Embed Size (px)

Citation preview

2014 Real Estate Market Update & 2015 Outlook

January 22, 2015

Presented by:

about myself

American National

More than 6 years experience in the local real estate industry

Winner of the 2014 Asia CEO Top Young Leader Award

Oversees sales, investments, and agency teams

Also founded KMC Solutions, a facilities and technology

outsourcing services provider

Previously worked in Silicon Valley (San Francisco Bay Area,

California) as a software and IT consultant from 2003 - 2007

kmc mag group introduction

Incorporated in 2009

Full Service Real Estate Firm

International Associate of Savills

Founders: Atty. Amanda Carpo, Michael

McCullough and Gregory Kittelson

Headquarters: Sun Life Centre, Bonifacio Global City

Globally recognized as Best Philippine Real

Estate Agency Award by the International

Property Awards

Over 100 competitive staff employed

300+ companies

assisted in the last few years in their business set up in the Philippines

230,000+ square meters of commercial & residential properties which were leased and sold for

as of 2014

Strong Media Exposure

major regional trends 2015

today’s topics

property trends - philippines

office market update

residential market update

key industry issues & challenges

10 things to look out for in the next 10 years

asia-pacific… sustainability

Source: Savills Research & Consultancy and KMC MAG Group Research

major regional trends 2015

The outlook for the Asia and Pacific region remains solid

Asia to remain the most dynamic region in the world

Vigilance and further reforms needed to sustain

momentum

GDP is forecast to grow by 5.5% in 2014, rising slightly to

5.6 % in 2015

Philippines among the top countries with 5.3% (3Q14)

Global QE and its impact on Asia?

Not US so much as Europe, Japan and China

Interest rate rises in 2015?

Real estate in China?

Cooling measures in Singapore, HK and China

Investor sentiment – core assets are scarce so must move up

on risk curve

Source: KMC MAG Group Research, NSCB, IMF

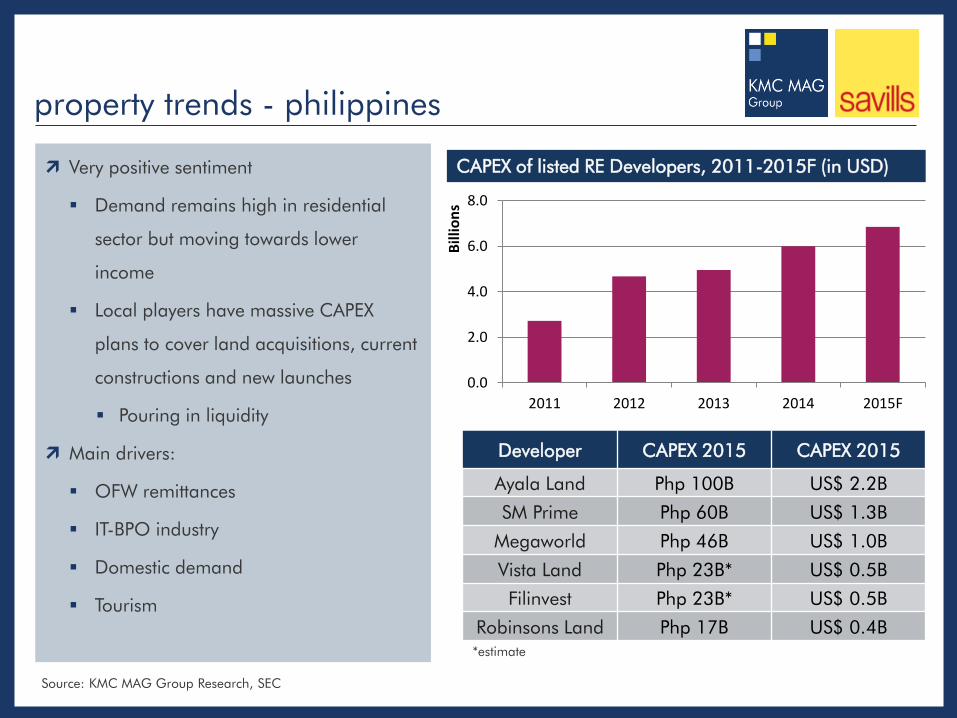

property trends - philippines

Very positive sentiment

Demand remains high in residential

sector but moving towards lower

income

Local players have massive CAPEX

plans to cover land acquisitions, current

constructions and new launches

Pouring in liquidity

Main drivers:

OFW remittances

IT-BPO industry

Domestic demand

Tourism

66% 9%

21%

4%

Office

Other

Dev site

Hotel

Transaction volume by type of use, last 12 months

Developer CAPEX 2015 CAPEX 2015

Ayala Land Php 100B US$ 2.2B

SM Prime Php 60B US$ 1.3B

Megaworld Php 46B US$ 1.0B

Vista Land Php 23B* US$ 0.5B

Filinvest Php 23B* US$ 0.5B

Robinsons Land Php 17B US$ 0.4B

Source: KMC MAG Group Research, SEC

0.0

2.0

4.0

6.0

8.0

2011 2012 2013 2014 2015F

Bill

ion

s

CAPEX of listed RE Developers, 2011-2015F (in USD)

*estimate

property cycle - PH

Mid end residential Hotel and Leisure

Luxury residential Office Industrial

Retail

Late upswing Early downswing Late downswing Early upswing

Sustained growth in demand, increasing construction

Positive but falling demand, increasing vacancy

Increasing demand, decreasing vacancy

Falling demand, decreasing vacancy

Source: KMC MAG Group Research

property trend questions

Questions?

business districts

Several emerging business districts are about to rise in the near future

Most anticipated are Bay City and Quezon City

Challenge for infrastructure on how to connect these together

Source: KMC MAG Group Research

the BPO industry in the Philippines

#2 in non-voice

complex

Began emerging in

2000

Growth at an annual rate of

26 percent over a decade

890,000 direct employees

by 2013

US$16

billion in revenues

2.0 million indirect

employees

Serving North America Asia EU

20+ sectors

Over 700 IT-

BPO companies and Global In-house Centers

Source: Business Process Association Philippines (BPAP)

3.2

4.8 6.1

7.1

8.9

11.0

13.6

16.0

18.0

25.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

-

5.0

10.0

15.0

20.0

25.0

30.0

2006 2007 2008 2009 2010 2011 2012 2013 2014F 2016F

Pers

ons

(mill

ion)

US$

(bill

ion)

Industry revenues Direct employment No signs of slowing down

Manila now the 2nd best outsourcing destination by Tholons

Concerted industry efforts and continued government support can get sector to US$20 billion by 2016

Strengthened public-private partnership can increase this to US $25 billion.

Average office space per employee is roughly 6 sqm/person, resulting in the annual demand of roughly 900,000 sqm for office space

CAGR 26%

CAGR ~18%

philippines IT-BPO industry

Source: Business Process Association Philippines (BPAP)

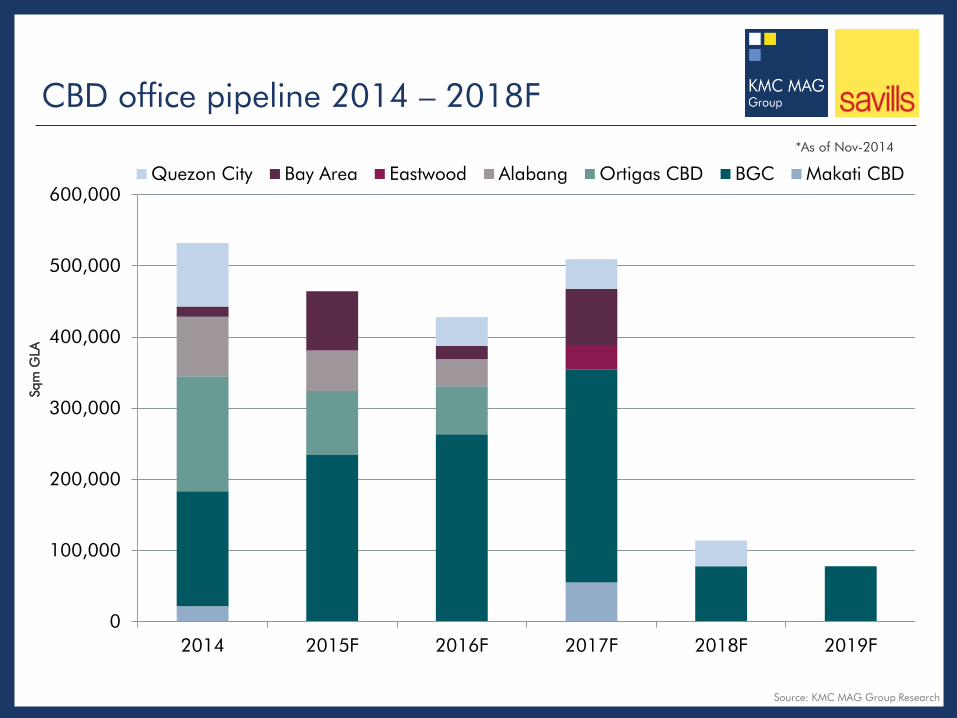

premium and grade a office supply (sq m of GLA)

Source: KMC MAG Group Research

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015F2016F2017F2018F2019F

Quezon City Bay Area Eastwood Alabang Ortigas CBD BGC Makati CBD

CBD office pipeline 2014 – 2018F *As of Nov-2014

Sqm

GLA

0

100,000

200,000

300,000

400,000

500,000

600,000

2014 2015F 2016F 2017F 2018F 2019F

Quezon City Bay Area Eastwood Alabang Ortigas CBD BGC Makati CBD

Source: KMC MAG Group Research

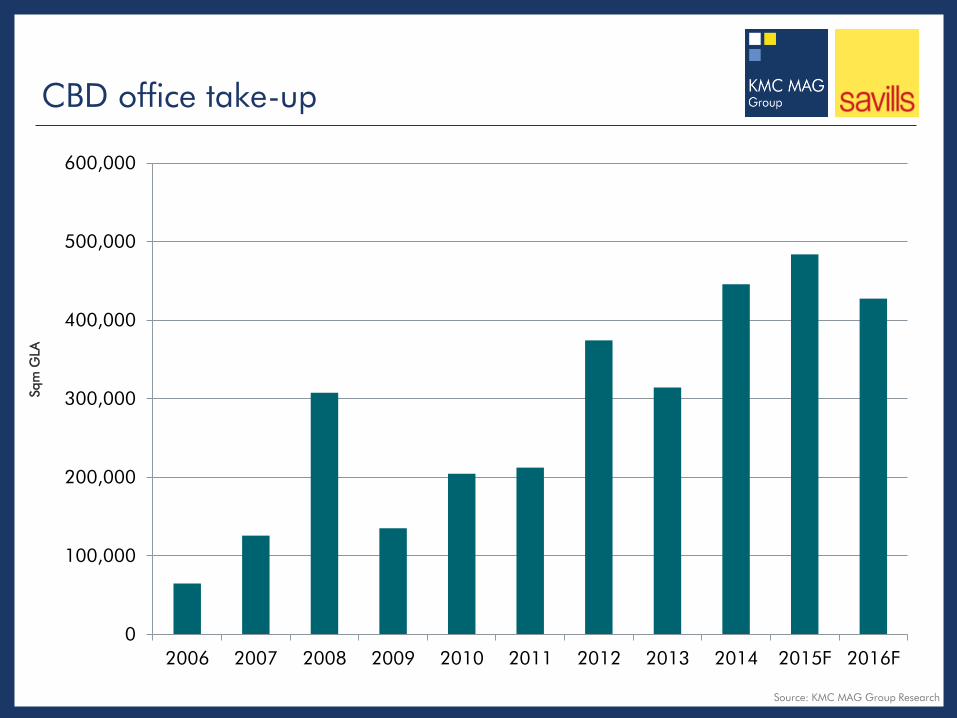

0

100,000

200,000

300,000

400,000

500,000

600,000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015F 2016F

CBD office take-up

Sqm

GLA

Source: KMC MAG Group Research

investor demand stays high

Leasing activity is

expected to continue and

reach new heights next

year

O&O industry

Tech sector

However, high liquidity in

the system will probably

keep the capital values

outpacing the rental

growth

Cap between capital values and rents is widening

Yield compression

Source: BSP, KMC MAG Group Research

0.0

50.0

100.0

150.0

200.0

250.0

300.0Grade A Office: Rental Index Grade A Office: Price Index

still a yield driven market

As a result of investment

rating upgrades, the

government’s borrowing cost

has reduced significantly

Making real estate look attractive

Despite the small yield compression, the yield spread has actually increased and is historically wider than ever

Suggesting undervalued Grade A Office

Source: PDEX, KMC MAG Group Research

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%Grade A Office: Yield Government Bonds: 10 Years

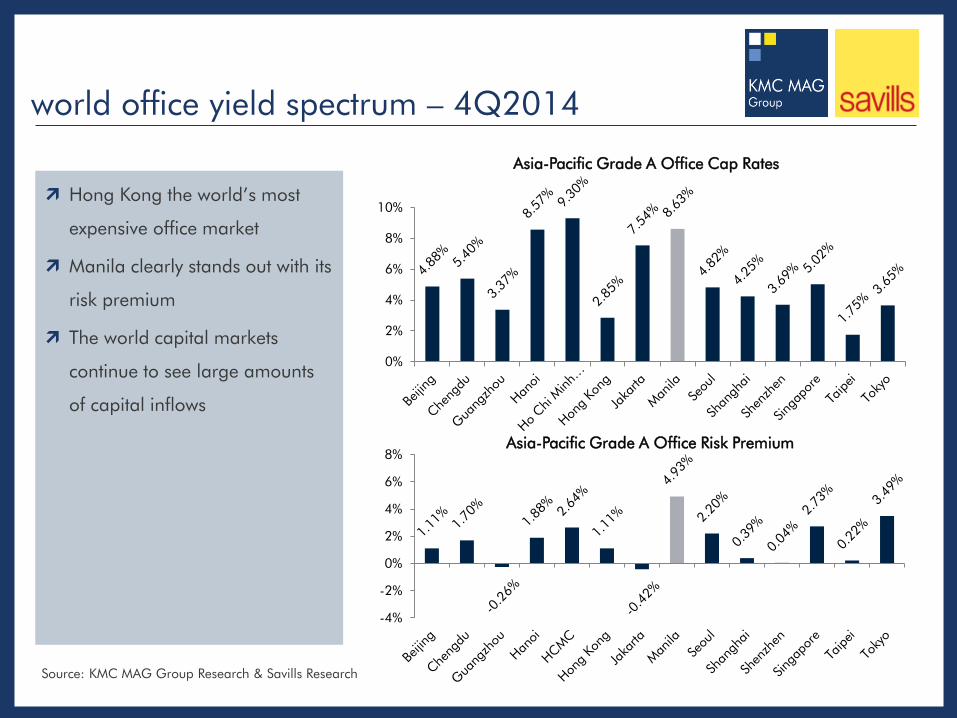

world office yield spectrum – 4Q2014

Hong Kong the world’s most

expensive office market

Manila clearly stands out with its

risk premium

The world capital markets

continue to see large amounts

of capital inflows

0%

2%

4%

6%

8%

10%

Asia-Pacific Grade A Office Cap Rates

-4%

-2%

0%

2%

4%

6%

8%Asia-Pacific Grade A Office Risk Premium

Source: KMC MAG Group Research & Savills Research

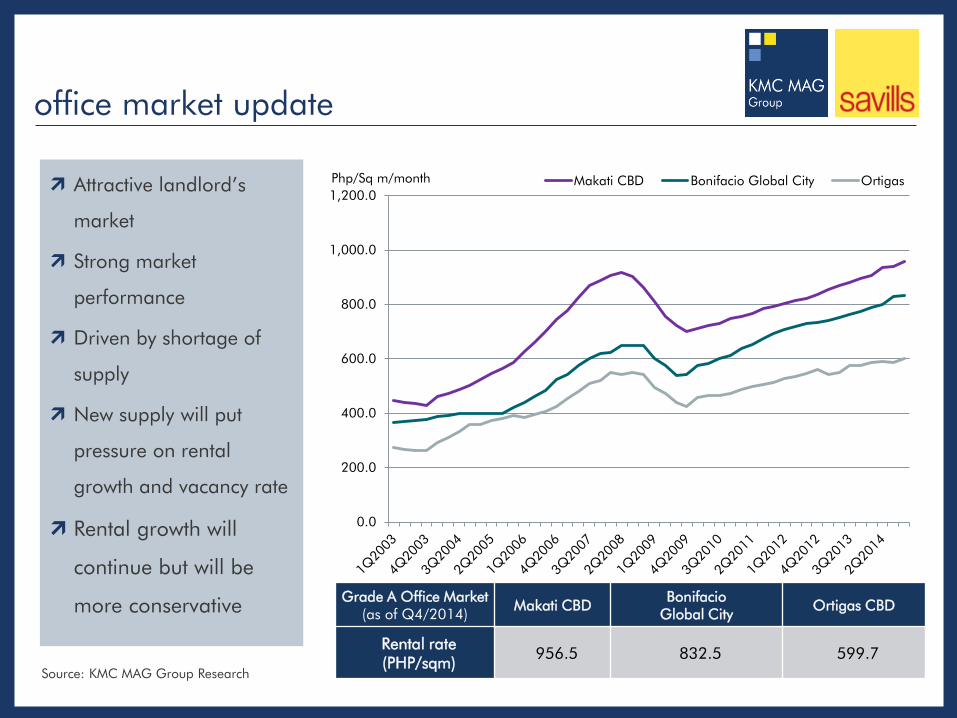

office market update

Attractive landlord’s

market

Strong market

performance

Driven by shortage of

supply

New supply will put

pressure on rental

growth and vacancy rate

Rental growth will

continue but will be

more conservative

Source: KMC MAG Group Research

Grade A Office Market (as of Q4/2014)

Makati CBD Bonifacio

Global City Ortigas CBD

Rental rate (PHP/sqm)

956.5 832.5 599.7 Source: KMC MAG Group Research

0.0

200.0

400.0

600.0

800.0

1,000.0

1,200.0

Php/Sq m/month

Makati CBD Bonifacio Global City Ortigas

trends in flexible work spaces

More and more companies looking towards

flexible work space options

Total capacity of 3 years ago will be built in

this year alone

Demand is expected to remain healthy in the

PH due to high occupancy and lease rates of

CBD buildings

Source: KMC MAG Group Research

Source: KMC MAG Group Research *Recently acquired by Regus

PH Largest Providers

Rank Providers Centres

1 Regus 13

2 KMC Solutions 8

3 Servcorp 2

4 Nomad Offices* 1

5 New Wave Offices 1

residential market update

Average rent Q3 2014 (Php/sqm)

QoQ Growth

Cap Rate

Makati CBD 773.0 0.6% 6.8%

Bonifacio Global City

880.17 0.7% 6.3%

Ortigas CBD 700.6 0.8% 5.7%

Slight increase in average rental rates from Q2

2014

Positive demand for residential market

Focus of developers is shifting to the low end

segments from the luxury segment

Middle income market keeps demand buoyant

Source: KMC MAG Group Research

residential stock 2013-2017F

BGC will almost double the supply in 5 years

Ayala:

HSS South Block

Avida projects in Uptown

Federal Land

Veritown Fort

Megaworld

Forbestown

Uptown

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

2013 2014F 2015F 2016F 2017F

Makati CBD Rockwell BGC Ortigas

Source: KMC MAG Group Research

end of office & residential updates

Questions?

property bubble|the central bank’s measures

The high activity has raised

issues of an overheated

property market

The Central Bank introduced

stress tests

Macro prudential measures

Ensure the banking

industry’s healthy exposure

to real estate lending

Good initiative to stabilise

liquidity and restrain

speculation

This will gear up the economy

for the possible normalization

of global interest rates 0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

0.0

100.0

200.0

300.0

400.0

500.0

600.0

700.0In Billions PHP

Commercial REL Residential REL Bank Average Lending Rate Reverse Repo Rate

Real estate loans and interest rates, 1999-1H/2014

Source: KMC MAG Group Research

upcoming cbd|quezon city

What makes Quezon City the next CBD?

Largest city in Metro Manila

Location of numerous government offices

and headquarters of PNP & AFP

Home of major broadcasting networks

Major educational institutions

Extensive railroad and road network

What areas does QC need to become a full-

fledged CBD?

Infrastructure interconnecting the sub-

districts

Public transport options

Source: KMC MAG Group Research

Average Rental Rate PHP 635.4/sq.m

Vacancy Rate 3.5%

0

100,000

200,000

300,000

400,000

500,000

Quezon City Grade A office stock sqm of GLA

upcoming cbd|bay city

What makes Bay City the next CBD?

Entertainment City

Future tourism hotspot

Multiple business parks being built:

Aseana City

Metropolitan Park (Metrobank Group)

Future City (SM)

What areas does Bay City need to become

a full-fledged CBD?

Proper support infrastructure (roads,

public transport, healthcare, etc.)

Source: KMC MAG Group Research

Average Rental Rate PHP 589.2/sq.m

Vacancy Rate 2.04%

0

100,000

200,000

300,000

400,000

500,000

Bay City Grade A office stock sqm of GLA

decongesting metro manila

Key to decongesting Metro Manila is

fixing the traffic and transport system

Poor infrastructure costs the PH P2.4B/day

All things needed to improve the situation

is ready and waiting for the go signal

The plans are there: JICA Study

The money is there: the Philippines has

the best credit ratings it has ever had

(cheaper debt)

Why is there no go signal?

Main issue is lack of political will

Source: KMC MAG Group Research, JICA, NEDA

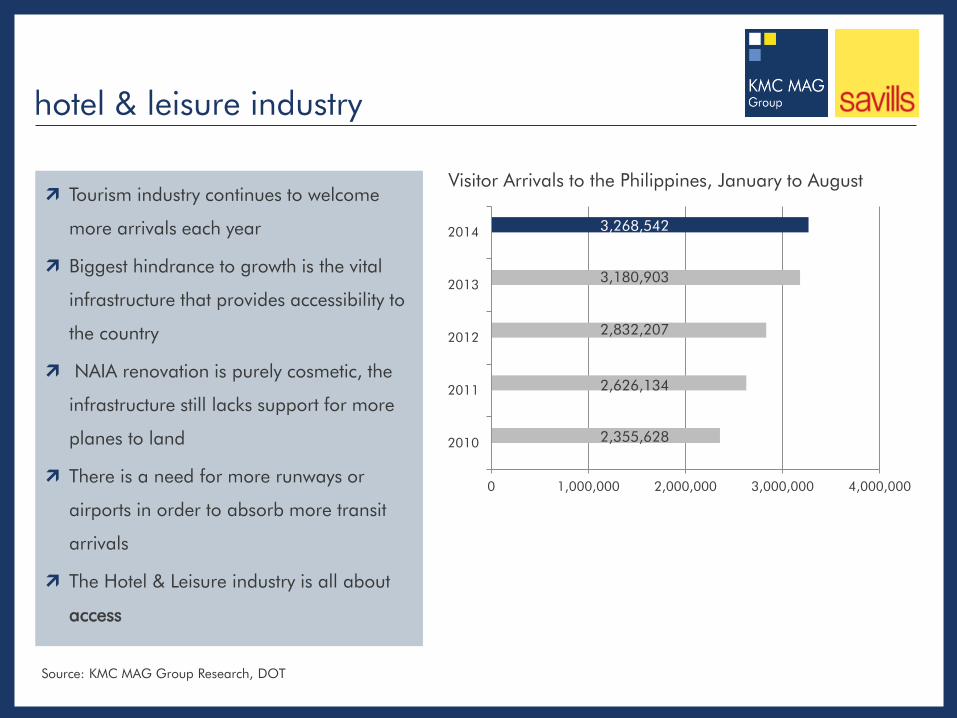

hotel & leisure industry

Tourism industry continues to welcome

more arrivals each year

Biggest hindrance to growth is the vital

infrastructure that provides accessibility to

the country

NAIA renovation is purely cosmetic, the

infrastructure still lacks support for more

planes to land

There is a need for more runways or

airports in order to absorb more transit

arrivals

The Hotel & Leisure industry is all about

access

0 1,000,000 2,000,000 3,000,000 4,000,000

2010

2011

2012

2013

2014

Visitor Arrivals to the Philippines, January to August

2,355,628

2,626,134

2,832,207

3,180,903

3,268,542

Source: KMC MAG Group Research, DOT

hotel & leisure industry

Outside of Metro Manila, developers are focusing on Cebu, Boracay, and Palawan particularly in

El Nido and San Vicente

Source: KMC MAG Group Research

Lio

Developed by Ayala Land

Located in El Nido, Palawan

Mactan Newtown

Developed by Megaworld

Located in Mactan, Cebu

Boracay Newcoast

Developed by Megaworld

Located in Boracay

Sta. Barbara

Developed by Megaworld

Located in Iloilo

Rents Capital Values

Yields Vacancy Supply

Office

Residential

Retail

property forecast

Source: KMC MAG Group Research

The outlook for the Asia and Pacific region and remains solid

All property sectors will benefit from current economic growth

Risks lie ahead in global monetary policy

Rising Tigers, Sleeping Giant – ASEAN & China

Investor appetite – more opportunistic

Local developers very cash rich and hoarding real estate

10 things to look out for over the next ten years

1 Global Monetary Policy

2 Infrastructure Spending (PPP)

10 Financial sector: • deregulation of supporting sectors, easier flow of personnel

5 ASEAN integration

4 Middle class consumers

8 Exchange rates

7 Movement to/development of suburbs

6 Elections 2016: • changes to foreign ownership restrictions?

3 BPO-Industry

9 Quality developments

Source: KMC MAG Group Research

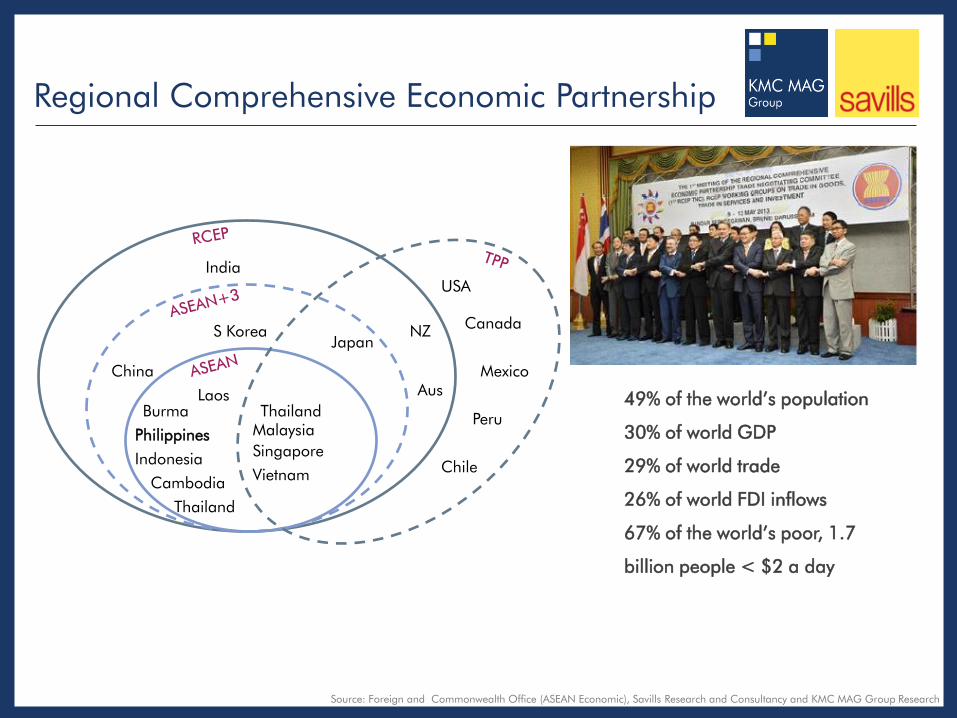

Regional Comprehensive Economic Partnership

India

China

S Korea Japan

NZ

Aus

USA

Canada

Mexico

Peru

Chile

Laos Burma

Philippines

Indonesia

Cambodia

Thailand

Thailand Malaysia

Singapore

Vietnam

49% of the world’s population

30% of world GDP

29% of world trade

26% of world FDI inflows

67% of the world’s poor, 1.7

billion people < $2 a day

Source: Foreign and Commonwealth Office (ASEAN Economic), Savills Research and Consultancy and KMC MAG Group Research

2014 Real Estate Market Update & 2015 Outlook

January 22, 2015

Presented by: