Embed Size (px)

Citation preview

© All Rights by InCoPro BVBA BE 0 877.807.636 [email protected] +32 473/38 16 13

InCoPro –D4MDesign for Margin D4M

Data to Information, Insights And Impact D2iii

FINANCIAL ESSENTIALS

FOR STARTUPS

Assessing the sales margins in

new business models

Workshop 3, Business plans, Bryo Leuven 23/05/May 2015

19 december

1

© All Rights by InCoPro BVBA BE 0 877.807.636 [email protected] +32 473/38 16 13

Our Journey:

• Some theoretical concepts– What make accounting difficult: or the difference between cash and profit

– The accounting canvas, the roadmap of our Fin. Plan

– The estimation of your Margin: it’s all about the margin

– Some Metrics for defining and controlling Margin with focus on SAAS

– Wrap up on margin

• New business models and the impact on working capital– Typology of cash-models

– Impact from License model to SAAS model on Cash

– Impact of the SAAS on investments and cash

• Platformization in BtoB market is at least as important as in BtoC

and P2P.

• Some general advises for Starters

2

© All Rights by InCoPro BVBA BE 0 877.807.636 [email protected] +32 473/38 16 13

InCoPro –D4MDesign for Margin D4M

Data to Information, Insights And Impact D2iii

Some theoretical concepts

from praxis 3

© All Rights by InCoPro BVBA BE 0 877.807.636 [email protected] +32 473/38 16 13

What is Profit?

4

1 Profit in terms of Cash:

+ All income received- All expenses paid= “Profit” is what lays in the register at the end or the balance of your bank account

Focus on short term, cash flow, solvency, Will I be able to pay everything at a specific period of time?

2 Profit in terms of accounting results

+ All period related revenues (independent from being actually received)-All period costs (independent from being paid to)= “ profit” of the period, or focus on profitability of the operationsFocus on long term cash flow, solvency, Will I be able to generate enough profit pay back may investors,to finance growth and and being sustainable in the longer run.

© All Rights by InCoPro BVBA BE 0 877.807.636 [email protected] +32 473/38 16 13

The accounting canvas:

The roadmap of our Fin. Plan

19 december

5

Cash PLANNING:Not Cash Flow but all cash movementPlanning of bank accountMoment of Payment

Start cash position:+ Cash Receipts

Revenue (VAT issue)EquityLoans (granted)Disinvestments

- Cash outPaying costs (VAT

Issue)Investments (assets)Payback of loansInterest loansTax

End Balance of cash

INVESTERINGSPLANImmaterial AssetsMaterial Assets Financial AssetsWorking capitalOn Active side: my properties acquired

Exploitation BUDGET (P&L)SalesPurchase directSales MarginIndirect cost

EBITDA (cash result)non- cash movementsDepreciations (Mat.)Amortizations (Imm. )Impairments ( value corrections, ex. bad debts)EBITFinancing costsCorporate TAXResults (Bottom Line)FINANCIERINGSPLAN

CapitalEquityReserves

Retained Profit/Loss Debts:Loans/leasingAre at the passive side of the balance: How paying my properties?

Revenue planningPricing modelsVolume planningCash flow modelsSegmentationSeasonalityGrowth /”Hauchlauf”

Direct Costs (Variable)Direct purchaseSub-contractorsSales effortsSegmentationSeasonalityGrowth /”Hauchlauf”

Break-Even point: Minimal operational activities / sales volumeHow many constraint units we have to sell to get enough margin to cover fix costs?

Balance sheet (BS)State of all property, assets and liabilities,

or the state of your wealth

Indirect Cost (Fix)Indirect staffMarketingOverheadInsuranceFinance costTaxes

Cash flow statement (CS)

Represent the change in your cash position from one period to the other based on the balance sheet movements and their impact on your cash position.

© All Rights by InCoPro BVBA BE 0 877.807.636 [email protected] +32 473/38 16 13

More in one of our next session on

The Financial Essentials for Startups

6

Next Session Probably end of August begin of September2015:4 hours course4 hours starting your plan

© All Rights by InCoPro BVBA BE 0 877.807.636 [email protected] +32 473/38 16 13

Ca

sh p

lan

nin

g

7

1 2 3 4 5 6 7 8 9 10 11 12

Start positie 0 30 000 29 604 1 267 13 788 52 879 45 723 29 943 17 504 31 676 30 963 18 545 28 461 2015

Revenue 0

Income Clients 49 050 60 000 10 000 10 000 25 000 37 500 20 000 16 000 25 000 12 500 265 050

VAT on invoice 21% 10 301 12 600 2 100 2 100 5 250 7 875 4 200 3 360 5 250 2 625 55 661

Directe cost

Direct cost -22 500 -30 000 -7 500 -7 500 -15 000 -22 500 -15 000 -12 000 -15 000 -7 500 -7 500 -162 000

VAT on invoice 15% 0 -3 375 -4 500 -1 125 -1 125 -2 250 -3 375 -2 250 -1 800 -2 250 -1 125 -1 125 -24 300

Indirect Cost

Staff -6 300 -6 300 -6 300 -6 300 -6 300 -6 300 -6 300 -6 300 -6 300 -6 300 -6 300 -69 300

Other -4 192 -4 077 -5 318 -2 567 -2 567 -3 817 -5 067 -2 567 -3 817 -3 067 -3 067 -40 120

VAT on invoice 15% -1 574 -1 557 -1 743 -1 330 -1 330 -1 518 -1 705 -1 330 -1 518 -1 405 -1 405 -16 413

VAT on invoice

VAT balance 0 0 0 -11 128 0 0 -4 297 0 0 -1 957 0 0 -17 383

Bank and Finance costs

Interest -153 -153 -153 -153 -157 -157 -189 -189 -192 -196 -196 -196 -2 083

Investeringen

Notary + Accountant -1 500 -1 500

Startup Acc + KBO etc -1 500 -1 500

IP -50 000 -50 000

Licenses -15 000 0 0 0 0 0 0 0 0 0 0 0 -15 000

Computer -1 500 0 0 0 0 0 0 0 -1 500 0 0 0 -3 000

Office Furniture -2 000 0 0 0 -2 000 0 0 0 0 -1 000 0 0 -5 000

Car 0 0 0 0 0 0 -15 000 0 0 0 0 0 -15 000

Financing

Equity 83 000 83 000

Loan start 0

Loan1 Licenses 15 000 0 0 0 0 0 0 0 0 0 0 0 15 000

Loan2 PC 1 500 0 0 0 0 0 0 0 1 500 0 0 0 3 000

Loan3 furniture 2 000 0 0 0 2 000 0 0 0 0 1 000 0 0 5 000

Loan5 Car 0 0 0 0 0 0 15 000 0 0 0 0 0 15 000

Loan Pay Back

Loan1 Licenses -179 -179 -179 -179 -179 -179 -179 -179 -179 -179 -179 -179 -2 143

Loan2 PC -31 -31 -31 -31 -31 -31 -31 -31 -63 -63 -63 -63 -500

Loan3 furniture -33 -33 -33 -33 -67 -67 -67 -67 -67 -83 -83 -83 -717

Loan4 Car 0 0 0 0 0 0 -417 -417 -417 -417 -417 -417 -2 500

Credit line 0

Creditline for #### 10 000 10 000

Wijziging operations 30 000 29 604 1 267 13 788 52 879 45 723 29 943 17 504 31 676 30 963 18 545 28 461 23 252 23 252

© All Rights by InCoPro BVBA BE 0 877.807.636 [email protected] +32 473/38 16 13

Cash and Profit

Cash thinking Let’s go back to basics:

The cash register of the butcher.

What is in, is cash, what you don’t find in, is called bookkeeping.

Cash thinking is simple.

Why do accountants made it so difficult?Van Doorselaere CEO Van de Velde Schellebelle

8

© All Rights by InCoPro BVBA BE 0 877.807.636 [email protected] +32 473/38 16 13

Cash Conversion Cycle: Cash is King

9

CASH

(in)direct Material (A/P)Investments (A/P)People (Payroll)

Inventory

Customers (A/R)

Collection Purchases

ConversionSales

CASHLoans

Grants

Capital

Taxes

Dividends

Repay/intrests

Shareholders

Banks/others

Gov / ...

Shareholders

Banks

Government

Op

era

tio

nal

No

n-

Op

era

tio

nal

© All Rights by InCoPro BVBA BE 0 877.807.636 [email protected] +32 473/38 16 13

Operational cash conversion cycle or Working Capital

10

Purchase

Accounts Payable Suppliers

Payment Bank

Working Capital needs: Customer Receivables – Suppliers Payables + Inventory

Inventory+ Added Value

Sale

Accounts Receivable Customer

Payment Bank

© All Rights by InCoPro BVBA BE 0 877.807.636 [email protected] +32 473/38 16 13

The focus of working capital

never ends.• Proximus groeit 5,5 procent

• De opbrengsten stijgen 5,5 procent,

• de courante bedrijfskasstroom neemt met 3,8 procent

toe.

• Veel meer werkkapitaal nodig

Zoals dividendzoekers weten, zit er echter een prijskaartje aan

de groei van Proximus. De vrije kasstroom daalde spectaculair

van 119 miljoen naar 8 miljoen euro door hogere investeringsuitgaven en een gestegen behoefte aan

werkkapitaal. Er was onder meer extra werkkapitaal nodig om

de voorraden aan te vullen na de eindejaarscampagne van

2014 en door een stijging van de handelsvorderingen, preciseert

Proximus.

11

© All Rights by InCoPro BVBA BE 0 877.807.636 [email protected] +32 473/38 16 13

First Estimate: of Margin

12

• Revenue = Avg Price (€) per sales unit X quantity of sales units• COGS: Avg variable or direct cost (€) per sales unit X quantity of

sales units (COGS:cost of goods sold)• Margin: Revenue - COGS

Sales unit: number of visitors, orders, order lines, baskets etc. Judged to covering fix-costs and bottom line profit targets in a Break-eve Analysis

Profit: Revenue- CostsProfit: Revenue- COGS– Fix CostProfit: Margin –Fix CostProfit: (P x Q) –(COGS x Q) - FixProfit: Q x (P - COGS)- Fix

© All Rights by InCoPro BVBA BE 0 877.807.636 [email protected] +32 473/38 16 13

Break-even analysis

• Break-Even (the intersection of turnover and total costs) -> TURNOVER = TOTAL COSTS

SALESPRICE PER PIECE x AMOUNT OF PIECES = TOTAL COST

SALESPRICE PER PIECE x AMOUNT OF PIECES = VARIABLE COST + FIXED COST

Classic: FIXED COST/ variable costs

New Economy: indirect /direct costs

• Margin:/Costs per key-unit:

• Key Unit Bottleneck or constraint unit

Fixed Costs (indirect costs)

Break-even point: -------------------------------------

Margin / constraint unit

(Turnover - Direct. Costs )

Margin / constraint unit -------------------------------

Constraint volume

Conclusion:

Margin per bottleneck unit = the key element. D4M is key!

© All Rights by InCoPro BVBA BE 0 877.807.636 [email protected] +32 473/38 16 13

It is all about The Long Tail

14

- Low volume, huge customer base- Nearly no transaction cost- Low specific development cost

- High End Margins- Transaction cost marginal in total price

© All Rights by InCoPro BVBA BE 0 877.807.636 [email protected] +32 473/38 16 13

The relative impact of price changes

on Revenue and Margin

Conclusion:

In high volume, small margin sectors (Long Tail) has relative small

increase of the sales price a huge impact on the relative

incremental evolution of the margin.

P Q Prijsverhoging

Omzet 10,0 € 1.000 10.000 100% 1,0% 10.100 100%

Cost 9,5 € 1.000 9.500 95% 9.500 94%

Marge 0,5 € 1.000 500 5% 20,0% 600 6%

Omzet 10,0 € 1.000 10.000 100% 1,0% 10.100 100%

Cost 9,1 € 1.000 9.100 91% 9.100 90%

Marge 0,9 € 1.000 900 9% 11,1% 1.000 10%

Omzet 10,0 € 1.000 10.000 100% 1,0% 10.100 100%

Cost 8,0 € 1.000 8.000 80% 8.000 79%

Marge 2,0 € 1.000 2.000 20% 5,0% 2.100 21%

Omzet 10,0 € 1.000 10.000 100% 1,0% 10.100 100%

Cost 7,0 € 1.000 7.000 70% 7.000 69%

Marge 3,0 € 1.000 3.000 30% 3,3% 3.100 31%

P Q Prijsdaling

Omzet 10,0 € 1 000 10 000 100% -1,0% 9 900 98%

Cost 9,5 € 1 000 9 500 95% 9 500 94%

Marge 0,5 € 1 000 500 5% -20,0% 400 4%

Omzet 10,0 € 1 000 10 000 100% -1,0% 9 900 98%

Cost 9,0 € 1 000 9 000 90% 9 000 89%

Marge 1,0 € 1 000 1 000 10% -10,0% 900 9%

Omzet 10,0 € 1 000 10 000 100% -1,0% 9 900 98%

Cost 8,0 € 1 000 8 000 80% 8 000 79%

Marge 2,0 € 1 000 2 000 20% -5,0% 1 900 19%

Omzet 10,0 € 1 000 10 000 100% -1,0% 9 900 98%

Cost 7,0 € 1 000 7 000 70% 7 000 69%

Marge 3,0 € 1 000 3 000 30% -3,3% 2 900 29%

© All Rights by InCoPro BVBA BE 0 877.807.636 [email protected] +32 473/38 16 13

The absolute impact of price

changes on Revenue and MarginPrijsdaling en hoeveel volume groei nodig

P Q

Omzet 10,0 € 1 000 10 000 100% -1,0% 9,9 € 1 250 12 375 100%

Cost 9,5 € 1 000 9 500 95% 0,0% 9,5 € 1 250 11 875 95%

Marge 0,5 € 1 000 500 5% -20,0% 0,4 € 25% 1 250 500 5%

Omzet 10,0 € 1 000 10 000 100% -1,0% 9,9 € 1 111 11 000 -28%

Cost 9,0 € 1 000 9 000 90% 0,0% 9,0 € 1 111 10 000 -76%

Marge 1,0 € 1 000 1 000 10% -10,0% 0,9 € 11% 1 111 1 000 -123%

Omzet 10,0 € 1 000 10 000 100% -1,0% 9,9 € 1 053 10 421 -28%

Cost 8,0 € 1 000 8 000 80% 0,0% 8,0 € 1 053 8 421 -76%

Marge 2,0 € 1 000 2 000 20% -5,0% 1,9 € 5,3% 1 053 2 000 -123%

Omzet 10,0 € 1 000 10 000 100% -1,0% 9,9 € 1 034 10 241 -28%

Cost 7,0 € 1 000 7 000 70% 0,0% 7,0 € 1 034 7 241 -76%

Marge 3,0 € 1 000 3 000 30% -3,3% 2,9 € 3,4% 1 034 3 000 -123%

Conclusion:

By low margin products, a relative small decrease of prices, can

only be compensated with a relative big increase in volumes to

maintain the absolute margin.

© All Rights by InCoPro BVBA BE 0 877.807.636 [email protected] +32 473/38 16 13

Margin estimation:

Easy said difficult in praxis

Complexity: Q &P & Cogs

• Product mix

• Market segments (geographic, types etc.)

• Distributions segments (online, shop in shop, direct/indirect,

commissions etc.)

• conversion rates: sales funnel (Prospects-> Customers)

Sensitivity analysises are helping to distinguish.

The difference is made in the details of a business.

You don’t have to know all details but you have to know which detail you have to know in detail.

17

Profit: Q x (P - COGS)- Fix

Margin: Q x(P-CoGS)

© All Rights by InCoPro BVBA BE 0 877.807.636 [email protected] +32 473/38 16 13

Types of products in a SAAS

• Software license

• Pay as use (consumption)

• Services

• Maintenance

• Education

• Support

• Space

• Etc.18

© All Rights by InCoPro BVBA BE 0 877.807.636 [email protected] +32 473/38 16 13

Segmentation with focus on

margin is key

19

© All Rights by InCoPro BVBA BE 0 877.807.636 [email protected] +32 473/38 16 13

Some statements about

segmentation and growth• Your best customers spend to 30x more than the Avg

• Your best customers spend to 5x more per order

- > focus on adopting tactics to increase average

order value -> clear opportunity

• The typical online store gets 43% of revenue from

repeat purchases,

-> put enough to encourage repeat buying?

• Getting the first $1 million of revenue is hard.

• Relative growth is one, but absolute growth the other.

The more mature the lower the growth rate but the

absolute value of growth is still impressive.

20

© All Rights by InCoPro BVBA BE 0 877.807.636 [email protected] +32 473/38 16 13

The sales funnel process:

Remark: what with VAT? Included or Not?

21

Jan Feb Mrt Apr

Number of communication readers 10 000 20 000 30 000 40 000

conversion 10% 20% 25% 30%

Number of Webpage visitors 1 000 4 000 7 500 12 000

conversion 10% 15% 10% 20%

Effective buyers 100 600 750 2 400

Number of orders (conversion) 1 2 2 4

Number of products 100 1 200 1 500 9 600

Avg Value of an orderline/item 10 € 10 € 10 € 10 €

Revenu 1 000 € 12 000 € 15 000 € 96 000 €

© All Rights by InCoPro BVBA BE 0 877.807.636 [email protected] +32 473/38 16 13 22

Don’t forget the VAT consequences for your listed Prices and in your Cash planning.Be happy, from now on you may play Tax collector.

What with VAT?

© All Rights by InCoPro BVBA BE 0 877.807.636 [email protected] +32 473/38 16 13

The Customer Lifecycle buckets:

• Acquisition:

• Conversion:

• Retention:

• Reactivation:

• Relative market share

Growth activities along the

customer lifecycle

23

© All Rights by InCoPro BVBA BE 0 877.807.636 [email protected] +32 473/38 16 13

Churn a key metric in long tail

businessesDefinition:

• the number of customers churning in a period

• the amount of revenue you lose from those customers

in that period.

24

© All Rights by InCoPro BVBA BE 0 877.807.636 [email protected] +32 473/38 16 13

Churn a key metric in long tail businessesSome difficulties with determination of the measurement

period:

– It should be large enough to minimize huge

variance.

– It shouldn’t be overly long.

– Seasonality

– the effect grows becoming a matured company.

25

© All Rights by InCoPro BVBA BE 0 877.807.636 [email protected] +32 473/38 16 13

Churn and

Customer activation• Customers are signing up and paying, not “fully

activated” and fall-out unsatisfied.

• The longer-term customers, the happy ones who are

successfully using your product, who suddenly quit

your platform.

• What is churn and what not? The only way to get clear

insights is detailed analysis and goods segmentations.

26

© All Rights by InCoPro BVBA BE 0 877.807.636 [email protected] +32 473/38 16 13

Customer Lifetime Value (CLV)

27

• Customer lifetime value (CLV):The present

value of the future cash flows attributed to the

customer during his/her entire relationship with

the company

CLV =Avg Monthly Revenue per Customer ∗ Gross Margin per Customer

Monthly Churn Rate

Remarck: you can subtract retention cost when it is not in de marging.

© All Rights by InCoPro BVBA BE 0 877.807.636 [email protected] +32 473/38 16 13

What is the right price?

28

Based on :Priceintelligently.com

© All Rights by InCoPro BVBA BE 0 877.807.636 [email protected] +32 473/38 16 13

What is the right price?

29

Based on :Priceintelligently.com

© All Rights by InCoPro BVBA BE 0 877.807.636 [email protected] +32 473/38 16 13

What is the right

price?Freemiums are to be handle carefully• If you do choose to provide a freemium offering, be aware of

the fact that freemium is a customer acquisition strategy, not a

revenue model.

• Offering a freemium plan a hefty marketing expense, as

conversion rates to paid are typically very low. (look to LinkedIn

users around you, bookbone)

• The fact is that only 38% of SaaS companies offer freemium

plans.

30

© All Rights by InCoPro BVBA BE 0 877.807.636 [email protected] +32 473/38 16 13

Clear tariff plans

Salesforce.com’s

CRM pricing Notice

the fact that

Salesforce’s pricing is

clearly defined

One Plan for

Each Persona You’re Targeting

31

© All Rights by InCoPro BVBA BE 0 877.807.636 [email protected] +32 473/38 16 13

The Margin assessments:

Some lessons• Keep the focus on simplicity and get started

• better be approximately right than precisely wrong

• Be careful with over precision, it lead to apparent accuracy and less

sustainable models.

• Be précises in product cost and prices (cents). Be rough in fix costs.

• Look for you’re the key metrics in your market

• What is your unique sales unit of measure?

• Be iterative and know that adding a dimension in the product market

combinations also needs reflection on direct costs

• Start from a white paper and beat it. Make your own model so you

understand it.

• Look to the margin, is it realistic? Not too good not too bad. Compare

with day to day values (Bread, Salary, Car cost etc).

• Make Sensitivity analysis. Which parameter boosts your model?

32

© All Rights by InCoPro BVBA BE 0 877.807.636 [email protected] +32 473/38 16 13

Getting paid is the final goal?

33

I want to increase payment terms

He will wait for his funds

I want to be paid earlier.

I will not finance his operations

© All Rights by InCoPro BVBA BE 0 877.807.636 [email protected] +32 473/38 16 13

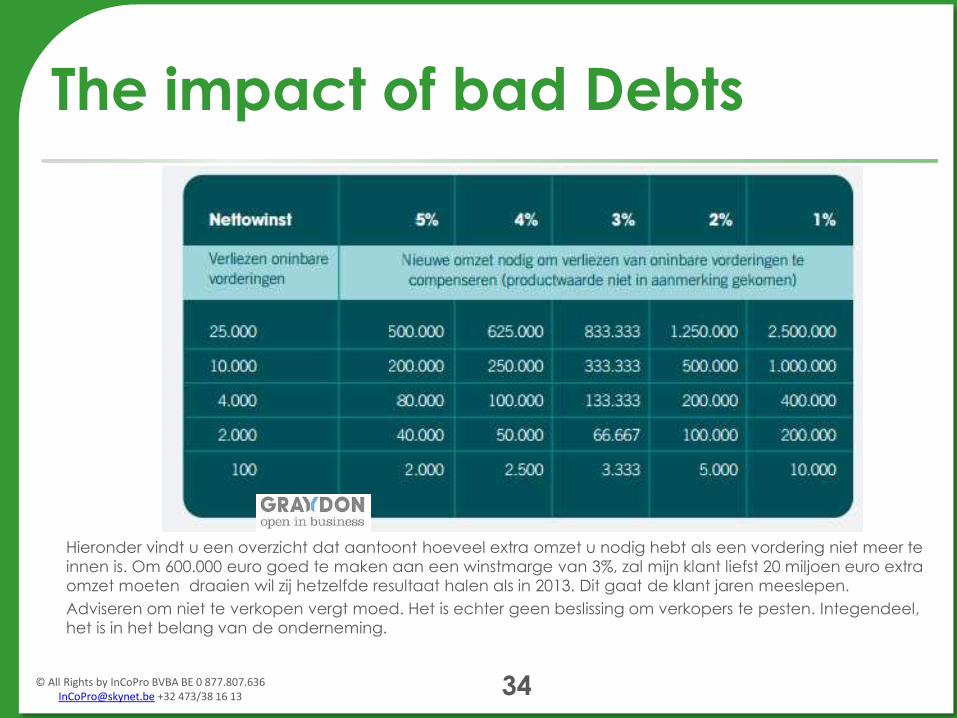

The impact of bad Debts

Hieronder vindt u een overzicht dat aantoont hoeveel extra omzet u nodig hebt als een vordering niet meer te

innen is. Om 600.000 euro goed te maken aan een winstmarge van 3%, zal mijn klant liefst 20 miljoen euro extra

omzet moeten draaien wil zij hetzelfde resultaat halen als in 2013. Dit gaat de klant jaren meeslepen.

Adviseren om niet te verkopen vergt moed. Het is echter geen beslissing om verkopers te pesten. Integendeel,

het is in het belang van de onderneming.

34

© All Rights by InCoPro BVBA BE 0 877.807.636 [email protected] +32 473/38 16 13

BIG DATA: A SIMPLE CONCEPT

35

DATA INSIGHTS:

• We all struggle still with the available enterprise data, and here is Big Data

• Companies that make the effort to manage and control their critical metadata are able to create more meaningful data-driven analyses, generate timely

actionable insights (Aberdeen 2015)

• As recent history has shown, information is

the byproduct of digital disruption and there

is lot of it. ( Digital disrupt or die, Mark J. Barrenechea )

© All Rights by InCoPro BVBA BE 0 877.807.636 [email protected] +32 473/38 16 13

InCoPro –D4MDesign for Margin D4M

Data to Information, Insights And Impact D2iii

New business models and the

impact on working capital

19 december

36

Going SAAS and the impact

on financing

© All Rights by InCoPro BVBA BE 0 877.807.636 [email protected] +32 473/38 16 13

The Typology of the Cash

models

1. Pay now

2. Pay Soon

3. Pay Later

4. Pay Never

5. Pay first

• Old ICT: Licenses

• Consulting model

• Typical saas (pay as you

use)

• Free economy,User as a

the product

• Retail, e-commerce

Bootstraps

37

© All Rights by InCoPro BVBA BE 0 877.807.636 [email protected] +32 473/38 16 13

More about the cash-models

38 19 december

• http://www.slideshare.net/omohout

© All Rights by InCoPro BVBA BE 0 877.807.636 [email protected] +32 473/38 16 13

SAAS: a game changer of the cash

model

traditional software world

• “perpetual license” customers

pay for the software license up

front

• typically pay a recurring

annual maintenance fee

(about 15-20% of the original

license fee).

• All of the license fee goes

direct in P&L: $1M license fee

sold in the quarter shows up as

$1M in revenue in the quarter.

• signing up to use the software on

an ongoing basis,

• typically contracts for 12-24 months

• revenue is recognize as the

software service is delivered

• But all its costs up front.: acquiring

cost,sales and marketing,

developing and maintenance,

hosting, infrastructure.

software as a service

39

© All Rights by InCoPro BVBA BE 0 877.807.636 [email protected] +32 473/38 16 13

Why shooing Esker SAAS service?

• Requiring little to no upfront investments

• (JFS:investment risk),

• Esker offers a pay-per-use SaaS

(JFS: price competition makes Risk by you)

• platform that allows you to implement AP automation rapidly

and cost effectively, without the need to build or expand an

in-house network while, moving from capital to operational

expenditure.

(JFS:Operationals expense to investments by provider)

• the web-based nature of SaaS lets you expand approval

workflow beyond the walls of the company — to subsidiary

offices, manufacturing facilities, etc. — without having to open

the corporate firewall.

(JFS: Security risk at Service provider) 40

Impact of changing into SAAS

© All Rights by InCoPro BVBA BE 0 877.807.636 [email protected] +32 473/38 16 13

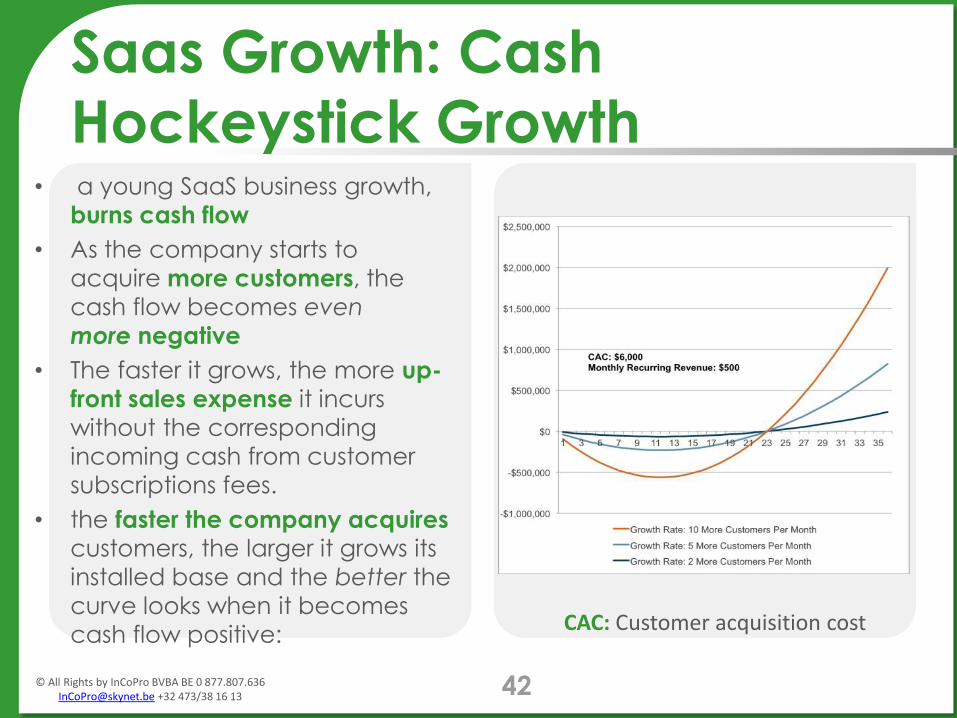

• Acquiring cost for a customer $6,000

• Monthly fee $500 per month

• break even after 13 months

Saas Growth: Cash HockeystickGrowth

41

Andreessen Horowitz is a Silicon Valley-based venture capital firm with $4.2 billion under management. The firm invests in entrepreneurs building companies at every stage – from seed to growth

© All Rights by InCoPro BVBA BE 0 877.807.636 [email protected] +32 473/38 16 13

• a young SaaS business growth,

burns cash flow

• As the company starts to

acquire more customers, the

cash flow becomes even

more negative

• The faster it grows, the more up-

front sales expense it incurs

without the corresponding

incoming cash from customer

subscriptions fees.

• the faster the company acquires

customers, the larger it grows its

installed base and the better the

curve looks when it becomes

cash flow positive:

Saas Growth: Cash Hockeystick Growth

42

CAC: Customer acquisition cost

© All Rights by InCoPro BVBA BE 0 877.807.636 [email protected] +32 473/38 16 13

Saas Growth: Cash Hockeystick

Growth

43

Stopcampaigns

• Your Working capital is used to financing sales actions for further growth• The service provider is investing in Hardware software and community growth. • The customer pays as he use in the future.

© All Rights by InCoPro BVBA BE 0 877.807.636 [email protected] +32 473/38 16 13 44

© All Rights by InCoPro BVBA BE 0 877.807.636 [email protected] +32 473/38 16 13 45

Operating profit remains resilient Operating profit declined 9% to €3.88 million in response to three main factors:• The accelerated transition to SaaS weighing in the short term on sales;(less

licences up front)• Significant investments by Esker Group to strengthen its capacity for

development and support improvements in its offering of solutions; (increase in sales cost)

• Exchange rate

Impact of changing into SAAS

© All Rights by InCoPro BVBA BE 0 877.807.636 [email protected] +32 473/38 16 13

The cash model of Airbnb

• When a guest submits a booking inquiry to a landlord, the guest

provides us with his or her payment details and approves the automatic

payment of a certain amount of money. We do not complete the

authorization if the booking inquiry is canceled, rejected or expires. In

that case we release all authorizations.

• If a booking inquiry is accepted, the entire payment is processed and

colelcted by Airbnb*. We retain the payment until 24 hours after

checking in before releasing it to the landlord, regardless of whether the

booking was made 2 days or 2 months in advance. This allows both

parties to take their time to check the room properly and make sure

everything is as expected.

*https://www.airbnb.be/help/article/51

46

10SLIDES2SUCCES © Omar Mohout (Sirris) and Jos Feyaerts (InCoPro)

PAY FIRST47

50.000

30.000

10.000

70.000

- 10.000

- 30.000

Month 20

Stop selling = Cash Flow take-off in all 3

- 50.000

Pay later

Pay First

Up front money from your crowd

Pay First-Turbo

Extra combustion by collecting money for your partners (ex.HouseOwners)

© All Rights by InCoPro BVBA BE 0 877.807.636 [email protected] +32 473/38 16 13

Bio-metrics of Jos

Feyaerts

Transition Projects

M&ATurnaround mgmt

Coaching &Sharing

Knowledge

TechnologyProcess &System

ERP, BPM, Data Analytics,

e-financial Supply Chain

Strategic finance Performance Measurement,

corporate restructuring, financing, etc.

www.Dyzo.be

Entrepreneurs on a crossroad

Horse insights for mgmt and

teams

e-SCStartups.be

Technics

BIMACControllers

connect

© All Rights by InCoPro BVBA BE 0 877.807.636 [email protected] +32 473/38 16 13

Bio-metrics of Jos Feyaerts

49

Experiences:– International Finance & controlling in industrial group (12 Years, BE, DE, ES, PT))

– CFO functions in divers SME and large Corporates, turnaround, Growth problems, carve-out, implementation of M&A, Shared Service Centers.

– ERP business lead/project mgmt, ERP-Post implementation remediation

– E-supply chain transition management (e-flows and Supply chain finance, e-payment)

– Design for margin, (Throughput, Bottleneck mgmt)

– Data for information, insight and impact

– InCoPro: independent since Oct. 2003.

– Horse Science for Management

Engagements: Stratups.be (financials) and adviser of Dyzo (SME with

continuity problems)

Hobby's: technology and technics, craftwork, outdoor sports,

Guest-lecturer : digitalization of the financial supply chain and supply chain

finance (KUL, HUB,EHB, congresses)

© All Rights by InCoPro BVBA BE 0 877.807.636 [email protected] +32 473/38 16 13

Design for Margin

Data to Information, Insights and Impact

D4M

D2iiiInCo

Pro

© All Rights by InCoPro BVBA BE 0 877.807.636 [email protected] +32 473/38 16 13

CIP : continuous improvement processToC : Theory of constraintsPerformance managementProcess MiningBPM: Business process modellingCash driven Business Cases Project ManagementSCF: supply chain finance and Working capital visibility

D2iii Data to information, insights and impact

51

D4MProductProduction processLogistic processesSupport processes Distributions channelSupply chain (Procurement/sourcing)Improve working capital and Throughput

D2iii

© All Rights by InCoPro BVBA BE 0 877.807.636 [email protected] +32 473/38 16 13

The End

“Think big, start up small, scale up fast!”

If you have a problem and nobody else can help you,

Jos FeyaertsD4M & D2iii@InCoPro BvBAMob:+32-473 38 16 13 Skype: [email protected]

please find us: