Embed Size (px)

Citation preview

Feeling the pressure? The challenge of enhancing return on equity

An Economist Intelligence Unit report

sponsored by

The Economist Intelligence UnitThe Economist Intelligence Unit is a specialist publisher serving companies establishing and managing operations across national borders. For 60 years it has been a source of information on business developments, economic and political trends, government regulations and corporate practice worldwide.

The Economist Intelligence Unit delivers its information in four ways: through its digital portfolio, where the latest analysis is updated daily; through printed subscription products ranging from newsletters to annual reference works; through research reports; and by organising seminars and presentations. The firm is a member of The Economist Group.

Copyright© 2008 The Economist Intelligence Unit Limited. All rights reserved. Neither this publication nor any part of it may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without the prior permission of The Economist Intelligence Unit Limited.

All information in this report is verified to the best of the author’s and the publisher’s ability. However, the Economist Intelligence Unit does not accept responsibility for any loss arising from reliance on it.

©TheEconomistIntelligenceUnit2008 �

In March 2008, the Economist Intelligence Unit surveyed 373 C-level, or board-level executives, from around the world about their attitudes to improving return on equity in the current business environment. The survey and paper were sponsored by The Royal Bank of Scotland.Respondents represent a range of industries, including financial services, professional services, manufactur-ing, and information technology. Approximately 50% of respondents represent companies with revenues in excess of US$500m. Around 50% of respondents are chief financial officers, and the remainder are chief executives or other C-level executives.Our editorial team conducted the survey and wrote the paper. The author was Christopher Watts and the editor was Rob Mitchell. The findings expressed in this paper do not necessarily reflect the views of our spon-sors. Our thanks go to the survey respondents and interviewees for their time and insight.

About this research

Feelingthepressure?Thechallengeofenhancingreturnonequity

2 ©TheEconomistIntelligenceUnit2008

Executive summary

l Return on equity is increasingly at risk. As the effects of the tightened credit environment spread from the US to the rest of the world, surveyed for this report are finding their ability to deliver improved return on equity curtailed. Beyond the increased cost and reduced availability of finance, a number of factors are exacerbating the problem. Chief among these are dampened business confi-dence, downward pressure on revenues, adverse exchange rate movements and rising costs.

l There is growing pressure on companies to increase return on equity. Just at a time when return on equity is under threat, investors and other stakeholders are intensifying pressure on management to deliver improved performance on this measure. Indeed, six in ten respondents say that they have experienced increased pressure to boost return on equity since the start of the credit crisis. Although executive management is most likely to drive initiatives to improve return on equity, shareholders and the general competitive environment are also exerting a strong influence.

l Executives are adopting a cautious approach to balance sheet leverage. Senior executives are finding themselves in a corner: where once they would have turned to balance sheet restructur-ing to drive return on equity, today, few have an appetite for this. Instead, many executives are cautiously bracing themselves for the possibility of more difficult times ahead by paying down debt and watching cash more closely. Those that have committed themselves to dividend and share buy-back programmes to increase return on equity plan to keep these on course; cancellation of such pro-grammes to conserve cash is a last-resort option.

l Greater operational efficiency is seen as an important source of improved return on equity. As companies look to the future, they expect to increase their reliance on operational efficiency as a source of enhanced return on equity. This could incorporate a range of initiatives, including greater efficiency of business processes, improved inventory management and a stronger focus on working capital management. Revenue diversifi-cation and enhancement, and renewed efforts to cut costs, are also seen as important tactics.

l For some executives, it is a time for disciplined acquisitions. Corporations with solid balance sheets and strong cash flows may find that the current environment is providing opportunities to drive return on equity by means of acquisitions. Many senior executives questioned for this survey see softening valuations of acquisition targets. In part, this is due to uncertain growth prospects and diminished competition from private equity oper-ators, whose access to abundant cash resources has been cut back. Yet a disciplined approach to acquisitions remains as critical as ever.

Feelingthepressure?Thechallengeofenhancingreturnonequity

©TheEconomistIntelligenceUnit2008 �

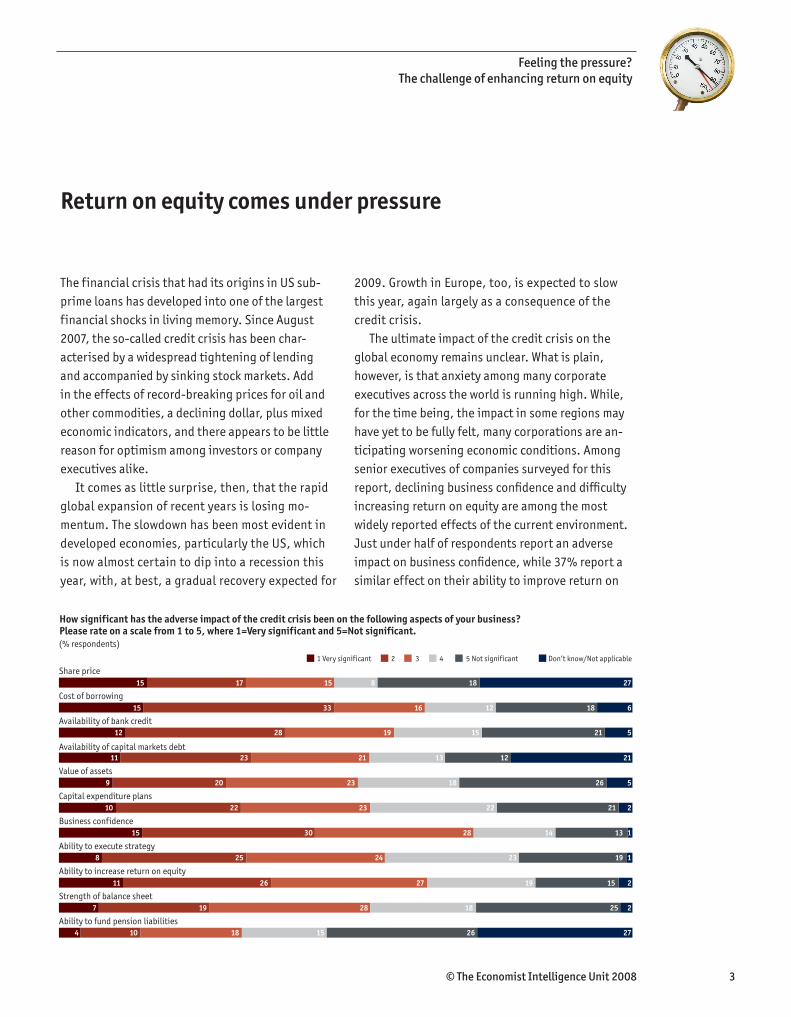

The financial crisis that had its origins in US sub-prime loans has developed into one of the largest financial shocks in living memory. Since August 2007, the so-called credit crisis has been char-acterised by a widespread tightening of lending and accompanied by sinking stock markets. Add in the effects of record-breaking prices for oil and other commodities, a declining dollar, plus mixed economic indicators, and there appears to be little reason for optimism among investors or company executives alike.

It comes as little surprise, then, that the rapid global expansion of recent years is losing mo-mentum. The slowdown has been most evident in developed economies, particularly the US, which is now almost certain to dip into a recession this year, with, at best, a gradual recovery expected for

2009. Growth in Europe, too, is expected to slow this year, again largely as a consequence of the credit crisis.

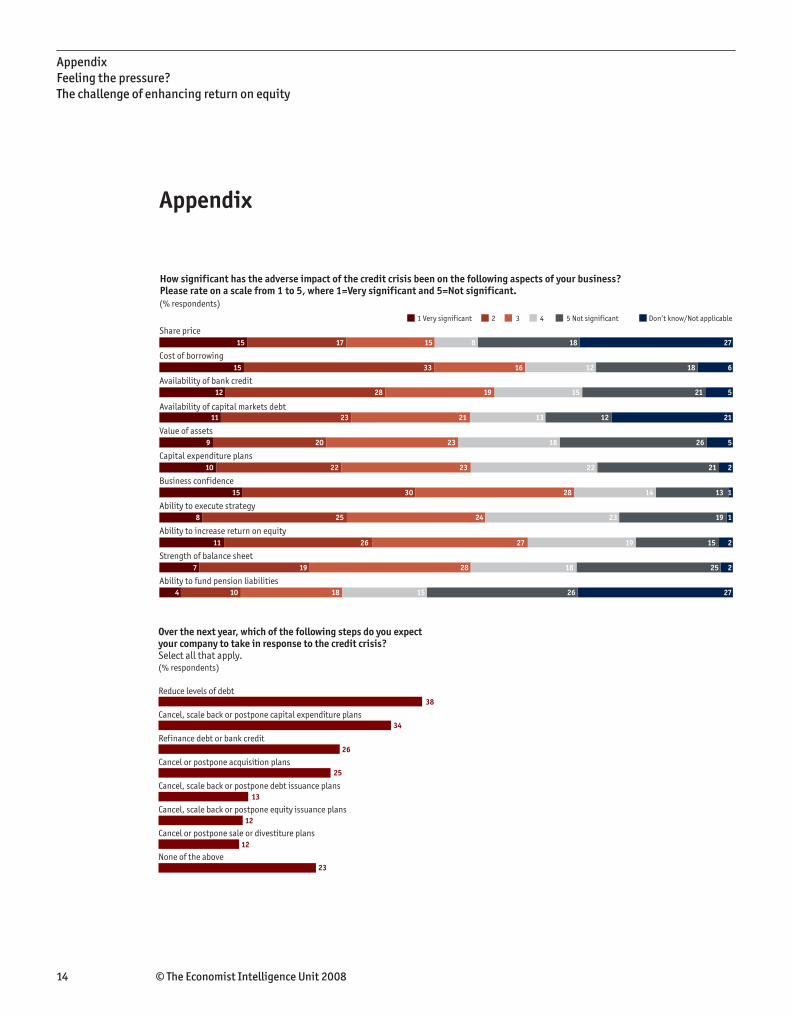

The ultimate impact of the credit crisis on the global economy remains unclear. What is plain, however, is that anxiety among many corporate executives across the world is running high. While, for the time being, the impact in some regions may have yet to be fully felt, many corporations are an-ticipating worsening economic conditions. Among senior executives of companies surveyed for this report, declining business confidence and difficulty increasing return on equity are among the most widely reported effects of the current environment. Just under half of respondents report an adverse impact on business confidence, while 37% report a similar effect on their ability to improve return on

Return on equity comes under pressure

11

11

27261518104

2251828197

21519272611

1192324258

11314283015

22122232210

5261823209

211213212311

52115192812

61812163315

27188151715

(% respondents)

How significant has the adverse impact of the credit crisis been on the following aspects of your business?Please rate on a scale from 1 to 5, where 1=Very significant and 5=Not significant.

Share price

Cost of borrowing

Availability of bank credit

Availability of capital markets debt

Value of assets

Capital expenditure plans

Business confidence

Ability to execute strategy

Ability to increase return on equity

Strength of balance sheet

Ability to fund pension liabilities

1 Very significant 2 3 4 5 Not significant Don’t know/Not applicable

Feelingthepressure?Thechallengeofenhancingreturnonequity

� ©TheEconomistIntelligenceUnit2008

equity. For those companies that carry debt on their balance sheets, the growing cost and shrinking availability of bank credit and capital markets debt are also perceived as a problem.

Herman Agneessens, of KBC, an integrated ban-cassurance group based in Belgium, says that he has already felt the impact of this changed environment. In December 2006, KBC communicated to investors and analysts its average return on equity target of 18.5%. But since then, the worsening environment has increased the challenge of meeting this meas-ure. “The targets we set at the end of 2006 will be more difficult to achieve in the environment that we see around us today,” he says.

For KBC, and many other companies like it, down-ward pressure on revenues is hampering executives’ efforts to deliver targeted return on equity. With a significant proportion of capital markets activity on hold, the company’s investment banking operations face a difficult environment; and in its retail asset management operations, slower customer growth is also set to weigh on revenues. One bright spot, however, is its exposure to central and eastern Europe, which have been less affected by the credit crisis than western Europe, and therefore help to stabilise revenues.

Companies are facing less direct revenue effects, too. For example, while central banks in the US and UK have loosened monetary policy in response to the credit crisis, the European Central Bank

has kept its interest rate steady due to inflation concerns. The resulting strength of the euro versus other currencies, such as the dollar and sterling, is likely to put downward pressure on European exporters’ revenues. The French automotive com-pany Renault, for example, reported in April that unfavourable exchange rates had dampened the revenues of its carmaking division by 2.1% in the first three months of this year.

It is not only revenues that are hit by the crisis – costs are, too. “The main effect of the current crisis is on our [cost of borrowing],” says Patrick Claude. He points out that, for Renault’s short-term commercial paper, the spread over European overnight rates had widened from six basis points (bp, hundredths of a percentage point) to 60 bp between the start of the credit crisis and April; for its European medium-term programme, spreads had widened from 40 bp over EURIBOR to 140 bp; and for its Japanese public debt, from 30 bp over LIBOR to 120 bp. The difference in interest expense (assuming Renault renewed at April 2008 rates the average debt it had outstanding under these pro-grammes in 2007) is equivalent to almost €50m an-nually – a cost burden of around 0.2% of Renault’s end-2007 equity. (The group’s return on equity in 2007 was 12.7%, according to Bloomberg data).

At the same time as return on equity is coming under strain, pressure on company management to increase returns is intensifying. Six out of every ten executives say that they have seen heightened pressure to improve return on equity since the credit crisis first emerged, with 13% reporting that the increase is “significant”. In some cases, this pressure is from inside the company, for example from owner-managers and from supervisory and executive management boards. In other cases, the pressure is from external parties, including institu-tional shareholders and activist investors, such as hedge funds.

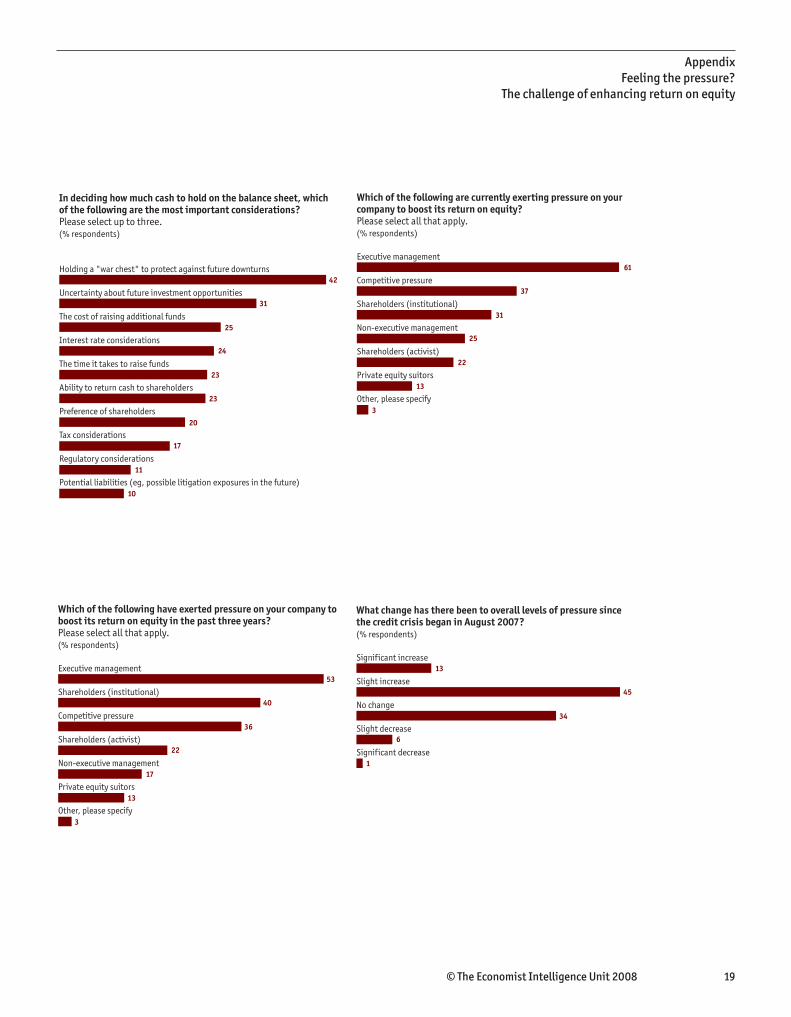

Significant increase

Slight increase

No change

Slight decrease

Significant decrease

What change has there been to overall levels of pressure since the credit crisis began in August 2007? (% respondents)

13

45

34

6

1

Feelingthepressure?Thechallengeofenhancingreturnonequity

©TheEconomistIntelligenceUnit2008 �

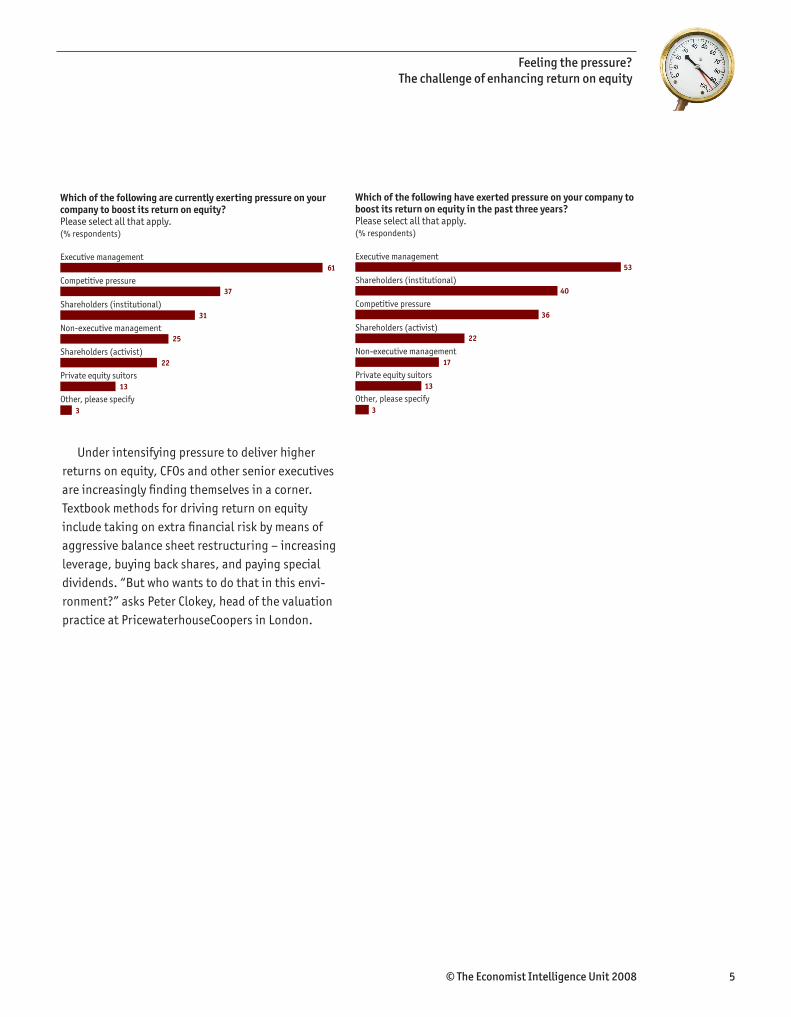

Under intensifying pressure to deliver higher returns on equity, CFOs and other senior executives are increasingly finding themselves in a corner. Textbook methods for driving return on equity include taking on extra financial risk by means of aggressive balance sheet restructuring – increasing leverage, buying back shares, and paying special dividends. “But who wants to do that in this envi-ronment?” asks Peter Clokey, head of the valuation practice at PricewaterhouseCoopers in London.

Executive management

Competitive pressure

Shareholders (institutional)

Non-executive management

Shareholders (activist)

Private equity suitors

Other, please specify

Which of the following are currently exerting pressure on your company to boost its return on equity? Please select all that apply.(% respondents)

61

37

31

25

22

13

3

Executive management

Shareholders (institutional)

Competitive pressure

Shareholders (activist)

Non-executive management

Private equity suitors

Other, please specify

Which of the following have exerted pressure on your company to boost its return on equity in the past three years? Please select all that apply.(% respondents)

53

40

36

22

17

13

3

Feelingthepressure?Thechallengeofenhancingreturnonequity

� ©TheEconomistIntelligenceUnit2008

In the wake of the galloping global economic growth, low interest rates, abundant capital, strong corporate earnings and rising stock mar-kets that characterised much of this decade, many corporate balance sheets are in robust health. As a result, some finance executives have come under pressure to drive returns by leveraging the bal-ance sheet. This was certainly the experience of Mr Agneessens of KBC. “If you read analyst reports from 15 months ago, you will find that we were heavily criticised for under-leveraging our bal-ance sheet, for carrying excess capital, for being too conservative and for not having sufficient risk appetite,” he says.

But now, such demands appear to be easing. Among respondents to our survey, 28% say that they have already noticed diminished pressure from activist investors, such as hedge funds and private equity investors, to increase levels of leverage. A further 43% anticipate this effect. In a related find-ing, almost three-quarters of executives have felt

or anticipate a reduced likelihood of takeover by a private equity operator, which may itself ease the pressure they perceive to increase leverage. Cer-tainly, an increased debt to equity ratio is not gen-erally seen as a favoured way of improving return on equity over the next three years – just 15% say that this will be an important approach for them.

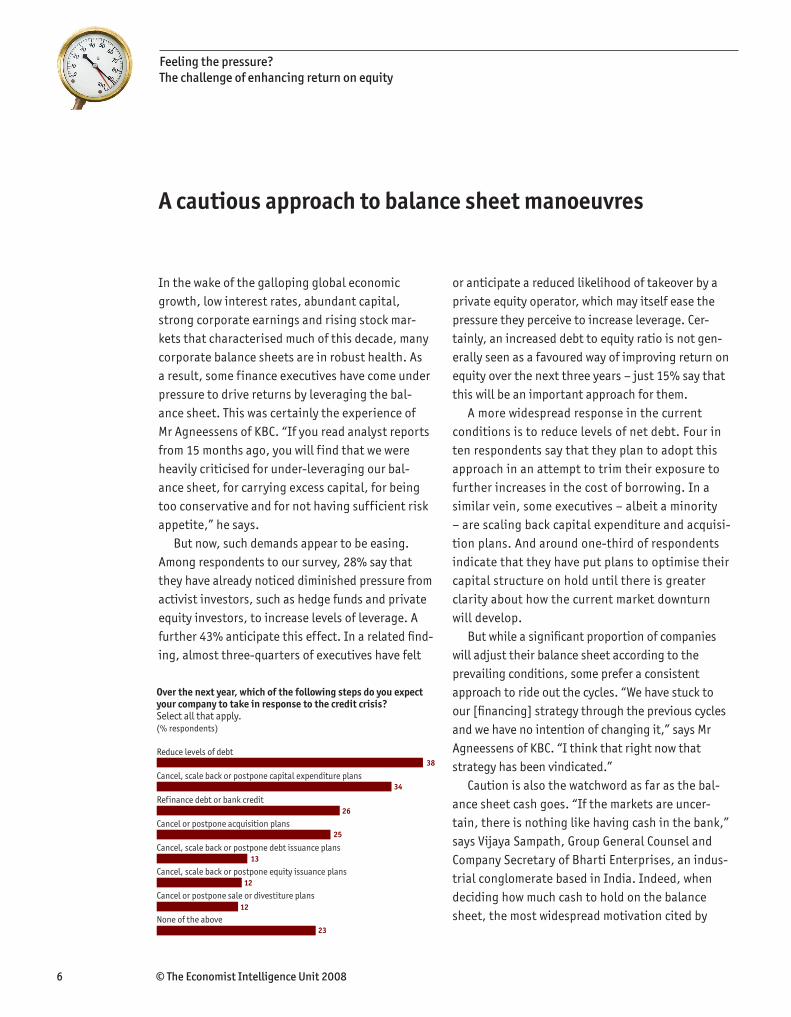

A more widespread response in the current conditions is to reduce levels of net debt. Four in ten respondents say that they plan to adopt this approach in an attempt to trim their exposure to further increases in the cost of borrowing. In a similar vein, some executives – albeit a minority – are scaling back capital expenditure and acquisi-tion plans. And around one-third of respondents indicate that they have put plans to optimise their capital structure on hold until there is greater clarity about how the current market downturn will develop.

But while a significant proportion of companies will adjust their balance sheet according to the prevailing conditions, some prefer a consistent approach to ride out the cycles. “We have stuck to our [financing] strategy through the previous cycles and we have no intention of changing it,” says Mr Agneessens of KBC. “I think that right now that strategy has been vindicated.”

Caution is also the watchword as far as the bal-ance sheet cash goes. “If the markets are uncer-tain, there is nothing like having cash in the bank,” says Vijaya Sampath, Group General Counsel and Company Secretary of Bharti Enterprises, an indus-trial conglomerate based in India. Indeed, when deciding how much cash to hold on the balance sheet, the most widespread motivation cited by

A cautious approach to balance sheet manoeuvres

Reduce levels of debt

Cancel, scale back or postpone capital expenditure plans

Refinance debt or bank credit

Cancel or postpone acquisition plans

Cancel, scale back or postpone debt issuance plans

Cancel, scale back or postpone equity issuance plans

Cancel or postpone sale or divestiture plans

None of the above

Over the next year, which of the following steps do you expect your company to take in response to the credit crisis? Select all that apply.(% respondents)

38

34

26

25

13

12

12

23

Feelingthepressure?Thechallengeofenhancingreturnonequity

©TheEconomistIntelligenceUnit2008 �

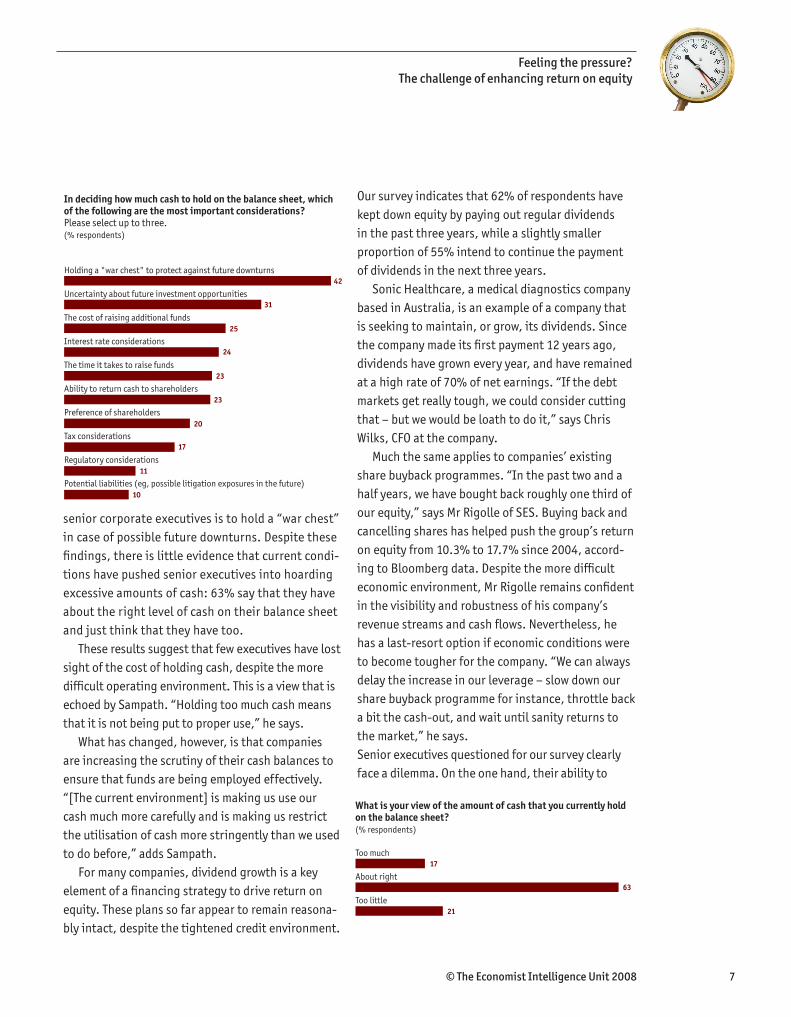

senior corporate executives is to hold a “war chest” in case of possible future downturns. Despite these findings, there is little evidence that current condi-tions have pushed senior executives into hoarding excessive amounts of cash: 63% say that they have about the right level of cash on their balance sheet and just think that they have too.

These results suggest that few executives have lost sight of the cost of holding cash, despite the more difficult operating environment. This is a view that is echoed by Sampath. “Holding too much cash means that it is not being put to proper use,” he says.

What has changed, however, is that companies are increasing the scrutiny of their cash balances to ensure that funds are being employed effectively. “[The current environment] is making us use our cash much more carefully and is making us restrict the utilisation of cash more stringently than we used to do before,” adds Sampath.

For many companies, dividend growth is a key element of a financing strategy to drive return on equity. These plans so far appear to remain reasona-bly intact, despite the tightened credit environment.

Our survey indicates that 62% of respondents have kept down equity by paying out regular dividends in the past three years, while a slightly smaller proportion of 55% intend to continue the payment of dividends in the next three years.

Sonic Healthcare, a medical diagnostics company based in Australia, is an example of a company that is seeking to maintain, or grow, its dividends. Since the company made its first payment 12 years ago, dividends have grown every year, and have remained at a high rate of 70% of net earnings. “If the debt markets get really tough, we could consider cutting that – but we would be loath to do it,” says Chris Wilks, CFO at the company.

Much the same applies to companies’ existing share buyback programmes. “In the past two and a half years, we have bought back roughly one third of our equity,” says Mr Rigolle of SES. Buying back and cancelling shares has helped push the group’s return on equity from 10.3% to 17.7% since 2004, accord-ing to Bloomberg data. Despite the more difficult economic environment, Mr Rigolle remains confident in the visibility and robustness of his company’s revenue streams and cash flows. Nevertheless, he has a last-resort option if economic conditions were to become tougher for the company. “We can always delay the increase in our leverage – slow down our share buyback programme for instance, throttle back a bit the cash-out, and wait until sanity returns to the market,” he says.Senior executives questioned for our survey clearly face a dilemma. On the one hand, their ability to

Holding a "war chest" to protect against future downturns

Uncertainty about future investment opportunities

The cost of raising additional funds

Interest rate considerations

The time it takes to raise funds

Ability to return cash to shareholders

Preference of shareholders

Tax considerations

Regulatory considerations

Potential liabilities (eg, possible litigation exposures in the future)

In deciding how much cash to hold on the balance sheet, which of the following are the most important considerations? Please select up to three.(% respondents)

42

31

25

24

23

23

20

17

11

10

Too much

About right

Too little

What is your view of the amount of cash that you currently hold on the balance sheet? (% respondents)

17

63

21

Feelingthepressure?Thechallengeofenhancingreturnonequity

8 ©TheEconomistIntelligenceUnit2008

CFOs turn to the bottom line

improve return on equity has been hampered by the credit crisis, which has placed revenues under threat and increased interest expense. On the other, many report intensifying pressure to deliver improved return on equity. In the current environment, few companies are willing to restructure the balance sheet to resolve this dilemma. And while there is no magic bullet to solve this problem, our research shows that, increasingly, CFOs and other executives are turning to the bottom line as a way of squaring this circle.

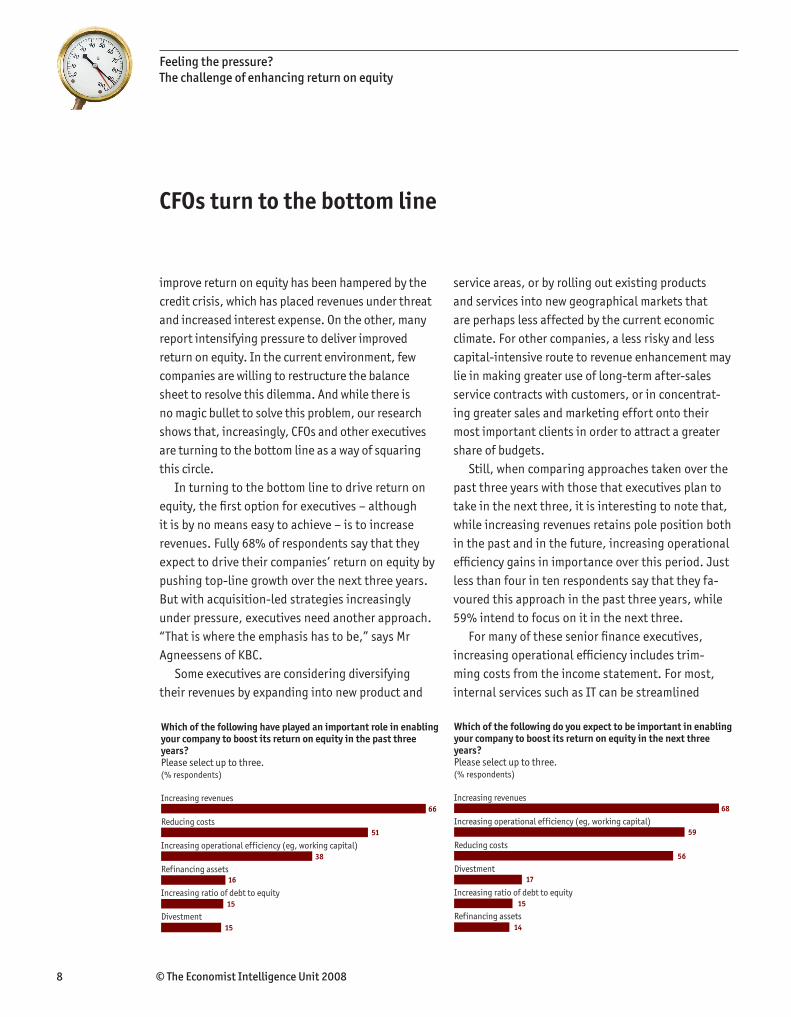

In turning to the bottom line to drive return on equity, the first option for executives – although it is by no means easy to achieve – is to increase revenues. Fully 68% of respondents say that they expect to drive their companies’ return on equity by pushing top-line growth over the next three years. But with acquisition-led strategies increasingly under pressure, executives need another approach. “That is where the emphasis has to be,” says Mr Agneessens of KBC.

Some executives are considering diversifying their revenues by expanding into new product and

service areas, or by rolling out existing products and services into new geographical markets that are perhaps less affected by the current economic climate. For other companies, a less risky and less capital-intensive route to revenue enhancement may lie in making greater use of long-term after-sales service contracts with customers, or in concentrat-ing greater sales and marketing effort onto their most important clients in order to attract a greater share of budgets.

Still, when comparing approaches taken over the past three years with those that executives plan to take in the next three, it is interesting to note that, while increasing revenues retains pole position both in the past and in the future, increasing operational efficiency gains in importance over this period. Just less than four in ten respondents say that they fa-voured this approach in the past three years, while 59% intend to focus on it in the next three.

For many of these senior finance executives, increasing operational efficiency includes trim-ming costs from the income statement. For most, internal services such as IT can be streamlined

Increasing revenues

Increasing operational efficiency (eg, working capital)

Reducing costs

Divestment

Increasing ratio of debt to equity

Refinancing assets

Which of the following do you expect to be important in enabling your company to boost its return on equity in the next three years? Please select up to three.(% respondents)

68

59

56

17

15

14

Increasing revenues

Reducing costs

Increasing operational efficiency (eg, working capital)

Refinancing assets

Increasing ratio of debt to equity

Divestment

Which of the following have played an important role in enabling your company to boost its return on equity in the past three years?Please select up to three.(% respondents)

66

51

38

16

15

15

Feelingthepressure?Thechallengeofenhancingreturnonequity

©TheEconomistIntelligenceUnit2008 �

without having any potential longer-term effects on the company; and shared service centres offer a chance to drive efficiency in areas such as finance and procurement. However, in those cases where CFOs are re-thinking budgets in areas such as sales and marketing, and research and development, they are doing so with caution, for fear of harming their companies’ medium and long-term revenue and earnings prospects.

The larger companies in the survey – those with revenues greater than US$1bn a year – are par-ticularly likely to focus on cost-cutting as a means to increase return on equity; those with revenues below that threshold are more likely to cite revenue growth as their preferred course of action. This finding is likely to reflect the difference between smaller, growing companies, that are looking to

expand, and more mature organisations, which may have less potential to grow.

As part of its mid-term strategy to drive earnings growth, Renault has put clear targets for cost control in place – a programme that has become all the more significant in the current climate. Measures include reducing procurement costs by 14% by the end of this year (using the 2005 level as a base); cutting manufacturing costs by 12% by the end of 2009; and making savings in logistics of 9% by the end of next year. Furthermore, general and administrative expenses are to be brought below 4% of revenues, down from 4.8% in 2007.

Increasing operational efficiency goes beyond cost-cutting, of course. Many CFOs are looking to drive operational efficiency by squeezing more out of existing balance sheet assets. For most, this

Case study

SES:InvestmentgrademantraNot all senior finance executives are paying down debt or putting plans for balance sheet restructuring on hold. Indeed, only around four in ten executives questioned for our survey say that they plan to cut back debt in response to the credit crisis. For those that do not plan to pay down debt, some are continuing with existing plans to invest capital or return cash to shareholders. In many cases, these are companies with solid balance sheets and strong cash flow generation.

Luxembourg-based satellite operator SES is one such company. When Mark Rigolle arrived as CFO in August 2004, he found a corporation deleveraging after having swallowed a big cash-and-stock acquisition three years previously. He also found a business with a very long operating cycle, including lead times of up to five years in capital expenditure and ten-year customer contracts. This meant that cash flows in and out of the company were little affected by short-term, or perhaps even mid-term, factors.

Bolstered by this long-term visibility in revenues, earnings and cash flows, the group decided to boost

return on equity by taking on greater debt and handing more cash to shareholders via share buybacks and dividends. Mr Rigolle set a target debt level of 3.5 times EBITDA (versus around 2.2 times at the end of 2004). “At that level, we would still probably have one [credit rating] notch between us and [sub-]investment grade,” he says.

At the end of 2007, SES closed its books with net debt

of €3.2bn, equivalent to just under three times EBITDA.

SES has bought back around one third of its equity in the

past three years, according to Mr Rigolle. In 2007 alone,

the group ploughed €1.6bn into share repurchases and

dividends. Return on equity soared to 17.7% in 2007,

from 10.3% back in 2004, according to Bloomberg data.

And over the same time-frame, the SES share price has

more than doubled.Despite SES’s strong financial position, Mr Rigolle

remained more than aware that sentiment on the credit market could worsen. Keeping an investment-grade credit rating has been the company’s mantra when it comes to determining the right level of leverage. “We take a very conservative view that as long as we remain investment grade, come credit crunch or whatever, at least we will be less exposed to erratic market sentiment,” he says.

Feelingthepressure?Thechallengeofenhancingreturnonequity

�0 ©TheEconomistIntelligenceUnit2008

includes working capital and tightening the use of cash to lower the interest expense. For CFOs in asset-light businesses, driving operational efficiency may mean better co-ordination of employees around the world, to facilitate transfer of best practice, to unify processes, and to co-ordinate output; for those in asset-intensive industries, it may include allocating capital expenditure to spruce up.

In the case of EC Harris, Mr Morling reports that his company, too, is planning to sharpen its focus on costs. First, the firm is tightening its cash management in order to keep interest expense to a minimum. A second area of focus is asset utilisation. “We are getting far stronger on asset utilisation, to make sure there isn’t an under-utilised resource in one area, that can be deployed elsewhere,” he explains. And third, he says, “we will be taking a far more critical view on performance on a location-by-location basis.”

Mr Agneessens of KBC also plans a renewed push for efficiency. “We have a very strong reputation for cost control but we will look at our expenses even more closely than before to see whether we can do even more,” he says. “It is a combination of setting ambitious targets throughout the organi-sation and monitoring the results very carefully and frequently.”

Feelingthepressure?Thechallengeofenhancingreturnonequity

©TheEconomistIntelligenceUnit2008 ��

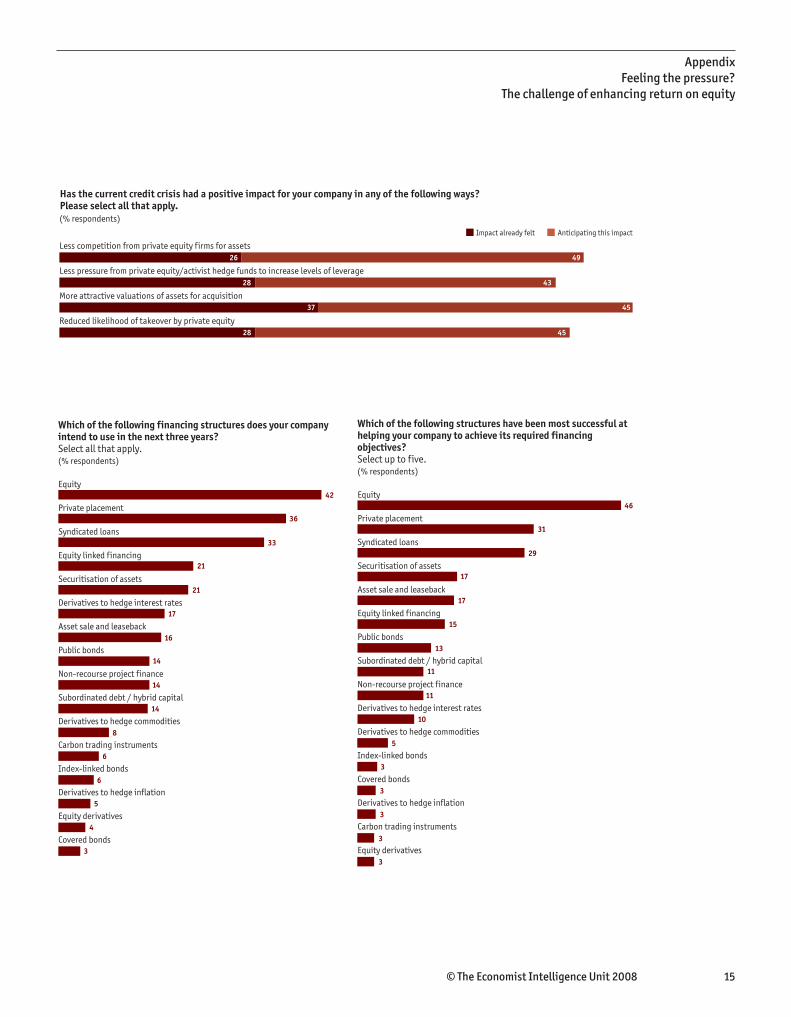

While some senior executives are cautiously bracing themselves for a possible worsening of economic conditions ahead, others see opportunities in the current environment. In one of the clearest-cut indications from executives polled for this report, 82% of executives say that they are feeling – or are expecting to feel – the positive impact from more attractive valuations of acquisition targets. In a related finding, 51% of respondents say that the current credit crisis has made conditions more favourable for the strategic acquisition of assets, despite tightening credit conditions. Only 12% disa-gree with this statement. “We have noticed some reduction in the competition from private equity firms,” says David Pace, CFO of Unicorn Investment Bank, a Bahrain-based Islamic investment bank, which has been making acquisitions not only in its core banking business at group level, but also as an active private equity investor.

In some cases, valuations are under pressure because of an increasingly negative – or, at the very least, uncertain – revenue and earnings outlook. But another significant factor weighing on the valuation of assets is reduced competition from private equity firms, according to executives. Around three-quarters of respondents are feeling – or are anticipating feeling – this effect.

When Sonic Healthcare considered acquisition targets in the course of 2007 – the company closed around US$1bn of deals during the year – Mr Wilks says that it came up against private equity operators bidding top prices. Bolstered by debt, some firms were bidding up to 13 times the target company’s EBITDA, while Sonic was reluctant to bid higher than ten times EBITDA, despite its greater potential to drive returns through synergies. Today, private equity firms’ restricted access to debt may put a more reasonable ceiling on valuations. “We might now see private equity start to suffer as the industry competes for new assets,” he says.

Needless to say, the companies that are now best positioned to make acquisitions are those that can finance deals with minimal recourse to external debt – for example those with strong operating cash flow. Our research suggests that few companies are likely significantly to increase debt in pursuit of acquisitions. An increase of borrowing costs, reduced flexibility, and the difficulty of servicing debt in a downturn were most commonly cited by senior executives as drawbacks of taking on greater levels of debt. “We are presently very comfortable in terms of leverage,” says Mr Sampath of Bharti Enterprises. “But if we have to take a big debt on a foreign acquisition, one [drawback] would be that

A time for disciplined acquisitions

45

45

43

49

28

37

28

26

(% respondents)

Has the current credit crisis had a positive impact for your company in any of the following ways?Please select all that apply.

Less competition from private equity firms for assets

Less pressure from private equity/activist hedge funds to increase levels of leverage

More attractive valuations of assets for acquisition

Reduced likelihood of takeover by private equity

Impact already felt Anticipating this impact

Feelingthepressure?Thechallengeofenhancingreturnonequity

�2 ©TheEconomistIntelligenceUnit2008

AnoteofcautionPeter Clokey, head of the valuation practice at

PricewaterhouseCoopers in the UK, is all too aware

of the effect of the credit crisis on asset valuations.

“Before the credit crunch, we were living in a world

where valuations were driven in many sectors by

the private equity community, especially in the US

and Europe,” he says. “There was a mass of money

and easy access to bank financing.” Auctions for

assets were increasingly being won by private equity

houses, where ordinarily a trade buyer with potential

for synergies would hope to win such a contest. With

large proportions of cheap debt in their financing

packages, though, private equity houses were able

to pay high prices and still expect a decent return on

their investment.

This is no longer the case. With the tightening of

the credit environment since August last year, asset

values have been under pressure. First, an uncertain

future outlook for revenues and earnings is weighing

on valuations; and second, the investment activities of

many private equity houses have been curtailed. “A bit

of froth has come out of the valuation,” points out Mr

Clokey. “There’s now a return to trying to understand

where the value lies.”

While the time may be ripe for trade buyers to

make selective acquisitions, Mr Clokey sounds a note

of caution. For one thing, he says, valuation has

become more difficult. “The one-year multiple [such

as a multiple of EBITDA] becomes a blunter tool at a

time when valuations are falling and there is a threat

to short-term profits.” Moreover, once an investment

has been made, it is now more difficult to retreat.

“If you make an [ill-advised] investment when the

market is hot, you can always exit it to remedy any

errors you make – perhaps even at a profit. Now, it’s

more difficult to do this.”

you have to earn a return on that debt. We need to see that the internal rate of return that we make on the acquisition is good enough.”

To be sure, acquisitions in the current environ-ment will be scrutinised more closely by investors, lenders and supervisory boards alike – increasing the pressure on executives to pursue only those deals that make a clear contribution to strategic, opera-tional and financial goals. Again, discipline is key. Sonic Healthcare’s strategy includes driving return on equity by folding small and mid-sized acquisitions into its infrastructure worldwide. “We try to be disci-plined in terms of return on equity, to drive value for shareholders. We would like to think return on equity will grow within 12 months of completing a strategic acquisition,” says CFO Mr Wilks.

So what effect is the worsening credit environment having? “Perhaps we are becoming a little choosier,” says Mr Wilks. “Of five acquisitions that we would have been completed previously, perhaps now we may only buy the three most synergistic ones.”

Feelingthepressure?Thechallengeofenhancingreturnonequity

©TheEconomistIntelligenceUnit2008 ��

CFOs in the US and beyond are now beginning to feel – or anticipate – the effects of the credit crisis that started in August 2007. For many executives, delivering improved return on equity is a growing challenge. At the same time, pressure on executives to enhance return on equity is intensifying.

But few executives are making significant changes to their long-term financial strategy. For the time being, executives are adopting a cau-tious approach to balance sheet restructuring and leverage, in anticipation of a possible worsening of economic conditions.

Rather than using the balance sheet to drive return on equity, executives appear to be turning to the bottom line in an effort to increase returns. For many, driving organic revenue growth – for example by diversification – is key; most executives are also planning cost efficiency measures.

For some companies with solid balance sheets and strong cash flow, the current environment is a time of opportunities for acquisitions that may drive returns. Executives report that asset valuations are under pressure, in part due to re-duced competition for assets from private equity operators. Still, discipline is key in ensuring that acquisitions make a valuable contribution to return on equity.

Conclusion

Feelingthepressure?Thechallengeofenhancingreturnonequity

�� ©TheEconomistIntelligenceUnit2008

AppendixFeelingthepressure?Thechallengeofenhancingreturnonequity

Appendix

11

11

27261518104

2251828197

21519272611

1192324258

11314283015

22122232210

5261823209

211213212311

52115192812

61812163315

27188151715

(% respondents)

How significant has the adverse impact of the credit crisis been on the following aspects of your business?Please rate on a scale from 1 to 5, where 1=Very significant and 5=Not significant.

Share price

Cost of borrowing

Availability of bank credit

Availability of capital markets debt

Value of assets

Capital expenditure plans

Business confidence

Ability to execute strategy

Ability to increase return on equity

Strength of balance sheet

Ability to fund pension liabilities

1 Very significant 2 3 4 5 Not significant Don’t know/Not applicable

Reduce levels of debt

Cancel, scale back or postpone capital expenditure plans

Refinance debt or bank credit

Cancel or postpone acquisition plans

Cancel, scale back or postpone debt issuance plans

Cancel, scale back or postpone equity issuance plans

Cancel or postpone sale or divestiture plans

None of the above

Over the next year, which of the following steps do you expect your company to take in response to the credit crisis? Select all that apply.(% respondents)

38

34

26

25

13

12

12

23

©TheEconomistIntelligenceUnit2008 ��

AppendixFeelingthepressure?

Thechallengeofenhancingreturnonequity

45

45

43

49

28

37

28

26

(% respondents)

Has the current credit crisis had a positive impact for your company in any of the following ways?Please select all that apply.

Less competition from private equity firms for assets

Less pressure from private equity/activist hedge funds to increase levels of leverage

More attractive valuations of assets for acquisition

Reduced likelihood of takeover by private equity

Impact already felt Anticipating this impact

Equity

Private placement

Syndicated loans

Equity linked financing

Securitisation of assets

Derivatives to hedge interest rates

Asset sale and leaseback

Public bonds

Non-recourse project finance

Subordinated debt / hybrid capital

Derivatives to hedge commodities

Carbon trading instruments

Index-linked bonds

Derivatives to hedge inflation

Equity derivatives

Covered bonds

Which of the following financing structures does your company intend to use in the next three years? Select all that apply.(% respondents)

42

36

33

21

21

17

16

14

14

14

8

6

6

5

4

3

Equity

Private placement

Syndicated loans

Securitisation of assets

Asset sale and leaseback

Equity linked financing

Public bonds

Subordinated debt / hybrid capital

Non-recourse project finance

Derivatives to hedge interest rates

Derivatives to hedge commodities

Index-linked bonds

Covered bonds

Derivatives to hedge inflation

Carbon trading instruments

Equity derivatives

Which of the following structures have been most successful at helping your company to achieve its required financing objectives? Select up to five.(% respondents)

46

31

29

17

17

15

13

11

11

10

5

3

3

3

3

3

�� ©TheEconomistIntelligenceUnit2008

AppendixFeelingthepressure?Thechallengeofenhancingreturnonequity

Current ratio (current assets divided by current liabilities)

Cash to debt ratio

3

12

25

14

11

8

5 5

2 2 23

10

1 10

1 10 0

7

7

22

25

16

46

23

1

3

01 1 1 1 1 1

0 0

4

(% respondents)Please indicate current measures for the following performance ratios.

10.09.59.08.58.07.57.06.56.05.55.04.54.03.53.02.52.01.51.00.50.0

10.09.59.08.58.07.57.06.56.05.55.04.54.03.53.02.52.01.51.00.50.0

617432411

311423311

Significant increase Slight increase No change Slight decrease Significant decrease

(% respondents)

What change has there been to these measures over the past year?

Current ratio

Cash to debt ratio

36

46

15242329

14222132

(% respondents)What is your current debt/equity ratio and what do you expect this to be in one year's time?

Currently

In one year's time

Between 0 and 0.5 Between 0.5 and 1 Between 1 and 2 Between 2 and 5 Between 5 and 10 More than 10

©TheEconomistIntelligenceUnit2008 ��

AppendixFeelingthepressure?

Thechallengeofenhancingreturnonequity

Increased compared with industry average

No change

Decreased compared with industry average

Don’t know

In the past three years, how has your company's debt to equity ratio changed in relation to your industry average? (% respondents)

20

38

26

17

Increased ratio of debt to equity

Increased ratio of equity to debt

No change

What changes have you made to levels of debt and equity in your company over the past three years? (% respondents)

30

36

34

Holding a "war chest" to protect against future downturns

Uncertainty about future investment opportunities

The cost of raising additional funds

Interest rate considerations

The time it takes to raise funds

Ability to return cash to shareholders

Preference of shareholders

Tax considerations

Regulatory considerations

Potential liabilities (eg, possible litigation exposures in the future)

In deciding how much cash to hold on the balance sheet, which of the following are the most important considerations? Please select up to three.(% respondents)

42

31

25

24

23

23

20

17

11

10

Too much

About right

Too little

What is your view of the amount of cash that you currently hold on the balance sheet? (% respondents)

17

63

21

Paid a regular dividend

Paid an extraordinary dividend

Repurchased shares

Which of the following have you used to return cash to shareholders in the past three years?(% respondents)

62

21

26

Paid a regular dividend

Paid an extraordinary dividend

Repurchased shares

Which of the following do you intend to use to return cash to shareholders in the next three years?(% respondents)

55

26

27

�8 ©TheEconomistIntelligenceUnit2008

AppendixFeelingthepressure?Thechallengeofenhancingreturnonequity

1613323512

2311343616

1512244215

2149272712

2029332610

14310293013

21114283213

1511254216

(% respondents)

How satisfied are you with the following aspects of your financial management?Please rate on a scale of 1 to 5, where 1=Very satisfied and 5=Not satisfied.

Overall capital structure

Return on equity

Debt issuance and management

Equity issuance and management

Dividend and share buyback policy

Cash management

Management of assets

Financial risk management

1 Very satisfied 2 3 4 5 Not satisfied Don’t know/Not applicable

11

11

11

11

11

84745

274627

123751

453124

363233

234234

304228

263539

(% respondents)Please indicate whether you agree or disagree with the following statements.

An asset-light business model is currently attractive to us

The tax advantages of debt are a strong incentive for us to increase leverage

We have put plans to optimise our capital structure on hold until there is greater clarity about how the current market downturn will develop

We would consider partnering with private equity firms to acquire assets

We would welcome an attempt by a sovereign wealth fund to take a stake in our company

The current environment has made conditions more favourable for the strategic acquisition of assets

We have been thwarted in our attempts to acquire assets in the past by private equity firms that use more aggressive balance sheet structures

We believe that our equity is currently undervalued by the market

Agree Neither agree nor disagree Disagree

©TheEconomistIntelligenceUnit2008 ��

AppendixFeelingthepressure?

Thechallengeofenhancingreturnonequity

Holding a "war chest" to protect against future downturns

Uncertainty about future investment opportunities

The cost of raising additional funds

Interest rate considerations

The time it takes to raise funds

Ability to return cash to shareholders

Preference of shareholders

Tax considerations

Regulatory considerations

Potential liabilities (eg, possible litigation exposures in the future)

In deciding how much cash to hold on the balance sheet, which of the following are the most important considerations? Please select up to three.(% respondents)

42

31

25

24

23

23

20

17

11

10

Executive management

Competitive pressure

Shareholders (institutional)

Non-executive management

Shareholders (activist)

Private equity suitors

Other, please specify

Which of the following are currently exerting pressure on your company to boost its return on equity? Please select all that apply.(% respondents)

61

37

31

25

22

13

3

Executive management

Shareholders (institutional)

Competitive pressure

Shareholders (activist)

Non-executive management

Private equity suitors

Other, please specify

Which of the following have exerted pressure on your company to boost its return on equity in the past three years? Please select all that apply.(% respondents)

53

40

36

22

17

13

3

Significant increase

Slight increase

No change

Slight decrease

Significant decrease

What change has there been to overall levels of pressure since the credit crisis began in August 2007? (% respondents)

13

45

34

6

1

20 ©TheEconomistIntelligenceUnit2008

AppendixFeelingthepressure?Thechallengeofenhancingreturnonequity

Increasing revenues

Increasing operational efficiency (eg, working capital)

Reducing costs

Divestment

Increasing ratio of debt to equity

Refinancing assets

Which of the following do you expect to be important in enabling your company to boost its return on equity in the next three years? Please select up to three.(% respondents)

68

59

56

17

15

14

Enabling more capital investments

Returning cash to shareholders

Satisfying activist investors

Defending against takeover

Other, please specify

Not applicable; we have not increased leverage

If you have increased leverage in the past three years, what have been the main objectives for this approach? Please select all that apply.(% respondents)

32

16

8

7

7

41

Enabling more capital investments

Returning cash to shareholders

Satisfying activist investors

Defending against takeover

Other, please specify

Not applicable; we do not expect to increase leverage

If you intend to increase leverage in the next year, what will be the main objectives for this approach? Please select all that apply.(% respondents)

35

18

10

7

5

39

Increase in borrowing costs

Issuing debt would lead to reduced financial flexibility in the future

Difficulty servicing debt in the event of a downturn

Negative impact on company's appeal to investors

Potential for lower credit rating

Potential for increase in interest rates

High transaction costs of issuing debt

What do you see as the main drawbacks of increasing leverage at your company?(% respondents)

26

19

16

11

11

11

5

Increasing revenues

Reducing costs

Increasing operational efficiency (eg, working capital)

Refinancing assets

Increasing ratio of debt to equity

Divestment

Which of the following have played an important role in enabling your company to boost its return on equity in the past three years?Please select up to three.(% respondents)

66

51

38

16

15

15

©TheEconomistIntelligenceUnit2008 2�

AppendixFeelingthepressure?

Thechallengeofenhancingreturnonequity

About the respondents

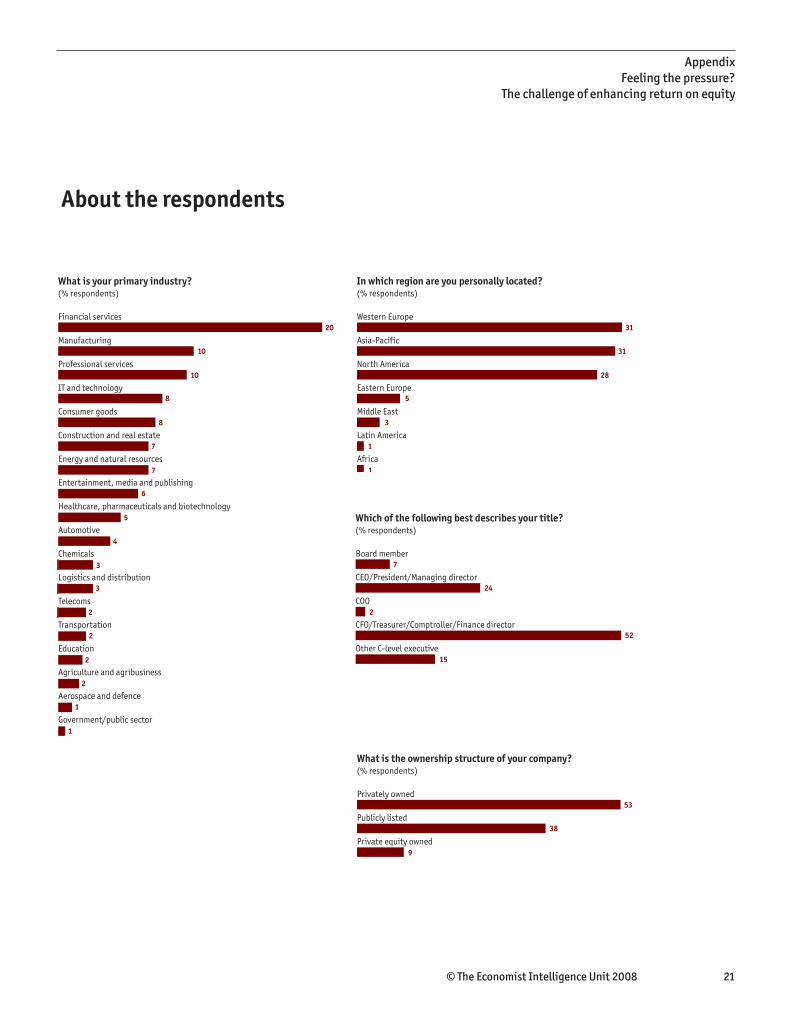

Financial services

Manufacturing

Professional services

IT and technology

Consumer goods

Construction and real estate

Energy and natural resources

Entertainment, media and publishing

Healthcare, pharmaceuticals and biotechnology

Automotive

Chemicals

Logistics and distribution

Telecoms

Transportation

Education

Agriculture and agribusiness

Aerospace and defence

Government/public sector

What is your primary industry? (% respondents)

20

10

10

8

8

7

7

6

5

4

3

3

2

2

2

2

1

1

3

2

Western Europe

Asia-Pacific

North America

Eastern Europe

Middle East

Latin America

Africa

In which region are you personally located? (% respondents)

31

31

28

5

3

1

1

Board member

CEO/President/Managing director

COO

CFO/Treasurer/Comptroller/Finance director

Other C-level executive

Which of the following best describes your title? (% respondents)

7

24

2

52

15

Privately owned

Publicly listed

Private equity owned

What is the ownership structure of your company?(% respondents)

53

38

9

22 ©TheEconomistIntelligenceUnit2008

AppendixFeelingthepressure?Thechallengeofenhancingreturnonequity

$500m or less

$500m to $1bn

$1bn to $5bn

$5bn to $10bn

$10bn or more

What are your company's annual global revenues in US dollars? (% respondents)

49

15

17

7

12

AAA (or equivalent)

AA+

AA

AA-

A+

A

A-

BBB+

BBB

BBB-

BB+

BB

BB-

B+

B

B-

CCC

Not rated

Does your company currently have a credit rating? Select all that apply.(% respondents)

7

7

7

3

2

5

3

3

2

1

2

1

1

1

1

0

0

55

LONDON26 Red Lion SquareLondon WC1R 4HQUnited KingdomTel: +44 (0) 20 7576 8181Fax: +44 (0) 20 7576 8476E-mail: [email protected]

NEW YORK111 West 57th StreetNew York NY 10019United StatesTel: +1 212 698 9745Fax: +1 212 586 0248E-mail: [email protected]

HONG KONG60/F, Central Plaza18 Harbour RoadWanchai Hong KongTel: +852 2802 7288Fax: +852 2802 7638E-mail: [email protected]