Embed Size (px)

Citation preview

التحليل األساسي للمهندسنيشركة األجيال القادمة لالستشارات

1

FGA GUARANTEE

▸ We guarantee to pay your money back with no questions asked if you are not satisfied at the end of this training session

تضمن الشركة إرجاع كامل الرسوم املدفوعة بدون مناقشة في َحال عدمرضا املشارك في الدورة التدريبية

2

السيرة الذاتية

▸ West Virginia بكالوريوس هندسة بترول University

▸ Kuwait Maastricht ماجستير ادارة اعمال Business School

الدورة التاسعة الهيئة العامة لالستثمار ▸

مكتب االستثمار الكويتي في لندن - قسم األسهم ▸األوروبية

الهيئة العامة لالستثمار - قسم املساهمات الخاصة ▸

عضو مجلس ادارة صندوق األجيال في املغرب ▸

عضو مجلس ادارة شركة UNITIC في البوسنة▸

3

▸ Golden Gate Capital مستشار لشركة

مدير عام شركة األجيال القادمة لالستشارات ▸ذ م م

كاتب اسبوعي في القبس االقتصادي ▸

مشارك اسبوعي في قناة العربية االقتصادية▸

أهداف الدورة

قراءة البيانات املالية ▸

تقييم الشركات املدرجة والخاصة ▸

التعرف على الجانب النفسي لعملية االستثمار▸

4

INTRODUCTION- MAJOR CONTRIBUTORS

▸ Benjamin Graham

▸ Professor at Columbia Business School

▸ Graham-Newman Partnership

▸ The Intelligent Investor

▸ Warren Buffett

▸ Studied at Columbia Business School

▸ Buffett Partnership Ltd

▸ Berkshire Hathaway

5

INTRODUCTION

▸ We don't know how to become rich quickly

▸ We don't know technical analysis

▸ We don't know which stocks go up

▸ We focus on understanding stocks like a business owner

▸ We use publicly reported financial reports

▸ We use publicly published reports from investment companies

6

▸ Share price is the beginning of analysis not the end

▸ Share price X number of shares = price of the business or market capitalization

▸ Determine earnings or profits over the coming years

▸ Check the certainty and the quality of the earnings

▸ Divide reasonable business earning by price of the business

▸ Compare return on investments between options

INTRODUCTION-BASIC MODEL OF OPERATION

7

▸ To understand quality and certainty of profits, we look at three main reports:

1. Income Statement

2. Balance Sheet

3. Statements of Cash Flow

INTRODUCTION-BASIC CASES

8

▸ Questions and break

INTRODUCTION - BREAK

9

INCOME STATEMENTBenjamin Graham: In the short run, the market is a voting machine, but in the long run it is a weighing machine

10

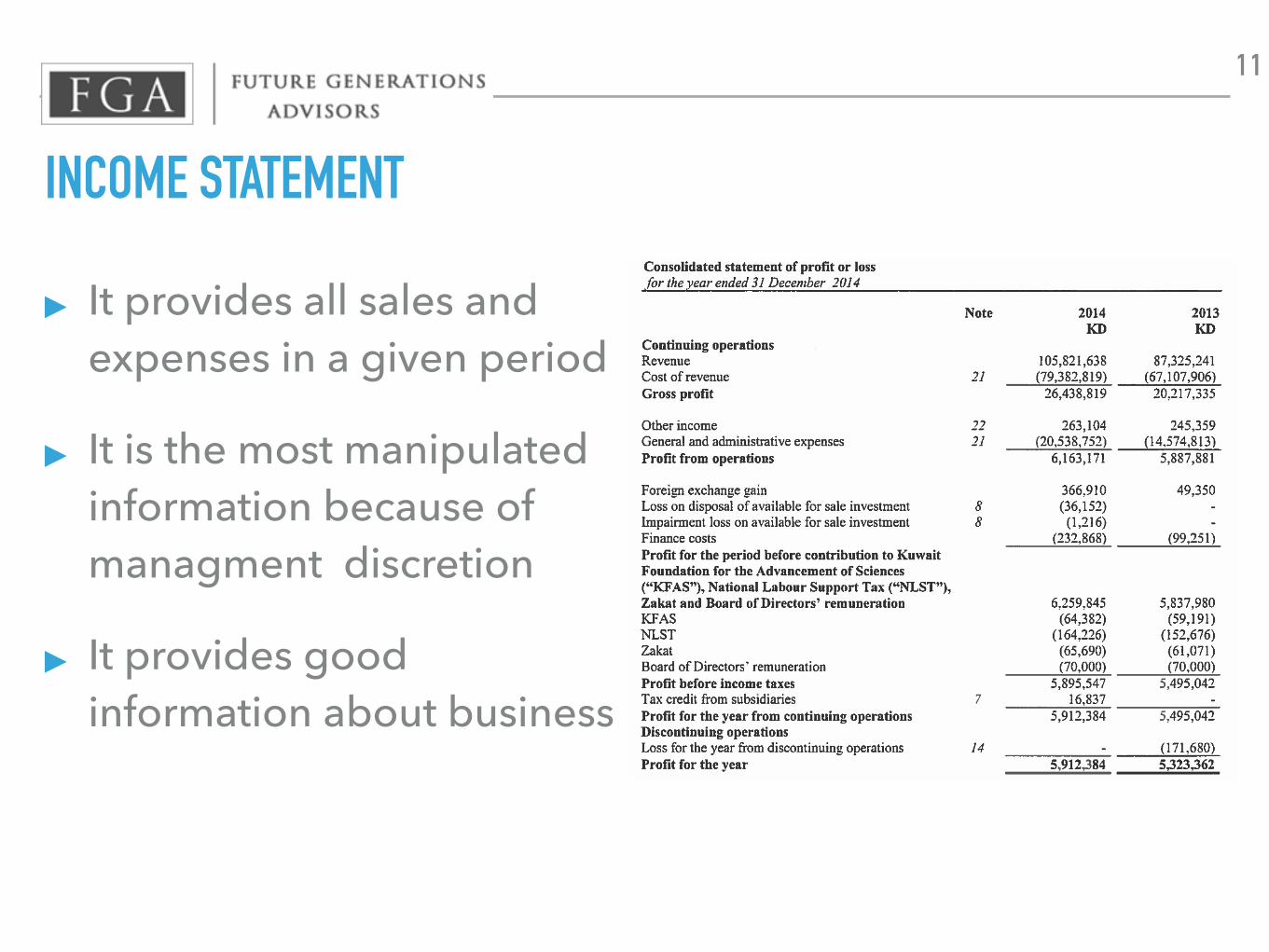

INCOME STATEMENT

▸ It provides all sales and expenses in a given period

▸ It is the most manipulated information because of managment discretion

▸ It provides good information about business

11

INCOME STATEMENT - COMMON SIZE ANALYSIS

Sales 106 100% 1000COGS (79) 75% 750Gross profit 26 25% 250SGA -20 19% 190Operating profit 6 6% 60Tax 0 NA NANet profit 6 6% 60

بالفلس

12

INCOME STATEMENT - MARGINS

▸ Margins can be used to compare businesses in the same sector

▸ Margins can be used to compare over time

▸ Higher profit margin indicates strength

13

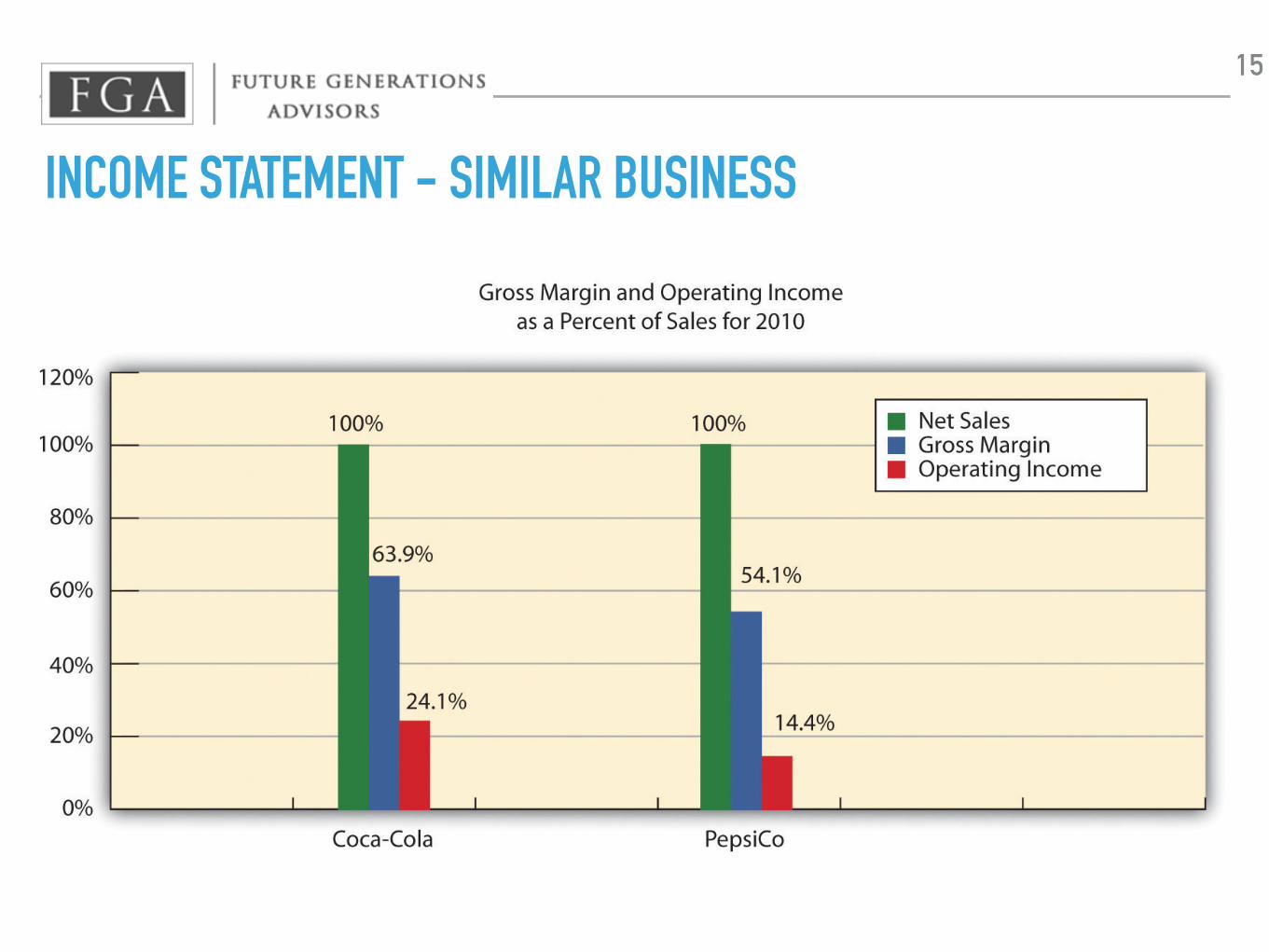

INCOME STATEMENT - SIMILAR BUSINESS

14

INCOME STATEMENT - SIMILAR BUSINESS

15

INCOME STATEMENT - CASES AFTER BREAK

طيران الجزيرة

ياكو الطبية

املجموعة البترولية

زين

16

INCOME STATEMENT - SAME BUSINESS OVER TIME

17

INCOME STATEMENT - MARGINS

▸ Higher gross margin leads to higher net margin

▸ Similar businesses should have similar margins

▸ Margins show managment skills and abilities

▸ Margins are also a function of industry wide effects

18

INCOME STATEMENT - MARGINS ACROSS SECTORS

19

INCOME STATEMENT - MARGINS ACROSS SECTORS

▸ Transportations and retail are low margin businesses

▸ Tech, tobacco, and pharmaceutical are high margin businesses

20

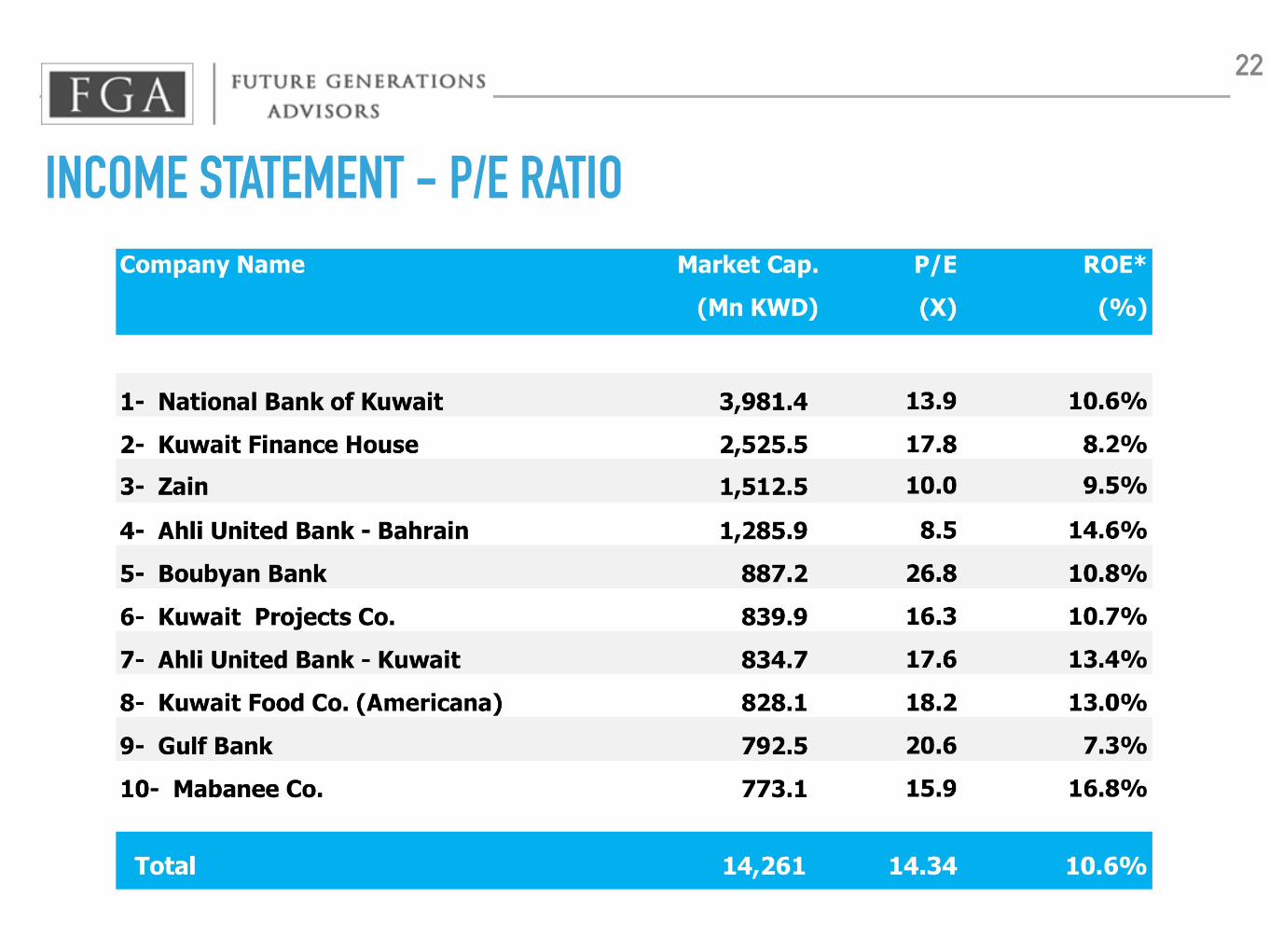

INCOME STATEMENT - P/E RATIO

▸ P/E ratio is most widely used comparison figure

▸ P/E is price of a share divided by earning per share

▸ Earning per share is net profit divided by total number of shares

21

INCOME STATEMENT - P/E RATIO

22

INCOME STATEMENT - ISSUES

▸ Managment have discretion on when to book earnings

▸ Revenue recognition

▸ Risk and rewards transfer

▸ Percentage of completion

▸ Loan allowances at banks

23

INCOME STATEMENT - BREAK

▸ Questions and break

24

INCOME STATEMENT - CONCLUSION

▸ Income statement is used to estimate reasonable business profit in the future

▸ Certainty and quality of profit are main skills that makes a difference

▸ Different people arrive at different numbers

▸ Average intelligent investor can arrive at a reasonable range

25

BALANCE SHEET

26

BALANCE SHEET

▸ It provides assets and debts in a given moment

▸ It shows risks in the business and capital needs

▸ It is very important for financial institutions like banks

27

BALANCE SHEET - DEBT OR LIABILITIES

▸ Always check for size of debt to the business

▸ Normal debt to asset ratio is 1:1

▸ Debt levels depends on the nature of the business

▸ Transportation companies usually carry high debt load

28

BALANCE SHEET - P/BV RATIO

▸ To analyze financial companies, we use book values since they are mostly cash

▸ Insurance, investment companies, and banks trade as a function of book value

▸ Higher risk assets reflects lower P/BV

▸ Higher leverage could also cause a lower P/BV

29

BALANCE SHEET - P/BV RATIO

30

BALANCE SHEET - P/BV RATIO

31

BALANCE SHEET - ISSUES

32

▸ Intangible assets are non cash

▸ Figures are historical

▸ Land is never depreciated

BALANCE SHEET - CASES AFTER BREAK

33

قطر لالستثمار

املستثمرون

السالم

BALANCE SHEET - CONCLUSION

34

▸ Assets on balance sheet should be scrutinized

▸ Debt and high leverage is major source of risks

▸ Book value is a good measure for financial companies

CASH FLOW STATMENT

Benjamin Graham: The primary use of the funds statement [cash flow statement] is to confirm or deny, over time, the amounts shown in the income statement

35

CASH FLOW STATEMENT

▸ This is where we can check earning numbers

▸ Sales see not always cash sales

▸ We can learn about managment

36

CASH FLOW STATEMENT

▸ Free Cash Flow = cash flow from operations - capital expenditure

▸ You can think of FCF as cash profit

▸ Over time FCF and profit should be the same

▸ Market cap/FCF is a ratio that can be used for comparison like P/E ratio

37

CASH FLOW STATEMENT

38

CASH FLOW STATEMENT

▸ Cash flow statement can show what manager is doing with cash from operations

▸ Business could be investing, paying dividends, or buying shares

39

CASH FLOW - BREAK

▸ Questions and break

40

CASH FLOW STATEMENT

▸ Cash flow from operations

▸ Net income + changes in working capital - non cash items

41

CASH FLOW STATEMENT

▸ Cash flow from investing

▸ Selling assets

▸ Buying assets

42

CASH FLOW STATEMENT

▸ Cash flow from financing

▸ Cash from banks and investors

43

CASH FLOW STATEMENT - ISSUES

▸ Buying back shares or paying dividends

▸ Borrowing to buy shares

44

CASH FLOW STATEMENT - CASES AFTER BREAK

فيفا

الزجاج

45

CASH FLOW STATEMENT - CONCLUSION

▸ Cash flow statement is more objective than income statement

▸ Fraud can be detected by reading cash flow statement

46

BASIC RATIOSWarren Buffett: Price is what you pay, value is what you get

47

BASIC RATIOS

▸ P/E or earning yield

▸ P/BV

▸ Dividend yield

▸ EV/EBITDA

▸ EV/(EBITDA-Cap Ex)

▸ Working capital ratios: (days receivables and others)

48

BASIC RATIOS - P/E

49

BASIC RATIOS - P/E

▸ P/E ratio is like pay back in years

▸ P/E ratio of 10 means you will receive your money back after 10 years

▸ You can invert the ratio (E/P) to get earning yield

▸ Earning yield is like estate income ratio

50

BASIC RATIOS - BREAK

▸ Questions and break

51

BASIC RATIOS - P/BV

52

BASIC RATIOS - P/BV

▸ Book value is what you get after paying debt and selling assets

▸ Paying debt doesn't normally happen but selling the business or its shares is the norm

▸ It is like buying a financed car and calculating net value

▸ Such a ratio is useful for comparing financial institutions

▸ It's a historical ratio and usually lower than market values

53

BASIC RATIOS - DIVIDEND YIELD

54

BASIC RATIOS - DIVIDEND YIELD

▸ Dividend is your cash income

▸ It is very difficult to manipulate

▸ It is a more certain and regular source of gains

▸ Banks and insurance company focus on paying regular dividends

55

BASIC RATIOS - EV/EBITDA

56

BASIC RATIOS - EV/EBITDA

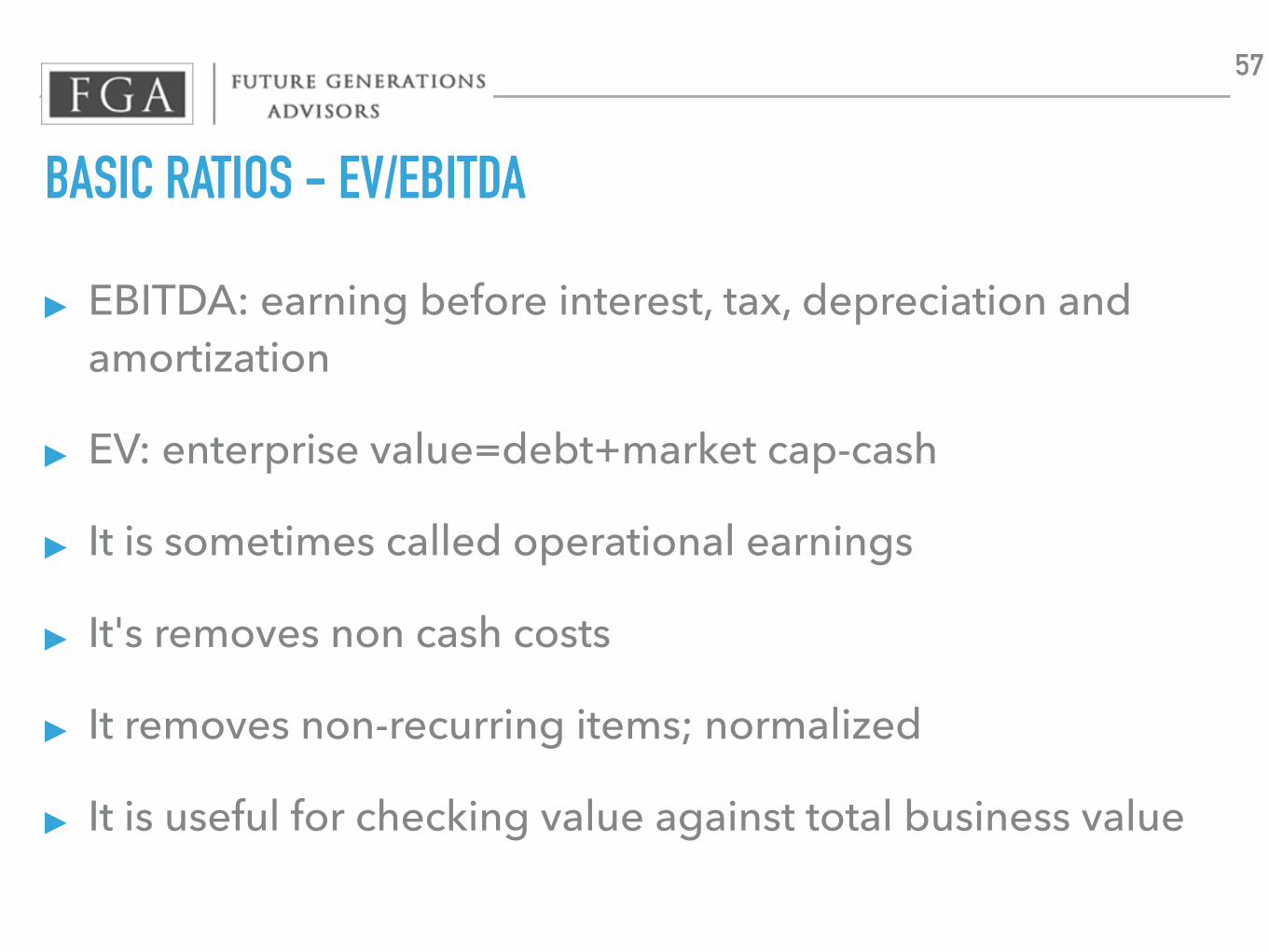

▸ EBITDA: earning before interest, tax, depreciation and amortization

▸ EV: enterprise value=debt+market cap-cash

▸ It is sometimes called operational earnings

▸ It's removes non cash costs

▸ It removes non-recurring items; normalized

▸ It is useful for checking value against total business value

57

BASIC RATIOS - CASES AFTER BREAK

صفقة فيفا

الزجاج

واتسب

58

WORKING CAPITAL RATIOS

59

▸ Days inventory = [inventory/Cost of goods sold] X 365

▸ Days receivables = [receivables/sales] X 365

▸ Days payables = [payables/ COGS] X 365

▸ Cash cycle = days inventory + days receivables - days payables

▸ Shorter cash cycle days is better

▸ This is where most private businesses fail

WORKING CAPITAL RATIOS

60

Kuwait PortlandPayables 23 17Cost of goods sold 60 72Days payables 140 86Inventory 24 8Cost of goods sold 60 72Days inventory 146 41Recievables 16 19Sales 83 83Days recievables 70 84Cash cycle days 76 38

TEMPERAMENTBenjamin Graham: Individuals who cannot master their emotions are ill-suited to profit from the investment process

61

APPENDIX

Benjamin Graham: And back in the spring of 1720, Sir Isaac Newton owned shares in the South Sea Company, the hottest stock in England. Sensing that the market was getting out of hand, the great physicist muttered that he “could calculate the motions of the heavenly bodies, but not the madness of the people.” Newton dumped his South Sea shares, pocketing a 100% profit totaling £7,000. But just months later, swept up in the wild enthusiasm of the market, Newton jumped back in at a much higher price—and lost £20,000 (or more than $3 million in today’s money). For the rest of his life, he forbade anyone to speak the words “South Sea” in his presence.

62

TEMPERAMENT

▸ All knowledge is worthless with the wrong attitude

▸ Prices are only an opportunity to buy or sell when you think it makes sense

▸ You should never be a forced seller

▸ Panic is how people lose money

63

TEMPERAMENT - CASES

64

▸ BP

▸ MasterCard

▸ Visa

▸ Apple

▸ Sequia fund, SEQUX

TEMPERAMENT - BREAK

▸ Questions and break

65

TEMPERAMENT - TOOLS

▸ Investing after market is down by 30%

▸ Investing in steps

▸ Investing when P/E ratio is below 10

▸ Investing in funds

66

APPENDIX

67

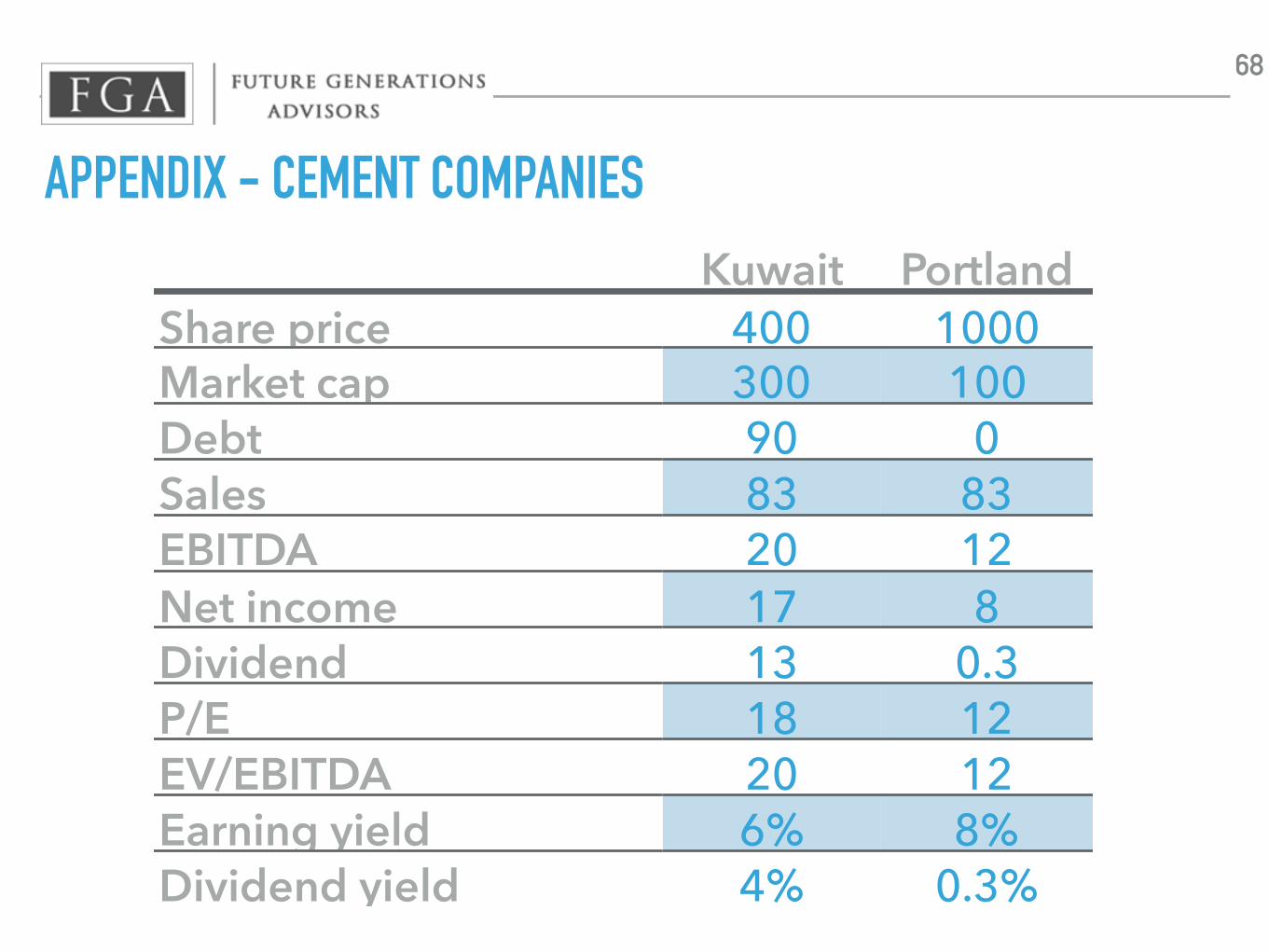

APPENDIX - CEMENT COMPANIES

68

Kuwait PortlandShare price 400 1000Market cap 300 100Debt 90 0Sales 83 83EBITDA 20 12Net income 17 8Dividend 13 0.3P/E 18 12EV/EBITDA 20 12Earning yield 6% 8%Dividend yield 4% 0.3%

APPENDIX - ELECTRONIC GAMES

69

EA ATVIShare price 64 35Market cap 20 25Debt 0 4.3Sales 4.5 4.4EBITDA 0.9 1Net income 0.9 0.8Dividend -- 0.1P/E 26x 24xEV/EBITDA 22x 29xEarning yield 4% 4%Dividend yield -- 0.7%

APPENDIX - OIL COMPANIES

70

XOM CVXShare price 79 85Market cap 314 154Debt 12 24Sales 394 200EBITDA 34 24Net income 32 19P/E 17x 19xEV/EBITDA 10x 7xEarning yield 6% 5%Dividend yield 3.7% 5.0%

APPENDIX - OIL COMPANIES

71

XOM CVX

Share price 79 85

Market cap 314 154

Debt 12 24

Reserves 25 11NPV 176 155

EV/Reserves 1.8x 1.0x

Price per proven barrel 13 16

APPENDIX - CASES AFTER BREAK

72

ياهو

مشرف

ابراج

الدينار

![CHAPTER 3 ENVIRONMENTAL COMPLIANCE …nromoef.gov.in/SMPR/12012016/2.pdfDEC. 2015 [[SIX MONTHLY COMPLIANCE REPORT OF GROUP HOUSING PROJECT AT SECTOR 77, GURGAON, HARYANA]] M/s JANPRIYA](https://img.dokumen.tips/doc/110x75/5b01e2607f8b9af1148ed7bd/chapter-3-environmental-compliance-2015-six-monthly-compliance-report-of.jpg)