Embed Size (px)

Citation preview

This document is offered compliments of BSP Media Group. www.bspmediagroup.com

All rights reserved.

Content Management for Digital Media Africa 2015 Conference

By: Monde Mbanga

PRESENTATION OUTLINE

� BROADCASTING SIGNAL DSTRIBUTION

� MODELLING CONVERGENCE

� ICT EVOLUTION AND INNOVATION

� TRIPLE PLAY

� TRIPLE PLAY INFRASTRUCTURE

� CLOUD COMPUTING TAXONOMY

� AFRICA: OVERVIEW

� UNIVERSAL ACCESS OBLIGATION

� THE ERA OF A KNOWLEDGE ECONOMY

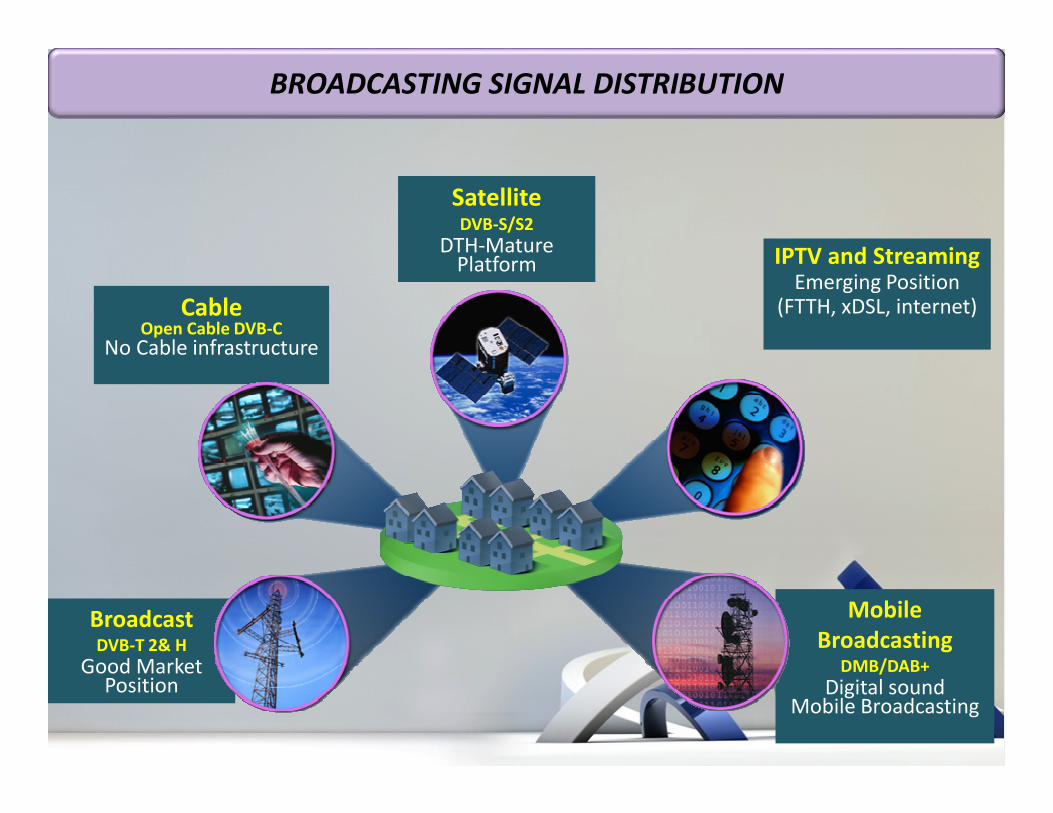

Mobile

BroadcastingDMB/DAB+

Digital soundMobile Broadcasting

IPTV and StreamingEmerging Position

(FTTH, xDSL, internet)CableOpen Cable DVB-C

No Cable infrastructure

SatelliteDVB-S/S2

DTH-Mature Platform

BroadcastDVB-T 2& H

Good Market Position

BROADCASTING SIGNAL DISTRIBUTION

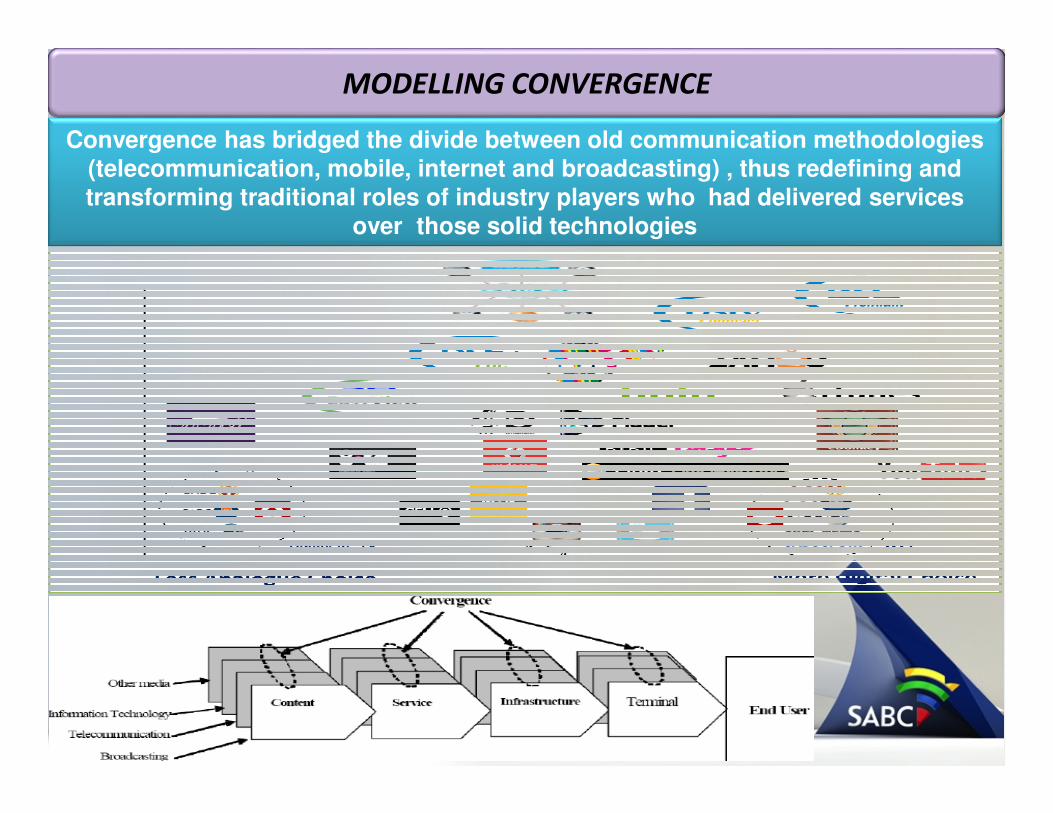

MODELLING CONVERGENCE

Convergence has bridged the divide between old communication methodologies (telecommunication, mobile, internet and broadcasting) , thus redefining and

transforming traditional roles of industry players who had delivered services over those solid technologies

5

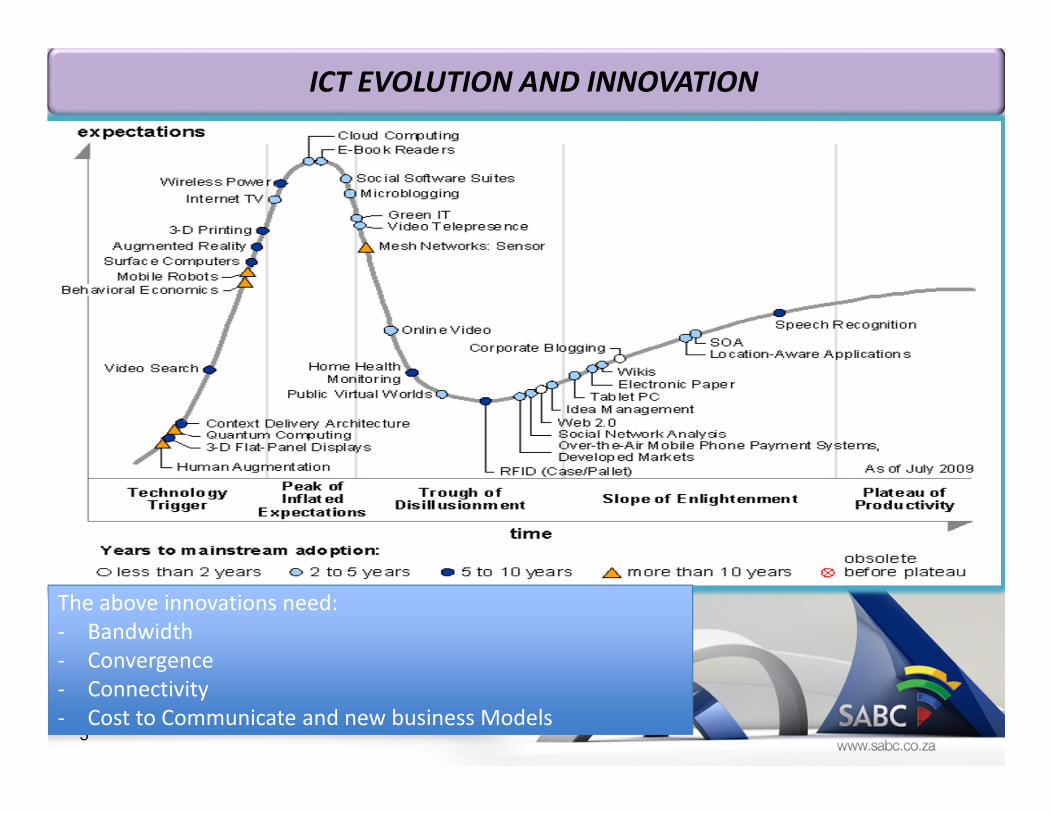

ICT EVOLUTION AND INNOVATION

The above innovations need:

- Bandwidth

- Convergence

- Connectivity

- Cost to Communicate and new business Models

6

E-Commerce/

Entertainment

Digital

Broadcasting and

the IP Network

Community Security

Video Meetings

Video Dating

Family

Monitoring

Local Content

Games

eHealthcare

Community Services

Community Info

THE FUTURE: COMMON IP TRIPLE PLAY NETWORK BECOMES A

PLATFORM FOR CONTINUAL SERVICE CREATION

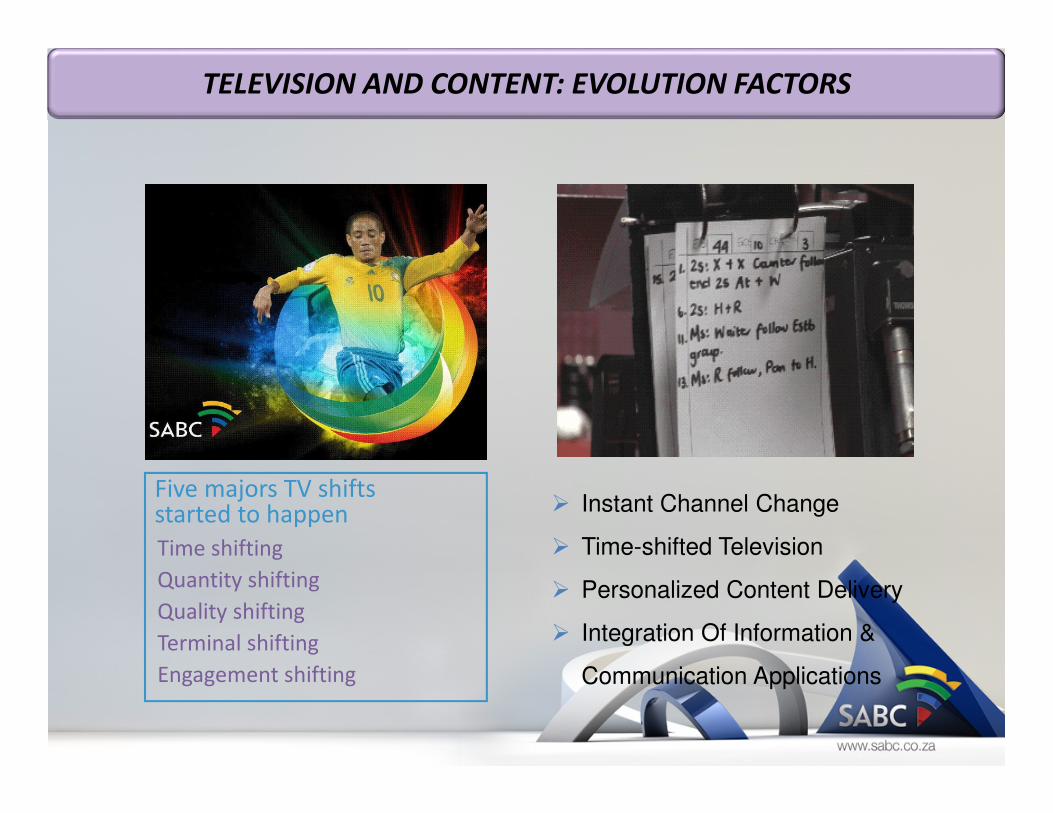

� Instant Channel Change

� Time-shifted Television

� Personalized Content Delivery

� Integration Of Information &

Communication Applications

Five majors TV shiftsstarted to happen

Time shifting

Quantity shifting

Quality shifting

Terminal shifting

Engagement shifting

TELEVISION AND CONTENT: EVOLUTION FACTORS

Increasing Innovation

Incr

ea

sin

g D

iffe

ren

tia

tio

n &

In

teg

rati

on

Mobile Office Voice

CMM and WPABX

Reachability-based

Communication

Voice/Video

Conferencing

IPTVInternet

Hybrid Phone

VoIP

CommercialBundles

EnhancedServices

BlendedServices

My Own TV,

Amigo TV

Classic Triple Play

POTS

The Challenge Is To Navigate This Trend While Optimizing Total Cost Of Ownership

Personalized

and Blended Services

Conversational

Services over TV

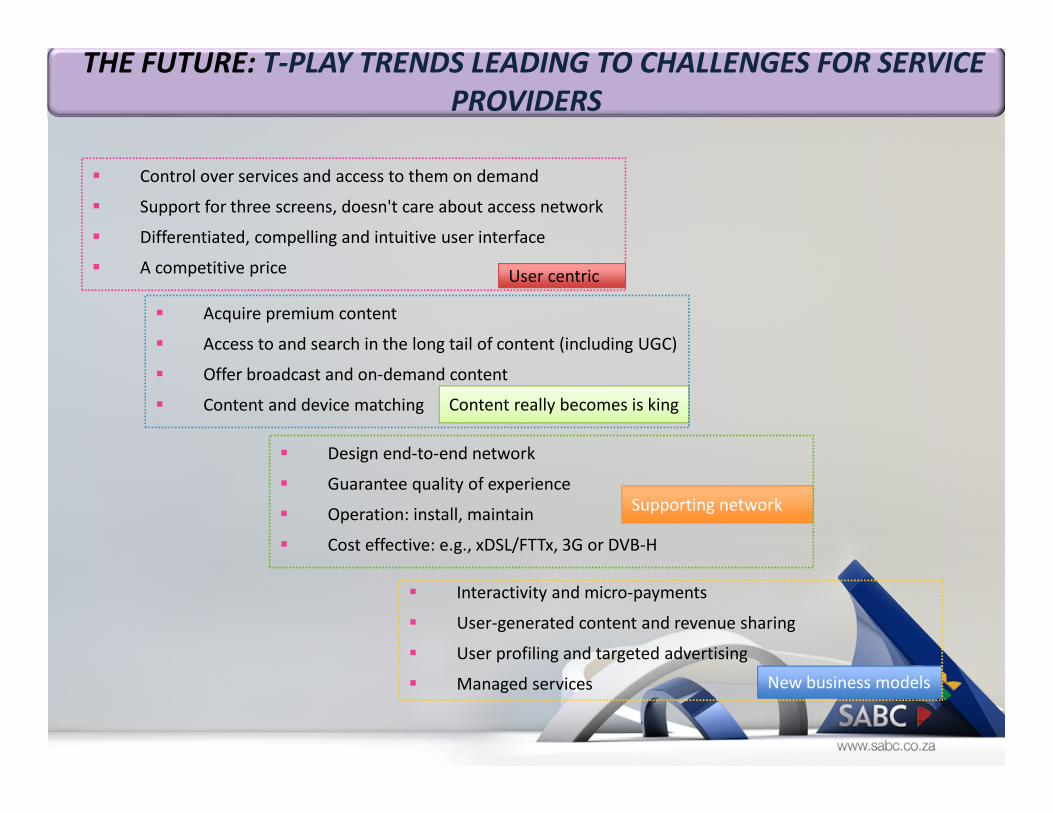

THE FUTURE: INNOVATION DRIVES DIFFERENTIATION

� Control over services and access to them on demand

� Support for three screens, doesn't care about access network

� Differentiated, compelling and intuitive user interface

� A competitive priceUser centric

Content really becomes is king

Supporting network

New business models

� Acquire premium content

� Access to and search in the long tail of content (including UGC)

� Offer broadcast and on-demand content

� Content and device matching

� Design end-to-end network

� Guarantee quality of experience

� Operation: install, maintain

� Cost effective: e.g., xDSL/FTTx, 3G or DVB-H

� Interactivity and micro-payments

� User-generated content and revenue sharing

� User profiling and targeted advertising

� Managed services

THE FUTURE: T-PLAY TRENDS LEADING TO CHALLENGES FOR SERVICE

PROVIDERS

10

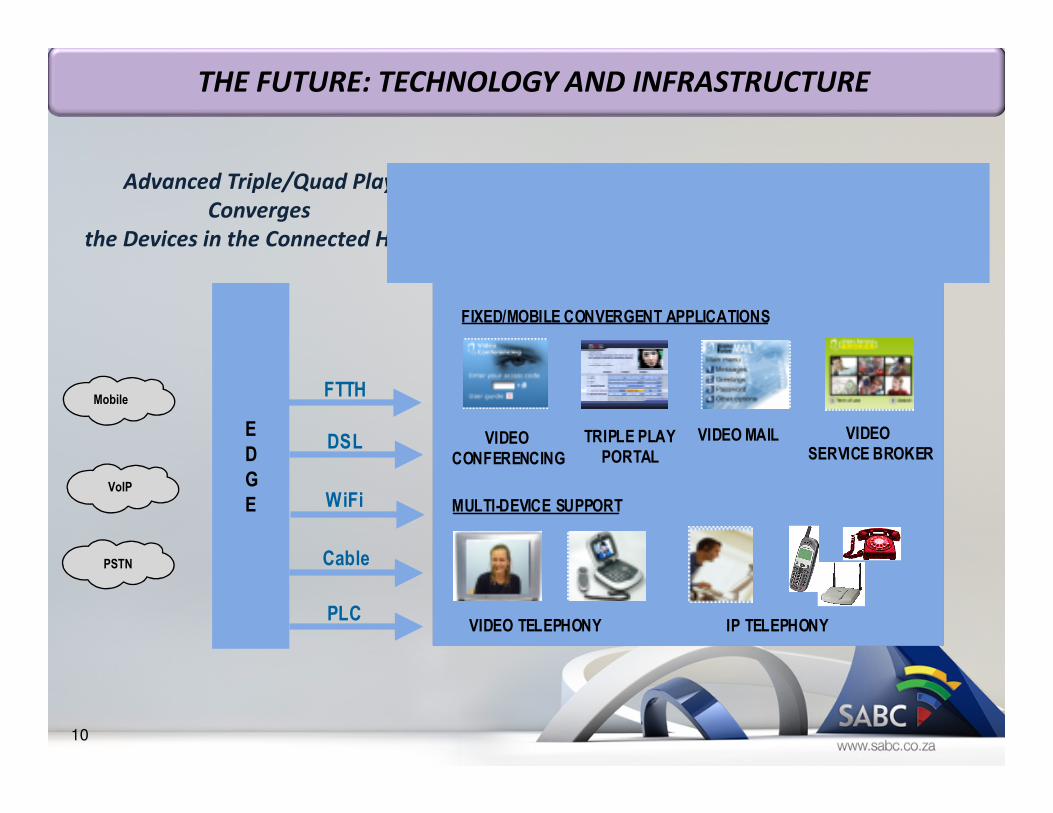

Advanced Triple/Quad Play

Converges

the Devices in the Connected Home

Mobile

VoIP

PSTN

E

D

G

E

VIDEO TELEPHONY IP TELEPHONY

VIDEO MAILTRIPLE PLAY

PORTAL

VIDEO

CONFERENCINGDSL

WiFi

Cable

PLC

FIXED/MOBILE CONVERGENT APPLICATIONS

MULTI-DEVICE SUPPORT

FTTH

VIDEO

SERVICE BROKER

THE FUTURE: TECHNOLOGY AND INFRASTRUCTURE

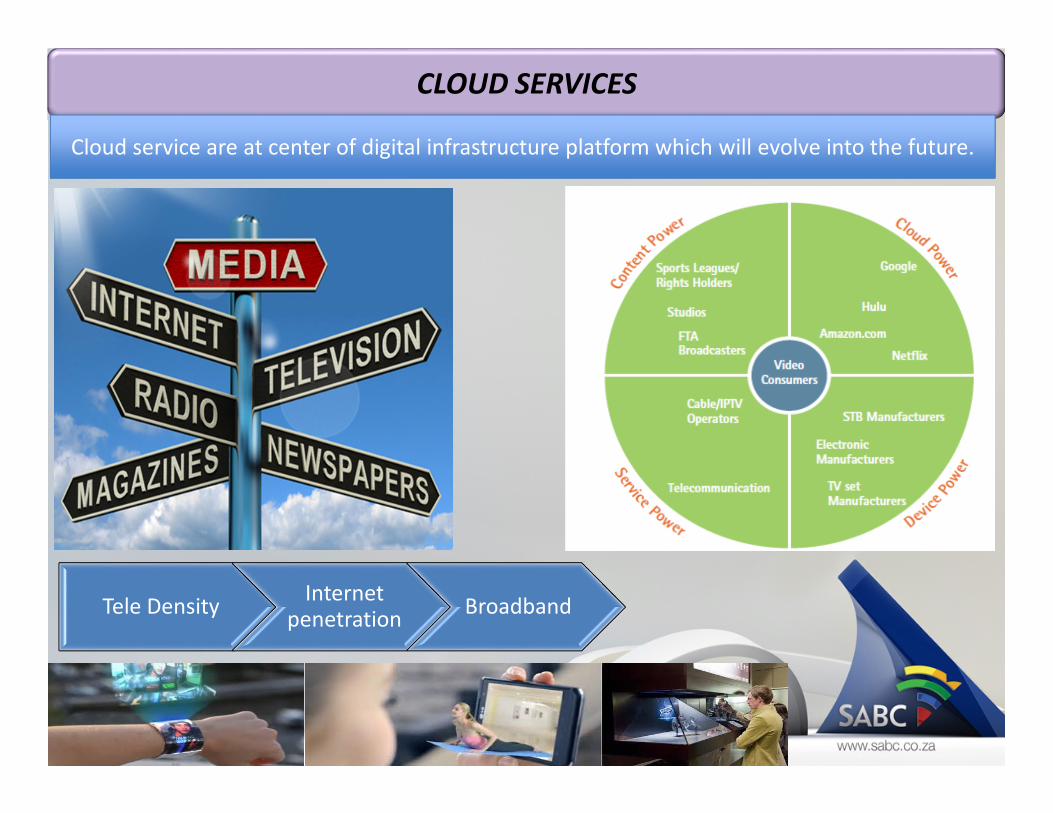

CLOUD SERVICES

Tele DensityInternet

penetrationBroadband

Cloud service are at center of digital infrastructure platform which will evolve into the future.

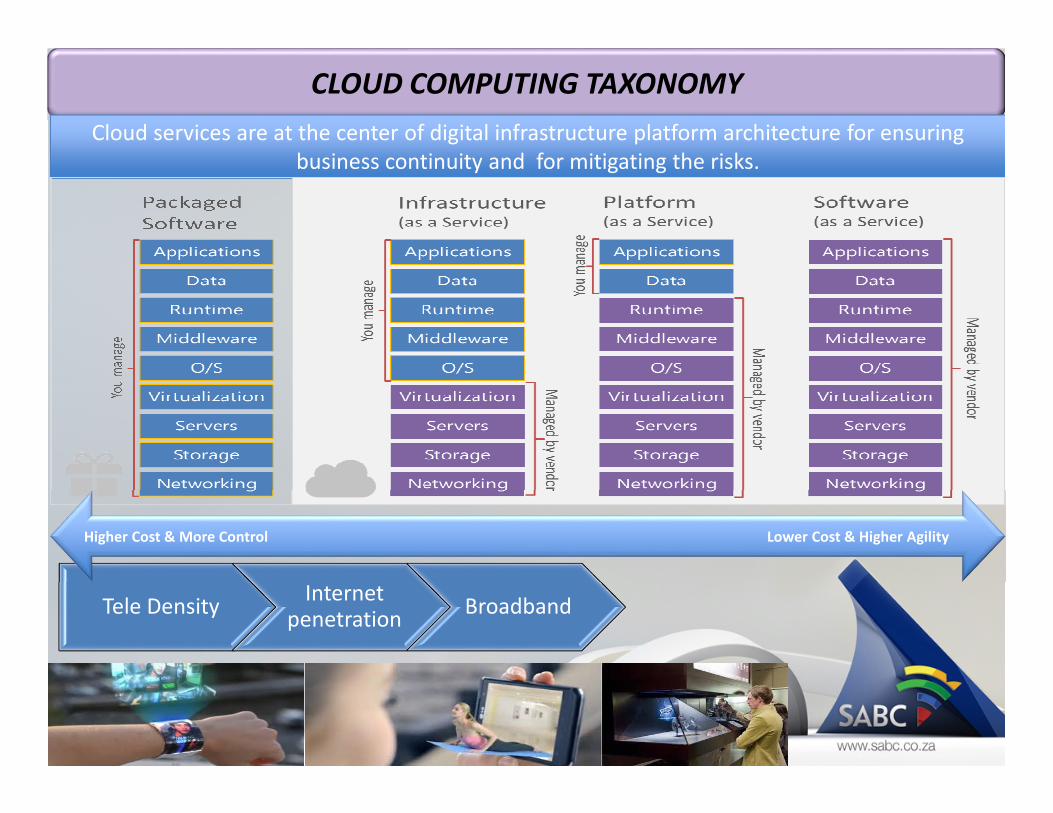

CLOUD COMPUTING TAXONOMY

Tele DensityInternet

penetrationBroadband

Cloud services are at the center of digital infrastructure platform architecture for ensuring

business continuity and for mitigating the risks.

Higher Cost & More Control Lower Cost & Higher Agility

New possibilities:

Interactivity

Parallel Broadcasting

Radio, TV, Data in one platform

Content , Anytime, Anywhere, Any platform, Any device!!! –Lower the cost to communicate

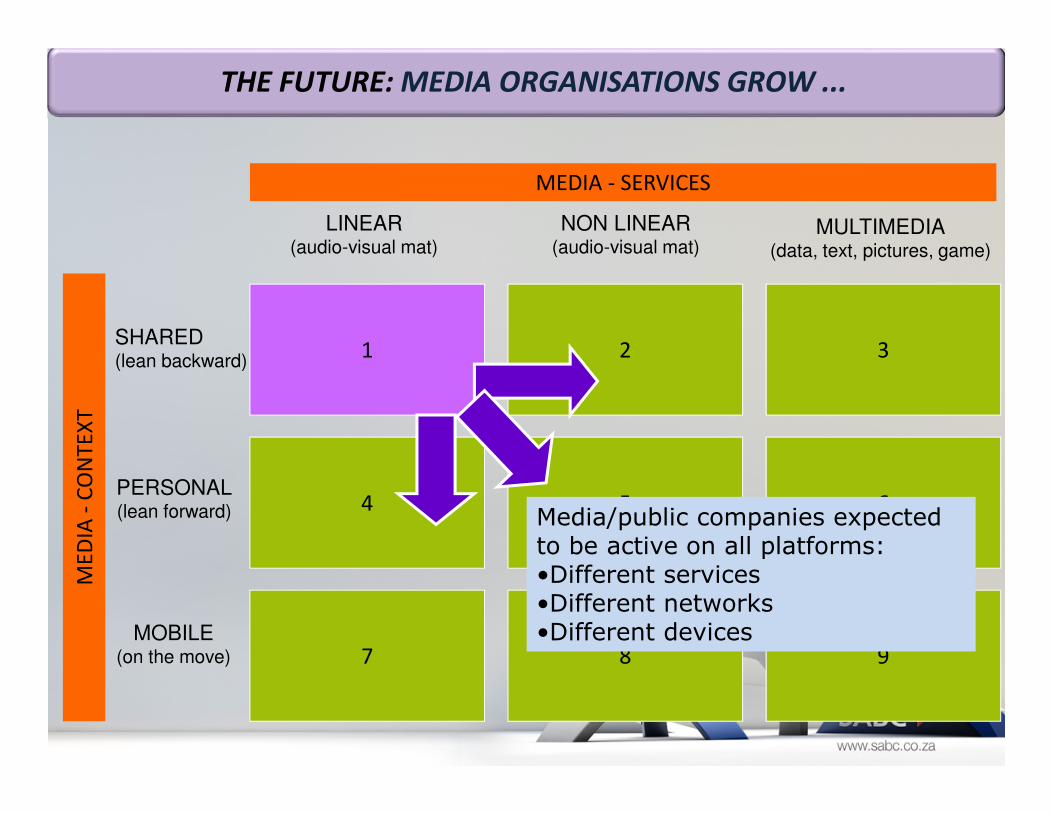

CONTENT DELIVERY PLATFORMS

1 2 3

4 5 6

7 8 9

LINEAR(audio-visual mat)

NON LINEAR(audio-visual mat)

MULTIMEDIA(data, text, pictures, game)

MEDIA - SERVICES

ME

DIA

-C

ON

TE

XT

SHARED(lean backward)

PERSONAL(lean forward)

MOBILE(on the move)

Media/public companies expected to be active on all platforms:•Different services•Different networks•Different devices

THE FUTURE: MEDIA ORGANISATIONS GROW ...

Poor infrastructure and slow pace of development Lower Cost & Higher Agility

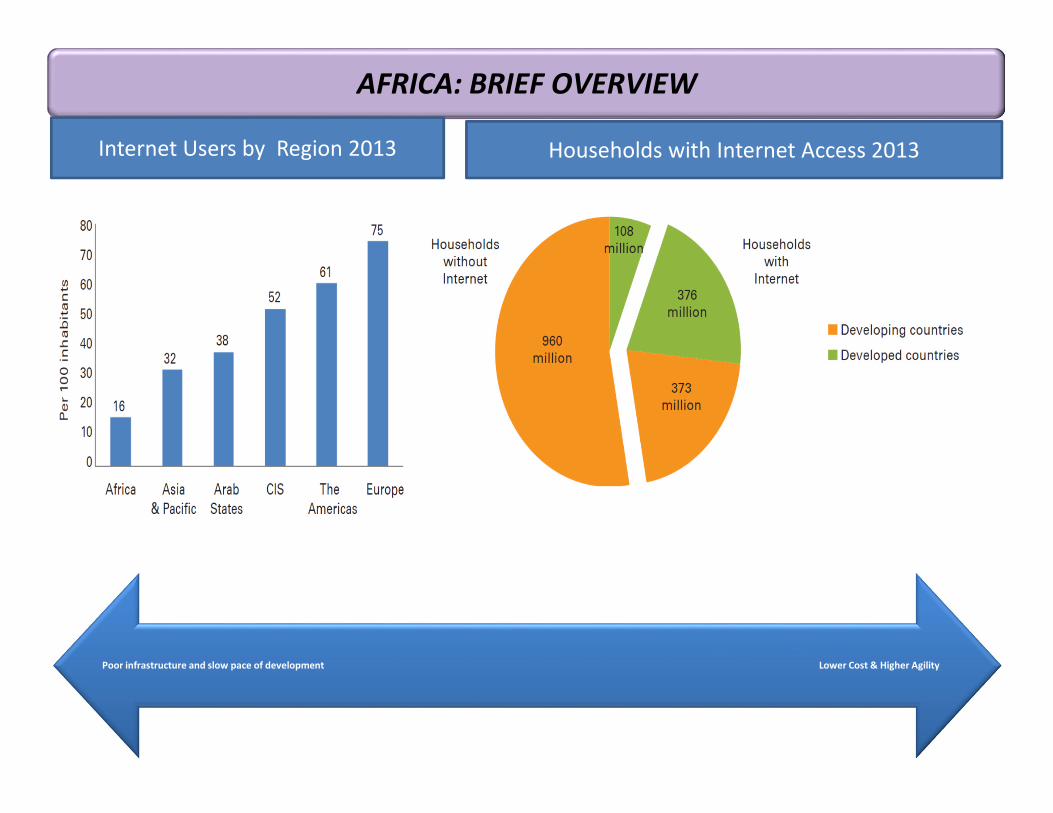

AFRICA: BRIEF OVERVIEW

Internet Users by Region 2013 Households with Internet Access 2013

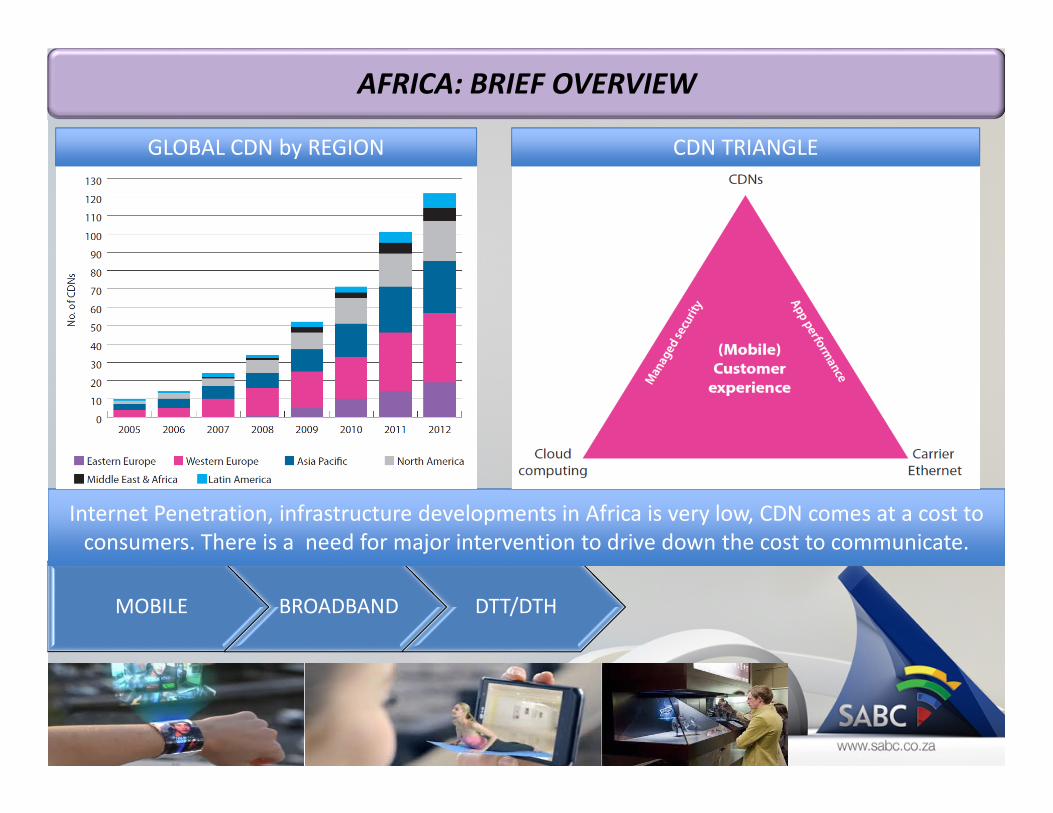

AFRICA: BRIEF OVERVIEW

MOBILE BROADBAND DTT/DTH

Internet Penetration, infrastructure developments in Africa is very low, CDN comes at a cost to

consumers. There is a need for major intervention to drive down the cost to communicate.

GLOBAL CDN by REGION CDN TRIANGLE

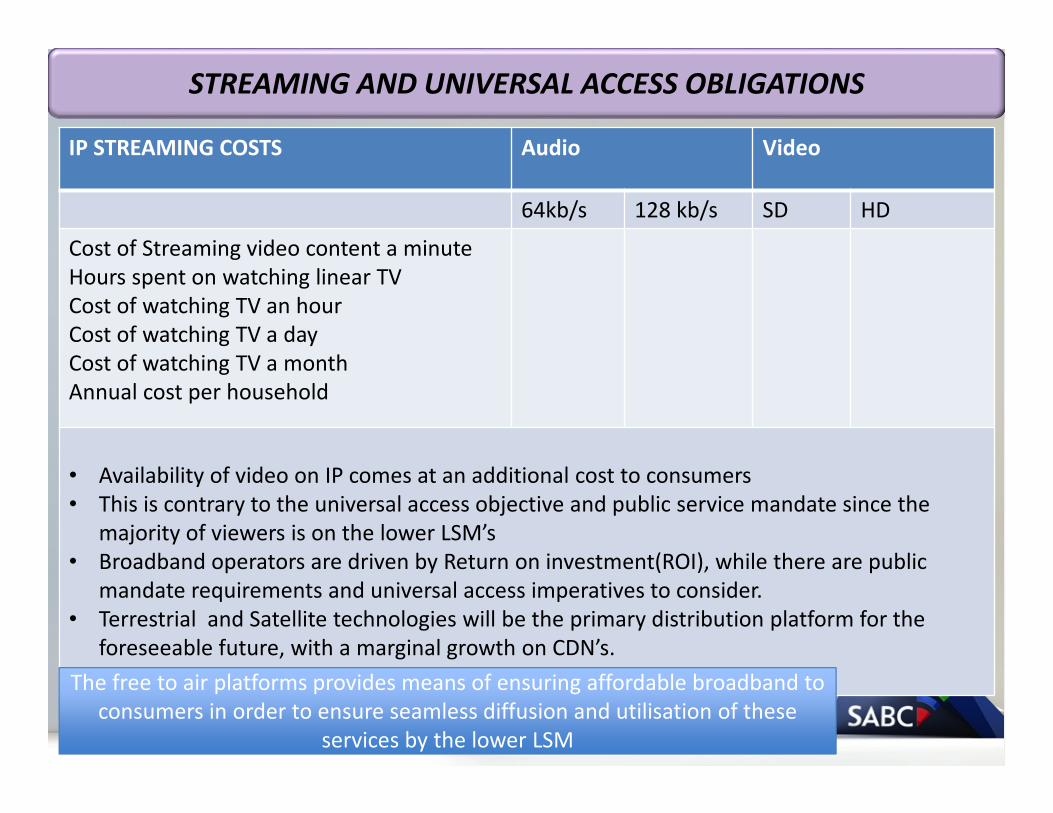

IP PLATFORMIP STREAMING COSTS Audio Video

64kb/s 128 kb/s SD HD

Cost of Streaming video content a minute

Hours spent on watching linear TV

Cost of watching TV an hour

Cost of watching TV a day

Cost of watching TV a month

Annual cost per household

• Availability of video on IP comes at an additional cost to consumers

• This is contrary to the universal access objective and public service mandate since the

majority of viewers is on the lower LSM’s

• Broadband operators are driven by Return on investment(ROI), while there are public

mandate requirements and universal access imperatives to consider.

• Terrestrial and Satellite technologies will be the primary distribution platform for the

foreseeable future, with a marginal growth on CDN’s.

STREAMING AND UNIVERSAL ACCESS OBLIGATIONS

The free to air platforms provides means of ensuring affordable broadband to The free to air platforms provides means of ensuring affordable broadband to

consumers in order to ensure seamless diffusion and utilisation of these

services by the lower LSM

Rich

Multimedia

Seamless

Experience

Common Service Delivery

Platform Supports Rich

Media Services:

Video on demand,

Personal TV,

Online gaming,

Sharing of music, photos

and home videos

Offers Highly Differentiated User Experience:Provides a personalized and interactive service mix that integrates seamlessly with end user’s communications, information and entertainment needsEnriches lives of end users

Subscriber

Control

Personalization

Interactivity Accessibility

Delivers Next Generation User-centric Services:

IPTV, residential VoIP and other converged multimedia applications

Provides a better triple play experience

THE FUTURE: BENEFITS FOR THE END USER AND THE SERVICE

PROVIDER: THE WIN-WIN DEAL

Recommendations

19

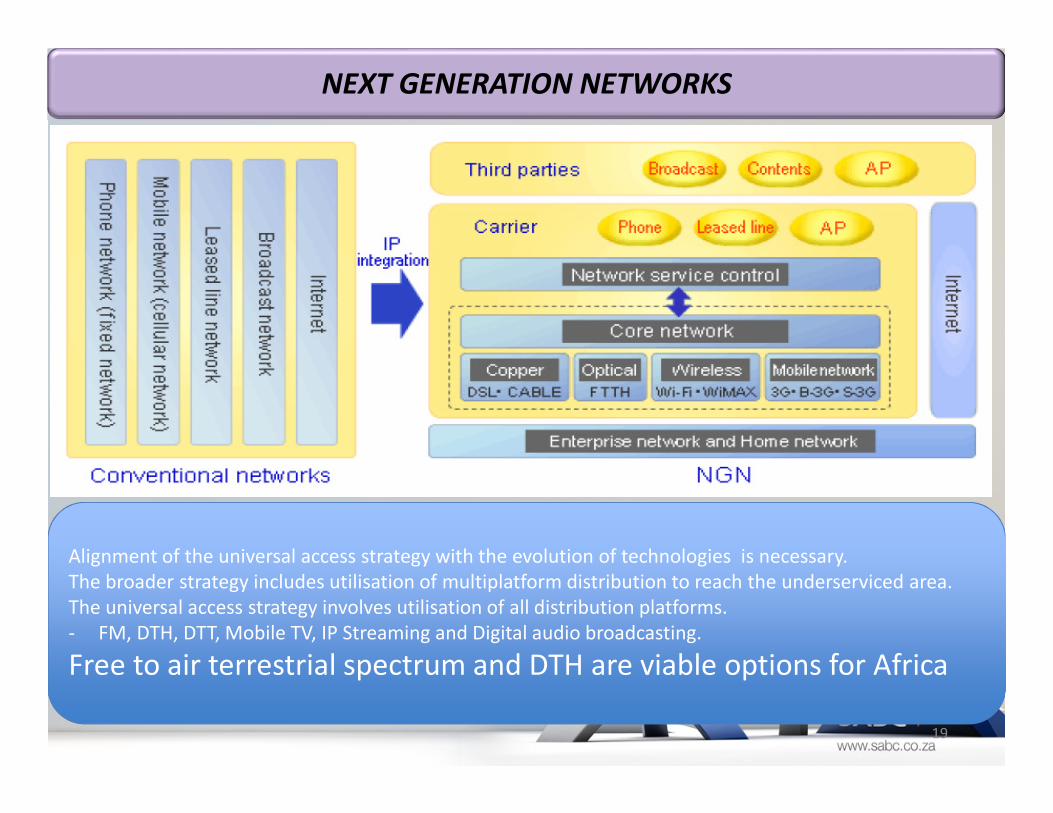

NEXT GENERATION NETWORKS

Alignment of the universal access strategy with the evolution of technologies is necessary.

The broader strategy includes utilisation of multiplatform distribution to reach the underserviced area.

The universal access strategy involves utilisation of all distribution platforms.

- FM, DTH, DTT, Mobile TV, IP Streaming and Digital audio broadcasting.

Free to air terrestrial spectrum and DTH are viable options for Africa

THE ERA OF A KNOWLEDGE ECONOMY

• Research links broadband to accelerated GDP growth.

• Opportunity to empower the citizens through knowledge thereby;

• Alleviation of socio economic challenges through ICT.

• Digital technology heralds the era of convergence and proliferation of media.

� Effectively Restructuring the composition of the GDP

� The national labour profile with an increase in demand for skilled labour.

� Developed arts and culture sector for export

� Engineering and production skills.

� Manufacturing industry.

� Plethora of educational and self skilling opportunities.

Policy and Regulatory paradigm shift/New Models

• Convergence

• ICT Integration

• Universal access and Public Mandate consideration[Costs to PBS

and consumer]

• Competition- eliminate anti competitive practices and barrier to

entry to ensure fully converged digital ecosystem.

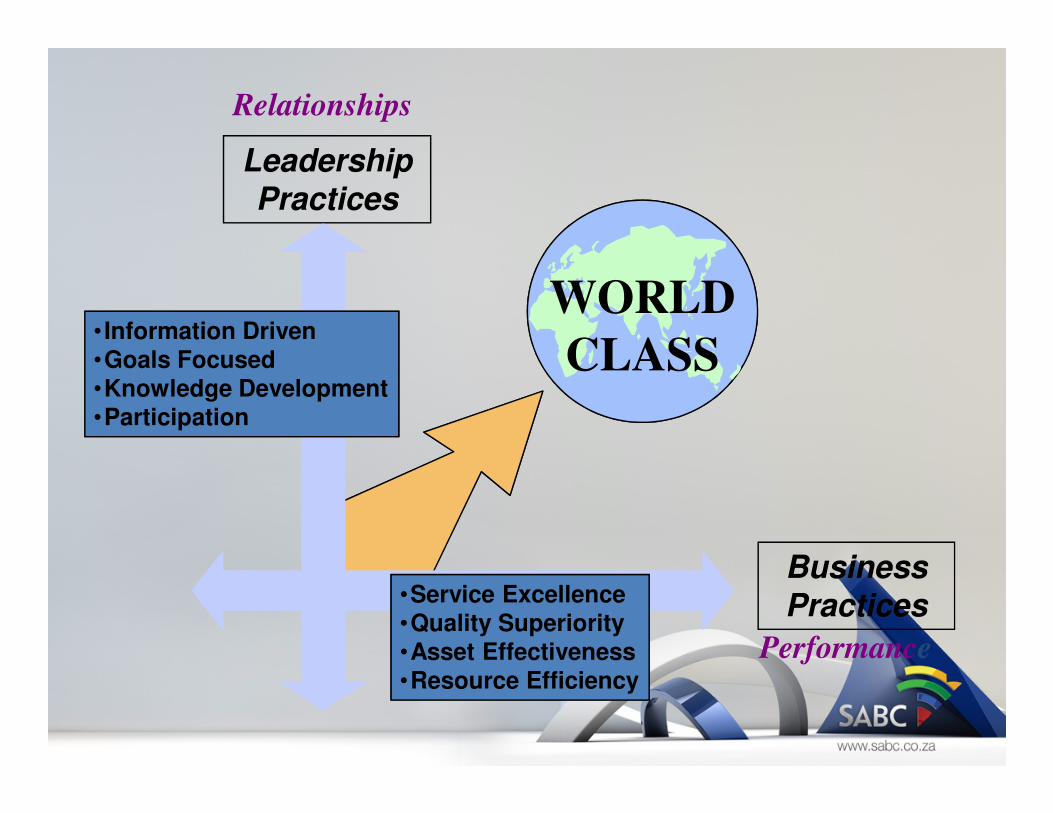

Leadership

Practices

Business

Practices

WORLD

CLASS

Relationships

Performance

• Information Driven

•Goals Focused

•Knowledge Development

•Participation

•Service Excellence

•Quality Superiority•Asset Effectiveness•Resource Efficiency