Embed Size (px)

Citation preview

Demand side –India will become a net importer of food and

grains

1

1

3

0

6

8

1

6

0

6

9

12

15

19

21

26

32

45

9

0 5 10 15 20 25 30 35 40 45 50

Bangladesh

Ethiopia & Eritrea

Indonesia

Nigeria

Mexico

Egypt

Pakistan

Iran

India

China

Million tons

20301990

215m

Source: WorldwatchInstitute.

India – Projected Supply/Demand Gap

Source: Surabhi Mittal, ICRIER

The Water Perspective

We must always keep in mind that agriculture is a water based business. Without this scarce resource there is no agriculture at all.

Water availability is key to this business. Projected global water consumption is tightly related to producing grains and food in general.

So, what is the current and projected water situations both in Africa and South America?

See UNEP/GRID Arendal Maps and Graphics Library. 2009. Trends in global water use by sector. http://maps.grida.no/go/graphic/trends-in-global-water-use-by-sector

Source: International Water Management Institute analysis done for the Comprehensive Assessment of Water Management in Agriculture using the Waterism model; chapter 2.

See UNEP/GRID Arendal Maps and Graphics Library, Areas of physical and economic water scarcity,

http://maps.grida.no/go/graphic/areas-of-physical-and-economic-water-scarcity

The Water Perspective

Operational Revenues: Crop Yields

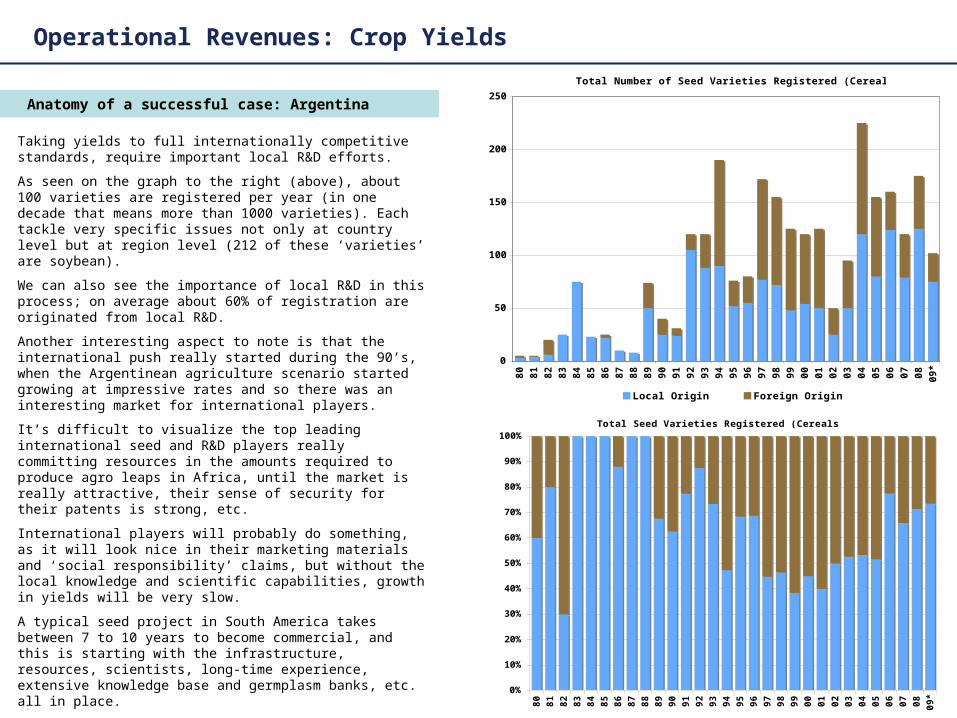

Anatomy of a successful case: Argentina

Taking yields to full internationally competitive standards, require important local R&D efforts.

As seen on the graph to the right (above), about 100 varieties are registered per year (in one decade that means more than 1000 varieties). Each tackle very specific issues not only at country level but at region level (212 of these ‘varieties’ are soybean).

We can also see the importance of local R&D in this process; on average about 60% of registration are originated from local R&D.

Another interesting aspect to note is that the international push really started during the 90’s, when the Argentinean agriculture scenario started growing at impressive rates and so there was an interesting market for international players.

It’s difficult to visualize the top leading international seed and R&D players really committing resources in the amounts required to produce agro leaps in Africa, until the market is really attractive, their sense of security for their patents is strong, etc.

International players will probably do something, as it will look nice in their marketing materials and ‘social responsibility’ claims, but without the local knowledge and scientific capabilities, growth in yields will be very slow.

A typical seed project in South America takes between 7 to 10 years to become commercial, and this is starting with the infrastructure, resources, scientists, long-time experience, extensive knowledge base and germplasm banks, etc. all in place.

In many African countries, this process is starting from scratch. We are probably looking at a 15 to 20 year lag. With international cooperation and cross country agreements, maybe it can be shortened to a 10 - 15 year, not much more than that.

Total Number of Seed Varieties Registered (Cereals & Oil seeds)

0

50

100

150

200

250

80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09*

Local Origin Foreign Origin

Total Seed Varieties Registered (Cereals & Oil seeds)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

80

81

82

83

84

85

86

87

88

89

90

91

92

93

94

95

96

97

98

99

00

01

02

03

04

05

06

07

08

09*

Conclusions on Crop Yields

Large scale agriculture as a business requires much more than just “good land” and “water / rain” availability. These are necessary conditions, but not even close to enough.

Reaching international competitive yields in Africa will take at least 10 to 15 years of serious R&D and important volumes of investments.

Simply importing seeds doesn’t make the cut as we have seen based on successful experiences in South America.

For the purpose of this report and given the above, when we say ‘South America’, we are referring to Argentina, Brazil, Paraguay and Uruguay.

For the purpose of this report and given the considerations above, when we say ‘Africa’ we are referring to Angola, Congo, Ethiopia, Kenya, Madagascar, Mozambique, Sudan, Tanzania, Zambia and Zimbabwe. There are some other countries in Africa promoting this method, but given their land extensions and potential or lack of information, they have not been considered; nevertheless, the conclusions might well apply for all of them.

News Releases from Top Agriculture Seed Providers

Syngenta and Embrapa establish multi-crop partnership to advance solutions for Brazilian growers.

Collaboration between Syngenta and IAC (Sao, Paulo - Brazil) accelerates sugar cane Research and Development activities.

Syngenta receives approval for new corn technologies in Argentina

Syngenta to develop high-sugar-content technology in cane, Sao Paulo - Syngenta Latin America.

Syngenta receives approval for new corn technologies in Brazil

Syngenta to acquire Monsanto’s hybrid sunflower seeds activities - further strengthening its leading sunflower business position in Europe and Latin America.

Syngenta Licenses Chromatin Gene Stacking Technology for Sugar cane (“which will give the a leading position in Brazil”)

Syngenta acquires Argentine seeds company SPS

April 28, 2010

Feb 08, 2010

Dec 22, 2009

Dec 16, 2009

Nov 13, 2009

Syngenta CEO expresses commitment to bringing technology and agronomic knowledge to African farmers.

Aug 25, 2009

Aug 06, 2009

Jun 26, 2009

Nov 10, 2008

Source: Syngenta Global Media Releases: http://www2.syngenta.com/en/media/mediareleases.html

May 31, 2010 10:25 (GMT-3)

• 9 out a total of 50 press releases talk about South America (concrete actions and achievements).

• 1 press release talks about Africa (a forward looking statement).

0 1 2 3 4 5 6 7

Sudan

Congo DR

Angola

Zimbabwe

Madagascar

Ethiopia

Kenya

Mozambique

Tanzania

Zambia

Paraguay

Brazil

Argentina

Uruguay

Civil LibertiesPolitical Freedom

The Social Perspective

Political and Freedom Index 2009

0-2 Free Countries

2-5 Relative Freedom

5-7 No Freedom

The Social Perspective

Political Stability Index (2008) [Range 2,5 to -2,5]

-2,5

-2

-1,5

-1

-0,5

0

0,5

1

Mo

zam

biq

ue

Zam

bia

Tan

zan

ia

Mad

agas

car

An

go

la

Ken

ya

Zim

bab

we

Eth

iop

ia

Co

ng

o D

R

Su

dan

Uru

gu

ay

Arg

enti

na

Bra

zil

Par

agu

ay

Au

stra

lia

Un

ited

Sta

tes

The Social Perspective

Rule of Law - Country Percentile of World (2008)

0 10 20 30 40 50 60 70

Uruguay

India

Tanzania

Brazil

Madagascar

Zambia

Ethiopia

Argentina

Mozambique

Kenya

Paraguay

Angola

Sudan

Congo, DR

Zimbabwe

The Social Perspective

Contract and Title Survival Risk Map

Our company developed this map to asses title and lease contact security based on the following assumptions:

• Very few contracts, especially with governments, survive long periods (20+ years) in emerging markets (statement generally valid both for Africa and South America).

• The chances of survival increase when these contracts are in areas that are not highly sensitive to the general electoral base – vote bank of the country.

• The higher the amount of population that lives in rural areas as farmers, the more sensitive is the ‘land issue’, as it applies to foreigners, and higher are the chances that it will be used by politicians, extremists or power groups to seek political benefits and nullify existing contracts.

• The lower the perceived legitimacy of the government, the higher the threat to titles, contracts and laws that were originated by that government.

Relative good protection by laws and the judicial system

Somewhat protected by laws and the judicial system

Low to very low protection by laws and the judicial system

% of Rural Population

Political Stability Index

And if things go wrong? :

About the Map:

The Land Ownership Risk Map and some Emblematic Cases: Africa vs South America

ZIMBABWE: 70% Rural Population

Low development indexes

High Political instability

= Almost all farms owned by “white” people have been confiscated since 2000.

MADAGASCAR: 75% Rural Population

Medium Political instability

Daewoo announced a big farmland lease agreement at the end of 2008.

= Immediate scandal and popular uprising, the deal was terminated.

PARAGUAY: 40% Rural Population

Low development indexes

Medium Political instability

President Lugo won election, among electoral campaign proposals was an important land reform.

= A law (not very radical) on this topic has been presented but has been stopped in parliament given that his party hasn’t got majority in congress.

ARGENTINA I: 8% Rural Population

Relative good development index

High political instability in 2001 (big economic crisis, government was out-thrown by social up-rise, 5 different presidents in 20 months.)

= Not once throughout the turmoil the topic of big farms or foreign investors in land appeared.

ARGENTINA II: The government needing additional funds, planned to increase taxes on some crops to farmers, the strategy to sell its project was talking about large land tenants, big groups in farming, etc.

= Not only the bill was stopped in parliament, but there were public demonstrations in urban areas supporting the farmers.

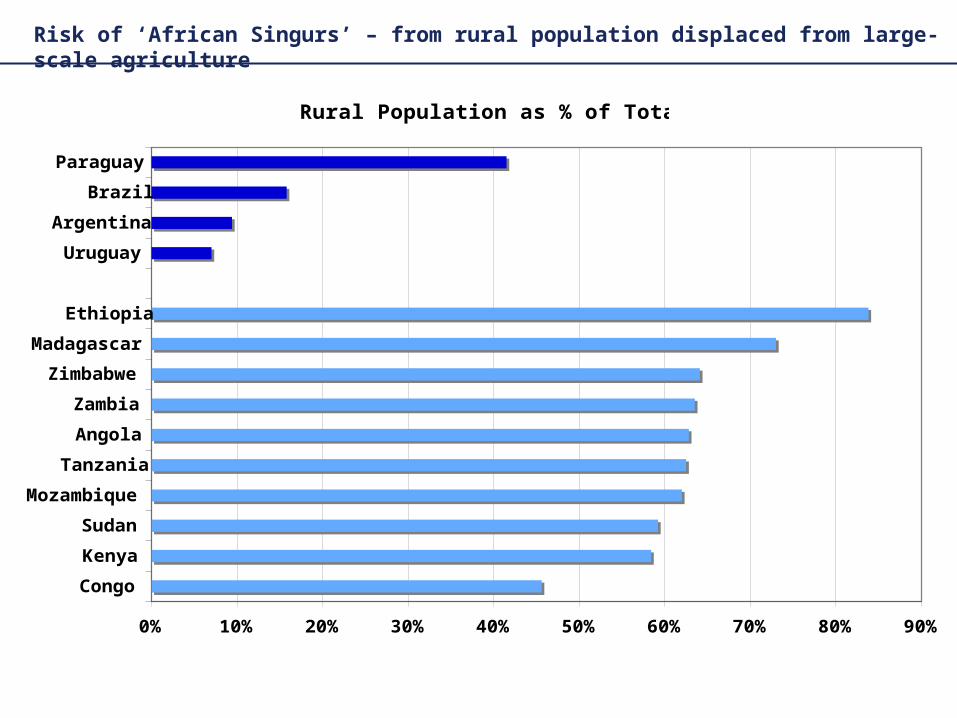

Risk of ‘African Singurs’ – from rural population displaced from large-scale agriculture

Rural Population as % of Total (2005)

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

Congo

Kenya

Sudan

Mozambique

Tanzania

Angola

Zambia

Zimbabwe

Madagascar

Ethiopia

Uruguay

Argentina

Brazil

Paraguay

In Africa, risk of ‘Singurs’ from population growth; favorable/cheap land leases are usually granted by governments with little political legitimacy; so risk of being overturned later

Source: UN Population Database

2005 2025 2050 2005 2025 2050Argentina 39 46 51 Ethiopia 75 120 174Brazil 186 214 218 Kenya 36 58 85Uruguay 3 4 4 Tanzania 39 67 109Paraguay 6 8 10 Madagascar 18 28 43

Mozambique 21 32 44Senegal 57 91 133Sudan 39 57 76

Population growth (in millions)

Population density (population per sq. km)

Source: UN Population Database

Year2005 2025 2050

Argentina 14 17 18Brazil 22 27 30Uruguay 19 20 21Paraguay 15 20 24India 345 440 504

Ethiopia 68 109 157Kenya 62 99 147Tanzania 41 71 116MadagascarMozambique 26 39 55Sudan 15 23 30

Population % with Access to Clean Water

0% 20% 40% 60% 80% 100%

Ethiopia

Angola

Madagascar

Congo

Mozambique

Kenya

Zambia

Tanzania

Sudan

Zimbabwe

Paraguay

Brazil

Argentina

Uruguay

Some other Indicators that might affect the initial ‘equilibrium’ in the future

Projected Annual Population Growth Rates (2015)

0,00% 0,50% 1,00% 1,50% 2,00% 2,50% 3,00% 3,50%

Congo

Angola

Kenya

Madagascar

Ethiopia

Sudan

Zambia

Tanzania

Mozambique

Zimbabwe

Paraguay

Brazil

Argentina

Uruguay

Some other Indicators that might affect the initial ‘equilibrium’ in the future

South America vs Africa

Brazil

Ethiopia

Also less water per capita in Africa compared to South America

TARWR/ m3/percapita/year

Argentina 20,940 Ethiopia 1,680

Brazil 45,470 Kenya 930

Uruguay 40,420 Tanzania 2,420

Paraguay 55,830 Madagascar 18,830

India 1,750 Mozambique 11,320

Sudan 1,880

Source: UN Aquastat

South America is an immediate opportunity

Buy/Lease Land Yes No (lease only)

Service Providers(planting/spraying etc.)

Yes No

Qualified Manpower Yes No

Political Risk(low populations, democracies, corruption etc.)

Low High

Tested high yield crop/seed varieties

Yes No

South America Africa

Regarding Almost “Free land” in Africa:Maintaing a gift elephant is not free

Note: Numbers based on median Latin American land conversion rates to convert raw land to agriculture ready land. Africa figures could be higher/

Making improvements on leased land is like putting in new brakes, clutch and tyres on a rental car

Other South American advantages for Indian

investors