Embed Size (px)

Citation preview

FOURTHQUARTER 2016 January 26, 2017

Tele2 AB

Group highlights – Q4 2016

2

Q4 2016 % Change Reported

LFL is constant currencies and pro forma for Altel and TDC Sweden

% ChangeLFL

Mobile end-user service revenue(SEK billion)

3.71 +14% +6%

EBITDA(SEK billion) 1.46 +9% +4%

Net sales(SEK billion) 8.22 +18% +2%

Delivering on our long term strategy

3

Winning People & Culture

Value Champion

Step-Change Productivity

Focused Technology

Choices

• Swedish and Baltics 4G population coverage above 99%• Netherlands population coverage now >99% outdoor, >90% indoor• Netherlands data on-loading on own network at 82%

• Sweden mobile end-user service revenue up 4%, excluding TDC• Baltics mobile end-user service revenue up 12%• Netherlands mobile customer base surpasses 1 million

• Strong cash contribution from Sweden and Baltics• Kazakhstan JV synergy progressing well, material EBITDA contribution• Challenger program delivering, annual run-rate benefits of SEK >600 million

• TDC Sweden acquisition completed October 31, welcoming 800 colleagues • Awarded BCG Global Child Forum prize and Allbright equality award• Moved to new, activity-based and open-plan HQ

3 299 3 053 3 018 3 095

4 029

Q4 15 Q1 16 Q2 16 Q3 16 Q4 16

Sweden – FinancialsNet sales(SEK million)

Mobile end-user serviceRevenue (SEK million)

Q4 Highlights

EBITDA and EBITDA margin(SEK million)

4

1 801 1 758 1 778 1 885 1 928

Q4 15 Q1 16 Q2 16 Q3 16 Q4 16

946 894 8461 068 1 028

29% 29% 28%

35%

26%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

-800

-300

200

700

1 200

Q4 15 Q1 16 Q2 16 Q3 16 Q4 16

TDC

– TDC Sweden consolidated as of October 31, 2016

– Net sales flat (excl. TDC) due to the higher mobile growth being offset by lower fixed telephony and wholesale revenues

– Continued strong mobile end-user service revenue growth of 4%, excl. TDC, driven by consumer postpaid and large enterprise segment

– EBITDA, excl. TDC, flat year-on-year due to higher marketing spend

+22% +7% +9%

3 2941 872

941

Sweden – Continuing momentumConsumer postpaid mobile end-user service revenue

Share of sales with bundle >0.5GB

Q4 Highlights

Geographic coverage2G/4G

Q4 15 Q4 16

5

71%

86%

Q4 15 Q4 16

86% 89%

Q4 15 Q4 16

– Consumer postpaid mobile end-user service revenue up 7% driven by increased data monetization and strong Comviq customer growth

– Tele2 increasingly taking share of premium value buckets

– Highest sales for the Comviq Christmas campaign

– Strong revenue and EBITDA growth within the large enterprise segment with record profit levels in TDC

+7%

Baltics – Financials

Q4 Highlights

6

Net sales(SEK million)

EBITDA and EBITDA margin(SEK million)

Mobile end-user service revenue (SEK million)

476 468 477 521 533

Q4 15 Q1 16 Q2 16 Q3 16 Q4 160

100

200

300

400

500

600

257 246 256287 264

32% 32% 33% 32% 28%

0%

10%

20%

30%

40%

50%

60%

Q4 15 Q1 16 Q2 16 Q3 16 Q4 160

50

100

150

200

250

300

350

815 770 787884 935

Q4 15 Q1 16 Q2 16 Q3 16 Q4 160

100

200

300

400

500

600

700

800

900

1 000

– Net sales growth driven by continued demand for data services and equipment sales

– Mobile end-user service revenue growth driven by prepaid to postpaid migration, data monetization and growth in mobile broadband

– EBITDA growth despite increased marketing investment into the mobile broadband segment in Lithuania

+15% +3%+12%

Baltics – Data monetization continues

7

ASPU development Share of 4G capable smartphones in base

Q4 Highlights

4G population coverage

– Strong data monetization driven by ongoing prepaid to postpaid transition and data centric pricing

– Strong ASPU growth, especially in Lithuania, driven by mobile broadband and consumer postpaid

– 4G handset penetration continues to drive data consumption

– 99% network coverage drives higher data usage and purchase of top-up data buckets

88%99%

Q4 15 Q4 16Q4 15 Q4 16

20%

37%

Q4 15 Q4 16

+7%

Netherlands – Financials

Q4 Highlights– Net sales up due to strong mobile momentum, slightly offset by decline in fixed

– Strong mobile end-user service revenue driven by 24% increase in customer base and solid ASPU development

– Excluding last year’s VAT adjustment of SEK 90 million, underlying mobile end-user service revenue grew 40%

– EBITDA impacted by investments related to mobile launch and benefit of VAT adjustment in Q4 2015

8

Net sales(SEK million)

EBITDA (SEK million)

Mobile end-user service revenue (SEK million)

403322 336

419 438

Q4 15 Q1 16 Q2 16 Q3 16 Q4 160

50

100

150

200

250

300

350

400

450

500

35

-31

-116

-2-23

Q4 15 Q1 16 Q2 16 Q3 16 Q4 16

-150

-100

-50

0

50

100

1 512 1 441 1 452 1 478 1 583

Q4 15 Q1 16 Q2 16 Q3 16 Q4 160

200

400

600

800

1 000

1 200

1 400

1 600

1 800

+5% -166%+9%

Netherlands – Continuing momentumSpontaneous brand awareness & brand consideration (Memo2)

Share of total new postpaid(GfK)

Data usage on own network

Q4 Highlights– Awareness and consideration remain at high levels supported by our ongoing innovative “Fun Rebel Campaign”

– Maintaining a solid market share of new postpaid contracts, 58k net intake in the quarter, despite increased competitive pressure

– Good progress in data on-loading on own network driven by network rollout now at >99% outdoor and >90% indoor coverage

– Doubled our 4G customer base year-on-year to >800k, of which >600k are provisioned for VoLTE and 170k active

9

27%

82%

Pre-launch Dec 164G

34%40%41%

52%

Pre-launch Dec 16

Awareness Consideration

12%

19%

Pre-launchOct 15

Q4 16

-38

14

47

84 92-5%

3%8%

14% 13%

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

Q4 15 Q1 16 Q2 16 Q3 16 Q4 16-40

10

60

110

160

– Net sales stable due to a heavy Altel equipment sales campaign in Q4 2015

– Significant mobile end-user service revenue growth due to higher ASPU and an increasing customer base

– Positive EBITDA development driven by revenue growth, improved operating leverage and synergies from JV integration

Kazakhstan – Financials

10

Q4 Highlights

LFL is constant currency and pro forma for Altel

Net sales, LFL (SEK million)

EBITDA and EBITDA margin, LFL (SEK million)

Mobile end-user service revenue, LFL (SEK million)

404 418 433 457 470

Q4 15 Q1 16 Q2 16 Q3 16 Q4 160

50

100

150

200

250

300

350

400

450

500706

545 574 611702

Q4 15 Q1 16 Q2 16 Q3 16 Q4 160

100

200

300

400

500

600

700

800

+343%+16%0%

6 114 6 440

Q4 15 Q4 16

+5%

Q4 15 Q4 16

Kazakhstan – Strong performanceASPU development, LFL Integration

Q4 Highlights

11

Customer base, LFL(thousands)

LFL is pro forma for Altel

– Customer base continues to grow year-on-year, despite competitive pressure

– Strong ASPU growth driven by our continued focus on improving data monetization

– JV integration well on track with all 2016 integration KPI targets met. ~500 base station sites merged as integration progresses into 2017

– New Altel campaign launched to promote speed, data usage and improved brand consideration

+8%

~500 sites merged

Challenger program on track

Simplify% of products harmonized

on shared platforms

Discipline% of spend strategically

sourced & procured

Consolidate% of reduction in IT OpEx

as share of revenue

Transform% of staff in

Shared Operations

2016 target 2018 targetBaseline

30% 40% 60%

40% 75% 80%

0% 5% 20%

12% 18% 25%

Key progress areas

Further progress made on consolidating key cost categories into strategic sourcing, reaching level above 75% by year end

Continued consolidation of Network & IT organizations into Shared Operations, with Baltics and Croatia joining in Q4 2016, enabling further economies of scale

Productivity improvement program implemented in Sweden, reducing more than 200 FTEs

Announced reduction of additional 75 FTEs in Netherlands

Product simplification initiative progressing. 950 products closed year to date

12

✔

✔

✔

✔

Financial Overview

13

3 242

3 711

12757 35

217 924

Q4 15 Sweden Baltics NL KZ RoW Oth Q4 16

Mobile end-user service revenue

Tele2 Group(SEK million)

14

3 242 3 1293 307

3 598 3 711

Q4 15 Q1 16 Q2 16 Q3 16 Q4 16

+14%

Development per market(SEK million)

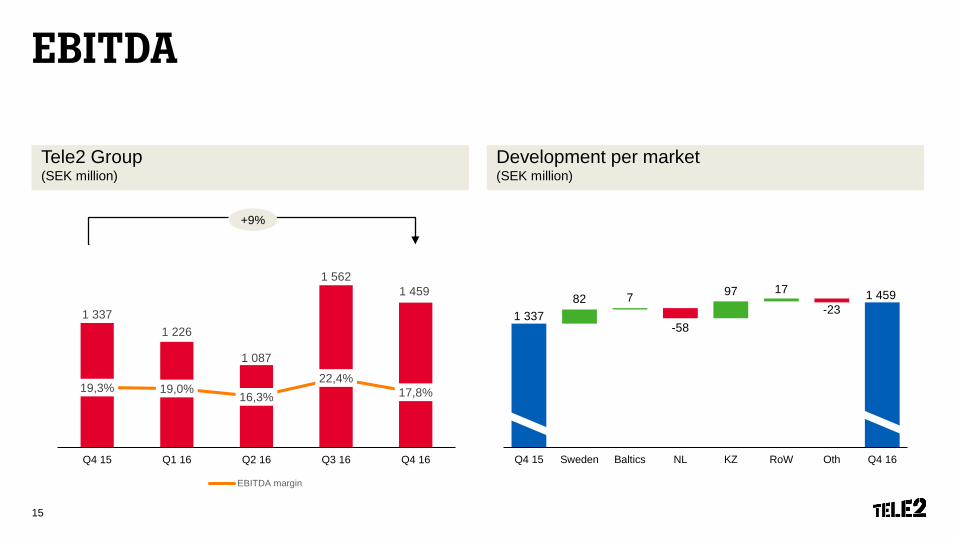

EBITDA

Tele2 Group(SEK million)

15

Development per market(SEK million)

1 3371 226

1 087

1 5621 459

19,3% 19,0%16,3%

22,4%17,8%

0,0%

10,0%

20,0%

30,0%

40,0%

50,0%

60,0%

600

800

1000

1200

1400

1600

Q4 15 Q1 16 Q2 16 Q3 16 Q4 16

EBITDA margin

+9%

1 337

1 45982 7

-58

97 17

-23

630

830

1 030

1 230

1 430

1 630

1 830

Q4 15 Sweden Baltics NL KZ RoW Oth Q4 16

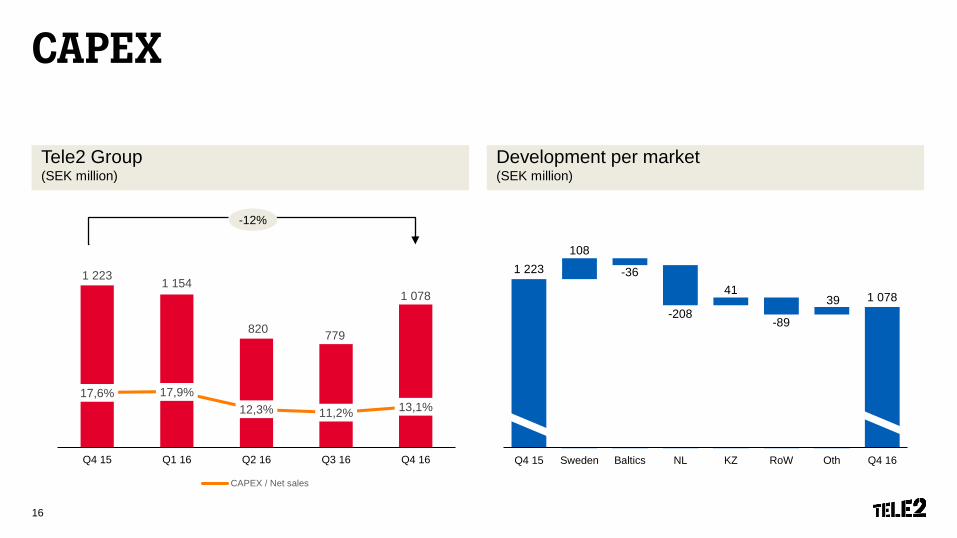

CAPEX

Tele2 Group(SEK million)

16

Development per market (SEK million)

1 223

1 078

108

-36

-208

41

-89

39

350

550

750

950

1 150

1 350

Q4 15 Sweden Baltics NL KZ RoW Oth Q4 16

1 223 1 154

820 779

1 078

17,6% 17,9%12,3% 11,2% 13,1%

0,0%

10,0%

20,0%

30,0%

40,0%

50,0%

60,0%

0

200

400

600

800

1000

1200

1400

Q4 15 Q1 16 Q2 16 Q3 16 Q4 16

CAPEX / Net sales

-12%

Free cash flowTotal operations

Tele2 Group(SEK million)

Development (SEK million)

Free cash flow = Cash flow from operating activities and CAPEX paid17

-291

-154

139

838

394

-500

-300

-100

100

300

500

700

900

Q3 15

Q1 16 Q1 16Q3 16 Q4 16

Q4 15

Q2 16

-291

394

122

-44 -24

130 0

-300

-200

-100

0

100

200

300

400

500

600

Q4 15 EBITDA Interest etc TaxesWorkingcapital CAPEX

One-offitems Q4 16

+235%

501

Cash generation in established markets

18Note: Cash generation defined as (EBITDA-CAPEX)/EBITDA,Established markets defined as Sweden and Baltics

83%80% 77%

66%69%

65%

79% 77%74%

2014 2015 2016

SE Baltics Established

Debt position and financial leverageEconomic net debt to EBITDA 12 m rolling

19 Economic net debt is defined as net debt excluding liabilities from Kazakhtelecom and liabilities guaranteed by Kazakhtelecom

1,88

LeverageSEK billion

9,9 9,4

11,7 11,0 10,4

2,6

1,88

0,0

0,5

1,0

1,5

2,0

2,5

0,0

2,5

5,0

7,5

10,0

12,5

Dec 2015 Mar 2016 Jun 2016 Sep 2016 Dec 2016

Economic net debt Dividend, announced Economic net debt to EBITDA

1,88

SEK 16 billion of debt refinanced

20

4,83,5

1,0 0

7,6

0-1 1-2 2-5 5+ years0,0

1,0

2,0

3,0

4,0

5,0

6,0

7,0

8,0

9,0

10,0

Utilized Unutilized

Maturity profile in Q4 2015(SEK billion)

Maturity profile in Q4 2016(SEK billion)

2,9 0

5,12,4

8,8

0-1 1-2 2-5 5+ years0,0

2,0

4,0

6,0

8,0

10,0

12,0

Utilized Unutilized

Average maturity of net financial debt 1,6 years Average maturity of net financial debt >5 years

Financial guidance 2017

*Based on LFL which is constant currencies and pro forma for Altel and TDC SwedenDividend policy: 2017 dividend to be paid in 2018 21

Net sales(SEK billion)

EBITDA(SEK billion)

31 – 32

5.9 – 6.2

CAPEX(SEK billion)

3.8 – 4.1

Mobile end-user service revenue

Mid-single digit % growth*

Dividend policy

Financial leverage

2017: 4 SEK / share Covered by eFCF from 2019

2.0 - 2.5

Summary

22

Key priorities moving forward

Growth from continued data monetization

Sustain momentum in Sweden and Baltics

Integration of TDC

Further leverage our challenger strategy in

Netherlands and Kazakhstan

Execute on Challenger and synergy programs

23

Winning People & Culture

Value Champion

Step-Change Productivity

Focused Technology

Choices

Tele2’s Way2Win

The Tele2 Way

We are challengers, fast-movers and will always offer our customers what they need for less

We will be champions of customer value in everything we do

How we win

Focused Technology

Choices

Value Champion

Step-Change Productivity

Winning People & Culture

Vision

Mission

Where we play

Mobile access

Our current footprint

Residential and Business

IoT

Responsible Challenger

23

THEEND