Embed Size (px)

Citation preview

February © 2015

From Technologies to Market

Status of Power Electronics

Industry 2015

Sample

From Technologies to Market

2

• Report Objectives 4

• What is in this report 5

• Glossary 8

• Executive Summary 9

• Power Electronics Basic Concepts 29

What are Power Electronics used for? 32

• PE Market 2010 - 2020 50

Wafer Market 58

Device Market 64

Inverter Market 71

• PE Technology Overview 75

Raw Materials 77

IGBTs Technology 86

SJ MOSFETs Technology 98

SiC FETs Technology 106

GaN HEMTs Technology 117

Power Packaging 130

• PE Applications Overview 138

PV Inverters 140

Wind Turbines 147

T&D 154

EV/HEV 163

Rail Traction 172

UPS 180

Industrial Motor Drives 187

• Key Players & PE Supply Chain 196

• PE Future Challenges 218

• Annex 223

• Yole Presentation 226

TABLE OF CONTENTS

©2015 | www.yole.fr | Status of Power Electronics Industry

3

COMPANIES CITED IN THE REPORT

ABB, Alstom, Amphenol, Amsc, AnsaldoBreda, BAIC, Baldor, BMW, Bolloré, Bombardier, Bosch, BYD, CAF, Chilicon Power, Continental, Converteam, CREE, CSR, Curamik, Daimler Chrysler, Danfoss, Delphi, Delta Energy Systems, Denso, DTW

elektronika, Dynex, Eaco, Eagtop, Eaton, Emerson Liebert, Enecsys, Enercon, Enphase Energy, Envision, Fairchild, Ford, Fuji Electric, EPC, EpiWorld, Gamesa, GaN Systems, General Electric, GeneSiC, Goldwind, Hitachi, Holy Stone Polytech, Honda, HYUNDAI

heavy industries, Icemos, Idealec, iEnergy, Infineon, Ingeteam, International Rectifier, Involar, Iveco, IXYS, KACO new energy, Kawasaki, LAAS-CNRS, Leroy Somer, LS Power Semitech, MasterVolt, MCB, Mersen, Methode, MicroGaN, Microsemi, Mingyang,

Mitsubishi Electric, Multi Contact, New Flyer, Nissan, Nordex, NXP, Omron, ON Semiconductor, Panasonic, Parker, Powdec, Powerex, Powersem, Poseico, Positronic, PSA, Raytheon, Renault, Renesas, RFMD, Rockwell Automation, Rogers Corporation,

Rohm, Schneider Electric, Samsung heavy industries, SanKen, SanRex, SBE, Semikron, Semisouth, SEPSA, Shindengen, SICC, Siemens, SMA Solar Technology, SMBE, Sinovel, SolarMax, STMicroelectronics, Sungrow, Tabuchi, TDK, TE connectivity, Tesla Motors, TMEIC, Toshiba, ToyoDenki, Toyota, Transphorm, TYSTC, United Power Technology, Vacon, Vestas, Vincotech, VisIC

Technologies, Vishay, Volvo, WDI, Yaskawa, Yutong…

©2015 | www.yole.fr | Status of Power Electronics Industry

4

OVERALL POWER ELECTRONICS MARKET

2014 – 2020 value chain analysis: system, device, wafer

The power electronics market perspectives are very optimistic with a CAGR superior than 6% for the period 2014-2020

Electronics Systems

$xxxx B

Power Inverters$xxxx B

Semiconductor power devices (discrete and

modules)

$11.5 B

Power wafers$xxxx B

Electronics Systems

$xxxx B

Power Inverters$xxxx B

Semiconductor power devices (discrete and

modules)

$17.2 B

Power wafers$xxxxB

2014 2020

CAGR: +xx%

CAGR: +6.9%

CAGR: +2%

CAGR: +6.1%

©2015 | www.yole.fr | Status of Power Electronics Industry

5

WAFER MARKET FORECAST 2010-2020

Market size split by diameter

The 6” (150mm) wafers are the most sold ones, but 200mm wafers will considerably increase its market share

©2015 | www.yole.fr | Status of Power Electronics Industry

6

INVERTER MARKETS AND DRIVERS

The overall inverter market in 2014 exceeded the $xx B

Andothers…

Drivers for inverter innovation

Drivers for application growth

Size reduction

Weight reduction

Efficiency improvement

Cost reduction

• Increase of CO2 emission taxes

• Demand and regulations for clean energy generation

• Need for mass transportation

• Need for efficient transportation

• Regulation on energy efficiency

• Data center and data storage market increase

• Utility grid stress increasing due to the use of clean energy

Depending on applications

Wind turbines$2.7 B -2.1%

PV inverter$xx B +2.2%

Motor drives

$xxx B +8%

Rail traction$3.3 B +5.2%

UPS$10 B +0.9%

EV/HEV$xxxx B +15%

Inverter markets*

* In 2014

©2015 | www.yole.fr | Status of Power Electronics Industry

7

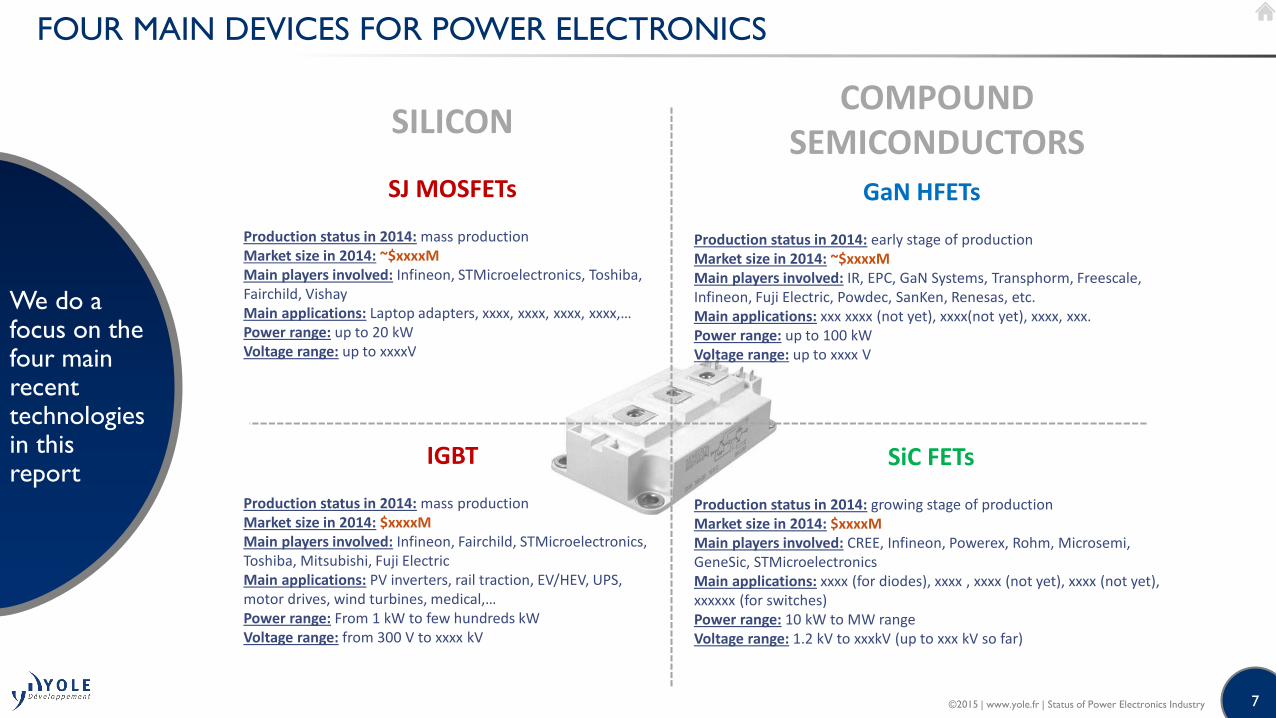

FOUR MAIN DEVICES FOR POWER ELECTRONICS

We do a focus on the four main recent technologies in this report

SiC FETs

Production status in 2014: growing stage of productionMarket size in 2014: $xxxxMMain players involved: CREE, Infineon, Powerex, Rohm, Microsemi, GeneSic, STMicroelectronicsMain applications: xxxx (for diodes), xxxx , xxxx (not yet), xxxx (not yet), xxxxxx (for switches)Power range: 10 kW to MW rangeVoltage range: 1.2 kV to xxxkV (up to xxx kV so far)

SJ MOSFETs

Production status in 2014: mass productionMarket size in 2014: ~$xxxxMMain players involved: Infineon, STMicroelectronics, Toshiba, Fairchild, VishayMain applications: Laptop adapters, xxxx, xxxx, xxxx, xxxx,…Power range: up to 20 kWVoltage range: up to xxxxV

GaN HFETs

Production status in 2014: early stage of productionMarket size in 2014: ~$xxxxMMain players involved: IR, EPC, GaN Systems, Transphorm, Freescale, Infineon, Fuji Electric, Powdec, SanKen, Renesas, etc.Main applications: xxx xxxx (not yet), xxxx(not yet), xxxx, xxx.Power range: up to 100 kWVoltage range: up to xxxx V

SILICONCOMPOUND

SEMICONDUCTORS

IGBT

Production status in 2014: mass productionMarket size in 2014: $xxxxMMain players involved: Infineon, Fairchild, STMicroelectronics, Toshiba, Mitsubishi, Fuji ElectricMain applications: PV inverters, rail traction, EV/HEV, UPS, motor drives, wind turbines, medical,…Power range: From 1 kW to few hundreds kWVoltage range: from 300 V to xxxx kV

©2015 | www.yole.fr | Status of Power Electronics Industry

8

SEMICONDUCTOR EVOLUTIONS

Power device technology positioning

WBG devices are primarily positioned in high-end applications

1200V or more

600V or less

Pro

du

ct r

ange

Voltage

IGBTThyristor

IGCT…

SiC

MOSFET

Triacs

Bipolar…

3.3kV and more200V

GaN GaN Yole Développement - December 2014

©2015 | www.yole.fr | Status of Power Electronics Industry

9

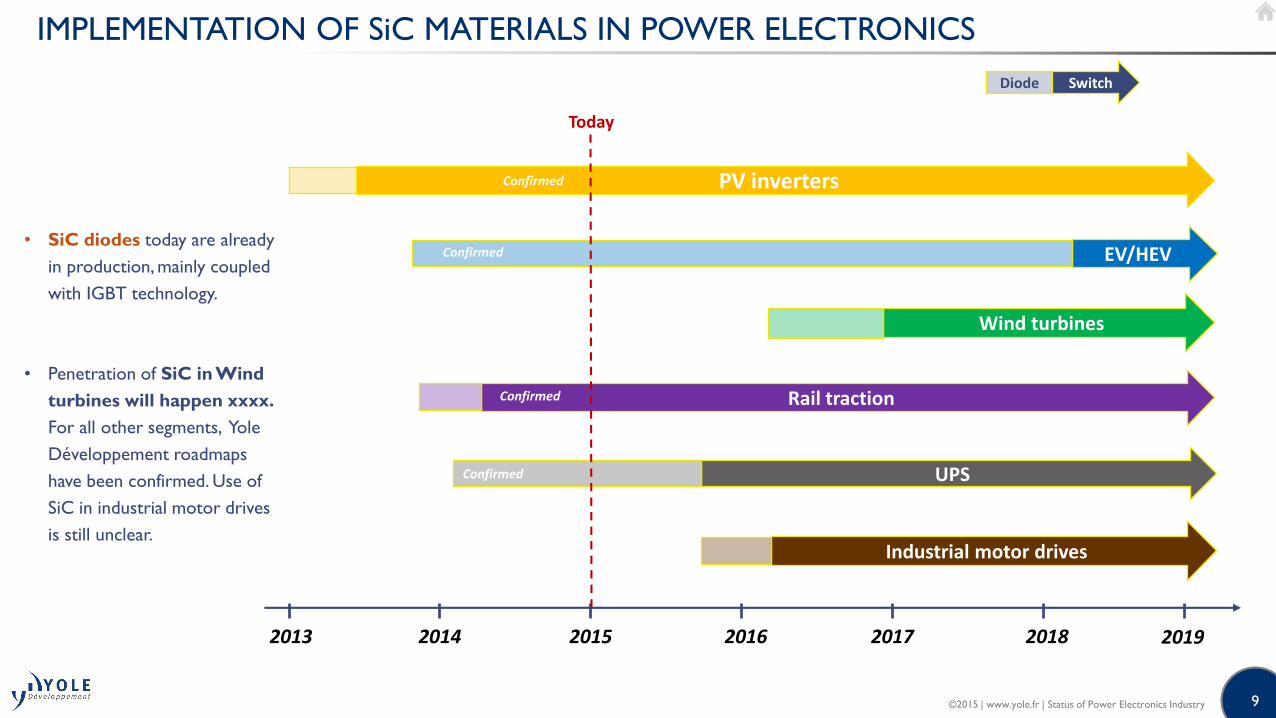

IMPLEMENTATION OF SiC MATERIALS IN POWER ELECTRONICS

• SiC diodes today are already

in production, mainly coupled

with IGBT technology.

• Penetration of SiC in Wind

turbines will happen xxxx.

For all other segments, Yole

Développement roadmaps

have been confirmed. Use of

SiC in industrial motor drives

is still unclear.

2013 2014 2015 2016 2017 2018 2019

Industrial motor drives

UPS

Rail traction

Wind turbines

EV/HEV

PV inverters

Confirmed

Confirmed

Confirmed

Today

Confirmed

Diode Switch

©2015 | www.yole.fr | Status of Power Electronics Industry

10

IMPLEMENTATION OF GaN MATERIALS IN POWER ELECTRONICS

• Characteristics of GaN-based

inverters will be:

• They will primarily target medium

voltage applications (in the 200 –

600V range)

• GaN targeted applications will

be very different from SiC, at

first. We will observe a competition

in xxxx. For the EV/HEV, xxxxxxx.

• GaN devices are excluded from

high-voltage applications such as

wind turbines and rail traction.

2013 2014 2015 2016 2017 2018 2019

Industrial motor drives

UPS

Rail traction

Wind turbine

EV/HEV

PV inverters

PFC/Power supplies

Small DC/DC converters Wireless chargers

Today

Confirmed

©2015 | www.yole.fr | Status of Power Electronics Industry

11

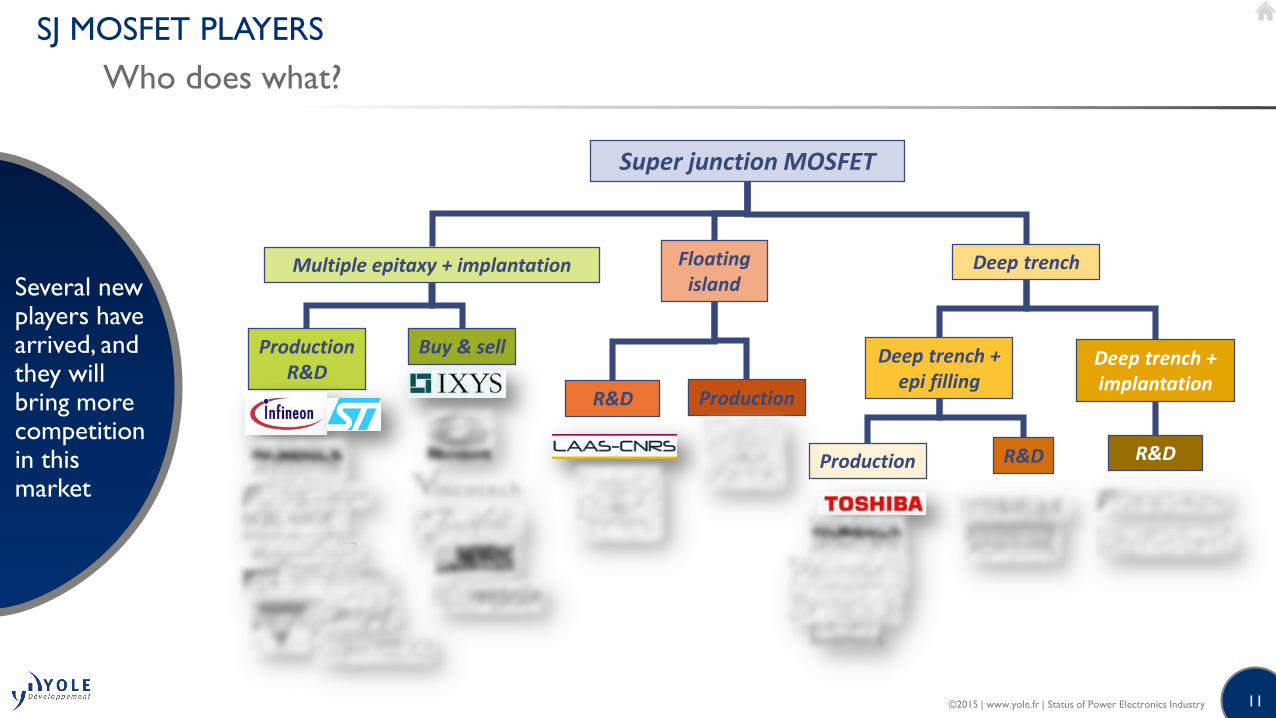

SJ MOSFET PLAYERS

Who does what?

Several new players have arrived, and they will bring more competition in this market

Super junction MOSFET

Multiple epitaxy + implantation Deep trench

ProductionR&D

Buy & sell

Production R&D

Deep trench + epi filling

Deep trench + implantation

R&D

Floating island

Production

R&D

2013

©2015 | www.yole.fr | Status of Power Electronics Industry

12

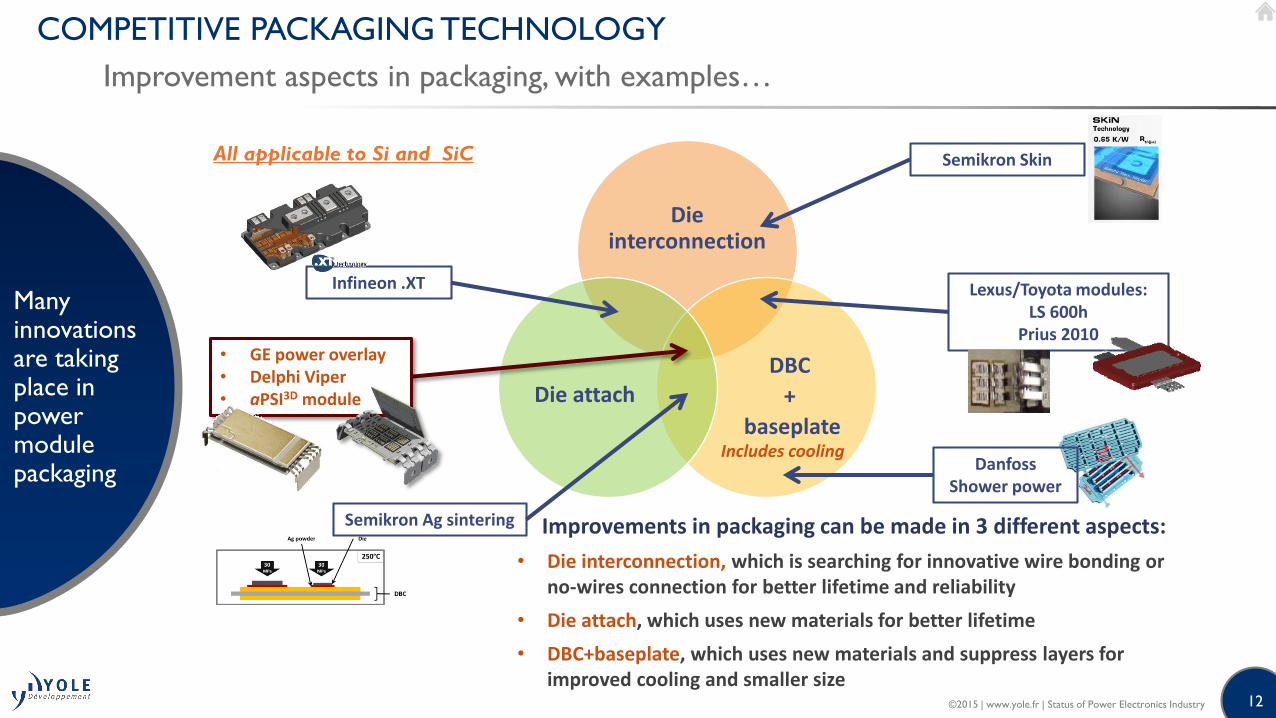

COMPETITIVE PACKAGING TECHNOLOGY

Improvement aspects in packaging, with examples…

Many innovations are taking place in power module packaging

Die interconnection

DBC

+

baseplate

Die attach

Infineon .XT Lexus/Toyota modules:LS 600h

Prius 2010

Semikron Ag sintering

Semikron Skin

• GE power overlay• Delphi Viper• aPSI3D module

Improvements in packaging can be made in 3 different aspects:

• Die interconnection, which is searching for innovative wire bonding or no-wires connection for better lifetime and reliability

• Die attach, which uses new materials for better lifetime

• DBC+baseplate, which uses new materials and suppress layers for improved cooling and smaller size

All applicable to Si and SiC

Includes coolingDanfoss

Shower power

©2015 | www.yole.fr | Status of Power Electronics Industry

13

INVERTER MARKET FORECAST

2010-2020

Description and market trends of each application are presented on this report

©2015 | www.yole.fr | Status of Power Electronics Industry

14

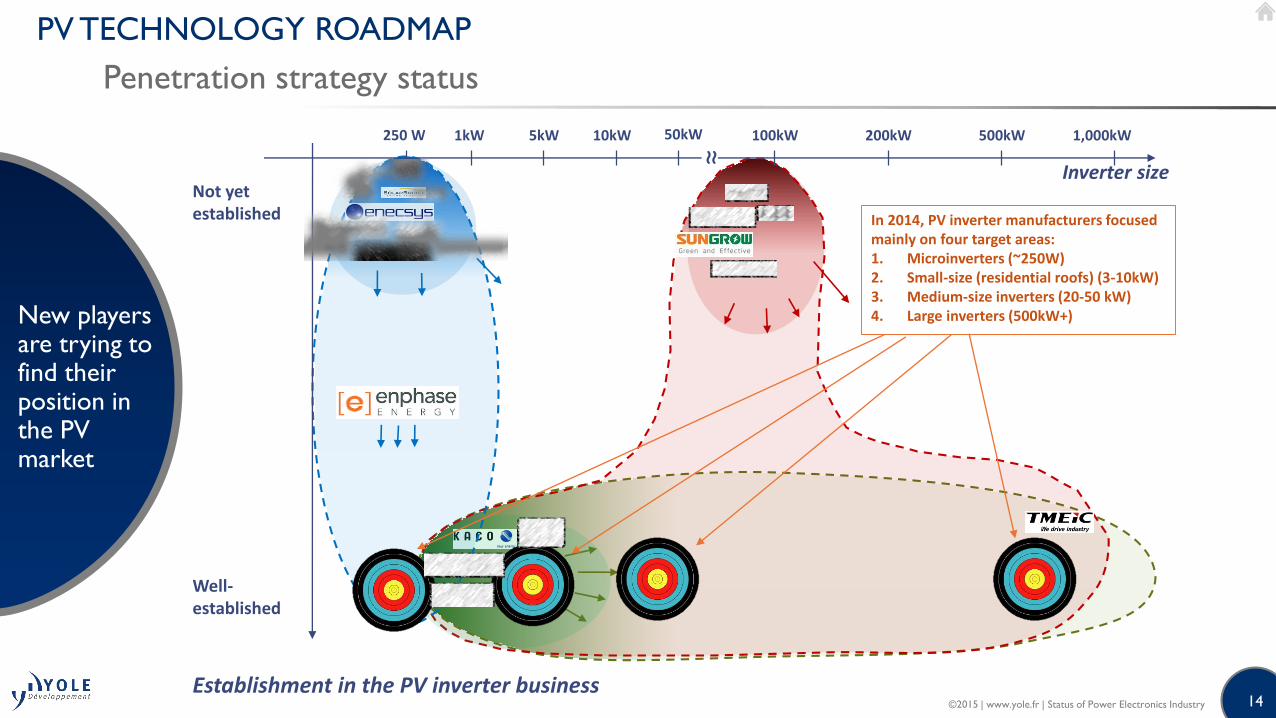

PV TECHNOLOGY ROADMAP

Penetration strategy status

New players are trying to find their position in the PV market

1,000kW500kW200kW100kW10kW5kW250 W 1kW 50kW

Not yet established

Well-established

Inverter size

Establishment in the PV inverter business

≈

In 2014, PV inverter manufacturers focused mainly on four target areas:1. Microinverters (~250W)2. Small-size (residential roofs) (3-10kW)3. Medium-size inverters (20-50 kW)4. Large inverters (500kW+)

©2015 | www.yole.fr | Status of Power Electronics Industry

15

WIND TURBINES MAIN PLAYERS LOCATION AND STRATEGY

Goldwind = No1. in China in 2013

GE Wind = No1. in the US in 2013

Chinese players are rapidly growing within China and looking for foreign markets. Some Chinese players have chosen the strategy of JV

with key EU technology players in order to speed-up their development.

All players are looking for new market opportunities: some by developing large turbines in 6MW+ size for offshore applications other via focusing on

promising new markets especially in South America.

©2015 | www.yole.fr | Status of Power Electronics Industry

16

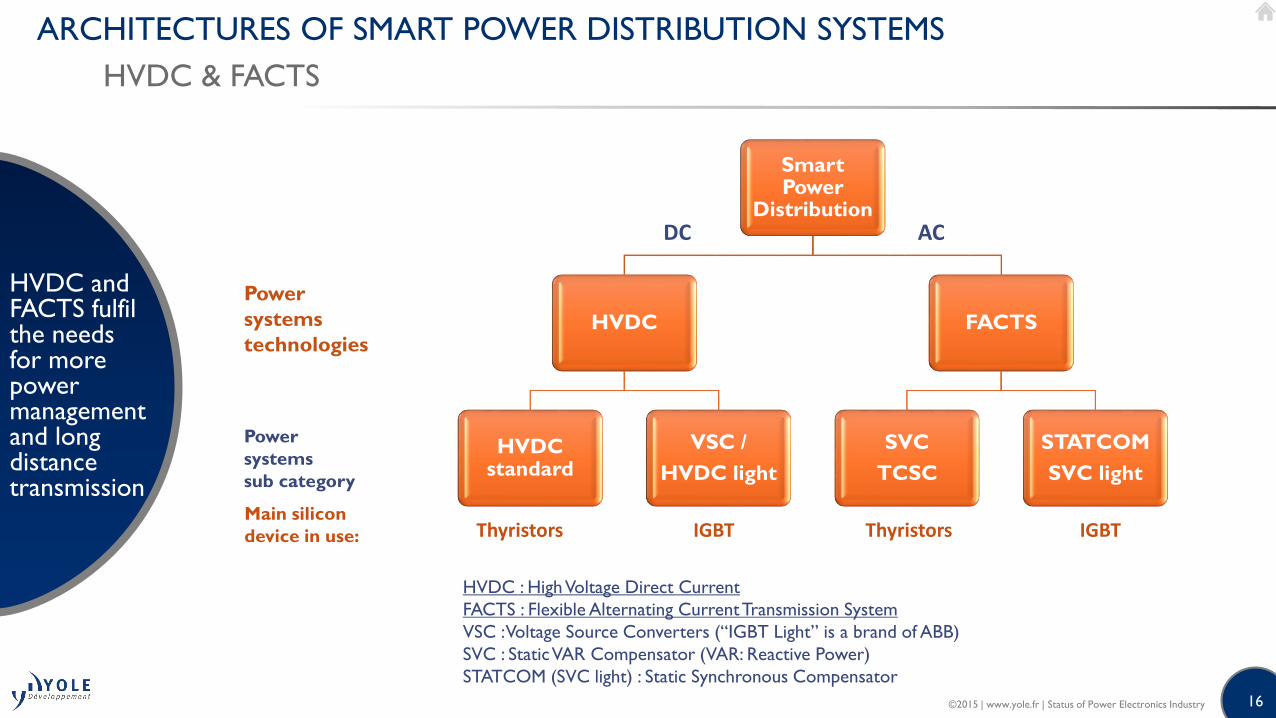

ARCHITECTURES OF SMART POWER DISTRIBUTION SYSTEMS

HVDC & FACTS

HVDC and FACTS fulfil the needs for more power management and long distance transmission

Smart Power

Distribution

HVDC

HVDC standard

VSC /

HVDC light

FACTS

SVC

TCSC

STATCOM

SVC light

Thyristors IGBT Thyristors IGBT

Power

systems

technologies

Power

systems

sub category

Main silicon

device in use:

HVDC : High Voltage Direct Current

FACTS : Flexible Alternating Current Transmission System

VSC : Voltage Source Converters (“IGBT Light” is a brand of ABB)

SVC : Static VAR Compensator (VAR: Reactive Power)

STATCOM (SVC light) : Static Synchronous Compensator

DC AC

©2015 | www.yole.fr | Status of Power Electronics Industry

17

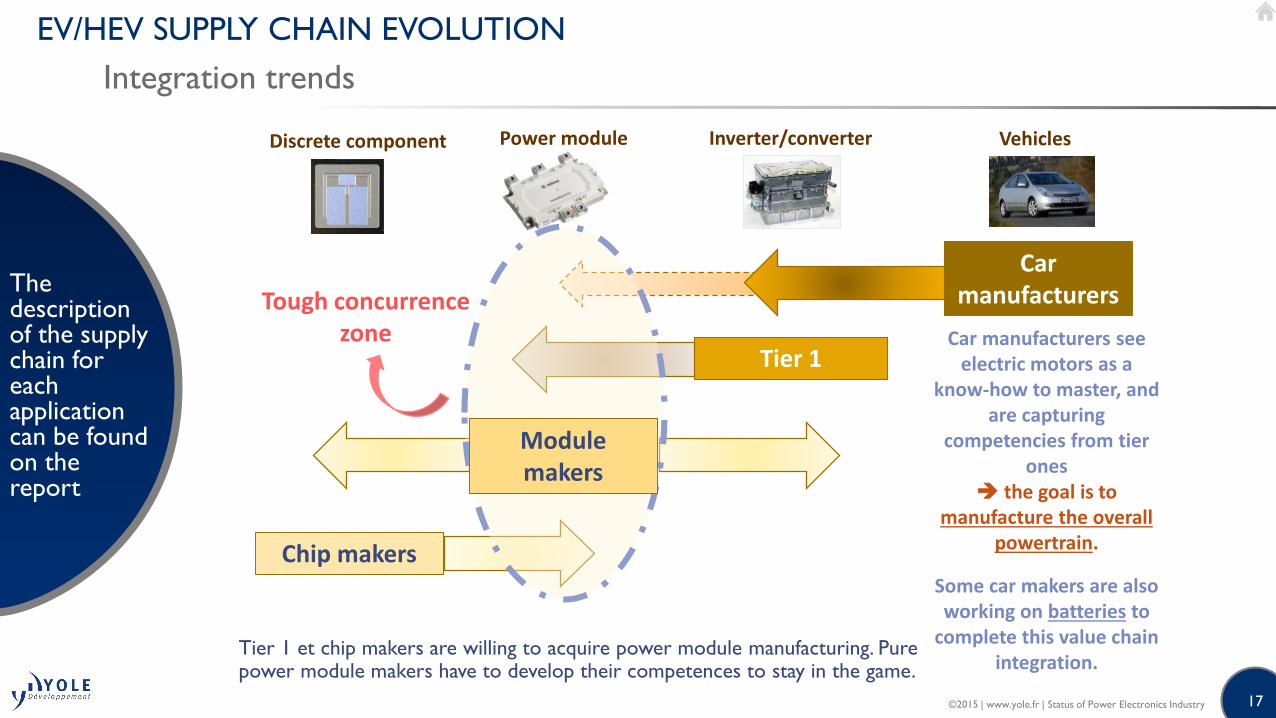

EV/HEV SUPPLY CHAIN EVOLUTION

Integration trends

Tier 1 et chip makers are willing to acquire power module manufacturing. Pure power module makers have to develop their competences to stay in the game.

Power module Inverter/converter VehiclesDiscrete component

Car manufacturers

Tier 1

Chip makers

Module makers

Tough concurrence zone Car manufacturers see

electric motors as a know-how to master, and

are capturing competencies from tier

ones the goal is to

manufacture the overall powertrain.

Some car makers are also working on batteries to

complete this value chain integration.

The description of the supply chain for each application can be found on the report

©2015 | www.yole.fr | Status of Power Electronics Industry

18

RAIL TRACTION SUPPLY CHAIN

DYNEX’s acquisition by CSR is an example of Asiatic vertical integration.

Dies IGBT modules Power Inverter Modules Train makers

©2015 | www.yole.fr | Status of Power Electronics Industry

19

UPS POWER ELECTRONICS

Component adoption for UPS inverters

• At the component level, we have observed two main trends:

• Adoption of power modules in opposition to power discrete devices, for the low power segment:

• xxxxx

• IGBT will be the most demanded device for UPS business within the next five years:

• xxxxxx

• xxxxxx

IGBTs are and will be the most used devices in UPS

Power range Number of devices Topology Device voltage

Low power UPS xxxx• H-bridge topology

• Single phasexxxx

Medium power UPS xxxx

• IGBT rectifier

• 3 phase

• Cascaded H-bridge or NPC topologiesxxxx

High power UPS xxxx

• IGBT rectifier

• 3 phase

• Multi-level topologies

©2015 | www.yole.fr | Status of Power Electronics Industry

20

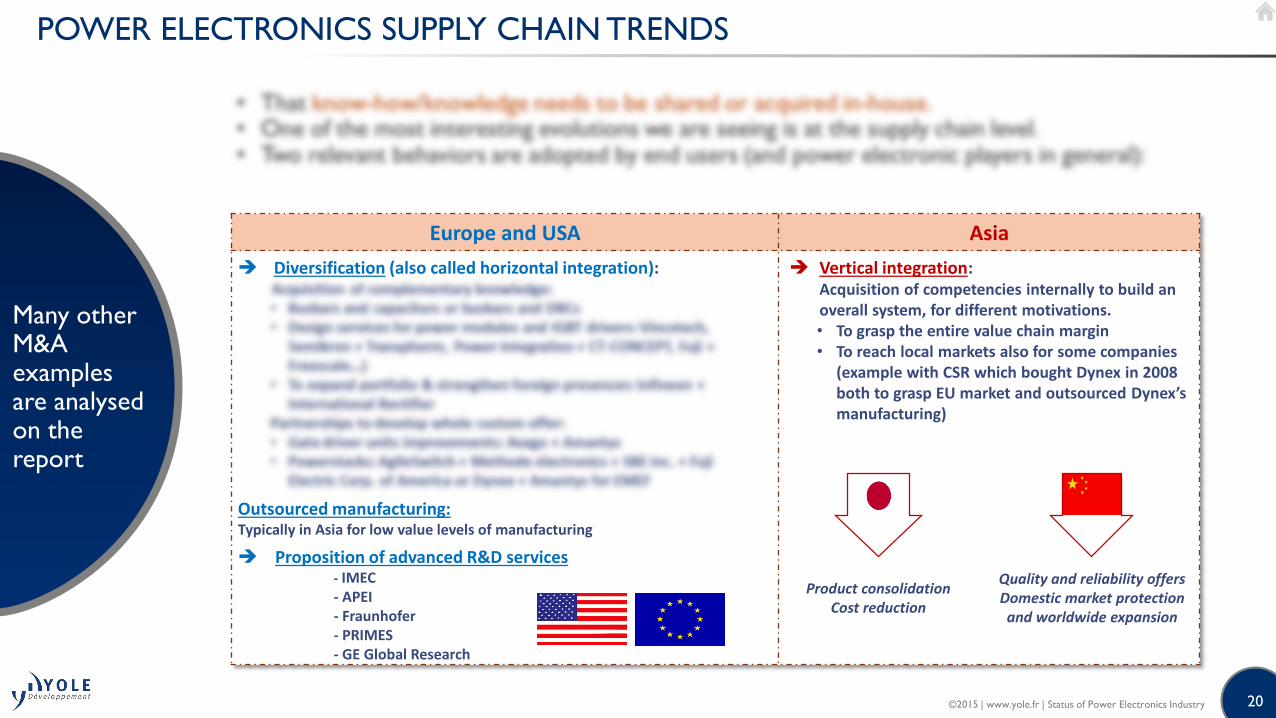

POWER ELECTRONICS SUPPLY CHAIN TRENDS

Many other M&A examples are analysed on the report

Europe and USA Asia

Vertical integration: Acquisition of competencies internally to build an overall system, for different motivations.• To grasp the entire value chain margin• To reach local markets also for some companies

(example with CSR which bought Dynex in 2008 both to grasp EU market and outsourced Dynex’smanufacturing)

Diversification (also called horizontal integration):

Outsourced manufacturing:Typically in Asia for low value levels of manufacturing

Proposition of advanced R&D services- IMEC- APEI- Fraunhofer- PRIMES- GE Global Research

Product consolidationCost reduction

Quality and reliability offersDomestic market protection and worldwide expansion

©2015 | www.yole.fr | Status of Power Electronics Industry

21

VERTICAL & HORIZONTAL INTEGRATION

A technological need

• The main purpose of power electronics continue to be integration.

• Therefore, establishing interactions and synergy dynamics among different players is necessary so that knowledge canbe shared and the overall system improved.Acquisitions and partnerships are the key:

Vertical integration helps reducing costs. Diversification takes profit of different synergies to get a more compact system.

Capacitor

Laminated busbar

Cooling system

INVERTERPossible by mastering both

technologies (examples: SBE and Methode Electronics, Eagtop…)

Can be extended toward IGBT stack/inverter assembly

with cooling systems, and other components (Power modules, IGBT drivers…)

IGBT driver

Power module

IGBT stack/inverter assembly

Capacitor+busbar assembly:

Resistor

Power stack backbone

©2015 | www.yole.fr | Status of Power Electronics Industry

22

UP-FRONT INTEGRATION

From chips to inverters

Many Japanese chip manufacturers have accessed higher added value markets

• Drivers for this integration are:

• Technology development: access to new skills

• Partnering, developing sales network

• Access to higher added value markets

• Main risks are:

– Customers becoming competitors

– Access new technologies, especially at the inverter

level

• Most concerned are Japanese players

Inverter makersSystem

integrators

Power module makers

Chip makers

Power discrete makers

Passive makers

Busbar and connector makers

Supplies to…

Expansion trend

©2015 | www.yole.fr | Status of Power Electronics Industry

23

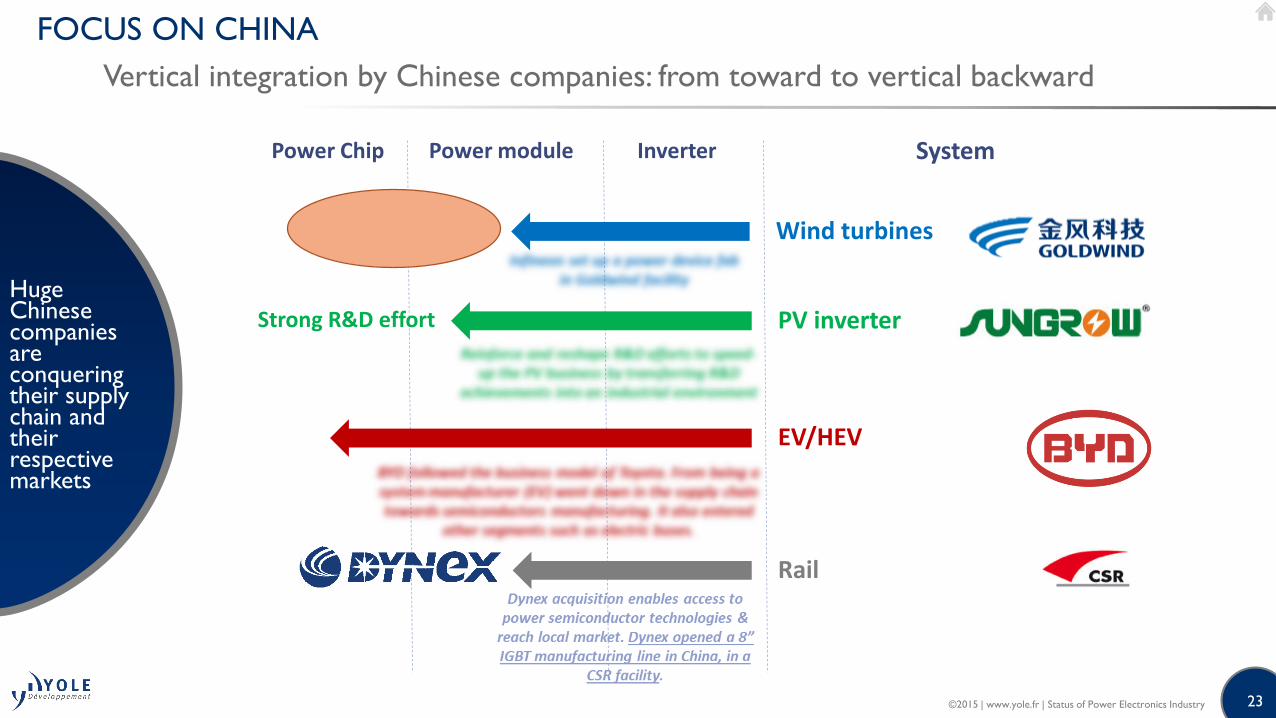

FOCUS ON CHINA

Vertical integration by Chinese companies: from toward to vertical backward

Huge Chinese companies are conquering their supply chain and their respective markets

SystemInverterPower modulePower Chip

Rail

EV/HEV

PV inverter

Wind turbines

Strong R&D effort

©2015 | www.yole.fr | Status of Power Electronics Industry