Embed Size (px)

Citation preview

TATA CONSULTANCY

SERVICES

ALEX PRAVEEN KUMAR (13AD02)

BOOPATHI.R (13AD07)

SIVAKUMAR.G (13AD35)

SUBBURAMAN.R (13AD37)

12 February 2015 1

Company Profile

• An Indian multinational information technology (IT) services,

business process and consulting company headquartered

in Mumbai, Maharashtra.

• Founded in 1968 by a division of Tata Sons Limited.

• CEO & Managing Director- Mr Natarajan Chandrasekaran

• Operates in 46 countries and has 199 branches across the

world.

12 February 2015 2

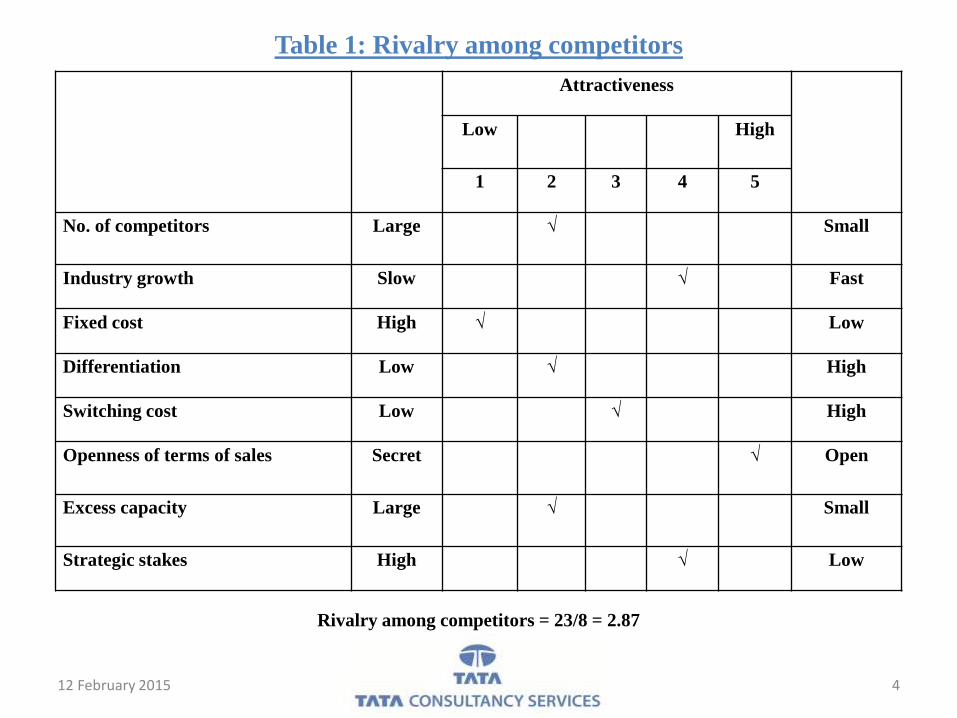

Porter’s Model:

12 February 2015 3

Attractiveness

Low High

1 2 3 4 5

No. of competitors Large √ Small

Industry growth Slow √ Fast

Fixed cost High √ Low

Differentiation Low √ High

Switching cost Low √ High

Openness of terms of sales Secret √ Open

Excess capacity Large √ Small

Strategic stakes High √ Low

Table 1: Rivalry among competitors

Rivalry among competitors = 23/8 = 2.87

12 February 2015 4

12 February 2015 5

Attractiveness

Low High

1 2 3 4 5

Asset specialization High √ Small

Cost of exit High √ Small

Government restrictions High √ Small

Table 2: Barriers to exit

Barriers to exit = 6/3 = 2

12 February 2015 6

Attractiveness

Low High

1 2 3 4 5

Economies of scale Small √ Large

Product differentiation Low √ High

Brand identity Low √ High

Switching cost Low √ High

Access to channels of

distribution

Easy √ Limited

Capital requirement Small √ Large

Access to technology Easy √ Restricted

Access to raw material Easy √ Restricted

Government protection None √ Substantial

Table 3: Barriers to entry

Barriers to entry = 23/9=2.56

12 February 2015 7

Attractiveness

Low High

1 2 3 4 5

Availability of close

substitutes

High √ Low

Switching cost Low √ High

Substitute's price-value Better √ Worse

Profitability of the producers

of substitutes

High √ Low

Table 4: Threat from substitutes

Threat from substitutes = 14/4 = 3.5

12 February 2015 8

Attractiveness

Low High

1 2 3 4 5

Number of buyers Small √ Large

Availability of substitutes Many √ Few

Switching cost Low √ High

Buyers threat of backward

integration

High √ Low

Industry's threat of forward

integration

Low √ High

Contribution to quality Low √ High

Contribution to cost High √ Low

Buyer's profitability Low √ High

Table 5: Bargaining power of buyers

Bargaining power of buyers = 30/8 = 3.75

12 February 2015 9

Attractiveness

Low High

1 2 3 4 5

Number of suppliers Small √ Large

Availability of substitutes Few √ Many

Switching cost High √ Low

Supplier's threat of forward

integration

High √ Low

Industry's threat of backward

integration

Low √ High

Contribution to quality High √ Low

Contribution to cost High √ Low

Industry's importance to

supplier

Low √ High

Table 6: Bargaining power of suppliers

Bargaining power of suppliers = 26/8 = 3.25

12 February 2015 10

Attractiveness

Low High

1 2 3 4 5

Industry protection Low √ High

Industry regulation High √ Low

Customs and tariff

restrictions abroad

High √ Low

Table 7: Government actions

Government actions = 12/3 = 3

12 February 2015 11

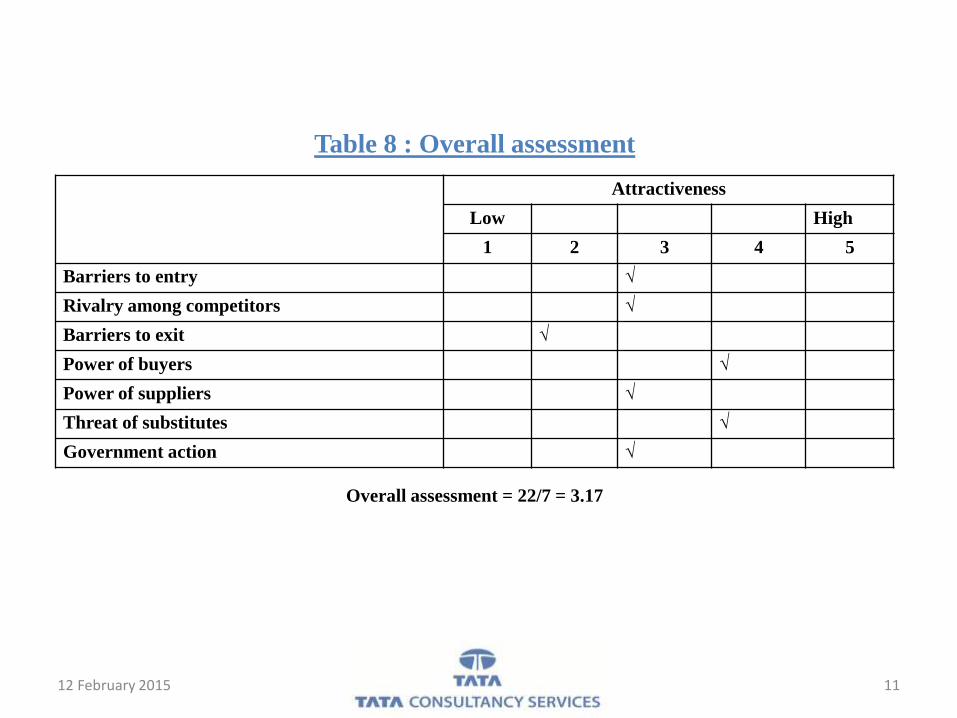

Attractiveness

Low High

1 2 3 4 5

Barriers to entry √

Rivalry among competitors √

Barriers to exit √

Power of buyers √

Power of suppliers √

Threat of substitutes √

Government action √

Table 8 : Overall assessment

Overall assessment = 22/7 = 3.17

CPM MatrixTCS INFOSYS WIPRO

Critical

Success

Factors

Weight Rating Score Rating Score Rating Score

Advertising 0.15 3 0.45 2 0.30 4 0.60

Market share 0.15 4 0.60 3 0.45 2 0.30

Product

quality

0.15 4 0.60 3 0.45 2 0.30

Price

competitivene

ss

0.10 3 0.30 4 0.40 2 0.20

Customer

loyalty

0.10 3 0.30 4 0.40 2 0.20

Global

expansion

0.15 4 0.60 3 0.45 2 0.30

Financial

position

0.20 4 0.80 3 0.60 2 0.40

Total 1.00 25 3.65 22 3.05 16 2.30

12 February 2015 12

BCG Matrix

STARS

BPO

Infrastructure services

QUESTION MARKS

KPO

Engineering and industrial services

Consulting

CASH COWS

Application development

Maintenance of software products

DOGS

None

12 February 2015 13

Percentage of total revenues in FY 2012-

13 by each service line

• Application development and maintenance (42.80%)

• Asset leverage solutions (2.70%)

• Assurance services (7.70%)

• Business process outsourcing (12.50%)

• Consulting (3.00%)

• Engineering and Industrial services (4.60%)

• Enterprise solutions (15.20%) and

• IT infrastructure services (11.50%)

12 February 2015 14

SWOT Matrix

12 February 2015 15

STRENGTHS

Extensive global reach

Strong financial performance

Employee management skills

Innovation labs

WEAKNESS

Significant exposure to financial services

market

Lags multinational high end consulting

offerings

Not strong in product segment

OPPORTUNITIES

Focus on SMB segment

Growth in worldwide IT services

Focus on high end business and IT

consulting

Expanding operations in countries like

China

SO Strategy

Market expansion in developing

countries(S1 & S2,O2)

Developing new products(S4,O3)

WO Strategy

Exposure to financial services

market(W1,O2)

Improving product SMB segment(W3,O1)

THREATS

Increasing employee costs

Intense competition from foreign firms

like Accenture, IBM, etc.

Economic uncertainty and currency

fluctuation

Increased competition from low-wage

countries like China, Indonesia etc.

ST Strategy

Tackle the market by innovative labs(S4,T2

& T4)

Acquisition of new companies related to

their business(S2,T2)

WT Strategy

Focus on high end consultancy

offerings(W2,T2)

Acquisition of small companies in

financial services marker(W1,T3)

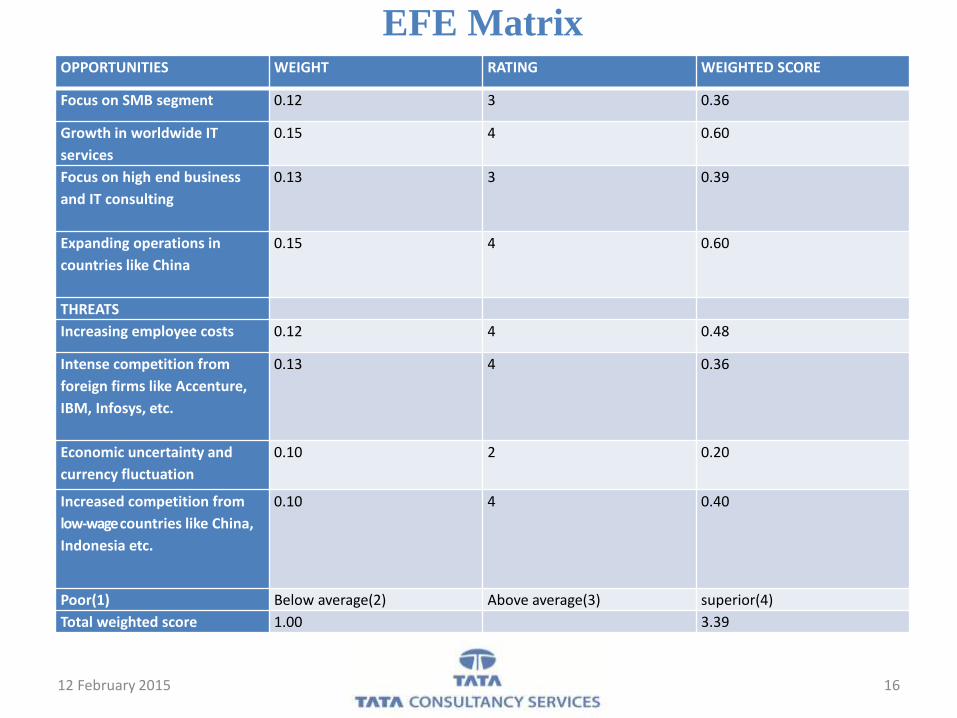

EFE Matrix

12 February 2015 16

OPPORTUNITIES WEIGHT RATING WEIGHTED SCORE

Focus on SMB segment 0.12 3 0.36

Growth in worldwide IT

services

0.15 4 0.60

Focus on high end business

and IT consulting

0.13 3 0.39

Expanding operations in

countries like China

0.15 4 0.60

THREATS

Increasing employee costs 0.12 4 0.48

Intense competition from

foreign firms like Accenture,

IBM, Infosys, etc.

0.13 4 0.36

Economic uncertainty and

currency fluctuation

0.10 2 0.20

Increased competition from

low-wage countries like China,

Indonesia etc.

0.10 4 0.40

Poor(1) Below average(2) Above average(3) superior(4)

Total weighted score 1.00 3.39

IFE Matrix

12 February 2015 17

INTERNAL STRENGTHS WEIGHT RATING WEIGHTED

SCORE

Extensive global reach 0.20 4 0.80

Strong financial performance 0.15 4 0.60

Employee management skills 0.15 3 0.45

Innovation labs 0.13 3 0.39

INTERNAL WEAKNESS

Significant exposure to financial services market 0.12 2 0.24

Lags multinational rivals in high end consulting offerings 0.15 2 0.30

Not strong in product segment 0.10 1 0.10

Major weakness(1) Minor

weakness(2)

Minor

strengths(3)

Major

strengths(4)

Total weighted score 1.00 2.88

IE Matrix

Strong

3.0 to 4.0

Average

2.0 to 2.99

Weak

1.0 to 1.99

EFE Total

Weighted

Scores

High 3.0 to 4.0

GROW AND BUILD

Medium

2.0 to 2.99

Low

1.0 to 1.99

12 February 2015 18

IFE Total

Weighted

Scores

EFE Total

Weighted

Scores

SPACE Matrix

12 February 2015 19

INTERNAL STRATEGIC POSITION EXTERNAL STRATEGIC POSITION

Financial Strength (FS): 1 to 6

ROI - 4

Liquidity - 4

Working Capital - 5

Cash flow - 5

Industry Strength (IS): 1 to 6

Growth Potential - 4

Profit Potential - 4

Financial Stability - 5

Technological Know-how - 5

Resource Utilization - 4

Competitive Advantage (CA): -1 to -6

Market Share - -1

Product quality - -2

Product life cycle - -3

Customer loyalty - -2

Know-how - -1

Environmental Stability (ES): -1 to -6

Technological Changes - -2

Inflation - -4

Demand variability - -3

Barriers to entry - -2

Competitive Pressure - -1

SPACE Matrix- Graph

12 February 2015 20

GRAND Strategy Matrix

Rapid market growth

Weak competitive position

Slow market growth

Strong competitive position

1. Market penetration2. Product development3. Forward integration4. Backward integration5. Horizontal integration6. Related diversification7. Market development

12 February 2015 21

QSPM Matrix

12 February 2015 22

MARKET PENETRATION PRODUCT DEVELOPMENT

KEY FACTORS WEIGHT ATTRACTIVE SCORE TOTAL ATTRACTIVE SCORE TOTAL

STRENGTHS

Extensive global reach 0.20 4 0.80 4 0.80

Strong financial performance 0.15 3 0.45 3 0.45

Employee management skills 0.15 3 0.45 2 0.30

Innovation labs 0.13 2 0.26 4 0.52

WEAKNESS

Significant exposure to

financial services market

0.12 3 0.36 3 0.36

Lags multinational rivals in

high end consulting offerings

0.15 3 0.45 4 0.60

Not strong in product

segment

0.10 2 0.20 3 0.30

Total Weights 2.97 3.33

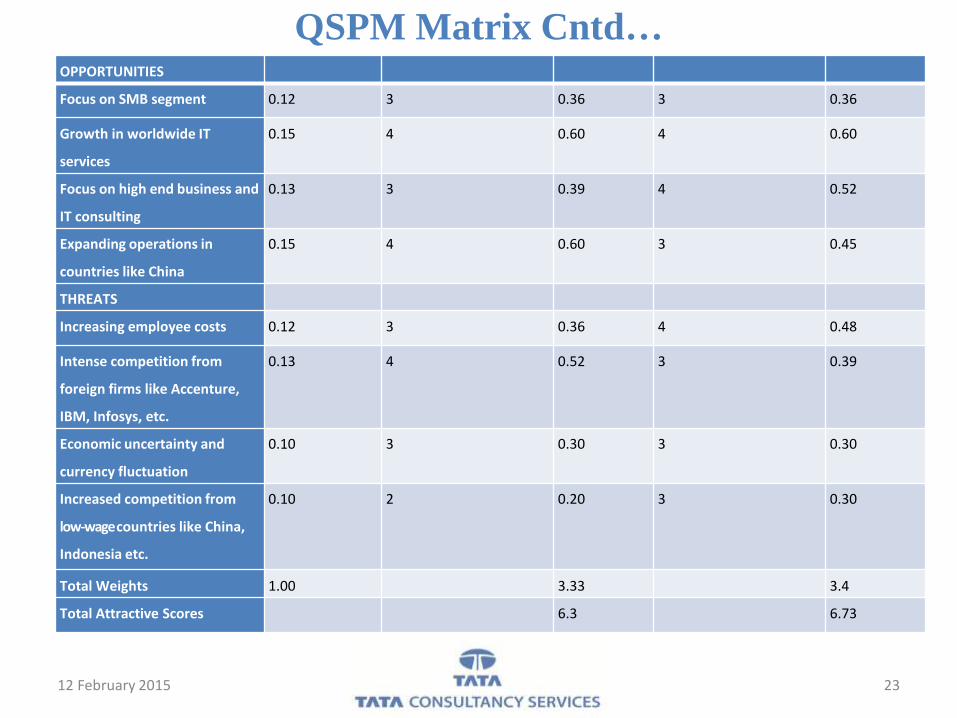

QSPM Matrix Cntd…

12 February 2015 23

OPPORTUNITIES

Focus on SMB segment 0.12 3 0.36 3 0.36

Growth in worldwide IT

services

0.15 4 0.60 4 0.60

Focus on high end business and

IT consulting

0.13 3 0.39 4 0.52

Expanding operations in

countries like China

0.15 4 0.60 3 0.45

THREATS

Increasing employee costs 0.12 3 0.36 4 0.48

Intense competition from

foreign firms like Accenture,

IBM, Infosys, etc.

0.13 4 0.52 3 0.39

Economic uncertainty and

currency fluctuation

0.10 3 0.30 3 0.30

Increased competition from

low-wage countries like China,

Indonesia etc.

0.10 2 0.20 3 0.30

Total Weights 1.00 3.33 3.4

Total Attractive Scores 6.3 6.73

THANK YOU

12 February 2015 24