Embed Size (px)

Citation preview

20th November 2015

Dear Client,

B U D G E T P R O P O S A L S - 2016

The maiden budget of the United National Party led National Government was presented today by Hon. Ravi Karunanayake, Minister of Finance. This was geared towards increasing the Government tax revenue without causing hardship to majority of the tax payers and ensuring sustainable economic growth of the country. The Micro and SME sector, Agriculture sector and investment promotion are primary areas focused in the 2016 proposals.

The salient features of the tax proposals have been summarized in this memorandum as a guide. These may be subject to changes at the time of legislation. Therefore, any conclusion or decision should be arrived at only after due consideration and consultation.

Key highlights include:

a) Streamlining of Corporate tax at 15% and 30%b) Flat rate for individual taxation 15% subject to increased tax free allowance of Rs. 2.4 Mnc) Increase of VAT to 12.5% for service providersd) NBT rate doubled to 4%e) ESC for profit making companies

For additional information and guidance on the proposed changes, the Tax and Business Advisory Services of SJMS Associates will be pleased to assist you.

This information could be viewed on our website at www.sjmsassociates.lk

Yours faithfully,

SJMS ASSOCIATESChartered Accountants

3

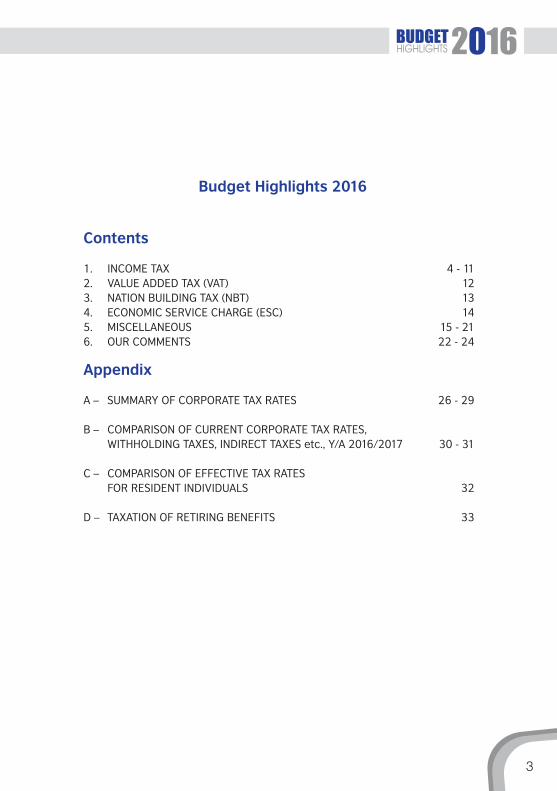

Budget Highlights 2016

Contents

1. INCOME TAX 4 - 112. VALUE ADDED TAX (VAT) 123. NATION BUILDING TAX (NBT) 134. ECONOMIC SERVICE CHARGE (ESC) 145. MISCELLANEOUS 15 - 216. OUR COMMENTS 22 - 24

Appendix

A – SUMMARY OF CORPORATE TAX RATES 26 - 29

B – COMPARISON OF CURRENT CORPORATE TAX RATES, WITHHOLDING TAXES, INDIRECT TAXES etc., Y/A 2016/2017 30 - 31

C – COMPARISON OF EFFECTIVE TAX RATES FOR RESIDENT INDIVIDUALS 32

D – TAXATION OF RETIRING BENEFITS 33

4

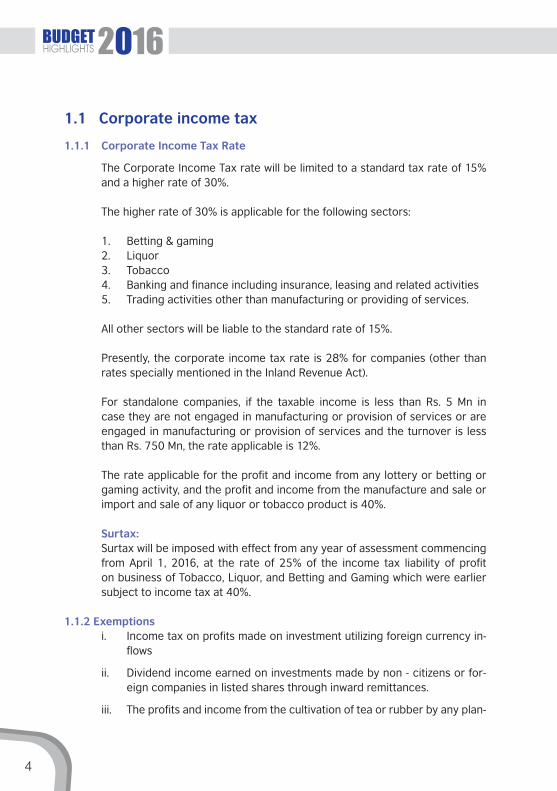

1.1 Corporate income tax

1.1.1 Corporate Income Tax Rate

The Corporate Income Tax rate will be limited to a standard tax rate of 15% and a higher rate of 30%.

The higher rate of 30% is applicable for the following sectors:

1. Betting & gaming2. Liquor3. Tobacco4. Banking and finance including insurance, leasing and related activities5. Trading activities other than manufacturing or providing of services.

All other sectors will be liable to the standard rate of 15%.

Presently, the corporate income tax rate is 28% for companies (other than rates specially mentioned in the Inland Revenue Act).

For standalone companies, if the taxable income is less than Rs. 5 Mn in case they are not engaged in manufacturing or provision of services or are engaged in manufacturing or provision of services and the turnover is less than Rs. 750 Mn, the rate applicable is 12%.

The rate applicable for the profit and income from any lottery or betting or gaming activity, and the profit and income from the manufacture and sale or import and sale of any liquor or tobacco product is 40%.

Surtax: Surtax will be imposed with effect from any year of assessment commencing

from April 1, 2016, at the rate of 25% of the income tax liability of profit on business of Tobacco, Liquor, and Betting and Gaming which were earlier subject to income tax at 40%.

1.1.2 Exemptionsi. Income tax on profits made on investment utilizing foreign currency in-

flows

ii. Dividend income earned on investments made by non - citizens or for-eign companies in listed shares through inward remittances.

iii. The profits and income from the cultivation of tea or rubber by any plan-

5

tation company of which the Government is a shareholder, will be ex-empted from income tax for a period of 2 years commencing from April 1, 2016.

iv. Tax exemptions granted to certain organizations under Section 7 and miscellaneous exemptions under Section 13 will be removed.

Removal of Institutional exemptions

- The exemption of profits and income of international institutions granted under Section 7 will be restricted to,

• Any profits and income other than profits and income from sources generated by charging any fee or contribution from the public in any other manner.

• The present exemption applicable to local institutions will be removed other than:

Any Government Department Foreign Government University Co-operative Society Central Bank including the Monetary Board Charitable Institutions (subject to conditions) or Government Assisted Schools.

Removal of Miscellaneous exemptions

- The following exemptions under Section 13 will be revoked:

• The profits and income arising or accruing to any person from any undertaking for the construction of any port in Sri Lanka.

• The profits and income arising or accruing to any person from the administration of any sports ground, stadium or sports complex.

• The profits and income arising or accruing to any company, partnership or body of persons in a country outside Sri Lanka, from any payment made for the use of any computer software, by Sri Lankan Airlines Ltd or Mihin Lanka (Pvt) Ltd, as a special requirement of such airlines, if a Double Taxation Avoidance Agreement providing relief for double taxation of such profits and income is not in force between Sri Lanka and that country or tax is not payable in such country on such profits and income.

6

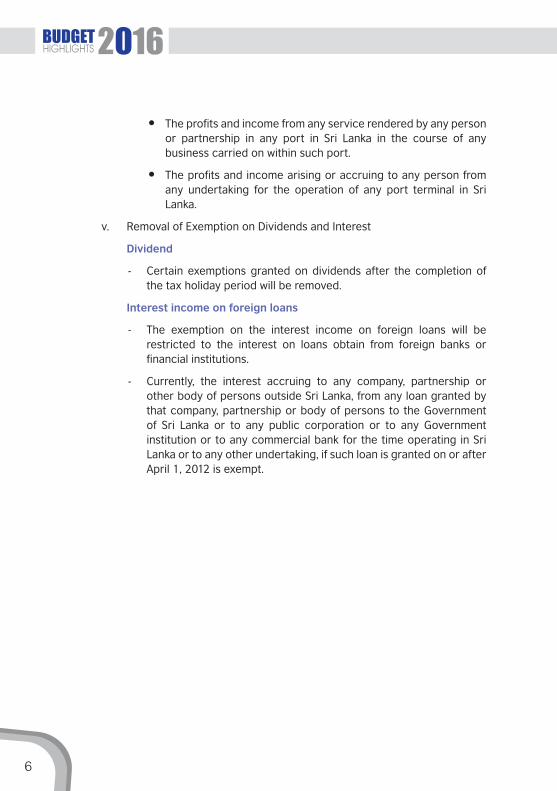

• The profits and income from any service rendered by any person or partnership in any port in Sri Lanka in the course of any business carried on within such port.

• The profits and income arising or accruing to any person from any undertaking for the operation of any port terminal in Sri Lanka.

v. Removal of Exemption on Dividends and Interest

Dividend

- Certain exemptions granted on dividends after the completion of the tax holiday period will be removed.

Interest income on foreign loans

- The exemption on the interest income on foreign loans will be restricted to the interest on loans obtain from foreign banks or financial institutions.

- Currently, the interest accruing to any company, partnership or other body of persons outside Sri Lanka, from any loan granted by that company, partnership or body of persons to the Government of Sri Lanka or to any public corporation or to any Government institution or to any commercial bank for the time operating in Sri Lanka or to any other undertaking, if such loan is granted on or after April 1, 2012 is exempt.

7

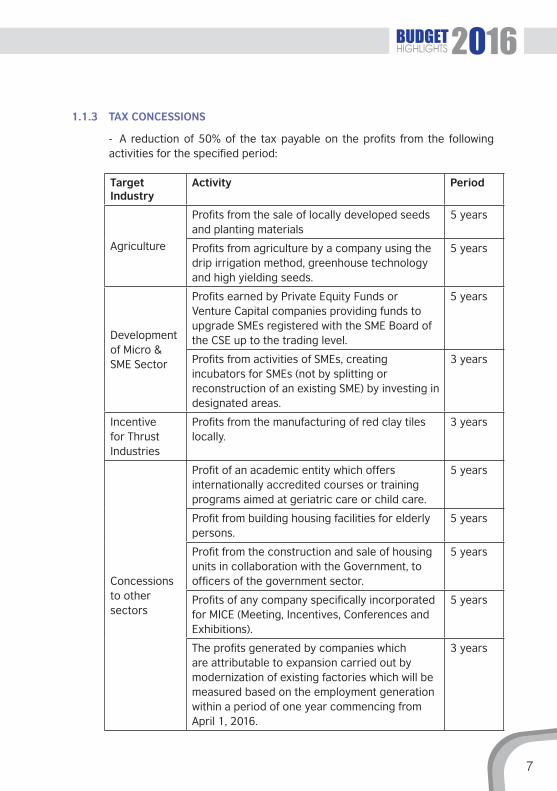

1.1.3 TAX CONCESSIONS

- A reduction of 50% of the tax payable on the profits from the following activities for the specified period:

Target Industry

Activity Period

Agriculture

Profits from the sale of locally developed seeds and planting materials

5 years

Profits from agriculture by a company using the drip irrigation method, greenhouse technology and high yielding seeds.

5 years

Development of Micro & SME Sector

Profits earned by Private Equity Funds or Venture Capital companies providing funds to upgrade SMEs registered with the SME Board of the CSE up to the trading level.

5 years

Profits from activities of SMEs, creating incubators for SMEs (not by splitting or reconstruction of an existing SME) by investing in designated areas.

3 years

Incentive for Thrust Industries

Profits from the manufacturing of red clay tiles locally.

3 years

Concessions to other sectors

Profit of an academic entity which offers internationally accredited courses or training programs aimed at geriatric care or child care.

5 years

Profit from building housing facilities for elderly persons.

5 years

Profit from the construction and sale of housing units in collaboration with the Government, to officers of the government sector.

5 years

Profits of any company specifically incorporated for MICE (Meeting, Incentives, Conferences and Exhibitions).

5 years

The profits generated by companies which are attributable to expansion carried out by modernization of existing factories which will be measured based on the employment generation within a period of one year commencing from April 1, 2016.

3 years

8

Concession on Investment in Lagging Region

A new company engaged in manufacturing (other than liquor or tobacco) or provision of services (not brought in to existence by splitting or reconstruction of an existing company) set up in any lagging region with a minimum investment of US$ 10 Mn or creating employment opportunities for 500 new employees (with new EPF Nos).

Note:If the new employment exceeds 800 If the investment is for theme park

5 years

8 years10 years

1.1.4 Withdrawal of Concession

Concessionary tax rates introduced in 2015 for the following categories will be revoked:

• Existing companies carrying on the business of manufacture of products (other than liquor and tobacco) upon expansion to provinces other than the Western province.

• New companies registered with the Department of Inland Revenue on or before 31.12.2015 with an investment of more than Rs. 500 Mn.

• Pioneering industries.

1.1.5 Extension of the deadline for listing in the Colombo Stock Exchange

In order to avail of the 50% rate reduction available under the Inland Revenue Act, an extension of time has been granted to companies to be listed on the Colombo Stock Exchange (CSE) as follows:

1.1.5.1 For listing in the CSE – The current deadline will be increased by a further 2 years

Proposed Deadline (5 years) Present Deadline (3 years)

From 01.04.2014 to 31.03.2019 From 01.04.2014 to 31.03.2017

1.1.5.2 For listing in the Foreign Stock Exchange - A period of 3 years will be granted (from 01.04.2016 to 31.03.2019).

9

1.1.6 AscertainmentofProfitsandIncome

• The triple tax deductions available for Research and Development activities will be extended to accommodate endowments given to our National Universities to engage in research in order to encourage persons to be a part of the country’s higher education revolution.

• The triple deduction for Research and Development expenses will be allowed only if a technology advancement and yield development is proved.

1.1.7 Qualifying payments

1.1.7.1 Fruit and Vegetable Industry The cost of acquisition of any machinery used for canning fruits and

vegetables will be treated as a qualifying payment in addition to the depreciation allowance claimable on such machinery.

1.1.7.2 Construction Industry The cost of acquisition of machinery necessary for purifying sea sand will

be treated as a qualifying payment in addition to the depreciation allowance claimable on such machinery.

1.1.7.3 Qualifying Payment for Acquisition or Merger of Banks The qualifying payment relief introduced on the expenditure associated

with the cost of acquisition or merger of banks or financial companies under the banking and financial institutions consolidation process will be removed considering that the deduction is already available as a cost, through amendments brought in 2015. As such this will be a retrospective amendment.

1.1.8 Miscellaneous

1.1.8.1 Management Fee A definition will be provided for the management fee with regard to the

insurance industry.

1.1.8.2 Income Tax Refund The refund claim for any year of assessment commencing on or after April

2016, should be finalized within three years from the claim of such refund (with the return). If not finalized, the refund would be allowed to be set off against the future tax liability of the same.

10

1.1.8.3 Penal Provisions With a view to strengthen the tax collection and compliance by tax payers

and tax practitioners, the existing penal provisions will be amended.

Further, provisions will be introduced to ensure the proper implementation of transfer pricing.

1.2 Personal Income Tax

1.2.1 Tax Free Allowance and Income Tax rate for Individuals The tax free allowance will be Rs. 2.4 Mn per annum (Rs. 200,000 per month).

This has been increased from the current tax-free allowance + qualifying payment relief totalling to Rs. 750,000 per annum (Rs. 62,500 per month).

The balance will be taxed at a standard rate of 15%. Previously progressive tax rates were applicable on the balance income as follows:

On the first Rs. 500,000 4% Next Rs. 500,000 8% Next Rs. 500,000 12% Balance 16%

The above tax treatment will be applicable to both employees subject to PAYE and self-employees.

1.2.2 Deduction from the total statutory income and assessable income Deductions from the Total Statutory Income and the Assessable Income will

be removed considering the new tax free allowance individuals, charitable institutions, etc. are entitled to deducted [except the losses incurred from trade, business, profession or vocation (deductible subject to 35% of the total statutory income)].

1.2.3 Theexemptiononprofitfromemployment The exemption on profit from employment referred to in Section 8 of the Act

will be removed except the following:

- Retiring benefits and pension paid out of the Consolidated Fund to Government employees.

- Earnings in foreign currency on employment out of the country, if such earnings are remitted to Sri Lanka.

- Exemptions for diplomatic missions and diplomatic personnel.- Release of the provident fund balance at the time of retirement.- Compensation for loss of office subject to conditions.

11

All the other cash and non-cash benefits (treated as benefit from employment) are liable to tax.

1.2.4 Employees employed under more than one employer Employees who are employed under more than one employer will be liable

to tax at the rate of 15%.

Presently, the rate of tax applicable to employees who are employed under more than one employer, where such remuneration is paid by any employer other than the main employer, is as follows:

Where the remuneration is less than Rs. 25,000 -10% Where the remuneration is not less than Rs. 25,000 -16%

1.2.5 Withholding tax on interest income from deposits - individuals and charitable institutions

The withholding tax rate of 2.5% introduced in 2015 will be removed and such income will be considered as part of the Total Statutory Income.

Presently, tax is withheld at the rate of 2.5%, irrespective of the amount of interest.

1.2.6 Deduction of withholding tax on interest income arising to individuals out of Sri Lanka (Sec 95)

Deduction of withholding tax on interest income arising to individuals out of Sri Lanka will be at the rate of 15%, subject to the rate specified under any Double Taxation Avoidance Agreement entered into with the Government of Sri Lanka.

Currently, the applicable withholding tax rate is 20% subject to the rate specified under any Double Taxation Avoidance Agreement entered into with the Government of Sri Lanka.

1.2.7 Special Privileges for Individual Taxpayers

Individual taxpayers who pay Rs. 25Mn or more as taxes will be granted special privileges.

1.3 Partnership Tax

This is a proposal to adjust the tax on partnership.

Presently, the tax-free allowance applicable for a partnership is Rs. 1,000,000 and the tax rate applicable is 8%.

12

2. VALUE ADDED TAX (VAT)

2.1 RATE

The present single rate will be revised to 3 bands.

Export of goods and provision of services for payment in foreign currency

outside Sri Lanka - 0%

Service Sector - 12.5%

Manufacturing or import of goods - 8% (with limitation of input tax)

Presently, the rate applicable is 0% and 11%.

2.2 REMOVAL OF EXEMPTIONS

The present exemptions given for the import or supply of telecom equipment

or machinery and high-tech equipment including copper cables for the

telecom industry will be removed.

2.3 EXCLUDED SUPPLIES

VAT on wholesale and retail trade was introduced on persons having quarterly

turnover/supplies (including exempt turnover/ supplies) of Rs. 500Mn or more

to the extent of liable supplies, in 2013. The quarterly threshold was reduced

in 2014 and 2015 as follows, to bring more companies into VAT Scheme:

2014 - Rs. 250Mn

2015 - Rs. 100Mn.

A proposal has been put forward to remove VAT on wholesale and retail trade

(other than by a manufacturer or importer).

2.4 REGISTRATION THRESHOLD

The existing threshold of Rs. 3.75Mn per quarter or Rs. 15Mn. per annum will

be revised to Rs. 3Mn per quarter or Rs. 12Mn per annum.

2.5 EFFECTIVE DATE OF PROPOSAL

These proposals in relation to VAT are expected to come in to effect from 1st

January 2016.

13

3. NATION BUILDING TAX (NBT)

3.1 RATE The NBT rate will be revised to 4%. Currently, the rate applicable is 2%.

3.2 REMOVAL OF EXEMPTIONS The present exemptions on the following articles or services will be removed:

- Telecommunication service - Supply of electricity - Lubricants.

3.3 REGISTRATION THRESHOLD The threshold will be revised to Rs. 3Mn per quarter or Rs. 12Mn per annum.

The existing threshold is Rs. 3.75Mn per quarter or Rs. 15Mn. per annum, except for the following categories of business where the threshold is Rs.25Mn per quarter.

- Operating a hotel, guest house, restaurant or other similar business;- The processing of any locally procured agricultural produce in the

preparation for sale;- Providing an educational service locally; or- Supply of labour.

The threshold of Rs. 25Mn per quarter will be removed, except for any locally procured agricultural produce in the preparation for sale.

3.4 EFFECTIVE DATE OF PROPOSAL These proposals in relation to NBT are expected to come in to effect from 1st

January 2016.

14

4. ECONOMIC SERVICE CHARGE (ESC)

I. Currently ESC is required to be paid by companies which are not paying income tax either due to incurring losses or being exempt from income tax. Companies that make profits and accordingly pay taxes are exempt from ESC.

A proposal has been put forward to withdraw the exemption given to profit making entities.

II. The present maximum liability of Rs. 120Mn per year will be removed

III. The ESC rate is increased from 0.25% to 0.5%

IV. The period for carried forward ESC to be set-off against the income tax payable for any period commencing from April 1, 2016, is reduced from 5 years to 3 years.

4.1 EFFECTIVE DATE OF PROPOSAL

These proposals in relation to NBT are expected to come in to effect from 1st April 2016.

15

5. MISCELLANEOUS

5.1 SHARE TRANSACTION LEVY (STL)

STL which is currently applicable at 0.3% will be removed with effect from January 1, 2016.

5.2 CONSTRUCTION INDUSTRY GUARANTEE FUND LEVY (CIGFL)

CIGFL was applicable on every contract enforced in Sri Lanka by every construction contractor at varying rates based on the contract value as follows:

Value of Contract Rate

Less than Rs. 15Mn Nil

Not Less than Rs. 15Mn but less than Rs. 50Mn 0.25%

Not Less than Rs. 50Mn but less than Rs. 150Mn 0.5%

Rs.150Mn or more 1%

CIGFL will be removed with effect from January 1, 2016.

5.3 LUXURY & SEMI LUXURY MOTOR VEHICLE TAX

The luxury & semi-luxury motor vehicle tax which is currently liable based on the engine capacity, will be removed with effect from April 1, 2016.

5.4 BETTING & GAMING LEVY

(i) The entry fee of US$ 100 per person (introduced in 2015) who enters a Casino for entertainment purposes will be removed.

(ii) The present annual levy of Rs. 200Mn for carrying on the business of playing rudjino will be reduced to Rs. 5Mn per year.

(iii) The present annual levy of Rs. 200Mn for carrying on the business of Casino will be increased to Rs. 400Mn per year.

(iv) Directors and shareholders will be personally liable for non-payment or any act which is done to avoid the payment of Casino Industry Levy (one off levy) introduced in the interim budget amounting to Rs. 250Mn.

16

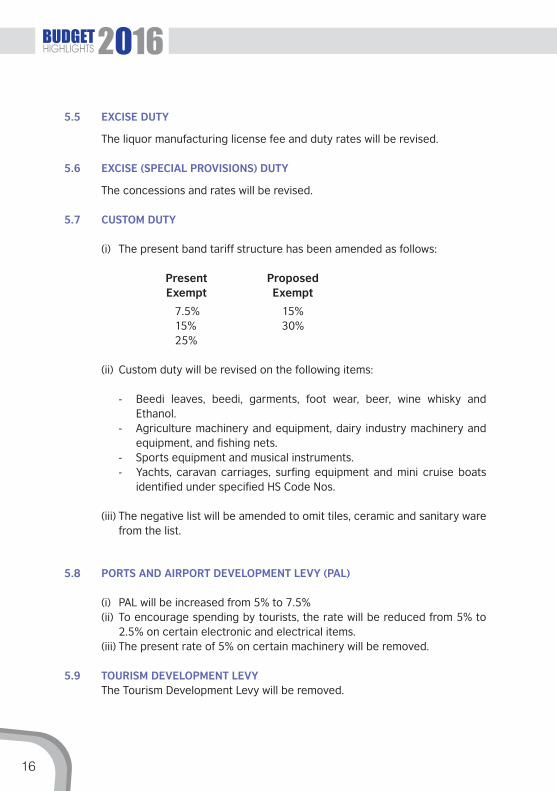

5.5 EXCISE DUTY

The liquor manufacturing license fee and duty rates will be revised.

5.6 EXCISE (SPECIAL PROVISIONS) DUTY

The concessions and rates will be revised.

5.7 CUSTOM DUTY

(i) The present band tariff structure has been amended as follows:

Present Proposed Exempt Exempt

7.5% 15% 15% 30% 25% (ii) Custom duty will be revised on the following items:

- Beedi leaves, beedi, garments, foot wear, beer, wine whisky and Ethanol.

- Agriculture machinery and equipment, dairy industry machinery and equipment, and fishing nets.

- Sports equipment and musical instruments.- Yachts, caravan carriages, surfing equipment and mini cruise boats

identified under specified HS Code Nos.

(iii) The negative list will be amended to omit tiles, ceramic and sanitary ware from the list.

5.8 PORTS AND AIRPORT DEVELOPMENT LEVY (PAL)

(i) PAL will be increased from 5% to 7.5% (ii) To encourage spending by tourists, the rate will be reduced from 5% to

2.5% on certain electronic and electrical items.(iii) The present rate of 5% on certain machinery will be removed.

5.9 TOURISM DEVELOPMENT LEVY The Tourism Development Levy will be removed.

17

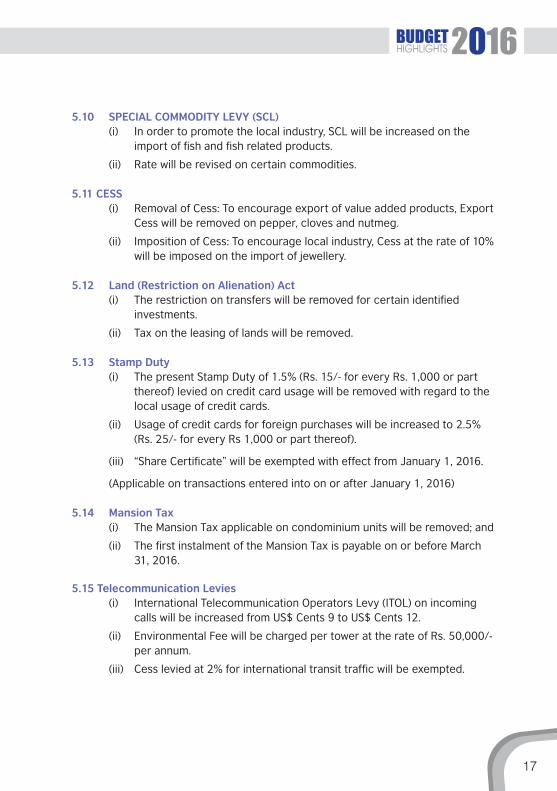

5.10 SPECIAL COMMODITY LEVY (SCL) (i) In order to promote the local industry, SCL will be increased on the

import of fish and fish related products.

(ii) Rate will be revised on certain commodities.

5.11 CESS (i) Removal of Cess: To encourage export of value added products, Export

Cess will be removed on pepper, cloves and nutmeg.

(ii) Imposition of Cess: To encourage local industry, Cess at the rate of 10% will be imposed on the import of jewellery.

5.12 Land (Restriction on Alienation) Act (i) The restriction on transfers will be removed for certain identified

investments.

(ii) Tax on the leasing of lands will be removed.

5.13 Stamp Duty (i) The present Stamp Duty of 1.5% (Rs. 15/- for every Rs. 1,000 or part

thereof) levied on credit card usage will be removed with regard to the local usage of credit cards.

(ii) Usage of credit cards for foreign purchases will be increased to 2.5% (Rs. 25/- for every Rs 1,000 or part thereof).

(iii) “Share Certificate” will be exempted with effect from January 1, 2016.

(Applicable on transactions entered into on or after January 1, 2016)

5.14 Mansion Tax (i) The Mansion Tax applicable on condominium units will be removed; and

(ii) The first instalment of the Mansion Tax is payable on or before March 31, 2016.

5.15 Telecommunication Levies (i) International Telecommunication Operators Levy (ITOL) on incoming

calls will be increased from US$ Cents 9 to US$ Cents 12.

(ii) Environmental Fee will be charged per tower at the rate of Rs. 50,000/- per annum.

(iii) Cess levied at 2% for international transit traffic will be exempted.

18

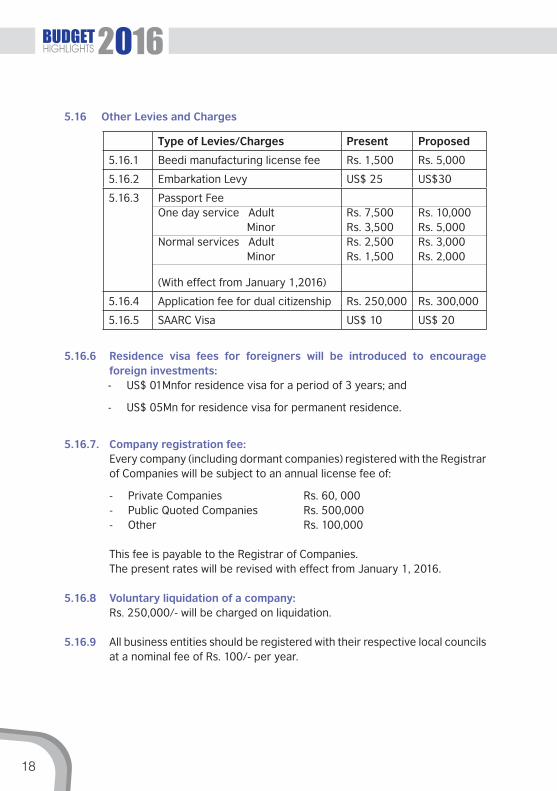

5.16 Other Levies and Charges

Type of Levies/Charges Present Proposed

5.16.1 Beedi manufacturing license fee Rs. 1,500 Rs. 5,000

5.16.2 Embarkation Levy US$ 25 US$30

5.16.3 Passport FeeOne day service Adult MinorNormal services Adult Minor

(With effect from January 1,2016)

Rs. 7,500Rs. 3,500Rs. 2,500Rs. 1,500

Rs. 10,000Rs. 5,000Rs. 3,000Rs. 2,000

5.16.4 Application fee for dual citizenship Rs. 250,000 Rs. 300,000

5.16.5 SAARC Visa US$ 10 US$ 20

5.16.6 Residence visa fees for foreigners will be introduced to encourage foreign investments:- US$ 01Mnfor residence visa for a period of 3 years; and

- US$ 05Mn for residence visa for permanent residence.

5.16.7. Company registration fee:Every company (including dormant companies) registered with the Registrar of Companies will be subject to an annual license fee of:

- Private Companies Rs. 60, 000- Public Quoted Companies Rs. 500,000- Other Rs. 100,000

This fee is payable to the Registrar of Companies.The present rates will be revised with effect from January 1, 2016.

5.16.8 Voluntary liquidation of a company: Rs. 250,000/- will be charged on liquidation.

5.16.9 All business entities should be registered with their respective local councils at a nominal fee of Rs. 100/- per year.

19

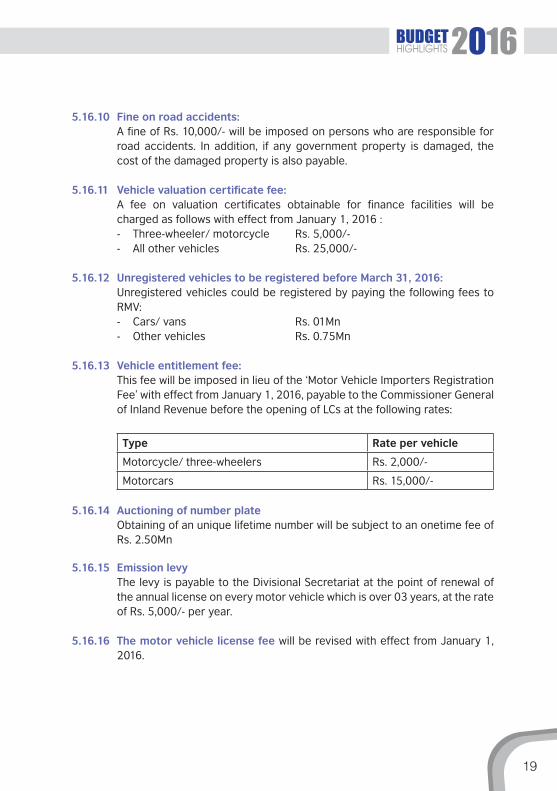

5.16.10 Fine on road accidents: A fine of Rs. 10,000/- will be imposed on persons who are responsible for

road accidents. In addition, if any government property is damaged, the cost of the damaged property is also payable.

5.16.11 Vehiclevaluationcertificatefee: A fee on valuation certificates obtainable for finance facilities will be

charged as follows with effect from January 1, 2016 :- Three-wheeler/ motorcycle Rs. 5,000/-- All other vehicles Rs. 25,000/-

5.16.12 Unregistered vehicles to be registered before March 31, 2016: Unregistered vehicles could be registered by paying the following fees to

RMV:- Cars/ vans Rs. 01Mn- Other vehicles Rs. 0.75Mn

5.16.13 Vehicle entitlement fee: This fee will be imposed in lieu of the ‘Motor Vehicle Importers Registration

Fee’ with effect from January 1, 2016, payable to the Commissioner General of Inland Revenue before the opening of LCs at the following rates:

Type Rate per vehicle

Motorcycle/ three-wheelers Rs. 2,000/-

Motorcars Rs. 15,000/-

5.16.14 Auctioning of number plate Obtaining of an unique lifetime number will be subject to an onetime fee of

Rs. 2.50Mn

5.16.15 Emission levy The levy is payable to the Divisional Secretariat at the point of renewal of

the annual license on every motor vehicle which is over 03 years, at the rate of Rs. 5,000/- per year.

5.16.16 The motor vehicle license fee will be revised with effect from January 1, 2016.

20

5.16.17 Import taxes on garments and footwear :

(i) The present composite tax imposed (at the Custom point) on sale of garments to the local market by export oriented companies [referred to in Section 22(1) of the VAT Act] will be increased from Rs. 25 to Rs. 200 /- per piece.

(ii) The same rate (Rs. 200) will be extended to the sale of footwear to the local market by export oriented companies.

(iii) The sale of export quality products to the local market by export oriented BOI companies will be restricted to 5% of the total turnover and will be subject to tax at the rate specified above.

5.16.18 A charge will be imposed on Airlines on the sale of international tickets at US$ 2.00 per passenger.

5.17 Revenue Administration Management Information System (RAMIS)

Relevant amendments will be incorporated (where necessary) for the implementation of RAMIS.

5.18 Approved Accountant (107 2(A) (B))

The expansion of the term “Approved Accountant” to include AAT members in 2015 has been amended as follows:

- Restricting the audits that this person is able to carry out with a turnover limit not exceeding Rs. 100 Mn brought down from Rs. 500 Mn.

5.19 Transfer Pricing on Domestic Transaction

Administration of transfer pricing on domestic transactions will be simplified and the areas will be specified limiting the scope considering the associated cost involved and we expect that companies who transact with each other and are liable for tax at the same rates will be excluded from the scope of domestic transactions since there is no base erosion.

21

5.20 Foreign Exchange Control

1. Securities and Investment Account (SIA):

SIA will be abolished. Foreign investments can be channelled through any bank account to Sri Lanka.

2. Exchange Control Act to be repealed:

To facilitate foreign investments, a new act which is to be named as “the Foreign Exchange Management Act” will be introduced.

5.21 Strategic Development Act

The Strategic Development Act will continue to be effective for existing companies that have availed the concessions under that act. For companies who make new investments, the Strategic Development Act will not apply. The New Investment Act will be enacted.

5.22 Tax concessions to be granted by the Ministry of Finance

The granting of tax concessions for any investment will be strictly under the supervision and monitoring of the Ministry of Finance which would be governed by regulations issued by the Minister. The Board of Investment or Department of Inland Revenue will not grant any new tax holidays other than the facilitation and implementation of concessions.

5.23 Effective Dates of Proposals

(i) Betting and Gaming Levy, and Land (Restriction on Alienation) Act will be implemented with effect from January 1, 2016.

(ii) Cess, Ports and Airport Development Levy, Custom Duty, Excise (Special Provisions) and Special Commodity Levy will take effect immediately.

22

OUR COMMENTS

BUDGET OVERVIEW

With a view of achieving sustainable economic growth in our country, this year’s budget presented by the newly elected parliament sees a strategic turnaround in the taxation and budget allocation proposals covering key areas of the economy.

The Government tax revenue to GDP ratio had fallen drastically from 19% achieved in 1990 to 10.2% by 2014. In this light, we capture below the key highlights of the tax proposals which seek to achieve economic growth through strengthening of the Government tax revenue.

Incentive for foreign investors on Land Ownership

The Land (Restrictions on Alienation) Act No.38 of 2014 prohibited the outright purchase of land by foreign investors. Under this Act, the foreign investors were permitted to hold land in Sri Lanka only by way of a lease, subject to a land lease tax of either 7.5% or 15%. This restriction discouraged foreign investments.

It has been proposed to not only remove this restriction on foreign ownership for identified investments but to remove the land lease tax imposed under this Act. This can be viewed as positive step towards attracting foreign inward investment.

Streamlining of Direct Tax for Companies

The corporate tax structure comprises of the standard rate of 28% and several concessionary rates across a range of sectors. It has been proposed to streamline this structure to only two levels. More specifically, companies in the sectors of betting & gaming, liquor, tobacco, banking/finance/leasing, trading (excluding manufactures and service providers) will be subjected to a higher rate of 30%. The lower rate of 15% is to apply to all other sectors.

While this is considered as a good measure towards streamlining corporate tax, the practical consideration of how it would assist to increase the Government tax revenue is questionable. If the envisaged objective is to be achieved, the Government will have to ensure the establishment of a sound tax compliance and enforcement mechanism.

ESCforprofitmakingcompanies

ESC operates as a minimum tax, which was payable only by loss making companies and companies enjoying a tax holiday. The objective was to reduce the tax burden on

23

tax liable companies. Accordingly, profit making companies who were paying income tax were not subjected to ESC.

However, as a measure of increasing the Government tax revenue, it has been proposed to remove the ESC exclusion granted to profit making companies. Therefore the profit making companies will have to pay ESC in addition to any income tax liability. Further it has been proposed to double the ESC rate to 0.5% from the existing 0.25%.

This measure defeats the purpose of ESC as a minimum tax and the proposal imposes an additional burden in the tax compliance process for tax paying companies.

Concession for Individuals

A notable tax concession is proposed for individuals to remove the current progressive income tax rates and increase the annual tax free allowance from Rs. 500,000 to Rs. 2.4Mn, applying only a flat rate of 15% on the balance income in excess of Rs. 2.4Mn. Further, the minimum WHT of 2.5% imposed on interest for individuals is to be removed.

While this is a positive measure towards reducing the tax burden of individuals as to whether the Government will achieve its objective of increase in Government tax revenue, is questionable. Since only individuals in the high income slab will be made liable for taxes, the Government should establish a sound tax compliance and enforcement mechanism to ensure collection of such tax from all liable persons.

Restructuring of Indirect taxes

The VAT and NBT registration thresholds have been reversed to the previously existing threshold of Rs. 12Mn per annum from the increased threshold of Rs. 15Mn per annum, which was made effective last year. Another reversal proposed is the exemption of wholesale and retail trade from the purview of VAT.

In 2005, though 41% of the total tax revenue was collected from VAT, its contribution to the tax revenue had decreased significantly to 26% by 2014. In this light, while it has been proposed to increase the VAT rate from 11% to 12.5% for service providers a reduced rate of 8% is proposed for manufacturers and importers of goods.

24

Companies engaged in the sectors of Telecommunication services, supply of electricity and lubricants are to brought under the ambit of NBT. Further it has been proposed to double the NBT rate to 4% from the existing rate of 2%.

Revision on Import Taxes

The maximum customs duty rate is proposed to be increased to 30% from the existing 25%. Further items such as tiles, ceramic and sanitary ware, the import of which is restricted are to be removed for the negative list.

Another increase is the PAL rate to 7.5% from the existing rate of 5%. However plant and machinery used for construction, dairy and agricultural industries is to be exempted from PAL.

Concessions for the Tourism industry

As a measure to boost the country’s foreign income through tourism, the PAL on certain electronic and electrical items is to be reduced from 5% to 2.5%. Further the present Tourism Development Levy of 1% charged on the tourism industry is to be removed.

Stamp Duty Considerations

While the stamp duty of 1.5% imposed on local credit card transactions is proposed to be removed, the stamp duty of foreign purchases is to be increased to 2.5%. Further exemption has been proposed for stamp duty imposed on share certificates.

However the Government’s objectives of the stamp duty proposals are unclear.

Analysing the above, while certain proposals can be considered as a positive measure towards achieving the Government’s objective, as to whether the envisaged revenue target will be achieved and how it will achieved should be given due consideration in light of the tax compliance and enforcement mechanism in Sri Lanka.

25

Appendix

26

2016/17

%

2015/16

%

2014/15

%

2013/14

%

2012/13

%

2011/12

%

Income Tax

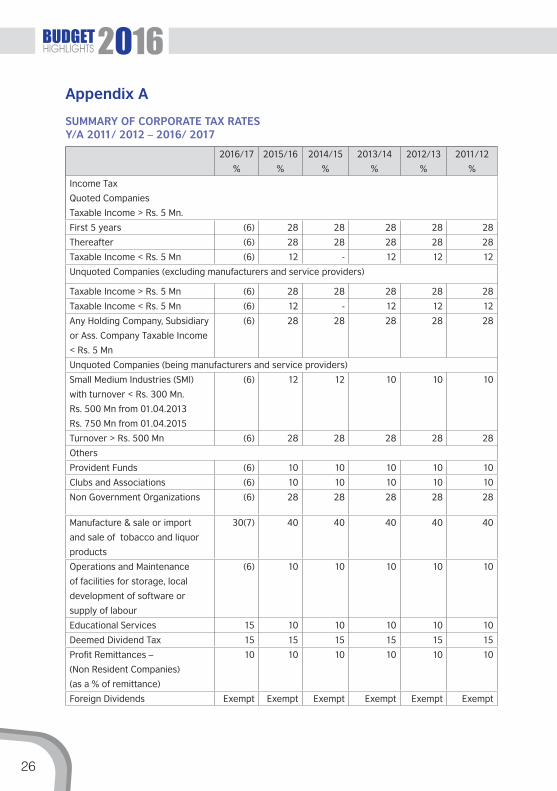

Quoted Companies

Taxable Income > Rs. 5 Mn.

First 5 years (6) 28 28 28 28 28

Thereafter (6) 28 28 28 28 28

Taxable Income < Rs. 5 Mn (6) 12 - 12 12 12

Unquoted Companies (excluding manufacturers and service providers)

Taxable Income > Rs. 5 Mn (6) 28 28 28 28 28

Taxable Income < Rs. 5 Mn (6) 12 - 12 12 12

Any Holding Company, Subsidiary

or Ass. Company Taxable Income

< Rs. 5 Mn

(6) 28 28 28 28 28

Unquoted Companies (being manufacturers and service providers)

Small Medium Industries (SMI)

with turnover < Rs. 300 Mn.

Rs. 500 Mn from 01.04.2013

Rs. 750 Mn from 01.04.2015

(6) 12 12 10 10 10

Turnover > Rs. 500 Mn (6) 28 28 28 28 28

Others

Provident Funds (6) 10 10 10 10 10

Clubs and Associations (6) 10 10 10 10 10

Non Government Organizations (6) 28 28 28 28 28

Manufacture & sale or import

and sale of tobacco and liquor

products

30(7) 40 40 40 40 40

Operations and Maintenance

of facilities for storage, local

development of software or

supply of labour

(6) 10 10 10 10 10

Educational Services 15 10 10 10 10 10

Deemed Dividend Tax 15 15 15 15 15 15

Profit Remittances –

(Non Resident Companies)

(as a % of remittance)

10 10 10 10 10 10

Foreign Dividends Exempt Exempt Exempt Exempt Exempt Exempt

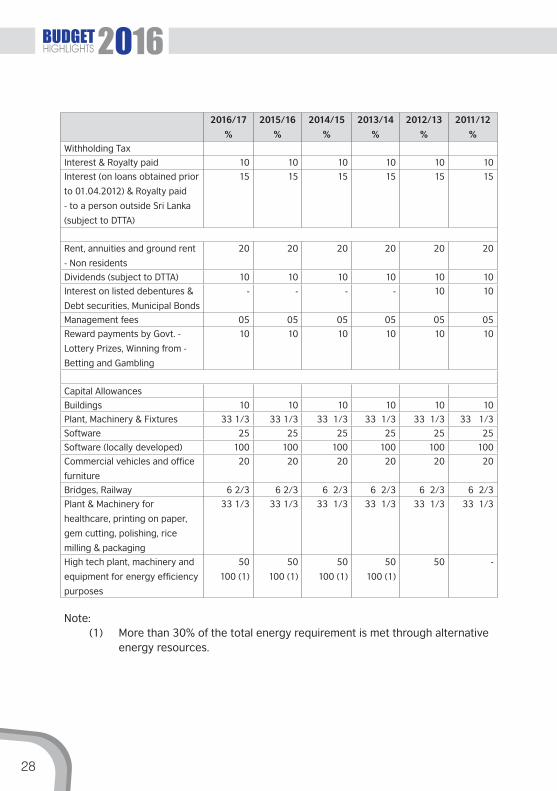

Appendix A

SUMMARY OF CORPORATE TAX RATESY/A 2011/ 2012 – 2016/ 2017

27

2016/17

%

2015/16

%

2014/15

%

2013/14

%

2012/13

%

2011/12

%

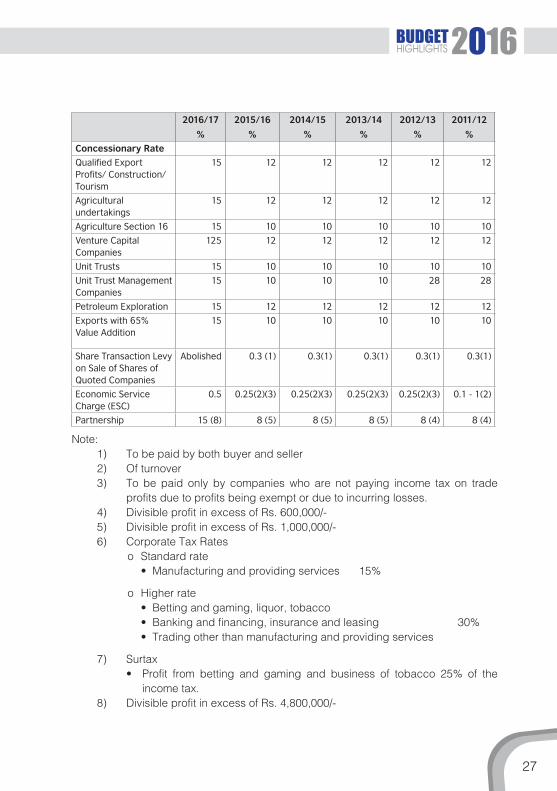

Concessionary Rate

Qualified Export Profits/ Construction/ Tourism

15 12 12 12 12 12

Agricultural undertakings

15 12 12 12 12 12

Agriculture Section 16 15 10 10 10 10 10

Venture Capital Companies

125 12 12 12 12 12

Unit Trusts 15 10 10 10 10 10

Unit Trust Management Companies

15 10 10 10 28 28

Petroleum Exploration 15 12 12 12 12 12

Exports with 65% Value Addition

15 10 10 10 10 10

Share Transaction Levy on Sale of Shares of Quoted Companies

Abolished 0.3 (1) 0.3(1) 0.3(1) 0.3(1) 0.3(1)

Economic Service Charge (ESC)

0.5 0.25(2)(3) 0.25(2)(3) 0.25(2)(3) 0.25(2)(3) 0.1 - 1(2)

Partnership 15 (8) 8 (5) 8 (5) 8 (5) 8 (4) 8 (4)

Note:1) To be paid by both buyer and seller2) Of turnover 3) To be paid only by companies who are not paying income tax on trade

profits due to profits being exempt or due to incurring losses.4) Divisible profit in excess of Rs. 600,000/-5) Divisible profit in excess of Rs. 1,000,000/-6) Corporate Tax Rates

o Standard rate · Manufacturing and providing services 15%

o Higher rate · Betting and gaming, liquor, tobacco · Banking and financing, insurance and leasing 30% · Trading other than manufacturing and providing services

7) Surtax· Profit from betting and gaming and business of tobacco 25% of the

income tax.8) Divisible profit in excess of Rs. 4,800,000/-

28

2016/17

%

2015/16

%

2014/15

%

2013/14

%

2012/13

%

2011/12

%

Withholding Tax

Interest & Royalty paid 10 10 10 10 10 10

Interest (on loans obtained prior

to 01.04.2012) & Royalty paid

- to a person outside Sri Lanka

(subject to DTTA)

15 15 15 15 15 15

Rent, annuities and ground rent

- Non residents

20 20 20 20 20 20

Dividends (subject to DTTA) 10 10 10 10 10 10

Interest on listed debentures &

Debt securities, Municipal Bonds

- - - - 10 10

Management fees 05 05 05 05 05 05

Reward payments by Govt. -

Lottery Prizes, Winning from -

Betting and Gambling

10 10 10 10 10 10

Capital Allowances

Buildings 10 10 10 10 10 10

Plant, Machinery & Fixtures 33 1/3 33 1/3 33 1/3 33 1/3 33 1/3 33 1/3

Software 25 25 25 25 25 25

Software (locally developed) 100 100 100 100 100 100

Commercial vehicles and office

furniture

20 20 20 20 20 20

Bridges, Railway 6 2/3 6 2/3 6 2/3 6 2/3 6 2/3 6 2/3

Plant & Machinery for

healthcare, printing on paper,

gem cutting, polishing, rice

milling & packaging

33 1/3 33 1/3 33 1/3 33 1/3 33 1/3 33 1/3

High tech plant, machinery and

equipment for energy efficiency

purposes

50

100 (1)

50

100 (1)

50

100 (1)

50

100 (1)

50 -

Note:(1) More than 30% of the total energy requirement is met through alternative

energy resources.

29

2016/17

%

2015/16

%

2014/15

%

2013/14

%

2012/13

%

2011/12

%

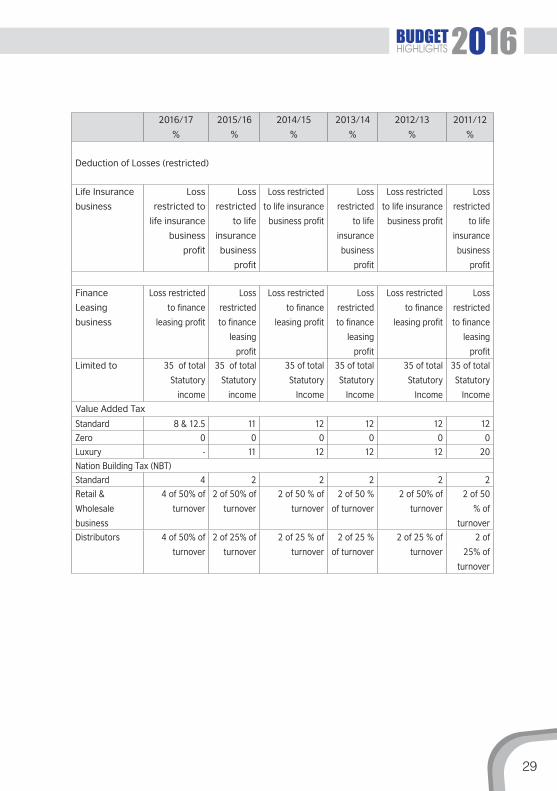

Deduction of Losses (restricted)

Life Insurance

business

Loss

restricted to

life insurance

business

profit

Loss

restricted

to life

insurance

business

profit

Loss restricted

to life insurance

business profit

Loss

restricted

to life

insurance

business

profit

Loss restricted

to life insurance

business profit

Loss

restricted

to life

insurance

business

profit

Finance

Leasing

business

Loss restricted

to finance

leasing profit

Loss

restricted

to finance

leasing

profit

Loss restricted

to finance

leasing profit

Loss

restricted

to finance

leasing

profit

Loss restricted

to finance

leasing profit

Loss

restricted

to finance

leasing

profit

Limited to 35 of total

Statutory

income

35 of total

Statutory

income

35 of total

Statutory

Income

35 of total

Statutory

Income

35 of total

Statutory

Income

35 of total

Statutory

Income

Value Added Tax

Standard 8 & 12.5 11 12 12 12 12

Zero 0 0 0 0 0 0

Luxury - 11 12 12 12 20

Nation Building Tax (NBT)

Standard 4 2 2 2 2 2

Retail &

Wholesale

business

4 of 50% of

turnover

2 of 50% of

turnover

2 of 50 % of

turnover

2 of 50 %

of turnover

2 of 50% of

turnover

2 of 50

% of

turnover

Distributors 4 of 50% of

turnover

2 of 25% of

turnover

2 of 25 % of

turnover

2 of 25 %

of turnover

2 of 25 % of

turnover

2 of

25% of

turnover

30

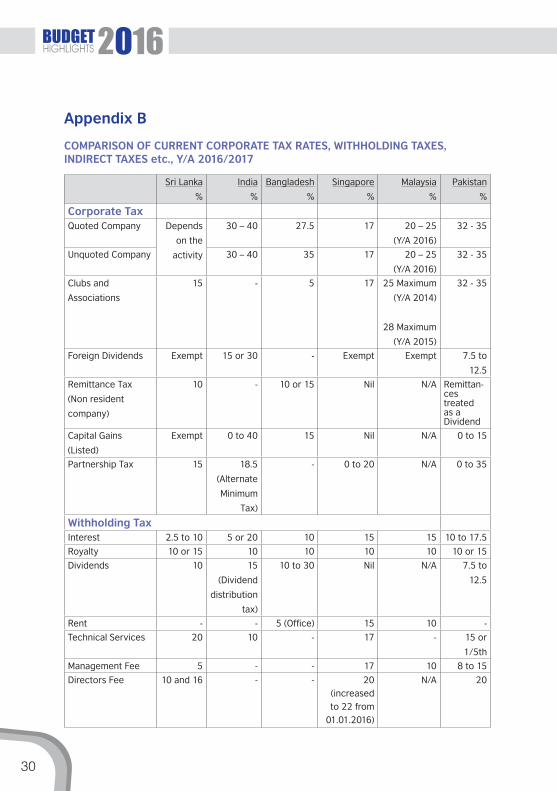

Sri Lanka

%

India

%

Bangladesh

%

Singapore

%

Malaysia

%

Pakistan

%

Corporate TaxQuoted Company Depends

on the

activity

30 – 40 27.5 17 20 – 25

(Y/A 2016)

32 - 35

Unquoted Company 30 – 40 35 17 20 – 25

(Y/A 2016)

32 - 35

Clubs and

Associations

15 - 5 17 25 Maximum

(Y/A 2014)

28 Maximum

(Y/A 2015)

32 - 35

Foreign Dividends Exempt 15 or 30 - Exempt Exempt 7.5 to

12.5

Remittance Tax

(Non resident

company)

10 - 10 or 15 Nil N/A Remittan-ces treated as a Dividend

Capital Gains

(Listed)

Exempt 0 to 40 15 Nil N/A 0 to 15

Partnership Tax 15 18.5

(Alternate

Minimum

Tax)

- 0 to 20 N/A 0 to 35

Withholding TaxInterest 2.5 to 10 5 or 20 10 15 15 10 to 17.5

Royalty 10 or 15 10 10 10 10 10 or 15

Dividends 10 15

(Dividend

distribution

tax)

10 to 30 Nil N/A 7.5 to

12.5

Rent - - 5 (Office) 15 10 -

Technical Services 20 10 - 17 - 15 or

1/5th

Management Fee 5 - - 17 10 8 to 15

Directors Fee 10 and 16 - - 20 (increased to 22 from

01.01.2016)

N/A 20

Appendix B

COMPARISON OF CURRENT CORPORATE TAX RATES, WITHHOLDING TAXES, INDIRECT TAXES etc., Y/A 2016/2017

31

Sri Lanka

%

India

%

Bangladesh

%

Singapore

%

Malaysia

%

Pakistan

%

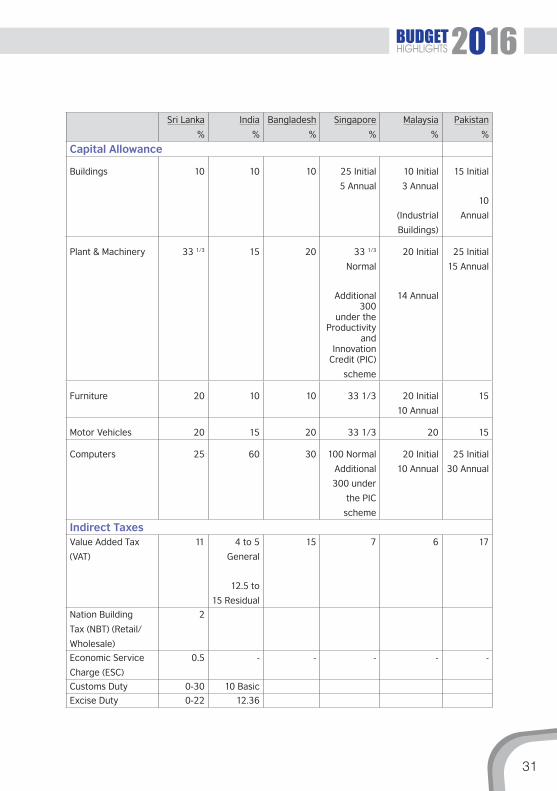

Capital Allowance

Buildings 10 10 10 25 Initial

5 Annual

10 Initial

3 Annual

(Industrial

Buildings)

15 Initial

10

Annual

Plant & Machinery 33 1/3 15 20 33 1/3

Normal

Additional 300

under the Productivity

and Innovation

Credit (PIC)

scheme

20 Initial

14 Annual

25 Initial

15 Annual

Furniture 20 10 10 33 1/3 20 Initial

10 Annual

15

Motor Vehicles 20 15 20 33 1/3 20 15

Computers 25 60 30 100 Normal

Additional

300 under

the PIC

scheme

20 Initial

10 Annual

25 Initial

30 Annual

Indirect TaxesValue Added Tax

(VAT)

11 4 to 5

General

12.5 to

15 Residual

15 7 6 17

Nation Building

Tax (NBT) (Retail/

Wholesale)

2

Economic Service

Charge (ESC)

0.5 - - - - -

Customs Duty 0-30 10 Basic

Excise Duty 0-22 12.36

32

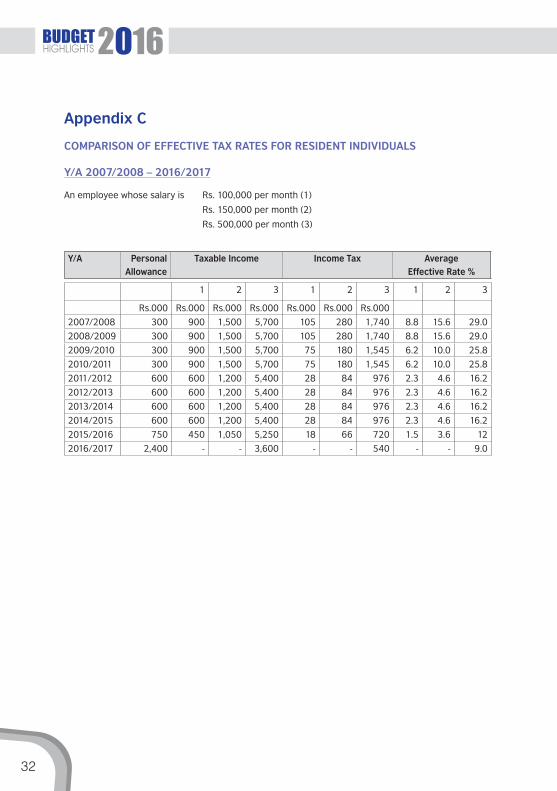

Appendix C

COMPARISON OF EFFECTIVE TAX RATES FOR RESIDENT INDIVIDUALS

Y/A 2007/2008 – 2016/2017

An employee whose salary is Rs. 100,000 per month (1)

Rs. 150,000 per month (2)

Rs. 500,000 per month (3)

Y/A PersonalAllowance

Taxable Income Income Tax AverageEffective Rate %

1 2 3 1 2 3 1 2 3

Rs.000 Rs.000 Rs.000 Rs.000 Rs.000 Rs.000 Rs.000

2007/2008 300 900 1,500 5,700 105 280 1,740 8.8 15.6 29.0

2008/2009 300 900 1,500 5,700 105 280 1,740 8.8 15.6 29.0

2009/2010 300 900 1,500 5,700 75 180 1,545 6.2 10.0 25.8

2010/2011 300 900 1,500 5,700 75 180 1,545 6.2 10.0 25.8

2011/2012 600 600 1,200 5,400 28 84 976 2.3 4.6 16.2

2012/2013 600 600 1,200 5,400 28 84 976 2.3 4.6 16.2

2013/2014 600 600 1,200 5,400 28 84 976 2.3 4.6 16.2

2014/2015 600 600 1,200 5,400 28 84 976 2.3 4.6 16.2

2015/2016 750 450 1,050 5,250 18 66 720 1.5 3.6 12

2016/2017 2,400 - - 3,600 - - 540 - - 9.0

33

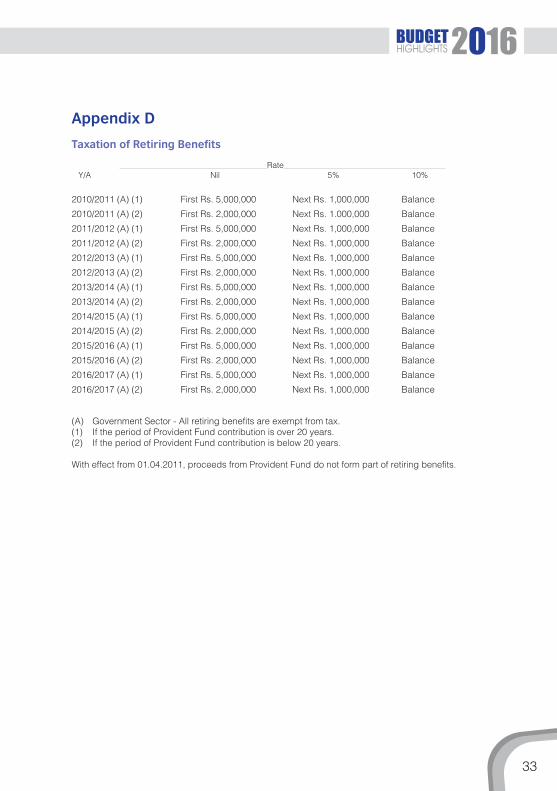

Appendix D

TaxationofRetiringBenefits

Rate Y/A Nil 5% 10%

2010/2011 (A) (1) First Rs. 5,000,000 Next Rs. 1,000,000 Balance

2010/2011 (A) (2) First Rs. 2,000,000 Next Rs. 1.000,000 Balance

2011/2012 (A) (1) First Rs. 5,000,000 Next Rs. 1,000,000 Balance

2011/2012 (A) (2) First Rs. 2,000,000 Next Rs. 1,000,000 Balance

2012/2013 (A) (1) First Rs. 5,000,000 Next Rs. 1,000,000 Balance

2012/2013 (A) (2) First Rs. 2,000,000 Next Rs. 1,000,000 Balance

2013/2014 (A) (1) First Rs. 5,000,000 Next Rs. 1,000,000 Balance

2013/2014 (A) (2) First Rs. 2,000,000 Next Rs. 1,000,000 Balance

2014/2015 (A) (1) First Rs. 5,000,000 Next Rs. 1,000,000 Balance

2014/2015 (A) (2) First Rs. 2,000,000 Next Rs. 1,000,000 Balance

2015/2016 (A) (1) First Rs. 5,000,000 Next Rs. 1,000,000 Balance

2015/2016 (A) (2) First Rs. 2,000,000 Next Rs. 1,000,000 Balance

2016/2017 (A) (1) First Rs. 5,000,000 Next Rs. 1,000,000 Balance

2016/2017 (A) (2) First Rs. 2,000,000 Next Rs. 1,000,000 Balance

(A) Government Sector - All retiring benefits are exempt from tax.(1) If the period of Provident Fund contribution is over 20 years.(2) If the period of Provident Fund contribution is below 20 years.

With effect from 01.04.2011, proceeds from Provident Fund do not form part of retiring benefits.

35

ABOUT SJMS ASSOCIATES

SJMS Associates is a multi-disciplinary professional services firm providing audit & assurance, business solutions, tax services, management consulting, financial advisory services and corporate risk services to a wide range of clients. SJMS Associates is an independent correspondent firm to Deloitte Touche Tohmatsu, a global leader in professional services with over 180,000 people in 150 countries / locations.

Our practice is one of the top accounting and auditing firms in Sri Lanka, with eleven partners and 350 staff. Our clients operate in diverse industries such as advertising, apparel, retail, financial services, manufacturing to hospitality and leisure. The firm has over 38 years presence in Sri Lanka and has been associated with Deloitte Touche Tohmatsu since 1997.

Our services portfolio:

Audit & Assurance Tax Compliance & Advisory

· Financial Assurance · Corporate Tax Compliance · Review Engagements · VAT compliance and advisory· Forensic Services · Expatriate Tax Consulting · Due Diligence · International Taxation · M & A Tax · Tax Management Advisory · Transfer Pricing Business Solutions Financial Advisory Services

· Outsourced Accounting Services Corporate Finance · Payroll & H.R.· Business process outsourcing · Mergers and Acquisitions· Company formation · Corporate Finance & Private Capital · Transaction Execution · Valuations

Management Consulting Restructure & Corporate Recovery

· General Management Consulting · Restructuring / Reorganization· Business Strategy Consulting · Corporate Closure Management· Foreign Investment Services · Liquidation Services

Corporate Risk Services

· Corporate Governance Advisory· Risk Management · Internal Audit· Information Systems Audit

36

Contacts

SJMS Associates

11 Castle Lane Tel. + 94 11 5444400 / 5444408/09 [email protected]

Colombo 04. Fax. + 94 11 2586068

Ms. S. Y. Kodagoda Tel. +94 11 5444400

(Ext. 102)/ 5444410 (D) [email protected]

Mr. P. Sivasubramaniam Tel. + 94 11 5444400

(Ext. 104)/ 5444408/09

Mr. T. Gobalasingham Tel. + 94 11 5444400

(Ext. 105 )5444408/09

Mr. M. C. Ratnayake Tel. + 94 11 5444400

(Ext. 106)/ 5444408/09 [email protected]

Ms. L. Fernando Tel. + 94 11 5444400

(Ext. 107 )/ 5444408/09 [email protected]

Ms. D. Dahanayake Tel. + 94 11 5444400

(Ext. 108) /5444408/09 [email protected]

Mr. D. Wakishta Tel. + 94 11 5444400

(Ext. 110)/ 5444408/09 [email protected]

Ms. G. Perera Tel. + 94 11 5444400

(Ext. 111)/ 5444408/09 [email protected]

BranchSJMS Associates Kandy Tel. + 94 081 2228684

or 5628649

25/1/1

George E. de Silva

Mawatha

Kandy Fax. +94 081 2203071

Mr. R. Rajendran [email protected]

Mr. Viraj Saman Kumara [email protected]

Prin

ted

by C

eylo

n Pr

inte

rs P

LC

![Gripper Side SJMS Budget Cover Randika [15 10 14] … · · 2014-11-23Gripper Side SJMS Budget Cover Randika [15_10_14 ... Budget Highlights 2015 2. VALUE ADDED TAX (VAT) 2.1 RATES](https://img.dokumen.tips/doc/110x75/5afcd5497f8b9a444f8ca1c5/gripper-side-sjms-budget-cover-randika-15-10-14-2014-11-23gripper-side-sjms.jpg)