Embed Size (px)

DESCRIPTION

Citation preview

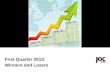

Asset Class Winners and Losers

Highest return

Lowest return

Illustration of the annual performance of various asset classes in relation to one another. This chart is for illustrative purposes only. It does not reflect the performance of any specific investment. Results shown are based on indexes and are illustrative; they assume reinvestment of income and no transaction costs or taxes. Past performance is no guarantee of future results. Index sources: Small Company Stocks—Dimensional Fund Advisors, Inc. (DFA) U.S. Micro Cap Portfolio thereafter; Large Company Stocks—Standard & Poor’s 500®, which is an unmanaged group of securities and considered to be representative of the stock market in general; International Stocks—Morgan Stanley Capital International Europe, Australasia, and Far East (EAFE®) Index; Government Bonds—20-year U.S. Government Bond; Treasury Bills—30-day U.S. Treasury Bill. Indexes are unmanaged. Direct investment cannot be made in an index. Used with permission. ©2003 Ibbotson Associates, Inc. All rights reserved. [Certain portions of this work were derived from the work of Roger G. Ibbotson and Rex Sinquefield.]

19981990 1991 1992 1993 1994 1995 1996 1997 1999 2000 2001 20021989

Internat’lstocks

Large stocks

LT gov’t bonds

Large stocks

LT gov’t bonds

Large stocks

LT gov’t bonds

Large stocks

LT gov’t bonds

LT gov’t bonds

Internat’lstocks

LT gov’t bonds

Large stocks

Internat’lstocks

Large stocks

Internat’lstocks

LT gov’t bonds

30 dayT-bills

30 dayT-bills

30 dayT-bills

30 dayT-bills

30 dayT-bills

30 dayT-bills

LT gov’t bonds

Internat’lstocks

Small stocks

Small stocks

Small stocks

Small stocks

Small stocks

Small stocks

LT gov’t bonds

Large stocks

Internat’lstocks

Small stocks

2003

Smallstocks

Largestocks

LT gov’t bonds

30 dayT-bills

Internat’lstocks

Internat’lstocks

30 dayT-bills

LT gov’tbonds

Smallstocks

Internat’lstocks

Small stocks

Large stocks

LT gov’tbonds

Internat’lstocks

30 dayT-bills

LT gov’tbonds

Smallstocks

Internat’lstocks

Large stocks

30 dayT-bills

Internat’lstocks

BondsCash

Stocks

Analysis of Worst Performance of Merrill Lynch Asset Allocation Models Over 12-, 24- and 36-Month Periods, 1970–2003

Capital Preservation

Income

Income/Growth

Growth

Aggressive Growth

Merrill Lynch Asset Allocation Models

Worst Performance Over a

12-month period

Worst PerformanceOver a

24-Month Period

Worst PerformanceOver a

36-Month period

-11.97%

-18.56%

-22.55%

-27.49%

-32.19%

-4.86%

-8.72%

-11.11%

-14.04%

-17.66%

-0.92%

-3.11%

-4.47%

-7.50%

-11.53%

12-, 24- and 36-Month Periods, 1970–2003

Returns shown are based on indexes and are illustrative; they assume reinvestment of income, no transaction costs or taxes, and that the allocation for each model remained consistent. The allocation models shown are current as of 1/2004. Merrill Lynch has changed the models in the past and may do so in the future. Past performance does not guarantee future results. Index sources: Stocks—Standard & Poor’s 500®, which is an unmanaged group of securities and considered to be representative of the stock market in general; Bonds—20-Year U.S. Government Bond; Cash—30-Day U.S. Treasury Bill. Direct investment cannot be made in an index. Source: Merrill Lynch Investment Strategy and Product Group/Strategic Planning. ©2002 Ibbotson Associates, Inc. All rights reserved. [Certain portions of this work were derived from the work of Roger G. Ibbotson and Rex Sinquefield.]

25

15

10

10

1010

50

45

25

40

25

40

50

80

65

Annual Returns of Merrill Lynch Asset Allocation Models

637 Twelve-Month Rolling Periods, 1950–2003

Results shown are based on indexes and are illustrative; they assume reinvestment of income, no transaction costs or taxes, and that the allocation for each model remained consistent. The allocation models shown are current as of 1/2004. Merrill Lynch has changed the models in the past and may do so in the future. Past performance does not guarantee future results. Index sources: Stocks—Standard & Poor’s 500®, which is an unmanaged group of securities and considered to be representative of the stock market in general; Bonds—20-Year U.S. Government Bond; Cash—30-Day U.S. Treasury Bill. Direct investment cannot be made in an index. Source: Merrill Lynch Investment Strategy and Product Group/Strategic Planning. ©2002 Ibbotson Associates, Inc. All rights reserved. [Certain portions of this work were derived from the work of Roger G. Ibbotson and Rex Sinquefield.]

Best Annual Return

Average Annual Return

Worst Annual Return

Income Income/Growth Growth

37.48%

7.72%

-11.97%

40.05%

8.83%

-18.56%

43.74%

9.55%

-22.55%

47.93%

10.53%

-27.49%

52.16%

11.53%

-32.19%

Asset Allocation:

Bonds

Cash

Stocks

25 2550 40 1545 50 1040 65 1025 80 1010

Capital Preservation Aggressive Growth

Stocks, Bonds, Cash and Inflation

Although stocks on average performed the strongest historically, they were subject to the greatest variance in annual returns.

Summary Statistics 1926–2003

Large Company Stocks

GovernmentBonds 5.4% 9.4%

Inflation 3.0% 4.3%

Cash 3.7% 3.1%

CompoundAnnualReturn

Risk(StandardDeviation) Distribution of Annual Returns

SmallCompany Stocks 12.7% 33.3%

*

5.8%

3.1%

3.8%

ArithmeticAnnualReturn

17.5%

*The 1933 small company stock total return was 142.9%. Results shown are based on indexes and are illustrative; they assume reinvestment of income and no transaction costs or taxes. Past performance is no guarantee of future results. Index sources: Large Company Stocks—Standard & Poor’s 500®, which is an unmanaged group of securities and considered to be representative of the stock market in general; Small Company Stocks—represented by the fifth capitalization quintile of stocks on the NYSE for 1926–1981 and the performance of the Dimensional Fund Advisors (DFA) Small company Fund thereafter; Government Bonds—20-year U.S. Government Bond; Cash—30-day U.S. Treasury Bill; Inflation—Consumer Price Index. Direct investment cannot be made in an index. Used with permission. ©2003 Ibbotson Associates, Inc. All rights reserved. [Certain portions of this work were derived from the work of Roger G. Ibbotson and Rex Sinquefield.]

10.4% 12.4% 20.4%

Stocks, Bonds, Cash and Inflation

Asset types perform differently, with stocks historically outperforming other asset categories. Note that risk and return are related; the higher the return, the greater the risk.

1925–2003EndingWealth

AverageReturn

Hypothetical value of $1 invested at year-end 1925. Results shown are based on indexes and are illustrative; they assume reinvestment of income and no transaction costs or taxes. Past performance is no guarantee of future results. Index sources: Small Company Stocks—represented by the fifth capitalization quintile of stocks on the NYSE for 1926–1981 and the performance of the Dimensional Fund Advisors, Inc. (DFA) U.S. Micro Cap Portfolio thereafter; Large Company Stocks—Standard & Poor’s 500®, which is an unmanaged group of securities and considered to be representative of the stock market in general; Government Bonds—20-year U.S. Government Bond; Cash—30 day U.S. Treasury Bill; Inflation—Consumer Price Index. Direct investment cannot be made in an index. Used with permission. ©2003 Ibbotson Associates, Inc. All rights reserved. [Certain portions of this work were derived from the work of Roger G. Ibbotson and Rex Sinquefield.]

$10 3.0%

Inflation

$.10

$1

$10

$1,000

$10,000$20,000

1925 1935 1945 1955 1965 1975 1985 2003

$100

1995

$18 3.7%

Treasury bills

$61 5.4%

Government bonds 10.4%$2,285Large company stocks $10,954 12.7%Small company stocks

Stocks and Bonds: Risk Versus Return

By investing in a mix of stocks and bonds, you can optimize risk and return.

1970–2003

9%

10%

11%

12%

13%

10% 11% 13% 15% 16% 17% 18%

100% bonds

25% 75% – Minimum risk portfolio

50% 50%

60% 40%

80% 20%

Maximum risk portfolio – 100% stocks

Risk

Re

turn

12% 14%

Risk is measured by standard deviation. Return is measured by arithmetic mean. Risk and return shown are based on indexes and are illustrative; they assume reinvestment of income and no transaction costs or taxes. Past performance is no guarantee of future results. Index sources: Stocks—Standard & Poor’s 500®, which is an unmanaged group of securities and considered to be representative of the stock market in general; Bonds—20-year U.S. Government Bond. Direct investment cannot be made in an index. Used with permission. ©2003 Ibbotson Associates, Inc. All rights reserved. [Certain portions of this work were derived from the work of Roger G. Ibbotson and Rex Sinquefield.]

Reduction of Risk Over Time

Each bar shows the range of compound annual returns for each asset class over the period 1926–2003.

-75%

-50%

-25%

0%

25%

50%

75%

100%

125%

150%

10.4%12.7% 5.4% 3.7%

Small Company Stocks

Large CompanyStocks

GovernmentBonds

Cash

5-Year Holding Periods

1-Year Holding Periods

20-Year Holding Periods

Compound Annual Return

1926–2003

Results shown are based on indexes and are illustrative; they assume reinvestment of income and no transaction costs or taxes. Past performance is no guarantee of future results. Index sources: Small Company Stocks—represented by the fifth capitalization quintile of stocks on the NYSE for 1926–1981 and the performance of the Dimensional Fund Advisors, Inc. (DFA) U.S. Micro Cap Portfolio thereafter; Large Company Stocks—Standard & Poor’s 500®, which is an unmanaged group of securities and considered to be representative of the stock market in general; Government Bonds—20-year U.S. Government Bond; Cash—30-day U.S. Treasury Bill. Direct investment cannot be made in an index. Used with permission. ©2003 Ibbotson Associates, Inc. All rights reserved. [Certain portions of this work were derived from the work of Roger G. Ibbotson and Rex Sinquefield.]

Potential to Reduce Risk or Increase Return

A change in diversification strategy can improve returns without increasing risk.

1970–2003

Risk is measured by standard deviation. Risk and return shown are based on indexes and are illustrative; they assume reinvestment of income, no transaction costs or taxes, and that the allocation for each portfolio remained consistent. Past performance is no guarantee of future results. Index source: Stocks—Standard & Poor’s 500®, which is an unmanaged group of securities and considered to be representative of the stock market in general; Bonds—20-year U.S. Government Bond; Cash—30-day U.S. Treasury Bill. Used with permission. ©2003 Ibbotson Associates, Inc. All rights reserved. [Certain portions of this work were derived from the work of Roger G. Ibbotson and Rex Sinquefield.]

Fixed income portfolio

ReturnRisk

8.6%7.8%

Bonds 85%

Cash 15%

ReturnRisk

8.6%5.7%

Bonds37%

Stocks21%Cash

42%

Lower risk portfolio Higher return portfolio

ReturnRisk

9.4%7.8%

Bonds37%

Stocks35%

Cash28%

Diversified Portfolios and Bear Markets

Mid-1970s Recession

$1,149

$1,014

Jun1976

$500

$1,000

$1,500

Dec1972

Dec1973

Dec1974

Diversified portfolio

Stocks

Diversified portfolios historically perform better through recessions.

1987 Market Crash

Dec1990

$500

$1,000

$1,500

Jun1987

Jun1988

Jun1989

$1,324

$1,227

Diversified portfolio

Stocks

Diversified portfolios also historically perform better through bear markets.

Mid-1970s Recession: December 1972 through June 1976. 1987 Market Crash: June 1987 through December 1990. Diversified Portfolio: 35% stocks, 40% bonds, 25% cash. Hypothetical value of $1,000 invested at month-end December 1972 and June 1987, respectively. Diversification does not eliminate risk of experiencing investment losses. Results shown are based on indexes and are illustrative; they assume reinvestment of income and no transaction costs or taxes. Past performance is no guarantee of future results. Index sources: Stocks—Standard & Poor’s 500®, which is an unmanaged group of securities and considered to be representative of the stock market in general; Bonds—20-year U.S. Government Bond; Cash—30-day U.S. Treasury Bill. Direct investment cannot be made in an index. Used with permission. ©2003 Ibbotson Associates, Inc. All rights reserved. [Certain portions of this work were derived from the work of Roger G. Ibbotson and Rex Sinquefield.]

Bond Market Performance

Bonds typically carry less risk, but on average have not performed as well as stocks historically.

1925–2003

AverageReturn

EndingWealth

Hypothetical value of $1 invested at year-end 1925. Results shown are based on indexes and are illustrative; they assume reinvestment of income and no transaction costs or taxes. Past performance is no guarantee of future results. Index sources: Stocks—Standard & Poor’s 500®, which is an unmanaged group of securities and is considered to be representative of the stock market in general; Corporate Bonds—Salomon Brothers Long-Term High-Grade Corporate Bond Index; Government Bonds—20-year U.S. Government Bond; Municipal Bonds—1926–1984, 20-year prime issues from Salomon Brothers’ Analytical Record of Yields and Yield Spreads and Moody’s Bond Record thereafter; Cash—30-day U.S. Treasury Bill. Direct investment cannot be made in an index. Used with permission. ©2003 Ibbotson Associates, Inc. All rights reserved. [Certain portions of this work were derived from the work of Roger G. Ibbotson and Rex Sinquefield.]

$.10

$1

$10

$100

$1,000

$10,000

1925 1935 1945 1955 1965 1975 1985 2003

3.7%$17.66

Treasury bills

1995

4.4%$27.71

Municipal bonds

5.4%$60.56

Government bonds

5.9%$86.82

Corporate bonds10.4%$2,285

Stocks

Relationship Between Bond Prices and Yields

When yields increase, bond prices decrease.

Price and yield are based on indexes and are illustrative; they assume reinvestment of income and no transaction costs or taxes. Past performance is no guarantee of future results. Index source: Government Bond—20-year U.S. Government Bond. Direct investment cannot be made in an index. Used with permission. ©2003 Ibbotson Associates, Inc. All rights reserved. [Certain portions of this work were derived from the work of Roger G. Ibbotson and Rex Sinquefield.]

$0

$.20

$.40

$.60

$.80

$1.00

$1.20

$1.40

$1.60

1925 1935 1945 1955 1965 1975 1985 2003

0%

2%

4%

6%

8%

10%

12%

14%

16%

Bond yields (%)Bond prices ($)

1995

Stock Performance During Recessions

Although stocks dip through recessions, they typically recover and perform better than before.

1945–2003

Hypothetical value of $1 invested at year-end 1945. Results shown are based on indexes and are illustrative; they assume reinvestment of income and no transaction costs or taxes. Past performance is no guarantee of future results. Index sources: Stocks—Standard & Poor’s 500®, which is an unmanaged group of securities and considered to be representative of the stock market in general; Recessions—National Bureau of Economic Research. Direct investment cannot be made in an index. Used with permission. ©2003 Ibbotson Associates, Inc. All rights reserved. [Certain portions of this work were derived from the work of Roger G. Ibbotson and Rex Sinquefield.]

1949

19541958

1960

19701974 1980

1982

1990

2001

$1

$10

$100

$.10

$1,000

1945 1955 1965 1975 1985 20031995

Shaded regions denote economic recessions

Stocks and Real Assets

Over the past 20 years, stocks on average have outperformed most real assets.

1983–2003

Hypothetical value of $1 invested at year-end 1983. Results shown are based on indexes and are illustrative; they assume reinvestment of income and no transaction costs or taxes. Past performance is no guarantee of future results. Index sources: U.S. Stocks—Standard & Poor’s 500®, which is an unmanaged group of securities and considered to be representative of the stock market in general; International Stocks—Morgan Stanley Capital International Europe, Australasia, and Far East (EAFE®) Index; Commodities—Goldman Sachs Commodity Index; Real Estate—NCREIF Property Index; Gold—1977–1987, Federal Reserve (2nd London fix), Wall Street Journal London P.M. closing price thereafter. Direct investment cannot be made in an index. Used with permission. ©2003 Ibbotson Associates, Inc. All rights reserved. [Certain portions of this work were derived from the work of Roger G. Ibbotson and Rex Sinquefield.]

$1.10

Ending

wealth

$8.26$11.50

$4.28$5.91

Average

return

0.5%

11.1%13.0%

7.5%9.3%

Gold

International stocksU.S. stocks

Real estateCommodities

$.10

$1

$10

$100

1983 1987 1991 1995 1999 2003

Results shown are based on indexes and are illustrative; they assume reinvestment of income and no transaction costs or taxes. Past performance is no guarantee of future results. Index sources: Stocks—Standard & Poor’s 500®, which is an unmanaged group of securities and is considered to be representative of the stock market in general; Bonds—20-year U.S. Government Bond; Cash—U.S. 30-day Treasury Bill; Inflation—Consumer Price Index. Direct investment cannot be made in an index. Used with permission. ©2003 Ibbotson Associates, Inc. All rights reserved. [Certain portions of this work were derived from the work of Roger G. Ibbotson and Rex Sinquefield.]

Returns Before and After Inflation

The following chart illustrates the impact of inflation on performance.

1926–2003

Co

mp

ou

nd

An

nu

al

Re

turn

Bonds Cash

10.4%

5.4%

3.7%

Stocks

7.2%

2.3%

0.7%

0%

4%

8%

12%

10%

6%

2%

Before Inflation

After Inflation

Dollar Cost Averaging

Dollar cost averaging creates opportunities to lower the average cost per share.

0

10

20

30

40

50

1st Quarter 2nd Quarter 3rd Quarter 4th Quarter

Units

$0

$10.00

$20.00

$30.00

$40.00

Price/Unit

$22.50

$21.05

Average share price

DCA price

Number of units

Price

Hypothetical illustration of a $600 quarterly investment. Dollar cost averaging does not ensure a profit or protect against a loss in declining markets. Dollar cost averaging involves continuous investment regardless of fluctuating prices. Investors should consider their financial ability to continue purchases through periods of low price levels. Used with permission. ©2003 Ibbotson Associates, Inc. All rights reserved. [Certain portions of this work were derived from the work of Roger G. Ibbotson and Rex Sinquefield.]

$11.50

$2.71 $2.79

$0

$5

$10

$15

S&P 500 S&P 500 minusbest 17 months

Cash

Dangers of Market Timing

Market timing can be an unreliable and hazardous practice. Missing only a fraction of time can have a profound impact on value.

Hypothetical Value of $1 Invested From Year-End 1983–2003

Results shown are based on indexes and are illustrative; they assume reinvestment of income and no transaction costs or taxes. Past performance is no guarantee of future results. Index sources: S&P 500—Standard & Poor’s 500®, which is an unmanaged group of securities and considered to be representative of the stock market in general; Cash—30-day U.S. Treasury Bill. Direct investment cannot be made in an index. Used with permission. ©2003 Ibbotson Associates, Inc. All rights reserved. [Certain portions of this work were derived from the work of Roger G. Ibbotson and Rex Sinquefield.]

Long-Term Dangers of Market Timing

The impact of mistakes in market timing are more apparent when viewed over the long term.

Hypothetical Value of $1 Invested From Year-End 1925–2003

Results shown are based on indexes and are illustrative; they assume reinvestment of income and no transaction costs or taxes. Past performance is no guarantee of future results. Index sources: S&P 500—Standard & Poor’s 500®, which is an unmanaged group of securities and considered to be representative of the stock market in general; Cash—30-day U.S. Treasury Bill. Direct investment cannot be made in an index. Used with permission. ©2003 Ibbotson Associates, Inc. All rights reserved. [Certain portions of this work were derived from the work of Roger G. Ibbotson and Rex Sinquefield.]

$2,285

$17.42 $17.66$0

$500

$1,000

$1,500

$2,000

S&P 500 S&P 500 minusbest 37 months

Cash

$2,500