Embed Size (px)

Citation preview

1.0 INTRODUCTION

A study of inventory management at SARK CABLES LTD is undertaken inorder to

know the inventory performance and position of the company and to know the strength and

weakness and to assess the profitability of the company. Inventories constitute most significant

part of assets of large majority of the companies in India. Inventory a double edged sword is

usually an asset of an organization, if not used properly it will become liability. It is therefore

absolutely important to manage inventories efficiently and effectively in order to overcome

unnecessary investment.

Improper inventory management affects long term profitability and may fail ultimately.

10 to 20% of inventory can be reduced without any adverse effect on production and sales by

using simple inventory planning and control techniques

The scope of inventory management concerns the fine lines between replenishment lead

time, carrying costs of inventory, asset management, inventory forecasting, inventory valuation,

inventory visibility, future inventory price forecasting, physical inventory, available physical

space for inventory, quality management, replenishment, returns and defective goods, and

demand forecasting. Balancing these competing requirements leads to optimal inventory levels,

which is an on-going process as the business needs shift and react to the wider environment.

Inventory management involves a retailer seeking to acquire and maintain a proper

merchandise assortment while ordering, shipping, handling, and related costs are kept in check.

It also involves systems and processes that identify inventory requirements, set targets, provide

replenishment techniques, report actual and projected inventory status and handle all functions

related to the tracking and management of material. This would include the monitoring of

material moved into and out of stockroom locations and the reconciling of the inventory

balances. It also may include ABC analysis, lot tracking, cycle counting support, etc.

Management of the inventories, with the primary objective of determining/controlling stock

1

levels within the physical distribution system, functions to balance the need for product

availability against the need for minimizing stock holding and handling costs.

1.1 COMPANY PROFILE

SARK CABLES PVT.LTD. the only one company of its kind in Kerala promoted over a

decade ago in manufacturing various cables as per Indian/International specifications. They

commenced its production in 1996, December at new industrial development area (NIDA),

Kanjikode , Palakkad District, Kerala as a small scale industrial unit with permanent SSI

registration number 090711939, they are also registered with NSIC vide registration number,

NSIC/KER/UP/RS/8-53/99. As well as SISI vide KSX registration number KSX/1357/G9 date

5/4/1999.c

The company is catering to the needs of public sector undertaking OEMS in INDIA and

also executed import substitute requirement as well as very stringent applications like cable for

the rocket launching purposes under water communications etc

The company is managed by a board of directors consisting of 6 persons out of whom

Mr. K Sajeev Kumar is the Managing Director and Mr. Sunil Joseph, Director (Technical

Services) take care of the day today management of the company. the company has a prestigious

ISI certificate it has got ISO 9001-2000 certification on 2004.

The company has started second unit in Coimbatore which went into production from 1st

October 2008. The company has another associate unit in Thodupuzha , namely COCHIN

POWER CABLES PVT.LTD, which also produces power cable

SARK CABLES is mainly producing the wires and cables for industrial purpose like

heavy duty power cables, control cables, telephone cables, switch board cables, co-axial cables

as per the requirement of the customers.

The company has won many laurels, best entrepreneur by the department of industries

and commerce (1998 and 1999) and best entrepreneur by the Management Association and

2

Business Deepika. The mission statement of the company is to provide beneficial and innovative

product in time to the customers at competitive prices that represent the high value for the money

in the industry. The company is holding BSI license for manufacturing heavy duty underground

cables as per IS 1554/1 under license number CM/L6180765 and also light duty cables as per IS

694/1990 license number CM/L6148062. The company was awarded the prestigious ISO 9001-

2000 certificate by Phoenix Certification Private Limited who are associated by RVA

SARK CABLES also holding approvals from PWD for using their cables for government

works, vide their approval letter number EL2050898 and M/s Kerala State Electricity board vide

letter number CE.SSTLC/REC/SKDA approval 2001-02/389 dated 09.05.2001 they are

approved vendor with M/s. Cochin Refineries Limited (code number 524135) M/s. Hindustan

news print Limited (code number 51023), M/s. BHEL (code number 29766P), M/s. Kerala

Minerals and Limited (code number 50025) etc.

It won’t be out of place to mention here that SARK CABLES have been satisfactorily

working at various sites inside and outside Kerala and they have received performance certificate

from M/s. Keltron, M/s. Malabar Cements Limited, M/s. Kerala State Electricity Board etc.

1.1.1MISSION OF THE COMPANY

The mission statement of the company is providing beneficial and innovative product in

time to the customers at competitive prices that represent the high value for money in the

industry.

1.1.2VISION OF THE COMPANY

The vision of the company is to make it a leading player in the field and to compete with

leading, in another two years time. It also aims to give more importance in keeping up the quality

of their products.

As it is, the company is in the SSI sector. Company is undergoing an expansion program

and a second unit of the company has already started functioning, augmenting the manufacturing

and supply efficiently.

3

1.1.3LOCATION OF THE COMPANY

The company is situated in New Industrial Development Area at Kanjikode in Palakkad

District. It is located near Kerala Tamilnadu boarder.

1.1.4CAPACITY OF THE PLANT

The plant has a capacity to manufacture 8600 core kilometers of various cables per

month.

1.1.5OBJECTIVE OF THE COMPANY

The company was incorporated with the intention of manufacturing and marketing

different kind of cables and wires. The main objective of the company is to supply different

types of cables and wires according to the requirement of the customers.

1.1.6WORK FORCE OF THE SARK CABLES

SARK CABLES has around 60 employees. They have 3 shifts in a day. The shifts start

from morning 8.30 am. First shift is the general shift. In this shift on an average 45 employees

are working it is from 8.30 am to 4.30 pm. Second shift is from 4.30 pm to 12.30 am. In this shift

around 10 employees are working. The final shift is the night shift and is from 12.30 am to 8.30

am in this shift 5 employees are working.

The company is stocking the final product in the factorial godown. The finished goods

are moved out of the company within 15 days. The raw materials are also kept the company. The

company has well experienced technicians for the different manufacturing process. There is a

manager for production and he controls all the production process.

1.1.7DEPARTMENTS OF SARK CABLE

Purchase department

Marketing department

Human resource department

Account department

Production department

4

1.1.8PRODUCT

Sark Cables Pvt Ltd was incorporated for manufacturing and marketing cables and wires.

The main products of Sark Cables are;

Power and control cables up to 1100 volts

Single core flexible cables

Multi core flexible cables

Submersible or water proof cables

Weather proof service wire

Single core flexible flame retardant (fr) PVC wires cables.

Telephone and switch board cables

Recommended cables size for motors with star-delta and dol started

1.2STATEMENT OF PROBLEM

In many organizations inventory forms the largest single expenditure item. Efficient

management of inventory is considered to be one of the challenging problems of any

manufacturing unit. Studies made by various researches indicate that the inventories account for

nearly 60 per cent of production cost. The company is trying to improve the overall efficiency

and effectiveness of its functions and now introduce a system in inventory management.

Inventory Management is the most challenging task for the management.

Emphasized the need to maintain inventories to smoothen production and sales

operations, which is for the day-to-day use. Holding of inventories is necessary to protect against

the risk of unpredictable changes in the market. There is a speculative element which influences

the decision to increase or decrease Inventory levels to take advantage of price change. It is

therefore absolutely very important to manage inventories efficiently and effectively in order to

overcome unnecessary investment. Major problems faced by Sark cables are

No proper inventory control techniques in use

Raw materials are not categorized

Production cost and holding cost are high

5

1.3OBJECTIVE OF THE STUDY

The main objectives of the study are:-

To determine the stock level of each raw materials at SARK CABLES PVT.LTD for

proper identification of inventory control techniques.

To identify problems related to inventory management and to find out suitable measures

to overcome them.

To study how ABC analysis need to be implement in inventory management at SARK

CABLES PVT.LTD

1.4RESEARCH METHODOLOGY

The basic concept of research methodology refers to the way in which companies

conduct their research and how they collect the data they need. Whenever a company or

organization needs to investigate a particular area of their business dealings, they need to adapt

the most suitable research methodology for the job. The method adopted for the study is

secondary data analysis which provided by the SARK CABLES Pvt. Ltd. Details regarding the

purchase procedures are provided from the materials department and sales details are obtained by

discussions made with the personnel who are involved in the sales department.

1.4.1 PERIOD OF STUDY:

The period of the study for the project is for 21 days.

1.4.2 METHODOLOGY OF DATA COLLECTION

a) Primary data

The primary data is collected by personal interviews with officials.

b) Secondary data

Data are those which have been collected by someone else and which already

have been passed through statistical process. Secondary data has been taken from internet,

newspaper, magazines and companies web sites.

6

c) Field work

This was under taken individually to collect various information regarding the study by

visiting following sections.

Stores department

Information regarding stocking of materials receipts and issues to workshops. Inventory

control procedures in various wards inside the department were obtained.

Accounts department

Remaining all the information was obtained from accounts department through personal

interviews with section officials

7

2.0 INVENTORY MANAGEMENT

Inventory management is the process of efficiently overseeing the constant flow of units

into and out of an existing inventory. This process usually involves controlling the transfer in of

units in order to prevent the inventory from becoming too high, or dwindling to levels that could

put the operation of the company into jeopardy. Competent inventory management also seeks to

control the costs associated with the inventory, both from the perspective of the total value of the

goods included and the tax burden generated by the cumulative value of the inventory. (N G

Nair1996)1

2.1 INVENTORY

Inventory is an idle stock of physical goods that contain economic value, and are held in

various forms by an organization in its custody awaiting packing, processing, transformation, use

or sale in a future point of time. (N G Nair1996)1

Any organization which is into production, trading, sale and service of a product will

necessarily hold stock of various physical resources to aid in future consumption and sale. While

inventory is a necessary evil of any such business, it may be noted that the organizations hold

inventories for various reasons, which include speculative purposes, functional purposes,

physical necessities etc. (N G Nair1996)1

Inventory of materials occurs at various stages and departments of an organization. A

manufacturing organization holds inventory of raw materials and consumables required for

production. It also holds inventory of semi-finished goods at various stages in the plant with

various departments. Finished goods inventory is held at plant, FG Stores, distribution centers

etc. Further both raw materials and finished goods those that are in transit at various locations

also form a part of inventory depending upon who owns the inventory at the particular juncture.

Finished goods inventory is held by the organization at various stocking points or with dealers

and stockiest until it reaches the market and end customers. (N G Nair1996)1

Besides Raw materials and finished goods, organizations also hold inventories of spare

parts to service the products. Defective products, defective parts and scrap also form a part of

8

inventory as long as these items are inventoried in the books of the company and have economic

value. (Bhattacharyaet al. 2001)6

2.2 OBJECTIVE OF INVENTORY CONTROL TECHNIQUES

To keep inventory at sufficiently high level to perform production and sales activities

smoothly.

To minimize investment in inventory at minimum level to maximize profitability.

To ensure that the supply of raw material & finished goods will remain continuous so that

production process is not halted and demands of customers are duly met.

To minimize carrying cost of inventory.

To keep investment in inventory at optimum level.

To reduce the losses of theft, obsolescence & wastage etc.

To makes arrangement for sale of slow moving items.

To minimize inventory ordering cost

9

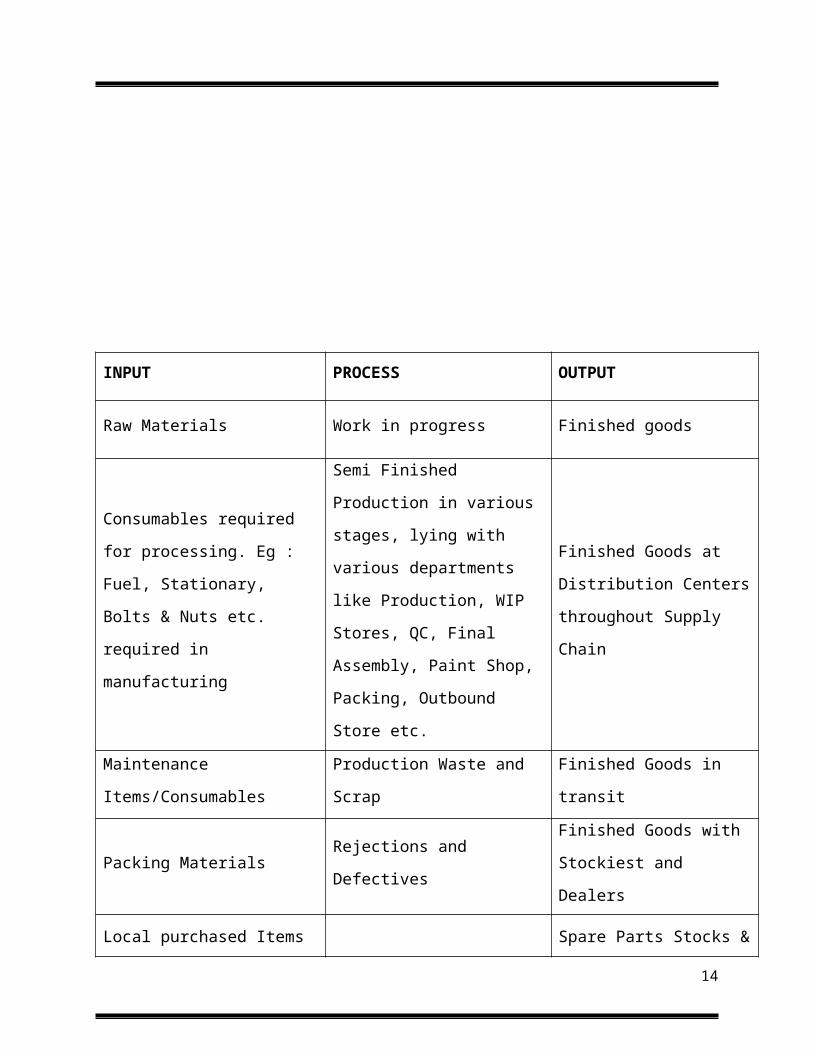

INPUT PROCESS OUTPUT

Raw Materials Work in progress Finished goods

Consumables required for

processing. Eg : Fuel, Stationary,

Bolts & Nuts etc. required in

manufacturing

Semi Finished Production in

various stages, lying with

various departments like

Production, WIP Stores, QC,

Final Assembly, Paint Shop,

Packing, Outbound Store etc.

Finished Goods at

Distribution Centers

throughout Supply Chain

Maintenance Items/Consumables Production Waste and Scrap Finished Goods in transit

Packing Materials Rejections and DefectivesFinished Goods with

Stockiest and Dealers

Local purchased Items required

for production

Spare Parts Stocks & Bought

Out items

Defectives, Rejects and Sales

Returns

Repaired Stock and Parts

Sales Promotion& Sample

Stocks

TABLE2.1 TYPE OF INVENTORY BY FUNCTIONS

(Cohen and Ernst (1988)8

10

2.3 THE ADVANTAGES OF INVENTORY MANAGEMENT SYSTEM

Supply and Demand

Having an adequate supply of a particular product to meet customer demand is crucial to

both sales increases and customer service. If a customer comes to a business to purchase a

product and it is out of stock, the sale is lost forever and the customer will probably go to a

competitor to find what they need. A good inventory management system, whether computerized

or manual, will identify sales trends and prepare for customer needs. (Flores and Whybark

1986)7.

Streamline Operations

Manufacturing facilities should always maintain proper inventory of the supplies

necessary to produce their products. If one component is missing from the inventory, the whole

production process is interrupted. Streamlined operations are an important benefit of an effective

inventory management system.(FloresandWhybark1986)7.

Lead Time Adjustments

Inventory management systems are important for determining when to order certain

items, especially for products with varying lead times. Some products take longer to receive from

the manufacturer than others, and it’s important to have an inventory management system that

accounts for lead time. If for example, a grocery store was going to have a sale on hotdogs, relish

and mustard, but the hotdogs took longer than three days to receive while the condiments took

five days; the inventory management system would need to ensure that all items were in stock in

time for the sale. (Flores and Whybark 1986)7.

Reduce Liabilities

Another significant advantage to an inventory management system is it reduces the

liabilities and loss created by overstock. Similar to monitoring supply and demand, a good

inventory management system will notice declines in sales or identify one-time occurrences to

prevent over-ordering certain products. For instance, if a clothing store was having a sale on a

certain style of jeans; it may order additional stock to meet customer demands. The inventory

management system should take the sale into account before ordering more of the jeans based on

11

the spike in sales. Otherwise, they store may have to offer even deeper discounts to get rid of the

excess inventory. (Flores and Whybark 1986)7.

Labor Cost

Well-defined inventory control policies can reduce the labor costs associated with

managing the inventory. Each time inventory gets handled, whether to move it from one location

to another, to retrieve it for order picking or to put it away for storage, it involves labor. This

handling makes up part of the cost associated with managing inventory. Companies prefer to

handle the inventory as little as possible. When a company constantly searches for lost inventory,

moves inventory from one location to another because of poor space utilization or handle the

inventory multiple times; it results in increased labor costs. Properly managed inventory reduces

these incidents and reduces the labor cost associated with the inventory. (William J

Stevenson2009)3

Inventory Costs

Lower inventory cost is a definite advantage for the company that effectively controls its

inventory. Business owners need to fully understand the costs of carrying inventory, not just how

much the inventory costs to purchase. Inventory carrying costs consist of all the expenses a

company incurs for owning inventory. These expenses include the cost of capital, storage and

risks costs (including obsolescence, damage, theft and deterioration) plus the appropriate taxable

amounts. Effective inventory control reduces these costs because it reduces the total amount of

inventory required to manage the business. Inventory control monitors the level of inventory and

proactively manages obsolescence and deterioration by ordering in the appropriate quantities.

Effective inventory control also reduces storage costs, because it orders enough inventories to fill

consumer demand and not much more. (William J Stevenson2009)3

2.4 INVENTORY CONTROL TECHNIQUES

Some of the techniques which will follow include methods of fixing purchase quantities,

setting of order points and safety stocks. The decisions as to which item to make when and to

keep inventories in balance requires application of wide range of techniques from simple

graphical methods to more sophisticate and complex quantitative techniques. Many of these

techniques employ concepts and tools of mathematical and statistical methods and make use

of various control theories from engineering and other fields. They are primarily aimed at

12

helping to make better decisions and getting people involved and follow a wise policy. As such,

they are far from academic exercises only. However, making decisions more intelligently and

making actions follow these decisions is not easy. Thus while these quantitative techniques have

taken much out of the decision-making managers what was being done through bunch or

intuitive judgment, real business acumen demands that these must be blended with practical

business sense. It is an axiomatic truth that these techniques alone cannot turn bad judgment into

good ones simply because they are exact. However, before focusing our attention on

such techniques, let us first attempt to analyze different types of inventories.(N G Nair1996)1

1. Determination of various levels of materials

2. Economic Order Quantity

3. ABC Analysis

4. Two Bin System

5. Fsn/Ved Analysis

2.4.1. DETERMINATION OF VARIOUS LEVELS OF MATERIALS

The store-keeper plays an important role in deciding upon the various levels materials. In

order to ensure that the optimum quantity of materials is purchased stocked neither less nor

more, the store keeper applies scientific techniques of material management. Fixing of certain

levels for each item of materials in one of techniques.

(a) Re-order Level

(b) Maximum Level

(c) Minimum Level

(d) Average Level

(e) Danger Level

13

(a) Re-order Level:

This level is that level of material at which it is necessary to initiate purchase requisition for

fresh supplies. This is normally the point lying between the maximum and the minimum levels.

Fresh orders must be placed before the actual stocks touch the minimum level.

This level is fixed in such a manner that the quantity of materials represented by the

difference between the re-order level and the minimum level will be sufficient to meet the

requirement of production till such time as the order materializes and materials are delivered.

The following factors are taken into account for fixing the Re-order level:

(i) Rate of consumption of material

(ii) Lead time, i.e., time required to receive the delivery of fresh purchase.

(iii) Re-order quantity

(iv) Minimum level

Re-order level can be calculated by applying the following formula:

Re-order level = Minimum level + consumption during period required to get fresh delivery

(b) Maximum Level:

The maximum level is that level of stock which can be held at any time. In other words, it is

the level beyond which stock should not be maintained. The purpose is to avoid over-stocking

and thereby using working capital in a proper way. This level is fixed after taking into account

the following factors:

(i) Rate of consumption

(ii) Lead time

(iii) Availability of capital

(iv) Storage capacity

(v) Cost of maintaining stores including insurance cost

14

(vi) Nature of commodity

(vii) Possibility of price fluctuation

(viii) Possibility of change in fashion, habit, etc.

(ix) Restrictions imposed by Govt., local authority or trade associations

(x) Re-order level it

(xi) Re-order quantity

Maximum level can be calculated by applying the following formula:

Maximum Level = Re-order level + Re-order Quantity - (Minimum consumption x Minimum

Re-order period)

(c) Minimum Level:

This is the level below which the stock of an item should not fall. This is known as safety or

buffer stock. An enterprise must maintain minimum quantity of stock so that the production is

not hampered due to non-availability of materials. This level is fixed after considering the

following factors:

(i) Re-order level

(ii) Lead time

(iii) Rate of consumption

The formula for calculating minimum level is:

Minimum level = Re-order level - (Normal consumption x Normal Re-order period)

(d) Average Level:

Average level can be calculated by applying the following formula:

Average level = Minimum level + of Re-order Quantity.

15

(e) Danger Level:

Usually stock should not be lower than the minimum level. But if for any reason, stock

comes down below the minimum level, it is called danger level. When the stock reaches danger

level, it is necessary to take urgent action on the part of the management for immediate

replenishment of stock to prevent stock-out situation. The danger level can be calculated by

applying the following formula:

Danger Level = Average consumption x Maximum Re-order period for emergency purchases

(Ray wild jan 17 2002 )2

2.4.2. ECONOMIC ORDER QUANTITY (EOQ)

The economic order quantity, known as EOQ, represents the most favorable quantity to

be ordered each time fresh orders are placed.

The quantity to be ordered is called economic order quantity because the purchase of this

size of material is most economical. It is helpful to determine in advance as to how much should

one buy when the stock level reaches the re-order level. If large quantities arc purchased, the

carrying costs would be high the other hand, if small quantities are purchased at frequent

intervals the ordering costs would be high. The economic order quantity is fixed at such a level

as to minimize the cost of ordering and carrying the stock. It is the size of the order which

produces the lowest cost of material ordered. While determining the economic order quantity, the

following three cost factors are taken into consideration:

(i) The cost of the material

(ii) The inventory carrying cost

(iii) The ordering cost

Carrying costs are the costs of holding the inventory in the stores. These are:

(i) Rent for the storage space.

(ii) Salaries and wages of the employees engaged in store keeping department.

16

(iii) Loss due to pilferage and deterioration.

(iv) Insurance charges.

(v) Stationery used in the stores.

(vi) Loss of interest on the capital locked up in materials.

Ordering costs are the costs of placing orders for the purchase of materials. These are:

(i) Salaries and wages of the employees engaged in purchasing department.

(ii) Stationary, postage, telephone expenses, etc. of the purchasing department.

(iii) Depreciation on equipments and furniture used by the purchasing department.

(iv) Rent for the space used by the purchasing department.

While placing orders for purchasing materials, the total cost to be incurred is kept in

view. As discussed earlier, if an order is placed for a large quantity at a time, the ordering cost is

less but the carrying cost would be more.(Ray wild jan 17 2002 )2

2.4.3. ABC ANALYSIS

This technique of inventory control is also known as Always Better Control technique.

ABC analysis is an analytical method of control which aims at concentrating efforts on those

areas where attention is needed most.

This is a principle of selective control. The emphasis of ABC analysis technique is that

the management should concentrate its energy in controlling those items that mostly affect the

organizational objects. Manufacturing concerns find it useful to group the materials into three

classes on the basis of investment involved.

Materials having higher values but constitute small percentage of total items, are

grouped in 'A' category. On the other hand, a large percentage of items of materials which

represent a smaller percentage of the values, are grouped in 'C' category. Items of materials

17

having moderate value 'and moderate size are grouped in 'B' category. On the basis of physical

quantities and value of arterials used, the following table illustrates the above classification:

After the items of materials are classified into A, B and C category, control can be

exercised in a selective manner as follows:

(i) Greater care and strict control should be exercised on the items of category 'A' as any loss or

breakage or wastage of any item of this category many prove to be very costly. Economic order

quantity and re-order level should be carefully fixed for such category of items.

(ii) Moderate and relaxed control is required for the items of category 'B'.

(iii) There is not much need for exercising control over the items of category 'C' Periodic or

annual verification is required for this category of materials (William J Stevenson2009)3

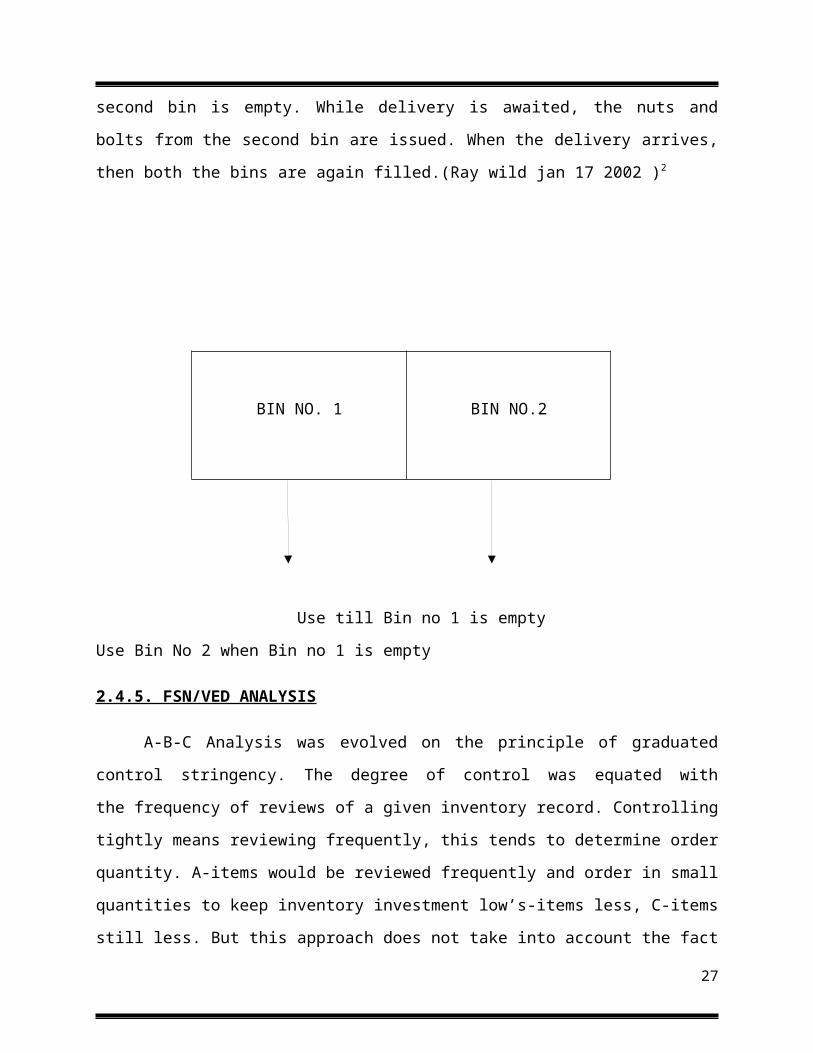

2.4.4. TWO BIN SYSTEM

One of the earliest systems of stock control is two-bin system, which is a simple method

of control exercised by two simple rules. One is when the order should be placed, and the other is

what quantity should be covered. The following diagram shows this simple method. The bins

contain, say, mild-steel bolts and nuts. The bolts and nuts are issued from the first bin as and

when required, and as soon as the first bin is empty, more bolts and nuts are ordered. The

replenishment arrives just when the second bin is empty. While delivery is awaited, the nuts and

bolts from the second bin are issued. When the delivery arrives, then both the bins are again

filled.(Ray wild jan 17 2002 )2

18

BIN NO. 1 BIN NO.2

Use till Bin no 1 is empty Use Bin No 2 when Bin no 1 is empty

2.4.5. FSN/VED ANALYSIS

A-B-C Analysis was evolved on the principle of graduated control stringency. The degree

of control was equated with the frequency of reviews of a given inventory record. Controlling

tightly means reviewing frequently, this tends to determine order quantity. A-items would be

reviewed frequently and order in small quantities to keep inventory investment low’s-items less,

C-items still less. But this approach does not take into account the fact that sometimes a low-

valued small item of critical nature needs as much attention as high-valued A-class item, so that

inventories also need to be classified according to Vital, Essential and Desirable (V -E-D), which

in essence means that stress is more on importance rather than on value.

Again, inventories may also be classified according to Fast-moving, Slow-moving and

Non-moving items in order to see the rapidity of their use and to weed out the unnecessary ones.

This is aimed at keeping the total inventory size down and reduces investment. Thus, selective

control may be exerted under different types of classification according to necessity. A single-

type approach may not prove fruitful under al circumstances. (William J Stevenson2009)3

2.4.6. ORDER CYCLING SYSTEM

This system is based upon a review timetable. According to this system, a review of the

entire inventory is done at regular intervals, such as 30 days, 60 days or 90 days. After the

review is done, the cost accountant views stock items with low quantities that will not last up to

the next review interval. The purchase order for such a stock item is placed immediately. The

19

order cycling system is not exactly foolproof and one requires a rather experienced cost

accountant to efficiently conduct it. (N G Nair1996)1

2.5 FUNCTIONAL DETAILS OF STORES AND PURCHASE

AT SARK CABLES

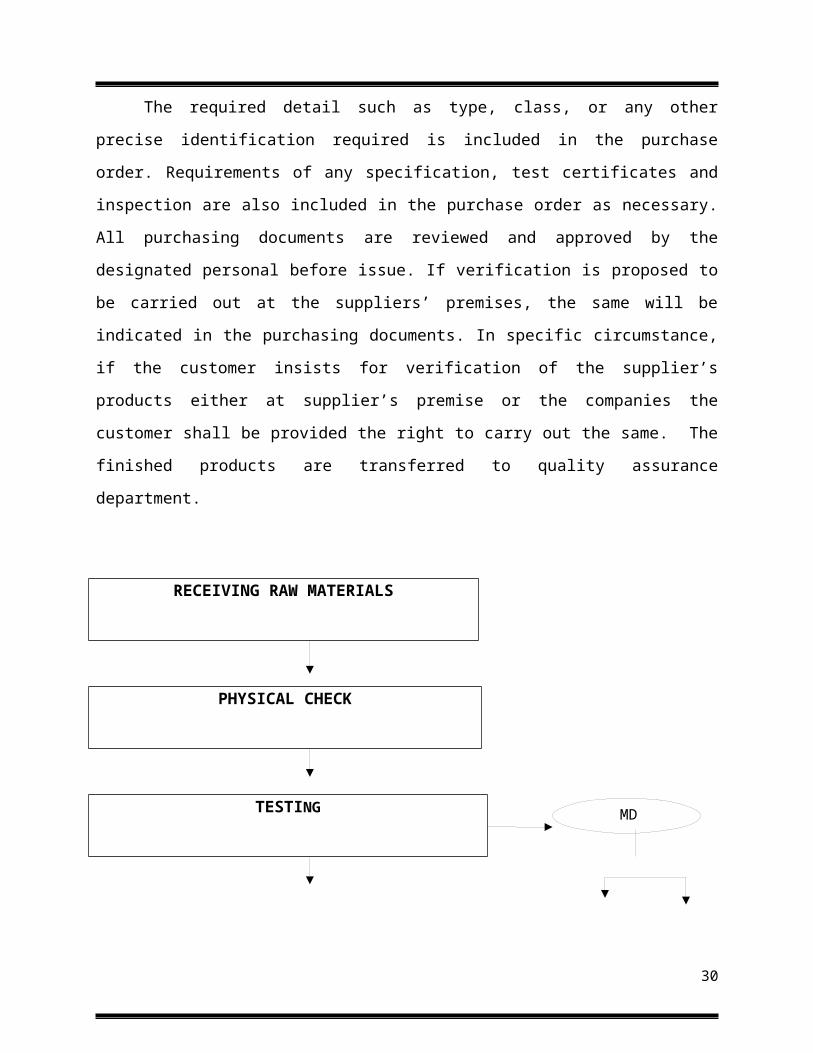

Production department receives the customer order vide through marketing department

and the same is recorded in the order register SARK/PDD/ORG/001. According to the orders

production department forwards raw material requisition slip to stores for issuing raw materials.

Purchase department purchase raw materials from different suppliers. Hindalco Industries

Ltd, Paras Wires Pvt Ltd, Grand Engineering Industries, Maddras Aluminum company Ltd,

Barath Aluminum company Ltd, Modern Engineering works, Tata SSL Ltd, Balaji wires Pvt Ltd,

Farcom cables system Pvt Ltd, SCJ plastic Ltd. Etc. all the suppliers are evaluated and selected

based on their ability to meet sub contract requirements including the requirement of quality

system and the company’s specific requirements. All the suppliers as on 1 March 2003 are

included in the list of approved suppliers.

HOD Stores and Purchase maintains a list of suppliers. The control exercised on the

suppliers is mainly based on the evidence of conformity furnished by the supplier and it varies

depending on the product, impact on the quality of the final product, and previously

demonstrated capability and performance of suppliers. Purchase orders released by the company

will indicate any specific requirements decided to be included to exercise control over the

suppliers. Purchases are made based on the purchase order released by the company.

The required detail such as type, class, or any other precise identification required is

included in the purchase order. Requirements of any specification, test certificates and inspection

are also included in the purchase order as necessary. All purchasing documents are reviewed and

approved by the designated personal before issue. If verification is proposed to be carried out at

the suppliers’ premises, the same will be indicated in the purchasing documents. In specific

circumstance, if the customer insists for verification of the supplier’s products either at supplier’s

20

premise or the companies the customer shall be provided the right to carry out the same. The

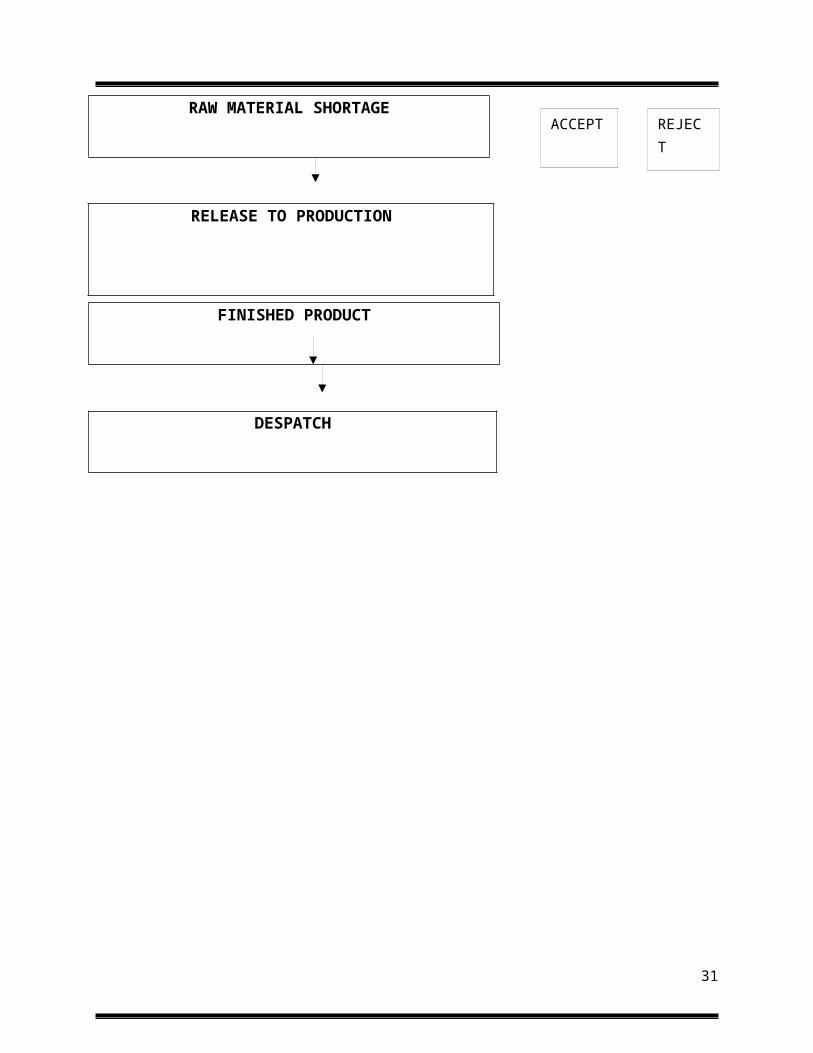

finished products are transferred to quality assurance department.

RECEIVING RAW MATERIALS

PHYSICAL CHECK

TESTING

RAW MATERIAL SHORTAGE

FINISHED PRODUCT

DESPATCH

21

MD

ACCEPT REJECT

RELEASE TO PRODUCTION

2.6 RAW MATERIALSAT SARK CABLES

2.6.1CABLES:-

Copper, aluminum, PVC etc are the main raw material of the firm. Purchase from

different customers. There are variety of papers are used in press for the needs of the users.

These all different quality papers and the rate also differ from one to other. From paper printing

we get variety of products for various purposes (company manual)

In case of PVC granules for insulation and sheath, received vide goods received note

SARK/SPD/GRN/001 are inspected by Quality Assurance Department as per the quality plan

and the observations are recorded in the raw material test register.(company manual)

After the inspection, the approval/rejection is indicated in the GRN/DN and sent back to

stores for further action.

The materials which meet the specified requirements are released to production for

further process. The materials which do not meet the specified requirements are put under

“HOLD” and recorded in non conformance register.

2.6.2 WORK IN PROGRESS AT SARK CABLES

In process inspection is carried out by the QA inspector supervisor as per the quality plan

and the observations are recorded in the route work order. The materials meeting the specified

requirements are released to next process. Such materials are identified by QA approved seal.

The materials which do not meet the specified requirements are put under hold.

2.6.3 FINISED PRODUCT AT SARK CABLES

The materials which meet the specified requirements are released for packaging.

Materials which do not meet the specified requirements are put under “hold” and recorded in non

conforming register.

22

2.7STORE DEPARTMENT PROCEDURE

Stores receives materials vide good received note (GRN) SARK/SPD/GRN/001 or

delivery note (DN), SARK/SPD/DN/002 and kept in raw material storage area. After verifying

the quantity and packaging of the materials, then GRN/DN are forward to QA department for

their information and approval. After QA approval the materials are identified by QA approved

tags. Materials put under Hold by QAD are segregated and kept in the NCR allocated area. The

materials are issued to production for further process by stores according to the raw material

requisition slip SARK/SPD/003, issued by production department. The minimum quantity of row

material is stored according to the minimum stock level SARK/SPD/004.Receipt and issues of

raw materials are recorded in raw material stock register SARK/SPD/RSR/005.Purchase indent,

SARK/SPD/PI/006, is forwarded to administration department for purchasing the required raw

materials. Finished products, received vide finished good transfer slip, SARK/PDD/FGT/004,

from QAD are duly packed and kept in the finished good storage area with proper identification.

Finished products are dispatched to the customers as per the invoice issued by the marketing

department. Receipt and issue of finished goods are recorded in finished product register

SARK/SPD/FPR/007. Inventory of raw material and finished goods are made once in a year. All

raw material suppliers are evaluated on the basis of the quality, quantity, delivery time and price

of the material (Company manual)

2.8 ABC INVENTORY CONTROLING TECHNIQUE AT SARK

CABLES

ABC analysis is meant for relative inventory control in which maximum attention can be

given to items which consume more money and a fair attention can be given to median value

items. The attention for low value can be reducing to routine procedure only. If all the store

items of an undertaking are analyzed in terms of annual consumption of each item in rupees, it

will be found that;

5-10 per cent of total annual consumption is only required and its value amount to 70 per

cent of the total inventory value. These items are stored in ‘A’ category in which

handling of these items should be in care and control.

23

15-20 per cent of total annual consumption is required in the total process and its value

also amount to 20 per cent of the total inventory value. These are controlled and card but

not as seen in ‘A’ category.

75-80 per cent of total annual consumption comes under this and its value pertains to 10

per cent of the total inventory value and less care is given to these types which are

classified as ‘C’ category.

Item classified according to the book value of the item stores is custodian every items.

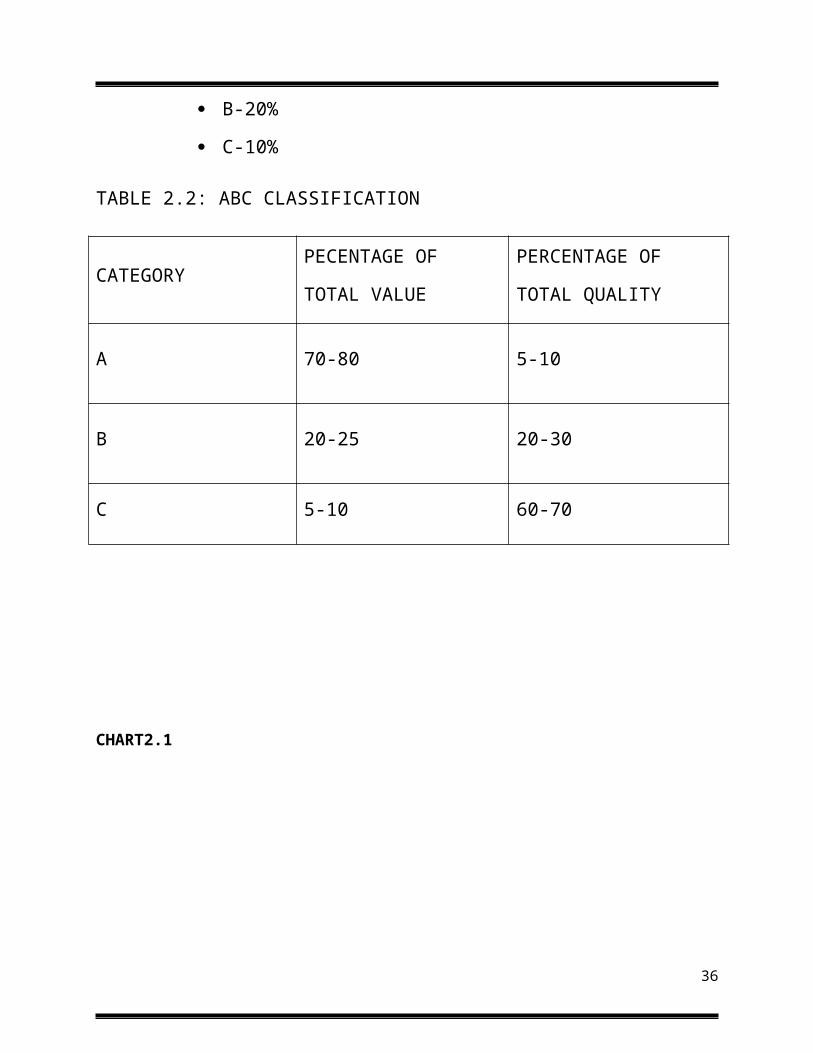

Break up of ABC:

A-70%

B-20%

C-10%

TABLE 2.2: ABC CLASSIFICATION

CATEGORYPECENTAGE OF

TOTAL VALUE

PERCENTAGE OF

TOTAL QUALITY

A 70-80 5-10

B 20-25 20-30

C 5-10 60-70

24

CHART2.1

71%

21%7%

PECENTAGE OF TOTAL VALUE

a b C

TABLE2.3 ABC classification and importance

A item B item C item

High consumption value Moderate value Low consumption value

High control Moderate control Low control

Minimization of waste

materialControl over waste Annual review of waste

No safety stock Low safety stock High safety stock

Frequent ordering Ordering 3 times in a monthBulk ordering once in a

month

Weakly control statement Monthly control Quality control report

25

“A” items are the most critical ones. These items require tight inventory controls;

frequent review of demand forecasts and usage rates; highly accurate part data; and frequent

cycle counts to verify perpetual inventory balance accuracy. Typically, these comprise 5 – 10%

of the total item count, and represent the top 70 – 85% of the total annual dollar value of usage.

“B” items are of lesser criticality. These items require nominal inventory controls;

occasional reviews of demand forecasts and usage rates; reasonably accurate part data; and less

frequent but regular cycle counting. They typically comprise the next 15 – 25% of the total item

count and represent the next 10 – 20% of the total annual dollar value of usage.

“C” items have the least impact in terms of warehouse activity and financials, and

therefore require minimal inventory controls. In fact, depending on the nature of the items, these

may be good candidates for free bin stores. Analysis of demand forecasts and usage rates on “C”

items is sometimes waived in favor of placing infrequent orders – often in large quantities – to

maintain plenty of stock on hand. “C” items typically comprise 65 – 80% of the total item count

26

and represent the last 5 – 10% of the total annual dollar value of usage. Because of low usage,

any dead or inactive inventory will normally fall into the “C” category.(Harhalakis, G. and

Zachman1989)9

We can combine both and classify materials depending upon the both consumption value

and criticality. It will give fruitful results.

The ABC classification allows organizations to separate inventory items into three

classes, viz. A—very important, B—moderately important and C—least important. The class A

items attract management’s utmost attention. The A, B and C classification of items has

generally been based on a single criterion (Colley et al.1977)4

i.e. money value per unit multiplied by usage rate . There are other criteria that represent

important considerations for management. Lead time, consumption rate, demand, and criticality

of items) are the other considerations that may need management’s utmost attention. The

conventional ABC classification system is intended for grouping items of a manufacturing firm

according to annual sales volume. The conventional classification technique is an attempt to

identify the small number of items that will account for most of the sales volume, and that are the

most important, in order to control for effective inventory management (Arsham 2005)5

The TOPSIS model was tested using inventory data from a famous pharmaceutical

industry, Dey’s Medical, located in the heart of Kolkata, India. The results of applying this

methodology were found to be encouraging. A sample of 50 items that are required for

producing seven drugs and formulations was selected for the experimentation using the proposed

model. Five pieces of information was recorded for each sample viz. unit cost consumption rate

(kg, g, or l/day), lead time (weeks), perishability of items (years) and cost of storing the items

(INR/unit/day). The attributes of each of the multiple criteria are listed in appendix A. For the

sake of confidentiality, item numbers have been substituted for actual item names. After careful

consideration, the authors of this paper and the management of the firm decided that the five

criteria mentioned above are the most important in classifying the inventory items. Unit cost is

included as a criterion for classification. It directly affects the holding cost of the item and also

increases idle capital. The rate of consumption of the items in producing pharmaceutical products

also directly affects the ABC classification. Lead time is the time elapsed between placing an

order with a vendor and when that order arrives. In the present case study, the average lead time

27

has been taken into consideration. As the organization is a pharmaceutical industry, perishability

of items is important. Every perishable item is liable to speedy decay, thereby losing its material

value as well as the direct loss of some capital resources. Some items of the industry are more

perishable than others and need special treatment for storage. This involves a cost. The costs are

calculated from the energy consumption during storage plus the costs involved for occupied floor

space. A decision matrix is constructed using the attribute values for each item (appendix A). A

pair-wise comparison matrix is constructed based upon the information from the management of

the firm concerning the relative importance of one attribute with respect to another (taken pair-

wise). The information is sought in terms of ratios. This matrix is a matrix whose diagonal

elements are unity.(case study: Bhattacharya2001)6

28

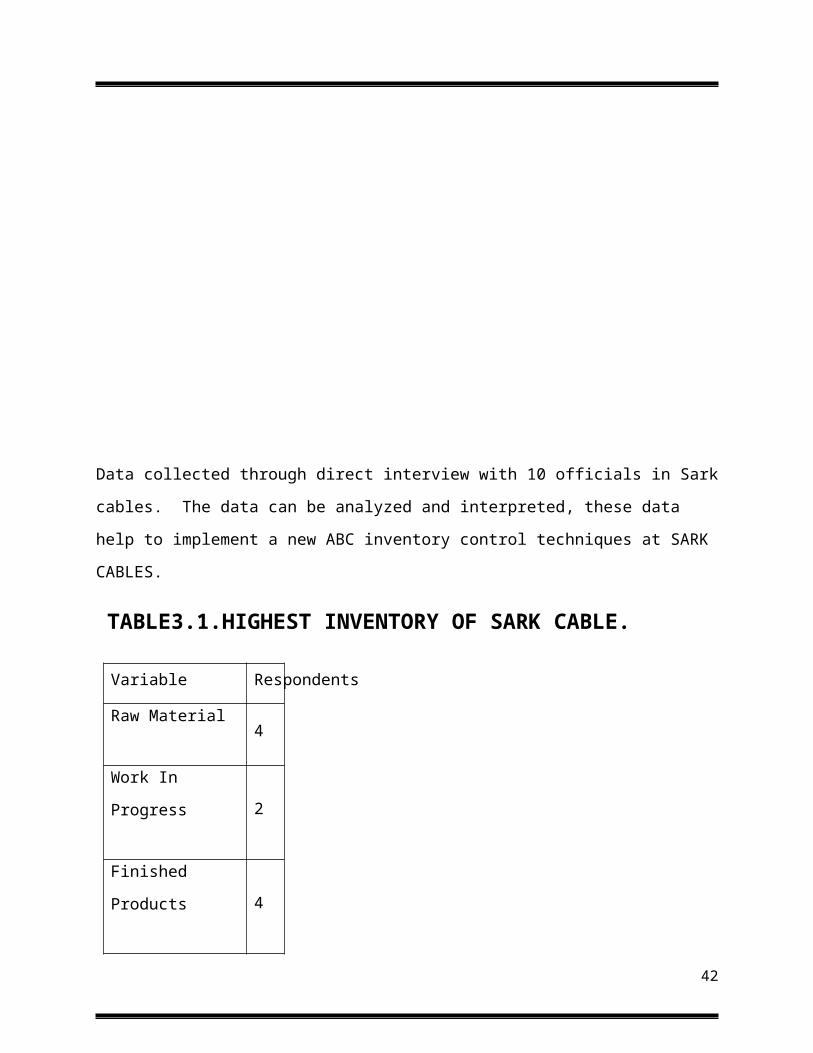

Data collected through direct interview with 10 officials in Sark cables. The data can be

analyzed and interpreted, these data help to implement a new ABC inventory control techniques

at SARK CABLES.

TABLE3.1.HIGHEST INVENTORY OF SARK CABLE.

Variable Respondents

Raw Material4

Work In Progress2

Finished Products4

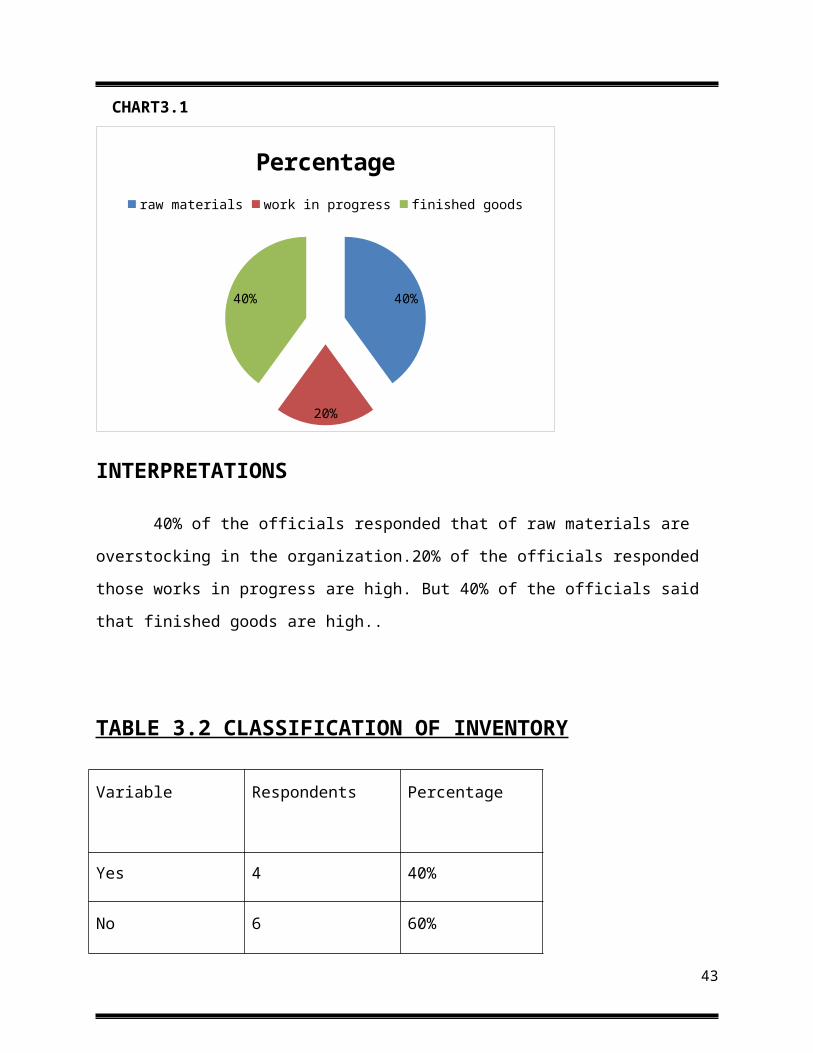

CHART3.1

40%

20%

40%

Percentage

raw materials work in progress finished goods

INTERPRETATIONS

40% of the officials responded that of raw materials are overstocking in the

organization.20% of the officials responded those works in progress are high. But 40% of the

officials said that finished goods are high..

29

TABLE 3.2 CLASSIFICATION OF INVENTORY

Variable Respondents Percentage

Yes 4 40%

No 6 60%

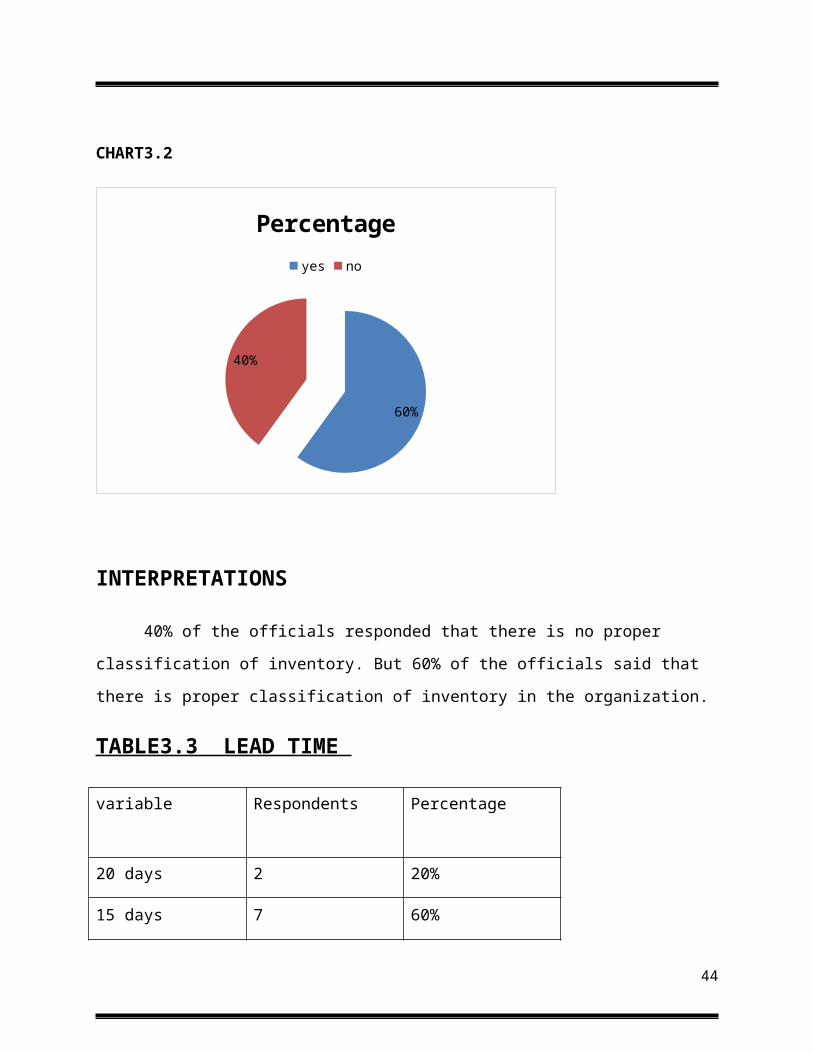

CHART3.2

60%

40%

Percentage

yes no

INTERPRETATIONS

40% of the officials responded that there is no proper classification of inventory. But

60% of the officials said that there is proper classification of inventory in the organization.

30

TABLE3.3 LEAD TIME

variable Respondents Percentage

20 days 2 20%

15 days 7 60%

10 days 1 20%

CHART3.3

60%20%

20%

Percentage

High Medium Low

INTERPRETATIONS

From the sample size 20% of them are responded that the lead time is 20 days but 60% of

then responded that 15 days are the normal lead time.

31

TABLE 3.4 DELAY OF INVENTORIES

Variable Respondents Percentage

Yes 6 60%

No 4 40%

CHART3.4

60%

40%

Percentage

yes no

INTERPRETATIONS

60% of the officials responded that the raw materials are not reaching the production department

on correct time. But 40% of them responded that raw materials are reaching on correct time.

32

TABLE 3.5 AVERAGE WASTAGE PER WEEK

Variable Respondents Percentage

High 6 60%

Medium 2 20%

Low 2 20%

CHART3.5

60%20%

20%

Percentage

High Medium Low

INTERPRETATIONS

60% of the officials responded that there is high level of wastages occurring. 20% of

them said that the average wastage per week is low.

33

TABLE 3.6 CALCULATION OF TOTAL COST OF INVENTORY

ITEMSPRICE PER UNIT

(Rs.)NO. OF UNIT

TOTAL COST(Rs)per

year

Iron 4.3 68867 296128.1

Copper 140 832 116480

Coke 17.31 246 4258.26

Lubricant 20.81 284 5910.04

Zinc 312.5 830 259375

Aluminum 3.08 2435 7499.8

Lead 480.29 987 474046.2

Plastic 2.8 4283 11992.4

INTERPRETATION

From the above table we can identify Lead having high unit price but it require only

small quantity but its total cost is very high. In the case of Iron the unit price is less than Lead but

it require large quantity so that the total cost of Iron is higher than Lead. Plastic having very less

unit price but lubricant and coke having high unit price than Plastic but total cost of the Plastic is

higher than coke and lubricant.

34

TABLE3.7 CALCULATION OF TOTAL COST IN DECLINING

ORDER

ITEMS PRICE PER UNIT

(Rs.)

NO. OF UNIT TOTAL COST(Rs)

Lead 480.29 987 474046.2

Iron 4.3 68867 296128.1

Zinc 312.5 830 259375

Copper 140 832 116480

Plastic 2.8 4283 11992.4

Aluminum 3.08 2435 7499.8

Lubricant 20.81 284 5910.04

Coke 17.31 246 4258.26

INTERPRETATION

This table is drawn on the basis of declining total cost of the inventory. Lead, Iron, zinc, copper

having high value. So we can say these inventories are very necessary for production. Lack of

these inventories affects the flow of production. Plastic have somewhat high value but Lubricant

and coke having less value of consumption.

35

CHART3.7. TOTAL COST IN DECLINING ORDER

Lead

Iron

zinc

Coppe

r

Plas

tic

Alumin

um

lubr

icant

Coke

0

50000

100000

150000

200000

250000

300000

350000

400000

450000

500000

PRICE PER UNIT (Rs.)

NO. OF UNIT

TOTAL COST(Rs)

INTERPRETATION

In this graph show that Lead, Iron, Zinc and copper have high cost and high value of

consumption. These raw materials are comes under A category because of that frequent ordering

is necessary. We want to give special attention to these materials otherwise it will affect the

production. With the help of this graph we can say Plastic is comes under B category. 'B' items

are important, but of course less important, than ‘A’ items and more important than ‘C’ items.

36

TABLE 3.8 CALCULATION OF CUMILATIVES OF

INVENTORIES

ITEMSPRICE PER

UNIT (Rs.)NO. OF UNIT

TOTAL

COST(Rs)CUMULATIVE

Lead 480.29 987 474046.23 474046.23

Iron 4.3 68867 296128.1 770174.33

Zinc 312.5 830 259375 1029549.33

Copper 140 832 116480 1146029.33

Plastic 2.8 4283 11992.4 1158021.73

Aluminum 3.08 2435 7499.8 1165521.53

lubricant 20.81 284 5910.04 1171431.57

Coke 17.31 246 4258.26 1175689.83

INTERPRETATION

Cumulative cost is the total expenditure on a task or product. From this graph we can say

the total expenditure of inventories are very high. The price of the product is depending on the

expenditure of the inventory also. So there should be a proper control over the wastage of the

inventory.

37

CHART3.8 CUMILATIVE TOTAL COST

Lead

Iron

zinc

Coppe

r

Plas

tic

Alumin

um

lubr

icant

Coke

0

200000

400000

600000

800000

1000000

1200000

PRICE PER UNIT (Rs.)

NO. OF UNIT

TOTAL COST(Rs)

cumilatives

INTERPRETATION

In this graph we can say the cumulative price of Lead is less and it is equal to total cost.

But in the case of plastic, aluminum, lubricant and coke price is very high. So when we control

the total cost of the inventory we can reduce cumulative cost. The aggregate amount that an

investment has gained or lost over time, independent of the period of time involved. Company

more likely to see a compound return than a cumulative return, as the compound return figure

will be annualized. This helps purchase department to compare different investment choices.

38

Classifying the group as A, B, and C based on the total cost

A CATEGORY

A=70% of the total cost= .70

Cumulative total*.70

1175689.83*.70= 822982.88

B CATEGORY

B=20% of the total cost= .20

Cumulative total* .20

1175689.83* .20 = 235137.96

C CATEGORY

C=10% of the total cost = .10

Cumulative total* .10

1175689.83* .10 = 117568.98

INTERPRETATION

'A' items are very important for an organization. Because of the high value of these ‘A’

items, frequent value analysis is required. In addition to that, an organization needs to choose an

appropriate order pattern (e.g. ‘Just- in- time’) to avoid excess capacity. 'B' items are important,

but of course less important, than ‘A’ items and more important than ‘C’ items. Therefore ‘B’

items are intergroup items’ are marginally important.

39

3.1ABC ANALYSIS PRIMARY STEPS AT SARK CABLES

On the bases of the above graphs and tables we implement ABC techniques at Sark

Cables. The typical ABC process isn’t overly complex and consists of a small number of steps –

you’ll usually need record the information onto a spreadsheet to simplify the analysis.

1. Gather the data

Typically ABC Analysis is reviewed by gathering, as a minimum

a) A list of part numbers from the ERP system

b) Obtaining the cost data for each part

c) Obtaining it’s consumption volume over a specific period

d) Calculating the consumption value for each part

2. Calculating the consumption value

The consumption value is calculated by multiplying the item cost by the quantity used in

the period.

3. Grouping your parts

Parts are grouped by the consumption value and typically split into 3 bands (note the

percent used here are for indicative purposes and your own organization may benefit from

different bands).

a) Band A – Material where the consumption value represents approximately 80% of the total

consumption value –this will be typically your high cost items here Lead, Copper, Zink are

comes under this category.

b) Band B – Material where the consumption value represents approximately 15% of the overall

value Plastic is comes under this category

c) Band C – Material where the consumption value represents approximately 5% of the overall

value. Lubricant and Cokes are comes under this category.

40

3.2 ABC ANALYSIS SECONDARY STEPS:

Once classified parts (and in many ERP systems you are able to populate the

classification data against the part in the parts master record). Use this data to drive key materials

management activity. For example co-coordinating your perpetual inventory management

activity – you can routinely verify your Category A parts like copper, zinc, Iron and lead on a

monthly basis but only review your category C parts; Lubricant and coke twice a year.

You can use scheduled orders for your Category C parts but may require detailed purchase

orders and negotiation for your Category A parts.

Carrying out an ABC analysis on your inventory can provide the foundation for

streamlining your materials management processes – focusing your time and effort on the parts

that need it most – ensuring that your processes are appropriately configured for the various

materials that you manage.

The ABC analysis ensures the handling and management of inventory in an effective

manner. The procedures so carried out are sufficient enough to manage the inventory. But the

system can be more efficient and cost effective if we can incorporate some other method with

ABC analysis. It can be VED Analysis, SDE Analysis, HML Analysis, and FSN Analysis. The

company will be able to manage the inventory in a more cost effective manner if they can

incorporate any of the above technique with ABC Analysis.

But choosing such a technique to incorporate should be good enough to handle the

inventory management requirement of the organization or rather say it should overcome all the

difficulties and problems. So this study suggesting a new method of inventory controlling

technique in which the SARK CABLES PVT LTD can adopt to increase the efficiency

41

TABLE 3.9 CLASSIFICATION OF INVENTORIES AT SARK

CABLES ACCORDING TO ABC TECHNIQUES

A category items B category items C category items

LEAD, IRON, ZINC,

COPPERPLASTIC

ALUMINIUM,

LUBRICANT,COKE

High consumption value Moderate value Low consumption value

High control Moderate control Low control

Minimization of waste

materialControl over waste Annual review of waste

No safety stock Low safety stock High safety stock

Frequent ordering Ordering 3 times in a monthBulk ordering once in a

month

Weakly control statement Monthly control Quality control report

Sark cables inventories are categorized into three A B and C. Lead, Iron,Zinc and copper

are comes under A category. These items have high consumption value so frequent order is

necessary otherwise it will affect the production process. Aluminum and plastics are comes

under B category it require only moderate control because moderate consumption value.

Lubricant and coke are comes under C category these items have less consumption value so low

control is enough

42

4.1 SUMMARY

Inventory management is so critical for planning or forecasting for the future needs and

for developing strategic plans to handle the market situation. It needs to a top down approach to

structure on effective way of taking inventory managing problems.

If SARK CABLE is to achieve incremental growth and maximize its market

capitalization, it has to give more emphasis on effective inventory control and use available

resource optimally.

To make it more efficient and effective this study is suggesting the system of ABC

Analysis. The data collected for this study was through direct observation and field study

conducted in the company. The other information available for this study was the company’s

records and manuals. This study gives an insight to the company’s inventory management and

helps to design a new method for improving the present system of inventory controlling.

43

4.2FINDINGS

There is no proper inventory control techniques in SARK CABLES pvt ltd

40% of the officials responded that of raw materials are overstocking in the

organization.20% of the officials responded those works in progress are high. But

40% of the officials said that finished goods are high.. (with reference to Table 3.1)

40% of the officials responded that there is no proper classification of inventory. But

60% of the officials said that there is proper classification of inventory in the

organization. (with reference to Table 3.2)

15 days are the real lead time of the inventory. (with reference to Table 3.3)

60% of inventories are not reaching in the production department on correct time due

to the lack of inventory control. (with reference to Table 3.4)

60% of the officials responded that there is high level of wastages occurring. 20% of

them said that the average wastage per week is low. (with reference to Table 3.5)

Lead, Zinc and copper having high cost (with reference to Table 3.6)

Lead, Zinc and copper are 'A' items. Frequent value analysis is required.(with

reference to Table 3.7 & chart3.7)

Plastic and Aluminum are (‘B’ items) intergroup items. .(with reference to Table 3.7

& chart3.7)

Lubricant and cokes are C items marginally important. .(with reference to Table 3.7

& chart3.7)

Cumulative cost helps purchase department to compare different investment choices. .

(with reference to Table 3.8 & chart3.8)

44

4.3 RECOMMENDATIONS

In store department items can be placed in sequential manner.

There shall be a system of monitoring and controlling the inventory

There shall be proper record of wastage. And the entire process of inventory

management can be properly coordinated and defects must be eliminated.

Lead, Iron, Zinc and copper have high cost and high value of consumption. These raw

materials are coming under A category because of that frequent ordering is necessary

The company can make use of a combined method of ABC and VED Analysis for better

inventory controlling and management.

Routinely verify A Category items on a monthly basis but only review C category items

twice a year.

Use scheduled orders for Category C items but require detailed purchase orders and

negotiation for Category A items

QUESTIONNAIRE

45

Q.1) Name of the Company: __________________

Q.2) Date: ___________________

Q.3) which is the high Inventory Items in your company ?

a) raw material b) work in progress c) Finished goods

Q.4) do you have classifications of all kind of inventories?

a) Yes b) No

Q.5 Company having any standard inventory control system?

a) Yes b) No

Q.6) estimated capacity of warehouse?

a) capacity above 1000 tones b) capacity 1000 tones c)capacity below 1000 tones

Q.7) there is any separate warehouses for various types of inventories?

Yes No

Q.8) Normal lead time of inventories?

a)20 days b)15 days c)10 day

Q.9) there is any delay transferring inventory?

a) Yes b) No

Q.10) average inventory wastage per week?

a) High b) Medium c) low

Q.11) Do you think there is any relevance for inventory control technique? a) Yes b) No

BIBLIOGRAPHY

46

Text reference

1. N G Nair -Production and Operation Management(1996)Tata McGrew-Hill publishing company

Ltd.

2. Ray wild -- Operations management (Jan 17, 2002)

3. William J Stevenson-Operations Management(2009) Tata McGrew-Hill Education Pvt Ltd .

Journals

4. Colley Jr, J.L., Landel, R.D. and Fair, R.R., Production, Operations, Planning &Control—Text

and Cases, 1977 (Holden–Day: USA).

5. Arsham, H., Tools for decision analysis. Available online at: http://www.mirrorservice.

org/sites/home.ubalt.edu/ntsbarsh/Business-stat/opre/partIX.htm (accessed 13 May 2005)

6. Bhattacharya, A., Sarkar, B. and Mukherjee, S.K., ABC analysis in multi-criteria environment—

an application of TOPSIS, in 1st International Conference on Logistics

7. Flores and Whybark 1986).operations & Supply Chain Management, 2001, pp. 489–

494.Flores, B.E., Olson, D.L. and Dorai, V.K., Management of multicriteria inventory

8. Cohen and Ernst (1988) classification. Math. Comput. Model. 1992, 16, 71–82.Cohen, M.A. and

Ernst, R., Multi-item classification and generic inventory stock control policies. Prod. Invent.

Mgmt., 1988, 29, 6–8.

9. Harhalakis, G. and Zachman, W.S., A dynamic planning and control system for inventories of

raw materials. Prod. Invent. Mgmt. J., 1989, Second Quarter, 12–17.

WEBSITES

http://managementstudyguide.com/inventory-classification.htm

http://en.wikipedia.org/wiki/Inventory

http://www.sarkcables.com/contactsark.php

47