Embed Size (px)

Citation preview

SWIFT_Digitisation_Prateek Roongta_vF.pptx 0

DIGITISATION AND DEMONETISATION Evolving into a cashless economy

Prateek Roongta Partner and Director, BCG

6th April 2017

India and Subcontinents

Regional Conference

Mumbai

6 April 2017

SWIFT_Digitisation_Prateek Roongta_vF.pptx 1

Payments in India have evolved rapidly

The payments space has witnessed large scale disruption

• Digital at the heart and centre – innovative, mobile based solutions

being deployed

• Entry of non-banks as payments service providers – threatens

disintermediation of banks

Consumer needs and expectations are evolving rapidly

Banks are responding rapidly in order to retain their customers and balances

• Guided by the experience offered by e-commerce players like

Amazon and Uber

• Increasing mobile and internet penetration provides further impetus

• Thinking like "non-banks" to deliver cutting-edge payments

experience

SWIFT_Digitisation_Prateek Roongta_vF.pptx 2

Digital payments gaining traction

639

389

172

9553

0

200

400

600

800

1,000

Number of transactions (million)

+86%

2016-

20171

2015-

16

2014-

15

2013-

14

2012-

13

814

604

255

108

33

0

200

400

600

800

1,000

Number of transactions (million)

+123%

2016-

171

2015-

16

2014-

15

2013-

14

2012-

13

Mobile Banking Mobile Wallets

Value

INR billion 60 224 1,035 10 29 82

2,367 6,022 306 270 321 INR / Txn

206

341

4,040

10,375

8,704

13,631

307

377 1,124

Note: 1. 9months data is taken for 2016-17 Source: RBI; Payment System Indicators.

SWIFT_Digitisation_Prateek Roongta_vF.pptx 3

Customers exploring digital payments beyond mobile recharge

22

29313136

5155

66

1620

28

1814

29

22

73

0

80

60

40

20

% respondents

Other

service

s

In store

(POS)

Fund

transfer

Travel

booking

Ecommerce Other

utility bills

Mobile bill

payment

Use cases

Prepaid

mobile

recharg

e

Non metro users Metro Users

POS payment and usage for other services low

Bill payment second largest use case

Prepaid recharge still the largest use case across metro and non metros

Source: Google-BCG market study based on Nielsen consumer survey Question: For what all purposes have you ever used a digital payments instrument?

SWIFT_Digitisation_Prateek Roongta_vF.pptx 4

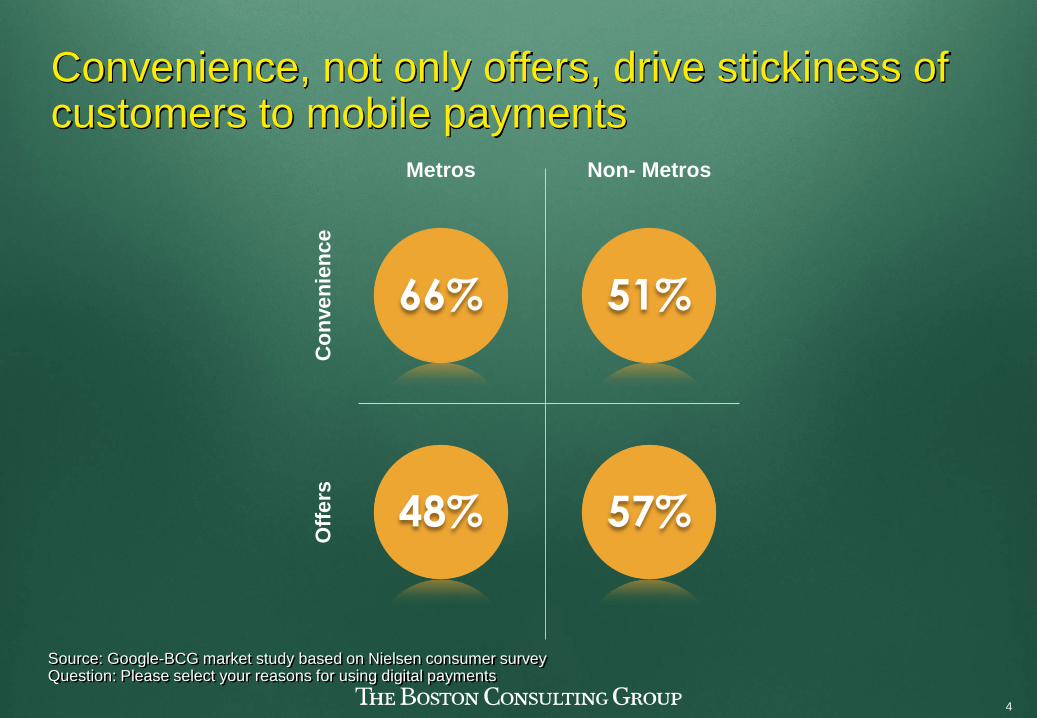

Convenience, not only offers, drive stickiness of customers to mobile payments

Co

nve

nie

nc

e

Off

ers

Metros Non- Metros

66% 51%

48% 57%

Source: Google-BCG market study based on Nielsen consumer survey Question: Please select your reasons for using digital payments

SWIFT_Digitisation_Prateek Roongta_vF.pptx 5

Customers open to using digital at physical POS

48

49

52

61

66

71

73

40 60 80 20 0 %

Unorganized retail

Travel and transport

Professional services

Utility bills

E-commerce

Organized retail

Food and entertainment

Large format POS use cases

Source: Google-BCG market study based on Nielsen consumer survey Question: Please tell us for which regular payments are you most likely to use digital payments instruments

SWIFT_Digitisation_Prateek Roongta_vF.pptx 6

Merchants open to accepting digital payment

Merchant acceptance network will grow 10X in the next five years

41%45%

58%

84%

Agree that

convenience is the

largest reason for

continued usage

Value the avoidance

of this struggle for

change

Value not having to

store and manage

cash

Find it a convenient

way to account and

track transactions

Source: Google-BCG market study based on Nielsen consumer survey Question: Please select the reasons that apply to you for businessmen started accepting digital payments

SWIFT_Digitisation_Prateek Roongta_vF.pptx 7

UPI and India Stack could be game changers

IND

IA S

TA

CK

Open Personal Data Store

CONSENT LAYER Permission "on demand"

IMPS, UPI, APB and AEPS

CASHLESS LAYER Financial tx "on demand"

e-KYC, e-sign, Digital Locker

PAPERLESS LAYER Documents "on demand"

Open access to biometric identification

PRESENCE-LESS LAYER Authentication "on

demand"

Source: India Stack website, ispirt presentation, https://medium.com/wharton-fintech/the-bedrock-of-a-digital-india-3e96240b3718#.h0a1hgcp2

SWIFT_Digitisation_Prateek Roongta_vF.pptx 8

Measures taken..

Banned Rs 500 and

Rs 1000

.. are resulting in a more digital economy

"Demonetisation" has provided an impetus to this digitization journey

• Almost all merchants need to accept digital

payments

• e.g. Paytm has increased its offline merchant

base from 8-8.5 lacs to 10 lacs

• Plans to hire additional 10,000 people to acquire

merchants (current team size - 4000)

More

cashless

• More people depositing money with banks

• Banks betting big on UPI

• e.g. ICICI Bank and a few others have inbuilt UPI

into its mobile banking app

Merchant

acquisition

more critical

UPI/Banking

larger

PPI non KYC limit

doubled to Rs 20k

No transaction

charges on debit

cards

• More people use cashless instruments- cards,

mobile, digital

• e.g. even small vendors prefer payment

through wallets rather than cheque

• Paytm - 7 mn txns daily > combined average

daily usage of credit and debit cards in India

SWIFT_Digitisation_Prateek Roongta_vF.pptx 9

Consumers, merchants adopting digital payments.. ~3.5X increase in POS demand, ~1.5X increase in POS transactions from Nov '16 to Dec '16

Merchant Consumer

3.5X increase in POS machine demand1

• from new categories of merchants such as

small kirana stores, vegetable vendors

3X jump in m-wallet merchant

registrations

• Number of Paytm merchant user base (mn)

Avg POS demand

(per month pre-demonetization) 6,000

Avg POS installed

(per month post demonetization) 20,000

Pending POS requests (total) 70,000

Source: 1. Secondary research 2. POS and PPI – Nov based on RBI reports, Dec based on projections of RBI representative data; UPI/USSD – NPCI data 3. BCG Center for Consumer Insight Survey Dec 2016 covering 1700 respondents across Metro to Tier 3 cities and SECs (A-D)

2016 2017 Target ~300%

1-1.5 5

# digital transactions post demonetization2

POS

usage # txns

(Mn)

Nov 2016

# txns

(Mn)

Dec 2016

~150% 501 332 ~130% ~650

Intent3

Intent3

PPI

usage # txns (Mn)

Nov 2016

# txns (Mn)

Dec 2016

252 169 ~150% ~500 ~200%

UPI/

USSD

usage # txns

(Mn)

Nov 2016

# txns

(Mn)

Dec 2016

Intent3

104 7 ~1400% ~150 ~150%

SWIFT_Digitisation_Prateek Roongta_vF.pptx 10

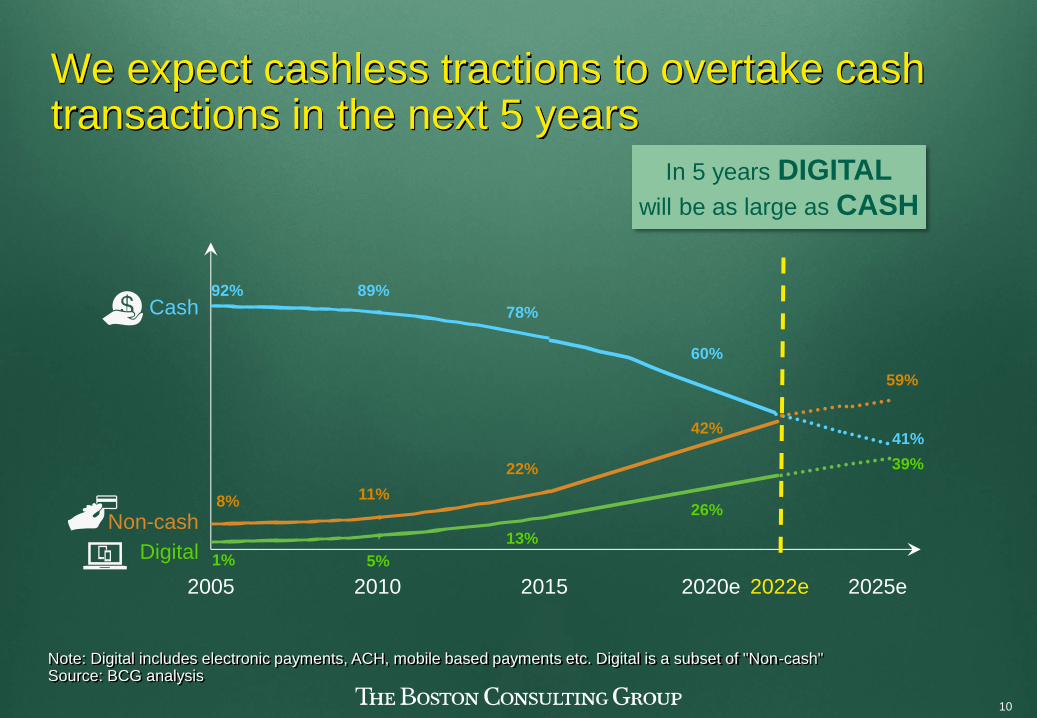

We expect cashless tractions to overtake cash transactions in the next 5 years

2005 2010 2015 2020e 2025e

89%

11%

5%

78%

22%

13%

60%

42%

26%

41%

59%

39%

In 5 years DIGITAL

will be as large as CASH

Cash

Non-cash

Digital

92%

8%

1%

Note: Digital includes electronic payments, ACH, mobile based payments etc. Digital is a subset of "Non-cash" Source: BCG analysis

2022e

SWIFT_Digitisation_Prateek Roongta_vF.pptx 11

Key questions for consideration of the panel What would drive sustained use of digital payment instruments?

What could be potential barriers for adoption of digital payments?

What role can banks and PSPs play in driving adoption?

Can UPI really be a game changer? How to make it happen?

How to drive digital payments for B2B payments (for MSMEs)?

How would digital payments providers build a sustainable business model?

What is expected from regulators / government to turbocharge adoption?

SWIFT_Digitisation_Prateek Roongta_vF.pptx 12

Thank you

bcg.com | bcgperspectives.com