Embed Size (px)

Citation preview

Venture Capital in Europe & IsraelVenture Investment Data: First Quarter 2017

Prepared by Gil Dibner

Berlin, view along the Spree River towards the Bode Museum (opened as the Kaiser-Friedrich-Museum in 1904) and the Fernsehturm television tower (368M, completed in 1969). blog

The data• The data in this report consists entirely of data I’ve gathered manually based on

publicly available, free sources• No paid data sources or API calls were harmed in the making of this dataset, every

investment was manually classified• This allows analysis of some aspects of the data I consider important – aspects that

don’t appear in other data sources. More importantly, it allows me to exclude deals that are really not “venture capital” rounds but tend to get included by others

• Seed investment is under-reported and adds a lot of noise to the data set, so I exclude deals under $500K

• The analysis is limited to ICT categories and excludes life sciences• The analysis excludes Turkey and FSU countries• All currencies converted into USD using monthly average exchange rates

Prepared by Gil Dibner follow me on (@gdibner), connect with me on , subscribe to my , or invest with me onblog 2

Top 10 deals by region in Q1 2017 (US $M)

France & Benelux IsraelIberia

UK & Ireland DACH Nordic

Prepared by Gil Dibner follow me on (@gdibner), connect with me on , subscribe to my , or invest with me onblog 3

15

15

21

24

25

25

26

28

53

100

104

Garrison Technology

Ecrebo

CompareEuropeGroup

Monzo

Evrythng

CurrencyCloud

Upstream

Whistle Sports

Arralis

Funding Circle

Atom Bank

0 50 100 150

16

18

20

22

32

32

53

70

127

165

Ottonova

WayRay

Knime

Book a Tiger

SolarisBank

Raisin

ResearchGate

SoundCloud

Lampenwelt.de

Tricentis

0 50 100 150 200

12

12

12

15

16

17

17

22

26

50

63

Fuse

Qapital

Xeneta

NA-KD

Skeleton Technologies

Pipedrive

Starship Technologies

Soundtrack Your Brand

24 Storage

Collibra

iZettle

0 20 40 60 80

2222234556

1112

175

ApartumMr. Jeff

Subasta de OcioGamelearnRocketROI21 Buttons

HundredroomsRavenPack

FeverOdilo

LogtrustScytl

LetGo

0 50 100 150 200

16

20

23

27

30

35

35

61

69

105

Databerries

Qwant

Bloomon

Doctolib

Bitfury

Guest2Guest

JobToday

Vestiaire…

Oodrive

Picnic

0 20 40 60 80 100 120

2020202020

232525

3030

4056

7075

HealthwatchDemisto

SamanageFeedvisor

VATboxReduxio

ValensFreightOSExabeamAutotalks

Transmit SecurityAppsflyer

SentinelOneKaminario

0 20 40 60 80

Top 10 deals by type in Q1 2017 (US $M)

Systems SaaSEnterprise

Consumer Financial Commerce

Prepared by Gil Dibner follow me on (@gdibner), connect with me on , subscribe to my , or invest with me onblog 4

26

27

28

35

61

70

104

105

127

175

24 Storage

Doctolib

Whistle Sports

Guest2Guest

Vestiaire Collective

SoundCloud

Atom Bank

Picnic

Lampenwelt.de

LetGo

0 50 100 150 200

32

35

40

50

53

56

69

70

75

165

Raisin

JobToday

Transmit Security

Collibra

ResearchGate

Appsflyer

Oodrive

SentinelOne

Kaminario

Tricentis

0 50 100 150 200

14

20

22

24

25

30

32

32

100

104

Earnix

VATbox

Creamfinance

Monzo

CurrencyCloud

Bitfury

SolarisBank

Raisin

Funding Circle

Atom Bank

0 20 40 60 80 100 120

10

12

13

15

16

17

20

53

63

75

Arktis

Famoco

Usound

EasyMile

Skeleton Technologies

Starship Technologies

Healthwatch

Arralis

iZettle

Kaminario

0 20 40 60 80

8

9

11

11

15

21

23

61

105

127

Blue Bay Travel

Restoflash

Campanda

Mycs

NA-KD

CompareEuropeGroup

Bloomon

Vestiaire Collective

Picnic

Lampenwelt.de

0 50 100 150

20

20

20

22

25

25

26

35

50

69

165

Demisto

Knime

Samanage

Soundtrack Your Brand

Evrythng

CurrencyCloud

Upstream

JobToday

Collibra

Oodrive

Tricentis

0 50 100 150 200

Quarterly pace of venture investment

• In 1Q17, Europe & Israel saw $4.0 billion flowing into 521 venture transactions

• 1Q17 was a record-breaking quarter in terms of the number of venture deals

• 1Q17 was the second-highest quarter in terms of amount invested

• These numbers, and the rest of this deck, do not reflect the $1B in debt raised by Spotify in March

Prepared by Gil Dibner follow me on (@gdibner), connect with me on , subscribe to my , or invest with me onblog 52,873

3,139

3,252

2,857

3,730

4,114

3,122

3,522

4,018

0

100

200

300

400

500

600

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

Qtr1 Qtr2 Qtr3 Qtr4 Qtr1 Qtr2 Qtr3 Qtr4 Qtr1

2015 2016 2017

Amou

nt in

vest

ed (U

S $M

)

VC Investments in Europe & Israel

Invested amount (US $M) Number of investments

Monthly pace of venture investment

• Looked at on a monthly basis, the strong first quarter was driven by a strong January and March

• January was very strong, on par with the previous year –this likely reflects pent up activity from 4Q getting announced publicly in 1Q

• Monthly deal volume throughout the quarter was near the historical ceiling of approximately 180 deals per month across the geography

Prepared by Gil Dibner follow me on (@gdibner), connect with me on , subscribe to my , or invest with me onblog 6

905971997791787

1,5611,518

5711,1641,0841,059

7151,6571,0511,0211,4011,4521,261

7251,1011,2961,4571,170

8951,640

9441,434

0

20

40

60

80

100

120

140

160

180

200

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

Jan

Feb

Mar

Apr

May Jun Jul

Aug

Sep

Oct

Nov De

cJa

nFe

bM

arAp

rM

ay Jun Jul

Aug

Sep

Oct

Nov De

cJa

nFe

bM

ar

Qtr1 Qtr2 Qtr3 Qtr4 Qtr1 Qtr2 Qtr3 Qtr4 Qtr1

2015 2016 2017

Amou

nt in

vest

ed (U

S $M

)

VC Investments in Europe & Israel(January 2015 - March 2017)

Invested amount (US $M) Number of investments

Mega-rounds skew the investment totals• This analysis breaks down VC

investments into brackets by size:

• Seed (less than $2M)• Early venture ($2-8M)• Venture ($8-20M)• Growth ($20-100M)• Mega ($100M+)

• Six mega-rounds took place in Europe in 1Q17

• Letgo (Spain, $175M)• Tricentis (Austria, $165M)• Lampenwelt (Germany, $127M)• Picnic (Netherlands, $105M)• Atom Bank (IUK, $104M)• Funding Circle (UK, $100M)

• Adjusting for mega-rounds, 1Q17 was a record quarter at $3.24B, just edging out 2Q16 ($3.21B)

Prepared by Gil Dibner follow me on (@gdibner), connect with me on , subscribe to my , or invest with me onblog 7

510 602 635 592 709 751559

730 695 752 651911

1,187

1,650 1,6791,336 1,197

1,366

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

Qtr4 Qtr1 Qtr2 Qtr3 Qtr4 Qtr1

2015 2016 2017

Amou

nt In

vest

ed (U

S $M

)

Pace of VC Investment in Europe and Israel

Mega (>100) Growth (20-100) Venture (8-20) Early Venture (2-8) Seed (.5-2)

Strong year-over-year growth

• All size brackets except growth saw YoY increases in 1Q17 compared to 1Q16

• Seed deal volume increase by 21%, early venture and venture both increased by 25%, and mega-deal volume increased by 36%

• Growth venture volume decreased by 17%

Prepared by Gil Dibner follow me on (@gdibner), connect with me on , subscribe to my , or invest with me onblog 8

177 215

602 751

730911

1,6501,366

571776

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

Qtr1 Qtr1

2016 2017

Tota

l VC

inve

stm

ent (

US $

M)

VC investment volume in Europe and Israel by bracket(1Q17 vs 1Q16)

Mega (>100) Growth (20-100) Venture (8-20) Early Venture (2-8) Seed (<2)

Number of investments, by bracket

• Excluding seed deals, the total number of VC investments per quarter was 314 in 1Q17, a new record level since I started tracking this data

Prepared by Gil Dibner follow me on (@gdibner), connect with me on , subscribe to my , or invest with me onblog 9

77 85 94140 153 157 144

182 1934262 44

4661 57 64

5376

3326 38

35

44 5240

35

39

66 4

3

4 41

6

6

0

50

100

150

200

250

300

350

Qtr1 Qtr2 Qtr3 Qtr4 Qtr1 Qtr2 Qtr3 Qtr4 Qtr1

2015 2016 2017

Num

ber o

f VC

inve

stm

ents

VC investment volume in Europe and Israel by bracket

Mega (>100) Growth (20-100) Venture (8-20) Early Venture (2-8)

No impact of Brexit on deal volume, but…

• Looking just at UK VC deal volume, there’s so far no evidence that Brexit caused any slowdown whatsoever in VC activity

• There were an average of 15 VC deals per month in the 18 months before the referendum

• There were an average of 20 VC deals per month since the referendum

Prepared by Gil Dibner follow me on (@gdibner), connect with me on , subscribe to my , or invest with me onblog 10

0

5

10

15

20

25

30

35

Jan

Feb

Mar Ap

rM

ay Jun Jul

Aug

Sep

Oct

Nov De

cJa

nFe

bM

ar Apr

May Jun Jul

Aug

Sep

Oct

Nov De

cJa

nFe

bM

ar

Qtr1 Qtr2 Qtr3 Qtr4 Qtr1 Qtr2 Qtr3 Qtr4 Qtr1

2015 2016 2017

Num

ber o

f VC

inve

stm

ents

VC investment volume in the UK by bracket

Mega (>100) Growth (20-100) Venture (8-20) Early Venture (2-8)

Pre-Brexit

avg = 15

Post-Brexit avg = 20

Total invested capital per quarter is down since Brexit

• Looking just at total invested capital in the UK, there does appear to be an impact since the Brexit referendum

• An average of $819M per quarter was invested in the UK in the 18 months before the referendum

• An average of $648M per quarter was invested in the UK since the referendum

• VC investment volume in the UK is down 21% per quarter since the Brexit referendum

Prepared by Gil Dibner follow me on (@gdibner), connect with me on , subscribe to my , or invest with me onblog 11

74 70 98 79 136 108 133 150 188165 166 96 128

172148

181 113160

459

180405

209

532

273 202191

149

210

150

275478

192

110275

204

0

200

400

600

800

1,000

1,200

Qtr1 Qtr2 Qtr3 Qtr4 Qtr1 Qtr2 Qtr3 Qtr4 Qtr1

2015 2016 2017

Num

ber o

f VC

inve

stm

ents

VC investment volume in the UK by bracket

Mega (>100) Growth (20-100) Venture (8-20) Early Venture (2-8)

Pre-Brexit avg = $819M

Post-Brexit avg = $648M

Corporate VC activity, by bracket

• Excluding seed deals, the total number of corporate VC investments rose to 54 in 1Q17 compared to 44 in 4Q16

• Corporate VC investments are trending towards later stage

Prepared by Gil Dibner follow me on (@gdibner), connect with me on , subscribe to my , or invest with me onblog 12

6 4 516

7

22 19 23 1927 24

43

9

12

7

12

6

1619 5

17

44

7

8

7

720

18

69

11

3

13

3

3

2

0

10

20

30

40

50

60

70

Qtr3 Qtr4 Qtr1 Qtr2 Qtr3 Qtr4 Qtr1 Qtr2 Qtr3 Qtr4 Qtr1

2014 2015 2016 2017

Num

ber o

f VC

inve

stm

ents

Corporate VC investment volume in Europe and Israel by bracket

Mega (>100) Growth (20-100) Venture (8-20) Early Venture (2-8)

Corporate VC activity, by country

• During 1Q17, Israel saw the highest number of corporate VC investments, with 18

• The UK saw 12 corporate VC investments during the quarter

• Germany and France took the third and fourth spots, with 7 and 4, respectively

• Corporate investors participated in two mega-rounds in the geography in the quarter

Prepared by Gil Dibner follow me on (@gdibner), connect with me on , subscribe to my , or invest with me onblog 13

85 4

2

5

43

2

5

2

2

0

2

4

6

8

10

12

14

16

18

20

Isra

el UK

Ger

man

y

Fran

ce

Net

herla

nds

Swed

en

Irela

nd

Pola

nd

Finl

and

Switz

erla

nd

Esto

nia

Italy

Num

ber o

f inv

estm

ents

Number of corporate VC investments in Europe and Israel by bracket(1Q17)

Mega (>100) Growth (20-100) Venture (8-20) Early Venture (2-8)

Average round size• This average excludes seed

rounds and mega rounds, so it reflects all rounds done in Europe & Israel between $2M and $100M

• With very few exceptions, most months saw average round sizes of $10-12M and there is seems to be little pattern other than mean reversion

• 3Q15 is the only systematic outlier to this trend, with average round sizes of $12-15M throughout the quarter

• As the six-month trailing average shows, average round sizes are drifting downward

Prepared by Gil Dibner follow me on (@gdibner), connect with me on , subscribe to my , or invest with me onblog 14

4

6

8

10

12

14

16

18

20

Jul

Aug

Sep

Oct

Nov De

cJa

nFe

bM

ar Apr

May Jun Jul

Aug

Sep

Oct

Nov De

cJa

nFe

bM

ar Apr

May Jun Jul

Aug

Sep

Oct

Nov De

cJa

nFe

bM

ar

Qtr3 Qtr4 Qtr1 Qtr2 Qtr3 Qtr4 Qtr1 Qtr2 Qtr3 Qtr4 Qtr1

2014 2015 2016 2017

Amou

nt In

vest

ed (U

S $M

)

Average investment size in Europe and Israel(Round sizes of 2-100M, and 6-month trailing average)

Total venture investment by country, 1Q 2017

• Israel saw the most VC investment in 1Q17, with $802M raised

• The UK came in second place, with $740M raised

• Germany saw the third-highest amount of venture investment, with $562M

• France was a close fourth, with $550M

Prepared by Gil Dibner follow me on (@gdibner), connect with me on , subscribe to my , or invest with me onblog 15

802

740

562

550

247

235

189

182

104

91

79

50

42

35

33

25

25

13

12

2

2

Israel

UK

Germany

France

Spain

Sweden

Netherlands

Austria

Ireland

Denmark

Switzerland

Estonia

Luxembourg

Belgium

Poland

Italy

Finland

Norway

Cyprus

Czech

Iceland

Total VC investment volume by country, 1Q17 (US $M)

Vive la Frenchtech!Total venture investment by country, 1Q15 to 1Q17

• To get a better sense of VC volumes in various countries, this analysis excludes mega-rounds

• With this filter, volumes and rankings are more consistent

• For the first time, France came in second, leapfrogging ahead of the UK and Germany in one quarter

• Sweden’s steady rise (five quarters of uninterrupted growth) is also worthy of note

• The UK and Germany seem to have levelled out over the past year

Prepared by Gil Dibner follow me on (@gdibner), connect with me on , subscribe to my , or invest with me onblog 16

543475

628699

963

1,064

877

490

802

719

437

625 444

871

553 544487 536

389

209

379342 335

429460

473

435

118

232 279224 279

367339 443

550

89 112

14084

139 151198 224 235

Qtr1 Qtr2 Qtr3 Qtr4 Qtr1 Qtr2 Qtr3 Qtr4 Qtr10

200

400

600

800

1000

1200

Tota

l VC

inve

stm

ent (

US $

M)

Total VC investment, 1Q15 - 1Q17 (top 5 countries, excluding mega-rounds)

IsraelUKGermanyFranceSweden

Total venture investment by country, 3Q14 to 4Q16

• To get a better sense of VC volumes in various countries, this analysis excludes mega-rounds

• The “second five” countries for VC investment in 2016 were Spain, Ireland, the Netherlands, Finland, and Denmark

Prepared by Gil Dibner follow me on (@gdibner), connect with me on , subscribe to my , or invest with me onblog 17

Qtr1 Qtr2 Qtr3 Qtr4 Qtr1 Qtr2 Qtr3 Qtr4 Qtr1

2015 2016 2017

0

20

40

60

80

100

120

140

Tota

l VC

inve

stm

ent (

US $

M)

Total VC investment, 1Q15 - 1Q17(countries ranked 6-10, excluding mega-rounds)

Spain IrelandNetherlands FinlandDenmark

Average venture round sizes, by region

• For a while, I had been seeing a trend towards convergence in the sizes of rounds across the geography

• Into 2017, this trend seems to be holding

• Most regions saw average round sizes flat or slightly down

• Average deal size in Israel is increasing

Prepared by Gil Dibner follow me on (@gdibner), connect with me on , subscribe to my , or invest with me onblog 18

Benelux, 4.7

Benelux, 10.8

DACH, 14.9

DACH, 11.4

France, 8.2 France, 8.1Iberia, 7.2

Iberia, 4.6

Israel, 15.9Israel, 15.2

Nordic, 11.5

Nordic, 9.9UK & Ireland, 8.5

UK & Ireland, 7.8

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

Qtr4 Qtr4 Qtr1

2014 2015 2017

Aver

age

roun

d si

ze (U

S $M

)

Average investment size in Europe and Israel (rounds of $2-100M)

Total venture investment by region

• When VC investments across Europe are aggregated into regions, UK & Ireland, DACH, Israel, DACH, and the Nordics are the clear and consistent leaders

• Benelux, Iberia, Southern Europe, and Eastern Europe do produce meaningful VC investments, but the volumes are still low

Prepared by Gil Dibner follow me on (@gdibner), connect with me on , subscribe to my , or invest with me onblog 19

UK & Ireland, 844

DACH, 822

Israel, 802

France, 550Nordic, 415Benelux, 266

Iberia, 247

South. Eur., 37

East. Eur., 35

Total VC investment by region, 1Q17

Rounds by bracket & region

• To get a better sense of deal volume, this analysis excludes seed deals which are often poorly reported

• Excluding seed deals, the UK and Ireland saw 79 venture deals in the fourth quarter

• Israel took third place with 52

Prepared by Gil Dibner follow me on (@gdibner), connect with me on , subscribe to my , or invest with me onblog 20

5245

20 24 25

8 114 4

18

10

18 15 9

3

7

4

146

4

3

0

10

20

30

40

50

60

70

80

90

UK &Ireland

France Israel DACH Nordic Benelux Iberia East. Eur. South. Eur.

Num

ber o

f inv

estm

ents

Number of investments in Europe and Israel by bracket, 1Q 2017

Mega (>100) Growth (20-100) Venture (8-20) Early Venture (2-8)

Participation rate of US VC firms, by bracket

• In the first quarter, US VCs participated in 8% of the VC financing rounds in EU and Israel

• As usual, US VCs are much more likely to participate in later rounds

Prepared by Gil Dibner follow me on (@gdibner), connect with me on , subscribe to my , or invest with me onblog 21

2%5%

20%31% 33%

98% 95%

80%69% 67%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Seed (.5-2) Early Venture (2-8) Venture (8-20) Growth (20-100) Mega (>100)

Perc

enta

ge o

f rou

nds

Did US VC firms participate in European VC rounds? (1Q17)

No Yes

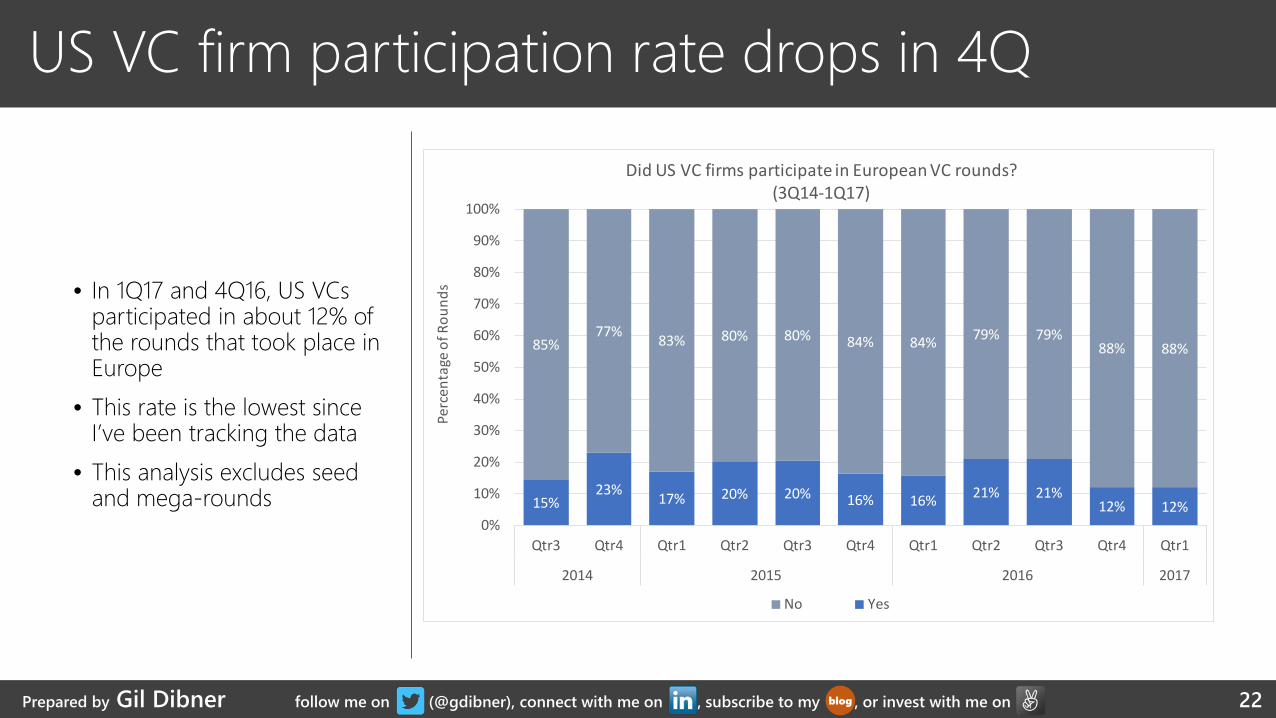

US VC firm participation rate drops in 4Q

• In 1Q17 and 4Q16, US VCs participated in about 12% of the rounds that took place in Europe

• This rate is the lowest since I’ve been tracking the data

• This analysis excludes seed and mega-rounds

Prepared by Gil Dibner follow me on (@gdibner), connect with me on , subscribe to my , or invest with me onblog 22

15%23% 17% 20% 20% 16% 16% 21% 21%

12% 12%

85%77% 83% 80% 80% 84% 84% 79% 79%

88% 88%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Qtr3 Qtr4 Qtr1 Qtr2 Qtr3 Qtr4 Qtr1 Qtr2 Qtr3 Qtr4 Qtr1

2014 2015 2016 2017

Perc

enta

ge o

f Rou

nds

Did US VC firms participate in European VC rounds?(3Q14-1Q17)

No Yes

Participation of US VC firms by country

• In 1Q17, US VCs firms were active in 9 different European countries

• US VC firms were most active in Israel, where they participated in 14 investment rounds

• The UK saw 12 US investments

• US VCs invested in 6 German companies

Prepared by Gil Dibner follow me on (@gdibner), connect with me on , subscribe to my , or invest with me onblog 23

1412

6

2 2 2 2 2 10

2

4

6

8

10

12

14

16

Isra

el UK

Ger

man

y

Esto

nia

Spai

n

Denm

ark

Fran

ce

Irela

nd

Aust

ria

Num

ber o

f VC

inve

stm

ents

Rounds with a US VC involved(1Q17)

Participation of US VC firms by country

• This chart shows US VC activity within Europe

• The overwhelming bulk of US VC activity is generally in Israel, the UK & Ireland, DACH

Prepared by Gil Dibner follow me on (@gdibner), connect with me on , subscribe to my , or invest with me onblog 24

Israel, 12 Israel, 14 Israel, 14 Israel, 14 Israel, 16

Israel, 27 Israel, 25

Israel, 12 Israel, 14

UK & Ireland, 10

UK & Ireland, 14UK & Ireland, 10 UK & Ireland, 8

UK & Ireland, 11

UK & Ireland, 11UK & Ireland, 12

UK & Ireland, 1

UK & Ireland, 14

DACH, 8

DACH, 6

DACH, 4 DACH, 9DACH, 6

DACH, 9 DACH, 8

DACH, 11

DACH, 7Nordic, 2

Nordic, 3

Nordic, 5Nordic, 5

Nordic, 5

Nordic, 4

Nordic, 6

Nordic, 4Iberia, 3

Iberia, 4 Iberia, 3

Iberia, 2

Iberia, 2France, 3

France, 2

France, 2

France, 3 France, 3

France, 2Benelux, 5

Benelux, 2 Benelux, 3

0

10

20

30

40

50

60

Qtr1 Qtr2 Qtr3 Qtr4 Qtr1 Qtr2 Qtr3 Qtr4 Qtr1

2015 2016 2017

Num

ber o

f VC

inve

stm

ents

Investments with US VC participation

Israel UK & Ireland DACH Nordic Iberia France Benelux East. Eur. South. Eur.

Dimension Categories Explanation/Example

1. Target market Consumer, SMB, Enterprise, Government, Telecom, OEM

What sort of customer does the company target?

2. Vertical marketAdtech, Communications, Data, Development, Durables, Education, Electronics, Employment, Energy, Fashion, Financial, Food, Gaming, Health, HMI, Industrial, Infrastructure, Lifestyle, Logistics, Marketing, Media, Productivity, Real Estate, Security, Sports, Storage, Transportation, Travel, Water

What type of problem does the company solve?

3. Business modelCommerce, Components, Content, Marketplace, SaaS, Semiconductors, Services, Software, Systems,

How does the company makemoney? How is value delivered to customers? What are customers paying for?

For example: Consumer + Travel + Marketplace AirBnB has built a travel-related marketplace for consumers

Three-dimensional approach to sector mapping

Prepared by Gil Dibner follow me on (@gdibner), connect with me on , subscribe to my , or invest with me onblog 25

• Excluding mega-rounds, investment activity was flat in consumer but increased in enterprise

What target markets are attracting the most VC investment in Europe & Israel?

Prepared by Gil Dibner follow me on (@gdibner), connect with me on , subscribe to my , or invest with me onblog 26

980 8501,177

931 1,076 1,244 1,097 1,004 1,017

953804

9101,110

1,6541,640

1,269962

1,636

275

224

270

285

182150

163 187

219448

254

0

500

1,000

1,500

2,000

2,500

3,000

3,500

Qtr1 Qtr2 Qtr3 Qtr4 Qtr1 Qtr2 Qtr3 Qtr4 Qtr1

2015 2016 2017

Tota

l VC

inve

stm

ents

(US $

M)

European & Israeli venture financing by target market3Q14 to 1Q17 (excluding mega-rounds, US $M)

Agriculture

Government

Telecom

OEM

SMB

Enterprise

Consumer

• When Israel is excluded from the sample, 46% of all VC dollars in Europe went to consumer-oriented companies

• Enterprise and SMB categories spiked in 1Q17

Consumer investment leads Europe

Prepared by Gil Dibner follow me on (@gdibner), connect with me on , subscribe to my , or invest with me onblog 27

62%

36%

56% 63% 62% 57% 53% 58% 52%45% 46%

18%

48%

34% 22% 24% 31% 35%33%

32%

29%36%

6%10% 4% 12% 8% 6% 5% 3%

7%

8%

12%5%4% 2% 4% 5% 6% 5% 8%

10%

5%6% 6%8%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Qtr3 Qtr4 Qtr1 Qtr2 Qtr3 Qtr4 Qtr1 Qtr2 Qtr3 Qtr4 Qtr1

2014 2015 2016 2017

European venture financing by target market3Q14 to 1Q17 (excluding Israel, percent of US $M)

Agriculture Government Telecom OEM SMB Enterprise Consumer

Breakdown by region & target market

• Regional differences are very apparent when VC investment are categorized by target market

Prepared by Gil Dibner follow me on (@gdibner), connect with me on , subscribe to my , or invest with me onblog 28

355 338

56

249121 144

212

278 336

641 242

163 105

133 88

52

100

74 4897

0

100

200

300

400

500

600

700

800

900

UK &Ireland

DACH Israel France Nordic Benelux Iberia South.Eur.

East. Eur.

Tota

l am

ount

inve

sted

(US $

M)

Investment in Europe and Israel by target market by region2017 (US $M)

Agriculture Government Telecom OEM SMB Enterprise Consumer

Distribution of investment rounds by country

• Across Europe & Israel, 42% of VC investment rounds were in consumer companies in 2016

• Over two-thirds of Israeli venture investments were into enterprise companies

• Three quarters of VC investments in Iberia were into consumer companies

Prepared by Gil Dibner follow me on (@gdibner), connect with me on , subscribe to my , or invest with me onblog 29

74%

69%

46%

42%

42%

42%

28%

16%

19%

25%

38%

26%

36%

42%

48%

69%

12%

21%

13%

8%

4%

6%

10%

8%

7%

4%

11%

7%

12% 4%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Iberia

South. Eur.

France

DACH

Nordic

UK & Ireland

Benelux

Israel

Investment in Europe and Israel by target market by country1Q17 (Number of investments)

Consumer Enterprise SMB OEM Telecom Government Agriculture

Growth rounds by target market

• Enterprise companies accounted for just over half of the later-stage market in Europe & Israel in 1Q17

Prepared by Gil Dibner follow me on (@gdibner), connect with me on , subscribe to my , or invest with me onblog 30

56%

37%46%

56%43% 39% 38% 43% 44%

34% 36%

25%

41%

46% 25%38% 50% 50%

50% 44%

32%

51%

6% 7%

5%

9% 12%3% 6% 5%

12%

7%6% 11% 6% 7% 5% 6% 5% 5%20%

7%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Qtr3 Qtr4 Qtr1 Qtr2 Qtr3 Qtr4 Qtr1 Qtr2 Qtr3 Qtr4 Qtr1

2014 2015 2016 2017

Investment in Europe and Israel by target market(Rounds over $20M, number of investments)

Government Telecom OEM SMB Enterprise Consumer

• Fintech was the most popular vertical across Europe & Israel, with 62 investments in the category

• Lifestyle (a catchall category for consumer commerce) was the second most popular vertical, with 35

Finance returned to being the top vertical

Prepared by Gil Dibner follow me on (@gdibner), connect with me on , subscribe to my , or invest with me onblog 31

55

66

88

999

1111

121212121212

1313

1618

1919

2224

2528

3031

3562

ProductivityHMI

IndustrialAgtech

CommunicationsLegal

Real EstateERP

SocialCRM

EntertainmentDevelopment

EnergyTravel

AutomotiveGaming

FoodPayments

LogisticsFashionAdtech

EducationData

HealthSecurity

ElectronicsEmployment

MarketingInfrastructure

LifestyleFinancial

European & Israeli venture financing by target market1Q17 (top 30 categories, number of investments)

• This graph shows the change in the number of investments by vertical from 1Q17 to 1Q16

• Lifestyle e-commerce, fashion, health, infrastructure, and electronics increased the most in frequency

• Logistics, CRM, and Industrial saw the biggest declines

Growth rates by vertical

Prepared by Gil Dibner follow me on (@gdibner), connect with me on , subscribe to my , or invest with me onblog 32

Industrial, -65%CRM, -45%

Logistics, -28%Development, -14%

Marketing, -9%Gaming, -8%

Food, -8%Security, 4%

Payments, 8%Energy, 9%

Grand Total, 11%Financial, 19%Adtech, 20%

Data, 27%Employment, 27%

Electronics, 32%Infrastructure, 35%

Health, 38%Fashion, 45%

Lifestyle, 67%

-80% -60% -40% -20% 0% 20% 40% 60% 80%

Change in the number of venture investments(1Q17 vs 1Q16, 20 most popular categories)

• Finance was once again the most frequently funded vertical, but with increased attention to enterprise and SMB

• Consumer lifestyle companies took second place

• Infrastructure jumped to third place

• Marketing dropped from third to fourth

Which verticals for which segments?

Prepared by Gil Dibner follow me on (@gdibner), connect with me on , subscribe to my , or invest with me onblog 33

Data

Education

Health

Security

Electronics

Employment

Marketing

Infrastructure

Lifestyle

Financial

0 10 20 30 40 50 60 70

European & Israeli venture financing by target market1Q17 (number of investments, top 10 verticals)

Consumer

Enterprise

SMB

OEM

Telecom

Government

• This chart shows the ten most commonly funded verticals across Europe & Israel by quarter

The most popular verticals in the past 2 years

Prepared by Gil Dibner follow me on (@gdibner), connect with me on , subscribe to my , or invest with me onblog 34

Qtr3 Qtr4 Qtr1 Qtr2 Qtr3 Qtr4 Qtr1 Qtr2 Qtr3 Qtr4 Qtr1

2014 2015 2016 2017

0

50

100

150

200

250

300

350

European & Israeli venture financing by vertical market(number of investments, top 10 verticals)

Adtech

Health

Logistics

Electronics

Lifestyle

Employment

Security

Infrastructure

Marketing

Financial

• Investors continue to favor financial, lifestyle, and health investments

• Education and fashion bounced back

• Logistics (ride sharing, taxi hailing, and the like) appears to be played out

• Food and travel seem to be in decline

Consumer VC investment trends

Prepared by Gil Dibner follow me on (@gdibner), connect with me on , subscribe to my , or invest with me onblog 35

Qtr3 Qtr4 Qtr1 Qtr2 Qtr3 Qtr4 Qtr1 Qtr2 Qtr3 Qtr4 Qtr1

2014 2015 2016 2017

0

20

40

60

80

100

120

140

160

180

European & Israeli venture financing by consumer verticals(number of investments, top 10 verticals)

Travel

Health

Fashion

Food

Electronics

Logistics

Gaming

Lifestyle

Financial

Education

• Security, financial, and HR/employment-related technology showing increases in 1Q17

• CRM and industrial declined in 1Q17

Enterprise VC investment trends

Prepared by Gil Dibner follow me on (@gdibner), connect with me on , subscribe to my , or invest with me onblog 36

Qtr3 Qtr4 Qtr1 Qtr2 Qtr3 Qtr4 Qtr1 Qtr2 Qtr3 Qtr4 Qtr1

2014 2015 2016 2017

0

20

40

60

80

100

120

140

160

180

European & Israeli venture financing by enterprise verticals(number of investments, top 10 verticals)

CRM

Financial

Industrial

Employment

Development

Data

Infrastructure

Adtech

Security

Marketing

• SaaS was the most funded business model in 1Q17, representing 27% of all VC dollars

• Services took 22% of the venture dollars invested in Europe & Israel

• Systems – complete physical products – took fourth place at 11% of all venture dollars

• Marketplaces – businesses that serve a price discovery function – rebounded to 9%

SaaS above all (but keep an eye on systems)

Prepared by Gil Dibner follow me on (@gdibner), connect with me on , subscribe to my , or invest with me onblog 37

SaaS, 887, 27%

Services, 721, 22%

Software, 457, 14%

Systems, 364, 11%Marketplace, 299, 9%

Commerce, 244, 8%

Media, 153, 5%

Semiconductors, 55, 2%

Components, 52, 2%

Materials, 11, 0%

European & Israeli venture financing by target market1Q17 (in US $M) (excluding mega-rounds)

• SaaS and Services remained the top two business models by funding volume

• Commerce collapsed from third place in 4Q16 to sixth place in 1Q17

• Systems maintained their fourth place ranking

• Marketplaces rebounded somewhat

Commerce disappears and systems rise

Prepared by Gil Dibner follow me on (@gdibner), connect with me on , subscribe to my , or invest with me onblog 38

0

200

400

600

800

1000

1200

Qtr3 Qtr4 Qtr1 Qtr2 Qtr3 Qtr4 Qtr1 Qtr2 Qtr3 Qtr4 Qtr1

2014 2015 2016 2017

European & Israeli venture financing by business model(top seven, in US $M, excluding mega-rounds)

Services

SaaS

Software

Commerce

Marketplace

Systems

Media

• This graph provides a quick overview of the ten most commonly funded segments across the top ten countries for those segments

• In a nutshell:• Consumer financial services

(Everywhere, but especially in the UK)

• UK marketing SaaS• Israeli enterprise security

software• French infrastructure SaaS• French adtech services• UK enterprise financial SaaS• French consumer electronics• And some other stuff….

EU+IL VC Cheat Sheet (1Q17)

Prepared by Gil Dibner follow me on (@gdibner), connect with me on , subscribe to my , or invest with me onblog 39

0 5 10 15 20 25 30 35

Consumer Education Services

Consumer Electronics Systems

Enterprise Financial SaaS

Enterprise Adtech Services

Enterprise Infrastructure SaaS

Consumer Fashion Commerce

Enterprise Data SaaS

Consumer Lifestyle Commerce

Enterprise Security Software

Enterprise Marketing SaaS

Consumer Financial Services

Number of VC investments

Investment in Europe & Israel by segment by country1Q17 (top 10 segments, top 10 countries)

UK FranceIsrael SwedenGermany IrelandSpain SwitzerlandPoland Italy

Focus on Infrastructure

• 1Q17 saw a dramatic rise in the number of infrastructure-oriented investments across Europe and Israel

• A lot of this had to do with a spike in activity in France

Prepared by Gil Dibner follow me on (@gdibner), connect with me on , subscribe to my , or invest with me onblog 40

0

5

10

15

20

25

30

Qtr3 Qtr4 Qtr1 Qtr2 Qtr3 Qtr4 Qtr1 Qtr2 Qtr3 Qtr4 Qtr1

2014 2015 2016 2017

Num

nber

of i

nves

tmen

ts

Infastructure - VC investment in Europe and Israel

Latvia Iceland Portugal Luxembourg GreeceDenmark Italy Poland Norway BelgiumIreland Netherlands Finland Switzerland Spain

Focus on Fashion

• 1Q17 also saw a spike in the number of fashion-oriented investments across Europe and Israel

• Activity in France, Italy, the UK, and Sweden was the main driver here

Prepared by Gil Dibner follow me on (@gdibner), connect with me on , subscribe to my , or invest with me onblog 41

0

2

4

6

8

10

12

14

16

18

Qtr3 Qtr4 Qtr1 Qtr2 Qtr3 Qtr4 Qtr1 Qtr2 Qtr3 Qtr4 Qtr1

2014 2015 2016 2017

Num

nber

of i

nves

tmen

ts

Fashion - VC investment in Europe and Israel

Greece Portugal Denmark Switzerland Lithuania Finland Netherlands

Italy Israel Sweden Spain France Germany UK

Based in , I was previously a partner at . Before that, I helped run the

European seed program for . I moved to London after seven years in

during which I worked as a VC with and . I’m originally from .

My VC investments include and . Angel investments include and many more.

If you found this useful, I hope you’ll subscribe to my blog.42

Gil Dibner

To invest in the best European & Israeli enterprise startups,

consider backing me on here. Lots of exciting stuff in thepipeline – and you’ll be in pretty good company.