Embed Size (px)

Citation preview

Nov 2011

2

Record crop in 10/11, but 11/12 will be smaller due to cyclical down-turn in Brazil

112.3

125.9

110.1

119.8

110.1

132.3

117.9

137.1

125.3

142.4

133.8

80

90

100

110

120

130

140

150

m. 6

0kg

bag

s

01/02 02/03 03/04 04/05 '05/06 '06/07 07/08 08/09 09/10 10/11 11/12

Crop year

Brazil-10/11 58.2 m. bags, 11/12 46.9 m. bags *- provisional

3

16

18

20

22

24

26

28

30

32

34

36

Jan-08 Apr-08 Jul-08 Oct-08 Jan-09 Apr-09 Jul-09 Oct-09 Jan-10 Apr-10 Jul-10 Oct-10 Jan-11 Apr-11 Jul-11 Oct-11

M g

ree

n b

ag

s

Green Arabicas Soluble Green Robustas

Brazil coffee exports remain at a high level

4

Colombian production is slowly recovering from disasters in 08/09 & 09/10

12.0 12.212.5

8.78.1 8.8

10.1

0

2

4

6

8

10

12

14

m. 6

0kg

bags

'05/06 '06/07 07/08 08/09 09/10 10/11 11/12*

Crop year

* Preliminary

5

Vietnam production remains at a high level, but is expected to fall in 10/11

0

2

4

6

8

10

12

14

16

18

20

22

M. b

ag

s

02/03 03/04 04/05 05/06 06/07 07/08 08/09 09/10 10/11*

* Preliminary.

6

Indonesia production is dipping due to excess rainfall during La Niña

7.07.7

10.0 9.89.1

6.2

0

2

4

6

8

10

12

m. 6

0kg

bags

'06/07 07/08 08/09 09/10 10/11 11/12*

Crop year

* Preliminary. Crop year start in April

7

80

90

100

110

120

130

140

150

160

170

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Mill

ion

60

kg

ba

gs

Total Demand

Demand is growing

Projection

1990-2000: 1.3% 2000-10: 2.1% 2010-20: 1.7%

8

40

45

50

55

60

65

70

75

80

85

90

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Mill

ion

60

kg

ba

gs

Developed Markets* Emerging Markets

Growth is coming from Emerging Markets

Projection

9

100

110

120

130

140

m. 6

0kg

bags

03/04 04/05 05/06 06/07 07/08 08/09 09/10 10/11 11/12

Coffee Year Production Consumption (Oct-Sep)

Production balanced with demand in last 2 coffee years, surplus develops at end of 11/12

10

-1%

0%

1%

2%

3%

4%

5%

6%

7%

SE Asia Brazil E.Europe

M. East N.America

Japan Other LatAmerica

W.Europe

World

2002-09 2010-20

Total Demand Growth by Regionpe

r ce

nt p

er a

nnum

11

Robusta Demand Growth by Region

-1%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

Brazil N. America SE Asia M. East E. Europe W. Europe Japan World

2002-09 2010-20

per

cen

t per

ann

um

12

Natural Demand Growth by Region

-1%

0%

1%

2%

3%

4%

5%

6%

Brazil N. America SE Asia M. East E. Europe W. Europe Japan World

2002-09 2010-20

per

cen

t per

ann

um

13

Robusta share tends to be higher in growing regions

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

O T H E R AS IA M ID D LE E AS T * E . E UR O P E B R AZ IL O T H E R AF R IC A T O T AL WO R LD W. E UR O P E JAP AN US A+C AN AD A

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

Share of Robusta (left) Forecast annual growth of coffee 2010-20 (right)

*- includes India & N. Africa

14

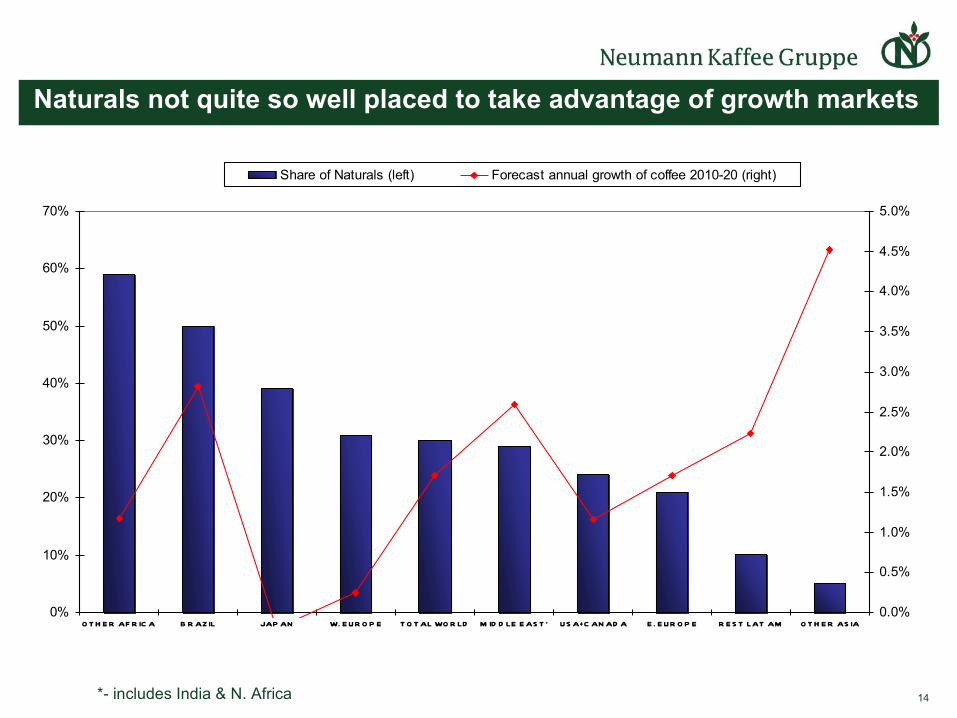

Naturals not quite so well placed to take advantage of growth markets

0%

10%

20%

30%

40%

50%

60%

70%

O T H E R AF R IC A B R AZ IL JAP AN W. E UR O P E T O T AL WO R LD M ID D LE E AS T * US A+C AN AD A E . E UR O P E R E S T LAT AM O T H E R AS IA

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

Share of Naturals (left) Forecast annual growth of coffee 2010-20 (right)

*- includes India & N. Africa

15

30

35

40

45

50

55

60

65

70

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Mill

ion

60

kg

ba

gs

Robusta Demand

Demand for robusta has also been strong

Projection

2000-10: 3.63% 2010-20: 2.3%

16

Increasing share of Robustas & Naturals in blend in importing countries

33% 32%28% 29% 29% 27% 28% 27% 28%

35%33%

34% 34% 35%34% 34% 37%

30%

0%

10%

20%

30%

40%

50%

60%

70%

2010 2009 2008 2007 2006 2005 2004 2003 2002

NATURALS ROBUSTAS

17

World Blend: Increasing use of Naturals in developed coffee markets of EU

28% 29%

32% 32% 32%33%

32%33% 34%

12%

14%15% 15%

17% 17%

24%25%

22%

10%

12%14%

16%

18%20%

22%24%

26%

28%30%

32%

34%36%

38%

2002 2003 2004 2005 2006 2007 2008 2009 2010

Robustas in EU15 Naturals in EU12

18

Arabica share tends to be higher in developed countries

0

10,000

20,000

30,000

40,000

50,000

60,000

Finland Australia USA Germany Japan S Korea Poland Russia China

GD

P p

er C

ap

ita

in c

urr

en

t US

$

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

GDP/Cap Share of Arabica

Shares based on green imports 2005-07

19

y = 0.2406Ln(x) - 1.8445

R2 = 0.7339

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0 10,000 20,000 30,000 40,000 50,000 60,000 70,000 80,000 90,000 100,000

GDP per capita in current US$

Sh

are

of

Ara

bic

a

The Changing Blend: As income increases the share of arabica increases.Finland

20

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2,400

2,600

00

0 b

ag

s

2003 2004 2005 2006 2007 2008 2009 2010 2011*

Sales of R.A. Coffee

Rainforest Alliance has highest sales growth

Average growth rate of 51% p.a since 2005

*- Projection

21

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

00

0 b

ag

s

2006 2007 2008 2009 2010*

Utz Certified Sales

Utz sales growth is averaging 39% per annum

*- Projection

22

-20-10

0102030405060708090

100

Jan-09

Mar-09

May-09

Jul-09

Sep-09

Nov-09

Jan-10

Mar-10

May-10

Jul-10

Sep-10

Nov-10

Jan-11

Mar-11

May-11

Jul-11

Sep-11

US ce

nts /

lb

Colombian Privates Honduras HG Costa Rica HB

Mild differentials have been almost as volatile as futures prices

Basis FOB Prompt Shipment

23

0

10

20

30

40

50

60

Jan-09

Mar-09

May-09

Jul-09

Sep-09

Nov-09

Jan-10

Mar-10

May-10

Jul-10

Sep-10

Nov-10

Jan-11

Mar-11

May-11

Jul-11

Sep-11

Nov-11

US ce

nts /

lb

Arb Honduras HG FOB diff minus Brazil FOB diff

And apparent loss of Brazil competitiveness

Basis FOB Prompt Shipment

24

ICE Stocks are at an extremely levels

0.0

1.0

2.0

3.0

4.0

5.0

6.0

J an-0 4

J ul -0 4

J an-0 5

J ul -0 5

J an-0 6

J ul-0 6

J an-0 7

J ul -0 7

J an-0 8

J ul -0 8

J an-0 9

J ul -0 9

J an-10

J ul -10

J an-11

J ul-11

m. b

ags

In EuropeIn the USA

To End Oct 2011

25

LIFFE Certified stocks have started to increase in 2011

0.00.51.01.52.02.53.03.54.04.55.05.56.06.57.0

D ec -0 7

M ar-0 8

J un-0 8

S ep -0 8

D ec -0 8

M ar-0 9

J un-0 9

S ep -0 9

D ec -0 9

M ar-10

J un-10

S ep -10

D ec -10

M ar-11

J un-11

S ep -11

m. b

ags

To End Oct 2011