Embed Size (px)

Citation preview

REGULATORY BARRIERS TO MICRO,

SMALL AND MEDIUM ENTERPRISES

ABOUT THE STUDY

Aims and Objectives

o Post- New Industrial Policy (1991) scenario: the

missing boom in the MSME sector- WHY?

o Comparative Evaluation: Business and Regulatory

Environment

Methodology

o Secondary Data Analysis

ABOUT THE STUDY

Research Question

o What have been the causes behind the inability

of MSMEs to realise their growth potential?

Hypothesis

o Given business environment; disparate growth…

Regulatory norms

serve as barriersBusiness environment:

non-conducive

LAYOUT OF THE PAPER/ PRESENTATION

o Introduction

o MSMEs v. Large Scale Industries

o Regulatory Norms

o International Comparison: EoDB Index

o Policy Recommendations

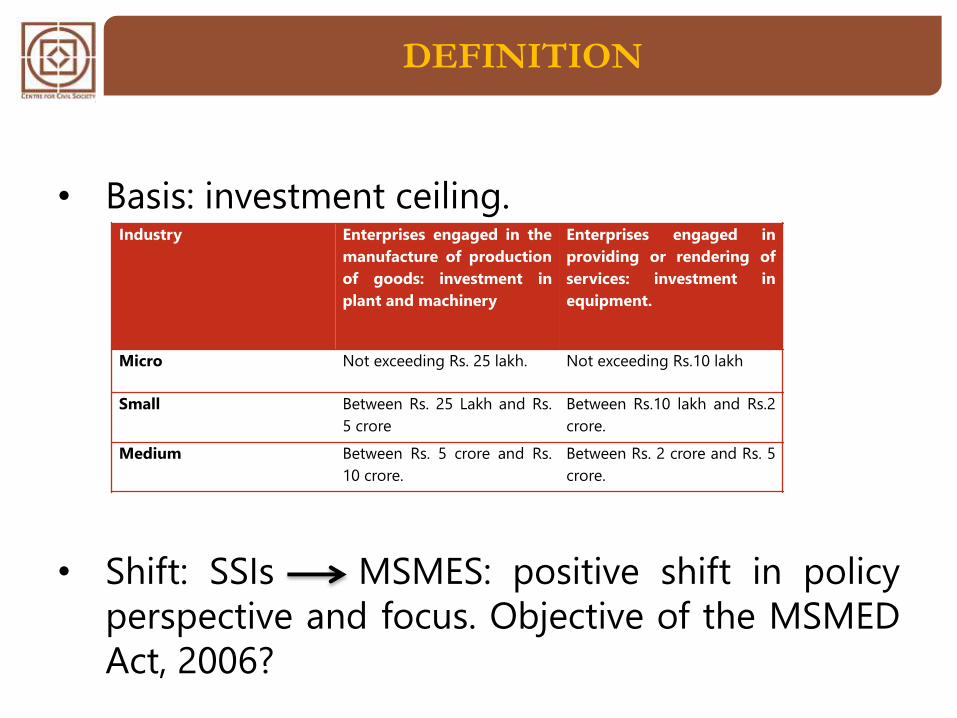

DEFINITION

• Basis: investment ceiling.

• Shift: SSIs MSMES: positive shift in policy

perspective and focus. Objective of the MSMED

Act, 2006?

Industry Enterprises engaged in the

manufacture of production

of goods: investment in

plant and machinery

Enterprises engaged in

providing or rendering of

services: investment in

equipment.

Micro Not exceeding Rs. 25 lakh. Not exceeding Rs.10 lakh

Small Between Rs. 25 Lakh and Rs.

5 crore

Between Rs.10 lakh and Rs.2

crore.

Medium Between Rs. 5 crore and Rs.

10 crore.

Between Rs. 2 crore and Rs. 5

crore.

CHALLENGES

Significance of study?

• Poor infrastructure

• Finance: lack of adequate and

timely access

• Marketing

• Regulatory norms: 142nd on the

EoDB

• Tax structure: number of

payments, procedure

• Lack of information flow

• Innovation/ R&D: missing

• Labour: Availability of skilled

and productive force

• Corruption

• Lumping MSMEs together:

POLICY PERSPECTIVE

CHALLENGE.

LARGE v. SMALL ENTERPRISES: POST 1991

What does liberalisation do?

o Access to capital/ technology + freedom to invest in

domestic industries = increased competition, creative

destruction/ innovation.

o Factors get reallocated as per productivity, with

inefficient firms driving out the inefficient ones- leads to

increased overall productivity and growth in the

economy.

LARGE v. SMALL ENTERPRISES: POST 1991

What did liberalisation do for MSMEs?

• Total working MSME units: 105.21 lakh (2001-02) v.

447.73 lakh (2011-12).

• Alteration in institutional arrangement: dereservation of

products for MSMEs; increased competition with the

large scale sector.

• Induction into a competitive environment proved too

sudden for MSMEs (given lack of capital, marketing

opportunities, innovation, skilled workforce); OUTCOME:

Sick units: 0.2 million (1990) v. 0.3 million (2000)/ Rate of

exports: 31% to 18%.

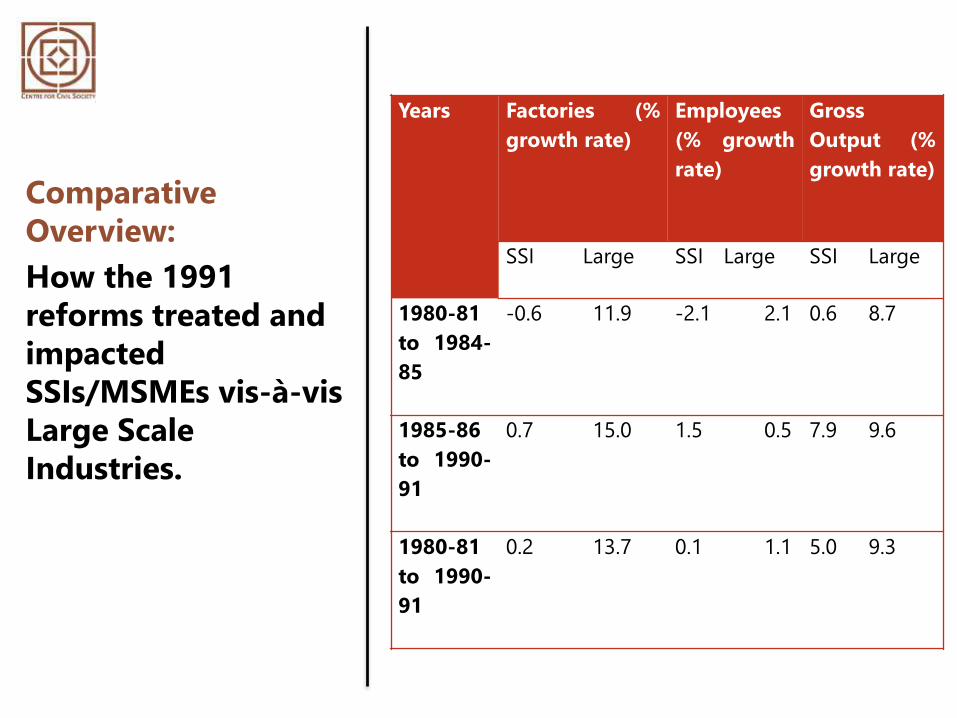

Comparative

Overview:

How the 1991

reforms treated and

impacted

SSIs/MSMEs vis-à-vis

Large Scale

Industries.

Years Factories (%

growth rate)

Employees

(% growth

rate)

Gross

Output (%

growth rate)

SSI Large SSI Large SSI Large

1980-81

to 1984-

85

-0.6 11.9 -2.1 2.1 0.6 8.7

1985-86

to 1990-

91

0.7 15.0 1.5 0.5 7.9 9.6

1980-81

to 1990-

91

0.2 13.7 0.1 1.1 5.0 9.3

DOCUMENTATION AND ANALYSIS OF

REGULATORY NORMS

Entry Continuance Exit

ENTRY

Registration

• PROCESS: S. 8(1), MSMED Act. Optional. Manufacturing: Memorandum of

Registration is mandatory.

• ADVANTAGE: Registration ensures the minimum financial interest of the seller

(the MSME owner)- that is, the price for his goods.

Licensing

• Licensing Exemption Notification (1991) under the IDR Act, 1951: no industrial

license required except in case of 6 product groups included in the compulsory

licensing group.

• Item groups reserved for exclusive manufacture by MSMEs.

PROCEDURAL NORMS (ENTRY)

• More significant than statutory stipulations in

terms of the hindrance they can potentially

pose: tedious and protracted nature.

• Starting a business: 11 associated procedures

(Delhi); 13 (Mumbai).

• Acquiring a construction permit: 27 steps/

procedures.

• Registering property (for the purpose of use as

a warehouse, for instance): 7 steps/ procedures.

ANALYSIS OF NORMS (ENTRY)

• Simplification of the registration process;

• Statutory protection to the financial interest of

the MSME owner;

• Minimal licensing obligations;

• Procedural barriers.

CONTINUANCE

Financing

• Outstanding credit gap (beginning of the 12th

plan period): 62% of the credit demand; total

credit demand for micro enterprises = INR 7.9

trillion (2012)!

• Availability of bank credit is low; credit to

MSMEs as a % of NBC: 14.6% (2000) to 8%

(2007).

• Master circular, RBI (2010): guidelines for

lending to MSMEs; targets?; specialised

branches.

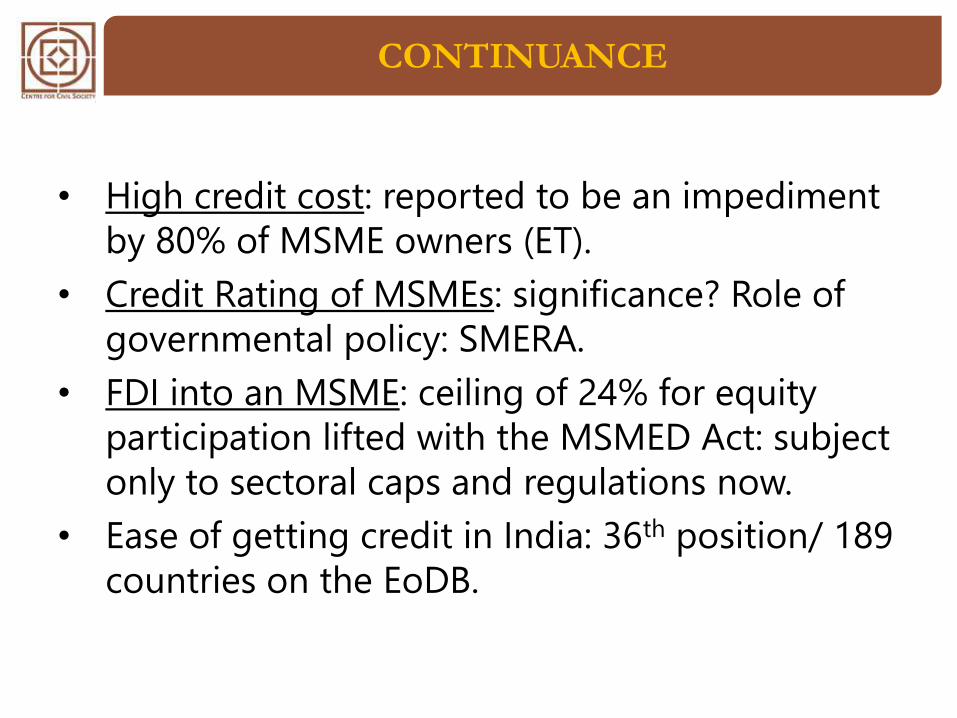

CONTINUANCE

• High credit cost: reported to be an impediment

by 80% of MSME owners (ET).

• Credit Rating of MSMEs: significance? Role of

governmental policy: SMERA.

• FDI into an MSME: ceiling of 24% for equity

participation lifted with the MSMED Act: subject

only to sectoral caps and regulations now.

• Ease of getting credit in India: 36th position/ 189

countries on the EoDB.

CONTINUANCE

Labour

• Concurrent List subject- 44 central enactments:

industrial relations, industrial safety and health,

child and women labour, social security, labour

welfare, employment and training, wages,

others.: irrelevant to the MSME sector.

• Lack of skilled labour.

CONTINUANCE

Taxation

• Concerns: Number of payments, long

procedure, non-uniformity across states (World

Bank): 33 annual tax payments; 243 hours/ year

spent in filing; tax payment amounts to 61.7% of

profit. India = 156th of 189 countries.

Tax Benefits, Schemes and Incentives for the

MSME Sector

• Deduction in respect of profit and gains:

ambiguity as to definition of SSIs

• Excise exemption

• Presumptive taxation

ANALYSIS OF NORMS (CONTINUANCE)

• Increasing availability of credit: positive role of

the RBI

• Betterment in FDI policy towards MSMEs

• Balancing labour interests with regulatory

framework: avoiding ‘over-legislation’

• Redundancy/ Inapplicability of labour laws

• Protracted procedure for tax payments

• Ambiguity as to definition of SSIs for tax

purposes

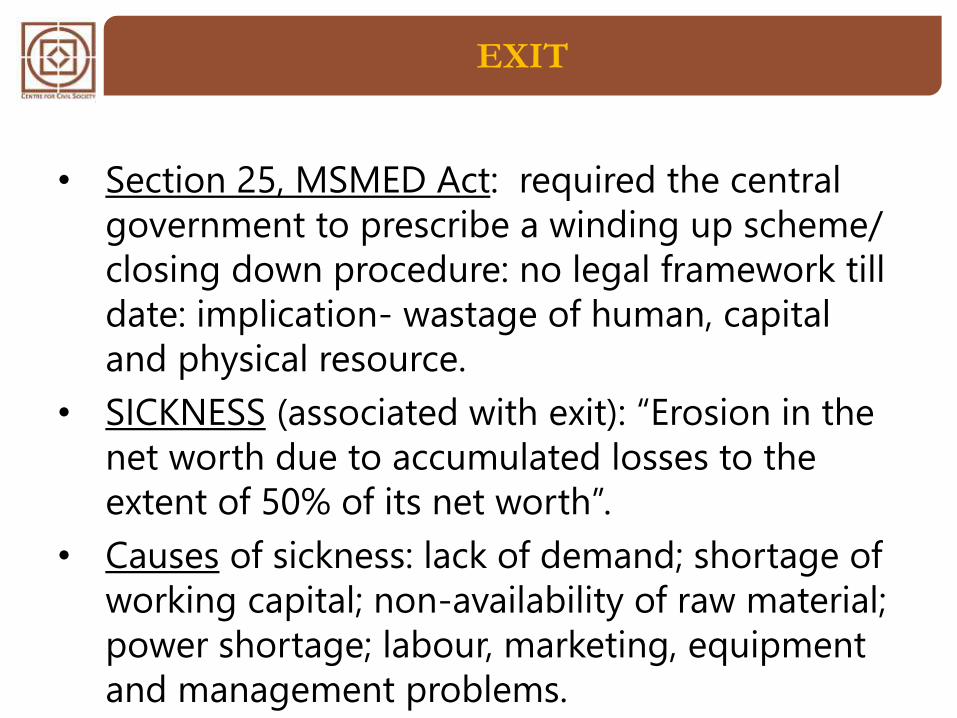

EXIT

• Section 25, MSMED Act: required the central

government to prescribe a winding up scheme/

closing down procedure: no legal framework till

date: implication- wastage of human, capital

and physical resource.

• SICKNESS (associated with exit): “Erosion in the

net worth due to accumulated losses to the

extent of 50% of its net worth”.

• Causes of sickness: lack of demand; shortage of

working capital; non-availability of raw material;

power shortage; labour, marketing, equipment

and management problems.

EXIT

• Revival of sick units- not a priority for banks-

conflicting interests.

• Presidency Towns Insolvency Act (1909)/

Provisional Insolvency Act (1920): disregard the

concept of limited liability; focus of litigation:

reovering statutory dues; not revival of the

MSME unit. LLP Act, 2008.

ANALYSIS OF NORMS (EXIT)

• Rehabilitation and resolving insolvency

measures to be aimed at revival

• Legal framework for exit

INTERNATIONAL COMPARISON

How does the EoDB Index

work?

o A composite of 2 measures:

• DTF Score

• EoDB Ranking

Indicators

• Starting a Business

• Construction Permits

• Getting Electricity

• Registering Property

• Getting Credit

• Protecting Minority

Investors

• Paying Taxes

• Trading Across Borders

• Resolving Insolvency

EoDB: Business

Environment in

India

Comparison with

China, Russia,

Bangladesh

Relevance of the EoDB for MSMEs

A comprehensive measure of how easy/

difficult it is for a local entrepreneur to

open and run a small to medium-sized

enterprise when complying with relevant

regulations.

Where does India Stand?

5

5

2

3

1

1

5

2

4

3

DB TOPIC/

PARAMETER

DB RANK

2015/2014

ALONG THE

TOPIC

DISTANCE TO

FRONTIER

SCORES

2015/2014

Starting a Business 158/ 156 (-2) 68.4/ 65.54

(+2.88)

Dealing with

Construction

Permits

184/183 (-1) 30.89/ 29.70

(+1.19)

Getting Electricity 137/ 134 (-3) 63.06/ 62.55

(+0.51)

Registering

Property

121/115 (-6) 60.40/ 60.40 (-)

Getting Credit 36/ 30 (-6) 65.00/ 65.00 (-)

Protecting

Minority Investors

7/ 21 (+14) 72.50/ 65.83

(+6.67)

Paying Taxes 156/ 154 (-2) 55.53/ 55.64 (-

0.11)

Trading Across

Borders

126/ 122 (-4) 65.47/ 64.89

(+0.58)

Enforcing

Contracts

186/ 18 (-) 25.81/ 25.81 (-)

Resolving

Insolvency

137/ 135 (-2) 32.60/ 32.43

(+0.17)

POLICY RECOMMENDATIONS

Drawing up a distinction

between micro, small and

medium enterprises at a policy

level

Starting a business:

minimisation of procedural

compliances required

Better monitoring mechanism

with respect to finance for

MSMEs

Simplification of labour

regulatory framework

Inclusive method of

checking compliance

with regulatory norms

Taxation: Need for

simpler procedure and

non-ambiguity in laws

Addressing lack of

awareness

Legal framework for an

exit scheme