Embed Size (px)

Citation preview

RACOFS© - Radhan’s Approach to Corporate Finance Services

RACOFS© - The Edge of Professional Approach

Radhan is based on the insight that corporate finance is a profession.

Therefore, Radhan is constantly engaged in developing and testing methodologies to create solutions that optimizecurrent market opportunities without compromising future sustainability.

Though based on rigorous analytical tools, RACOFS is far from being academic. It is a systemized optimization of corporatefinance solutions, based on the specific needs of each client on the one hand and an accurate mapping of availablesources on the other hand. It also incorporates the best practices of approaching each finance provider according to eachof the providers regulations and standards.

RACOFS relates to all aspects of the interface between Radhan and its clients, from the pre-engagement analysis up to thecompletion. In some cases only part of the RACOFS methodology is relevant and in these cases it is applied accordingly.

Radhan actively encouragers discourse with both clients and finance providers regarding RACOFS and, as much aspossible, is transparent in sharing its elements.

Phase IPre-NDACapital

StructureAnalysis

Capital Structure Classification

Capital Structure Adaptability

Phase IIClient

Engagement

CSC - E CSC - I

CSC - R CSC - U

CSC - C

CSA - A CSA - B

CSA - C

Post NDA CS Analysis

Terms of Reference

Engagement Letter

Phase IIIFull Analysis

Phase IVProcess

Crossroad

Phase VProcess Design

Phase VIDelivery

Internal Analysis

Financial Model

Funded Instruments

(debt, equity, m&a, restructuring,

Structured finance)

TransactionManagement

External Analysis

Benchmark Analysis

Forecast Analysis

Balance Sheet Development

KPI

Volatility Analysis

Value Chain

Competitive Setting

Exogenous Impacts

business

financial

Assumption Analysis

Back testing

Financial Sources Matrix

Term Sheet Preparation

Negotiation Planning

ProcessScheduling

Non Funded Instruments

(credit rating, non deal roadshow)

Targeted Presentation

Analytical Backup

Commercial Negotiations

Legal Completion

Radhan Data Banks

Capital Structure

Industry Map

Source Map

M&A Matrix

Course of Action

While the capital structure does not restrain the ability of the corporation to achieve its goal, the structure can be more efficient usually from cost perspective or capital deployment

Phase IPre-NDACapital

StructureAnalysis

Capital Structure Classification

Capital Structure Adaptability

CSC - E

CSC - I

CSC - R

CSC - U CSC - C

CSA - A CSA - B CSA - C

Phase IIClient

Engagement

Phase IIIFull Analysis

Phase IVProcess

Crossroad

Phase VProcess Design

Phase VIDelivery

Attends to identifying the potential gap between the existing capital structure and the corporate goals. This classification is crucial as it assists in defining the motives for a transaction and setting its concrete objectives.

The capital structure is suitable to the corporation’s goals and is set in optimal terms and conditions

Capital structure that does not allow the corporation to fulfill its plans because of constraints in cash flow or available funds

A capital structure that will require refinancing within two years in order for the corporation to meet its obligations

A capital structure that includes obligations in default, or will do so with high degree of certainty

Capital structure adaptability is ranked A to C, A reflecting flexibility and therefore low expected complexity; B medium complexity and C rigidness and high complexity

This scale is an initial opinion as to the legal and practical complexity of changing the existing capital structure. It is based on a basic analysis of the structure in parameters such as:• Legal terms of the indentures • Number of stakeholders• Public/ Private securities• Assets available as security• Liquidity

Phase IIClient

Engagement

Phase IPre-NDACapital

Structure Analysis

Phase IIIFull Analysis

Phase IVProcess

Crossroad

Phase VProcess Design

Phase VIDelivery

Post NDA CS Analysis

Terms of Reference

Engagement Letter

Since most of Radhan’s services are transaction based, the engagement with the client isusually preceded with an initial feasibility stage which includes the capital structure analysis.Sometimes, of course, the client requests a segment of the full scale services are rendered(such as rating advisory or IPO advisory). Even in these cases, Radhan aims to understand

the nature of the service in the broader perspective and refrains from a technical approach

In cases were the client is identified by Radhan the analysis is first based on public information and later on, after a NDA is signed on confidential information

Based on the capital structure analysis the terms of reference for the engagement are mutually agreed upon with the client and only then the client is engaged

Phase IIIFull Analysis

Phase IPre-NDACapital

Structure Analysis

Phase IIClient

Engagement

Phase IVProcess

Crossroad

Phase VProcess Design

Phase VIDelivery

Internal Analysis

KPI

Efficient capital structure is based upon a deep understanding of the corporation’s business positioning and required capital allocation. Therefore Radhan’s approach to a corporate finance transaction follows through an analysis of the corporation and its environment

This analysis does not presume to be of strategic nature, but rather to reflect the impact of different potential scenarios on the capital structure and devise a structure that will be solid enough to withstand the possible setbacks ahead. The robustness of the capital structure takes into account the risk appetite of the decision makers in the corporation. We do not assume to replace their judgment, but rather to put a “risk tag” on the alternatives

The evolvement of the balance sheet over a three to five years timeperiod (depends on the industry) is an inclusive analysis of how theaccounting and business facets of the corporation interact as well as howthe financials are influenced by different events. Over this timeframe it isalso possible to understand how the p&l and cash plow influence thebalance sheet and how flexible is the capital structure

Balance Sheet Development

The key performance indicators will be defined based on the analysis of the parameters that influenced the balance sheet development

Phase IIIFull Analysis

Phase IPre-NDACapital

Structure Analysis

Phase IIClient

Engagement

Phase IVProcess

Crossroad

Phase VProcess Design

Phase VIDelivery

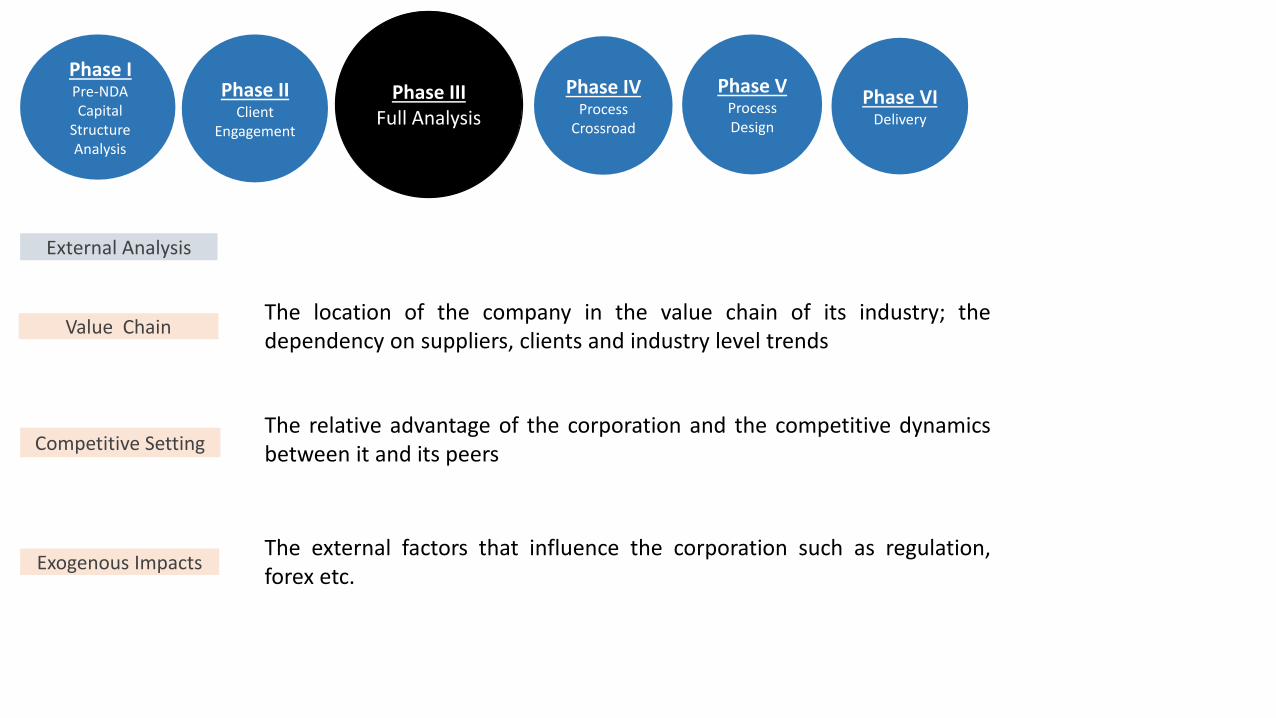

External Analysis

Value Chain

Competitive Setting

Exogenous Impacts

The location of the company in the value chain of its industry; thedependency on suppliers, clients and industry level trends

The relative advantage of the corporation and the competitive dynamicsbetween it and its peers

The external factors that influence the corporation such as regulation,forex etc.

Phase IIIFull Analysis

Phase IPre-NDACapital

Structure Analysis

Phase IIClient

Engagement

Phase IVProcess

Crossroad

Phase VProcess Design

Phase VIDelivery

Comparative qualitative and quantitative inquiries into the business strategiesand operations of the comparables

Based on the analysis conducted the range of possible scenarios is defined tomodel the potential outcomes and their financial implications

Benchmark Analysis

Volatility Analysis

business

financial financial benchmarking to the comparables. Examination of the leverage,financial profile and covenants typical to the industry

Phase IIIFull Analysis

Phase IPre-NDACapital

Structure Analysis

Phase IIClient

Engagement

Phase IVProcess

Crossroad

Phase VProcess Design

Phase VIDelivery

Forecast Analysis

Assumption Analysis

Back testing

drilling down to the assumptions driving the forecast and classifying thisassumptions according to their source between market changes and internalchanges. Then each of the category is tested as to understand to what degreethese assumptions can be substantiated

Once the assumptions are identified, the expected forecast is back tested toexamine what would have been the outcome in the past under theseassumptions. Any discrepancies between the forecast and the back testingresults are analyzed

Phase IVProcess

Crossroad

Phase IPre-NDACapital

Structure Analysis

Phase IIClient

Engagement

Phase IIIFull

Analysis

Phase VProcess Design

Phase VIDelivery

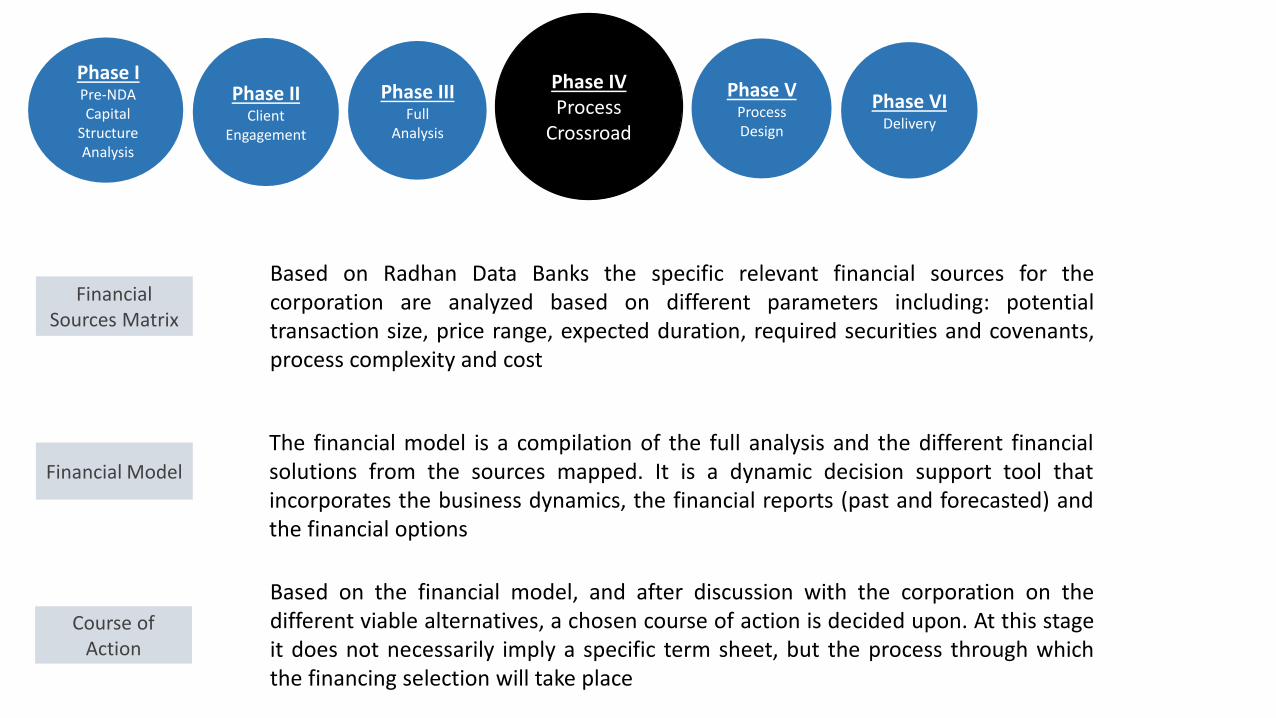

The financial model is a compilation of the full analysis and the different financialsolutions from the sources mapped. It is a dynamic decision support tool thatincorporates the business dynamics, the financial reports (past and forecasted) andthe financial options

Based on Radhan Data Banks the specific relevant financial sources for thecorporation are analyzed based on different parameters including: potentialtransaction size, price range, expected duration, required securities and covenants,process complexity and cost

Financial Model

Financial Sources Matrix

Course of Action

Based on the financial model, and after discussion with the corporation on thedifferent viable alternatives, a chosen course of action is decided upon. At this stageit does not necessarily imply a specific term sheet, but the process through whichthe financing selection will take place

Phase VProcess Design

Phase IPre-NDACapital

Structure Analysis

Phase IIClient

Engagement

Phase IIIFull

Analysis

Phase IVProcess

Crossroad

Phase VIDelivery

Funded Instruments

(debt, equity, m&a, restructuring,

Structured finance)

Term Sheet Preparation

Negotiation Planning

ProcessScheduling

Non Funded Instruments

(credit rating, non deal roadshow)

Targeted Presentation

The term sheet includes all relevant parameters: volume, price andbusiness and legal major clauses. It is adjusted to meet each financialsource requirements

Setting the parameters on which the negotiation will be held. It is alsocrucial to preset the covenant and security packages (in case of debt) oroption and price mechanisms (in case of equity); analyzing thenegotiations dynamics and preparing for it

The timetable for the transaction is also preset, especially since multipletasks are assigned to different teams (accounting, legal etc.)

The targeted presentation is the marketing material designatedspecifically for each potential financing source it includes relevant information from the full analysis stage and the financial model

Rating agencies use matrices andmethodologies that are constantlychanging and are industry specific.Radhan has intimate knowledge ofthe processes and models used bythe rating agencies.

The outputs of this phase are: afinancial model adjusted to theformat required by the ratingagency and a full presentation ofthe argument, that serves asframework for the analysis

Non-deal road-shows are plannedin a similar manner to an issuanceroad show

Phase VIDelivery

Phase IPre-NDACapital

Structure Analysis

Phase IIClient

Engagement

Phase IIIFull

Analysis

Phase IVProcess

Crossroad

Phase VProcess Design

Transaction Management

Analytical Backup

Commercial Negotiations

Legal Completion

oversee the correlation between the commercial understandings and the legal outcome andbalancing the protection of the client’s legal rights with the need business flexibility

Manage the process proactively according to the designed plan in order to arrive at the bestpossible result for the client

Use a supporting model adjusted to meet regulatory restrictions while enabling investors’ analyststo single out the investment in a easy, structured manner

Execute of the transaction planned in the previous phases. It includes management of all relatedfacets of the investors road show or any other competitive process up to completion

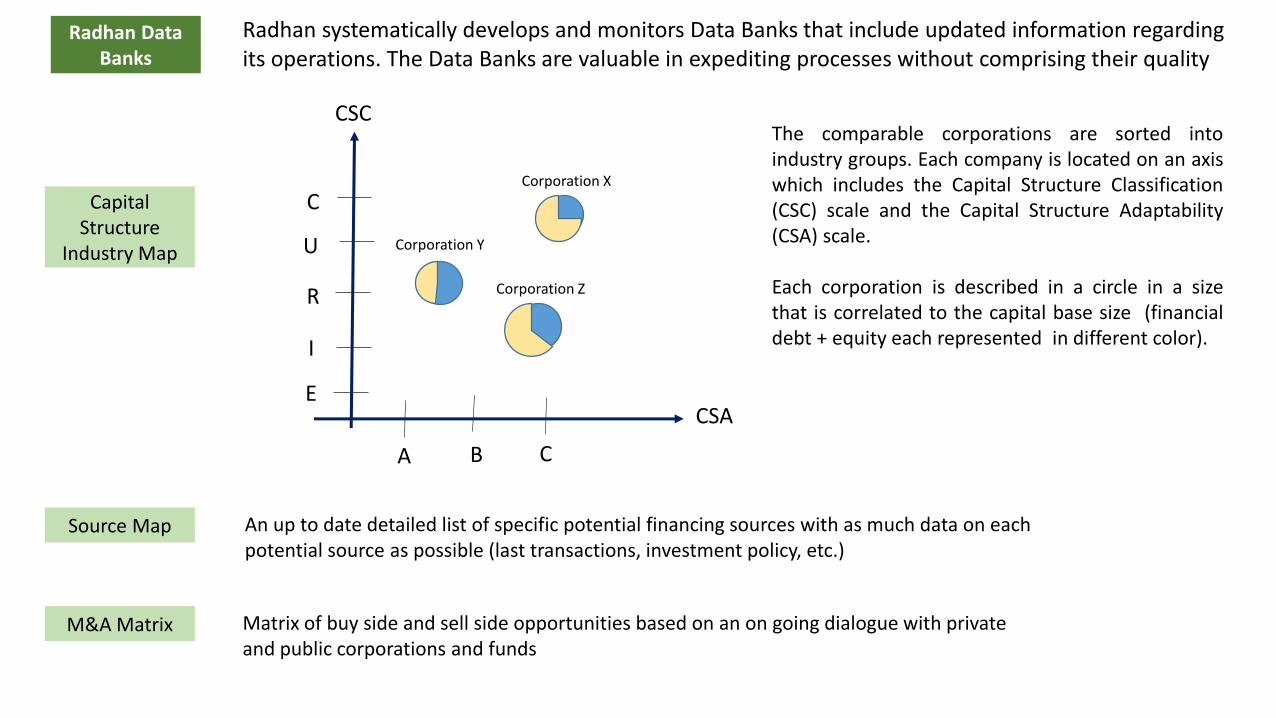

Radhan Data Banks

Capital Structure

Industry Map

Source Map

M&A Matrix Matrix of buy side and sell side opportunities based on an on going dialogue with private and public corporations and funds

CSC

CSA

A B C

E

I

R

U

CCorporation X

Corporation Y

Corporation Z

Radhan systematically develops and monitors Data Banks that include updated information regarding its operations. The Data Banks are valuable in expediting processes without comprising their quality

The comparable corporations are sorted intoindustry groups. Each company is located on an axiswhich includes the Capital Structure Classification(CSC) scale and the Capital Structure Adaptability(CSA) scale.

Each corporation is described in a circle in a sizethat is correlated to the capital base size (financialdebt + equity each represented in different color).

An up to date detailed list of specific potential financing sources with as much data on eachpotential source as possible (last transactions, investment policy, etc.)

![ENGLISH VERSION BELOW BY SMOKETOWN BY … Keys Scales Manual.pdfENGLISH VERSION BELOW BY SMOKETOWN BY SMOKETOWN Fie das M] Taste BY SMOKETOWN BY SMOKETOWN BY SMOKETOWN BY SMOK BY SMOK](https://img.dokumen.tips/doc/110x75/5e49aa658a8728674a131469/english-version-below-by-smoketown-by-keys-scales-english-version-below-by-smoketown.jpg)