Embed Size (px)

Citation preview

Shopper Expectations in the Digital AgeGuided Selling Live!June 23, 2016

Gabe WeissRetail Innovation Lead

Copyright © 2016 Sapient Corporation

Copyright © 2016 Sapient Corporation

Gabe WeissRetail Innovation Lead

iN: gabeweiss @geedub_nyc

Copyright © 2016 Sapient Corporation | Confidential

Copyright © 2016 Sapient Corporation

Agenda

01 Shopper Expectations

02 Experience Matters

03 Ways to Win at Retail Today, and in the Future

Copyright © 2016 Sapient Corporation

Guided Selling Live!Exclusive Shopper Research

Available Soon

2005 2013

Profound changes have

rocked our world

Vatican SquareAnnouncement of New Pope

7

The “Always-On” consumer is accessing multiple kinds of content across multiple devices everyday

The average person spends 5.6 hours a day with digital media

8

94% have done online research prior to buying

44% purchased through smartphone's web

browser

44% purchased through retailer app

Digital plays a major role in modern purchase

61% prefer shopping in digital channels (website/app)

Source: GSL May 2016

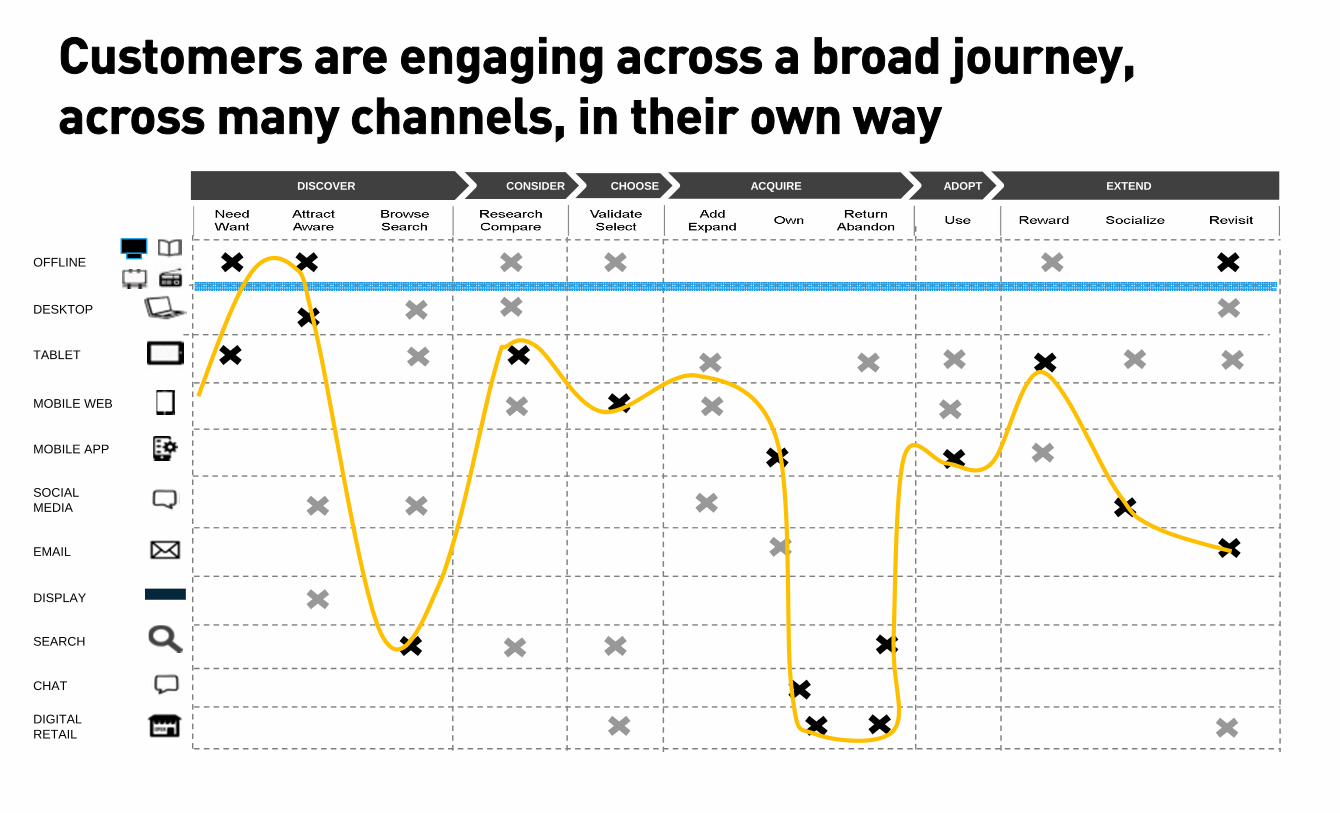

Customers are engaging across a broad journey, across many channels, in their own way

EXTENDADOPTACQUIRECHOOSECONSIDERDISCOVER

DESKTOP

MOBILE WEB

MOBILE APP

SOCIAL MEDIA

DIGITAL RETAIL

CHAT

DISPLAY

TABLET

SEARCH

OFFLINE

`

10

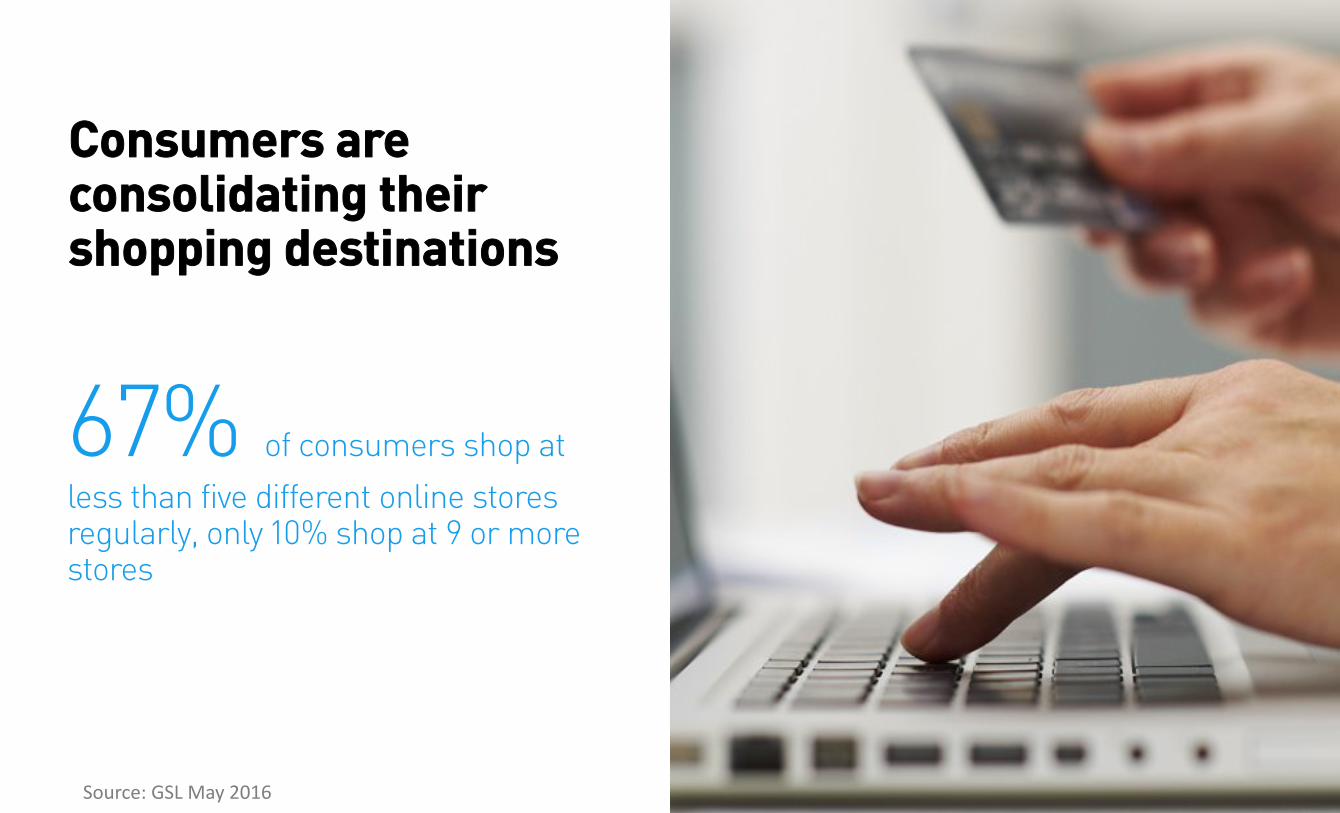

Consumers are consolidating their shopping destinations

67% of consumers shop at

less than five different online stores regularly, only 10% shop at 9 or more stores

Source: GSL May 2016

Copyright © 2016 Sapient Corporation

The global retail industry is being disrupted

12

Online dominates consumers’ changing preferences

44% of favorite places to

shop are websites, then store (39%) and store apps (17%)

Source: GSL May 2016

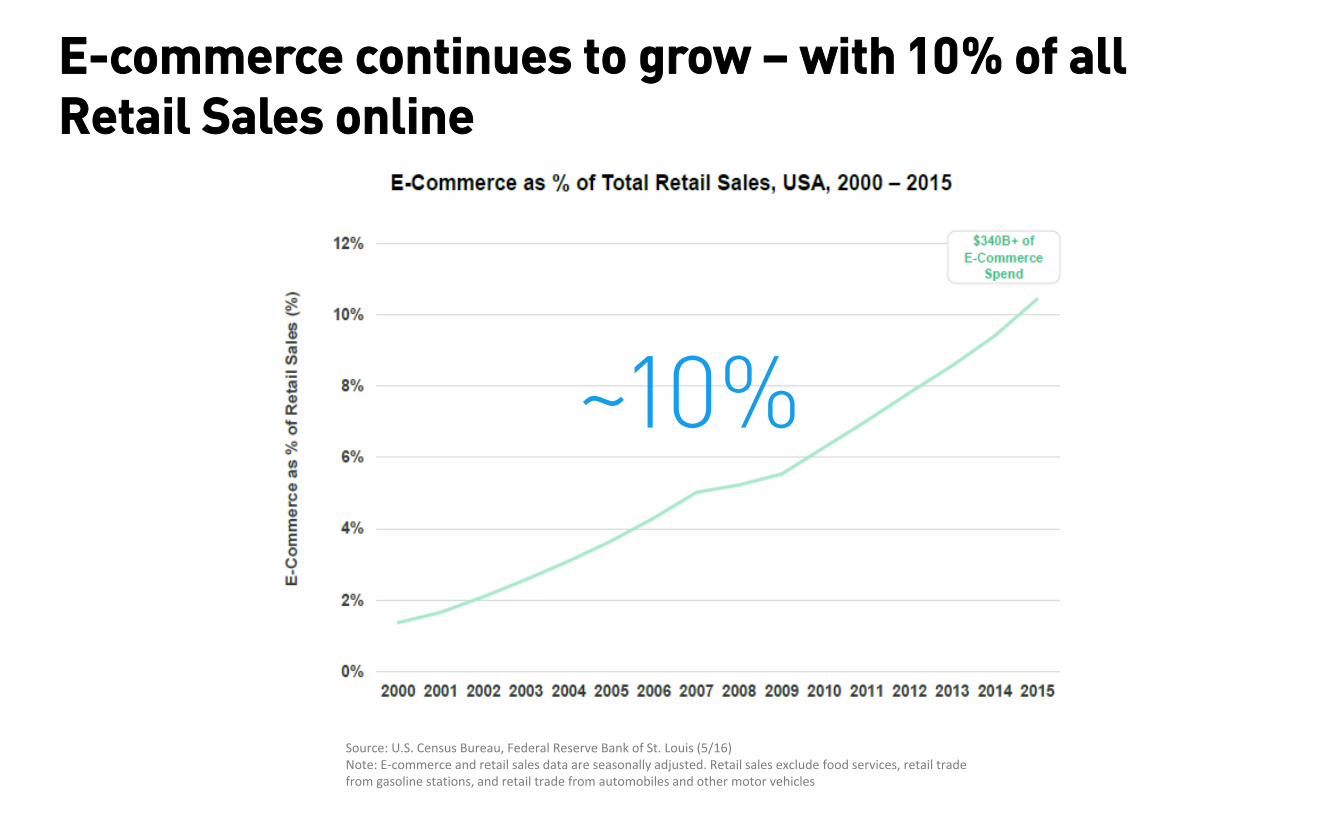

E-commerce continues to grow – with 10% of all Retail Sales online

Source: U.S. Census Bureau, Federal Reserve Bank of St. Louis (5/16)Note: E‐commerce and retail sales data are seasonally adjusted. Retail sales exclude food services, retail trade from gasoline stations, and retail trade from automobiles and other motor vehicles

~10%

14

Amazon is leading the transformation

51% of all online retail

growth in 2015 was on Amazon

24% of all retail growth in

2015 was on Amazon

Source: NYTimes, It’s Amazon and Also‐Rans in Retailers’ Race for Online Sales, 12/30/15

Copyright © 2016 Sapient Corporation

“How did you go bankrupt?"“Two ways. Gradually, then suddenly.”

― Ernest HemingwayThe Sun Also Rises

Copyright © 2016 Sapient Corporation

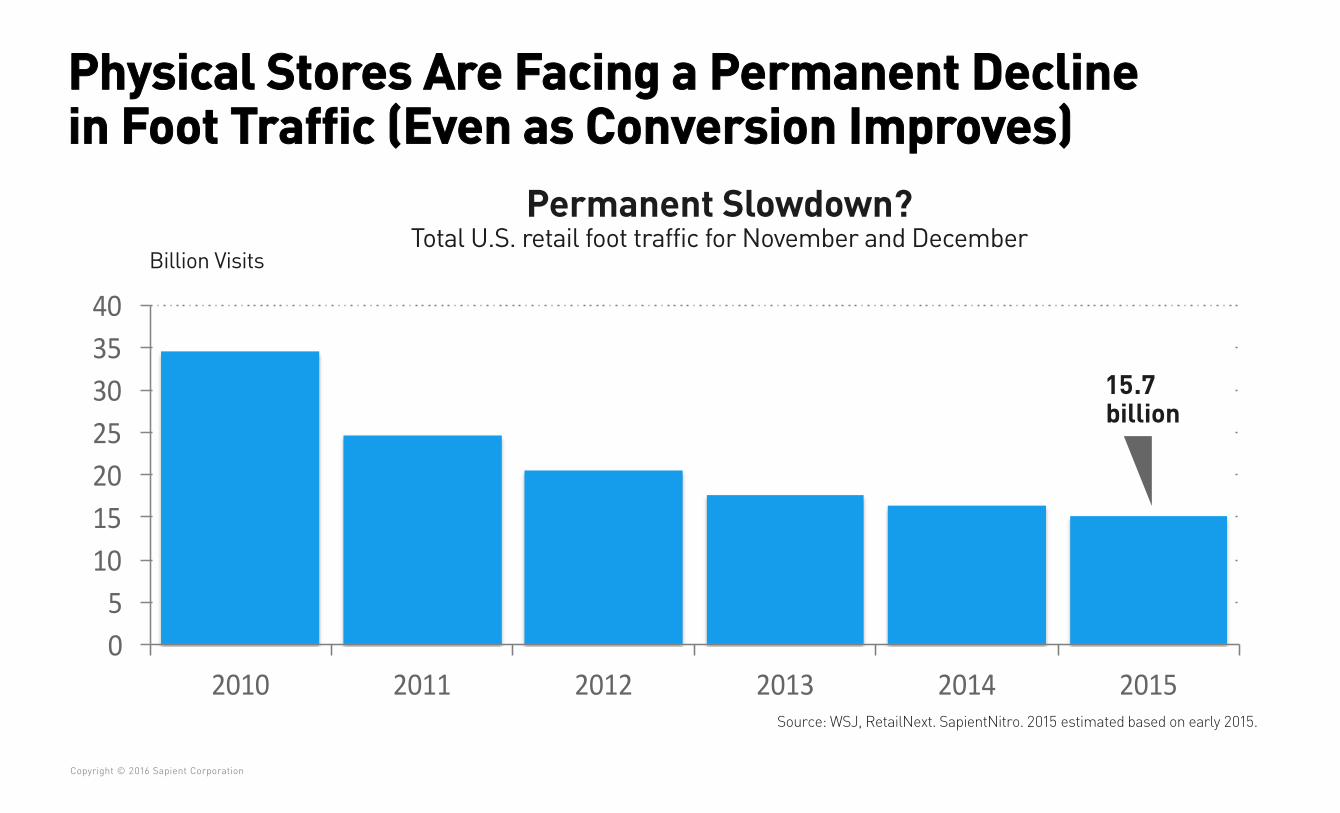

05

10152025303540

2010 2011 2012 2013 2014 2015

Physical Stores Are Facing a Permanent Decline in Foot Traffic (Even as Conversion Improves)

Source: WSJ, RetailNext. SapientNitro. 2015 estimated based on early 2015.

Billion Visits

15.7billion

Permanent Slowdown?Total U.S. retail foot traffic for November and December

17Source: http://www.businessinsider.com/photos-that-show-why-sears-is-vanishing-2013-10

Copyright © 2016 Sapient Corporation

Businesses have to differentiate by offering consumers something

that goes beyond low price…

A Better Experience

Copyright © 2016 Sapient Corporation

The Retail Experience Transformation Imperative

Experience Matters

20

Consumers value great prices, easy shopping experiences with a good selection

Source: GSL May 2016

Characteristics of favorite shops:

21

After fair price, consumers want an ideal selection and easy to find and discover products

Source: GSL May 2016

Characteristics of the ideal store (online or physical store):

2%

28%

44%

61%

67%

85%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

Other

Support in selecting the right product for me

Helpful service

Easy to find what I need and ability to discover new,interesting products

Broad selection

Fair price

Copyright © 2016 Sapient Corporation

Modern Consumers Prefer Self-Service Options

23

Self-service benefits:

• 55% convenience

• 49% ease of use

• 43% speed compared to human service

32% liked not having to interact with anyone

Modern consumers prefer self-service options

55% would prefer self-service instead of speaking to a company representative.

Source: GSL May 2016

24

Biggest self-service challenge?

67% contacted a call center after a digital self-service option didn't solve their problem

Source: GSL May 2016

Of the following, what made it less than

satisfactory?

• Problems take too long to resolve 21%

• Suggested solution may not help me 19%

• Confusing to use 16%

#FAIL

25

US consumers prefer self-service options compared to other markets

Only 34% of German respondents were satisfied (Top 2 Box) with self-service vs. 54% of U.S. and 52% U.K. consumers.

Source: GSL May 2016

81% of Germany respondents who didn’t solve their problem via digital self-service, didn’t call after vs. 58% of U.S. and U.K. consumers.

Copyright © 2016 Sapient Corporation

Modern Consumers Want Help Assessing Their Options

27

The top aspects that inform the purchase decision-making process are:

40% How a product is different

46% How the product suits the consumer's needs and requirements specifically

63% Performance, functionality and reliability of the product

Consumers are seeking help understanding the benefits of individual products in purchase decision process

What does it do better?

How does it support my needs?

What does it do?

Source: GSL May 2016

Copyright © 2016 Sapient Corporation | Confidential

The Paradox of Choice

“You have so much choice in the US – you have whole, 1%, 2%, half & half…we just have milk”

- Karen, visiting US from UK

29

Brands need to educate about differences to support the purchase decision process

American consumers were more likely to comparison shop than European consumers

Source: GSL May 2016

67% of U.S. consumers considered multiple

products vs. 57% of British and German

consumers.

30

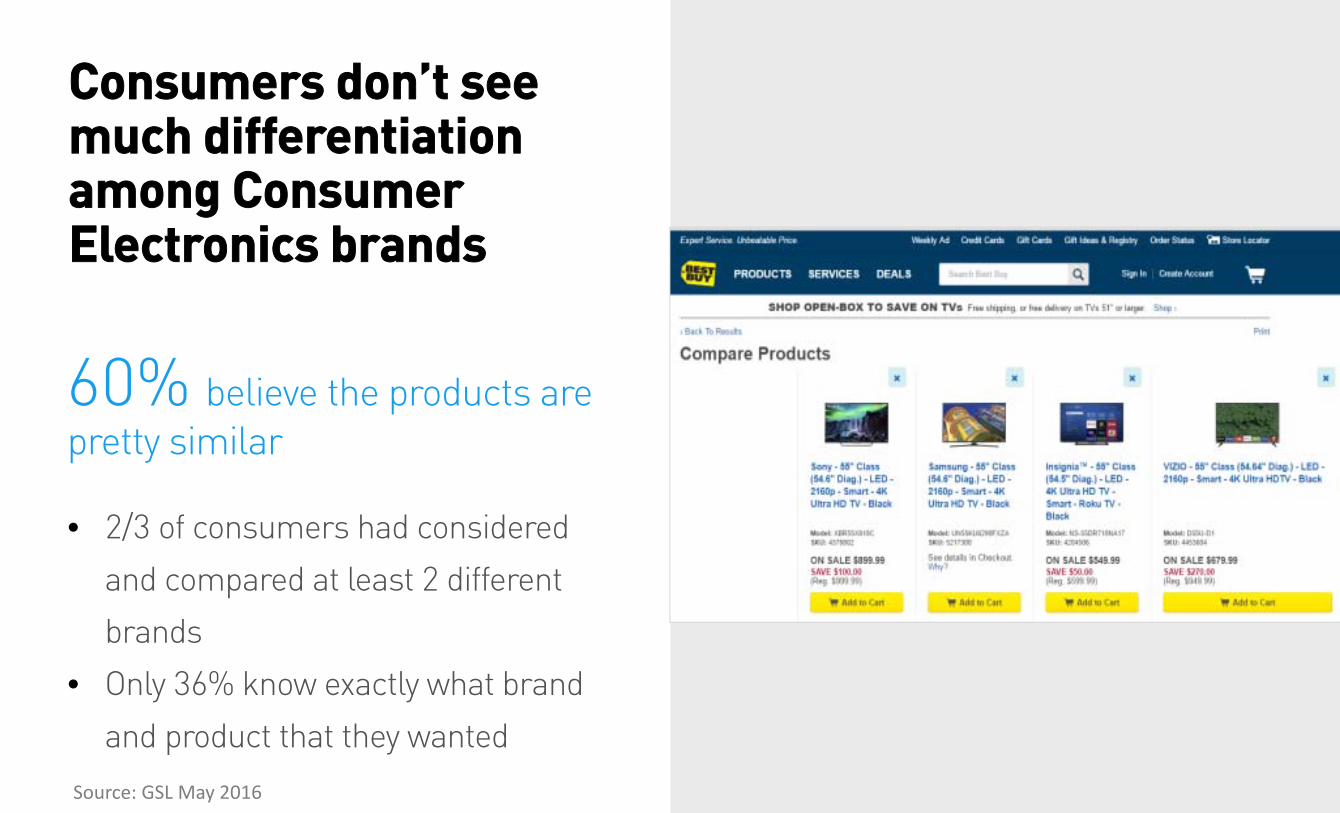

Consumers don’t see much differentiation among Consumer Electronics brands

60% believe the products are pretty similar

Source: GSL May 2016

• 2/3 of consumers had considered

and compared at least 2 different

brands

• Only 36% know exactly what brand

and product that they wanted

MODERN CONSUMERS ARE SEEKINGREDUCED COMPLEXITY

32

Telecom Service providers fail to communicate product benefits and educate customers

53% of people who are less satisfied with their carrier don't understand their mobile phones vs. 85% who are satisfied and do understand their phones

58% of surveyed people who are less satisfied don't understand their mobile plansvs. 84% of the satisfied who do understand their plans

Source: GSL May 2016, Assumes: Correlation between satisfaction and plan understanding

33

Plans are still too complex and not communicated well

20% said it was too difficult to choose between plans

9% of people who are less satisfied with their current plan don’t switch because they find it too confusing to choose

Source: GSL May 2016

34

Good service is the main reason why respondents don’t switch

59% who are satisfied with their current provider rated it due to friendly, knowledgeable, and helpful staff

Source: GSL May 2016

35

SHOPPER EXPECTIONS IN THE DIGITAL AGE

Digital plays a major role in modern purchase

Experience matters

Modern consumers prefer self-service options

Modern consumers are seeking help assessing their options

Modern consumers are seeking reduced complexity

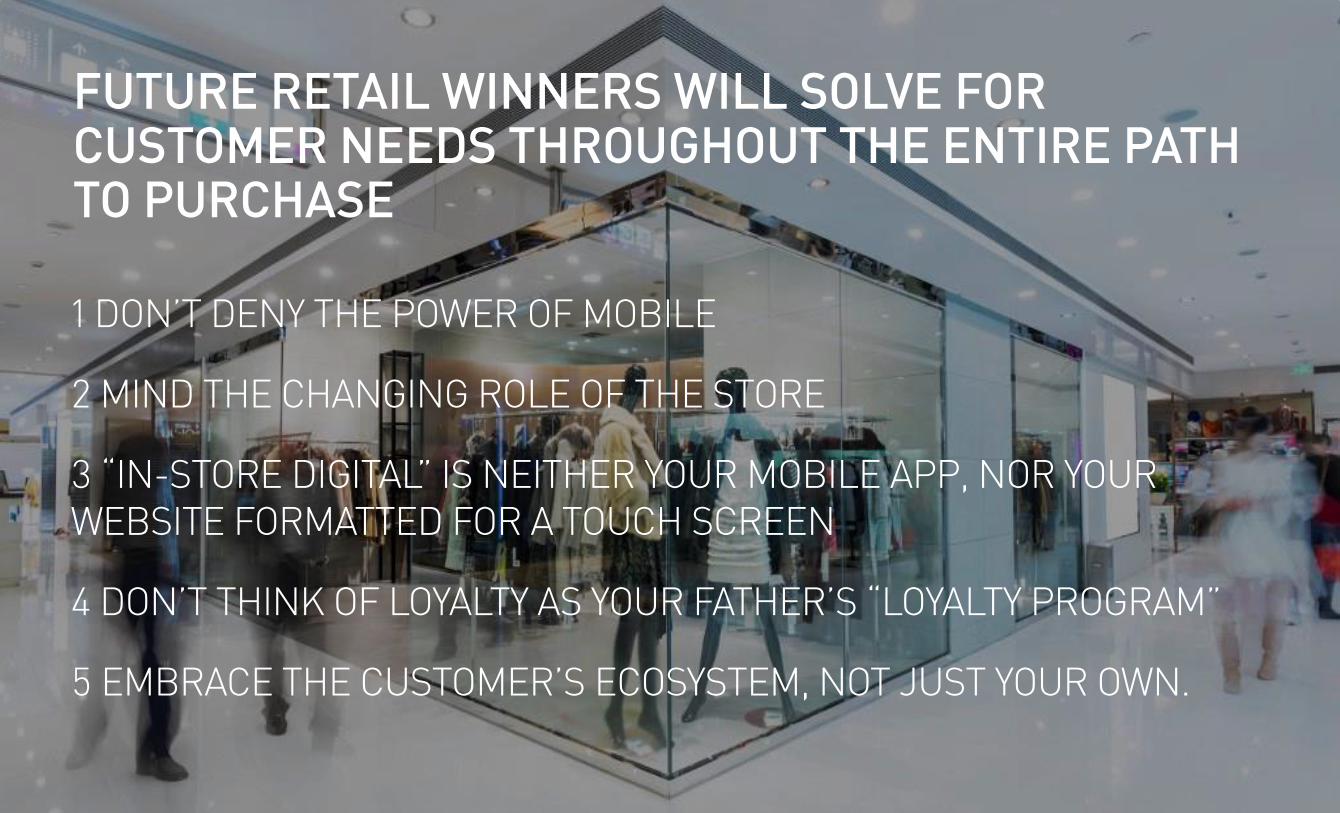

FUTURE RETAIL WINNERS WILL SOLVE CUSTOMER

NEEDS ACROSS THE ENTIRE PURCHASE PATH

37

1 DON’T DENY THE POWER OF MOBILE

Mobile platforms dominate because they connect consumers at all times and places, and help create a more individualized experience

38

MOBILE: TARGET’S CARTWHEEL SAVINGS APP

Encourages increased customer engagement • Scanning• Exclusive offers• Social integration• Game-like rewards

39

MOBILE: TARGET’S CARTWHEEL SAVINGS APP

$1 billion in sales annually *

Cartwheel users spend more per trip and visit more often*

Sources: Chart: comScore Custom Solutions, U.S., Q1 2016*Fortune. “Target Finds Rare Tech Edge: Its Popular Cartwheel Shopping App.” http://fortune.com/2014/06/05/target‐cartwheel/

40

2 MIND THE CHANGING ROLE OF THE STORE

Brick & mortar spaces should expand beyond sales - Media and content ecosystems- Decision support- Deeper service

Ultimately a foothold for all activities, rather than just as its experience journey’s final frame

41

42

43

44

45

46

47

48

49

50

51

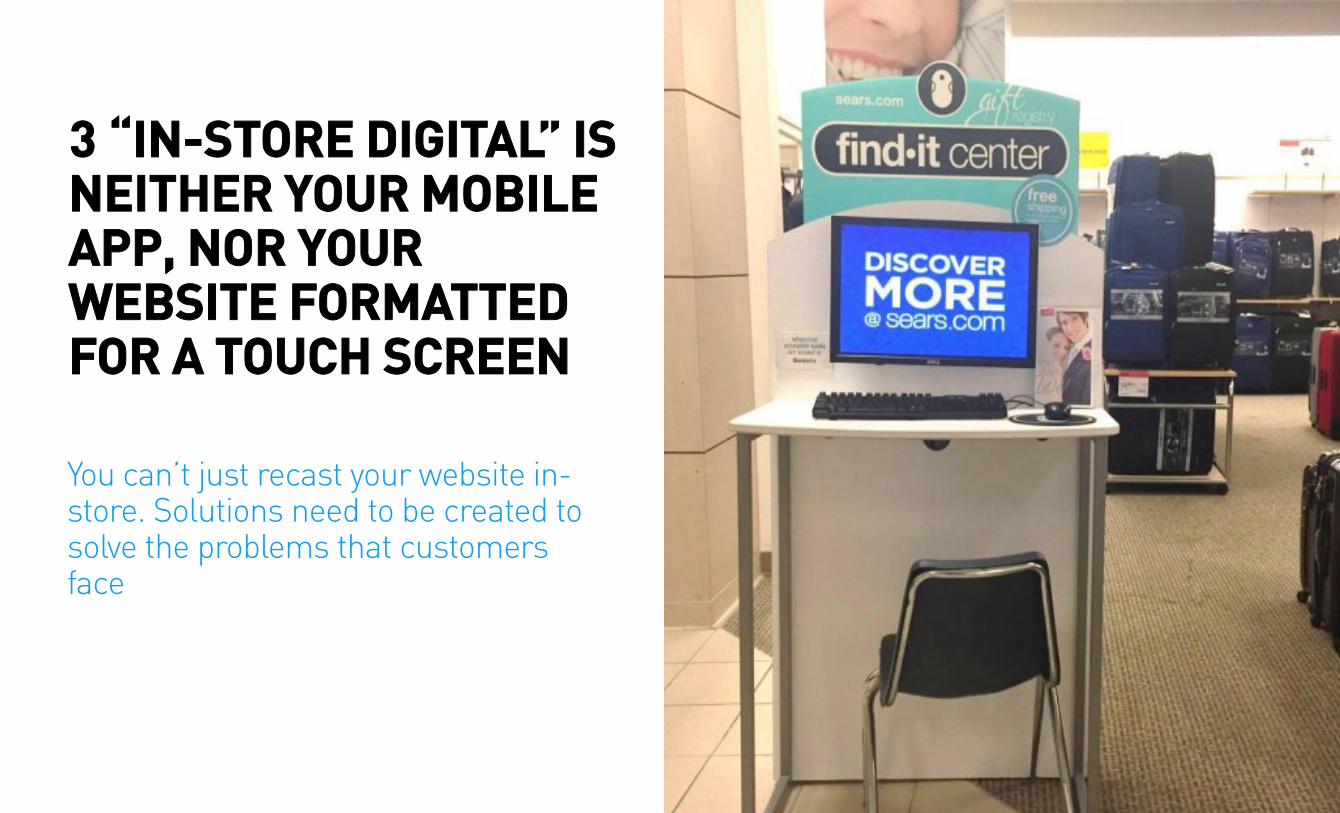

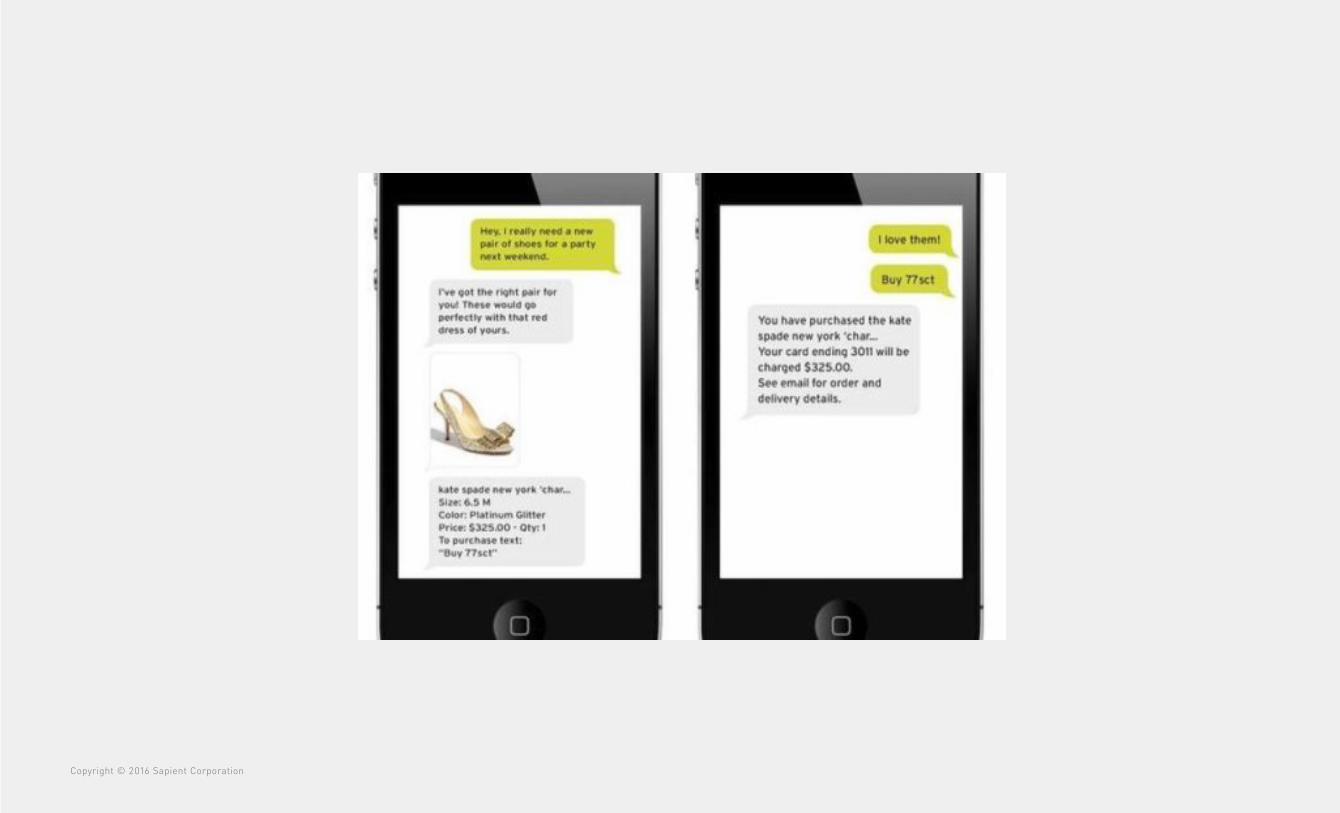

3 “IN-STORE DIGITAL” IS NEITHER YOUR MOBILE APP, NOR YOUR WEBSITE FORMATTED FOR A TOUCH SCREEN

You can’t just recast your website in-store. Solutions need to be created to solve the problems that customers face

56

4 DON’T THINK OF LOYALTY AS YOUR FATHER’S “LOYALTY PROGRAM”

STARBUCKS MOBILE WALLET + ORDER

of all retail transactions are conducted before the customer walks in the door

25%

Source: Business Insider. “Starbucks’ Controversial Rewards Program Changes Drove Almost 1 Million Customers to Join.” http://www.businessinsider.com/starbucks‐new‐rewards‐program‐pays‐off‐2016‐4.

57

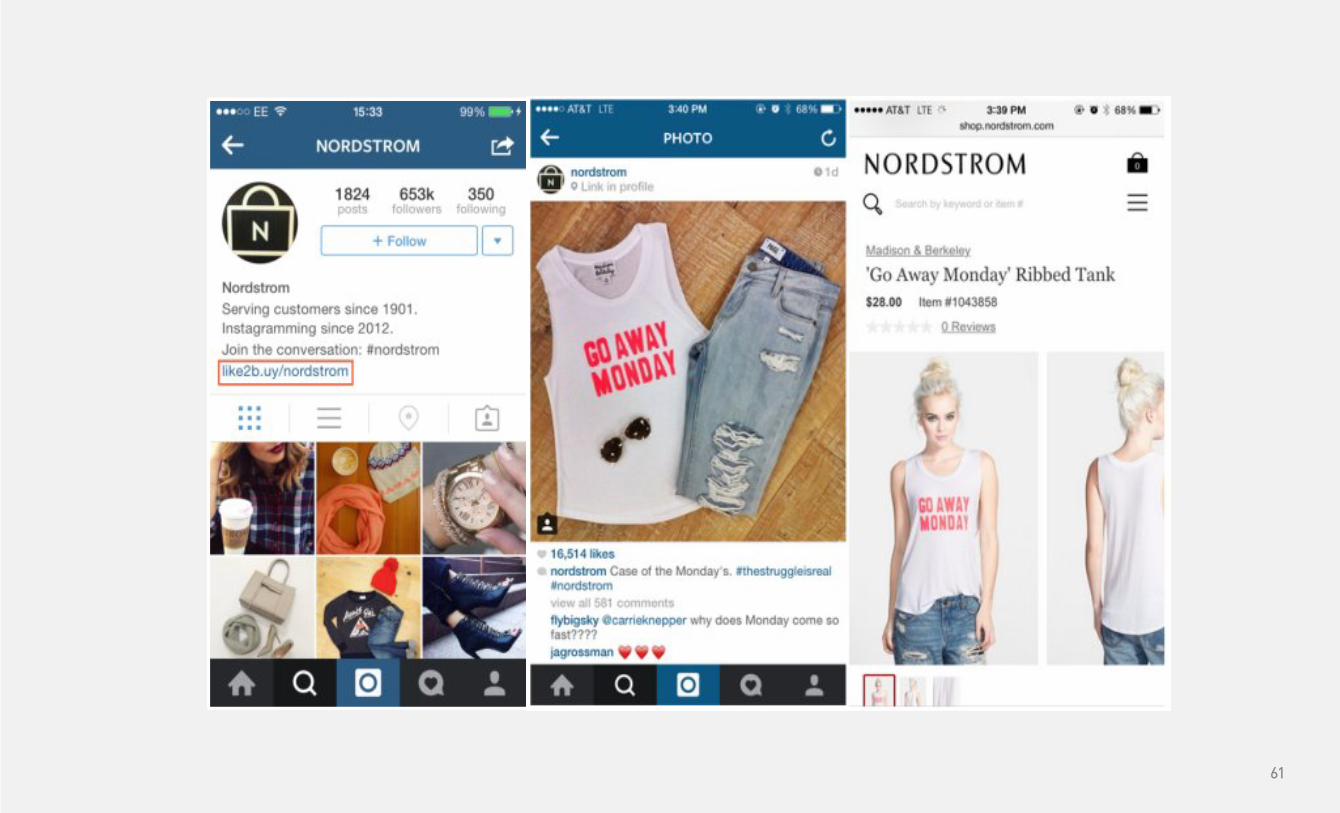

5 EMBRACE THE CUSTOMER’S ECOSYSTEM, NOT JUST YOUR OWN.

Nordstrom is famously focused on great products and stellar customer service

Nordstrom engages uniquely in every channel their customer is in

58

59

60

61

62

Copyright © 2016 Sapient Corporation

Copyright © 2016 Sapient Corporation

65

FUTURE RETAIL WINNERS WILL SOLVE FOR CUSTOMER NEEDS THROUGHOUT THE ENTIRE PATH TO PURCHASE

1 DON’T DENY THE POWER OF MOBILE

2 MIND THE CHANGING ROLE OF THE STORE

3 “IN-STORE DIGITAL” IS NEITHER YOUR MOBILE APP, NOR YOUR WEBSITE FORMATTED FOR A TOUCH SCREEN

4 DON’T THINK OF LOYALTY AS YOUR FATHER’S “LOYALTY PROGRAM”

5 EMBRACE THE CUSTOMER’S ECOSYSTEM, NOT JUST YOUR OWN.

Copyright © 2016 Sapient Corporation

Guided Selling Live!Exclusive Shopper Research

Available Soon

Copyright © 2016 Sapient Corporation

INSIGHTS

Shopper Expectations in the Digital AgeGuided Selling Live!

Copyright © 2016 Sapient Corporation

Gabe WeissRetail Innovation Lead@geedub_nyc