Embed Size (px)

Citation preview

Australian / Mongolian Business Forum - 2011

David Paterson

Country Director Mongolia

Oyu Tolgoi CopperMongolian partnership in action

Australian / Mongolian Business Forum - 2011

Rio Tinto is one of the world’s leading companies

• Approximately 60,000 employees world wide

• Operations in over 40 countries

• 2010 global revenues of >US$60 billion

• US$12 billion in major capital growth projects approved for 2010/2011

2

Australian / Mongolian Business Forum - 2011

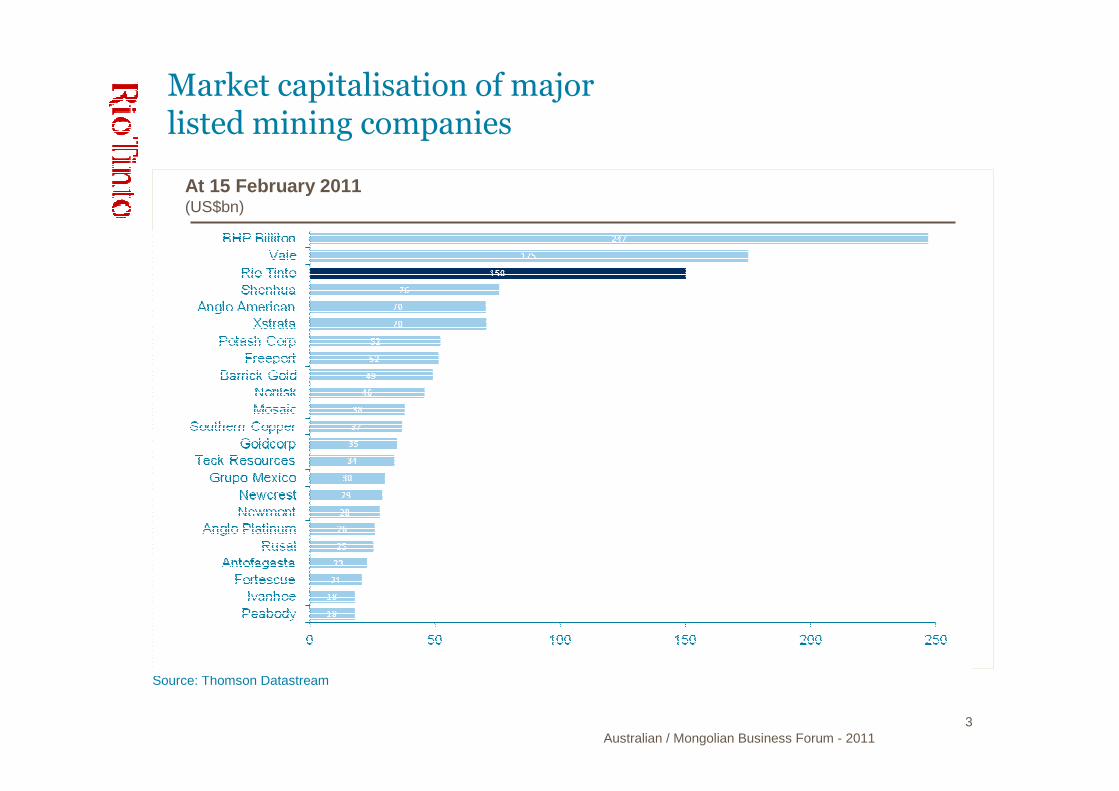

Market capitalisation of majorlisted mining companies

3

At 15 February 2011(US$bn)

Source: Thomson Datastream

Australian / Mongolian Business Forum - 2011Source: Rio Tinto

Rio Tinto is a global leader in the development of key mining technologies

Advanced mineral recovery

Advanced flotation modelling and control

Technology platform for sorting bulk commodities

Linking orebody knowledge with selective leaching

Advanced FlotationSorting Platform Selective Leaching

• Two new tunnelling concepts that are more productive and cost effective than traditional methods.

• Integrated shaft boring machinery with the potentialto dramatically improve safety while reducing construction time.

Rapid underground development

4

Australian / Mongolian Business Forum - 2011

Where we operate Copper

Note: Shaded areas denote countries where Rio Tinto has a presence through operations, offices or exploration.

Source: Rio Tinto 5

Other Rio Tinto

Pebble (USA)

Kennecott (USA)

Resolution (USA)

Eagle (USA)

La Granja (Peru)

Escondida (Chile)

Palabora (South Africa)

Northparkes (Australia)

Grasberg (Indonesia)

Sulawesi (Indonesia)

OyuTolgoi (Mongolia)

Australian / Mongolian Business Forum - 2011

Rio Tinto Copper: Unparalleled capabilities

6

Mining & Processing

Global Diversity

Innovation & Technology

Governance

Sustainable Development

Functional support

Full Range of Copper Mining & Processing

• From Open cut to underground block cave

• Milling & smelting to SXEW, leaching & autoclave

True Global Company

• Proven capacity to develop large, low cost, long life operations in a range of different global settings (1st world to 3rd world)

Global Leader in Mining Innovation

• Advanced development of leading step change technologies with the greatest potential to create value in copper

Flexibility & Experience

• Proven capacity to successfully develop and operate with a rangeof different ownership structures (100% owner to minority JV’s)

Global Miner of Choice

• Strategic commitment by leadership of Rio Tinto

• Leading HSEC performance, systems, and standards

End to End Skills

• World class expertise in all related mining support functions, from exploration to marketing

Australian / Mongolian Business Forum - 2011

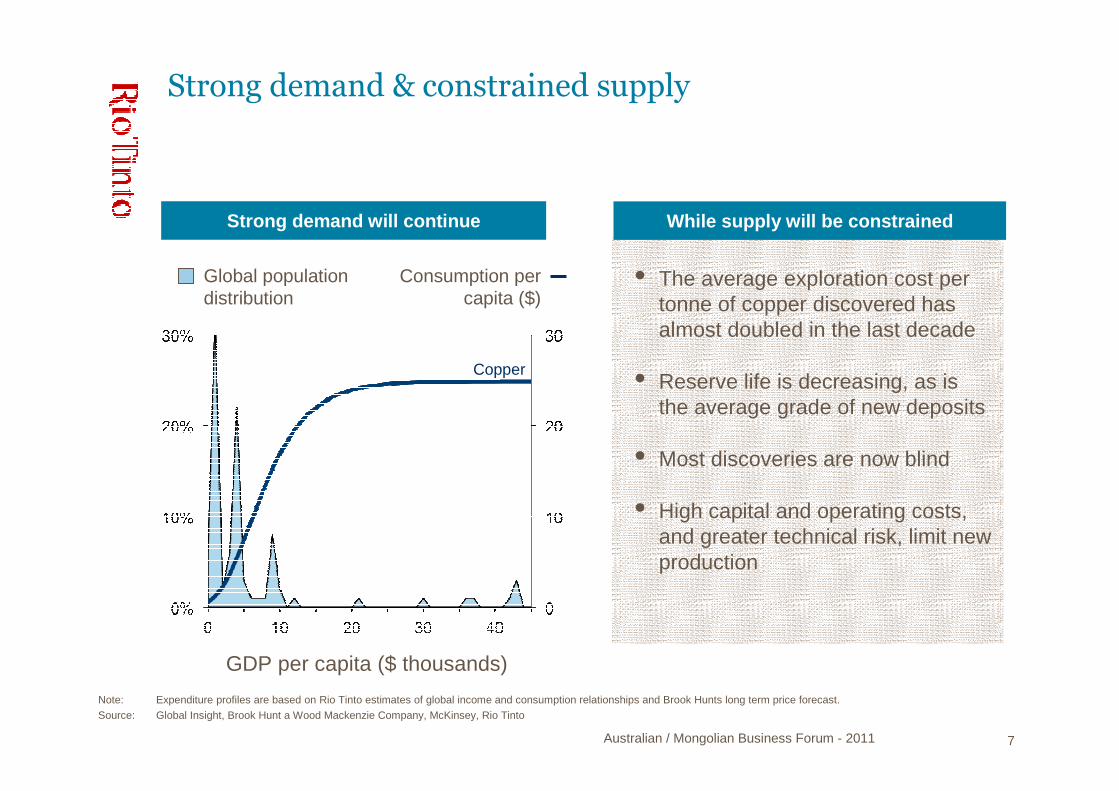

Note: Expenditure profiles are based on Rio Tinto estimates of global income and consumption relationships and Brook Hunts long term price forecast.

Source: Global Insight, Brook Hunt a Wood Mackenzie Company, McKinsey, Rio Tinto

Strong demand & constrained supply

Global population distribution

Consumption per capita ($)

GDP per capita ($ thousands)

Copper

While supply will be constrainedStrong demand will continue

• The average exploration cost per tonne of copper discovered has almost doubled in the last decade

• Reserve life is decreasing, as is the average grade of new deposits

• Most discoveries are now blind

• High capital and operating costs, and greater technical risk, limit new production

7

Australian / Mongolian Business Forum - 2011

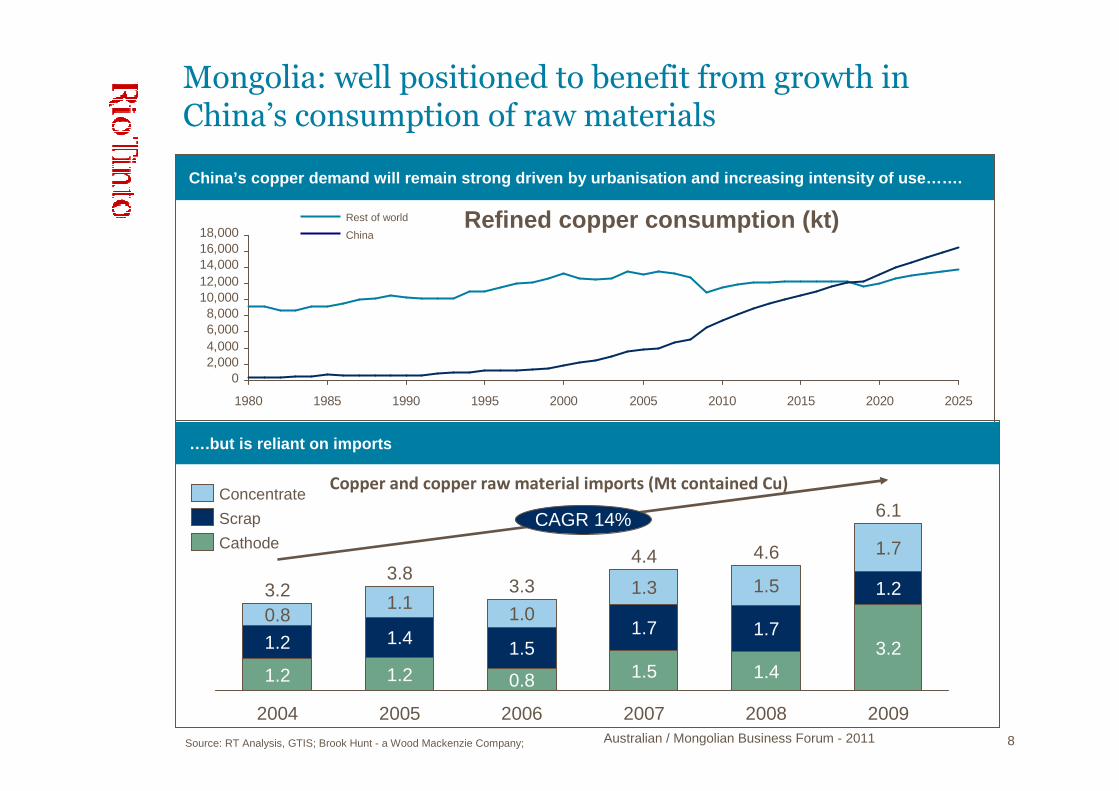

Mongolia: well positioned to benefit from growth in China’s consumption of raw materials

02,0004,0006,0008,000

10,00012,00014,00016,00018,000

1980 1985 1990 1995 2000 2005 2010 2015 2020 2025

China’s copper demand will remain strong driven by urbanisation and increasing intensity of use…….

Rest of world

ChinaRefined copper consumption (kt)

Source: RT Analysis, GTIS; Brook Hunt - a Wood Mackenzie Company; 8

CAGR 14%

2009

6.1

3.2

1.2

1.7

2008

4.6

1.4

1.7

1.5

2007

4.4

1.5

1.7

1.3

2006

3.3

0.8

1.5

1.0

2005

3.8

1.2

1.4

1.1

2004

3.2

1.2

1.2

0.8

Cathode

Scrap

ConcentrateCopper and copper raw material imports (Mt contained Cu)

….but is reliant on imports

Australian / Mongolian Business Forum - 2011

Growth in concentrate demand

Global concentrate balance (‘000 tonnes contained Cu)

Source: CRU; Brook Hunt - a Wood Mackenzie Company; Rio Tinto Analysis

-10

40

10

20

30

0

50

10,0008,0006,0004,0002,000

Chinese Smelters

New Chinese smelters are low cost

High cost smelters are vulnerable to closure

-2,058

-1,274-1,525

-1,307

-678

-5

201520142013201220112010

Global concentrate deficit continues to grow…

Low cost capacity forecast to increase

0

1,000

2,000

3,000

4,000

5,000

1990 1995 2000 2005 2010 2015

Driven by Chinese smelter capacity expansion

Copper production from concentrates (Kt contained Cu)

China

Japan

China has over taken Japan as the largest consumer of custom concentrates (6.1 Mt – 2009)

Most smelters in China are positioned in the lower quartile of the cost curve

Low cost capacity will continue to be built in China while marginal producers will be vulnerable to closure

Cts/lb

9

Australian / Mongolian Business Forum - 2011

Oyu Tolgoi

10

Australian / Mongolian Business Forum - 2011

Oyu Tolgoi is a Tier one asset

1111

Note: 1. Copper assets include those in Pre-Production or Feasibility and the ten largest assets with Active Reserves Development as defined by MEG.

2. Rio Tinto’s owns 100% of La Granja, 55% of Resolution, has a 22.4% interest in Ivanhoe Mines Limited (with the option to increase to 44%) who own 66% of Oyu Tolgoi and a 19.8% interest in Northern Dynasty Minerals Limited who own 50% of Pebble. Deposit data for La Granja, Resolution and Oyu Tolgoi is from the JORC compliant ore reserves and resources statement outlined in the 2009 Annual Report, pp. 68-77. Pebble deposit data is 43-101 compliant, derived from the “Updates Mineral Resource Estimate…” news release dated 01/02/2010.

Source: Metals Economics Group, Rio Tinto, Northern Dynasty

Bubble size denotes size of asset (contained Cu)

Resolution

La Granja

Oyu Tolgoi

Pebble

Comparison of undeveloped copper assets 1

Grade(%Cu)

Reserves & resources (Mt)

Rio Tinto interests

Australian / Mongolian Business Forum - 2011

• Long term investment

• Transparent reporting

Terms of Investment

• Stable tax environment

• Tax and royalty revenue

Taxation

• Flexible energy options

• Provision for roads

Infrastructure

Source: Oyu Tolgoi LLC

• 90% Mongolian employees

• 5 yr training & strategy plan

Employment & Training

• New regional council

• Transparent communities plans

Regional development

• Detailed environmental impact assessments and protection plan

Environment

12

A landmark investment agreement

Australian / Mongolian Business Forum - 2011

Benefits for Mongolia

Capital expenditure

Education & Training

Employment

• Estimated investment of ~US$6 billion

• US$100 million committed, training for 3,300 operators initially

• 150 scholarships awarded

• Workforce will peak at 17,000 during construction

• Experienced in Western methods, process and standards

• 90% Mongolian nationals during operations

Procurement

Infrastructure

Sustainable development

• Estimated $500-800m per annum when operational

• Infrastructure plans include an airstrip, water, transport and power developments

• Contributing to sustainable development was a key foundation forinvestment agreement

• Rio Tinto sponsored General Equilibrium Model

The development of Oyu Tolgoi is a catalyst for eco nomic and social development

13

Australian / Mongolian Business Forum - 2011 14

Oyu Tolgoi will increase the Mongolian economy by over 35% by 2020

Mongolian real gross domestic productMNT trillions and annual growth • By 2020 Oyu Tolgoi’s

impact will increase GDP by around a third.

• Oyu Tolgoi will lift GDP per person by MNT1.7 million (over $1000) in 2020 – an increase equivalent to over 60% of today's GDP per person.

• GDP growth peaks at 22% in 2016.

• The average growth rate from 2013-2020 is projected to be 12.7% compared to 7.7% without Oyu Tolgoi.

0

5

10

15

20

25

30

0%

4%

8%

12%

16%

20%

24%

2010 2015 2020 2025

Real GDP in OT scenario

% annual growth

MNT trillions (2010)

Real GDP in reference case

Annual growth in OT scenario

Annual growth in reference case

Long run copper price of $2.50/lb ($5,500/ton)Long run gold price of $1000/oz

Australian / Mongolian Business Forum - 2011

Focus on training and development

Traineeships / Apprentices• 148 Mongolians currently on Traineeships studying mining skills• Expect an addition 172 Traineeships to be awarded by February 2012

Scholarships• 30 Mongolian students awarded scholarships as at end 2010• Expect an additional 200 scholarships to be awarded over the next 6 years

“Rio Tinto will bring world standards and advanced technologies”

Batsukh GalsanChairman, Oyu Tolgoi

15

Australian / Mongolian Business Forum - 2011

OT Current Status: Investment & Ownership

• Secure additional funding for the project; and

• Enabled Rio Tinto to assume management control

16

Rio Tinto has invested over US$2.3 billion in OT ov er the past 4 years

Rio Tinto42.1%

OtherShareholders

Ivanhoe66%

Govt of Mongolia 34%

Oyu Tolgoi

• In December 2010, Rio Tinto and IVN announced a number of key agreements.

These agreements:

• Provide Rio Tinto with a clear pathway to 49% ownership in IVN (32.3% of the OT project)

Australian / Mongolian Business Forum - 2011

The transition to Rio Tinto management control will provide significant additional benefits

17

OT Project will be carried out with

access to the full functional and

technical expertise of Rio Tinto.

OT will be able to utilize the suite of

Rio Tinto’s intellectual property relevant to the OT

Project.

OT Project will benefit from the

combined practical experience gleaned from operating in over 40 countries

worldwide .

Functional & Technical Expertise

GlobalExperience

Intellectual Property

Australian / Mongolian Business Forum - 2011

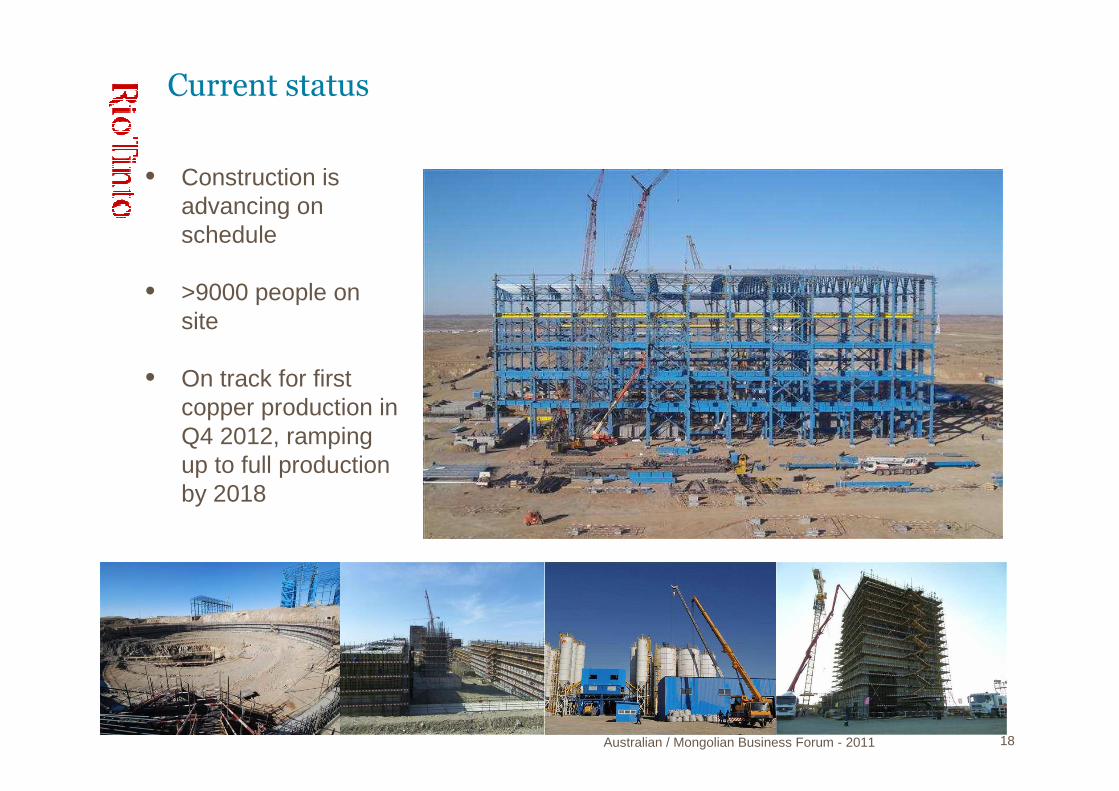

Current status

• Construction is advancing on schedule

• >9000 people on site

• On track for first copper production in Q4 2012, ramping up to full production by 2018

18

Australian / Mongolian Business Forum - 2011

The benefits of doing business in Mongolia

Source: Oyu Tolgoi LLC

Liberal political environment

Supportive of foreign investment

Commitment to develop infrastructure

Financial system restructuring

• Transparent, long-term vision, neutral foreign relations policy• Maintaining prudent macroeconomic and structural policies

• Tax policies protecting the rights and interests of foreign investors• Willingness to negotiate on terms

• Government proactively legislating • Railway and Air network development

• More prudent monetary policy• Strengthening of the banking and financial system• IMF says there is “low risk of debt distress”

“Looking forward, the economic outlook is very favo urable, driven by the signing of the Oyu Tolgoi investment agreement in O ctober 2009.”

World Bank Mongolia Monthly Economic Update

Rich in natural resources

• Highly prospective region• In close proximity to China & Russia• Growing Mongolian Mining Sector

19

Questions?