Embed Size (px)

Citation preview

Master in International business for small

and medium enterprises - MIBS

International Accounting

Michele Fabrizi

Master in International business for small

and medium enterprises - MIBS

Measuring and reporting cash flows

MIBSObjectives

• Discuss the crucial importance of cash to a business

• Explain the nature of cash flow statement and discuss how it can be helpful in identifying cash flow problems

• Prepare a cash flow statement

• Interpret a cash flow statement

MIBS

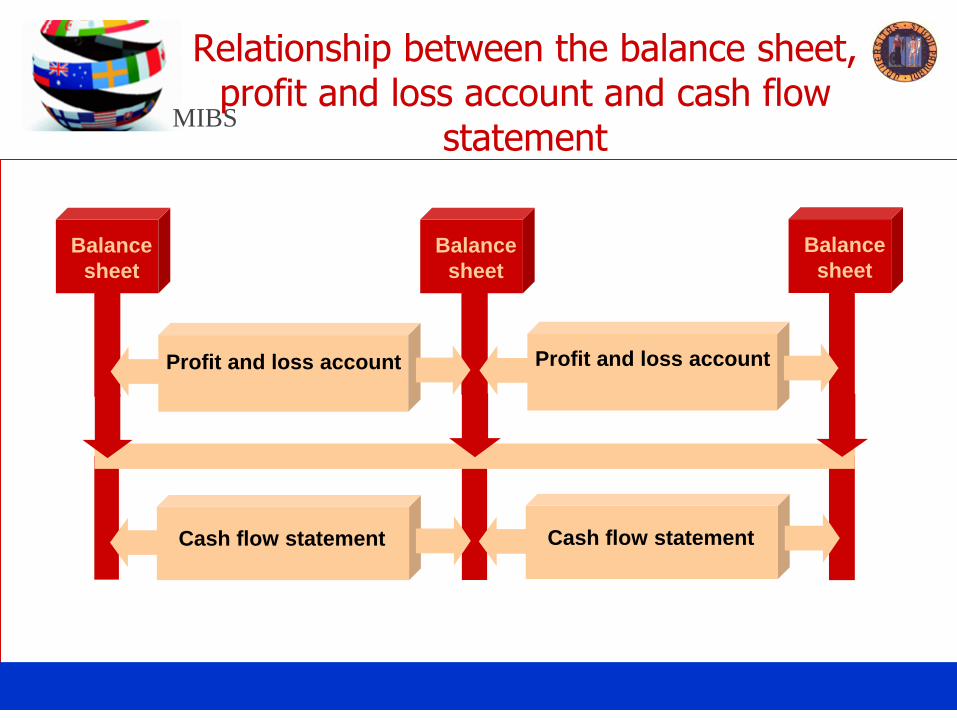

Relationship between the balance sheet, profit and loss account and cash flow

statement

Profit and loss account

Cash flow statement

Balance

sheet

Balance

sheet

Balance

sheet

Profit and loss account

Cash flow statement

MIBS

State the increase, decrease or no effect on both cash and profit for the following business events:

1. Repayment of a loan 2. Making a sale on credit3. Buying a fixed asset on credit4. Receiving cash from a trade debtor5. Depreciating a fixed asset6. Buying stock for cash7. Making a share issue for cash

Activity 6.2

MIBS

(what is) the cash flow statement

• Summary of the cash receipts and payments over the period concern

• All receipts and payments of a particular type are added together to give just one figure that appears in the statement

• The net total of the statement is the net increase or decrease of the cash of the business over the period

• The C/F statement is now accepted, along with P/L and B/S, as a primary financial statement

MIBS

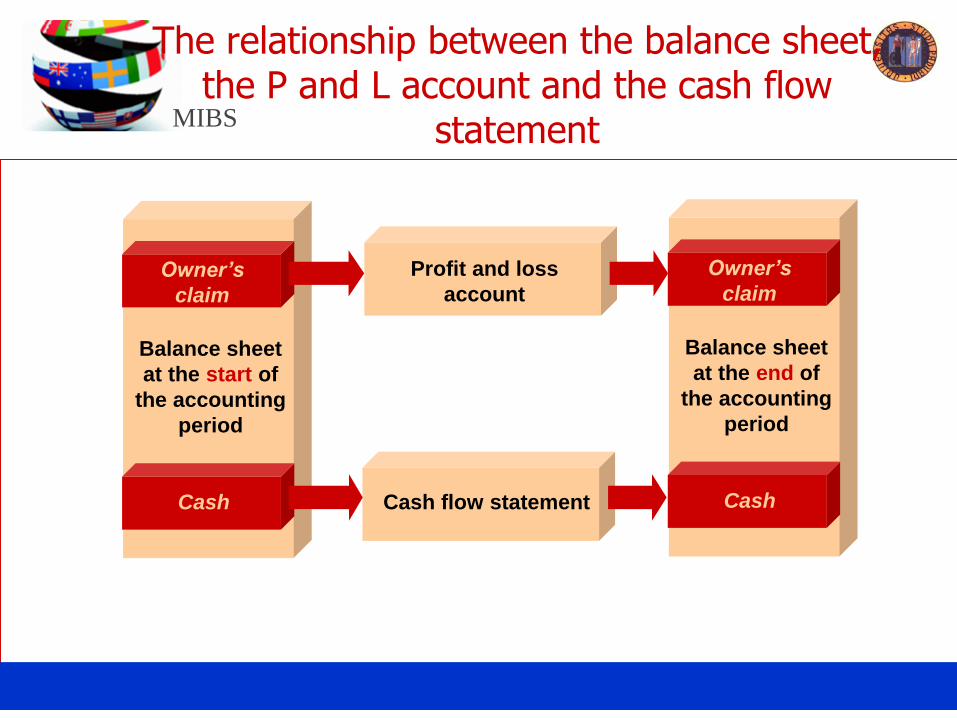

The relationship between the balance sheet, the P and L account and the cash flow

statement

Balance sheet

at the start of

the accounting

period

Owner’s

claim

Cash

Balance sheet

at the end of

the accounting

period

Owner’s

claim

CashCash flow statement

Profit and loss

account

MIBS

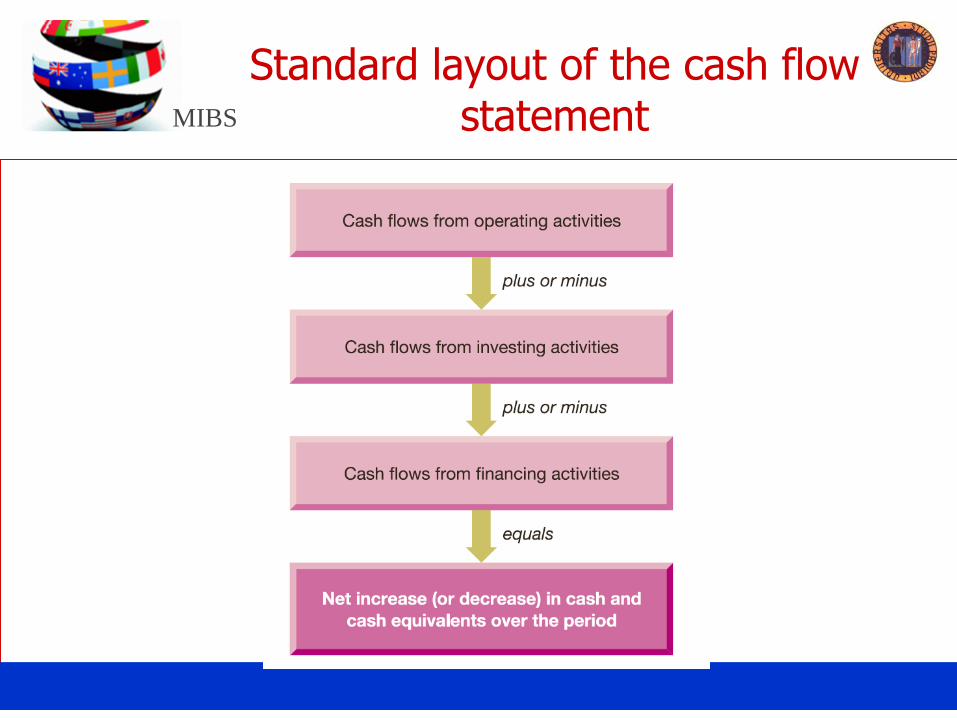

Standard layout of the cash flow statement

MIBS

Diagrammatical representation of the cash flow statement

MIBS

Deducing net cash (in)flows from operating activities

• The direct method involves the analysis of the cash records of the business for the period, picking out all payments and receipts relating to operating activities. Not many businesses adopt this approach.

• The indirect method derives the cash flow statement from profit and loss account and from balance sheet. It is the most popular method.

MIBS

Deducing net cash (in)flows from operating activities

Cash From Sales = Sales - ∆ trade receivables

MIBS

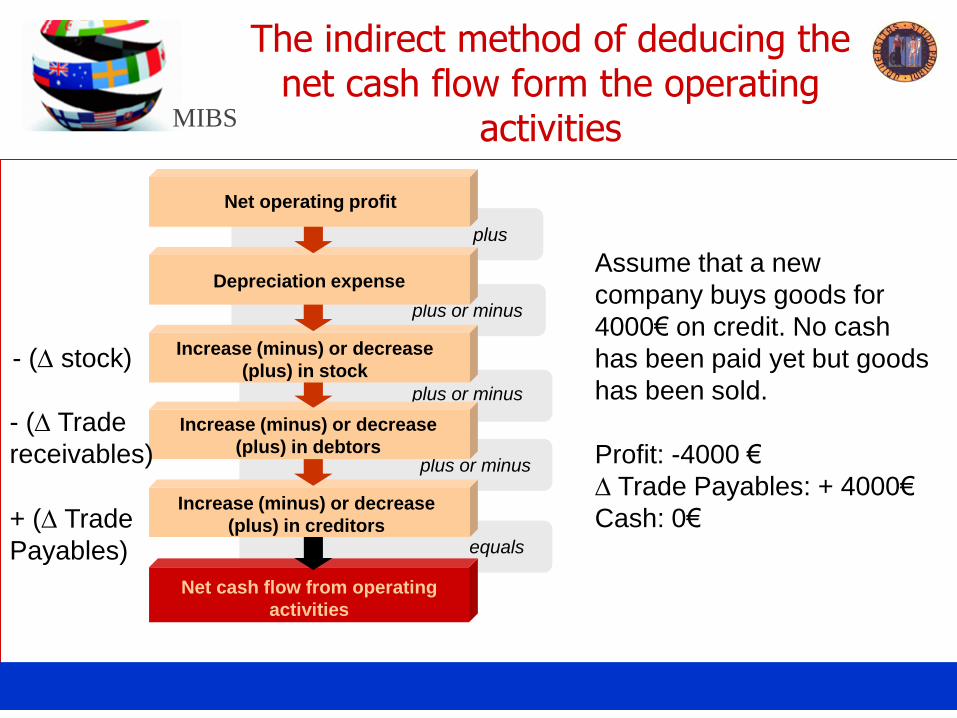

The indirect method of deducing the net cash flow form the operating

activities

plus

plus or minus

equals

plus or minus

plus or minus

Net cash flow from operating

activities

Net operating profit

Depreciation expense

Increase (minus) or decrease

(plus) in stock

Increase (minus) or decrease

(plus) in debtors

Increase (minus) or decrease

(plus) in creditors

- (D stock)

- (D Trade

receivables)

+ (D Trade

Payables)

MIBS

The indirect method of deducing the net cash flow form the operating

activities

plus

Net operating profit

Depreciation expense

These costs are not

monetary! They do not

imply a cash outflow!

MIBS

The indirect method of deducing the net cash flow form the operating

activities

plus

Net operating profit

Depreciation expense

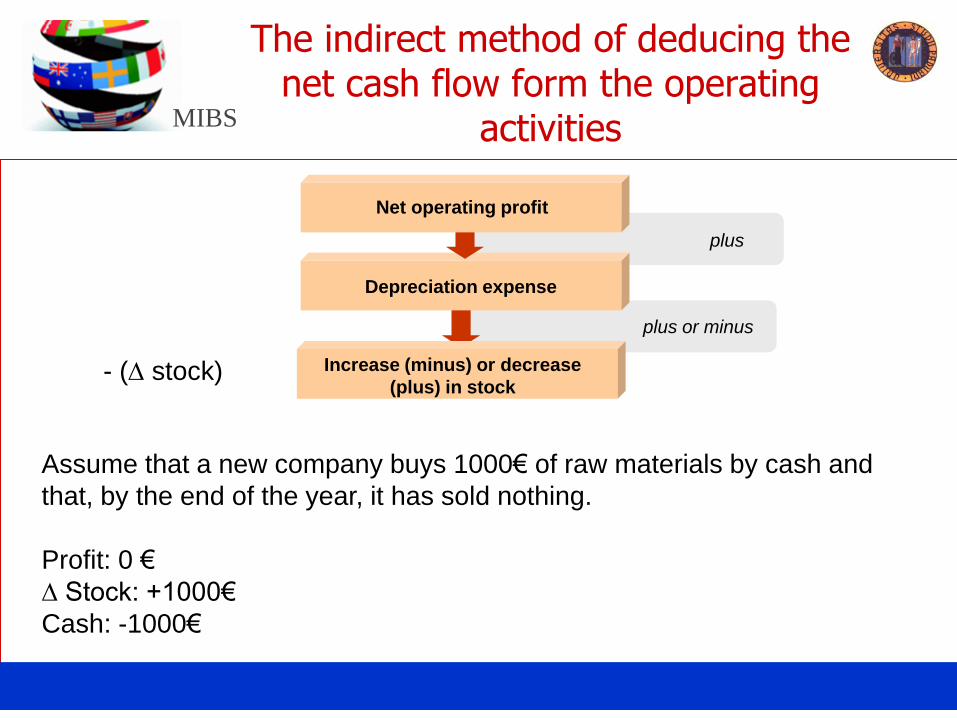

Assume that a new company buys 1000€ of raw materials by cash and

that, by the end of the year, it has sold nothing.

Profit: 0 €

∆ Stock: +1000€

Cash: -1000€

plus or minus

Increase (minus) or decrease

(plus) in stock- (D stock)

MIBS

The indirect method of deducing the net cash flow form the operating

activities

plus

Net operating profit

Depreciation expense

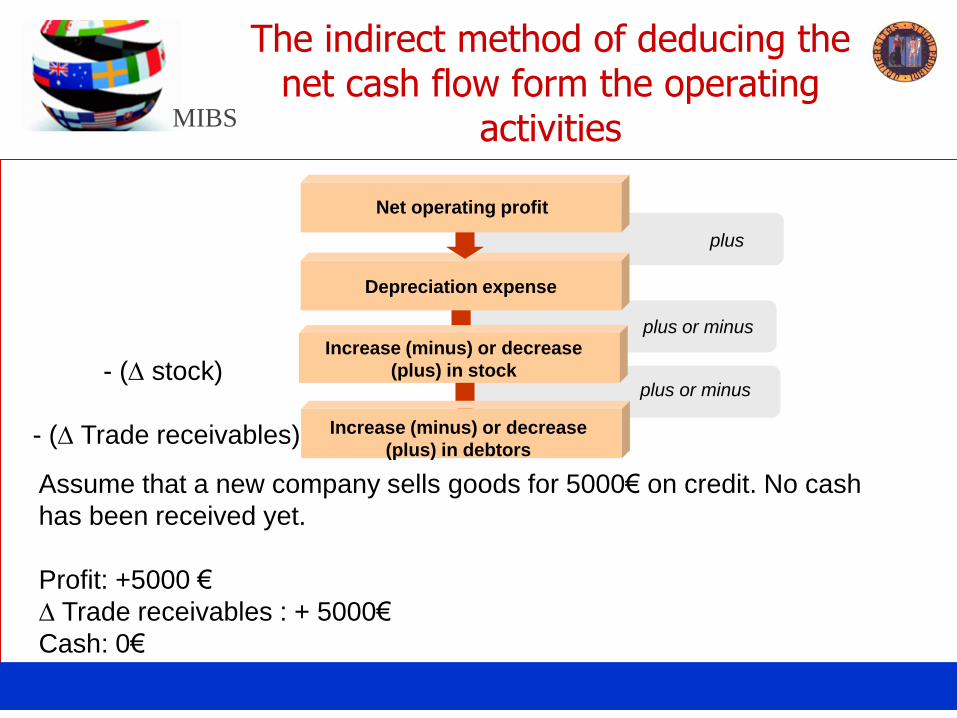

plus or minusIncrease (minus) or decrease

(plus) in stock- (D stock)plus or minus

Increase (minus) or decrease

(plus) in debtors- (D Trade receivables)

Assume that a new company sells goods for 5000€ on credit. No cash

has been received yet.

Profit: +5000 €

∆ Trade receivables : + 5000€

Cash: 0€

MIBS

The indirect method of deducing the net cash flow form the operating

activities

plus

plus or minus

equals

plus or minus

plus or minus

Net cash flow from operating

activities

Net operating profit

Depreciation expense

Increase (minus) or decrease

(plus) in stock

Increase (minus) or decrease

(plus) in debtors

Increase (minus) or decrease

(plus) in creditors

- (D stock)

- (D Trade

receivables)

+ (D Trade

Payables)

Assume that a new

company buys goods for

4000€ on credit. No cash

has been paid yet but goods

has been sold.

Profit: -4000 €

∆ Trade Payables: + 4000€

Cash: 0€

MIBS

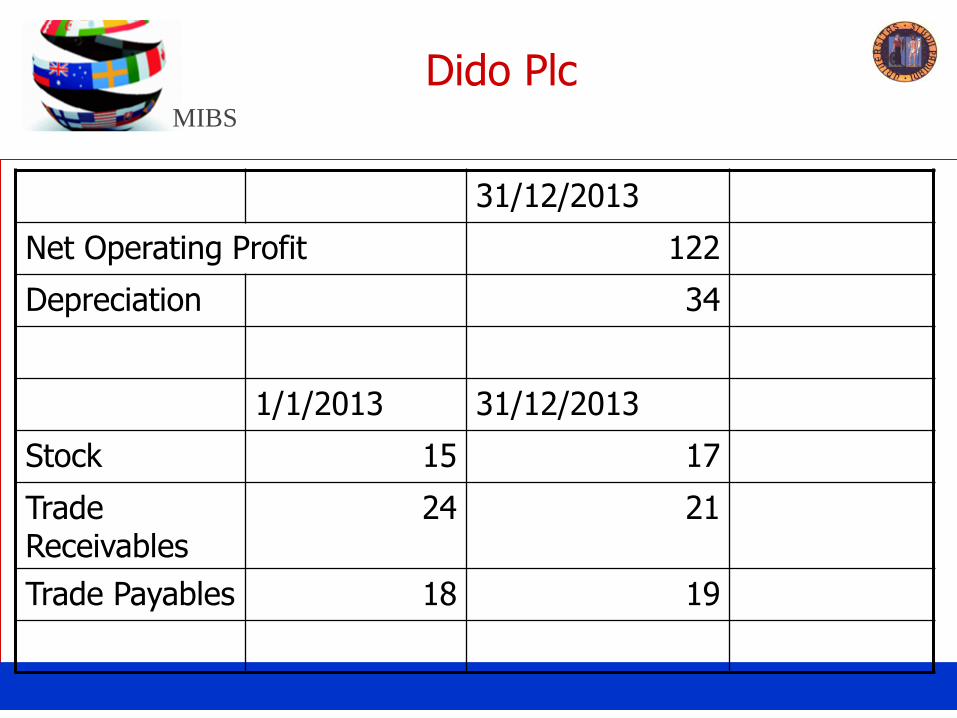

Dido Plc

31/12/2013

Net Operating Profit 122

Depreciation 34

1/1/2013 31/12/2013

Stock 15 17

TradeReceivables

24 21

Trade Payables 18 19

MIBS

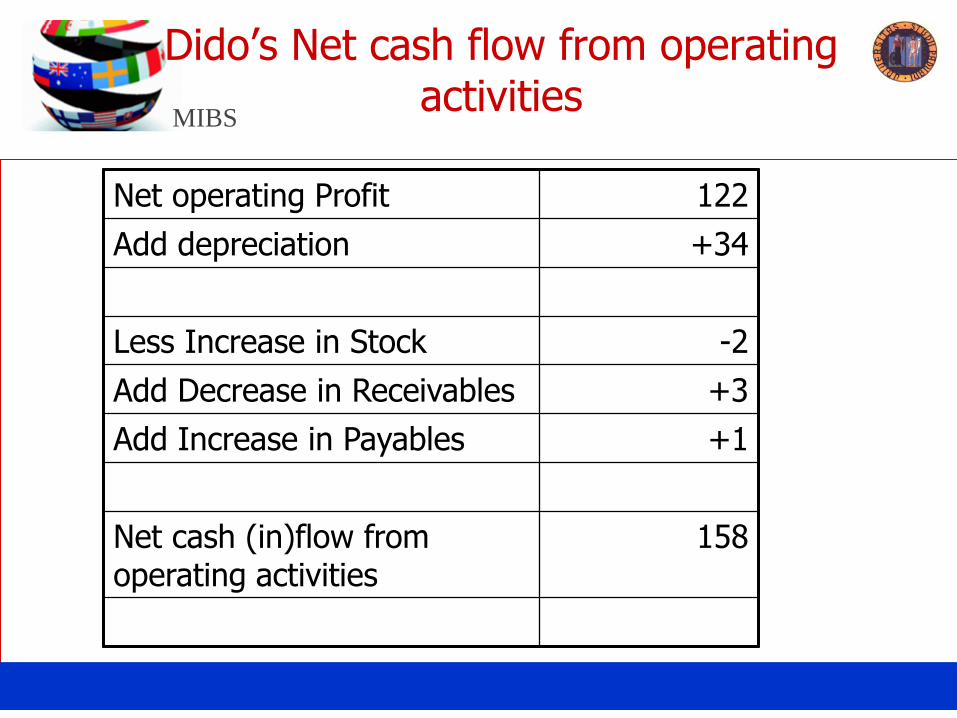

Dido’s Net cash flow from operating activities

Net operating Profit 122

Add depreciation +34

Less Increase in Stock -2

Add Decrease in Receivables +3

Add Increase in Payables +1

Net cash (in)flow from operating activities

158