Embed Size (px)

Citation preview

COMMERCIAL REAL ESTATE: 2015 INVESTMENT OUTLOOK

LAWRENCE YUN, PhD

Chief Economist, Sr. VP

National Association of REALTORS®

DONALD E. HUFFNER

Managing Director, Head of Americas

AIG Global Real Estate

RICHARD M. GATTO

Executive Vice President

The Alter Group

ANDREW H. TROTTER, III

Chief Investment Officer

Centennial Holding Company

COMMERCIAL ECONOMIC ISSUES & TRENDS FORUM

Commercial Real Estate Trends and Outlook

Lawrence Yun, Ph.D.Chief Economist

NATIONAL ASSOCIATION OF REALTORS®

Presentation at:NAR Annual Commercial Real Estate Forum

New Orleans, LA

November 7, 2014

Commercial Investment Sales of Large Properties(Properties valued at $2.5 million and over)

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

130

212

362423

571

174

67

147

233299

355400 420 430

Commercial Sales in $Billions

Federal Reserve Commercial Property Price Index

2000 - Q1

2000 - Q4

2001 - Q3

2002 - Q2

2003 - Q1

2003 - Q4

2004 - Q3

2005 - Q2

2006 - Q1

2006 - Q4

2007 - Q3

2008 - Q2

2009 - Q1

2009 - Q4

2010 - Q3

2011 - Q2

2012 - Q1

2012 - Q4

2013 - Q3

0

50

100

150

200

250

300

GDP Reboundin 2014 Q2 and Q3

2007 - Q1

2007 - Q3

2008 - Q1

2008 - Q3

2009 - Q1

2009 - Q3

2010 - Q1

2010 - Q3

2011 - Q1

2011 - Q3

2012 - Q1

2012 - Q3

2013 - Q1

2013 - Q3

2014 - Q1

2014 - Q3

-10

-8

-6

-4

-2

0

2

4

6

GDP Annualized Growth Rate

GDP Still not Robust … Below 3% for 9 straight years

19501953

19561959

19621965

19681971

19741977

19801983

19861989

19921995

19982001

20042007

20102013

-4

-2

0

2

4

6

8

10

GDP Annual Growth Rate

Household Net Worth at All-Time High

2000 - Q1

2000 - Q4

2001 - Q3

2002 - Q2

2003 - Q1

2003 - Q4

2004 - Q3

2005 - Q2

2006 - Q1

2006 - Q4

2007 - Q3

2008 - Q2

2009 - Q1

2009 - Q4

2010 - Q3

2011 - Q2

2012 - Q1

2012 - Q4

2013 - Q3

40000

45000

50000

55000

60000

65000

70000

75000

80000

85000$ billion

Monetary Policy by Federal Reserve (zero rate policy for 6 years!)

2005 2006 2007 2008 2009 2010 2011 2012 2013 20140

1

2

3

4

5

6

Fed Funds %

Federal Reserve Balance Sheet from Quantitative Easing

2005 - Jan 2006 - Apr 2007 - Jul 2008 - Oct 2010 - Jan 2011 - Apr 2012 - Jul0

500000

1000000

1500000

2000000

2500000

3000000

3500000

4000000

Total Asset Purchase

$ million

10-year Treasury Yield

2000 - Jan 2002 - Jan 2004 - Jan 2006 - Jan 2008 - Jan 2010 - Jan 2012 - Jan 2014 - Jan0

1

2

3

4

5

6

7

Non-worrisome CPI Inflation – YetCOLA of 1.7% in 2015

2000 - Jan 2002 - Jan 2004 - Jan 2006 - Jan 2008 - Jan 2010 - Jan 2012 - Jan 2014 - Jan

-3

-2

-1

0

1

2

3

4

5

6

Rising Renters’ and Homeowners’ Rent Growth

(Above 3%)

2003 - Jan 2004 - Jul 2006 - Jan 2007 - Jul 2009 - Jan 2010 - Jul 2012 - Jan 2013 - Jul-1

0

1

2

3

4

5

Owners' Equivalent Rent Renters' Rent

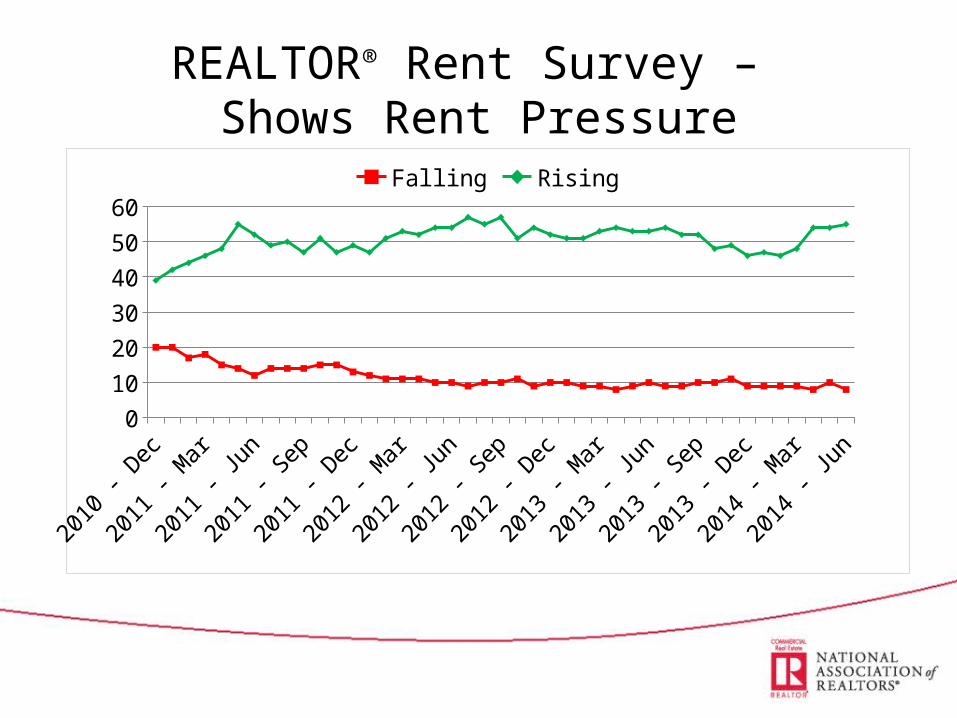

REALTOR® Rent Survey – Shows Rent Pressure

2010 - Dec

2011 - Feb

2011 - Apr

2011 - Jun

2011 - Aug

2011 - Oct

2011 - Dec

2012 - Feb

2012 - Apr

2012 - Jun

2012 - Aug

2012 - Oct

2012 - Dec

2013 - Feb

2013 - Apr

2013 - Jun

2013 - Aug

2013 - Oct

2013 - Dec

2014 - Feb

2014 - Apr

2014 - Jun

0

10

20

30

40

50

60

Falling Rising

Oil Price

2000 - Jan 2002 - Jan 2004 - Jan 2006 - Jan 2008 - Jan 2010 - Jan 2012 - Jan 2014 - Jan0

20

40

60

80

100

120

140

160

U.S. Dollar Strength vs Euro

2000 - Jan 2002 - Jan 2004 - Jan 2006 - Jan 2008 - Jan 2010 - Jan 2012 - Jan 2014 - Jan0.8

0.9

1

1.1

1.2

1.3

1.4

1.5

1.6

1.7

$US per One Euro

U.S. Dollar Weakness vs Chinese Yuan

2000 - Jan 2002 - Jan 2004 - Jan 2006 - Jan 2008 - Jan 2010 - Jan 2012 - Jan 2014 - Jan6

6.5

7

7.5

8

8.5

Yuan per $1

Monetary Policy

• Quantitative Easing … Finished

• Fed Funds Rate … hike in 2015 Q1/Q2

• Earlier Move to Tighten because of Inflation Pressure

• Long-term Steady State Rate (2016 onwards) .. 10 year Treasury at 5.0%

• Mortgage Rates reaching 6% by 2016

Jobs(8 million lost … 10 million gained)

2000 - Jan 2002 - Apr 2004 - Jul 2006 - Oct 2009 - Jan 2011 - Apr 2013 - May124000

126000

128000

130000

132000

134000

136000

138000

140000

142000In thousands

Weekly New Unemployment Insurance Claims

2000 - Jan 2002 - Jan 2004 - Jan 2006 - Jan 2008 - Jan 2010 - Jan 2012 - Jan 2014 - Jan250

300

350

400

450

500

550

600In thousands

Job Market Comparisons by StateFast Growing States 1-year Growth Rate

North Dakota 4.5

Nevada 3.7

Texas 3.4

Florida 2.9

Utah 2.9

Colorado 2.8

Oregon 2.7

Delaware 2.6

West Virginia 2.5

California 2.2

Slow Moving States 1-year Growth Rate

Michigan 0.7

Alabama 0.6

Wyoming 0.6

South Dakota 0.3

Virginia 0.3

New Jersey 0.1

Illinois 0.0

Alaska 0.0

New Mexico -0.1

Vermont -0.2

REALTOR® Markets & Deal Size(Not $2.5 million Properties)

< $250,000

$250,000 - $500,000

$500,000 - $1,000,000

$1,000,000 - $2,000,000

$2,000,000 - $5,000,000

$5,000,000 - $10,000,000

> $10,000,000

21%

22%

26%

17%

12%

1%

2%

2013 CRE Lending Survey: Value of most recent sales transaction

Source: NAR

8%

17%

25%

7%6%

4%

18%

1% 11%

3%Current sources of financing for commercial dealsNational banks (“Big four”)

Regional banks

Local banks

Credit unions

Life insurance companies

REITs

Private investors

Public companies

Small Business Administration

Other, please specify

Source: NAR

Small Banks Important to REALTORS®

NAR Member Commercial Activity Survey2nd Quarter, 2014

• Sales volume rose 7% YoY

• Sales prices increased 3% YoY

• Cap rates averaged 8.3%

Main market challenges:

• Inventory shortage

• Pricing gap between buyers and sellers

• Local economies

REALTORS® Help Small Businesses

< $250,000

$250,000 - $499,999

$500,000 - $999,999

$1,000,000 - $1,999,999

$2,000,000 - $4,999,999

$5,000,000 - $10,000,000

$10,000,000 <

16%

25%

25%

17%

10%

4%

3%

Average Value of Sale Transaction

2011 2012 2013 20140%

10%

20%

30%

40%

50%

60%

70%

80%

Did you close a sale in the past 12 months?

Yes No N/A

Credit Difficulty

2011 2012 2013 20140%

10%

20%

30%

40%

50%

60%

70%

80%

Sales transaction fail during the past 12 months due to lack of financing

Yes No N/A

17%

63%

20%

If answered "Yes," the reason was:

Financing availabilityLoan underwrit-ing / lender re-quirementsAppraisal / valuation

A Typical Commercial REALTOR®

BUSINESS REVENUE AND FIRM AFFILIATION

• The median gross annual income of commercial members was $96,200 in 2013, an increase from $90,200 in 2012. The median gross annual income of commercial members has increased for the past four years.

• Eighty percent of commercial members work at least 40 hours a week.

• Sixty-two percent of commercial members of NAR derived 50 percent or more of their income from all commercial real estate in 2013.

• Fifty-seven percent of members work for a local commercial real estate firm.

BUSINESS ACTIVITIES OF NAR COMMERCIAL MEMBERS

• Commercial members completed a median of eight transactions in 2013.

• The median sales transaction volume in 2013 for members who had a transaction was $2,554,700 – an increase from $2,507,700 in 2012.

• The median gross leasing volume was $431,600 in 2013– a decrease from the $476,400 in 2012.

CCIM Member Survey on Cap Rates

2005.Q3

2006.Q1

2006.Q3

2007.Q1

2007.Q3

2008.Q1

2008.Q3

2009.Q1

2009.Q3

2010.Q1

2010.Q3

2011.Q1

2011.Q3

2012.Q1

2012.Q3

2013.Q1

2013.Q3

2014.Q1

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0 SIOR Index

Industrial Office

Sources: SIOR, NAR

SIOR Member Survey on Activity

Economic Forecast2013 2014

Likely2015

Forecast2016

ForecastGDP Growth 2.2% 2.2% 2.7% 2.9%

Job Growth +2.3 million +2.5 million +2.5 million +2.6 million

CPI Inflation 1.5% 1.6% 2.7% 3.3%

Consumer Confidence

73 87 95 98

10-year Treasury

2.5% 2.6% 3.2% 4.3%

OFFICE 2014 2015 2016Vacancy Rate 16.2% 15.8% 15.6%Net Absorption ('000 sq. ft.) 36,192 50,678 57,782Completions ('000 sq. ft.) 26,450 41,799 44,862Rent Growth 2.6% 3.2% 3.6%

INDUSTRIAL 2014 2015 2016Vacancy Rate 8.9% 8.5% 8.1%Net Absorption ('000 sq. ft.) 107,580 104,948 105,044Completions ('000 sq. ft.) 83,424 68,755 61,720Inventory ('000,000 sq. ft.) 8,468 8,537 8,598Rent Growth 2.4% 2.8% 2.9%

RETAIL 2014 2015 2016Vacancy Rate 9.8% 9.7% 9.4%Net Absorption ('000 sq. ft.) 11,214 19,314 24,313Completions ('000 sq. ft.) 7,275 12,196 16,342Rent Growth 2.0% 2.4% 3.0%

MULTI-FAMILY 2014 2015 2016Vacancy Rate 4.0% 4.0% 4.2%Net Absorption (Units) 223,421 170,065 140,128Completions (Units) 191,481 146,461 122,381Rent Growth 4.0% 3.9% 3.5%

Sources: National Association of REALTORS® / Reis, Inc.

Commercial Real Estate Forecast

Washington Policy Watch onCommercial Real Estate

• Facilitate Covered Bonds to help credit flow

• Raise cap on holding of commercial RE loans by credit unions

• Preserve Like-Kind Exchanges

• Preserve Terrorism Insurance

• Preserve capital gains status on carried interest

• Depreciation Rules should match economic life

• Oppose lease-accounting changes

Richard M. GattoExecutive Vice President

The Alter Group

Donald E. HuffnerManaging Director, Head of the

AmericasAIG Global Real Estate

Andrew H. Trotter, IIIChief Investment Officer

Centennial Holding Company

COMMERCIAL REAL ESTATE: 2015 INVESTMENT OUTLOOK

LAWRENCE YUN, PhD

Chief Economist, Sr. VP

National Association of REALTORS®

DONALD E. HUFFNER

Managing Director, Head of Americas

AIG Global Real Estate

RICHARD M. GATTO

Executive Vice President

The Alter Group

ANDREW H. TROTTER, III

Chief Investment Officer

Centennial Holding Company

COMMERCIAL ECONOMIC ISSUES & TRENDS FORUM