Embed Size (px)

Citation preview

FICO® TRIAD® Customer Manager empowers clients to make better customer decisions in revolving and deposit portfolios to increase revenue, reduce losses and operational costs, while reducing capital requirements. This white paper outlines how TRIAD customers that actively use the product see even greater benefits that can lead to tens of millions of dollars in incremental profit.

Three important insights regarding TRIAD usage have emerged from a recently conducted analytical review of TRIAD users:

First, the highest levels of account profitability were achieved by the most active TRIAD Customer Manager users—those who utilized the most advanced product features, upgraded to the latest and most capable versions of TRIAD Customer Manager, or integrated TRIAD Customer Manager with other FICO modeling and optimization products and services.

Second, those who utilized more of the advanced capabilities of their TRIAD systems are achieving significantly higher levels of controlled account profitability, compared to less active TRIAD users—without incurring increased levels of delinquencies and defaults.

Third, TRIAD customers that are using older versions or have not updated the initial decision support capabilities are still seeing significant benefits from TRIAD Customer Manager, but are leaving money on the table by not upgrading and/or taking full advantage of TRIAD Customer Manager’s capabilities.

A range of more active approaches are available to current TRIAD users. This white paper defines and analyzes how active TRIAD users are achieving major improvements in profitability—identifying which advanced features are proving most profitable, which new areas of account management are being addressed profitably with TRIAD Customer Manager and which other FICO products or services enhance TRIAD value when integrated.

www.fico.com Make every decision countTM

WHITE PAPER

Active usage of FICO® TRIAD® Customer Manager can yield millions in incremental profits

“Assuming 5,000 charge off accounts per month, active TRIAD customers can realize an annualized savings of $48 million in bad debt vs. passive TRIAD customers.”

©2014 Fair Isaac Corporation. All rights reserved. page 2

In today’s tough competitive business environment, it’s rare to find up to $48 million of added income or reduced costs in an operating business—without liquidating valuable assets or major investment. It’s even more rare to find that a business already has the tools to achieve significantly higher levels of profitability—and only needs to utilize its current tools in a more effective and comprehensive manner.

That’s precisely the situation for more than 50% of FICO® TRIAD® Customer Manager users who are currently using only a portion of their TRIAD system’s decision support capabilities. Their TRIAD Customer Manager system has helped them make account management decisions that increased risk-related revenue, reduced losses, automated manual processes to reduce operational costs and reduced capital requirements. While their TRIAD system met their most immediate decision support needs when first put into operation, many TRIAD systems continue to operate unchanged over many years with only the most basic functions enabled.

These increases in account profitability through more active TRIAD Customer Manager use have been documented both in very large financial organizations and smaller businesses, and across a range of regions. To achieve these improvements, TRIAD users can expand their usage in a number of ways. More capabilities of their current TRIAD system can be engaged by using more TRIAD decision areas, developing custom decision keys, and utilizing event triggers and other easily adopted features. Older TRIAD systems can be updated to the most current version with advanced features such as Decision Graph, internal triggering, multiple strategies linking, FICO® Blaze Advisor® business rules management system and use of multiple random digits. TRIAD strategies can be seamlessly exchanged with FICO’s advanced decision modeling and optimization products to keep strategies continuously updated. Moreover, FICO strategic consulting services can provide TRIAD users with the level of support needed anywhere across the entire credit lifecycle.

The goal of this paper is to provide TRIAD users with relevant case studies, identifying and quantifying the financial benefits of using more, and more advanced, TRIAD features—and assistance in determining which would be most profitable and the highest priority enhancements to pursue for their businesses.

Expanding the Value of FICO® TRIAD® Customer Manager

• Asbusinessneedsandprioritieschange,accountmanagement strategies need to be refreshed and sharpened.

• Asexpectedwithmaturingsystems,FICOregularlyintroduces new versions of the TRIAD product with more advanced features, and encourages clients to upgrade to stay current with the newest capabilities and technologies.

• CostsassociatedwithincreasingtheuseofTRIADCustomer Manager are minimal.

• Andmostimportantly,FICO’smostrecentstudiesofTRIADclient usage have indicated that expanded and enhanced TRIAD usage results in significant increases in the profitability of customer accounts—without incurring increased levels of delinquencies and defaults.

There are a number of compelling reasons To consider increasing The uTilizaTion of fico® Triad® cusTomer manager

Introduction

©2014 Fair Isaac Corporation. All rights reserved. page 3

Do active users of FICO® TRIAD® Customer Manager, along with other complementary FICO tools, perform better than passive users—and by how much? This case study analyzes the portfolio performance of 34 financial institutions using TRIAD Customer Manager, comparing the portfolio performance of the most active and the most passive users of the system over a 12-month period.

defining active versus passive Triad users

The scorecard below (Chart 1) provides the criteria used in this study to classify a client as active or passive. The scorecard lists 11 available features of TRIAD Customer Manager, TRIAD add-on functionality, and other related FICO tools and services. Any client using seven or more of these features is considered active, while clients using less than seven features are classified as passive. FICO categorized the clients as active or passive, representing five countries: United States, Canada, United Kingdom, Mexico and Puerto Rico (Chart 2.)

Expanding the Value of FICO® TRIAD® Customer Manager

charT 1: acTive vs. passive scorecard

Features Active User Passive User (7 or more of 11 features) (Less than 7 of 11 features)

Core Strategies (minimum)

CDA Strategies (Reissue, Pricing, etc.)

Custom Keys

Custom Scores

Credit Line Offers

OCLR (On-demand credit line review)

Estimators

Intracycle event triggers

Ongoing Strategic Development

FICO Consulting

FICO® Decision Optimizer (Strategy Optimization)

charT 2: acTive vs. passive by counTry

Country Active Users Passive Users

United States 5 9

Canada 6 2

United Kingdom 5 4

México & Puerto Rico 0 3

How Active Versus Passive TRIAD Use Affects Portfolio Performance

3

3

3

3

3

3

3

3

3

3

3

3

3

3

3

3

3

©2014 Fair Isaac Corporation. All rights reserved. page 4

The first, most active group is an engaged set of financial institutions. They take full advantage of the standard tools and features in FICO® TRIAD® Customer Manager, the FICO® Blaze Advisor® rules management system and Decision Graph. They also leverage FICO Consulting services. The active group regularly utilizes champion/challenger testing, creates sophisticated solutions using the configurable decision areas, employs event triggers to call TRIAD Customer Manager outside of the regular billing cycles, utilizes multiple random digit numbers and links decision areas to drive credit line increases and marketing offers. This group effectively uses internal and external data to create custom decision keys and custom scores to improve decisions. They also use TRIAD Customer Manager strategically to create processes that meet regulatory mandates without compromising or eliminating core practices that contribute to increased revenues. In addition, some clients in this group further complement and enhance their internal analytic resources with the FICO® Decision Optimizer decision management tool.

The second, more passive group uses TRIAD Customer Manager conventionally: limited champion/challenger testing and strategy updates, rare use of new decision areas and minimal use of TRIAD features such as event or internal triggers. There is little linking of strategies and typically only leverage the standard set of decision keys. This group also has conservative credit line increase policies and pricing management programs in response to the latest regulatory changes.

FICO compared the performance of the active and passive groups using the selected metrics. Both have the same risk management tools at their disposal but their results are quite different and compelling. The results reveal a strong financial case for increasing the degree of account management activity using TRIAD Customer Manager and other FICO tools and services.

Expanding the Value of FICO® TRIAD® Customer Manager

• AverageCurrentBalance

• AverageInterestIncomeperAccount

• PercentAccountswithBalance

• 1–2CycleRollRates

• 2+CycleDelinquency

• AverageCharge-Off(C/O)Balance

how porTfolio performance is measured

FICO selected a set of metrics to determine if dynamic use of TRIAD Customer Manager positively influences portfolio performance:

©2014 Fair Isaac Corporation. All rights reserved. page 5

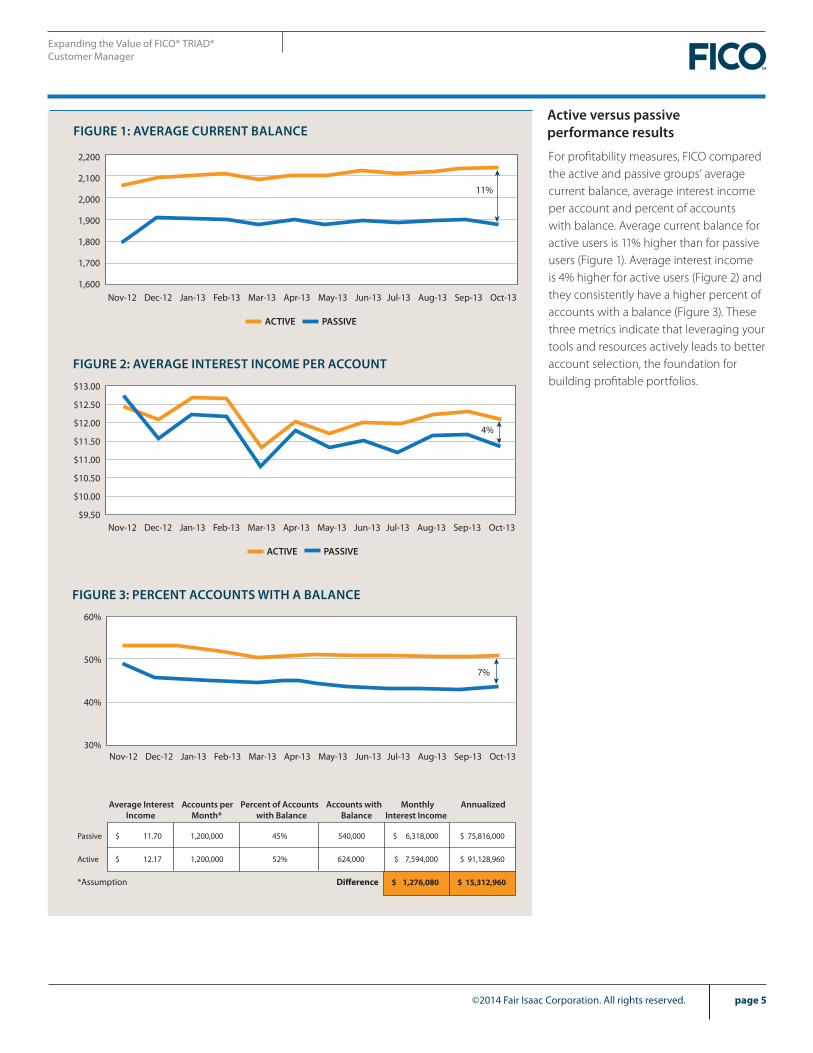

active versus passive performance results

For profitability measures, FICO compared the active and passive groups’ average current balance, average interest income per account and percent of accounts with balance. Average current balance for active users is 11% higher than for passive users (Figure 1). Average interest income is 4% higher for active users (Figure 2) and they consistently have a higher percent of accounts with a balance (Figure 3). These three metrics indicate that leveraging your tools and resources actively leads to better account selection, the foundation for building profitable portfolios.

Expanding the Value of FICO® TRIAD® Customer Manager

2,200

2,100

2,000

1,900

1,800

1,700

1,600Nov-12 Dec-12 Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13 Aug-13 Sep-13 Oct-13

ACTIVE PASSIVE

11%

figure 1: average currenT balance

$13.00

$12.50

$12.00

$11.50

$11.00

$10.50

$10.00

$9.50Nov-12 Dec-12 Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13 Aug-13 Sep-13 Oct-13

ACTIVE PASSIVE

4%

figure 2: average inTeresT income per accounT

60%

50%

40%

30%Nov-12 Dec-12 Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13 Aug-13 Sep-13 Oct-13

ACTIVE PASSIVE

7%

figure 3: percenT accounTs wiTh a balance

Average Interest Accounts per Percent of Accounts Accounts with Monthly Annualized Income Month* with Balance Balance Interest Income

Passive $ 11.70 1,200,000 45% 540,000 $ 6,318,000 $ 75,816,000

Active $ 12.17 1,200,000 52% 624,000 $ 7,594,000 $ 91,128,960

$ 1,276,080 $ 15,312,960*Assumption Difference

©2014 Fair Isaac Corporation. All rights reserved. page 6

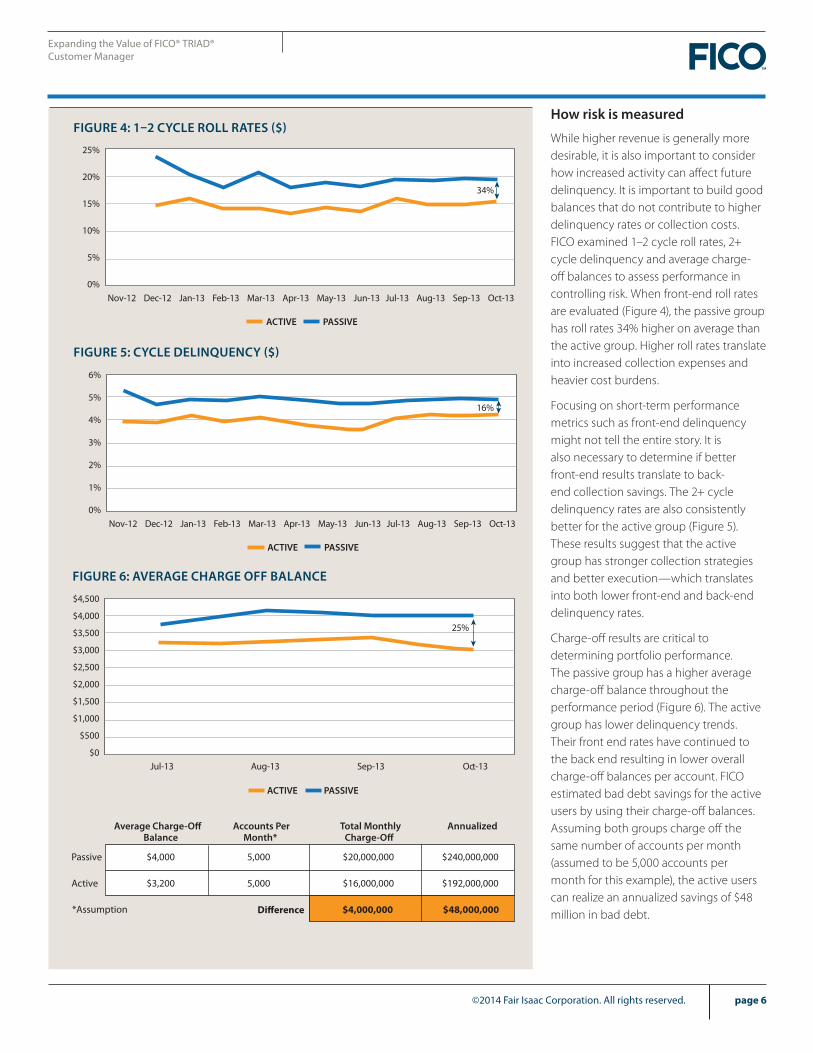

how risk is measured

While higher revenue is generally more desirable, it is also important to consider how increased activity can affect future delinquency. It is important to build good balances that do not contribute to higher delinquency rates or collection costs. FICO examined 1–2 cycle roll rates, 2+ cycle delinquency and average charge-off balances to assess performance in controlling risk. When front-end roll rates are evaluated (Figure 4), the passive group has roll rates 34% higher on average than the active group. Higher roll rates translate into increased collection expenses and heavier cost burdens.

Focusing on short-term performance metrics such as front-end delinquency might not tell the entire story. It is also necessary to determine if better front-end results translate to back-end collection savings. The 2+ cycle delinquency rates are also consistently better for the active group (Figure 5). These results suggest that the active group has stronger collection strategies and better execution—which translates into both lower front-end and back-end delinquency rates.

Charge-off results are critical to determining portfolio performance. The passive group has a higher average charge-off balance throughout the performance period (Figure 6). The active group has lower delinquency trends. Their front end rates have continued to the back end resulting in lower overall charge-off balances per account. FICO estimated bad debt savings for the active users by using their charge-off balances. Assuming both groups charge off the same number of accounts per month (assumed to be 5,000 accounts per month for this example), the active users can realize an annualized savings of $48 million in bad debt.

Expanding the Value of FICO® TRIAD® Customer Manager

ACTIVE PASSIVE

25%

20%

15%

10%

5%

0%

Nov-12 Dec-12 Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13 Aug-13 Sep-13 Oct-13

34%

figure 4: 1–2 cycle roll raTes ($)

6%

5%

4%

3%

2%

1%

0%

Nov-12 Dec-12 Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13 Aug-13 Sep-13 Oct-13

ACTIVE PASSIVE

16%

figure 5: cycle delinQuency ($)

$4,500

$4,000

$3,500

$3,000

$2,500

$2,000

$1,500

$1,000

$500

$0

ACTIVE PASSIVE

Jul-13 Aug-13 Sep-13 Oct-13

25%

figure 6: average charge off balance

Average Charge-Off Accounts Per Total Monthly Annualized Balance Month* Charge-Off

Passive $4,000 5,000 $20,000,000 $240,000,000

Active $3,200 5,000 $16,000,000 $192,000,000

$4,000,000 $48,000,000Difference*Assumption

©2014 Fair Isaac Corporation. All rights reserved. page 7

This data demonstrates that active usage of FICO® TRIAD® Customer Manager results in revenue increases and loss decreases simultaneously, which is an outcome every risk manager strives for.

Triad performance in smaller financial organization portfolios

This analysis raises a fundamental question: Are these benefits limited to very large financial institutions, or can smaller organizations also reap the benefits of active usage? The active group in this study includes seven small clients (those having less than 1 million accounts). This represents 44% of the Active user pool of 16, using the same performance and risk metrics. Below we show the results for our three smallest users in the Active pool. Comparing the average current balance and 1–2 cycle roll rates, the smallest users have higher average current balances and similar front-end roll rates when compared to the entire active peer sample.

In assessing the performance of the three smallest users in the pool compared to the entire group of active users, it is clear that the smallest users have also successfully used TRIAD Customer Manager to both manage risk and improve reward. It is therefore reasonable to conclude that optimal performance is not dependent upon having large portfolios to manage. Organizations with smaller portfolios will also reap the benefits of active TRIAD use.

The compelling case for more active Triad use

The active group’s willingness to exploit their TRIAD tool arsenal, implement sophisticated TRIAD functionality such as optimized strategies and leverage FICO Consulting translates into better risk discrimination and maximization of revenue. This case study reveals two key findings:

1. Following a conservative approach by not taking advantage of all the TRIAD tools available may restrict profit potential and contribute to higher long-term losses.

2. A greater commitment to sound risk management principles and practices contributes to long-term profitability with low incremental costs.

The payoff is clearly worth the investment. Active use of TRIAD Customer Manager and other FICO tools will yield good results for all portfolio sizes and types.

Expanding the Value of FICO® TRIAD® Customer Manager

2,400

2,350

2,300

2,250

2,200

2,150

2,100

2,050

2,000

1,950

1,900

ACTIVE 3 SMALLEST ACTIVE

Nov-12 Dec-12 Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13 Aug-13 Sep-13 Oct-13

18%

16%

14%

12%

10%

8%

6%

4%

2%

0%

ACTIVE 3 SMALLEST ACTIVE

Nov-12 Dec-12 Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13 Aug-13 Sep-13 Oct-13

Three smallesT acTive clienTs

average currenT balance 1–2 cycle roll raTes ($)

©2014 Fair Isaac Corporation. All rights reserved. page 8

Expanding the Value of FICO® TRIAD® Customer Manager

The underutilized features and potential new applications of a presently operating FICO® TRIAD® Customer Manager are the ultimate low-hanging fruit. A wealth of additional TRIAD features are on-board and easily activated. Often, all it takes is a bit of FICO training to put these powerful TRIAD capabilities to work:

decision areas: put Triad predictive analytics to work in more ways

TRIAD Customer Manager is typically implemented initially to manage risk for a single or multiple products, and is most frequently used to assign credit limits or determine whether to approve card transactions. TRIAD Customer Manager can be put to work profitably in other customer decision areas such determining the best collection strategy or targeted marketing offers.

custom Keys: gain a competitive edge with unique customer data

Every organization’s customers are different from those of its competitors—and its customer database contains insights that competitors cannot know or utilize. TRIAD Customer Manager can create custom decision keys based on this unique customer data to reveal and quickly explore these differentiating customer characteristics, potentially gaining a competitive edge. For example, additional payment history insight can be gained by creating a key that measures the number of late payments in the past year, or a key that helps understand credit utilization trends by comparing current utilization rates with those over the past six months. Footprint or relationship data can also help segment high-value cardholders and tailor their handling and services accordingly.

event Triggers: put Triad decision support on-call whenever needed

TRIAD Customer Manager is most commonly utilized on a scheduled monthly basis tied to billing cycles. However, TRIAD Custom Event Triggers can also employ TRIAD Customer Manager situationally in response to internal or external events. For instance, a major bank in Central Europe creates event-triggered marketing offers in response to a customer’s most recent activity, significantly improving customer response, product penetration and customer loyalty. TRIAD Customer Manager can also adjust collections strategies based on customer actions, or even based on adverse conditions such as those reported in credit reports.

Fair Isaac® Advisors will be happy to help determine which features of TRIAD Customer Manager can be most easily and profitably utilized. To begin assessing the TRIAD system’s current and potential usage, please consult the step-by-step evaluation roadmap: “Steps to Achieving Maximum Value with TRIAD Customer Manager” on page 13.

Unleash the Full Potential of the Existing TRIAD System

Expanding the Value of FICO® TRIAD® Customer Manager

While nobody can predict the future, it’s safe to say that it will bring change. The evolution of business policies, corporate strategy, customer demands, product innovation, competitive pressure and regulatory changes all drive change. The strategies used in FICO® TRIAD® Customer Manager today must also adapt to the changing economic conditions. Active users don’t make frequent changes to their decision strategies; rather, it is an iterative process. They are constantly hypothesizing, testing and implementing new strategies.

In order to take maximal advantage of TRIAD Customer Manager, organizations need to take three key steps:

1. Set up appropriate test groups via use of TRIAD Customer Manager’s random digit group functionality.

2. Create and deploy promising challenger strategies.

3. Measure strategy efficacy and rigorously promote the best strategies.

These steps are the tried and tested methodology to increase the profitability of a portfolio but they can be supercharged with modern analytic tools that further enhance the benefit of TRIAD decisions. Since the deployment of these tools is in TRIAD Customer Manager, costs remain manageable.

decision modeling and optimization

Improving how challenger strategies are created is the most impactful means of increasing the value of TRIAD Customer Manager. The most effective approaches involve the combination of sophisticated decision models and optimization tools FICO® Decision Optimizer and FICO® Model Builder has been used to create successful challenger strategies for a number of TRIAD decision areas in a wide variety of markets and regulatory environments. The most common challenger strategies have been derived for credit line management, addressing both increases and decreases. FICO has also helped many clients improve authorizations and collections decisions.

Strategy improvements can be made based on empirical analysis and on experience-based conjectural processes. Historically, one of the impediments to rapid development and deployment of empirically-derived strategies has been overcoming the challenge associated with deploying them into a runtime environment. Optimized strategies are by their nature very large and complex. Coding those into a runtime environment is sometimes a barrier.

TRIAD Customer Manager, Decision Optimizer and Model Builder are designed to increase the agility of this process by allowing strategies to be passed seamlessly from TRIAD Customer Manager to Model Builder or Decision Optimizer. Users can then utilize the full power of those tools to enhance their strategies. Once those enhancements have been made, they can very simply be transferred back into TRIAD Customer Manager.

The process of enhancing strategies in advanced analytical tools now becomes completely frictionless and allows financial institutions to constantly operate with up-to-date decision strategies.

©2014 Fair Isaac Corporation. All rights reserved. page 9

Supercharging TRIAD Customer Manager

©2014 Fair Isaac Corporation. All rights reserved. page 10

Expanding the Value of FICO® TRIAD® Customer Manager

building predictive models, action-effect models and decision models

FICO® TRIAD® Customer Manager users have been successfully leveraging predictive models for over 20 years. Predictive models that estimate probability of default, probability of attrition, and expected revenue and losses are widely used and have proven essential to effective strategy creation. These predictive models are elaborate mathematical formulas that convert observable factors (e.g., historical payments, purchase activity, etc.) into a single prediction for how someone will behave (e.g., probability of default, etc.).

However, issuers have several opportunities to explicitly impact the behavior of their customers and the resultant outcomes. Decisions such as credit line assignment, whether to approve an over-limit authorization and what actions to take on a delinquent account can all have considerable impact on the subsequent behavior of the cardholder. Action-effect models explicitly take this into account and are different from predictive models in two key ways:

1. Action-effect models use issuer actions as an input to the model.

2. Action-effect models make multiple predictions for each customer, one for each action under consideration.

A well-built action-effect model will accurately capture not just the relative and absolute difference in expected revenue but also the relative and absolute difference in how responsive each customer will be to the various actions that the issuer can take.

maximizing value with model optimization

Once the decision model is built and tested, it can be leveraged by sophisticated optimization algorithms to determine the action that best meets the organization’s objectives. Optimization software such as FICO® Decision Optimizer can find the combination of actions for a portfolio that maximizes profitability while simultaneously meeting operational and business constraints. Examples of operational constraints include rules such as “Don’t increase anyone with a credit score less than 680,” or “Only give increases larger than $3,000 to people who have had a revolving balance over $5,000 in the past 12 months.” Examples of business constraints include, “Don’t select any line management policy that will lead to an increase in loss rate more than 2 basis points,” or “Don’t increase aggregate exposure by more than 5%.”

With so much flexibility to specify a wide range of constraints, it is very common to run dozens of different optimization jobs with varying levels of constraints. This allows portfolio managers to explore a range of options and weigh trade-offs between profits, losses, exposure and other key metrics. Once the desired operating point has been identified, the optimal policy is converted into a strategy tree that can be executed in TRIAD Customer Manager on a monthly, daily or transactional basis.

Quickstarting active Triad use with fico® custom scores and fico® custom models

While many TRIAD users have considerable analytic resources and multiple FICO tools available, some TRIAD users may find it more efficient to leverage FICO’s expertise for developing custom scores, models or entire fully-optimized strategies.

©2014 Fair Isaac Corporation. All rights reserved. page 11

Expanding the Value of FICO® TRIAD® Customer Manager

custom scores: The fast lane to increased profitability

No organization in the commercial world has more experience than FICO in applying advanced scoring techniques to enhance the critical business operations of banks, insurance firms and other financial organizations. FICO can put an advanced customer scoring system into service for virtually any business in a matter of days. Scorecards created by FICO and implemented in FICO® TRIAD® Customer Manager help financial institutions better predict the probability of default, bankruptcy or attrition. For example, behavior models have been shown to reduce bad rates by 10%–30%.

custom models: advanced decision support at your command

FICO custom modeling has put the power of predictive financial models to work quickly and cost-effectively for hundreds of smaller organizations. FICO predictive models have also provided innovative solutions to other major business challenges—such as redeploying airline planes and crews during and after large-scale weather delays.

fico® model central™ solution: managing models for compliance and profit

As financial models proliferate across diverse business units, maintenance and regulatory compliance become increasingly difficult. The FICO Model Central Solution provides full documentation of each model—from its initial concept and goals, through its sources and validation of data, to implementation and deployment, and any subsequent changes and enhancements. Queries by management or regulators can be fully and easily answered, and developers can understand which models can be effectively applied in new environments.

custom strategies: challenged, proven and compliant

FICO has delivered optimized, TRIAD-ready strategies for credit line management (increase only, increase and decrease, and decrease only), collections and authorizations across many different markets and regulatory environments. In each case, these optimized strategies were implemented as challengers and their performance was tracked relative to the existing champion strategy.

strategic consulting for customer management

The goal of Fair Isaac® Advisors is to assist clients in identifying strategic business objectives that can be addressed in TRIAD Customer Manager. They will work collaboratively with clients to devise, define and enter challenger strategies in TRIAD Customer Manager. They keep clients apprised of industry trends and best practices to ensure strategies and solutions are best in class. The Fair Isaac Advisors team is comprised of business consultants whose expertise spans the entire credit lifecycle—originations, fraud, account and customer management, as well as collections and recoveries.

creating an actionable roadmap for improvements

Working collaboratively with the business, FICO can provide an actionable roadmap of improvements. By considering current business constraints and understanding the wider context of performance objectives (size, maturity, market, etc.), FICO can provide a prioritized list of recommendations that will include many quick wins—e.g., those that can be implemented within 90 days—along with longer-term strategies. The team can operate as part of a wider implementation of FICO tools, applications and analytics, or on a stand-alone basis to address a specific business need.

Fair Isaac® Advisors can provide guidance in industry best practices and making informed strategic decisions related to the specific business objectives of portfolios. The role of the strategy advisor is to help facilitate the use of FICO® TRIAD® Customer Manager and other adjunct products such as FICO® Blaze Advisor® business rules management system, FICO® Decision Optimizer and Decision Graph. They can help improve and expand the use of TRIAD Customer Manager and help bring account management policies, strategies and decisions to an advanced level of sophistication.

closing the customer management loop

More active use of TRIAD Customer Manager can be the first step to a much broader customer engagement strategy for an organization and FICO has a rich portfolio of solutions to help develop better customer relationships. FICO customer management solutions help with the Assess and Decide components of financial strategies related to authorizations, credit line increases or pre-delinquency. Then FICO® Customer Communication Services enable real-time consumer interactions to help the organization Act and Resolve those strategies.

For example, real-time approvals or declines can be made for an overlimit credit card transaction. If a communication of a fee is required to approve the transaction, FICO Customer Communication Services can make an interactive voice call, or send an interactive text, email or mobile application notification to alert the customer on their mobile right at the point of sale, allowing the customer to accept or decline the fee associated with the overlimit approval. For high risk accounts, an automated message can be sent to inform the customer of the situation and help reduce inbound call volume.

These two technologies can be used in several ways to deliver closed loop customer management and communication strategies that improve customer engagement and the bottom line. Here are some examples of customer management programs that can be improved:

©2014 Fair Isaac Corporation. All rights reserved. page 12

Expanding the Value of FICO® TRIAD® Customer Manager

Real-time approvals and declines and lineincreases made instantly

Assess customer’s ability to pay and communicate line changes at the right time and right place

Authorizations

Credit Facilities

Marketing Communications

Performance-BasedPricing

Collections

Reissue

Overlimit Protection

Credit LimitChanges

Target Offers

Rate and FeeManagement

Early Warning Risk

Inactive Accounts

Improve take-up rate by delivering target offers at the right time and right place

Determine and communicate fee waivers andrate changes

Send payment reminders when and wherecustomers will be most likely to see them

Stimulate card usage with the right offer at the right place and right time to the right customer

Assess

Decide

Act

Resolve

closed loop cusTomer managemenT and communicaTion sTraTegies

©2014 Fair Isaac Corporation. All rights reserved. page 13

Expanding the Value of FICO® TRIAD® Customer Manager

In this paper, a strong statistical case has been made that increased use of FICO® TRIAD® Customer Manager results in significantly better portfolio performance, regardless of the size or location of your organization. We also highlight the specific decision areas or features that can be greatly improved with TRIAD capabilities.

Becoming an active TRIAD user begins with identifying unused areas of the system that would be most beneficial to the organization. What additional decision areas can help boost profits? Are there other decision areas that will help control future delinquent losses? Which of these capabilities and benefits are relevant to your specific organization… and how do you get there from here?

Start by engaging in conversations with Fair Isaac® Advisors to discuss strategic business objectives. The roadmap provided below is meant to help you get started on the path to becoming a more active TRIAD user.

Steps to Achieving Maximum Value with TRIAD Customer Manager

fico® Triad® cusTomer manager—eighT acTive sTeps To a beTTer roadmap

This is a roadmap that can guide you through an evaluation of where you stand, and where you might want to go in expanding your customer management capabilities and beyond.

do an inventory of all the fico tools in your arsenal

• List which tools are utilized:

• FICO® Falcon® Fraud Manager

• FICO® TRIAD® Customer Manager

• FICO®BlazeAdvisor®businessrules management system

• etc.

• List which tools are not utilized.

• Do you know how to use the tools?

• Do you need training?

• Discuss with Fair Isaac® Advisors to identify potential opportunities.

do an inventory of internal resources available:

• Analytic resources

• Modeling resources

• Risk Management

• Data Warehouse

• Areas of expertise

• Where you need more help or resources

list data collection (reports, metrics, etc.) and analytical practices:

• Identify gaps

• Identify potential custom keys or custom scores development

• Discuss with Fair Isaac Advisors to identify potential opportunities

engaged fico consulting: do i know fair isaac advisors?

• Schedule on-going reviews to discuss best practices and review performance

• Create roadmap to increase activity

start with core strategies

• Assess, redevelop, deploy (start process to close gaps)

• IntegrateunusedtoolsandfeaturessuchasFICOBlaze Advisor business rules management system (to develop custom keys and scores), mid-cycle calls, linking core strategies

evaluate advanced configurable decision areas (cda) to enhance core strategies and interact with customers

• Pre-delinquency (reach out to current but risky accounts)

• TRIAD Payment Protector (stop bust-out payments)

• Product change (upgrades)

• Marketing Solicitations (direct client solicitations)

develop and deploy cda strategies

identify opportunities for optimization of core and cda strategies

• FICO® Decision Optimizer

• Custom scores (revenue, attrition, risk behavior, bankruptcy, offer response, etc.)

3 3

3

3

3

3

3

3

Expanding the Value of FICO® TRIAD® Customer Manager

Since 1980, FICO® TRIAD® Customer Manager has been a powerful asset to help retail banks and issuers increase risk-related revenue, reduce losses, automate manual processes to reduce operational costs, and reduce capital requirements. This paper shows that leveraging TRIAD Customer Manager comprehensively favorably impacts profitability measures.

It demonstrates how leveraging TRIAD Customer Manager actively leads to better account selection while lowering delinquency roll rates and charge-off balances. The combined impact of these benefits can result in tens of millions of dollars in additional profits. Approximately half of the TRIAD user population is forfeiting these substantial benefits by using only a portion of their TRIAD system’s decision support capabilities.

FICO recommends that users review the capabilities offered by TRIAD Customer Manager and explore ways to increase their usage of the product to derive more benefit with little or no incremental costs. Fair Isaac® Advisors can help build a roadmap for clients that will quickly address the areas of highest opportunity based on each client’s specific capabilities. FICO experts help train users and leverage both their FICO product expertise and deep knowledge of financial industry practices to help clients maximize their business benefits from their TRIAD system.

Beyond the immediate gains of more active TRIAD use, consider implementing additional tools for advanced analytics—which can be directly deployed in newer versions of TRIAD Customer Manager—to take customer management decisions to the highest level.

Conclusion and Recommendations

For more information North America Latin America & Caribbean Europe, Middle East & Africa Asia Pacificwww.fico.com +18883426336 +551151898222 +44(0)2079408718 +6564227700 [email protected] [email protected] [email protected] [email protected]

FICO, Fair Isaac, TRIAD, Blaze Advisor, Falcon, Model Central and “Make every decision count” are trademarks or registered trademarks of Fair Isaac Corporation in the United States and in other countries. Other product and company names herein may be trademarks of their respective owners. © 2014 Fair Isaac Corporation. All rights reserved.

3083EX 04/14 PDF

FICO (NYSE: FICO) is a leading analytics software company, helping businesses in 90+ countries make better decisions that drive higher levels of growth, profitability and customer satisfaction. The company’s groundbreaking use of Big Data and mathematical algorithms to predict consumer behavior has transformed entire industries. FICO provides analytics software and tools used across multiple industries to manage risk, fight fraud, build more profitable customer relationships, optimize operations and meet strict government regulations. Many of our products reach industry-wide adoption—such as the FICO® Score, the standard measure of consumer credit risk in the United States. FICO solutions leverage open-source standards and cloud computing to maximize flexibility, speed deployment and reduce costs. The company also helps millions of people manage their personal credit health. Learn more at www.fico.com.