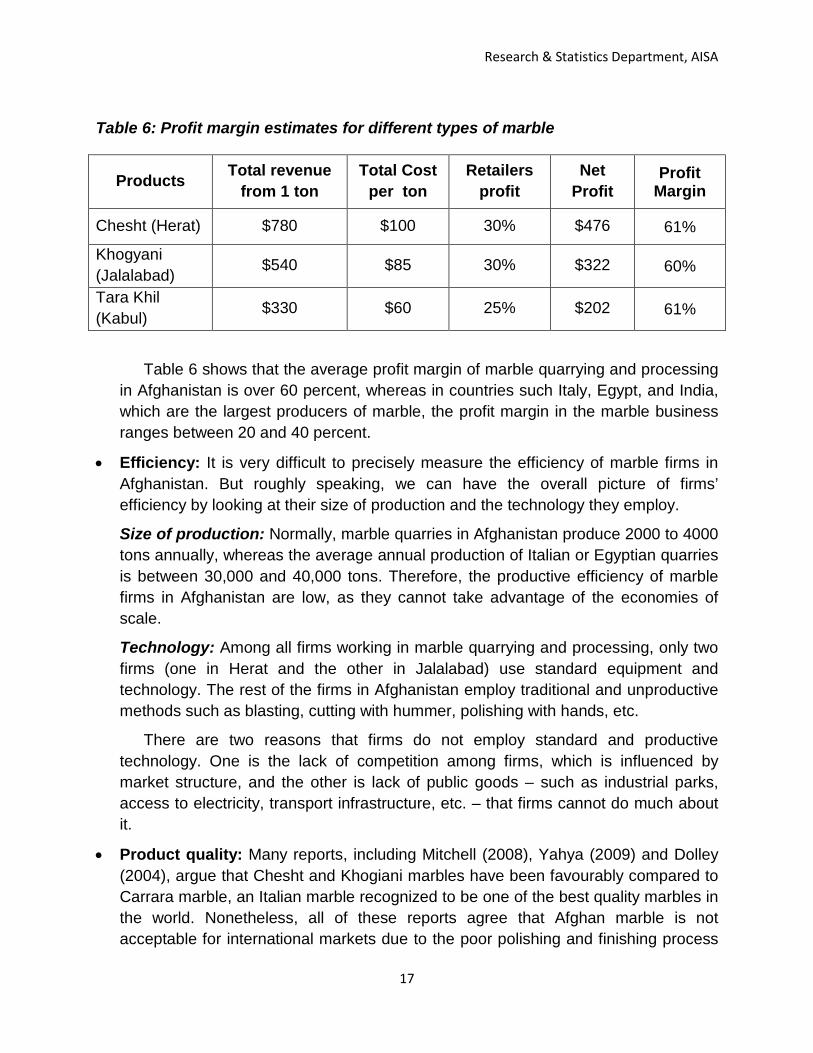

The market price of 1m Chesht marble (with 30cm breadth, and 2cm thickness) is $24 to $28, while 1m Afghan White marble is sold at a price between $16 and $20, and the Tara Khel marble is priced $10 to $12. Normally, 30 percent of the final price is the profit of retailers. Therefore, the net profit of marble producers (both in quarrying and processing activities), calculated as the total revenue minus total cost and retailers’ profit, is $476 for the Chesht marble, $322 for Afghan White marble and $222 for Tara Khel marble. Table 6 estimates the profit margin for different types of Afghan marble.

30cm

1m

Research & Statistics Department, AISA

17

Table 6 shows that the average profit margin of marble quarrying and processing in Afghanistan is over 60 percent, whereas in countries such Italy, Egypt, and India, which are the largest producers of marble, the profit margin in the marble business ranges between 20 and 40 percent.

• Efficiency: It is very difficult to precisely measure the efficiency of marble firms in Afghanistan. But roughly speaking, we can have the overall picture of firms’ efficiency by looking at their size of production and the technology they employ.

Size of production: Normally, marble quarries in Afghanistan produce 2000 to 4000 tons annually, whereas the average annual production of Italian or Egyptian quarries is between 30,000 and 40,000 tons. Therefore, the productive efficiency of marble firms in Afghanistan are low, as they cannot take advantage of the economies of scale.

Technology: Among all firms working in marble quarrying and processing, only two firms (one in Herat and the other in Jalalabad) use standard equipment and technology. The rest of the firms in Afghanistan employ traditional and unproductive methods such as blasting, cutting with hummer, polishing with hands, etc.

There are two reasons that firms do not employ standard and productive technology. One is the lack of competition among firms, which is influenced by market structure, and the other is lack of public goods – such as industrial parks, access to electricity, transport infrastructure, etc. – that firms cannot do much about it.

• Product quality: Many reports, including Mitchell (2008), Yahya (2009) and Dolley (2004), argue that Chesht and Khogiani marbles have been favourably compared to Carrara marble, an Italian marble recognized to be one of the best quality marbles in the world. Nonetheless, all of these reports agree that Afghan marble is not acceptable for international markets due to the poor polishing and finishing process

Table 6: Profit margin estimates for different types of marble

Products Total revenue from 1 ton

Total Cost per ton

Retailers profit

Net Profit

Profit Margin

Chesht (Herat) $780 $100 30% $476 61%

Khogyani (Jalalabad) $540 $85 30% $322 60%

Tara Khil (Kabul) $330 $60 25% $202 61%

Research & Statistics Department, AISA

18

they receive. Therefore, in most cases quarried marble is exported to Pakistan for processing purposes – much of this shipping happens illegally. These are often re-imported as higher value-added polished marble product, or exported from Pakistan to international markets as Pakistani marble.

During our interviews with marble processing firms, we learned that Afghan firms pay less effort to employ advanced polishing technology and do not care much about expanding their market both domestically and internationally. Such behaviour of Afghan firms may have been influenced by two factors. First, acquiring modern technology for marble polishing requires substantial amount of capital, which these firms do not possess. Lack of access to finance is a major constraint for economic development in Afghanistan. Secondly, Afghan firms do not have long-term insight for their business development due to lack of strategic management skills.

Research & Statistics Department, AISA

19

Chapter 3:

Market Opportunities

Research & Statistics Department, AISA

20

3. Market Opportunities

To find out market opportunities, we use a simple supply-demand model. Our approach will consist of studying the quality and quantity of raw materials (i.e. marble) available in Afghanistan, and assessing the current and future demand for marble at local and foreign markets. In a second step, we will thoroughly evaluate the factors of production (i.e. land, labour, machinery and equipment, capital, and entrepreneurship) and study the potential for investment opportunities in marble industry. Finally, we will identify the barriers and constraints that firms are faced with, in order to evaluate the implicit costs which exist in the market. In the next chapter, we will have policy recommendations to government and private sector to overcome the persisting constraints and challenges.

3.1. Raw materials

The US geological survey estimated the value of marble reserves in Afghanistan around $200 billion. Having considered this fact, Mitchell (2008) emphasizes that “Afghanistan has the potential to supply Middle Eastern and Asian markets with an almost unlimited supply of marble”. Moreover, most Afghan provinces have marble mines. According to recent geological findings, marble deposits formed during the Proterozoic age (542 – 2500 million years ago) are some of the best known marbles in the world. Below is a description of marble reserves in Afghanistan.

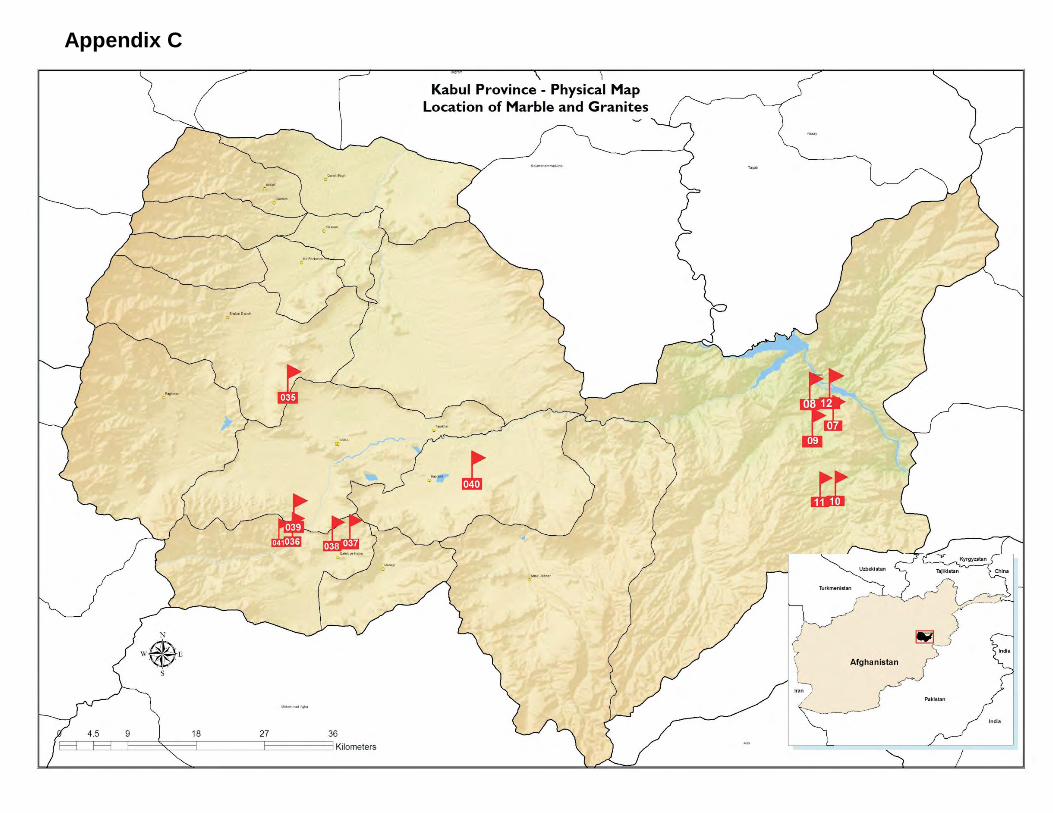

• Kabul province: The proterozoic marble quarries are in Ghazak, Karez-e Mir, Tarakhel, Hazara-e Baghal, Pul-e Charkhi, and Qalamkar. The Ghazak marble which is known as the “Black Ghazak” is located 32km east of Kabul. The Karez-e Mir marble consists of granular white, and rarely grey-yellow marble, which is situated 40km north of Kabul. In total, there are 13 marble deposits in Kabul.

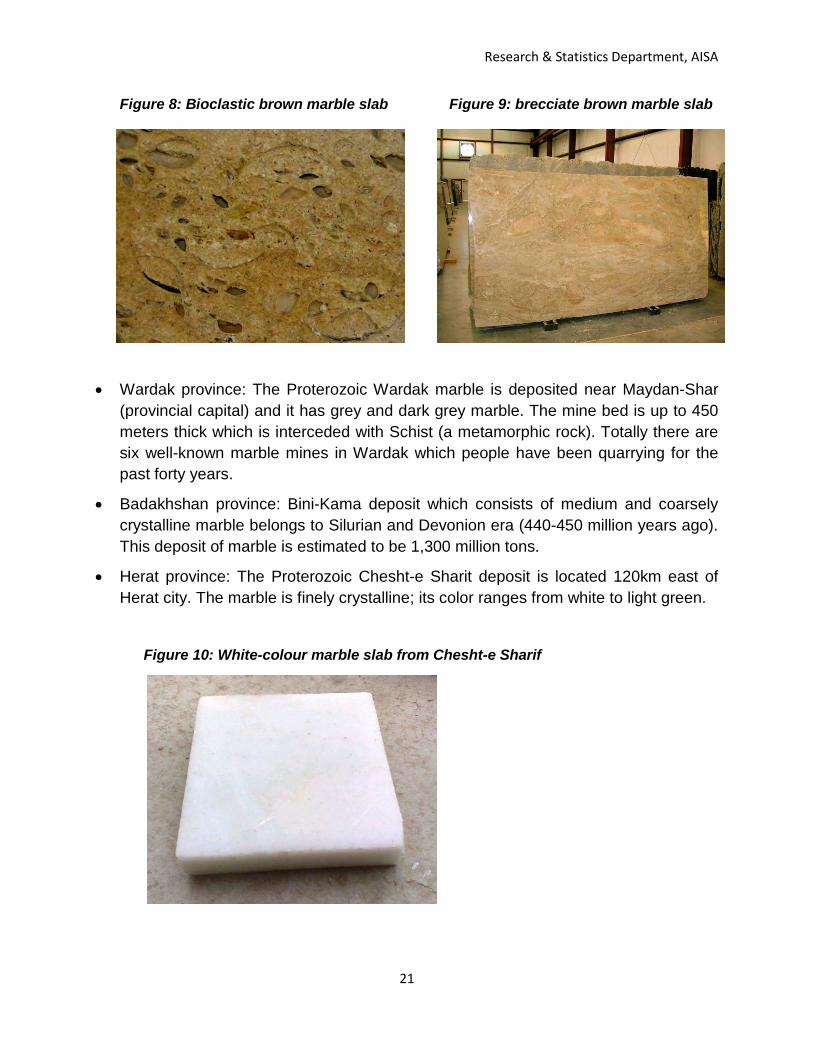

• Logar province: The proterozoic marble is quarried in Awbazak, Dehnow and Mohammad Agha. Awbazak marble is bioclastic and brown in color (Figure 8), whereas Dehnow marble is brecciate and brown in color (Figure 9) and Mohammad Agha marble is black and white in colour.

Research & Statistics Department, AISA

21

Figure 8: Bioclastic brown marble slab Figure 9: brecciate brown marble slab

• Wardak province: The Proterozoic Wardak marble is deposited near Maydan-Shar (provincial capital) and it has grey and dark grey marble. The mine bed is up to 450 meters thick which is interceded with Schist (a metamorphic rock). Totally there are six well-known marble mines in Wardak which people have been quarrying for the past forty years.

• Badakhshan province: Bini-Kama deposit which consists of medium and coarsely crystalline marble belongs to Silurian and Devonion era (440-450 million years ago). This deposit of marble is estimated to be 1,300 million tons.

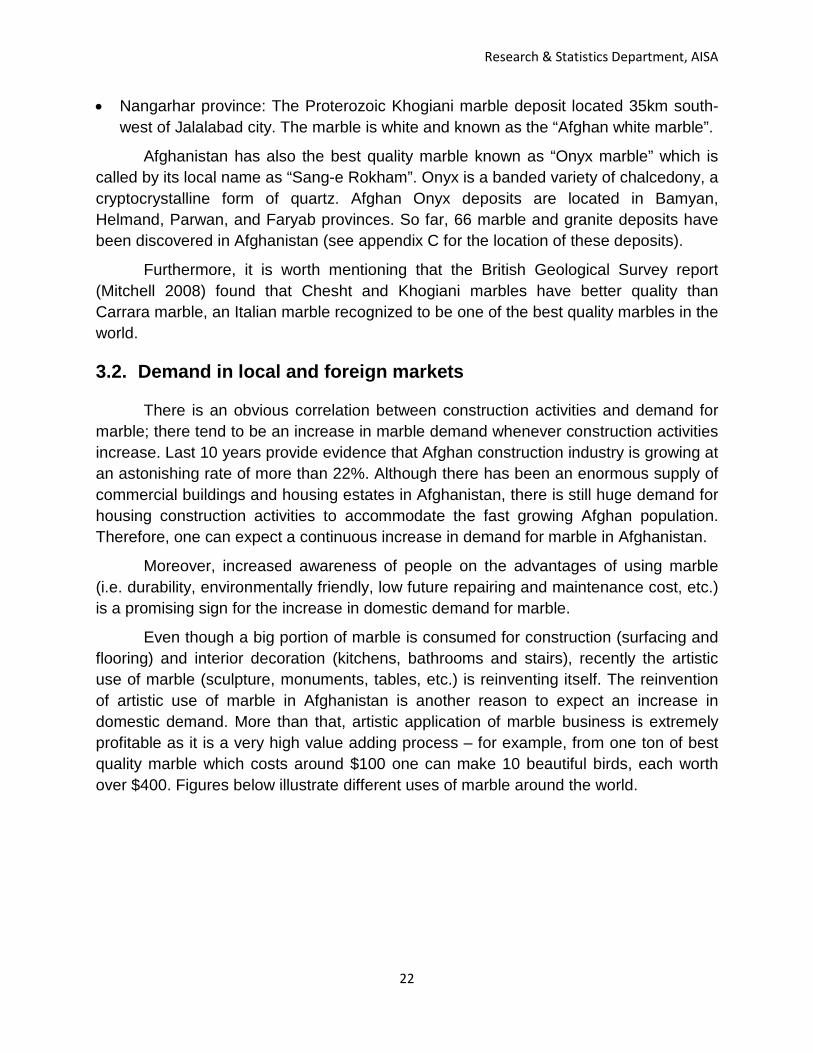

• Herat province: The Proterozoic Chesht-e Sharit deposit is located 120km east of Herat city. The marble is finely crystalline; its color ranges from white to light green.

Figure 10: White-colour marble slab from Chesht-e Sharif

Research & Statistics Department, AISA

22

• Nangarhar province: The Proterozoic Khogiani marble deposit located 35km south-west of Jalalabad city. The marble is white and known as the “Afghan white marble”.

Afghanistan has also the best quality marble known as “Onyx marble” which is called by its local name as “Sang-e Rokham”. Onyx is a banded variety of chalcedony, a cryptocrystalline form of quartz. Afghan Onyx deposits are located in Bamyan, Helmand, Parwan, and Faryab provinces. So far, 66 marble and granite deposits have been discovered in Afghanistan (see appendix C for the location of these deposits).

Furthermore, it is worth mentioning that the British Geological Survey report (Mitchell 2008) found that Chesht and Khogiani marbles have better quality than Carrara marble, an Italian marble recognized to be one of the best quality marbles in the world.

3.2. Demand in local and foreign markets

There is an obvious correlation between construction activities and demand for marble; there tend to be an increase in marble demand whenever construction activities increase. Last 10 years provide evidence that Afghan construction industry is growing at an astonishing rate of more than 22%. Although there has been an enormous supply of commercial buildings and housing estates in Afghanistan, there is still huge demand for housing construction activities to accommodate the fast growing Afghan population. Therefore, one can expect a continuous increase in demand for marble in Afghanistan.

Moreover, increased awareness of people on the advantages of using marble (i.e. durability, environmentally friendly, low future repairing and maintenance cost, etc.) is a promising sign for the increase in domestic demand for marble.

Even though a big portion of marble is consumed for construction (surfacing and flooring) and interior decoration (kitchens, bathrooms and stairs), recently the artistic use of marble (sculpture, monuments, tables, etc.) is reinventing itself. The reinvention of artistic use of marble in Afghanistan is another reason to expect an increase in domestic demand. More than that, artistic application of marble business is extremely profitable as it is a very high value adding process – for example, from one ton of best quality marble which costs around $100 one can make 10 beautiful birds, each worth over $400. Figures below illustrate different uses of marble around the world.

Research & Statistics Department, AISA

23

Figures 11: Buildings and structures with marble

(1) Taj Mahal is made of white domed marble (2) A luxury bathroom made of marble

(3) A marble structure at Salim Karwan square in Kabul

According to our findings, annual marble consumption in Afghanistan is between 920,000 to 1,230,000 tons. But domestic quarries can only produce between 184,500 and 246,000 tons per year. Part of unprocessed Afghan marbles is exported to Pakistan for processing purpose. These are often re-imported to Afghanistan as higher value-added (processed) marble. Therefore, over 85 percent of marble consumption in Afghanistan (almost 780,000 to 1,000,000 tons) is met by imported marbles, mostly from Pakistan. In order to capture the bigger share of the market, Afghan firms need to struggle intensively. They need to be as efficient as possible by adapting lean production concept. To do so, firms need to reconsider their management, technology, and production and marketing strategies. First, they should improve their management skills through hiring professional staff for the management of their enterprises. Second, they should update their technology and equipments, and employ the latest generation of machineries available at the international markets. Finally, they must have clear

Research & Statistics Department, AISA

24

understanding of the fact that increasing market share by lowering their prices (and thus increasing their sales) is a good strategy rather than looking for high profit with small market share and yet for a short-term.

Given the high quality of Afghan marble, there is a huge demand in regional countries (mainly Turkmenistan, Saudi Arabia, Kuwait, and UAE) and in some international markets (such as Italy, Germany, the UK and the US). Nonetheless, many challenges need to be overcome by the government and the private sector, so that Afghan firms can access these international markets. First, Afghan firms need to increase their polishing quality; they can only do this by employing new standard technology. Secondly, the relevant government institutions – mainly the Export Promotion Agency of Afghanistan – should provide the necessary physical and institutional facilities to help Afghan firms access international markets.

It is worth mentioning that the industry is growing at a 60-percent rate (in terms of output) which is very promising for the investors, and we expect that by the end of 2016 total value-added created by this sector can reach as high as $800 million.

3.3. Factors of production

By factors of production we mean all inputs, such as land, labour, machinery and equipment, capital, and entrepreneurship that produce finished and final products such as marble slabs, tiles, sculptures, tables, etc.

• Land: For quarrying activities, no additional land is needed. However, for processing plants, lack of access to land is the biggest obstacle per the following explanations: 1. It is very difficult to access land in Kabul or other provinces where security is not

a big concern and where public goods such as electricity, water supply, and road infrastructure are available.

2. The price of land to purchase or to rent is too expensive and costly. 3. According to our research, minimum land required for standard marble

processing plant is around 2500m2, while processing plants in Egypt and Turkey operate using 5000m2 of land. It is very difficult to find such large-size land in Kabul or other major provinces.

4. Processing plants are not located in a single cluster to take advantage of the economies of agglomeration.

• Labour: There is a lack of skilled labour force in Afghanistan. In fact, there are no technical training centres which could train workers in marble quarrying and processing. However, due to abundant labour in Afghanistan, it is fairly feasible to provide on-the-job training for unskilled labours. In processing plants, a very short-term training on the job is sufficient. Therefore, lack of labour is not a serious issue in this business.

Research & Statistics Department, AISA

25

• Required Capital: The amount of required capital differs for quarrying and processing activities. Generally, quarrying business requires less capital compared to processing. However, the required capital varies from one site to another depending on location, availability of road, and geological circumstances.

According to our survey, the minimum capital required for quarrying activity (employing standard technology and not blasting) is around $250,000 whereas for the processing plants the minimum capital required is over $400,000. It should be noted that with $400,000 of investment, one can have very good machineries which are almost 10 times more productive than average old processing plants. This in turn can provide competitive edge for the investor.

Access to capital remains restricted in Afghanistan. Commercial banks do not offer large-size, long-term credit, and businesses find it hard to borrow from abroad. Lack of capital is, thus, a major constraint in this business in Afghanistan.

• Entrepreneurial skills: In today’s challenging business environment, entrepreneurial skills are the key to success and survival of a business. However, in Afghanistan, marble producers neither have efficient entrepreneurial skills (including large firms) nor they have any intention to build such capacity within their enterprises. The following entrepreneurial skills are the essential requirements for those who run a marble company in order for them to grab the opportunities which exist in local and foreign markets:

o Management skills – the ability to efficiently manage time and people (i.e. the production process, operations, and activity of the firm)

o Strategic decision-making and planning o Financial literacy o Market research skills: to assess the market demand, suppliers, customers,

and the competition o Marketing techniques o Innovative ideas, methods and techniques o Ability to develop a successful business plan for a new venture o Willingness to take risks (or at least not be risk averse) o Willingness to change their routine behaviour, if necessary o Awareness of laws and regulations

• Technology: One of the most important factors of production in marble industry is technology (i.e. machineries and equipment in use). Due to the nature of business, machineries play a big role in the success and productivity of firms. By employing standard machineries, they can enormously increase their productivity; e.g. a firm with standard machineries can produce 10 times more marble than a firm with old system of operation.

In quarrying activity, blasting is the old method of production, while diamond wire cutting is the new method of quarrying. With blasting, quarries not only lose 50 to 80 percent of the material, they also cause great damage to the entire quarry by enforcing micro-fractures throughout the entire deposit. Whereas with diamond wire saw cutting, the percentage of waste can be reduced to 7 percent, while creating no damage to the marble deposit. Standard machineries required for quarrying marble

Research & Statistics Department, AISA

26

are listed below. However, it does not imply that all these machineries are necessary to have to be able to start a quarrying operation.

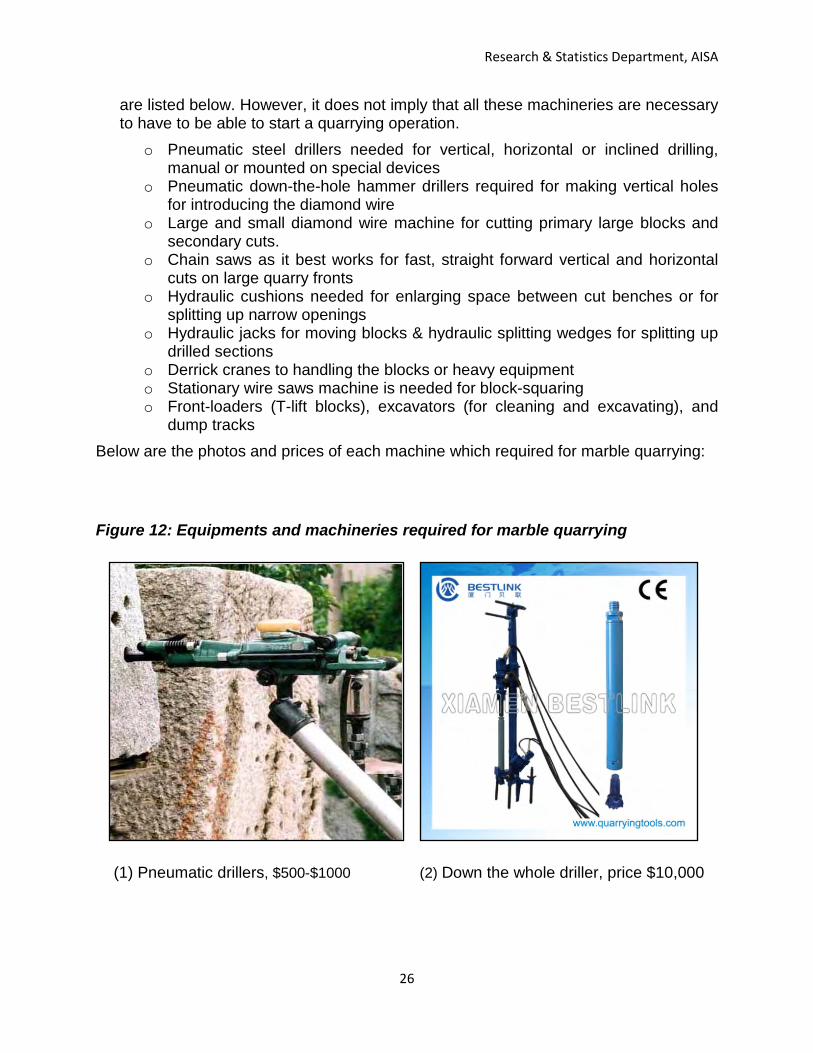

o Pneumatic steel drillers needed for vertical, horizontal or inclined drilling, manual or mounted on special devices

o Pneumatic down-the-hole hammer drillers required for making vertical holes for introducing the diamond wire

o Large and small diamond wire machine for cutting primary large blocks and secondary cuts.

o Chain saws as it best works for fast, straight forward vertical and horizontal cuts on large quarry fronts

o Hydraulic cushions needed for enlarging space between cut benches or for splitting up narrow openings

o Hydraulic jacks for moving blocks & hydraulic splitting wedges for splitting up drilled sections

o Derrick cranes to handling the blocks or heavy equipment o Stationary wire saws machine is needed for block-squaring o Front-loaders (T-lift blocks), excavators (for cleaning and excavating), and

dump tracks Below are the photos and prices of each machine which required for marble quarrying: Figure 12: Equipments and machineries required for marble quarrying (1) Pneumatic drillers, $500-$1000 (2) Down the whole driller, price $10,000

Research & Statistics Department, AISA

27

(3) Diamond wire machines for large primary cuts, $10,000-$15,000

(4) Quarry saw machine, $40,000-$50,000

(5) Hydraulic cushions, $100 per piece (6) Rock splitting machine, $10,000

Research & Statistics Department, AISA

28

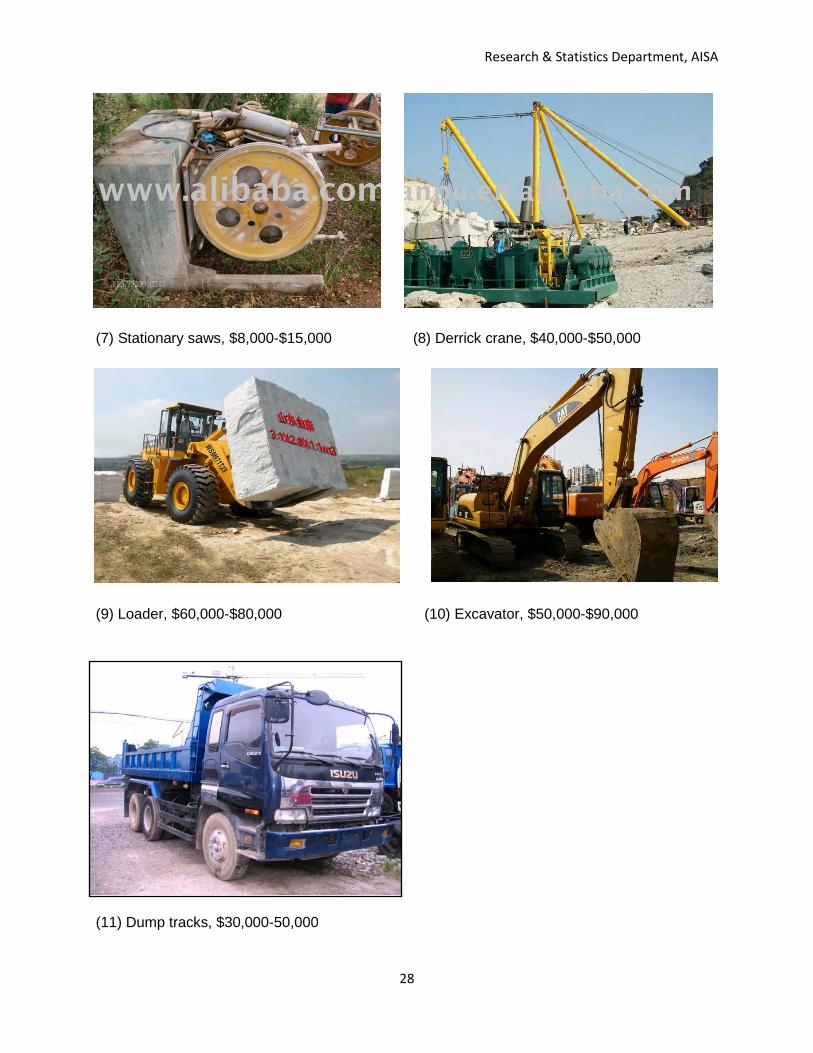

(7) Stationary saws, $8,000-$15,000 (8) Derrick crane, $40,000-$50,000

(9) Loader, $60,000-$80,000 (10) Excavator, $50,000-$90,000

(11) Dump tracks, $30,000-50,000

Research & Statistics Department, AISA

29

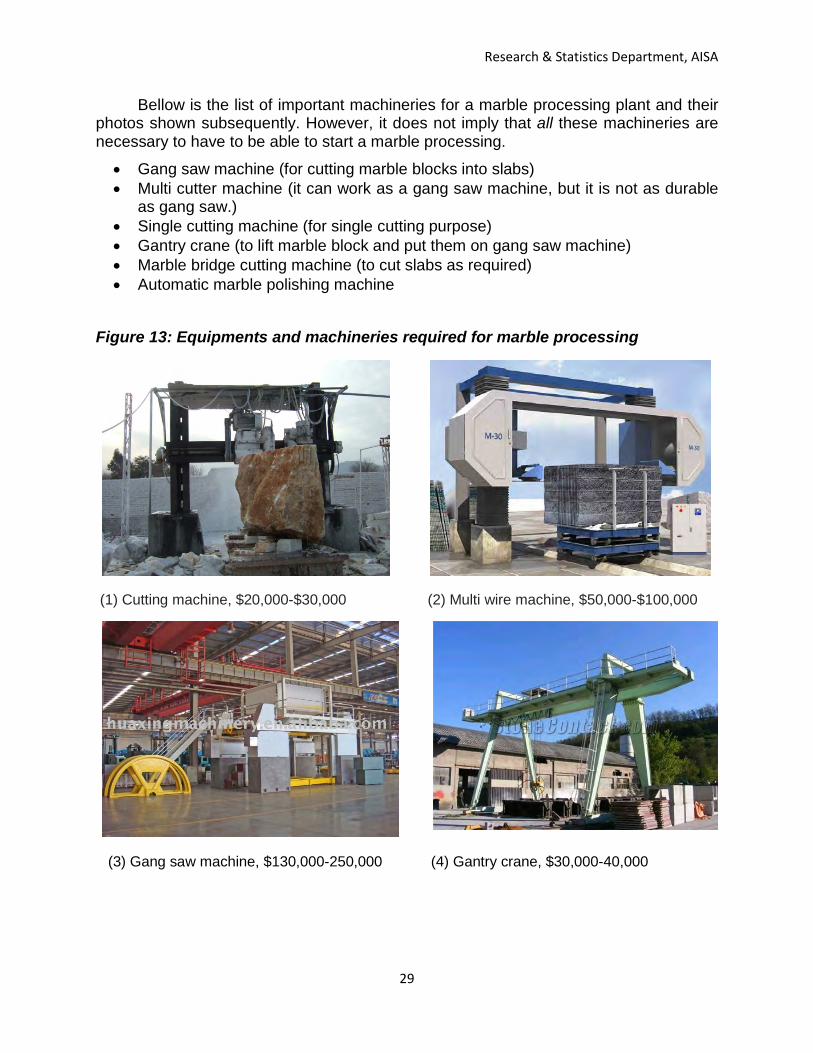

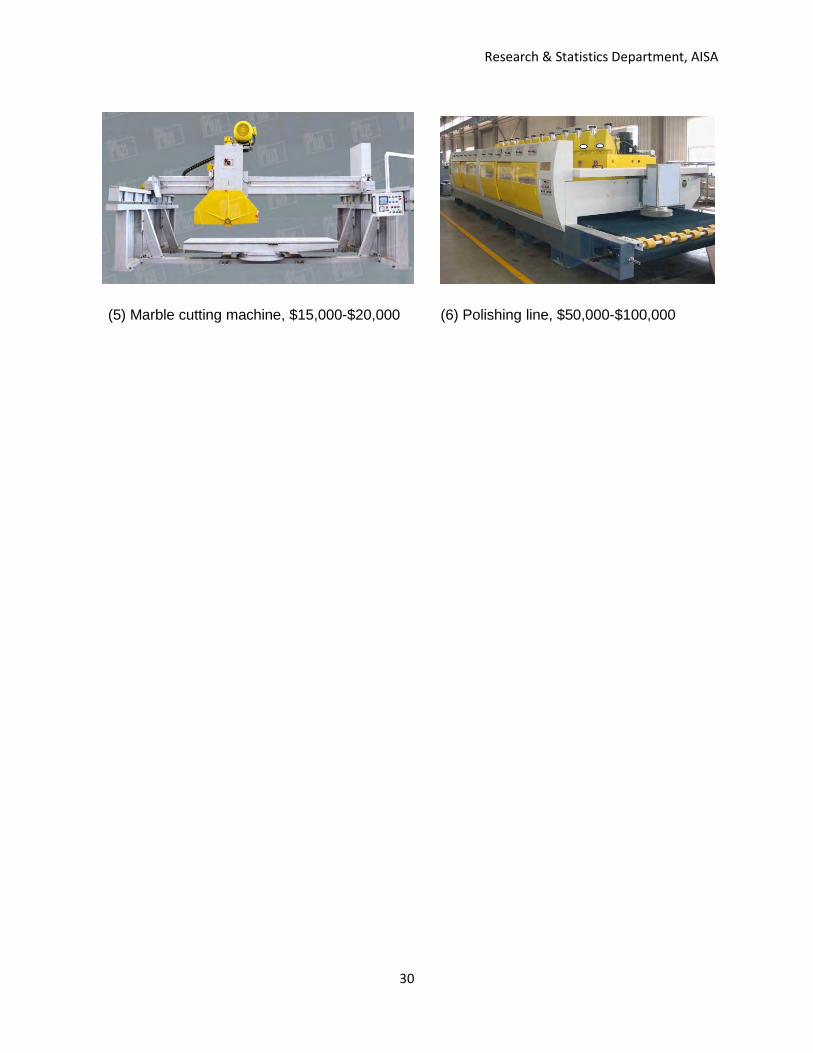

Bellow is the list of important machineries for a marble processing plant and their photos shown subsequently. However, it does not imply that all these machineries are necessary to have to be able to start a marble processing.

• Gang saw machine (for cutting marble blocks into slabs) • Multi cutter machine (it can work as a gang saw machine, but it is not as durable

as gang saw.) • Single cutting machine (for single cutting purpose) • Gantry crane (to lift marble block and put them on gang saw machine) • Marble bridge cutting machine (to cut slabs as required) • Automatic marble polishing machine

Figure 13: Equipments and machineries required for marble processing

(1) Cutting machine, $20,000-$30,000 (2) Multi wire machine, $50,000-$100,000

(3) Gang saw machine, $130,000-250,000 (4) Gantry crane, $30,000-40,000

Research & Statistics Department, AISA

30

(5) Marble cutting machine, $15,000-$20,000 (6) Polishing line, $50,000-$100,000

Research & Statistics Department, AISA

31

Chapter 4:

Recommendations

Research & Statistics Department, AISA

32

4. Recommendations

Despite the fact that there is almost infinite best quality marble deposits throughout the country and enormous demand exists within the domestic and international markets, Afghan firms are not performing very well – price is high, quality of finished product in terms of polishing and finishing is dire, innovation lacks, market is dominated by foreign products, and export of marble is low. Moreover, the current market condition cannot attract enough investment. Reasons for this situation range from undesirable legal framework and bureaucracy to lack of factors of production. But the reason for bad performance of established firms is lack of direction which is caused by both lack of incentives and lack of effective regulation by the government.

4.1. Role of government

In order to push private firms to perform well (i.e. to decrease their prices and to increase their quality of products), the Afghan government, especially the Ministry of Mines should take the following steps:

1. The MoM should provide strong incentives for quarries to increase their production and output. Such a supply-side policy will encourage the firms to employ modern technology and use more efficient extraction methods to benefit from the incentive. This, in turn, will enable the firms to benefit from the economies of scale, to decrease their total cost, to supply at a lower price and thus to increase their competitiveness. Moreover, employing modern technology will also have positive effect on the quality of their products.

A simple incentive mechanism can be offering discounts on the royalty fees for each additional amounts of marble produced. For example, quarry A is supposed to extract 10,000 tons of marble per year according to its contract with the MoM. If this firm extracts 20,000 tons within a year, the MoM should give a 50% royalty discount on the additional amount (i.e. 10,000 tons). For the next 10,000 additional tons of marble, the ministry should offer a 75% discount.

Such a mechanism can provide strong incentive for quarries to produce more. Afghan firms will benefit from the economies of scale and will have lower total cost. They can thus easily sell at a lower and competitive price, and will be able to compete with Pakistani marbles. Eventually Afghan firms can increase their share at the local market, and even at foreign markets.

Nonetheless, the decrease in royalty revenue of the government will be more than offset by an increase in income/sales tax, business receipt tax (BRT) and other types of taxes due to increased production of marble in the economy.

Research & Statistics Department, AISA

33

2. The Ministry of Mines must prohibit the use of explosive materials in extracting marble. Prohibition of explosive devices can save 50 to 70 of waste and prevent damage to the entire deposit. It can also push the quarrying firms to use standard technology which is more productive and safe.

3. Ministry of Mines should also provide incentives for the use of standard technology (e.g. a royalty discount) or prioritize in the bidding process those companies which employ standard technology and modern machineries.

4. The Afghan government should adopt policies which promote domestic marble usage and encourage purchase of Afghan marble products throughout their procurement system - by adopting “Afghan product first” policy. Such policies increase domestic demand for Afghan marble and ensure a sustainable expansion of Afghan marble market.

5. Ministry of finance (MoF) should increase export tax on row marble (unprocessed marble blocks). This will insure continuous supply of marble for processing firms as well as encouraging value added activities to take place within the country.

6. In order to promote private investment in marble industry, the government should provide necessary public goods and access to factors of production for marble producers. Infrastructure, land, and capital are such goods need to be facilitated by the government. Below, specific policies have been proposed for each factor or services.

Land: Land is the first required factor of production, and marble processing business needs over 2500m2 of land. Finding and leasing such large area of land in and around Kabul city is the biggest barrier for new entries and for existing firms to employ more machinery. Therefore, there is a strong need to build a specialized industrial park for marble industry. All neighbouring countries including Pakistan, India, and Iran have especial cities for marble and granite industry. For instance, Pakistan has 5 big marble cities. In 2005, the Government of Pakistan created an industrial park for marble and granite which brought the country a great success in terms of attracting investment and increasing marble production and exports.

When we look at the strategies of regional countries (such as India, Malaysia and Iran) in attracting investment and promoting growth, we find that their top priority has been to develop special economic zones (SEZs). It should be emphasized that without having enough SEZs, Afghanistan cannot rebuild and nurture its industries which play a substantial role in achieving a sustainable growth. Therefore, in order to find a permanent solution for the lack of industrial land in Afghanistan, the Government of Afghanistan should take a comprehensive approach by creating an independent Industrial Parks Development Authority. The agency will be responsible

Research & Statistics Department, AISA

34

for the construction and development of industrial parks, prioritizing industrial sectors, distribution of land plots, and all relevant services.

This paper emphasizes that the creation of an independent and competent agency for the development of industrial parks will be a big achievement for the Afghan government. The agency could play an important role in the development of Afghan industries, and shape Afghanistan’s future industrial growth path. Nevertheless, for the time being, Afghanistan Investment Support Agency and the Ministry of Commerce and Industries – which both have departments for the development and administration of industrial parks – should allocate land plots for marble and granite processing plants in one of their industrial parks.

Labour: As mentioned in the previous chapter, there is no vocational and technical training centre in Afghanistan to train workers for marble quarrying activities. Therefore, the Afghan ministries such Ministry of Mines, Ministry of Labour and Ministry of Education should collaborate to build such training centres. This will not only provide know-how skills to the market but it can also increase investment in the mining sector.

Required Capital: Entering the marble quarrying and processing business requires investing huge amount of capital. Access to large-size credit is restrained in Afghanistan, as commercial banks and other financial institutions do not offer large-size long-term loans. Borrowing from abroad is not a good option due to risks associated with currency exchange. Therefore, the government should initiate a public credit scheme and public guarantee scheme to help the companies in need of capital. At least, the government should provide “leasing finance” to marble quarrying and processing firms as to enable them acquire necessary machineries and equipment.

Entrepreneurial skills: As emphasized in the previous chapter, entrepreneurial skills are the key to success and survival of a business. Afghan firms remain less competitive and less productive, due to their inefficient management techniques. Therefore, the Afghan government should provide capacity development programs to Afghan industrialists, and help them increase their managerial skills and technical efficiency. AISA can be the relevant institution in this regard.

4.2. Role of Private Sector

The biggest weakness of private firms in the marble market is lack of management skills. Managers and owners of these firms do not employ efficient management techniques. During our survey and visits from companies, we found that firms do not have any professional staff to use financial management methods and to conduct marketing operations and market research, and these firms do not have any

Research & Statistics Department, AISA

35

R&D unit. This paper emphasizes that private firms along with their association must take the management issue very seriously. The paper presents the following recommendations for private firms and their associations:

1. There are two associations of marble producers in Afghanistan, namely Afghanistan Marble Granite Processing Association (AMGPA) and Afghanistan Marble Industry Association (AMIA). The paper strongly recommends that these two associations merge into a single association in order to have a stronger negotiation power. Merging both associations into one can help both the government to provide them with a single help package, and the association to have more power for lobbying. It can help them to solve the problem of their industrial park in Arghandai.1

2. Since entering the marble business and establishing a quarry or processing unit requires investing huge capital, and since the concentration ratio in the marble market is higher and most firms struggle to expand or to even conserve their share at the market, this paper suggest that firms can engage in mergers and/or create joint-ventures. This can help them raise sufficient capital and use the information and experience of each other in the market to become more competitive.

Moreover, merging to a unified association has other benefits e.g. it will cost less to provide training for the members and they can benefit from the spillover effect of their activity within the association.

3. Marble firms should hire professional managers or build their management capacity. This will help them increase their efficiency, and practice successful market and production strategies, which will ensure their long-term growth.

4. The marble associations should hire professional staff to manage their affairs and to provide them with professional advises. They should using modern marketing tools such creation of a website, and carry out R&D activities. This can bring transparency and alleviate conflict of interest within the association.

5. In terms of strategy, private firms should practice competition through prices. By decreasing their prices, they can increase their sales and thus expand their market share. This in turn increases their profit. Such a strategy has been discussed in detail in Chapter 2.

4.3. Role of donors

According to the World Bank data, Afghanistan has been one of the major aid recipients in the last decade. Since the fall of Taliban regime, Afghanistan received over

1 Afghanistan Marble Industry Association (AMIA) members bought land in Arghandai (West of Kabul City) for the purpose of building an industrial park. They are asking the government to provide the infrastructure facilities such as electricity and road construction. But AMGPA members are not involved in this initiative. Therefore AMIA members are left alone in their request and demand for the construction of the industrial park.

Research & Statistics Department, AISA

36

$30 billion of aid through the assistance of donor countries. Most of what has been done in the process of economic development in Afghanistan is the result of such huge foreign aid inflows. However, there is no doubt that the foreign assistance could have been spent more effectively and could have been more successful.

Donors as supporting institutions should provide hand-on support to productive and promising sectors such mining, manufacturing, production of construction materials, etc. To help the marble industry grow, donors can consider the following recommendations:

• Major donor agencies such as USAID, DFID, European Commission, the World Bank and others should allocate part of their funds in the form of long-term credit and investment to Afghan marble enterprises. These institutions can practice different forms of investment and credit facilities which can be in accordance to their agencies’ objectives and programs.

• They can also provide technical assistance to quarrying and processing firms on different areas such as on industrial management, production techniques, installation and operation of machineries, marketing management, distribution activities, etc. The donor institutions can also fund exhibitions, trade shows and other events which can help market the Afghan marble products.

• Donor agencies can fund geological surveys in order to determine the size and quality of existing marble deposits in Afghanistan, and to discover new marble deposits in the country which could be designed in the form of new investment projects.

• Donor institutions should provide capacity development programs to the Ministry of Mine’s personnel and help them in designing strategies and policies to attract foreign investment in the marble sector.

Research & Statistics Department, AISA

37

5. Conclusion

The paper studied the Afghan marble market in terms of market structure and performance, looked at potential opportunities from an investor’s prospective, identified the constraints and factors of market failure, and finally recommended some measures and actions for the development of this industry.

Looking at the global and regional markets, it found that there are huge export opportunities for Afghan marble. By comparing Afghanistan with Pakistan, the paper found an interesting fact: despite the fact that Pakistan has lower quality and less quantity of marble compared to Afghanistan, its marble industry is much bigger in terms of number of firms, level of production, exports value, etc. Therefore, there is no doubt that marble industry in Afghanistan has good potential to grow if market and institutional barriers are removed. The paper forecasts that within the next 5 years, the marble industry in Afghanistan can grow 5 folds if the major market constraints are eliminated.

With regard to market structure and performance, we found that although marble industry is fragmented, few big players control and set the prices. Therefore, there is no full competition in the market, and this creates an environment in which Afghan firms adopt such behaviour that neither helps themselves nor the consumers – price is high, quality of finished product in terms of polishing and finishing is dire, innovation lacks, market is dominated by foreign products, etc. Such unfriendly market behaviour is due to lack of competition in the market and lack of management skills for firms’ owners. Hence, we strongly recommend that the Government of Afghanistan, especially Ministry of Mines, provide incentives for firms to increase their production. Such a supply-side policy helps them benefit from the economies of scale, decrease their total cost, sell at a competitive price, and finally increase their market share. In addition, the government and the private sector must focus on improving the management skills of firms’ managers which helps them increase their firms’ efficiency.

In terms of market opportunities, the paper argues that there is huge demand for Afghan marble both at domestic and foreign markets, due to its high quality. However, looking at the factors of production, there are many challenges which hinders the foreseen opportunities; i.e. lack of access to land, lack of access to capital, lack of skilled workers, and lack of necessary infrastructure. The paper recommends both institutional and market reforms to the government to tackle some of the existing challenges; including construction and development of a specialized industrial park for marble processing firms, provision of long-term financing solutions, technical and management skills trainings, etc.

Research & Statistics Department, AISA

38

6. References ASMED (2010), Afghanistan Marble Industry Directory. http://www.asmed.af/marble

BGS (2012), Marble brochure, http://www.bgs.ac.uk/AfghanMinerals/scripts [Accessed, January 2012]

Korai, M,A., Hussain, S. & Abro, A. (2011), “A report on marble & Granite”, Trade Development Authority of Pakistan, http://www.tdap.gov.pk/doc_reports/tdap_report_on_marble_and_granite.pdf

Mehdi, Abbas, (2006), “Diagnostic Study: Marble & Granite Cluster”, UNIDO-SMEDA Cluster Development Programme, Pakistan

Minerals Law of Afghanistan (2005), Article four: Ownership of Minerals, Kabul.

Mitchell, Clive, (2008), “Afghanistan Revival & Redevelopment”, British Geological Survey, Kabul.

MoM, (2012), Ministry of Mines website: http://mom.gov.af/en/page/4832 [Accessed, January 2012]

Remarks at Afghanistan Minerals Roadshow. Available from: http://www.implu.com/government_news/474/192823 [Accessed, January 2012]

Stephen G. Peters and others (2007), “Preliminary Non-fuel Mineral Resource Assessment of Afghanistan”, Kabul

The OTF Group (2006), “Afghanistan Competitiveness Project”, Kabul.

The OTF Group (2006), “Business Plan template”, Kabul.

Thomas P. Dolley (2004), “Stone Dimension”, Kabul.

US Embassy (2010), Press Releases: Afghanistan International Marble Conference Kicks Off in Herat

Research & Statistics Department, AISA

39

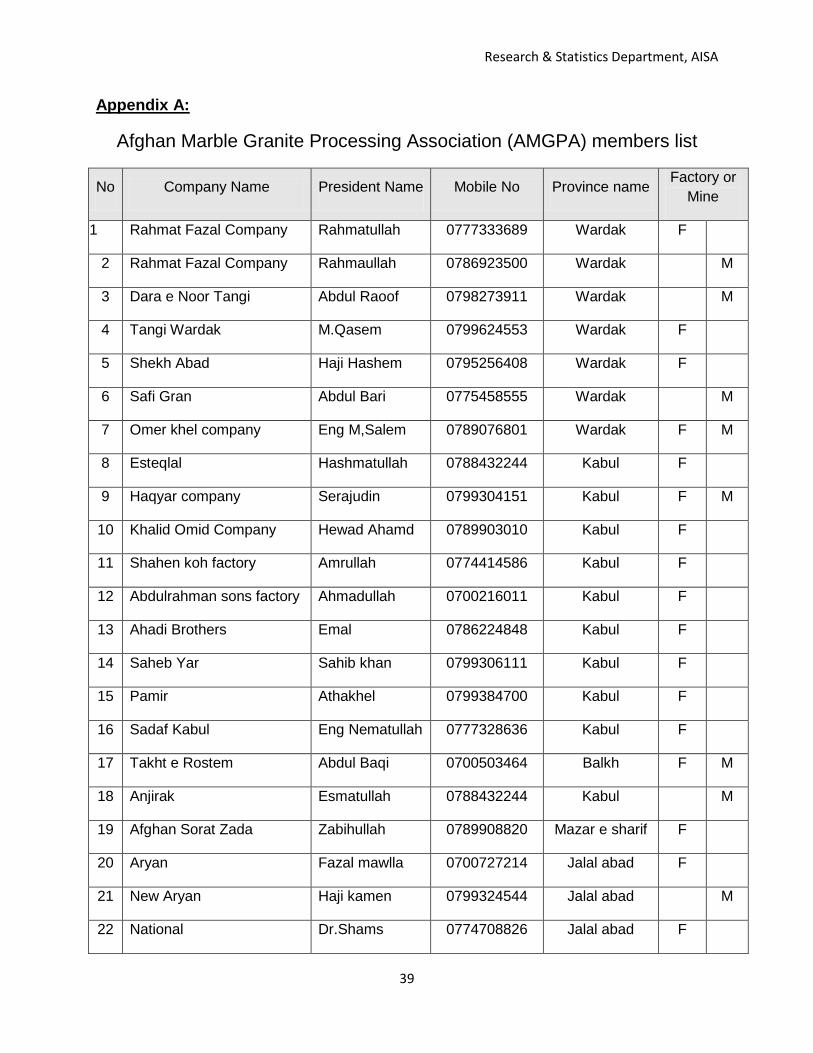

Afghan Marble Granite Processing Association (AMGPA) members list

Appendix A:

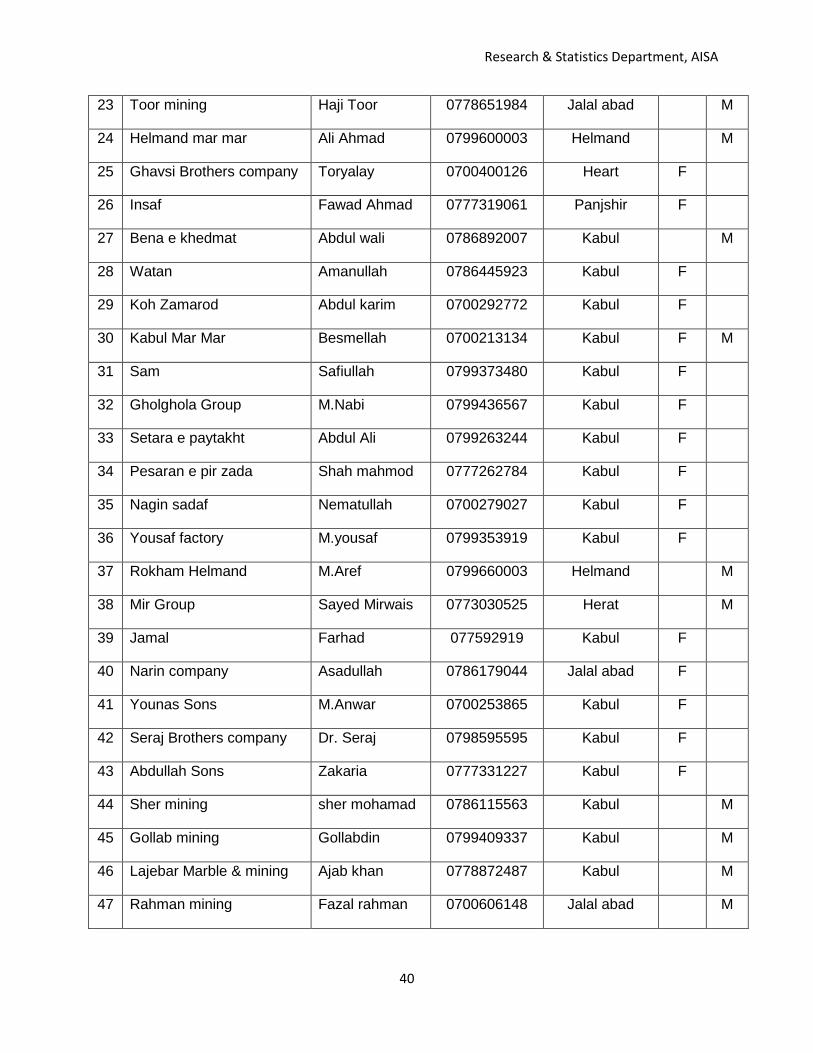

No Company Name President Name Mobile No Province name Factory or Mine

1 Rahmat Fazal Company Rahmatullah 0777333689 Wardak F

2 Rahmat Fazal Company Rahmaullah 0786923500 Wardak M

3 Dara e Noor Tangi Abdul Raoof 0798273911 Wardak M

4 Tangi Wardak M.Qasem 0799624553 Wardak F

5 Shekh Abad Haji Hashem 0795256408 Wardak F

6 Safi Gran Abdul Bari 0775458555 Wardak M

7 Omer khel company Eng M,Salem 0789076801 Wardak F M

8 Esteqlal Hashmatullah 0788432244 Kabul F

9 Haqyar company Serajudin 0799304151 Kabul F M

10 Khalid Omid Company Hewad Ahamd 0789903010 Kabul F

11 Shahen koh factory Amrullah 0774414586 Kabul F

12 Abdulrahman sons factory Ahmadullah 0700216011 Kabul F

13 Ahadi Brothers Emal 0786224848 Kabul F

14 Saheb Yar Sahib khan 0799306111 Kabul F

15 Pamir Athakhel 0799384700 Kabul F

16 Sadaf Kabul Eng Nematullah 0777328636 Kabul F

17 Takht e Rostem Abdul Baqi 0700503464 Balkh F M

18 Anjirak Esmatullah 0788432244 Kabul M

19 Afghan Sorat Zada Zabihullah 0789908820 Mazar e sharif F

20 Aryan Fazal mawlla 0700727214 Jalal abad F

21 New Aryan Haji kamen 0799324544 Jalal abad M

22 National Dr.Shams 0774708826 Jalal abad F

Research & Statistics Department, AISA

40

23 Toor mining Haji Toor 0778651984 Jalal abad M

24 Helmand mar mar Ali Ahmad 0799600003 Helmand M

25 Ghavsi Brothers company Toryalay 0700400126 Heart F

26 Insaf Fawad Ahmad 0777319061 Panjshir F

27 Bena e khedmat Abdul wali 0786892007 Kabul M

28 Watan Amanullah 0786445923 Kabul F

29 Koh Zamarod Abdul karim 0700292772 Kabul F

30 Kabul Mar Mar Besmellah 0700213134 Kabul F M

31 Sam Safiullah 0799373480 Kabul F

32 Gholghola Group M.Nabi 0799436567 Kabul F

33 Setara e paytakht Abdul Ali 0799263244 Kabul F

34 Pesaran e pir zada Shah mahmod 0777262784 Kabul F

35 Nagin sadaf Nematullah 0700279027 Kabul F

36 Yousaf factory M.yousaf 0799353919 Kabul F

37 Rokham Helmand M.Aref 0799660003 Helmand M

38 Mir Group Sayed Mirwais 0773030525 Herat M

39 Jamal Farhad 077592919 Kabul F

40 Narin company Asadullah 0786179044 Jalal abad F

41 Younas Sons M.Anwar 0700253865 Kabul F

42 Seraj Brothers company Dr. Seraj 0798595595 Kabul F

43 Abdullah Sons Zakaria 0777331227 Kabul F

44 Sher mining sher mohamad 0786115563 Kabul M

45 Gollab mining Gollabdin 0799409337 Kabul M

46 Lajebar Marble & mining Ajab khan 0778872487 Kabul M

47 Rahman mining Fazal rahman 0700606148 Jalal abad M

Research & Statistics Department, AISA

41

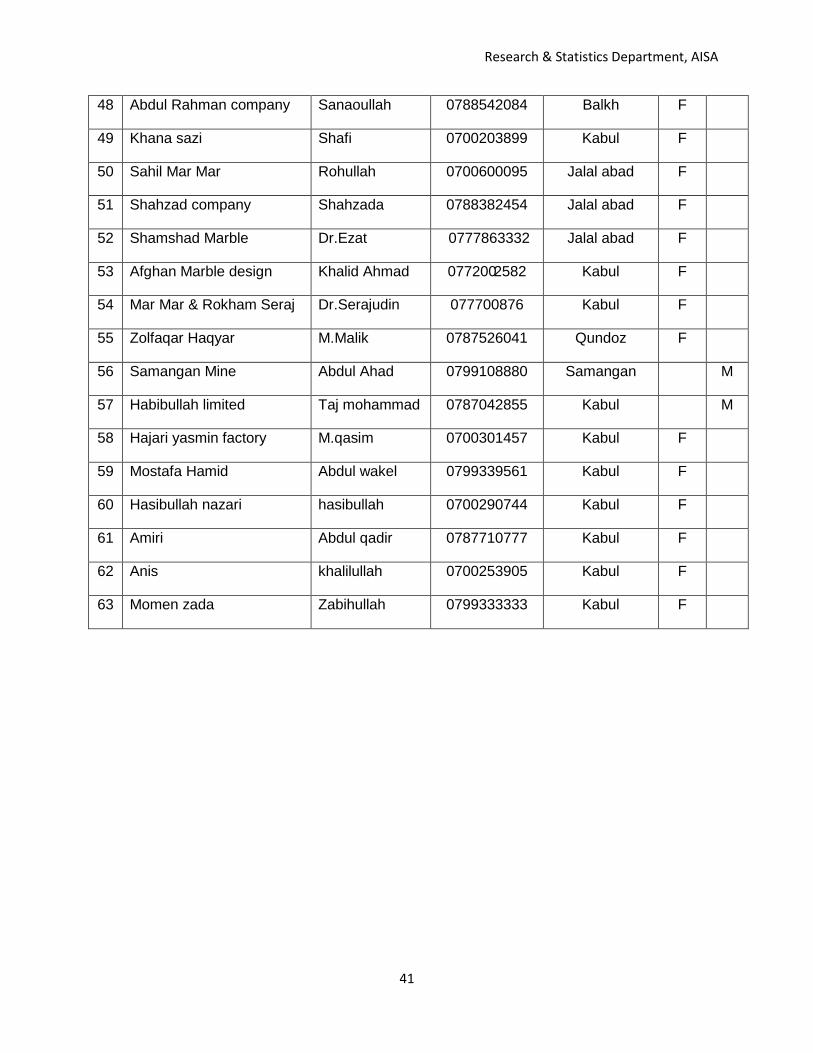

48 Abdul Rahman company Sanaoullah 0788542084 Balkh F

49 Khana sazi Shafi 0700203899 Kabul F

50 Sahil Mar Mar Rohullah 0700600095 Jalal abad F

51 Shahzad company Shahzada 0788382454 Jalal abad F

52 Shamshad Marble Dr.Ezat 0777863332 Jalal abad F

53 Afghan Marble design Khalid Ahmad 0772002582 Kabul F

54 Mar Mar & Rokham Seraj Dr.Serajudin 077700876 Kabul F

55 Zolfaqar Haqyar M.Malik 0787526041 Qundoz F

56 Samangan Mine Abdul Ahad 0799108880 Samangan M

57 Habibullah limited Taj mohammad 0787042855 Kabul M

58 Hajari yasmin factory M.qasim 0700301457 Kabul F

59 Mostafa Hamid Abdul wakel 0799339561 Kabul F

60 Hasibullah nazari hasibullah 0700290744 Kabul F

61 Amiri Abdul qadir 0787710777 Kabul F

62 Anis khalilullah 0700253905 Kabul F

63 Momen zada Zabihullah 0799333333 Kabul F

Research & Statistics Department, AISA

42

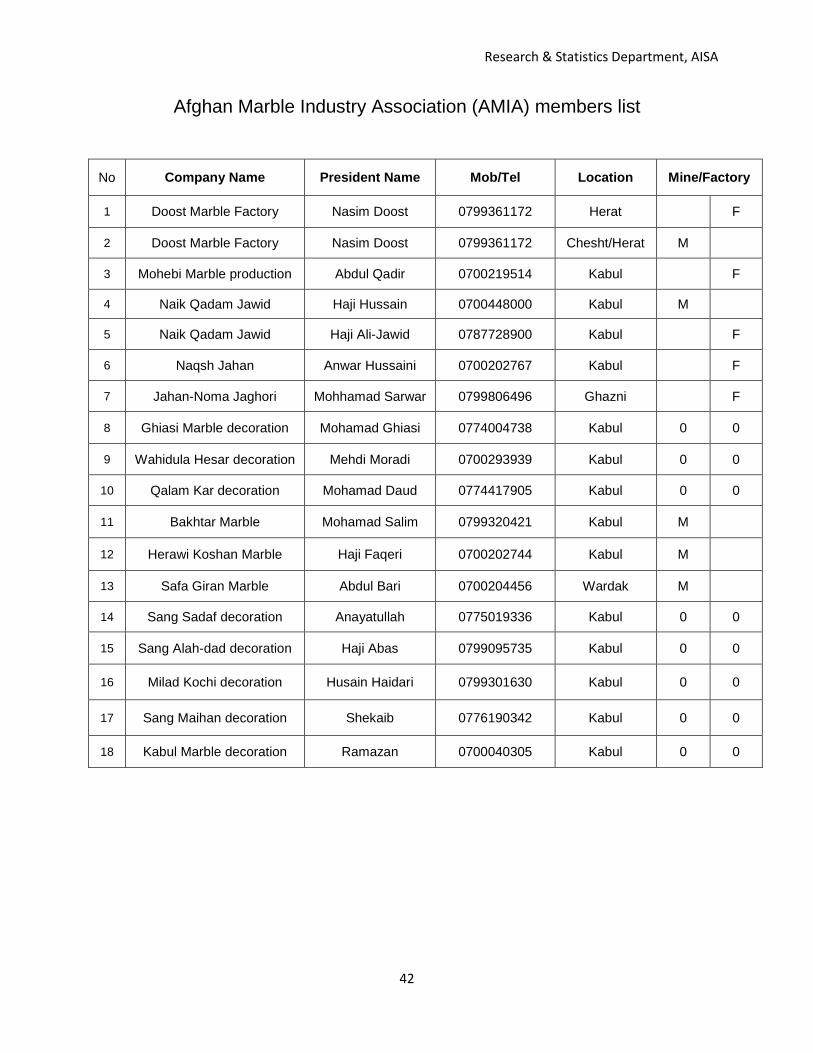

Afghan Marble Industry Association (AMIA) members list

No Company Name President Name Mob/Tel Location Mine/Factory

1 Doost Marble Factory Nasim Doost 0799361172 Herat F

2 Doost Marble Factory Nasim Doost 0799361172 Chesht/Herat M

3 Mohebi Marble production Abdul Qadir 0700219514 Kabul F

4 Naik Qadam Jawid Haji Hussain 0700448000 Kabul M

5 Naik Qadam Jawid Haji Ali-Jawid 0787728900 Kabul F

6 Naqsh Jahan Anwar Hussaini 0700202767 Kabul F

7 Jahan-Noma Jaghori Mohhamad Sarwar 0799806496 Ghazni F

8 Ghiasi Marble decoration Mohamad Ghiasi 0774004738 Kabul 0 0

9 Wahidula Hesar decoration Mehdi Moradi 0700293939 Kabul 0 0

10 Qalam Kar decoration Mohamad Daud 0774417905 Kabul 0 0

11 Bakhtar Marble Mohamad Salim 0799320421 Kabul M

12 Herawi Koshan Marble Haji Faqeri 0700202744 Kabul M

13 Safa Giran Marble Abdul Bari 0700204456 Wardak M

14 Sang Sadaf decoration Anayatullah 0775019336 Kabul 0 0

15 Sang Alah-dad decoration Haji Abas 0799095735 Kabul 0 0

16 Milad Kochi decoration Husain Haidari 0799301630 Kabul 0 0

17 Sang Maihan decoration Shekaib 0776190342 Kabul 0 0

18 Kabul Marble decoration Ramazan 0700040305 Kabul 0 0

Research & Statistics Department, AISA

43

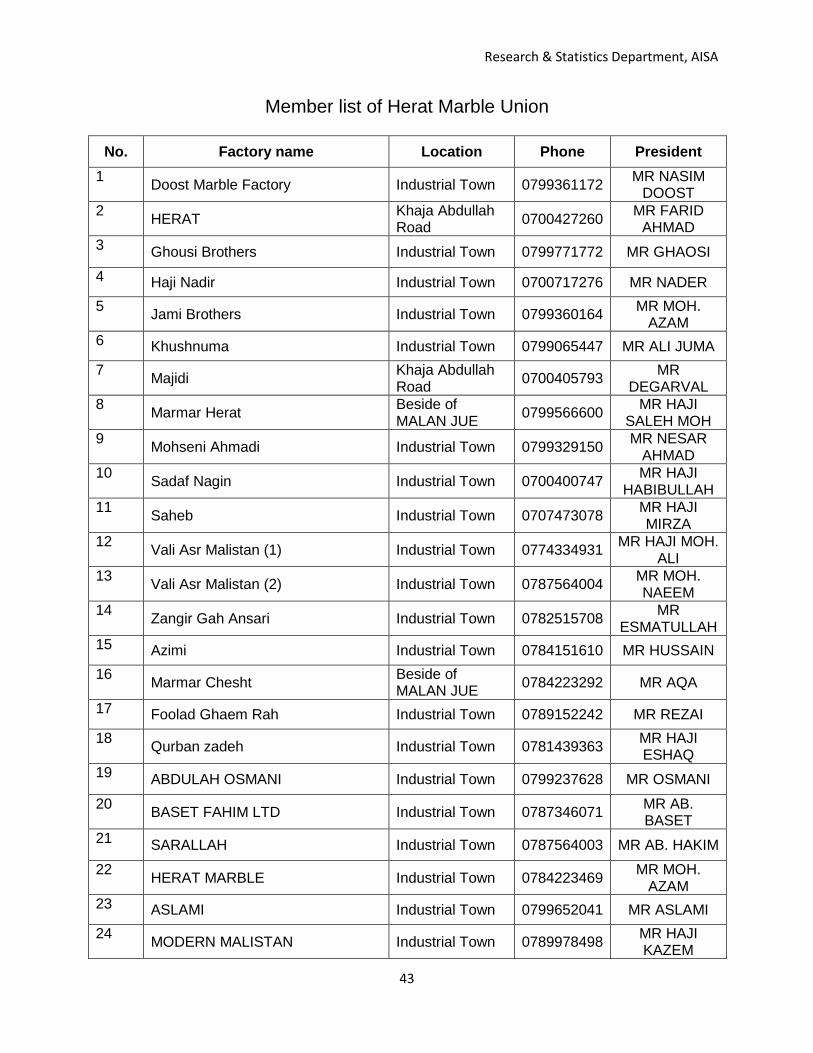

Member list of Herat Marble Union

No. Factory name Location Phone President 1 Doost Marble Factory Industrial Town 0799361172 MR NASIM

DOOST 2 HERAT Khaja Abdullah

Road 0700427260 MR FARID AHMAD

3 Ghousi Brothers Industrial Town 0799771772 MR GHAOSI 4 Haji Nadir Industrial Town 0700717276 MR NADER 5 Jami Brothers Industrial Town 0799360164 MR MOH.

AZAM 6 Khushnuma Industrial Town 0799065447 MR ALI JUMA 7 Majidi Khaja Abdullah

Road 0700405793 MR DEGARVAL

8 Marmar Herat Beside of MALAN JUE 0799566600 MR HAJI

SALEH MOH 9 Mohseni Ahmadi Industrial Town 0799329150 MR NESAR

AHMAD 10 Sadaf Nagin Industrial Town 0700400747 MR HAJI

HABIBULLAH 11 Saheb Industrial Town 0707473078 MR HAJI

MIRZA 12 Vali Asr Malistan (1) Industrial Town 0774334931 MR HAJI MOH.

ALI 13 Vali Asr Malistan (2) Industrial Town 0787564004 MR MOH.

NAEEM 14 Zangir Gah Ansari Industrial Town 0782515708 MR

ESMATULLAH 15 Azimi Industrial Town 0784151610 MR HUSSAIN 16 Marmar Chesht Beside of

MALAN JUE 0784223292 MR AQA

17 Foolad Ghaem Rah Industrial Town 0789152242 MR REZAI 18 Qurban zadeh Industrial Town 0781439363 MR HAJI

ESHAQ 19 ABDULAH OSMANI Industrial Town 0799237628 MR OSMANI

20 BASET FAHIM LTD Industrial Town 0787346071 MR AB. BASET

21 SARALLAH Industrial Town 0787564003 MR AB. HAKIM 22 HERAT MARBLE Industrial Town 0784223469 MR MOH.