Embed Size (px)

Citation preview

MinEx Consulting Strategic advice on mineral economics & exploration

The Importance of the Junior Sector

for mineral discovery in NSW Richard Schodde Managing Director, MinEx Consulting Adjunct Professor, University of Western Australia

Keynote presentation to the Exploration in the House 2015 16th June 2015, Sydney

MinEx Consulting Strategic advice on mineral economics & exploration

Overview

1. The long wave of history … NSW’s contribution to Australia’s mining heritage

2. Trends in exploration spend 3. Number of discoveries made 4. Location of recent discoveries in NSW 5. Discovery performance … NSW versus Australia

6. Who made the discoveries ? … importance of Junior Explorers

7. Current financial situation for Junior Explorers in NSW 8. Outlook for mining in NSW … urgent need to find and develop new projects

9. Summary / Conclusions

2

MinEx Consulting Strategic advice on mineral economics & exploration

1. THE LONG WAVE OF HISTORY Over the last 160 years Australia has gone through several waves of discovery

3

MinEx Consulting Strategic advice on mineral economics & exploration

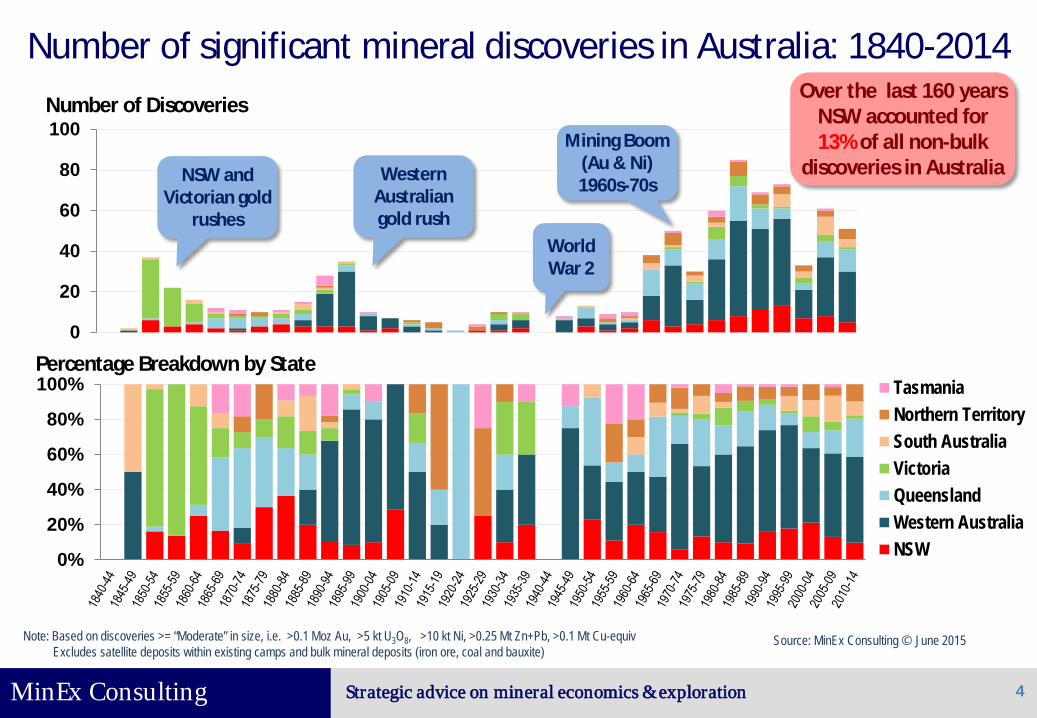

Number of significant mineral discoveries in Australia: 1840-2014

0

20

40

60

80

100

4

0%

20%

40%

60%

80%

100% TasmaniaNorthern TerritorySouth AustraliaVictoriaQueenslandWestern AustraliaNSW

NSW and Victorian gold

rushes

Western Australian gold rush

World War 2

Mining Boom (Au & Ni) 1960s-70s

Number of Discoveries

Percentage Breakdown by State

Note: Based on discoveries >= “Moderate” in size, i.e. >0.1 Moz Au, >5 kt U3O8, >10 kt Ni, >0.25 Mt Zn+Pb, >0.1 Mt Cu-equiv Excludes satellite deposits within existing camps and bulk mineral deposits (iron ore, coal and bauxite)

Source: MinEx Consulting © June 2015

Over the last 160 years NSW accounted for 13% of all non-bulk

discoveries in Australia

MinEx Consulting Strategic advice on mineral economics & exploration

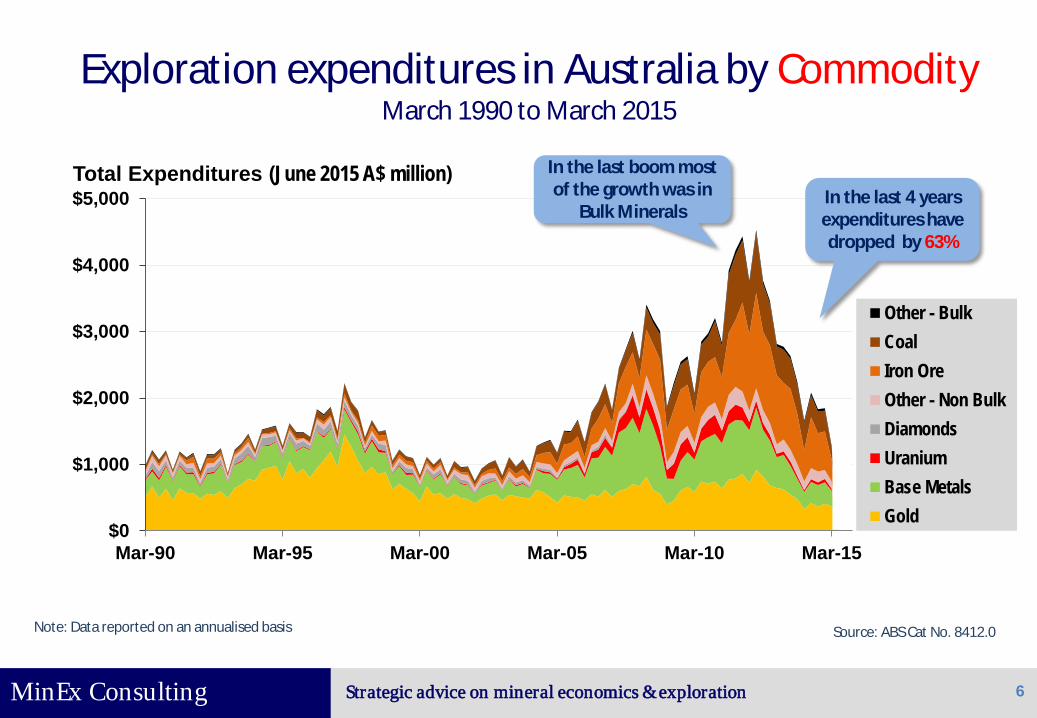

2. TRENDS IN EXPLORATION SPEND Exploration expenditures in Australia reached an all-time high in 2012

5

MinEx Consulting Strategic advice on mineral economics & exploration

$0

$1,000

$2,000

$3,000

$4,000

$5,000

Mar-90 Mar-95 Mar-00 Mar-05 Mar-10 Mar-15

Other - BulkCoalIron OreOther - Non BulkDiamondsUraniumBase MetalsGold

6

Source: ABS Cat No. 8412.0 Note: Data reported on an annualised basis

Total Expenditures (June 2015 A$ million) In the last boom most of the growth was in

Bulk Minerals

Exploration expenditures in Australia by Commodity March 1990 to March 2015

In the last 4 years expenditures have dropped by 63%

MinEx Consulting Strategic advice on mineral economics & exploration

$0

$1,000

$2,000

$3,000

$4,000

$5,000

Mar-90 Mar-95 Mar-00 Mar-05 Mar-10 Mar-15

Other - Non BulkDiamondsUraniumBase MetalsGold

7

Source: ABS Cat No. 8412.0 Note: Data reported on an annualised basis

Total Expenditures (June 2015 A$ million)

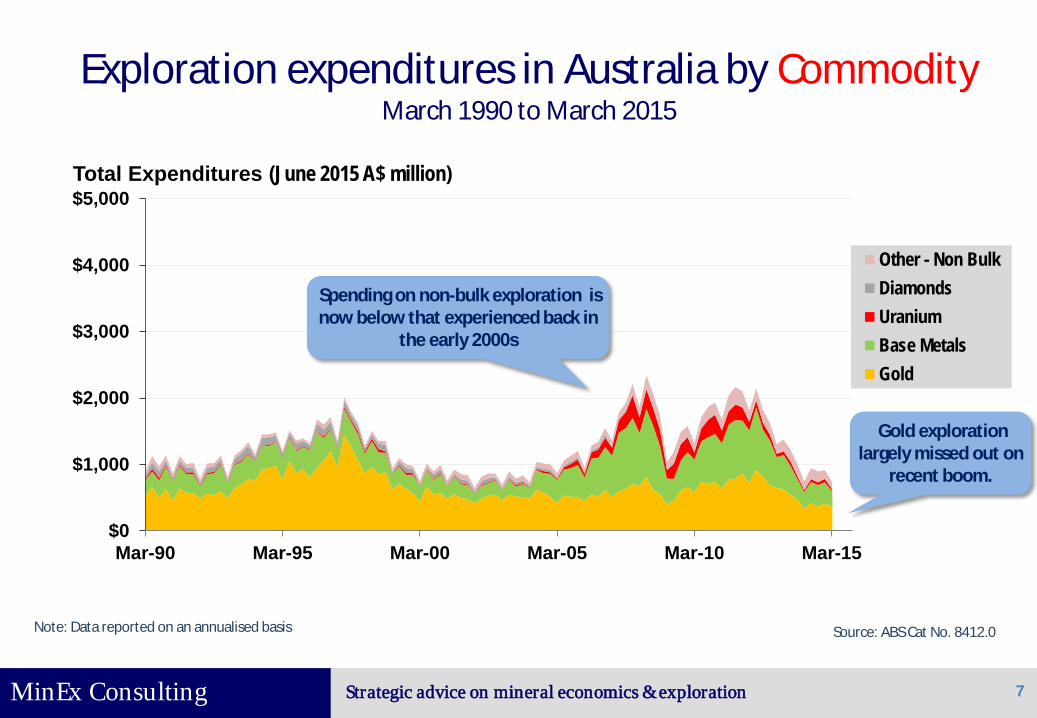

Exploration expenditures in Australia by Commodity March 1990 to March 2015

Spending on non-bulk exploration is now below that experienced back in

the early 2000s

Gold exploration largely missed out on

recent boom.

MinEx Consulting Strategic advice on mineral economics & exploration

$0

$1,000

$2,000

$3,000

$4,000

$5,000

Mar-90 Mar-95 Mar-00 Mar-05 Mar-10 Mar-15

Western AustraliaQueenslandTasmaniaVictoriaNorthern TerritorySouth AustraliaNSW

8

Source: ABS 8412

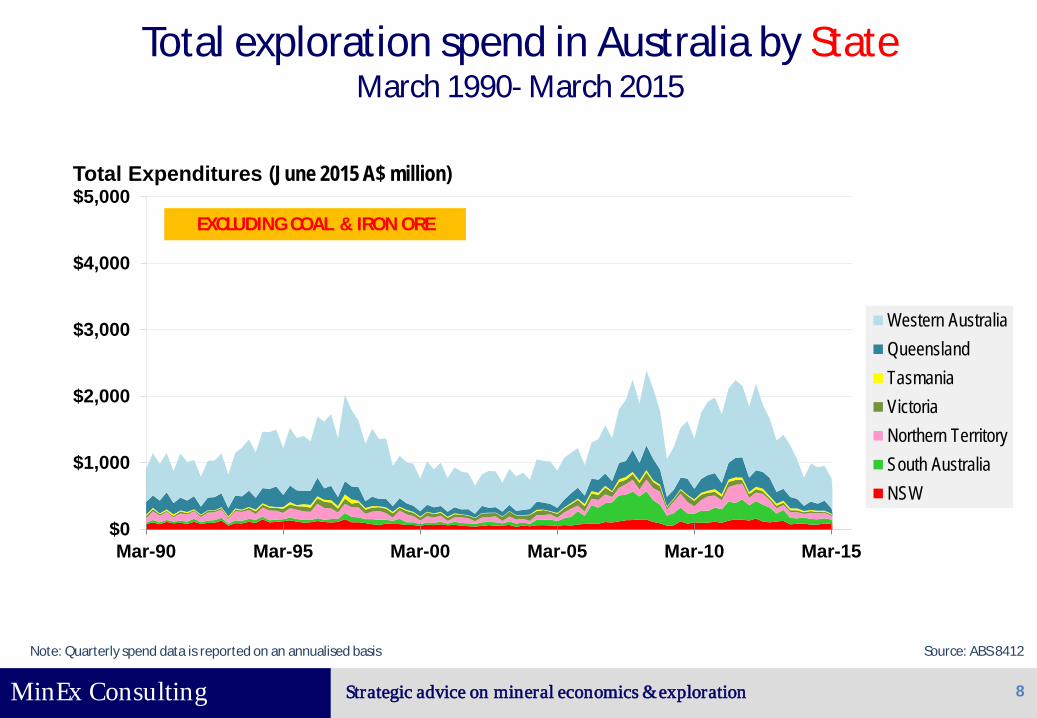

Total exploration spend in Australia by State March 1990- March 2015

Note: Quarterly spend data is reported on an annualised basis

Total Expenditures (June 2015 A$ million)

EXCLUDING COAL & IRON ORE

MinEx Consulting Strategic advice on mineral economics & exploration

0%

20%

40%

60%

80%

100%

Mar-90 Mar-95 Mar-00 Mar-05 Mar-10 Mar-15

Western AustraliaQueenslandTasmaniaVictoriaNorthern TerritorySouth AustraliaNSW

9

Source: ABS 8412

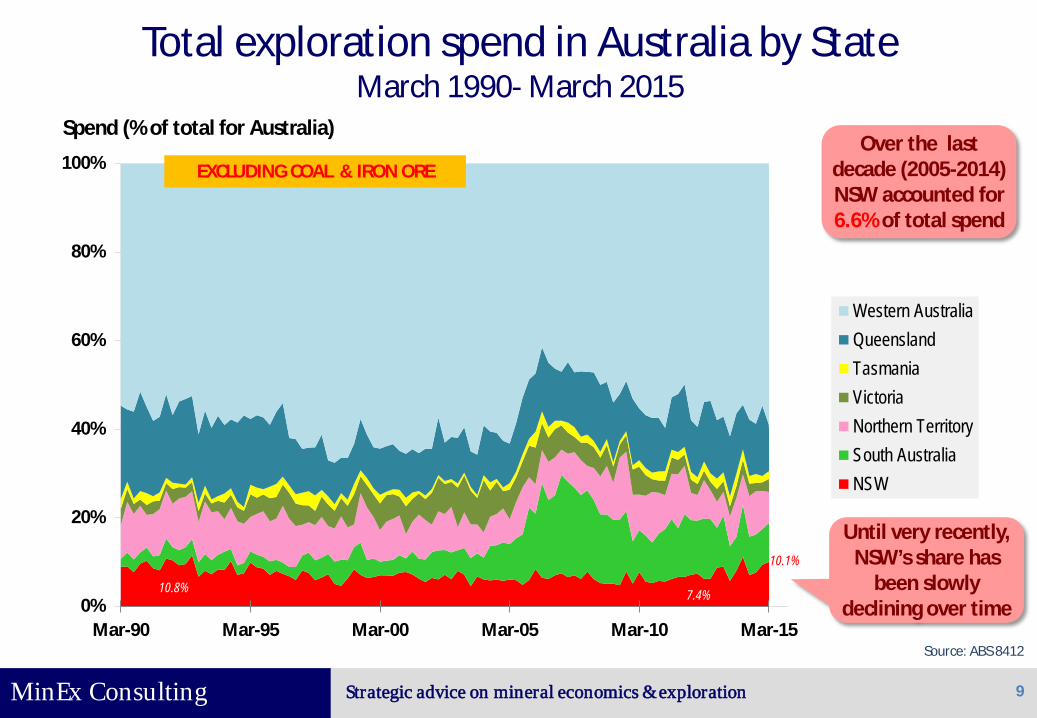

Total exploration spend in Australia by State March 1990- March 2015

Spend (% of total for Australia)

Until very recently, NSW’s share has

been slowly declining over time

7.4% 10.8%

Over the last decade (2005-2014) NSW accounted for 6.6% of total spend

10.1%

EXCLUDING COAL & IRON ORE

MinEx Consulting Strategic advice on mineral economics & exploration

3. NUMBER OF DISCOVERIES MADE In the last decade NSW accounted for 12% of all discoveries made in Australia

10

MinEx Consulting Strategic advice on mineral economics & exploration

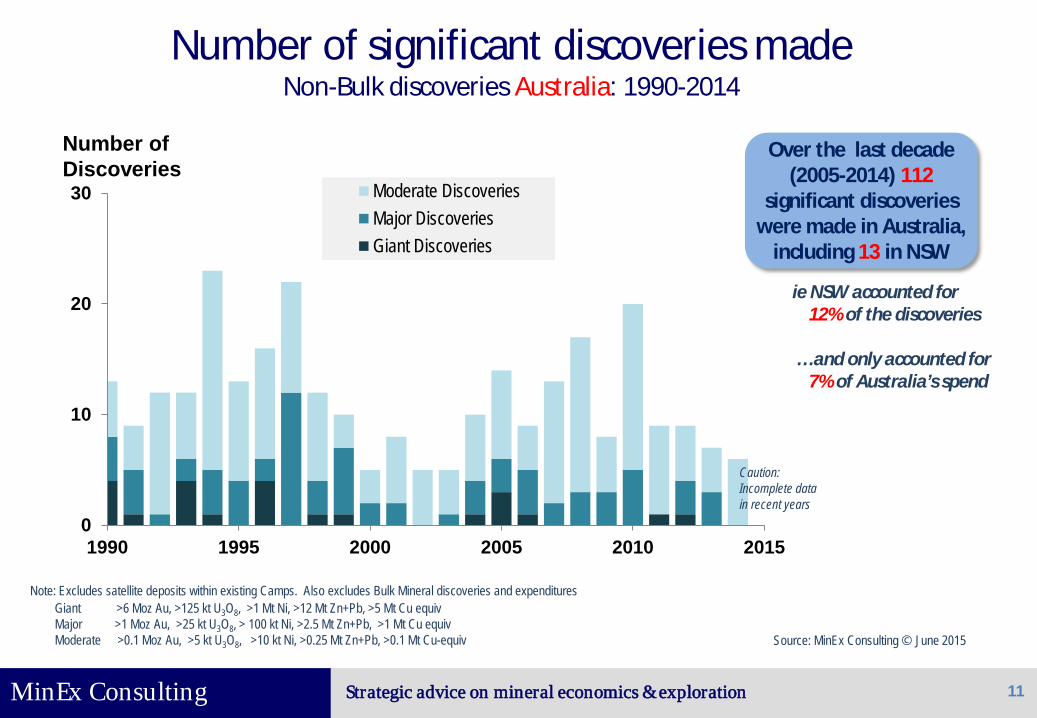

Number of significant discoveries made Non-Bulk discoveries Australia: 1990-2014

0

10

20

30

1990 1995 2000 2005 2010 2015

Moderate DiscoveriesMajor DiscoveriesGiant Discoveries

11

Number of Discoveries

Source: MinEx Consulting © June 2015

Over the last decade (2005-2014) 112

significant discoveries were made in Australia,

including 13 in NSW

ie NSW accounted for 12% of the discoveries … and only accounted for 7% of Australia’s spend

Note: Excludes satellite deposits within existing Camps. Also excludes Bulk Mineral discoveries and expenditures Giant >6 Moz Au, >125 kt U3O8, >1 Mt Ni, >12 Mt Zn+Pb, >5 Mt Cu equiv

Major >1 Moz Au, >25 kt U3O8, > 100 kt Ni, >2.5 Mt Zn+Pb, >1 Mt Cu equiv Moderate >0.1 Moz Au, >5 kt U3O8, >10 kt Ni, >0.25 Mt Zn+Pb, >0.1 Mt Cu-equiv

Caution: Incomplete data in recent years

MinEx Consulting Strategic advice on mineral economics & exploration

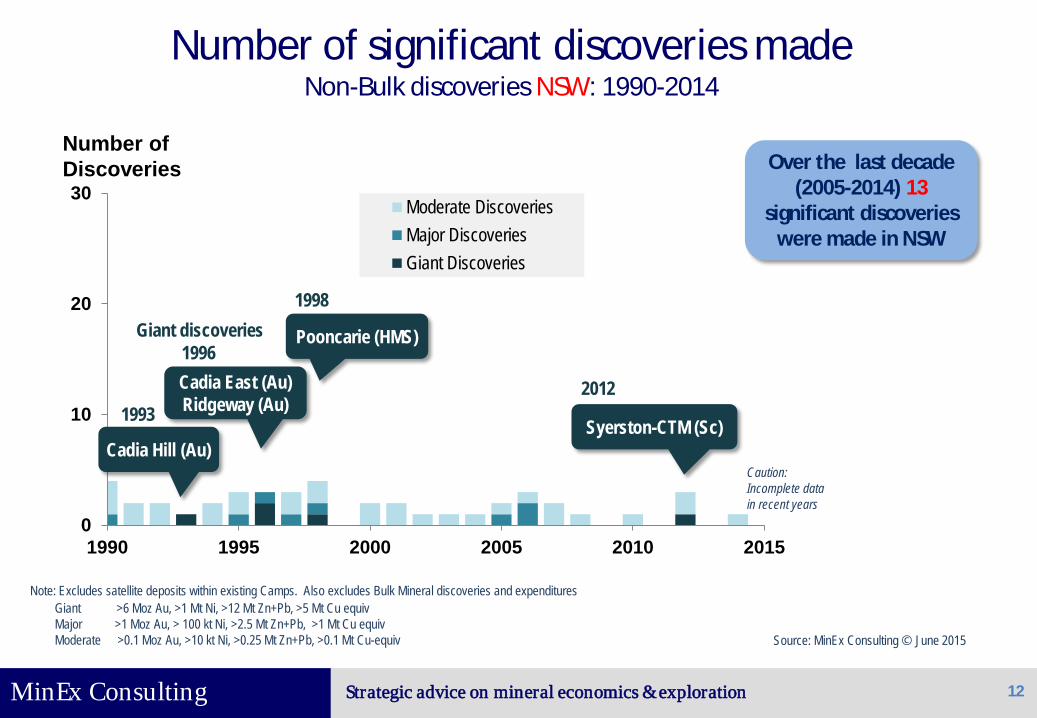

Number of significant discoveries made Non-Bulk discoveries NSW: 1990-2014

0

10

20

30

1990 1995 2000 2005 2010 2015

Moderate DiscoveriesMajor DiscoveriesGiant Discoveries

12

Number of Discoveries

Note: Excludes satellite deposits within existing Camps. Also excludes Bulk Mineral discoveries and expenditures

Source: MinEx Consulting © June 2015

Over the last decade (2005-2014) 13

significant discoveries were made in NSW

Caution: Incomplete data in recent years

Syerston-CTM (Sc) Cadia Hill (Au)

Cadia East (Au) Ridgeway (Au)

Pooncarie (HMS) Giant discoveries

2012

1998

1996

1993

Giant >6 Moz Au, >1 Mt Ni, >12 Mt Zn+Pb, >5 Mt Cu equiv Major >1 Moz Au, > 100 kt Ni, >2.5 Mt Zn+Pb, >1 Mt Cu equiv Moderate >0.1 Moz Au, >10 kt Ni, >0.25 Mt Zn+Pb, >0.1 Mt Cu-equiv

MinEx Consulting Strategic advice on mineral economics & exploration

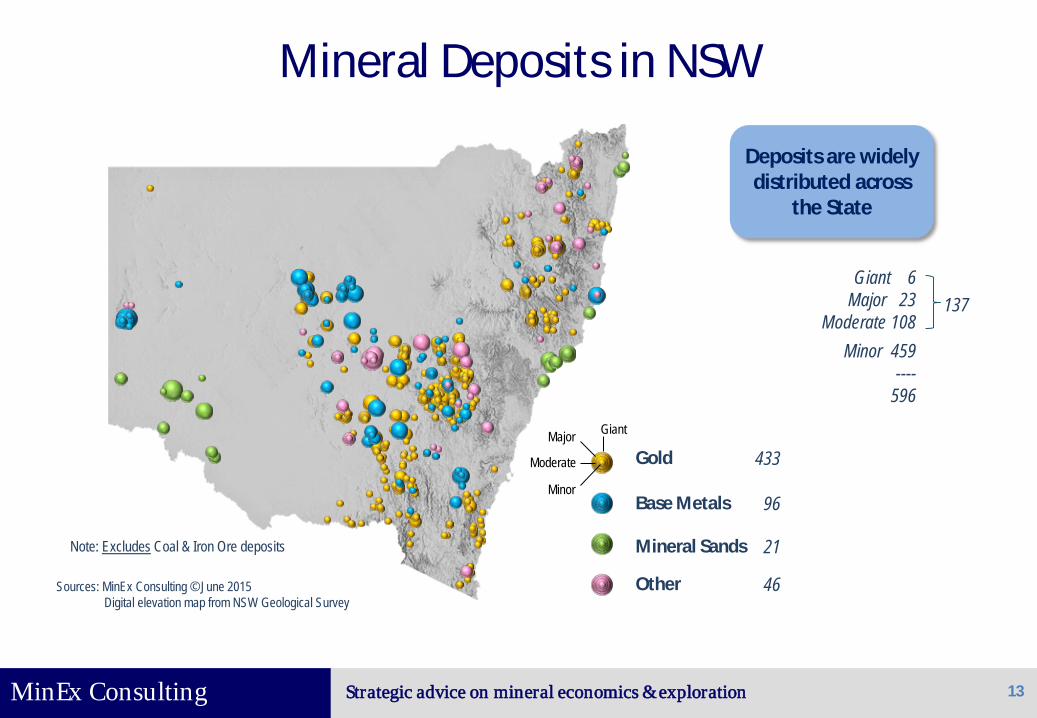

Mineral Deposits in NSW

13

Mineral Sands

Base Metals

Other

Giant Major

Moderate

Minor

Gold

Note: Excludes Coal & Iron Ore deposits Sources: MinEx Consulting © June 2015

Digital elevation map from NSW Geological Survey

Deposits are widely distributed across

the State

433

96

21

46

Giant 6 Major 23

Moderate 108 137

Minor 459 ----

596

MinEx Consulting Strategic advice on mineral economics & exploration

4. LOCATION OF DISCOVERIES IN NSW Over the last decade 13 significant discoveries were made in NSW

14

MinEx Consulting Strategic advice on mineral economics & exploration

Mineral Discoveries in NSW : Since 2005

15

Mineral Sands

Base Metals

Other

Giant Major

Moderate

Minor

Gold

McPhillamys (Au: 2006)

Syerston (Sc : 2012) Atlas-Campaspe

(HMS: 2005)

Note: Excludes Coal & Iron Ore deposits Names & dates refer to “Major” & “Giant” discoveries Sources: MinEx Consulting © June 2015

Digital elevation map from NSW Geological Survey

Collerina (Ni: 2006)

With 5 discoveries being made in since 2010

• 2010 Sorpresa [Au-Ag] Moderate • 2012 Mallee Bull [Cu-Ag-Au-Zn] Moderate • 2012 Syerston - Jervois [Sc] Moderate • 2012 Syerston - CTM [Sc] Giant • 2014 Commonwealth [Au-Zn-Pb] Moderate

Kingsgate (Mo)

Yiddah (Cu)

Culingerai (Cu)

West Balranald Extension (HMS)

Mt Carrington (Ag)

Commonwealth (Au)

Sorpresa (Au) Mallee Bull (Cu)

13 significant discoveries made in

the last decade

MinEx Consulting Strategic advice on mineral economics & exploration

5. DISCOVERY PERFORMANCE

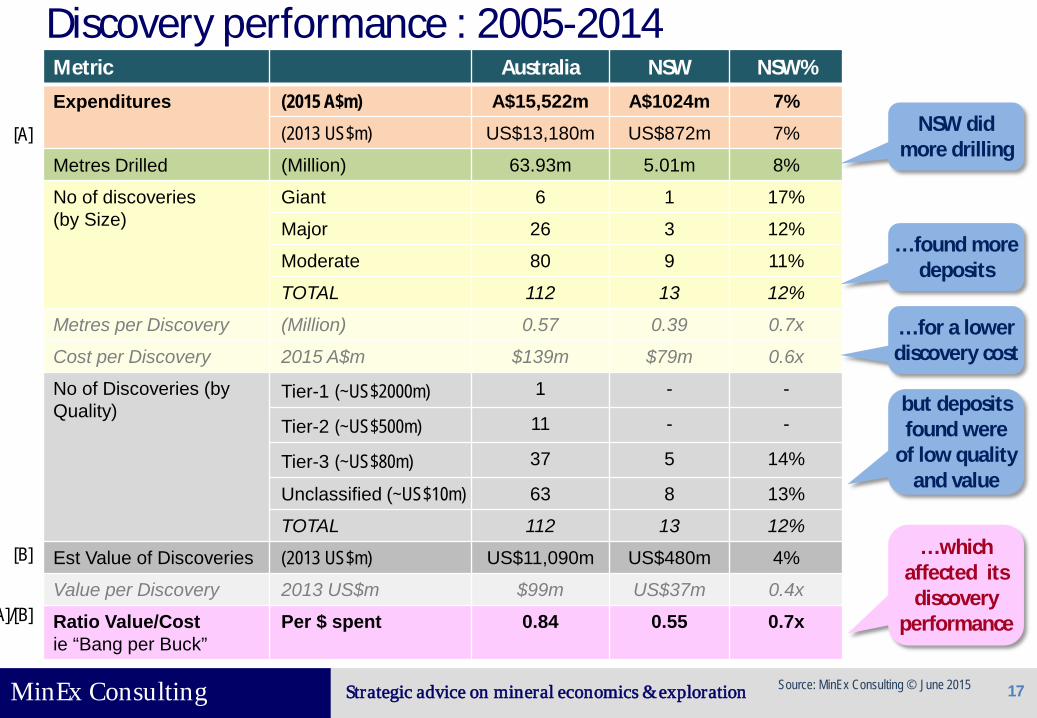

In terms of dollars spent, NSW has found more deposits than the National average. However most of these discoveries were of low value

16

MinEx Consulting Strategic advice on mineral economics & exploration

Discovery performance : 2005-2014 Metric Australia NSW NSW% Expenditures (2015 A$m) A$15,522m A$1024m 7%

(2013 US$m) US$13,180m US$872m 7%

Metres Drilled (Million) 63.93m 5.01m 8%

No of discoveries (by Size)

Giant 6 1 17%

Major 26 3 12%

Moderate 80 9 11%

TOTAL 112 13 12%

Metres per Discovery (Million) 0.57 0.39 0.7x

Cost per Discovery 2015 A$m $139m $79m 0.6x

No of Discoveries (by Quality)

Tier-1 (~US$2000m) 1 - -

Tier-2 (~US$500m) 11 - -

Tier-3 (~US$80m) 37 5 14%

Unclassified (~US$10m) 63 8 13%

TOTAL 112 13 12%

Est Value of Discoveries (2013 US$m) US$11,090m US$480m 4%

Value per Discovery 2013 US$m $99m US$37m 0.4x

Ratio Value/Cost ie “Bang per Buck”

Per $ spent 0.84 0.55 0.7x

17

[A]

[B]

A]/[B]

NSW did more drilling

… found more deposits

… for a lower discovery cost

but deposits found were

of low quality and value

… which affected its

discovery performance

Source: MinEx Consulting © June 2015

MinEx Consulting Strategic advice on mineral economics & exploration

Expenditures versus drilling activity Exploration expenditures and metres drilled non-bulk discoveries NSW: 2000-2014

0.0

0.2

0.4

0.6

0.8

1.0

$0

$25

$50

$75

$100

$125

$150

2000 2005 2010

Expenditures - Non-BulkMillion Metres Drilled - TotalMillion Metres Drilled - Greenfield

18

Note: Excludes expenditures and drilling on coal and iron ore

Million Metres Drilled

Drilling activity (especially

greenfield drilling) has not kept pace with exploration

expenditures

2015 A$ Million

0.11 0.02

0.74

0.43

$129m

$79m

Sources: NSW Geological Survey March 2015 ABS 8412

0.09

0.30

MinEx Consulting Strategic advice on mineral economics & exploration

Discoveries versus Drilling Drilling activity and non-bulk discoveries Australia: 1985-2014

0

5

10

15

0

5

10

15

20

25

1990 2000 2010

Moderate DepositsMajor DepositsGiant DepositsMetres Drilled (rhs)

19

Note: Excludes bulk mineral discoveries (ie coal and iron ore) “Moderate” >100koz Au, >10kt Ni, >100Kt Cu equiv, 250kt Zn+Pb, >5kt U3O8 “Major” >1Moz Au, >100kt Ni, >1Mt Cu equiv, 2.5Mt Zn+Pb, >25kt U3O8 “Giant” >6Moz Au, >1Mt Ni, >5Mt Cu equiv, 12Mt Zn+Pb, >125kt U3O8

Sources: MinEx Consulting © June 2015 and ABS 8412

No of Discoveries Metres Drilled (Million)

Caution: Incomplete data in recent years

Good correlation between drilling and number of

deposits found

“if you don’t drill you won’t discover”

MinEx Consulting Strategic advice on mineral economics & exploration

Number of discoveries made versus metres drilled Metres drilled versus non-bulk discoveries NSW: 2000-2014

0.0

0.2

0.4

0.6

0.8

1.0

0

1

2

3

4

5

2000 2005 2010 2015

Moderate DiscoveriesMajor DiscoveriesGiant DiscoveriesMillion Metres Drilled - TotalMillion Metres Drilled - Greenfield

20

Note: Excludes satellite deposits within existing Camps. Also excludes Bulk Mineral discoveries and expenditures

Sources: NSW Geological Survey March 2015 MinEx Consulting © June 2015

Caution: Incomplete data in recent years

Giant >6 Moz Au, >1 Mt Ni, >12 Mt Zn+Pb, >5 Mt Cu equiv Major >1 Moz Au, > 100 kt Ni, >2.5 Mt Zn+Pb, >1 Mt Cu equiv Moderate >0.1 Moz Au, >10 kt Ni, >0.25 Mt Zn+Pb, >0.1 Mt Cu-equiv

Million Metres Drilled

Over the last decade (2005-2014) 5.0 million metres

was drilled (in 68,219 holes) for 13 discoveries

ie 385,000 metres or 5250 holes per discovery

Number of Discoveries

NSW’s discovery data is “noisy” because very few deposits are

found each year

MinEx Consulting Strategic advice on mineral economics & exploration

6. WHO MADE THE DISCOVERIES ? Over the last decade 80% of all discoveries in NSW were made by Junior Explorers

21

MinEx Consulting Strategic advice on mineral economics & exploration

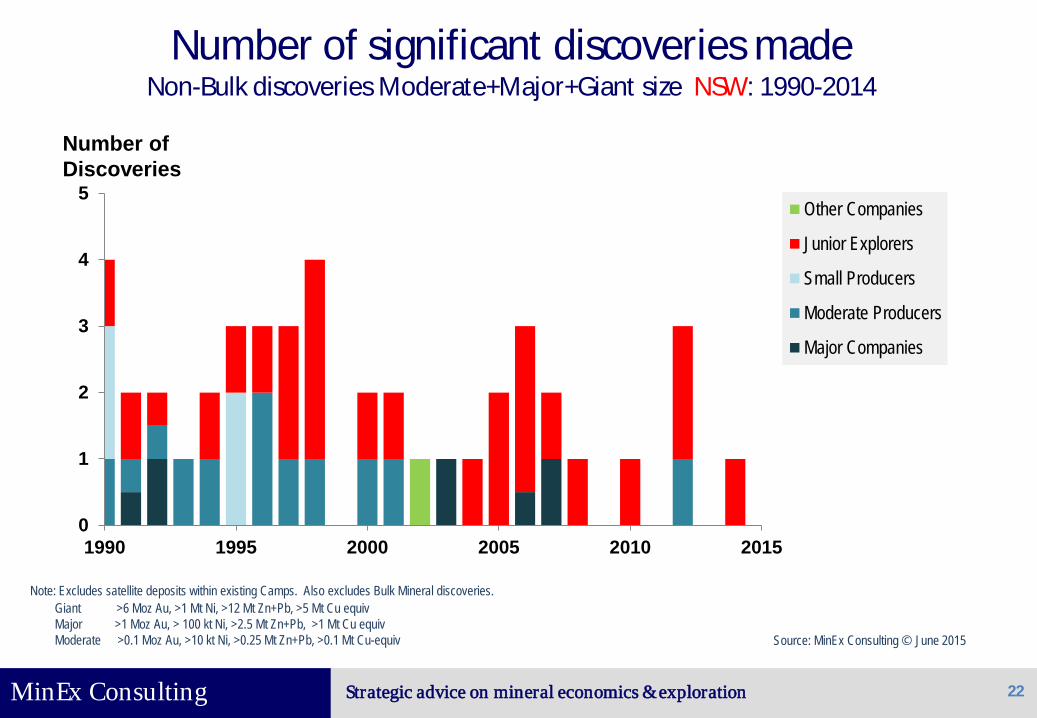

Number of significant discoveries made Non-Bulk discoveries Moderate+Major+Giant size NSW: 1990-2014

0

1

2

3

4

5

1990 1995 2000 2005 2010 2015

Other Companies

Junior Explorers

Small Producers

Moderate Producers

Major Companies

22

Number of Discoveries

Note: Excludes satellite deposits within existing Camps. Also excludes Bulk Mineral discoveries.

Source: MinEx Consulting © June 2015

Giant >6 Moz Au, >1 Mt Ni, >12 Mt Zn+Pb, >5 Mt Cu equiv Major >1 Moz Au, > 100 kt Ni, >2.5 Mt Zn+Pb, >1 Mt Cu equiv Moderate >0.1 Moz Au, >10 kt Ni, >0.25 Mt Zn+Pb, >0.1 Mt Cu-equiv

MinEx Consulting Strategic advice on mineral economics & exploration

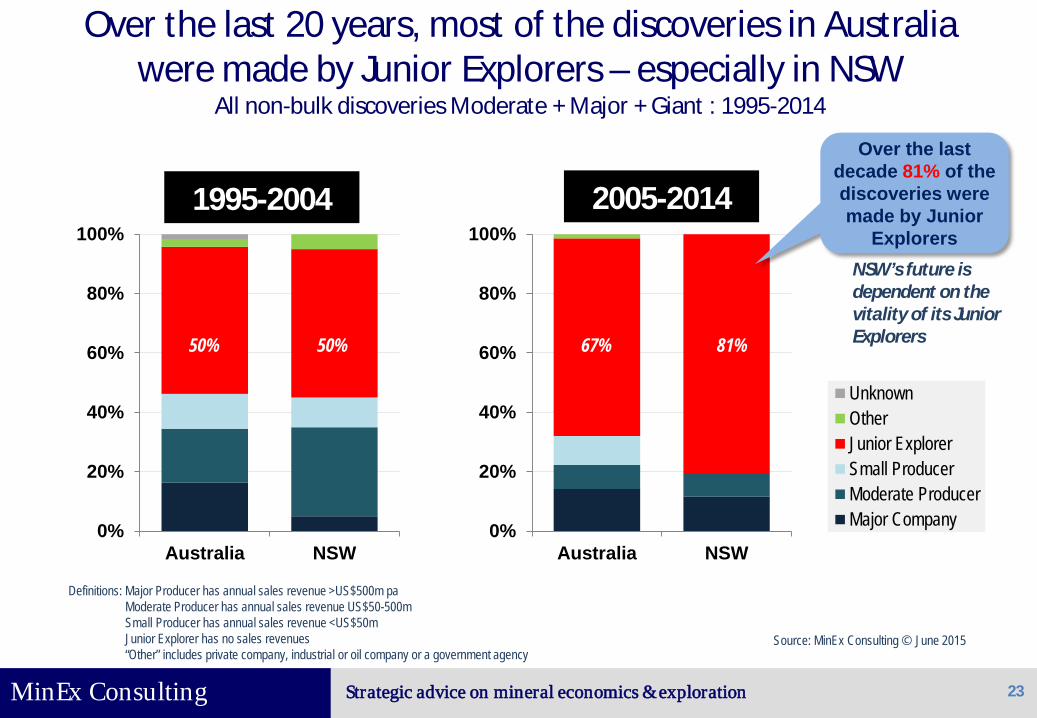

Over the last 20 years, most of the discoveries in Australia were made by Junior Explorers – especially in NSW

All non-bulk discoveries Moderate + Major + Giant : 1995-2014

2005-2014

0%

20%

40%

60%

80%

100%

Australia NSW

UnknownOtherJunior ExplorerSmall ProducerModerate ProducerMajor Company

23

0%

20%

40%

60%

80%

100%

Australia NSW

1995-2004

81% 67% 50% 50%

Source: MinEx Consulting © June 2015

Definitions: Major Producer has annual sales revenue >US$500m pa Moderate Producer has annual sales revenue US$50-500m Small Producer has annual sales revenue <US$50m Junior Explorer has no sales revenues “Other” includes private company, industrial or oil company or a government agency

Over the last decade 81% of the discoveries were made by Junior

Explorers NSW’s future is dependent on the vitality of its Junior Explorers

MinEx Consulting Strategic advice on mineral economics & exploration

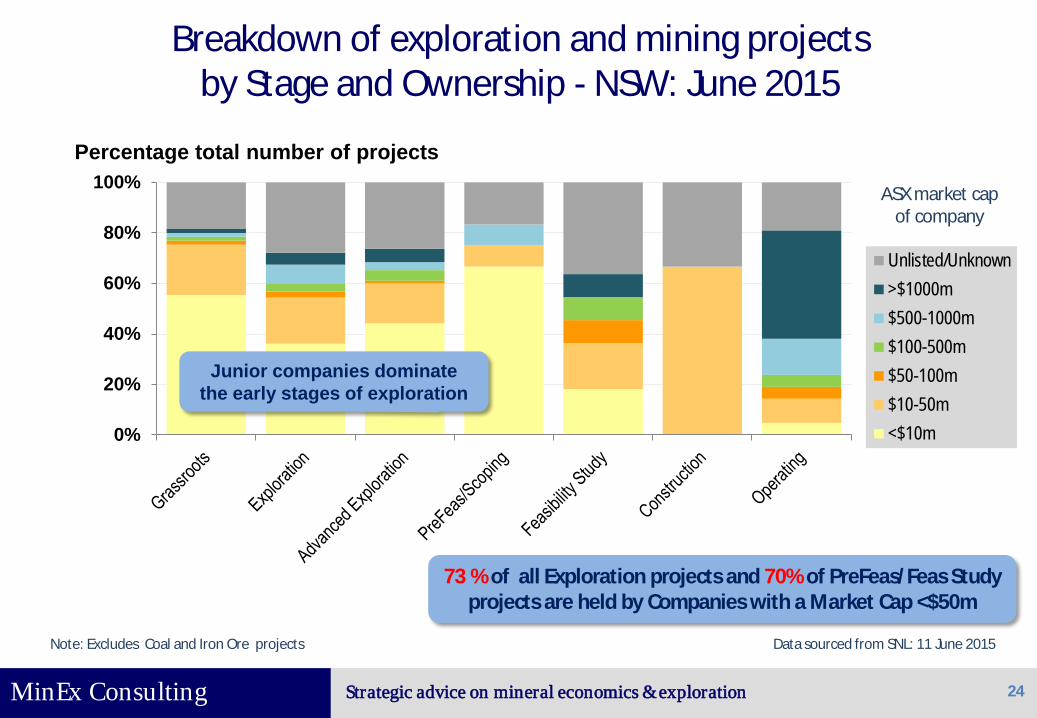

Breakdown of exploration and mining projects by Stage and Ownership - NSW: June 2015

0%

20%

40%

60%

80%

100%

Unlisted/Unknown>$1000m$500-1000m$100-500m$50-100m$10-50m<$10m

24

Percentage total number of projects

ASX market cap of company

Data sourced from SNL: 11 June 2015 Note: Excludes Coal and Iron Ore projects

Junior companies dominate the early stages of exploration

73 % of all Exploration projects and 70% of PreFeas/Feas Study projects are held by Companies with a Market Cap <$50m

MinEx Consulting Strategic advice on mineral economics & exploration

7. CURRENT FINANCIAL SITUATION FOR JUNIOR EXPLORERS IN NSW

Junior companies are doing it “tough”

25

MinEx Consulting Strategic advice on mineral economics & exploration

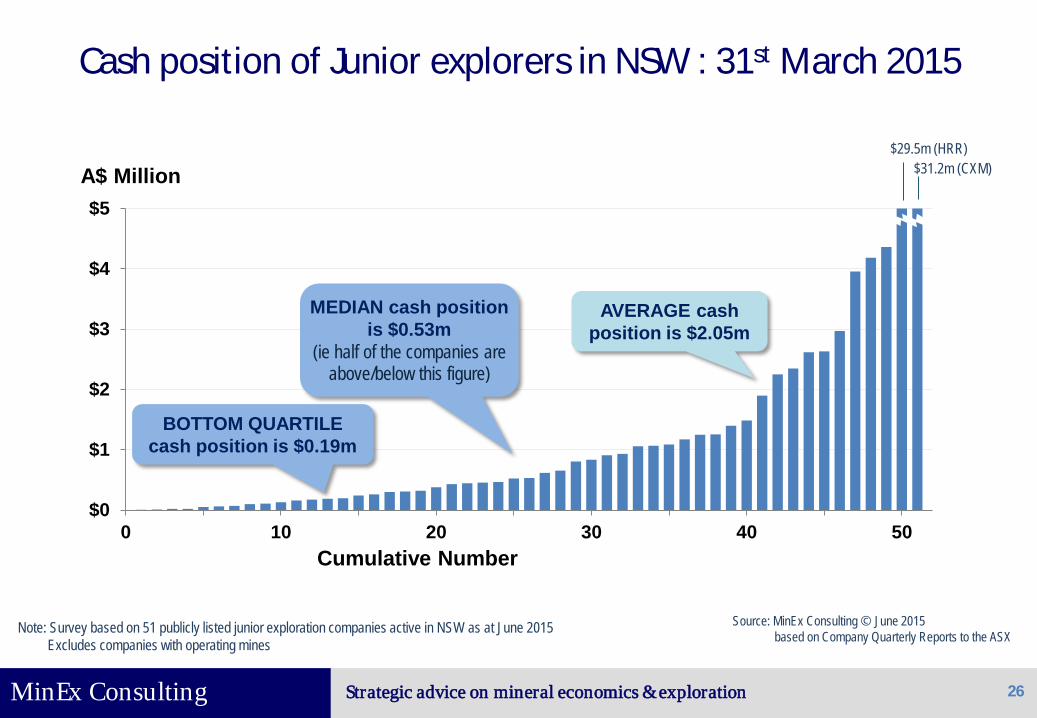

Cash position of Junior explorers in NSW : 31st March 2015

$0

$1

$2

$3

$4

$5

0 10 20 30 40 50

26

A$ Million $29.5m (HRR)

MEDIAN cash position is $0.53m

(ie half of the companies are above/below this figure)

AVERAGE cash position is $2.05m

Cumulative Number

BOTTOM QUARTILE cash position is $0.19m

$31.2m (CXM)

Note: Survey based on 51 publicly listed junior exploration companies active in NSW as at June 2015 Excludes companies with operating mines

Source: MinEx Consulting © June 2015 based on Company Quarterly Reports to the ASX

MinEx Consulting Strategic advice on mineral economics & exploration

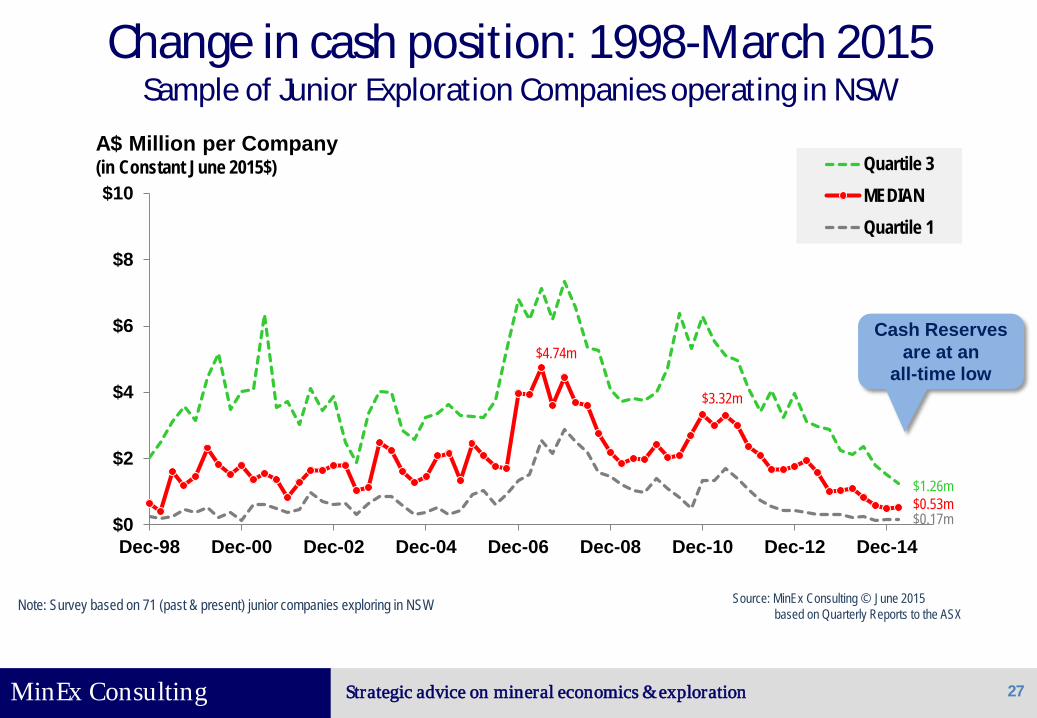

Change in cash position: 1998-March 2015 Sample of Junior Exploration Companies operating in NSW

$0

$2

$4

$6

$8

$10

Dec-98 Dec-00 Dec-02 Dec-04 Dec-06 Dec-08 Dec-10 Dec-12 Dec-14

Quartile 3MEDIANQuartile 1

27

Note: Survey based on 71 (past & present) junior companies exploring in NSW

A$ Million per Company (in Constant June 2015$)

$0.53m $1.26m

$0.17m

Cash Reserves are at an

all-time low $4.74m

$3.32m

Source: MinEx Consulting © June 2015 based on Quarterly Reports to the ASX

MinEx Consulting Strategic advice on mineral economics & exploration

Cash burn rate for NSW Junior Explorers Annualised operating expenditures divided by cash reserves

0

1

2

3

4

5

6

Dec-98 Dec-00 Dec-02 Dec-04 Dec-06 Dec-08 Dec-10 Dec-12 Dec-14

Quartile 3MEDIANQuartile 1

28

Note: Survey based on 71 (past & present) junior companies exploring in NSW.

Years

0.61 Years

1.76 Years

0.28 years

2.18

Source: MinEx Consulting © June 2015 based on Quarterly Reports to the ASX

The Median Cash Burn Rate is normally around 1-2 years

2.97

Currently only have 7 months of

cash reserves

MinEx Consulting Strategic advice on mineral economics & exploration

Cash Reserves and Expenditures for the MEDIAN Junior Exploration Company in NSW : 1998-March 2015

-$2

-$1

$0

$1

$2

$3

$4

$5

Dec-98 Dec-00 Dec-02 Dec-04 Dec-06 Dec-08 Dec-10 Dec-12 Dec-14

29

June 2015 A$ Million pa

Note: Survey based on 71 (past & present) junior companies exploring in NSW. “Net Other” includes production and other costs less interest income, mine revenue, Government Assistance and R&D tax credits Quarterly spend data has been multiplied by 4x to produce an annualised spend rate

Cash Reserves

Exploration & Development

Administration

Net Other

Source: MinEx Consulting © June 2015 based on Quarterly Reports to the ASX

During a downturn, “in-field” exploration &

development expenditures are cut the most

Admin costs tend

to be “fixed”

Cash Reserves are at an

all-time low

MinEx Consulting Strategic advice on mineral economics & exploration

$0

$5

$10

$15

$20

$25

$30

$35

$40

$0 $10 $20 $30 $40 $50

The lack of cash is of most concern to those junior companies with low market caps

30

Cash Reserves (A$ Million) as at 30 March 2015

Market Cap (A$ Million) as at 11 June 2015

Companies can raise cash by issuing new shares ... but that’s difficult if the market cap is low

Note: Survey based on 47 publicly listed junior exploration companies active in NSW as June 2015. Excludes 4 companies currently suspended from trading. Excludes companies with operating mines.

Source: MinEx Consulting © June 2015 based on Company Quarterly Reports to the ASX

Most of NSW’s Junior Explorers

have a market cap <$15m

~20% of Junior Explorers in NSW have a market Cap <$2m and have <$1m in cash reserves

MinEx Consulting Strategic advice on mineral economics & exploration 31

…. But junior explorers are incredibly resilient and most will survive

“Junior companies are like cockroaches … they can both survive a nuclear winter !” Source: Canadian Mining Industry spokesperson (who wishes to remain anonymous) March 2014

MinEx Consulting Strategic advice on mineral economics & exploration

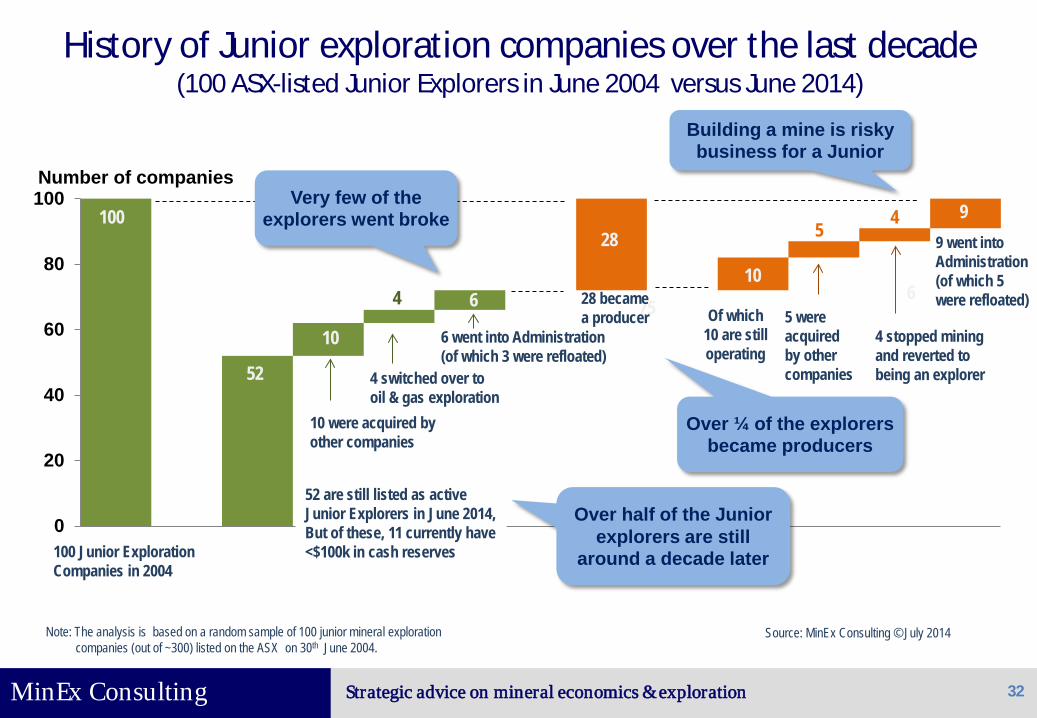

History of Junior exploration companies over the last decade (100 ASX-listed Junior Explorers in June 2004 versus June 2014)

0

20

40

60

80

100

32

100 Junior Exploration Companies in 2004

100

52

10 75

28

10 6

9

Note: The analysis is based on a random sample of 100 junior mineral exploration companies (out of ~300) listed on the ASX on 30th June 2004.

Source: MinEx Consulting © July 2014

52 are still listed as active Junior Explorers in June 2014, But of these, 11 currently have <$100k in cash reserves

4 switched over to oil & gas exploration

6 went into Administration (of which 3 were refloated)

4 28 became a producer Of which

10 are still operating

5 were acquired by other companies

9 went into Administration (of which 5 were refloated)

10 were acquired by other companies

Over half of the Junior explorers are still

around a decade later

Very few of the explorers went broke

Over ¼ of the explorers became producers

Building a mine is risky business for a Junior

6

5 4

4 stopped mining and reverted to being an explorer

Number of companies

MinEx Consulting Strategic advice on mineral economics & exploration

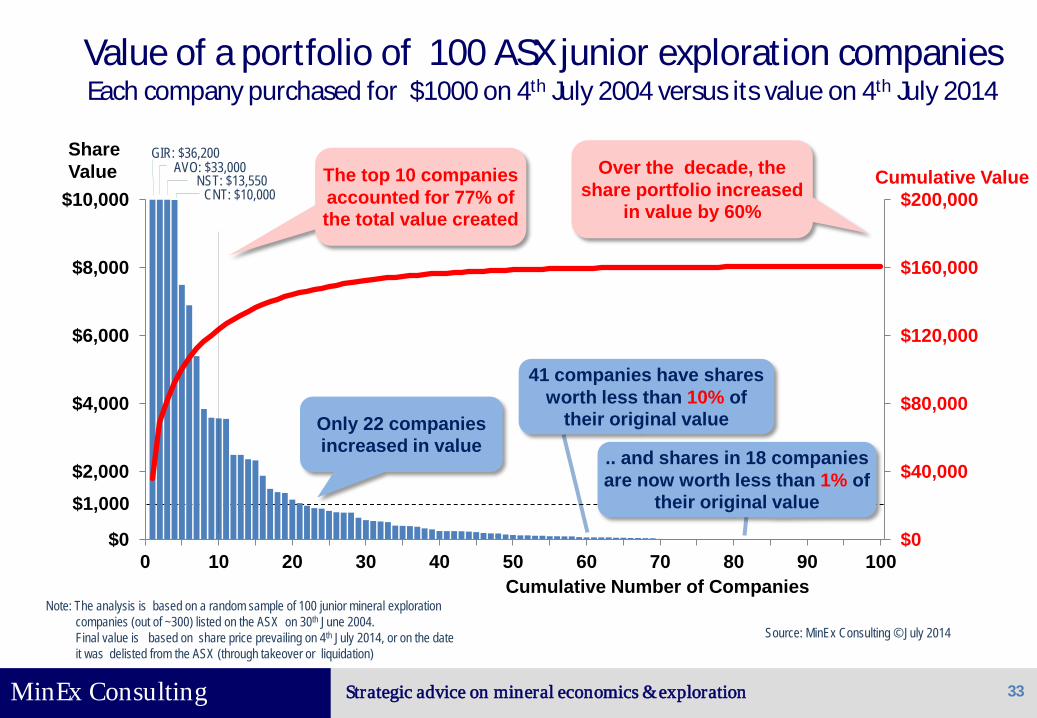

Value of a portfolio of 100 ASX junior exploration companies Each company purchased for $1000 on 4th July 2004 versus its value on 4th July 2014

$0

$40,000

$80,000

$120,000

$160,000

$200,000

$0

$2,000

$4,000

$6,000

$8,000

$10,000

0 10 20 30 40 50 60 70 80 90 100

33

GIR: $36,200 AVO: $33,000

NST: $13,550 CNT: $10,000

Share Value

Cumulative Number of Companies

Source: MinEx Consulting © July 2014

Cumulative Value

Only 22 companies increased in value

$1,000

The top 10 companies accounted for 77% of the total value created

41 companies have shares worth less than 10% of

their original value

.. and shares in 18 companies are now worth less than 1% of

their original value

Note: The analysis is based on a random sample of 100 junior mineral exploration companies (out of ~300) listed on the ASX on 30th June 2004. Final value is based on share price prevailing on 4th July 2014, or on the date it was delisted from the ASX (through takeover or liquidation)

Over the decade, the share portfolio increased

in value by 60%

MinEx Consulting Strategic advice on mineral economics & exploration

8. OUTLOOK FOR MINING IN NSW

For the industry to be sustainable it needs to urgently find and develop new mines

34

MinEx Consulting Strategic advice on mineral economics & exploration

Number of mines operating in NSW: 1990-2040 for operations mining >100 ktpa of ore

35

Note: Limited to operations mining >100ktpa of ore. The forecast figures are based on dividing the current reported Reserves and Resources by the production rate in 2014. Excludes coal and iron ore mines

Source: Estimates by MinEx Consulting © June 2015, based on latest published Reserves & Resources

Number of Mines

Historical Forecast

11

15 16

8

2

8

1 2

In terms of current Reserves, half of NSW’s mines will close by 2020 (ie 5 years time). In terms of current

Resources, half will close by 2028 (ie 13 years time)

The challenge is that it typically takes 10-15 years to turn a new discovery into a mine … to avoid a hiatus in production we need to explore now !

0

5

10

15

20

1990 1995 2000 2005 2010 2015 2020 2025 2030 2035 2040

Forecast (Based on current Resources)Forecast (Based on current Reserves)Historical

MinEx Consulting Strategic advice on mineral economics & exploration

8. SUMMARY / CONCLUSIONS

There is an urgent need to find and develop new mines to replace those closing down. The Junior Explorers have a key role to play in this

36

MinEx Consulting Strategic advice on mineral economics & exploration

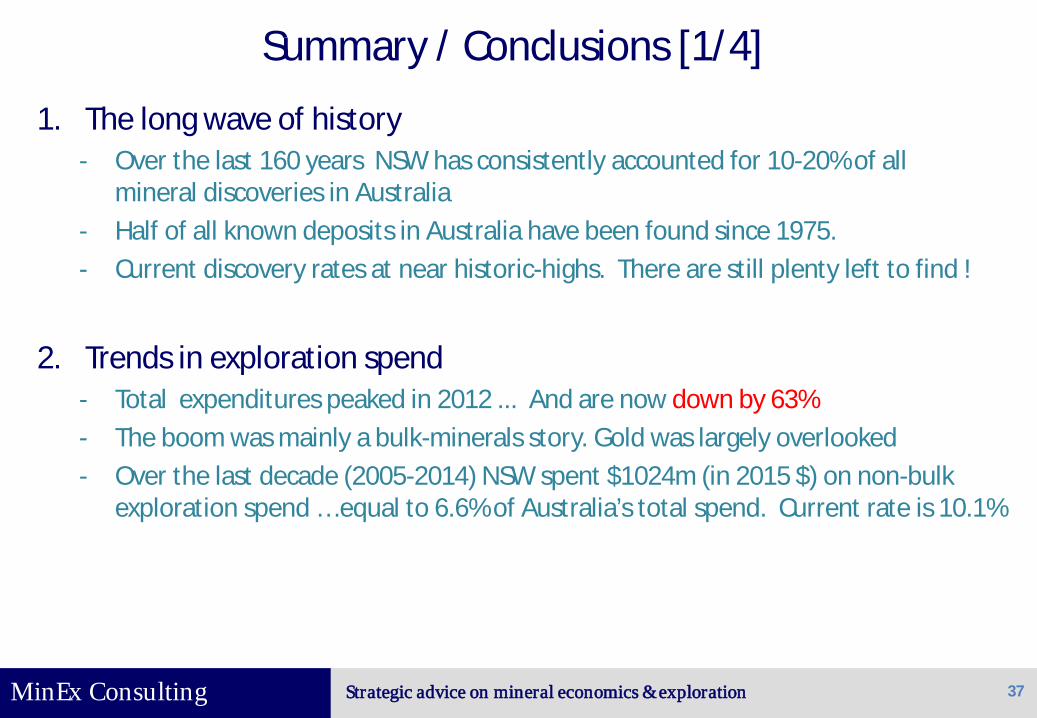

Summary / Conclusions [1/4]

1. The long wave of history - Over the last 160 years NSW has consistently accounted for 10-20% of all

mineral discoveries in Australia - Half of all known deposits in Australia have been found since 1975. - Current discovery rates at near historic-highs. There are still plenty left to find !

2. Trends in exploration spend

- Total expenditures peaked in 2012 ... And are now down by 63% - The boom was mainly a bulk-minerals story. Gold was largely overlooked - Over the last decade (2005-2014) NSW spent $1024m (in 2015 $) on non-bulk

exploration spend … equal to 6.6% of Australia’s total spend. Current rate is 10.1%

37

MinEx Consulting Strategic advice on mineral economics & exploration

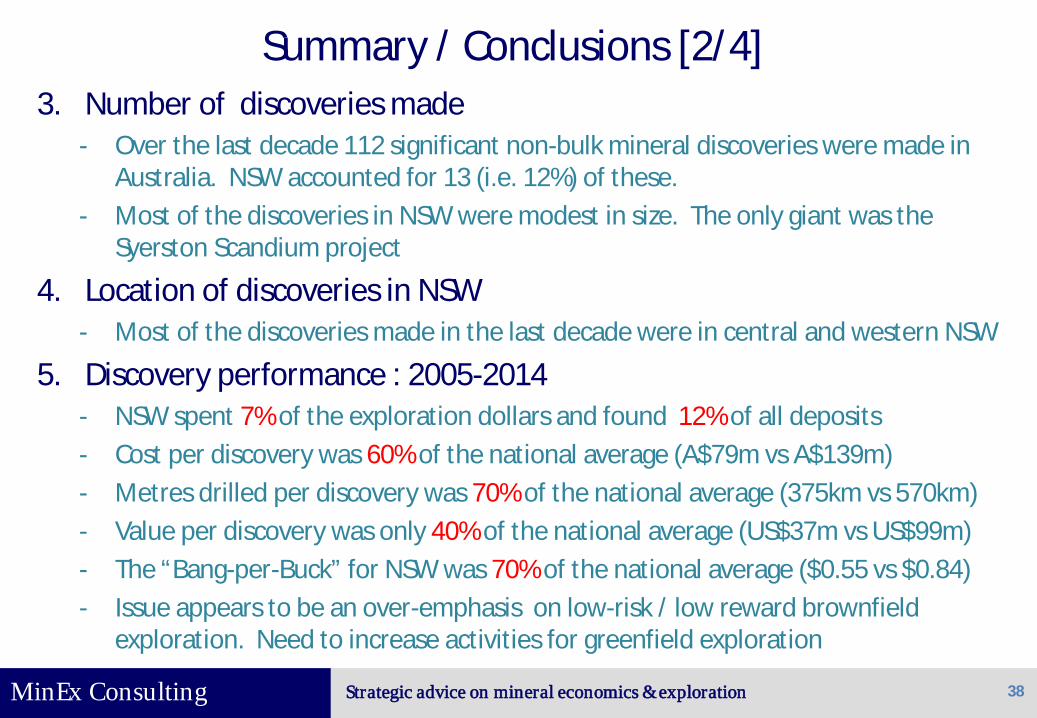

Summary / Conclusions [2/4] 3. Number of discoveries made

- Over the last decade 112 significant non-bulk mineral discoveries were made in Australia. NSW accounted for 13 (i.e. 12%) of these.

- Most of the discoveries in NSW were modest in size. The only giant was the Syerston Scandium project

4. Location of discoveries in NSW - Most of the discoveries made in the last decade were in central and western NSW

5. Discovery performance : 2005-2014 - NSW spent 7% of the exploration dollars and found 12% of all deposits - Cost per discovery was 60% of the national average (A$79m vs A$139m) - Metres drilled per discovery was 70% of the national average (375km vs 570km) - Value per discovery was only 40% of the national average (US$37m vs US$99m) - The “Bang-per-Buck” for NSW was 70% of the national average ($0.55 vs $0.84) - Issue appears to be an over-emphasis on low-risk / low reward brownfield

exploration. Need to increase activities for greenfield exploration

38

MinEx Consulting Strategic advice on mineral economics & exploration

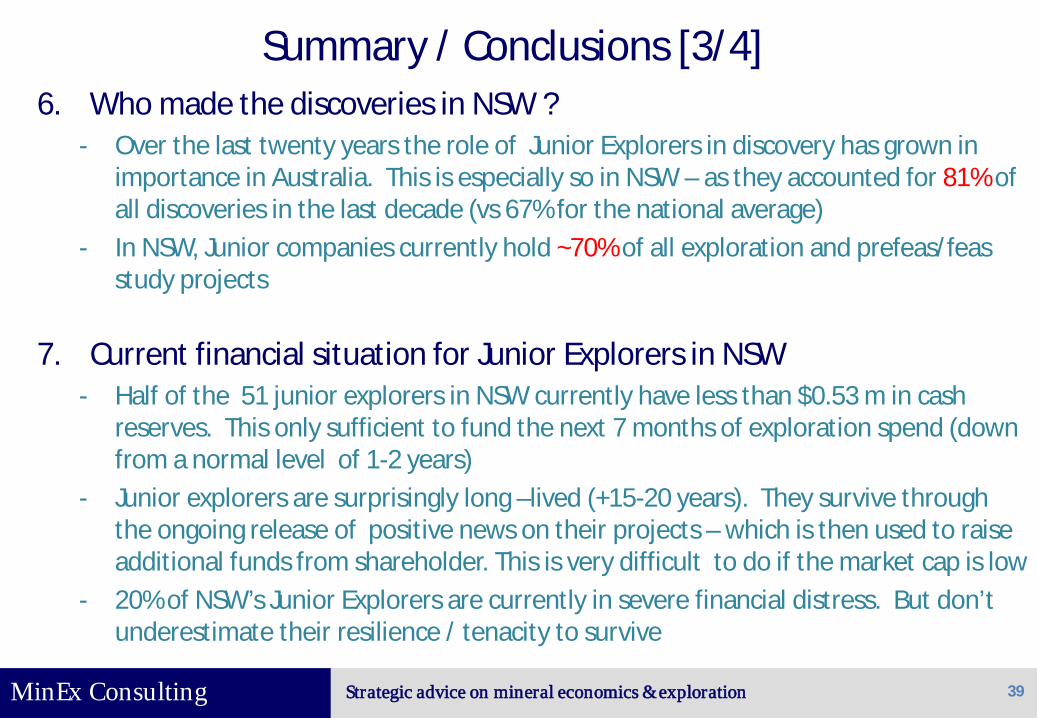

Summary / Conclusions [3/4] 6. Who made the discoveries in NSW ?

- Over the last twenty years the role of Junior Explorers in discovery has grown in importance in Australia. This is especially so in NSW – as they accounted for 81% of all discoveries in the last decade (vs 67% for the national average)

- In NSW, Junior companies currently hold ~70% of all exploration and prefeas/feas study projects

7. Current financial situation for Junior Explorers in NSW - Half of the 51 junior explorers in NSW currently have less than $0.53 m in cash

reserves. This only sufficient to fund the next 7 months of exploration spend (down from a normal level of 1-2 years)

- Junior explorers are surprisingly long –lived (+15-20 years). They survive through the ongoing release of positive news on their projects – which is then used to raise additional funds from shareholder. This is very difficult to do if the market cap is low

- 20% of NSW’s Junior Explorers are currently in severe financial distress. But don’t underestimate their resilience / tenacity to survive

39

MinEx Consulting Strategic advice on mineral economics & exploration

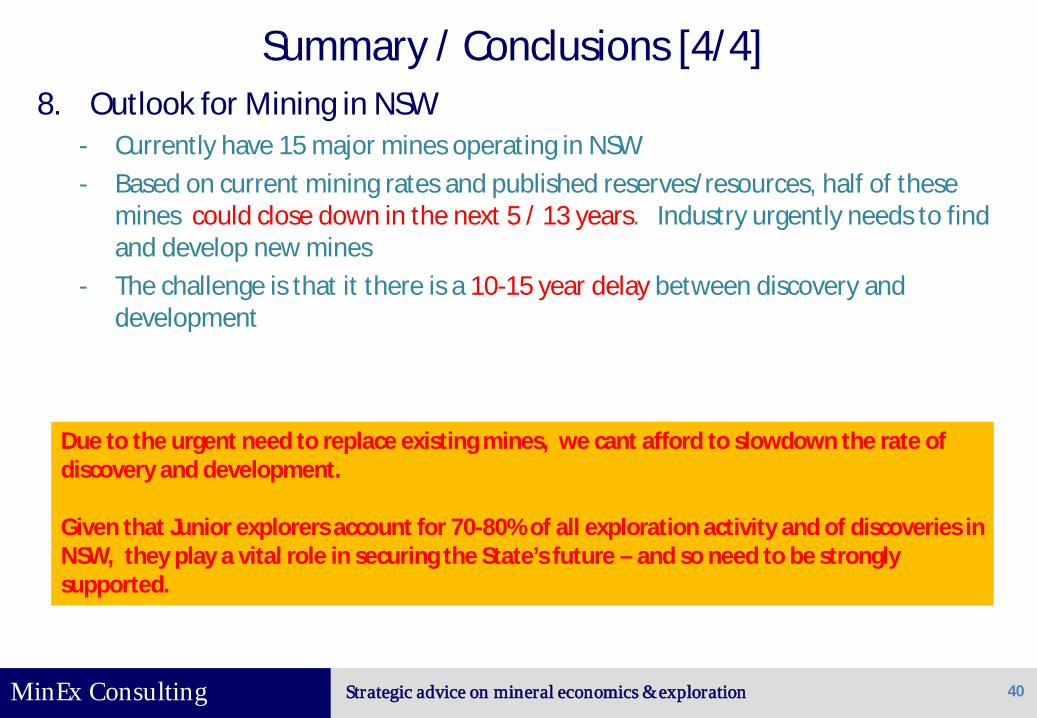

Summary / Conclusions [4/4] 8. Outlook for Mining in NSW

- Currently have 15 major mines operating in NSW - Based on current mining rates and published reserves/resources, half of these

mines could close down in the next 5 / 13 years. Industry urgently needs to find and develop new mines

- The challenge is that it there is a 10-15 year delay between discovery and development

40

Due to the urgent need to replace existing mines, we cant afford to slowdown the rate of discovery and development. Given that Junior explorers account for 70-80% of all exploration activity and of discoveries in NSW, they play a vital role in securing the State’s future – and so need to be strongly supported.

MinEx Consulting Strategic advice on mineral economics & exploration 41

Contact details Richard Schodde Managing Director MinEx Consulting Melbourne, Australia Email: [email protected] Website: MinExConsulting.com

Copies of this and other similar presentations can be downloaded from

my website