Embed Size (px)

Citation preview

2001ANNUAL REPORT

the separation is behind us

there are manyopportunities toenhance returns

our prime focusis operationalimprovement

2 Chairman’s review

4 Chief executive’s review

6 Building Products

8 Concrete

10 Construction

11 Distribution

12 People & safety

13 Environment & community

14 Fletcher Building’s profile

16 Fletcher Building directors

18 Corporate governance

21 Fletcher Building management

22 Financial review

24 Financial statements

56 Audit report

57 Statutory disclosure

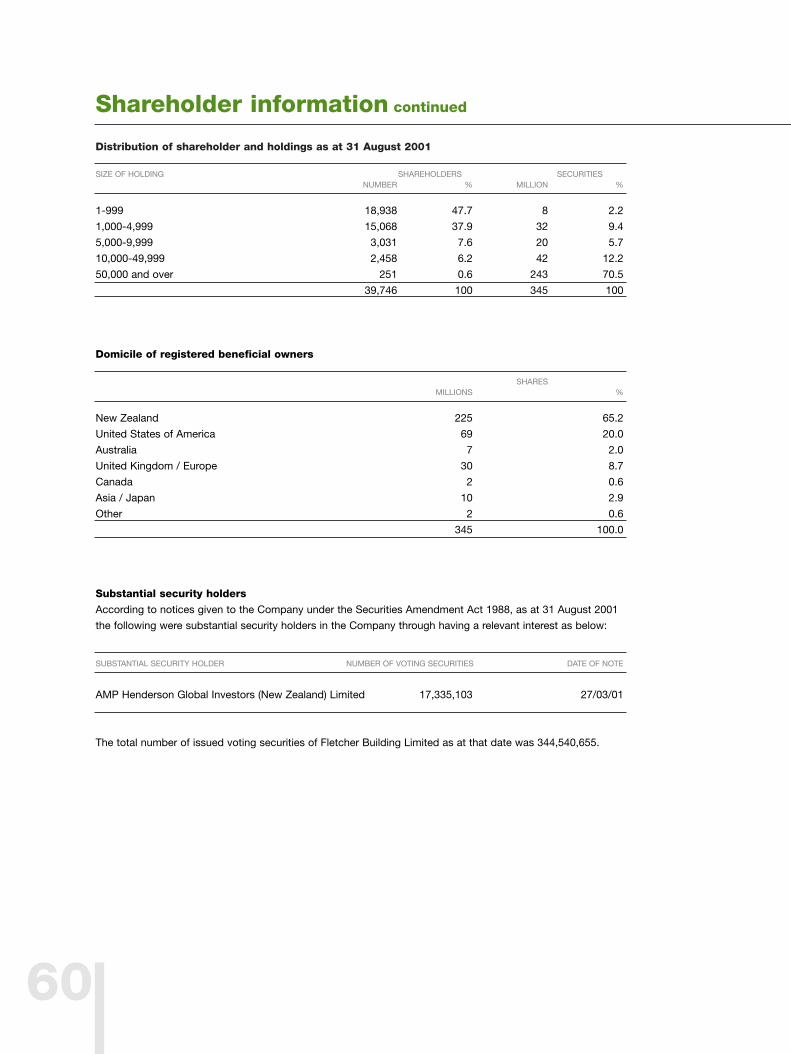

59 Shareholder information

61 Investor information

www.fletcherbuilding.com

Fletcher Building is committed to a high level of customer service. As part of this commitment,

we recently launched a significantly upgraded internet site. The new site displays information

on Fletcher Building’s operations and highlights our well established, powerful brands.

Contents

01

Chairman’s reviewA new beginning As your Chairman, I am

pleased to report, on behalf of the Board of

Directors, on the results and progress of our

new company – Fletcher Building Limited.

On 23 March this year, Fletcher BuildingLimited acquired the operations, assetsand liabilities previously attributed toFletcher Challenge Limited – BuildingOperations, completed the separationprocess from the former parent companyand began a new stand-alone corporateexistence.

This resolved an extended period ofuncertainty about the future of the business. During this time, its futureownership and the value that might beachieved were very much in question,and much forbearance was asked of theshareholders. The Directors of FletcherBuilding are very conscious of the faithshareholders have invested in them andthe company, and will use their bestendeavours to ensure that the investmentis justified.

Thus the results for this new companyare only for the period 24 March to 30June, which will be the normal year endfor Fletcher Building. In that limited trading period, improved operating performance and some recovery indemand led to significant increases inearnings and cash flow when comparedto the approximately nine months periodprior to separation.

Net earnings before unusual items were$22 million in the June period (comparedto $12 million for the rest of the year),and cash flow from operations was$159 million in the June period ($92 million in the rest of the year). Thisstrong recent improvement stands thecompany in good stead as we moveinto the current year.

A difficult full yearIt has been a complex year for FletcherBuilding. Not only was demand sharplydown compared to the previous year,but the process of separation fromFletcher Challenge was very disruptive.Initially, the Fletcher Challenge Board ofDirectors was prepared to consider asale of Fletcher Building as an alternativeto transferring it to existing FletcherChallenge shareholders. This necessitated anumber of potential acquirers conductingdue diligence to enable them to formulateoffers, and this was demanding and distracting for management. In the end,the Fletcher Challenge Board rejectedthe sale option, believing that highervalue would be created if FletcherBuilding was transferred to shareholders.In that context, it is particularly pleasingto note the recent lift in operating performance and the improved share

02

price since the establishment of FletcherBuilding as a stand-alone company – although the share price has beenaffected by the recent catastrophicevents in the United States.

It is also appropriate to note at thispoint that the separation process madeconsiderable demands on the manage-ment and staff of the company. I wouldlike to record the warmest appreciationof the Board for their efforts and loyaltyduring this exacting period.

The results for the nine months prior toseparation are relevant to shareholdersfor two reasons – firstly because, alongwith adjustments to the carrying valuesof assets, they directly affected the valuesat which Fletcher Building acquiredassets from Fletcher Challenge; andsecondly because trading in that periodinfluenced the initial Fletcher Buildingshare price. Further, it is important toreport the 12 months period so thatyear-on-year comparisons can bemade. Thus pro forma accounts for the12 months have been prepared andthese are reported beside those for theperiod 24 March to 30 June.

Revenues for the year were $2,273 million, a reduction of 4 per cent on theprevious 12 months. Net profit after taxand minorities was $34 million beforeunusual items, and a loss of $272 millionafter unusual items. This result wasaffected by $181 million of unusual items,plus the write-off of tax benefits of $125million. Some of these changes wereassociated with the separation from theold Fletcher Challenge Group, while others

resulted from a comprehensive reviewof the carrying values of the assets. Fulldetails are included in the financial sec-tion of this report.

The way aheadWhen the company commenced business on 24 March 2001, MichaelAndrews, the former Fletcher ChallengeChief Executive, was the Acting Chief Executive of Fletcher Building. We informed you in the separationInformation Memorandum that theBoard’s first key task was to identifyand appoint a suitable full time ChiefExecutive. After an international search,the Board appointed Ralph Waters on 1 June. Ralph was previously theManaging Director of Email Limited, a major Australian diversified industrialcompany where he had held seniorpositions over his 18 years of service.Ralph’s long experience in highly competitive industrial markets will beinvaluable, and considerable progress in lifting operating performance isalready evident.

I am confident your new Board, whosesole focus is Fletcher Building, and asubstantially renewed managementteam, will together not only improveresults in the short term, but also shapethe company so as to ensure better resultsare sustainable for the coming years.

I believe the Board we have assembledfor Fletcher Building has the right combination of commercial acumen,experience, fresh perspective and familiarity with the business to take the company forward.

There are seven directors – Ralph Norrisand Ralph Waters are new to the company, Sir Dryden Spring who was a relatively recent appointment to theFletcher Challenge Board and PaulBaines, Hugh Fletcher, Kerrin Vautierand I who are longer-standing membersof the Fletcher Challenge Board andthus have a considerable knowledge of the Fletcher Building operations.

OutlookWith the separation process behind usand the senior management team nowin place, the primary focus for the yearahead will be operational improvement.There are still many challenges. Demandremains subdued, especially in our majormarket of Auckland, there are underper-forming assets in South America and inSteel where solutions will not be easilyfound, and there are energy supply andpricing concerns. However, the core ofFletcher Building is a range of excellentbusinesses with strong market positionsand their recent performance gives the Board confidence about the immediate future.

R S DeaneChairman

03

Fletcher Building Share Price23 March to 11 September 2001

25 M

AR

01

30 M

AR

01

6 A

PR

01

13 A

PR

01

20 A

PR

01

20 A

PR

01

27 A

PR

01

4 M

AY

01

11 M

AY

01

18 M

AY

01

25 M

AY

01

1 JU

N 0

1

8 JU

N 0

1

15 J

UN

01

22 J

UN

01

29 J

UN

01

6 JU

L 01

13 J

UL

01

20 J

UL

01

27 J

UL

01

3 A

UG

01

10 A

UG

01

17 A

UG

01

24 A

UG

01

31 A

UG

01

7 S

EP

01

2.80

2.70

2.60

2.50

2.40

2.30

2.20

2.10

2.00

04

These business segments have clearNew Zealand market leadership in oneor more of their activities. WinstoneWallboards, Golden Bay Cement, Firth’s readymixed concrete, WinstoneAggregates, Fletcher Construction,Pacific Coil Coaters, and PlaceMakersare the major examples.

Although demand did not favour any ofthe businesses, there were good resultsfrom some business units – for example,the full year results from Golden BayCement and Winstone Wallboards, andmuch improved last quarters from FletcherConstruction, Fletcher Residential andPlaceMakers. Wood Panels, Aluminium,Firth and Winstone Aggregates allreported profits well down on the previous year through lower demandand a range of cost issues. Some ofthese were one-time costs such asthose resulting from our exit of the LunnAvenue quarry while others, includingfuel increases in the transport intensivebusinesses and resin in Wood Panels,continue into the new year. The Steelbusiness units were affected by poordomestic demand, competitive pricingand difficulties relating to the implemen-tation of a new information technologysystem. The South American businessesincurred significant losses.

The operational review that follows covers all of the company’s businesses.Whilst the full year results are quite

unsatisfactory, the results of FletcherBuilding Limited since trading com-menced on 24 March 2001 are anencouraging indication of what share-holders might expect of the companygoing forward. Also, resolution of somelong-running disputes in constructionprojects in Australia and New Zealandhas removed further uncertainty fromforward prospects.

Cash flow during the year was strong – particularly in the last quarter, where a $159 million inflow resulted in a year-end net debt of $274 million, comparedto $485 million a year earlier. Thus wehave entered the new financial year withimproving earnings, a strong balancesheet and all major disputes now resolved,providing a sound base for our first fullyear of trading as a stand-alone company.

OperationalimprovementsTo achieve its earnings potential,Fletcher Building will have to commit toa continuous improvement programmethat will affect all facets of the business.There are a number of areas wherechanges have been made to improveperformance.

OrganisationThe company has now been organisedaround four separate operating groups.Each is headed by a chief executiveoverseeing a range of businesses with acommon discipline at its core. The broader,

flatter organisation structure should alloweach chief executive more time to devoteto new initiatives such as new products,new processes, new technologies, ornew complementary business activities.The broader structure did not require thecreation of new positions; it simplyrequired some existing positions to reportdirectly to the Fletcher Building CEO,rather than through an additional level.

ManagementThe senior management team has beensubstantially changed from that in placeprior to separation from Fletcher Challenge.The Executive Committee comprises theseven most senior executives of thecompany. Only two of the present committee were also members of thesenior executive team prior to separation.

Reporting to the operating group chiefexecutives are business unit generalmanagers, and a number of these positions have also undergone or areundergoing change. It is vital that for allgeneral management positions and abovethere be a greater degree of ownershipof, and accountability for, their resultsthan might have been the case in the past.

RemunerationIncentive arrangements have beenchanged to link all performance-basedremuneration to the achievement of asatisfactory level of earnings. Thisreplaced a scheme that rewardedimprovement on the prior year.

Chief executive’s reviewOperations summary The pro forma results for the 2001 year

have been reported for each of the major segments in which

Fletcher Building conducts business. These are Building

Products, Concrete, Construction and Distribution.

Thus, while incentive remuneration entitlements are low given the poorearnings for the 2001 financial year, the previous scheme would, in the 2002financial year, have rewarded improve-ment from this low base.

CostsA hard-headed approach to all costs isvital. Fletcher Building’s head office teamhas been substantially reduced andmajor service providers have also beensubjected to a competitive pricingprocess that has achieved valuable sav-ings. Rather than use its size to achievebetter commercial terms, there is clearevidence that the reverse had occurredin too many areas. Fletcher Buildingparticipates in very competitive markets.It must be vigilant in ensuring it isachieving the lowest supplier cost andoperating its businesses with best prac-tice overhead levels. There is still muchto be done in these areas.

ConsultantsA greater level of self-sufficiency will resultin a substantial reduction in consultants’costs. Despite an over-reliance on externaladvice in the past, there is too little success to show for it.

Capital ExpenditureA disciplined review process for all capitalexpenditure is an imperative of well-runbusinesses. Management’s delegatedauthority level has been reduced fromprevious arrangements to ensure Directorsare more fully informed of investmentsand their implications. It is difficult not toconclude, given the large scale of write-downs on previous capital projects, thatthe review, approval, monitoring andpost-implementation audit processeswere not operating effectively.

InitiativeIt is insufficient to operate in a disciplinedand cost-effective manner. Markets aredynamic and products and processes are

made obsolete by new developments,new technologies and other innovations.Business units will be measured on theirinitiative and innovation, as these arevital ingredients in maintaining marketleadership.

The strategic agendaThe earnings of Fletcher Building arebuilt on a foundation of leading marketpositions for a number of the company’sbusinesses. However, the full potential ofthese leading positions is compromisedby unsatisfactory results from a numberof other involvements.

The strategic priority for the company is to assess whether these under-performingbusinesses can be improved underFletcher Building’s ownership, or whetherthey should be divested. Other businessesalso warrant review because of industrystructure, size, or relevance to FletcherBuilding’s core portfolio.

The major problems are easily identified,but finding a satisfactory solution will bethe greater challenge. To sell an under-performing business at a satisfactoryprice, an opportunity for industry ratio-nalisation is usually required. Where nosuch opportunity exists, the companyfaces the decision of whether to incurfurther write-offs to effect a sale, or bemore patient with the underperformingbusiness. If the outlook is for continuinglosses, action will be taken even if thisresults in under-realisation of asset values.

As a consequence, there are likely to befurther asset sales in the year ahead.Since balance date, an aluminium distri-bution business and our interest in theLunn Avenue quarry have been sold.

VALEIt is with deep regret that we advise ofthe death of Neil Gunn on 17 August2001. Neil was a long-serving seniorexecutive of the Company and theGeneral Manager of Winstone Wallboardsfrom 1990 to 2001. Winstone Wallboardshas long been one of Fletcher Building’smost successful businesses and Neil’sextraordinary passion for excellence andinnovation was a key part of that success.

Ralph WatersChief Executive Officer

05

06

Results were affected by the drop inresidential construction activity in NewZealand and Australia, and increasedcosts flowing from a weaker New Zealanddollar. In the last three months of theyear, results improved in line withincreased activity, particularly in thecommercial sector, offset by increasedenergy costs.

Domestic demand for plasterboarddeclined, with sales volumes down by12%. EBIT was approximately 10%lower than that for the previous year.Product prices were higher and performance board volumes improvedfrom the previous year; however, thecost of imported raw material increasedbecause of the weak New Zealand dollar.

Wood products sales volumes werelower in both the New Zealand andAustralian markets. Whilst the weakerNew Zealand dollar had a positiveimpact on export revenues, resin andshipping costs increased.

The aluminium operations experienceda significant downturn in New Zealand,with sales volumes to franchisees 19%below those for the same period in theprevious year. Export sales, particularlyto Australia, also fell. This was duelargely to the sale of the Hamilton plant,which extruded shapes for export toAustralia, in April 2000. In July 2001, the assets of the Fletcher AluminiumSolution Centres, which distributedrolled and other aluminium productswithin New Zealand, were sold to theUllrich Aluminium Company. Our corebusiness, comprising the windows anddoors operations, has been retained.

Our panel and hardware distributionoperations maintained their revenuesand EBIT in what was a difficult year. In door manufacturing, our volumeswere down 9% and average prices alsofell, while raw material costs increased.

Steel volumes were at a record high asexport orders increased, aided by thelower New Zealand dollar. Domesticprices were weak however, and

extraordinarily high energy prices in thelast quarter of the year had an adverseimpact on margins, especially in steelmanufacturing. Overall steel revenuesincreased by 3%, while EBIT declinedby 55%.

In steel manufacturing, domestic demandfor most products continued to weakenthroughout the year and domestic salesprices were on average $41 per tonnelower than last year. Production wasdiverted to lower margin export markets.Production costs per tonne increasedby approximately 20%, primarily due tohigher scrap prices and electricity charges.

Building ProductsAn integrated business providing customer solutions based onwood-based panels, gypsum plasterboard, aluminium windows,building papers, doors, steel and steel products

Earnings reduced by slump in residential activity

Armour HDM is the latest

innovation from Fletcher

Wood Panels – it’s virtually

indestructible and highly

versatile, which makes it

ideal for security applications

and high impact surfaces

(bank teller counter pictured).

PRO FORMA24 MARCH TO 12 MONTHS 12 MONTHS

BUILDING 30 JUNE 2001 JUNE 2001 JUNE 2000PRODUCTS $ M $ M $ M

Operating revenue 232 840 852

EBITDA(1) 26 96 120

EBIT(2) 16 58 87

Total funds employed 450 450 510

Capital expenditure 4 24 29

(1) Earnings before interest, tax, depreciation, amortisation and unusual items

(2) Earnings before interest, tax and unusual items

07

Increased competition and weakerdemand in steel distribution and roofingled sales and margins to decline andrestructuring costs of $1 million wereincurred. Our continuous paint coatingplant maintained its sales volumes inthe domestic market, but saw a sharpdecline in its export markets during theyear. These operations also experienceddifficulties with the implementation oftheir new information technology systemswhich adversely affected customerservice, margins and administration costs.

An increase in scrap metal prices,together with an increase in throughput,led to a higher dividend for the year

from our joint venture partner, SimsPacific Metal Industries.

Focus and outlook for the 2002 yearAlthough conditions in the residentialmarket are expected to improve, thiswill be steady rather than strong growth.We are well placed to take advantage of any such upturns in the market. In addition, a number of new productsshould provide increased returns. On the negative side international markets, particularly in Asia, have begun the year on a quiet note.

Domestic and international steel pricesare expected to decrease during thisyear, and our focus will be on improvingthe operational performance of the business. As a priority, we will also beseeking to determine the best outcomefor the steel business in any restructuringof the Australasian steel industry.

08

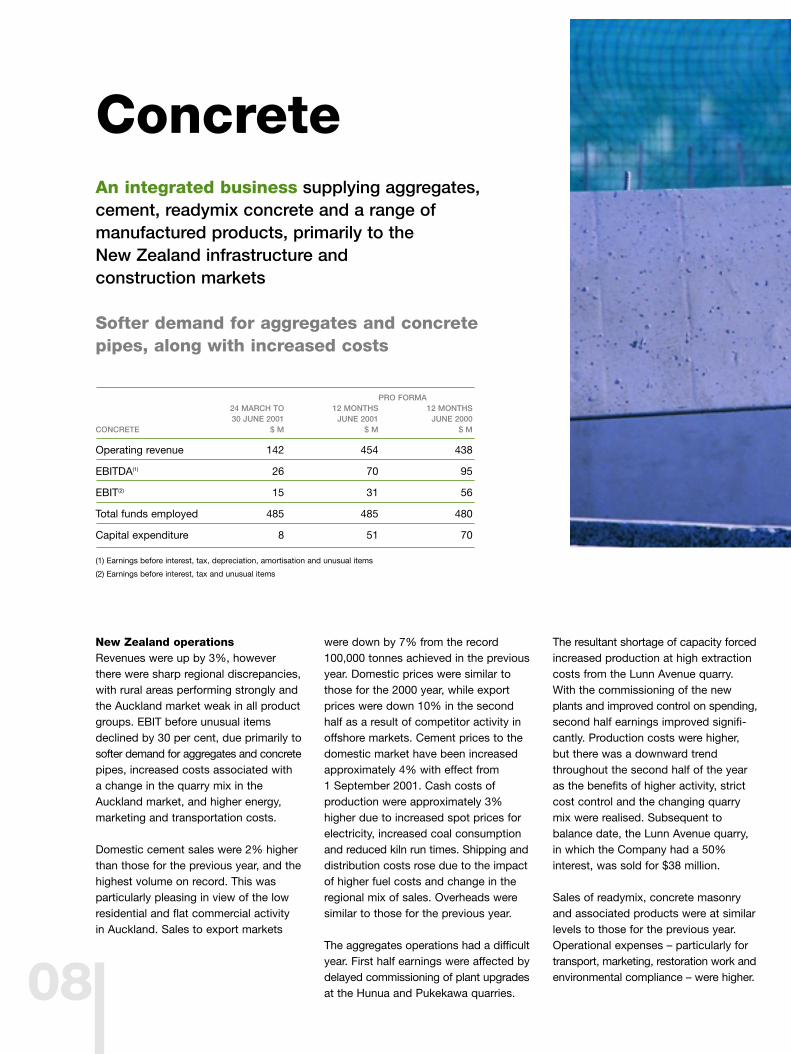

New Zealand operationsRevenues were up by 3%, howeverthere were sharp regional discrepancies,with rural areas performing strongly andthe Auckland market weak in all productgroups. EBIT before unusual itemsdeclined by 30 per cent, due primarily tosofter demand for aggregates and concretepipes, increased costs associated witha change in the quarry mix in theAuckland market, and higher energy,marketing and transportation costs.

Domestic cement sales were 2% higherthan those for the previous year, and thehighest volume on record. This was particularly pleasing in view of the lowresidential and flat commercial activityin Auckland. Sales to export markets

were down by 7% from the record100,000 tonnes achieved in the previousyear. Domestic prices were similar tothose for the 2000 year, while exportprices were down 10% in the secondhalf as a result of competitor activity inoffshore markets. Cement prices to thedomestic market have been increasedapproximately 4% with effect from 1 September 2001. Cash costs of production were approximately 3%higher due to increased spot prices forelectricity, increased coal consumptionand reduced kiln run times. Shipping anddistribution costs rose due to the impactof higher fuel costs and change in theregional mix of sales. Overheads weresimilar to those for the previous year.

The aggregates operations had a difficultyear. First half earnings were affected bydelayed commissioning of plant upgradesat the Hunua and Pukekawa quarries.

The resultant shortage of capacity forcedincreased production at high extractioncosts from the Lunn Avenue quarry.With the commissioning of the newplants and improved control on spending,second half earnings improved signifi-cantly. Production costs were higher,but there was a downward trendthroughout the second half of the yearas the benefits of higher activity, strictcost control and the changing quarrymix were realised. Subsequent to balance date, the Lunn Avenue quarry,in which the Company had a 50% interest, was sold for $38 million.

Sales of readymix, concrete masonryand associated products were at similarlevels to those for the previous year.Operational expenses – particularly fortransport, marketing, restoration work andenvironmental compliance – were higher.

ConcreteAn integrated business supplying aggregates, cement, readymix concrete and a range of manufactured products, primarily to the New Zealand infrastructure and construction markets

Softer demand for aggregates and concrete pipes, along with increased costs

PRO FORMA24 MARCH TO 12 MONTHS 12 MONTHS30 JUNE 2001 JUNE 2001 JUNE 2000

CONCRETE $ M $ M $ M

Operating revenue 142 454 438

EBITDA(1) 26 70 95

EBIT(2) 15 31 56

Total funds employed 485 485 480

Capital expenditure 8 51 70

(1) Earnings before interest, tax, depreciation, amortisation and unusual items

(2) Earnings before interest, tax and unusual items

09

Tighter control on costs should improveearnings in the current financial year.The pre-stressed concrete productsoperations recorded a loss, but havemade significant progress in improvingtheir underlying performance.

Earnings from concrete pipes werereduced by a 20-30% fall in North Islandinfrastructure and pipeline activity. Thismeant our plants ran significantly belowcapacity, resulting in higher manufacturingcosts per tonne, while prices came underpressure from increased competition.

International operationsWeaker than expected market conditionsin Peru and Bolivia resulted in a loss atthe EBIT level. In addition, assets werewritten down by $70 million as the company recognised that the morerecent and prolonged earnings and

economic downturns warranted areassessment of the carrying value of the assets in both countries. Thebusinesses are currently under intensereview. Both management teams have been strengthened and capitalexpenditure is being held to a minimum.

In Peru, the economy has not seen anyimprovement in activity as a consequenceof the recent elections, but someimprovement is forecast over the courseof the year. In Bolivia, the outlook is lesspromising, with activity levels unlikely toimprove until the next financial year atthe earliest. Overall, the South Americanactivities plan to generate positive cashflow next year.

In India, our 50% joint venture operationsin Bangalore and Hyderabad continuedto experience a growing market forreadymix concrete and recorded a smallprofit at the EBIT level.

Focus and outlook for the 2002 yearParticular emphasis will be on achievinga more robust performance in the keyAuckland market, particularly with respectto aggregates and readymix concrete.This will be sought through tighter costcontrol, improved asset utilisation andbetter market penetration.

In offshore markets, the emphasis willbe on obtaining better performancefrom our South American assets, whilesimultaneously establishing the longer-term position of these businesses.

Stresscrete’s timely production and delivery of pre-cast products was a crucial factor in meeting the challenging

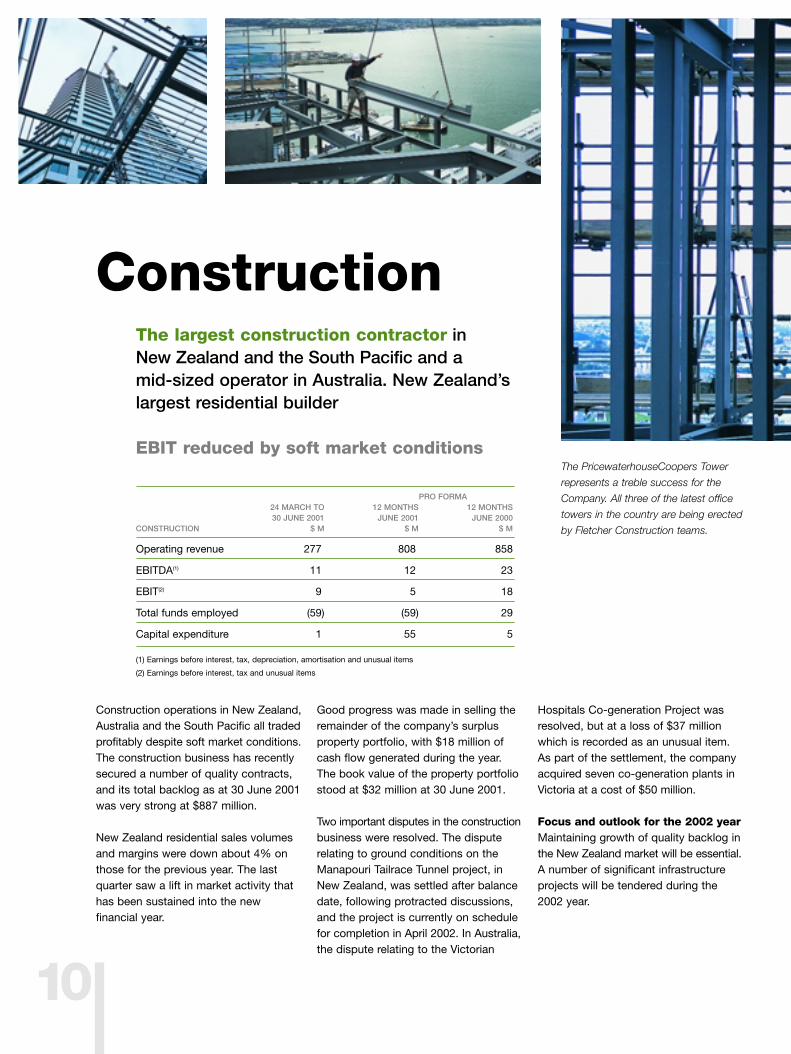

construction timetable – one floor per week – for the PricewaterhouseCoopers Tower project, in Auckland.

10

Construction

The PricewaterhouseCoopers Tower

represents a treble success for the

Company. All three of the latest office

towers in the country are being erected

by Fletcher Construction teams.

Construction operations in New Zealand,Australia and the South Pacific all tradedprofitably despite soft market conditions.The construction business has recentlysecured a number of quality contracts,and its total backlog as at 30 June 2001was very strong at $887 million.

New Zealand residential sales volumesand margins were down about 4% onthose for the previous year. The lastquarter saw a lift in market activity thathas been sustained into the new financial year.

Good progress was made in selling theremainder of the company’s surplusproperty portfolio, with $18 million ofcash flow generated during the year.The book value of the property portfoliostood at $32 million at 30 June 2001.

Two important disputes in the constructionbusiness were resolved. The disputerelating to ground conditions on theManapouri Tailrace Tunnel project, inNew Zealand, was settled after balancedate, following protracted discussions,and the project is currently on schedulefor completion in April 2002. In Australia,the dispute relating to the Victorian

Hospitals Co-generation Project wasresolved, but at a loss of $37 millionwhich is recorded as an unusual item.As part of the settlement, the companyacquired seven co-generation plants inVictoria at a cost of $50 million.

Focus and outlook for the 2002 yearMaintaining growth of quality backlog inthe New Zealand market will be essential.A number of significant infrastructureprojects will be tendered during the2002 year.

The largest construction contractor in New Zealand and the South Pacific and a mid-sized operator in Australia. New Zealand’slargest residential builder

EBIT reduced by soft market conditions

PRO FORMA24 MARCH TO 12 MONTHS 12 MONTHS30 JUNE 2001 JUNE 2001 JUNE 2000

CONSTRUCTION $ M $ M $ M

Operating revenue 277) 808) 858

EBITDA(1) 11) 12) 23

EBIT(2) 9) 5) 18

Total funds employed (59) (59) 29

Capital expenditure 1) 55) 5

(1) Earnings before interest, tax, depreciation, amortisation and unusual items

(2) Earnings before interest, tax and unusual items

11

Customer service in action at The Building Depot,

Mt Wellington.

DistributionBuilding materials distribution throughout New Zealand, to the commercialand residential construction, alterations, additions and DIY markets

A solid performance in a difficult year

Total revenues, including gross jointventure revenue, from the brandedstores PlaceMakers and The BuildingDepot were at 95% of the previousyear’s level, assisted by a small overall increase in cash sales. Thiswas a solid performance in what was

a difficult year in both residential and commercial construction.

Margins improved slightly throughinternal efficiency measures, whichare expected to bring further gains in the coming year.

Focus and outlook for the 2002 yearThe focus will be on further gainsfrom performance improvementmeasures, which are already having a positive impact on operations.

PRO FORMA24 MARCH TO 12 MONTHS 12 MONTHS30 JUNE 2001 JUNE 2001 JUNE 2000

DISTRIBUTION $ M $ M $ M

Operating revenue of owned stores(1) 45 171 223

EBITDA(2) 5 13 15

EBIT(3) 4 6 8

Total funds employed 56 56 70

Capital expenditure 5 3

(1) This does not include the Group’s interest in the joint venture stores

(2) Earnings before interest, tax, depreciation, amortisation and unusual items

(3) Earnings before interest, tax and unusual items

People & safety

12

“Border control” to Fletcher Construction

sites now involves a check that all workers

on site possess a current SiteSafe

Passport, indicating that they have under-

gone a training programme on safe work

practices. On the Courtney Central site in

Wellington, the Fletcher Construction

gatehouse has been embellished with

domestic touches as a counterpoint to

the solemnity of the hazards board.

Building safety into the businessThe building industry in New Zealandhas had a poor safety record. Becauseso many separate groups of peoplework in close proximity in potentiallyhazardous situations, it requires a concerted effort by all parties to achievesafe sites. Pan-industry safety improve-ments have only begun to occur asleading players have demonstrated thenecessary leadership.

SiteSafe is an initiative that FletcherBuilding has embraced and supportedboth financially and with executive support. Through its subsidiary FletcherConstruction, the Company providedseed funding, an inaugural chairmanand subsequent board members andsafety specialists.

A key campaign has been the SiteSafePassport, whereby complying sitesallow employees of contractors andsubcontractors to work on site only ifthey have attended an in-depth safety programme and been issued with the“passport” document. The constructionindustry has, as a result of this increasedsafety focus, experienced a dramaticreduction in work fatalities, down from17 last year to 9 this year. FletcherBuilding's commercial and residential

businesses are actively promoting theSiteSafe campaign on their sites. Thefocus is on general awareness, identifi-cation of specific hazards and practicalsteps to be taken to manage the risk.

Fletcher Building is looking to facilitateefficient sharing of best practice acrossthe business and the development ofcommon core safety standards. Safetychampions are meeting monthly and arecurrently establishing a peer review proce-dure for investigating any serious incident.

The Accident Compensation Corporation(ACC) Partnership Programme is anotherway that Fletcher Building is drivingchange. By self-managing all work-related safety issues and providing self-cover for costs, we not only benefitfrom a rigorous external audit, butreduced premiums provide tangibleendorsement of our sound safety management practices. The most recentACC review elevated Fletcher Building'saccreditation status and complimentedthe Company on the very high level ofemployee involvement in the safetyassessment process.

Other initiatives are also underway.Fletcher Steel is utilising both subjectiveand objective measures in its SmartSiteprogramme. As well as work-related healthmanagement, there are also initiativesfor personal health assessments andseminars under the "Safe & Well” programme which is provided with the

support of the Fletcher Building EmployeeWelfare Fund and the Fletcher BuildingEducational Fund.

The Fletcher Building Employee Educa-tional Fund (EEF) has been establishedto recognise, encourage and financiallysupport vocational learning, and thesharing of learning, amongst FletcherBuilding’s employees and their families.

The EEF is independent of FletcherBuilding, but is an exciting and innovativeplatform for assisting in the developmentof the people who are responsible forFletcher Building’s reputation today andencouraging the people who will shapethe Company for tomorrow. If employeesor their dependants have an educationopportunity and some assistance is need-ed to progress it, the EEF may be able toprovide financial assistance for trainingincluding literacy, vocation, personal skillsdevelopment or extramural education.

Another important initiative is the availability of a special fund, the FletcherBuilding Employee Welfare Fund, to helpemployees and their families in the eventof an unexpected loss such as personalaccident, sickness, death, disability orsubsequent financial hardship. While thisFund is also independent of FletcherBuilding, it assists in creating a supportiveworking environment for our employeesin New Zealand.

Fletcher Building’s operations includenatural resource development andextraction, waste recycling, manufactur-ing and distribution. Our key areas ofenvironmental focus are:• Securing resource consents for

operations• Managing operations to meet

appropriate environmental standards• Innovative business planning to

identify and implement sustainablesolutions

• Participation in regulatory processesto promote effective and practicableenvironmental controls.

Fletcher Building regards environmentalperformance as a key element of sustainable value creation. Our operatingunits are required to comply with environ-mental legislation and regulations, andto report regularly on their performancein this regard. This reporting is supple-mented from time to time by externalaudits. We have made significant investments in plant and equipment in order to maintain compliance.

Our operations are subject to numerousnational and local regulatory regimes forenvironmental performance. In someoperating arenas outside New Zealand,these are at a relatively early stage ofdevelopment. Where this is the case,rather than operating only to local standards we apply a uniform risk management approach that requires theidentification of appropriate measuresand controls to achieve environmentallyresponsible outcomes. We believe that,in general, our international operationshave environmental performance levelshigher than those of locally-ownedcompanies in the countries in whichthey operate.

Fletcher Building is monitoring closely thepotential implications of the New ZealandGovernment’s commitment to ratify theKyoto Protocol on climate change andgreenhouse gas emissions. While wesupport the drive to reduce emissions,and our operations have provided tangiblebacking in recent years through theimplementation of voluntary reductionagreements, we are concerned to ensurethat this aim is achieved in a mannerthat is equitable for all sectors andstakeholders in the New Zealand econ-omy. The issues in terms of internationaltrade and an appropriate domestic policy mix are far from simple, andinformed debate is essential.

Wherever possible, we seek to resolveenvironmental issues in ways that benefitthe community and the company. Oneexample of this approach is at FletcherWood Panels’ Taupo site, where waste-water and stormwater have been divertedfor irrigation, enabling an iwi trust toestablish a thriving dairy farm.

The Wood Panels site, which uses250,000 cubic metres of water annually,had spent 10 years piping processwater 10 kilometres to soak holes in forest plantations. With surface irrigationbecoming the disposal method preferred by environmental authorities,the Company looked to neighbouringfarmland owned by the Tauhara North3B Trust. A successful trial led to a jointventure between the company and thetrust. Eventually, consent was gainedfrom Environment Waikato to irrigate for 30 years over 170 hectares.

Irrigation has enabled the trust to establisha 500 cow dairy herd (eventually to beexpanded to 1000), which deliveredabove-budget production in its first sixmonths of operation. The farm standsout not only for its performance, but alsofor its appearance. While neighbouringproperties wear a sunburnt look in summer,its pastures remain consistently green.

Fletcher Building’s relationship withTangaroa College, in the Auckland suburb of Otara, continued into itssixth year. This involvement providesongoing administrative and strategicsupport for the school, along with amentoring programme for senior students. Other support is providedaccording to need, but has at timesincluded training programmes for teaching and other staff, and advice on human resources, finance, planningand other administrative functions.

Environment & community

13

Surface irrigation of waste water from the

Fletcher Wood Panels Taupo plant has

enabled a neighbouring farmer to establish

a dairy herd that has achieved production

above expectation.

Fletcher Building’s profile

Building Products

Major products

PlasterboardMedium density fibreboard ParticleboardBuilding papers & foilsDoors – interiorAluminium windows & doors

Reinforcing barMerchant barWire rodPipePainted coilWireLong run metal roofing & claddingRoll formed structural products

Key operating statistics

Plasterboard & Building Papers34 million m2 of plasterboard capacity (2 plants)A building paper production facility

Wood Panels & Doors130,000m3 of particleboard capacity (2 plants)160,000 m3 of medium density fibreboard

capacity (1 plant)4 million m2 of hardboard/softboard capacity

(1 plant)2 laminating operationsA door manufacturing plant & 4 prehanging plants12 company owned outlets

Aluminium9,000 tonne capacity in 2 extrusion presses6,500 tonne capacity remelt facility90 franchised fabricators

Upstream Steel300,000 tonne capacity mini-mill steel plant340,000 tonne capacity rolling mill (200,000 bar

and 140,000 rod)A fully integrated wire mill/wire products plantA ferrous & non-ferrous scrap facility

(50% owned)

Downstream Steel12 branch steel merchandising business

nationwide2 metal processing & 5 reinforcing

fabrication facilitiesA continuous paint coating plant11 branch roofing businesses nationwide A steel framed house design & fabrication plant2 galvanising plants2 structural products rollforming factories

Sales by destination %

New Zealand 78Australia 9Asia/Pacific 10North America 3

Competitive strengths

Low cost position in NZ board/panel marketsRespected brandsTrading skills & customer relationships in AsiaBroad distribution networkNZ’s only producer of long steel productsNZ’s only integrated producer of wire & wire

productsAbility to supply a large range of products

within competitive lead times

14

For the 12 months pro forma period ending 30 June 2001

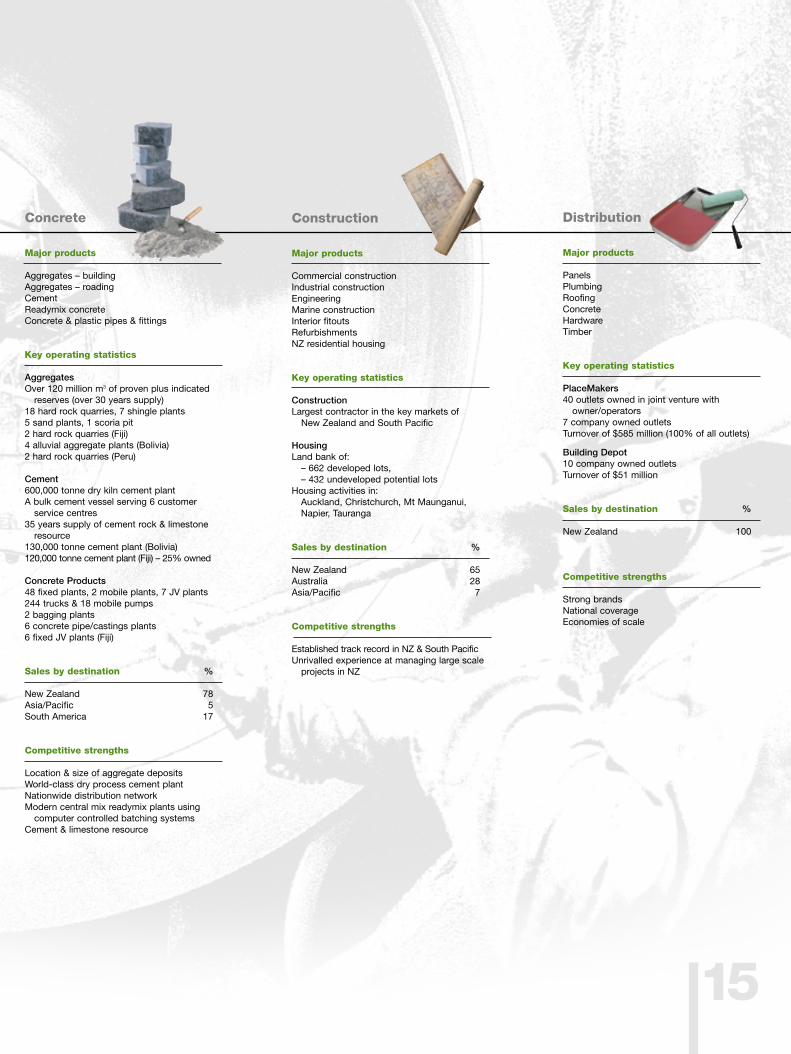

Distribution

Major products

PanelsPlumbingRoofingConcreteHardwareTimber

Key operating statistics

PlaceMakers40 outlets owned in joint venture with

owner/operators7 company owned outletsTurnover of $585 million (100% of all outlets)

Building Depot10 company owned outletsTurnover of $51 million

Sales by destination %

New Zealand 100

Competitive strengths

Strong brandsNational coverageEconomies of scale

Construction

Major products

Commercial constructionIndustrial constructionEngineeringMarine constructionInterior fitoutsRefurbishmentsNZ residential housing

Key operating statistics

ConstructionLargest contractor in the key markets of

New Zealand and South Pacific

HousingLand bank of:

– 662 developed lots,– 432 undeveloped potential lots

Housing activities in:Auckland, Christchurch, Mt Maunganui,Napier, Tauranga

Sales by destination %

New Zealand 65Australia 28Asia/Pacific 7

Competitive strengths

Established track record in NZ & South PacificUnrivalled experience at managing large scale

projects in NZ

Concrete

Major products

Aggregates – buildingAggregates – roadingCementReadymix concreteConcrete & plastic pipes & fittings

Key operating statistics

AggregatesOver 120 million m3 of proven plus indicated

reserves (over 30 years supply)18 hard rock quarries, 7 shingle plants5 sand plants, 1 scoria pit2 hard rock quarries (Fiji)4 alluvial aggregate plants (Bolivia)2 hard rock quarries (Peru)

Cement600,000 tonne dry kiln cement plantA bulk cement vessel serving 6 customer

service centres35 years supply of cement rock & limestone

resource130,000 tonne cement plant (Bolivia)120,000 tonne cement plant (Fiji) – 25% owned

Concrete Products48 fixed plants, 2 mobile plants, 7 JV plants244 trucks & 18 mobile pumps2 bagging plants6 concrete pipe/castings plants6 fixed JV plants (Fiji)

Sales by destination %

New Zealand 78Asia/Pacific 5South America 17

Competitive strengths

Location & size of aggregate depositsWorld-class dry process cement plantNationwide distribution networkModern central mix readymix plants using

computer controlled batching systemsCement & limestone resource

15

Roderick Sheldon DeanePhD, LLD (Hon), BCom(Hons), FACA, FCIS, FNZIM

Chairman of Directors

Dr Deane, 60, is Chairman ofTelecom New Zealand, havingretired as Chief Executive ofthat company in 1999. He isalso Chairman of ANZ BankingGroup (NZ), Te Papa Tongarewa(the Museum of New Zealand),New Zealand Seed FundManagement and New ZealandSeed Fund Partnership. Dr Deane is a director ofTransAlta Corporation (ofCanada), Australia and NewZealand Banking Group andWoolworths (both Australiancompanies). He is Professor ofEconomics and Management atVictoria University of Wellingtonand is on the Board ofGovernance of IHC Inc. Dr Deane has previously beenChief Executive of the ElectricityCorporation of New Zealand,Chairman of Fletcher Challengeand the State ServicesCommission, Deputy Governorof the Reserve Bank of NewZealand, and AlternateExecutive Director of theInternational Monetary Fund.

Paul Edward Alex BainesBCA, CA, MPP

Non-Executive Director Chairman of the AuditCommittee

Mr Baines, 51, is Chairman ofTower Managed Funds and aDirector of Comalco NewZealand, Gough, Gough andHamer, Greenstone Fund, theReserve Bank of New Zealand,Telecom New Zealand andWrightson, and is a memberof the P A Consulting GroupAdvisory Board. He was previously a director ofFletcher Challenge, NewZealand Post and SouthEastern Utilities, and ChiefExecutive Officer of CS FirstBoston New Zealand from1990 until 1993. Prior to thathe held a number of seniorpositions in the sharebrokingand investment banking firmof Jarden & Co.

Hugh Alasdair FletcherMCom (Hons), MBA(Stanford), BSc

Non-Executive DirectorMember of the AuditCommittee

Mr Fletcher, 53, is Chairmanof New Zealand Insurance,CGNU Insurance Australia, a Director of VCU Technology,Infrastructure Auckland andRubicon, a member of the AsiaPacific Advisory Committee ofthe New York Stock Exchange,the Business Advisory Councilof the United Nations Officefor Project Services, the Tertiary Education AdvisoryCommission, the InvestmentCommittee of No 8 Ventures,and the University of AucklandCouncil. Mr Fletcher was previously a director of FletcherChallenge and its ChiefExecutive Officer from 1987until his retirement in 1997.

Ralph James NorrisFNZCS, FNZIM

Non-Executive DirectorMember of the RemunerationCommittee

Mr Norris, 52, is Head ofInternational Financial Servicesfor the Commonwealth BankGroup, a role responsible forthe Group’s operations in New Zealand, the Pacific andAsia and is Managing Directorand CEO of ASB Group. He isalso Chairman of SovereignAssurance and the NewZealand Business Roundtable,Deputy Chairman of the NewZealand Bankers Association,a Director of Air New Zealand,Ansett Holdings and NewZealand’s America’s Cupdefence company. He is alsoa trustee of the Woolf FisherTrust, Northern LifeguardServices and the StarshipChildren’s Hospital Foundation.

16

The Board of Directors

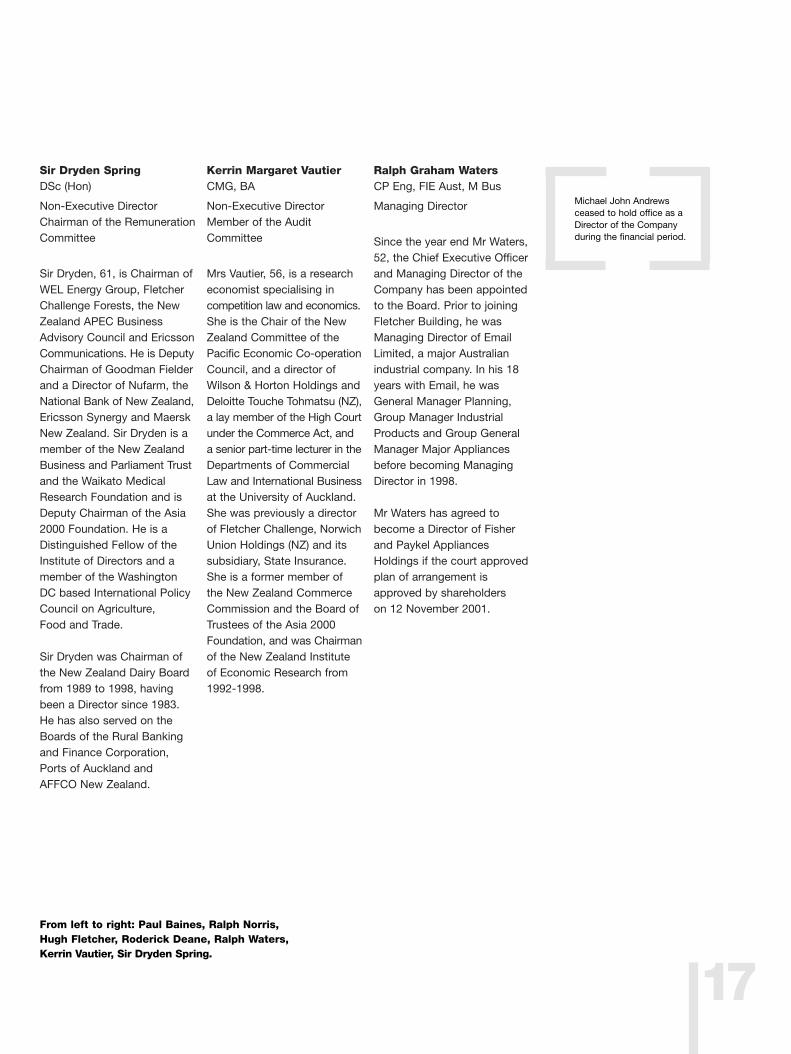

Sir Dryden SpringDSc (Hon)

Non-Executive DirectorChairman of the RemunerationCommittee

Sir Dryden, 61, is Chairman ofWEL Energy Group, FletcherChallenge Forests, the NewZealand APEC BusinessAdvisory Council and EricssonCommunications. He is DeputyChairman of Goodman Fielderand a Director of Nufarm, theNational Bank of New Zealand,Ericsson Synergy and MaerskNew Zealand. Sir Dryden is amember of the New ZealandBusiness and Parliament Trustand the Waikato MedicalResearch Foundation and isDeputy Chairman of the Asia2000 Foundation. He is aDistinguished Fellow of theInstitute of Directors and amember of the WashingtonDC based International PolicyCouncil on Agriculture, Food and Trade.

Sir Dryden was Chairman ofthe New Zealand Dairy Boardfrom 1989 to 1998, havingbeen a Director since 1983.He has also served on theBoards of the Rural Bankingand Finance Corporation,Ports of Auckland and AFFCO New Zealand.

Kerrin Margaret VautierCMG, BA

Non-Executive DirectorMember of the AuditCommittee

Mrs Vautier, 56, is a researcheconomist specialising incompetition law and economics.She is the Chair of the NewZealand Committee of thePacific Economic Co-operationCouncil, and a director ofWilson & Horton Holdings andDeloitte Touche Tohmatsu (NZ),a lay member of the High Courtunder the Commerce Act, anda senior part-time lecturer in theDepartments of CommercialLaw and International Businessat the University of Auckland.She was previously a directorof Fletcher Challenge, NorwichUnion Holdings (NZ) and itssubsidiary, State Insurance.She is a former member of the New Zealand CommerceCommission and the Board ofTrustees of the Asia 2000Foundation, and was Chairmanof the New Zealand Instituteof Economic Research from1992-1998.

Ralph Graham WatersCP Eng, FIE Aust, M Bus

Managing Director

Since the year end Mr Waters,52, the Chief Executive Officerand Managing Director of theCompany has been appointedto the Board. Prior to joiningFletcher Building, he wasManaging Director of EmailLimited, a major Australianindustrial company. In his 18years with Email, he wasGeneral Manager Planning,Group Manager IndustrialProducts and Group GeneralManager Major Appliancesbefore becoming ManagingDirector in 1998.

Mr Waters has agreed tobecome a Director of Fisherand Paykel AppliancesHoldings if the court approvedplan of arrangement isapproved by shareholders on 12 November 2001.

Michael John Andrewsceased to hold office as aDirector of the Companyduring the financial period.

From left to right: Paul Baines, Ralph Norris,Hugh Fletcher, Roderick Deane, Ralph Waters,Kerrin Vautier, Sir Dryden Spring.

17

GovernanceFletcher Building Limited is a NewZealand based building materials manufacturer whose securities are listed on the New Zealand, New Yorkand Australian stock exchanges. Inaccordance with the generally acceptedrequirement by the three exchanges forformal adoption by boards of directorsof approved corporate governancepractices, the Board advises that it is committed to the highest standards ofbehaviour and accountability, and hasadopted the following policies and procedures:

Role of the BoardThe Board has statutory responsibility forthe activities of the Company, which inpractice is exercised through delegationto the Company’s Chief ExecutiveOfficer (CEO) who is charged with theday-to-day leadership and managementof the Company. The CEO also has special responsibility to manage theinterfaces between the Company andthe public, and to act as the principalrepresentative for the Company.

The Board has the obligation to protectand enhance the value of the assets ofthe Company and act in the interests ofthe Company. It exercises this throughthe approval of appropriate corporatestrategies, with particular regard to port-folio composition and return expectations,including the approval of transactionsrelating to acquisitions and divestmentsand capital expenditures above delegatedauthority limits, financial and dividendpolicy and the review of performanceagainst strategic objectives.

The Board evaluates the performance of the CEO and the CEO’s direct reportsannually. The evaluation is based on criteria which include the performanceof the business, the accomplishment oflong-term strategic objectives and othernon-quantitative objectives establishedat the beginning of each year.

The Board supports the concept of theseparation of the role of Chairman fromthat of the CEO. The Chairman’s role isto manage the Board effectively, to pro-vide leadership to the Board, and tointerface with the CEO.

The Board expects to meet formally atleast ten times during the year for a fullday including time allocated to on-sitereview of operations.

The Board believes that the Code ofPractice it applies is consistent with that of the Institute of Directors in NewZealand (Incorporated).

Board compositionAlthough Directors are elected by theshareholders to bring special expertiseor perspectives to Board deliberations,the best interests of the Company mustbe paramount at all times.

The constitution provides that theappropriate size for the Board isbetween three and nine members. Onethird of all Directors stand for electionevery year. The Directors who retire ineach year are those who have beenlongest in office since their last election.The Directors at the commencement oftrading of the Company on 24 March2001 are all considered to have takenoffice at the same time, and may agreea basis for determining those Directorsstanding for re-election.

The terms of reference for the Board,the Chairman, the Committees and theCEO are reviewed annually by theBoard. The Chairman assesses thecomposition and effectiveness of theBoard and its Committees annually.

Board committeesCommittees established by the Boardreview and analyse policies and strategies,usually developed by Management,which are within their terms of reference.They examine proposals and, whereappropriate, make recommendations tothe full Board. Committees do not takeaction or make decisions on behalf ofthe Board unless specifically mandatedby prior Board authority to do so.

The current Committees of the Boardare Audit and Remuneration, whichmeet when necessary and consistentirely of non-executive Directors. The Remuneration Committee has been established as of 13 August 2001,before which all Directors were involvedin remuneration matters. The Boarddoes not have a formal nominationscommittee as all non-executive Directorsare involved in the appointment of newDirectors. A Due Diligence Committeeoperated until 30 June 2001, when it ceased to be a standing committee.From time to time the Board may createad hoc committees to examine specificissues on behalf of the Board.

A Committee or individual Director mayengage separate independent counselat the expense of the Company inappropriate circumstances, with theapproval of the Chairman of the Board.

Corporate Governance

18

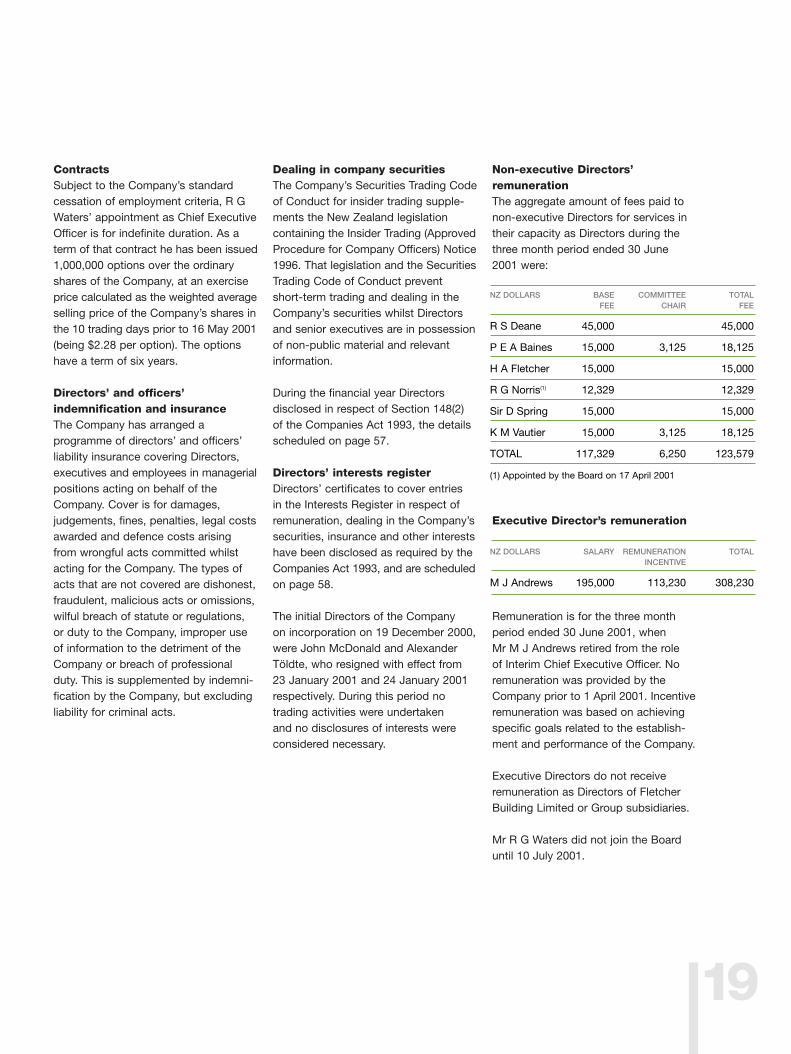

ContractsSubject to the Company’s standardcessation of employment criteria, R GWaters’ appointment as Chief ExecutiveOfficer is for indefinite duration. As aterm of that contract he has been issued1,000,000 options over the ordinaryshares of the Company, at an exerciseprice calculated as the weighted averageselling price of the Company’s shares inthe 10 trading days prior to 16 May 2001(being $2.28 per option). The optionshave a term of six years.

Directors’ and officers’ indemnification and insuranceThe Company has arranged a programme of directors’ and officers’liability insurance covering Directors,executives and employees in managerialpositions acting on behalf of theCompany. Cover is for damages, judgements, fines, penalties, legal costsawarded and defence costs arisingfrom wrongful acts committed whilstacting for the Company. The types ofacts that are not covered are dishonest,fraudulent, malicious acts or omissions,wilful breach of statute or regulations,or duty to the Company, improper useof information to the detriment of theCompany or breach of professionalduty. This is supplemented by indemni-fication by the Company, but excludingliability for criminal acts.

Dealing in company securitiesThe Company’s Securities Trading Codeof Conduct for insider trading supple-ments the New Zealand legislation containing the Insider Trading (ApprovedProcedure for Company Officers) Notice1996. That legislation and the SecuritiesTrading Code of Conduct prevent short-term trading and dealing in theCompany’s securities whilst Directorsand senior executives are in possessionof non-public material and relevantinformation.

During the financial year Directors disclosed in respect of Section 148(2)of the Companies Act 1993, the detailsscheduled on page 57.

Directors’ interests registerDirectors’ certificates to cover entries in the Interests Register in respect ofremuneration, dealing in the Company’ssecurities, insurance and other interestshave been disclosed as required by theCompanies Act 1993, and are scheduledon page 58.

The initial Directors of the Company on incorporation on 19 December 2000,were John McDonald and AlexanderTöldte, who resigned with effect from23 January 2001 and 24 January 2001respectively. During this period no trading activities were undertaken and no disclosures of interests were considered necessary.

Non-executive Directors’ remunerationThe aggregate amount of fees paid tonon-executive Directors for services intheir capacity as Directors during thethree month period ended 30 June2001 were:

Executive Director’s remuneration

Remuneration is for the three monthperiod ended 30 June 2001, when Mr M J Andrews retired from the role of Interim Chief Executive Officer. Noremuneration was provided by theCompany prior to 1 April 2001. Incentiveremuneration was based on achievingspecific goals related to the establish-ment and performance of the Company.

Executive Directors do not receiveremuneration as Directors of FletcherBuilding Limited or Group subsidiaries.

Mr R G Waters did not join the Board until 10 July 2001.

19

NZ DOLLARS BASE COMMITTEE TOTALFEE CHAIR FEE

R S Deane 45,000 45,000

P E A Baines 15,000 3,125 18,125

H A Fletcher 15,000 15,000

R G Norris(1) 12,329 12,329

Sir D Spring 15,000 15,000

K M Vautier 15,000 3,125 18,125

TOTAL 117,329 6,250 123,579

NZ DOLLARS SALARY REMUNERATION TOTALINCENTIVE

M J Andrews 195,000 113,230 308,230

(1) Appointed by the Board on 17 April 2001

20

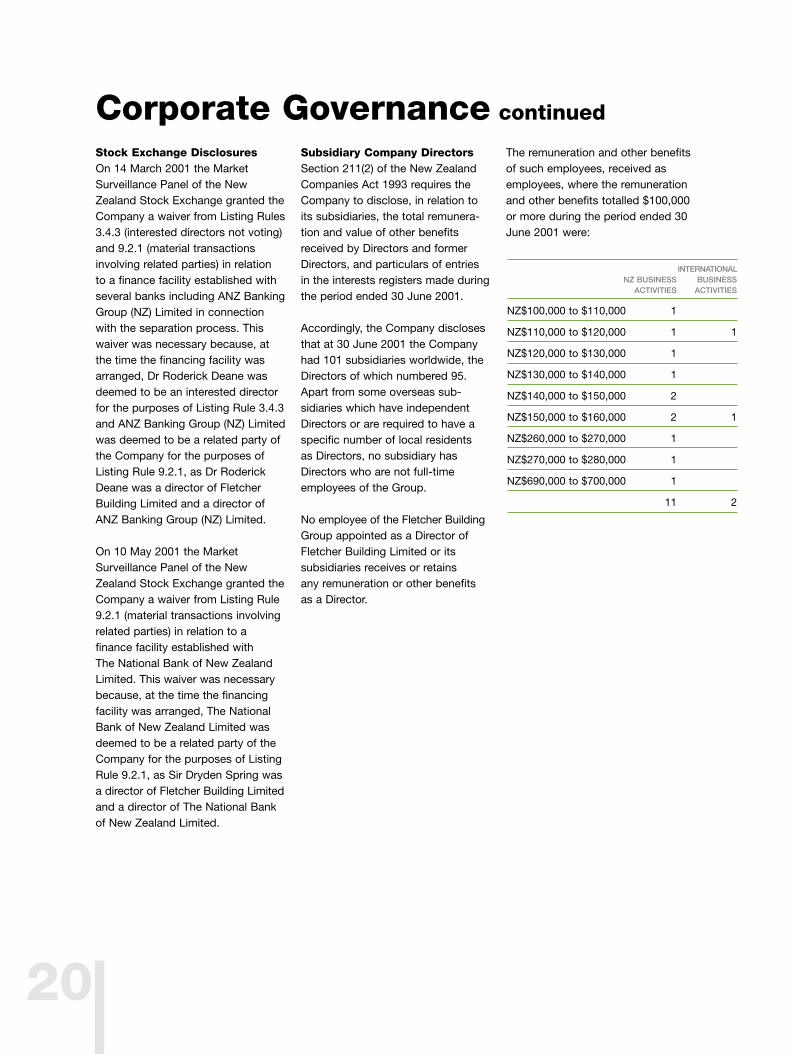

Stock Exchange DisclosuresOn 14 March 2001 the MarketSurveillance Panel of the NewZealand Stock Exchange granted theCompany a waiver from Listing Rules3.4.3 (interested directors not voting)and 9.2.1 (material transactionsinvolving related parties) in relation to a finance facility established withseveral banks including ANZ BankingGroup (NZ) Limited in connectionwith the separation process. Thiswaiver was necessary because, atthe time the financing facility wasarranged, Dr Roderick Deane wasdeemed to be an interested directorfor the purposes of Listing Rule 3.4.3and ANZ Banking Group (NZ) Limitedwas deemed to be a related party ofthe Company for the purposes ofListing Rule 9.2.1, as Dr RoderickDeane was a director of FletcherBuilding Limited and a director ofANZ Banking Group (NZ) Limited.

On 10 May 2001 the MarketSurveillance Panel of the NewZealand Stock Exchange granted theCompany a waiver from Listing Rule9.2.1 (material transactions involvingrelated parties) in relation to afinance facility established with The National Bank of New ZealandLimited. This waiver was necessarybecause, at the time the financingfacility was arranged, The NationalBank of New Zealand Limited wasdeemed to be a related party of theCompany for the purposes of ListingRule 9.2.1, as Sir Dryden Spring wasa director of Fletcher Building Limitedand a director of The National Bankof New Zealand Limited.

Subsidiary Company Directors Section 211(2) of the New ZealandCompanies Act 1993 requires theCompany to disclose, in relation toits subsidiaries, the total remunera-tion and value of other benefitsreceived by Directors and formerDirectors, and particulars of entriesin the interests registers made duringthe period ended 30 June 2001.

Accordingly, the Company disclosesthat at 30 June 2001 the Companyhad 101 subsidiaries worldwide, theDirectors of which numbered 95.Apart from some overseas sub-sidiaries which have independentDirectors or are required to have aspecific number of local residents as Directors, no subsidiary hasDirectors who are not full-timeemployees of the Group.

No employee of the Fletcher BuildingGroup appointed as a Director ofFletcher Building Limited or its subsidiaries receives or retains any remuneration or other benefits as a Director.

The remuneration and other benefitsof such employees, received asemployees, where the remunerationand other benefits totalled $100,000or more during the period ended 30June 2001 were:

Corporate Governance continued

INTERNATIONALNZ BUSINESS BUSINESS

ACTIVITIES ACTIVITIES

NZ$100,000 to $110,000 1

NZ$110,000 to $120,000 1 1

NZ$120,000 to $130,000 1

NZ$130,000 to $140,000 1

NZ$140,000 to $150,000 2

NZ$150,000 to $160,000 2 1

NZ$260,000 to $270,000 1

NZ$270,000 to $280,000 1

NZ$690,000 to $700,000 1

11 2

21

Executive Committee

Chief Executive Officer and Managing DirectorRalph Waters

Company SecretaryMartin Farrell

Chief Financial OfficerBill Roest

Chief Executive – ConcreteMark Binns

Chief Executive – ConstructionMark Binns

Chief Executive – Building ProductsAndrew Reding

Chief Executive – DistributionAppointment pending

General Manager – Planning & Corporate SupportMalcolm Hope

Senior Management Team

Building Products

Fletcher Wood PanelsBob Linton

Scott Panel & HardwareJoan Young (acting GM)

Winstone WallboardsDavid Thomas

Fletcher AluminiumAlec Mandis

Plyco DoorsJo Clayton

Fletcher EasySteelJohn Beveridge

DimondTo be appointed

CSP GalvanizingShane Mitchell

Pacific CoilcoatersRob Hartley

Fletcher ReinforcingRobert Sim

Pacific SteelPacific WireSteel Shared ServicesAlan Pearson

CycloneScott Paterson

Distribution

PlaceMakersKeith Avery

Building DepotGarry Stone

Hire A HubbyWarren Powell

Construction

Chief Financial OfficerCarl Munkowits

NZ Upper North & South Island Peter Neven

NZ Wellington & Lower North IslandBob Hall

AustraliaGraham Taylor

EngineeringGraham Darlow

Fletcher ResidentialBruce Nixon

Concrete

Golden Bay CementRoss Harper

Firth IndustriesChris Badger

StresscreteRobert Gibbes

Winstone AggregatesChris Ellis

Humes Pipeline SystemsJohn Williamson

PeruRoberto Silva

BoliviaKen Cowie

Corporate

TreasurySara Ellis

Chief Information OfficerPaul Knight

Financial ControllerJohn Hames

Fletcher PropertyDavid Wood

ProcurementIan Maynard

Management

From left to right: Martin Farrell, Bill Roest, Malcolm Hope,Ralph Waters, Mark Binns, Andrew Reding.

22

Financial Review

Fletcher Building Limited commenced trading as a stand-alone entity on 24 March 2001, following the acquisition ofthe operations, assets and liabilities previously attributed toFletcher Challenge Limited – Building Operations, as part ofthe Fletcher Challenge Group separation process. The AnnualReport is for the period since incorporation on 19 December2000 but as no trading was undertaken until 24 March 2001,this Report records the financial results for the “TradingPeriod,” being the period 24 March 2001 to 30 June 2001.

For comparative purposes, pro forma accounts have beenprepared. The pro forma results include the earnings of allbusinesses as if the operations, assets and liabilities previouslyattributed to Fletcher Challenge Limited – Building Operationswere part of Fletcher Building Limited from 1 July 2000.Comparative figures for the previous corresponding year have been prepared on a similar basis.

Revenues for the “Trading Period” ended 30 June 2001 were$696 million and reflect external sales only. Earnings beforeinterest, tax and unusual items in the same period were $42million. Compared to the $94 million for the 12 months period,the “Trading Period” result showed a marked improvementthrough better operational performance and some recovery in demand. Net profit after tax and minorities was $22 millionbefore unusual items, and $19 million after unusual items.

Pro forma net profit after tax and minorities was $34 millionbefore unusual items, compared to $106 million for the corresponding period. After unusual items a loss of $272 millionresulted, compared to a profit of $63 million last year.

Despite the difficult trading year, cash generation throughworking capital reductions, construction progress paymentsand improved earnings in the “Trading Period” was encouraging.

The strong cash flow is reflected in Fletcher Building’s ratio ofdebt to total capitalisation (debt to debt plus equity and capitalfunds at book value) reducing to 25.8% from 33.4%, theequivalent ratio at June 2000. Interest cover (EBITDA beforeunusual items / interest paid) for the “Trading Period” was 7.4 times, in line with that achieved at June 2000. At year endFletcher Building had available undrawn facilities of $235 million.

The return on permanent capital (excluding unusual items) forthe “Trading Period” was 17% on an annualised basis. Thiscompares with the return for the 12 months ended June 2001and June 2000 of 10% and 16% respectively. Based on thepro forma 12 months accounts, about 45% of the year’searnings at the EBIT level, and 63% of the year’s cash flow,were generated in the “Trading Period” of just over three months.

While there was a net loss after tax and minorities for the 12months ended 30 June 2001 of $272 million, this result wasaffected by a number of adverse adjustments:

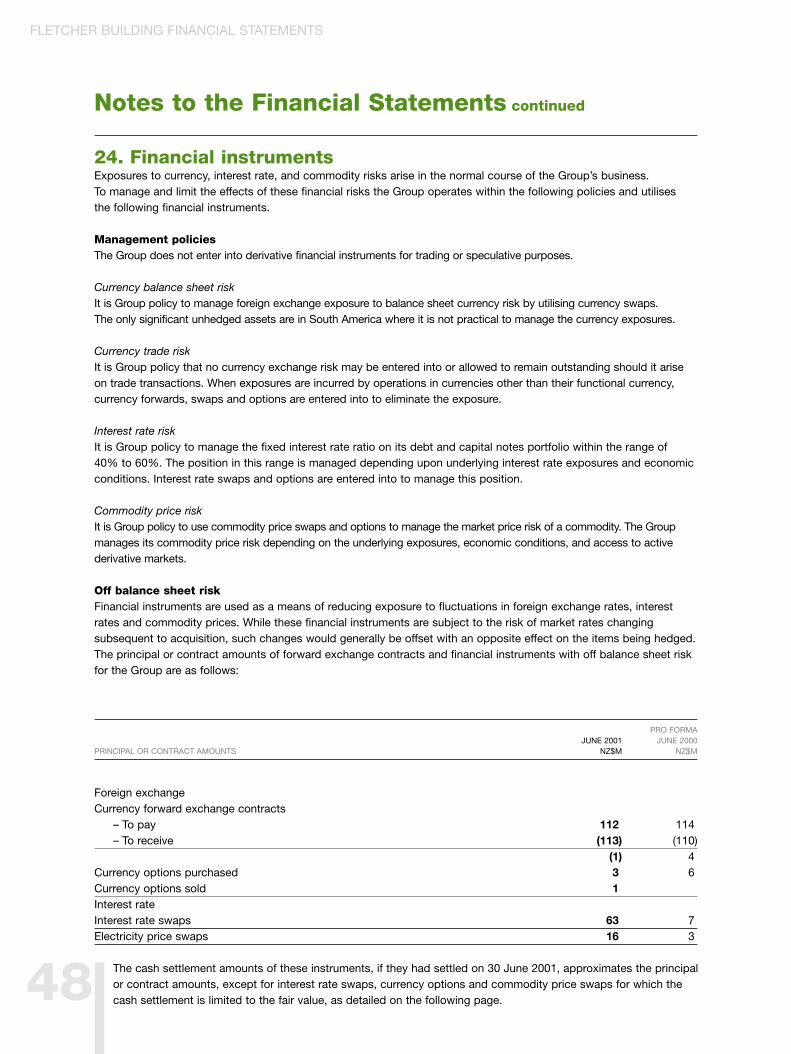

Risk managementThe Company has an integrated programme to manage risksassociated with interest rate, commodity price and exchangerate movements. This hedge programme aims to assure abase level of profitability and reduce volatility in earnings.

RevaluationFollowing the acquisition of the assets of Fletcher ChallengeLimited – Building Operations, the Directors have adopted apolicy to revalue land, buildings and plant and machinery inaccordance with Financial Reporting Standard No 3 “Accountingfor Property, Plant and Equipment.” These valuations havebeen prepared by independent and suitably qualified valuersand have resulted in an uplift of $91 million in the value ofthese assets, a net transfer to the revaluation reserve of $73million and a reduction in the deferred tax asset of $18 million.

Capital notesThe Company will consider replacing capital notes with normaldebt funding as the opportunity arises, and the terms for theOctober 2001 noteholders’ election reflect this.

The initial trading period produced significant increases

in both earnings and cash flow.

$ MILLION

Restructuring and separation costs 43

Permanent impairment 101

Victorian co-generation settlement 37

Unusual items 181

Taxation adjustments 125

Total adjustments 306

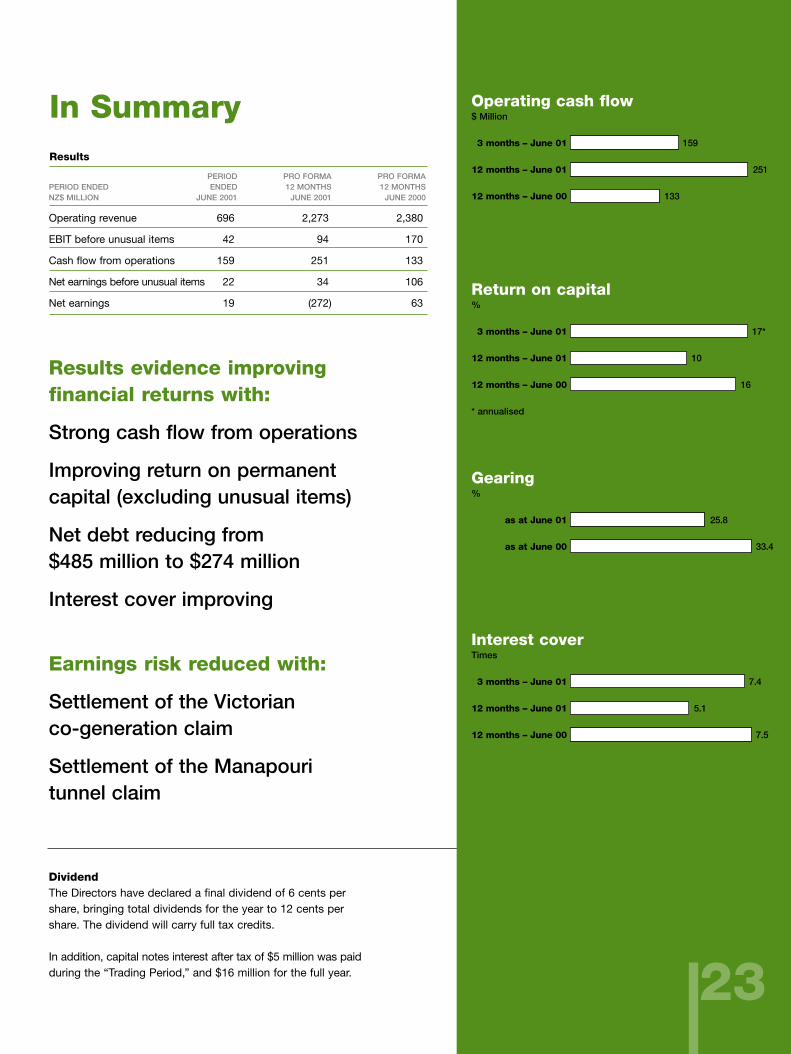

In SummaryResults

PERIOD PRO FORMA PRO FORMAPERIOD ENDED ENDED 12 MONTHS 12 MONTHSNZ$ MILLION JUNE 2001 JUNE 2001 JUNE 2000

Operating revenue 696) 2,273) 2,380)

EBIT before unusual items 42) 94) 170)

Cash flow from operations 159) 251) 133)

Net earnings before unusual items 22) 34) 106)

Net earnings 19) (272) 63)

Results evidence improving financial returns with:

Strong cash flow from operations

Improving return on permanent capital (excluding unusual items)

Net debt reducing from $485 million to $274 million

Interest cover improving

Earnings risk reduced with:

Settlement of the Victorian co-generation claim

Settlement of the Manapouri tunnel claim

23

Operating cash flow$ Million

13 months – June 01 159

12 months – June 01 251

12 months – June 00 133

Return on capital%

13 months – June 01 17*

12 months – June 01 10

12 months – June 00 16

* annualised

Interest coverTimes

13 months – June 01 7.4

12 months – June 01 5.1

12 months – June 00 7.5

Gearing%

as at June 01 25.8

as at June 00 33.4

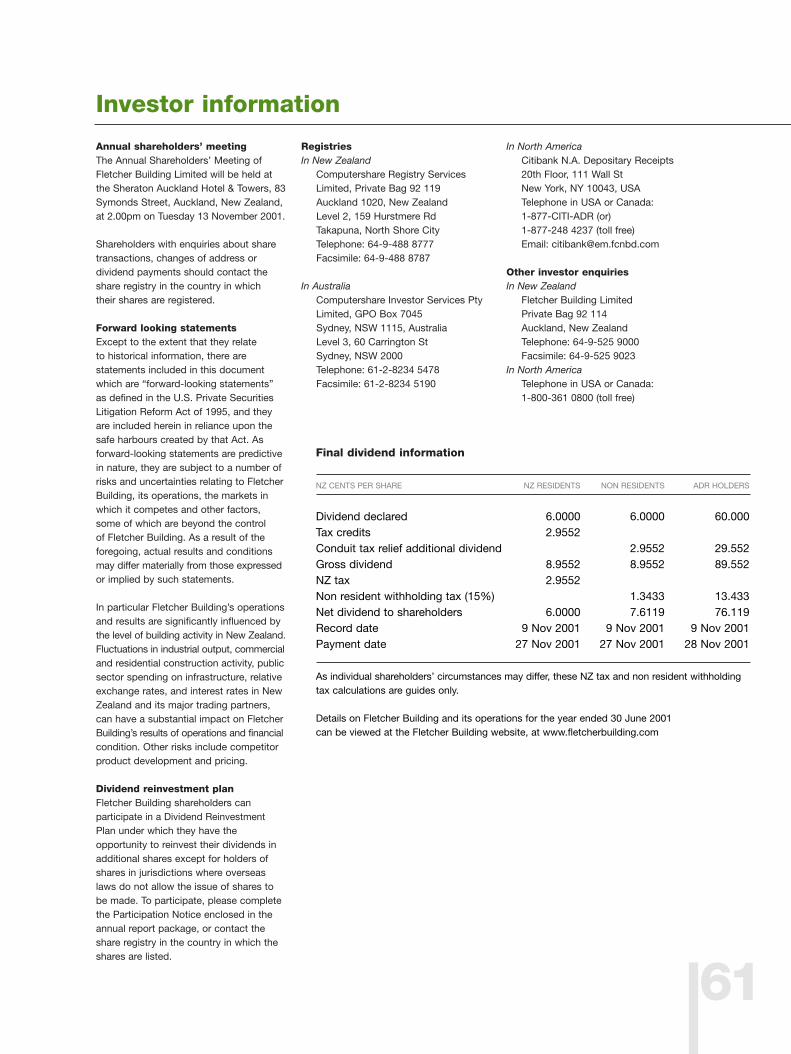

DividendThe Directors have declared a final dividend of 6 cents pershare, bringing total dividends for the year to 12 cents pershare. The dividend will carry full tax credits.

In addition, capital notes interest after tax of $5 million was paidduring the “Trading Period,” and $16 million for the full year.

Financials

24

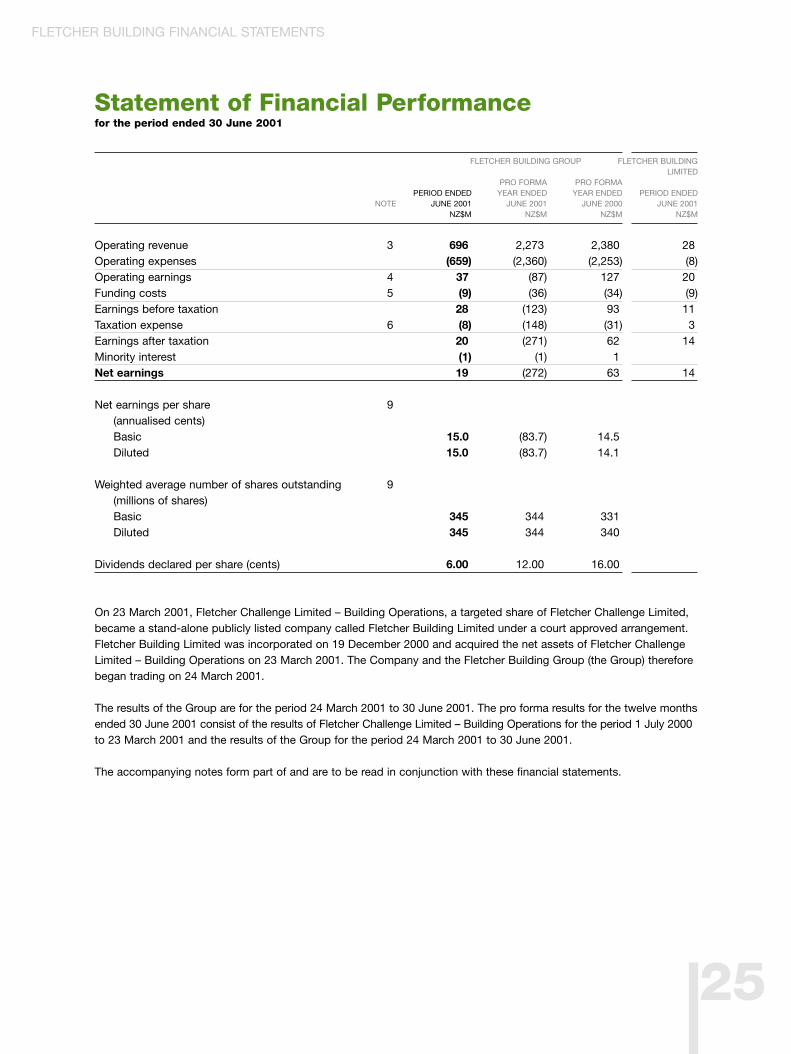

Statement of Financial Performancefor the period ended 30 June 2001

FLETCHER BUILDING GROUP FLETCHER BUILDING LIMITED

PRO FORMA PRO FORMAPERIOD ENDED YEAR ENDED YEAR ENDED PERIOD ENDED

NOTE JUNE 2001 JUNE 2001 JUNE 2000 JUNE 2001NZ$M NZ$M NZ$M NZ$M

Operating revenue 3) 696) 2,273) 2,380) 28)Operating expenses (659) (2,360) (2,253) (8)Operating earnings 4) 37) (87) 127) 20)Funding costs 5) (9) (36) (34) (9)Earnings before taxation 28) (123) 93) 11)Taxation expense 6) (8) (148) (31) 3)Earnings after taxation 20) (271) 62) 14)Minority interest (1) (1) 1)Net earnings 19) (272) 63) 14)

Net earnings per share 9)(annualised cents)Basic 15.0) (83.7) 14.5)Diluted 15.0) (83.7) 14.1)

Weighted average number of shares outstanding 9)(millions of shares)Basic 345) 344) 331)Diluted 345) 344) 340)

Dividends declared per share (cents) 6.00) 12.00) 16.00)

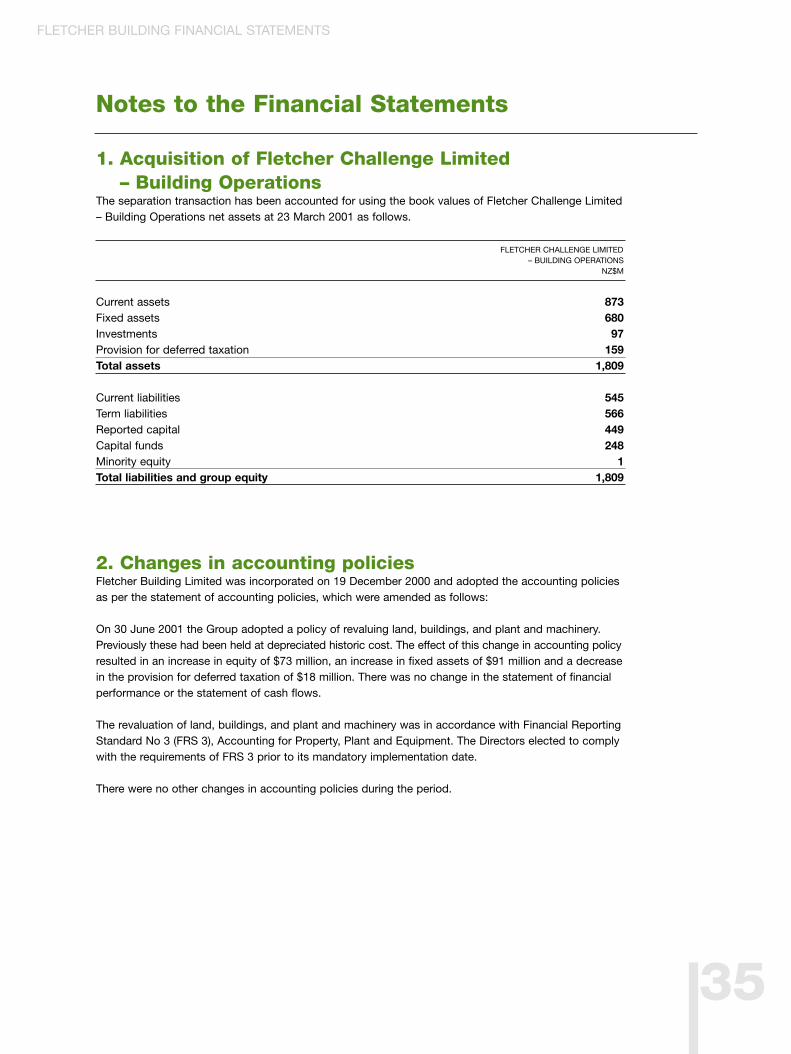

On 23 March 2001, Fletcher Challenge Limited – Building Operations, a targeted share of Fletcher Challenge Limited, became a stand-alone publicly listed company called Fletcher Building Limited under a court approved arrangement. Fletcher Building Limited was incorporated on 19 December 2000 and acquired the net assets of Fletcher Challenge Limited – Building Operations on 23 March 2001. The Company and the Fletcher Building Group (the Group) therefore began trading on 24 March 2001.

The results of the Group are for the period 24 March 2001 to 30 June 2001. The pro forma results for the twelve months ended 30 June 2001 consist of the results of Fletcher Challenge Limited – Building Operations for the period 1 July 2000to 23 March 2001 and the results of the Group for the period 24 March 2001 to 30 June 2001.

The accompanying notes form part of and are to be read in conjunction with these financial statements.

FLETCHER BUILDING FINANCIAL STATEMENTS

25

26

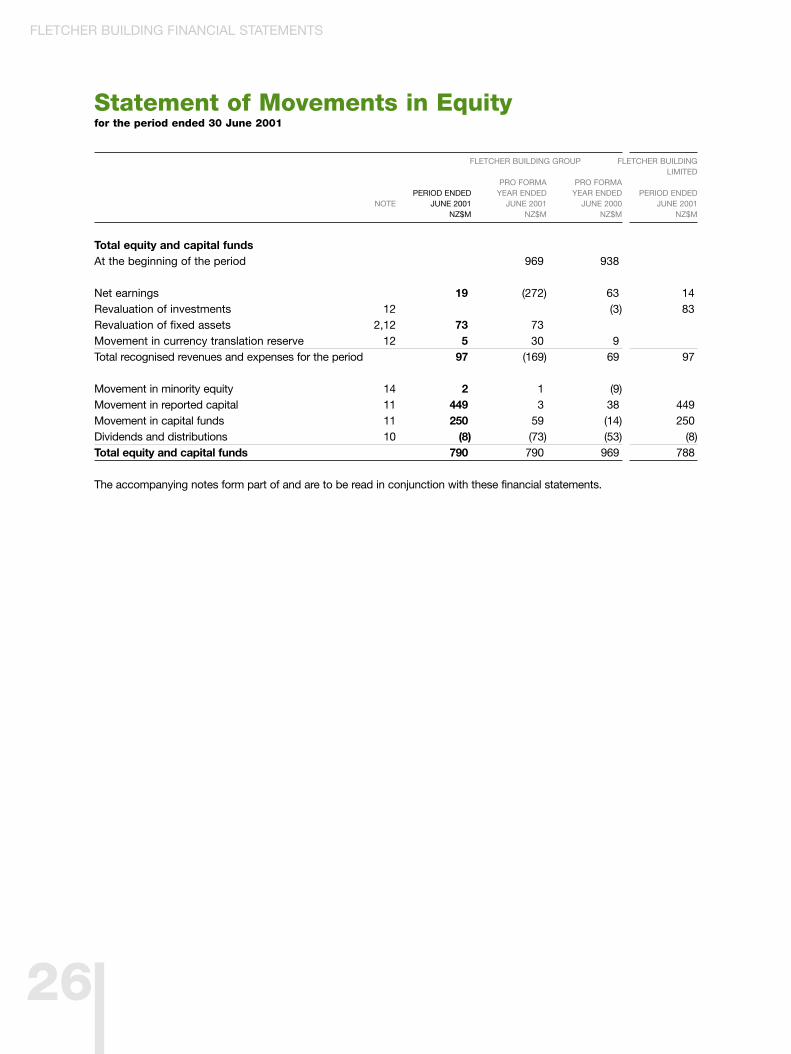

Statement of Movements in Equityfor the period ended 30 June 2001

FLETCHER BUILDING GROUP FLETCHER BUILDING LIMITED

PRO FORMA PRO FORMAPERIOD ENDED YEAR ENDED YEAR ENDED PERIOD ENDED

NOTE JUNE 2001 JUNE 2001 JUNE 2000 JUNE 2001NZ$M NZ$M NZ$M NZ$M

Total equity and capital fundsAt the beginning of the period 969) 938)

Net earnings 19) (272) 63) 14)Revaluation of investments 12 (3) 83)Revaluation of fixed assets 2,12 73) 73)Movement in currency translation reserve 12 5) 30) 9)Total recognised revenues and expenses for the period 97) (169) 69) 97)

Movement in minority equity 14 2) 1) (9)Movement in reported capital 11 449) 3) 38) 449)Movement in capital funds 11 250) 59) (14) 250)Dividends and distributions 10 (8) (73) (53) (8)Total equity and capital funds 790) 790) 969) 788)

The accompanying notes form part of and are to be read in conjunction with these financial statements.

FLETCHER BUILDING FINANCIAL STATEMENTS

27

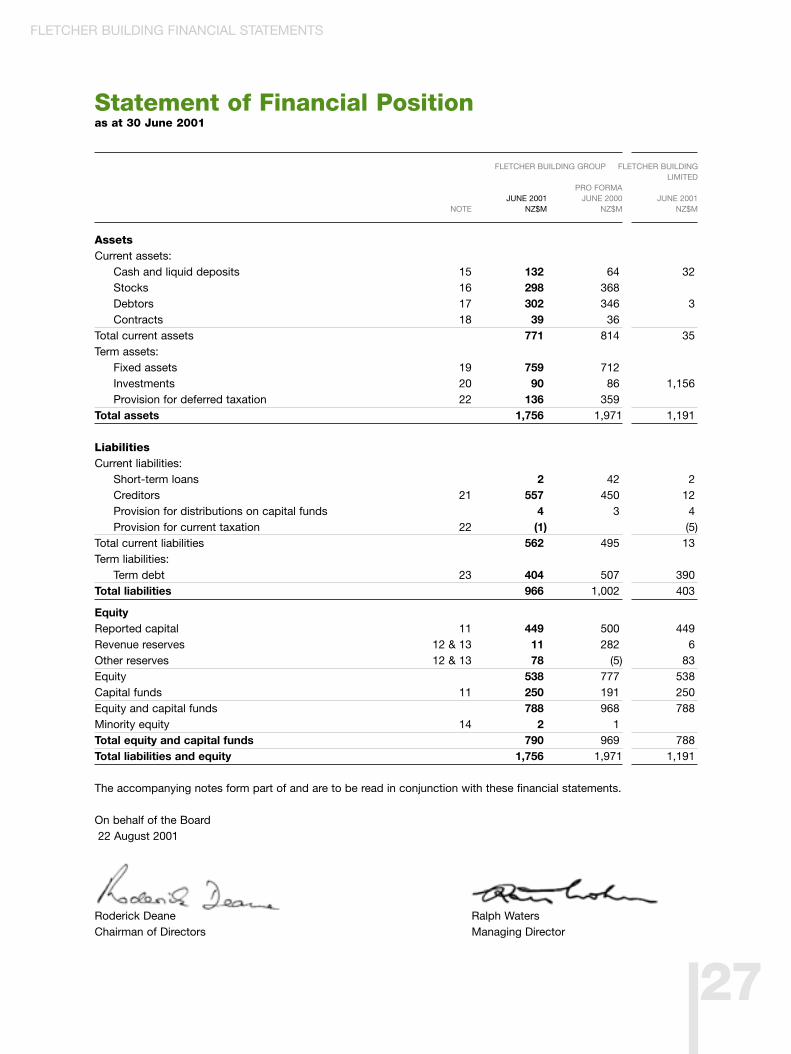

Statement of Financial Positionas at 30 June 2001

FLETCHER BUILDING GROUP FLETCHER BUILDINGLIMITED

PRO FORMAJUNE 2001 JUNE 2000 JUNE 2001

NOTE NZ$M NZ$M NZ$M

AssetsCurrent assets:

Cash and liquid deposits 15 132) 64) 32)Stocks 16 298) 368)Debtors 17 302) 346) 3)Contracts 18 39) 36)

Total current assets 771) 814) 35)Term assets:

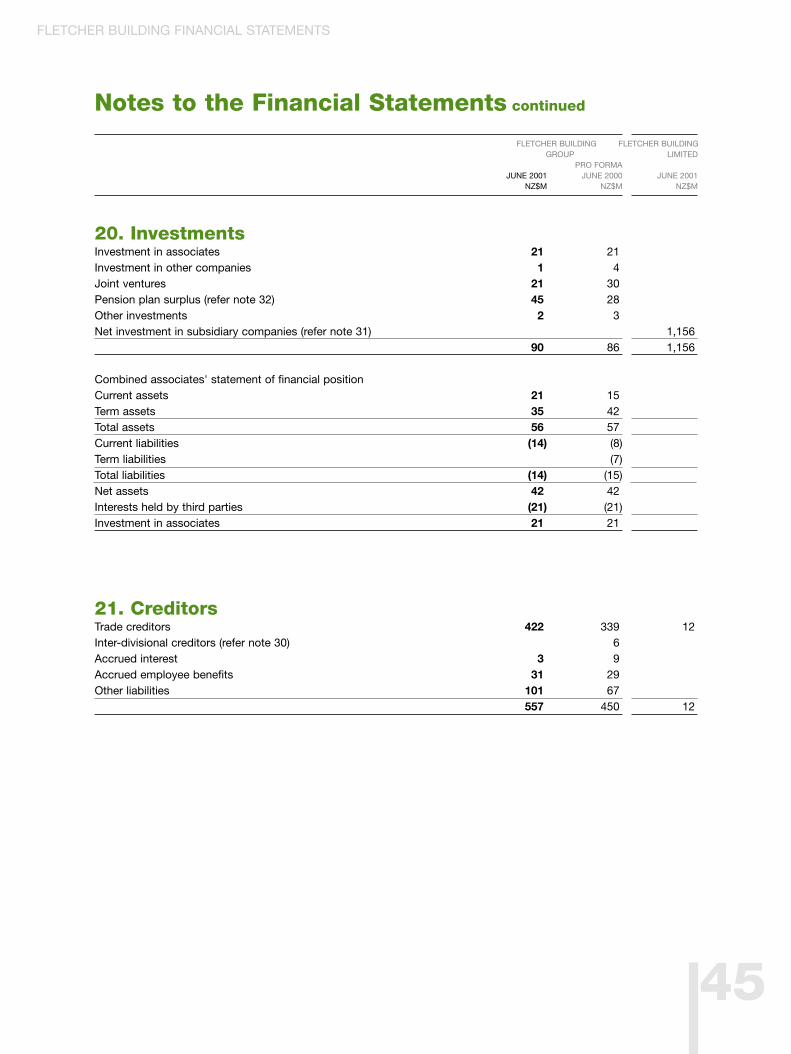

Fixed assets 19 759) 712)Investments 20 90) 86) 1,156)Provision for deferred taxation 22 136) 359) )

Total assets 1,756) 1,971 1,191)

LiabilitiesCurrent liabilities:

Short-term loans 2) 42) 2)Creditors 21 557) 450) 12)Provision for distributions on capital funds 4) 3) 4)Provision for current taxation 22 (1) (5)

Total current liabilities 562) 495) 13)Term liabilities:

Term debt 23 404) 507) 390)Total liabilities 966) 1,002) 403)

EquityReported capital 11 449) 500) 449)Revenue reserves 12 & 13 11) 282) 6)Other reserves 12 & 13 78) (5) 83)Equity 538) 777) 538)Capital funds 11 250) 191) 250)Equity and capital funds 788) 968) 788)Minority equity 14 2) 1)Total equity and capital funds 790) 969) 788)Total liabilities and equity 1,756) 1,971 1,191)

The accompanying notes form part of and are to be read in conjunction with these financial statements.

On behalf of the Board22 August 2001

Roderick Deane Ralph WatersChairman of Directors Managing Director

FLETCHER BUILDING FINANCIAL STATEMENTS

28

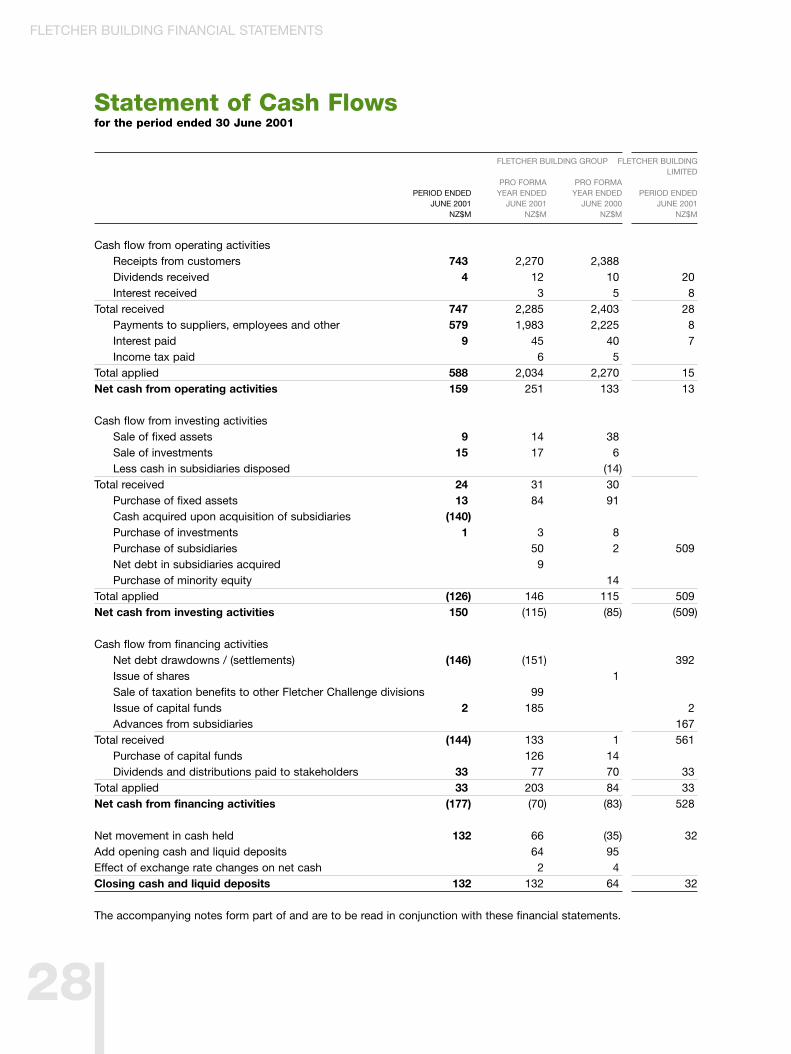

Statement of Cash Flowsfor the period ended 30 June 2001

FLETCHER BUILDING GROUP FLETCHER BUILDINGLIMITED

PRO FORMA PRO FORMAPERIOD ENDED YEAR ENDED YEAR ENDED PERIOD ENDED

JUNE 2001 JUNE 2001 JUNE 2000 JUNE 2001NZ$M NZ$M NZ$M NZ$M

Cash flow from operating activitiesReceipts from customers 743) 2,270) 2,388)Dividends received 4) 12) 10) 20)Interest received 3) 5) 8)

Total received 747) 2,285) 2,403) 28)Payments to suppliers, employees and other 579) 1,983) 2,225) 8)Interest paid 9) 45) 40) 7)Income tax paid 6) 5)

Total applied 588) 2,034) 2,270) 15)Net cash from operating activities 159) 251) 133) 13)

Cash flow from investing activitiesSale of fixed assets 9) 14) 38)Sale of investments 15) 17) 6)Less cash in subsidiaries disposed (14)

Total received 24) 31) 30)Purchase of fixed assets 13) 84) 91)Cash acquired upon acquisition of subsidiaries (140)Purchase of investments 1) 3) 8)Purchase of subsidiaries 50) 2) 509)Net debt in subsidiaries acquired 9)Purchase of minority equity 14)

Total applied (126) 146) 115) 509)Net cash from investing activities 150) (115) (85) (509)

Cash flow from financing activitiesNet debt drawdowns / (settlements) (146) (151) 392)Issue of shares 1)Sale of taxation benefits to other Fletcher Challenge divisions 99)Issue of capital funds 2) 185) 2)Advances from subsidiaries 167)

Total received (144) 133) 1) 561)Purchase of capital funds 126) 14)Dividends and distributions paid to stakeholders 33) 77) 70) 33)

Total applied 33) 203) 84) 33)Net cash from financing activities (177) (70) (83) 528)

Net movement in cash held 132 66) (35) 32 Add opening cash and liquid deposits 64) 95)Effect of exchange rate changes on net cash 2) 4)Closing cash and liquid deposits 132 132) 64) 32

The accompanying notes form part of and are to be read in conjunction with these financial statements.

FLETCHER BUILDING FINANCIAL STATEMENTS

Statement of Cash Flows continuedfor the period ended 30 June 2001

FLETCHER BUILDING GROUP FLETCHER BUILDINGLIMITED

PRO FORMA PRO FORMAPERIOD ENDED YEAR ENDED YEAR ENDED PERIOD ENDED

JUNE 2001 JUNE 2001 JUNE 2000 JUNE 2001NZ$M NZ$M NZ$M NZ$M

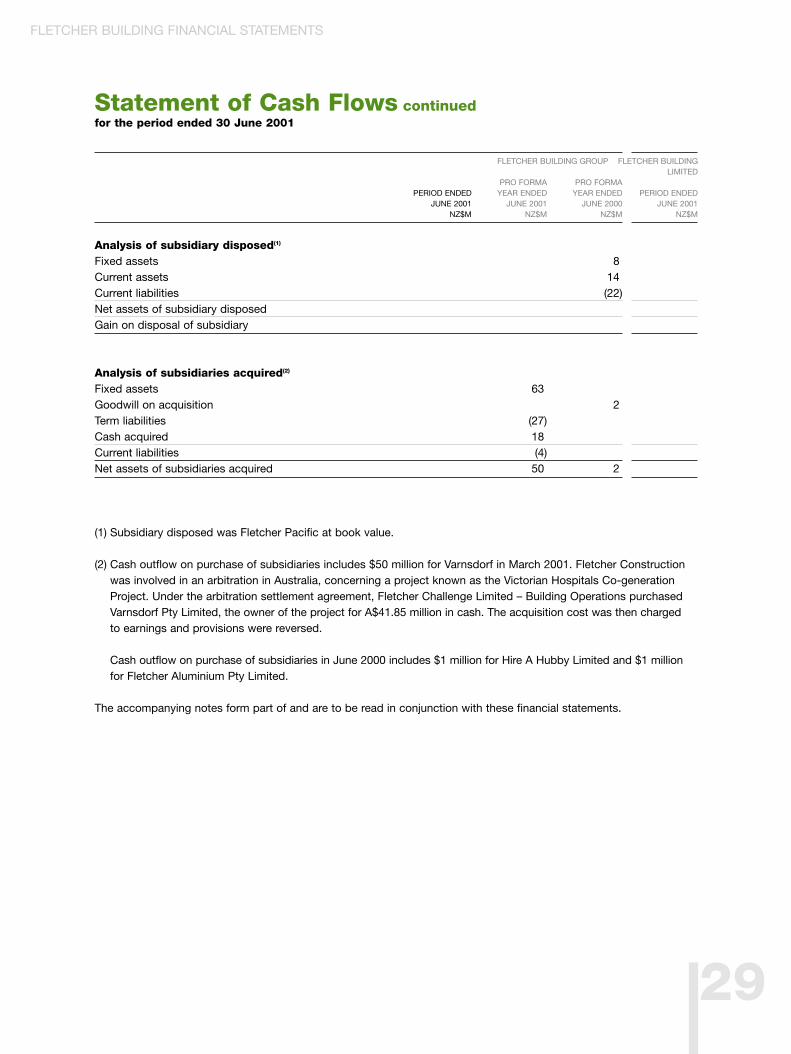

Analysis of subsidiary disposed(1) )Fixed assets 8)Current assets 14)Current liabilities (22)Net assets of subsidiary disposedGain on disposal of subsidiary

Analysis of subsidiaries acquired(2)

Fixed assets 63)Goodwill on acquisition 2)Term liabilities (27)Cash acquired 18)Current liabilities (4)Net assets of subsidiaries acquired 50) 2)

(1) Subsidiary disposed was Fletcher Pacific at book value.

(2) Cash outflow on purchase of subsidiaries includes $50 million for Varnsdorf in March 2001. Fletcher Construction was involved in an arbitration in Australia, concerning a project known as the Victorian Hospitals Co-generation Project. Under the arbitration settlement agreement, Fletcher Challenge Limited – Building Operations purchased Varnsdorf Pty Limited, the owner of the project for A$41.85 million in cash. The acquisition cost was then charged to earnings and provisions were reversed.

(2) Cash outflow on purchase of subsidiaries in June 2000 includes $1 million for Hire A Hubby Limited and $1 millionfor Fletcher Aluminium Pty Limited.

The accompanying notes form part of and are to be read in conjunction with these financial statements.

29

FLETCHER BUILDING FINANCIAL STATEMENTS

30

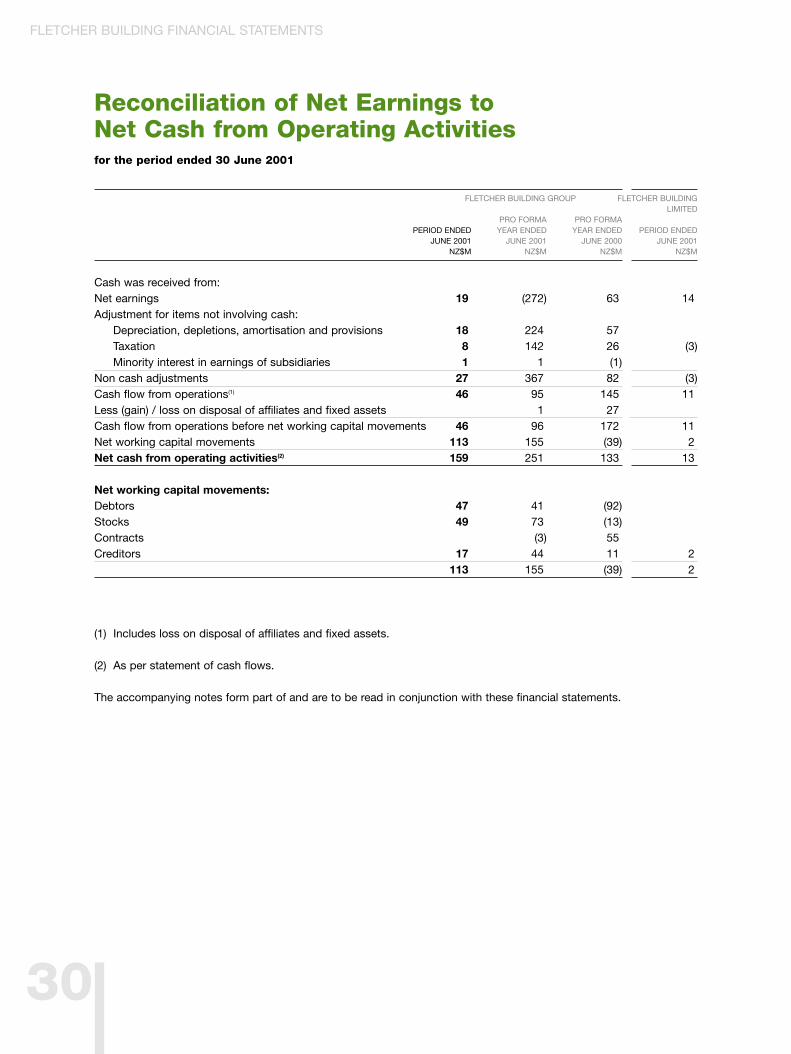

Reconciliation of Net Earnings to Net Cash from Operating Activitiesfor the period ended 30 June 2001

FLETCHER BUILDING GROUP FLETCHER BUILDINGLIMITED

PRO FORMA PRO FORMAPERIOD ENDED YEAR ENDED YEAR ENDED PERIOD ENDED

JUNE 2001 JUNE 2001 JUNE 2000 JUNE 2001NZ$M NZ$M NZ$M NZ$M

Cash was received from:Net earnings 19) (272) 63) 14)Adjustment for items not involving cash:

Depreciation, depletions, amortisation and provisions 18) 224) 57)Taxation 8) 142) 26) (3)Minority interest in earnings of subsidiaries 1) 1) (1)

Non cash adjustments 27) 367) 82) (3)Cash flow from operations(1) 46) 95) 145) 11)Less (gain) / loss on disposal of affiliates and fixed assets 1) 27)Cash flow from operations before net working capital movements 46) 96) 172) 11)Net working capital movements 113) 155) (39) 2)Net cash from operating activities(2) 159) 251) 133) 13)

Net working capital movements:Debtors 47) 41) (92)Stocks 49) 73) (13)Contracts (3) 55)Creditors 17) 44) 11) 2)

113) 155) (39) 2)

(1) Includes loss on disposal of affiliates and fixed assets.

(2) As per statement of cash flows.

The accompanying notes form part of and are to be read in conjunction with these financial statements.

FLETCHER BUILDING FINANCIAL STATEMENTS

31

Statement of Accounting Policiesfor the period ended 30 June 2001

Basis of presentationThe financial statements presentedare those of Fletcher Building Limited(the “Company”) and its subsidiaries(the “Group”). Fletcher BuildingLimited is a company domiciled inNew Zealand, is registered under the Companies Act 1993, and is anissuer in terms of the Securities Act1978 and the Financial Reporting Act1993. The financial statements arepresented in accordance with theCompanies Act 1993 and have beenprepared in accordance with theFinancial Reporting Act 1993.

The financial statements comprisestatements of the following: financialperformance, movements in equity,financial position, cash flows,significant accounting policies, aswell as the notes to these statements.

On 23 March 2001, FletcherChallenge Limited – BuildingOperations, a targeted share ofFletcher Challenge Limited, becamea stand-alone publicly listedcompany called Fletcher BuildingLimited under a court approvedarrangement. Fletcher BuildingLimited was incorporated on 19 December 2000 and acquired thenet assets of Fletcher ChallengeLimited – Building Operations on 23 March 2001. The Company andGroup therefore began trading on 24 March 2001.

The results of the Fletcher BuildingGroup are for the period 24 March2001 to 30 June 2001. The pro formaresults for the twelve months ended30 June 2001 consist of the resultsof Fletcher Challenge Limited –Building Operations for the period 1 July 2000 to 23 March 2001 andthe results of the Fletcher BuildingGroup for the period 24 March 2001to 30 June 2001.

Fletcher Challenge Limited – BuildingOperations financial statements forthe year ended 30 June 2000 havebeen provided for comparativepurposes. For the year ended 30June 2000 and for the period up to23 March 2001, Fletcher ChallengeLimited – Building Operations was a division and targeted share ofFletcher Challenge Limited. As thefinancial statements of FletcherChallenge Limited – BuildingOperations are derived from thefinancial statements of FletcherChallenge Limited, they should at all times be read in conjunction withthe financial statements of FletcherChallenge Limited and in particularwith the basis of attributing assets,liabilities, income and expenses to the then divisions of FletcherChallenge Limited as set out in thestatement of adopted policies.

Accounting conventionThe financial statements are basedon the general principles of historicalcost accounting with the exceptionof investments and specific fixedassets as noted below. Thesefinancial statements have beenprepared in accordance withgenerally accepted accountingpractice in New Zealand (GAAP).Where no financial reportingstandard or statement of standardaccounting practice exists in NewZealand in relation to a particularissue, the accounting policiesadopted have been determinedhaving regard to authoritativesupport. These policies have beenapplied on a consistent basis exceptas disclosed in note 2, changes inaccounting policies.

EstimatesThe preparation of financialstatements in conformity with GAAPrequires the Directors to makeestimates and assumptions thataffect the reported amounts ofassets and liabilities, disclosure ofcontingent assets and liabilities atthe date of the financial statementsand the reported amounts ofrevenues and expenses during thereporting period. Actual results coulddiffer from those estimates.

Basis of consolidationThe consolidated financial statementscomprise the Company and itssubsidiaries, and the Group’s interestin associates, partnerships and jointventures. Inter-company transactionsare eliminated in preparing theconsolidated financial statements.

SubsidiariesSubsidiaries are included in theconsolidated financial statementsusing the purchase method ofconsolidation, except for theacquisition of the assets andliabilities of Fletcher ChallengeLimited – Building Operations, whichwere at book value. The Companyhas revalued its investment insubsidiaries to net asset backing.

AssociatesThe equity method has been usedfor associate entities in which theGroup has a significant but notcontrolling interest.

FLETCHER BUILDING FINANCIAL STATEMENTS

32