Embed Size (px)

Citation preview

VE 02i. Product Markets: Monopolistic Competition and Oligopoly Varsity Economics – Product Markets: Monopolistic Competition and Oligopoly

1 Which of the following is a characteristic of monopolistic competition? A standardized product B a relatively small number of firms C absence of nonprice competition D relatively easy entry

2 A monopolistically competitive industry is like a purely competitive industry in that A each industry produces a standardized product. B nonprice competition is a feature in both industries. C neither industry has significant barriers to entry. D firms in both industries face a horizontal demand curve.

3 Which assumption is part of the model of monopolistic competition? A Firms make identical or homogeneous products. B There is no collusion mutual interdependence among firms. C There are significant barriers to entry into the market. D Firms have no control over their products’ prices.

4 Monopolistic competition is characterized by firms A producing differentiated products. B making economic profits in the long run. C producing at optimal productive efficiency. D producing where price equals marginal cost.

5 In which industry is monopolistic competition most likely to be found? A utilities B agriculture C retail trade D mining

6 One difference between monopolistic competition and pure competition is that A products may be homogeneous in monopolistic competition. B there is some control over price in monopolistic competition. C monopolistic competition has significant barriers to entry. D firms differentiate their products in pure competition.

VE 02i. Product Markets: Monopolistic Competition and Oligopoly 7 Which set of characteristics below best describes the basic features of monopolistic

competition? A easy entry, many firms, and standardized products B barriers to entry, few firms, and differentiated products C easy entry, many firms, and differentiated products D easy entry, few firms, and standardized products

8 The goal of product differentiation and advertising in monopolistic competition is to make A the firm allocatively efficient even if it is not productively efficient. B the firm productively efficient even if it is not allocatively efficient. C price less of a factor and product differences more of a factor in consumer purchases. D price more of a factor and product differences less of a factor in consumer purchases.

9 Which industry would be best characterized as monopolistically competitive? A smart-phone manufacturing B Internet-search sites C web design consulting D business cloud-computing services

10 Under monopolistic competition, entry to the industry is A completely free of barriers. B more difficult than under pure competition but not nearly as difficult as under pure

monopoly. C more difficult than under pure monopoly. D blocked.

11 Demand and marginal revenue curves are downsloping for monopolistically competitive firms because A each firm has to take the market price as given. B product differentiation allows each firm some degree of monopoly power. C there are a few large firms in the industry and they each act as a monopolist. D mutual interdependence among all firms in the industry leads to collusion.

12 The downward-sloping demand curve of a monopolistic competitor A reflects some level of control over its own price. B becomes eventually horizontal in the long run. C indicates collusion among the members of the product group. D ensures that the firm will produce at minimum average cost in the long run.

VE 02i. Product Markets: Monopolistic Competition and Oligopoly 13 The monopolistically competitive seller's demand curve will become more elastic with

A a larger number of competitors. B a greater degree of product differentiation. C more significant barriers to entry. D a smaller number of competitors.

14 The demand curve faced by a monopolistically competitive firm A is more elastic than the monopolist's demand curve. B is less elastic than the monopolist's demand curve. C will shift outward as new firms enter the industry. D is more elastic than the demand curve faced by the purely competitive firm.

15 In monopolistic competition, which of the following would make an individual firm's demand curve less elastic? A the purchase of more efficient machinery B an increase in the price of the firm's product C increased brand loyalty toward the firm's product D an increase in the number of rival firms

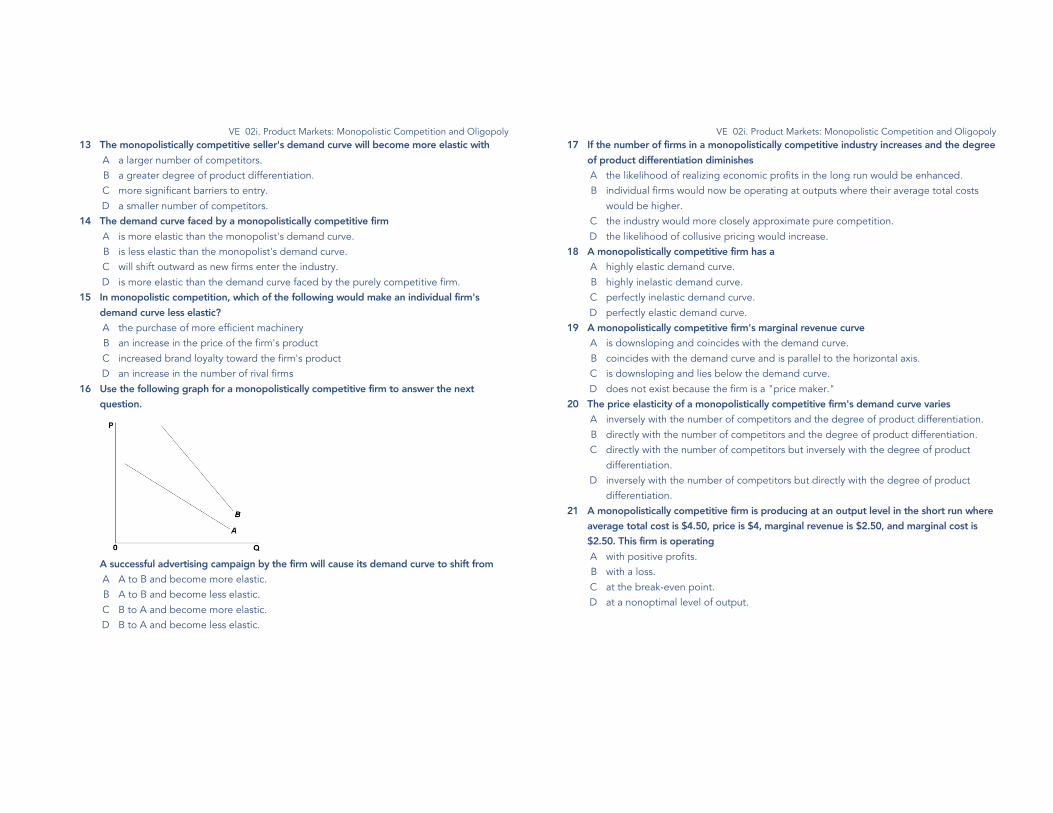

16 Use the following graph for a monopolistically competitive firm to answer the next question.

A successful advertising campaign by the firm will cause its demand curve to shift from A A to B and become more elastic. B A to B and become less elastic. C B to A and become more elastic. D B to A and become less elastic.

VE 02i. Product Markets: Monopolistic Competition and Oligopoly 17 If the number of firms in a monopolistically competitive industry increases and the degree

of product differentiation diminishes A the likelihood of realizing economic profits in the long run would be enhanced. B individual firms would now be operating at outputs where their average total costs

would be higher. C the industry would more closely approximate pure competition. D the likelihood of collusive pricing would increase.

18 A monopolistically competitive firm has a A highly elastic demand curve. B highly inelastic demand curve. C perfectly inelastic demand curve. D perfectly elastic demand curve.

19 A monopolistically competitive firm's marginal revenue curve A is downsloping and coincides with the demand curve. B coincides with the demand curve and is parallel to the horizontal axis. C is downsloping and lies below the demand curve. D does not exist because the firm is a "price maker."

20 The price elasticity of a monopolistically competitive firm's demand curve varies A inversely with the number of competitors and the degree of product differentiation. B directly with the number of competitors and the degree of product differentiation. C directly with the number of competitors but inversely with the degree of product

differentiation. D inversely with the number of competitors but directly with the degree of product

differentiation. 21 A monopolistically competitive firm is producing at an output level in the short run where

average total cost is $4.50, price is $4, marginal revenue is $2.50, and marginal cost is $2.50. This firm is operating A with positive profits. B with a loss. C at the break-even point. D at a nonoptimal level of output.

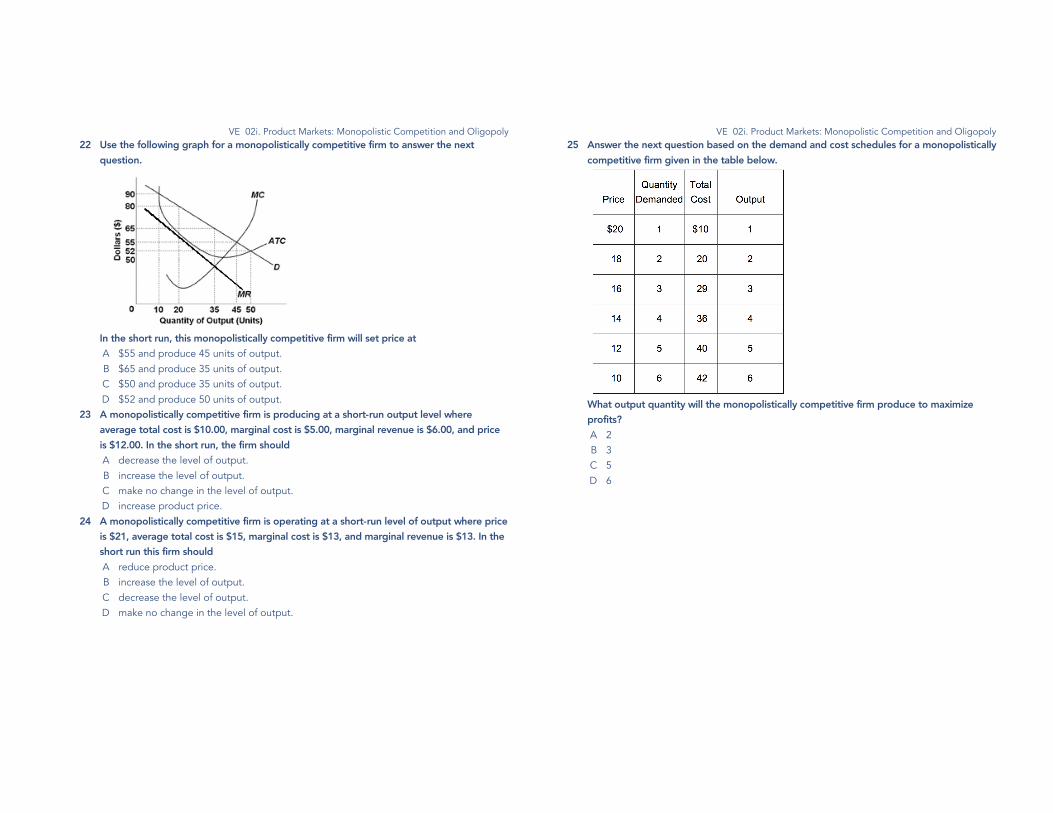

VE 02i. Product Markets: Monopolistic Competition and Oligopoly 22 Use the following graph for a monopolistically competitive firm to answer the next

question.

In the short run, this monopolistically competitive firm will set price at A $55 and produce 45 units of output. B $65 and produce 35 units of output. C $50 and produce 35 units of output. D $52 and produce 50 units of output.

23 A monopolistically competitive firm is producing at a short-run output level where average total cost is $10.00, marginal cost is $5.00, marginal revenue is $6.00, and price is $12.00. In the short run, the firm should A decrease the level of output. B increase the level of output. C make no change in the level of output. D increase product price.

24 A monopolistically competitive firm is operating at a short-run level of output where price is $21, average total cost is $15, marginal cost is $13, and marginal revenue is $13. In the short run this firm should A reduce product price. B increase the level of output. C decrease the level of output. D make no change in the level of output.

VE 02i. Product Markets: Monopolistic Competition and Oligopoly 25 Answer the next question based on the demand and cost schedules for a monopolistically

competitive firm given in the table below.

What output quantity will the monopolistically competitive firm produce to maximize profits? A 2 B 3 C 5 D 6

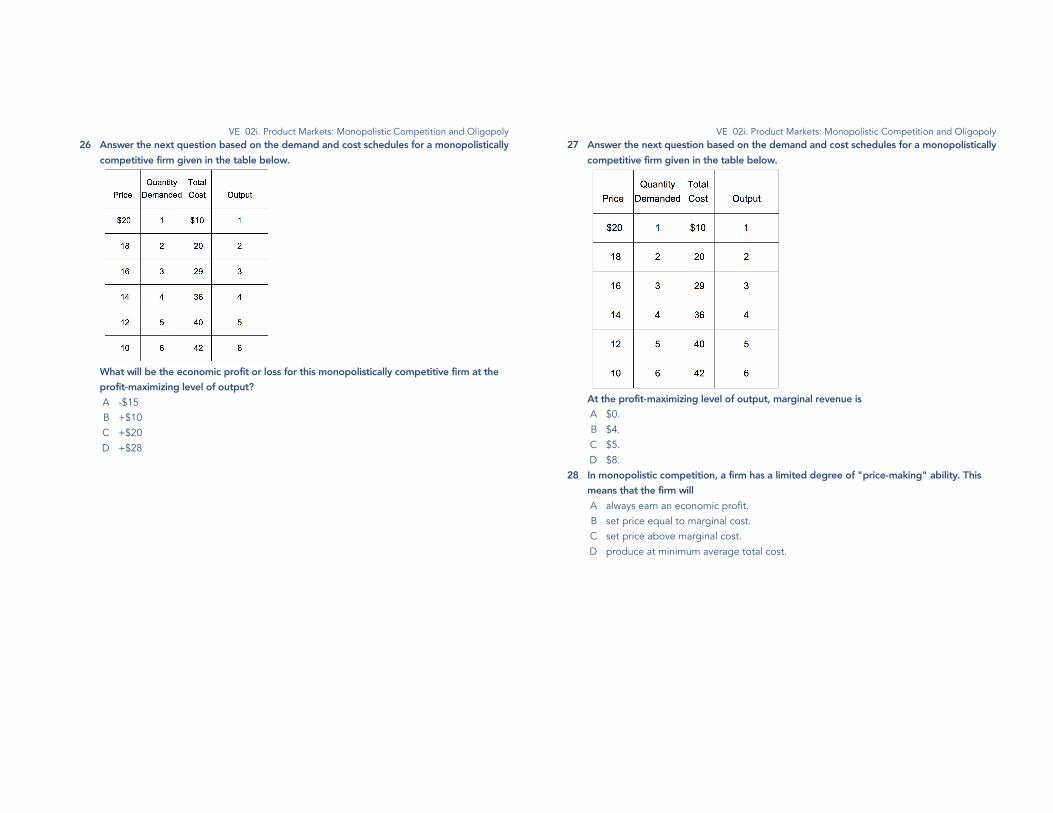

VE 02i. Product Markets: Monopolistic Competition and Oligopoly 26 Answer the next question based on the demand and cost schedules for a monopolistically

competitive firm given in the table below.

What will be the economic profit or loss for this monopolistically competitive firm at the profit-maximizing level of output? A -$15 B +$10 C +$20 D +$28

VE 02i. Product Markets: Monopolistic Competition and Oligopoly 27 Answer the next question based on the demand and cost schedules for a monopolistically

competitive firm given in the table below.

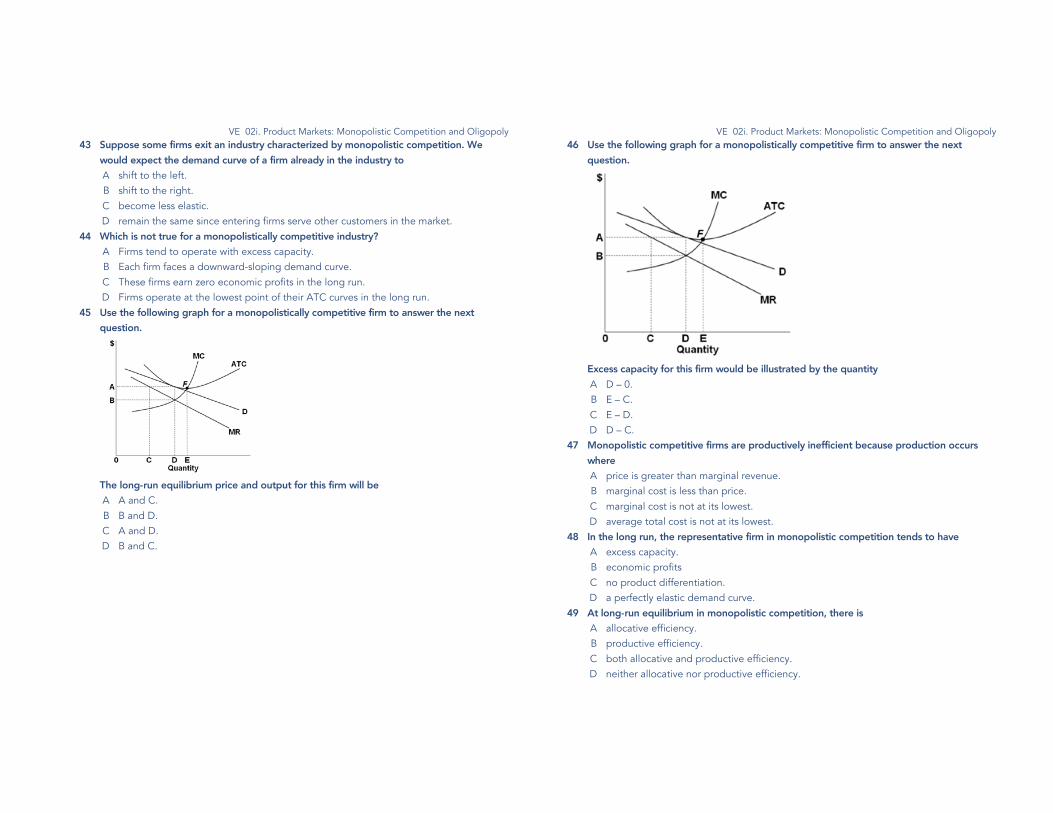

At the profit-maximizing level of output, marginal revenue is A $0. B $4. C $5. D $8.

28 In monopolistic competition, a firm has a limited degree of "price-making" ability. This means that the firm will A always earn an economic profit. B set price equal to marginal cost. C set price above marginal cost. D produce at minimum average total cost.

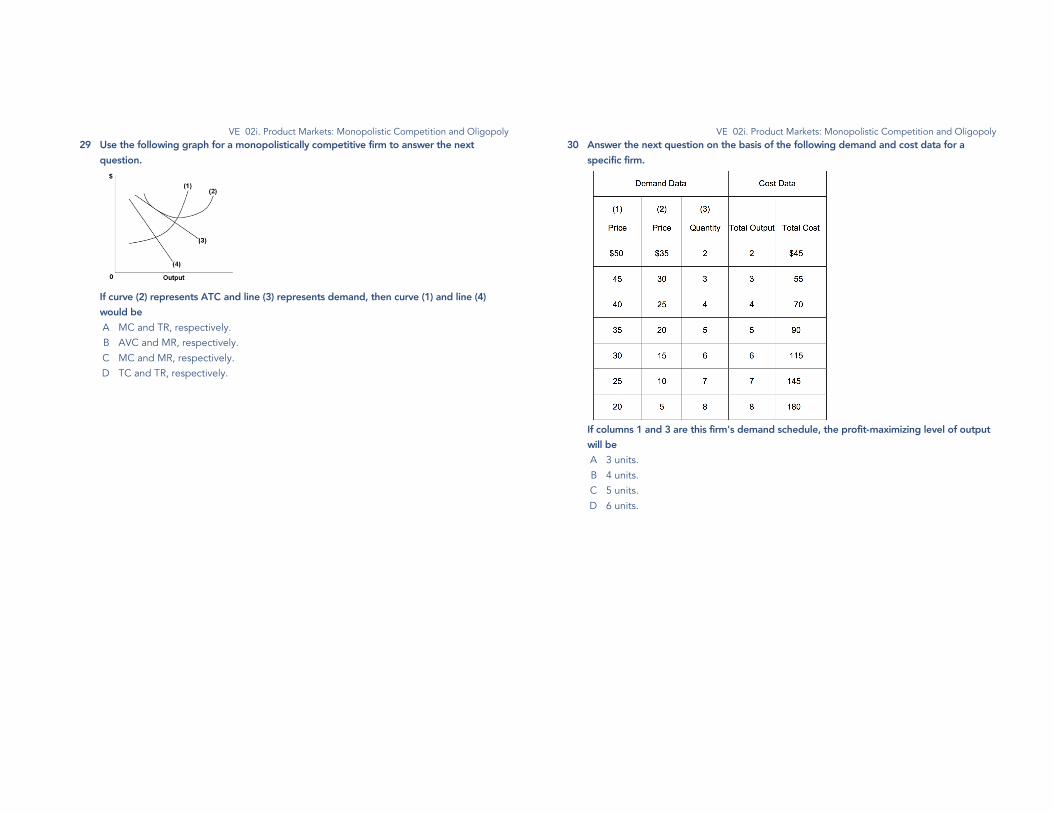

VE 02i. Product Markets: Monopolistic Competition and Oligopoly 29 Use the following graph for a monopolistically competitive firm to answer the next

question.

If curve (2) represents ATC and line (3) represents demand, then curve (1) and line (4) would be A MC and TR, respectively. B AVC and MR, respectively. C MC and MR, respectively. D TC and TR, respectively.

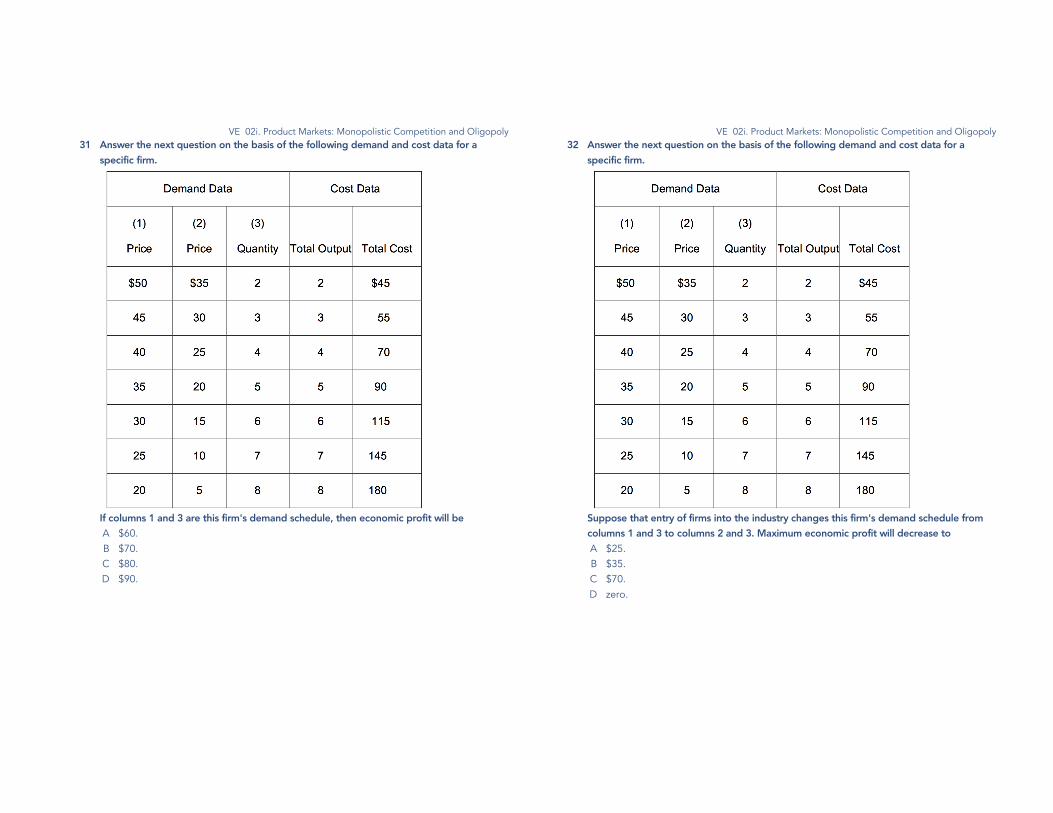

VE 02i. Product Markets: Monopolistic Competition and Oligopoly 30 Answer the next question on the basis of the following demand and cost data for a

specific firm.

If columns 1 and 3 are this firm's demand schedule, the profit-maximizing level of output will be A 3 units. B 4 units. C 5 units. D 6 units.

VE 02i. Product Markets: Monopolistic Competition and Oligopoly 31 Answer the next question on the basis of the following demand and cost data for a

specific firm.

If columns 1 and 3 are this firm's demand schedule, then economic profit will be A $60. B $70. C $80. D $90.

VE 02i. Product Markets: Monopolistic Competition and Oligopoly 32 Answer the next question on the basis of the following demand and cost data for a

specific firm.

Suppose that entry of firms into the industry changes this firm's demand schedule from columns 1 and 3 to columns 2 and 3. Maximum economic profit will decrease to A $25. B $35. C $70. D zero.

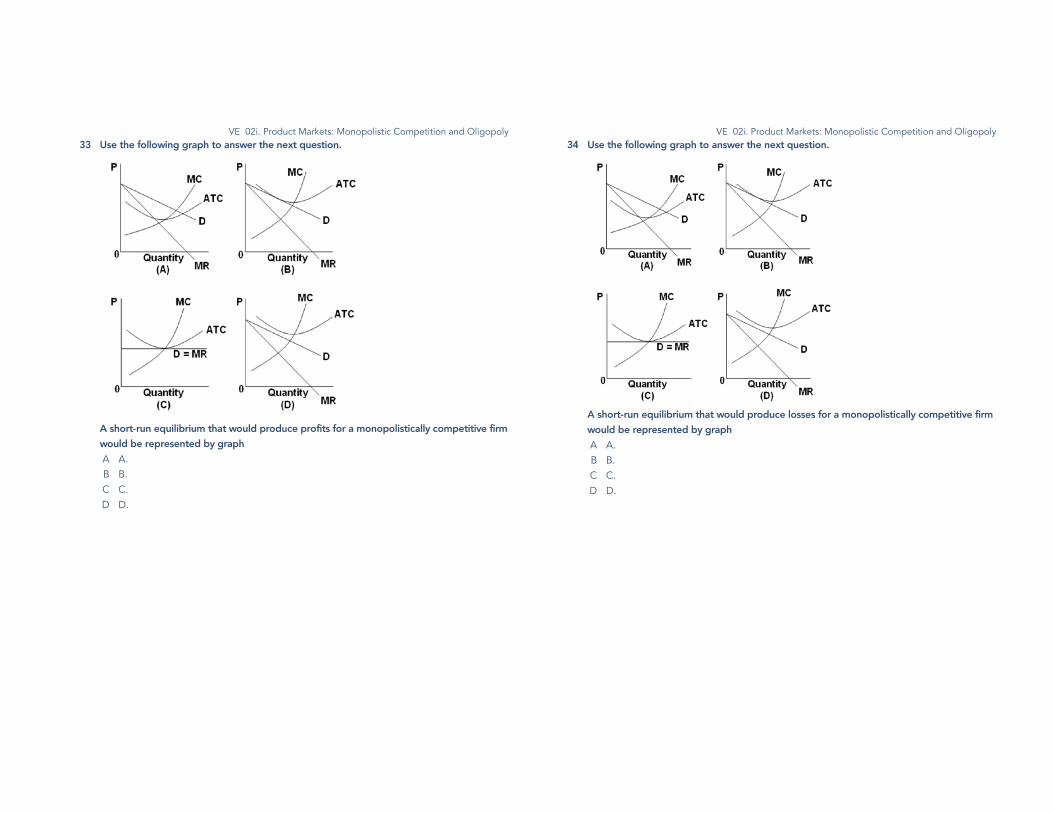

VE 02i. Product Markets: Monopolistic Competition and Oligopoly 33 Use the following graph to answer the next question.

A short-run equilibrium that would produce profits for a monopolistically competitive firm would be represented by graph A A. B B. C C. D D.

VE 02i. Product Markets: Monopolistic Competition and Oligopoly 34 Use the following graph to answer the next question.

A short-run equilibrium that would produce losses for a monopolistically competitive firm would be represented by graph A A. B B. C C. D D.

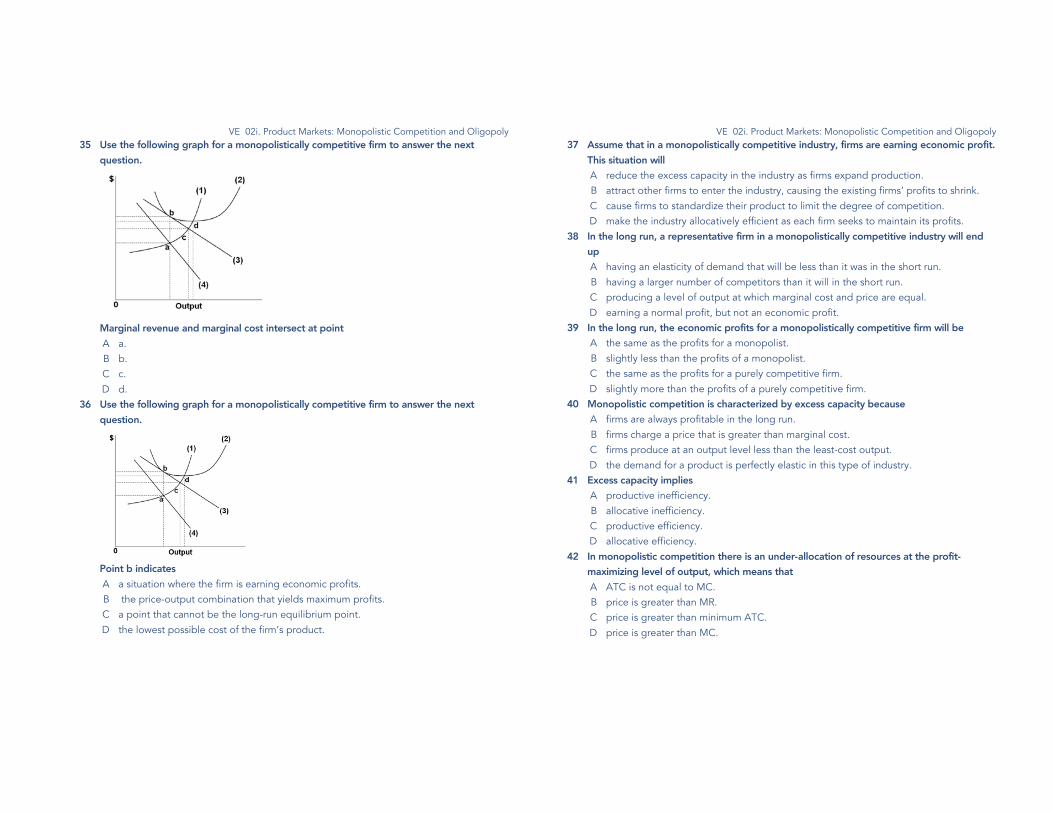

VE 02i. Product Markets: Monopolistic Competition and Oligopoly 35 Use the following graph for a monopolistically competitive firm to answer the next

question.

Marginal revenue and marginal cost intersect at point A a. B b. C c. D d.

36 Use the following graph for a monopolistically competitive firm to answer the next question.

Point b indicates A a situation where the firm is earning economic profits. B the price-output combination that yields maximum profits. C a point that cannot be the long-run equilibrium point. D the lowest possible cost of the firm’s product.

VE 02i. Product Markets: Monopolistic Competition and Oligopoly 37 Assume that in a monopolistically competitive industry, firms are earning economic profit.

This situation will A reduce the excess capacity in the industry as firms expand production. B attract other firms to enter the industry, causing the existing firms’ profits to shrink. C cause firms to standardize their product to limit the degree of competition. D make the industry allocatively efficient as each firm seeks to maintain its profits.

38 In the long run, a representative firm in a monopolistically competitive industry will end up A having an elasticity of demand that will be less than it was in the short run. B having a larger number of competitors than it will in the short run. C producing a level of output at which marginal cost and price are equal. D earning a normal profit, but not an economic profit.

39 In the long run, the economic profits for a monopolistically competitive firm will be A the same as the profits for a monopolist. B slightly less than the profits of a monopolist. C the same as the profits for a purely competitive firm. D slightly more than the profits of a purely competitive firm.

40 Monopolistic competition is characterized by excess capacity because A firms are always profitable in the long run. B firms charge a price that is greater than marginal cost. C firms produce at an output level less than the least-cost output. D the demand for a product is perfectly elastic in this type of industry.

41 Excess capacity implies A productive inefficiency. B allocative inefficiency. C productive efficiency. D allocative efficiency.

42 In monopolistic competition there is an under-allocation of resources at the profit-maximizing level of output, which means that A ATC is not equal to MC. B price is greater than MR. C price is greater than minimum ATC. D price is greater than MC.

VE 02i. Product Markets: Monopolistic Competition and Oligopoly 43 Suppose some firms exit an industry characterized by monopolistic competition. We

would expect the demand curve of a firm already in the industry to A shift to the left. B shift to the right. C become less elastic. D remain the same since entering firms serve other customers in the market.

44 Which is not true for a monopolistically competitive industry? A Firms tend to operate with excess capacity. B Each firm faces a downward-sloping demand curve. C These firms earn zero economic profits in the long run. D Firms operate at the lowest point of their ATC curves in the long run.

45 Use the following graph for a monopolistically competitive firm to answer the next question.

The long-run equilibrium price and output for this firm will be A A and C. B B and D. C A and D. D B and C.

VE 02i. Product Markets: Monopolistic Competition and Oligopoly 46 Use the following graph for a monopolistically competitive firm to answer the next

question.

Excess capacity for this firm would be illustrated by the quantity A D – 0. B E – C. C E – D. D D – C.

47 Monopolistic competitive firms are productively inefficient because production occurs where A price is greater than marginal revenue. B marginal cost is less than price. C marginal cost is not at its lowest. D average total cost is not at its lowest.

48 In the long run, the representative firm in monopolistic competition tends to have A excess capacity. B economic profits C no product differentiation. D a perfectly elastic demand curve.

49 At long-run equilibrium in monopolistic competition, there is A allocative efficiency. B productive efficiency. C both allocative and productive efficiency. D neither allocative nor productive efficiency.

VE 02i. Product Markets: Monopolistic Competition and Oligopoly 50 Which statement concerning monopolistic competition is false?

A In the long run P = AC > MC. B Firms may experience losses in the short run. C Firms differentiate their products, but the products are relatively substitutable. D Firms may experience positive economic profits in the long run.

51 In the long-run equilibrium of a monopolistically competitive industry A P = minimum (ATC). B P > minimum (ATC). C P = MC. D P < MC.

52 In long-run equilibrium, a profit-maximizing firm in a monopolistically competitive industry will produce the quantity of output where A ATC = P, MR = MC = P. B ATC < P, MR = MC = P. C ATC < P, MR + MC < P. D ATC = P, MR = MC < P.

53 If monopolistically competitive firms in an industry are making an economic profit, then new firms will enter the industry and the product demand facing existing firms will A increase. B become less elastic. C not be affected. D decrease.

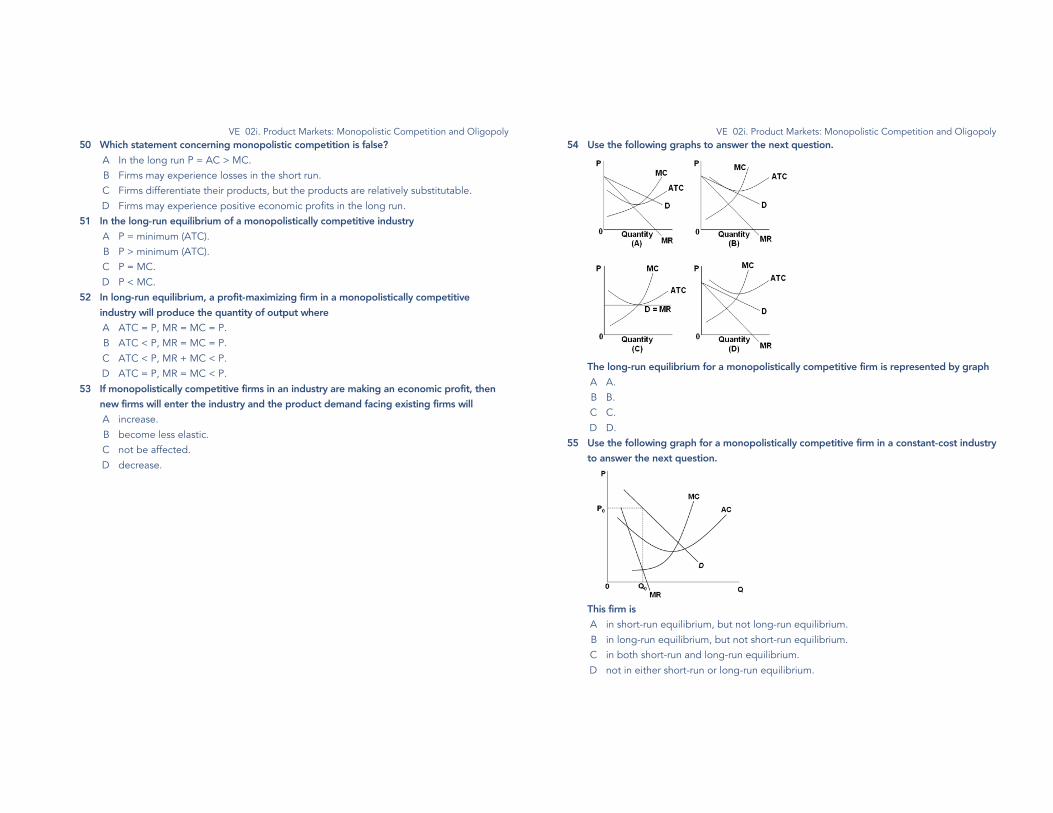

VE 02i. Product Markets: Monopolistic Competition and Oligopoly 54 Use the following graphs to answer the next question.

The long-run equilibrium for a monopolistically competitive firm is represented by graph A A. B B. C C. D D.

55 Use the following graph for a monopolistically competitive firm in a constant-cost industry to answer the next question.

This firm is A in short-run equilibrium, but not long-run equilibrium. B in long-run equilibrium, but not short-run equilibrium. C in both short-run and long-run equilibrium. D not in either short-run or long-run equilibrium.

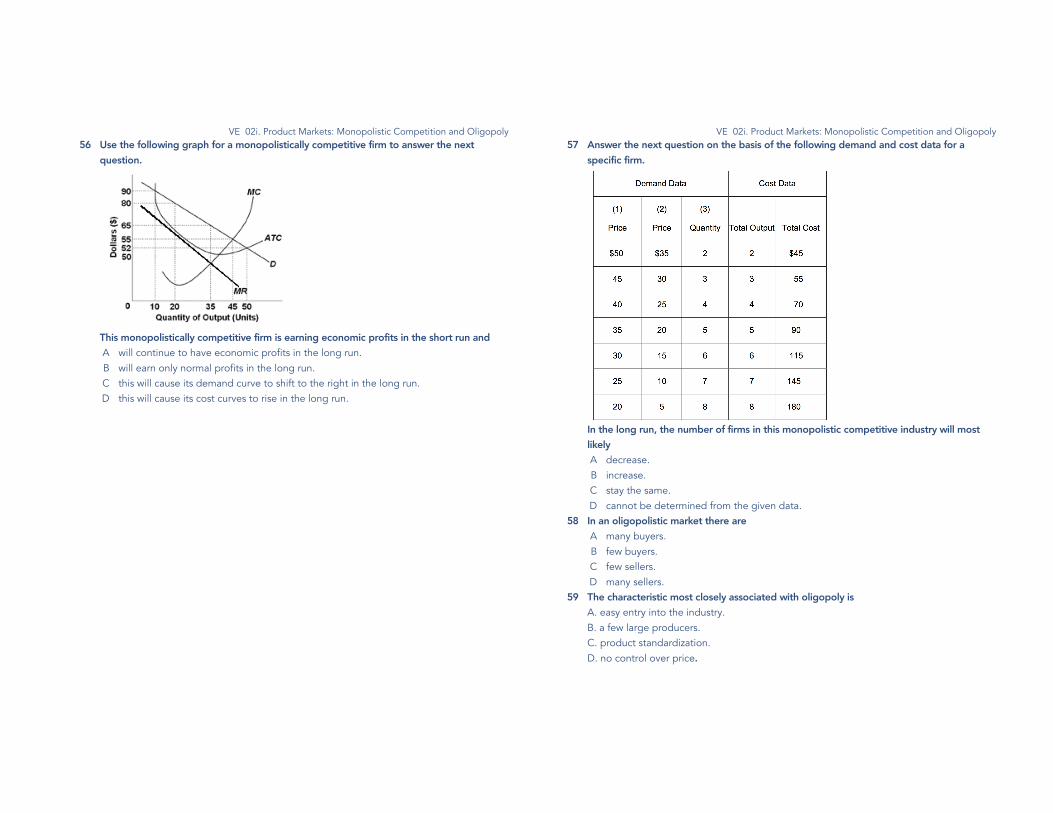

VE 02i. Product Markets: Monopolistic Competition and Oligopoly 56 Use the following graph for a monopolistically competitive firm to answer the next

question.

This monopolistically competitive firm is earning economic profits in the short run and A will continue to have economic profits in the long run. B will earn only normal profits in the long run. C this will cause its demand curve to shift to the right in the long run. D this will cause its cost curves to rise in the long run.

VE 02i. Product Markets: Monopolistic Competition and Oligopoly 57 Answer the next question on the basis of the following demand and cost data for a

specific firm.

In the long run, the number of firms in this monopolistic competitive industry will most likely A decrease. B increase. C stay the same. D cannot be determined from the given data.

58 In an oligopolistic market there are A many buyers. B few buyers. C few sellers. D many sellers.

59 The characteristic most closely associated with oligopoly is A. easy entry into the industry. B. a few large producers. C. product standardization. D. no control over price.

VE 02i. Product Markets: Monopolistic Competition and Oligopoly 60 The consumer wifi-service providers’ market is best described as a

A. monopolistic competition. B. monopoly. C. differentiated oligopoly. D. homogeneous oligopoly.

61 A unique feature of an oligopolistic industry is A low barriers to entry. B standardized products. C diminishing marginal returns. D mutual interdependence.

62 Mergers of firms in an industry tend to A transform monopolistic competition into pure competition. B transform monopolistic competition into oligopoly. C reduce the Herfindahl index for the industry. D break up an oligopoly.

63 A major distinction between a monopolistically competitive firm and an oligopolistic firm is that A one is a price taker and the other is a price maker. B a recognized interdependence exists between firms in one industry but not in the

other. C one always produces differentiated products and the other always produces a

homogeneous product. D one necessarily faces a downward-sloping demand curve and the other a horizontal

demand curve. 64 In which set of market models are there the most significant barriers to entry?

A monopolistic competition and pure competition B monopolistic competition and pure monopoly C oligopoly and monopolistic competition D oligopoly and pure monopoly

65 Mutual interdependence means that each firm in an oligopoly A faces a perfectly inelastic demand for its product. B considers the reactions of its rivals when it determines its pricing policy. C depends on the other firms for its inputs. D depends on the other firms for its markets.

VE 02i. Product Markets: Monopolistic Competition and Oligopoly 66 Mutual interdependence means that a firm’s

A behavior is affected by other firms’ actions. B profits are affected by other firms’ entry or exit. C costs are affected by other firms’ costs. D revenues are affected by other firms’ demand for its product.

67 In which market model is there mutual interdependence? A monopolistic competition B pure competition C pure monopoly D oligopoly

68 A firm in an oligopoly is similar to a monopoly in that both firms A do not face competition from others. B could have significant market power and control over price. C face very inelastic demand for their products. D do not need to advertise.

69 Which cannot be a characteristic of an oligopolistic industry? A differentiated products B a large number of consumers C significant barriers to entry D a perfectly elastic firm demand curve

70 Which statement about oligopoly is false? A Oligopolistic firms recognize their interdependence. B Prices in oligopoly are predicted to fluctuate widely and frequently. C A few firms play an important role in the sale of a product. D One firm's behavior is a function of what its rivals do.

71 Which of the following has not contributed to the development of oligopolies in the U.S. economy? A mergers B patents C economies of scale D interindustry competition

VE 02i. Product Markets: Monopolistic Competition and Oligopoly 72 Interindustry competition refers to the fact that

A Oligopolistic producers establish a common price for their products. B Products are identical in a purely competitive industry. C Firms that sell a product at one stage of production buy materials and parts from

other firms at prior stages of production. D In some markets the producers of a certain commodity might face competition from

products of other industries 73 When firms in an industry reach an agreement to fix prices, divide up market share, or

otherwise restrict competition, they are practicing the strategy of A interindustry competition. B limit pricing. C price leadership. D collusion.

74 Game theory, which is used in studying oligopoly behavior, originated from the study of games such as the following, except A poker. B solitaire. C chess. D bridge.

75 Collusion refers to a situation where rival firms decide to A compete aggressively against each other. B cheat on each other. C agree with each other to set prices and output. D combine their operations and merge with each other.

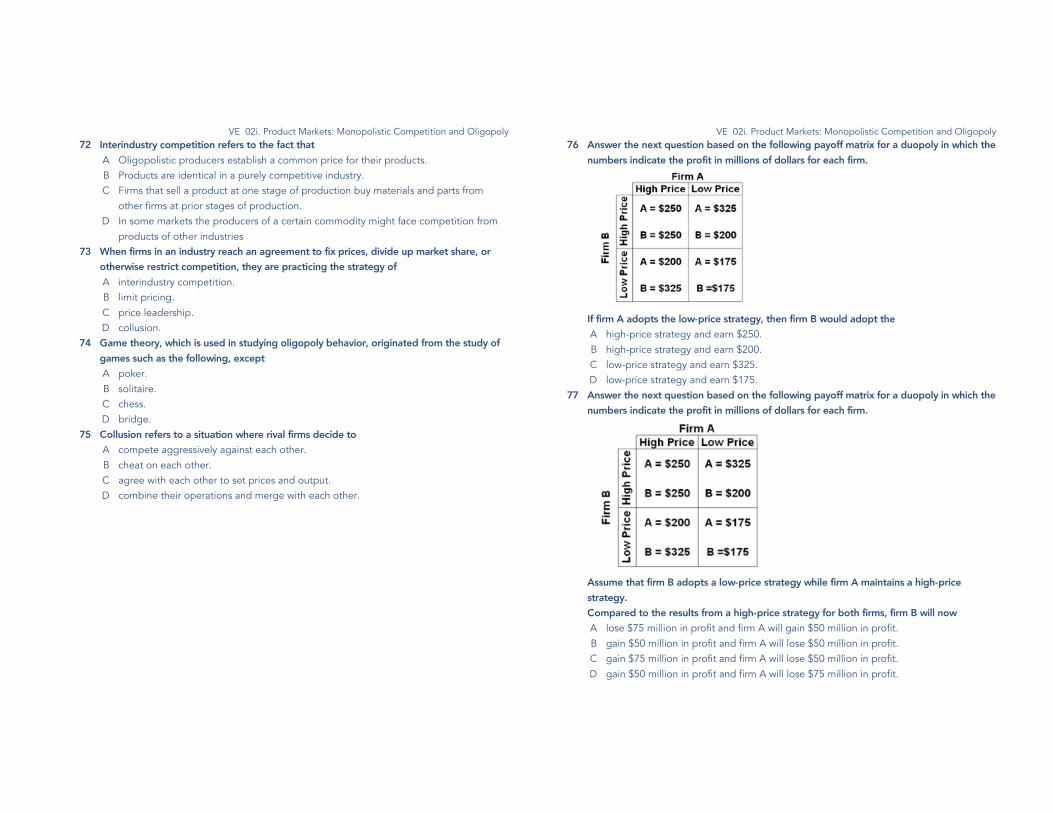

VE 02i. Product Markets: Monopolistic Competition and Oligopoly 76 Answer the next question based on the following payoff matrix for a duopoly in which the

numbers indicate the profit in millions of dollars for each firm.

If firm A adopts the low-price strategy, then firm B would adopt the A high-price strategy and earn $250. B high-price strategy and earn $200. C low-price strategy and earn $325. D low-price strategy and earn $175.

77 Answer the next question based on the following payoff matrix for a duopoly in which the numbers indicate the profit in millions of dollars for each firm.

Assume that firm B adopts a low-price strategy while firm A maintains a high-price strategy. Compared to the results from a high-price strategy for both firms, firm B will now A lose $75 million in profit and firm A will gain $50 million in profit. B gain $50 million in profit and firm A will lose $50 million in profit. C gain $75 million in profit and firm A will lose $50 million in profit. D gain $50 million in profit and firm A will lose $75 million in profit.

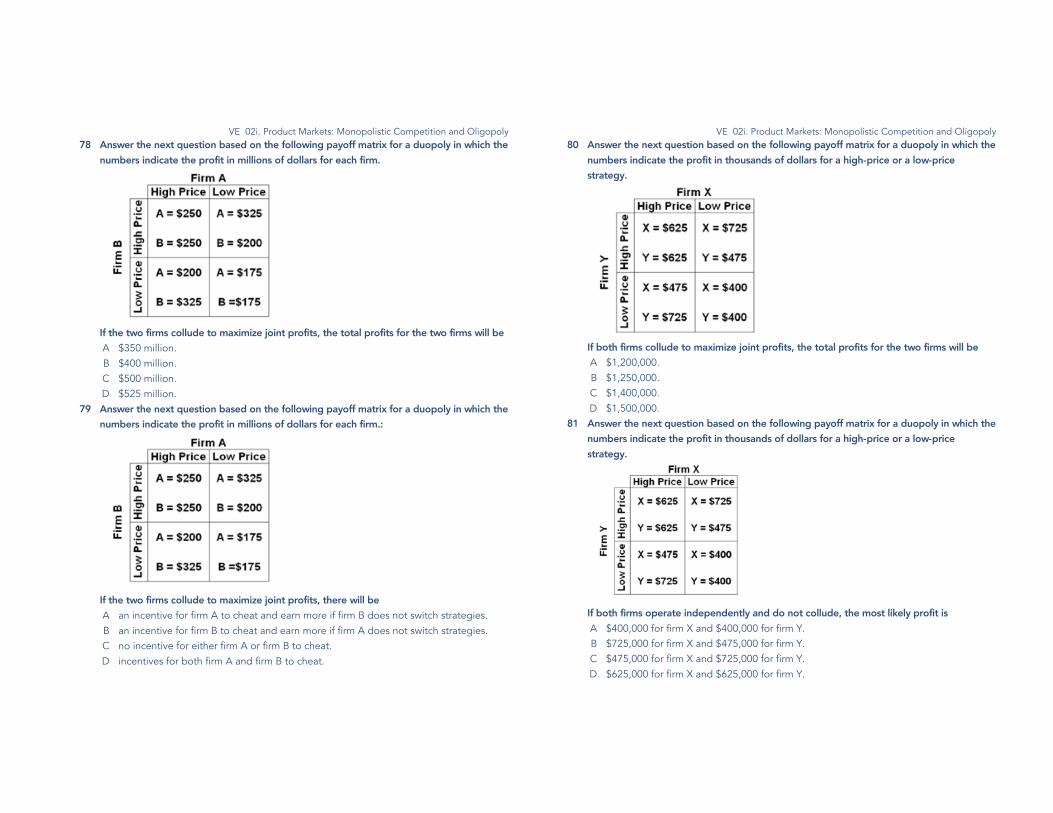

VE 02i. Product Markets: Monopolistic Competition and Oligopoly 78 Answer the next question based on the following payoff matrix for a duopoly in which the

numbers indicate the profit in millions of dollars for each firm.

If the two firms collude to maximize joint profits, the total profits for the two firms will be A $350 million. B $400 million. C $500 million. D $525 million.

79 Answer the next question based on the following payoff matrix for a duopoly in which the numbers indicate the profit in millions of dollars for each firm.:

If the two firms collude to maximize joint profits, there will be A an incentive for firm A to cheat and earn more if firm B does not switch strategies. B an incentive for firm B to cheat and earn more if firm A does not switch strategies. C no incentive for either firm A or firm B to cheat. D incentives for both firm A and firm B to cheat.

VE 02i. Product Markets: Monopolistic Competition and Oligopoly 80 Answer the next question based on the following payoff matrix for a duopoly in which the

numbers indicate the profit in thousands of dollars for a high-price or a low-price strategy.

If both firms collude to maximize joint profits, the total profits for the two firms will be A $1,200,000. B $1,250,000. C $1,400,000. D $1,500,000.

81 Answer the next question based on the following payoff matrix for a duopoly in which the numbers indicate the profit in thousands of dollars for a high-price or a low-price strategy.

If both firms operate independently and do not collude, the most likely profit is A $400,000 for firm X and $400,000 for firm Y. B $725,000 for firm X and $475,000 for firm Y. C $475,000 for firm X and $725,000 for firm Y. D $625,000 for firm X and $625,000 for firm Y.

VE 02i. Product Markets: Monopolistic Competition and Oligopoly 82 Under oligopoly, if one firm in an industry significantly increases advertising expenditures

in order to capture a greater market share, it is most likely that other firms in that industry will A pursue a strategy to reduce advertising expenditures to maintain profits. B decide to increase advertising expenditures even if it means a reduction in profits. C make no changes in advertising expenditures because advertising is effective in the

short run, but not the long run. D increase the price of the product to improve profits and then increase advertising

expenditures. 83 Collusive control over price may permit oligopolists to

A use new technology, achieve economies of scale, and get government subsidies. B achieve economies of scale, reduce costs, and prevent price cheating. C increase product demand, increase product supply, and lower cost. D reduce uncertainty, increase profits, and possibly limit entry of new firms.

84 If oligopolistic firms facing similar cost and demand conditions successfully collude, price and output results in this industry will be most accurately predicted by which of the following models? A the kinked demand curve model of oligopoly B the price-leadership model of oligopoly C the pure monopoly model D the monopolistic competition model

85 A cartel is A a form of covert collusion. B legal in the United States. C always successful in raising profits. D a formal agreement among firms to collude.

86 A major reason that firms form a cartel is to A reduce the elasticity of demand for the product. B enlarge the market share for each producer. C minimize the costs of production. D maximize joint profits.

VE 02i. Product Markets: Monopolistic Competition and Oligopoly 87 Collusion among oligopolistic firms

A is common in world markets, but does not happen in the U.S. B becomes more difficult if there were fewer firms in the group. C becomes easier during a recession when sales are falling. D becomes more difficult if the firms all have different cost and demand curves.

88 An increase in which of the following factors does not increase the incentive to cheat within a cartel? A the number of firms in the cartel B economic performance and industry sales C the number of potential entrants into the industry D the cost-differences among firms

89 In an oligopoly, producers' agreements to restrict output tend to be unstable because each firm has an incentive to A produce more than its output quota. B lower both its price and its output. C raise its price above the cooperative price. D establish competitive price and output levels.

90 Informal collusion to restrict output and increase prices is sometimes referred to as a A merger. B cartel. C tacit understanding. D kinked-demand oligopoly.

91 Which constitutes an obstacle to collusion among oligopolists? A a standardized product B a large number of firms C prosperous economic conditions D trademarks and copyrights

92 The strategy of establishing a price that prevents the entry of new firms is called A cartel pricing. B limit pricing. C price leadership. D profit maximizing price.

VE 02i. Product Markets: Monopolistic Competition and Oligopoly 93 In an oligopolistic market there is likely to be

A little consideration of the actions of rival firms. B price-taking behavior on the part of firms. C homogeneous but not differentiated products. D neither allocative nor productive efficiency.

94 When near-monopolies like Google in Internet search and Amazon in online shopping start infringing on each other’s turf, what kind of competition results? A pure competition B monopolistic competition C oligopolistic competition D legislated competition