Embed Size (px)

DESCRIPTION

Michael Roche, Chief Executive Officer, Queensland Resources Council delivered this presentation at the Galilee Basin Coal & Energy Conference 2012. This two day event looks at the significant proposed investment in the Galilee area including coal mining, underground coal gasification, coal seam gas, geothermal, shale and much more, bringing together the wide variety of explorers, project developers, service providers and government representatives under the one roof. For more information about the annual industry gathering in Brisbane/Australia please visit the conference website: http://bit.ly/1fvyzHz

Citation preview

Michael Roche

Chief Executive

Queensland’s resources outlook

Galilee Basin Coal and Energy Conference Hilton Hotel, Brisbane 12 November 2012

Today‟s messages

• Days of easy money on the back of high commodity prices are over

• Hard work ahead is growing volumes, boosting productivity, getting costs down and holding onto or growing market share

• Time to get serious about labour market, skilling, infrastructure and taxation reforms

• Tough market globally and will be for some time but signs of prices bottoming

• Confident about long-term growth prospects.

> The Queensland Resources Council (QRC) is a not-for-profit peak industry

association representing the commercial developers of Queensland‟s

minerals and energy resources

> 90 full members – explorers, miners, mineral processors, site contractors,

oil and gas producers, electricity generators

> 178 service members - providers of goods or services to the sector

Who is the Queensland Resources Council?

90

full

members

178

service

members

41

associate

members

Aberdare Collieries

Adani Mining

A.J. Lucas Coal Technologies

Alcyone Resources

Allegiance Coal

Altona Mining

Ambre Energy

Anglo American Exploration

Anglo American Metallurgical Coal

Aquila Resources

Arrow Energy

Bandanna Energy

BHP Billiton Cannington

BHP Billiton Mitsubishi Alliance

Birla Mt. Gordon

Blackwood Corporation

Caledon Coal

Cape Alumina

Cape Flattery Silica Mines

Carabella Resources

Carbon Energy

Carpentaria Gold

Cement Australia

Civil Mining and Construction

Clean Energy Australasia

Clean Global Energy

Coalbank

Cockatoo Coal

CuDeco

Downer EDI Mining

Eagle Downs Coal Management

Ensham Resources

ERM Power

Evolution Mining

Exco Resources

Golding Contractors

Guildford Coal

GVK Hancock Coal

Investigator Resources

Ivanhoe Australia

Jellinbah Resources

Jindal Steel & Power

John Holland

Lagoon Creek Resources

Leighton Contractors

Liberty Resources

Linc Energy

Macmahon Holdings

MacMines Austasia

Mastermyne

Mega Uranium

Metallica Minerals

MetroCoal

Millmerran Power Management

Minerals and Metals Group

Mitsubishi Development

New Hope Group

Norton Gold Fields

Origin Energy

Paladin Resources

Peabody Energy

QCoal

QER

QGC

Rio Tinto Alcan

Rio Tinto Coal Australia

Santos/TOGA

Sibelco Australia

Sojitz Coal Mining

Sonoma Mine Management

Stanmore Coal

Strait Resources

Summit Resources

Superior Coal

Tata Steel Resources Australia

Thiess

Undamine Industries

Vale

Vital Metals

Watpac Civil & Mining

Wesfarmers Resources

Westside Corporation

Whitehaven Coal

Xstrata Coal Australia

Xstrata Copper

Xstrata Zinc Australia

Yancoal Australia

The way it was: Growth Outlook Study – November 2011

QRC commissioned study to provide government/industry with thorough and consistent

understanding of ability of Queensland economy to expand to meet needs of expected

growth in the resources sector.

• 71 companies approached

• 32 companies with qualifying projects (>$300m spend)

Information collected on 66 projects with specific details of:

1. electricity demand

2. water demand

3. labour requirements (construction and operation)

4. capital spend and output

Total capital expenditure of $142b by 2020 if all projects proceed – which of course

was never going to happen

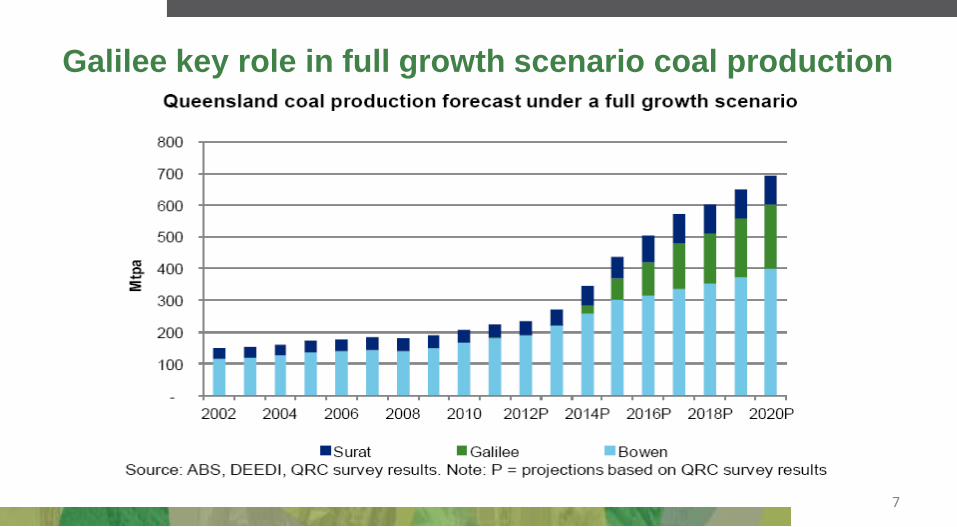

Galilee advanced coal projects*

GVK Alpha Project $6.4 billion Kevin’s Corner $4.2 billion Adani Carmichael $7.1 billion Bandanna South Galilee $4.2 billion Waratah China First $8.1 billion * China Stone – Terms of Reference out for consultation Source: Coordinator-General, Queensland Government November 2011

Galilee key role in full growth scenario coal production

7

New Qld resource projects – Nov 2011

Qld resource projects balance sheet

November 2012

DEBIT

Norwich Park, Gregory open cut coking coal

mines closed

Shutdown of Blair Athol accelerated

Peak Downs expansion shelved, Red Hill and

Saraji East planning halted

Ensham accelerating open cut wind-down

Several coal company project teams

disbanded or wound back

CREDIT

Caval Ridge & Daunia (BHPB) coking open-

cuts ($4.2b + $1.6b)

Vale‟s Eagle Downs underground coking coal

($1.25b)

GVK-Hancock‟s approvals in for Alpha mine,

rail and port - but go-ahead deferred ($10b)

Grosvenor coal mine (Anglo-American) board

approval ($US1.7b)

$45b CSG-LNG industry contracted and

delivering 2014-15

Incremental expansions by Xstrata Copper,

Xstrata Zinc

Uranium mining go-ahead - projects at least 4

years off

To be advised

Arrow Energy LNG project – decision late 2013

Xstrata Coal Wandoan project – decision due end-2012?

Adani Carmichael project in Galilee Basin – EIS soon?

Other Galilee projects progressing through EIS process

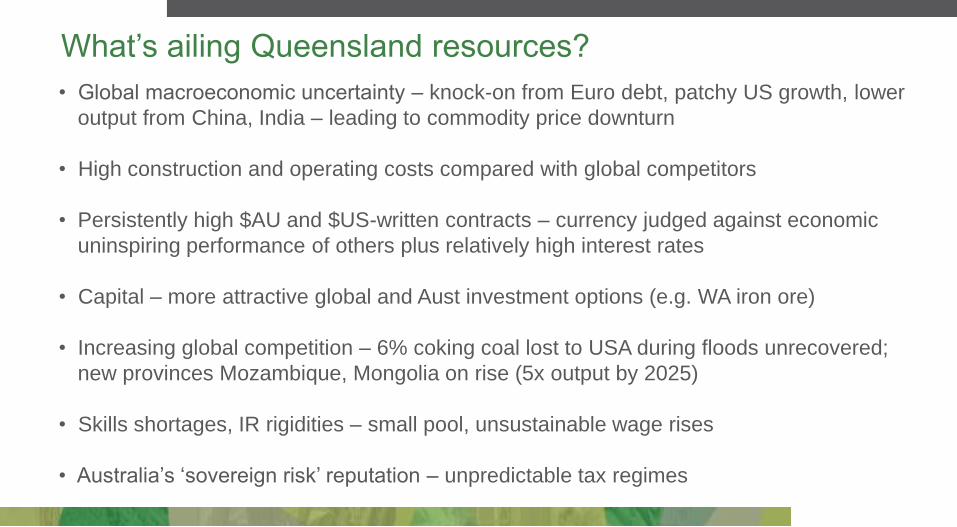

What‟s ailing Queensland resources?

• Global macroeconomic uncertainty – knock-on from Euro debt, patchy US growth, lower

output from China, India – leading to commodity price downturn

• High construction and operating costs compared with global competitors

• Persistently high $AU and $US-written contracts – currency judged against economic

uninspiring performance of others plus relatively high interest rates

• Capital – more attractive global and Aust investment options (e.g. WA iron ore)

• Increasing global competition – 6% coking coal lost to USA during floods unrecovered;

new provinces Mozambique, Mongolia on rise (5x output by 2025)

• Skills shortages, IR rigidities – small pool, unsustainable wage rises

• Australia‟s „sovereign risk‟ reputation – unpredictable tax regimes

Current Qld coal mines uncompetitive

Source: Port

Jackson Partners

(2012), Regaining

our competitive edge

in minerals

resources. Minerals

Council of Australia

– Minerals Week

presentation, 30 May

2012

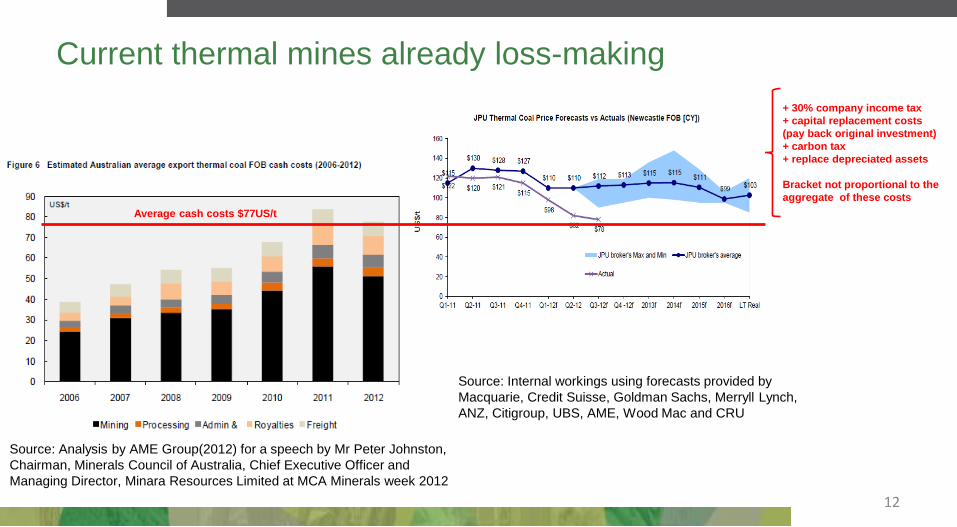

Current thermal mines already loss-making

12

Source: Analysis by AME Group(2012) for a speech by Mr Peter Johnston,

Chairman, Minerals Council of Australia, Chief Executive Officer and

Managing Director, Minara Resources Limited at MCA Minerals week 2012

Source: Internal workings using forecasts provided by

Macquarie, Credit Suisse, Goldman Sachs, Merryll Lynch,

ANZ, Citigroup, UBS, AME, Wood Mac and CRU

+ 30% company income tax

+ capital replacement costs

(pay back original investment)

+ carbon tax

+ replace depreciated assets

Bracket not proportional to the

aggregate of these costs

Average cash costs $77US/t

Source: Internal workings using forecasts provided by

Macquarie, Credit Suisse, Goldman Sachs, Merrill Lynch,

ANZ, Citigroup, UBS, AME, Wood Mac and CRU

Current coking mines becoming marginal

+ 30% company income tax

+ capital replacement costs

(pay back original investment)

+ carbon tax

+ replace depreciated assets

Bracket not necessarily

proportional to the aggregate

of these costs

Source: Analysis by AME Group(2012) for a speech by Mr Peter Johnston,

Chairman, Minerals Council of Australia, Chief Executive Officer and

Managing Director, Minara Resources Limited at MCA Minerals week 2012

Note - These are premium brand

hard coking prices. Average

prices for semi-hard and

semi-soft brands can be

$20-$40/t less in value

2012 level of cash costs US$107/t

New resource development projects in Qld costly

Source: Port Jackson Partners

(2012), Regaining our

competitive edge in minerals

resources. Minerals Council of

Australia – Minerals Week

presentation, 30 May 2012

Queensland coal‟s high effective tax

rate

Lessons for Galilee Basin

Galilee projects must target first or second quartile costs to be successful

Regulatory complexity must give way to rational planning for growth

Examples – rushed, flawed strategic cropping land law, urban buffer zones, one-size-fits-

all land access rules, out-of-control conditioning of projects, including „wish-list‟ Social

Impact Management Plans (SIMPs)

Under previous govt: Projects conditioned in advance of formal government policies;

environmental, Coordinator-General approvals prescriptive, not risk/outcomes based

Regulatory risk faced by resource projects (but not other economic pillars) has been to

be assessed against regulations at time of decision, not the time of application.

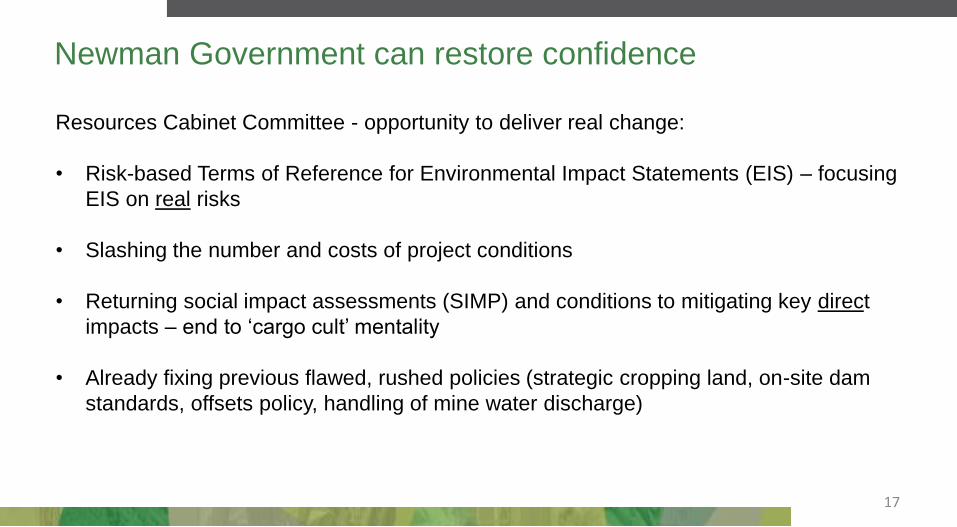

Newman Government can restore confidence

17

Resources Cabinet Committee - opportunity to deliver real change:

• Risk-based Terms of Reference for Environmental Impact Statements (EIS) – focusing

EIS on real risks

• Slashing the number and costs of project conditions

• Returning social impact assessments (SIMP) and conditions to mitigating key direct

impacts – end to „cargo cult‟ mentality

• Already fixing previous flawed, rushed policies (strategic cropping land, on-site dam

standards, offsets policy, handling of mine water discharge)

Industries under attack

> Greenpeace, Lock the Gate, The Australia

Institute et al behind concerted campaign

> Support sought from international foundations

and wealthy Australians

> Government-funded Environmental Defenders

Offices in NSW and Qld foundation contributors

> Objective: Shut down and closure of the coal

industry in the name of climate change

> Strategies: Colonise genuine community groups

and influence concerns, delay coal projects, then

undermine the social licence of the industry;

finally shaking confidence of investment

community to stop growth

Greenpeace targets Galilee Basin projects

> “Cooking the Climate, Wrecking the Reef”

(Sept 12) the latest Greenpeace anti-coal

salvo

> Claims Galilee projects will produce 330 mt

of coal and add to Australian carbon

emissions by 180% (by counting use of our

coal overseas)

> All up Greenpeace claims Queensland will

be exporting 1,056 mt of coal

NGOs exploiting Great Barrier Reef fears

20

• Key to anti-coal movement strategy led by environmental activists: raise spectre of

alarmist coal growth scenarios: coal „super highway‟, >1 billion tonnes of coal exports

by 2020, generating over 11,000 coal ship movements

• Generate community pressure on governments to delay/stop projects

• Industry working with Government in fighting back with comprehensive Cumulative

Impact Assessment, reef-wide shipping study and realistic industry growth and shipping

data. Working closely with state and federal Governments and UNESCO World

Heritage Committee on Strategic Assessments.

• State Ports Strategy: focus growth in existing port precincts

• Fact: took past 13 years to grow coal exports by 71 MT. Greenpeace says it can grow

> x6 in one decade. Federal forecasts says by 2020, coal exports may get to 300-320

MT (depending on what happens in Galilee Basin, Wandoan project)

Reef Wide Shipping impact

assessment (October 2012) Optimistic coal ship number is 4,200 or 37%

of Greenpeace number.

Shipping through reef highly regulated and

monitored.

Management of shipping impacts and risks

extremely well-managed and improving

Forecast ship numbers: minimal risk change

Can do more to ensure vetting quality of ships

and ship crews.

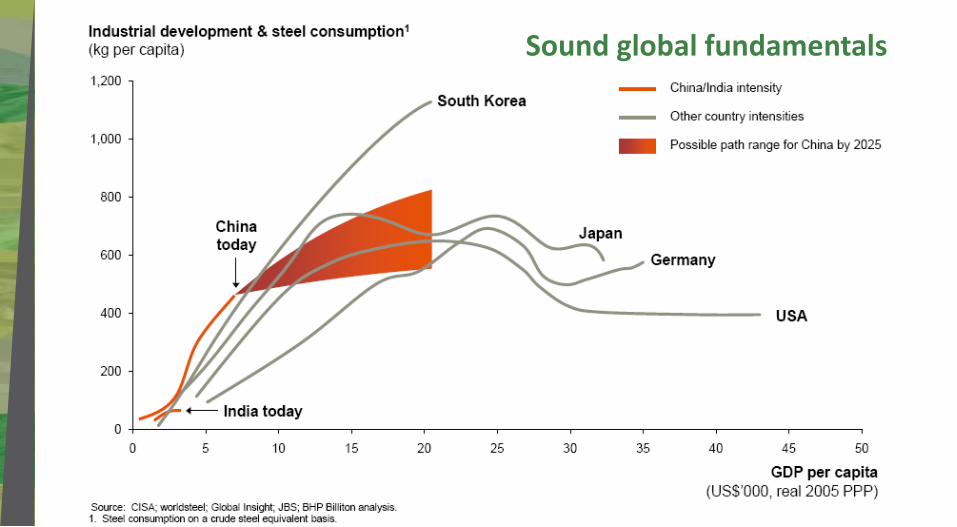

Asian Century – opportunity and challenge 4 billion people in continental Asia Striving to achieve in decades what took centuries for ‘West’ Asia needs energy, steel and metals.

Both new markets and new (cheaper) competitors in the region

Title Subtitle

Sound global fundamentals

Sound global fundamentals

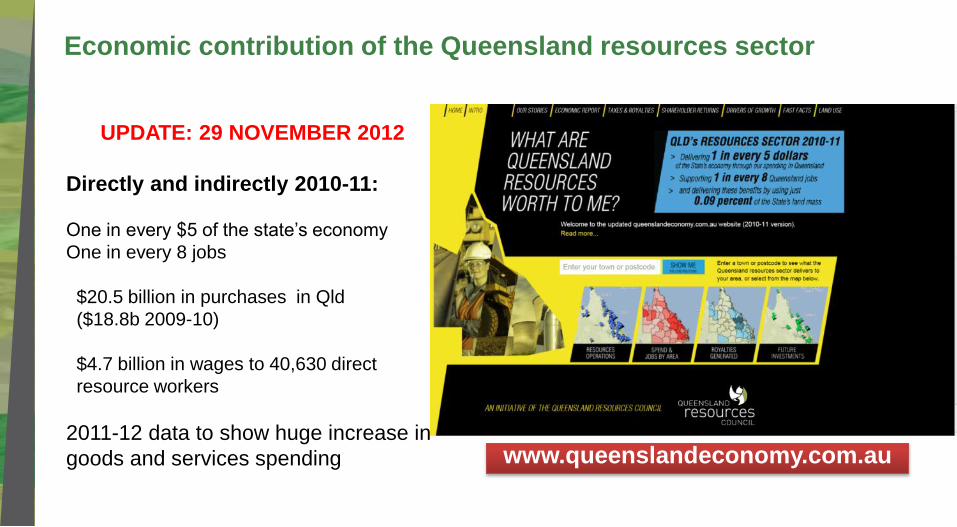

Economic contribution of the Queensland resources sector

www.queenslandeconomy.com.au

UPDATE: 29 NOVEMBER 2012

Directly and indirectly 2010-11:

One in every $5 of the state‟s economy

One in every 8 jobs

$20.5 billion in purchases in Qld

($18.8b 2009-10)

$4.7 billion in wages to 40,630 direct

resource workers

2011-12 data to show huge increase in

goods and services spending

Michael Roche

Chief Executive

Queensland’s resources outlook

Galilee Basin Coal and Energy Conference Hilton Hotel, Brisbane 12 November 2012