Embed Size (px)

Citation preview

Indian Insurance Industry: Reaching

out to Exponential Growth

Analysis and Report by Resurgent India

June 2016

2

Report Contents

Message from the desk of Sh JP Gadia

Section 1 : Industry Overview and Performance

Section 2 : Key Issues and Challenges

Section 3 : Growth Drivers

Section 4 : Recent Government Initiatives to drive growth in the Insurance Industry

Section 5 : Recent Industry Trends

Section 6 : Conclusion and Way Forward

About RESURGENT INDIA

3

Message from the desk of

Sh. JP Gadia

A well-developed and evolved insurance sector is a boon for economic development

of any country -- it provides long- term funds for infrastructure development at the

same time strengthening the risk taking ability and social security of the country. On

account of an improved consumer and business environment, the global direct

premiums grew by 3.7% in 2015 to USD 4,778 billion after a year of stagnation in the

previous year. During the same period, the Indian Insurance sector grew by 5.3% in

terms of total premium collected. The sluggishness was led more by Life segment,

due to much needed recent regulatory reforms, that made the operators question

and work towards improving the business model. Non-life segment on the other

hand, has seen more consistent growth over the years, with some challenges on

account of claim related losses.

Being a relatively new industry, the players would need to evolve with the regulations

and dynamic eco-system. This would pose various challenges for both the life and

non-life segments (low interests, soft pricing etc.). The report covers all such issues

in depth that can potentially halt the organic growth of the sector and would need to

be addressed by players and regulators alike to continue to deliver on the

shareholders return expectations. The few broad imperatives involve: a. making

efficient deployment of available resources b. driving multi-channel distribution

efficiency and synergy c. increasing investment in product innovations towards

affordable and relevant offerings d. sustained efforts on consumer awareness e.

close coordination with regulatory authority f. building technological advances

towards cost effective reach and distribution model

The strong fundamentals of the industry augur well for a roadmap to be drawn for

sustainable long-term growth. The available headroom for development, sustainable

external growth drivers, and competitive strategies would continue to drive growth in

the insurance industry. We are hopeful that this report will be helpful in diagnosing

the right pushes and allowing the industry to move forward with the continued

positive momentum.

4

Industry Overview and Performance

5

Industry Overview

From Insurance being seen as a basic protection instrument against expected

losses, the Indian Insurance industry has surely come a long way to become an

absolute critical driver of economic prosperity and growth. The sector has helped

account for risks; provide funds for capital intensive national building efforts besides

lending social security to the citizens. Over a period of decade and a half, the

industry has witnessed phases of spurt growth and moderation, intensifying

competition and expansion of customer and geographic coverage.

In terms of total premium, the insurance industry in India grew by 5.3% during the

period 2014-15. Structurally, the Indian insurance industry consists of 52 insurance

companies of which 24 are in life insurance business and 28 are non-life insurers.

This also substantiates the two broad categories under Insurance sector i.e. Life and

Non-Life or General. Of the 53 companies presently in operation, eight are in the

public sector - two are specialized insurers, namely ECGC and AIC, one in life

insurance namely LIC, four in non-life insurance and one in reinsurance. The

remaining forty five companies are in the private sector

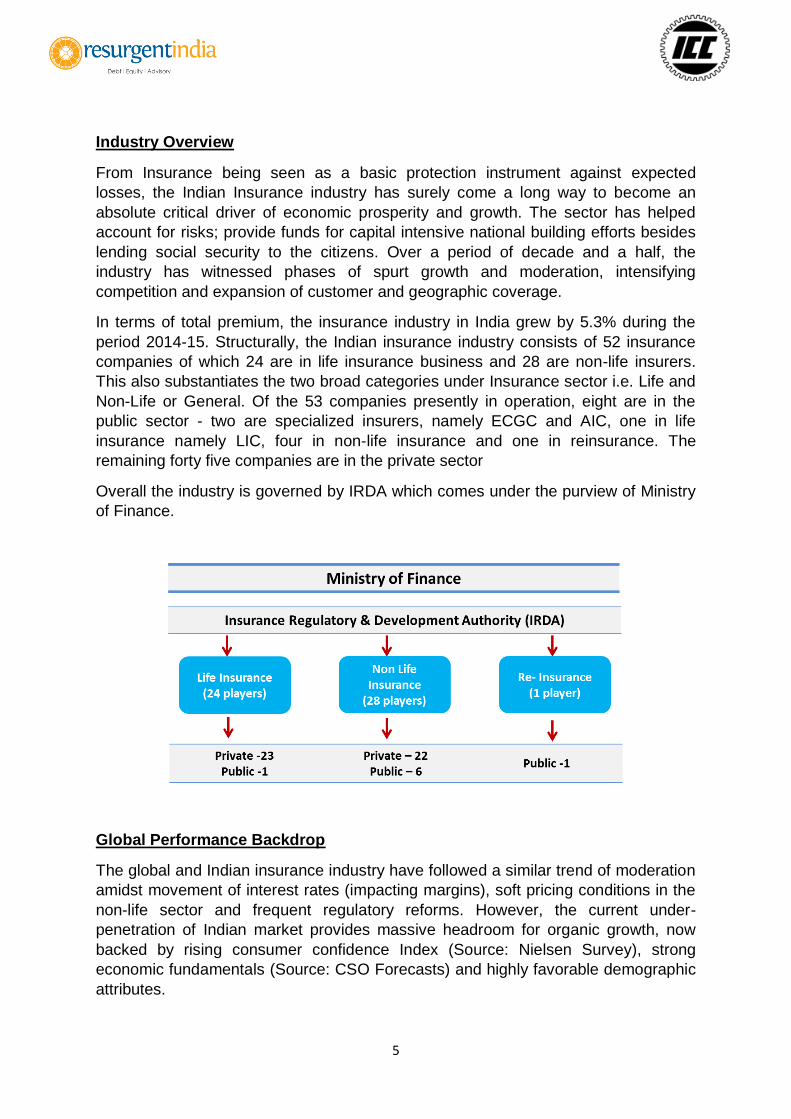

Overall the industry is governed by IRDA which comes under the purview of Ministry

of Finance.

Global Performance Backdrop

The global and Indian insurance industry have followed a similar trend of moderation

amidst movement of interest rates (impacting margins), soft pricing conditions in the

non-life sector and frequent regulatory reforms. However, the current under-

penetration of Indian market provides massive headroom for organic growth, now

backed by rising consumer confidence Index (Source: Nielsen Survey), strong

economic fundamentals (Source: CSO Forecasts) and highly favorable demographic

attributes.

6

Against the global backdrop of improved consumer and business environment,

insurance sector picked up good pace in 2014-15 having grown Total direct premium

by 3.7 per cent against 1.4 per cent for the previous year (Source: Swiss Re,

Sigma).The Indian Insurance sector was no different.

India ranked 11 in Life Insurance Business and 20th in Non-Life Insurance Business

among the 88 countries, for which data is published by Swiss Re. India’s share in

global life insurance market was 2.08 per cent against 0.69 per cent in global non-life

insurance premium in 2014. This indicates huge opportunity to grow.

Globally, Switzerland leads on insurance density and Taiwan on penetration. Taiwan

has the largest Life Insurance penetration, US is most penetrated in Non-life

segment as per Swiss Re Sigma Report 4/2015.

Performance Overview

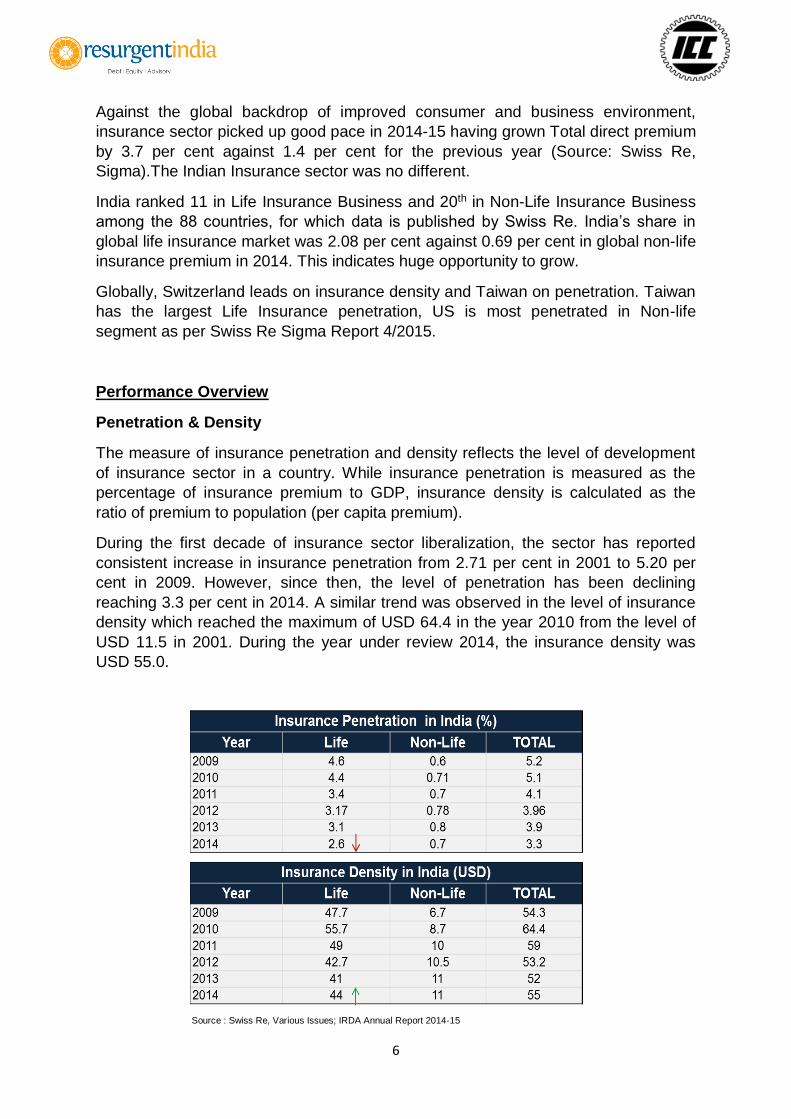

Penetration & Density

The measure of insurance penetration and density reflects the level of development

of insurance sector in a country. While insurance penetration is measured as the

percentage of insurance premium to GDP, insurance density is calculated as the

ratio of premium to population (per capita premium).

During the first decade of insurance sector liberalization, the sector has reported

consistent increase in insurance penetration from 2.71 per cent in 2001 to 5.20 per

cent in 2009. However, since then, the level of penetration has been declining

reaching 3.3 per cent in 2014. A similar trend was observed in the level of insurance

density which reached the maximum of USD 64.4 in the year 2010 from the level of

USD 11.5 in 2001. During the year under review 2014, the insurance density was

USD 55.0.

Source : Swiss Re, Various Issues; IRDA Annual Report 2014-15

7

Premium

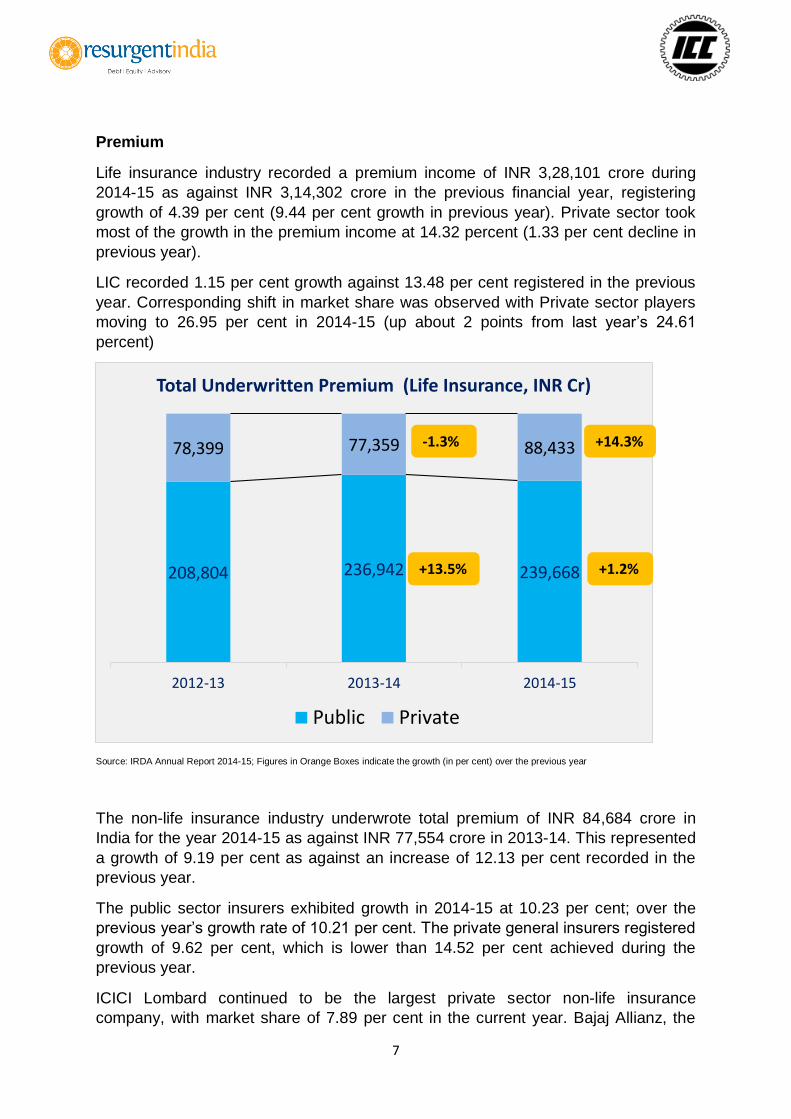

Life insurance industry recorded a premium income of INR 3,28,101 crore during

2014-15 as against INR 3,14,302 crore in the previous financial year, registering

growth of 4.39 per cent (9.44 per cent growth in previous year). Private sector took

most of the growth in the premium income at 14.32 percent (1.33 per cent decline in

previous year).

LIC recorded 1.15 per cent growth against 13.48 per cent registered in the previous

year. Corresponding shift in market share was observed with Private sector players

moving to 26.95 per cent in 2014-15 (up about 2 points from last year’s 24.61

percent)

Source: IRDA Annual Report 2014-15; Figures in Orange Boxes indicate the growth (in per cent) over the previous year

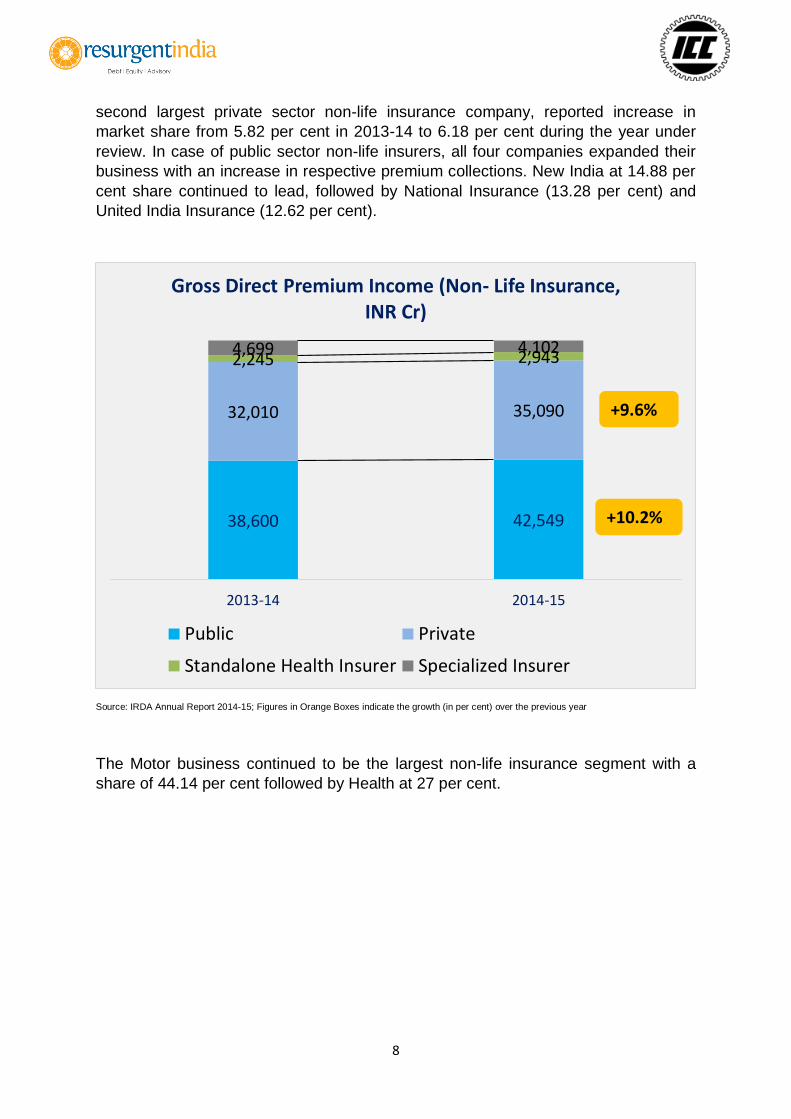

The non-life insurance industry underwrote total premium of INR 84,684 crore in

India for the year 2014-15 as against INR 77,554 crore in 2013-14. This represented

a growth of 9.19 per cent as against an increase of 12.13 per cent recorded in the

previous year.

The public sector insurers exhibited growth in 2014-15 at 10.23 per cent; over the

previous year’s growth rate of 10.21 per cent. The private general insurers registered

growth of 9.62 per cent, which is lower than 14.52 per cent achieved during the

previous year.

ICICI Lombard continued to be the largest private sector non-life insurance

company, with market share of 7.89 per cent in the current year. Bajaj Allianz, the

208,804 236,942 239,668

78,399 77,359 88,433

2012-13 2013-14 2014-15

Total Underwritten Premium (Life Insurance, INR Cr)

Public Private

+13.5%

-1.3% +14.3%

+1.2%

8

second largest private sector non-life insurance company, reported increase in

market share from 5.82 per cent in 2013-14 to 6.18 per cent during the year under

review. In case of public sector non-life insurers, all four companies expanded their

business with an increase in respective premium collections. New India at 14.88 per

cent share continued to lead, followed by National Insurance (13.28 per cent) and

United India Insurance (12.62 per cent).

Source: IRDA Annual Report 2014-15; Figures in Orange Boxes indicate the growth (in per cent) over the previous year

The Motor business continued to be the largest non-life insurance segment with a

share of 44.14 per cent followed by Health at 27 per cent.

38,600 42,549

32,010 35,090

2,245 2,9434,699 4,102

2013-14 2014-15

Gross Direct Premium Income (Non- Life Insurance, INR Cr)

Public Private

Standalone Health Insurer Specialized Insurer

+10.2%

+9.6%

9

Key Issues and Challenges

10

While a range of economic and financial reforms have helped the insurance sector

grow, there remains a host of challenges which need to be addressed for harnessing

the full potential of the sector:

Key Challenges

a. Lack of Consumer Awareness: In spite of opening of the insurance sector

for private participation, the levels of insurance penetration and density are

very low. The main reason for low penetration is lack of awareness about the

insurance products and its benefits. It is important (and IRDA has been

working on it) to educate general public about the benefits of insurance, how

to select an insurance product and to educate them about the grievance

redress mechanism in case they are not satisfied with the services provided

and have a complaint against financial service providers.

b. Negative Consumer Experience and Perception: One of the critical levers

is to manage consumer expectations and service. The industry has been

plagued by perceptions of slow, unreliable and at times harassing consumer

delivery. A lot of new entrants have worked at addressing the barriers through

their consumer interactions and working models, the same needs to be

strengthened across, especially with the onset of social media. Insurers

should identify areas, which are most vulnerable to frequent critical

comments, analyze the reasons for such underperformance, and take steps to

enhance the service delivery.

c. Poor offtake of micro-insurance- Micro insurance (life, disability and health)

coverage of the economically disadvantaged sections of Indian society is

dismally low. Several factors have impeded the growth of micro insurance in

the country. Most customers in the target segment have low financial literacy

and are unable to view insurance as a risk mitigation tool. Further, lack of

adequate products, poorly designed policies, lack of education, mis-selling

through inadequately trained agents and rejections during claims settlement

has led to lack of trust with this customer segment. The feasibility of various

products is often lacking or low in quality. On the distribution front, limited

incentive on a low premium products makes it difficult to cover operational

costs of reaching out to the customers. For micro insurance to succeed,

demand has to be created through building awareness among the target

segment, creating simple and need based products and most importantly,

simplifying the processes of underwriting and claims management.

d. Agency led Distribution Model: With reduced commission structures, high

attrition rates and dwindling perception attractiveness of agency as a career

options, the agency channel is under stress. This has led to reduced

dependence on the model and subsequently significant reduction in number

of offices in the private space.

11

Source: IRDAI Handbook 2013-14

e. Distribution Costs: Life insurance companies spend a significant portion of

their budget to set-up and streamline the operating model and the distribution

process towards business acquisition. Distribution is not only the forefront of

the operations but also forms a large proportion of the operating expenses.

Accordingly, inefficient agent recruitment and high employee attrition increase

the operational costs. For insurers to realize the highest value from

distribution, they must define an operating model which supports a

multiproduct, multi-channel distribution model that compliments an insurer’s

revenue objectives and profit margins.

f. Lack of Alternate Distribution Channels: While banc-assurance is

expected to drive near term growth and online holds a promise for the future,

agency channel continues to dominate the channel mix today. There is an

urgent need to take initiatives to revamp the agency channel to become cost

effective and in tandem, identify alternative networks that complement the

existing channels.

g. Lack of Product Innovations and Customizations: There have always

been a few life insurers who have sought to identify niche markets like

women-oriented products, worksite marketing, children future protection

markets and pension markets. But these have not been happening on a

consistent basis. The industry’s business model needs to constantly innovate

and evolve. However, off late this is witnessing a change with increasing

number of insurers looking to introduce new and innovative products aimed at

meeting evolving customer needs.

h. To highlight the point further, Pension and retirement products is a big gap in

the current product portfolios. While the demographics (percentage share of

60+ is expected to go up to 12 per cent by 2030) support the need for a

product, it has remained largely under-leveraged by consumers and

marketers alike on account of a. low consumer awareness and thus perceived

relevance b. Difficulty in providing long term insurance guarantees c. long

gestation period of returns etc.

890

1,327

1,593 1,575

1,3021,081

950 993

0

200

400

600

800

1000

1200

1400

1600

1800

FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14

Individual Agent Count – Private life Insurers (000s)

12

i. Intense Market Competition: The Indian insurance industry is gradually

evolving and thus remains highly competitive. The insurance public and

private players compete on the basis of reliability, financial strength and

stability, ratings, underwriting consistency, service, business ethics, price,

performance, capacity, policy terms and coverage conditions. In addition, the

company also faces competition from other financial institutions such as

banks, securities firms etc. which have started cross selling products that

directly or indirectly competes with various insurance products.

Given the inability of general insurers to differentiate on the basis of product

offerings along with the lack of customer awareness towards product features,

the competition will mainly be price led, which will further impact margins for

the sector.

j. Human Resource Challenge: Keeping attrition in check and ensuring

availability of continuous talent is a key task. Further, the insurance market is

now filled with players, who are mature, globally prominent and big players,

each of them has ability to influence the market which is likely to further up the

challenge in this area.

k. Regulatory Challenges: As the competition gets acute, the customer

becomes more vulnerable to the vagaries on market environment. The

regulators with a view of driving transparency, consumer protection,

simplifying portfolio and creating a long term sustainable eco-system and

business model have driven a few frequent changes in the regulations. Some

of the key changes which played a dominant role in charting the course for the

industry were the introduction of cap in charges on linked products,

restrictions on pension and index-linked products, and persistency norms for

agents; while the general insurance sector was affected by price de-

tarrification and motor third party risk pooling arrangements.

E.g. IRDA had announced rules pertaining to capping of expenses -- no

insurer should spend more than an aggregate 10% of all first year premiums

and 4% of all renewal premiums on policies granting deferred annuities for

more than one premium; 5% of premiums received during the year on single-

premium annuity products and 1/20th of 1% of the average of the total sums

assured by policies excluding single-premium policies. While it aims to protect

long term interests, in the short run, it will put pressure on insurance

companies to cut costs by innovation, digitization, reducing customer

acquisition costs and reducing turnaround time. [Source: Economic Times,

June ’15 Report]

k. Volatility in Global Financial Markets: Though, coordinated actions by

several governments did restore some confidence in the volatile global

markets, market participants remained jittery. As a result, whenever there is a

withdrawal of foreign portfolio investments from Indian equity and debt

markets, investment returns booked by insurers are likely to suffer.

13

l. Costs and Profitability: Insurers’ fascination for top line growth at any cost

has resulted in inefficient operating models and hence inferior operating ratios

as compared to global benchmarks, in both life and non–life. Clubbed with

high claims costs and regulatory constraints (as discussed above) have led to

tightening of insurer margins, impacting category profitability.

m. Adverse Claims Ratio for Non-Life Insurance: The sector has been making

significant underwriting losses from its core operations since 2007. In 2014-

15, the net incurred claims for the industry rose 12.3 per cent to INR 55,232

crores against INR 49,179 crores in 2013-14, stressing thereby the

underwriting profits. Within Non-life sector, the health and motor insurance

lines, which are also the biggest and the fastest growing segments, had the

highest claims ratios of 97 percent and 77 percent respectively

14

Growth Drivers

15

Growth Drivers

a. Strong Economic Fundamentals: Looking at GDP growth forecasts, India is

likely to figure amongst the faster growing economies from around the world.

This is a healthy indicator for insurance sector when studied in conjunction

with YoY growing savings rate and %financial savings/ total savings.

Source: IBEF Research, ICICI, RBI Annual Report

b. Increased consumer awareness and demand: The working population (25–

60 years) is expected to increase from 675.8 million in 2006 to 795.5 million in

2026. Increased incomes are expected to result in large disposable incomes,

which can help drive growth for the sector if desired consumer pull can be

created. E.g. The growing affluence of the Indian middle-class accompanied

with lifestyle-related diseases, inflationary healthcare costs combined with

increased awareness generated through specific IRDA measures and

insurers’ communication, are driving the demand for health insurance in India

c. Organic Headroom to Grow: There is a lot of untapped market in the

country. This gives space for all players to grow and expand the insurance

industry. Increased investments will allow for stronger distribution and

corresponding expansion in the underpenetrated segments of the population,

like those in smaller towns and non-urban areas.

In the recent past, the industry has witnessed the emergence of alternate

distribution channels. The typical distribution channels used by insurance

companies now include bancassurance, direct selling agents, brokers, online

distribution, corporate agents , tie-ups of para-banking companies with local

corporate agencies (for example NGOs) in remote areas.

Further, technology has emerged as a big enabler among global evidence

that internet penetration and usage have a positive correlation with the

performance and activities of insurance companies at various levels – lower

customer acquisition costs, improved access to information, product

innovation that cater to the needs of the customers and enhanced

convenience. It is estimated that digitization will reduce 15-20 per cent of total

cost for life insurance and 20-30 per cent for non-life insurance. While the

45

141

188202

0

50

100

150

200

250

2000 2010 2013 2015

Financial Savings (USD Bn)

16

current size is marginal as compared to overall customer base and

underwritten premium, the segment shall witness growth and reach a

significant size in the future as the internet penetration increases and

awareness of the customers also rises

d. Growing Investment in Product Design and Delivery: Globally, product

innovation has proved to be critical for insurers to succeed in mature

markets. As per a report in Economic Times dated Dec’15, insurers are

investing significantly in improved product manufacturing capabilities globally,

including building product life cycle management strategies and considering

the product needs of future demo-graphic segments.

With customers asking for increased levels of customization, product

innovation is one of the best strategies for companies to increase their market

share. In India, however, the innovation has been limited to minor

modifications on tariffs and features, add-on covers such as dental cover,

daily cash benefits for hospitalization and the like. The sector will need to

cover the bridge by introducing differentiated and multi-tiered long- term

products. The journey has begun with players investing time and thought on

innovations around product and delivery.

e. Conducive Policy and Regulatory Environment : With slew of recent

reforms like FDI relaxation, Insurance Bill, tax incentives, clarity on IPOs etc.,

there is enough potential for positive growth of the Indian insurance industry

given the focused, synergistic efforts of the regulator, government and

industry players in the backdrop of rising demand for insurance.

17

Recent Government Initiatives to

drive growth

18

The Government of India has taken a number of initiatives to boost the insurance

industry. Some of the recent initiatives announced in the union budget 2016 are -

a. India's government has further liberalized the foreign direct investment

rules for the insurance sector with a new regulation allowing overseas

companies to own up to 49% of domestic insurers without prior

approval. As per the earlier norms, FDI of up to 26% is permitted

through automatic approval route, but for FDI of up to 49%, the

approval of the Foreign Investment Promotion Board is required. The

FIPB is an inter-ministerial panel and can approve foreign investment

proposals of up to 50 billion rupees (USD 754 million). This means that

investors will not have to approach the FIPB for increasing their stakes

up to 49% in the JV. However, the foreign investment proposals up to

49% of the total paid up equity of the Indian insurance company shall

be allowed on the automatic route subject to verification by the

Insurance Regulatory and Development Authority of India. Besides

speeding up the deal completion process, the new rule is also

expected to attract more foreign investments.

b. The government proposed listing of four wholly-owned PSU general

insurance companies in the capital market. The four PSU general

insurance companies are — New India Assurance Company Ltd,

National Insurance Company Ltd, Oriental Insurance Co Ltd and

United India Insurance Co Ltd. Apart from the benefit of realizing value,

this move will make these insurers more market responsive and

accountable for performance and underwriting quality.

c. Service tax on single premium annuity policies has been reduced from

3.5 per cent to 1.4 per cent of the premium paid in certain cases. This

move is a positive for policyholders because single premium annuity

products are usually high-ticket policies and service tax also works out

to a fairly high sum.

d. Service tax on service of life insurance business provided by way of

annuity under the National Pension System regulated by Pension Fund

Regulatory and Development Authority (PFRDA) being exempted, with

effect from 1 April 2016.

e. Service tax on service of life insurance business provided by way of

annuity under the National Pension System regulated by Pension Fund

Regulatory and Development Authority (PFRDA) will be exempted with

effect from 1st April 2016. These services attracted a composite rate of

tax at 3.5%.

f. Service tax on the services of general insurance business provided

under ‘Niramaya Health Insurance Scheme' launched by National Trust

for the Welfare of Persons with Autism, Cerebral Palsy, Mental

19

Retardation and Multiple Disability will be exempted, with effect from

01.04.2016. Extant premium attract service tax at 14%. A cut in service

tax on the insurance policies should reduce the premium for these

policies. This makes them affordable.

g. TDS has been reduced from 2 per cent to 1 per cent on the benefit

payouts from life insurance policies. This will benefit insurance

customers who fall in lower tax brackets. Also TDS threshold limit on

commission payout to agents has been reduced from current Rs

20,000 to Rs 15,000 which will lead to higher tax deduction even for

agents with low income

h. On the indirect tax front, the budget proposes additional 0.5% cess on

insurance premium through imposition of Krishi Kalyan Cess on all

services which will take the effective service tax rate to 15%. In a

country with low life insurance penetration, the additional cess makes

life insurance even more expensive. The government should consider

leaving out life insurance plans that promote protection and long-term

savings from this increase in cess

i. Government allocated a sum of INR 5,500 crore to the recently

announced ‘Pradhan Mantri Fasal Bima Yojana’ (PMFBY) scheme

which aims at providing crop insurance cover to at least half of

country’s 14 million farmers by the end of FY19. Under PMFBY, losses

incurred by farmers at any stage of the farming activity, from the

sowing to the post-harvest season would be covered. As per the

scheme, the farmers' share of premium under PMFBY will be based on

one season, one rate. While the farmers will have to pay only 1.5 per

cent of premium for Rabi crop, they will be asked to pay 2 per cent of

premium for kharif crop. The remaining premium will be paid as

subsidy by the Centre and state governments together. The use of

technology has been mandated in PMFBY unlike its predecessors. The

agriculture ministry has empaneled ten private sector companies and

state-owned Agriculture Insurance Company (AIC) to implement the

new scheme. However, the four PSU insurers- National Insurance

Company, New India Assurance Company, Oriental Insurance

Company and United India Insurance Company are not part of the

chosen insurers to handle the scheme. IRDA is planning to take up the

matter of non-inclusion of these public sector general insurance

companies in PMFBY scheme with the government of India. These four

insurers which have evinced interest in being part of the scheme

collectively boast of 9,000 offices and 3 lakh agents across the country.

They are suitably placed to leverage their extensive network and play a

crucial role in popularizing the scheme in rural India.

20

Recent Industry Trends

21

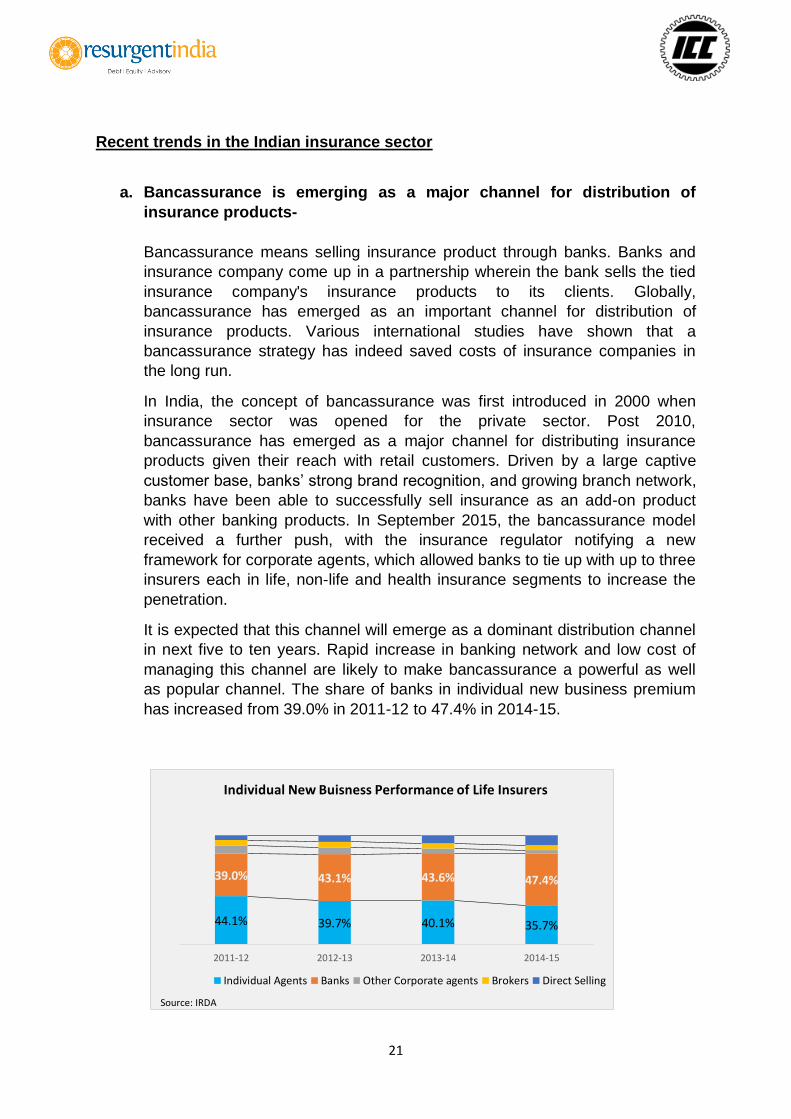

44.1% 39.7% 40.1% 35.7%

39.0% 43.1% 43.6% 47.4%

2011-12 2012-13 2013-14 2014-15

Individual New Buisness Performance of Life Insurers

Individual Agents Banks Other Corporate agents Brokers Direct Selling

Recent trends in the Indian insurance sector

a. Bancassurance is emerging as a major channel for distribution of

insurance products-

Bancassurance means selling insurance product through banks. Banks and

insurance company come up in a partnership wherein the bank sells the tied

insurance company's insurance products to its clients. Globally,

bancassurance has emerged as an important channel for distribution of

insurance products. Various international studies have shown that a

bancassurance strategy has indeed saved costs of insurance companies in

the long run.

In India, the concept of bancassurance was first introduced in 2000 when

insurance sector was opened for the private sector. Post 2010,

bancassurance has emerged as a major channel for distributing insurance

products given their reach with retail customers. Driven by a large captive

customer base, banks’ strong brand recognition, and growing branch network,

banks have been able to successfully sell insurance as an add-on product

with other banking products. In September 2015, the bancassurance model

received a further push, with the insurance regulator notifying a new

framework for corporate agents, which allowed banks to tie up with up to three

insurers each in life, non-life and health insurance segments to increase the

penetration.

It is expected that this channel will emerge as a dominant distribution channel

in next five to ten years. Rapid increase in banking network and low cost of

managing this channel are likely to make bancassurance a powerful as well

as popular channel. The share of banks in individual new business premium

has increased from 39.0% in 2011-12 to 47.4% in 2014-15.

Source: IRDA

22

b. Growing online channel is quickly emerging as a cost effective model

for distribution of insurance products

Insurance companies are also exploring other cost-effective modes of

distribution such as the ‘online channel’. As per estimates by BCG, the overall

online market for insurance sector stands at around 1% for both life and non-

life segments. In life insurance, term plans are the most bought product

online, while in non-life, it is motor, health and travel insurance. The online

market has grown six to seven times in the past six to seven years. This

channel is expected to gain significant momentum in the coming years as

insurance awareness grows among people.

c. Launch of new and innovative products with high levels of

customization

With the passing of the Insurance Laws (Amendment) Bill 2015, the sector

has witnessed a fresh inflow of capital, and introduction of new and innovative

products. Post the approval of 49 per cent direct foreign investment in the

sector, new players have entered the market leading to more, new and

innovative product offerings for consumers to choose from. Further in a move

towards providing customized insurance, more number of life insurance to

general insurance players are offering a customized insurance plan based on

certain fixed parameters and guidelines. Amongst all the insurance segments,

health insurance has witnessed maximum innovation- Life stage based plans,

city based plans, and many new innovative products are being introduced by

various insurance companies to tap the health insurance market.

d. Digital technologies are expected to transform insurance business-

The role of technology has brought about a major change in the sector. As per

a recent report from Accenture, it is expected that the next wave of

technology- Internet of Things (IoT), platform-based ecosystems and artificial

intelligence will significantly change and transform the very nature of the

insurance industry.

The emerging digital technologies- intelligent automation, liquid workforce,

platform economy, predictable disruption and digital trust are offering insurers

an opportunity to shift from their traditional business model to automated

models which they can automatically assess and price risk directly,

individually and in real-time. This digital transformation in insurance

companies will involve continuous disruption to existing business models,

products, services and experiences enabled by data and technology.

Digital services offer convenience, choice and comparison. Digital

technologies can be rooted across the core elements of the insurance value

chain, right from product development to claim settlement. Many Insurers are

now using technology to track all its potential claims, thereby speeding up

claim verification. Moreover, these technologies enable insurers to leverage

23

24.61%

26.95%

2013-14 2014-15

Market Share of Private Players in Life insurance Total premium Income

historical data for predicting future patterns so as to gain a deeper

understanding of the emerging needs of their customers, partners and

employees. This information can be used to build a suitable digital strategy.

An effective digital strategy can allow insurers to reduce customer service

costs, increasing customer fulfilment and retention, while enhancing process

efficiency. As a part of their digital strategy, increasing number of insurance

companies are developing mobile applications to meet the growing demand

for real time services among smartphone users. The mobile applications also

offer a significant potential for enhancing customer service experience in the

form of speedier sales closure, better access to policy details and making

hassle-free renewal payments.

As per a recent EY global Digital Survey it was found that insurers who

developed a digital strategy were more successful than their competitors at

reducing customer service costs while increasing customer loyalty.

e. Growing market share of private players in the life insurance segment

The share of private sector in the life insurance business has witnessed a

marginal increase in the FY15 over FY14. On the basis of total premium

income in life insurance business, the share of private insurers has increased

from 24.61 per cent in 2013-14 to 26.95 per cent in 2014-15. Private insurers

gained market share mainly because of high growth recorded in

bancassurance channel. Moreover, rationalization & transparent pricing along

with the smart interplay of digital and technology push has helped private

insurers to market and deliver products better than before, thereby resulting

in an increased share in the overall business.

f. Regulatory reforms to promote a competitive environment in both the

life and non-life insurance sectors

Source: IRDA

24

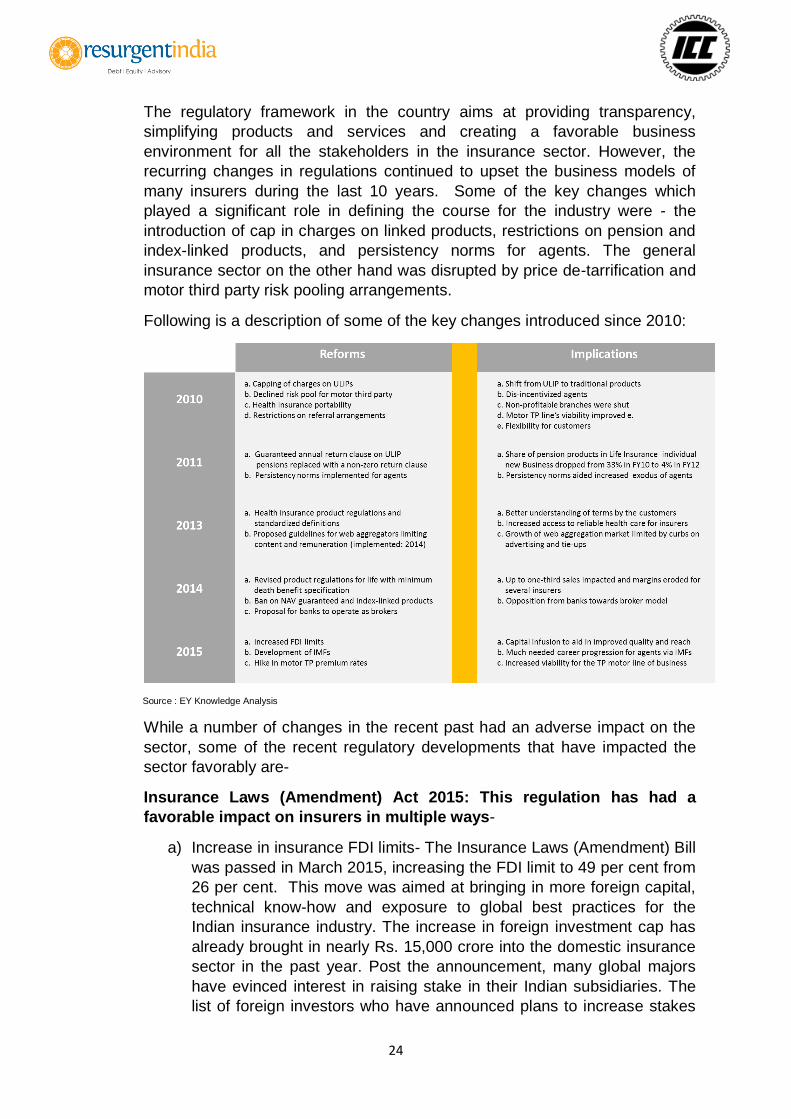

The regulatory framework in the country aims at providing transparency,

simplifying products and services and creating a favorable business

environment for all the stakeholders in the insurance sector. However, the

recurring changes in regulations continued to upset the business models of

many insurers during the last 10 years. Some of the key changes which

played a significant role in defining the course for the industry were - the

introduction of cap in charges on linked products, restrictions on pension and

index-linked products, and persistency norms for agents. The general

insurance sector on the other hand was disrupted by price de-tarrification and

motor third party risk pooling arrangements.

Following is a description of some of the key changes introduced since 2010:

Source : EY Knowledge Analysis

While a number of changes in the recent past had an adverse impact on the

sector, some of the recent regulatory developments that have impacted the

sector favorably are-

Insurance Laws (Amendment) Act 2015: This regulation has had a

favorable impact on insurers in multiple ways-

a) Increase in insurance FDI limits- The Insurance Laws (Amendment) Bill

was passed in March 2015, increasing the FDI limit to 49 per cent from

26 per cent. This move was aimed at bringing in more foreign capital,

technical know-how and exposure to global best practices for the

Indian insurance industry. The increase in foreign investment cap has

already brought in nearly Rs. 15,000 crore into the domestic insurance

sector in the past year. Post the announcement, many global majors

have evinced interest in raising stake in their Indian subsidiaries. The

list of foreign investors who have announced plans to increase stakes

25

in their ventures includes French insurer Axa, Japan's Nippon Life and

Mitsui Sumitomo Insurance, Bupa of United Kingdom and Dutch

insurer Aegon, BNP Paribas Cardif, IAG, Aviva, Standard Life, AIA,

QBE and Fairfax have also announced plans to increase stakes in their

ventures.

b) Abolition of standard prescribed expense limits- The new law eased the

regulation around insurer’s annual management expenses. The earlier

law limited the insurer’s ability to expand into newer territories involving

high set up costs. As per the new provisions IRDA has been authorized

to regulate management expenses of insurers, thereby bringing in

more flexibility to define expense limits.

c) Relaxed provisions for payout to agents -The new law has removed the

restriction of maximum payout to agents or any other intermediary.

Under the new provisions, the regulator is expected to regulate the

commission at a product level, thereby ensuring meeting of product

margins.

d) Task of hiring agents assigned to insurers- The new regulation allows

the regulator to frame rules regarding the agent’s eligibility,

qualifications and other related aspects. In an attempt to make the

agent hiring process more consultative, the insurers have been

permitted to appoint the agents without any intervention from the

regulator.

e) Withdrawal of requirement of deposit with the RBI- Insurers were

earlier required to maintain a deposit of USD 1.5 mn with the Reserve

Bank of India. In the amended bill, this requirement has been waived

off, offering flexibility to new insurers with lower top-line to effectively

deploy this additional fund.

Some recent regulatory reforms introduced by IRDA-

a) IRDA issued revised guidelines in the “File & Use Procedure” in the

general insurance segment - Until very recently, the IRDAI's Guidelines

on "File and Use" Requirements for General Insurance Products of

28th September 2006 governed the procedures and processes for

introducing, modifying and withdrawing general insurance products.

The procedures and processes have now significantly changed with

the introduction of the IRDAI's revised guidelines on "Product Filing

Procedures for General Insurance Products", which were introduced on

18th February 2016. The revised guidelines come into force on 1st

April 2016 and will, therefore, apply to all new general insurance

products filed on or after 1st April 2016. The revised guidelines apply to

all general insurance products except health, personal accident and

travel insurance products which are governed by the IRDA (Health

Insurance) Regulations 2013 and the accompanying guidelines. As per

the revised guidelines, all general insurance products are meant to be

classified as "retail products" or "commercial products" where, broadly,

retail products are those issued to individual customers (and their

26

families) and commercial products are those issued to entities other

than individuals such as firms, companies or trusts. The Revised

Guidelines do not require products approved under the previous File &

Use Guidelines to be re-filed, but if Insurers wish to continue offering

those products, they will need to classify those products as "retail

products" or "commercial products" and file a list of those products

(duly certified by the CEO and Appointed Actuary) with the IRDAI

within 60 days of the issuance of the revised guidelines. Insurers may

also choose to withdraw any of their existing products by following the

procedure set out in the Revised Guidelines.

The revised guidelines set out detailed guiding principles for product

introduction, product design and rating. One of the most significant

changes introduced by the Revised Guidelines is the role of the

Product Management Committee (PMC). All Insurers are required to

form a PMC which shall include "high level officers" of the Insurer and

perhaps including the Appointed Actuary, Chief Underwriting Officer,

Chief Financial Officer, Chief Marketing Officer, Chief Risk Officer,

Compliance Officer and Head Reinsurance. The PMC is required to act

as a ‘self governing’ body to ensure quality product design, filing with

complete compliance of the regulatory requirements and performance

review. The revised guidelines make it clear that the CEO of the

Insurer shall have overall responsibility to ensure that a robust due

diligence process is in place to "mitigate risks of new and current

products. Another significant change is the revised requirements

pertaining to the lawyer's certification of the terms and conditions in

each product.

The revised guidelines have been largely received positively within the

industry. These guidelines are a significant step towards a self-

regulated regime where Insurers will be required to carry out their own

internal due diligence and certification with significantly increased

responsibility on the management of the Insurer.

b) Revised listing guidelines for insurers- IRDA plans to come up with

revised IPO guidelines soon to enable companies enter the capital

markets. Besides improving transparency and corporate governance,

listing would improve governance and disclosure to public and

customer perception. Few big players like HDFC Standard Life and

ICICI Prudential Life Insurance are already firming up plans to raise

funds from the capital markets by diluting equity. As per the norms laid

down earlier by the regulator, it was mandatory for companies in

operation for more than 10 years to list their shares. The regulator

considers the financial performance, capital structure after offer and

solvency margin, among other factors, to give its approval. Though it

was earlier anticipated that life insurers would bring out IPOs soon after

completing 10 years in the industry, none of them did so. That was due

27

to stress in business, low foreign direct investment cap (it has now

been raised to 49 per cent) and poor market conditions, among other

things.

c) IRDA has issued the final norms on corporate governance for the

insurance sector. It aims to strengthen the boards of insurance

companies. As per the new norms, the Board will have to look at a

broad range of areas such as overall direction of business of the

insurance company, including policies, strategies and risk management

across all functions. It would also have to look at projections on capital

requirements, revenue streams, expenses and profitability. While

laying down projections, the Board must address expectations of

shareholders and policyholders. All compliance to the Insurance Act

would rest with the Board. The Board is also required to set up

committees like audit committee, risk management committee,

policyholder protection committee, investment committee, nomination

and remuneration committee and CSR committee.

d) IRDA has formulated a draft regulation, IRDAI (Obligations of Insures

to Rural and Social Sectors) Regulations, 2015, in pursuance of the

amendments brought about under section 32 B of the Insurance Laws

(Amendment) Act, 2015. These regulations impose obligations on

insurers towards providing insurance cover to the rural and

economically weaker sections of the population.

e) IRDAI has set up a 7-member committee for establishment of

insurance service centers with an aim to provide prompt servicing of

policyholder in the most cost efficient manner

f) IRDA has formed two committees to explore and suggest ways to

promote e-commerce in the sector in order to increase insurance

penetration and bring financial inclusion.

g. General insurers are making underwriting losses in the motor and health

segment

Off late, it has been witnessed that General insurers are incurring substantial

losses in their insurance business mainly due to underwriting losses in health

and motor segments. Almost 75 percent of premiums in the industry come

from motor and health segment. This is mainly on account of increasing trend

of claims in health and motor insurance including own damage and third party

claims. While Insurers are making profits in segments like fire, engineering

and others where volumes are relatively small, the health and motor

insurance are not profitable. With rising medical costs, there may be a

requirement of price correction and change in the insurers’ business

strategies to make health and motor insurance profitable in the times to come.

28

Conclusion & Way Forward

The insurance companies have played a major role in the development of the

country. The Insurance sector has supported the Government’s various

developmental activities, be it in providing capital for infrastructure projects or the

implementation of government's insurance schemes. After going through a difficult

phase in recent years, the forecast for the Indian life insurance industry looks

buoyant. The recent spurt of regulatory reforms and positive policy action is

expected to drive the next phase of growth in the insurance industry.

In order to realize its full potential, the industry must focus on building value for all its

stakeholders- Customers, Distributors and Shareholders. Customer centricity and

creating value for customer will go a long way in securing long their term loyalty.

Insures can leverage global best practices from foreign partners to enhance the level

of customer experience through the adoption of new and innovative mobile

applications / technologies. The insurance industry also needs to create significant

value for the distributor. This can be achieved by working towards developing

distributor capabilities and creating an environment which offers them prospects for

long term growth in earnings. The insurers should also aim to create substantial

shareholder value. This can be realized if it successfully caps costs across the value

chain, primarily in the area of claims, by adopting robust claims administration

systems, greater use of analytics for preventing frauds and adopting new methods of

accurately pricing new business. Finally, the insurer should create value for itself by

29

focusing on a sustainable growth. Besides employing the capital effectively, the

insurer should also ensure adequate skilling of its employees and setting practices

aimed to make it future ready.

The insurance sector is now looking forward to a rejuvenated time ahead. A

favorable regulatory framework and positive demographic factors such as growing

middle class, young insurable population and growing awareness of the need for

protection and retirement planning will support the growth of Indian insurance sector.

30

About ICC Founded in 1925, Indian Chamber of Commerce (ICC) is the leading and only National Chamber of

Commerce operating from Kolkata, and one of the most pro-active and forward-looking Chambers in

the country today. Its membership spans some of the most prominent and major industrial groups in

India. ICC is the founder member of FICCI, the apex body of business and industry in India. ICC’s

forte is its ability to anticipate the needs of the future, respond to challenges, and prepare the

stakeholders in the economy to benefit from these changes and opportunities. Set up by a group of

pioneering industrialists led by Mr G D Birla, the Indian Chamber of Commerce was closely

associated with the Indian Freedom Movement, as the first organised voice of indigenous Indian

Industry. Several of the distinguished industry leaders in India, such as Mr B M Birla, Sir Ardeshir

Dalal, Sir Badridas Goenka, Mr S P Jain, Lala Karam Chand Thapar, Mr Russi Mody, Mr Ashok Jain,

Mr.Sanjiv Goenka, among many others, have led the ICC as its President. Currently, Mr. Shiv

Siddhant Kaul is leading the Chamber as it’s President.

The Chamber has proven capabilities in business development across geographical boundaries and

capacity building. ICC is the only Chamber from India to win the first prize in World Chambers

Competition in Quebec, Canada. Also, ICC was selected as one of the top finalists at the 2013 World

Chambers’ Congress in Doha, Qatar. ICC was selected for it’s innovative project - the ‘Better Calcutta

Contest for Schools’, which is run by ICC Calcutta Foundation, a charitable trust set up with the

objective of promoting the well-being of Calcutta. In 2014, ICC was the only Chamber from India to

have bid for the World Chambers’ Congress to be held in 2017, and was one of the 4 Chambers to

give the bid presentation in Tokyo.

The ICC also has a very strong focus upon Economic Research & Policy issues - it regularly

undertakes Macro-economic Surveys/Studies, prepares State Investment Climate Reports and Sector

Reports, provides necessary Policy Inputs & Budget Recommendations to Governments at State &

Central levels.

While the ICC has grown rapidly over the last few years, and expanded it’s operations with the goal of

serving Industry better across regions & states, and effectively addressing issues related to sub-

national growth, the Chamber’s major focus will continue to be on the East & North-East of India.

Being headquartered in Kolkata, the Indian Chamber has worked closely with all the State

Governments in the region, and particularly, has been the Govt. of West Bengal’s partner in progress

over the years. The ICC is recognized by the Ministry of DoNER, Govt. of India as the “Nodal

Chamber” for the North-East, and has worked relentlessly for the progress of the North-East region

which has unparalleled and majorly untapped economic opportunities. The Indian Chamber, along

with the Ministry of DoNER, has been organizing the ‘North-East Business Summit’ , the largest and

most prestigious Summit cum Exposition on India’s North-East region over the years. Till now, 10

Summits have been organized between 2002 and 2014 in places including New Delhi, Guwahati,

Kolkata, Mumbai, Dibrugarh and the Conferences have been able to address key developmental

issues of the NER by bringing together all relevant stakeholders from across sectors & regions. Apart

from being the Partner Chamber in all previous North-East Business Summits organized by the

Ministry, the Indian Chamber has also organized mega trade & investment shows on the North-East

abroad, particularly in South & South-East Asian countries, which, the ICC feels, can be natural trade

partners of the North-East region because of the latter’s strategic location and proximity to these

countries. Several high-profile Delegation Exchanges with South & South-East Asian countries like

Bangladesh, Bhutan, Myanmar, Thailand, Vietnam & Singapore to foster trade through the NER have

been organized quite frequently by the Chamber over the last few years, in sync with the Govt. of

India’s erstwhile ‘Look East’ , and now ‘Act East’ Policy. The ICC strongly believes that if India has to

‘Act East’, the Eastern & the North-Eastern States have to play a significant role in connecting the

31

whole of India with South & South-East Asia, and will gain tremendously through the various

backward & forward linkages , in the process.

The Indian Chamber has set it’s Theme for 2015-’16 as - “Make India”, which refers to the overall

development, both social and economic, of the country through substantial and sustained

improvements in infrastructure & connectivity, manufacturing, healthcare, higher education & skill

development. Further, a comprehensive legal framework (covering labour, the establishment,

governing and closing of companies, environmental rules and quick enforcement of contracts) is

essential to enable entrepreneurial risk-taking and hence development. The Chamber’s Theme is

complementary with the Govt. of India’s ‘Make in India’ campaign. To boost Manufacturing, an

appropriate physical & social infrastructure has to be established. Skill development, education and

healthcare is essential to ensure there is adequate human capital while physical infrastructure

ensures that large supply-chain ecosystems develop.

The ICC headquartered in Kolkata, over the last few years has truly emerged as a National Chamber

of repute, with full-fledged offices in New Delhi, Mumbai, Guwahati, Patna, Bhubaneshwar & Ranchi

functioning efficiently, and building meaningful synergies among Industry and Government by

addressing strategic issues of national significance.

For a Chamber which started in Kolkata and played an inspiring role in India’s Freedom struggle by

bringing indigenous businesses together, it has been a long and eventful journey. Today, as the

Chamber continues to grow across states and regions, it is adhering more strongly to it’s primary aim

of creating a conducive and sustainable environment to enable social, industrial and economic growth

of the country.

ICC’s flagship Annual Conferences include the North-East Business Summit, India Energy Summit,

Convergence India Leadership Summit, Agro Protech, ICC Insurance Summit, ICC Mutual Fund

Summit, to name a few. These Summits take place all across India and abroad, and address key

strategic issues in important sectors like Agriculture, Infrastructure & Energy, Environment,

MSME , Capital Markets & Finance, etc.

As a pro-active Industry Association , thus ICC is directly involved in impacting Policy Making in the

country by bringing Industry & key Regulatory Bodies together , and these Conferences & Exhibitions

go a long way in creating the necessary forward & backward linkages required for industrial &

economic growth. The networking opportunities that the ICC Conferences provide to the participants,

are also significant, and these Forums create newer business opportunities in the process.

Contact :

Indian Chamber of Commerce, Head Office

Dr. Rajeev Singh

Director General-ICC,

4 India Exchange Place

Kolkata 700 001

Phone: 033-22303242

Fax: 033 2231 3380, 3377

Email: [email protected]

Website: www.indianchamber.net

32

About Resurgent India Ltd. DEBT I EQUITY I ADVISORY Resurgent India is a full service investment bank providing customized solutions in the areas of debt, equity and merchant banking. We offer independent advice on capital raising, mergers and acquisition, business and financial restructuring, valuation, business planning and achieving operational excellence to our clients. Our strength lies in our outstanding team, sector expertise, superior execution capabilities and a strong professional network. We have served clients across key industry sectors including Infrastructure & Energy, Consumer Products & Services, Real Estate, Metals & Industrial Products, Healthcare & Pharmaceuticals, Telecom, Media and Technology. In the short period since our inception, we have grown to a 100 people team with a pan-India presence through our offices in New Delhi, Kolkata, Mumbai, and Bangalore. Resurgent is part of the Golden Group, which includes GINESYS (an emerging software solutions company specializing in the retail industry) and Saraf & Chandra (a full service accounting firm, specializing in taxation, auditing, management consultancy and outsourcing). www.resurgentindia.com © Resurgent India Limited, 2015. All rights reserved.

Disclosures This document was prepared by Resurgent India Ltd. The copyright and usage of the document is owned by Resurgent India Ltd. Information and opinions contained herein have been compiled or arrived by Resurgent India Ltd from sources believed to be reliable, but Resurgent India Ltd has not independently verified the contents of this document. Accordingly, no representation or warranty, express or implied, is made as to and no reliance should be placed on the fairness, accuracy, completeness or correctness of the information and opinions contained in this document. Resurgent India ltd accepts no liability for any loss arising from the use of this document or its contents or otherwise arising in connection therewith. The document is being furnished information purposes. This document is not to be relied upon or used in substitution for the exercise of independent judgment and may not be reproduced or published in any media, website or otherwise, in part or as a whole, without the prior consent in writing of Resurgent. Persons who receive this document should make themselves aware of and adhere to any such restrictions.