Embed Size (px)

Citation preview

Rapid Growth Opportunities – Independent Power Producers in South Africa

Gareth Blanckenberg, Research Analyst

Energy & PowerEnergy & Power

September 7, 2011

Functional Expertise

• Experience in analysis and research, including several market and academic research projects.

Industry Expertise

� Experience in the energy and power sector

- Analysis of investment opportunities in Sub-Saharan Africa energy sector

- Energy efficiency research

What I bring to the Team

• General and varied experience

• Financial background

Career Highlights

• Professional Sailor

Today’s Presenter: Gareth Blanckenberg

Gareth BlanckenbergResearch AnalystEnergy and Power Systems

2

Education

• BBusSc in Management Studies from University of Cape Town, South Africa

Systems

Frost & SullivanAfricaCape Town

Key Market Drivers and Restraints

Private Power Generation: Key Market Restraints (South Africa), 2011

Historically Low Tariffs

Uncertainty

Skewed RiskAllocation

3

Private Power Generation: Key Market Drivers (South Africa), 2011

Tariff Increases

Growing Demand

Constraints on Eskom Liberalization of

ElectricityIndustry

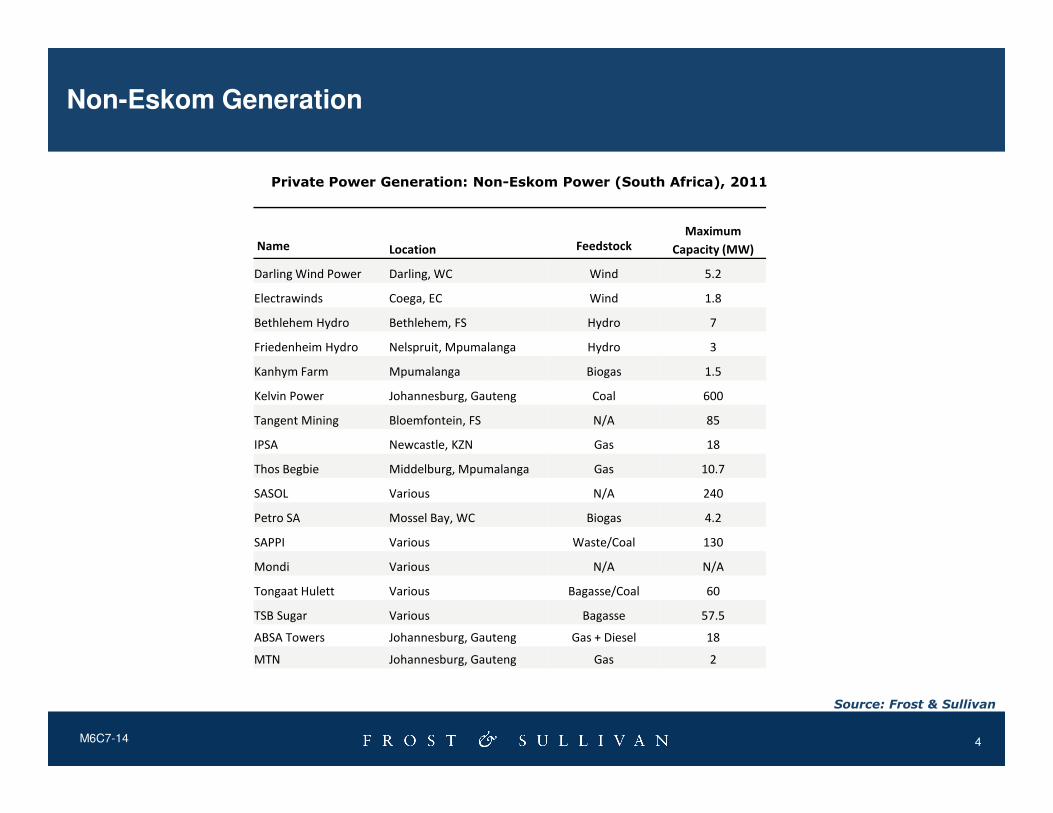

Non-Eskom Generation

Name Location FeedstockMaximum

Capacity (MW)

Darling Wind Power Darling, WC Wind 5.2

Electrawinds Coega, EC Wind 1.8

Bethlehem Hydro Bethlehem, FS Hydro 7

Friedenheim Hydro Nelspruit, Mpumalanga Hydro 3

Kanhym Farm Mpumalanga Biogas 1.5

Kelvin Power Johannesburg, Gauteng Coal 600

Private Power Generation: Non-Eskom Power (South Africa), 2011

4M6C7-14

Source: Frost & Sullivan

Tangent Mining Bloemfontein, FS N/A 85

IPSA Newcastle, KZN Gas 18

Thos Begbie Middelburg, Mpumalanga Gas 10.7

SASOL Various N/A 240

Petro SA Mossel Bay, WC Biogas 4.2

SAPPI Various Waste/Coal 130

Mondi Various N/A N/A

Tongaat Hulett Various Bagasse/Coal 60

TSB Sugar Various Bagasse 57.5

ABSA Towers Johannesburg, Gauteng Gas + Diesel 18

MTN Johannesburg, Gauteng Gas 2

IRP 2010: Capacity Requirements by Technology

New Build Options

Coal CCGT OCGTImport Hydro

Wind Solar PV CSP NuclearTotal New Build

Total System Capacity

2010 0 0 0 0 0 0 0 0 640 44535

2011 0 0 0 0 0 0 0 0 809 45344

2012 0 0 0 0 0 300 0 0 1103 46447

2013 0 0 0 0 0 300 0 0 2901 49348

2014 500 0 0 0 400 300 0 0 3021 52369

2015 500 0 0 0 400 300 0 0 2564 54933

2016 0 0 0 0 400 300 100 0 1432 56365

0 0 0 0 400 300 100 0 2968 59333

Private Power Generation: IRP2010 New Build Analysis (South Africa), 2011

5M6C7-14

2017 0 0 0 0 400 300 100 0 2968 59333

2018 0 0 0 0 400 300 100 0 1523 60856

2019 250 237 0 0 400 300 100 0 2496 63352

2020 250 237 0 0 400 300 100 0 2010 65362

2021 250 237 0 0 400 300 100 0 1212 66574

2022 250 0 805 1143 400 300 100 0 1365 67939

2023 250 0 805 1183 400 300 100 1600 2358 70297

2024 250 0 0 283 800 300 100 1600 2424 72721

2025 250 0 805 0 1600 1000 100 1600 3835 76556

2026 1000 0 0 0 400 500 0 1600 3500 80056

2027 250 0 0 0 1600 500 0 0 2350 82406

2028 1000 474 690 0 0 500 0 1600 1414 83820

2029 250 237 805 0 0 1000 0 1600 2764 86584

2030 1000 948 0 0 0 1000 0 0 2948 89532

6250 2370 3910 2609 8400 8400 1000 9600 45637

Note: All figures are rounded; Source: IRP2010

IPP Procurement Programme

• REFIT scrapped in favour of Competitive Bidding process

Technology Capacity Price Cap

Onshore Wind 1,850 MW R1.15 kWh

Solar PV 1,450 MW R2.85 kWh

CSP 200 MW R2.85 kWh

Biomass Solid 12,5 MW R1.07 kWh

6M6C7-14

• Projects need to be able to feasibly enter commercial operation by June 2014

• CSP by June 2015

Biomass Solid 12,5 MW R1.07 kWh

Biogas 12,5 MW R0.80 kWh

Landfill Gas 25 MW R0.60 kWh

Small Hydro 75 MW R1.03 kWh

Small Projects (<5MW) 100 MW

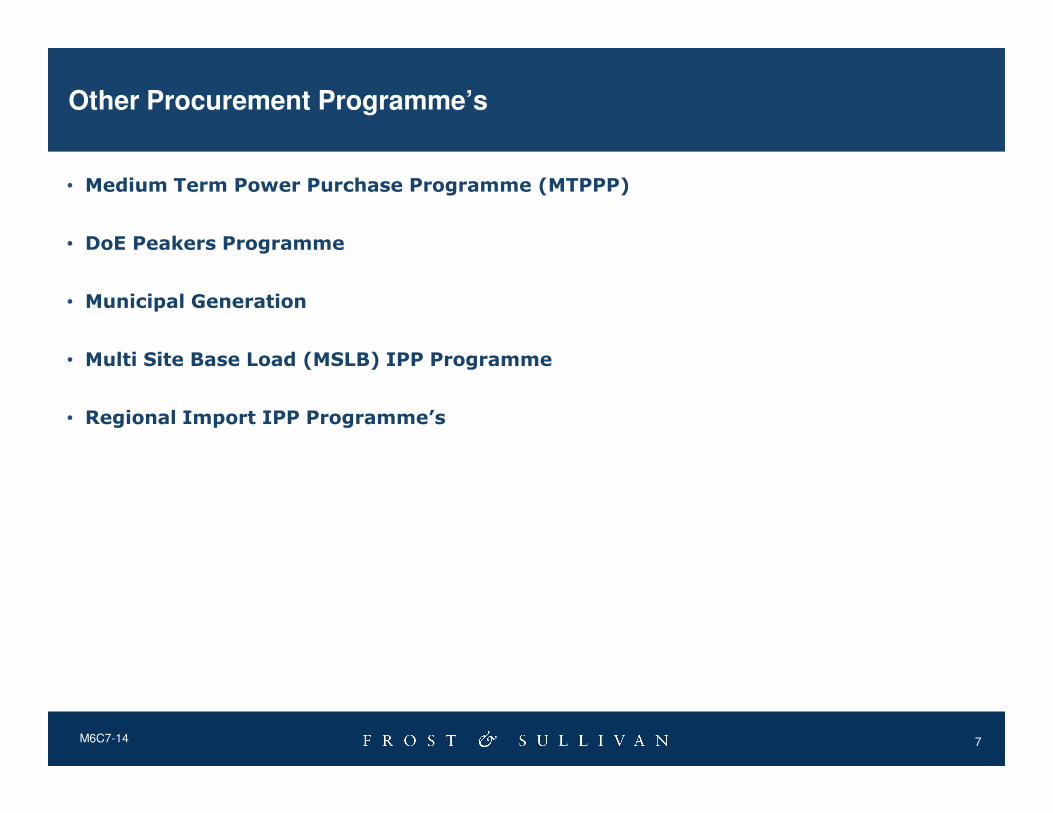

Other Procurement Programme’s

• Medium Term Power Purchase Programme (MTPPP)

• DoE Peakers Programme

• Municipal Generation

• Multi Site Base Load (MSLB) IPP Programme

Regional Import IPP Programme’s

7M6C7-14

• Regional Import IPP Programme’s

Electricity Tariff Path

Period 07/08 08/09 09/10 10/11 12/13 13/14 14/15 15/16

Private Power Generation: Average Tariff Changes (South Africa), 2011

8M6C7-14

Average Tariff R0.19 R0.25 R0.33 R0.41 R0.52 R0.66 R0.82 R1.03

Rate of Increase 34.2% 31% 24.8% 25.8% 25.9% 25% 25%

CAGR 27.3%

Source: Frost & Sullivan

Opportunity for IPP’s

50,000

60,000

70,000

80,000

90,000

Growth and Mix of Generation Capacity IRP2010

Other

• South Africa is blessed with natural resources for generation utilising all available feedstock.

• Until 2011, market development has been restrained.

• The first round of the IPP

9M6C7-14

-

10,000

20,000

30,000

40,000

50,000

Capacity in 2010 Capacity in 2030

Other

Pumped Storage

Nuclear

Renewables

Hydrocarbons

• The first round of the IPP Procurement Program for Renewables should open the floodgates and pave the way for other projects.

• A DOUBLING of current generation capacity is required, so the opportunity is large.

Source: Frost & Sullivan

Next Steps

� Request a proposal for Growth Partnership Services or Growth Consulting Services to support you and your team to accelerate the growth of your company. ([email protected])

� Join us at our annual Growth, Innovation, and Leadership 2012: A Frost & Sullivan Global Congress on Corporate Growthoccurring 15 – 16 May, 2012 (www.gil-global.com)

10

� Register for Frost & Sullivan’s Growth Opportunity Newsletter and keep abreast of innovative growth opportunities (www.frost.com/news)

Your Feedback is Important to Us

Growth Forecasts?

Competitive Structure?

What would you like to see from Frost & Sullivan?

11

Emerging Trends?

Strategic Recommendations?

Other?

Please inform us by rating this presentation

Frost & Sullivan’s Growth Consulting can assist with your growth strategies

Follow Frost & Sullivan on Facebook, LinkedIn, SlideShare, and Twitter

http://www.facebook.com/FrostandSullivan

http://www.linkedin.com/companies/4506

12

http://twitter.com/frost_sullivan

http://www.linkedin.com/companies/4506

http://www.slideshare.net/FrostandSullivan

For Additional Information

Samantha James

Corporate Communications

Industry

(021) 680-3566

Stephane Gay

Sales Manager

Energy & Power

(021) 680-3286

13

Cornelis van der Waal

Research Manager

Energy & Power

(021) 680-3266