Embed Size (px)

Citation preview

Nikita BhatkarOperations Specialization

Activity-based costing (ABC) is a costing methodology that identifies activities in an organization and assigns the cost of each activity with resources to all products and services according to the actual consumption by each.

Resources are assigned to activities, and activities to cost objects based on consumption estimates. The latter utilize cost drivers to attach activity costs to outputs

It enables a business to decide which products, services, and resources are increasing their profitability, and which are contributing to losses

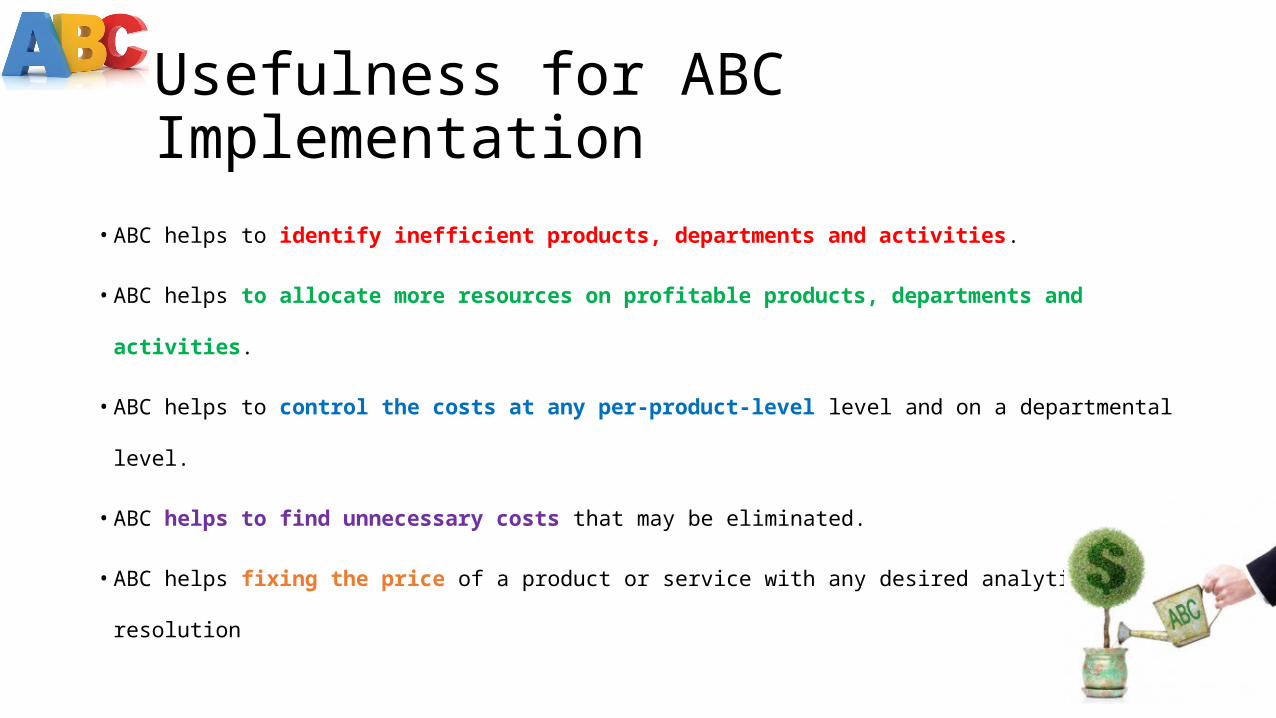

Usefulness for ABC Implementation• ABC helps to identify inefficient products, departments and activities.

• ABC helps to allocate more resources on profitable products, departments and

activities.

• ABC helps to control the costs at any per-product-level level and on a departmental

level.

• ABC helps to find unnecessary costs that may be eliminated.

• ABC helps fixing the price of a product or service with any desired analytical resolution

Reasons for ABC implementation• Better Management

• Budgeting, performance measurement

• Calculating costs more accurately

• Ensuring product /customer profitability

• Evaluating and justifying investments in new technologies

• Improving product quality via better product and process design

• Increasing competitiveness or coping with more competition

• Management

• Managing costs

• Providing behavioral incentives by creating cost consciousness among employees

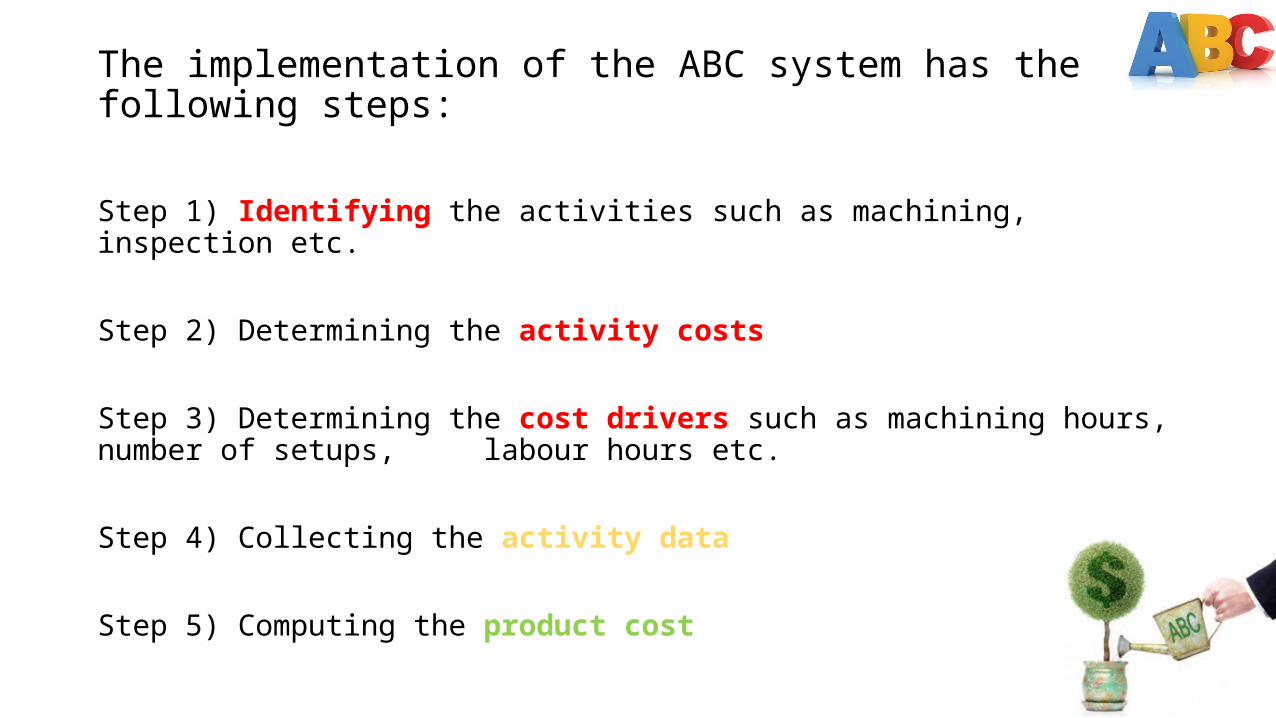

The implementation of the ABC system has the following steps:

Step 1) Identifying the activities such as machining, inspection etc.

Step 2) Determining the activity costs

Step 3) Determining the cost drivers such as machining hours, number of setups, labour hours etc.

Step 4) Collecting the activity data

Step 5) Computing the product cost

A Comparative Analysis and Implementation of

Activity Based Costing (ABC) and

TraditionalCost Accounting (TCA) Methods

in anAutomobile Parts Manufacturing Company:

A Case Study

A CASE of: Nitin Kumar & Dalgobind MahtoGlobal journal of Management and Business ResearchVolume XIII Issue IV Version IYear 2013

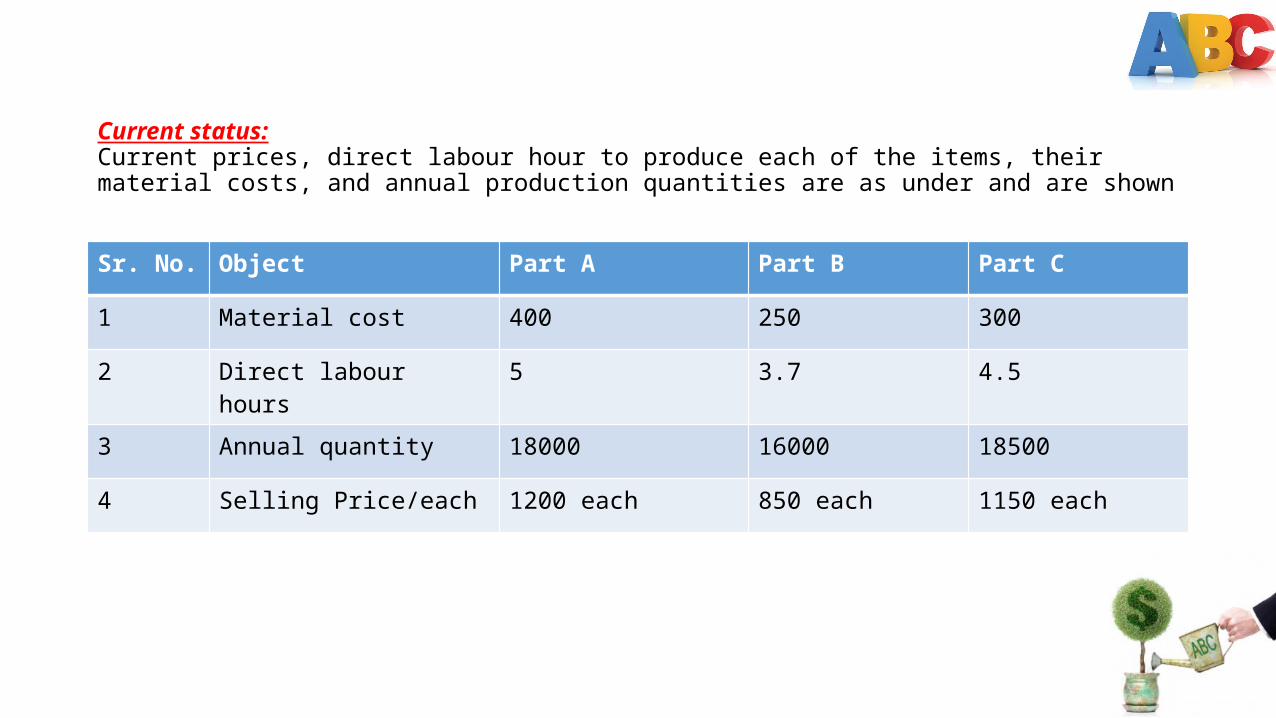

Current status:Current prices, direct labour hour to produce each of the items, their material costs, and annual production quantities are as under and are shown

Sr. No. Object Part A Part B Part C

1 Material cost 400 250 300

2 Direct labour hours 5 3.7 4.5

3 Annual quantity 18000 16000 18500

4 Selling Price/each 1200 each 850 each 1150 each

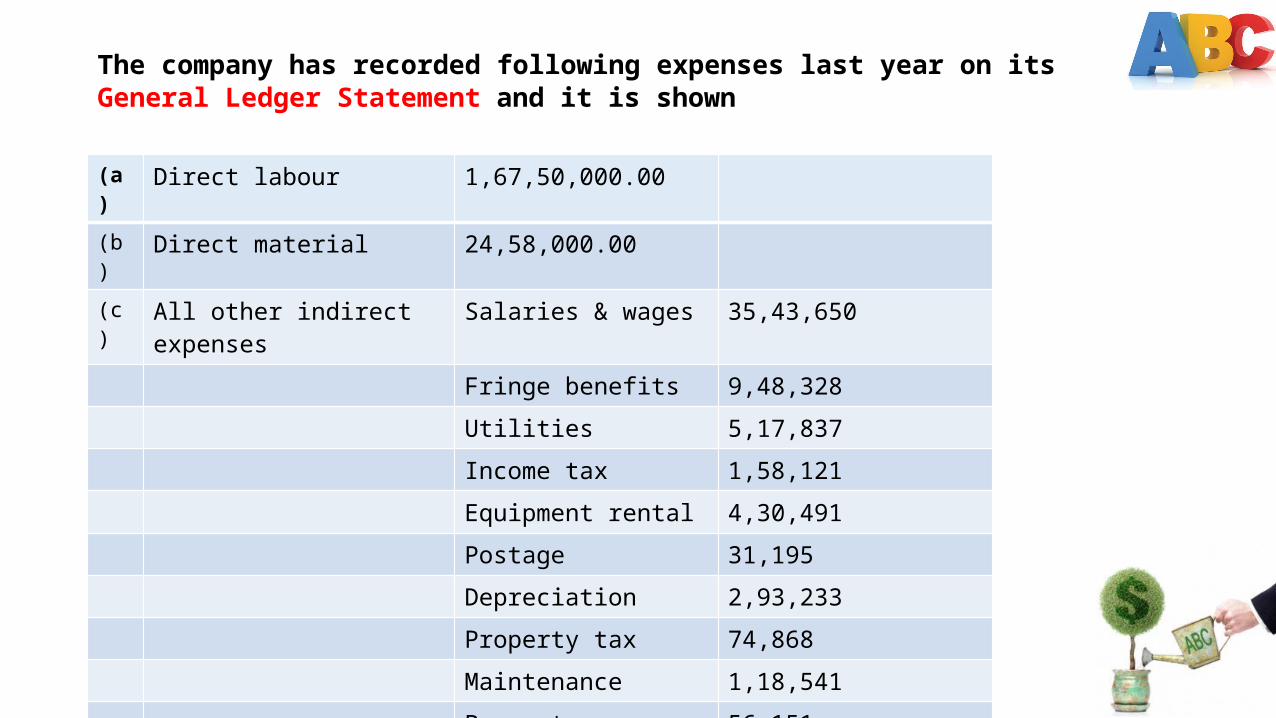

The company has recorded following expenses last year on its General Ledger Statement and it is shown

(a) Direct labour 1,67,50,000.00(b) Direct material 24,58,000.00(c) All other indirect expenses Salaries & wages 35,43,650

Fringe benefits 9,48,328

Utilities 5,17,837

Income tax 1,58,121

Equipment rental 4,30,491

Postage 31,195

Depreciation 2,93,233

Property tax 74,868

Maintenance 1,18,541

Property insurance 56,151

Tools 93,585

Total 62,66,000

In Traditional costing method

Total Labour hours required

Part A = (18,000 × 5) = 90,000 hrs

Part B = (16,000 × 3.7) = 59,200 hrs

Part C = (18,500 × 4.5) = 83,250 hrs

Total labour hours = 2, 32,450 hrs

Direct labour hour cost

Direct labour hour cost = (1,67,50,000/2,32,450) = 72.05 ₹/hr

Total/overall indirect cost

Total indirect cost = 62,66,000

Over cost/labour hour

Over cost/labour hour = (62,66,000.00/2,32,450) =26.95 ₹/hr

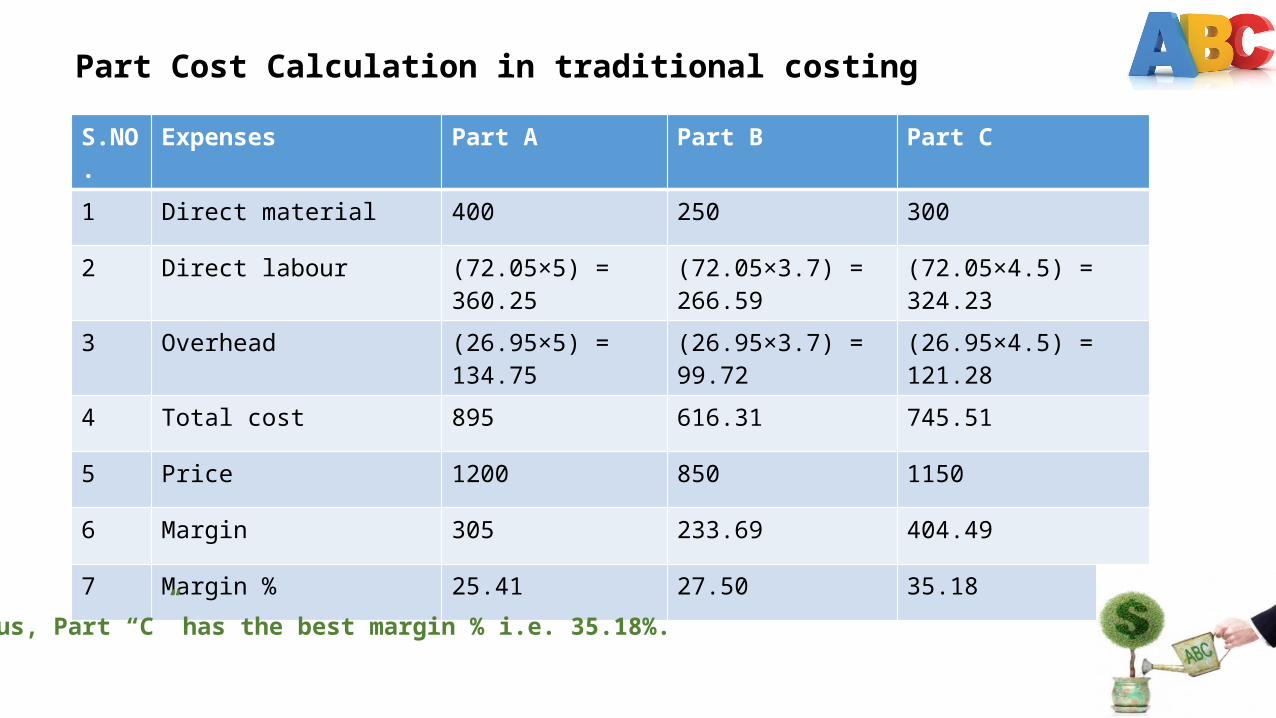

Part Cost Calculation in traditional costingS.NO. Expenses Part A Part B Part C

1 Direct material 400 250 300

2 Direct labour (72.05×5) = 360.25 (72.05×3.7) = 266.59 (72.05×4.5) = 324.23

3 Overhead (26.95×5) = 134.75 (26.95×3.7) = 99.72 (26.95×4.5) = 121.28

4 Total cost 895 616.31 745.51

5 Price 1200 850 1150

6 Margin 305 233.69 404.49

7 Margin % 25.41 27.50 35.18

Thus, Part “C” has the best margin % i.e. 35.18%.

Now, True Cost calculation of parts by Activity Based Costing (ABC) Method :

Flashback…….

After interviewing the staff of company; some of the information was received from the Company’s recordsSr. No. Object Part A Part B Part C Total

1 Customer orders 1,800 2,000 2,500 63,00

2 Parts manufactured 18,000 16,000 18,500 52,500

3 Work orders 110 100 120 330

4 Set-ups 110 100 120 330

5 Machine hours/unit 5 3.7 4.5

6 Material cost/unit 400 350 200

7 Labour hours/unit 5 3.7 4.5

8 Total labour hours 18,000 16,000 18,500

9 Selling price/part 1,200 850 1,150

Activity determination : The staff questionnaire revealed that the company uses 25 employees and they are in the following work groups as shown

Sr. No. Activity No. of People % of total

1 Processing orders 12 24%

2 Scheduling orders 10 20%

3 Die maintenance and storage 14 28%

4 Inspection 08 16%

5 Shipping (dispatch) orders 06 12%

6 Total 50 100%

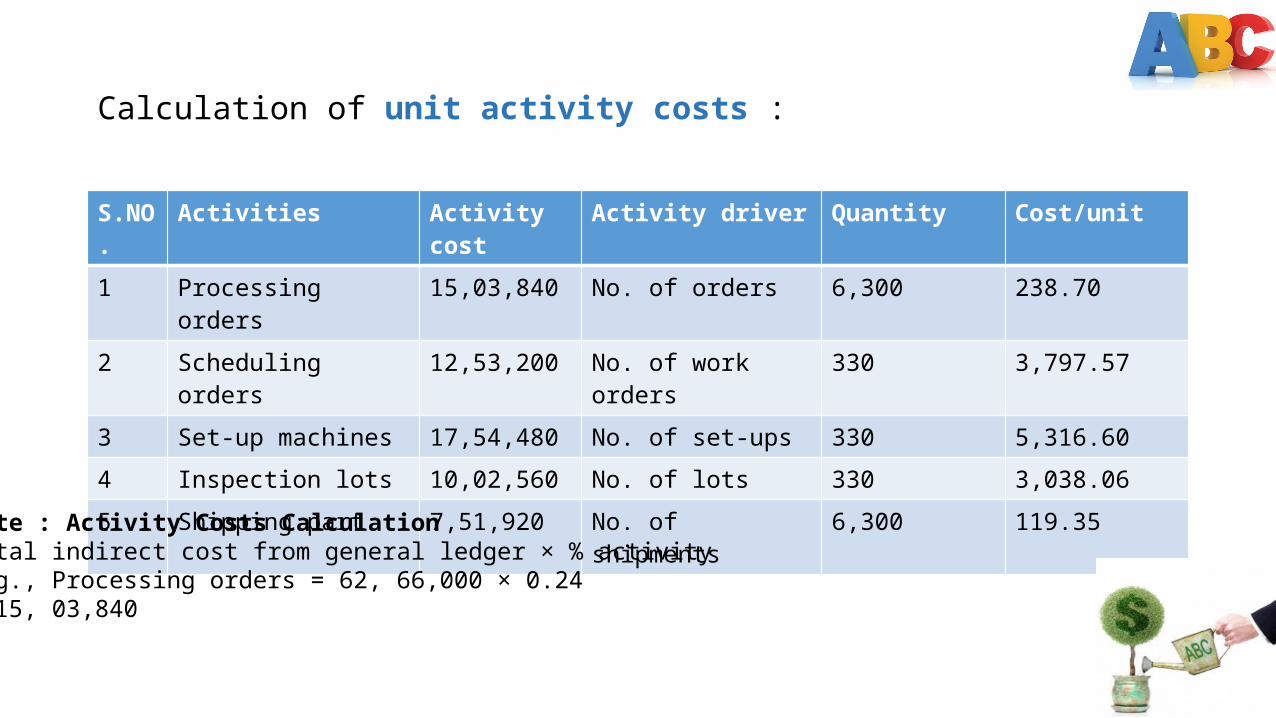

Calculation of unit activity costs :

S.NO. Activities Activity cost Activity driver Quantity Cost/unit

1 Processing orders 15,03,840 No. of orders 6,300 238.70

2 Scheduling orders 12,53,200 No. of work orders 330 3,797.57

3 Set-up machines 17,54,480 No. of set-ups 330 5,316.60

4 Inspection lots 10,02,560 No. of lots 330 3,038.06

5 Shipping part 7,51,920 No. of shipments 6,300 119.35

Note : Activity Costs CalculationTotal indirect cost from general ledger × % activitye.g., Processing orders = 62, 66,000 × 0.24= 15, 03,840

Activity Costs : Part A Part B Part C

Sr. No

Activity Cost Vol. Total Cost UnitCost

Vol. TotalCost

UnitCost

Vol. Total Cost UnitCost

1 ProcessingOrders

238.70 1,800 4,29,660 23.87 2,000 4,77,400 29.83 2,500 5,96,750 32.25

2 SchedulingOrders

3,797.57 110 4,17,732.7 23.20 100 3,79,757 23.73 120 4,55,708.4 24.63

3 Set-upmachines

5,316.60 110 5,84,826 32.49 100 5,31,660 33.22 120 6,37,992 34.48

4 Inspectionlots

3,038.06 110 3,34,186.6 18.56 100 3,03,806 18.98 120 36,45,67.2 19.70

5 Shippingparts

119.35 1,800 2,14,830 11.93 2,000 2,38,700 14.91 2,500 2,98,375 16.12

6 Total 110.05 119.67 127.18

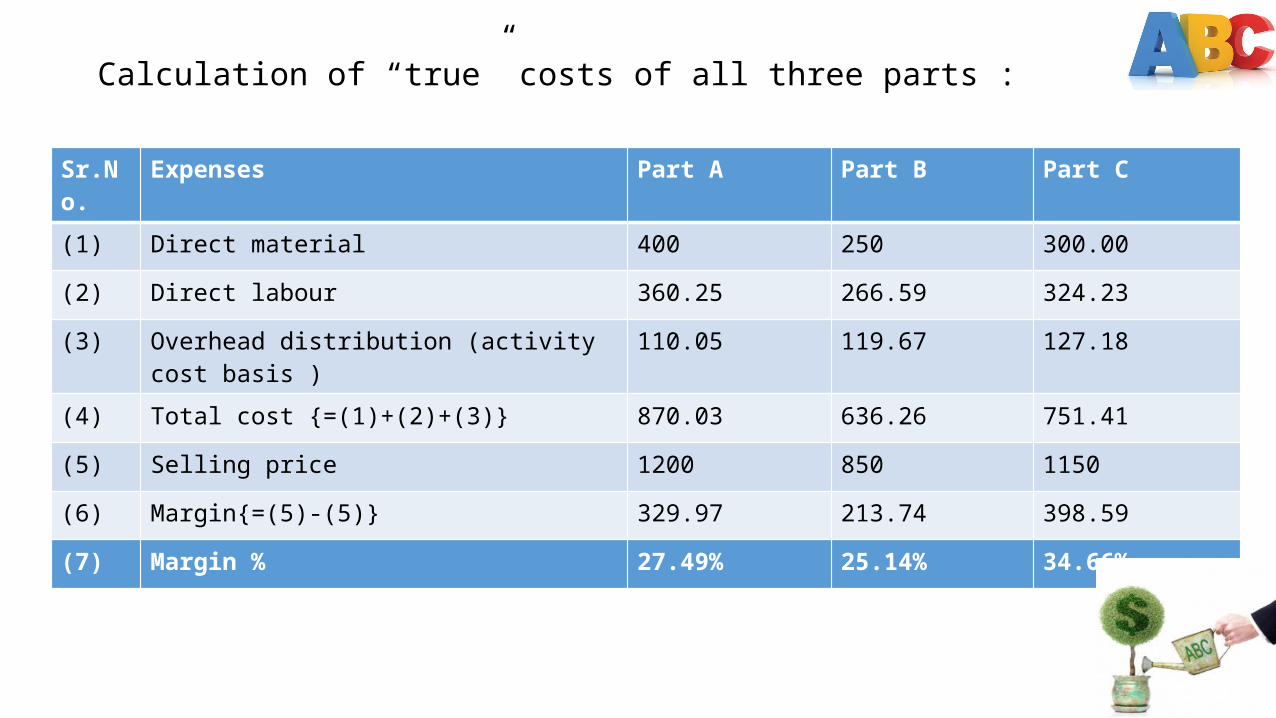

Calculation of “true” costs of all three parts :

Sr.No. Expenses Part A Part B Part C

(1) Direct material 400 250 300.00

(2) Direct labour 360.25 266.59 324.23

(3) Overhead distribution (activity cost basis ) 110.05 119.67 127.18

(4) Total cost {=(1)+(2)+(3)} 870.03 636.26 751.41

(5) Selling price 1200 850 1150

(6) Margin{=(5)-(5)} 329.97 213.74 398.59

(7) Margin % 27.49% 25.14% 34.66%

ComparisonPART Selling price TCA cost TCA margin TCA margin% ABC cost ABC cost margin ABC cost margin%

Part “A” 1,200 895 305 25.41% 870.03 329.97 27.49%

Part “B” 850 616.31 233.69 27.50% 636.26 213.74 25.14%

Part “C” 1,150 745.51 404.49 35.18% 751.41 398.59 34.66%